cfpb readiness series: understanding udaap€¦ · understanding udaap . ... •inherited...

TRANSCRIPT

CFPB Readiness Series:

Understanding UDAAP

Legal Disclaimer

This information is not intended to be legal advice and may not be used as legal advice. Legal advice must be tailored to the specific circumstances of each case. Every effort has been made to assure that this information is up-to-date as of the date of publication. It is not intended to be a full and exhaustive explanation of the law in any area, nor should it be used to replace the advice of your own legal counsel.

Who is KirkpatrickPrice?

KirkpatrickPrice is a licensed CPA firm, providing assurance services to over 200 clients in more than 40 states, Canada, Asia and Europe. The firm has over 10 years of experience in information assurance by performing assessments, audits, and tests that strengthen information security, and compliance controls.

Welcome

Tomio Narita is a partner with the California law firm, Simmonds & Narita. His practice focuses on defending creditors, debt buyers, collection agencies, and collection law firms in consumer litigation, including individual actions and class actions arising under the Fair Debt Collection Practices Act, the Fair Credit Reporting Act and the Telephone Consumer Protection Act.

Topics to Be Covered

• Overview of CFPB Authority

• Definition of “UDAAP”

• CFPB Guidance/Expectations

• CFPB/FTC Enforcement Trends

• Hot Buttons

Scope of CFPB Authority

• Inherited regulatory powers, including FDCPA • Supervision and Examination Powers • More than just Larger Participants • Rulemaking authority, including FDCPA • Enforcement powers • FTC still active; sharing information • Coordinating with state attorney generals

UDAAP Defined

• Dodd-Frank Act prohibits “unfair, deceptive or abusive” acts or practices by covered persons when collecting consumer debts

• The contours of “unfair” and “deceptive” practices under the Dodd-Frank Act will be “informed by the standards for the same terms under Section 5” of the FTC Act

• “Abusive” is a new concept

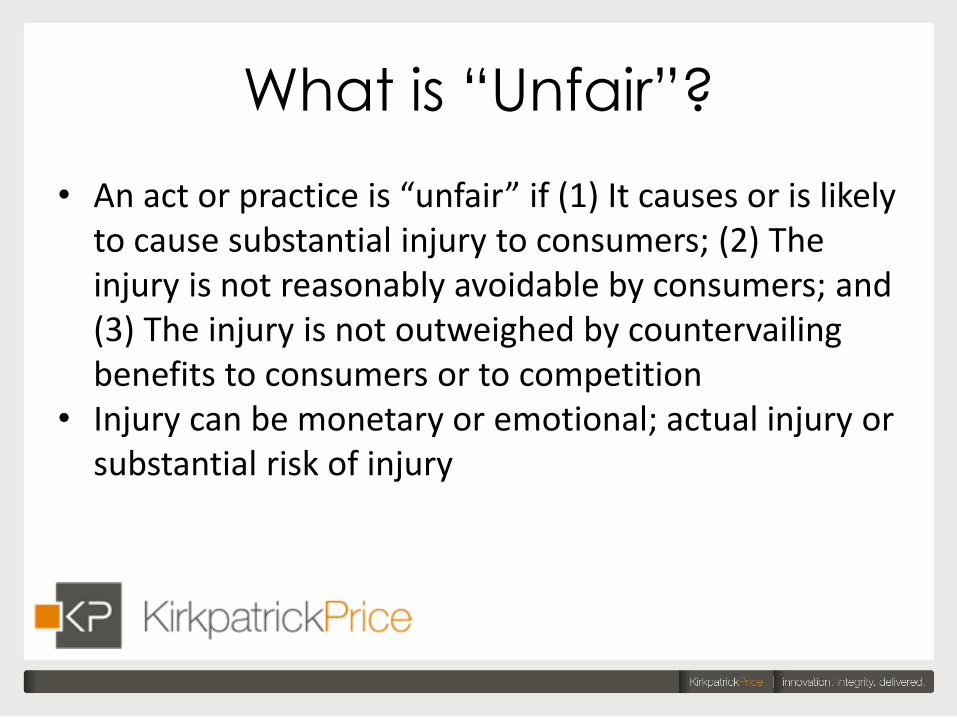

What is “Unfair”?

• An act or practice is “unfair” if (1) It causes or is likely to cause substantial injury to consumers; (2) The injury is not reasonably avoidable by consumers; and (3) The injury is not outweighed by countervailing benefits to consumers or to competition

• Injury can be monetary or emotional; actual injury or substantial risk of injury

What is “Deceptive”?

