cgx: an expert support system for credit granting

TRANSCRIPT

European Journal of Operational Research 45 (1990) 293-308 293 North-Holland

CGX: An expert support system for credit granting

Venkat SRINIVASAN Northeastern University, 413 Hayden Hall Boston, MA 02115, and SR Research, Inc., Boston, MA, USA

Bharat RUPAREL Northeastern University, 413 Hayden Hall, Boston, MA 02115, and SR Research, Inc., Boston, MA, USA

Abstract: Computer and information technologies have made significant strides in the last two decades. Adaptation of these advances to support decision making has manifested itself in two classes of systems: decision support systems and expert systems. In this paper, we describe CGX, an expert support system for credit granting in nonfinancial firms. CGX is now undergoing extensive validation in several Fortune 500 corporations.

Keywords: Credit granting, expert systems, financial management

I. Introduction

The tremendous progress in computer and in- formation technologies in the last two decades has induced a qualitative change in the potential use of computers to aid decision making. The adapta- tion of such technological advances to support decision making has manifested itself in two classes of systems: decision support systems (DSS) and expert systems (ES). DSS originated with the idea that technological advances can be channeled to support and improve the effectiveness of managerial decision making. The emphasis in a traditional DSS is, therefore, on supporting managers and not replacing them. On the other hand, ES are an outgrowth of attempts to apply artificial intelligence technology and create intelli- gent systems that are used not only to perform storage, retrieval and computational tasks, but analytical and inferential tasks as well.

A common finding of many surveys of corpo- rate financial management practice has been that

Received August 1989

the real world usage of normative financial models is infrequent. It is widely recognized that this phenomenon is directly related to the complexity of the decision environment presented in norma- tive models, the lack of attention to such critical details as the availability of necessary information and the difficulty of usage. The onset of DSS and ES has significantly altered this scenario. Design- ing intelligent DSS and ES for corporate financial management can act as a major catalyst in our efforts to increase real world adoption of norma- tive financial models.

There is evidence that firms in the financial services industry have invested heavily in artificial intelligence technology with a view to developing a wide range of expert systems (Nisse, 1987). Some examples of systems reported in the litera- ture include the Authorizer's Assistant developed by American Express for credit authorization (Newquist, 1987), Trader's Assistant jointly devel- oped by Arthur D. Little and six financial institu- tions for selecting security brokers (Duffy, 1986), and the Portfolio Advisor developed by Athena Group for assisting fund managers in applying

0377-2217/90/$3.50 © 1990 - Elsevier Science Publishers B.V. (North-Holland)

294 v. Srinivasan, B. Ruparel / CGX: An expert support system for credit granting

qualitative techniques for portfolio selection. While there is little evidence on financial expert system development efforts in nonfinancial corporations, we are aware of a significant amount of work in progress on this front.

Expert systems for corporate financial deci- sions are likely to differ from conventional expert systems in at least one important way. Histori- cally, expert systems have been designed to be consultative in nature. Such systems prompt the user with a series of questions in the process of evaluating rules and stop when the facts supplied by the user satisfy a rule. However, in the context of financial expert systems, it is likely that a large amount of data will be repeatedly analyzed. This will make a sequential question-and-answer from very tedious and impractical. A better approach in these cases is to design the expert system around an efficient data base where all the relevant data can be stored and the rules can be automatically applied to the relevant set of data.

The data intensive nature of financial expert systems also imposes constraints on the type of expert systems tools that are most suited. While many commercial shells are available, financial systems will require the capability to seemlessly interface with data bases where the relevant data are being stored. Shells like lst-Class Fusion not only allow the developer to create knowledge bases that rely on extracted rules and facts but also allow easy interfaces with popular data base packages like DBASE III. A second alternative is to use a powerful relational data base manager for both data and rules (i.e., represent rules as data), use a 4-th generation language to design an in- ference engine and adopt an object oreinted de- sign philosophy. Other alternatives include the use of natural languages, instead of ready-made shells, like LISP and PROLOG. Here again, the connec- tivity with data bases is likely to be a crucial issue.

The main focus of this paper is on the design and development of CGX, and expert support system for credit granting in nonfinancial firms. The paper is divided into 5 sections. Section 2 presents a review of the corporate credit granting process both as prescribed in normative finance theory and as practiced in the real world. In Section 3, we briefly describe the design of the initial prototype. CGX is described in Section 4. The paper concludes with a summary and identi- fies extensions in progress.

2. Corporate credit granting

2.1. The normative point o f view

The basic goal of the industrial credit granting process is to balance the potential risk of loss against the probability of profits from granting credit. Academic research in this area can be grouped into three categories:

(i) attempts to evaluate customers' credit- worthiness by using a variety of multivariate sta- tistical procedures to optimally separate 'good' credit risks from 'bad ' credit risks (see, e.g., Buck- ley, 1971; Cyert and Thompson, 1968; Myers and Forgy, 1963),

(ii) attempts to explicitly consider future ben- efits and losses in credit granting (e.g., Bierman and Hausman, 1970; Dirickx and Wakeman, 1976; Mehta, 1970; Stowe, 1986; Srinivasan and Kim, 1987b), and

(iii) attempts to integrate the results from clas- sification models with the benefits and losses from granting credit (Srinivasan and Kim, 1987a).

Other than the choice of a classificatory model to separate customer groups on the basis of creditworthiness, the prescriptions of normative theory in credit granting can be summarized as follows:

(i) credit granting is a multiperiod problem implying that granting credit may not only enable the firm to make the current sale but also sell in the future to the same customer;

(ii) the extent of credit investigation must be determined by the tradeoff between the incremen- tal costs of investigation and the amount of credit involved;

(iii) estimate the present value of benefits and losses from granting credit for all the periods in the planning horizon, given the customer's action in the immediately prior period;

(iv) integrate probabilities of collection and de- fault with benefits and losses each period to com- pute the net present value from each period; and

(v) grant credit, if computed net present value is positive and reject full credit, otherwise. Note that where computed net present value is negative and credit for the requested amount is rejected, the customer may need to be reevaluated for a lower credit amount (if feasible) and the whole process repeated again. This is because the

V. Srinioasan, B. Ruparel / CGX: An expert support system for credit granting 295

probabilities of default and collection may be a function of the size of the credit request.

The choice of a classificatory model for assess- ing creditworthiness is largely an unresolved one. The assessment of default risk probabilities of customers is typically based on an evaluation of several customer attributes, financial and non- financial, that are perceived/found to reflect customer creditworthiness. Two basic approaches have evolved to facilitate such assessment of customer attributes: judgemental and statistical. All credit analysis, irrespective of the approach used, operate on similar principles. The basic premise in both sets of systems is that past experi- ence can be used as a guide in predicting the creditworthiness of future customers or existing customers in the future.

In a judgemental system, the credit applicant is evaluated by a credit analyst. The evaluation is based on a subjective assessment by the credit analyst of the applicant's attributes. The deter- ruination of which attributes are important is at least partially based on the analyst's past experi- ence. Judgemental systems have been criticized on several grounds (Eisenbeis, 1980). The fundamen- tal problem with judgemental systems that under- lies the various criticisms is the potential for lack of consistency in evaluating applicants. Statistical systems operate in much the same way as judge- mental systems. However, they rely upon multi- variate statistical methods and not on the experi- ence and judgement of the individual credit analyst. 1

A variety of multivariate statistical methodologies can be used depending on the nature of the problem and the un- derlying customer attribute data. These methods can be broadly categorized into two groups: simultaneous and sequential classification methods. Conventional methods like the MDA and logit are simultaneous classification methods since they attempt to derive customer groups by simulta- neously considering all customer attributes for which data are available. Relatively newer methods like goal program- ming and rank discriminant analsis also fall into this cate- gory. Methods like recursive partitioning and Quinlan's al- gorithm are sequential classification methods that repeatedly partition the customer attribute data to achieve group sep- aration. The theoretical motivation for repeated partitioning methods is essentially one of a conditional nested relation- ship between customer attributes, where the relevance/extent of influence of a customer attribute may depend on the relevance/extent of influence of other customer attributes.

