chapter 4. understanding interest rates present value yield to maturity other yields other...

Post on 21-Dec-2015

225 views

TRANSCRIPT

Chapter 4. Understanding Interest Chapter 4. Understanding Interest RatesRatesChapter 4. Understanding Interest Chapter 4. Understanding Interest RatesRates

• Present Value

• Yield to Maturity

• Other Yields

• Other Measurement Issues

• Present Value

• Yield to Maturity

• Other Yields

• Other Measurement Issues

I. Measuring Interest RatesI. Measuring Interest RatesI. Measuring Interest RatesI. Measuring Interest Rates

A. Credit Market Instruments

• simple loan borrower pays back loan and

interest in one lump sum

A. Credit Market Instruments

• simple loan borrower pays back loan and

interest in one lump sum

• fixed-payment loan loan is repaid with equal (monthly)

payments each payment is combination of

principal and interest

• fixed-payment loan loan is repaid with equal (monthly)

payments each payment is combination of

principal and interest

• coupon bond purchase price (P) interest payments (6 months) face value at maturity (F) size of interest payments

-- coupon rate

-- face value

• coupon bond purchase price (P) interest payments (6 months) face value at maturity (F) size of interest payments

-- coupon rate

-- face value

• discount bond zero coupon bond purchased price less than face

value

-- F > P face value at maturity no interest payments

• discount bond zero coupon bond purchased price less than face

value

-- F > P face value at maturity no interest payments

B. Present & Future ValueB. Present & Future ValueB. Present & Future ValueB. Present & Future Value

• time value of money

• $100 today vs. $100 in 1 year not indifferent! money earns interest over time, and we prefer consuming today

• time value of money

• $100 today vs. $100 in 1 year not indifferent! money earns interest over time, and we prefer consuming today

example: future valueexample: future valueexample: future valueexample: future value

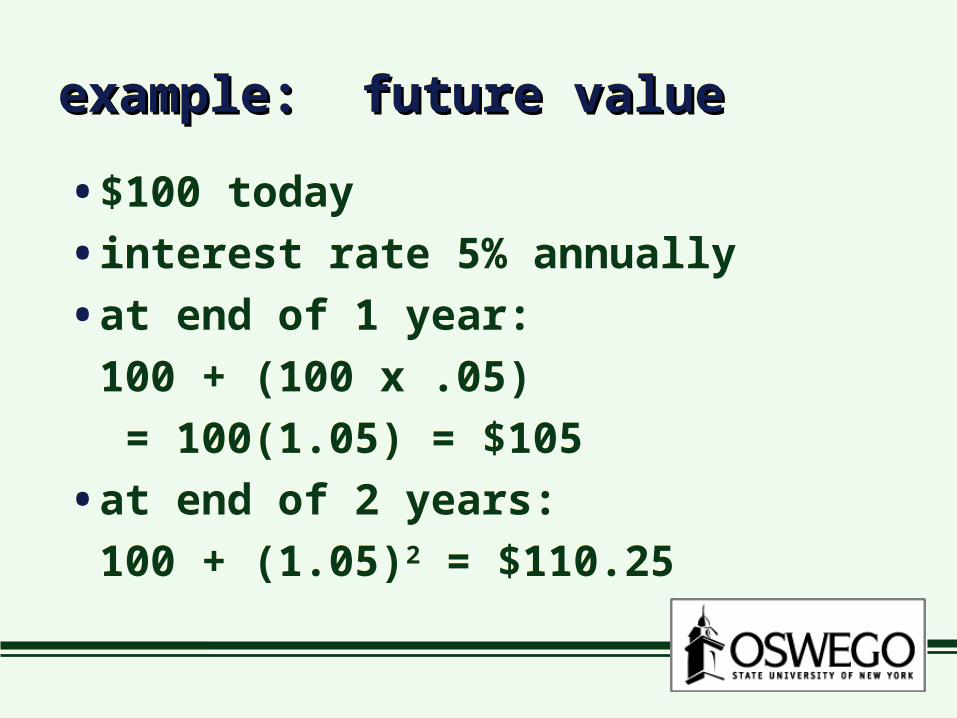

• $100 today

• interest rate 5% annually

• at end of 1 year:

100 + (100 x .05)

= 100(1.05) = $105

• at end of 2 years:

100 + (1.05)2 = $110.25

• $100 today

• interest rate 5% annually

• at end of 1 year:

100 + (100 x .05)

= 100(1.05) = $105

• at end of 2 years:

100 + (1.05)2 = $110.25

future valuefuture valuefuture valuefuture value

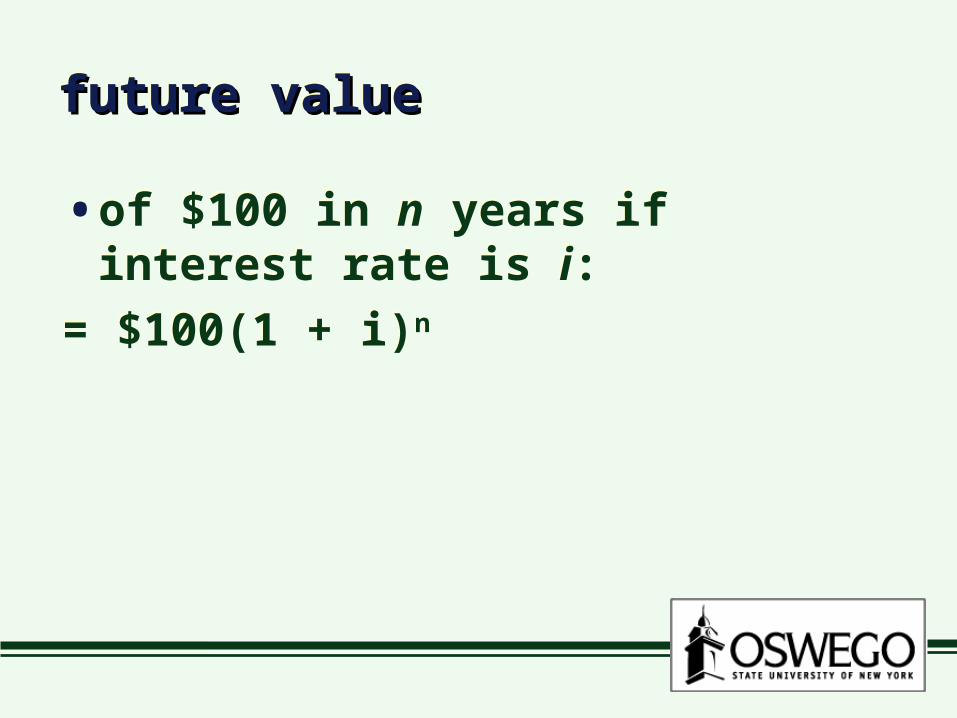

• of $100 in n years if interest rate is i:

= $100(1 + i)n • of $100 in n years if interest rate is i:

= $100(1 + i)n

present valuepresent valuepresent valuepresent value

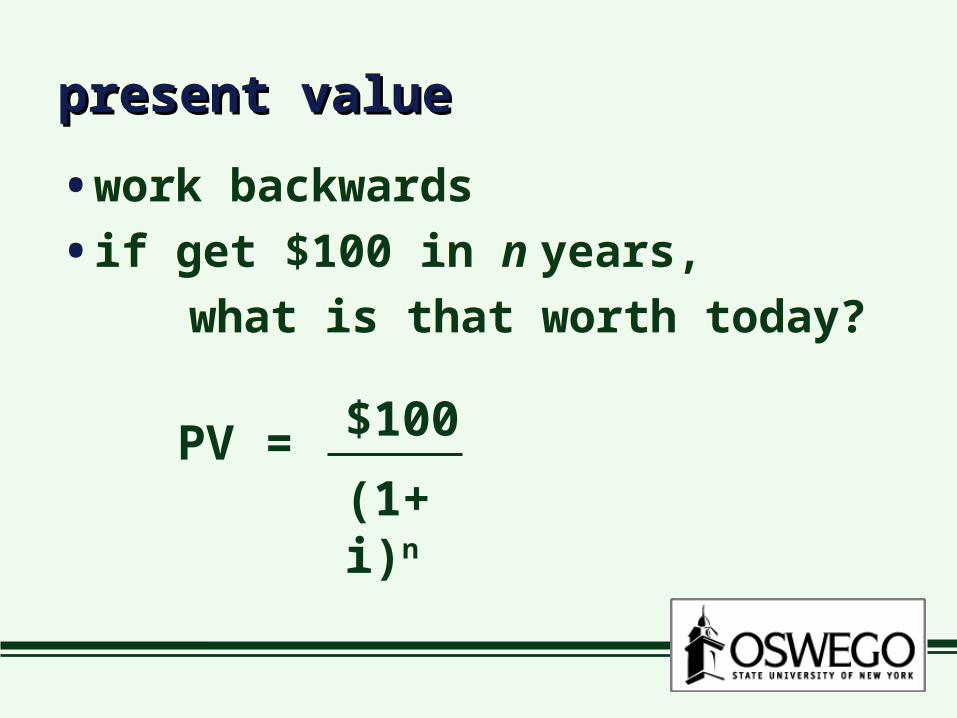

• work backwards

• if get $100 in n years,

what is that worth today?