• An act or practice is “deceptive” if (1) The act or practice misleads or is likely to mislead the consumer; (2) The consumer’s interpretation is reasonable under the circumstances; and (3) The misleading act or practice is material

• Omissions and implied representations covered; full context is considered

• Material if would impact the consumer’s choices regarding the product or service

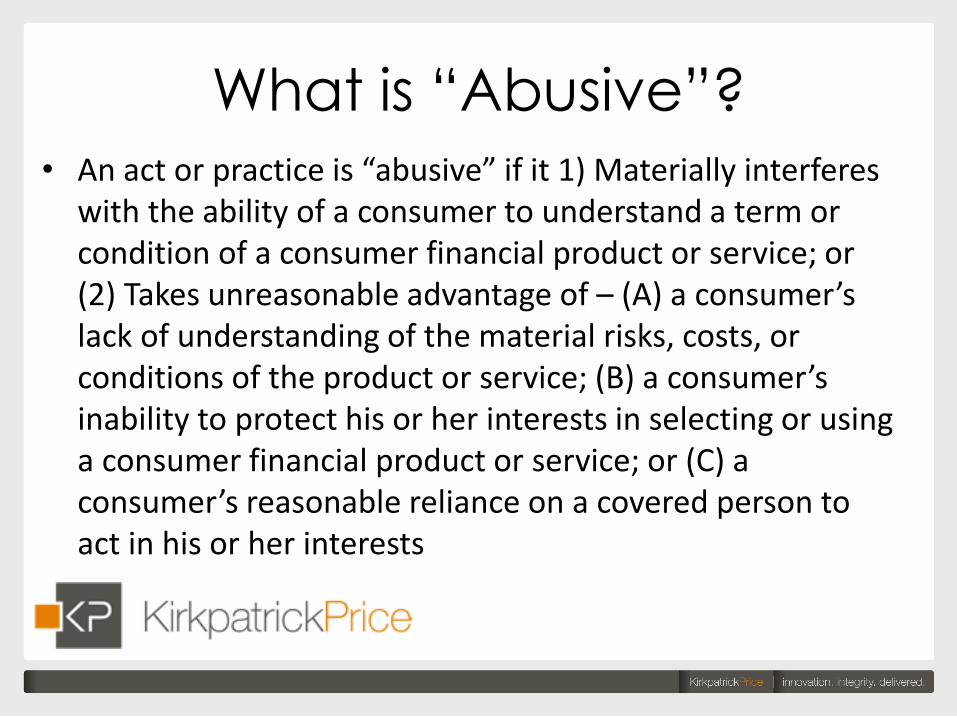

What is “Abusive”? • An act or practice is “abusive” if it 1) Materially interferes

with the ability of a consumer to understand a term or condition of a consumer financial product or service; or (2) Takes unreasonable advantage of – (A) a consumer’s lack of understanding of the material risks, costs, or conditions of the product or service; (B) a consumer’s inability to protect his or her interests in selecting or using a consumer financial product or service; or (C) a consumer’s reasonable reliance on a covered person to act in his or her interests

