can dynamic risk investing solve the defined-benefit … · standard of living in retirement ......

TRANSCRIPT

Can Dynamic Risk Investing Solve the

Defined-Benefit Conundrum

Tuesday, May 3, 2010

6:30 AM – 7:45 AM

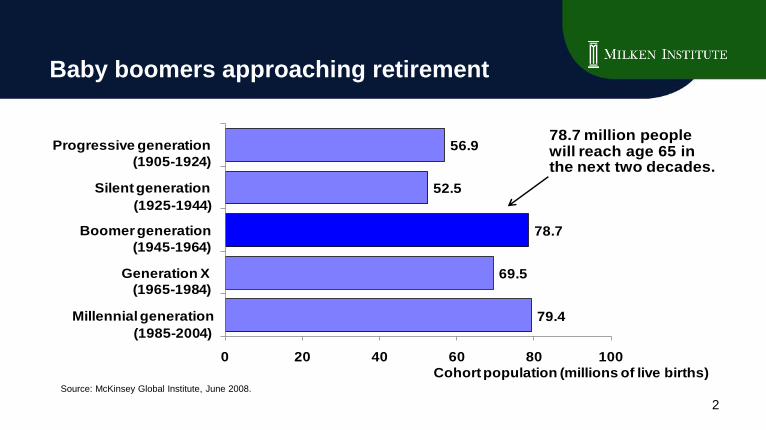

Baby boomers approaching retirement

Source: McKinsey Global Institute, June 2008.

79.4

69.5

78.7

52.5

56.9

0 20 40 60 80 100

Millennial generation

Generation X

Boomer generation

Silent generation

Progressive generation

Cohort population (millions of live births)

(1905-1924)

(1925-1944)

(1945-1964)

(1965-1984)

(1985-2004)

78.7 million people will reach age 65 in the next two decades.

2

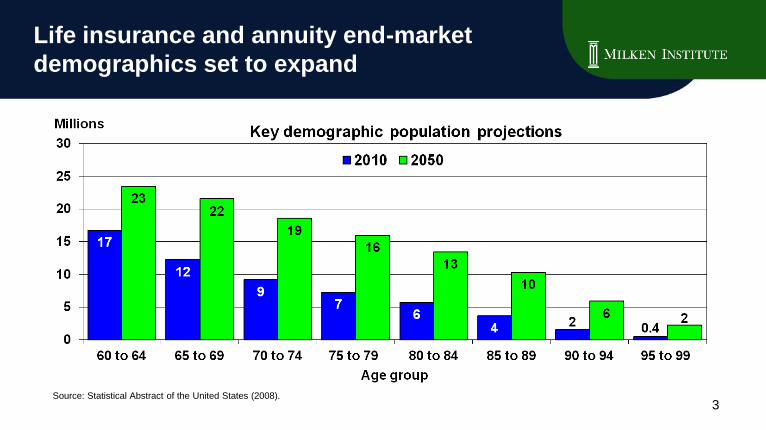

Life insurance and annuity end-market

demographics set to expand

Source: Statistical Abstract of the United States (2008).3

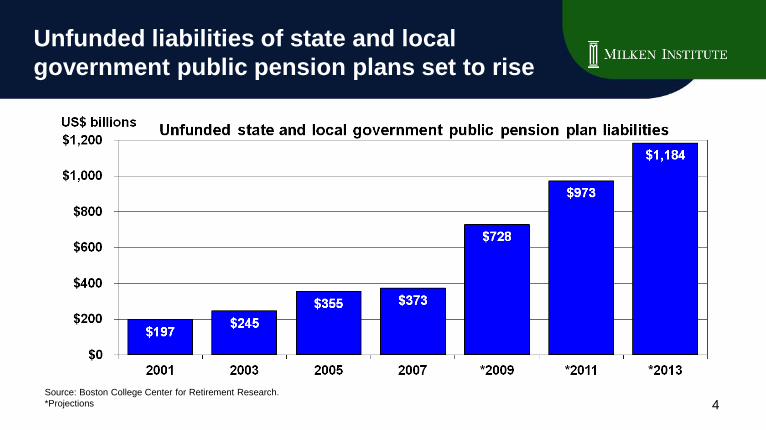

Unfunded liabilities of state and local

government public pension plans set to rise

Source: Boston College Center for Retirement Research.

*Projections 4

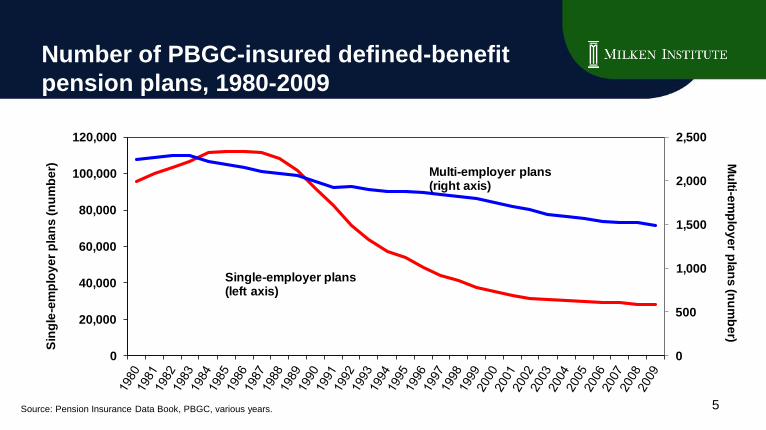

Source: Pension Insurance Data Book, PBGC, various years. 5

Number of PBGC-insured defined-benefit

pension plans, 1980-2009

0

500

1,000

1,500

2,000

2,500

0

20,000

40,000

60,000

80,000

100,000

120,000

Single-employer plans(left axis)

Multi-employer plans(right axis)

Mu

lti-em

plo

ye

r pla

ns

(nu

mb

er)

Sin

gle

-em

plo

ye

r p

lan

s (n

um

be

r)

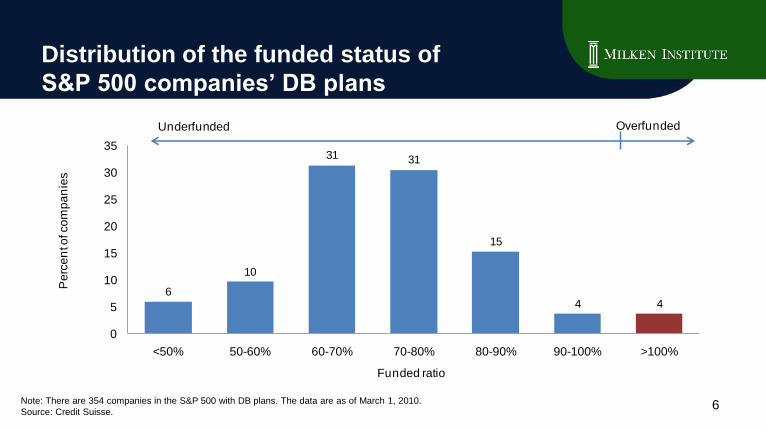

Note: There are 354 companies in the S&P 500 with DB plans. The data are as of March 1, 2010.

