chapter 15 capital budgetingfaculty.business.utsa.edu/sasthana/sharad/public/acc3123/solmanua… ·...

TRANSCRIPT

426 © 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly

accessible website, in whole or in part.

CHAPTER 15

CAPITAL BUDGETING

21. a. Payback = $3,000,000 ÷ $600,000 per year = 5 years

b. Year Amount Cumulative Amount

1 $300,000 $ 300,000

2 300,000 600,000

3 300,000 900,000

4 300,000 1,200,000

5 300,000 1,500,000

6 400,000 1,900,000

7 400,000 2,300,000

8 400,000 2,700,000

9 400,000 3,100,000

10 400,000 3,500,000

The payback is eight years plus [(3,000,000 – 2,700,000) ÷ 400,000] or 8.75

years.

22. a. Investment = $140,000 + $180,000 = $320,000

Year Amount Cumulative Amount

1 $70,000 $ 70,000

2 78,000 148,000

3 72,000 220,000

4 56,000 276,000

5 50,000 326,000

6 48,000 374,000

7 44,000 418,000

Payback = 4 years + [($320,000 – $276,000) ÷ $50,000] = 4.9 years

Based on the payback criterion, Houston Fashions should not invest in the pro-

posed product line.

b. Yes. Houston Fashions should also use a discounted cash flow technique so as

to consider both the time value of money and the cash flows that occur after the

payback period.

23. Point in Time Cash Flows PV Factor Present Value

0 $(1,800,000) 1.0000 $(1,800,000)

1 280,000 0.8929 250,012

2 280,000 0.7972 223,216

3 340,000 0.7118 242,012

4 340,000 0.6355 216,070

5 340,000 0.5674 192,916

6 288,800 0.5066 146,306

7 288,800 0.4524 130,653

8 288,800 0.4039 116,646

9 260,000 0.3606 93,756

Chapter 15 427

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly

accessible website, in whole or in part.

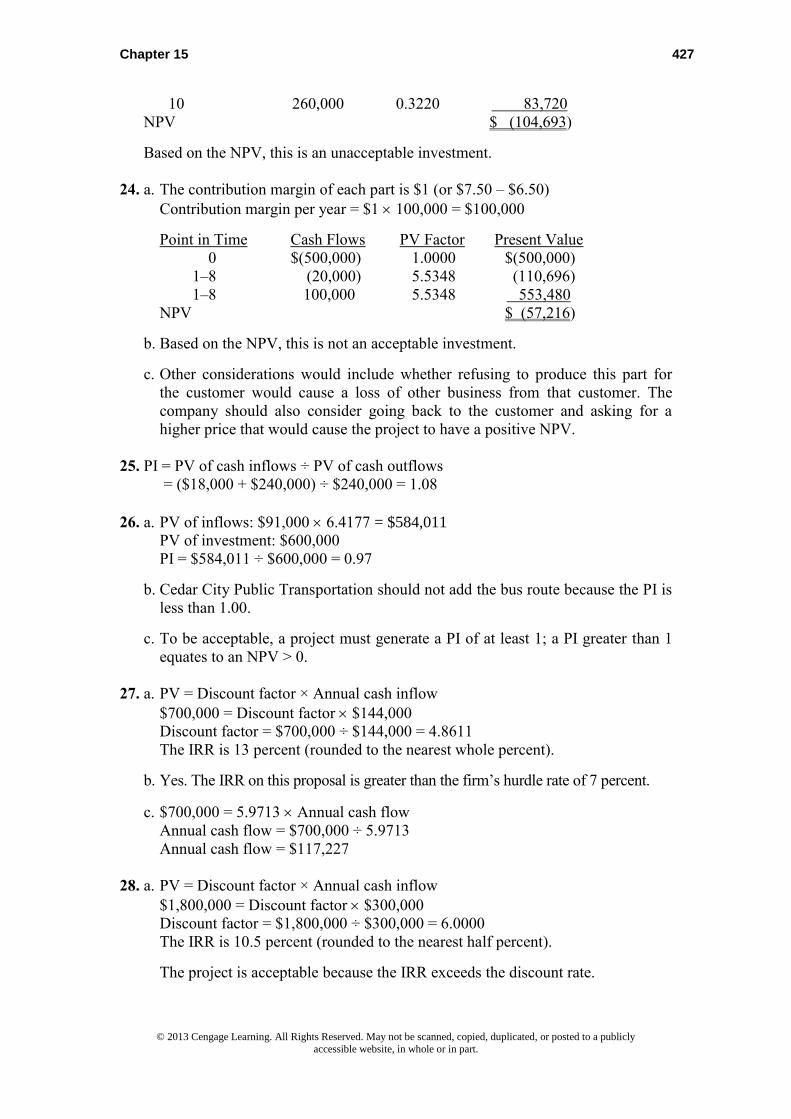

10 260,000 0.3220 83,720

NPV $ (104,693)

