chapter vi perceptions and problems of bankers – an...

TRANSCRIPT

216

Chapter VI

PERCEPTIONS AND PROBLEMS OF BANKERS – AN ANALYSIS

This chapter tries to analyse the perceptions and problems of bank officials

regarding various aspects of the agricultural lending. This chapter is presented in

two sections and the first section describes the perceptions and the problems

associated with the lending are analysed in the second section. The perceptions of

the bank officials regarding the criteria followed for the identification of loan

borrowers and for determination of loan amount are measured and ranked for

identifying the prominent factors considered for the identification of borrowers

and determination of loan amount. The views of the officials regarding pre and

post field visit, value added services, time lag in sanction and disbursement of

loan, DRI loans to agriculture, proportion of crop loan and term loan, achievement

in agricultural lending, defaults and NPA, mis-utilization of loan amount, etc. are

considered for evaluating the perceptions.

Selection of Bank Officials The bank officials identified for the study include officers of both public

and private sector banks. The number of officers from public and private sector

has been decided on the basis of number of bank branches in the sample districts

i.e. Thiruvananthapuram from Southern Region, Kottayam from Central Region

and Malappuram from Northern Region. Using the random sampling technique, 10

per cent of the total number of bank branches (as in March 2005) were identified

as sample population and accordingly 36 bank branches from South (27 Public and

9 Private sector), 27 from Central region (17 Public and 10 Private sector) and 24

from Northern region (18 Public and 6 Private sector) were identified. The

217

following table shows the details of branches selected from each sample district of

the three regions.

Table 6.1.1: Sample Design

Region Public Sector Private Sector Total

Total No. of

Branches

Sample Branches

Total No. of

Branches

Sample Branches

Total Bank

Branches

No. of Sample Branches

South (Thiruvanan-

thapuram)

268 (74)

27 (75)

92 (26)

9 (25)

360 (100)

36 (100)

Central (Kottayam)

175 (63)

17 (63)

104 (37)

10 (37)

279 (100)

27 (100)

North (Malapuram)

178 (77)

18 (75)

54 (23)

6 (25)

232 (100)

24 (100)

Total 621 (71)

62 (71)

250 (29)

25 (29)

871 (100)

87 (100)

Source: Primary data The proportion of public and private sector bank branches in the

Thiruvananthapuram district comes to 268 (74%) and 92 (26%), totalling 360

commercial banks. The total number of bank branches in the Kottayam district

comes to 279 of which 175 (63%) are in public sector and 104 (37%) in private

sector. The proportion of public and private sector branches in the Malapuram

district comes to 178 (77%) and 54 (23%) respectively totalling 232. Therefore,

the number of bank branches in the sample population constitutes 27 public and 9

private sector bank branches from the Thiruvananthapuram district and 17 public

and 10 private sectors from Kottayam district. The sample branches from

Malapuram district come to 18 public and 6 private sector banks. So the total

number of public sector bank branches comes to 62 and 25 from private sector,

totalling 87 commercial bank branches. Region-wise number of bank branches

218

constitutes 36 from the Southern region (Thiruvananthapuram), 27 from Central

(Kottayam) and 24 from the Northern region (Malapuram).

Section- I Selection of Eligible Borrowers The criteria normally followed by the banks for the identification of

beneficiaries are: credibility of the borrower, feasibility and viability of the

project, character and integrity of the borrower, the tangible security offered by the

borrowers as security, recommendation of government or governmental agencies,

etc. The respondents are required to rank the criteria adopted for the selection of

beneficiaries from 1 to 5 and the scores are assigned as 5, 4, 3, 2 and 1

respectively for first, second, third, fourth and fifth ranks. The scores are

measured, totalled and averaged for comparison and overall ranking of preferences

is presented in table 6.1.2.

Table 6.1.2: Criteria for Selection of Eligible Borrowers- Sector

Source: Primary data The criteria adopted for the selection of eligible borrowers reveals that the

credibility of the borrower is ranked first in both the public and private sectors.

Criteria Public Sector Private Sector

Mean Score Rank Mean

Score Rank

Credibility 4.53 1 4.2 1

Feasibility and Viability of the Project 3.31 2 3.96 2

Tangible Security Offered 3.00 3 3.04 3

Character and Integrity of the Borrower 2.66 4 2.8 4

On Recommendations 1.02 5 1.00 5

219

The order of ranks is the same in both sectors and they are: feasibility and viability

of the project, tangible security, character and integrity of the borrower and

recommendation respectively. The expected mean score comes to three and

criteria having a mean score of more than three can be considered as one having

much influence in the selection of borrowers. Accordingly credibility, feasibility

and viability of the project and security offered are the most influencing criteria

for the selection of borrowers in both sectors. It is noted that there is no difference

in the criteria adopted for the selection of beneficiaries in both sectors.

The region-wise order of criteria for the identification of the beneficiaries is

shown in table 6.1.3.

Table 6.1.3: Criteria for Selection of Eligible Borrowers – Region

Source: Primary data The region-wise order of criteria for the selection of eligible borrowers

shows that there is regional difference. The region-wise analysis reveals that

credibility and feasibility & viability of the project are the major criteria for

identification of borrowers in southern region, having a mean score of more than

Criteria South Central North

Mean Score Rank Mean

Score Rank Mean Score Rank

Credibility 4.6 1 4.59 1 4.00 1

Feasibility and Viability of the Project 3.36 2 3.3 2 3.92 2

Tangible Security Offered 2.92 3 3.1 3 3.1 3

Character and Integrity of the Borrower 2.28 4 3.00 4 3.00 4

On Recommendations 1.00 5 1.04 5 1.00 5

220

three. In central and northern regions credibility, feasibility & viability of the

project, tangible security offered and character and integrity of the borrower are

the determining factors, having an average mean score of more than three.

Recommendation of the Government or Government agencies is the least

influencing factor in the selection process of eligible borrowers.

Determination of Loan Amount The criteria normally followed by the banks for determination of loan

amount are: the guidelines followed by the bank, financial outlay of the project,

value of security offered, repaying capacity of the borrowers and feasibility of the

project. The respondents are required to rank the criteria adopted for the selection

of beneficiaries from 1 to 5 and the scores are assigned as 5, 4, 3, 2 and 1

respectively for first, second, third, fourth and fifth ranks. The scores are

measured, totalled and averaged for comparison and overall ranking of preferences

is shown in table 6.1.4.

Table 6.1.4: Criteria for Determination of Loan Amount – Sector

Source: Primary data

Criteria Public Sector Private Sector

Mean Score Rank Mean

Score Rank

Guidelines Followed by the Bank 4.87 1 4.88 1

Financial Outlay of Project 2.65 3 2.84 2

Value of Security Offered 2.39 4 2.4 4

Repaying Capacity 3.18 2 2.8 3

Feasibility of the Project 2.1 5 2.24 5

221

The main considerations for determination of loan amount are ranked in

their order of preference in table 6.1.4. The ranking reveals that guidelines

followed by the bank are the first criterion, which determines the loan amount in

both sectors, having a mean score of 4.87 and 4.88, much above the expected

mean score of three. The other influencing factors in the public sector are:

repaying capacity, financial outlay of the project, value of security offered and

feasibility of the project. In the public sector, it is noted that all the factors except

the repaying capacity of the borrower have a mean score of less than three

showing the insignificant influence on determining the loan amount. The order of

preferences of the private sector is: financial outlay of the project, repaying

capacity of the borrower, value of security offered and feasibility of the project. It

is evident from the analysis that in the private sector, all the factors except

guidelines followed by the bank have a mean score of less than three, showing the

insignificant influence on determining loan amount.

The region-wise mean score and rank of different criteria adopted for the

determination of loan amount are given in table 6.1.5.

Table 6.1.5: Criteria for Determination of Loan Amount - Region

Source: Primary data

Criteria South Central North

Mean Score Rank Mean

Score Rank Mean Score Rank

As per Guidelines of the Bank 4.94 1 4.85 1 4.79 1

Total Financial Outlay of Project 2.14 5 3.15 2 2.25 5

Value of Security Offered 2.3 4 2.26 4 2.67 4

Repaying Capacity of the Borrower 3.36 2 2.78 3 2.96 2

Feasibility of the Project 2.39 3 1.96 5 2.75 3

222

The region-wise mean score for different factors influencing the

determination of the loan amount reveals that the guidelines followed by the banks

are the most important criterion in all regions, having a very high mean score of

4.94, 4.85 and 4.79 respectively. The region-wise analysis reveals some regional

difference in the factors that influence the determination of loan amount. Repaying

capacity is ranked second in southern and northern region; whereas it is total

financial outlay in central region. All other factors, which have influence on the

determination of the loan amount has a mean score of less than three and shows an

insignificant influence on determination of loan amount.

Pre-Sanction Field Visit Pre-sanction field visit by bank officials is essential for evaluating financial

viability of the project and credit worthiness of the borrowers. So normally as a

pre requirement, the bank officials make a pre-sanction field visit and the

frequency of such visits is given in table 6.1.6

Table 6.1.6: Pre-Sanction Field Visit –Sector

Source: Primary data Significant Difference (Sig. value 0.039)

Pre-Sanction Field Visit

Public Sector Private Sector Total

No. % No. % No. %

Always 41 66 22 88 63 72

Frequently 19 31 2 8 21 24

Occasionally 2 3 1 4 3 4

Total 62 100 25 100 87 100

223

Of the total respondents, 72 per cent always make pre-sanction field visit

for sanctioning the loan proposals. 24 per cent of the officials make frequent pre

sanction field visit and four per cent make occasional field visit. Therefore, it is

clear that 96 per cent of the officials conducted pre sanction field visit always or

frequently. The sector-wise analysis reveals that more number of private sector

officials (88%) always make pre-sanction field visits than the public sector (66%).

