chapter 12: derivatives and foreign currency transactions

TRANSCRIPT

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-1

Chapter 12: Derivatives and Foreign Currency Transactions

by Jeanne M. David, Ph.D., Univ. of Detroit Mercy

to accompanyAdvanced Accounting, 10th editionby Floyd A. Beams, Robin P. Clement,

Joseph H. Anthony, and Suzanne Lowensohn

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-2

Derivative and Foreign Currency Transactions: Objectives1. Understand the definition of a derivative and the

types of risks that derivatives can reduce.2. Understand the structure, benefits, and costs of

options, futures, and forward contracts. 3. Understand the most common approaches to

determining hedge effectiveness and the criteria used to judge whether a hedge is or is not effective.

4. Understand the definition of a cash flow hedge and the circumstances in which a derivative is accounted for as a cash flow hedge.

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-3

Objectives (cont.)5. Understand the definition of a fair value hedge and the

circumstances in which a derivative is accounted for as a fair value hedge.

6. Account for a cash flow hedge situation from inception through settlement and for a fair value hedge situation from inception through settlement.

7. Explain the difference between receivable or payable measurement and denomination.

8. Understand key concepts related to foreign currency exchange rates, such as indirect and direct quotes; floating, fixed, and multiple exchange rates; and spot, current, and historical exchange rates.

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-4

Objectives (cont.)9. Record foreign currency-denominated sales/receivables

and purchases/payables at the initial transaction date, year-end, and the receivable or payable settlement date.

10. Understand the special derivative accounting related to hedges of existing foreign currency denominated receivables and payables.

11. Understand the International Accounting Standards Board accounting for derivatives.

12. Comprehend the footnote disclosure requirements for derivatives.

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-5

1: Derivatives and Risk Management1: Derivatives and Risk ManagementDerivatives and Foreign Currency Transactions

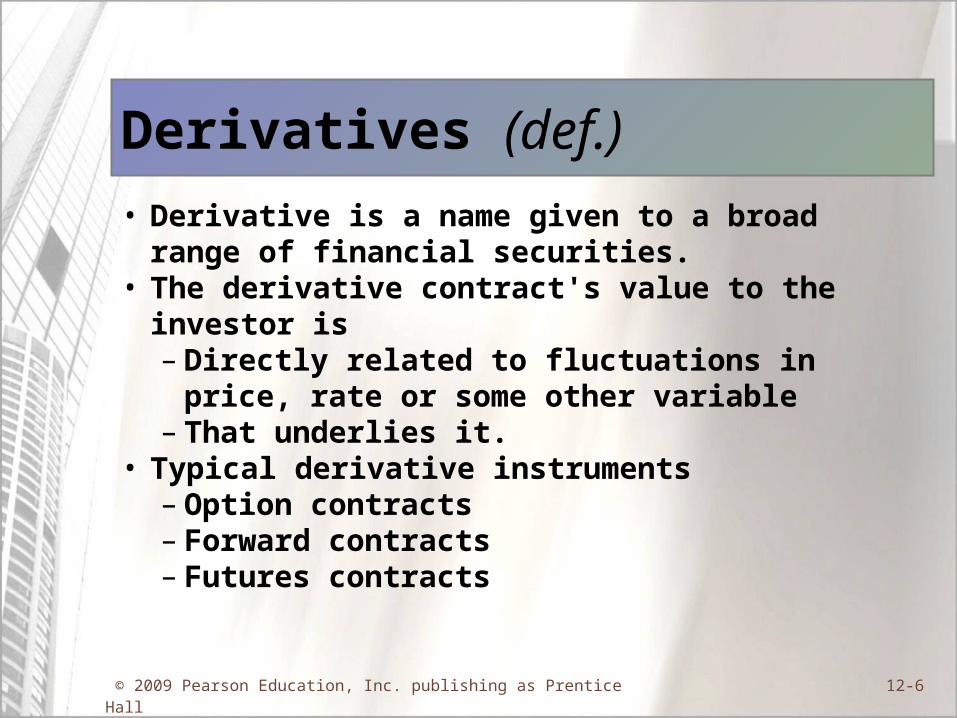

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-6

Derivatives (def.)• Derivative is a name given to a broad range of

financial securities.• The derivative contract's value to the investor is

– Directly related to fluctuations in price, rate or some other variable

– That underlies it.• Typical derivative instruments

– Option contracts– Forward contracts– Futures contracts

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-7

2: Types of Derivatives2: Types of DerivativesDerivatives and Foreign Currency Transactions

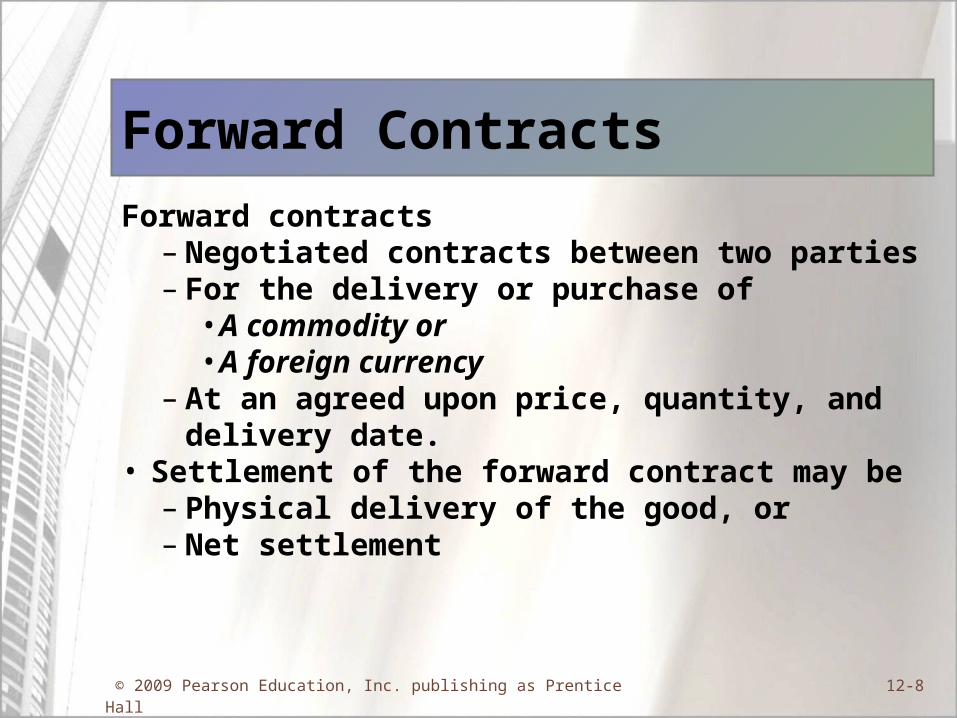

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-8

Forward ContractsForward contracts

– Negotiated contracts between two parties– For the delivery or purchase of

• A commodity or• A foreign currency

– At an agreed upon price, quantity, and delivery date.