• work backwards

• if get $100 in n years,

what is that worth today?

PV = $100

(1+ i)n

exampleexampleexampleexample

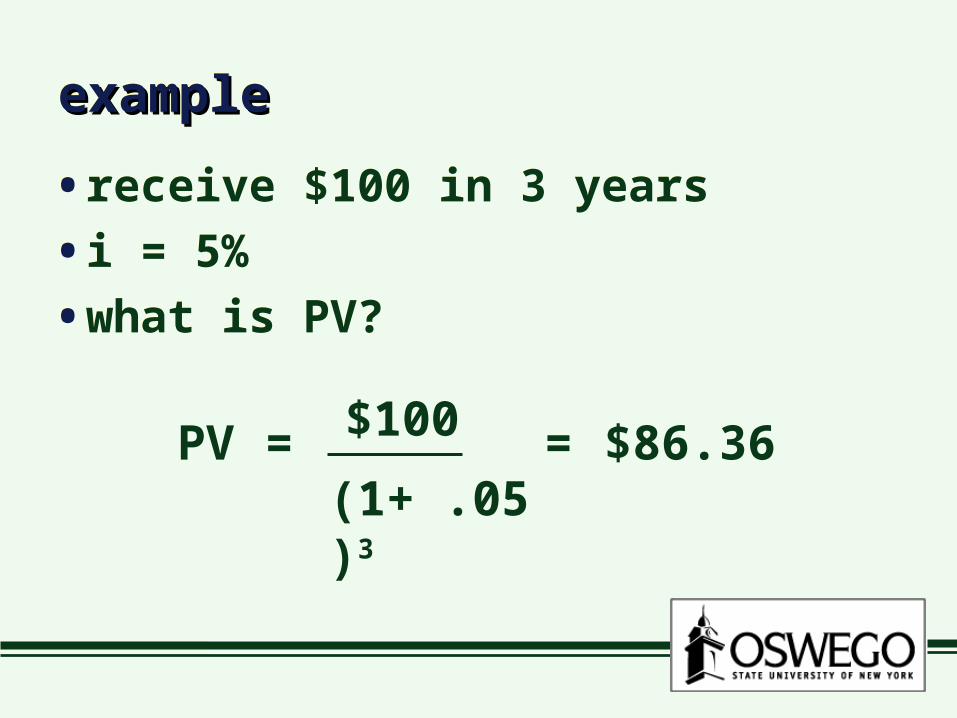

• receive $100 in 3 years

• i = 5%

• what is PV?

• receive $100 in 3 years

• i = 5%

• what is PV?

PV = $100

(1+ .05)3

= $86.36

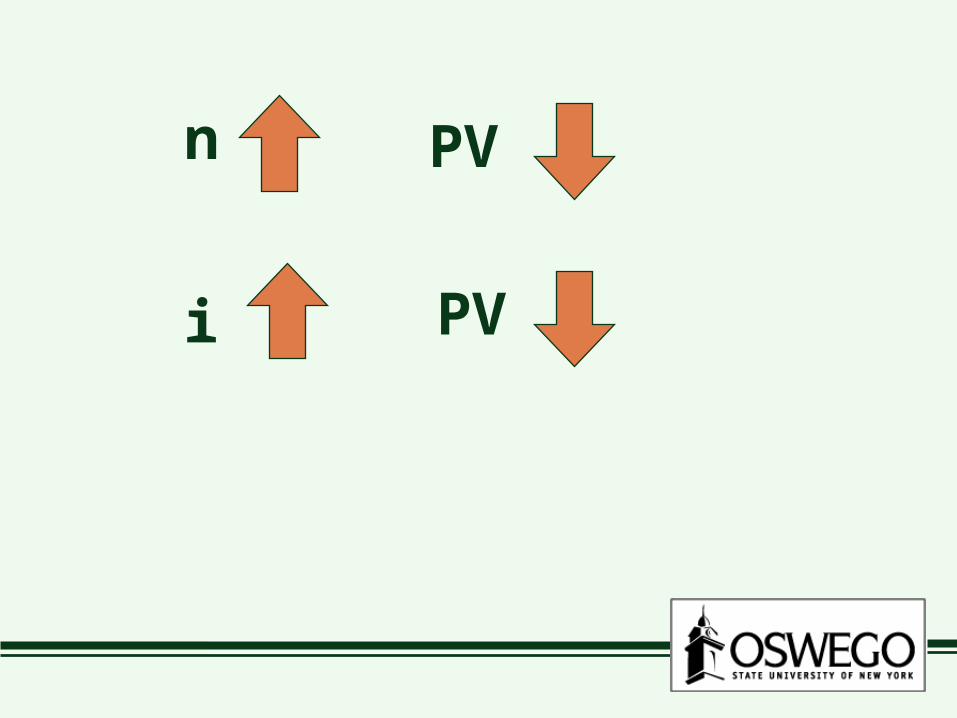

n

i

PV

PV

C. Yield to Maturity (YTM)C. Yield to Maturity (YTM)C. Yield to Maturity (YTM)C. Yield to Maturity (YTM)

• a measure of interest rate

• interest rate where• a measure of interest rate

• interest rate where

P = PV of cash flows

example 1: simple loanexample 1: simple loanexample 1: simple loanexample 1: simple loan

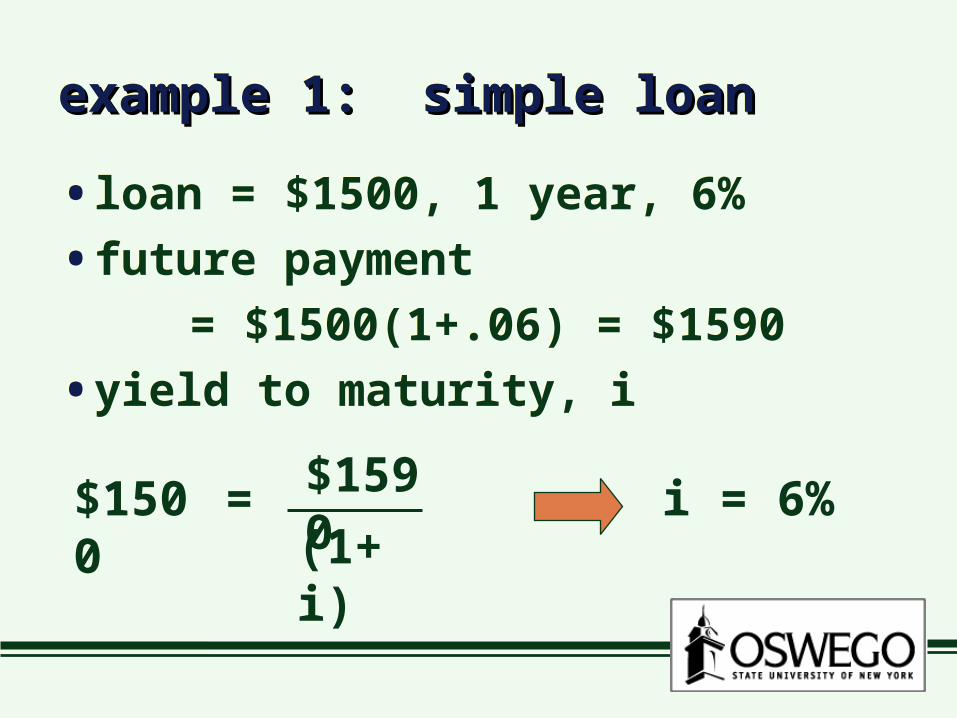

• loan = $1500, 1 year, 6%

• future payment

= $1500(1+.06) = $1590

• yield to maturity, i

• loan = $1500, 1 year, 6%

• future payment

= $1500(1+.06) = $1590

• yield to maturity, i

$1500 = $1590

(1+ i)i = 6%

example 2: fixed pmt. loanexample 2: fixed pmt. loanexample 2: fixed pmt. loanexample 2: fixed pmt. loan