Source: Credit Suisse.6

Distribution of the funded status of

S&P 500 companies’ DB plans

6

10

31 31

15

4 4

0

5

10

15

20

25

30

35

<50% 50-60% 60-70% 70-80% 80-90% 90-100% >100%

Pe

rce

nt o

f co

mp

an

ies

Funded ratio

Underfunded Overfunded

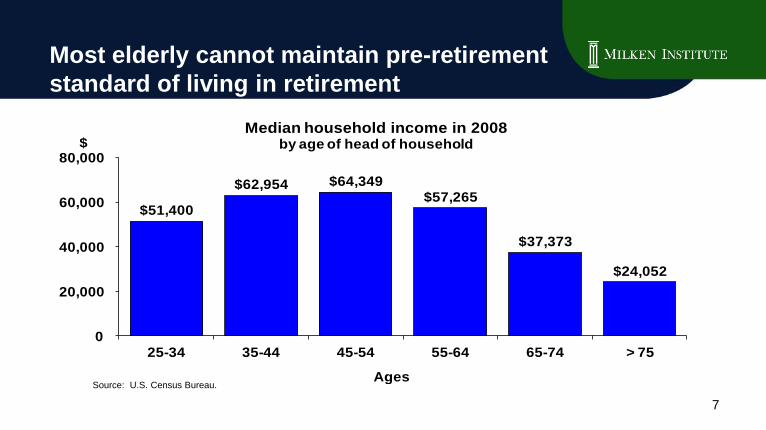

Most elderly cannot maintain pre-retirement

standard of living in retirement

$51,400

$62,954 $64,349 $57,265

$37,373

$24,052

0

20,000

40,000

60,000

80,000

25-34 35-44 45-54 55-64 65-74 > 75

$

Ages

Median household income in 2008by age of head of household

Source: U.S. Census Bureau.

7

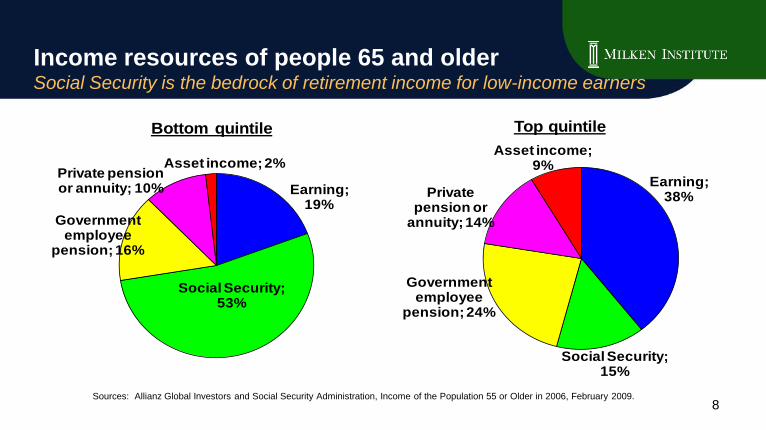

Income resources of people 65 and olderSocial Security is the bedrock of retirement income for low-income earners

Sources: Allianz Global Investors and Social Security Administration, Income of the Population 55 or Older in 2006, February 2009.

Bottom quintile

Social Security; 53%

Private pension or annuity; 10%

Asset income; 2%

Earning; 19%

Government employee

pension; 16%

Top quintile

Social Security; 15%

Private pension or

annuity; 14%

Asset income; 9%

Earning; 38%

Government employee

pension; 24%

8

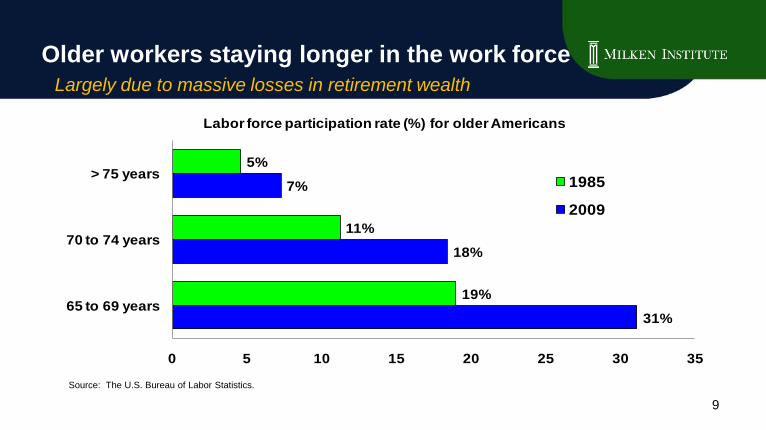

Older workers staying longer in the work force

Largely due to massive losses in retirement wealth

Source: The U.S. Bureau of Labor Statistics.

31%

18%

7%

19%

11%

5%

0 5 10 15 20 25 30 35

65 to 69 years

70 to 74 years

> 75 years

Labor force participation rate (%) for older Americans

1985

2009

9

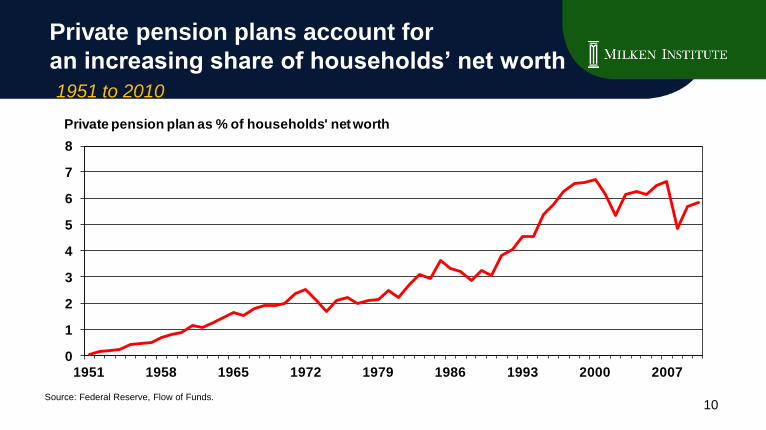

Private pension plans account for

an increasing share of households’ net worth

1951 to 2010

10Source: Federal Reserve, Flow of Funds.

0

1

2

3

4

5

6

7

8

1951 1958 1965 1972 1979 1986 1993 2000 2007

Private pension plan as % of households' net worth

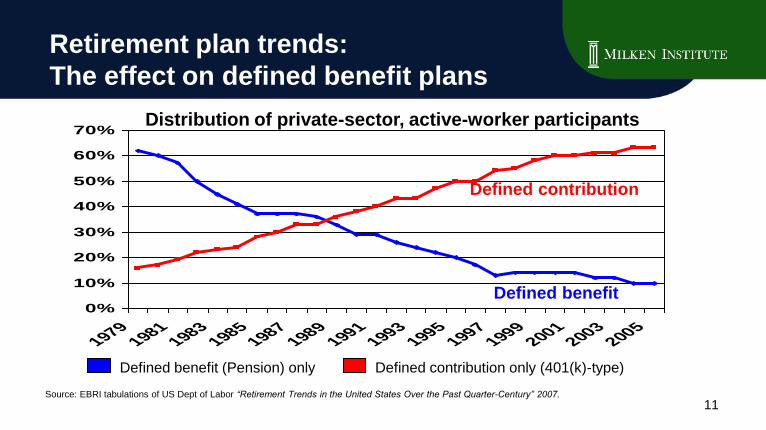

Retirement plan trends:

The effect on defined benefit plans

0%

10%

20%

30%

40%

50%

60%

70%

19791981

19831985

19871989

19911993

19951997

19992001

20032005

Defined benefit (Pension) only Defined contribution only (401(k)-type)

Source: EBRI tabulations of US Dept of Labor “Retirement Trends in the United States Over the Past Quarter-Century” 2007.