It is clear that there is significant sector-wise variation in pre-sanction field visits

in both sectors. The Chi square test also reveals the significant statistical sector-

wise difference (at 5 per cent level) in the opinion of the respondent’s with regard

to the pre-sanction field visit.

The region-wise frequency of pre-sanction field visit is given in table 6.1.7.

Table 6.1.7: Pre-Sanction Field Visit – Region

Source: Primary data The region-wise pre-sanction field visit by the bank officials reveals that

bank officials of the southern region makes more pre-sanction field visits (78%)

than the central (70%) and northern region (67%). However such difference

among the banks from different regions appeared to be marginal only.

Pre-Sanction Field Visit

South Central North Total

No. % No. % No. % No. %

Always 28 78 19 70 16 67 63 72

Frequently 7 19 7 26 7 29 21 24

Occasionally 1 3 1 4 1 4 3 4

Total 36 100 27 100 24 100 87 100

224

Post- Sanction Field Visits Post-sanction field visits are made by the bank officials in order to assess

the effectiveness in the utilization of the loan amount and to ensure timely

repayment of the loan. The frequency of post-sanction field visit by the bank

officials is given in table 6.1.8.

Table 6.1.8: Post- Sanction Field Visits- Sector

Source: Primary data Of the total, 25 per cent of the officials did not make any post sanction field

visits and 40 per cent made annual visits. Nine per cent of the bank officials

claimed that they made quarterly post-loan field visit. The sector- wise analysis

reveals that 36 per cent of private sector and 34 per cent of public sector officials

make quarterly or half yearly post-loan visits. The post-sanction field visits reveal

the poor monitoring and supervision of agricultural loans.

The region-wise post-Sanction field visits conducted by the bank officials is

shown in table 6.1.9

Post- Sanction Field Visits

Public Sector Private Sector Total

No. % No. % No. %

Quarterly 3 5 5 20 8 9

Half Yearly 18 29 4 16 22 25

Yearly 25 40 10 40 35 41

No Visit 16 26 6 24 22 25

Total 62 100 25 100 87 100

225

Table 6.1.9: Post- Sanction Field Visits – Region

Source: Primary data

The region- wise analysis reveals that more (50%) officials of the southern

region made yearly post-sanction field visit than the central (33%) and northern

regions (34%). 20 per cent of the southern and 29 per cent each of the central and

northern regions did not make any post-sanction field visits. 22 per cent and 30

per cent carry out half yearly post-sanction field visits in the southern and central

region whereas it is 25 per cent in the Northern region.

Value Added Services in Agricultural loans The value added services provided by banks to borrowers include:-

a. Technical services

b. Arrange for marketing the agricultural products.

c. Help in acquisition of assets

d. Advice for minimization of cost of loan

e. Advice on technology changes/ market situations, etc.

The table 6.1.10 shows the sector-wise details of value added services

provided by the banks to the borrowers.

Post- Sanction Field Visits

South Central North Total

No. % No. % No. % No. %

Quarterly 3 8 2 8 3 12 8 9

Half Yearly 8 22 8 30 6 25 22 25

Yearly 18 50 9 33 8 34 35 41

No Visit 7 20 8 29 7 29 22 25

Total 36 100 27 100 24 100 87 100

226

Table 6.1.10: Value Added Services Provided by Banks- Sector

Source: Primary data Significant Difference (Sig. value 0.004) Of the total, 48 per cent of the banks did not provide any value added

services to the loan beneficiaries. 38 per cent provide advice for minimization of

the cost of loan. 10 per cent each of the bank officials provide some technical

services and also helped in the acquisition of agricultural assets. It is clear that

only two per cent of the banks provide marketing assistance to the borrowers,

which is one of the main constraints faced by most of the farmers. The sector-wise

analysis reveals that more private sector banks provide value added services to the

borrowers. 20 per cent each of the private sector provide technical services and

help in acquisition of assets, whereas it is six per cent each in the public sector.

The variation in opinion about value added services is corroborated with the help

of Chi square test, which indicates that sector-wise difference is statistically

significant at 1 per cent level.

Value Added Services

Public Sector

Private Sector Total

No. % No. % No. %

Technical Service 4 6 5 20 9 10

Arrange for Marketing 2 3 - - 2 2

Help in Acquisition of Assets 4 6 5 20 9 10

Advice for Minimization of Cost of Loan 20 32 13 52 33 38

Advice on Technology Change /Market etc. 2 3 3 12 5 6

No Additional Services 36 58 6 24 42 48

227

The region-wise analysis of the value added services provided by banks is

shown in table 6.1.11.

Table 6.1.11: Value Added Services Provided by Banks – Region

Source: Primary data

Region-wise analysis of value added services provided by the banks reveals

that more technical services are provided in the northern region. Majority banks of

the central and northern region did not provide any additional services to the

borrowers.

Time Lag in Sanctioning Loan Amount Time lag in sanction of loan amount means the time taken by the banks for

processing the application, i.e. the difference between the date of application and

date of sanctioning of loan amount. The time lag in sanctioning the loan is

analyzed in two ways:

Value Added Services South Central North Total

No. % No. % No. % No. %

Technical Services 3 8 - - 6 25 9 10

Arrange for Marketing - - 1 4 1 4 2 2

Helps in Acquisition of Assets 5 14 1 4 3 13 9 10

Advice for Minimization of Cost of

Loan 14 39 10 37 9 38 33 38

Advice on Technology Charge /Market etc. - - 1 4 4 17 5 6

No Additional Services 14 39 16 59 12 50 42 48

228

a) Time lag in processing the loan application which can be sanctioned at the

branch level and

b) Those which require approval of higher authorities.

Time Lag in Sanction - Within the Power of Branch Manager

Based on the quantum of loan amount, loan applications are sanctioned

either at the branch level or with the approval of the higher authorities. The sector-

wise time lag in sanctioning loan at the branch level is depicted in table 6.1.12.

Table 6.1.12: Time Lag in Sanction - within the Power of Manager- Sector

Source: Primary data

Significant Difference (Sig. value 0.000)

Of the total, the majority (67%) of bank officials state that they sanctioned

the loan application within 4-7 days. 23 per cent of the officials claim that they

sanction the loan application within 3 days. 10 per cent have the opinion that they

need more than 7 days for sanctioning the loan amount. The sector-wise analysis

reveals that the majority (56%) of private sector banks sanctioned the loan within

3 days, whereas it is 10 per cent in the public sector. There is more delay in the

public sector because of ‘public’ character and cumbersome official formalities

Time Lag Public Sector Private Sector Total

No. % No. % No. %

Within 3 Days 6 10 14 56 20 23

4 -7 Days 49 79 9 36 58 67

Above 7 Days 7 11 2 8 9 10

Total 62 100 25 100 87 100

229

fixed by regulatory agencies. The variation in opinion about time lag in

sanctioning the loan is corroborated with the help of Chi square test which

indicates that sector-wise difference is statistically significant at 1 per cent level.

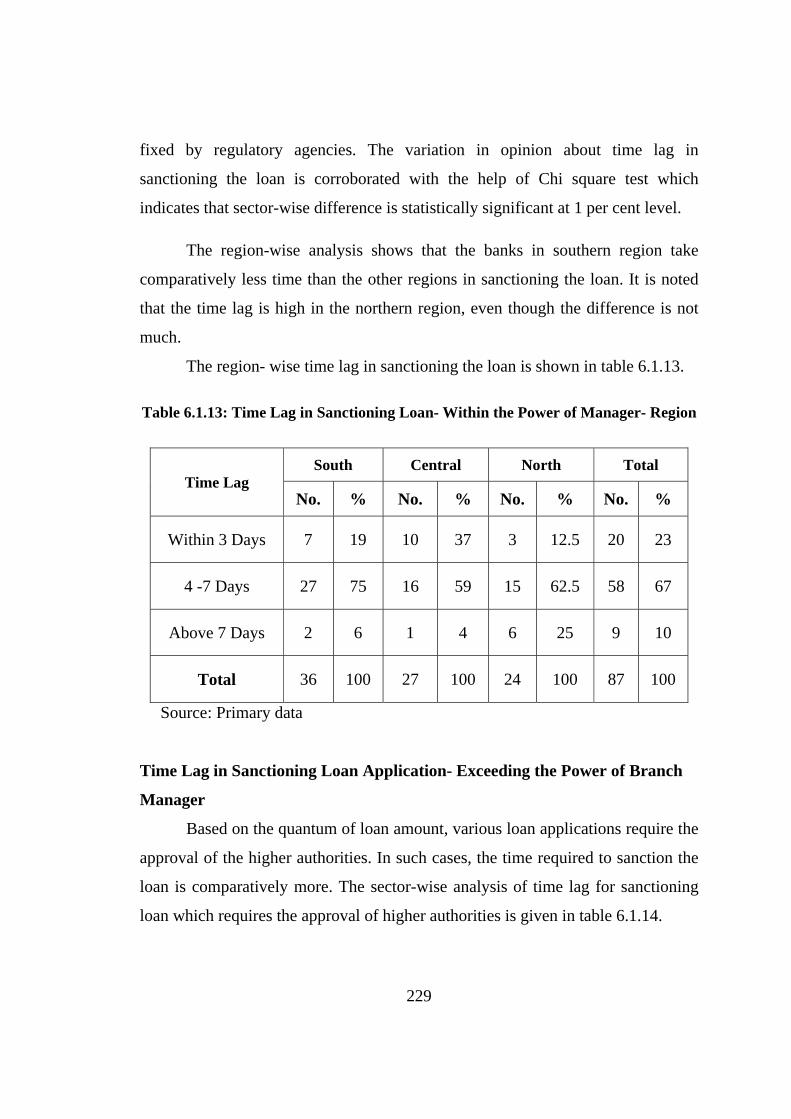

The region-wise analysis shows that the banks in southern region take

comparatively less time than the other regions in sanctioning the loan. It is noted

that the time lag is high in the northern region, even though the difference is not

much.

