california geothermal forum · california geothermal forum “a path to increasing geothermal...

TRANSCRIPT

California Geothermal Forum

“A path to Increasing Geothermal Development in California”

October 20, 2016

Berkshire Hathaway Energy Overview• 11.5 million customers

worldwide

• 21,000 employees worldwide

• $85.0 billion of assets

• $18.1 billion of revenue

• 32,600 miles of transmission lines

• 16,400 miles of natural ,gas pipeline

• More than 34,000 MW of owned and contracted generationcontracted generation capacity

• 34% renewableor non-carbon

22

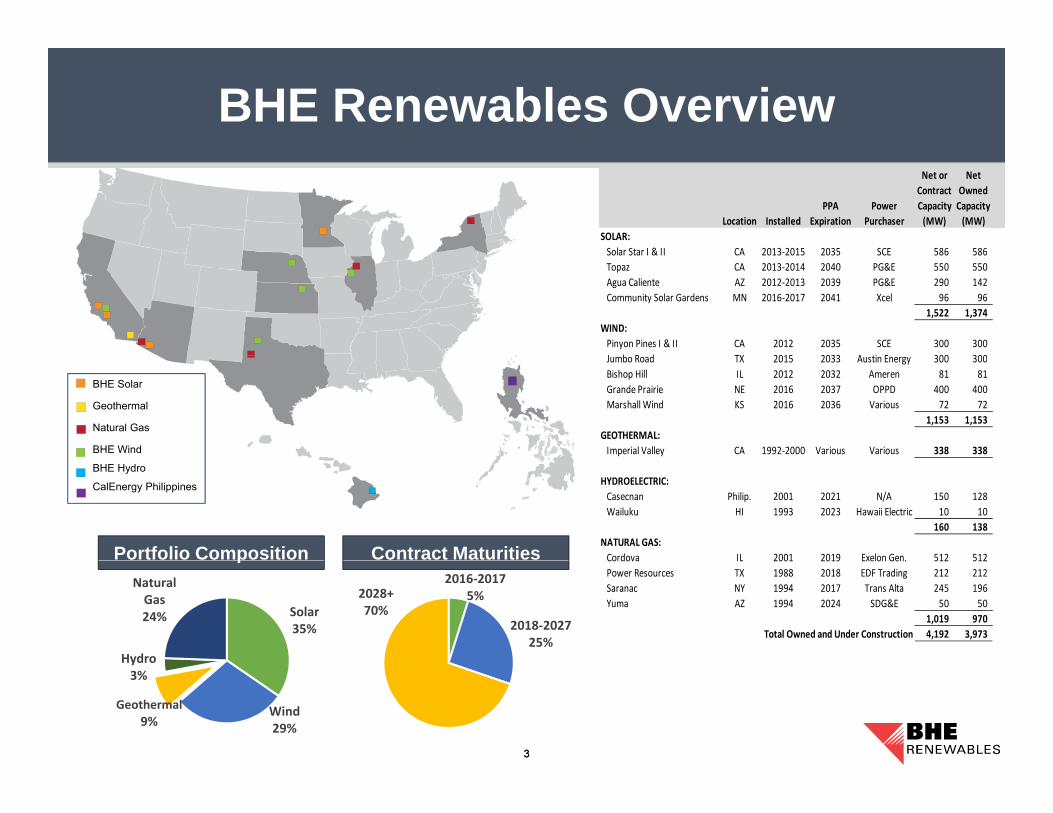

BHE Renewables OverviewNet or NetContract Owned

PPA Power Capacity CapacityLocation Installed Expiration Purchaser (MW) (MW)

SOLAR:Solar Star I & II CA 2013‐2015 2035 SCE 586 586 Solar Star I & II CA 2013 2015 2035 SCE 586 586

Topaz CA 2013‐2014 2040 PG&E 550 550 Agua Caliente AZ 2012‐2013 2039 PG&E 290 142 Community Solar Gardens MN 2016‐2017 2041 Xcel 96 96

1,522 1,374 WIND: Pinyon Pines I & II CA 2012 2035 SCE 300 300 J b R d TX 2015 2033 A i E 300 300

BHE Solar

Geothermal

Natural Gas

BHE Wind

Jumbo Road TX 2015 2033 Austin Energy 300 300 Bishop Hill IL 2012 2032 Ameren 81 81 Grande Prairie NE 2016 2037 OPPD 400 400 Marshall Wind KS 2016 2036 Various 72 72