Defined benefit

Defined contribution

Distribution of private-sector, active-worker participants

11

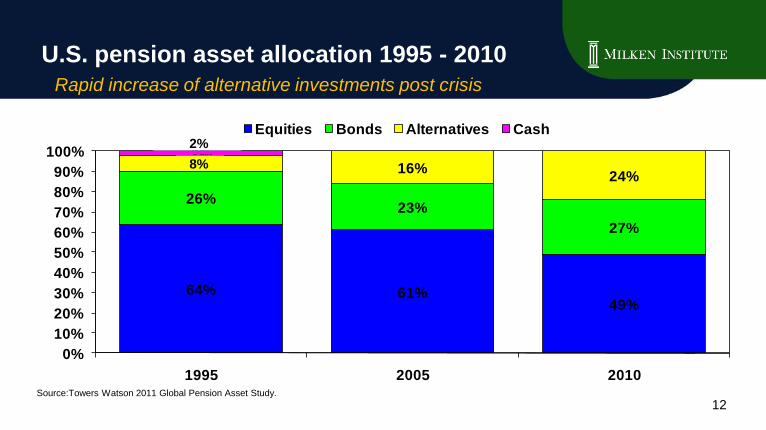

Source:Towers Watson 2011 Global Pension Asset Study.

12

64% 61%49%

26%23%

27%

8% 16%24%

2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1995 2005 2010

Equities Bonds Alternatives Cash

U.S. pension asset allocation 1995 - 2010

Rapid increase of alternative investments post crisis

8%

2%

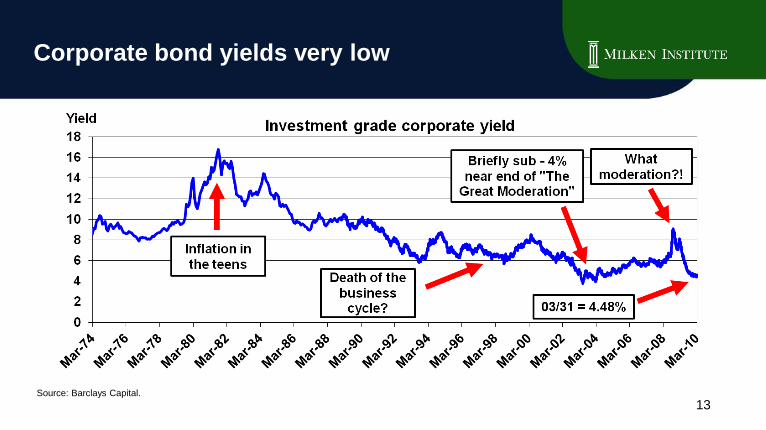

Corporate bond yields very low

Source: Barclays Capital.

13

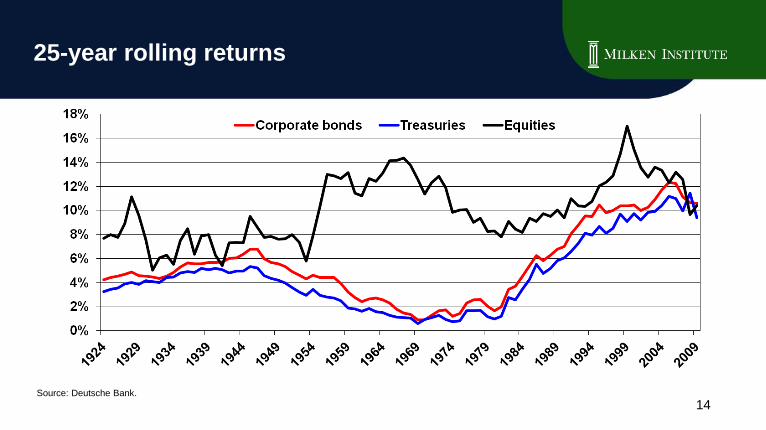

25-year rolling returns

Source: Deutsche Bank.

14

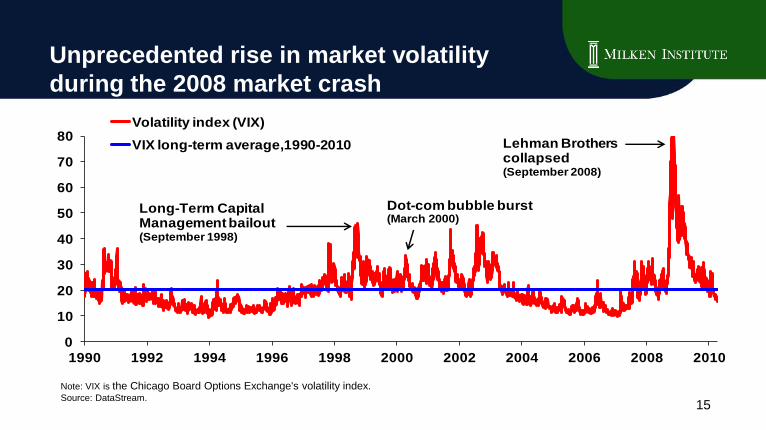

Unprecedented rise in market volatility

during the 2008 market crash

Note: VIX is the Chicago Board Options Exchange's volatility index. Source: DataStream.

0

10

20

30

40

50

60

70

80

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Volatility index (VIX)

VIX long-term average,1990-2010 Lehman Brotherscollapsed (September 2008)

Dot-com bubble burst (March 2000)

Long-Term Capital Management bailout (September 1998)

15

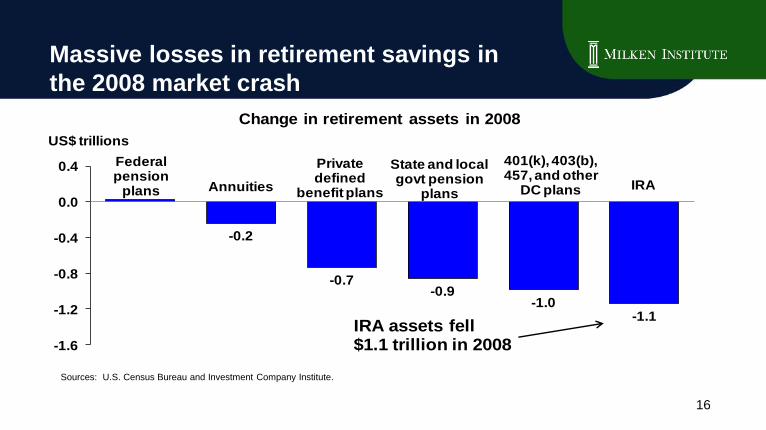

Massive losses in retirement savings in

the 2008 market crash

Sources: U.S. Census Bureau and Investment Company Institute.

-0.2

-0.7-0.9

-1.0-1.1

-1.6

-1.2

-0.8

-0.4

0.0

0.4

US$ trillions

Change in retirement assets in 2008

IRA

401(k), 403(b), 457, and other

DC plans

State and local govt pension

plans

Private defined

benefit plansAnnuities

Federalpension

plans

IRA assets fell $1.1 trillion in 2008

16

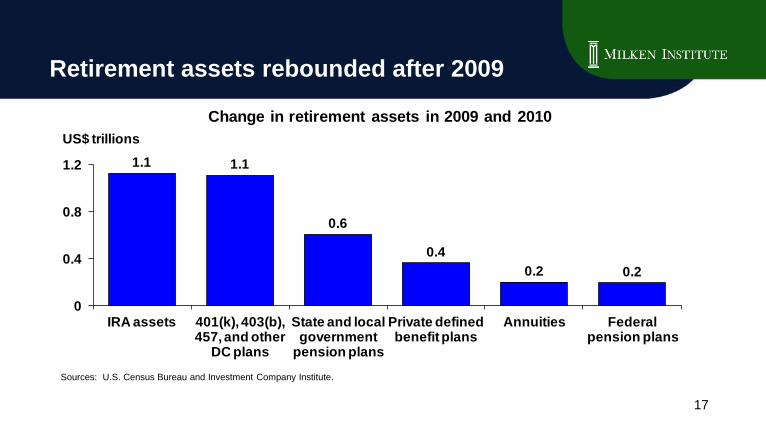

Retirement assets rebounded after 2009

17

Sources: U.S. Census Bureau and Investment Company Institute.

