ch 0.1 - money management - parivartan learning … money test... · money management is very...

TRANSCRIPT

Money management is very important. Money is necessary to

live and live well in our society. If you reviewed your

expenditures for an entire year, you would see that

unexpected expenses inevitably occur. Having savings

available means you can tide over that expense. This book

intends to explain you the concepts which can help you in

proper money management. Money management happens

through balancing income and expenses, Regular savings,

investing savings in investment products and last money can

make more money though investment. This is the reason why

one should learn money management lesson.

MONEYMATTERS

Income, Expenses and Saving

Role and Importance of Budgeting

Inflation

Debt & Debt Management

Banking

Financial Planning (What, Why and how)

Power of Compounding

Insurance

Investments

Introduction to Traditional and Modern Investments

Introduction of Asset Classes

Mutual Funds & SIP

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

Chapters

- CONTENT -

Chapter 1

`

Hi! I am Sir Nerdy. I am here to explain the concept of

INCOME, EXPENSES AND SAVING

1

Income is the money you make by either offering a service or running a business or through some kind of investment. Most people under the age of 65 receive salary income for working in offices or earn profits by doing some sort of business, while elderly people earn mainly from investments or pensions.

2

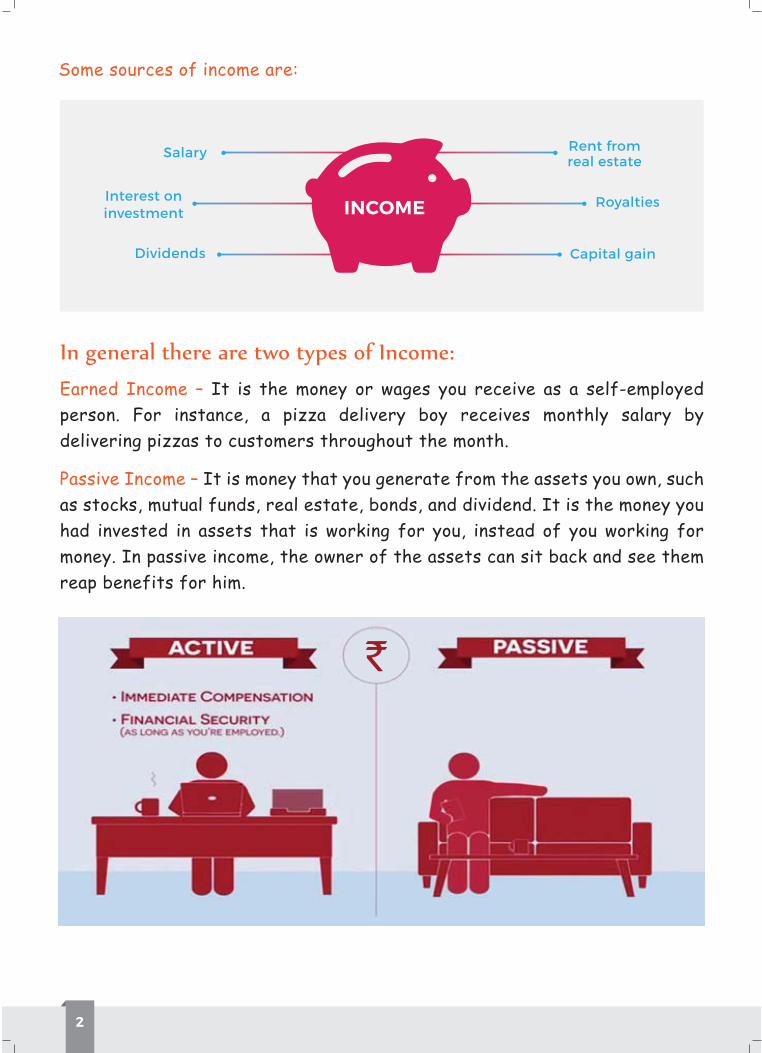

Some sources of income are:

Earned Income – It is the money or wages you receive as a self-employed person. For instance, a pizza delivery boy receives monthly salary by delivering pizzas to customers throughout the month.

Passive Income – It is money that you generate from the assets you own, such as stocks, mutual funds, real estate, bonds, and dividend. It is the money you had invested in assets that is working for you, instead of you working for money. In passive income, the owner of the assets can sit back and see them reap benefits for him.

Royalties

Rent fromreal estate

Capital gain

Salary

Interest oninvestment

Dividends

INCOME

`

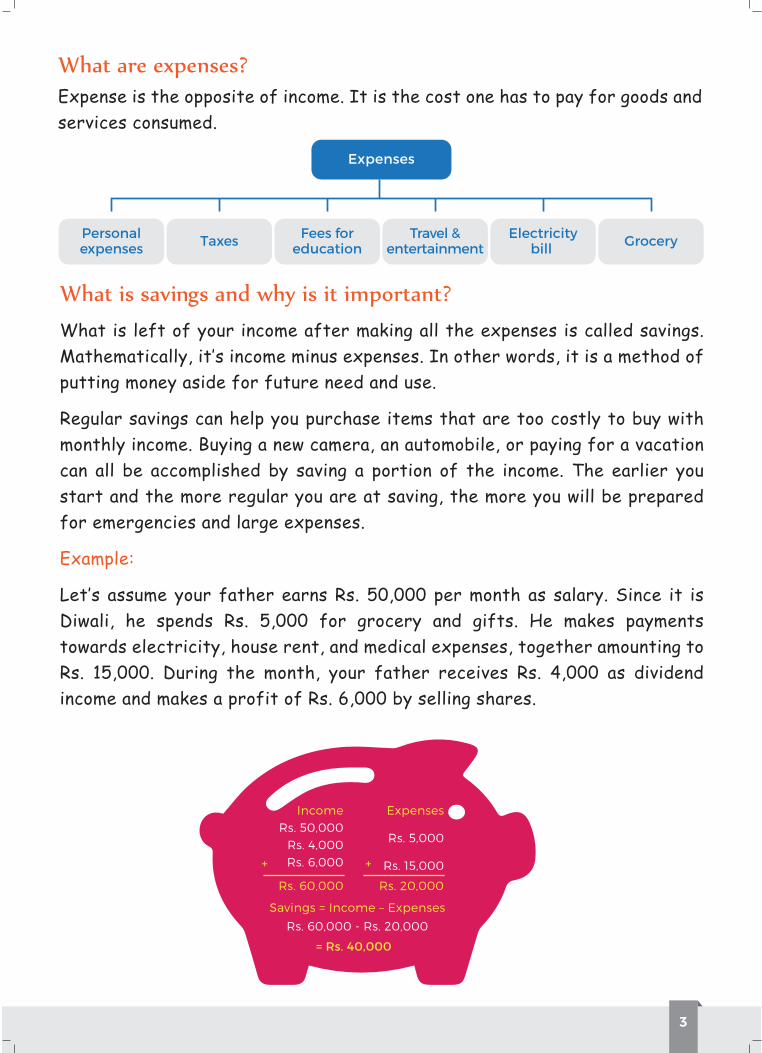

3

What is left of your income after making all the expenses is called savings.

putting money aside for future need and use.

can all be accomplished by saving a portion of the income. The earlier you

for emergencies and large expenses.

Example:

Expenses

GroceryPersonalexpenses Taxes Electricity

bill Fees for

educationTravel &

entertainment

IncomeRs. 50,000

Rs. 4,000Rs. 6,000

Rs. 60,000 Rs. 20,000

Expenses

Rs. 5,000

Rs. 15,000

Savings = Income – Expenses

Rs. 60,000 - Rs. 20,000

++

= Rs. 40,000

services consumed.

4

Besides family, friends, and education, money is an essential part of your life as it helps you lead a comfortable life. Relevant expenses are a must, but you also have to keep a check on your non-essential expenses in order to save for the future. If you can save, you can also make that money grow by investing.

implement the following equation in our lives: Income – Savings = Expense

Income is money that goes into our pocket

Expense is the cost you pay for goods and services consumed

Saving is the method of putting money aside for future use

Make "Income – Savings = Expenses" a thumb rule for life

Chapter 2

ROLE AND IMPORTANCE OF

BUDGETING

5

6

Example:

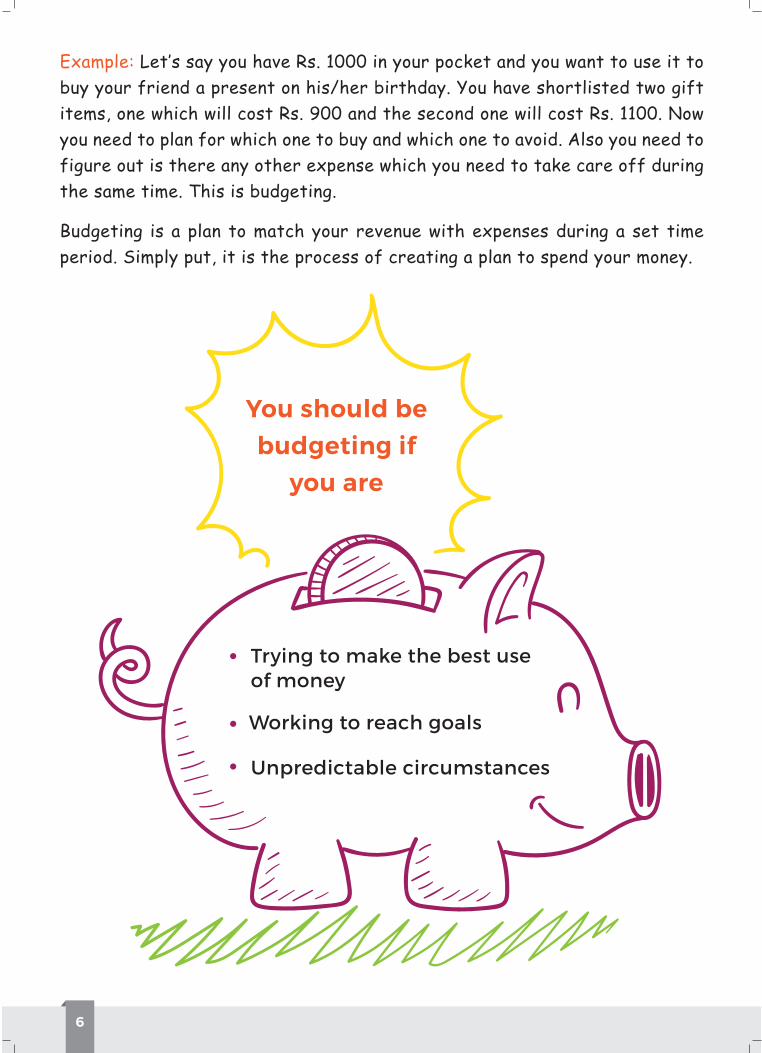

You should be budgeting if

you are

Trying to make the best useof money

Working to reach goals

Unpredictable circumstances

7

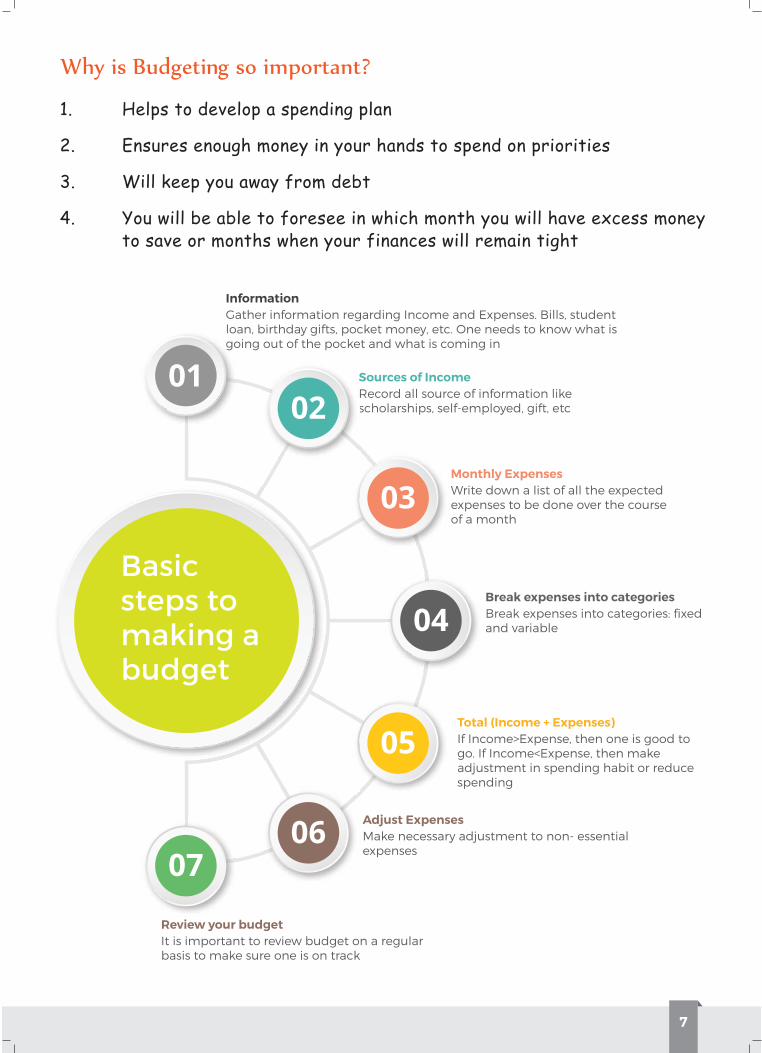

1. Helps to develop a spending plan

2. Ensures enough money in your hands to spend on priorities

3. Will keep you away from debt

4. You will be able to foresee in which month you will have excess money to save or months when your finances will remain tight

Gather information regarding Income and Expenses. Bills, student loan, birthday gifts, pocket money, etc. One needs to know what is going out of the pocket and what is coming in

Information

Record all source of information like scholarships, self-employed, gift, etc

Sources of Income

Write down a list of all the expected expenses to be done over the course of a month

Monthly Expenses

Break expenses into categories: fixed and variable

Break expenses into categories

If Income>Expense, then one is good to go. If Income<Expense, then make adjustment in spending habit or reduce spending

Total (Income + Expenses)

Make necessary adjustment to non- essential expenses

Adjust Expenses

It is important to review budget on a regular basis to make sure one is on track

Review your budget

logo

01s

S

02

03

04

05

0607

Basic steps to making a budget

8

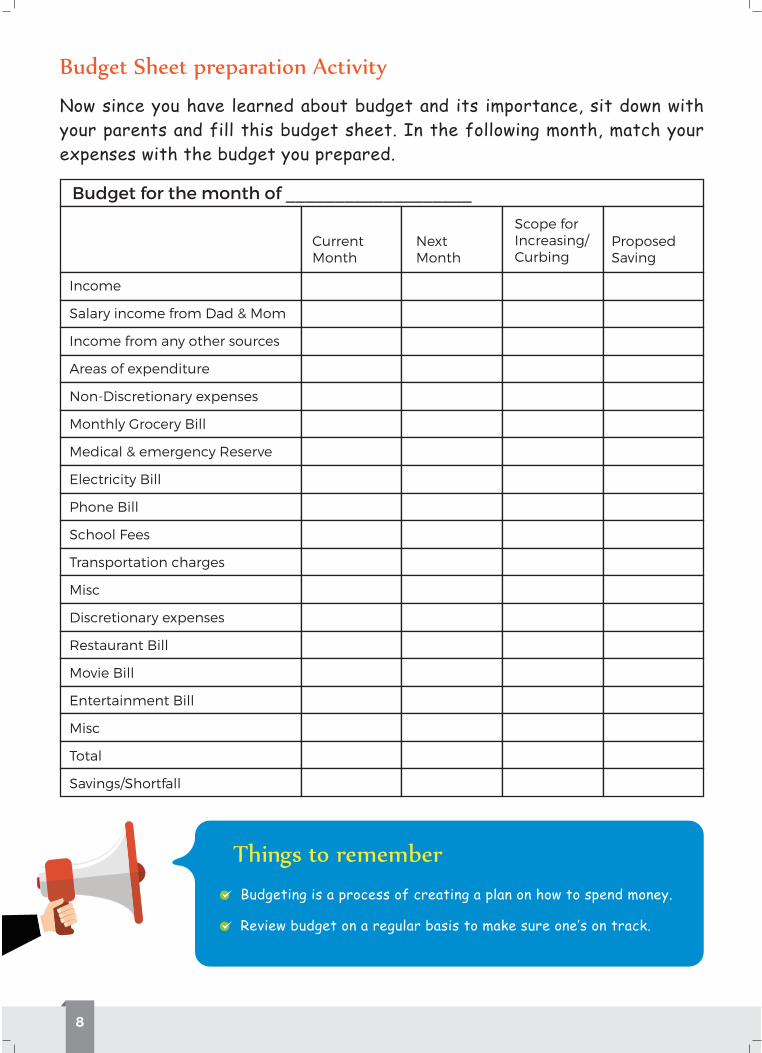

Budgeting is a process of creating a plan on how to spend money.

