cash flow analysis.pptx

TRANSCRIPT

Cash Flow Statement, Concept, It’s

Preparation and Relevance

CASH FLOW ANALYSIS

Cash Flow Statements - is a financial statement that classifies changes in the Balance Sheet items as being Operating, Investing or Financing activities.

- it gives the user

of this report an idea as to where the funds came from (sources) and where it went to (uses) during a given period.

CONCEPT

Statement of Cash Flows required by PAS 7 provides information about cash inflows and outflows during an accounting period as well as the net change in cash from the operating, investing and financing activities in a manner that reconciles the beginning and ending cash balances.

To provide relevant information about a company’s cash receipts and cash payments during an accounting period that is useful in evaluating the preceding items.

NATURE & PURPOSE

PAS 7 states that the information in a statement of cash flows, if used with information in the financial statements, should help users to assess and evaluate..(a)…a company’s ability to generate positive

future net cash flows,(b)…a company’s ability to meet it’s obligations

and pay dividends,(c)…a company’s need for external financing’(d)…the reasons for differences between a

company’s net income and associated cash receipts and payments, and

(e)…both the cash and noncash aspects of a company’s financing and investing transactions during the accounting period.

PURPOSE

Cash is broadly defined to include both cash and cash equivalents.

Cash equivalents consist of short-term, highly liquid investments such as treasury bills, SEC registered commercial papers and money market funds.

Such investments are made solely for the purpose of generating a return on funds that are temporarily idle.

BASIC APPROACH

Operating Activities- the amount of cash flows arising from operating activities is a key indicator of the extent to which the operations of the enterprise have generated sufficient cash flows to repay loans, maintain the operating capability of the enterprise, pay dividends and make new investments without recourse to external sources of financing. -It includes delivering or producing goods for sale and providing services; and the cash effects of transactions and other events that enter into the determination of income.

CLASSIFICATION OF CASH FLOW ACTIVITIES

Sales of goodsRevenue from

servicesInterestDividendsReceipts from

contracts held for dealing and trading purposes

Tax refunds

Payments for purchases of inventories

Payments for operating expenses

Payments for purchase from

suppliers other than inventory

Payments for lenders

Payment for taxes

INFLOWS OUTFLOWS

EXAMPLES OF OPERATING ACTIVITIES

It is important because the cash flows represent the extent to which expenditures have been made for resources intended to generate future income and cash flows.It includes acquiring and selling or depositing of securities that are not cash equivalents and productive assets that are expected to benefit the firm for long periods of time and lending money and collecting on loans.

INVESTING ACTIVITIES

Sales of long-lived assets (PPE; intangibles and other long-term assets)

Sales of debt or equity securities of other entities

Collection of loans to others

Acquisitions of long-lived assetsPurchases of debt or equity securities of other entitiesLoans to others

INFLOWS OUTFLOWS

INVESTING ACTIVITIES

It is useful in predicting claims on future cash flows by

providers of capital to the enterprise.

It includes borrowing from creditors and repaying the principal; and obtaining

resources from owners and providing them with a return on

the investments.