• Settlement of the forward contract may be– Physical delivery of the good, or– Net settlement

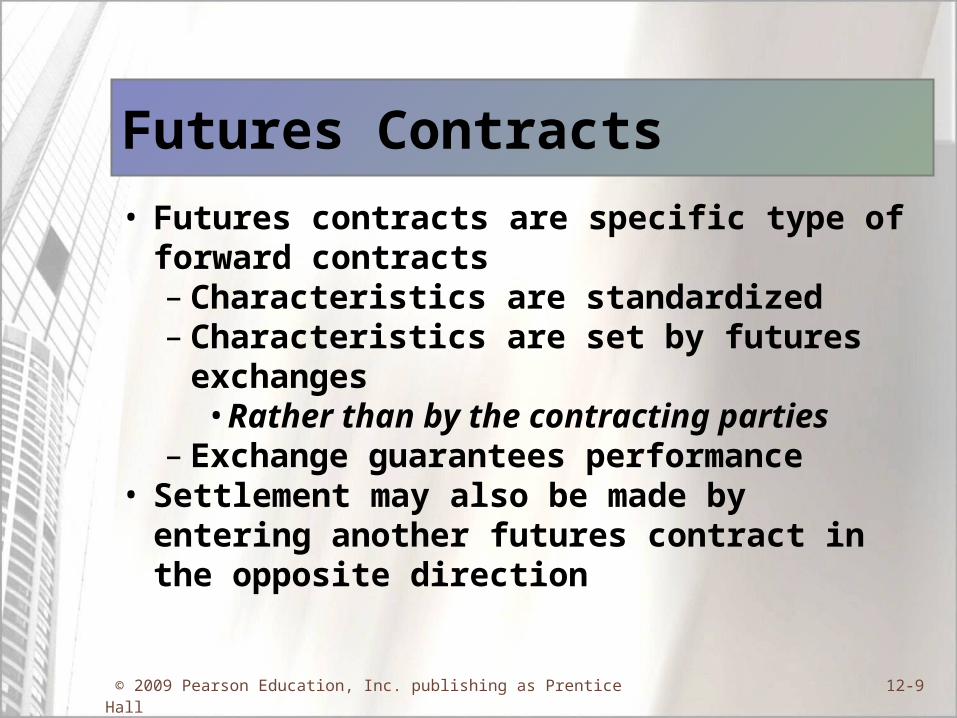

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-9

Futures Contracts• Futures contracts are specific type of forward

contracts– Characteristics are standardized– Characteristics are set by futures exchanges

• Rather than by the contracting parties– Exchange guarantees performance

• Settlement may also be made by entering another futures contract in the opposite direction

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-10

Options• With options, only one party is obligated to

perform• The other party has

– Ability,– But not obligation to perform

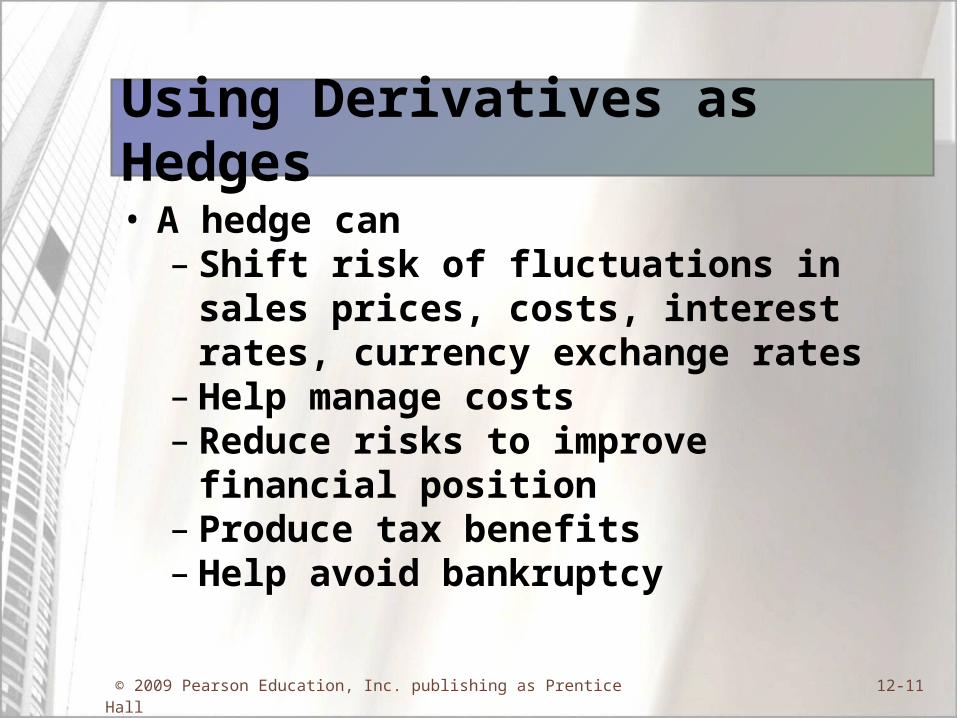

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-11

Using Derivatives as Hedges• A hedge can

– Shift risk of fluctuations in sales prices, costs, interest rates, currency exchange rates

– Help manage costs– Reduce risks to improve financial position– Produce tax benefits– Help avoid bankruptcy

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-12

Hedge Accounting• At inception, document the hedge

– Relationship between hedged item and derivative instrument

– Risk management objective and strategy for hedge• Hedged instrument• Hedged item• Nature of risk being hedged• Means of assessing effectiveness

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-13

3: Hedge Effectiveness3: Hedge EffectivenessDerivatives and Foreign Currency Transactions

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-14

EffectivenessTo qualify for hedge accounting, the derivative

instrument must be– Highly effective in offsetting– Gains or losses– In the item being hedged

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-15

Critical Term Analysis• Effectiveness considers

– Nature of the underlying variable– Notional amount– Item being hedged– Delivery date of derivative– Settlement date of the underlying

• If critical terms are identical, effectiveness is assumed

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-16

Example of Effectiveness• Item to be hedged

– Accounts payable– Due January 1, 2007– For delivery of 10,000 euros– Variable is the changing value of euros

• Hedge instrument– Forward contract– To accept delivery of 10,000 euros– On January 1, 2007

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-17

Statistical Analysis• If critical terms of item to be hedged and hedge

instrument do not match• Statistical analysis can determine effectiveness

– Regression analysis– Correlation analysis

• Example– Using derivatives based on heating oil or

crude oil to hedge jet fuel costs

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-18

4: Cash Flow Hedges4: Cash Flow HedgesDerivatives and Foreign Currency Transactions

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-19

Cash Flow Hedge• Hedges

– Anticipated or forecasted transactions

• Hedges exposure to variability in expected future cash flows associated with a risk.