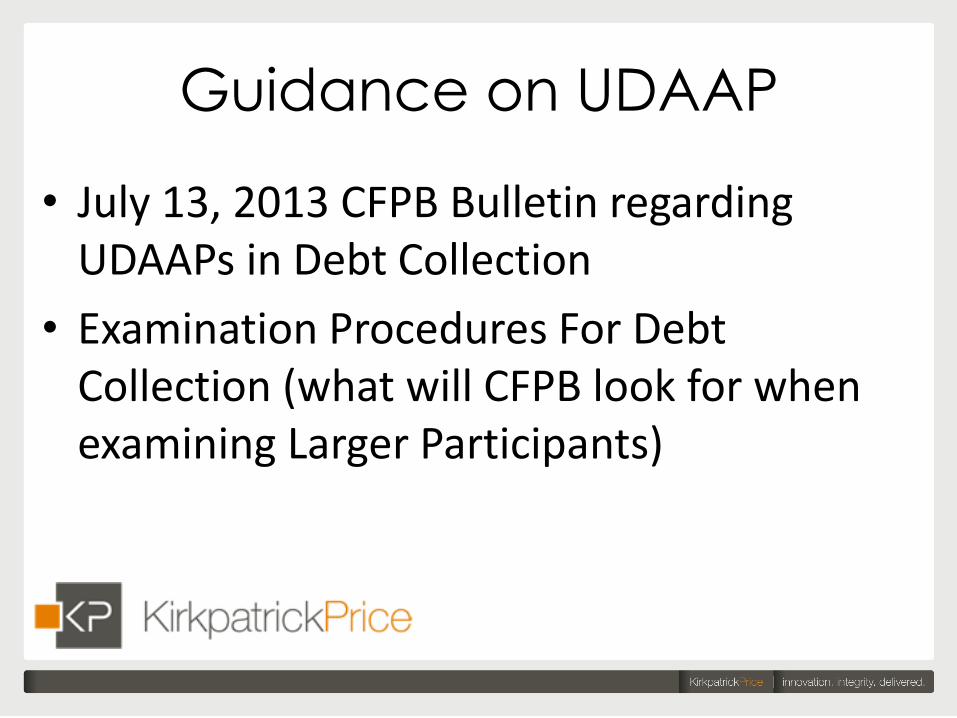

Guidance on UDAAP

• July 13, 2013 CFPB Bulletin regarding UDAAPs in Debt Collection

• Examination Procedures For Debt Collection (what will CFPB look for when examining Larger Participants)

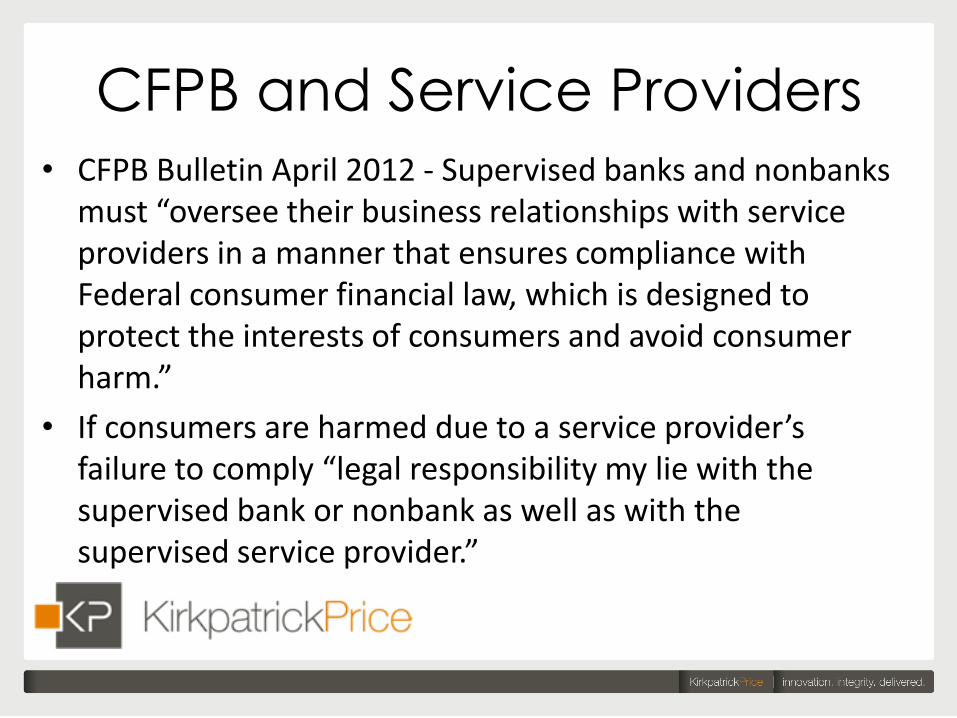

CFPB and Service Providers • CFPB Bulletin April 2012 - Supervised banks and nonbanks

must “oversee their business relationships with service providers in a manner that ensures compliance with Federal consumer financial law, which is designed to protect the interests of consumers and avoid consumer harm.”

• If consumers are harmed due to a service provider’s failure to comply “legal responsibility my lie with the supervised bank or nonbank as well as with the supervised service provider.”