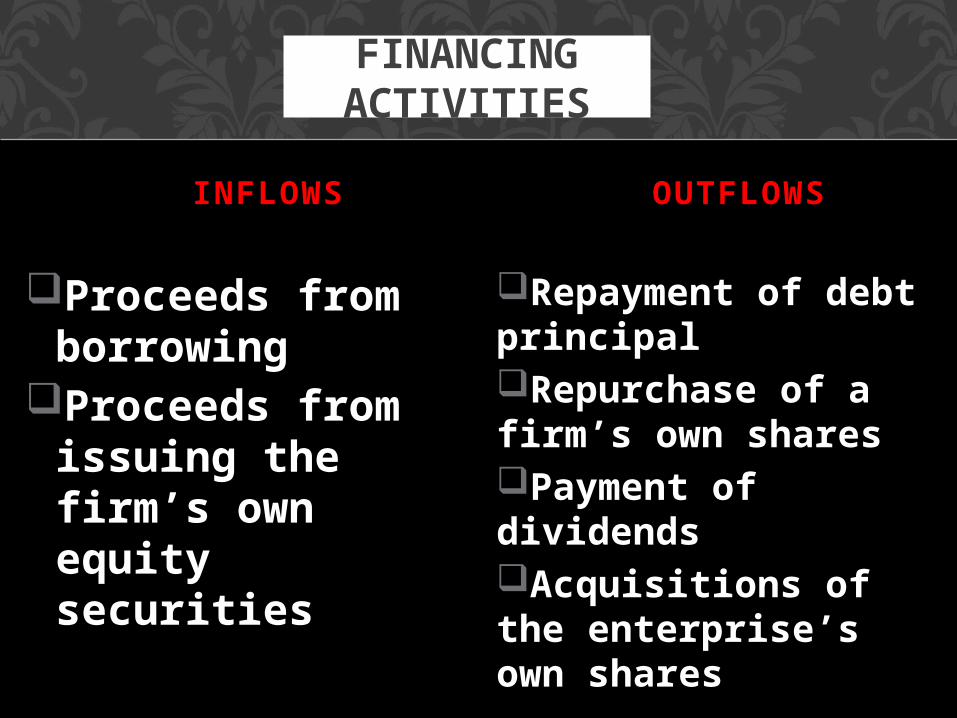

FINANCING ACTIVITIES

Proceeds from borrowing

Proceeds from issuing the firm’s own equity securities

Repayment of debt principalRepurchase of a firm’s own sharesPayment of dividendsAcquisitions of the enterprise’s own shares

INFLOWS OUTFLOWS

FINANCING ACTIVITIES

Statement of Cash Flows (SCF) for a period shall report the following:

A. Net Cash 1. Provided or used by operating activities 2. Provided or used by investing activities 3. Provided or used by financing activitiesB. Net effect of those flows on cash and cash equivalents during

the period in a manner that reconciles the beginning and ending cash and cash equivalents.

Noncash investing and financing activities affecting the financial position shall be excluded from a cash flow statement. Such transactions should be disclosed elsewhere in the financial statements e.g. notes to financial statements.

CONTENT AND FORM

VISUAL INSPECTION METHOD- used when the financial statements are not complex and when the relationship between the changes in account balances can be easily observed and analyzed

WORKSHEET METHOD OF ANALYSIS- used in practice because analysis of even the most complex set of financial statements may be documented in a relatively concise working paper. - before the SCF is prepared, a worksheet is prepared and the cash flows effects of operating, investing, and financing activities during the accounting period are first analyzed.