• Hedged risk– Variability in expected future cash flows

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-20

Accounting for Cash Flow Hedge• Hedge instrument is recorded at cost• Adjust to fair value• Change in fair value is recorded as Other

Comprehensive Income (OCI)• When the forecasted transaction impacts the

income statement– Reclassify OCI to the hedged revenue or

expense account

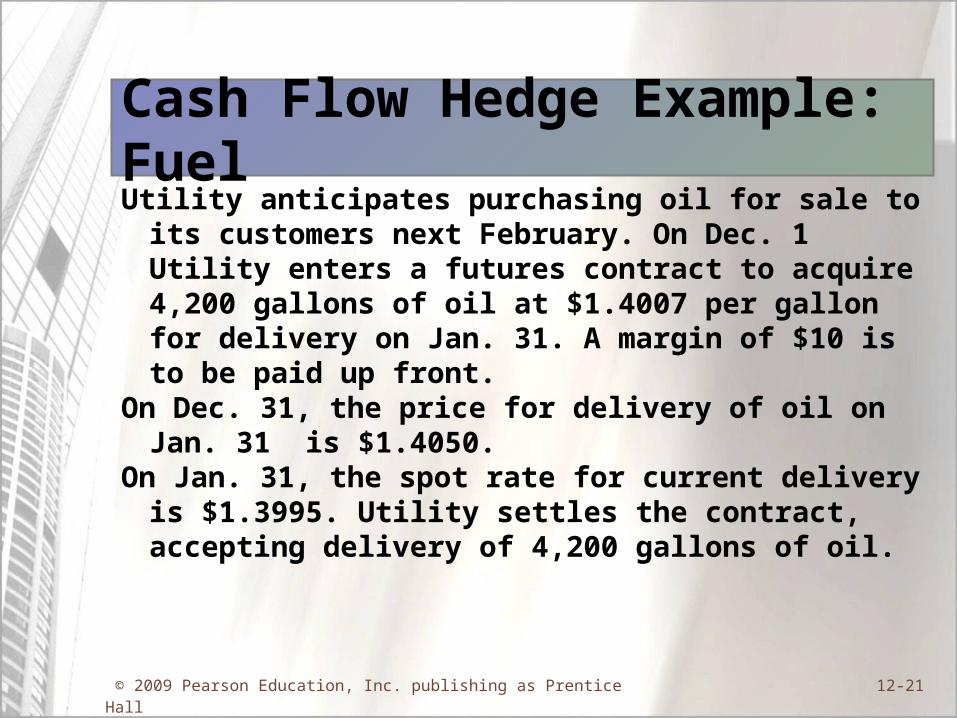

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-21

Cash Flow Hedge Example: FuelUtility anticipates purchasing oil for sale to its customers

next February. On Dec. 1 Utility enters a futures contract to acquire 4,200 gallons of oil at $1.4007 per gallon for delivery on Jan. 31. A margin of $10 is to be paid up front.

On Dec. 31, the price for delivery of oil on Jan. 31 is $1.4050.

On Jan. 31, the spot rate for current delivery is $1.3995. Utility settles the contract, accepting delivery of 4,200 gallons of oil.

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-22

Hedge: Fuel (cont.)• In Feb. Utility sells all the oil to its customers for

$8,400 and reclassifies its OCI from the hedge as cost of sales. Pertinent rates:

• Change in futures contract to Dec. 31 = $18.06• Change in futures contract to Jan. 31 = ($23.10)• The loss on the contract is ($5.04) OCI, and this serves

to increase the cost of sales.

12/1 12/31 1/31Futures rate, for 1/31 $1.4007 $1.4050 $1.3995 Cost of 4,200 barrels $5,882.94 $5,901.00 $5,877.90

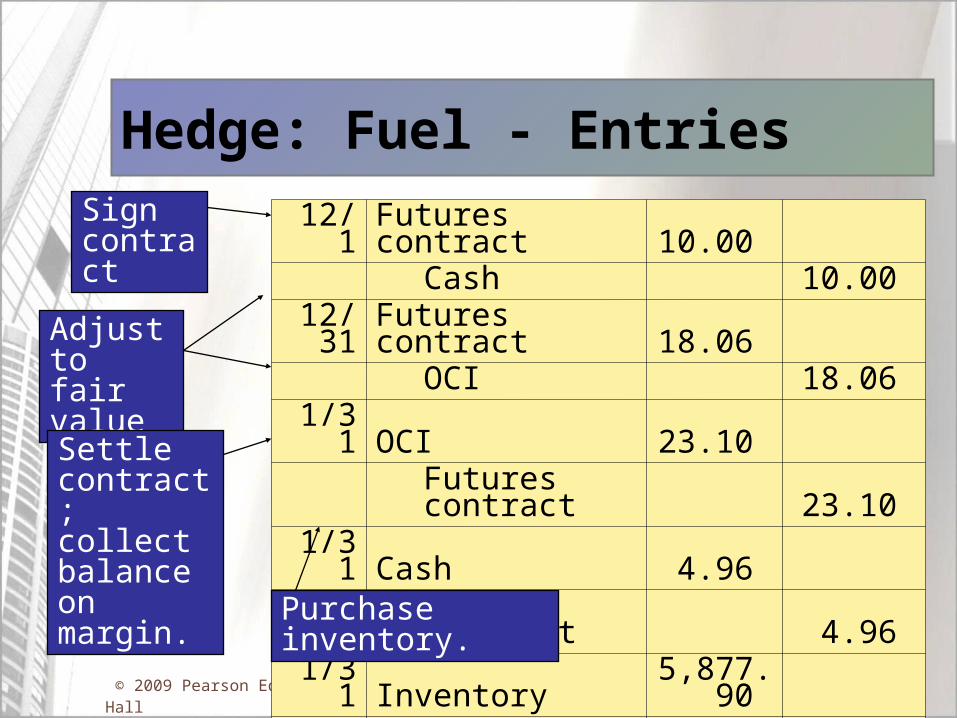

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-23

Hedge: Fuel - Entries12/1 Futures contract 10.00

Cash 10.00 12/31 Futures contract 18.06 OCI 18.06

1/31 OCI 23.10 Futures contract 23.10

1/31 Cash 4.96 Futures contract 4.96

1/31 Inventory 5,877.90 Cash 5,877.90

Adjust to fair value

Settle contract; collect balance on margin.

Purchase inventory.

Sign contract

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-24

Hedge: Fuel – Example (cont.)Feb. Cash 8,400.00

Sales 8,400.00 Feb. Cost of sales 5,877.90

Inventory 5,877.90 Feb. Cost of sales 5.04

OCI 5.04

Record the sale and cost of sales.