1,153 1,153 GEOTHERMAL: Imperial Valley CA 1992‐2000 Various Various 338 338

Portfolio Composition Contract Maturities

BHE Hydro

CalEnergy Philippines HYDROELECTRIC: Casecnan Philip. 2001 2021 N/A 150 128 Wailuku HI 1993 2023 Hawaii Electric 10 10

160 138 NATURAL GAS:Cordova IL 2001 2019 Exelon Gen. 512 512p

2016‐20175%

2018‐202725%

2028+70%Solar

35%

Hydro

Natural Gas24%

Cordova IL 2001 2019 Exelon Gen. 512 512 Power Resources TX 1988 2018 EDF Trading 212 212 Saranac NY 1994 2017 Trans Alta 245 196 Yuma AZ 1994 2024 SDG&E 50 50

1,019 970 Total Owned and Under Construction 4,192 3,973

Wind29%

Geothermal9%

y3%

33

History of CalEnergy

Ownership History

1980s Two Competing Businesses - Unocal & Magma

Development Timeline

1993 Magma Purchases Unocal’s Interest

1995 CalEnergy Purchases Magma’s Interest

1999 MEHC* & El Paso Energy 50/50 Ownership1999 MEHC & El Paso Energy 50/50 Ownership

2003 MEHC* & TransAlta 50/50 Ownership

2014 Berkshire Hathaway Energy 100% Ownership * MEHC – MidAmerican Energy Holding Company

Capacity Brine ProcessingPlant Start-Up MW Technology Unit 1 1982 10 pH-Mod/CRC*Vulcan 1986 38 pH-Mod/CRC*Hoch 1989 42 pH Mod/CRC*

gy g p y

Hoch 1989 42 pH-Mod/CRCElmore 1989 42 CRCUnit 3 1989 50 pH-Mod/CRC*Unit 2 1990 18 pH-Mod/CRC*Leathers 1990 42 CRCUnit 4 1996 44 pH-Mod/CRC*

4

Unit 5 2000 46 pH-Mod/CRC*Turbo-expander 2000 10 pH-Mod/CRC* Total 342

* Combination of patented CrystallizerCrystallizer, Reactor, Clarifier andpH-Modification technology