Several problems surface when an attempt is made to translate the normative prescriptions for credit granting into practice. First, it is very dif- ficult, if not impossible, to estimate future benefits and losses from granting credit and, hence, the potential for future benefits can at best be consid- ered qualitatively. Second, firms usually have only incomplete information on customers and classifi- cation models estimated with full information will be inapplicable. Third, some of the attributes are qualitative in nature, e.g., management quality. It may be difficult to quantify them for the purposes of a multivariate statistical model.

2.2. Credit granting process in a Fortune 500 corpo- ration

The credit granting process in a participating Fortune 500 corporation (PC) should provide use- ful additional insight into the nature of the credit granting problem as practiced in the real world. The process in the PC was primarily studied through a series of in-depth interviews of the credit management staff as well as an extensive study of actual decision by credit analysts as they were made. Credit management staff at various level of the credit management hierarchy were interviewed. This provided a broad spectrum of perspectives along the strategic and operational dimensions of the credit granting process. The study design was an iterative one, and, at each iteration, we used the results of the previous itera- tion to obtain additional insight into the process. The iterations enabled us to refine and, in some cases, change initial estimations. The overall ob- jective of the iterative process was to move to- wards a consensus with respect to customer evaluation. One senior credit manager (designated as the 'expert') was involved in all iterations and stages of our analysis. We describe the identified process below.

The credit granting process in the PC consist of two related segments: setting credit limits and reviewing them once a year, and dealing with exceptions on a daily basis. All major credit lines (exceeding $20000) are reviewed at least once a year. Current credit limits are reviewed to reflect updated information on the customers. On the other hand, exceptions refer to new customers or customers who will exceed their current limits if their orders are approved or customers who have

296 I1". Srinioasan, B. Ruparel / CGX: An expert support system for credit granting

payments past due and need their orders ap- proved. The PC's computer order processing sys- tem has built-in checks that determine whether there are exceptions on any given day. Exceptions are then flagged and credit analysts having re- sponsibility for the customers review the cus- tomers' files and decide on credit extension.

Based on an analysis of the cost of investiga- tion and obtaining information, the PC has estab- lished a credit investigation sequence. All credit request for less than $5000 are investigated in terms of a background information card provided by the customer. Additional investigation in such cases is done if the analyst has any apparently negative information on the customer. Credit re- quests between $5000 and $20000 fall in the next level in the sequence. In this level, the credit analyst obtains financial information and letters from bank references. In some cases, subject to the discretion of the credit analyst, Dun and Bradstreet (D&B) reports on these customers are obtained on a one-time basis. For requests greater than $20000 but less than $50000, a more in- depth analysis is done based on the customers financial statements, D&B reports and bank ref- erences. Customers having credit limits greater than $50 000 undergo a very extensive evaluation. D & B reports for such customers are always ordered on a continuous basis.

The credit decision in the PC is primarily based on an assessment of the relevant customer attri- butes. Marketing a n d / o r promotional strategies have relatively less influence on the credit deci- sion. However, in marginal a n d / o r exceptional cases, credit may be granted due to strategic con- siderations, e.g., new product promotion. Analysis of the creditworthiness of customers in the PC can be synthesized in terms of five broad attribute categories. Within each of the categories, a variety of variables are assessed:

(a) Financial strength: Audited or unaudited statements. Proforma or actual statements. Profitability. Debt management:

Secured of unsecured. Off-balance sheet liabilities.

Liquidity. Intangibles.

(b)Customer background: Number of years in business.

Number of years of relationship with the PC. Perceived management quality. Recent filing of bankruptcy/l iquidat ion. Nature of bank references.

(c)Payment record: Past payment record (with the PC). Past payment record (trade). Internal of cash flow problems.

(d) Business potential and frequency: Growth potential. Customer's market position. Market for firm's other products. Order frequency.

(e) Geographical location: Perceived economic climate in customer lo- cation. Past experience in customer location.

The relative importance of the above factors and the degree of investigation by the credit analyst, of course, differs depending upon the level in which the customer falls. Further, credit investigation proceeds hierarchically starting with financial conditions. In other words, the analyst starts by reviewing the customer's financial condi- tion and conditional on h is /her findings will pro- ceed to investigate other customer attributes. The hierarchical order of investigation depends on the level of credit investigation and information avail- able. Typically, evaluation of financial soundness is followed by an examination of pay record, customer background, business potential and frequency and geographical location. Credit limits are set judgementally by linking the results of the customer evaluation process and the benefits and losses from the credit granting decision.

It may be useful to compare the identified process with the normative prescriptions outlined in the previous section. The credit granting proc- ess in the PC does consider the tradeoff between costs of investigation. The process also considers future benefits and losses, albeit qualitatively. Customer evaluation and setting of credit limits are judgemental. It should be further recognized that the credit granting process really consists of two phases:

(i) the customer evaluation phase in which the analyst evaluates customer attributes, and

(ii) the credit limit determination phases where the analyst judgementally collects h is /her evalua-

V. Srinivasan, B. Ruparel / CGX: An expert support system for credit granting 297

Level 1: Goal

Level 2: Criteria

Level 3: Objectives

Maximize Shareholder [ Wealth ]

Background I Record Potential Soundness

t I I Grant Deny Credit Credit

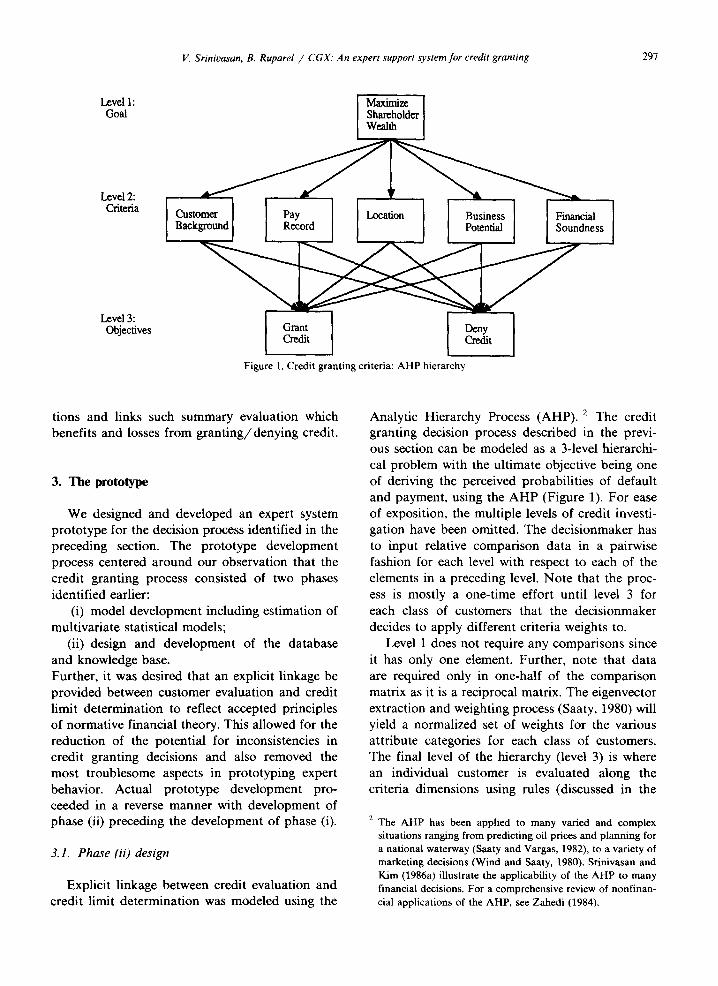

Figure 1. Credit granting criteria: AHP hierarchy

tions and links such summary evaluation which benefits and losses from grant ing/denying credit.