The region- wise time lag in sanctioning the loan is shown in table 6.1.13.

Table 6.1.13: Time Lag in Sanctioning Loan- Within the Power of Manager- Region

Time Lag South Central North Total

No. % No. % No. % No. %

Within 3 Days 7 19 10 37 3 12.5 20 23

4 -7 Days 27 75 16 59 15 62.5 58 67

Above 7 Days 2 6 1 4 6 25 9 10

Total 36 100 27 100 24 100 87 100

Source: Primary data

Time Lag in Sanctioning Loan Application- Exceeding the Power of Branch

Manager

Based on the quantum of loan amount, various loan applications require the

approval of the higher authorities. In such cases, the time required to sanction the

loan is comparatively more. The sector-wise analysis of time lag for sanctioning

loan which requires the approval of higher authorities is given in table 6.1.14.

230

Table 6.1.14: Time Lag in Sanctioning Loan- Exceeding the Power of Branch Manager- Sector

Source: Primary data

Majority (75%) of the respondents sanction the loan within a period of one

to three weeks and seven per cent within one week. 18 per cent took more than

three weeks for sanctioning the loan. The sector-wise analysis discloses that the

majority (60%) of private sector banks take less than two weeks time to sanction

the loan whereas it is 34 per cent in the public sector. It is noted that public sector

takes more time to sanction the loan which requires the approval of higher

authorities.

The region-wise time lag in the sanctioning of loan that exceeds the power

of manager is shown in table 6.1.15.

Time Lag Public Sector Private Sector Total

No. % No. % No. %

< 1 Week 1 2 5 20 6 7

1-2 Week 20 32 10 40 30 35

2 -3 Week 29 47 6 24 35 40

3 -4 Week 10 16 4 16 14 16

> 4 Week 2 3 - - 2 2

Total 62 100 25 100 87 100

231

Table 6.1.15: Time Lag in Sanctioning Loan- Exceeding the Power of Manager –Region

Time Lag South Central North Total

No. % No. % No. % No. %

< 1 Week 1 3 4 15 1 4 6 7

1- 2 Weeks 14 39 9 33 7 29 30 35

2 -3 Week 16 44 12 45 7 29 35 40

3 -4 Week 5 14 2 7 7 29 14 16

> 4 Weeks - - - - 2 9 2 2

Total 36 100 27 100 24 100 87 100

Source: Primary data

The region- wise analysis reveals that more officials of the central region

(48%) sanctioned the loan within two weeks whereas it is 42 per cent and 33 per

cent in the southern and northern regions. It is observed that the northern region

consumes more time than the other regions.

Time Lag in Disbursement of Loan Amount Sanction and actual disbursement of the loan amount are the two distinct

stages in the lending process. Normally the banks take some added time to the

actual disbursement of the amount after sanctioning the loan. The time lag in the

disbursement loan is analysed sector- wise in table 6.1.16.

232

Table 6.1.16: Time Lag in Disbursement - Within the Power of Manager- Sector

Source: Primary data

Significant Difference (Sig. value 0.016)

The majority (53%) of respondents disburse the loan amount within two

days of sanction. 45 per cent disburse it within a period of 3-5 days. The sector-

wise analysis reveals that the private sector is more prompt in disbursement of

loan amount than the public sector. The variation in opinion about time lag in

disbursement of loan is corroborated with the help of Chi square test which

indicates that sector-wise difference is statistically significant at 5 per cent level.

The region-wise time lag in disbursement of the loan amount, which can be

sanctioned within the power of branch manager, is shown in table 6.1.17.

Time Lag

Public Sector Private Sector Total

No. % No. % No. %

Within 2 Days 27 44 19 76 46 53

3 -5 Days 33 53 6 24 39 45

> 5 Days 2 3 - - 2 2

Total 62 100 25 100 87 100

233

Table 6.1.17: Time Lag in Disbursement– Within the Power of Manager- Region

Time Lag South Central North Total

No. % No. % No. % No. %

Within 2 Days 20 55 15 55 11 46 46 53

3 -5 Days 15 42 11 41 13 54 39 45

> 5 Days 1 3 1 4 - - 2 2

Total 36 100 27 100 24 100 87 100

Source: Primary data

The region-wise analysis shows that the majority respondents of the south

and central region (55%) disbursed the loan amount within two days, whereas it is

46 per cent in the northern region. More respondents of the northern region took 3

- 5 days for disbursing the loan amount.

Disbursement of Loan Amount- Exceeding the Power of Manager The sector-wise time lag in disbursement of loan amount exceeding the

power of branch manager shows (Table 6.1.18) that the majority of (51%) banks

disbursed the loan amount within three days and 37 per cent in 4- 6 days. The

sector-wise analysis shows that the private sector is more punctual in disbursement

of loan amounts than the public sector.

234

Table 6.1.18: Time Lag in Disbursement - Exceeding the Power of Manager-Sector

Source: Primary data

The region-wise time lag in disbursement of loan amount which exceeds

the power of branch manager is given in table 6.1.19.

Table 6.1.19: Time Lag in Disbursement – Exceeding the Power of Manager- Region

Source: Primary data

The majority of branch managers of the south and central region disbursed

the loan amount within three days of sanction, whereas it is 46 per cent in north. It

Time Lag Public Sector Private Sector Total

No. % No. % No. %

Within 3 Days 28 45 16 64 44 51

4 -6 Days 31 50 6 24 37 42

Above 6 Days 3 5 3 12 6 7

Total 62 100 25 100 87 100

Time Lag South Central North Total

No. % No. % No. % No. %

With in 3 Days 19 53 14 52 11 46 44 51

4 -6 Days 15 42 11 41 11 46 37 42

Above 6 Days 2 5 2 7 2 8 6 7

Total 36 100 27 100 24 100 87 100

235

is observed that more time is taken in the northern region compared to the other

regions.

DRI Loan for Agricultural Purposes

As per the RBI Guidelines, ‘Differential Rate of Interest’ (DRI) loans are to

be granted by the commercials banks to the weaker sections of the society at a

lower rate of interest at four per cent. The RBI directs the commercial banks to

advance loans and advances under the DRI scheme up to a minimum of one per

cent of the Net Bank Credit (NBC). The recent statistics shows that the

achievement under the scheme is very low, i.e. 0.01 per cent to 0.02 per cent of the

NBC. Therefore, an attempt is made to identify the level of DRI loan to

agricultural sector and the sector-wise responses are shown in table 6.1.20.

Table 6.1.20: DRI Loans for Agricultural Purposes – Sector

Source: Primary data

The majority (55%) of respondents never allowed DRI loans to the

agricultural sector. 39 per cent allowed DRI loans occasionally and only five per

cent frequently.

DRI Loans Public Sector Private Sector Total

No. % No. % No. %

Always 1 2 - - 1 1

Frequently 2 3 2 8 4 5

Occasionally 25 40 9 36 34 39

Never 34 55 14 56 48 55

Total 62 100 25 100 87 100

236

The region- wise analysis of DRI loan to agriculture is shown in table

6.1.21.

Table 6.1.21: DRI Loans for Agricultural Purposes – Region

DRI Loans South Central North Total

No. % No. % No. % No. %

Always - - - - 1 4 1 1

Frequently 2 6 1 4 1 4 4 5

Occasionally 13 36 7 26 14 58 34 39

Never 21 58 19 70 8 34 48 55

Total 36 100 27 100 24 100 87 100

Source: Primary data

Significant Difference (Sig. value 0.026)

Table 6.1.21 shows the region-wise disbursement of the DRI loan to the

agriculture sector. It is clear that more DRI loans are granted in the northern

region (66%) than the southern (42%) and central (30%) region. The variation in

the opinion about granting of DRI loans to agriculture is corroborated with the

help of Chi square test which reveals that the difference is statistically significant

at 5 per cent level.

Share DRI Loans to Agriculture

As per RBI guidelines, every banking company in India is required to grant

DRI loans to weaker sections of the society, at least one per cent of the Net Bank

Credit. The majority of the agriculturists of the State are marginal and small

237

farmers having too little income from agriculture. The major portion of the

workforce of the State is also involved in agriculture and their earning is skimpy,

as compared to the secondary and tertiary sector. Therefore, the majority of the

farmers and agricultural labours are eligible for the concessional DRI loans.

Hence, an attempt is made to analyse the extent of concessional lending to

agricultural sector and the responses are analyzed on the basis of sector and

region. The sector-wise share of DRI loans to agricultural activities is depicted in

table 6.1.22.