Based on the NPV, this is an unacceptable investment.

24. a. The contribution margin of each part is $1 (or $7.50 – $6.50)

Contribution margin per year = $1 100,000 = $100,000

Point in Time Cash Flows PV Factor Present Value

0 $(500,000) 1.0000 $(500,000)

1–8 (20,000) 5.5348 (110,696)

1–8 100,000 5.5348 553,480

NPV $ (57,216)

b. Based on the NPV, this is not an acceptable investment.

c. Other considerations would include whether refusing to produce this part for

the customer would cause a loss of other business from that customer. The

company should also consider going back to the customer and asking for a

higher price that would cause the project to have a positive NPV.

25. PI = PV of cash inflows ÷ PV of cash outflows

= ($18,000 + $240,000) ÷ $240,000 = 1.08

26. a. PV of inflows: $91,000 6.4177 = $584,011

PV of investment: $600,000

PI = $584,011 ÷ $600,000 = 0.97

b. Cedar City Public Transportation should not add the bus route because the PI is

less than 1.00.

c. To be acceptable, a project must generate a PI of at least 1; a PI greater than 1

equates to an NPV > 0.

27. a. PV = Discount factor × Annual cash inflow

$700,000 = Discount factor $144,000

Discount factor = $700,000 ÷ $144,000 = 4.8611

The IRR is 13 percent (rounded to the nearest whole percent).

b. Yes. The IRR on this proposal is greater than the firm’s hurdle rate of 7 percent.

c. $700,000 = 5.9713 Annual cash flow

Annual cash flow = $700,000 ÷ 5.9713

Annual cash flow = $117,227

28. a. PV = Discount factor × Annual cash inflow

$1,800,000 = Discount factor $300,000

Discount factor = $1,800,000 ÷ $300,000 = 6.0000

The IRR is 10.5 percent (rounded to the nearest half percent).

The project is acceptable because the IRR exceeds the discount rate.

428 Chapter 15

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly

accessible website, in whole or in part.

b. The main qualitative factors would be the effect of the technology on the per-

ceived quality of the food that is processed by the new machinery. An addition-

al consideration would be the effect of the technology on employees,

particularly if the investment would cause layoffs.

29. Investment cost = $375,000 × Discount factor for 14%, 7 years

= $375,000 × 4.2883 = $1,608,113

NPV = $375,000 × Discount factor (10%, 7 years) – $1,608,113

= ($375,000 × 4.8684) – $1,608,113 = $217,537

30. a. Annual depreciation = $1,000,000 ÷ 8 years = $125,000 per year

Tax benefit = $125,000 0.30 = $37,500

PV = $37,500 5.7466 = $215,498

b. Accelerated method

$1,000,000 0.30 0.40 0.9259 = $111,108

$600,000 0.30 0.40 0.8573 = 61,726

$360,000 0.30 0.40 0.7938 = 34,292

$216,000 0.30 0.40 0.7350 = 19,051

$129,600* 0.30 0.6806 = 26,462

Total $252,639

*In the final year, the remaining undepreciated cost is expensed.

c. The depreciation benefit computed in (b) exceeds that computed in (a) solely

because of the time value of money. The depreciation method in (b) allows for

faster recapture of the cost; therefore, there is less discounting of the future cash

flows.