3. The prototype

We designed and developed an expert system prototype for the decision process identified in the preceding section. The prototype development process centered around our observation that the credit granting process consisted of two phases identified earlier:

(i) model development including estimation of multivariate statistical models;

(ii) design and development of the database and knowledge base. Further, it was desired that an explicit linkage be provided between customer evaluation and credit limit determination to reflect accepted principles of normative financial theory. This allowed for the reduction of the potential for inconsistencies in credit granting decisions and also removed the most troublesome aspects in prototyping expert behavior. Actual prototype development pro- ceeded in a reverse manner with development of phase (ii) preceding the development of phase (i).

3.1. Phase (ii) design

Explicit linkage between credit evaluation and credit limit determination was modeled using the

Analytic Hierarchy Process (AHP). 2 The credit granting decision process described in the previ- ous section can be modeled as a 3-level hierarchi- cal problem with the ultimate objective being one of deriving the perceived probabilities of default and payment, using the A H P (Figure 1). For ease of exposition, the multiple levels of credit investi- gation have been omitted. The decisionmaker has to input relative comparison data in a pairwise fashion for each level with respect to each of the elements in a preceding level. Note that the proc- ess is mostly a one-time effort until level 3 for each class of customers that the decisionmaker decides to apply different criteria weights to.

Level 1 does not require any comparisons since it has only one element. Further, note that data are required only in one-half of the comparison matrix as it is a reciprocal matrix. The eigenvector extraction and weighting process (Saaty, 1980) will yield a normalized set of weights for the various attribute categories for each class of customers. The final level of the hierarchy (level 3) is where an individual customer is evaluated along the criteria dimensions using rules (discussed in the

2 The AHP has been applied to many varied and complex situations ranging from predicting oil prices and planning for a national waterway (Saaty and Vargas, 1982), to a variety of marketing decisions (Wind and Saaty, 1980). Srinivasan and Kim (1986a) illustrate the applicability of the AHP to many financial decisions. For a comprehensive review of nonfinan- cial applications of the AHP, see Zahedi (1984).

298 V. Srinivasan, B. Ruparel / CGX: An expert support system for credit granting

next section). Integrating the local weights of the final revel with the appropriate global weights f rom the criterion level (level 2) will yield a final set of weights for an individual customer. These weights are the relative weights for granting and denying credit. In effect, they represent the expert 's estimates of prior probabilities of payment and default. 3

The weights for granting and denying can now be integrated with the expected cashflows associ- ated with the two outcomes. Letting Pl and P2 denote the relative weights for granting and deny- ing, respectively, c, the contr ibution margin per- centage, v, the variable cost propor t ion repre- senting incremental cash outflow, and s, the amount of credit requested (all in present value terms), the integration can be achieved using the conventional N P V framework:

N P V =p~cs - p2vs. (1)

The decision rule is to grant full credit, if the N P V is positive, and reject full credit, otherwise.

Frequently, two additional issues are of inter- est:

(i) what is the min imum weight at which the customer can be granted full credit, i.e., the breakeven weight for granting credit; and

(ii) what is the max imum credit that can be extended to the applicant on the current credit request, i.e., how much collateral should be ob- tained. The answer to both questions is straightforward. The min imum weight at which the customer may be granted full credit is when the relative weight for granting credit, Pl, equals the variable cost ratio, v (alternatively, when the relative weight for denying credit, P2, equals the contr ibut ion margin

3 To illustrate the process of weighting, consider any two adjacent levels in a hierarchy, i and i + 1. Each level has its own decision elements. Let the first element of the i-th level be denoted as 01( 0 . If one compares the elements of level i + 1 with respect to 01(0, a comparison matrix will result whose eigenvector describes the relative local priorities of elements in level i + 1 with respect to 01( 0. Let us denote this vector by wv Similarly comparisons are made with respect to each of the n elements in level i. This process results in n m-dimensional local priority vectors, where m is the number of elements in level i + 1. To find the global priorities of elements in the i + 1 level: Ws(i + 1 ) = [w 1, w 2 ..... w,]ws(i ), where wg(i) is the global priority vector for the elements of the i-th level.

percentage, c). Similarly, the maximum amount of credit that may be granted to the customer can be found as the level of credit at which benefits equal losses:

p lcs - p 2 v c l = 0, (2)

where c 1 is the max imum credit limit that can be granted to the customer. Note that (2) is useful to estimate the amoun t of collateral that will serve to release the current order. However, if the customer does not offer any collateral, c a may not be the appropria te amount of credit to grant. In such cases, the customer needs to be evaluated at vari- ous lower levels (in terms of credit request) to see if the perceived probabilities change at lower levels of exposure.

Initial experimental evaluation of the model was done by randomly selecting 3 customers such that one customer was perceived to be a nigh credit risk, another consti tuted a negligible level of credit risk and the third customer was perceived to be a marginal customer. The 3 customers were then evaluated by several credit managers includ- ing the 'expert ' and the credit analyst who picked the customers. The evaluators were asked to con- sider a hypothet ical si tuation where the customers had requested for a credit of $100 000 to cover an order for a part icular product . The credit managers evaluated the hierarchy presented in Figure 1, and analysis of the judgementa l data yielded three sets of relative priorities for the 3 customers. The implied credit limits confirmed the ' a priori ' cate- gorization of the 3 customers and there was little variance in the results obtained f rom the three sets of priorities. The model was refined by conduct ing a series of discussions with the 'expert ' and by evaluating a few more r andom customers.

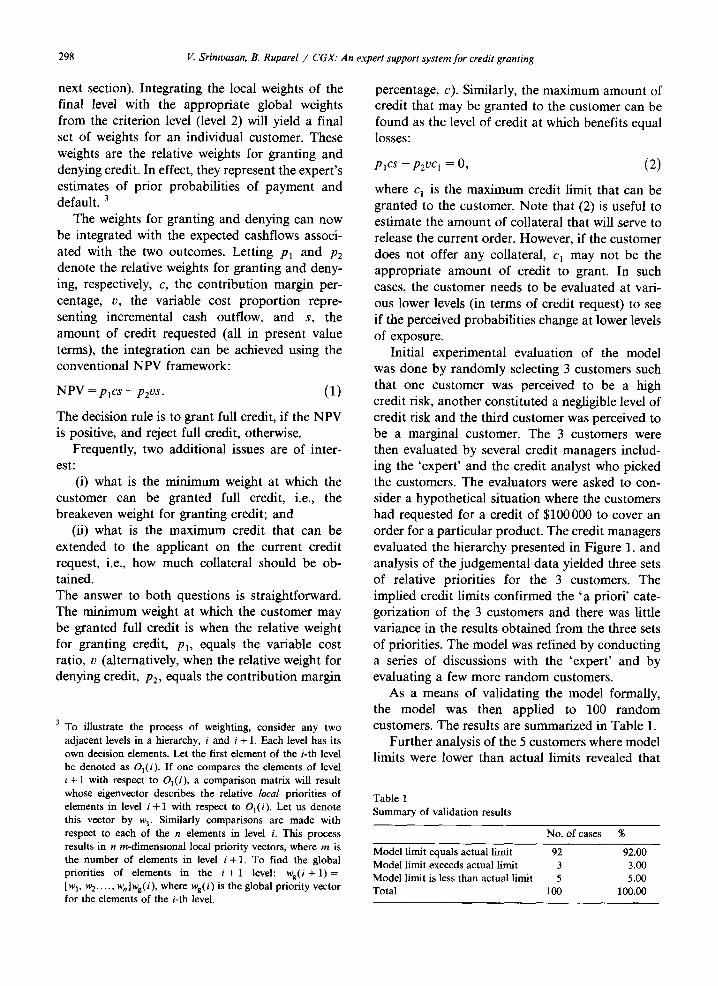

As a means of validating the model formally, the model was then applied to 100 r andom customers. The results are summarized in Table 1.