Table 6.1.22: Share of DRI Loans to Agriculture –Sector

Source: Primary data

Of the total respondents, the majority (55%) never granted DRI loans to the

agriculturists. The percentage share of DRI loans for agricultural activities reveals

that 67 per cent of the bank officials who allowed DRI loan to agriculture,

sanctioned up to 25 per cent of the total DRI loans. 28 per cent allowed DRI loans

to agriculture to the extent of 25 -50 per cent and 5 per cent above 50 per cent. The

sector-wise analysis shows that public sector is in a superior position than the

private sector in disbursing DRI loan to agriculture sector. 36 per cent of the

Share of DRI Loans Public Sector Private Sector Total

No. % No. % No. %

< 25% 18 64 8 73 26 67

25 – 50% 8 29 3 27 11 28

50 – 75% 1 3.5 - - 1 2.5

> 75% 1 3.5 - - 1 2.5

Total 28 100 11 100 39 100

238

public sector granted DRI loans to the extent of above 25 per cent of the total DRI

loans to agriculture sector, while it is 27 per cent in the private sector.

The region -wise percentage share of DRI loan to agricultural sector is

given in table 6.1.23.

Table 6.1.23: Share of DRI Loans to Agriculture –Region

Share of DRI Loans

South Central North Total

No. % No. % No. % No. %

< 25% 9 60 6 75 11 69 26 67

25 – 50% 4 26 2 25 5 31 11 28

50 – 75% 1 7 - - - - 1 2.5

> 75% 1 7 - - - - 1 2.5

Total 15 100 8 100 16 100 39 100

Source: Primary data

The region-wise analysis reveals that more DRI loans are disbursed to the

agricultural sector in the southern region than in the other regions. It is noted that

in central and northern region, the percentage distribution of DRI loan to the

agriculture sector is less than 50 per cent of the total DRI loans.

Proportion of Crop Loan and Term Loan Accounts

The loans and advances granted to agriculture sector are basically classified

into crop loans and term loans. The classification is based on the nature and period

of the loan. The crop loans are considered as production credit, normally for a

period of one year and term loans are mainly for investment purposes, having

more than one-year time frame for the settlement. The proportion of crop loan

239

accounts in total agriculture lending is evaluated, sector-wise and region-wise in

table 6.1.24 and 6.1.25.

Proportion of Crop Loan

The banks allow crop loans to the agriculturists mainly for meeting the

cultivation and operational expenses. The crop loans are normally sanctioned for

a period of one year and the borrowers are required to repay the amount with

interest, within the same period. Term loan includes medium and long-term loans

sanctioned by banks for agriculture and allied activities for a period of more than

one year. These loans are mainly sanctioned for the purpose of making

investments and developmental activities in agricultural land, agricultural

machinery, irrigation facility, etc. The sector-wise proportion of crop loans to the

total agriculture loan accounts is depicted in table 6.1.24.

Table 6.1.24: Proportion of Crop Loan Accounts to Total Agriculture Loan- Sector

Source: Primary data

The proportion of crop loan to total agriculture loan is above 80 per cent

among 54 per cent sample branches and between 60- 80 per cent in 43 per cent. It

Proportion of Crop

Loan

Public Sector Private Sector Total

No. % No. % No. %

< 60% 2 3 1 4 3 3

60 -80% 23 37 14 56 37 43

> 80% 37 60 10 40 47 54

Total 62 100 25 100 87 100

240

is observed that the share of crop loan to total agricultural loan is very high and the

public sector banks made more crop loan than the private sector.

Table 6.1.25 shows the region-wise proportion of crop loan to total

agricultural lending.

Table 6.1.25: Proportion of Crop Loan Accounts to Total Agricultural Loan –

Region

Proportion of

Crop Loan

South Central North Total

No. % No. % No. % No. %

< 60% 1 3 2 8 - - 3 3

60 -80% 14 39 12 44 11 46 37 43

> 80% 21 58 13 48 13 54 47 54

Total 36 100 27 100 24 100 87 100

Source: Primary data

The region-wise analysis shows that the majority of respondents of the

southern (58%) and northern regions (54%) have more than 80 per cent crop loan

accounts for the total agricultural lending. It is noted that more crop loan accounts

for total agriculture lending are in the northern and southern region than in the

central region.

Achievement in Agricultural Lending The RBI guidelines direct the commercial banks to lend at least 18 per cent

of Net Bank Credit (NBC) to the agriculture sector- the largest share in priority

sector lending. So an attempt is made to identify the extent of agricultural loans

granted by the banks to the agriculture sector and the analysis is presented in the

241

following tables. The sector-wise percentage achievement in agriculture lending

is shown in table 6.1.26.

Table 6.1.26: Achievement in Agriculture Lending – Sector

Source: Primary data

The achievement in agricultural lending by the respondent banks reveals

that 41 per cent attains 10-20 per cent target achievement and 31 per cent at level

of 20-40 per cent. 21 per cent achieves a higher level of above 40 per cent. The

sector-wise analysis shows that more achievement is among the public sector than

the private sector.

The region-wise achievement in agricultural lending is shown in table

6.1.27.

Achievement Public Sector Private Sector Total

No. % No. % No. %

< 10% 5 8 1 4 6 7

10 -20% 25 40 11 44 36 41

20 -40% 18 29 9 36 27 31

40 -60% 9 15 4 16 13 15

> 60% 5 8 - - 5 6

Total 62 100 25 100 87 100

242

Table 6.1.27: Achievement in Agriculture Lending - Region

Achievement South Central North Total

No. % No. % No. % No. %

< 10% 2 5.5 3 11 1 4 6 7

10 -20% 15 42 12 44 9 37.5 36 41

20 -40% 9 25 9 33 9 37.5 27 31

40 -60% 8 22 2 8 3 13 13 15

> 60% 2 5.5 1 4 2 8 5 6

Total 36 100 27 100 24 100 87 100

Source: Primary data

The region-wise analysis shows that achievement in agriculture lending is

more by the banks in northern and southern region than those in the central region,

even though the difference is not much wide.

Defaults in Agricultural Loan Default in loan means the failure of the borrowers to repay the amount

when it is due or delayed beyond a specified time. Agriculture is an economic

activity and income generated from it is a critical factor, which influences the

timely repayment of the loan. The extent of default is analyzed by sector and

region, in the following tables.

The sector-wise extent of defaults in agricultural loan is incorporated in

table 6.1.28.

243

Table 6.1.28: Defaults in Agricultural Loan –Sector

Source: Primary data

Of the total, 18 per cent of the banks have less than 5 per cent defaults in

agricultural lending. 45 per cent banks have defaults of 5-10 per cent and 30 per

cent of the banks have defaults to the extent of 10-20 per cent. 7 per cent banks

have a default of above 20 per cent. The sector-wise analysis exposes that more

defaults are in the public sector than the private sector. 76 per cent of private

sector banks have less than 10 per cent loan default, whereas it is 58 per cent in the

public sector. It is noted that the private sector banks are more profit- oriented and

they follow an effective follow-up and timely action for the recovery of loan than

the public sector, which reduces the defaults.

Region-wise defaults (6.1.29) reveal that more defaults are in the southern

region than the other regions. In the south, percentage of loan defaults is above 10

per cent in 41 per cent cases, as against 37 and 29 per cent of the central and

northern regions.

Defaults

Public Sector Private Sector Total

No. % No. % No. %

< 5% 11 18 5 20 16 18

5 -10% 25 40 14 56 39 45

10 -20% 22 35.5 4 16 26 30

> 20% 4 6.5 2 8 6 7

Total 62 100 25 100 87 100

244

Table 6.1.29: Defaults in Agricultural Loan – Region

Defaults South Central North Total

No. % No. % No. % No. %

< 5% 6 17 5 19 5 21 16 18

5 -10% 15 42 12 44 12 50 39 45

10 -20% 13 36 7 26 6 25 26 30

> 20% 2 5 3 11 1 4 6 7

Total 36 100 27 100 24 100 87 100

Source: Primary data

Non Performing Assets (NPA) in Agricultural Lending

Non-Performing Assets (NPA) means an asset or account of a borrower,

which has been classified as substandard, doubtful or loss asset, as per the

guidelines applicable for the asset classification, issued by the RBI. With a view to

moving towards international best practices and to ensure greater transparency, it

has been decided to adopt the '90 days overdue' norm for identification of NPAs,

from the year ending March 31, 2004. Accordingly, with effect form March 31,

2004, a non-performing asset shall be a loan or an advance where:

i. Interest and /or instalment of principal remains overdue for a period of

more than 90 days in respect of a term Loan

ii. The account remains 'out of order' for a period of more than 90 days, in

respect of an overdraft/ cash Credit (OD/CC),

245

iii. The bill remains overdue for a period of more than 90 days in the case of

bills purchased and discounted,

iv. Interest and/ or instalment of principal remains overdue for two harvest

seasons, but for a period not exceeding two half years in the case of an

advance granted for agricultural purpose, and

v. Any amount to be received remains overdue for a period of more than 90

days in respect of other accounts.

It is worthwhile to spotting the NPA altitude of the respondent banks, in

agricultural lending. The NPA echelon of the banks in agricultural lending is

analyzed by sector in table 6.1.30.

Table 6.1.30: NPA in Agricultural Lending – Sector

Source: Primary data

The majority of the respondent banks (55%) have less than two per cent

NPA and 36 per cent have 2 - 5 per cent. Nine per cent banks have NPA level of

above five per cent in agricultural lending. The sector-wise analysis shows that 55

per cent and 56 per cent of the public and private sector banks have very low NPA

level of less than 2 per cent and 35 per cent and 36 per cent have 2 - 5 per cent

NPA Public Sector Private Sector Total

No. % No. % No. %

< 2% 34 55 14 56 48 55

2-5% 22 35 9 36 31 36

> 5% 6 10 2 8 8 9

Total 62 100 25 100 87 100

246

NPA. The sector-wise descriptive analysis discloses that there is no wide variation

between the public and the private sector in their NPA levels.