4

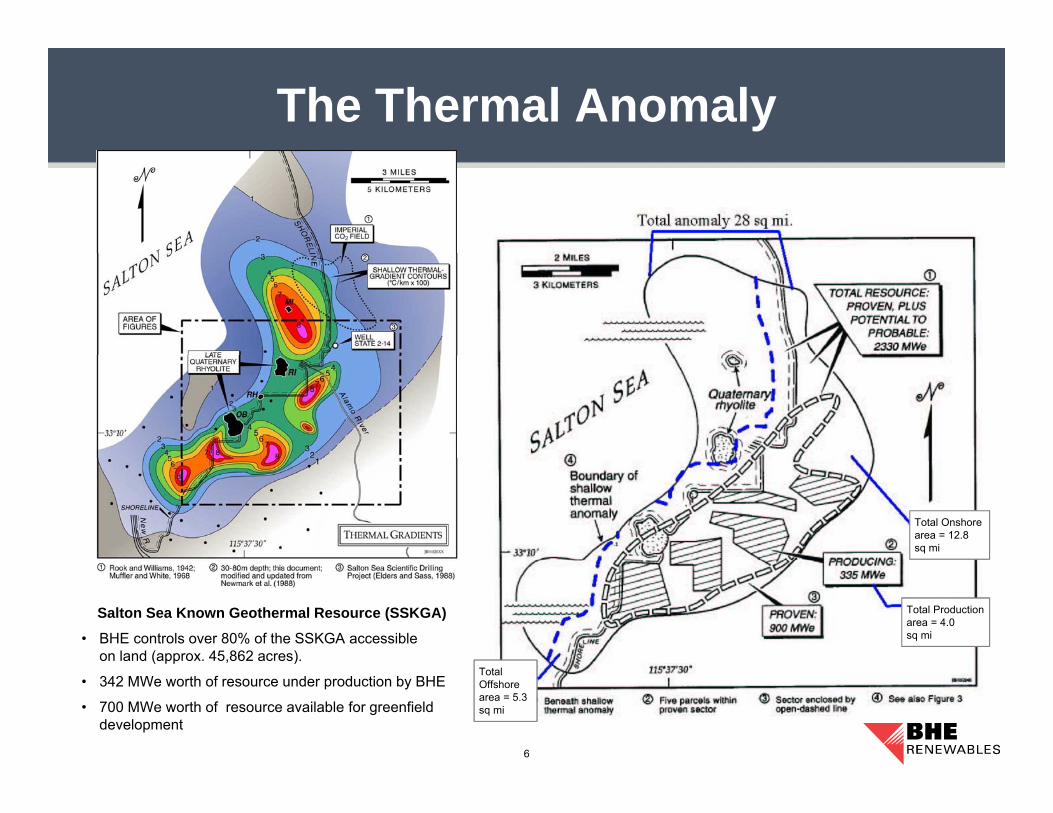

Southern end of Salton Sea

5

The Thermal Anomaly

Total Onshore area = 12.8 sq mi

Total Production area = 4.0 sq mi

Salton Sea Known Geothermal Resource (SSKGA)

• BHE controls over 80% of the SSKGA accessibleon land (approx. 45,862 acres).

Total Offshore area = 5.3 sq mi

6

( pp )

• 342 MWe worth of resource under production by BHE

• 700 MWe worth of resource available for greenfield development

BHE Production Units

Total Onshore area = 12.8 sq mi

Total Production area = 4.0 sq mi

Total Offshore area = 5.3 sq mi

Production Units Power Plants Capacity

Region 1 Unit S S Unit 1 10 MWRegion 1 Unit S.S. Unit 1 10 MWS.S. Unit 2 17 MWS.S. Unit 3 50 MWS.S. Unit 4 44 MWS.S. Unit 5 46 MW

Region 2 Unit Vulcan 38 MWHoch/Del Ranch 42 MW

7

Hoch/Del Ranch 42 MWCE Turbo 10 MW

Elmore Unit Elmore 42 MW

River Ranch Unit Leathers 42 MW(a.k.a. Leathers Unit)