1.1 1.1

0.6

0.4

0.2 0.2

0

0.4

0.8

1.2

IRA assets 401(k), 403(b), 457, and other

DC plans

State and local government

pension plans

Private defined benefit plans

Annuities Federal pension plans

US$ trillions

Change in retirement assets in 2009 and 2010

Milken Conference

May 1, 2011

Dynamic Risk Investing

Kenneth Yip, PhD

Investor Science Group, LLC.

Please note that important information regarding the information and views expressed in this material at the end of this presentation under “Important Legal Information” and is available upon request

Copyright © 2006-2011, Investor Science Group, LLC. All rights reserved.This document, which is protected by copyright and other intellectual property rights, is confidential and has been prepared solely for the information of the person to whom it has been delivered on behalf of Investor Science Group, LLC.

It may not be reproduced, distributed, or used for any other purpose. Your acceptance of this document constitutes your acknowledgement of and agreement to abide by these terms and conditions.

Today’s discussion

I. The failure of conventional thinking

II. Dynamic risk investing: A new paradigm

III. Case study & implementation

19

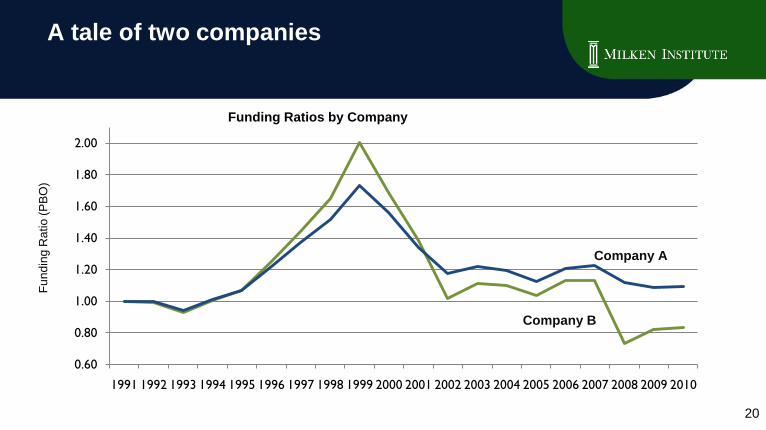

A tale of two companies

20

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Funding Ratios by Company

Fu

nd

ing

Ratio

(P

BO

)

Company B

Company A

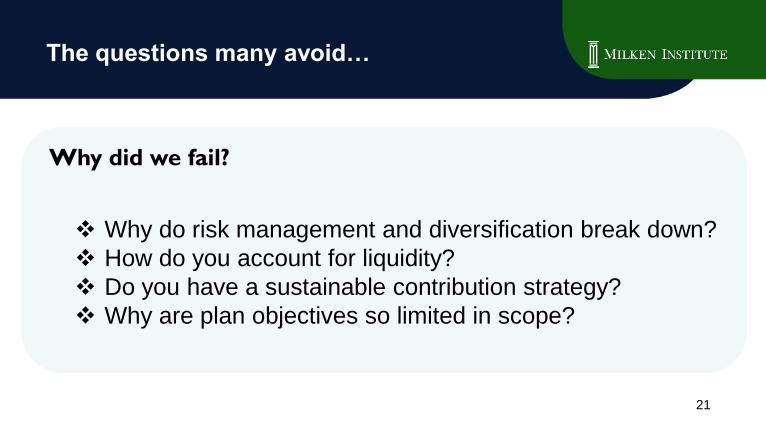

The questions many avoid…

Why did we fail?

Why do risk management and diversification break down?

How do you account for liquidity?

Do you have a sustainable contribution strategy?

Why are plan objectives so limited in scope?

21

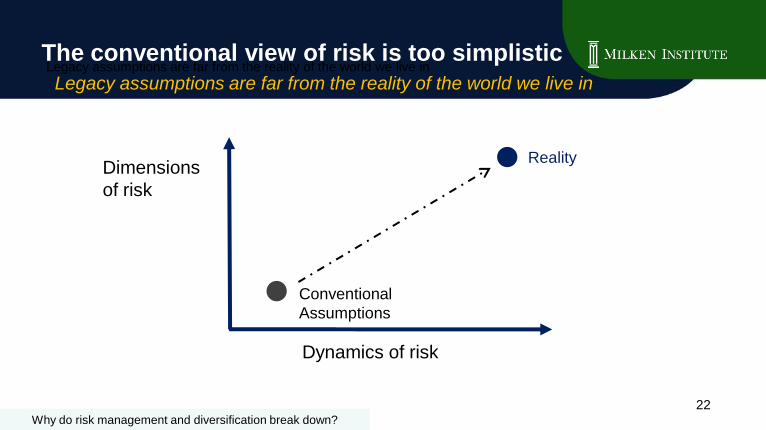

Dimensions

of risk

Dynamics of risk

Conventional

Assumptions

Reality

Legacy assumptions are far from the reality of the world we live in

Why do risk management and diversification break down?

22

The conventional view of risk is too simplistic

Legacy assumptions are far from the reality of the world we live in

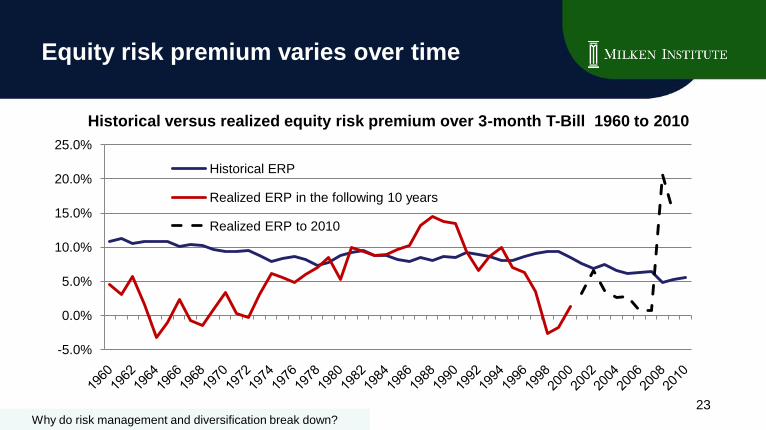

Equity risk premium varies over time

Historical versus realized equity risk premium over 3-month T-Bill 1960 to 2010

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Historical ERP

Realized ERP in the following 10 years

Realized ERP to 2010

23Why do risk management and diversification break down?