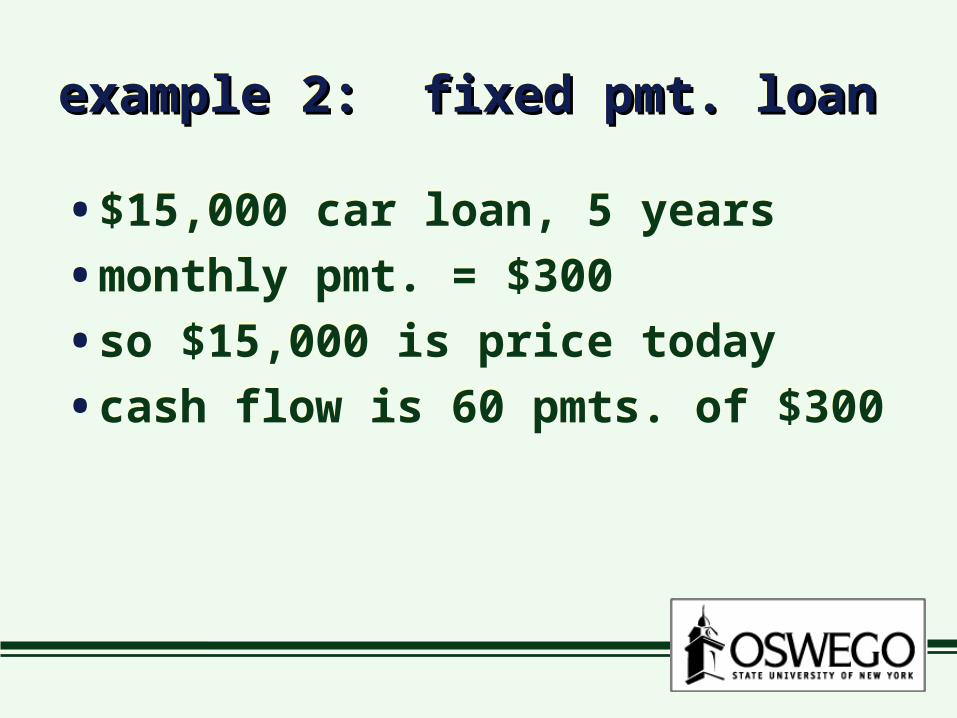

• $15,000 car loan, 5 years

• monthly pmt. = $300

• so $15,000 is price today

• cash flow is 60 pmts. of $300

• $15,000 car loan, 5 years

• monthly pmt. = $300

• so $15,000 is price today

• cash flow is 60 pmts. of $300

• YTM solves• YTM solves

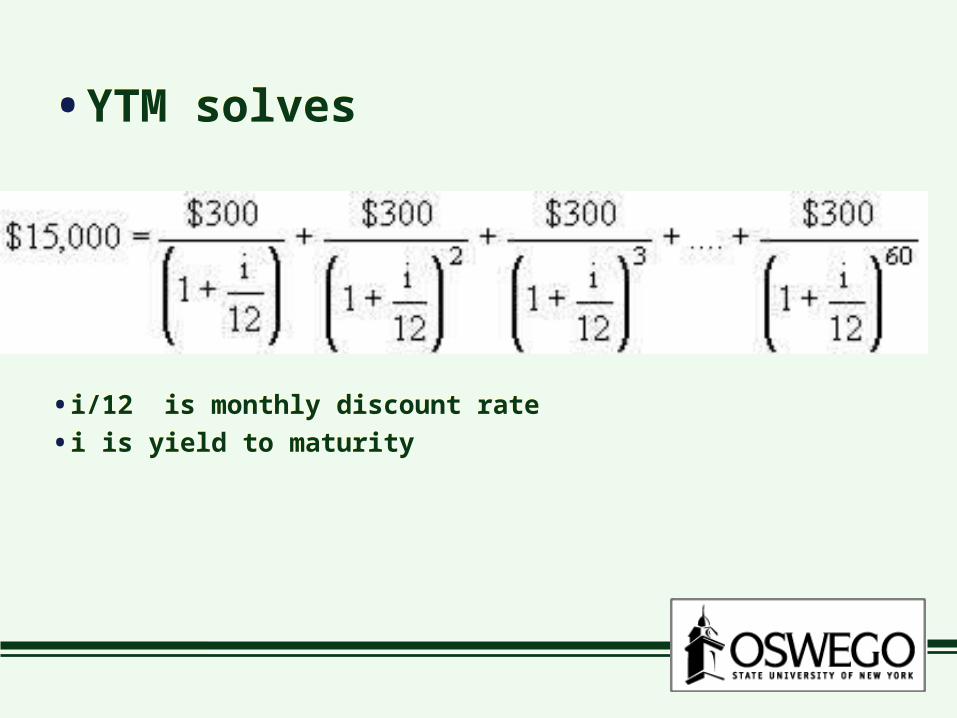

• i/12 is monthly discount rate

• i is yield to maturity• i/12 is monthly discount rate

• i is yield to maturity

• how to solve for i? trial-and-error bond table* financial calculator spreadsheet

• how to solve for i? trial-and-error bond table* financial calculator spreadsheet

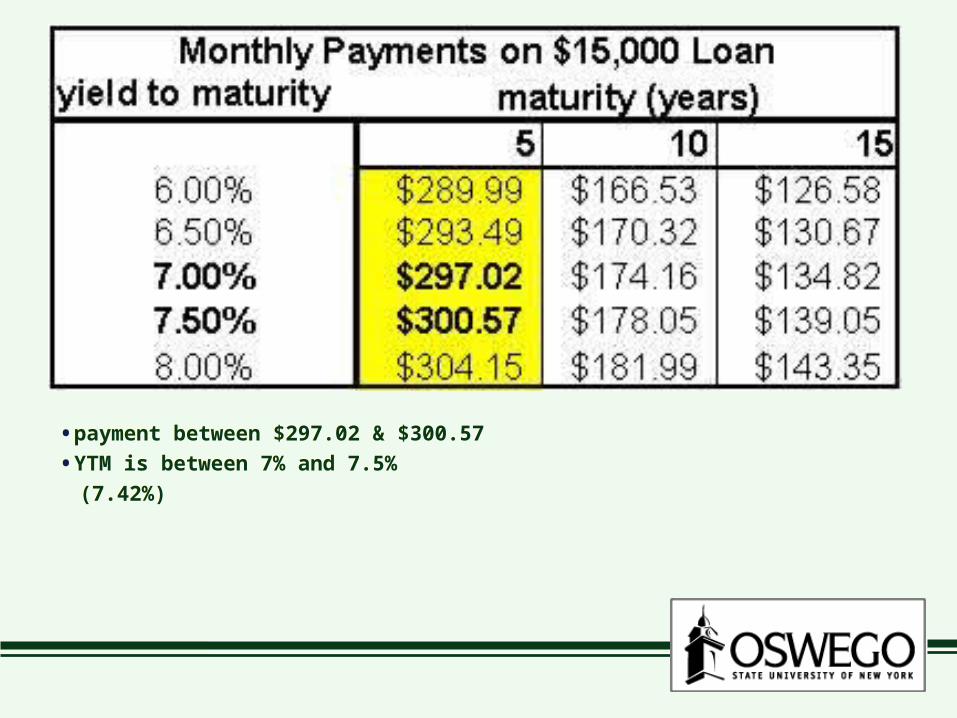

• payment between $297.02 & $300.57

• YTM is between 7% and 7.5%

(7.42%)

• payment between $297.02 & $300.57

• YTM is between 7% and 7.5%

(7.42%)