Fur ther analysis of the 5 customers where model limits were lower than actual limits revealed that

Table 1 Summary of validation results

No. of cases %

Model limit equals actual limit 92 92.00 Model limit exceeds actual limit 3 3.00 Model limit is less than actual limit 5 5.00 Total 100 100.00

V. Srinivasan, B. Ruparel / CGX: An expert support system for credit granting 299

in all the 5 cases extraneous factors not considered in the model influenced the credit decision. If these extraneous influences are removed, the re- suits from the model are consistent with actual practice. The effective proportion of correct cases is, therefore, 97.00%. In addition, we investigated the 3 cases where the model suggested limit was higher than actual limit and found that some additional refinement was needed in the criteria weights.

It should be noted that the AHP model, as it has been presented, assumes that the decision- maker will be willing to assume greater risk for increased return monotonically. If the firm does not want to assume increased risk as a monotone function of profitability, the model can be mod- ified by imposing a fixed level of maximum re- turns. Such a practice would be consistent with the widespread finding that managers' risk behav- ior often implies a target rate of return and that managers' risk preferences are truncated beyond a maximum.

3.2. Phase (i) design

In this phase, the credit evaluation process of the managers was to be studied and captured in a knowledge base. By a process of in-depth inter- views, the initial prototype knowledge base was structured into the following 3 categories:

- Financial.

- Pay habits.

- Background.

The structuring process itself yielded an initial set of rules which were input using a commercial expert system shell. This initial knowledge base was refined in the process of applying it to a set of 100 random customers. The refined knowledge base consisted of a limited set of rules that could be applied in a consultative mode. The consulta- tive mode called for the user to supply facts per- taining to a customer. Conclusions reached by the prototype were supported by a limited amount of reasoning text that was designed for every rule.

4. CGX: An expert credit support system

The prototype, albeit limit in its knowledge, reasoning and support capabilities, was perceived to be a success. A much more detailed and com-

Rules

_1 Engine l J Action i.e.

Conclusion/ Recommendations

Figure 2. Users Interface: CGXshell

prehensive design and development task was un- dertaken with the encouragement and support of several Fortune 500 firms and the Credit Research Foundation, Inc. Development plans for CGX required a complete redesign of system structure, design philosophy and user's interface. The follow- ing sections describe CGX's structural design, the contents of its knowledge base, and additional features that make it a complete expert support system for credit granting.

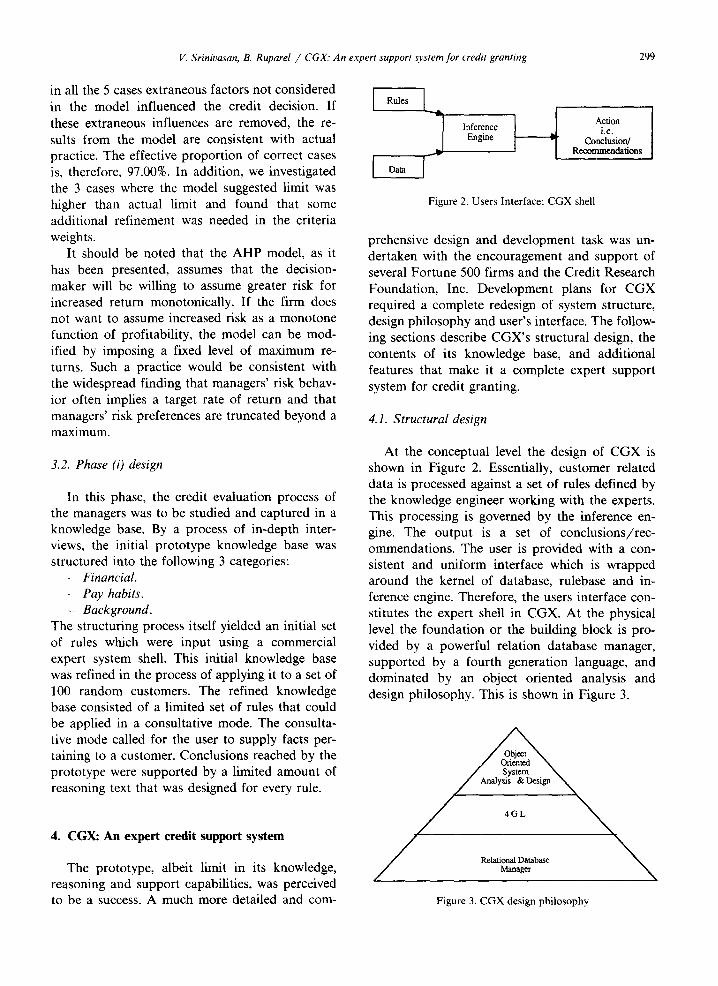

4.1. S tructural design

At the conceptual level the design of CGX is shown in Figure 2. Essentially, customer related data is processed against a set of rules defined by the knowledge engineer working with the experts. This processing is governed by the inference en- gine. The output is a set of conclusions/rec- ommendations. The user is provided with a con- sistent and uniform interface which is wrapped around the kernel of database, rulebase and in- ference engine. Therefore, the users interface con- stitutes the expert shell in CGX. At the physical level the foundation or the building block is pro- vided by a powerful relation database manager, supported by a fourth generation language, and dominated by an object oriented analysis and design philosophy. This is shown in Figure 3.

Figure 3. CGX design philosophy

300 V. Srinivasan, B. Ruparel / CGX: An expert support system for credit granting

Objected oriented analysis and design have been applied to both the CGX database and rulebase. The database design is nothing new. The database consists of tables representing various customer related entities; e.g., trade-reference information, bank information, contact information etc. Vari- ous one-to-one, one-to-many and many- to-many relationship were resolved during the process of normalization. Normalization helps to avoid re- dundancy of data and maintain consistency and uniformity at the same time.

Design of the rulebase is more interesting. The same relational data manager which stores cus- tomer specific information is also used to store the rules. Therefore, the rulebase which is a collection of rules, also resides in the database. This is a rather subtle but very important issue. This scheme of implementation presents as with a tremendous degree of flexibility. The processing of data against the rulebase is seemless and transparent to the user.

A rule is essentially a meta-object, i.e., it can be thought of as an entity. It can be created, updated, and deleted just like any entity in object oriented databases. We employ a scheme of successive and stepwise refinments to break the rule into smaller objects down to the atomic level. We then work backwards to create a scheme of relational tables to store and implement a rule. This is consistent with top down design and bot tom up implementa- tion.

The rule is quite similar to an IF . . . condi t ion

. . . T H E N .. . resul ts . . . statement in conven- tional programming language environments. It es- sentially consists of two components: a condition component and a result component. In this sys- tem, the condition component can consist of a simple condition or a number of simple conditions connected by the logical AND operator. The result component, a score, a weight or a probability, is atomic or monotonic. However, in general, it can also be a number of smaller actions connected together.