The region- wise level of NPA in agricultural lending is shown in table

6.1.31.

Table 6.1.31: NPA in Agricultural Lending – Region

NPA South Central North Total

No. % No. % No. % No. %

< 2% 21 58 13 48 14 58 48 55

2 -5% 11 31 12 45 8 34 31 36

> 5% 4 11 2 7 2 8 8 9

Total 36 100 27 100 24 100 87 100

Source: Primary data

The region-wise analysis discloses that majority (58%) of the southern and

northern regions have less than two per cent NPA, whereas it is 48 per cent in the

central region. 31 per cent of the southern region has NPA of 2-5 per cent

whereas it is 45 per cent and 34 per cent respectively in central and northern

region..

Level of NPA in Crop and Term Loans The extent of NPA in crop loans and term loans is analysed in the following

tables.

247

Level of NPA in Crop Loans Crop loans are granted for meeting the cultivation expenses normally for a

period of one year. The sector-wise level of NPA in crop loans is shown in table

6.1.32.

Table 6.1.32: Level of NPA in Crop Loans- Sector

Source: Primary data

Majority (75%) of the banks have less than 2 per cent NPA in crop loans.

22 per cent banks have an NPA level of 2-5 per cent. The sector-wise analysis

shows that 74 per cent of the public and 76 per cent of private sector banks have

less than 2 per cent NPA in crop loans. It is observed that the public sector banks

have a fairly little more NPA level than the private sector banks in crop loans.

The region-wise level of NPA in crop loan is given in table 6.1.33.

Level of NPA – Crop Loans

Public Sector Private Sector Total

No. % No. % No. %

< 2% 46 74 19 76 65 75

2-5% 14 23 5 20 19 22

> 5% 2 3 1 4 3 3

Total 62 100 25 100 87 100

248

Table 6.1.33: Level of NPA in Crop Loans- Region

Level of NPA - Crop Loans

South Central North Total

No. % No. % No. % No. %

< 2% 27 75 21 78 17 71 65 75

2 -5% 7 19 6 22 6 25 19 22

> 5% 2 6 - - 1 4 3 3

Total 36 100 27 100 24 100 87 100

Source: Primary data

The region-wise analysis shows that the extent of NPA is more in southern

and northern region than in the central region, even though there is no much

difference.

Level of NPA in Term Loans

Term loans are allowed to investments in agricultural operation for a period

of more than one year. Term loan includes both medium term and long term loans

for agricultural purposes. The NPA levels in agricultural term loans are analyzed

by sector and region in the table 6.1.34 and 6.1.35. The sector- wise extent of

NPA in term loans (Table 6.1.34) shows that 62 per cent banks have less than 2

percent and 31 per cent have 2-5 per cent NPA in term loans. The sector- wise

analysis shows that 61 per cent of the public sector has less than 2 per cent NPA

and it is 64 per cent in the private sector. The sector- wise analysis reveals that the

public sector has a little more term loan NPA than the private sector.

249

Table 6.1.34: Level of NPA in Term Loans – Sector

Source: Primary data

The region- wise level of NPA in term loan is given in table 6.1.35.

Table 6.1.35: Level of NPA in Term Loans- Region

Level of NPA -

Term Loans

South Central North Total

No. % No. % No. % No. %

< 2% 24 67 16 59 14 58 54 62

2 -5% 11 30 9 33 8 33 27 31

> 5% 1 3 2 8 2 9 6 7

Total 36 100 27 100 24 100 87 100

Source: Primary data

Level of NPA – Term Loans

Public Sector Private Sector Total

No. % No. % No. %

< 2% 38 61 16 64 54 62

2-5% 20 32 7 28 27 31

> 5% 4 7 2 8 6 7

Total 62 100 25 100 87 100

250

The region-wise analysis shows that 67 per cent of the southern region has

less than 2 per cent NPA in agricultural term loans. The level of NPA in term loan

is moderately high in north and central regions in comparison with the south.

Inducement for Agricultural Loan The RBI prioritizes the agricultural lending in India and set a target of 18

per cent of the Net Bank Credit to the sector. Thus the commercial banks are

committed to attaining the target specification. The target stipulation sometimes

forces the bank officials to include other loans under the head ‘agriculture’. Table

6.1.36 shows the sector- wise responses of the respondents in this regard.

Table 6.1.36: Inducement for Agricultural Loan –Sector

Source: Primary data

Of the total, 70 per cent respondents sometimes or frequently, induce the

borrowers to avail themselves of loan under the head agriculture. The sector-wise

analysis shows that more inducement is given by the public sector than the private

sector, even though the difference is marginal.

Inducement for

Agricultural Loan

Public Sector Private Sector Total

No. % No. % No. %

Frequently 20 32 6 24 26 30

Sometimes 25 40 10 40 35 40

Never 17 28 9 36 26 30

Total 62 100 25 100 87 100

251

The region-wise inducement for availing the agricultural loan is given in

table 6.1.37.

Table 6.1.37: Inducement for Agricultural Loan – Region

Inducement for

Agricultural Loan

South Central North Total

No. % No. % No. % No. %

Frequently 12 33 9 33.3 5 21 26 30

Sometimes 15 42 9 33.3 11 46 35 40

Never 9 25 9 33.3 8 33 26 30

Total 36 100 27 100 24 100 87 100

Source: Primary data

The region-wise analysis discloses that more inducement for agriculture

loan is made at the southern region than the other regions. However the difference

seems to be normal.

Reasons for Inducement The bankers encourage the borrowers to utilize the agricultural credit

facility due to various reasons. They are: procedural simplicity, longer period for

NPA, attainment of target, security advantages, corporate practice and low interest

rate. The table 6.1.38 shows the sector-wise reasons for inducement. Procedural

simplicity is the reasons for the inducement among 24 per cent respondents and

longer period for NPA in 21 per cent cases. 18 per cent are induced for target

attainment and 17 per cent as a corporate practice. In 14 per cent cases, security

advantage is the reason for inducement and 6 per cent are induced by low interest

252

rate. The sector-wise analysis shows that procedural simplicity is the reason for

inducement in 24 per cent cases. The other major reasons are longer period for

NPA (23%), corporate practice (18%) and target attainment (16%) and in private

sector these are attainment of target (24%) longer period for NPA and corporate

practice (16% each). It is noted that the target achievement is one prominent

reason in the private sector.

Table 6.1.38: Reasons for Inducement – Sector

Source: Primary data

The region-wise analysis (Table 6.1.39) shows that the major influencing

factors in the southern region for inducement are: procedural simplicity (25%),

attainment of target (22%) and longer period for NPA (22%). In the central

region, it is procedural simplicity (22%), corporate practice (22%) and attainment

Reasons for Inducement Public Sector Private Sector Total

No. % No. % No. %

Procedural Simplicity 15 24 6 24 21 24

Longer Period for NPA 14 23 4 16 18 21

Attainment of Target 10 16 6 24 16 18

Security Advantages 9 14 3 12 12 14

Corporate Practice 11 18 4 16 15 17

Low Interest Rate 3 5 2 8 5 6

Total 62 100 25 100 87 100

253

of target (19%). In northern region, procedural simplicity (25%) and longer period

for NPA (25%) are the major influencing factors.

Table 6.1.39: Reasons for Inducement –Region

Reasons for Inducement

South Central North Total

No. % No. % No. % No. %

Procedural Simplicity 9 25 6 22 6 25 21 24

Longer Period for NPA 8 22 4 15 6 25 18 21

Attainment of Target 8 22 5 19 3 13 16 18

Security Advantages 5 14 3 11 4 17 12 14

Corporate Practice 5 14 6 22 4 17 15 17

Low Interest Rate 1 3 3 11 1 3 5 6

Total 36 100 27 100 24 100 87 100

Source: Primary data

Mis-utilisation of Agricultural Loan

Mis- utilisation means improper or diverted usage of the loan amount. If the

borrowers employ the loan amount for purposes other than the stipulated one, it is

termed as mis-utilisation. The opinion of bank officials regarding the mis-

utilisation of agricultural loan shown in Table 6.1.40 discloses that the majority

(70%) of bank officials have the opinion that there is occasional mis- utilisation of

loan amount by the borrowers. 24 per cent of the officials remarked that the mis-

utilisation of agricultural loan is frequent. The sector-wise analysis shows that

more officials of the public sector (71%) have the opinion that there is occasional

mis-utilisation compared with the private sector (68%). 26 per cent and 20 per

254

cent respondents of both public and private sectors subscribe the feeling that

frequent mis-utilisation of agricultural loan is a fact. It is noted that 97 per cent of

the public sector have the opinion that there is mis- utilisation of loan either

occasionally or frequently, whereas it is 88 per cent in private sector.

Table 6.1.40: Mis-utilisation of Agricultural Loan - Sector

Mis-utilisation of Loan Public Sector Private Sector Total

No. % No. % No. %

Always 1 1.5 2 8 3 4

Frequently 16 26 5 20 21 24

Occasionally 44 71 17 68 61 70

Never 1 1.5 1 4 2 2

Total 62 100 25 100 87 100

Source: Primary data

The region-wise analysis exposes that 41 per cent respondents of the central

region have the opinion that the mis- utilisation is frequent, whereas it is 22 per

cent in the south and 8 per cent in the north. Majority of the respondents of the

southern and northern region have the opinion that there is occasional mis-

utilisation of loan amount.