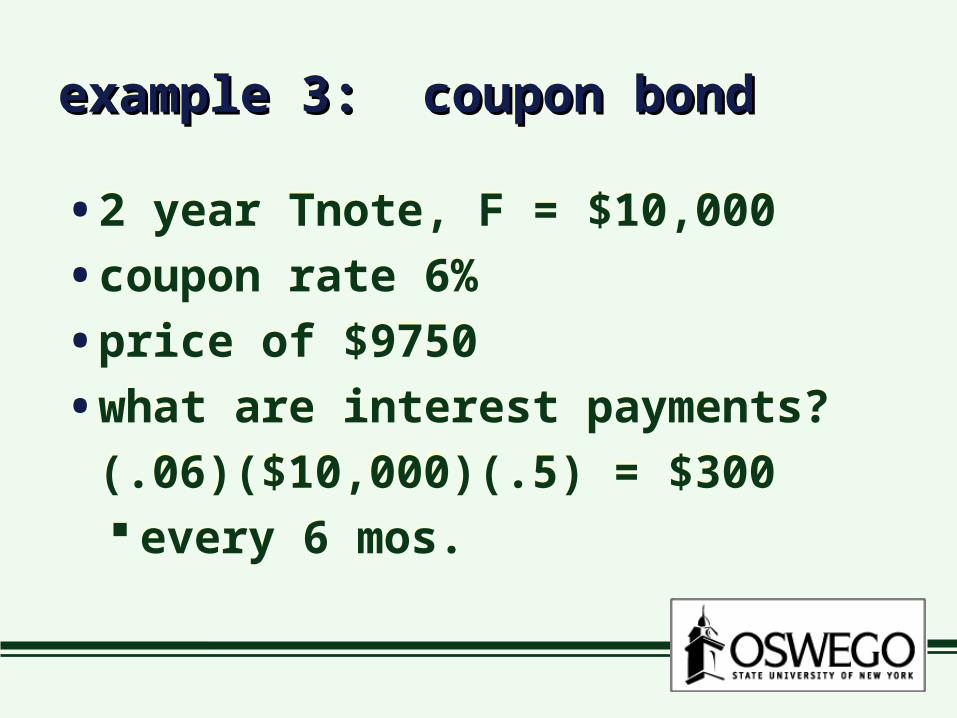

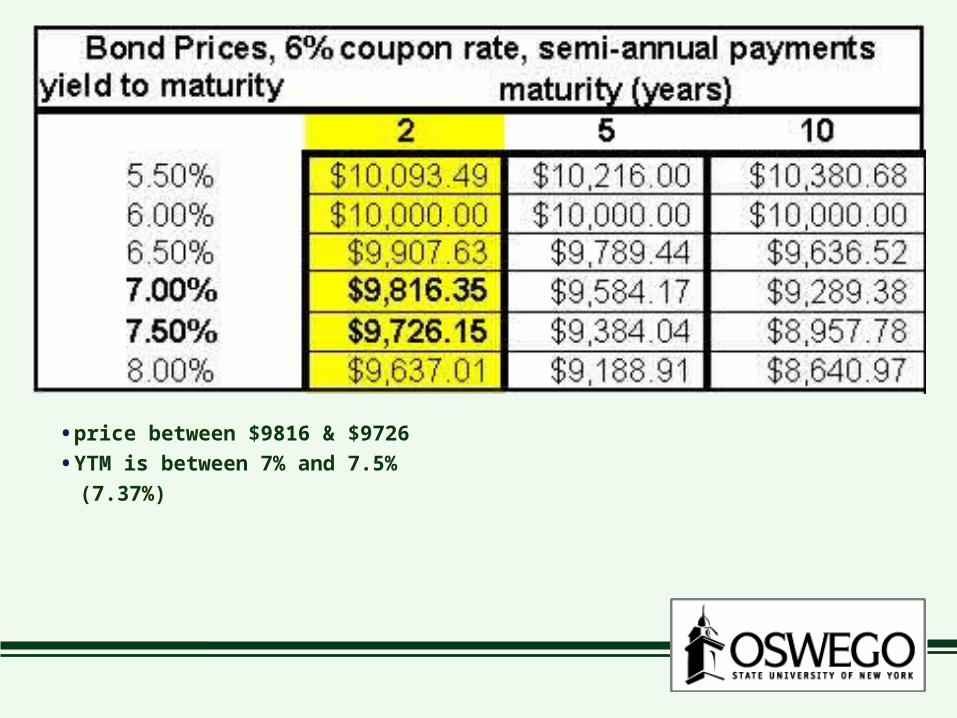

example 3: coupon bondexample 3: coupon bondexample 3: coupon bondexample 3: coupon bond

• 2 year Tnote, F = $10,000

• coupon rate 6%

• price of $9750

• what are interest payments?

(.06)($10,000)(.5) = $300 every 6 mos.

• 2 year Tnote, F = $10,000

• coupon rate 6%

• price of $9750

• what are interest payments?

(.06)($10,000)(.5) = $300 every 6 mos.

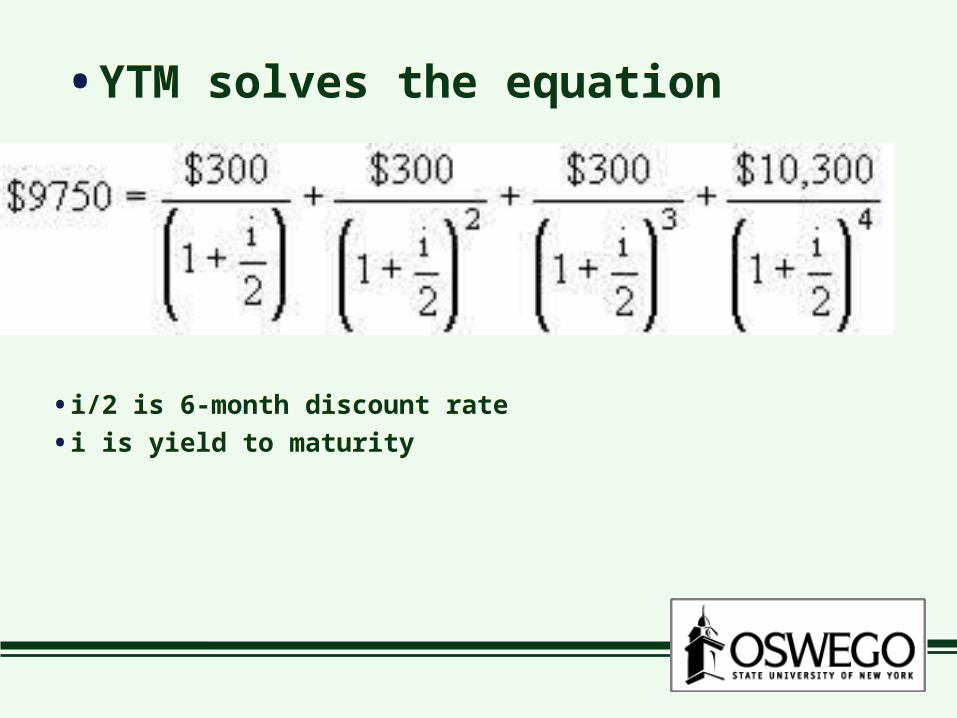

• YTM solves the equation• YTM solves the equation

• i/2 is 6-month discount rate

• i is yield to maturity• i/2 is 6-month discount rate

• i is yield to maturity

• price between $9816 & $9726

• YTM is between 7% and 7.5%

(7.37%)

• price between $9816 & $9726

• YTM is between 7% and 7.5%

(7.37%)

P, F and YTMP, F and YTMP, F and YTMP, F and YTM

• P = F then YTM = coupon rate

• P < F then YTM > coupon rate bond sells at a discount

• P > F then YTM < coupon rate bond sells at a premium

• P = F then YTM = coupon rate

• P < F then YTM > coupon rate bond sells at a discount

• P > F then YTM < coupon rate bond sells at a premium

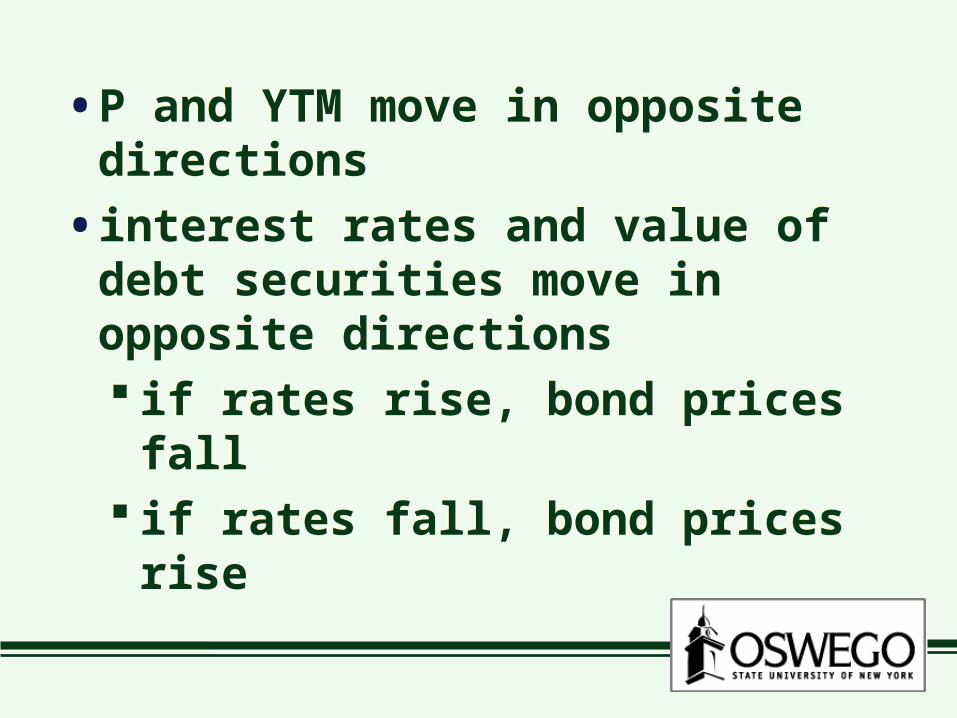

• P and YTM move in opposite directions

• interest rates and value of debt securities move in opposite directions if rates rise, bond prices fall if rates fall, bond prices rise