The last entry reclassifies the loss on the contract from OCI into Cost of sales. The effect is to increase Cost of sales to $5,882.94. This is the cost of the oil based on the futures contract signed on Dec. 1.

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-25

5: Fair Value Hedges5: Fair Value HedgesDerivatives and Foreign Currency Transactions

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-26

Fair Value Hedge• Hedges

– An existing asset or liability position, or– A firm purchase or sales commitment

• Hedged risk – Change in the value of the asset, liability, or

commitment

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-27

6: Accounting for Hedges6: Accounting for HedgesDerivatives and Foreign Currency Transactions

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-28

Accounting for a Fair Value Hedge• Exchange gains and losses are recognized

immediately in income– Exchange gain or loss

• Offset by related losses and gains on the hedged item

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-29

7: Foreign Currencies: Measurement 7: Foreign Currencies: Measurement versus Denominationversus Denomination

Derivatives and Foreign Currency Transactions

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-30

Measurement and Denomination• Measured in a currency

– Recorded in the financial records in that currency• Denominated in a currency

– Requires settlement (payment or receipt) in that currency

• For US firms– US dollar is the measurement currency– Payables and receivables may be denominated in

US dollars or other currencies

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-31

8: Foreign Currency Exchange Rates8: Foreign Currency Exchange RatesDerivatives and Foreign Currency Transactions

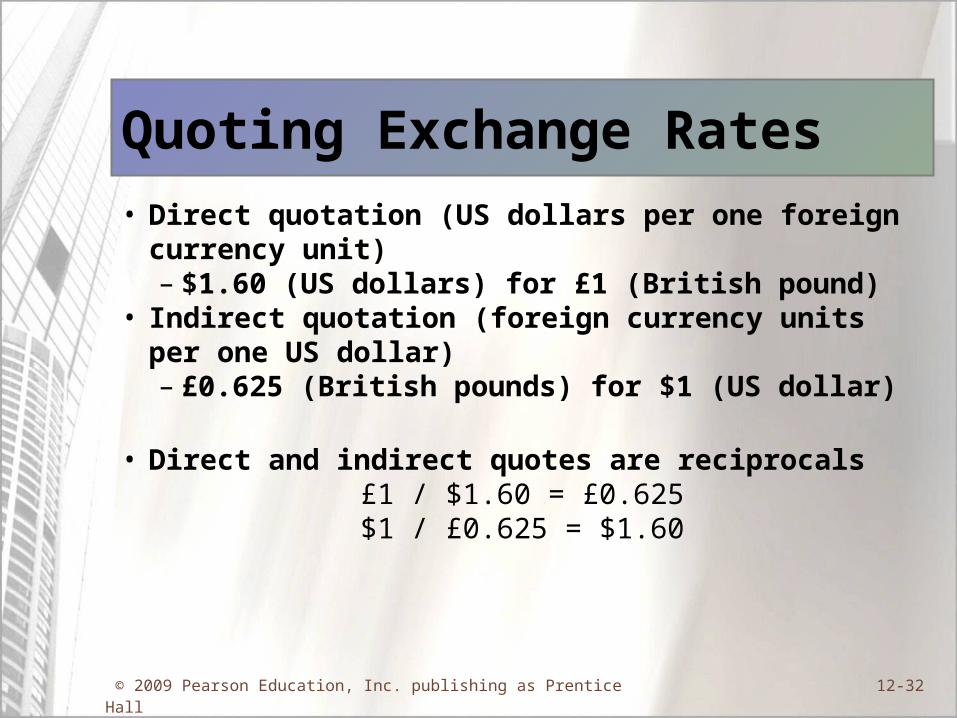

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-32

Quoting Exchange Rates• Direct quotation (US dollars per one foreign currency

unit)– $1.60 (US dollars) for £1 (British pound)

• Indirect quotation (foreign currency units per one US dollar)– £0.625 (British pounds) for $1 (US dollar)

• Direct and indirect quotes are reciprocals£1 / $1.60 = £0.625$1 / £0.625 = $1.60

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-33

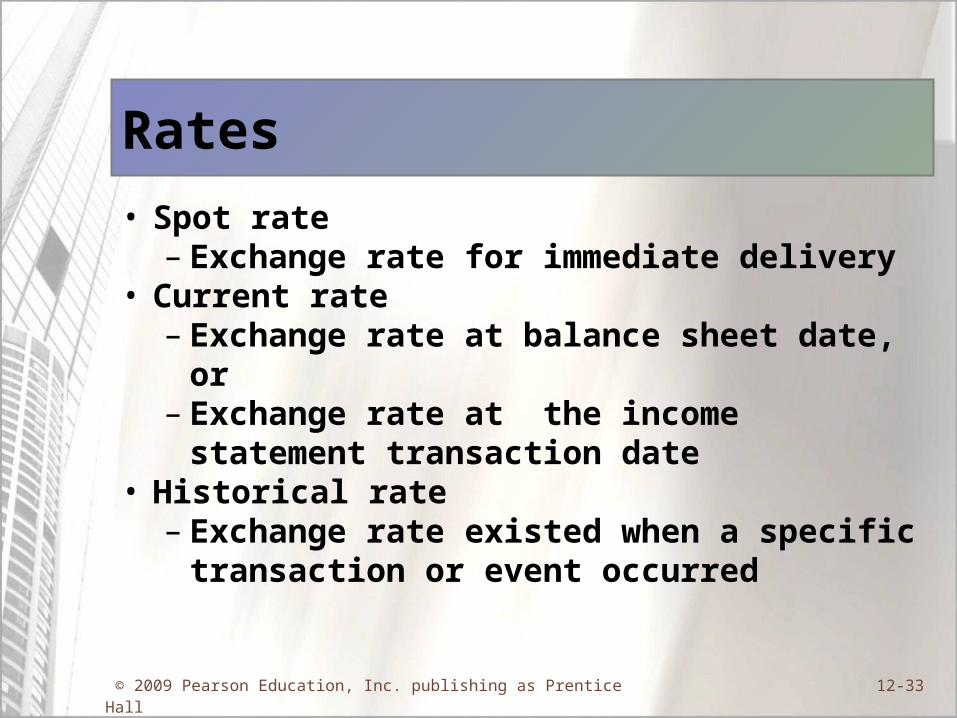

Rates• Spot rate

– Exchange rate for immediate delivery• Current rate

– Exchange rate at balance sheet date, or– Exchange rate at the income statement

transaction date• Historical rate

– Exchange rate existed when a specific transaction or event occurred

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-34

9: Sales and Purchases Denominated 9: Sales and Purchases Denominated in Foreign Currencyin Foreign Currency