255

Table 6.1.41: Mis-utilisation of Agricultural Loan –Region

Mis-utilisation of Loan

South Central North Total

No. % No. % No. % No. %

Always 1 3 2 7 - - 3 4

Frequently 8 22 11 41 2 8 21 24

Occasionally 27 75 13 48 21 88 61 70

Never - - 1 4 1 4 2 2

Total 36 100 27 100 24 100 87 100

Source: Primary data

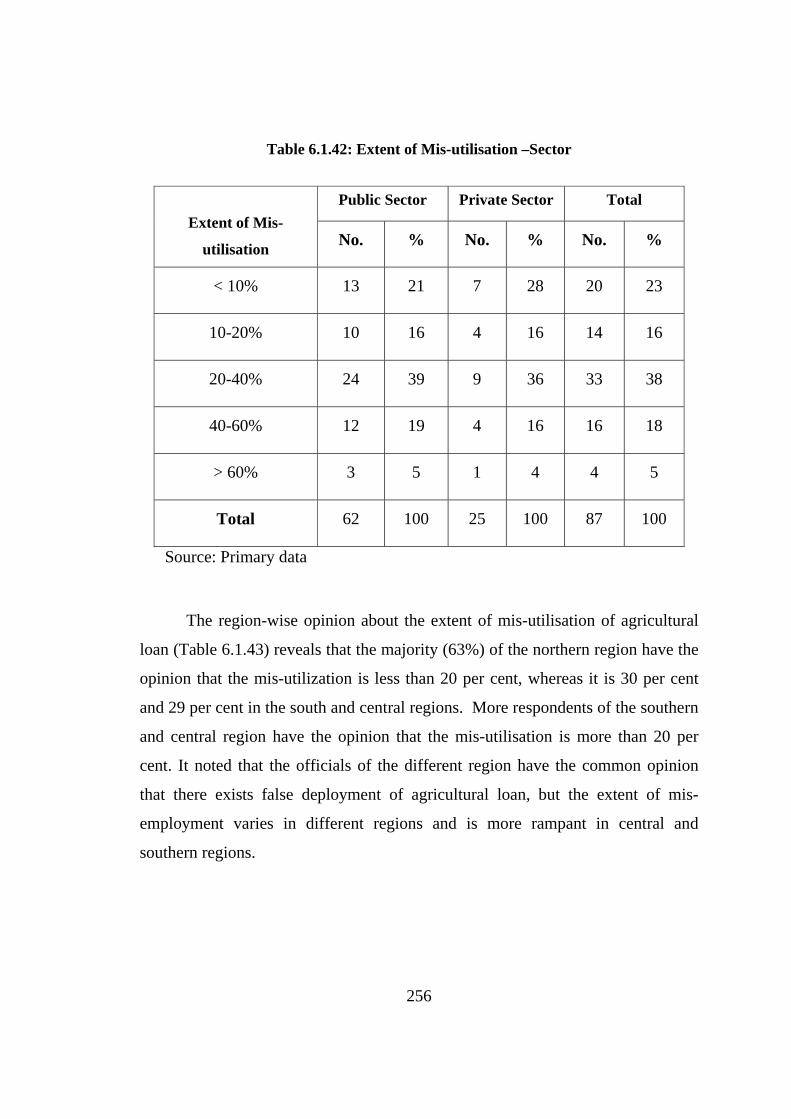

Extent of Mis-utilisation of Agricultural Loan The opinion of bank officials to the extent of mis-utilisation of loans given

in table 6.1.42 discloses that 38 per cent of the respondents have the opinion that

there is mis-utilisation of loan to the extent of 20- 40 per cent and 23 per cent as

less than 10 per cent. 23 per cent opines the mis-utilisation is above 40 per cent.

The sector-wise analysis shows that more public sector respondents have the

opinion that there is higher level of mis- utilisation than the private sector. 28 per

cent of private sector bank officials have the opinion that there is less than 10 per

cent mis-utilisation, whereas it is 21 per cent in the public sector.

256

Table 6.1.42: Extent of Mis-utilisation –Sector

Extent of Mis-

utilisation

Public Sector Private Sector Total

No. % No. % No. %

< 10% 13 21 7 28 20 23

10-20% 10 16 4 16 14 16

20-40% 24 39 9 36 33 38

40-60% 12 19 4 16 16 18

> 60% 3 5 1 4 4 5

Total 62 100 25 100 87 100

Source: Primary data

The region-wise opinion about the extent of mis-utilisation of agricultural

loan (Table 6.1.43) reveals that the majority (63%) of the northern region have the

opinion that the mis-utilization is less than 20 per cent, whereas it is 30 per cent

and 29 per cent in the south and central regions. More respondents of the southern

and central region have the opinion that the mis-utilisation is more than 20 per

cent. It noted that the officials of the different region have the common opinion

that there exists false deployment of agricultural loan, but the extent of mis-

employment varies in different regions and is more rampant in central and

southern regions.

257

Table 6.1.43: Extent of Mis-utilisation- Region

Extent of Mis- utilisation

South Central North Total

No. % No. % No. % No. %

< 10% 4 11 6 22 10 42 20 23

10-20% 7 19 2 7 5 21 14 16

20-40% 18 50 9 34 6 25 33 38

40-60% 5 14 8 30 3 12 16 18

> 60% 2 6 2 7 - - 4 5

Total 36 100 27 100 24 100 87 100

Source: Primary data

Significant Difference (Sig. value 0.022)

The variation in opinion about the mis-utilisation of loan is corroborated

with the help of Chi square test, the result of which proves that region- wise

difference is statistically significant at 5 percent level.

258

Section- II

Problems Faced by Commercial Banks in Agricultural

Lending

For studying the problems faced by the commercial banks in agricultural

lending, a Structured Interview Schedule was circulated among 87 selected bank

officials. It was to measure the level of agreement or disagreement on the

identified problems in agriculture lending. The problems in the agricultural

lending are divided into four heads: -

1) Lending and monitoring problems,

2) Repayment and related problems

3) Overdue and related problems and

4) General problems in agricultural lending.

Under the head lending and monitoring, 8 problems are identified and 5

problems each under the head repayment and overdue problems. 7 problems are

identified under the head general problems in agricultural lending. The identified

problems are ranked by using weighted mean score and appropriate statistical tests

like one way ANOVA, student’s t test, etc. are used to test the level of significance

of the identified problems in agricultural lending.

Lending and Monitoring Problems The extent of problems faced by the bank officials in connection with the

lending and monitoring of agricultural loan was analyzed by using weighted mean

259

score. For this a Structured Interview Schedule is circulated among the bank

officials and by using 5-point scale, the responses are scored and analyzed. On the

basis of the mean score, the problems are ranked and the results are incorporated

in table 6.2.1. The lending and monitoring problems identified for the analysis are:

1. Rigidity in lending rates

2. Cumbersome lending procedure

3. Excessive Regulations of the controlling authorities

4. Oral lease agreements

5. Insufficient tangible collateral security

6. Ineffective follow up

7. Mis-utilisation of the loan amount by borrowers

8. Lack of corrective action on mis-utilisation

Rigidity refers to inflexibility or resistance to change. In agricultural

lending the banks normally follow a rigid lending rate policy, which in most cases

unrealistic to the farmers. Agriculture now becoming as an unprofitable economic

activity and therefore, the lending rates should be sufficiently flexible to suit to the

changed situations.

The word cumbersome means difficult to handle because of complexity. In

agricultural lending, the commercial banks followed some cumbersome lending

procedures which make many difficulties to the officials as well as borrowers. The

procedural complexities insisted on by the bank for effectively protecting their

interest that creates problems in lending.

The operations of the commercial banks in India are controlled and

monitored by the RBI and the Government. The regulations and guidelines issued

by the controlling authorities from time to time create many difficulties for the

banks as well the borrowers. The opinion of the officials regarding such controls is

sought and incorporated in the study.

Lease agreement may be in written or oral. For granting agriculture credit

to the lease farmers, they are required to provide written lease agreement to the

260

bank. But in some areas, the landowners are reluctant to enter a written lease

agreement and they will enter only an oral lease agreement. Such oral lease

agreements create some difficulties for the bank officials and borrowers in

agricultural financing.

The capacity of the borrower to provide adequate collateral security to the

loan amount is another problem faced by the bank officials. The lending norms of

the bank insist on sufficient security for the loan amount, for properly protecting

the interests of the bank, but the incapability of the farmers to provide such

security creates some problems in agricultural lending.

Effective follow-up is very essential for the proper utilization and

repayment of the loan amount. For various reasons the bank officials are not in a

position to make effective follow up on agricultural loans. The ineffective follow

up of the agricultural loans creates some difficulties.

The utilization of the agricultural loan amount for other purposes especially

for unproductive purposes is another problem in agricultural lending. Fund

diversion leads to loan default and ultimately the lending capacity of the banks.

The target based lending to agriculture resists the correction of mis -

utilisation of the loan. Even though the loan agreement gives power to the banker

to take corrective action on mis-utilisation, the banks are reluctant to take such

corrective actions due to varying reasons. The lack of corrective action on mis-

utilisation is another major problem in agricultural lending.

The extent of problems associated with lending and monitoring are

measured by using five point scale. The respondents are required to mark the

degree of agreement or disagreement to the identified problems and the scores are

assigned as 5, 4, 3, 2 and 1 respectively for strongly agree, agree, neutral, disagree

and strongly disagree. The scores are measured totalled and averaged for

comparison and overall ranks are assigned on the basis of the weighted score. The

mean score and ranks of the associated problems of lending and monitoring are

incorporated in table 6.2.1.