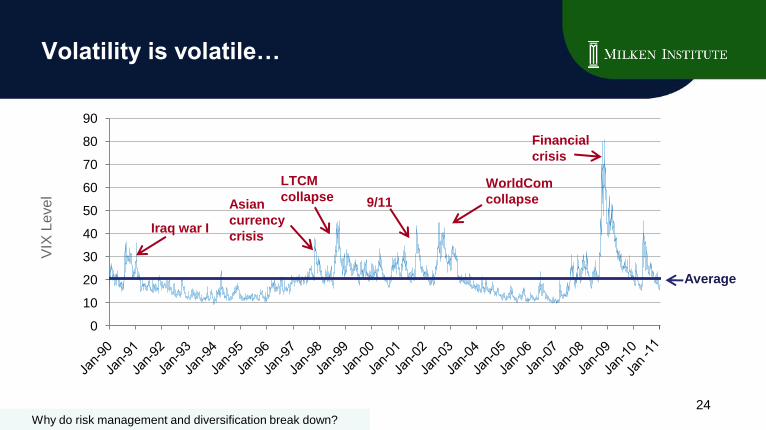

Volatility is volatile…

0

10

20

30

40

50

60

70

80

90

Iraq war I

Asian

currency

crisis

LTCM

collapse 9/11

WorldCom

collapse

Financial

crisis

Average

VIX

Leve

l

24Why do risk management and diversification break down?

Correlation is also volatile

Rolling 24-month correlation of S&P500 and long Government bond

-0.80

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

Rolling 24-month Correlation Average Correlation25

Why do risk management and diversification break down?

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

Jun-9

2

Jan-9

3

Aug-9

3

Mar-

94

Oct-

94

Ma

y-9

5

Dec-9

5

Jul-96

Feb

-97

Sep-9

7

Apr-

98

Nov-9

8

Jun-9

9

Jan-0

0

Aug-0

0

Mar-

01

Oct-

01

Ma

y-0

2

Dec-0

2

Jul-03

Feb

-04

Sep-0

4

Apr-

05

Nov-0

5

Jun-0

6

Jan-0

7

Aug-0

7

Mar-

08

Oct-

08

Ma

y-0

9

Dec-0

9

Jul-10

Constant 80/20 Average Volatility

Realized portfolio volatility, 1992-2010

26

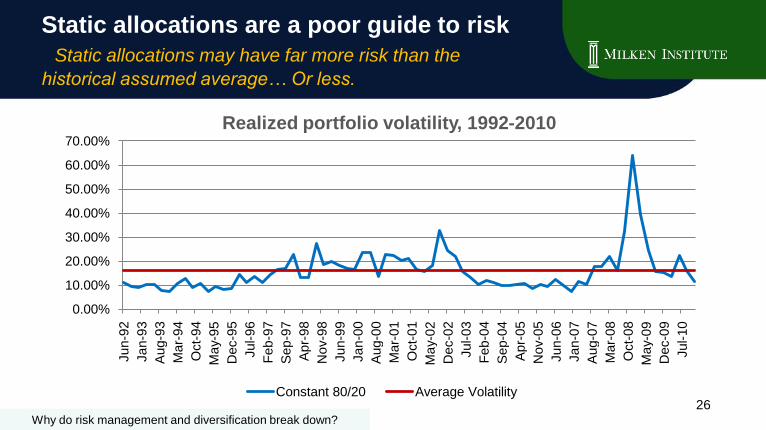

Static allocations are a poor guide to risk

Static allocations may have far more risk than the

historical assumed average… Or less.

Why do risk management and diversification break down?

Liquidity is most expensive

when needed most

Credit market freeze

Hedge fund gates

Private equity capital calls

Real estate market shutdown

• Liquidity events affect both sources of liquidity: accessing credit and liquidating assets

• It is rarely integrated into portfolio construction

27How do you account for liquidity?

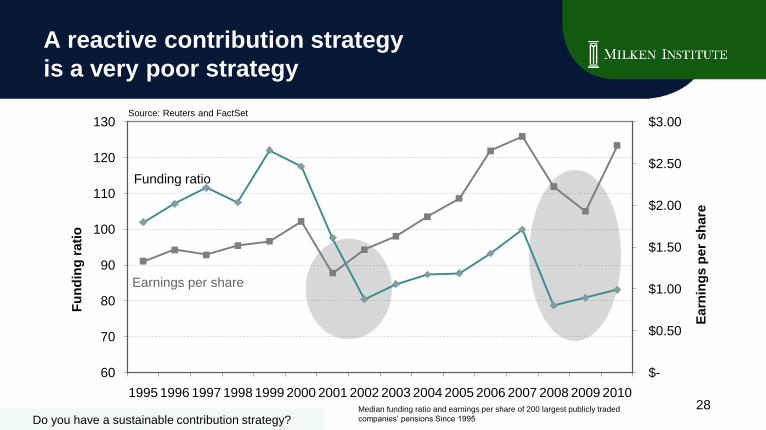

$-

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

60

70

80

90

100

110

120

130

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Do you have a sustainable contribution strategy?Median funding ratio and earnings per share of 200 largest publicly traded

companies’ pensions Since 1995

Source: Reuters and FactSet

Earn

ing

s p

er

sh

are

Fu

nd

ing

rati

o

Funding ratio

Earnings per share

28

A reactive contribution strategy

is a very poor strategy

Investment objectives need to evolve

Asset only Asset +

Liability +

Financial flexibility +

Fiscal health of

sponsor organization

Asset +

Liability

ISOLATED INTEGRATED

Why are plan objectives so limited in scope?

29

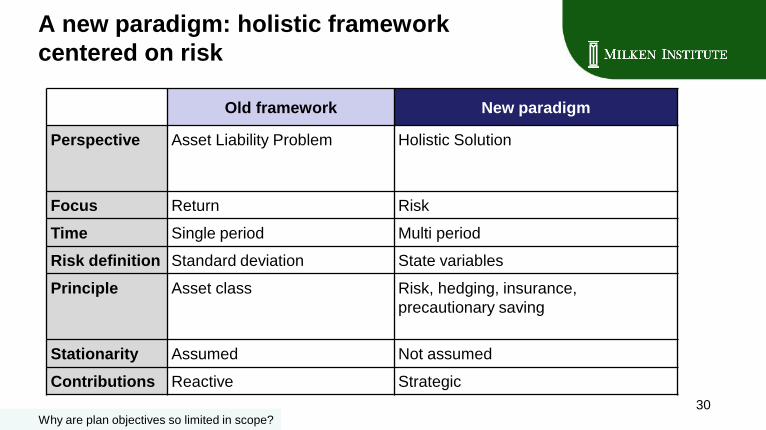

A new paradigm: holistic framework

centered on risk

Old framework New paradigm

Perspective Asset Liability Problem Holistic Solution

Focus Return Risk

Time Single period Multi period

Risk definition Standard deviation State variables

Principle Asset class Risk, hedging, insurance,

precautionary saving

Stationarity Assumed Not assumed

Contributions Reactive Strategic

Why are plan objectives so limited in scope?