Now since you have learned about budget and its importance, sit down with your parents and fill this budget sheet. In the following month, match your expenses with the budget you prepared.

Budget for the month of ___________________

CurrentMonth

NextMonth

Scope forIncreasing/Curbing

ProposedSaving

Income

Salary income from Dad & Mom

Income from any other sources

Areas of expenditure

Non-Discretionary expenses

Monthly Grocery Bill

Medical & emergency Reserve

Electricity Bill

Phone Bill

School Fees

Transportation charges

Misc

Discretionary expenses

Restaurant Bill

Movie Bill

Entertainment Bill

Misc

Total

Savings/Shortfall

Chapter 3

Hi, I am Sir Nerdy, and I am here to explain the concept of

INFLATION

9

10

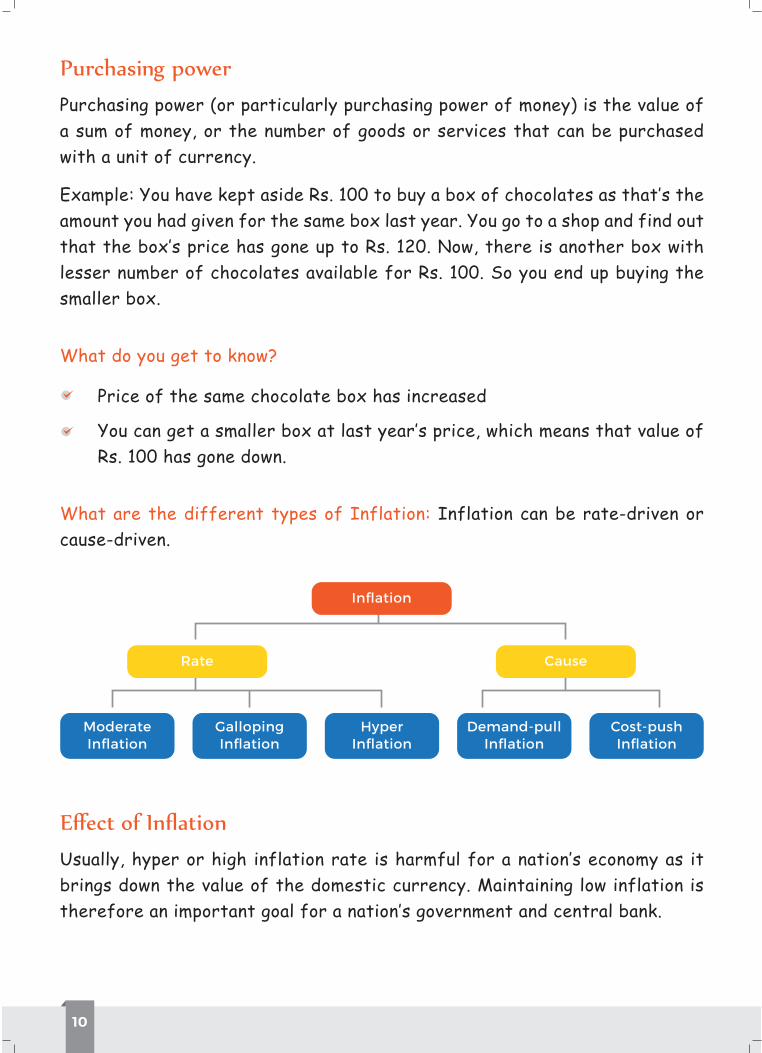

Purchasing power (or particularly purchasing power of money) is the value of a sum of money, or the number of goods or services that can be purchased with a unit of currency.

amount you had given for the same box last year. You go to a shop and find out

lesser number of chocolates available for Rs. 100. So you end up buying the smaller box.

Price of the same chocolate box has increased

Rs. 100 has gone down.

brings down the value of the domestic currency. Maintaining low inflation is

What do you get to know?

What are the different types of Inflation: Inflation can be rate-driven or cause-driven.

Inflation

Rate

ModerateInflation

GallopingInflation

HyperInflation

Demand-pullInflation

Cost-pushInflation

Cause

11

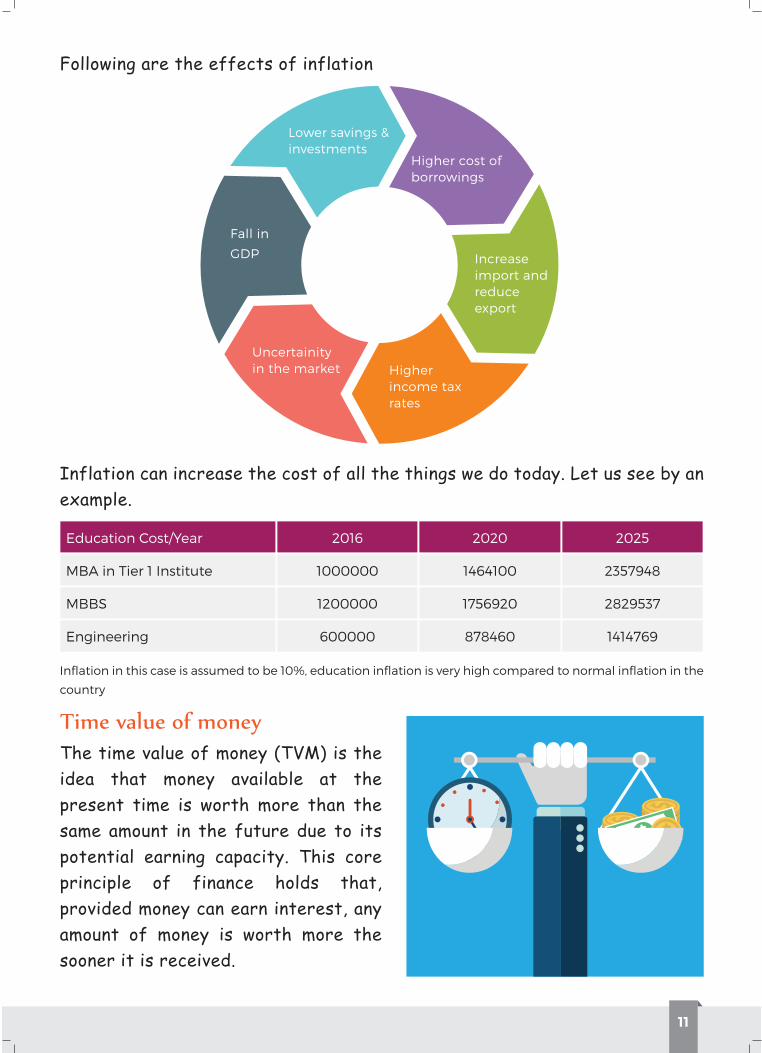

Inflation can increase the cost of all the things we do today. Let us see by an example.

Inflation in this case is assumed to be 10%, education inflation is very high compared to normal inflation in the

country

The time value of money (TVM) is the idea that money available at the present time is worth more than the same amount in the future due to its potential earning capacity. This core principle of finance holds that, provided money can earn interest, any amount of money is worth more the sooner it is received.

Lower savings & investments

Higher cost of borrowings

Increase import and reduce export

Higher income tax rates

Uncertainity in the market

Fall in

GDP

Education Cost/Year

MBA in Tier 1 Institute

MBBS

Engineering

2016

1000000

1200000

600000

2020

1464100

1756920

878460

2025

2357948

2829537

1414769

Following are the effects of inflation

12

FV = Future value of money; PV = Present value of money

i = interest rate; n = number of compounding periods per year

t = number of years

Based on these variables, the formula for TVM is:

FV = PV x (1 + (i / n)) ^ (n x t)

For example, assume a sum of Rs. 10,000 is invested for one year at 10% interest. The future value of that money is:

FV = Rs. 10,000 x (1 + (10% / 1) ^ (1 x 1) = Rs. 11,000

The formula can also be rearranged to find the value of the future sum in present day rupee. For example, the value of Rs. 5,000 one year from today, compounded at 7% interest, is:

PV = Rs. 5,000 / (1 + (7% / 1) ^ (1 x 1) = Rs. 4,673

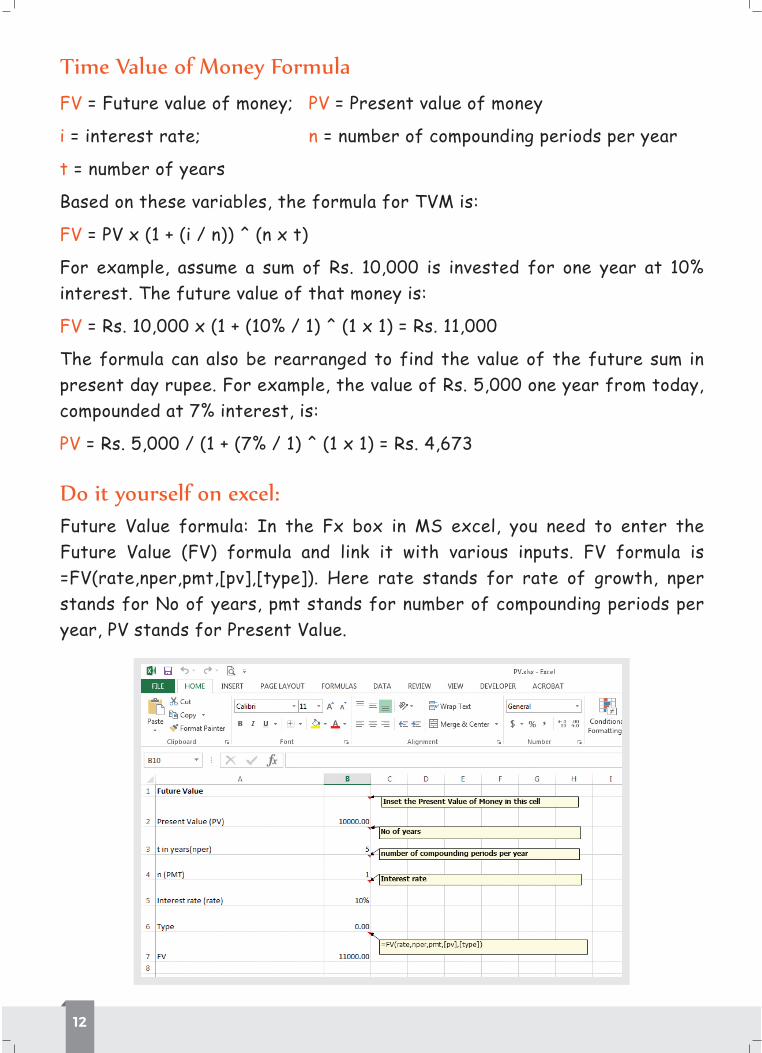

Future Value formula: In the Fx box in MS excel, you need to enter the Future Value (FV) formula and link it with various inputs. FV formula is =FV(rate,nper,pmt,[pv],[type]). Here rate stands for rate of growth, nper stands for No of years, pmt stands for number of compounding periods per year, PV stands for Present Value.

13

When investing, you have to make sure that the rate of return on your investment is higher than the rate of inflation.

can surely protect yourself from the adverse impact by applying some smart

power from eroding.

of the penny saved could be much less than when it was earned.

If you save money by just putting it in your piggy bank, it will lose value over time. So, always invest money to beat inflation and get some handsome

parents or some elder person in the family for their guidance or invest in a

not just lock your money up in your safe and keep it stagnant. If you do this, you will be losing money without even knowing it. The more money you keep stagnant the more money you will be losing.

Educate yourself so that you can earn enough money

Try to save more and spend less

Invest your savings smartly to earn more

14

If the rate of inflation is 10%, you should look for an investment avenue that will return at a rate more than 10%. So your money grows at a faster rate

down.

What is rate of

return on

investment?

What is rate

of Inflation?

The rate of return is how much you make on an investment.

Suppose you invest Rs.100 in the market and over a year, you make Rs.110, then your rate of return is 10%.

= (Latest price/Old price-1)*100

= (110/100-1)*100 = 10%

A general increase in prices is called inflation and rate at which or how much the prices go up is called rate of inflation.

If the price of chocolate is Rs. 80 then after a year with a 4% rate of inflation the price will go up to (Rs. 80 x 1.04) = 83.2

Inflation erodes the value of money

Remain ahead of the inflation course by investing the right way

Chapter 4

Hi I am Sir Nerdy, I am here to explain the meaning of debt and how important it is to manage your debt.

What do you do if you need money to buy your favorite item?

First you will see your piggybank. If sufficient money is not available, then you will ask your parents, elder sister or brother, or a close friend. If you get the money from your close friend and promise him to repay the amount within a specific time period it is called borrowing or having a debt burden.

DEBT AND DEBT MANAGEMENT

15

DEBT

16

If you pay the amount on or before time, you and your friend both would be very happy. It is because you have been relieved from a debt burden and your friend has received his money back. On the contrary, if you do not pay money on time then your friend will be less willing to give you money again in the future as you have not followed the rules agreed to at the time of borrowing money.

In the commercial world, lending and borrowing is a little different. A borrower who borrows money has to pay specific interest on annual or monthly basis at regular intervals along with the borrowing amount or principal amount at the end or in equal installments.

Thus, money comes from two sources; owned (piggybank) and borrowed (parents, sister, brother, friend or any other person). Owned money is your money while borrowed means taken from others.