• P and YTM move in opposite directions

• interest rates and value of debt securities move in opposite directions if rates rise, bond prices fall if rates fall, bond prices rise

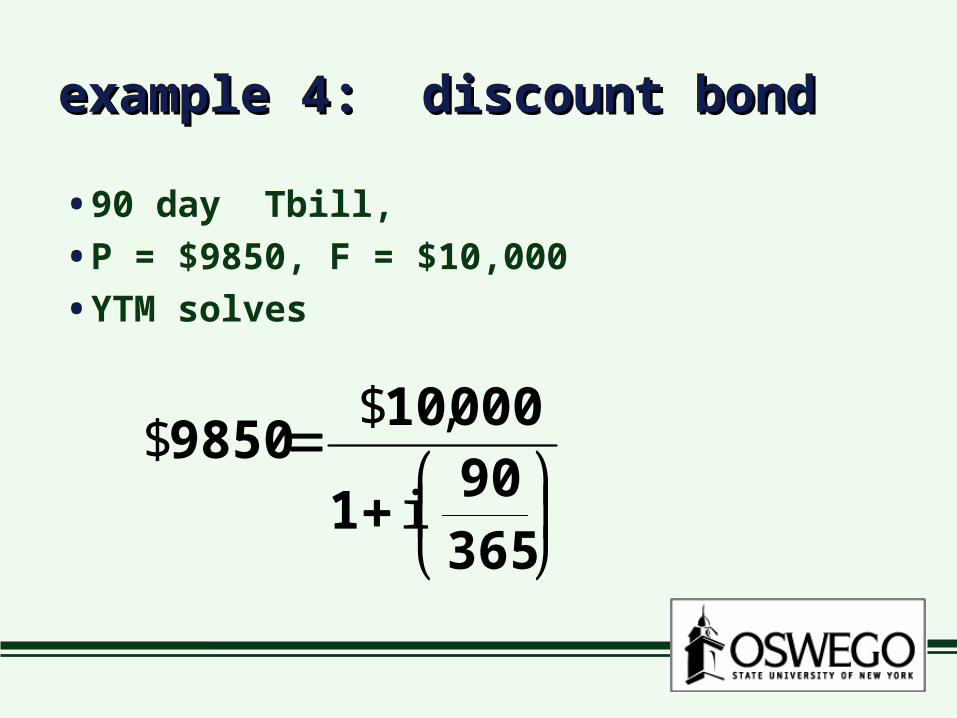

example 4: discount bondexample 4: discount bondexample 4: discount bondexample 4: discount bond