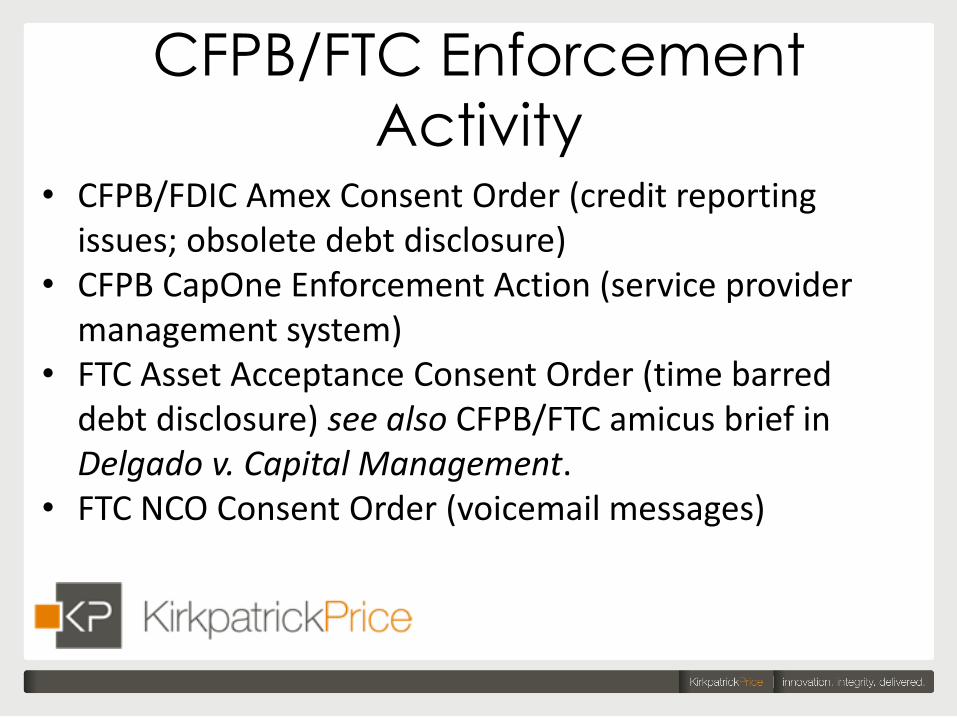

CFPB/FTC Enforcement

Activity • CFPB/FDIC Amex Consent Order (credit reporting

issues; obsolete debt disclosure) • CFPB CapOne Enforcement Action (service provider

management system) • FTC Asset Acceptance Consent Order (time barred

debt disclosure) see also CFPB/FTC amicus brief in Delgado v. Capital Management.

• FTC NCO Consent Order (voicemail messages)

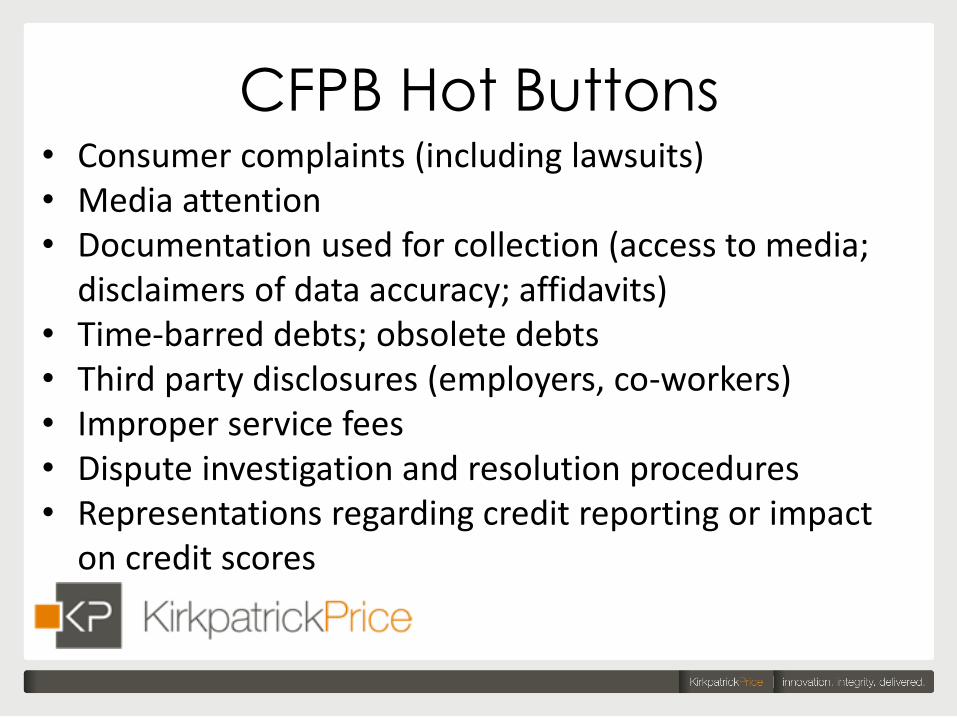

CFPB Hot Buttons • Consumer complaints (including lawsuits) • Media attention • Documentation used for collection (access to media;

disclaimers of data accuracy; affidavits) • Time-barred debts; obsolete debts • Third party disclosures (employers, co-workers) • Improper service fees • Dispute investigation and resolution procedures • Representations regarding credit reporting or impact

on credit scores

Welcome

Jessie Skibbe is a former Chief Compliance Officer with over 10 years of ARM industry experience. A recent addition to the KirkpatrickPrice team, she is focused on assisting clients in meeting regulatory compliance & information security objectives.