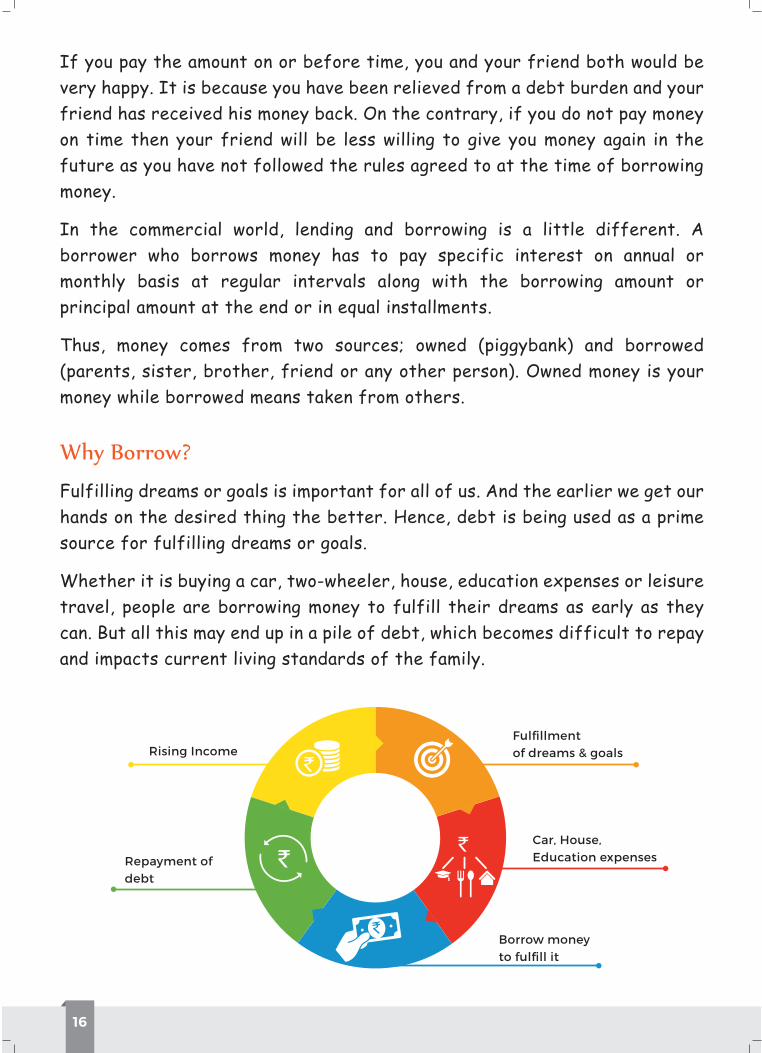

Fulfilling dreams or goals is important for all of us. And the earlier we get our hands on the desired thing the better. Hence, debt is being used as a prime source for fulfilling dreams or goals.

Whether it is buying a car, two-wheeler, house, education expenses or leisure travel, people are borrowing money to fulfill their dreams as early as they can. But all this may end up in a pile of debt, which becomes difficult to repay and impacts current living standards of the family.

Rising Income

Repayment of debt

Borrow moneyto fulfill it

Fulfillment of dreams & goals

Car, House,Education expenses

17

To avoid getting into this debt trap, it is important to see ones current financial position and accordingly take a decision to buy or spend. Debt should be taken in case of emergency or if the benefit is higher than the cost.

To ease the burden of debt, payment can also be done on monthly basis, which

it can be calculated.

Equated monthly installment or EMI is a fixed payment amount paid by a borrower to a lender every month at a specified date. EMI amount includes both interest and part of principal every month to ensure that over a specified number of years, the loan is paid off fully. EMI is being used in almost every type of spending or buying an asset to repay loans or borrowings. It is easy for the borrower because fixed amount is deducted and no further hassles. It is also easy for the lender because he gets both principal and interest regularly.

By using this manual formula or using PMT formula in Microsoft Excel the EMI comes to Rs. 11,978.72. This EMI has to be paid every month for 24 months, which includes both principal and interest. In this EMI amount, initially the interest is high and principal is less but as time goes, principal increases and interest reduces to nil till the end. EMI is useful to the ones who do not have instant cash to pay for the expenses but should also check the interest rate charged and the total interest amount to be paid over the tenure of the payment. In the middle of the EMI payment, if surplus cash is available than pay off the remaining principal at one go to avoid extra interest payment.

EMI formula = [P x R x (1+R)^N]

[(1+R)^N-1]

P- Principal

R- Rate of Interest

N - Number of monthsLet us look at an example:Principal/Borrowing Amount - Rs. 1 lakhRate of Interest – 11% per annumDebt repayment period – 24 months

18

A heavy debt burden is not considered a healthy sign. But today people borrow money for all the expensive items they spend or for buying an asset or property. Spending money through plastic card or credit card is also a way of borrowing and it is growing continuously.

While using credit card, you borrow money for a month from the bank and pay it before the due date to avoid penalty and heavy interest. If not paid before due date because of any reason, the amount increases every month. Interest rate and penalty is so high that after some months, the total payable amount

interest rate increases the burden of payment.

If you borrow Rs. 1 lakh today at 15% rate of interest per annum, what will be the total borrowed amount after 33 years?

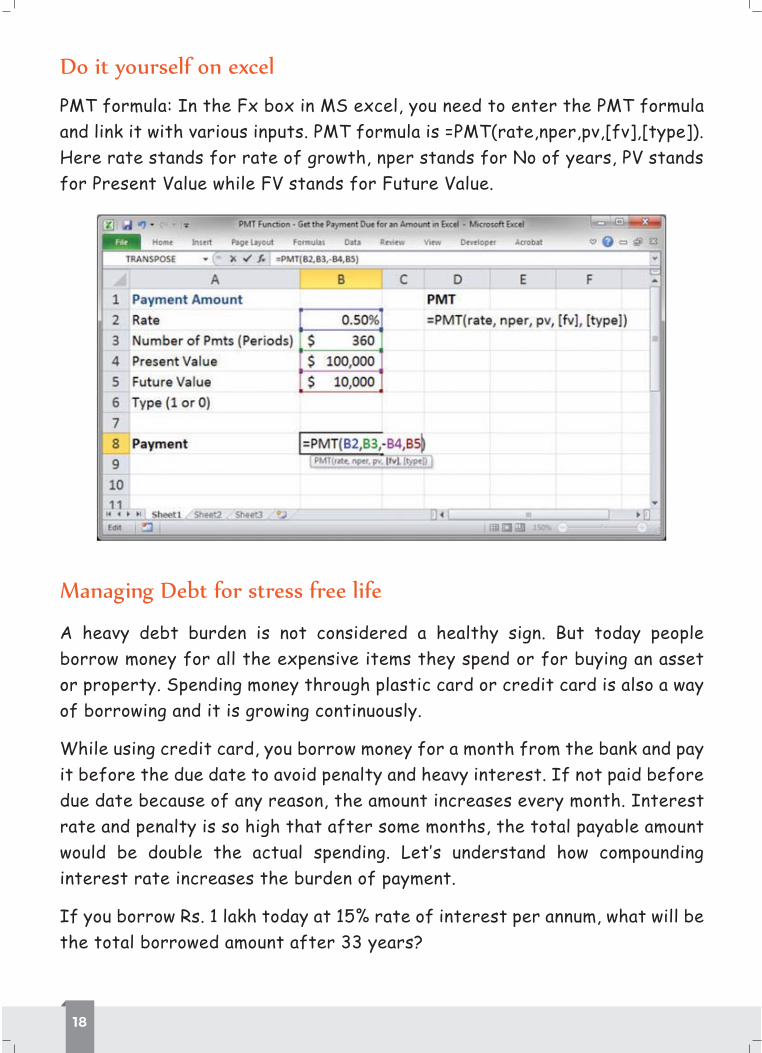

PMT formula: In the Fx box in MS excel, you need to enter the PMT formula and link it with various inputs. PMT formula is =PMT(rate,nper,pv,[fv],[type]). Here rate stands for rate of growth, nper stands for No of years, PV stands for Present Value while FV stands for Future Value.

19

Debt is like a vicious circle

Debt is an emergency fund

Repay Debt before time

Avoiding credit card debt trap

gadgets

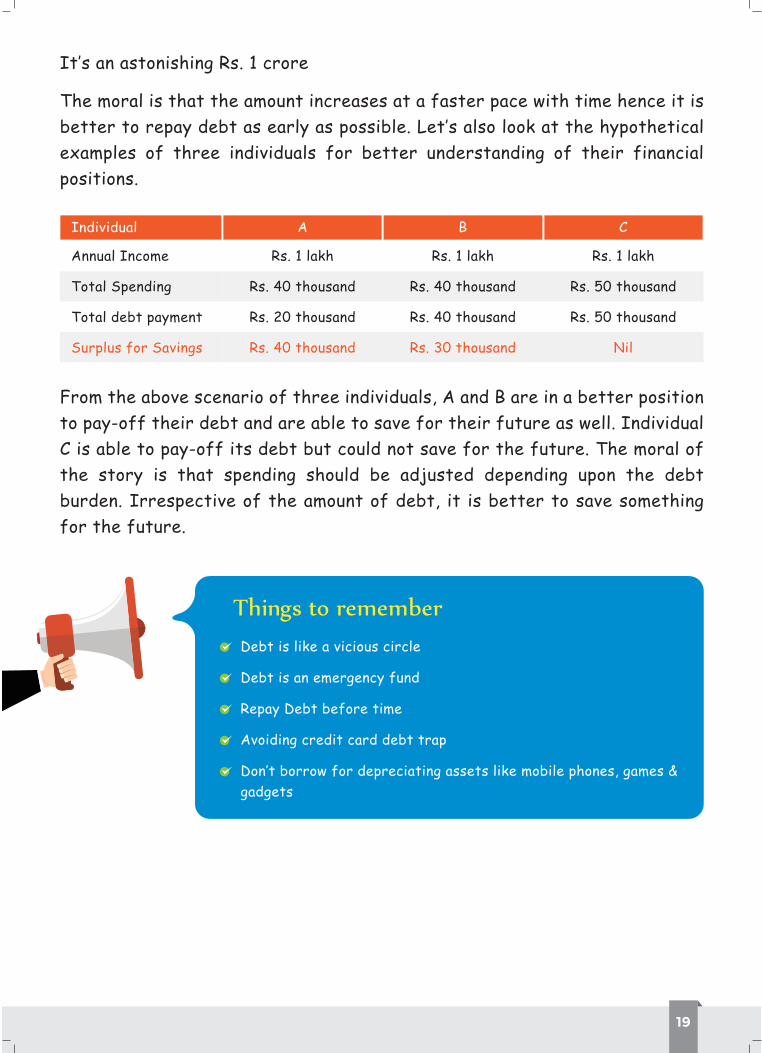

A C

Nil

Chapter 5

BANKING

20

21

A place which looks after your money, and saves it on your behalf, so that you can buy things with it, is a bank. Not only that, it also pays you for every rupee you put into it, which is known as interest.

For instance, you earn Rs. 500 every month as pocket money. If you put that

Did you notice all that extra money you earned just by keeping it in the bank?

Savings account: A deposit in the bank where you keep your money so that it can be used later. It also acts as a record of the money you deposit and take out from your bank account. You get a unique number for your account.

Recurring account: An account where you can keep a fixed amount of money every month.

Term deposit: It is an account with a short-term maturity period that can range between a month and a few years.

Deposit: It is the act of putting money into the savings account, because of which the account balance grows.

Withdrawal: Withdrawal happens when you take money out of your account, and the balance moves down.

Account balance: The amount of money your account holds after you have deposited and/or withdrawn money into/from it.

For example, your account already has Rs. 500 when you added Rs. 250 to it,

box of chocolates and so withdraw Rs. 200 from the account. Your balance

22

Interest: It is the money that the bank pays you over and above your deposit. The more money you deposit and maintain, the more interest you will earn.

Loan: When you borrow money from the bank in order to buy something with it, it is called a loan. You need to give back the same amount of money to the bank over a certain period of time, along with an interest.

Cheque: It is a document issued by the bank which you can use to pay a sum to say, your friend. While you need not pay your friend by cash, the bank will withdraw the exact sum promised in the cheque from your account and deposit it

ATM:cash. An ATM or an Automated Teller Machine contains money, and you can draw cash from it around the clock.

Internet banking: In this digital age, you can do all your banking work without even going to the bank. Sit at your computer, click the mouse and check your balance, transfer money to a friend, or pay your electricity bill, all from the comfort of your house.

You can open a junior account, similar to a regular savings account. However, there are certain guidelines you should follow. They are:

23

What are the rules?

An individual below 18 years of age can have a minor bank account. It will be jointly held by a parent or guardian who needs to have their individual account with the same bank.

A minor over 10 years is allowed access to their own account.

A junior savings bank account will have same rules as a regular savings account, e.g. annual charges, withdrawal limits, and minimum balance rules.

Most banks issue cheque books, and ATM-debit cards to minor account holders.

What documents do you need for opening an account?

Photo Identity Proof - You need to provide one of the following documents as photo identity proof:

i. Passport

ii. Permanent Account Number (PAN)

iii. Ration card

Address Proof – One of the following documents will suffice:

i. Passport

ii. Telephone bill

iii. Electricity bill

Note: While opening an account with the bank, always remember to carry original documents along with photocopies of each document.

24

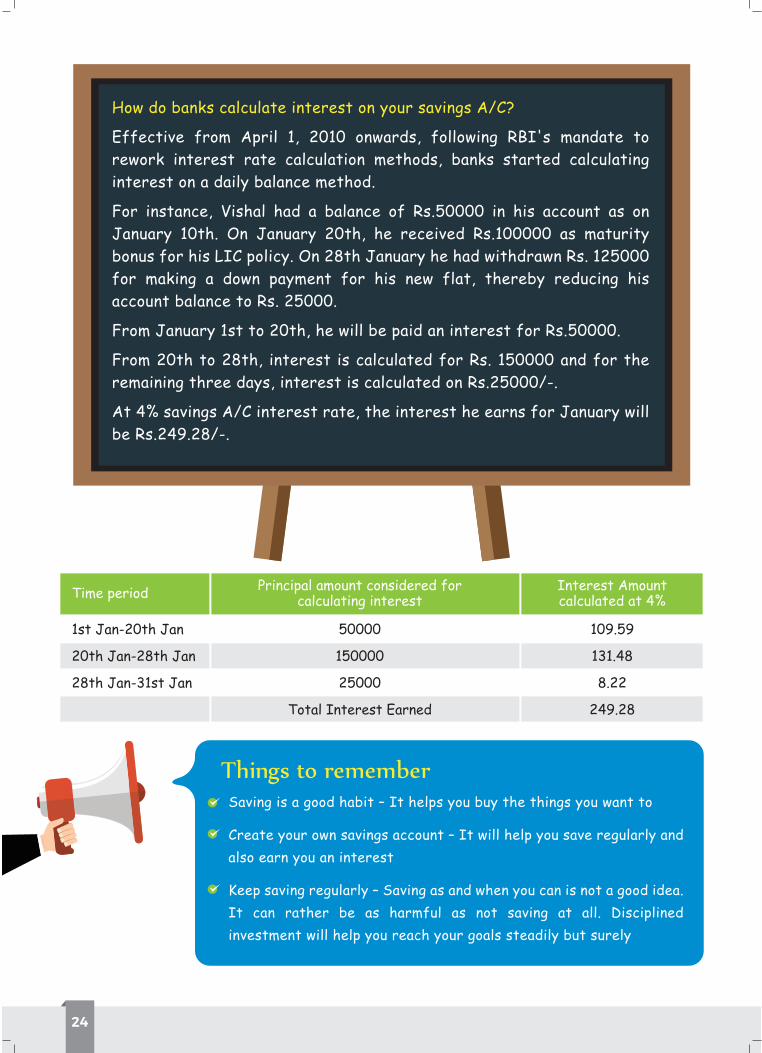

Saving is a good habit – It helps you buy the things you want to

Create your own savings account – It will help you save regularly and also earn you an interest

Keep saving regularly – Saving as and when you can is not a good idea. It can rather be as harmful as not saving at all. Disciplined investment will help you reach your goals steadily but surely

How do banks calculate interest on your savings A/C?