Derivatives and Foreign Currency Transactions

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-35

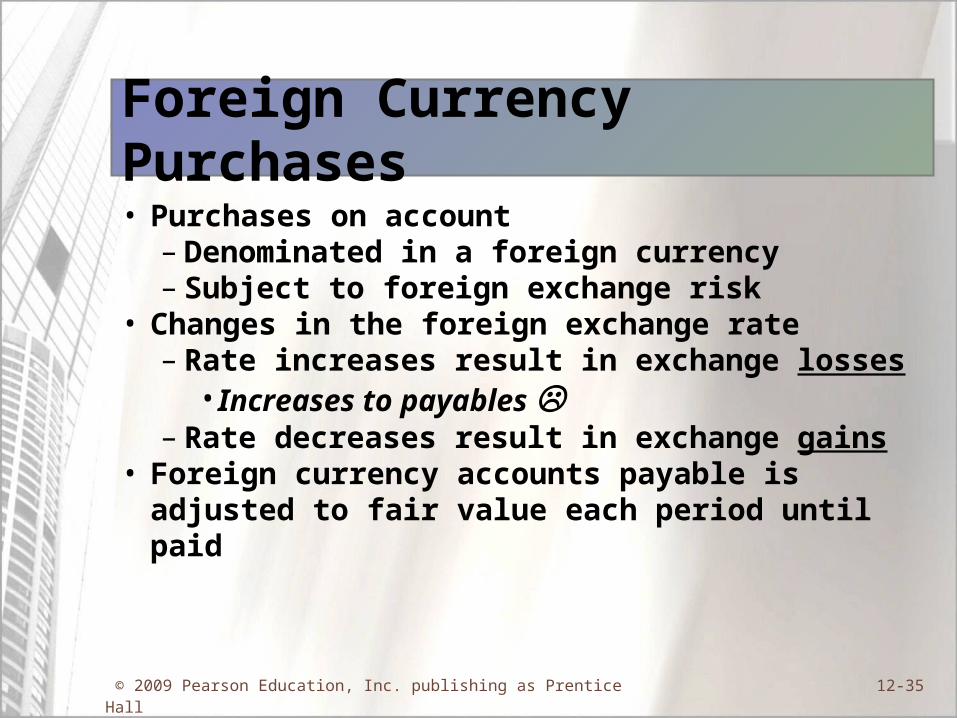

Foreign Currency Purchases• Purchases on account

– Denominated in a foreign currency– Subject to foreign exchange risk

• Changes in the foreign exchange rate– Rate increases result in exchange losses

• Increases to payables – Rate decreases result in exchange gains

• Foreign currency accounts payable is adjusted to fair value each period until paid

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-36

Foreign Currency Sales• Sales on account

– Denominated in a foreign currency– Subject to foreign exchange risk

• Changes in the foreign exchange rate– Rate increases result in exchange gains

• Increases to receivables – Rate decreases result in exchange losses

• Foreign currency accounts receivable is adjusted to fair value each period until collected.

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-37

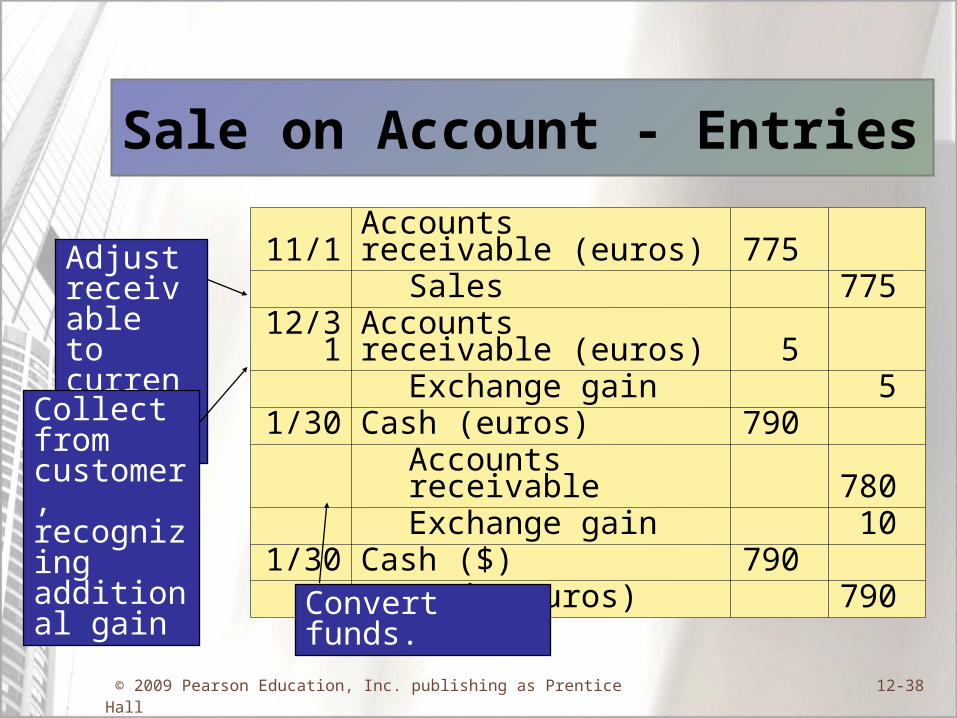

Example: Sale on Account• On 11/1 Sam sells goods for 500 euros on

account. The customer pays on 1/30 and cash is converted on that date. Pertinent rates:

Date Spot rate Acct Rec Gain (Loss)11/1 $1.55 $775

12/31 $1.56 $780 $5 1/30 $1.58 $790 $10

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-38

Sale on Account - Entries11/1 Accounts receivable (euros) 775

Sales 775 12/31 Accounts receivable (euros) 5

Exchange gain 5 1/30 Cash (euros) 790

Accounts receivable 780 Exchange gain 10

1/30 Cash ($) 790 Cash (euros) 790

Adjust receivable to current rate.

Collect from customer, recognizing additional gain

Convert funds.

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-39

10: Accounting for Foreign Currency 10: Accounting for Foreign Currency HedgesHedges