METHODS OF ANALYSIS TO PREPARE SCF

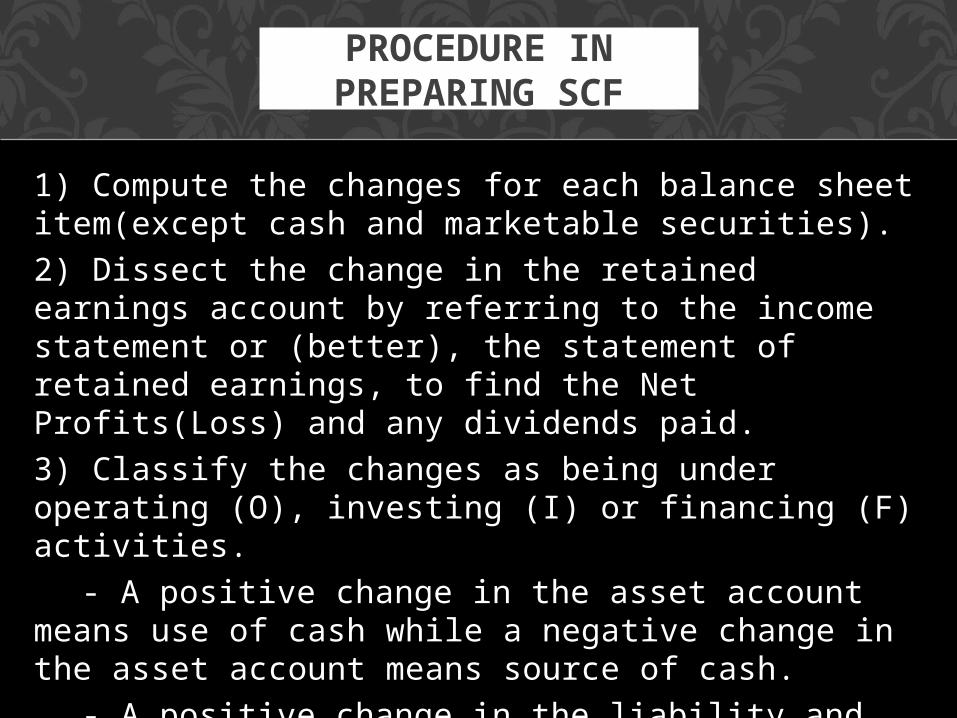

1) Compute the changes for each balance sheet item(except cash and marketable securities).2) Dissect the change in the retained earnings account by referring to the income statement or (better), the statement of retained earnings, to find the Net Profits(Loss) and any dividends paid.3) Classify the changes as being under operating (O), investing (I) or financing (F) activities.

- A positive change in the asset account means use of cash while a negative change in the asset account means source of cash.

- A positive change in the liability and stockholder’s equity account means source of cash, while a negative change means use of cash.4) Prepare the formal cash flow statement.

PROCEDURE IN PREPARING SCF

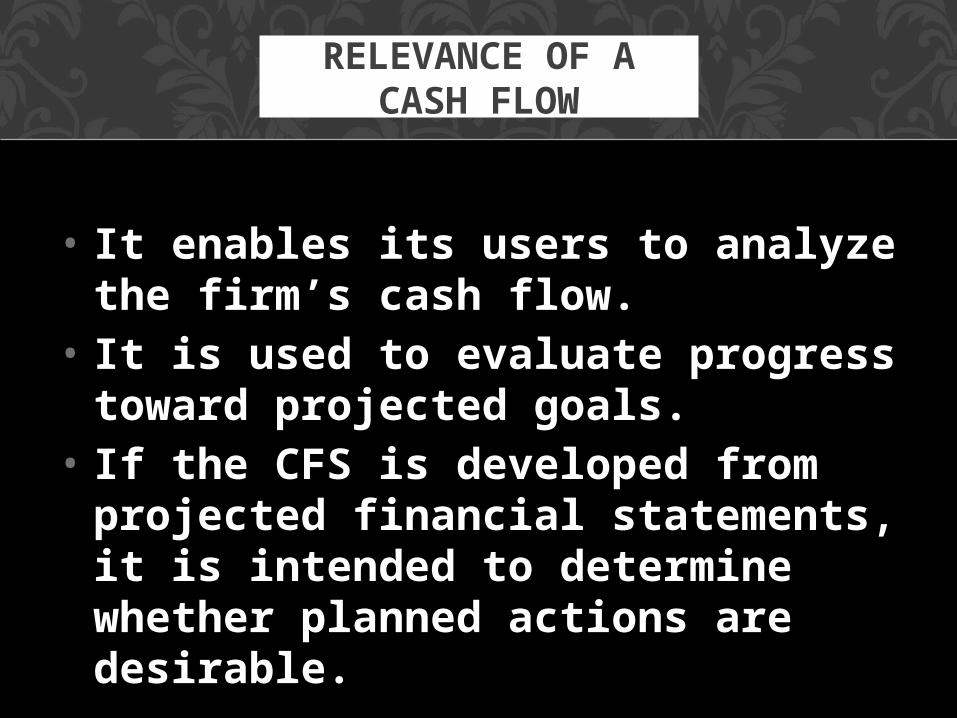

• It enables its users to analyze the firm’s cash flow.

• It is used to evaluate progress toward projected goals.

• If the CFS is developed from projected financial statements, it is intended to determine whether planned actions are desirable.

RELEVANCE OF A CASH FLOW