Effective from April 1, 2010 onwards, following RBI's mandate to rework interest rate calculation methods, banks started calculating interest on a daily balance method.

For instance, Vishal had a balance of Rs.50000 in his account as on January 10th. On January 20th, he received Rs.100000 as maturity bonus for his LIC policy. On 28th January he had withdrawn Rs. 125000 for making a down payment for his new flat, thereby reducing his account balance to Rs. 25000.

From January 1st to 20th, he will be paid an interest for Rs.50000.

From 20th to 28th, interest is calculated for Rs. 150000 and for the remaining three days, interest is calculated on Rs.25000/-.

At 4% savings A/C interest rate, the interest he earns for January will be Rs.249.28/-.

1st Jan-20th Jan

20th Jan-28th Jan

28th Jan-31st Jan

50000

150000

25000

Total Interest Earned

109.59

131.48

8.22

249.28

Principal amount considered forcalculating interest

Interest Amountcalculated at 4%Time period

Chapter 6

Hello, students, Sir Nerdy here. Let us do some planning today, but it is not your regular planning. I am talking about financial planning, which refers to taking charge and managing your finances to ensure financial well-being. Financial planning is very important for fulfilling financial responsibilities in life.

Often you hear elders deliberating over buying household

colour, size and company and would love it if it comes before Diwali, but father is concerned that the said model may cost more than what he can afford.

FINANCIAL PLANNING

25

26

And then suddenly a family wedding invitation comes along the way and the new fridge has to wait for another two-three months as buying gift for the couple becomes more important. Such discussions are common in every

Therefore, planning ahead can save one a lot of headache.

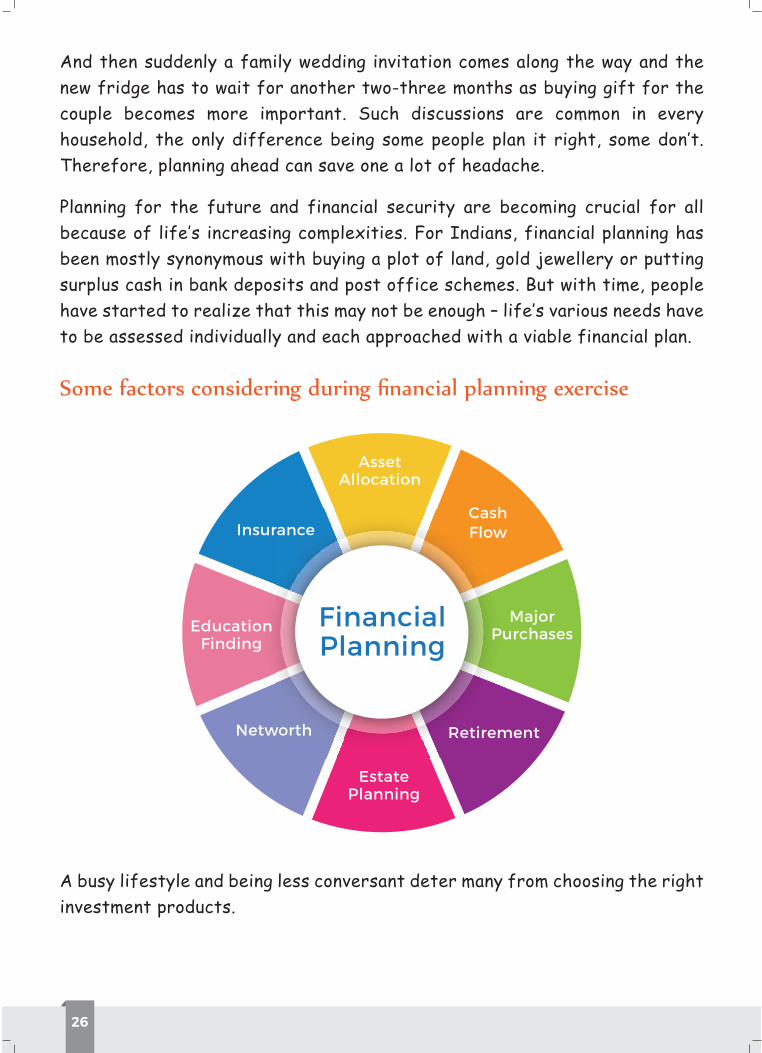

Planning for the future and financial security are becoming crucial for all

been mostly synonymous with buying a plot of land, gold jewellery or putting surplus cash in bank deposits and post office schemes. But with time, people

to be assessed individually and each approached with a viable financial plan.

A busy lifestyle and being less conversant deter many from choosing the right investment products.

Financial Planning

Asset Allocation

CashFlow

Major Purchases

Retirement

Estate Planning

Networth

Education Finding

Insurance

27

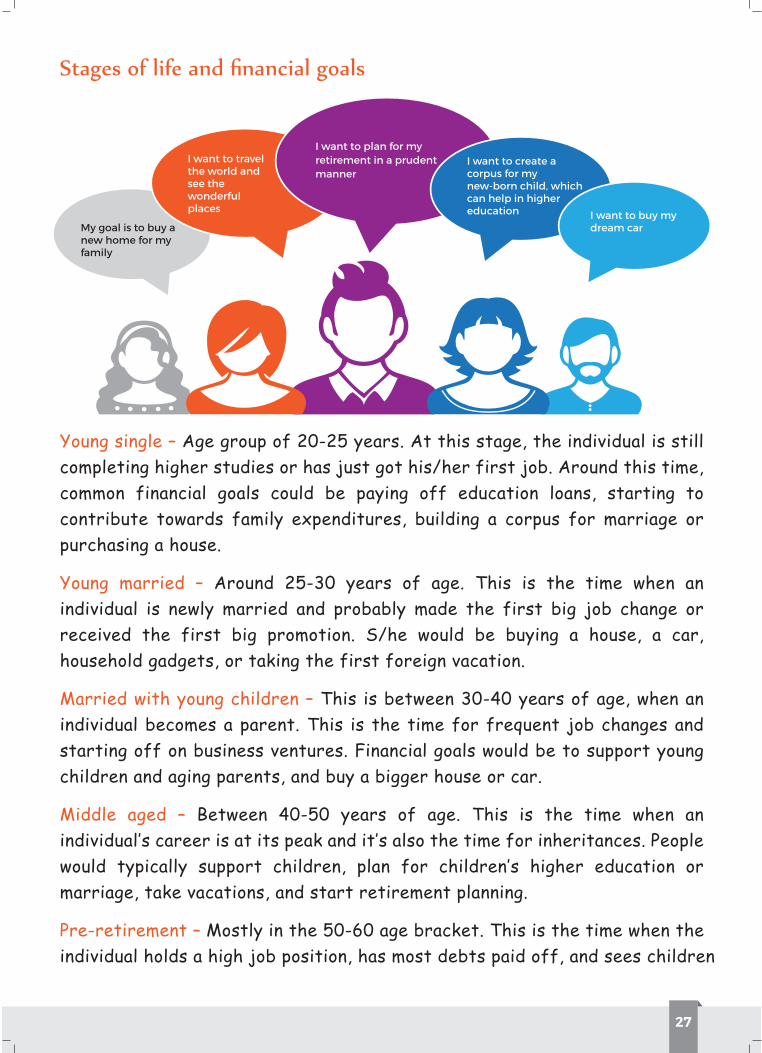

My goal is to buy a new home for my family

I want to travel the world and see the wonderful places

I want to plan for my retirement in a prudent manner

I want to create a corpus for my new-born child, which can help in higher education I want to buy my

dream car

Young single – Age group of 20-25 years. At this stage, the individual is still completing higher studies or has just got his/her first job. Around this time, common financial goals could be paying off education loans, starting to contribute towards family expenditures, building a corpus for marriage or purchasing a house.

Young married – Around 25-30 years of age. This is the time when an individual is newly married and probably made the first big job change or received the first big promotion. S/he would be buying a house, a car, household gadgets, or taking the first foreign vacation.

Married with young children – This is between 30-40 years of age, when an individual becomes a parent. This is the time for frequent job changes and starting off on business ventures. Financial goals would be to support young children and aging parents, and buy a bigger house or car.

Middle aged – Between 40-50 years of age. This is the time when an

marriage, take vacations, and start retirement planning.

Mostly in the 50-60 age bracket. This is the time when the individual holds a high job position, has most debts paid off, and sees children

28

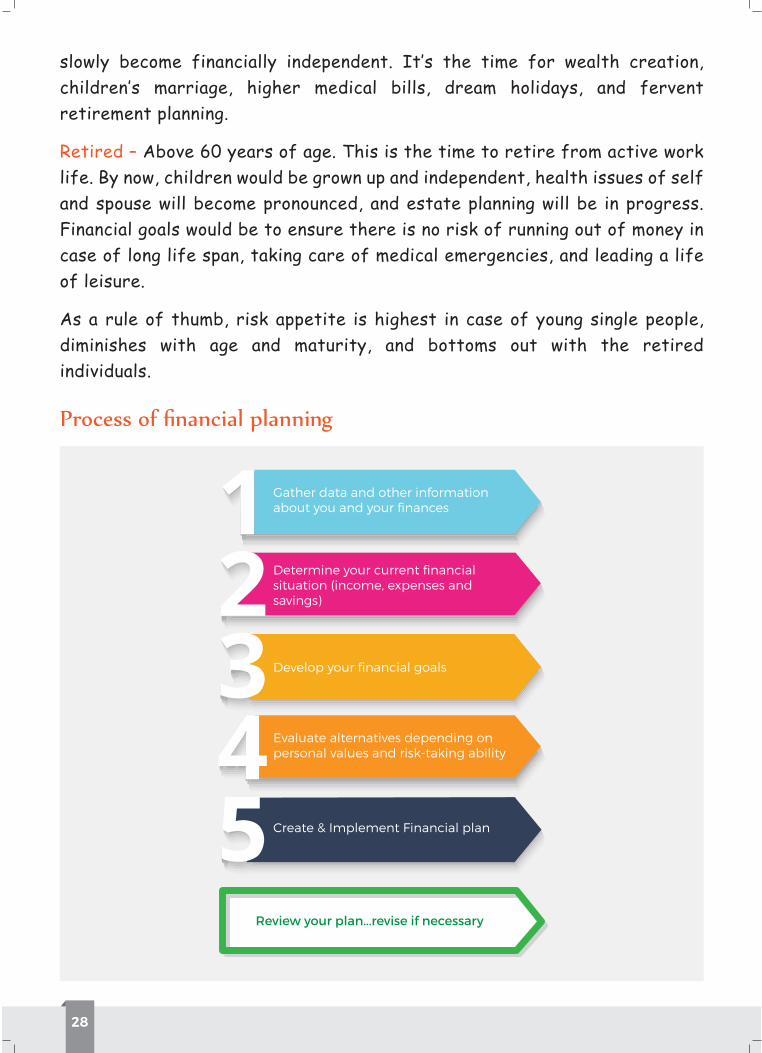

1 Gather data and other information about you and your finances

2345

Determine your current financial situation (income, expenses andsavings)

Evaluate alternatives depending on personal values and risk-taking ability

Create & Implement Financial plan

Develop your financial goals

Review your plan...revise if necessary

29

Financial planning is very important

It is equally important to review on a regular basis whether the financial planning you did is working for you or not.

Chapter 7

There is no better way of understanding compounding than

working with money or investments. The basic fundamental of

compounding is earning additional interest on interest. That

is, once you earn interest it is added back to the principal

amount, thereby, gradually increasing the base on which you

earn subsequent interests. So here Sir nerdy tries explaining

POWER OF COMPOUNDING

30

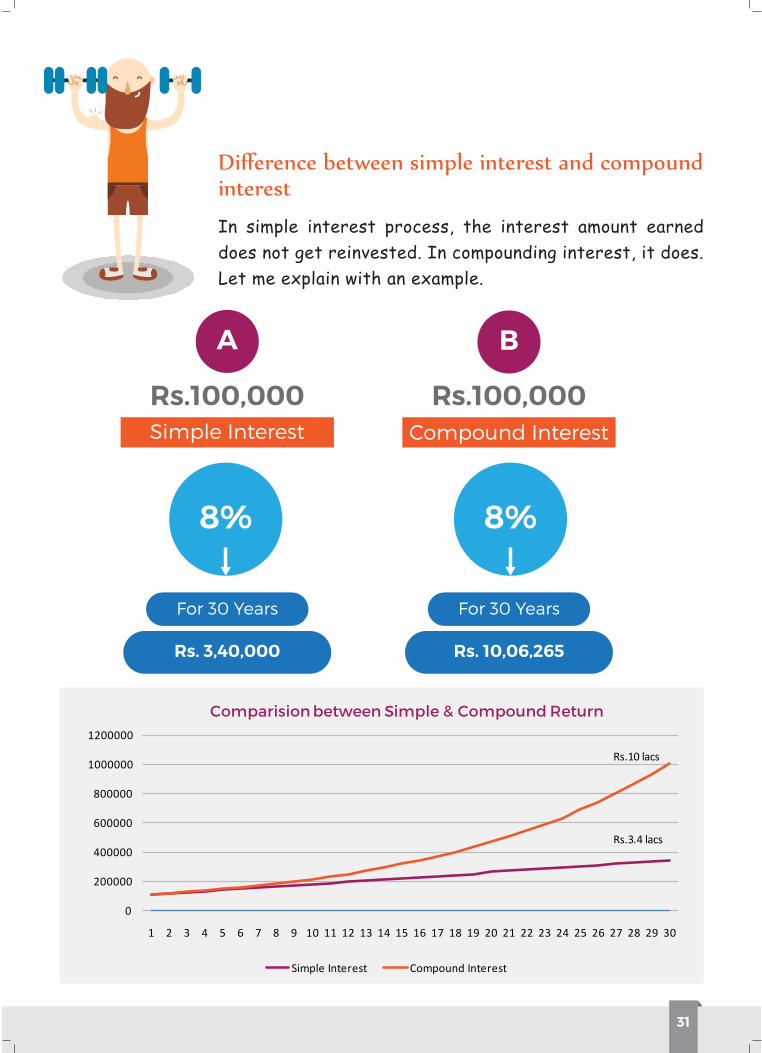

31

0

200000

400000

600000

800000

1000000

1200000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

Comparision between Simple & Compound Return

Simple Interest Compound Interest

Rs.10 lacs

Rs.3.4 lacs

In simple interest process, the interest amount earned does not get reinvested. In compounding interest, it does. Let me explain with an example.