– Certified Credit & Collections Compliance Officer (CCCO)

– Certified Information Systems Security Professional (CISSP)

– Certified Information Security Manager (CISM)

Operational Objectives

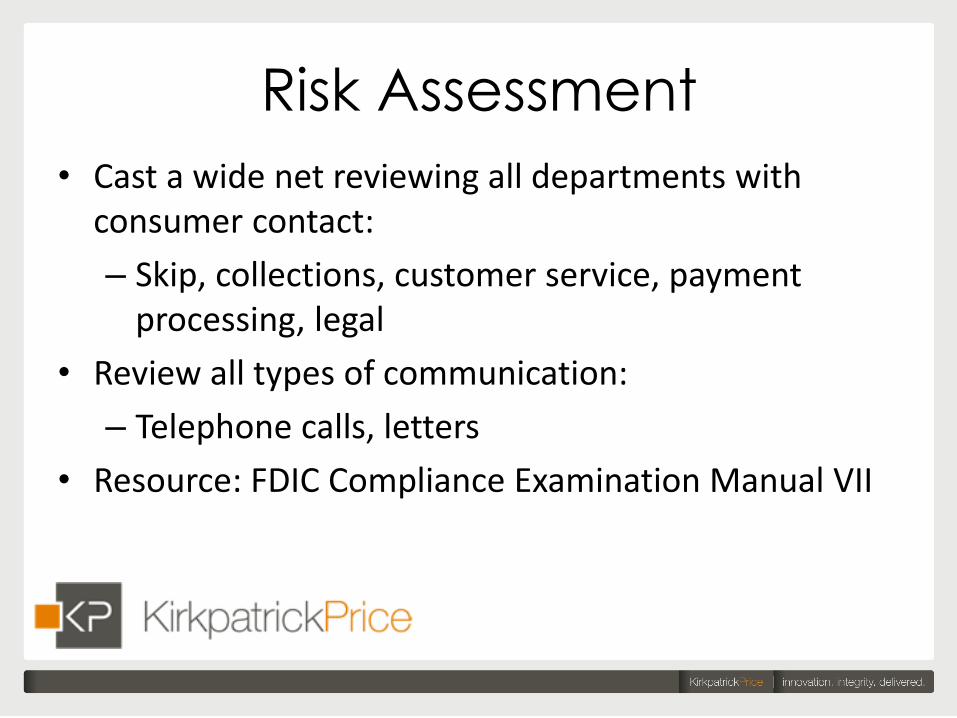

Risk Assessment

• Cast a wide net reviewing all departments with consumer contact:

– Skip, collections, customer service, payment processing, legal

• Review all types of communication:

– Telephone calls, letters

• Resource: FDIC Compliance Examination Manual VII

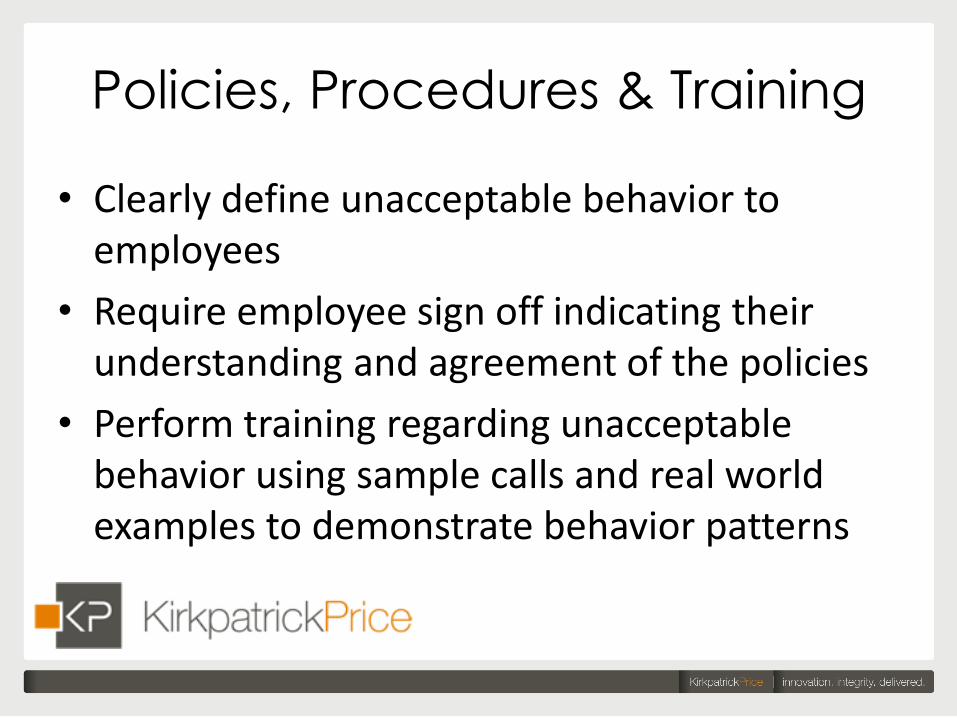

Policies, Procedures & Training

• Clearly define unacceptable behavior to employees

• Require employee sign off indicating their understanding and agreement of the policies

• Perform training regarding unacceptable behavior using sample calls and real world examples to demonstrate behavior patterns

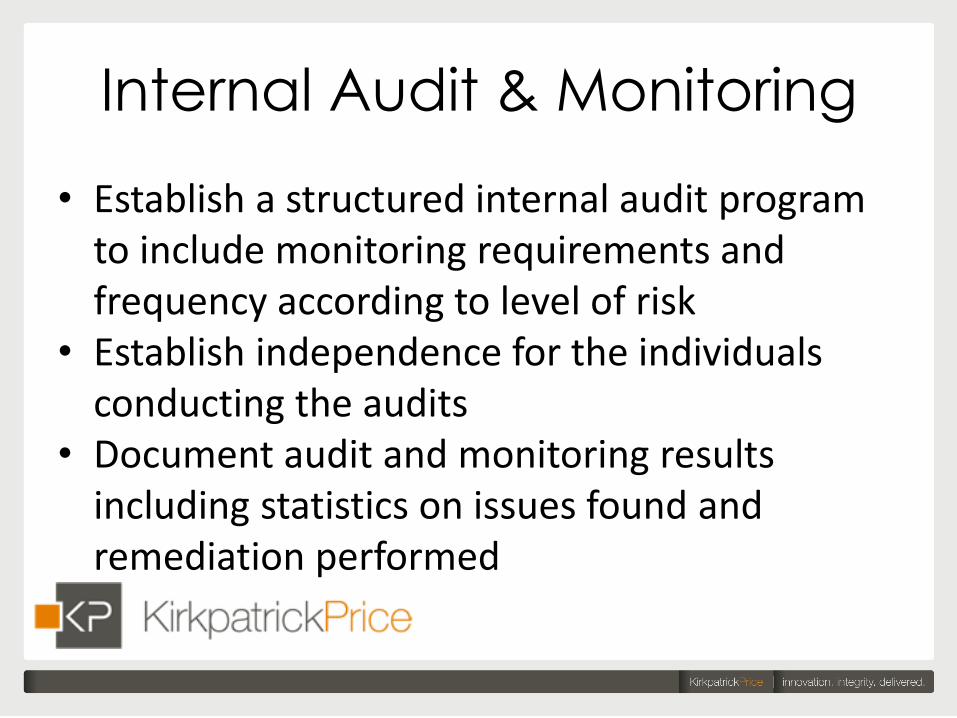

Internal Audit & Monitoring

• Establish a structured internal audit program to include monitoring requirements and frequency according to level of risk

• Establish independence for the individuals conducting the audits

• Document audit and monitoring results including statistics on issues found and remediation performed

Consumer Complaint Tracking

• Indicate potential UDAAP violations via your complaint tracking log

• Indicate the source of the complaint so that improvement efforts can be measured and documented

• Utilize key words and phrases to indicate a UDAAP related complaint

Third-Party Monitoring

• Don’t forget about third-party activity!!!

• Include third parties in:

– Risk Assessment Process

– Policy & Procedure Review

– Training Evaluation

– Audit and Monitoring efforts

– Complaint Tracking

Thank you for attending our

Webinar

Q & A

For further information contact:

Todd Stephenson

800.977.3154 Ext. 202