Imperial Valley Geothermal

8

Elmore Facility and Red Hill Bay ̴ 2006

9

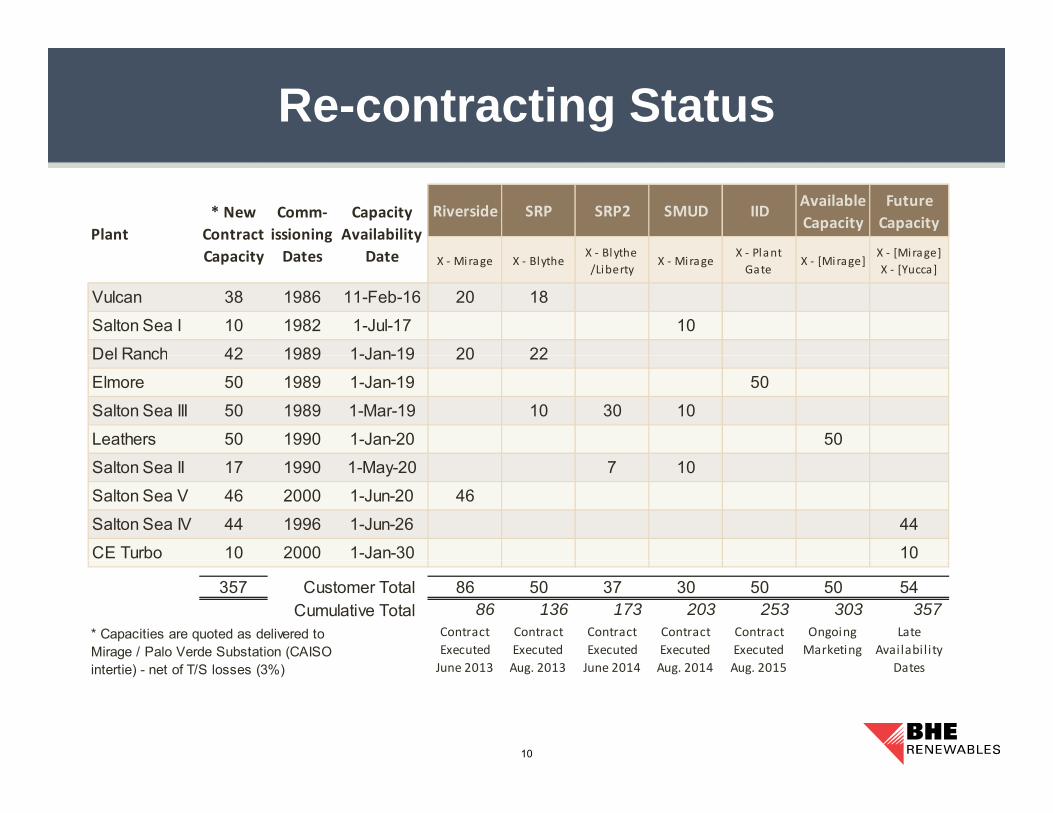

Re-contracting Status

Riverside SRP SRP2 SMUD IIDAvailableCapacity

FutureCapacity

X Blythe X Plant X [Mirage]

Capacity Availability

D tPlant

* New Contract C it

Comm‐issioningD t X ‐ Mirage X ‐ Blythe

X ‐ Blythe/Liberty

X ‐ MirageX ‐ Plant Gate

X ‐ [Mirage]X ‐ [Mirage]X ‐ [Yucca]

Vulcan 38 1986 11-Feb-16 20 18

Salton Sea I 10 1982 1-Jul-17 10

Del Ranch 42 1989 1-Jan-19 20 22

DateCapacity Dates

Del Ranch 42 1989 1-Jan-19 20 22

Elmore 50 1989 1-Jan-19 50

Salton Sea III 50 1989 1-Mar-19 10 30 10

Leathers 50 1990 1-Jan-20 50

Salton Sea II 17 1990 1-May-20 7 10

Salton Sea V 46 2000 1-Jun-20 46

Salton Sea IV 44 1996 1-Jun-26 44

CE Turbo 10 2000 1-Jan-30 10

357 Customer Total 86 50 37 30 50 50 54Cumulative Total 86 136 173 203 253 303 357

Contract Executed

20 3

Contract Executed

20 3

Contract Executed

20

Contract Executed

20

Contract Executed

20

Ongoing Marketing

Late Availability

* Capacities are quoted as delivered to Mirage / Palo Verde Substation (CAISO

10

June 2013 Aug. 2013 June 2014 Aug. 2014 Aug. 2015 Datesintertie) - net of T/S losses (3%)

Salton Sea Known Geothermal Resource Area (SSKGRA)( )

• Everything we do is with precipitating brines as our primary focusprimary focus

Or cause to happen suddenly or unexpectedly a change from a liquid to a solid

– And a picture is worth …….

11

Salton Sea Known Geothermal Resource Area (SSKGRA)( )