A B

Rs.100,000 Rs.100,000 Simple Interest Compound Interest

8% 8%

For 30 Years

Rs. 3,40,000 Rs. 10,06,265

For 30 Years

32

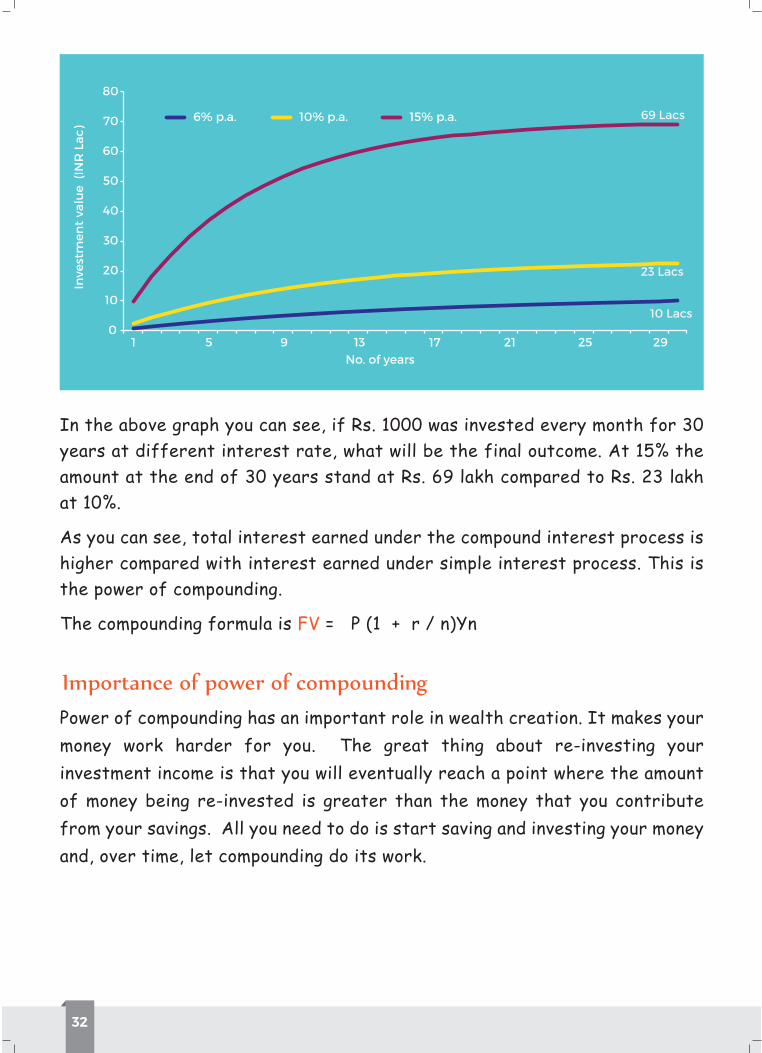

Power of compounding has an important role in wealth creation. It makes your money work harder for you. The great thing about re-investing your investment income is that you will eventually reach a point where the amount of money being re-invested is greater than the money that you contribute from your savings. All you need to do is start saving and investing your money and, over time, let compounding do its work.

In the above graph you can see, if Rs. 1000 was invested every month for 30 years at different interest rate, what will be the final outcome. At 15% the amount at the end of 30 years stand at Rs. 69 lakh compared to Rs. 23 lakh at 10%.

As you can see, total interest earned under the compound interest process is higher compared with interest earned under simple interest process. This is the power of compounding.

The compounding formula is FV = P (1 + r / n)Yn

0

10

20

30

40

50

60

70

80

1 5 9 13 17 21 25 29

Inve

stm

ent

valu

e (I

NR

Lac

)

No. of years

6% p.a. 10% p.a. 15% p.a.

10 Lacs

23 Lacs

69 Lacs

33

Saving is good (it makes life a lot simpler and helps you get the things you fancy)

Invest early (you saw what happened to Shyam)

Stay invested (invest with discipline and for any reason if you have to stop, forget about the accumulated money. Treat it the way you treat your coin or stamp collection – you collect these when you are a child and then one fine day you grow out of it. But the hard-put-together collection remains. You take it out once in a while, see, treasure, and keep it back safe.)

The earlier you start the better. Let me explain with a small example:

Ram and Shyam are two friends. When Ram was 25 years of age, he started investing Rs. 10,000 per year at an interest rate of 10% (say). By virtue of compounding, the amount stood at Rs. 108347, when he turned 50 years old (investment horizon of 25 years). Now, Shyam started investing the same amount when he was 35 years old. Assuming, the same interest rate of 10% interest p.a., the total amount earned by him at the age of 50 years is Rs. 41772. So you see, Ram was clever to start investing at an early age.

Chapter 8

Each and every one of us is always exposed to different kinds of risks, which involves losses. Every day we hear stories about some unfortunate happenings around us like accidents, suddenly someone falling seriously ill, or destruction of property and livelihood in cyclones and tsunamis.

To cover the various risks around, us we need to plan our future accordingly. Many a times we have seen that our parents or elders save money for the future. They do it to

the uncertainties of life.

INSURANCE

34

35

P

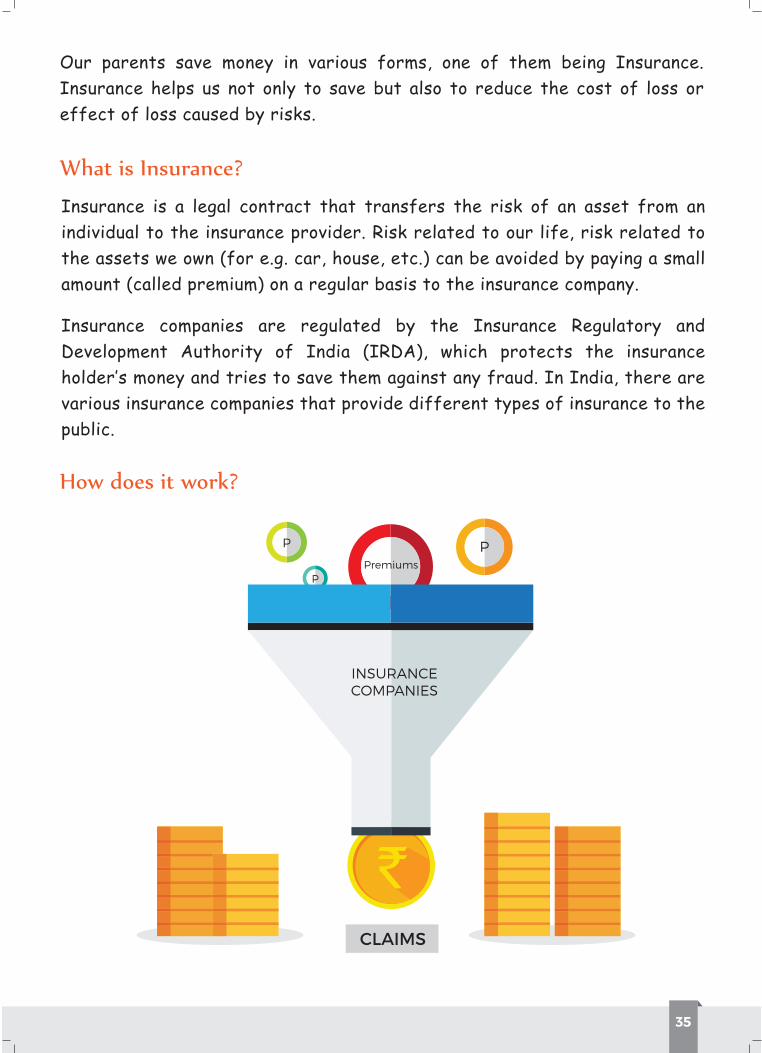

Our parents save money in various forms, one of them being Insurance. Insurance helps us not only to save but also to reduce the cost of loss or effect of loss caused by risks.

Insurance is a legal contract that transfers the risk of an asset from an individual to the insurance provider. Risk related to our life, risk related to the assets we own (for e.g. car, house, etc.) can be avoided by paying a small amount (called premium) on a regular basis to the insurance company.

Insurance companies are regulated by the Insurance Regulatory and Development Authority of India (IRDA), which protects the insurance

various insurance companies that provide different types of insurance to the public.

Premiums

INSURANCECOMPANIES

CLAIMS

PP

36

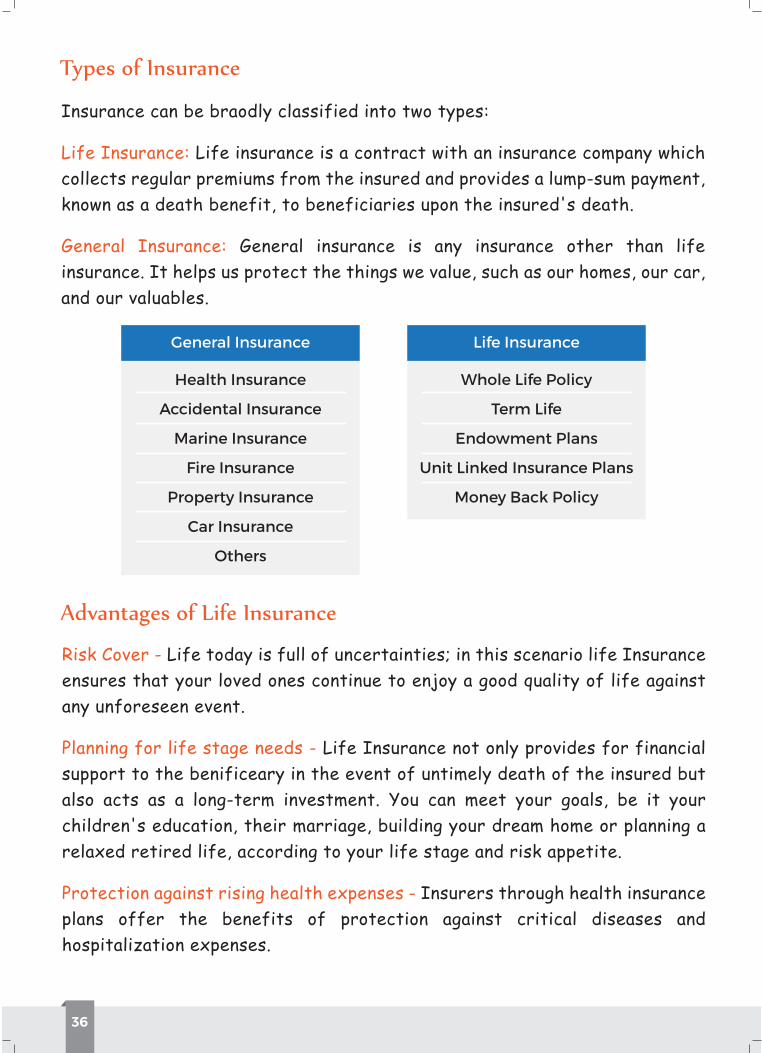

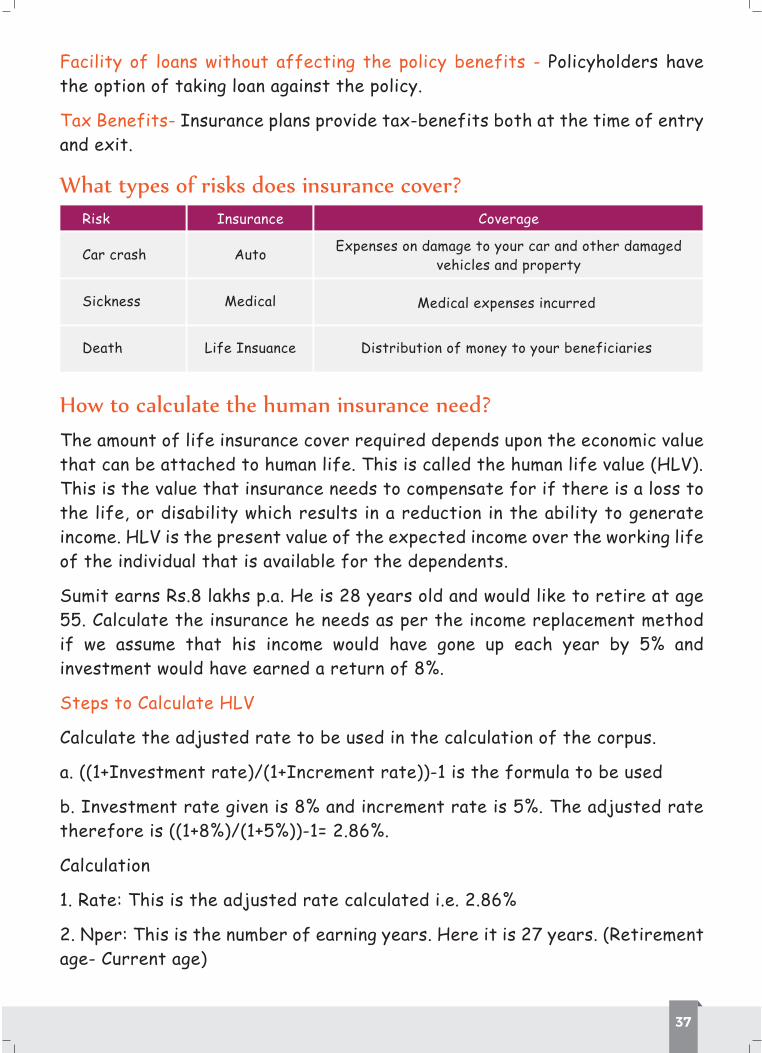

Insurance can be braodly classified into two types:

Life Insurance: Life insurance is a contract with an insurance company which collects regular premiums from the insured and provides a lump-sum payment, known as a death benefit, to beneficiaries upon the insured's death.

General Insurance: General insurance is any insurance other than life insurance. It helps us protect the things we value, such as our homes, our car, and our valuables.

Risk Cover - Life today is full of uncertainties; in this scenario life Insurance ensures that your loved ones continue to enjoy a good quality of life against any unforeseen event.

Planning for life stage needs - Life Insurance not only provides for financial support to the benificeary in the event of untimely death of the insured but also acts as a long-term investment. You can meet your goals, be it your children's education, their marriage, building your dream home or planning a relaxed retired life, according to your life stage and risk appetite.

Protection against rising health expenses - Insurers through health insurance plans offer the benefits of protection against critical diseases and hospitalization expenses.

Whole Life Policy

Term Life

Endowment Plans

Unit Linked Insurance Plans

Money Back Policy

Life Insurance

Health Insurance

Accidental Insurance

Marine Insurance

Fire Insurance

Property Insurance

Car Insurance

Others

General Insurance

37

Facility of loans without affecting the policy benefits - Policyholders have the option of taking loan against the policy.

Tax Benefits- Insurance plans provide tax-benefits both at the time of entry and exit.

The amount of life insurance cover required depends upon the economic value that can be attached to human life. This is called the human life value (HLV). This is the value that insurance needs to compensate for if there is a loss to the life, or disability which results in a reduction in the ability to generate income. HLV is the present value of the expected income over the working life of the individual that is available for the dependents.

Sumit earns Rs.8 lakhs p.a. He is 28 years old and would like to retire at age 55. Calculate the insurance he needs as per the income replacement method if we assume that his income would have gone up each year by 5% and investment would have earned a return of 8%.