Derivatives and Foreign Currency Transactions

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-40

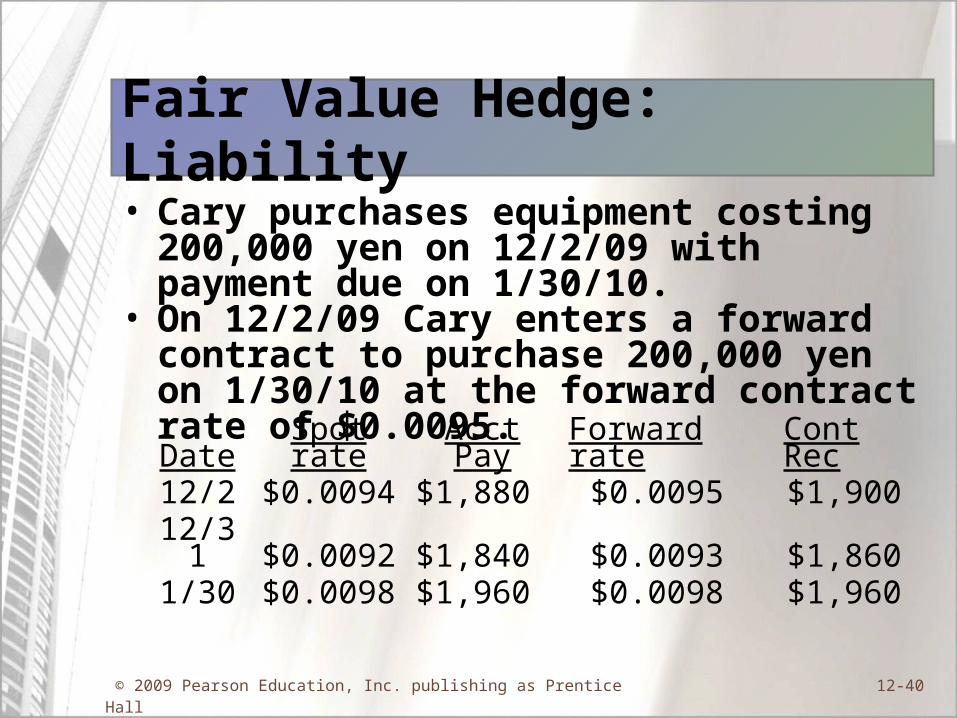

Fair Value Hedge: Liability • Cary purchases equipment costing 200,000 yen

on 12/2/09 with payment due on 1/30/10.• On 12/2/09 Cary enters a forward contract to

purchase 200,000 yen on 1/30/10 at the forward contract rate of $0.0095.

Date Spot rate Acct Pay Forward rate Cont Rec12/2 $0.0094 $1,880 $0.0095 $1,900

12/31 $0.0092 $1,840 $0.0093 $1,860 1/30 $0.0098 $1,960 $0.0098 $1,960

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-41

Hedge: Liability – Effect (cont.)• Accounts payable:

Gain of $40 for December Loss of $120 for January

• Contract receivable:Loss of $40 for DecemberGain of $100 for January

• The net gain/loss for December = $0.• The net loss for January = ($20)

• Total exchange loss on the transaction = ($20)

• Spread between the spot and forward rate on 12/2 determines the total loss, e.g., cost of hedging.

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-42

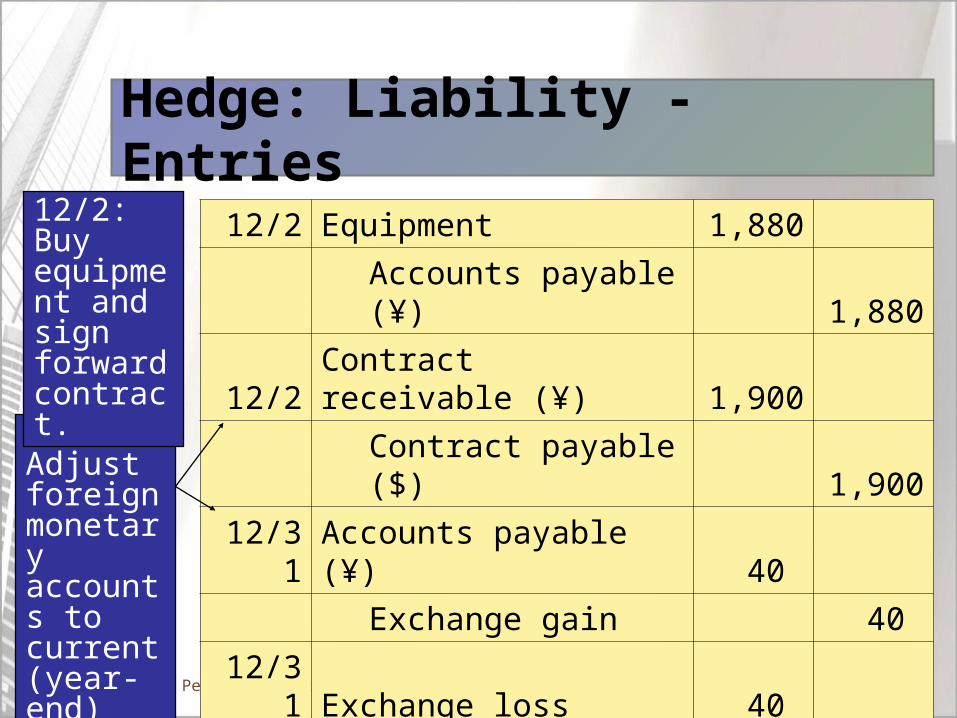

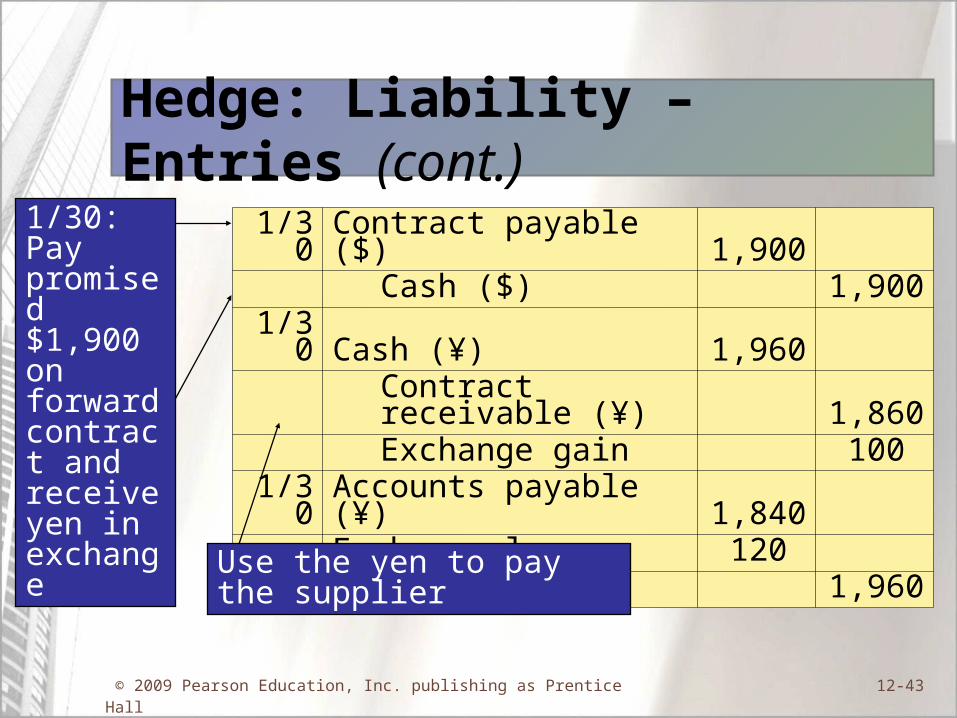

Hedge: Liability - Entries

12/2 Equipment 1,880 Accounts payable (¥) 1,880

12/2 Contract receivable (¥) 1,900 Contract payable ($) 1,900

12/31 Accounts payable (¥) 40 Exchange gain 40

12/31 Exchange loss 40 Contract receivable (¥) 40

12/31: Adjust foreign monetary accounts to current (year-end) rate.

