chapter : measurement and reporting of revenues and expenses, gains and losses

TRANSCRIPT

Chapter : Measurement and Reporting of Revenues and Expenses , Gains and

Losses

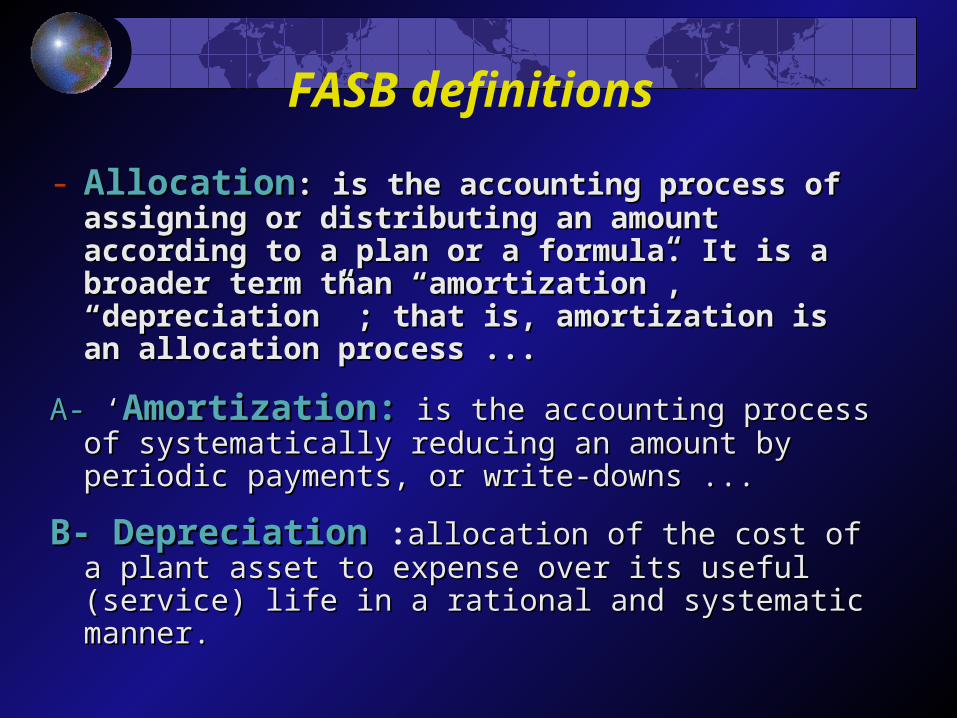

FASB definitions

- AllocationAllocation:: is the accounting process of is the accounting process of assigning or distributing an amount assigning or distributing an amount according to a plan or a formula. It is a according to a plan or a formula. It is a broader term than “amortization”, broader term than “amortization”, “depreciation” ; that is, amortization is an “depreciation” ; that is, amortization is an allocation process ...allocation process ...

A-A- ‘ ‘Amortization:Amortization: is the accounting process of is the accounting process of systematically reducing an amount by periodic systematically reducing an amount by periodic payments, or write-downs ... payments, or write-downs ...

B- Depreciation B- Depreciation :allocation of the cost of a allocation of the cost of a plant asset to expense over its useful (service) plant asset to expense over its useful (service) life in a rational and systematic manner.life in a rational and systematic manner.