Since the action component is simpler for this system, we will deal with it first. An atomic ob- ject: i.e. the score here, can be stored in a table using the well-accepted principles of normaliza- tion. This table essentially has a rule-identifier field, a score or weight field and a note or memo field for expert comments. If the condition com- ponent consists of multiple conditions, it can be

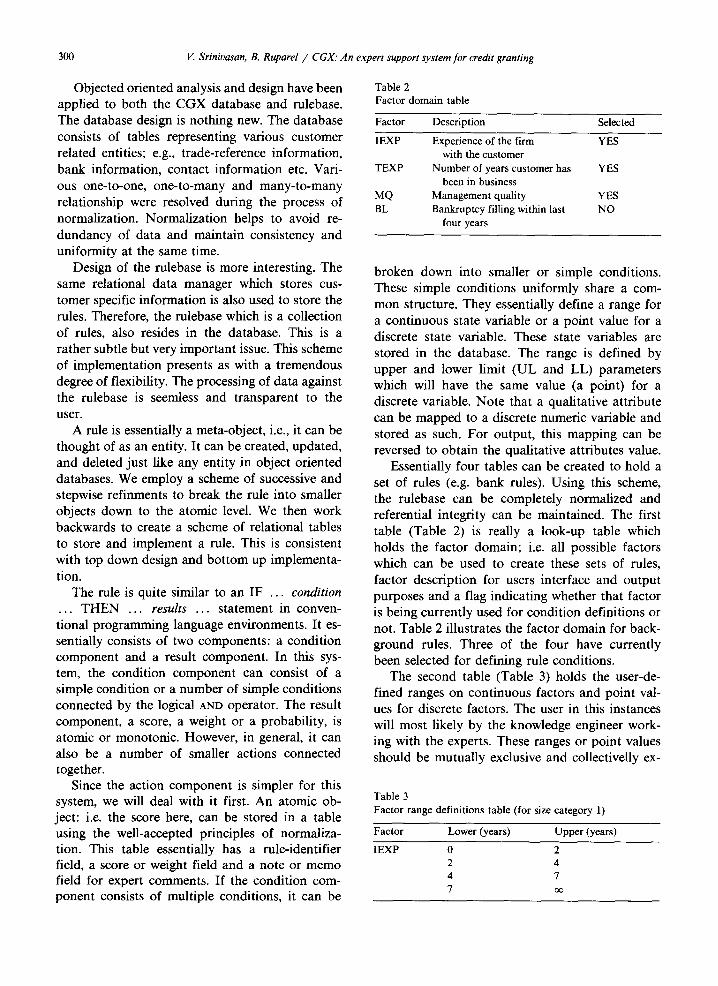

Table 2 Factor domain table

Factor Description Selected

IEXP Experience of the firm YES with the customer

TEXP Number of years customer has YES been in business

MQ Management quality YES BL Bankruptcy filling within last NO

four years

broken down into smaller or simple conditions. These simple conditions uniformly share a com- mon structure. They essentially define a range for a continuous state variable or a point value for a discrete state variable. These state variables are stored in the database. The range is defined by upper and lower limit (UL and LL) parameters which will have the same value (a point) for a discrete variable. Note that a qualitative attribute can be mapped to a discrete numeric variable and stored as such. For output, this mapping can be reversed to obtain the qualitative attributes value.

Essentially four tables can be created to hold a set of rules (e.g. bank rules). Using this scheme, the rulebase can be completely normalized and referential integrity can be maintained. The first table (Table 2) is really a look-up table which holds the factor domain; i.e. all possible factors which can be used to create these sets of rules, factor description for users interface and output purposes and a flag indicating whether that factor is being currently used for condition definitions or not. Table 2 illustrates the factor domain for back- ground rules. Three of the four have currently been selected for defining rule conditions.

The second table (Table 3) holds the user-de- fined ranges on continuous factors and point val- ues for discrete factors. The user in this instances will most likely by the knowledge engineer work- ing with the experts. These ranges or point values should be mutually exclusive and collectivelly ex-

Table 3 Factor range definitions table (for size category 1)

Factor Lower (years) Upper (years)

IEXP 0 2 2 4 4 7 7 oo

V. Srinivasan, B. Ruparel / CGX: An expert support system for credit granting 301

Table 4 Rule condition table

Factor Lower Upper Rule ID

IEXP 2 4 10 TEXP 5 7 10 ML 1 1 10

among the 4 tables can be graphically shown as follows:

Rule

Condition Result (atomic and monotonic)

haustive. Any number of ranges or values can be defined. This depends on how thorough the de- briefing is. For example, Table 3 presents ranges for the IEXP factor in Table 2. Note that ranges may be different for customers of different sizes. Size here is proxied by the amount of credit sought by the customer.

The second table defines the domain for the third table (Table 4). The third table hold the total condition component of the rule in the form of one or more row. If the condition components consists of a simple condition defined as a range or a point value on a factor then that rule can be represented by only one row in Table 4. Similarly, the number of rows required to represent a rule is the same as the number of simple conditions de- fined on various factors. To illustrate, Table 4 presents a rule with 3 simple conditions. Further, the third condition relates to the management quality factor which is a discrete variable. As stated before, in the case of discrete factors, the lower and upper range definitions are the same effectively yielding a point value.

The fourth table (Table 5) holds the result component. As pointed out earlier, this holds the rule identifier, score and expert text. Every rule has a unique expert text which comprises the reasoning component of the system. The fourth table completes the normalization process to the 3rd normal form. The hierarchical relationship

Table 5 Result table

Rule ID Score Expert text

10 10 Customer has been in business for more than five years

We have had a business relationship with the customer for between two and four years

Customer 's management quality is perceived to be excellent

Overall, customer 's background is considered excellent

Hence, there is a one-to-one relationship between the condition component and the rule component. Further, the relationship between the condition component and simple conditions forms the next level of the hierarchy:

Condition

S i m p l e ~ ~ S i m ~ Simple condition 1 condition 2 , • • condition x

Finally, the simple conditions can be repre- sented in terms of a factor, a lower limit and an upper limit as follows:

Simple condition

Factor pper limit ~ " Lower limit (atomic and (atomic and monotonic) (atomic and monotonic) monotonic)

Summing up, a rule consists of a condition and a result. The condition is an aggregate of simple conditions. A simple condition is either a range on a factor defined by upper and lower limits or a point value of that factor. This completes the stepwise splitting (or refinement) process to the point where all the attributes and parameters are in atomic state. This is the basis of object oriented design. In conclusion, object oriented analyses and design coupled with 4GL and a relational data- base manager provides an attractive environment for developing data intensive expert systems.

As discussed earlier, data from the database supplied to the enference engine to be processed against the rulebase. The rules which succeed are fired. Triggers can be attached to the rules so that they initiate the desired action upon being fired. The resulting conclusions are aggregated and pre- sented. This type of expert system can be com- pared to batch-processing systems in classic MIS environment. On the opposite end are diagnostic experts systems like MYCIN which can be com- pared to interactive processing. While one is not

302 l/:. Srinivasan, B. Ruparel / CGX: An expert support system for credit granting

necessarily better than the other, for a data inten- sive application such as this, the approach dis- cussed here is better suited as is now being in- creasingly recognized (Holsapple and Whinston, 1987).

4.2. Knowledge base contents

As stated earlier, the knowledge base for CGX consists of two components: a customer database and a rulebase. The customer database contains all available data pertaining to the PC's customers. The database design is a 'relational' one which allows for efficient storage and retrieval of sizable amounts of data. The contents of the database are presented in Figure 4. The various blocks of data (rectangular boxes in Figure 4) will be referred to as 'files'. The database is logically divided into

many files according to the attribute group to which a specific data item might belong:

Pay habits. Background information:

Basic customer information. Management data. Trade reference data. Bank reference data. Collateral information. D & B information.

Financial information: Income statements. Balance sheets. Financial ratios.