12/2: Buy equipment and sign forward contract.

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-43

Hedge: Liability – Entries (cont.)1/30 Contract payable ($) 1,900

Cash ($) 1,900 1/30 Cash (¥) 1,960

Contract receivable (¥) 1,860 Exchange gain 100 1/30 Accounts payable (¥) 1,840

Exchange loss 120 Cash (¥) 1,960

1/30: Pay promised $1,900 on forward contract and receive yen in exchange

Use the yen to pay the supplier

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-44

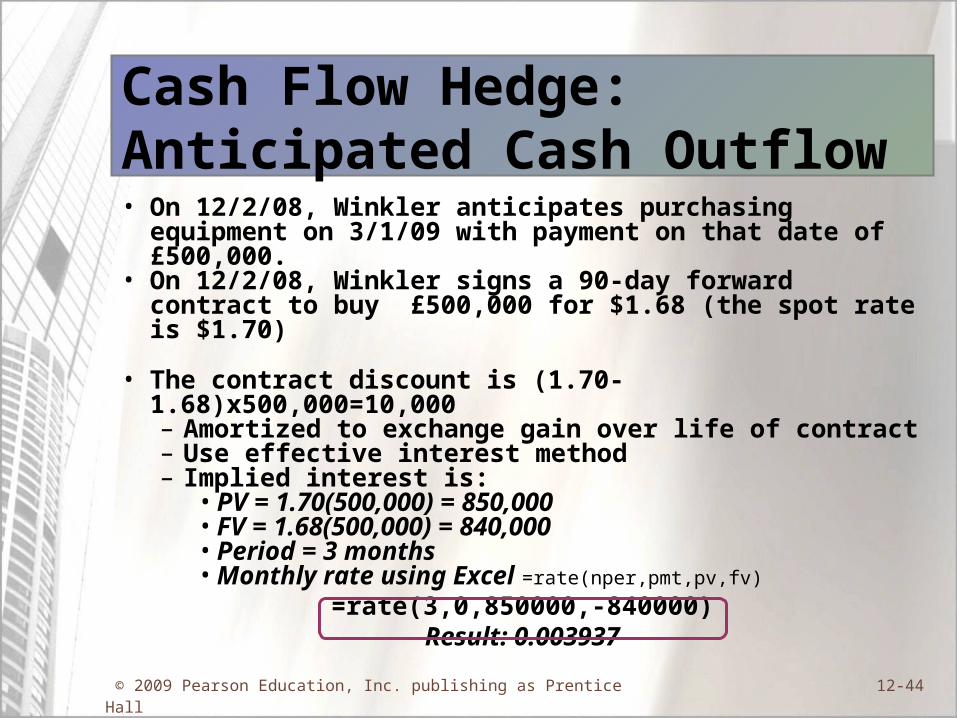

Cash Flow Hedge: Anticipated Cash Outflow• On 12/2/08, Winkler anticipates purchasing equipment on

3/1/09 with payment on that date of £500,000. • On 12/2/08, Winkler signs a 90-day forward contract to

buy £500,000 for $1.68 (the spot rate is $1.70)

• The contract discount is (1.70-1.68)x500,000=10,000– Amortized to exchange gain over life of contract– Use effective interest method– Implied interest is:

• PV = 1.70(500,000) = 850,000• FV = 1.68(500,000) = 840,000• Period = 3 months• Monthly rate using Excel =rate(nper,pmt,pv,fv)

=rate(3,0,850000,-840000)Result: 0.003937

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-45

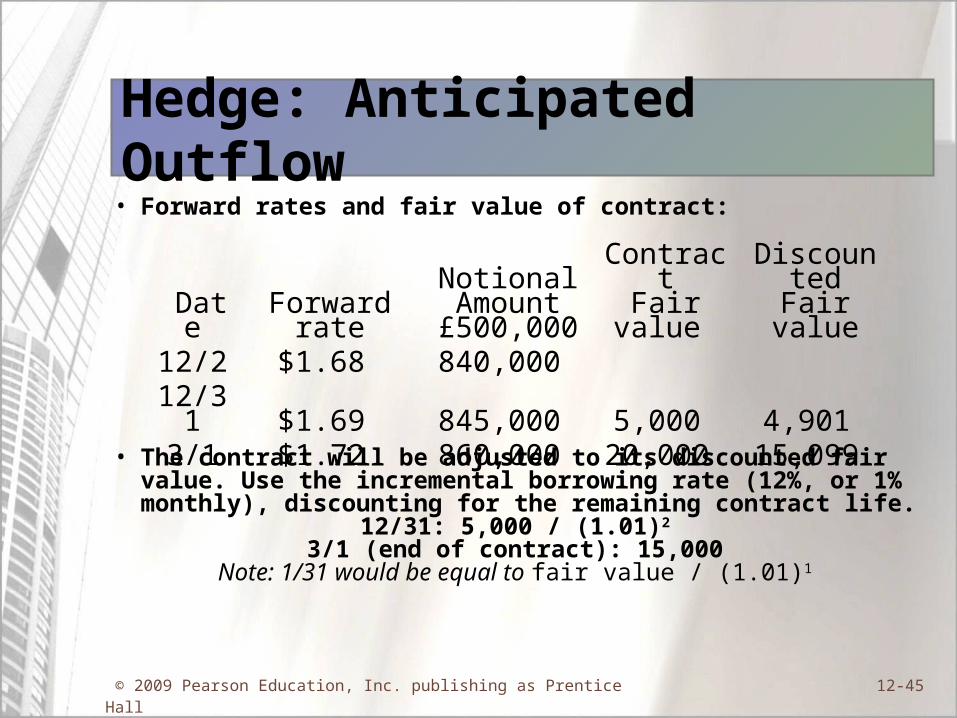

Hedge: Anticipated Outflow• Forward rates and fair value of contract:

• The contract will be adjusted to its discounted fair value. Use the incremental borrowing rate (12%, or 1% monthly), discounting for the remaining contract life.