Steps to Calculate HLV

Calculate the adjusted rate to be used in the calculation of the corpus.

a. ((1+Investment rate)/(1+Increment rate))-1 is the formula to be used

b. Investment rate given is 8% and increment rate is 5%. The adjusted rate therefore is ((1+8%)/(1+5%))-1= 2.86%.

Calculation

1. Rate: This is the adjusted rate calculated i.e. 2.86%

2. Nper: This is the number of earning years. Here it is 27 years. (Retirement age- Current age)

Risk Insurance Coverage

Car crash

Sickness

Death

Auto

Medical

Life Insuance

Expenses on damage to your car and other damagedvehicles and property

Medical expenses incurred

Distribution of money to your beneficiaries

38

3. PMT: This is the income in each year starting with Rs.8 lakhs in the first year in this example.

4. The amount calculated is the corpus required to generate the income that Sumit would have earned over 27 years. In this case it is Rs. 1,53,39,470.

Save Money for Future – As we learned above saving is a good habit beacuase whenever we require a large amount suddenly, we can take that amount from our savings.

Start Early – The earlier we start investing, the more we and our family will get secured.

like property, car, family, etc.

Chapter 9

Hi, I am Sir Nerdy, and I am here to explain the concept of Investment.

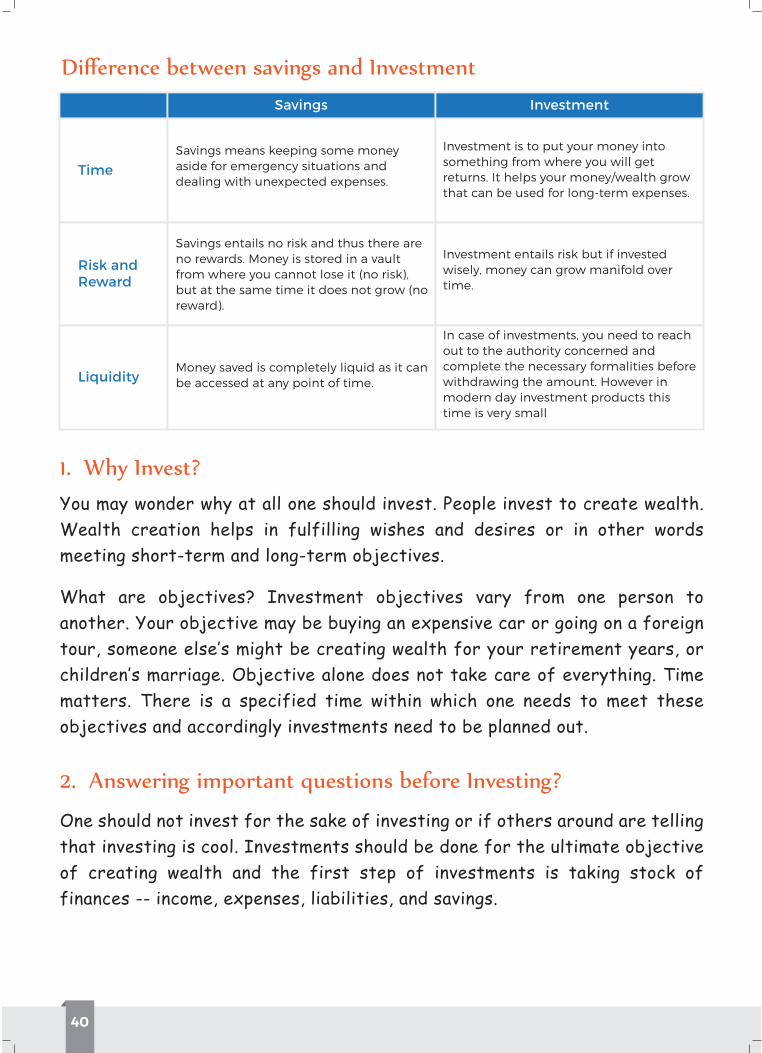

At the very onset let me clear the never-ending confusion between savings and investments. Both are used for meeting

two. After making all the expenses, the money that is left in

either be saved or invested.

INVESTMENTS

39

40

You may wonder why at all one should invest. People invest to create wealth. Wealth creation helps in fulfilling wishes and desires or in other words meeting short-term and long-term objectives.

What are objectives? Investment objectives vary from one person to another. Your objective may be buying an expensive car or going on a foreign

objectives and accordingly investments need to be planned out.

that investing is cool. Investments should be done for the ultimate objective

finances -- income, expenses, liabilities, and savings.

Di

Time

Savings Investment

Risk andReward

Liquidity

Savings means keeping some money aside for emergency situations and dealing with unexpected expenses.

Savings entails no risk and thus there are no rewards. Money is stored in a vault from where you cannot lose it (no risk), but at the same time it does not grow (no reward).

Money saved is completely liquid as it can be accessed at any point of time.

In case of investments, you need to reach out to the authority concerned and complete the necessary formalities before withdrawing the amount. However in modern day investment products this time is very small

Investment entails risk but if invested wisely, money can grow manifold over time.

Investment is to put your money into something from where you will get returns. It helps your money/wealth grow that can be used for long-term expenses.

41

Then answering these important questions:

1. What are my investment objectives?

2. What is the investment time frame?

3. What kind of investments are to be made?

4. How much money do I invest and on what frequency?

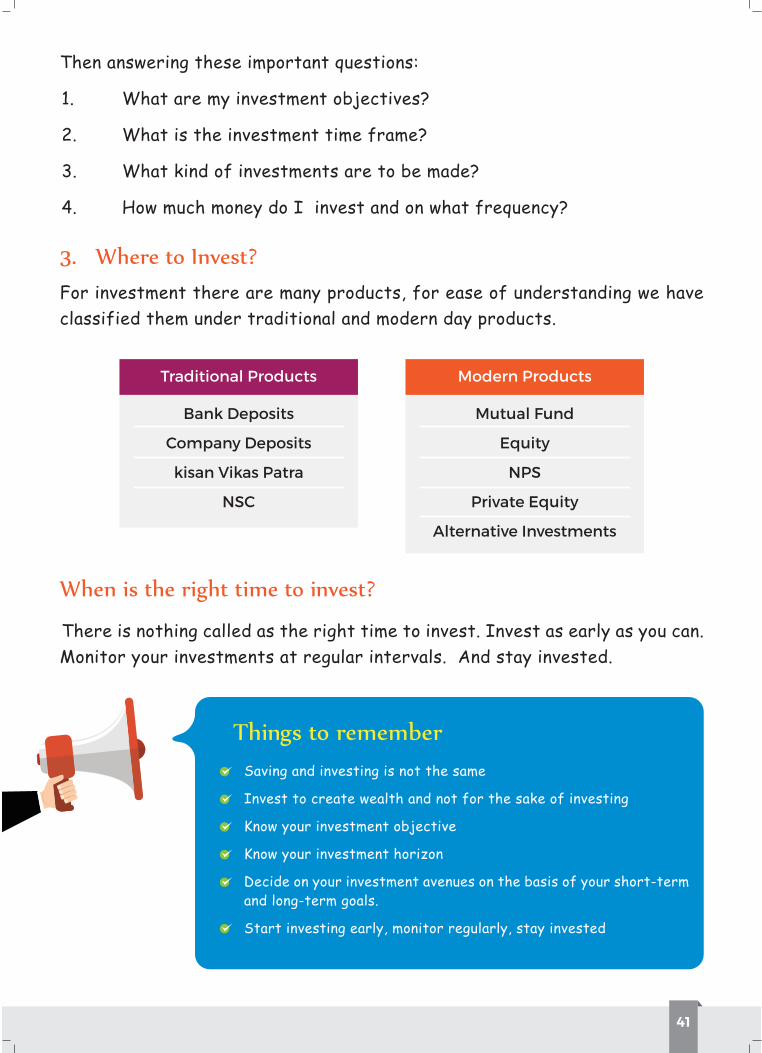

For investment there are many products, for ease of understanding we have classified them under traditional and modern day products.

Mutual Fund

Equity

NPS

Private Equity

Alternative Investments

Modern Products

Bank Deposits

Company Deposits

kisan Vikas Patra

NSC

Traditional Products

There is nothing called as the right time to invest. Invest as early as you can. Monitor your investments at regular intervals. And stay invested.

Saving and investing is not the same

Invest to create wealth and not for the sake of investing

Know your investment objective

Know your investment horizon

Decide on your investment avenues on the basis of your short-term and long-term goals.

Start investing early, monitor regularly, stay invested

5

5

`

Chapter 10

Hello!! I am Sir Nerdy and today I will tell you about traditional investments. From the olden days, people have put in their money in some of the low-risk traditional investment options that are still worth investing your money in. In finance, the notion of traditional investments refers to putting money into well-known assets so that one enjoys capital appreciation, earns dividends, and interest. The investment you select depends on your financial goals, your investment preferences, and your tolerance for risk.

INTRODUCTION TO TRADITIONAL

AND MODERN INVESTMENTS

42

43

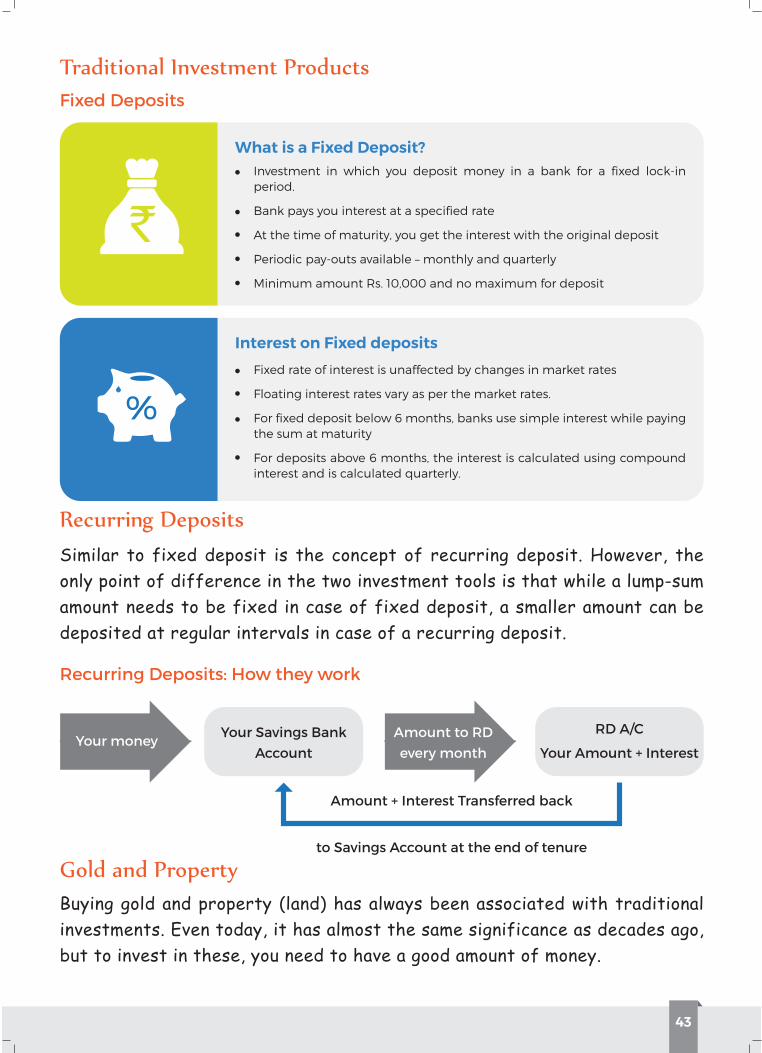

Fixed Deposits

What is a Fixed Deposit?Investment in which you deposit money in a bank for a fixed lock-in period.

Bank pays you interest at a specified rate

At the time of maturity, you get the interest with the original deposit

Periodic pay-outs available – monthly and quarterly

Minimum amount Rs. 10,000 and no maximum for deposit

Interest on Fixed deposits

Fixed rate of interest is unaffected by changes in market rates

Floating interest rates vary as per the market rates.

For fixed deposit below 6 months, banks use simple interest while paying the sum at maturity

For deposits above 6 months, the interest is calculated using compound interest and is calculated quarterly.

%

Similar to fixed deposit is the concept of recurring deposit. However, the only point of difference in the two investment tools is that while a lump-sum amount needs to be fixed in case of fixed deposit, a smaller amount can be deposited at regular intervals in case of a recurring deposit.

Recurring Deposits: How they work

Your moneyYour Savings Bank

AccountAmount to RDevery month

RD A/C

Your Amount + Interest

Amount + Interest Transferred back

to Savings Account at the end of tenure

Buying gold and property (land) has always been associated with traditional investments. Even today, it has almost the same significance as decades ago, but to invest in these, you need to have a good amount of money.

44

Kisan Vikas Patra (KVP) is an investment option that is issued by the government of India. The KVP is a certificate that can be purchased from any post office in India. Any Indian citizen can purchase a KVP individually or jointly. A guardian can do the same for a minor child. This is a long-term investment plan where your main investment doubles in eight years and seven months. As it is issued by the government, the investments are safe and risk-free.

Public Provident Fund (PPF) scheme is a popular long term investment option backed by Government of India which offers safety with attractive interest rate and returns that are fully exempted from Tax. Investors can invest minimum Rs. 500 to maximum Rs. 1,50,000 in one financial year and can get the facilities such as loan, withdrawal and extension of account.

National Savings Certificates, popularly known as NSC, is an Indian Government Savings Bond, primarily used for small savings and income tax saving investments in India. It is part of the postal savings system of Indian Postal Service (India Post). Rate of interest under the scheme is 8.10%. Maturity value of a certificate of Rs.100/- purchased on or after 1.4.2012 shall be Rs. 147.61 after 5 years. Investment up to Rs. 1,00,000/- per annum qualifies for IT Rebate under section 80C of Income Tax Act.

Small savings is another popular savings tool. The name itself suggests that these tools are meant for saving money in small amounts. Let us look into some of the most prominent schemes under this.

National Pension Scheme is one of the most popular schemes for ensuring a regular pension amount to individuals working in both the private and public sectors. The scheme offers withdrawal of deposited amount only once the account holder reaches the age of 60 years. The amount withdrawn on

45

Objective Eligiblity Who can invest?