30

I. The failure of conventional thinking

II. Dynamic risk investing: A new paradigm

III. Case study & implementation

Today’s discussion

31

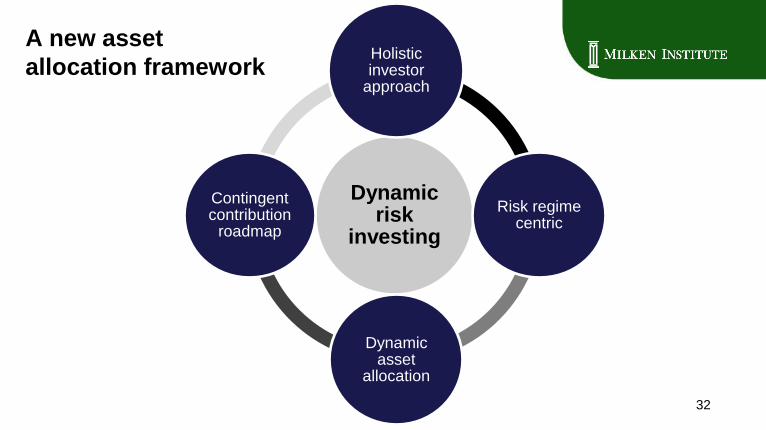

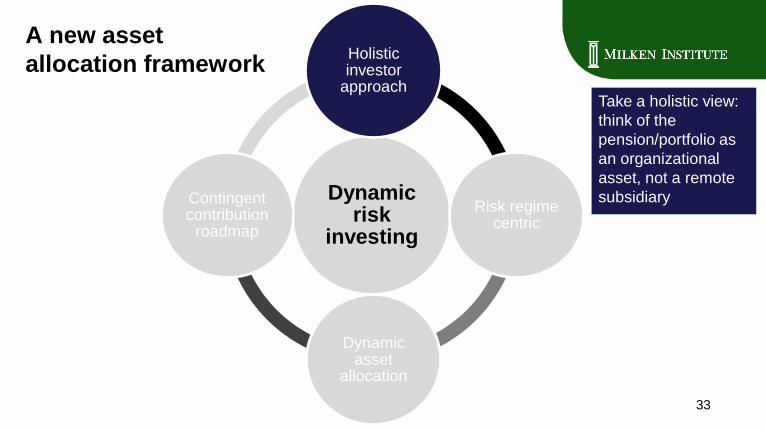

A new asset

allocation framework

32

Dynamic risk

investing

Holistic investor

approach

Risk regime centric

Dynamic asset

allocation

Contingent contribution

roadmap

A new asset

allocation framework

Take a holistic view:

think of the

pension/portfolio as

an organizational

asset, not a remote

subsidiary

33

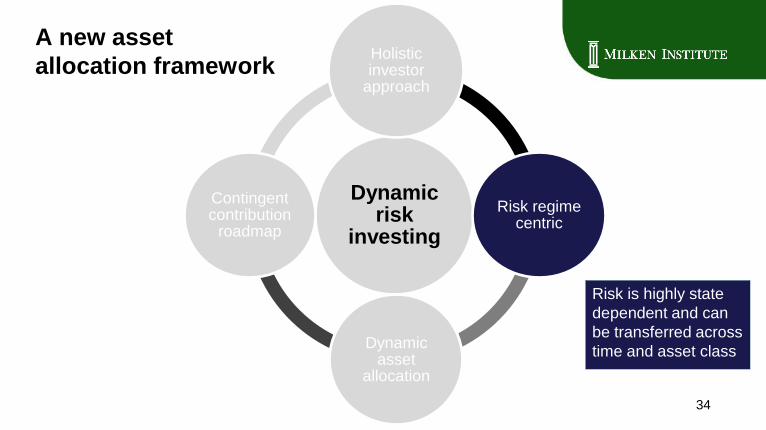

Dynamic risk

investing

Holistic investor

approach

Risk regime centric

Dynamic asset

allocation

Contingent contribution

roadmap

A new asset

allocation framework

Risk is highly state

dependent and can

be transferred across

time and asset class

Dynamic risk

investing

Holistic investor

approach

Risk regime centric

Dynamic asset

allocation

Contingent contribution

roadmap

34

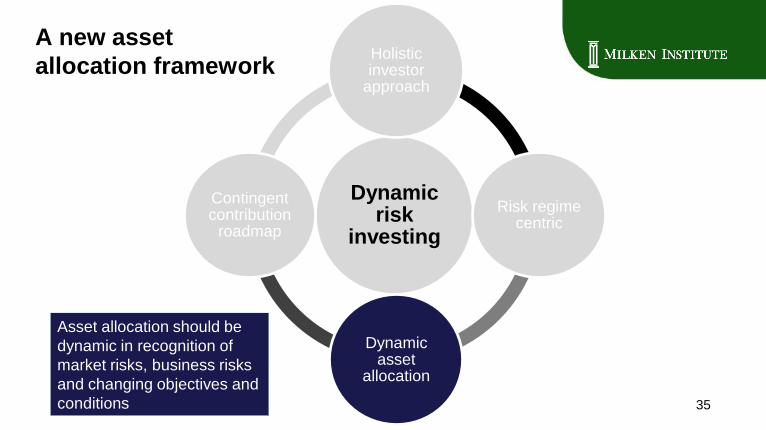

Asset allocation should be

dynamic in recognition of

market risks, business risks

and changing objectives and

conditions 35

A new asset

allocation framework

Dynamic risk

investing

Holistic investor

approach

Risk regime centric

Dynamic asset

allocation

Contingent contribution

roadmap

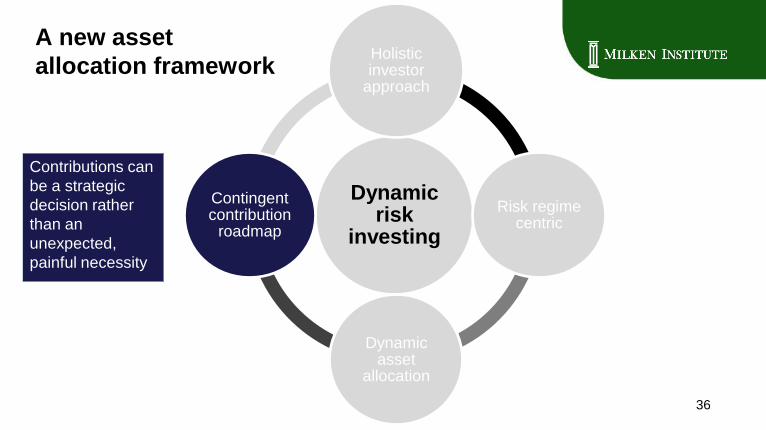

Contributions can

be a strategic

decision rather

than an

unexpected,

painful necessity

36

A new asset

allocation framework

Dynamic risk

investing

Holistic investor

approach

Risk regime centric

Dynamic asset

allocation

Contingent contribution

roadmap

Risk regime

framework

Dynamic multi-period

process

Forecast models

Alternatives

capabilities

– Non-Normal/Short

data histories

– Illiquid investments

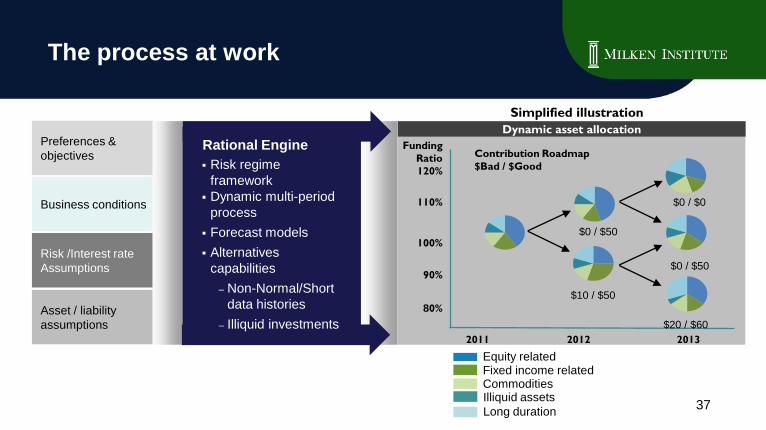

The process at work

Preferences &

objectives

Business conditions

Risk /Interest rate

Assumptions

Asset / liability

assumptions

Dynamic asset allocation

2011 2012 2013

Funding

Ratio

120%

110%

100%

90%

80%

Contribution Roadmap

$Bad / $Good

Simplified illustration

$0 / $50

$10 / $50

$0 / $0

$0 / $50

$20 / $60

Equity relatedFixed income relatedCommoditiesIlliquid assets

Long duration37

Rational Engine

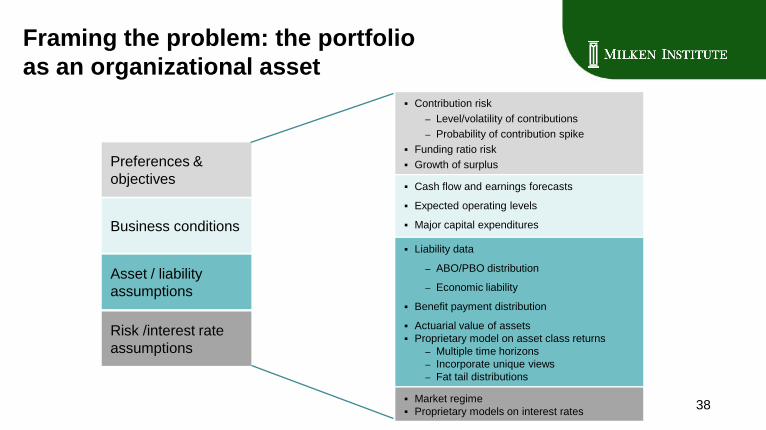

Framing the problem: the portfolio

as an organizational asset

Preferences &

objectives

Business conditions

Asset / liability

assumptions

Risk /interest rate

assumptions

Contribution risk

– Level/volatility of contributions

– Probability of contribution spike

Funding ratio risk

Growth of surplus

Cash flow and earnings forecasts

Expected operating levels

Major capital expenditures

Market regime

Proprietary models on interest rates

Liability data

– ABO/PBO distribution

– Economic liability

Benefit payment distribution

Actuarial value of assets

Proprietary model on asset class returns

– Multiple time horizons

– Incorporate unique views

– Fat tail distributions

38

Today’s discussion

39

I. The failure of conventional thinking

II. Dynamic risk investing: A new paradigm

III. Case study & implementation

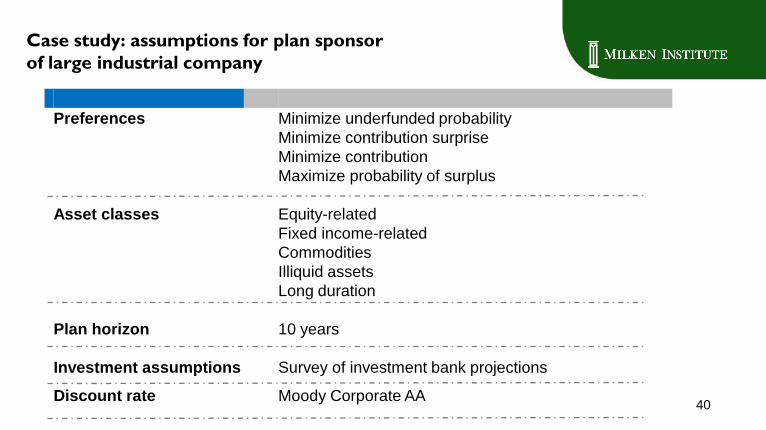

Case study: assumptions for plan sponsor

of large industrial company

Preferences Minimize underfunded probability

Minimize contribution surprise

Minimize contribution

Maximize probability of surplus

Asset classes Equity-related

Fixed income-related

Commodities

Illiquid assets

Long duration

Plan horizon 10 years

Investment assumptions Survey of investment bank projections

Discount rate Moody Corporate AA40

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Pro

bability d

ensi

ty

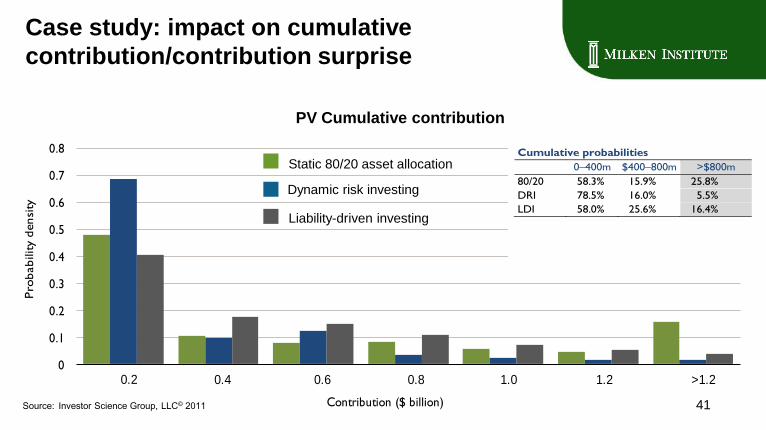

Contribution ($ billion)

PV Cumulative Contribution

0.2 0.4 0.6 0.8 1.0 1.2 >1.2

Case study: impact on cumulative

contribution/contribution surprise

Source: Investor Science Group, LLC© 2011 41

Cumulative probabilities

0–400m $400–800m >$800m

80/20 58.3% 15.9% 25.8%

DRI 78.5% 16.0% 5.5%

LDI 58.0% 25.6% 16.4%

Liability-driven investing

Static 80/20 asset allocation

Dynamic risk investing

PV Cumulative contribution

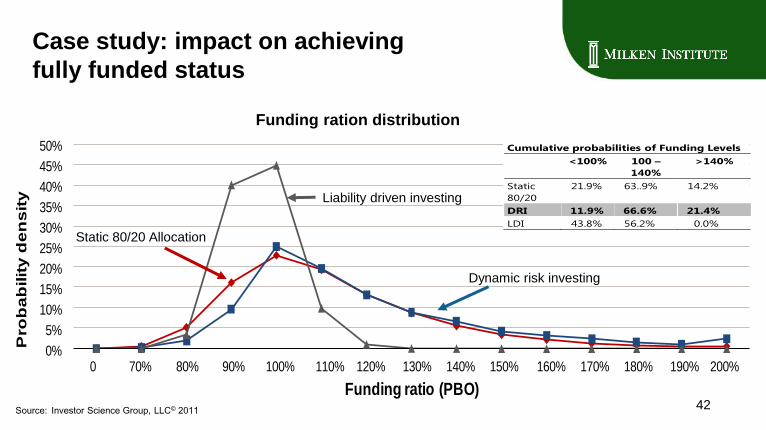

Case study: impact on achieving

fully funded status

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Pro

ba

bilit

y d

en

sit

y

Funding ratio (PBO)

Funding Ratio Distribution

0 70% 80% 90% 100% 110% 120% 130% 140% 150% 160% 170% 180% 190% 200%

Source: Investor Science Group, LLC© 2011

Liability driven investing

Static 80/20 Allocation

Dynamic risk investing

42

Cumulative probabilities of Funding Levels

<100% 100 –

140%

>140%

Static

80/20

21.9% 63..9% 14.2%

DRI 11.9% 66.6% 21.4%

LDI 43.8% 56.2% 0.0%

Funding ration distribution

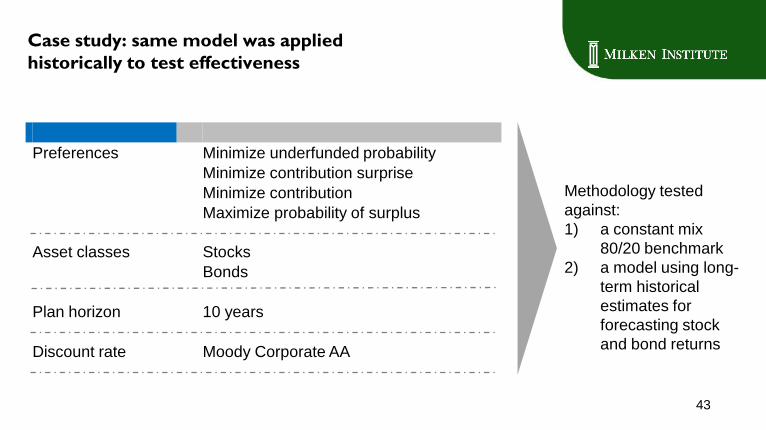

Case study: same model was applied

historically to test effectiveness

Preferences Minimize underfunded probability

Minimize contribution surprise

Minimize contribution

Maximize probability of surplus

Asset classes Stocks

Bonds

Plan horizon 10 years

Discount rate Moody Corporate AA

43

Methodology tested

against:

1) a constant mix

80/20 benchmark

2) a model using long-

term historical

estimates for

forecasting stock

and bond returns

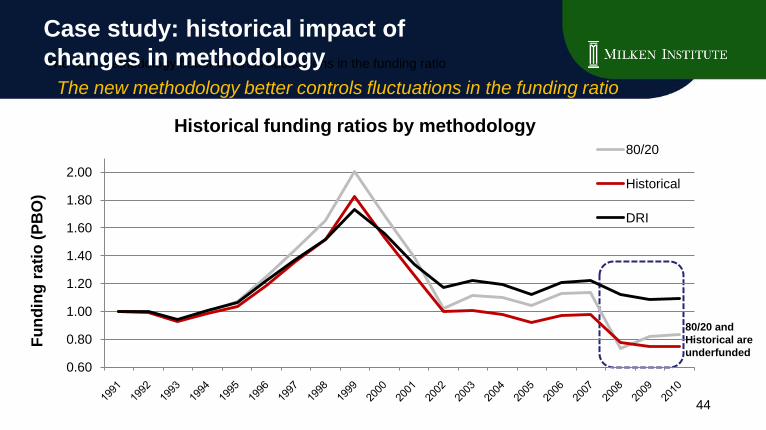

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

80/20

Historical

DRI

80/20 and

Historical are

underfunded

Historical funding ratios by methodology

Fu

nd

ing

ra

tio

(P

BO

)

The new methodology better controls fluctuations in the funding ratio

Case study: historical impact of

changes in methodology

The new methodology better controls fluctuations in the funding ratio

44

30%

40%

50%

60%

70%

80%

90%

100%

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Historical DRI

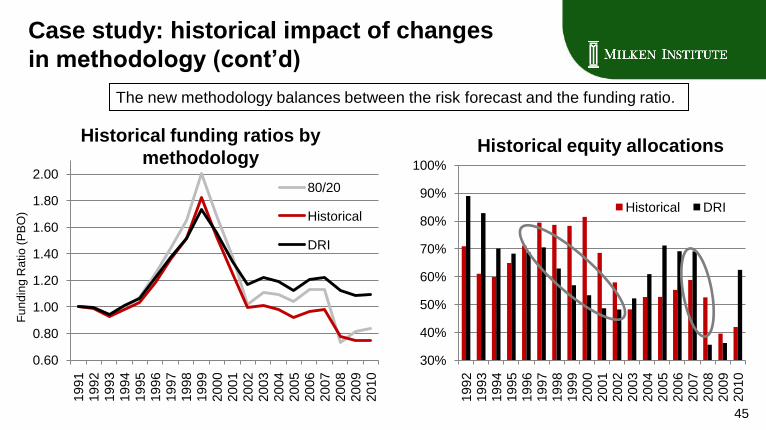

Case study: historical impact of changes

in methodology (cont’d)

Historical equity allocations

Fu

nd

ing

Ratio

(P

BO

)

Historical funding ratios by

methodology

The new methodology balances between the risk forecast and the funding ratio.

45

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

80/20

Historical

DRI

Takeaways

A tale of two companies:

» Conventional approach to asset-liability management

failed, plan dissolved

» Dynamic risk investing worked

A mind shift is necessary to understand and exploit risk

dynamically

Financial technology and decision framework innovation

allow us to harness the economic opportunities today 46

Speaker biography

Ken Yip is the founder and Chief Executive of Investor Science Group, a financial software and consulting firm

specializing in asset/liability management and investment solutions, designed primarily for large Pension Funds.

Before returning to Investor Science Group, Ken was Managing Director and head of the US Investment Solutions

Group at Credit Suisse Asset Management. Prior to founding the Investor Science Group in 2006, he co-founded

and was CIO of Thunder Bay Capital Management, New York, a multi-strategy quantitative hedge fund (AUM USD

110m). Before that, he was a Managing Director at Deutsche Asset Management and head of their Global Research

Center, where he was responsible for the development of next generation investment products and solution

processes to meet sophisticated asset/liability needs of major pension plan sponsors, corporations, endowment and

foundation, and wealthy families in the US, Europe, Australia and Asia.

Ken has been featured in Plan Sponsor magazine, The Wall Street Journal, and Australian Financial Review. He

has been an invited speaker at The Berkeley Program in Finance, The GARP Conference, Institutional Investor

Conference, GAIM Conference, CFA Societies, and Society of Actuaries Meetings.

Prior to joining the financial services industry, Ken was a Principal Research Scientist in the Artificial Intelligence

Laboratory and a visiting professor at MIT and before that was an Assistant Professor at Yale’s Department of

Computer Science, where he won the prestigious National Science Foundation Young Investigator Award, and the

Yale College Teaching Award for excellence in teaching undergraduate natural sciences. Ken holds a BS, MS, and

PhD in Computer Science from MIT.

Kenneth Yip, PhD

Founder, Investor Science Group, LLC

phone: 646 287 9478 email: [email protected]

47

Important legal information

There is no and will be no agreement, arrangement, or understanding that the information provided in connection herein will

be used as a primary basis for any investment decisions, including, without limitation, the purchase of any Investor Science

Group products or engagement of Investor Science Group consulting services. No person shall rely on this information as a

primary basis for any investment decision with respect to any employee benefit plan, including, without limitation, the

purchase of any Investor Science Group products or engagement of Investor Science Group consulting services on behalf of

such plan; and there is no, and will be no, agreement, arrangement, or understanding to the contrary.

This material has been prepared by Investor Science Group, LLC on the basis of publicly available information, internally

developed data and other third party sources believed to be reliable. However, no assurances are provided regarding the

reliability of such information. All opinions and views constitute judgments as of the date of writing, and are subject to change

at any time without notice. The investment views and market opinions/analyses expressed may not reflect those of Investor

Science Group, LLC as a whole and different views may be expressed based on different investment styles, objectives, views

or philosophies.

No graph or formula can, by itself, guarantee, promise or predict investment results. No graph or formula can

determine what securities should be bought or sold or when to buy or sell them, nor can it assist someone in making a

decision regarding security purchases or timing decisions. The data and information contained in this presentation is for

informational and illustrative purposes only. This material should not be viewed as a current or past recommendation or a

solicitation of an offer to buy or sell any securities or investment products or to adopt any investment strategy.

Investing entails risks, including possible loss of principal. Past performance is no guarantee of future results.

The use of leverage involves substantial risk. The more leverage that is employed by a market participant, the more likely a

substantial change will occur, either up or down, in the value of such market participant’s portfolio. The use of leverage to

acquire positions will subject a market participant to major losses in the event that market disruptions destroy the hedged

nature of such positions. 48