• 90 day Tbill,

• P = $9850, F = $10,000

• YTM solves

• 90 day Tbill,

• P = $9850, F = $10,000

• YTM solves

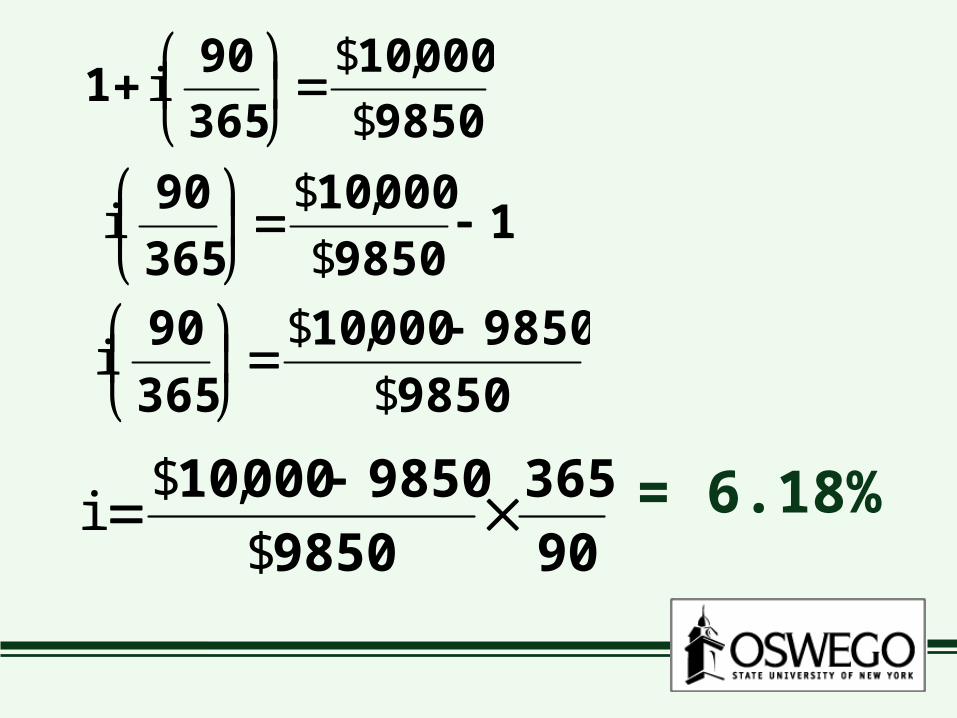

36590

1

000109850

i

,$$

9850

00010

365

901

$

,$i

19850

00010

365

90

$

,$i

9850

985000010

365

90

$

,$i

90

365

9850

985000010

$

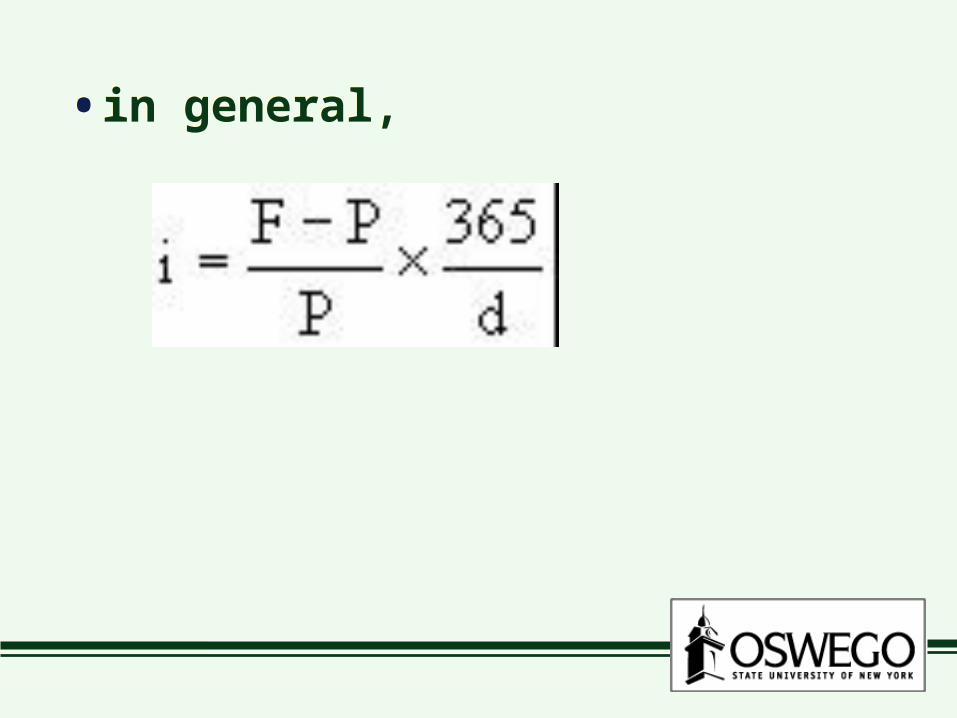

,$i = 6.18%

• in general,• in general,

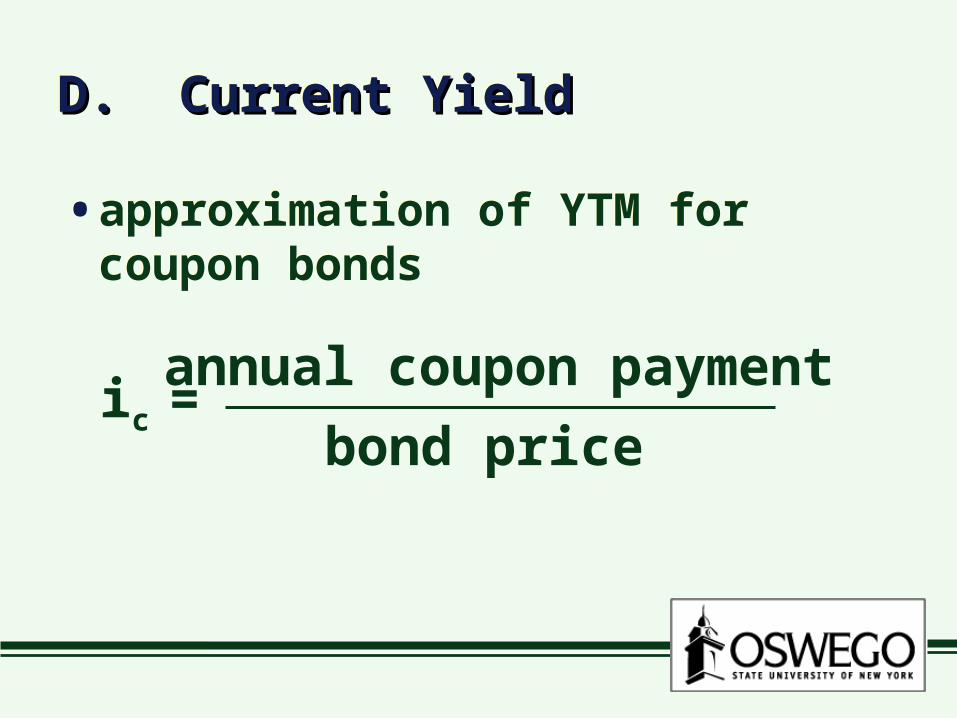

D. Current YieldD. Current YieldD. Current YieldD. Current Yield

• approximation of YTM for coupon bonds• approximation of YTM for coupon

bonds

ic =annual coupon payment

bond price

• better approximation when maturity is longer P is close to F

• better approximation when maturity is longer P is close to F

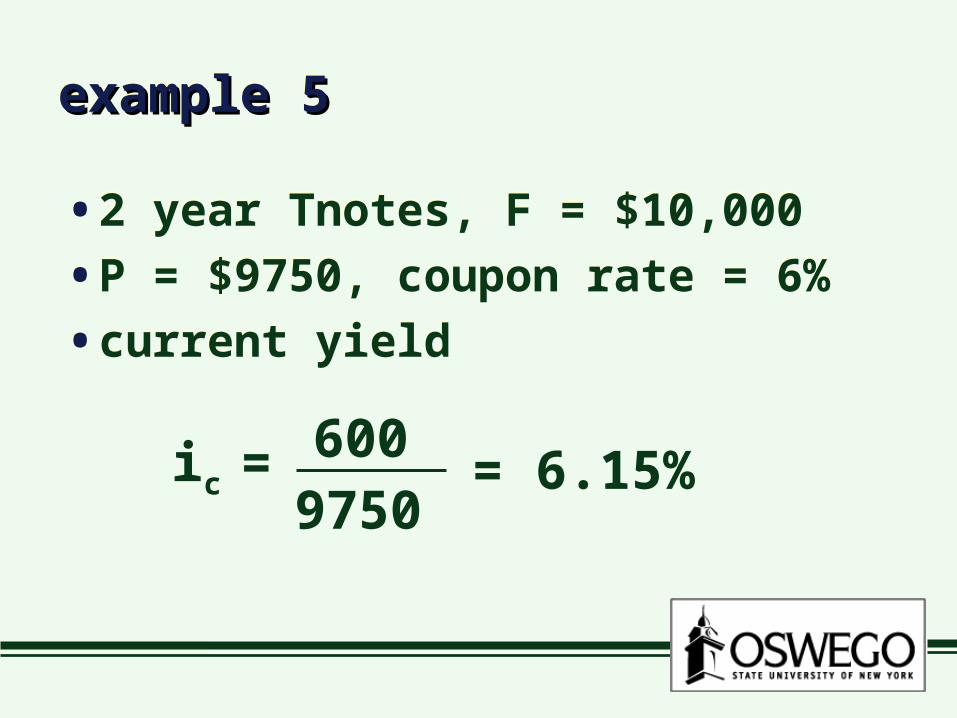

example 5example 5example 5example 5

• 2 year Tnotes, F = $10,000

• P = $9750, coupon rate = 6%

• current yield

• 2 year Tnotes, F = $10,000

• P = $9750, coupon rate = 6%

• current yield

ic =600

9750= 6.15%

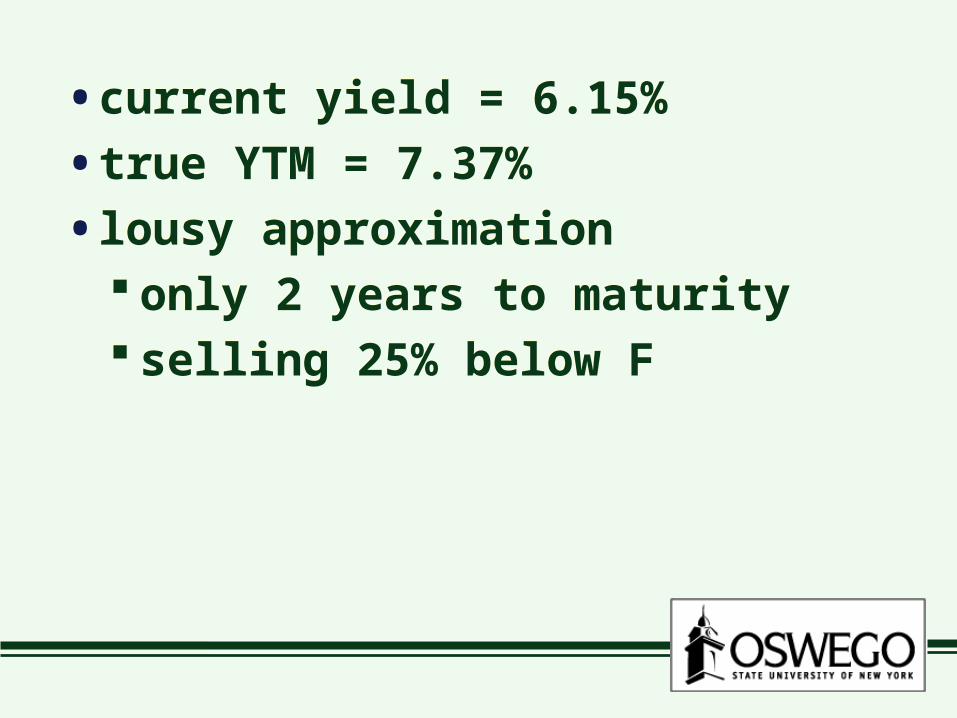

• current yield = 6.15%

• true YTM = 7.37%

• lousy approximation only 2 years to maturity selling 25% below F

• current yield = 6.15%