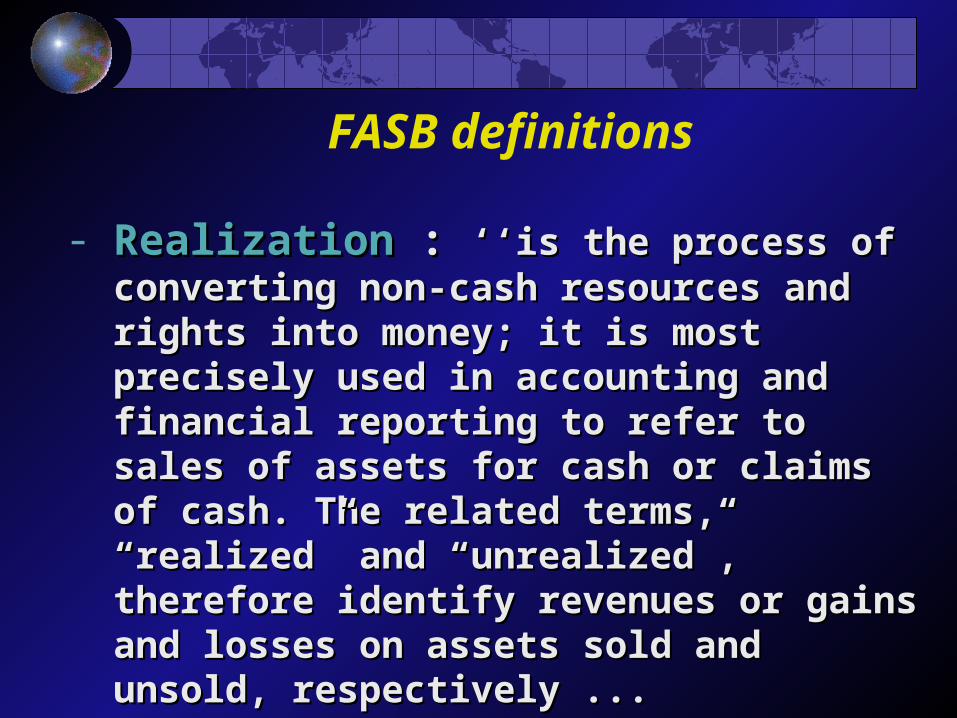

- RealizationRealization : : ‘‘is the process of ‘‘is the process of converting non-cash resources and converting non-cash resources and rights into money; it is most precisely rights into money; it is most precisely used in accounting and financial used in accounting and financial reporting to refer to sales of assets reporting to refer to sales of assets for cash or claims of cash. The related for cash or claims of cash. The related terms, “realized” and “unrealized”, terms, “realized” and “unrealized”, therefore identify revenues or gains therefore identify revenues or gains and losses on assets sold and unsold, and losses on assets sold and unsold, respectively ... respectively ...

FASB definitions

FASB definitions

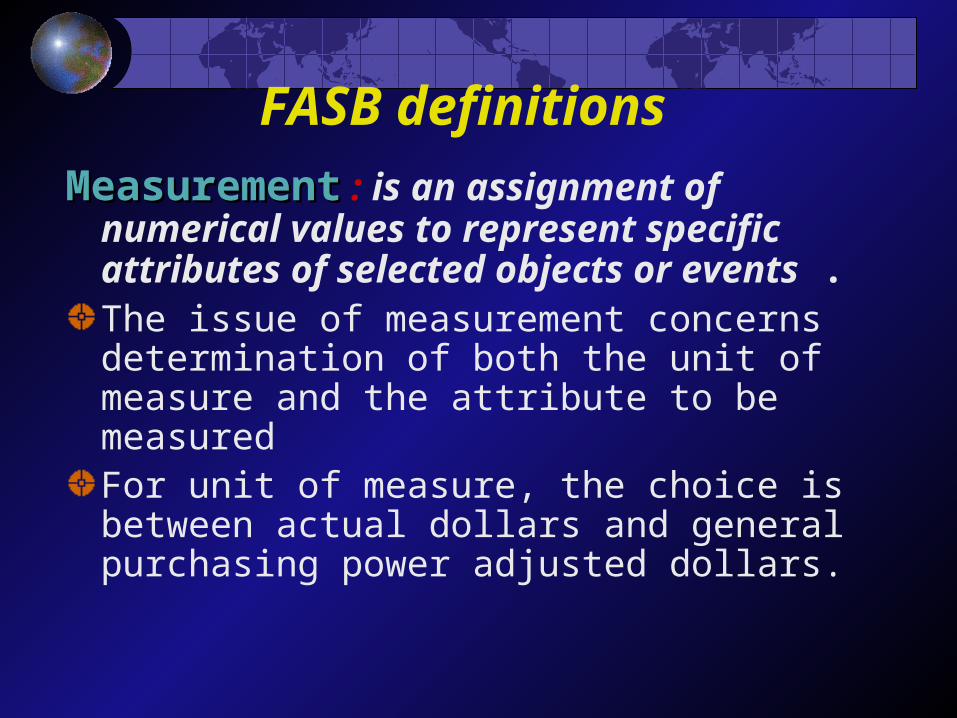

MeasurementMeasurement : is an assignment of numerical values to represent specific attributes of selected objects or events .The issue of measurement concerns determination of both the unit of measure and the attribute to be measuredFor unit of measure, the choice is between actual dollars and general purchasing power adjusted dollars.

Revenue:

- The definition :revenues. N. Increases in income from the main business activities of a company. Revenue is measured as the dollar amount received for activities such as selling products or performing services.

See page 247 -248

Revenue:

- Component of Revenue

There are two views regarding this subject :

1-According to the asset/liability view, revenues are defined as increases in the assets or decreases in the liabilities that do not affect capital.

Revenue:

- Component of Revenue

2- According to the revenue/expense view, revenues result from the sale of goods and services and include gains from the sale and exchange of assets other than inventories, interests and dividends earned on investments, and other increases in owners’ equity during a period other than capital contributions and adjustments

Revenue:

- Measurement of Revenue

- Revenue is measured by the exchange value of the product or service of the enterprise .