12

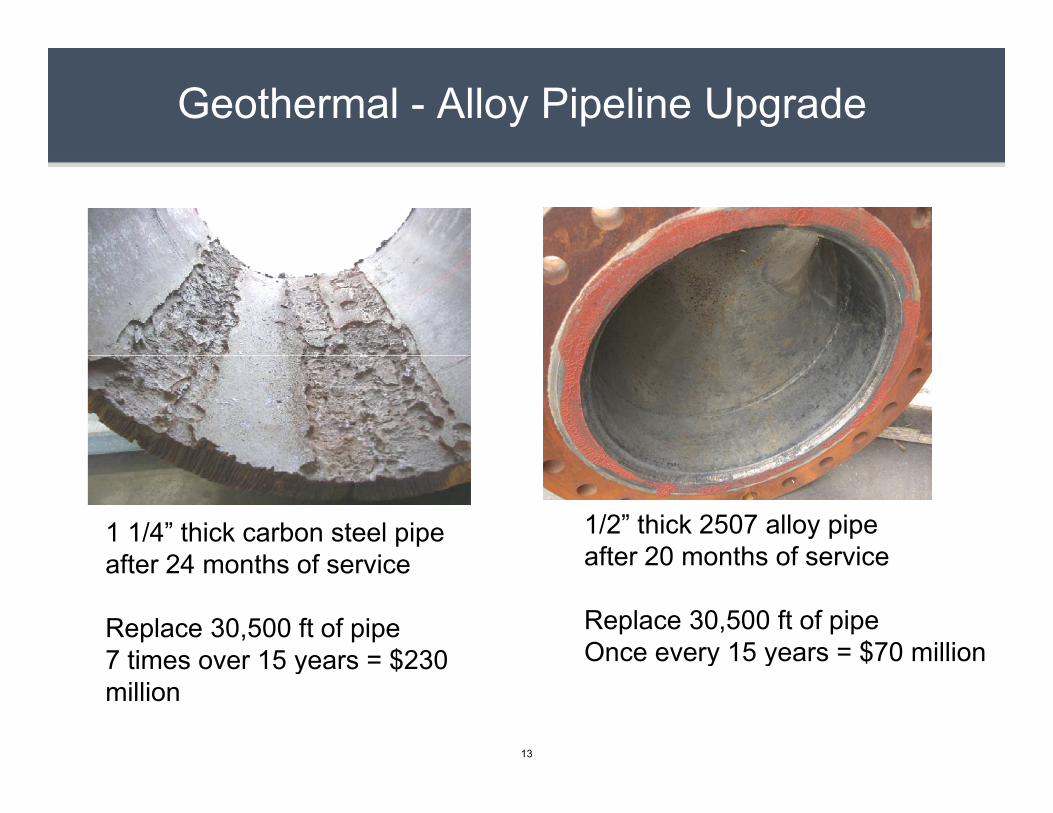

Geothermal - Alloy Pipeline Upgrade

1 1/4” thick carbon steel pipeafter 24 months of service

1/2” thick 2507 alloy pipeafter 20 months of serviceafter 24 months of service

Replace 30,500 ft of pipe7 times over 15 years = $230

after 20 months of service

Replace 30,500 ft of pipeOnce every 15 years = $70 million7 times over 15 years = $230

milliony y $

13

Flexibility or Load Following Geothermal Generation

• Operational Challenges at the SSKGRA

− Each time you change the temperature or flow of the brine you create scale or something falls out of solution To combat we use alloy piping in all conduit that has any possibility of To combat, we use alloy piping in all conduit that has any possibility of

contacting the brine. Approx. 35 miles at CalEnergy 10 times the cost of traditional carbon steel

− Each production well has the life expectancy of 25 thermal cycling events, whether one week or 20 years Cost of new production well, approx. $12 to $16m

14

Flexibility or Load Following Geothermal Generation (cont )Generation (cont.)

− Even a partial thermal cycle or restricting the flow of brine from a “steady state” will stress the entire well integritya steady state will stress the entire well integrity

The reservoir is under-pressured and the wells are not flowing artisan. The wells have to be induced to flow but once flowing, the g,production wells are free flowing. If the wells are shut in for a significant period of time, they lose the ability to flow. Starting a well to flow again requires days to reach temperatures.

Not keeping stable flow in injection and production pipelines casing static brine to sit in place. This leads to precipitation of scale in the pipelines

15

Flexibility or Load Following Geothermal Generation (cont.)Generation (cont.)

• Operational Challenges at the SSKGRA (cont.)

− Uninterrupted brine flow and temperature incorporating a “by passing” approach would create a negative environmental impactimpact To circumvent the production process and vent to atmosphere or “flow

thru” in lieu of abatement of H2S, CO2,benzene, and noise, would significantly violate permits.

− Geothermal brines contain significant concentrations of non-condensable gases, such as hydrogen sulfide, carbon dioxide,

d th lik S h ti l l h d lfid tand the like. Such gases, particularly hydrogen sulfide must be abated to comply with environmental restrictions. Abatement methods are very expensive