261

It is evident that the overall weighted mean score of the lending and

monitoring problems of the bank is 2.48, which is below the median score of

three. This reveals that the gravity of such problems is relatively low among the

commercial banks in Kerala. The problems with a mean score of three or more

are: lack of corrective action on mis- utilisation of loan amount and mis-utilisation

of loan by the beneficiaries. In all other identified problems the mean score is less

than three which means that the bank officials face low- to- moderate problems in

this regard. Cumbersome lending procedures and excessive regulations of the

controlling authorities are the problems occupying third and fourth position in

terms of intensity among the eight identified problems related to agricultural

lending and monitoring.

Table 6.2.1: Lending and Monitoring Problems- Mean Score and Rank

Problems Mean Score Rank

1. Rigidity in Lending Rates 2.7 VI

2. Cumbersome Lending Procedures 2.88 III 3. Excessive Regulation of the Controlling

Authorities 2.84 IV

4. Oral Lease Agreements 2.34 VIII

5. Insufficient Tangible Collateral Security 2.65 VII

6. Ineffective Follow up 2.78 V

7. Mis-utilisation of Loan by Borrowers 3.08 II

8. Lack of Corrective Action on Mis-utilisation 3.18 I

Over All average score 2.48

Sign Test p value 0.1445

Source: Primary data

262

By using One Sample Sign Test, the study has tested the null hypothesis

of µ = 3 (lending and monitoring problems are moderate among the commercial

banks), against the alternate hypothesis of µ<3 (i.e., lending and monitoring

problems are relatively low) at five per cent level of significance. The test found

rejection of alternative hypothesis at this level which leads to the conclusion that

the commercial banks in Kerala are facing problems at moderate scale with

regard to lending and monitoring of agricultural credit to their customers.

Lending and Monitoring Problems – Sector-wise Comparison

The sector- wise mean score and rank of lending and monitoring problems

is shows in Table 6.2.2.

Table 6.2.2: Lending and Monitoring Problems- Mean Score and Rank- Sector

Problems Public Sector Private Sector

Mean Score Rank Mean

Score Rank

1. Rigidity in Lending Rates 2.82 VI 2.4 V

2. Cumbersome Lending Procedures 3.04 III 2.48 IV

3. Excessive Regulations of the Controlling Authorities 2.95 V 2.56 III

4. Oral Lease Agreements 2.44 VIII 2.12 VII

5. Insufficient Tangible Collateral Security 2.73 VII 2.48 IV

6. Ineffective Follow Up 2.97 IV 2.32 VI

7. Mis-utilisation of Loan by Borrowers 3.26 II 2.64 II

8. Lack of Corrective Action on Mis- utilisation 3.34 I 2.8 I

Over All Mean 2.94 -- 2.48 --

Source: Primary data

263

The sector- wise mean score and rank of lending and monitoring problems

reveal that lack of corrective action on mis-utilisation of the loan amount is the

major problem faced by the bank officials in the agricultural lending and both the

public and the private sector. Mis-utilisation of the loan by the loan beneficiaries is

ranked second in both the sectors. Cumbersome lending procedures and

ineffective follow-up and excessive regulations of the controlling authorities

ranked as third, fourth and fifth problems in agricultural lending by the public

sector, whereas these are excessive regulations of the controlling authority,

cumbersome lending procedure and rigidity in lending rates in the private sector.

The mean score of the problems is higher in the public sector, revealing that the

public sector faces more lending related problems than the private sector. It is also

noted that none of the problems have a mean score of above 3 in the private sector

which means all the private sector officials face low- to- moderate problems in the

lending and monitoring of agricultural loans.

In order to verify whether there is any sector-wise variation in lending and

monitoring the problems, student’s t- test is applied and the result is shown in the

table 6.2.3.

Table 6.2.3: Mean Score Difference in Lending and Monitoring Problems -

Student’s‘t’ Test

Sector N Mean SD. Df. t P. Value

Public 62 26.27 3.44 85 4.803 0.000*

Private 25 22.28 3.68

*Significant at 1 per cent level

The student’s t test shows that there is significant sector-wise variation in

lending and monitoring problems in agricultural lending operations in Kerala. The

264

lending and monitoring problems are denser in the public sector than in the private

sector, as revealed by the test result.

Lending and Monitoring Problems – Region-wise Comparison

The region-wise mean score and rank of lending and monitoring problems

are incorporated in table 6.2.4.

Table 6.2.4: Lending and Monitoring Problems – Mean Score and Rank- Region

Problems South Central North Mean Score Rank Mean

Score Rank Mean Score Rank

1. Rigidity in Lending Rates 2.58 VI 2.59 V 3.00 IV

2. Cumbersome Lending Procedures 2.86 III 2.89 II 2.92 V

3. Excessive Regulations of the Controlling Authorities 2.75 V 2.89 II 2.92 V

4. Oral Lease Agreements 2.17 VIII 1.93 VI 3.08 III

5. Insufficient Tangible Collateral Security 2.42 VII 2.67 IV 3.00 IV

6. Ineffective Follow Up 2.83 IV 2.81 III 2.67 VI

7. Mis-utilisation of Loan by Borrowers 3.08 II 2.89 II 3.29 I

8. Lack of Corrective Action on Mis-utilisation 3.14 I 3.26 I 3.17 II

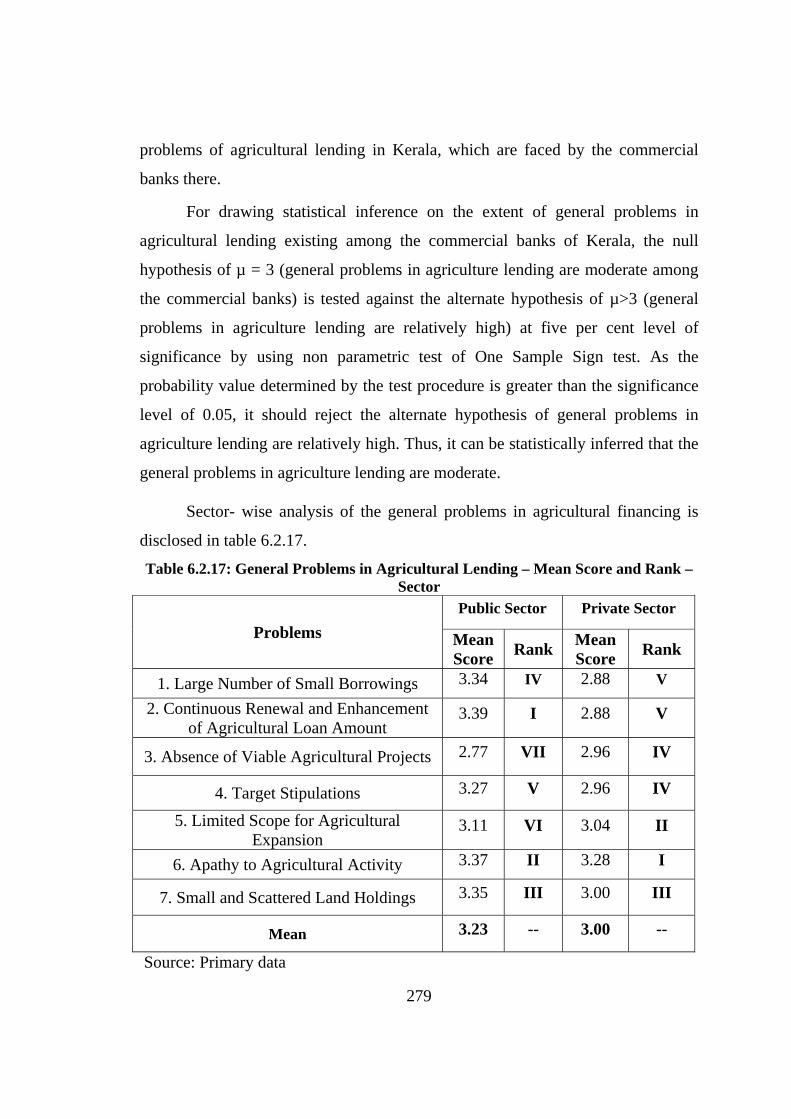

Mean 2.73 -- 2.74 -- 3.00 -- Source: Primary data

The mean score of the lending and monitoring problems in the three regions

are 2.73, 2.74 and 3. The major problems in the lending and monitoring are the

same in different regions and the problems having a mean score of more than three

are mis-utilisation of the loan by the borrowers and lack of corrective action on

mis-utilisation. The prominent problem in the southern region is cumbersome

265

lending procedures, ineffective follow-up in the central region and oral lease

agreements in the northern region. Ineffective follow-up and excess regulation of

controlling authorities are ranked fourth and fifth in the south, whereas it is

ineffective follow up and rigidity in lending rate are in the central region.

Insufficient collateral security and regulations of the controlling authorities are

ranked fourth and fifth in the northern region. The region-wise magnitude of the

lending and monitoring problems, as measured by the weighted mean score are

high in the northern region, as compared to the south and central regions.

In order to verify whether there is any region-wise variation in the problems

faced by the bank in lending and monitoring, one-way ANOVA is applied and the

test result found significance of difference in the magnitude of lending and

monitoring problems across the regions (Table 6.2.5).