35. a NPV PI IRR

Film studios $3,578,910 1.18 13.03%

Cameras & equipment 1,067,920 1.33 18.62

Land improvement 2,250,628 1.45 19.69

Motion picture #1 1,040,276 1.06 12.26

Motion picture #2 1,026,008 1.09 14.09

Motion picture #3 3,197,320 1.40 21.32

Corporate aircraft 518,916 1.22 18.15

b. Ranking according to:

NPV PI IRR

1. Film studios Land improvement MP #3

2. MP #3 MP #3 Land improvement

3. Land improvement Cameras & equip. Cameras & equip.

4. Cameras & equip. Corp. aircraft Corp. aircraft

5. MP #1 Film studios MP #2

6. MP #2 MP #2 Film studios

7. Corp. aircraft MP #1 MP #1

c. Suggested purchases: NPV

1. Motion picture #3 @ $8,000,000 $3,197,320

2. Land improvement @ $5,000,000 2,250,628

Chapter 15 429

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly

accessible website, in whole or in part.

3. Cameras & equipment @ $3,200,000 1,067,920

4. Corporate aircraft @ $2,400,000 518,916

Total NPV $7,034,784

35. a. Project Name NPV PI IRR

Film studios $3,578,910 1.18 13.03%

Cameras & equipment 1,067,920 1.33 18.62

Land improvement 2,250,628 1.45 19.69

Motion picture #1 1,040,276 1.06 12.26

Motion picture #2 1,026,008 1.09 14.09

Motion picture #3 3,197,320 1.40 21.32

Corporate aircraft 518,916 1.22 18.15

d. Ranking according to:

NPV PI IRR

8. Film studios Land improvement MP #3

9. MP #3 MP #3 Land improvement

10. Land improvement Cameras & equip. Cameras & equip.

11. Cameras & equip. Corp. aircraft Corp. aircraft

12. MP #1 Film studios MP #2

13. MP #2 MP #2 Film studios

14. Corp. aircraft MP #1 MP #1

e. Suggested purchases: NPV

5. Motion picture #3 @ $8,000,000 $3,197,320

6. Land improvement @ $5,000,000 2,250,628

7. Cameras & equipment @ $3,200,000 1,067,920

8. Corporate aircraft @ $2,400,000 518,916

Total NPV $7,034,784

45. a. ($000s omitted)

t0 t1 t2 t3 t4 t5 t6 t7 t8 Investment –(190)

New CM 60 60 60 60 60 60 60 60

Oper. costs 0 –20 –27 –27 –27 –30 –30 –30 –33

Cash flow –(190) 40 33 33 33 30 30 30 27

b. Year Cash Flow Cumulative Cash Flow

1 $40,000 $ 40,000

2 33,000 73,000

3 33,000 106,000

4 33,000 139,000

5 30,000 169,000

6 30,000 199,000

Payback = 5 + [($190,000 – $169,000) ÷ $30,000] = 5.7 years

c. Time Cash Flow PV Factor for 8% Present Value

0 $(190,000) 1.0000 $(190,000)

1 40,000 0.9259 37,036

430 Chapter 15

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly

accessible website, in whole or in part.

2 33,000 0.8573 28,291

3 33,000 0.7938 26,195

4 33,000 0.7350 24,255

5 30,000 0.6806 20,418

6 30,000 0.6302 18,906

7 30,000 0.5835 17,505

8 27,000 0.5403 14,588

NPV $ (2,806)

46. a. Time: t0 t1 t2 t3 t4 t5 t6 t7

Amount: ($41,000) $5,900 $8,100 $8,300 $8,000 $8,000 $8,300 $9,200

b. Year Cash Flow Cumulative

1 $5,900 $ 5,900

2 8,100 14,000

3 8,300 22,300

4 8,000 30,300

5 8,000 38,300

6 8,300 46,600

Payback = 5 years + [($41,000 – $38,300) ÷ $8,300] = 5.3 years

c. Cash Flow Discount Present

Description Time Amount Factor Value

Purchase the truck t0 $(41,000) 1.0000 $(41,000)

Cost savings t1 5,900 0.9259 5,463

Cost savings t2 8,100 0.8573 6,944

Cost savings t3 8,300 0.7938 6,589

Cost savings t4 8,000 0.7350 5,880

Cost savings t5 8,000 0.6806 5,445

Cost savings t6 8,300 0.6302 5,231

Cost savings t7 9,200 0.5835 5,368

NPV $ (80)

44. 47. a. Year Cash Flow PV Factor PV

0 $(5,000,000) 1.0000 $(5,000,000)

1–7 838,000 5.5824 4,678,051

7 400,000 0.6651 266,040

NPV $ (55,909)

b. No, the NPV is negative; therefore this is an unacceptable project.