16

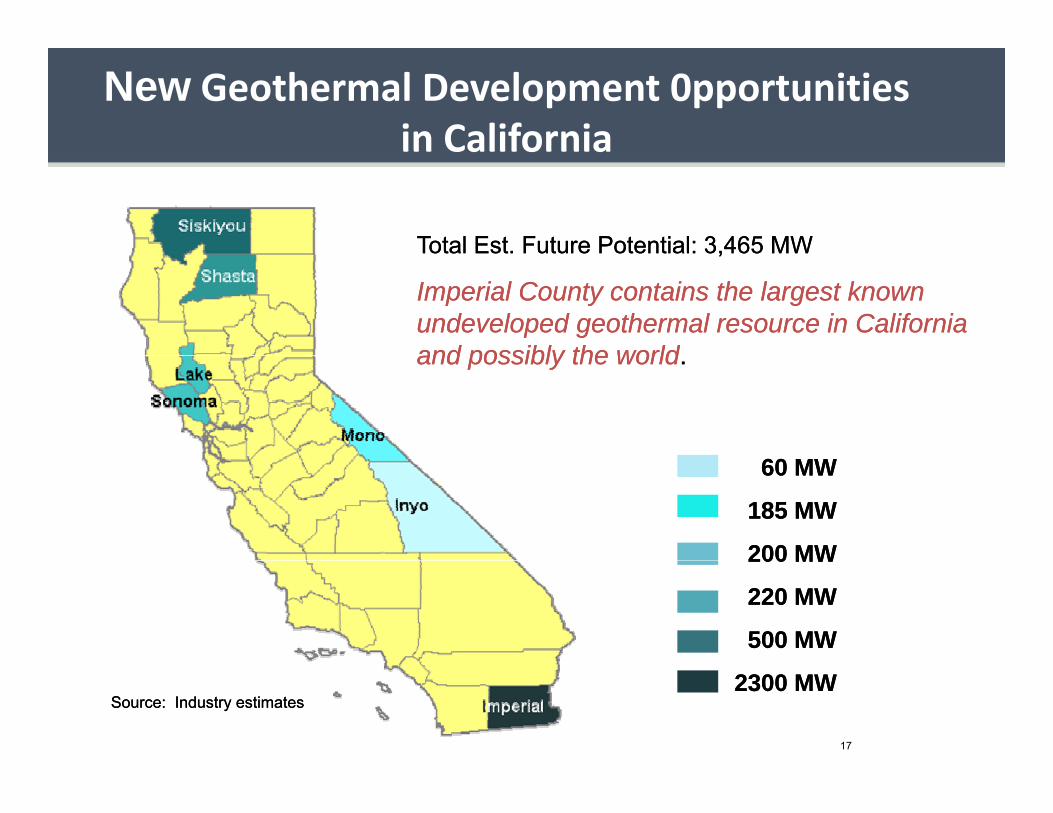

New Geothermal Development 0pportunities in Californiain California

Total Est. Future Potential:Total Est. Future Potential: 33,,465465 MWMWTotal Est. Future Potential: Total Est. Future Potential: 33,,465 465 MWMW

Imperial County contains the largest known Imperial County contains the largest known undeveloped geothermal resource in California undeveloped geothermal resource in California and possibly the worldand possibly the worldand possibly the worldand possibly the world..

60 60 MWMW

185 185 MWMW

200 MW200 MW200 MW200 MW

220 MW220 MW

500 MW500 MW

2300 2300 MWMWSource: Industry estimatesSource: Industry estimates

17

BHE Future Development Resources

Future Black Rock Development

- Approximately 700 MW of fi ld d l t t ti l

18

greenfield development potential

- 159 MW fully permitted

- Subsurface leases held without production until 2025

Black Rock 1 Black Rock 1 -- 3 and 4 3 and 4 -- 66

BR 4-6BR 4-6

LeathersElmore

HochAdminBR 1-3

19

Vulcan

“Shovel Ready” BR 1-3 Project

• CalEnergy’s Black Rock 1-3 project is immediate or gy p j“shovel ready” for construction− 159 MW project currently licensed by the CEC, (amend to 235

MW)MW)− Proven Resource and site control is in place− Construction financing completely attained = Cash− Valid generator interconnection agreement− Valid generator interconnection agreement − Existing transmission capacity available− Could be commercial in 36 to 48 months

Black Rock 4 6 lags 24 months− Black Rock 4-6 lags 24 months

20

Other Developers at the Salton Sea

• EnergySource– 49 9 MW operating plant – 201249.9 MW operating plant 2012– 85 MW Imperial Wells – development pipeline

• Controlled Thermal Resources– 250 MW Hell’s Kitchen – development pipeline

21

So what’s the problem?