• true YTM = 7.37%

• lousy approximation only 2 years to maturity selling 25% below F

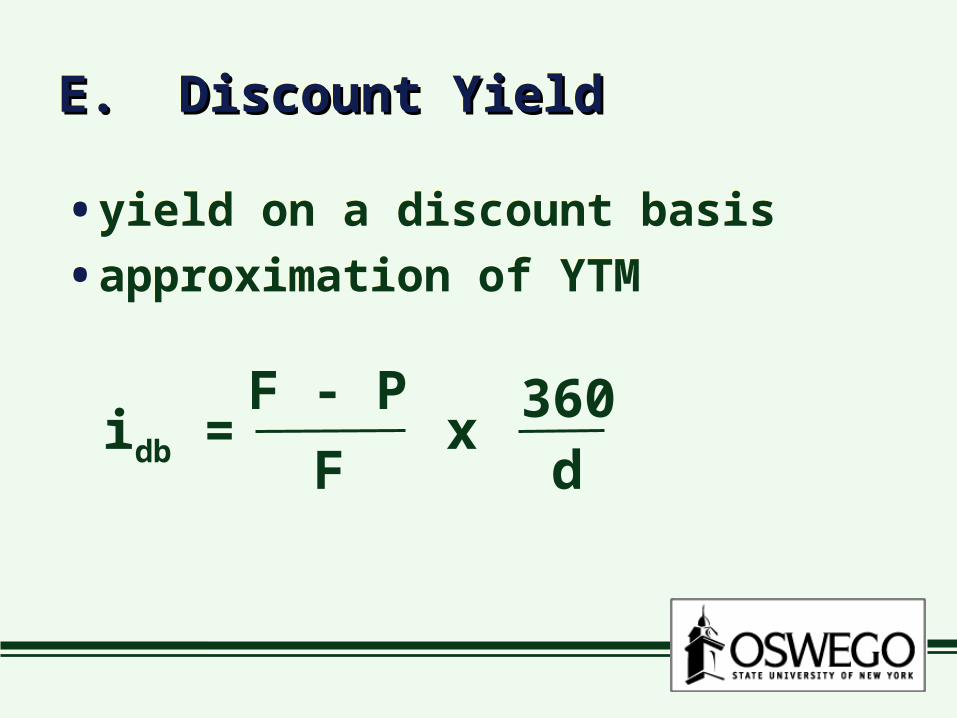

E. Discount YieldE. Discount YieldE. Discount YieldE. Discount Yield

• yield on a discount basis

• approximation of YTM• yield on a discount basis

• approximation of YTM

idb = F - P

Fx

360d

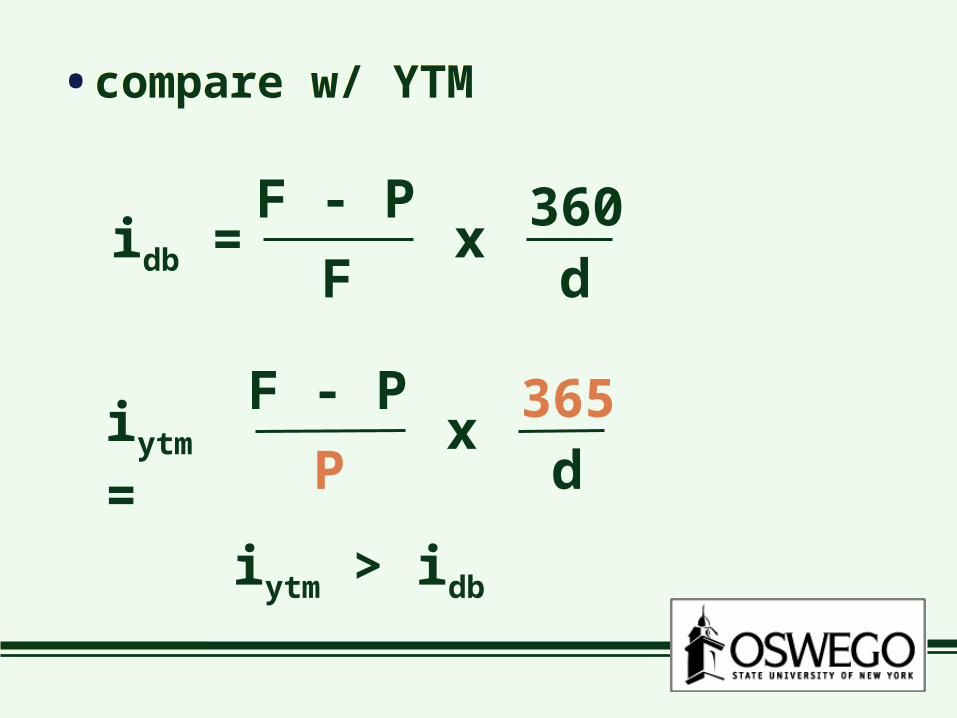

• compare w/ YTM• compare w/ YTM

idb = F - P

Fx

360d

iytm = F - P

Px

365d

iytm > idb

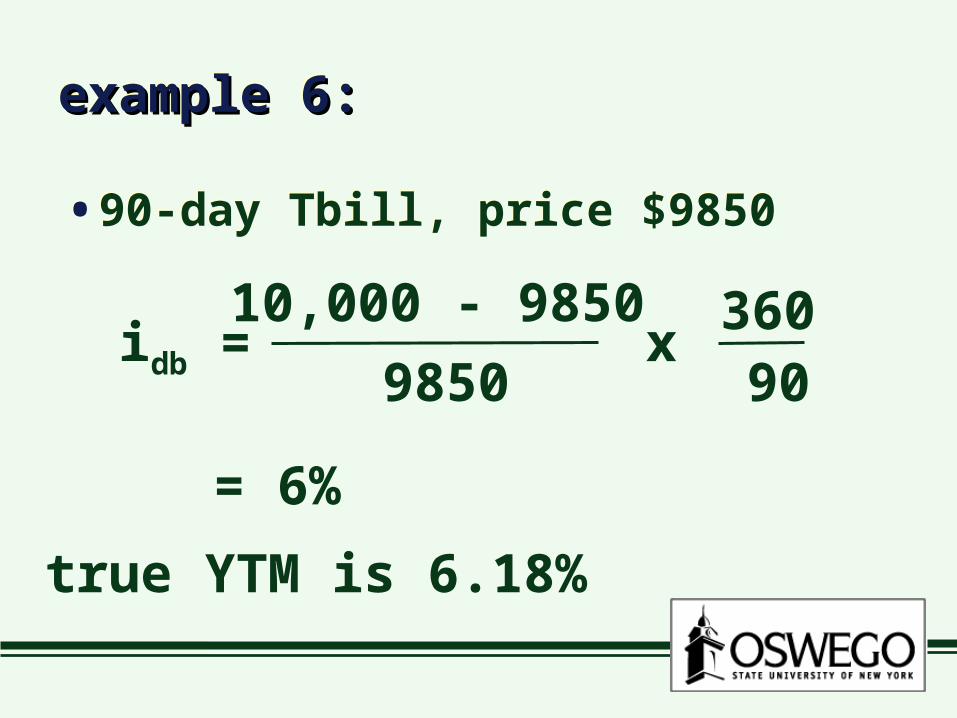

example 6:example 6:example 6:example 6:

• 90-day Tbill, price $9850• 90-day Tbill, price $9850

idb = 10,000 - 9850

9850x

36090

= 6%

true YTM is 6.18%

II. Other measurement issuesII. Other measurement issuesII. Other measurement issuesII. Other measurement issues

A. Interest rates vs. return

• YTM assumes bond is held until maturity

• if not, resale price is important

A. Interest rates vs. return

• YTM assumes bond is held until maturity

• if not, resale price is important

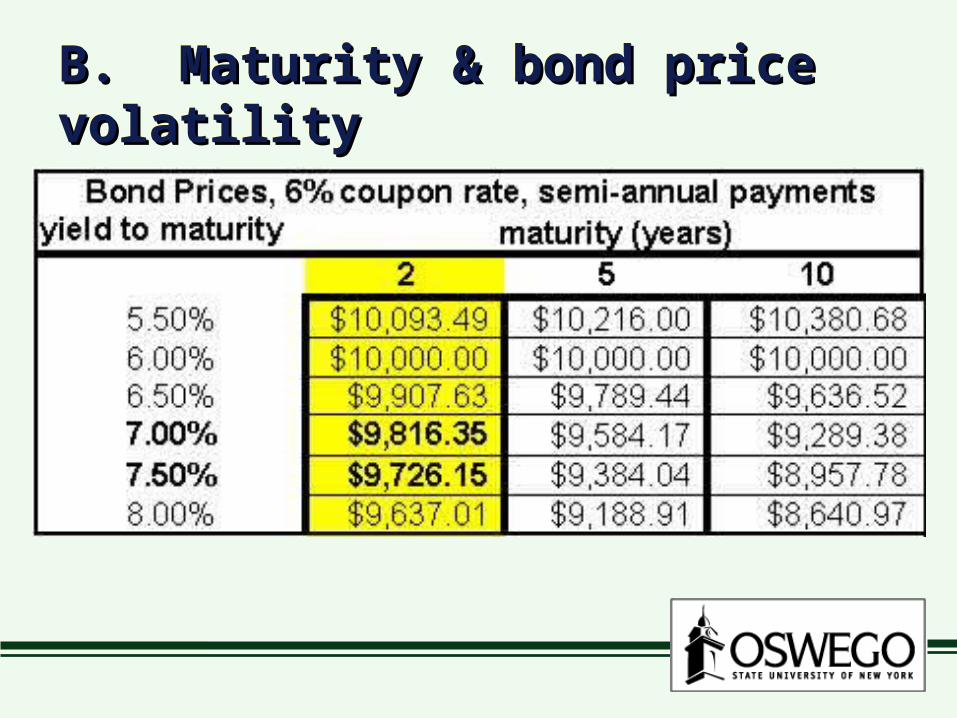

B. Maturity & bond price volatilityB. Maturity & bond price volatilityB. Maturity & bond price volatilityB. Maturity & bond price volatility