Tax benefit Interest rate Deposit

Withdrawal Where to open the account Transferability

Maturity

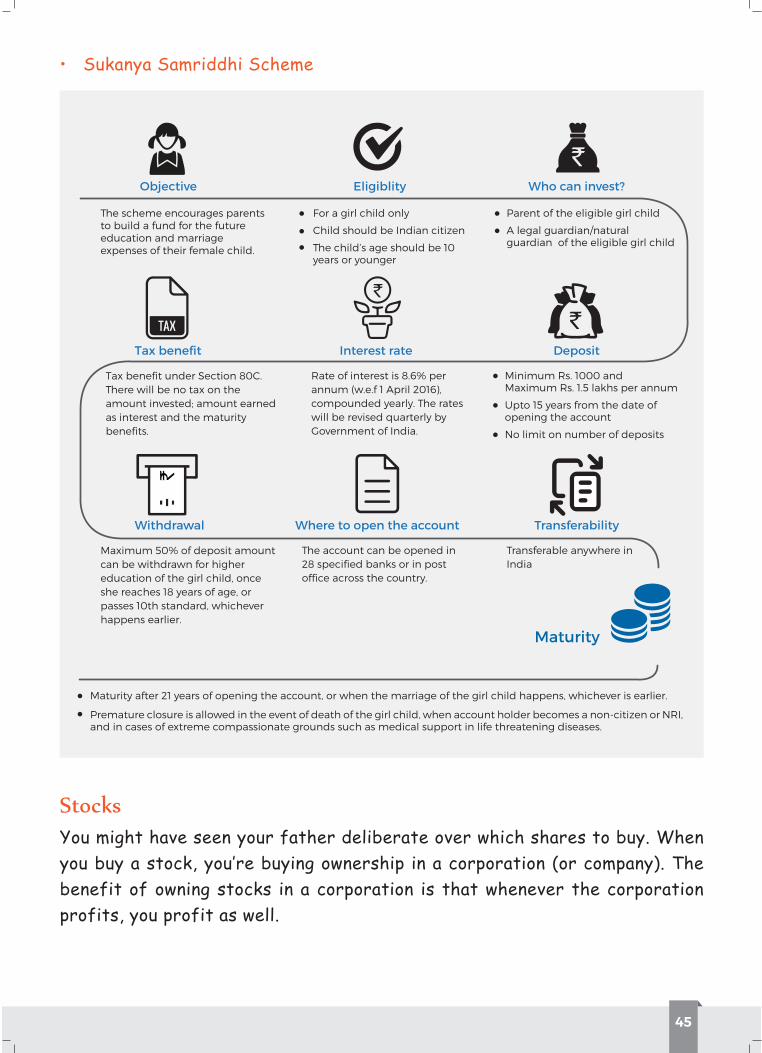

The scheme encourages parents to build a fund for the future education and marriage expenses of their female child.

Tax benefit under Section 80C. There will be no tax on the amount invested; amount earned as interest and the maturity benefits.

For a girl child only

Child should be Indian citizen

The child’s age should be 10 years or younger

Rate of interest is 8.6% per annum (w.e.f 1 April 2016), compounded yearly. The rates will be revised quarterly by Government of India.

Maximum 50% of deposit amount can be withdrawn for higher education of the girl child, once she reaches 18 years of age, or passes 10th standard, whichever happens earlier.

Maturity after 21 years of opening the account, or when the marriage of the girl child happens, whichever is earlier.

Premature closure is allowed in the event of death of the girl child, when account holder becomes a non-citizen or NRI, and in cases of extreme compassionate grounds such as medical support in life threatening diseases.

The account can be opened in 28 specified banks or in post office across the country.

Transferable anywhere in India

Parent of the eligible girl child

A legal guardian/natural guardian of the eligible girl child

Minimum Rs. 1000 and Maximum Rs. 1.5 lakhs per annum

Upto 15 years from the date of opening the account

No limit on number of deposits

Stocks

46

These are some of the low or moderate risk traditional investments. Though these investment instruments are also not 100% secure, but still one must invest some part of their money into any of these to beat inflation and help their money grow.

Conclusion

In a mutual fund, hundreds and thousands of people/investors pool in money. The money is invested by a fund manager (expert) to build a collection of stocks, bonds, real estate, or other securities with the aim of increasing the value of each share. Each investor gets a part of the total pie. Thus, a mutual fund is one of the most viable investment options for the common man as it offers an opportunity to invest in a diversified, professionally- managed basket of securities at a relatively low cost. Please refer chapter 12 for details about this product.

The investment you select depends on your financial goals, your investment preferences, and your tolerance for risk.

Traditional investments are time-tested, low-risk options.

company).

The idea behind small schemes is to inculcate the habit of saving among people.

Chapter 11

INTRODUCTION OF ASSET CLASSES

47

48

Suppose your mother sends you to the grocery store to get a few things for the kitchen. She asks you to buy turmeric powder, oregano, cardamom, onion, and potatoes. While the first three items on the list can be grouped under

are:

i. Debt–

ii. Property –buying a house, it typically means owning commercial property like offices, warehouses, and industrial units.

iii. Equities or company shares – Owning a share of a company implies owning a part of that company. This enables you to get a portion of the profits the

49

financial goals would be best met by investing in small-cap stocks. But it is even more crucial to remember not to invest the entire amount in small-cap stocks, or any other single asset class for that matter. Diversification is the key word here.

Heard of the saying, “never put all your eggs in one basket”? There you go!

What kind of shares can one invest in?

There are a variety of shares to choose from, depending on your financial goals. These categories can be broken down on the basis of:

a. Size – Large to small companies

b. Industry – Industries like technology, hospitality, or healthcare

c. Country-wise – Indian companies or Asian companies

d. Type – It can be further classified into Value and Growth

Example: If you had spent Rs 55,000 to buy a Royal Enfield motorcycle in 2001, you would now have an old, rugged bike. But if you had invested the same Rs 55,000 in shares (at Rs 17.50 per share) of Eicher Motors, the company that makes Enfield bikes, your investment will be worth Rs 4.75 crore now.

If I had the technology to send a message back in time, I would tell my father in 1980 to “Use Rs.10,000 to buy 100 shares of Wipro as an one-time investment and never sell it for the next 30-35 years.” If he had done that his investment would now be worth about Rs.535 crores. Yes, you read that right. Crores, not thousands or lakhs.

Commodity: In this asset class investment is made in precious commodities like gold and silver

50

i. Choose the asset-class mix – One should find out what mix works best

Chapter 12

Hi, I am Sir Nerdy, and I am here to explain the concept of Mutual fund is modern day investment

MUTUAL FUNDS & SIP

51

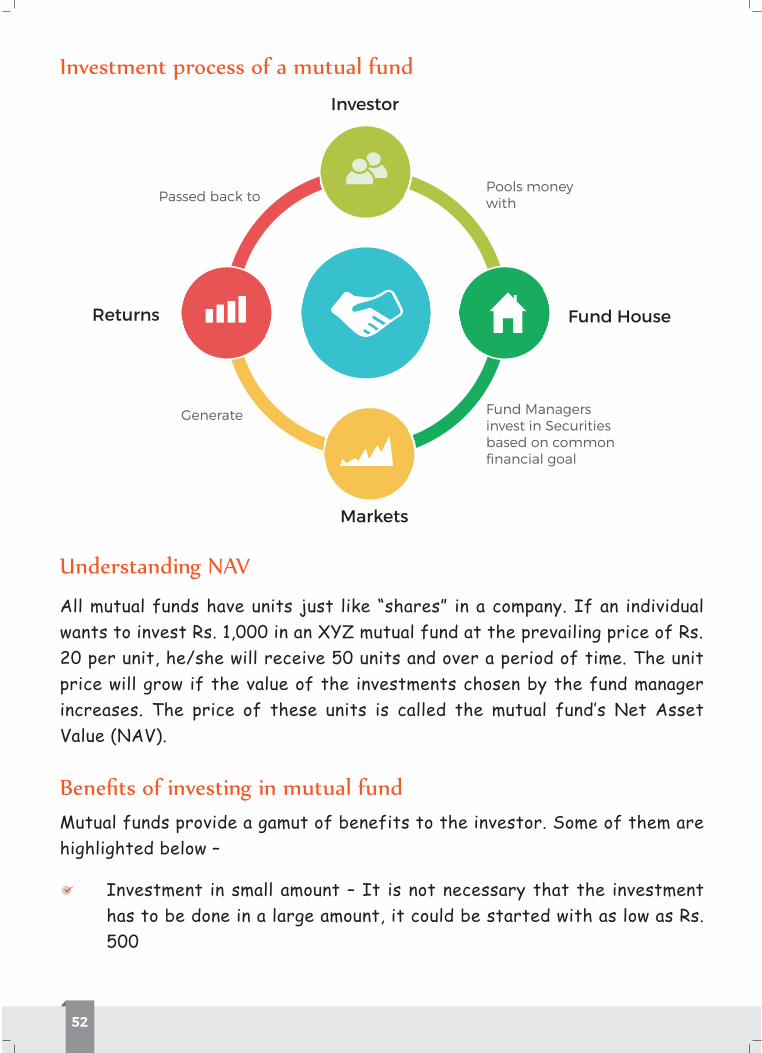

In a mutual fund, hundreds and thousands of people/investors

52

All mutual funds have units just like “shares” in a company. If an individual wants to invest Rs. 1,000 in an XYZ mutual fund at the prevailing price of Rs. 20 per unit, he/she will receive 50 units and over a period of time. The unit price will grow if the value of the investments chosen by the fund manager

Mutual funds provide a gamut of benefits to the investor. Some of them are highlighted below –

Investment in small amount – It is not necessary that the investment has to be done in a large amount, it could be started with as low as Rs. 500

Investor

Pools moneywith

Fund House

Fund Managersinvest in Securitiesbased on commonfinancial goal

Markets

Generate

Returns

Passed back to

53

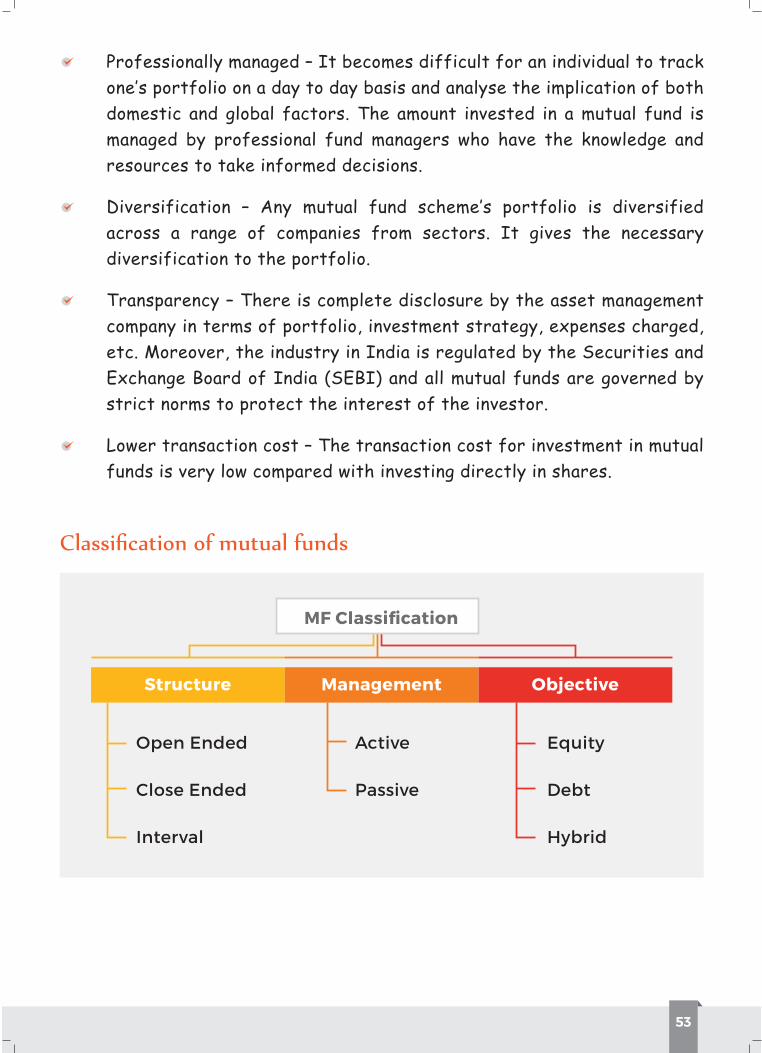

Structure Management Objective

Open Ended

Close Ended

Interval

Active

Passive

Equity

Debt

Hybrid

MF Classification

Professionally managed – It becomes difficult for an individual to track

resources to take informed decisions.

54

SIP is an easy and convenient mode of investing a fixed amount at regular intervals in a mutual fund scheme. It is conceptually similar to bank Recurring Deposit (RD) but there are a few differences, like –

Rate of return is predefined in bank RD but in case of SIP, it depends upon the prevailing market conditions

Over the long run, the returns generated through a, SIP in equity fund is likely to outperform the returns generated through a bank RD

An open ended mutual fund is open at all time for entry and exit for the investor. So one can invest in it anytime and can also get out of it anytime. Whereas, in a close ended mutual fund, there is a specified entry and exit time and it comes with a pre-defined time frame.

A mutual fund can either be actively managed or passively managed depending upon the investment objective. In an actively managed fund, the fund manager goes through data and information, researches the company, the economy, analyses market trends and then takes the investment decision. Whereas, in a passively managed fund, the fund manager tries to replicate the performance of the benchmark index.

Another way of classifying mutual funds is based on the underlying asset class where majority of the investment has been done by the fund manager keeping in mind the investment objective.

Equity Mutual Fund are those that invests majority of its money in companies shares (equity).

Debt Mutual Fund are those that invests majority of its money in debt instruments such as debentures, Govt. securities, commercial papers, etc.,

Hybrid Mutual Funds are those that invest in both equity and debt in a balanced ratio.