MarketMarket• To expensive – Least Cost – Least Cost (Absent Best Fit)

• No Investor Owned Utility procured any meaningful Geothermal generation to reach 33% RPS

• Mostly Solar and a little Wind

• Geothermal is undervalued• Geothermal is undervalued

22

Main barriers preventing more geothermal generation g

• Material Integration with other renewable technologies g gthat recognize − Property tax exemption status− Federal incentives or subsidizesFederal incentives or subsidizes − Time of use pricing − Appropriate adder valuation of non renewable backstopping of

intermittent resourcesintermittent resources Including an adder caused by an increase of carbon

– Level the playing fieldLevel the playing field

23

Main barriers preventing more geothermal generation g

• Ancillary Values Integration Recognition y g g

– Geothermal plants provide the counties that they are sited in, generally with the highest revenue streams in the county

– Geothermal plants require between 5 and 19 time as many employees to operate compared to other intermittent resources

– Importing out-of-state generation provides zero benefit to the schools and communities of Californians

24

Main barriers preventing more geothermal generation g

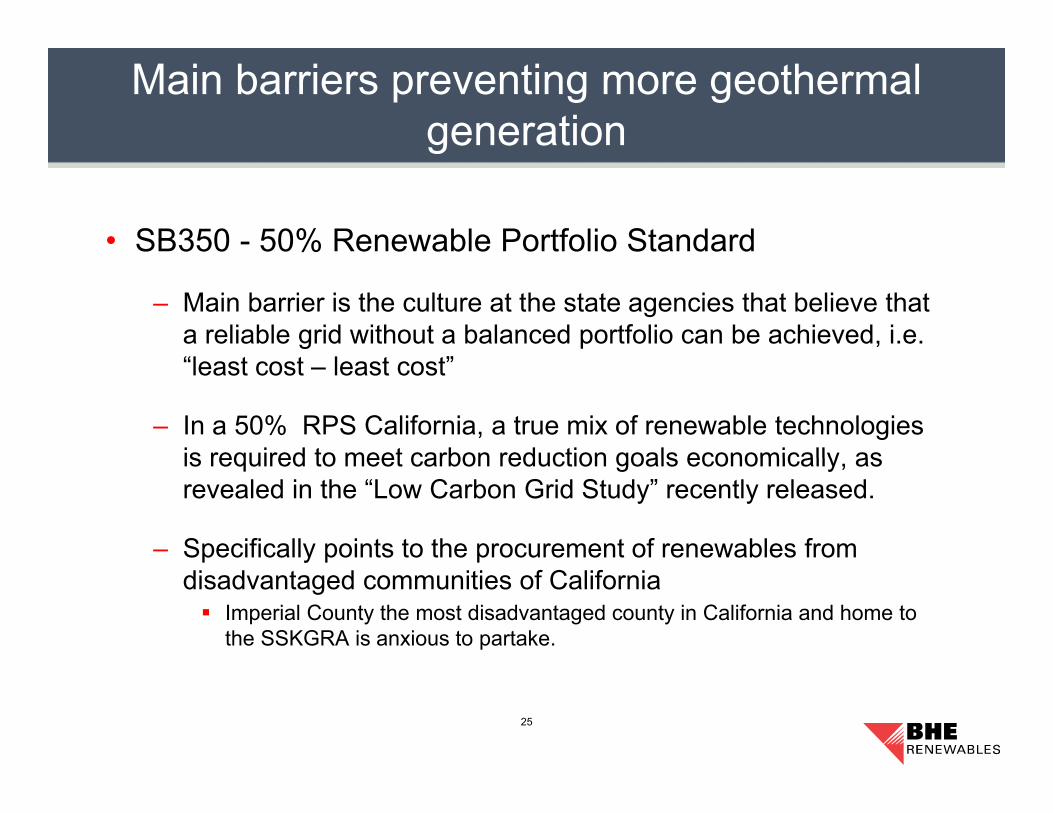

• SB350 - 50% Renewable Portfolio Standard

‒ Main barrier is the culture at the state agencies that believe that a reliable grid without a balanced portfolio can be achieved, i.e. “least cost – least cost”

‒ In a 50% RPS California, a true mix of renewable technologies is required to meet carbon reduction goals economically asis required to meet carbon reduction goals economically, as revealed in the “Low Carbon Grid Study” recently released.

‒ Specifically points to the procurement of renewables from p y p pdisadvantaged communities of California Imperial County the most disadvantaged county in California and home to

the SSKGRA is anxious to partake.