• YTM rises from 6 to 8% bond prices fall but 10-year bond price falls the

most

• Prices are more volatile for longer maturities long-term bonds have greater

interest rate risk

• YTM rises from 6 to 8% bond prices fall but 10-year bond price falls the

most

• Prices are more volatile for longer maturities long-term bonds have greater

interest rate risk

• Why? long-term bonds “lock in” a

coupon rate for a longer time if interest rates rise

-- stuck with a below-market coupon rate

if interest rates fall

-- receiving an above-market coupon rate

• Why? long-term bonds “lock in” a

coupon rate for a longer time if interest rates rise

-- stuck with a below-market coupon rate

if interest rates fall

-- receiving an above-market coupon rate

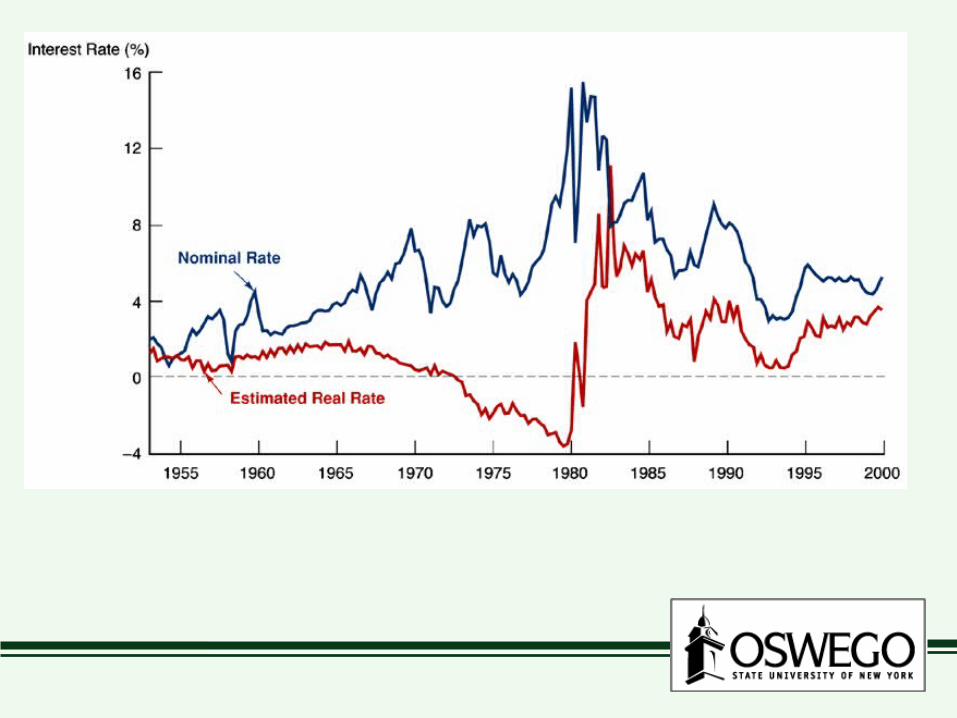

C. Real vs. Nominal Interest RatesC. Real vs. Nominal Interest RatesC. Real vs. Nominal Interest RatesC. Real vs. Nominal Interest Rates

• thusfar we have calculated nominal interest rates ignores effects of rising inflation

• thusfar we have calculated nominal interest rates ignores effects of rising inflation

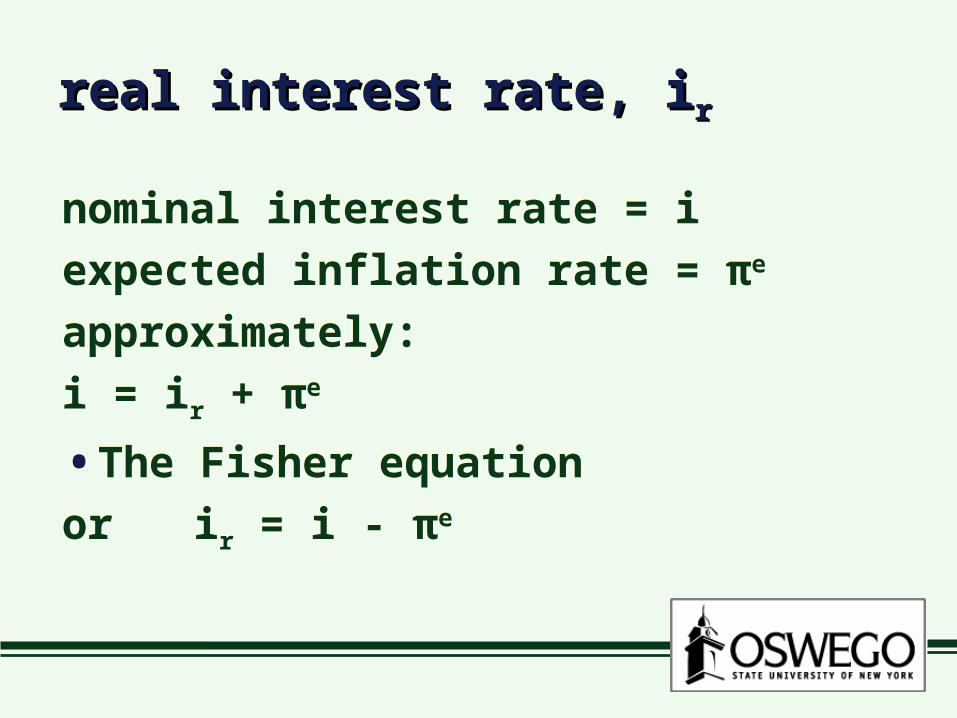

real interest rate, ireal interest rate, irrreal interest rate, ireal interest rate, irr

nominal interest rate = i

expected inflation rate = πe

approximately:

i = ir + πe

• The Fisher equation

or ir = i - πe

nominal interest rate = i

expected inflation rate = πe

approximately:

i = ir + πe

• The Fisher equation

or ir = i - πe

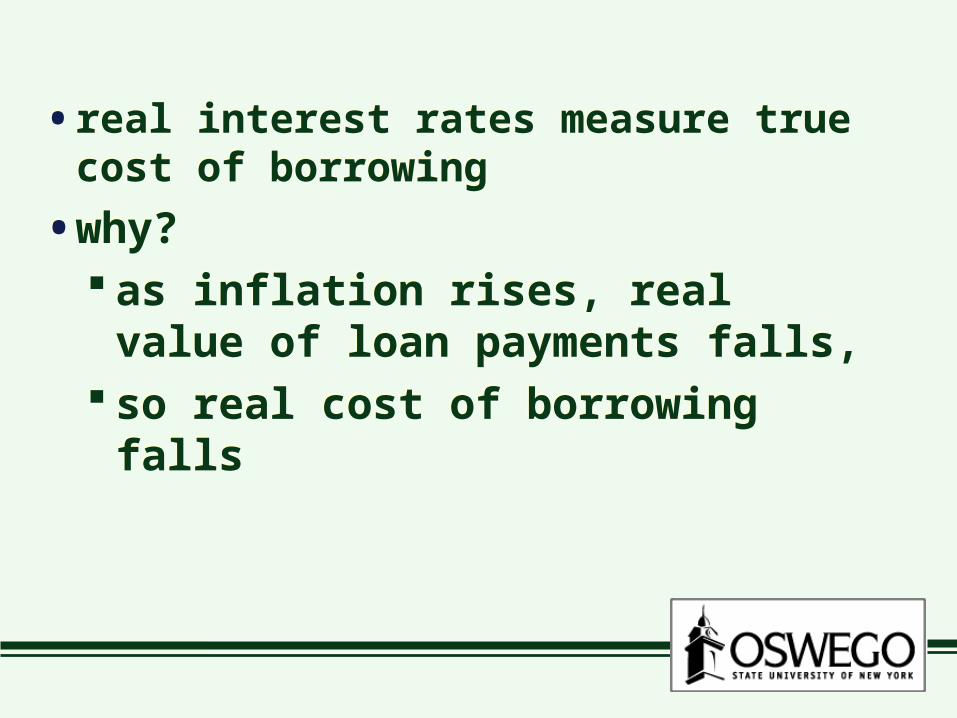

• real interest rates measure true cost of borrowing

• why? as inflation rises, real value of loan

payments falls, so real cost of borrowing falls

• real interest rates measure true cost of borrowing

• why? as inflation rises, real value of loan

payments falls, so real cost of borrowing falls