12/31: 5,000 / (1.01)2

3/1 (end of contract): 15,000Note: 1/31 would be equal to fair value / (1.01)1

Date Forward rate

Notional Amount£500,000

ContractFair value

Discounted Fair value

12/2 $1.68 840,000 12/31 $1.69 845,000 5,000 4,901 3/1 $1.72 860,000 20,000 15,099

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-46

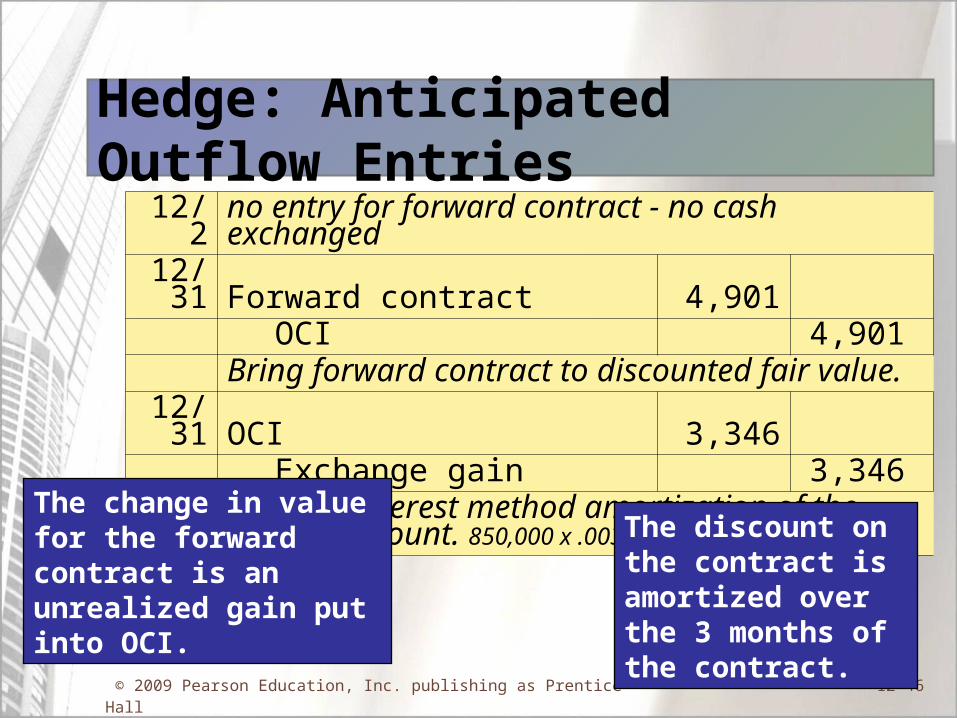

Hedge: Anticipated Outflow Entries12/2 no entry for forward contract - no cash exchanged

12/31 Forward contract 4,901 OCI 4,901 Bring forward contract to discounted fair value.12/31 OCI 3,346 Exchange gain 3,346

Effective interest method amortization of the 10,000 discount. 850,000 x .003937

The change in value for the forward contract is an unrealized gain put into OCI.

The discount on the contract is amortized over the 3 months of the contract.

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-47

Hedge: Entries (cont.)

The final balance in OCI is $10,000 CR.This will reduce the equipment's depreciation over its life.

3/1 Forward contract 15,099 OCI 15,099 Bring forward contract to fair value, $20,0003/1 Cash 20,000 Forward contract 20,000

for net settlement of contract: 860,000 current - 840,000 contract

3/1 Equipment 860,000 Cash 860,000 Purchase equipment from supplier3/1 OCI 6,654 Exchange gain 6,654 remaining amortization: 10,000 - 3,346

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-48

11: IASB Standards11: IASB StandardsDerivatives and Foreign Currency Transactions

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-49

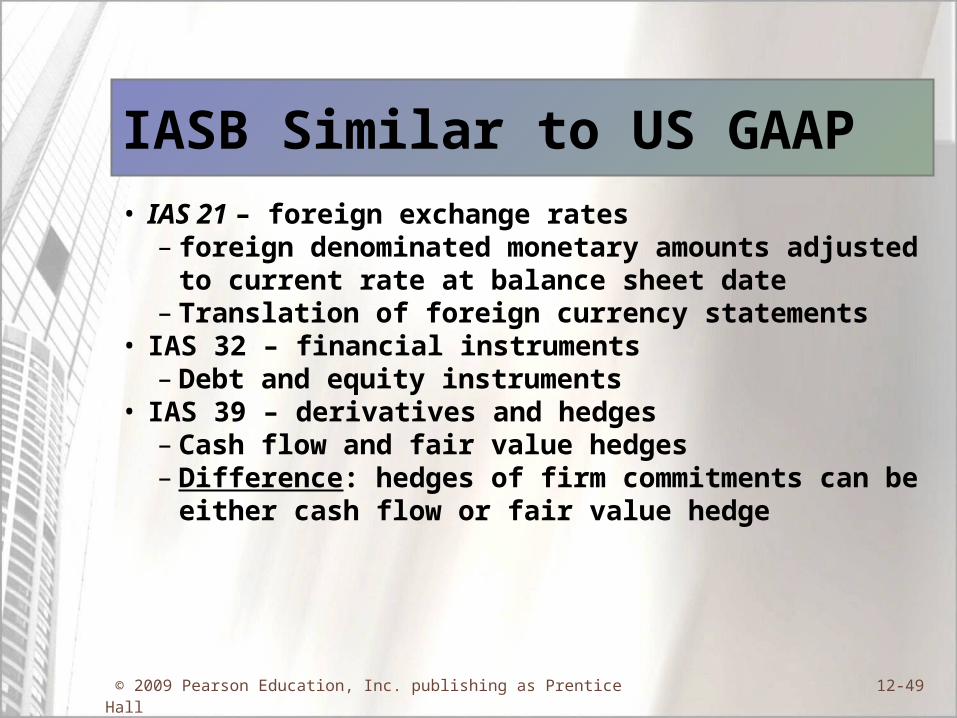

IASB Similar to US GAAP• IAS 21 – foreign exchange rates

– foreign denominated monetary amounts adjusted to current rate at balance sheet date

– Translation of foreign currency statements• IAS 32 – financial instruments

– Debt and equity instruments• IAS 39 – derivatives and hedges

– Cash flow and fair value hedges– Difference: hedges of firm commitments can be

either cash flow or fair value hedge

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-50

12: Disclosures12: DisclosuresDerivatives and Foreign Currency Transactions

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-51

Footnote DisclosuresFootnote Disclosures• Focus on risk management objectives and

strategies• Fair value hedges

– Net gain or loss in earnings, placement on statements, effectiveness and ineffectiveness

• Cash flow hedges– Hedge ineffectiveness gain or loss, placement on

statements, types of situations hedged, expected length of time, effect of discontinuance of hedge

© 2009 Pearson Education, Inc. publishing as Prentice Hall 12-52

Copyright © 2009 Pearson Education, Inc. Copyright © 2009 Pearson Education, Inc. Publishing as Prentice HallPublishing as Prentice Hall

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic,

mechanical, photocopying, recording, or otherwise, without the prior written permission of the publisher. Printed in the United States of America.