Each of the files in the database has atleast one unique index key and may have multiple index keys to efficiently perform various search and retrieval tasks. The unique index keys may be

Income K: Cusino Year U/A I/F

BSheet K: C"usino Year U/A I/F

R~os K: Custno Yc~ U/A UF

Cusmo

Basic K: Custno

Industry Staadard Ks: Class

SIC Area

l~fno

L ~-] K: Custno

K Cusmo

l.~gead: U/A = Unauditexl/Audited I/F--Interim/Final K = Index Fields Casino -- Customer Identitical

Figure 41 Database structure

V. Srinioasan, B. Ruparel / CGX: An expert support system for credit granting 303

Financial Trend Rules

Ovea-all Financial Rules

I Pay Rules

Management Rules

Business Potential Rules

Location Rules

I Profitability Rules

Debt Management Rules

Limit Rules [

AHP Model

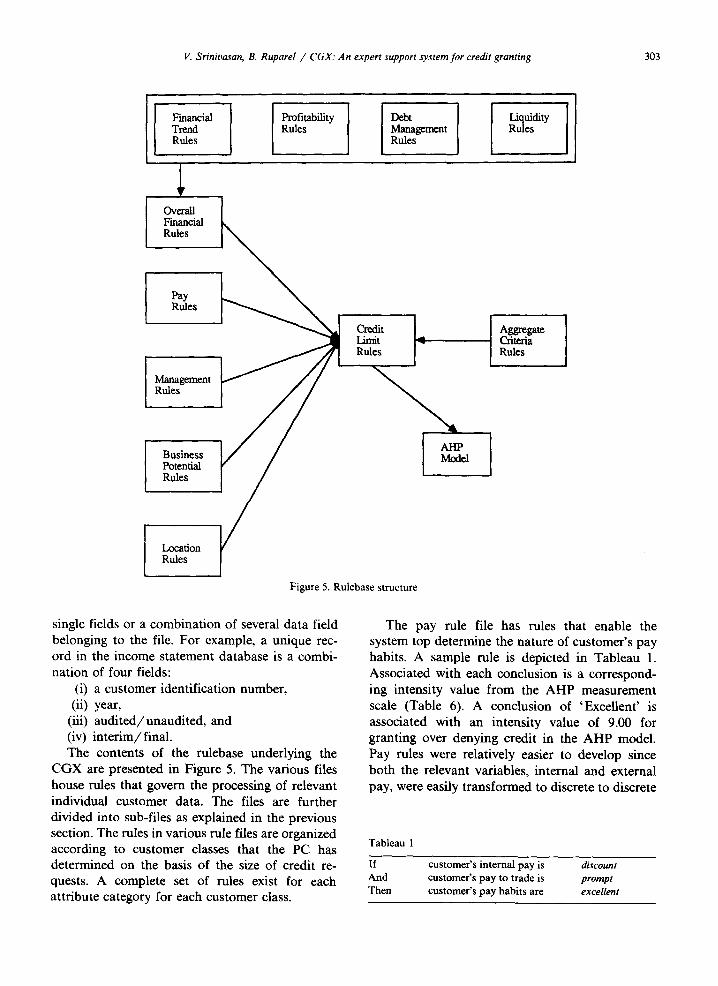

Figure 5. Rulebase structure

Liquidity [ Rules

I Aggregate ] Criteria Rules

single fields or a combination of several data field belonging to the file. For example, a unique rec- ord in the income statement database is a combi- nation of four fields:

(i) a customer identification number, (ii) year,

(iii) audited/unaudited, and (iv) interim/final. The contents of the rulebase underlying the

CGX are presented in Figure 5. The various files house rules that govern the processing of relevant individual customer data. The files are further divided into sub-files as explained in the previous section. The rules in various rule files are organized according to customer classes that the PC has determined on the basis of the size of credit re- quests. A complete set of rules exist for each attribute category for each customer class.

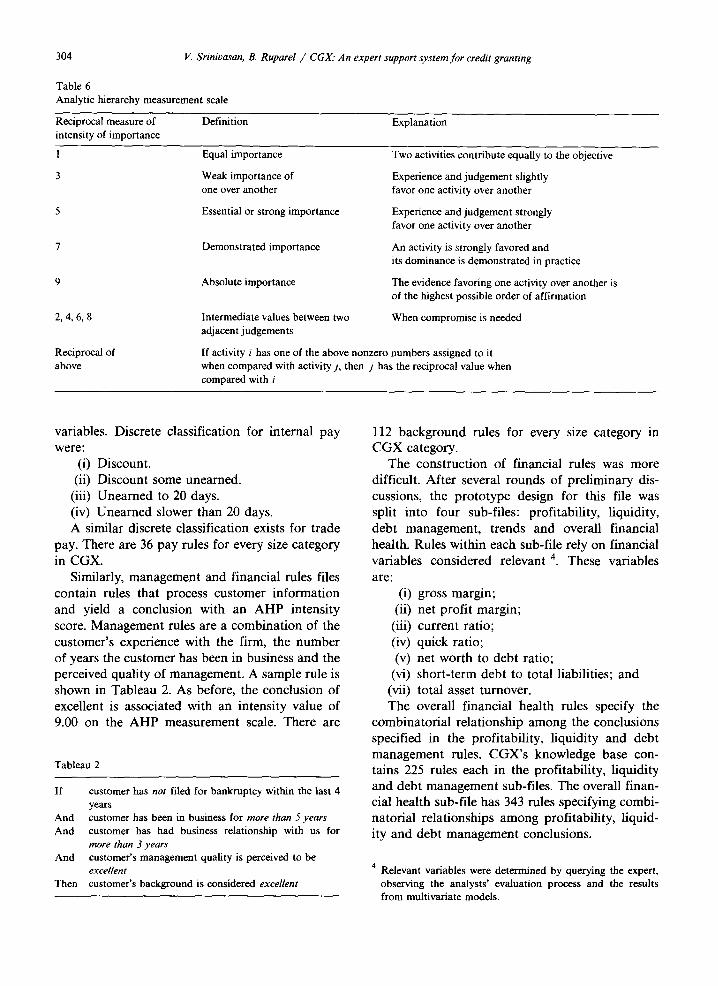

The pay rule file has rules that enable the system top determine the nature of customer's pay habits. A sample rule is depicted in Tableau 1. Associated with each conclusion is a correspond- ing intensity value from the AHP measurement scale (Table 6). A conclusion of 'Excellent' is associated with an intensity value of 9.00 for granting over denying credit in the AHP model. Pay rules were relatively easier to develop since both the relevant variables, internal and external pay, were easily transformed to discrete to discrete

Tableau 1

If And Then

customer's internal pay is discount customer's pay to trade is prompt customer's pay habits are excellent

304 V. Srinivasan, B. Ruparel / CGX." An expert support system for credit granting

Table 6 Analytic hierarchy measurement scale

Reciprocal measure of Definition Explanation intensity of importance

9

2,4,6,8

Reciprocal of above

Equal importance

Weak importance of one over another

Essential or strong importance

Demonstrated importance

Absolute importance

Intermediate values between two adjacent judgements

Two activities contribute equally to the objective

Experience and judgement slightly favor one activity over another

Experience and judgement strongly favor one activity over another

An activity is strongly favored and its dominance is demonstrated in practice

The evidence favoring one activity over another is of the highest possible order of affirmation

When compromise is needed

If activity i has one of the above nonzero numbers assigned to it when compared with activity j, then j has the reciprocal value when compared with i

variables. Discrete classification for internal pay were:

(i) Discount. (ii) Discount some unearned.

(iii) Unearned to 20 days. (iv) Unearned slower than 20 days. A similar discrete classification exists for trade

pay. There are 36 pay rules for every size category in CGX.

Similarly, management and financial rules files contain rules that process customer information and yield a conclusion with an AHP intensity score. Management rules are a combination of the customer's experience with the firm, the number of years the customer has been in business and the perceived quality of management. A sample rule is shown in Tableau 2. As before, the conclusion of excellent is associated with an intensity value of 9.00 on the AHP measurement scale. There are

Tableau 2

If customer has not filed for bankruptcy within the last 4 years

And customer has been in business for more than 5 years And customer has had business relationship with us for

more than 3 years And customer's management quality is perceived to be

excellent Then customer's background is considered excellent

112 background rules for every size category in CGX category.

The construction of financial rules was more difficult. After several rounds of preliminary dis- cussions, the prototype design for this file was split into four sub-files: profitability, liquidity, debt management, trends and overall financial health. Rules within each sub-file rely on financial variables considered relevant 4. These variables are:

(i) gross margin; (ii) net profit margin;

(iii) current ratio; (iv) quick ratio; (v) net worth to debt ratio;

(vi) short-term debt to total liabilities; and (vii) total asset turnover. The overall financial health rules specify the

combinatorial relationship among the conclusions specified in the profitability, liquidity and debt management rules. CGX's knowledge base con- tains 225 rules each in the profitability, liquidity and debt management sub-files. The overall finan- cial health sub-file has 343 rules specifying combi- natorial relationships among profitability, liquid- ity and debt management conclusions.