55

1

2

3

4

Total

Average Purchase Price

Average Cost Per Unit

1000

1000

1000

1000

4000

10

12

14

16

52

13

12.61

100

83.33

71.43

62.5

317.26

10

8

6

4

28

7

6.23

100

125

166.67

250

641.67

10

12

8

10

40

10

9.8

100

83.33

125

100

408.33

Month AmountInvested

Rising Market

NAV Units NAV Units NAV Units

Failing Market Volatile Market

Example

If you started investing Rs. 10,000 a month from your 40th birthday, in 20

Discipline

Power of compounding

Rupee cost averaging

Convenience

Lower transaction cost

Ad

van

tag

es o

f S

IP

The main advantages of investment in mutual fund through SIP mode are –

helps in building a portfolio

be the returns

equities

56

Mutual fund is a convenient way to invest in capital markets

Mutual funds can help an investor build a diversified portfolio at a lower cost

SIP is a smart and hassle-free mode for investing money in mutual funds

SIP is a planned approach towards investments and helps in inculcating the habit of regular savings and building wealth for the future

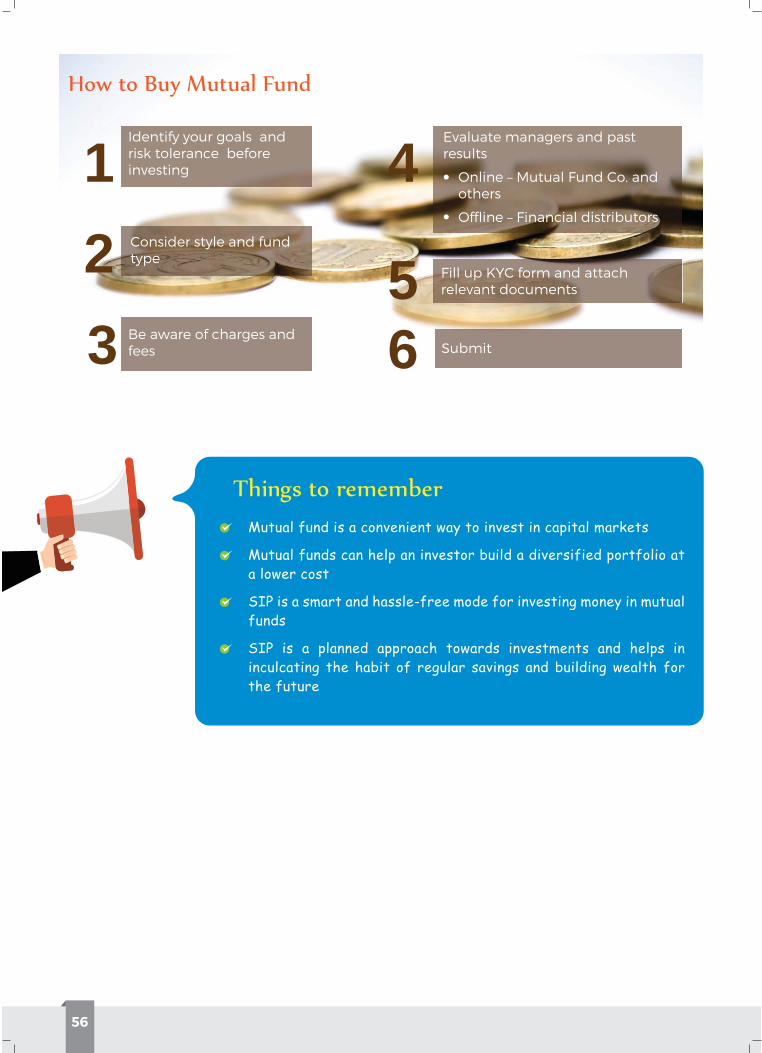

123

4

5Submit6

Identify your goals and risk tolerance before investing

Evaluate managers and past results

Online – Mutual Fund Co. and others

Offline – Financial distributors

Fill up KYC form and attach relevant documents

Consider style and fund type

Be aware of charges and fees

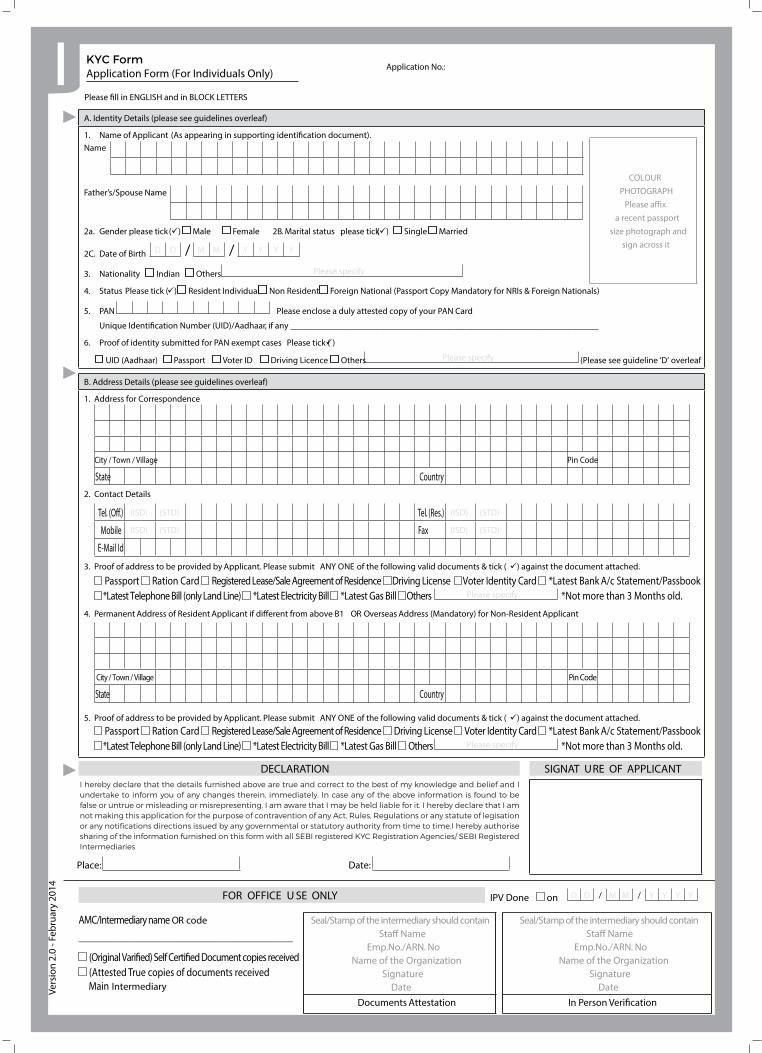

KYC FormApplication Form (For Individuals Only)

Please fill in ENGLISH and in BLOCK LETTERS

A. Identity Details (please see guidelines overleaf)

1. Name of Applicant (As appearing in supporting identification document).Name

Father’s/Spouse Name

2a. Gender please tick ( ) Male Female 2B. Marital status please tick ( ) Single Married

2C. Date of Birth D D / M M / Y Y Y Y

3. Nationality Indian Others Please specify

4. Status Please tick ( ) Resident Individual Non Resident Foreign National (Passport Copy Mandatory for NRIs & Foreign Nationals)

5. PAN Please enclose a duly attested copy of your PAN Card

Unique Identification Number (UID)/Aadhaar, if any _____________________________________________________________________

6. Proof of identity submitted for PAN exempt cases Please tick ( )

UID (Aadhaar) Passport Voter ID Driving Licence Others Please specify (Please see guideline ‘D’ overleaf

B. Address Details (please see guidelines overleaf)

1. Address for Correspondence

City / Town / Village Pin Code

State Country2. Contact Details

Tel. (Off.) (ISD) (STD) Tel. (Res.) (ISD) (STD)

Mobile (ISD) (STD) Fax (ISD) (STD)

E-Mail Id

3. Proof of address to be provided by Applicant. Please submit ANY ONE of the following valid documents & tick ( ) against the document attached. Passport Ration Card Registered Lease/Sale Agreement of Residence Driving License Voter Identity Card *Latest Bank A/c Statement/Passbook *Latest Telephone Bill (only Land Line) *Latest Electricity Bill *Latest Gas Bill Others Please specify *Not more than 3 Months old. 4. Permanent Address of Resident Applicant if different from above B1 OR Overseas Address (Mandatory) for Non-Resident Applicant

City / Town / Village Pin Code

State Country

5. Proof of address to be provided by Applicant. Please submit ANY ONE of the following valid documents & tick ( ) against the document attached.

Passport Ration Card Registered Lease/Sale Agreement of Residence Driving License Voter Identity Card *Latest Bank A/c Statement/Passbook *Latest Telephone Bill (only Land Line) *Latest Electricity Bill *Latest Gas Bill Others Please specify *Not more than 3 Months old.

DECLARATION SIGNAT URE OF APPLICANT

Place: Date:

FOR OFFICE U SE ONLY IPV Done on D D / M M / Y Y Y Y

AMC/Intermediary name OR code

__________________________________________

(Original Varified) Self Certified Document copies received (Attested True copies of documents received Main Intermediary

Seal/Stamp of the intermediary should containStaff Name

Emp.No./ARN. NoName of the Organization

SignatureDate

Seal/Stamp of the intermediary should containStaff Name

Emp.No./ARN. NoName of the Organization

SignatureDate

Documents Attestation In Person Verification

Application No.:

COLOURPHOTOGRAPH

Please affixa recent passport

size photograph andsign across it

Vers

ion

2.0

- Feb

ruar

y 20

14

I hereby declare that the details furnished above are true and correct to the best of my knowledge and belief and I undertake to inform you of any changes therein, immediately. In case any of the above information is found to be false or untrue or misleading or misrepresenting, I am aware that I may be held liable for it. I hereby declare that I am not making this application for the purpose of contravention of any Act, Rules, Regulations or any statute of legisation or any notifications directions issued by any governmental or statutory authority from time to time.I hereby authorise sharing of the information furnished on this form with all SEBI registered KYC Registration Agencies/ SEBI Registered Intermediaries

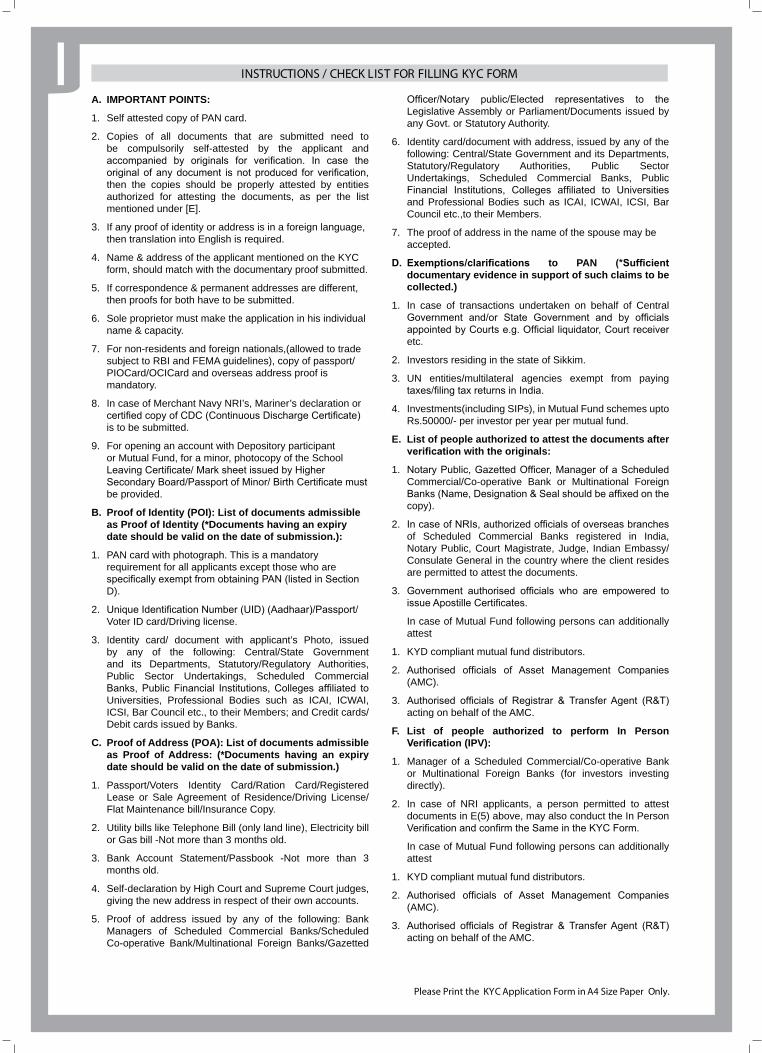

INSTRUCTIONS / CHECK LIST FOR FILLING KYC FORM

A. IMPORTANT POINTS:

1. Self attested copy of PAN card.

2. Copies of all documents that are submitted need to be compulsorily self-attested by the applicant and

then the copies should be properly attested by entities authorized for attesting the documents, as per the list mentioned under [E].

3. If any proof of identity or address is in a foreign language, then translation into English is required.

4. Name & address of the applicant mentioned on the KYC form, should match with the documentary proof submitted.

5. If correspondence & permanent addresses are different, then proofs for both have to be submitted.

6. Sole proprietor must make the application in his individual name & capacity.

7. For non-residents and foreign nationals,(allowed to trade subject to RBI and FEMA guidelines), copy of passport/PIOCard/OCICard and overseas address proof is mandatory.

8. In case of Merchant Navy NRI’s, Mariner’s declaration or

is to be submitted.

9. For opening an account with Depository participant or Mutual Fund, for a minor, photocopy of the School

be provided.

B. Proof of Identity (POI): List of documents admissible as Proof of Identity (*Documents having an expiry date should be valid on the date of submission.):

1. PAN card with photograph. This is a mandatory requirement for all applicants except those who are

D).

2. Voter ID card/Driving license.

3. Identity card/ document with applicant’s Photo, issued by any of the following: Central/State Government and its Departments, Statutory/Regulatory Authorities, Public Sector Undertakings, Scheduled Commercial

Universities, Professional Bodies such as ICAI, ICWAI, ICSI, Bar Council etc., to their Members; and Credit cards/Debit cards issued by Banks.

C. Proof of Address (POA): List of documents admissible as Proof of Address: (*Documents having an expiry date should be valid on the date of submission.)

1. Passport/Voters Identity Card/Ration Card/Registered Lease or Sale Agreement of Residence/Driving License/Flat Maintenance bill/Insurance Copy.

2. Utility bills like Telephone Bill (only land line), Electricity bill or Gas bill -Not more than 3 months old.

3. Bank Account Statement/Passbook -Not more than 3 months old.

4. Self-declaration by High Court and Supreme Court judges, giving the new address in respect of their own accounts.

5. Proof of address issued by any of the following: Bank Managers of Scheduled Commercial Banks/Scheduled Co-operative Bank/Multinational Foreign Banks/Gazetted

Legislative Assembly or Parliament/Documents issued by any Govt. or Statutory Authority.

6. Identity card/document with address, issued by any of the following: Central/State Government and its Departments, Statutory/Regulatory Authorities, Public Sector Undertakings, Scheduled Commercial Banks, Public

and Professional Bodies such as ICAI, ICWAI, ICSI, Bar Council etc.,to their Members.

7. The proof of address in the name of the spouse may be accepted.

to PAN documentary evidence in support of such claims to be collected.)

1. In case of transactions undertaken on behalf of Central

etc.

2. Investors residing in the state of Sikkim.

3. UN entities/multilateral agencies exempt from paying

4. Investments(including SIPs), in Mutual Fund schemes upto Rs.50000/- per investor per year per mutual fund.

E. List of people authorized to attest the documents after with the originals:

1. Commercial/Co-operative Bank or Multinational Foreign

copy).

2. of Scheduled Commercial Banks registered in India, Notary Public, Court Magistrate, Judge, Indian Embassy/Consulate General in the country where the client resides are permitted to attest the documents.

3.

In case of Mutual Fund following persons can additionally attest

1. KYD compliant mutual fund distributors.

2. (AMC).

3. acting on behalf of the AMC.

F. List of people authorized to perform In Person (IPV):

1. Manager of a Scheduled Commercial/Co-operative Bank or Multinational Foreign Banks (for investors investing directly).

2. In case of NRI applicants, a person permitted to attest documents in E(5) above, may also conduct the In Person

In case of Mutual Fund following persons can additionally attest

1. KYD compliant mutual fund distributors.

2. (AMC).

3. acting on behalf of the AMC.

Please Print the KYC Application Form in A4 Size Paper Only.

Disclaimer

All information contained in this document has been obtained by ICRA Online Limited

from sources believed by it to be accurate and reliable. Although reasonable care has been

taken to ensure that the information herein is true, such information is provided ‘as is’

without any warranty of any kind, and ICRA Online Limited or its affiliates or group

companies and its respective directors, officers, or employees in particular, makes no

representation or warranty, express or implied, as to the accuracy, suitability, reliability,

timelines or completeness of any such information. All information contained herein must

be construed solely as statements of opinion, and ICRA Online Limited, or its affiliates or

group companies and its respective directors, officers, or employees shall not be liable for

any losses or injury, liability or damage of any kind incurred from and arising out of any use

of this document or its contents in any manner, whatsoever. Opinions expressed in this

document are not the opinions of our holding company, ICRA Limited (ICRA), and should

not be construed as any indication of credit rating orgrading of ICRA for any instruments

that have been issued or are to be issued by any entity.