- This value represents either the net cash equivalent or the present discounted value of money claims to be received eventually from the revenue transaction.

Revenue:

- The Timing of Revenue Recognition:

dictates that revenue should be recognized in the accounting period in which it is earned.

• When a sale is involved, generally revenue is recognized at the point of sale.

See page 249-250

Revenue:

1- PERCENTAGE-OF-COMPLETION METHOD

2- INSTALLMENT METHOD

PERCENTAGE-OF-COMPLETION METHOD OF REVENUE RECOGNITION

• In long-term construction contracts, revenue recognition is usually required before the contract is completed.

• The percentage-of-completion method recognizes revenue on the basis of reasonable estimates of progress toward completion.

• A project’s progress toward completion is measured by comparing the costs incurred in a year to total estimated costs of the entire project.

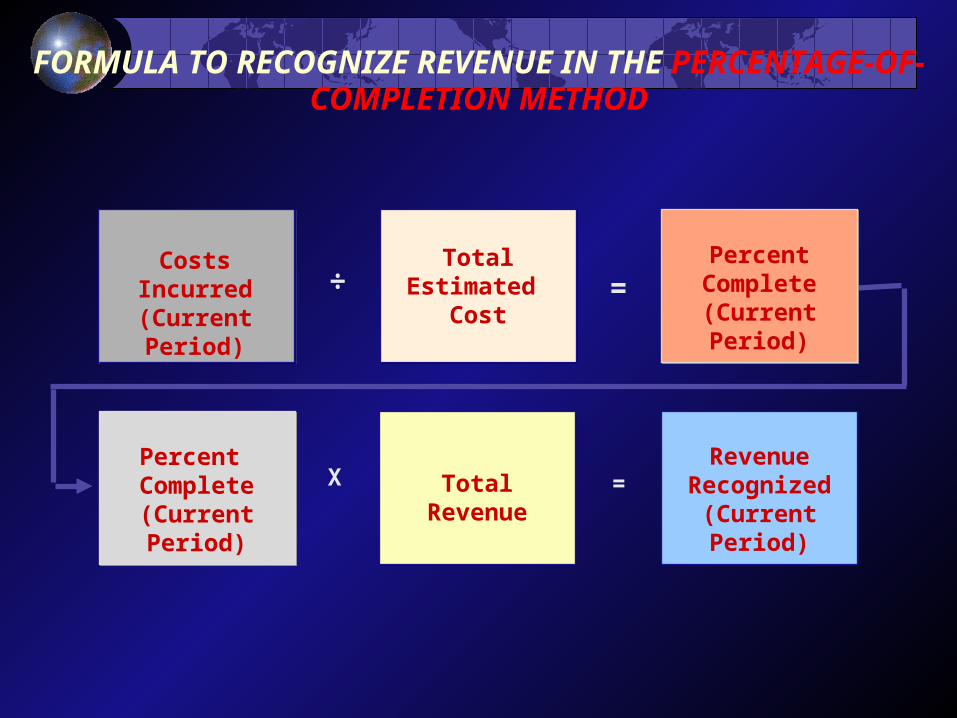

FORMULA TO RECOGNIZE REVENUE IN THE PERCENTAGE-OF-COMPLETION METHOD

Costs Incurred(Current Period)

÷ =Total

Estimated Cost

PercentComplete(Current Period)

Total RevenueX =Revenue

Recognized(Current Period)

Percent Complete(Current Period)

FORMULA TO COMPUTE GROSS PROFITIN CURRENT PERIOD

Cost Incurred(Current Period)

- =Gross ProfitRecognized

(Current Period)

RevenueRecognized

(Current Period)

The costs incurred in the current period are then subtracted from the revenue recognized during the current period to arrive at the gross profit.

The costs incurred in the current period are then subtracted from the revenue recognized during the current period to arrive at the gross profit.