25

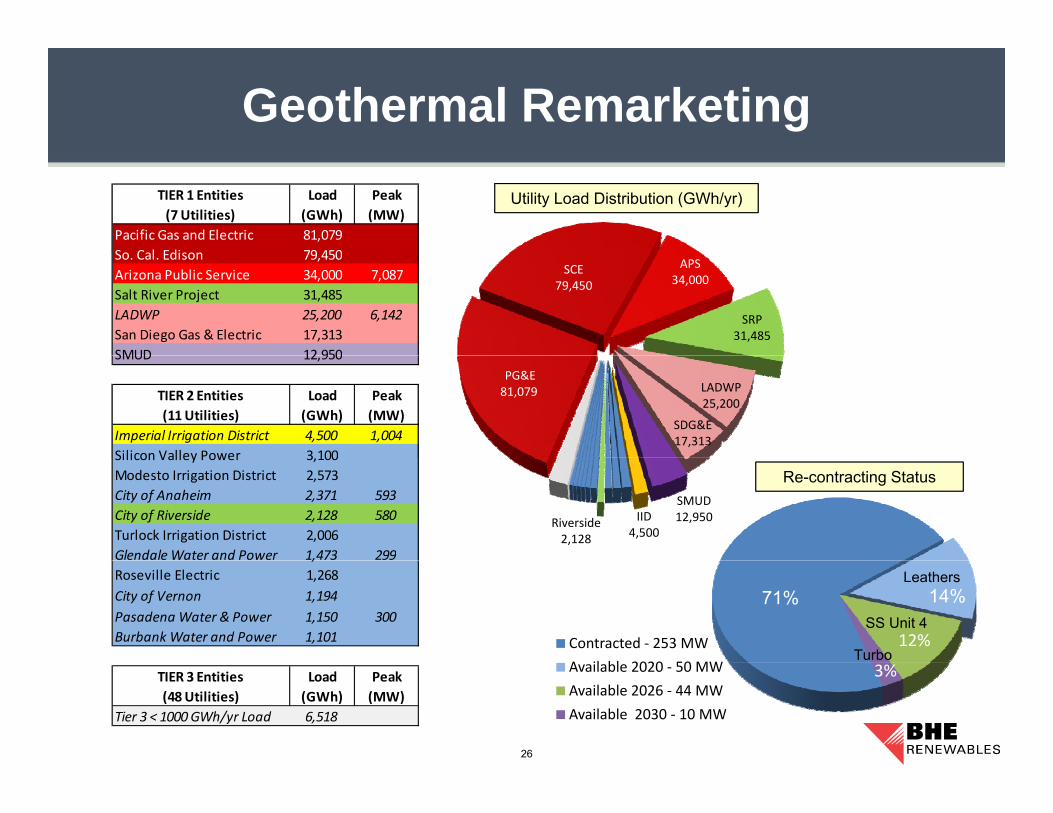

Geothermal RemarketingUtility Load Distribution (GWh/yr)

Pacific Gas and Electric 81,079So Cal Edison 79 450

TIER 1 Entities(7 Utilities)

Peak (MW)

Load(GWh)

SCE79,450

APS34,000

SRP31,485

So. Cal. Edison 79,450Arizona Public Service 34,000 7,087Salt River Project 31,485LADWP 25,200 6,142San Diego Gas & Electric 17,313SMUD 12 950

PG&E 81,079 LADWP

25,200

SDG&E17,313

SMUD 12,950

Imperial Irrigation District 4,500 1,004Silicon Valley Power 3 100

Load(GWh)

TIER 2 Entities(11 Utilities)

Peak (MW)

SMUD12,950IID

4,500Riverside2,128

Re-contracting StatusSilicon Valley Power 3,100Modesto Irrigation District 2,573City of Anaheim 2,371 593City of Riverside 2,128 580Turlock Irrigation District 2,006Glendale Water and Power 1,473 299

Contracted ‐ 253 MWA il bl 2020 50 MW

14%

12%

71%

,Roseville Electric 1,268City of Vernon 1,194Pasadena Water & Power 1,150 300Burbank Water and Power 1,101

Leathers

SS Unit 4

Turbo

26

Available 2020 ‐ 50 MWAvailable 2026 ‐ 44 MWAvailable 2030 ‐ 10 MW

3%

Tier 3 < 1000 GWh/yr Load 6,518

TIER 3 Entities(48 Utilities)

Load(GWh)

Peak (MW)