4 Relevant variables were determined by querying the expert, observing the analysts' evaluation process and the results from multivariate models.

V. Srinivasan, B. Ruparel / CGX: An expert support system for credit granting 305

Rule development for assessing customers' management and financial strength was com- plicated by the fact that many of the variables were continuous. To keep the number of rules finite and feasible, these variables needed to dis- cretized. Discretization was accomplished as fol-

lows: (a) Select a sample of customers within each

class. (b) Obtain expert conclusions for each of the

attribute categories (files and sub-files). (c) Analyze the expert's conclusions and attri-

bute values using a classification procedure. A number of classification procedures could be used to analyze the expert conclusions. For con- venience, we used an information theoretic classi- fication procedure (Quinlan, 1983) that is quite popular in the AI literature (commonly referred to as the Quinlan procedure). Rules that were ob-

Tableau 3

Profitability If sales trend is And customer's net profit margin is And customer's net profit margin

trend is And customer's gross margin is And customer's gross margin trend is Then customer's profitability is

Liquidity If sales trend is And customer's current ratio is

current ratio trend is quick ratio is quick ratio trend is liquidity is

And customer's And customer's And customer's Then customer's

Debt management If sales trend is And customer's debt to net worth

ratio is And customer's debt to net worth

ratio trend is And customer's short-term debt

to total debt is And customer's short-term debt

to total debt trend is And customer's interest coverage is Then customer's debt exposure is

Overall financial health If customer's profitability is And customer's liquidity is And customer's debt exposure is Then customer's financial health is

improving greater than 5 % improving

greater than 12 % improving excellent

improving greater than 1.50 increasing greater than 0.80 increasing excellent

improving less than 0.30

decreasing

less than O. 40

decreasing

greater than 4.0 excellent

excellent excellent excellent excellent

tained by applying the Quinlan procedure were modified by the expert as a result of applying them to additional customers. A sample set of financial rules is depicted in Tableau 3. The dis- cretized value for each factor are the ranges on the factors. Each factor also has a "not available" value that allows the system to proceed even when data is incomplete. Further, note that the length of the rules within a sub-file is not standard. Some rules may require the evaluation of more variables to reach a conclusion than others. The above set of rules also serve to illustrate the forward chain- ing aspect of the rules. The profitability, liquidity and debt management rules are chained forward to obtain the overall financial health conclusion.

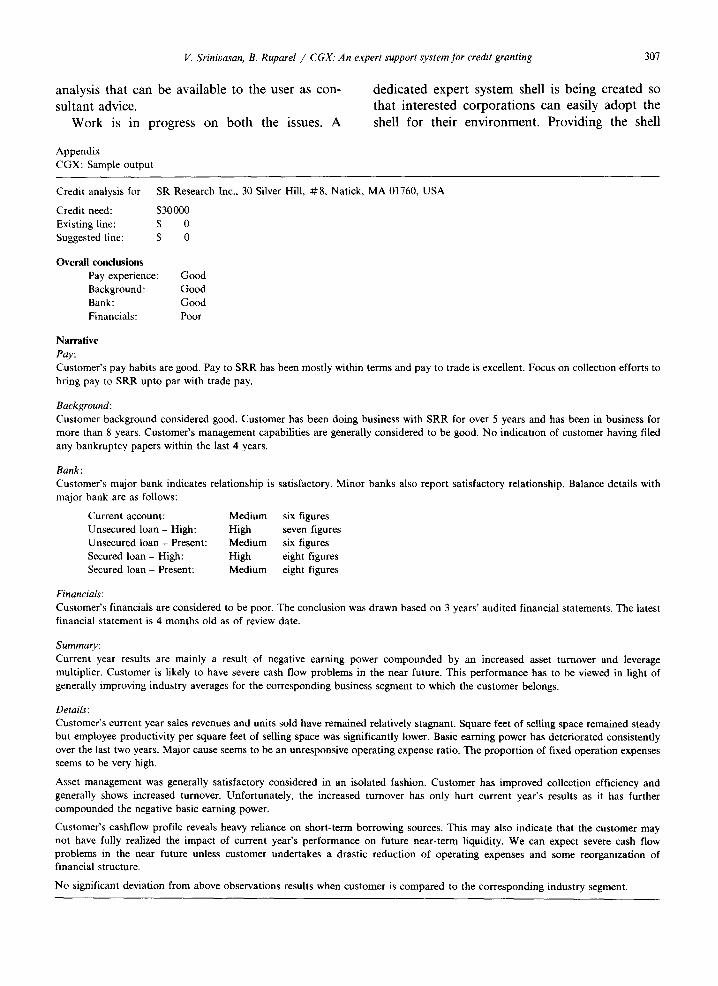

4.3. Sample results

A typical sample of results from using the prototype are presented in the Appendix. The suggested line is the system processed credit limit for the customer. It is found by applying the AHP model to the intensity values provided by the various rules and then integrated as illustrated earlier. Each conclusion is followed by a brief explanation that comprises the reasoning ability of the prototype.

4.4. Supporting other segments of the credit decision process

CGX, as described in the previous sections, focuses on only one major aspect of the credit decision process. From an implementational per- spective, a better approach is to increase the func- tionality of the system to also intelligently support other aspects of the credit decision process. Accordingly, a variety of options and features were added to CGX to significantly increase its functionality. Among the major support features are:

1. Tickler sub-system: The credit decision proc- ess has a number of related tasks that need peri- odic monitoring, e.g., customer credit evaluation, collateral expiry, bank reference updates, trade- references updates, financial statement updates, Dun & Bradstreet report updates, etc. The data- base structures were expanded to store user-de- fined tickler frequencies for a variety of action variables. The tickler sub-system can be invoked by the user with a listing of tickler actions that are

306 V. Srinivasan, B. Ruparel / CGX." An expert support system for credit granting

due. The user has the option to execute some of the actions directly from the tickler sub-system. The user can also suspend the tickler operation to perform actions that cannot be performed from within the tickler sub-system and resume tickler processing where suspended.

2. Industry patterns: Comparison of customers implies the existence of a standard. Frequently, experts would desire to examine aggregate in- dustry patterns before deciding on standards. A common practice is to look up published industry average data by the Standard Industrial Classifica- tion (SIC) code. In CGX, the users have ad- ditional options to examine the aggregate behavior of the customers in the CGX database alone. Further, customers in CGX can be identified by several industry affiliation variables effectively al- lowing users to examine micro-segments of the industry as portrayed by the firm's customers. For example, in one implementation in the computer industry, there were 3 industry related variables that allowed the users to examine customer data according to business focus, class of trade, market segement and any combination thereof.

3. Sensitivity analyses: Often, the information on customers is received late and, thus, the credit manager has to form expectations about future behavior based on outdated data. Under such circumstances, sensitivity analyses obviously be- come crucial. However, instead of the user having to modify customer data in the database, a num- ber of different "What If" options were added to facilitate easy sensitivity analysis. This set of op- tions also includes the ability to forecast customer financial statements so that the user can evaluate the customer based on forecasted financial state- ments.

4. Special management reports: Aside from the operational aspect of the credit granting process, there is also the need to support a number of tactical dimensions of the process including an aggregate evaluation of the quality of the firm's receivables, internal control reports, etc. Receiva- bles quality can be proxied by computing dollar- weighted AHP weights and monitoring such weights over time. A number of other reporting options were added to generate reports typically required by higher level managers.

5. Form letters: The most common mode for updating customer data is to mail standardized letters to various constituencies requesting for up-

dates. Since these letters are mostly standard, their processing can be automated by storing standard letters and using user-defined tickler conditions to mail them. Accordingly, 2 sets of capabilities were added to CGX:

(i) the ability to design and store standard letters requesting information from Dun & Bradstreet, bank references, trade references, and customer; and

(ii) the ability to automatically generate these letters for mailing. The above enhancement to CGX transform it from being a narrowly defined expert system to a more complete expert support system for all aspects of the credit granting process.