Table 6.2.5: Mean Score Difference in Lending and Monitoring Problems One-way ANOVA

Region N Mean S.D F P. Value

South 36 24.25 3.62

4.289 0.017* Central 27 24.59 4.04

North 24 27.04 3.76 *Significant at 5 per cent level Repayment and Related Problems

The repayment and related problems normally faced by the bank officials in

agricultural lending are identified and the level of agreement or disagreement is

measured by using five point scale. The respondents are required to mark the

degree of agreement or disagreement to the identified problems and the scores are

assigned as 5, 4, 3, 2 and 1 respectively for strongly agree, agree, neutral, disagree

and strongly disagree. The scores are calculated, totalled and averaged for

266

comparison and overall ranks are assigned on the basis of the weighted score. The

repayment and related problems identified are:

1. Waiver syndrome/ OTS policy of the government

2. Intentional failure of the borrowers to repay the loan amount

3. Natural calamity and crop failure

4. Inadequate return of agricultural activity

5. Absence of incentive/ subsidy for prompt repayment

The term ‘waiver’ means a formal written statement of relinquishment or

discharge of an obligation. In waiver, the lender does not insist on the borrowers

repaying the debt when it is due. The term syndrome refers to a set of signs that

tend to occur together and which reflect the presence of a particular abnormal

condition. The waiver syndrome here means the practice of the Government to

write off the agricultural loans obligations. The one time settlement policy- the

policy set by the Government for the recovery of overdue by offering some

concessions to the defaulters. Even though the government formulates such

schemes, for providing relief to the farmers, they stimulate the intentional loan

defaults. So such practices give some bad signal to the society and they will create

some problems to the lending institutions.

Willful default means the intentional failure of the borrower to repay the

loan even though he is in a position to do so. Waiver syndrome/ OTS policy of the

Government, to some extent, promotes the willful defaults in agricultural credit. In

such cases, some of the beneficiaries intentionally make default for the repayment

of the debt obligations in order to avail the concessions.

Natural calamity– the act of God- may adversely affect the repayment

performance of the borrowers. Natural calamity and crop failure are one of the

main problems, faced by the farmers. Natural calamity may occur in the form of

drought, flood, earthquake, land slide, storm, etc. Crop failure may be due to the

natural calamity or pest attack. Effective insurance protection is a must for

relieving the farmer of such setbacks.

267

In the present scenario, the return from the agricultural activities is

insufficient to meet the day-to-day affairs of the farmers and for the repayment of

the loan. The inadequate return from the agricultural activities is another factor

affecting the repayment performance of the borrowers.

In agricultural lending there is no practice of providing any incentives or

concession to the prompt re-payers. By the introduction of the waiver/ OTS policy,

actually the defaulters get benefited and prompt re-payers are penalized.

Table 6.2.6: Repayment and Related Problems- Mean Score and Rank

Problems Mean Score Rank

1. Waiver Syndrome/ OTS Policy of the Government 3.14 II

2. Intentional Failure of the Borrowers 2.57 IV

3. Natural Calamity and Crop Failure 2.44 V

4. Inadequate Return of Agricultural Activity 2.63 III

5. Absence of Incentive/ Subsidy for Prompt Repayment 3.51 I

Mean 2.96 --

Sign Test P value 0.499

Source: Primary data

The mean score and rank of the repayment and related problems are shown

in table 5.2.6. Analysis of the table reveals that among the five identified problems

relating to repayment and related aspects, absence of incentives on prompt

repayment and waiver syndrome/ One Time Settlement policy of the Government

are the most proximate issues faced by the commercial banks in Kerala, while

extending agricultural credit. Inadequate return from agriculture and intentional

failure are ranked third and fourth in terms of its intensity. The mean score of 2.96,

268

very close to the median score of 3, given an indication of moderate degree of

problems faced by banks related to repayment of agricultural loans.

For drawing statistical inference on the extent of repayment and related

problems existing among the commercial banks, the null hypothesis of µ = 3

(repayment and related problems are moderate among the commercial banks) is

tested, against the alternate hypothesis of µ<3 (i.e., repayment and related

problems are relatively low) at 5 percent level of significance by using non

parametric test of one sample Sign Test. Test result indicates commercial banks in

Kerala are facing moderate degree of such problems.

The sector-wise analysis of the repayment related problems of the banks is

shown in table 6.2.7.

Table 6.2.7: Repayment and Related Problems- Mean Score and Rank –Sector

Problems

Public Sector Private Sector

Mean Score Rank Mean

Score Rank

1. Waiver Syndrome/ OTS Policy of the Government 3.31 II 2.72 II

2. Intentional Failure of the Borrowers 2.69 IV 2.28 III

3. Natural Calamity and Crop Failure 2.55 V 2.16 V

4. Inadequate Return of Agricultural Activity 2.79 III 2.24 IV

5. Absence of Incentive/ Subsidy for Prompt Repayment 3.69 I 3.04 I

Mean 3.01 -- 2.49 --

Source: Primary data

The sector-wise analysis reveals that the absence of incentive/ subsidy on

prompt repayment is the main problem acknowledged by the respondents of both

the sectors. In the present scenario, there is a feeling among the farmers that

defaulters are supported and prompt re-payers are penalized by the financial

269

agencies. The mean score of the repayment problems in public sector is 3.01, just

above the expected average mean score, enlightening the repayment-related

problems whereas it is 2.49 in the private sector. It means that the impact is

moderate. Waiver syndrome/ OTS policy is ranked II in both the sectors.

Inadequate return from the agricultural activity ranked third in the public sector,

whereas it is intentional failure in the private sector. The impact of natural

calamity and crop failure is the slightest problem in both sectors.

In order to verify whether there is any significant difference in the opinion

of the bank officials of the public and private sectors about the difficulties faced

by them in repayment and related aspects, student’s t- test is applied.

Table 6.2.8: Mean Score Difference in Repayment and Related Problems

Student’s ‘t’ Test

Sector N Mean SD. Df t P Value

Public 62 15.03 2.6049

85 4.594 0.000*

Private 25 12.44 1.6852

*Significant at 1 per cent level

Test result reported in table 6.2.8 shows that there is significant difference

in the opinion of the bank officials of the public and private sectors regarding the

repayment and related problems in their agricultural lending. The repayment and

related problems are more severe in the public sector than in the private sector.

Region-wise analysis of the repayment and related problems are shown in

table 6.2.9 reveals that the absence of incentives / subsidy for prompt repayment

and waiver syndrome are the main problems faced by the bank officials,

irrespective of any regional variation. Natural calamity and crop failure is the third

problem in the southern region, whereas it is inadequate return from agricultural

operations in the central region. Intentional failure of the borrowers is the third

270

problem faced by the bank officials of the northern region. Inadequate return from

agriculture and intentional failure are ranked IV and V in the southern region,

whereas it is intentional failure and natural calamity in the central region.

Inadequate return from agriculture and natural calamity are ranked IV and V in the

northern region.

Table 6.2.9: Repayment and Related Problems – Mean Score and Rank –Region

Problems South Central North

Mean Score Rank Mean

Score Rank Mean Score Rank

1. Waiver Syndrome/ OTS Policy of the Government 3.36 II 2.74 II 3.25 II

2. Intentional Failure of the Borrowers 2.55 V 2.3 IV 2.92 III

3. Natural Calamity and Crop Failure 2.89 III 2.07 V 2.17 V

4. Inadequate Return of Agricultural Activity 2.72 IV 2.52 III 2.62 IV

5. Absence of Incentive/ Subsidy for Prompt Repayment 3.61 I 3.33 I 3.54 I

Mean 3.03 -- 2.59 -- 2.9 --

Source: Primary data

In order to verify whether there is any significant difference among the

selected banks from the three regions in the problems faced by them with regard to

repayment of agricultural loans, one-way ANOVA is carried out at one per cent

level of significance and the result is shown in Table 6.2.10.

Table 6.2.10: Mean Score Difference in Repayment and Related Problems One-way ANOVA

Region N Mean SD. F P- Value

South 36 15.14 2.54

5.938 0.004* Central 27 12.96 2.36

North 24 14.50 2.61

*Significant at 1 per cent level

271

ANOVA result shows that there is significant difference in repayment and

related problems faced by the commercial banks across the different regions of the

State.

Overdue and Related Problems Overdue means debt not repaid within the scheduled time. The amount of

loan not repaid as per the schedule of repayment is considered as overdue. In

agricultural financing, the bankers have to face some overdue-related problems.

The opinion of the respondents relating to the overdue and related problems was

analyzed on the basis of the identified problems. The identified overdue and

related-problems of the bank officials in agricultural lending are:

1. Complicated recovery procedures

2. High share of agricultural NPA

3. Lack of sufficient support from Government agencies

4. Ineffective insurance/ compensation on calamities

5. Social/ political influence on recovery of agricultural loans

For the recovery of the agricultural loans, the banker has to follow some

intricate procedures. The procedures involve sending of notice to the defaulter as a

step for revenue recovery. There are many procedural formalities in this process

that should be followed by the banker.

Lending to Agriculture is prioritized; therefore, the banker has to face some

NPA problems. In order to meet the target obligations, the banks have to lend

agricultural advances without effective security and therefore, they have to face

some NPA problems.

For the effective realization of the loan amount, the banker has to obtain the

support of the Government agencies especially for the revenue recovery. In most

cases, the banks have to face some difficulties due to the ineffective support of the

Government machinery.

272

Effective insurance coverage against natural calamities and crop failure are

essential requirements, especially for perennial and annual crops. In Kerala, there

is no such false- proof insurance coverage/ compensation package. This leads to

many problems in repayment performance of the loans.

Social and political influence on recovery of loans is another factor, which