c. PI = ($4,678,051 + $266,040) ÷ $5,000,000 = 0.99

d. PV of annual cash flows = $5,000,000 – $266,040

PV of annual cash flows = $4,733,960

PV of annual cash flows = Annual cash flow 5.5824

$4,733,960 = Annual cash flow 5.5824

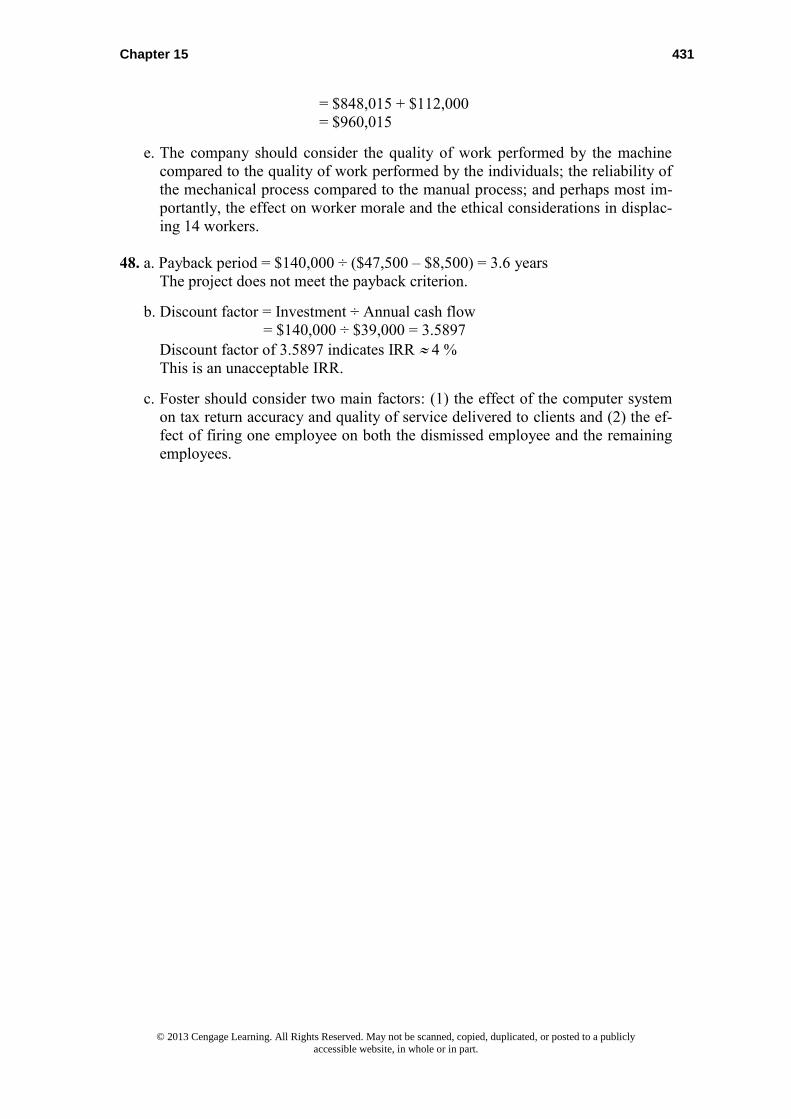

Annual cash flow = $4,733,960 ÷ 5.5824 = $848,015

Minimum labor savings = $848,015 + Operating costs

Chapter 15 431

© 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied, duplicated, or posted to a publicly

accessible website, in whole or in part.

= $848,015 + $112,000

= $960,015

e. The company should consider the quality of work performed by the machine

compared to the quality of work performed by the individuals; the reliability of

the mechanical process compared to the manual process; and perhaps most im-

portantly, the effect on worker morale and the ethical considerations in displac-

ing 14 workers.

48. a. Payback period = $140,000 ÷ ($47,500 – $8,500) = 3.6 years

The project does not meet the payback criterion.

b. Discount factor = Investment ÷ Annual cash flow

= $140,000 ÷ $39,000 = 3.5897

Discount factor of 3.5897 indicates IRR 4 %

This is an unacceptable IRR.

c. Foster should consider two main factors: (1) the effect of the computer system

on tax return accuracy and quality of service delivered to clients and (2) the ef-

fect of firing one employee on both the dismissed employee and the remaining

employees.