5. Summary and extensions

The tremendous interest among corporations to exploit advances in artificial intelligence technol- ogy in the form of expert systems is not unwar- ranted. Expert systems have the potential to sig- nificantly increase productivity and as a result help in controll ing/reducing operating costs. In the previous sections, we have attempted to de- scribe CGX, and expert support system for credit granting in nonfinancial firms. CGX has attracted the attention of several large Fortune 500 corpora- tions. It is currently undergoing extensive valida- tion in participating firms and is being extended to other firms on an experimental basis.

There are at least 2 major dimensions in which CGX can be and is being extended. First, an issue that is of practical interest is the ease with which CGX can be adopted by corporations at large. We find from studying the credit granting process in several other corporations that there is a signifi- cant degree of commonality and stability in the process across corporations. In particular, while divergence in parameter values is widespread, only in a few cases there is divergence in the factors themselves. Generalization, while feasible at a cer- tain level of aggregation, requires several signifi- cant structural changes in the data and rule bases in order to maintain the integrity of the data and rules as well as to allow for the divergence. The second issue relates to the adequacy of expert knowledge particularly as it relates to the analysis of financial statements. It behooves that CGX contain external expert knowledge on financial

V. Srinivasan, B. Ruparel / CGX: An expert support system for credit granting 307

analysis that can be available to the user as con- sultant advice.

Work is in progress on both the issues. A

dedicated expert system shell is being created so that interested corporations can easily adopt the shell for their environment. Providing the shell

Appendix CGX: Sample output

Credit analysis for SR Research Inc., 30 Silver Hill, ~ 8 , Natick, MA 01760, USA

Credit need: $30000 Existing line: $ 0 Suggested line: $ 0

Overall conclusions Pay experience: Good Background: Good Bank: Good Financials: Poor

Narrative Pay: Customer 's pay habits are good. Pay to SRR has been mostly within terms and pay to trade is excellent. Focus on collection efforts to bring pay to SRR upto par with trade pay.

Background: Customer background considered good. Customer has been doing business with SRR for over 5 years and has been in business for more than 8 years. Customer 's management capabilities are generally considered to be good. No indication of customer having filed any bankruptcy papers within the last 4 years.

Bank: Customer 's major bank indicates relationship is satisfactory. Minor banks also report satisfactory relationship. Balance details with major bank are as follows:

Current account: Medium six figures Unsecured loan - High: High seven figures Unsecured loan - Present: Medium six figures Secured loan - High: High eight figures Secured loan - Present: Medium eight figures

Financials : Customer 's financials are considered to be poor. The conclusion was drawn based on 3 years' audited financial statements. The latest financial statement is 4 months old as of review date.

Summary: Current year results are mainly a result of negative earning power compounded by an increased asset turnover and leverage multiplier. Customer is likely to have severe cash flow problems in the near future. This performance has to be viewed in light of generally improving industry averages for the corresponding business segment to which the customer belongs.

Details: Customer 's current year sales revenues and units sold have remained relatively stagnant. Square feet of selling space remained steady but employee productivity per square feet of selling space was significantly lower. Basic earning power has deteriorated consistently over the last two years. Major cause seems to be an unresponsive operating expense ratio. The proportion of fixed operation expenses seems to be very high.

Asset management was generally satisfactory considered in an isolated fashion, Customer has improved collection efficiency and generally shows increased turnover. Unfortunately, the increased turnover has only hurt current year's results as it has further compounded the negative basic earning power.

Customer 's cashflow profile reveals heavy reliance on short-term borrowing sources. This may also indicate that the customer may not have fully realized the impact of current year's performance on future near-term liquidity. We can expect severe cash flow problems in the near future unless customer undertakes a drastic reduction of operating expenses and some reorganization of financial structure.

No significant deviation from above observations results when customer is compared to the corresponding industry segment.

308 V. Srinivasan, B. Ruparel / CGX: An expert support system for credit granting

with expertise for analyzing financial statements first requires that the process of financial analysis and interpretation be structured. A comprehensive structured approach has been developed for analyzing financial statements and is now in the process of being validated before equipping the shell with such knowledge.

Acknowledgement

We thank the corporations participating in this research effort for their cooperation and support. Partial support for Venkat Srinivasan through the Joseph G. Riesman Research Professorship and travel funding from the Credit Research Founda- tion, Inc. are gratefully acknowledged.

Nathalie Durand provided excellent research assistance.

All errors are our own.

References

Athena Group (1986), Portfolio Management Advisor Applica- tion Note, New York.

Bierman, H., and Hauseman, W. (1970), "The credit granting decision", Management Science, 519-532.

Buchanan, B.G., and Shortcliffe, E.H. (1984), Rule-Based Ex- pert Systems: The MYCIN Experiments of the Stanford Heuristic Programming Project, Addison-Wesley, Reading, MA.

Buckley, J.W. (1971), "A systematic credit screening model", Proceedings of the International Symposium on Model and Computer-Based Corporate Planning, Cologne.

Cyert, R.M., and Thompson, G.L. (1968), "Selecting a port- folio of credit risks by Markov chains", Journal of Business, 39-46.

Dirickx, Y.M.I., and Wakeman, L. (1976), "An extension of the Bierman-Hausman model for credit granting", Man- agement Science, 1229-1237.

Eisenbeis, R.A. (1980), "Selection and disclosure of reasons for adverse action in credit granting systems", Federal Reserve Bulletin, 727-736.

Fichtner, J. (1986), "On deriving priority vectors from matrices of pairwise comparisons", Socio-Economic Planning Scien- ces, 341-346.

Holsapple, C.W., Tam, K.Y., and Whinston, A.B. (1988), "Adapting expert system technology to financial manage- ment", Working paper, Krannert School of Management, Purdue University.

Holsapple, C.W., and Whinston, A.B. (1987), Business Expert Systems, Irwin, Homewood, IL.

Mehta, D. (1970), "Optimal credit policy selection: A dynamic approach", Journal of Financial and Quantitative Analysis, 421-444.

Myers, J.H., and Forgy, E.W. (1963), "The development of numerical credit evaluation systems", Journal of American Statistical Association, 799-806.

Newquist, H. (1987), "American Express and AI: Don't leave home without them", AI Expert 2.

Nisse, J. (1987), "Banking tomorrow-Big spenders", The Banker, 64-67.

Quinlan, J.R. (1983), "Learning efficient classification proce- dures and their application to chess end games", in: R.S. Michalski, J.F. Carbonell and T.M. Mitchell (eds.), Ma- chine Learning, Tioga Publishing, Palo Alta, CA.

Saaty, T.L. (1980), The Analytic Hierarchy Process, McGraw- Hill, New York.

Saaty, T.L., and Vargas, L.G. (1982), The Logic of Priorities: Applications in Business, Energy, Health and Transportation, Kluwer-Nijhoff, Boston.

Srinivasan, V., and Kim, Y.H. (1986a), "Financial applications of the analytic hierarchy process", TIMS XXVII Interna- tional Meetings, Gold Coast.

Srinivasan, V., and Kim, Y.H. (1986b), "Designing expert systems for credit management", Financial Management Association Meetings, New York.

Srinivasan, V., and Kim, Y.H. (1987), "Credit granting: A comparative analysis of classification procedures", Journal of Finance, 661-680.

Srinivasan, V., and Kim, Y.H. (1987b), "The Bierman-Haus- man credit granting model: A note", Management Science, 1361-1362.

Srinivasan, V., and Ruparel, B. (1988), "CGX: A dedicated shell for designing expert credit decision support systems", EURO IX TIMS XXVII, Paris.

Wind, Y., and Saaty, T.L (1980), "Marketing applications of the analytic hierarchy process", Management Science, 641- 658.

Zahedi, F. (1985), "The AHP: A survey of the method and its applications", Interfaces, 96-108.