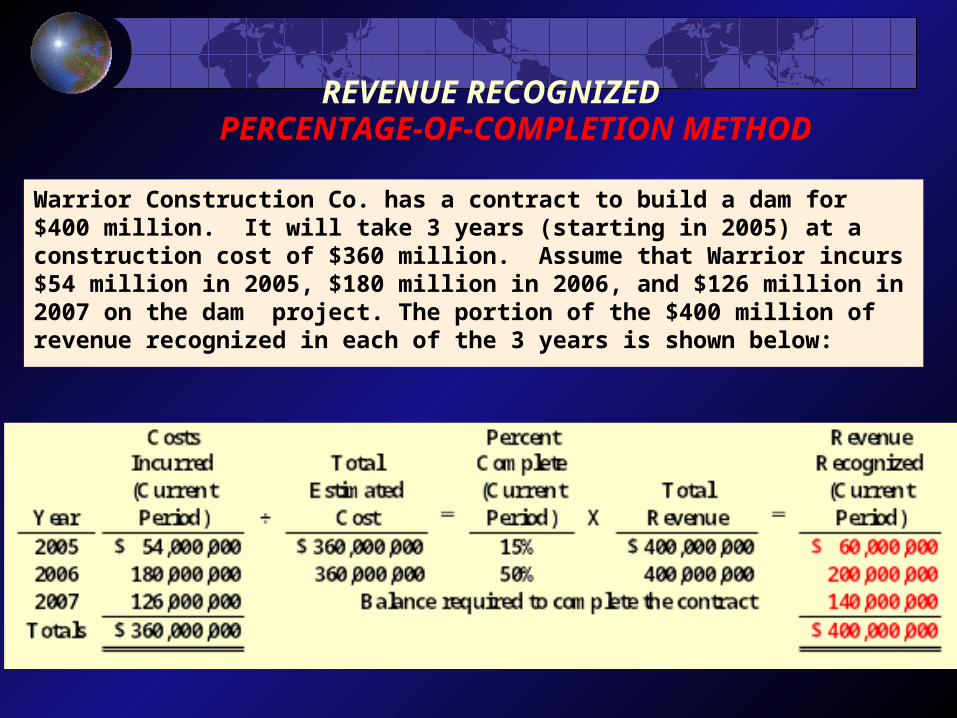

Warrior Construction Co. has a contract to build a dam for $400 million. It will take 3 years (starting in 2005) at a construction cost of $360 million. Assume that Warrior incurs $54 million in 2005, $180 million in 2006, and $126 million in 2007 on the dam project. The portion of the $400 million of revenue recognized in each of the 3 years is shown below:

REVENUE RECOGNIZED PERCENTAGE-OF-COMPLETION METHOD

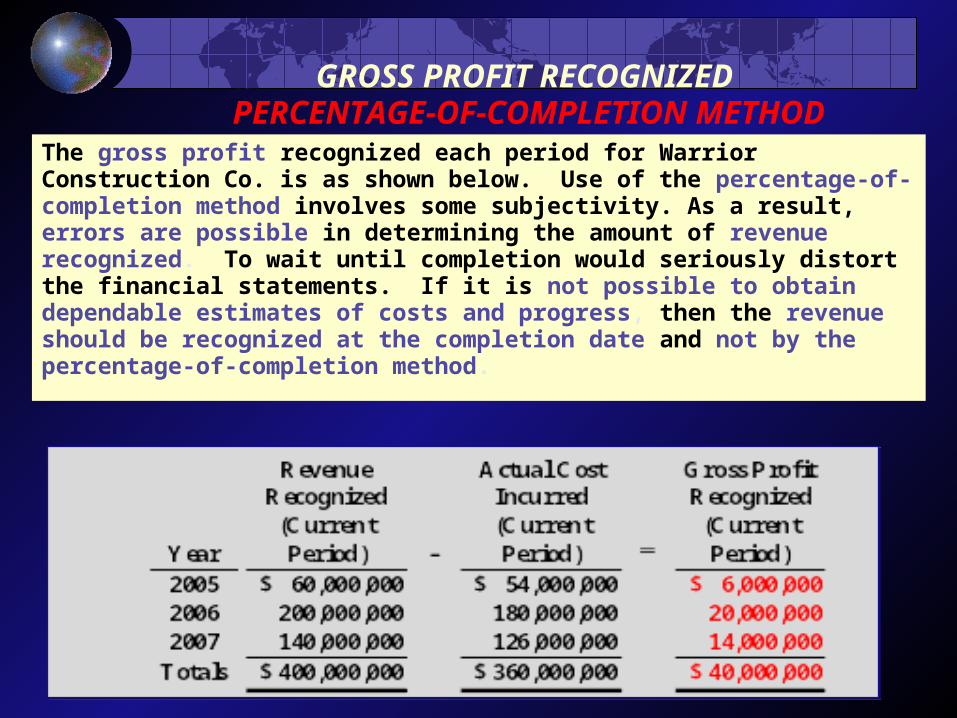

The gross profit recognized each period for Warrior Construction Co. is as shown below. Use of the percentage-of-completion method involves some subjectivity. As a result, errors are possible in determining the amount of revenue recognized. To wait until completion would seriously distort the financial statements. If it is not possible to obtain dependable estimates of costs and progress, then the revenue should be recognized at the completion date and not by the percentage-of-completion method.

GROSS PROFIT RECOGNIZED PERCENTAGE-OF-COMPLETION METHOD