business valuation imec7 22-14-final

TRANSCRIPT

1

o What is My Business Worth?o The Valuation Process

o Asset Approach

o Income Approach

o Market Approach

o Maximize Your Valueo Manufacturing Specific

BUSINESS VALUATION

2

Question: What is my Business Worth?

• Answer: What do you mean by “business?”

o Hint: There is no right or wrong answer to this question!

www.hbcpas.com

3

What Do You Mean By “Business?”

• Does it include or exclude these assets?o Casho Receivableso Real Estateo A company caro Life insurance policies

• Does it include or exclude these liabilities?o Accounts payableo BANK DEBT

www.hbcpas.com

4

Are Buyer and Seller Talking About the Same Thing?

• Buyer and Seller can agree on a “price,” but that doesn’t mean they are on the same page!o #1 – Buyer wants to buy assets of the company for $7 milliono #2 – Seller wants to sell stock for $7 million (which includes $5 million

of bank debt)

• Both “prices” are $7 million, but the asset price is $7 million in #1 vs. $12 million in #2—That’s $5 million off (40%)!o Assets = Equity (Stock) + Liabilitieso Asset Price = Cash Paid for Stock + Liabilities Assumed o $7 million in stock + $5 million in bank debt = $12 million in assets

www.hbcpas.com

5

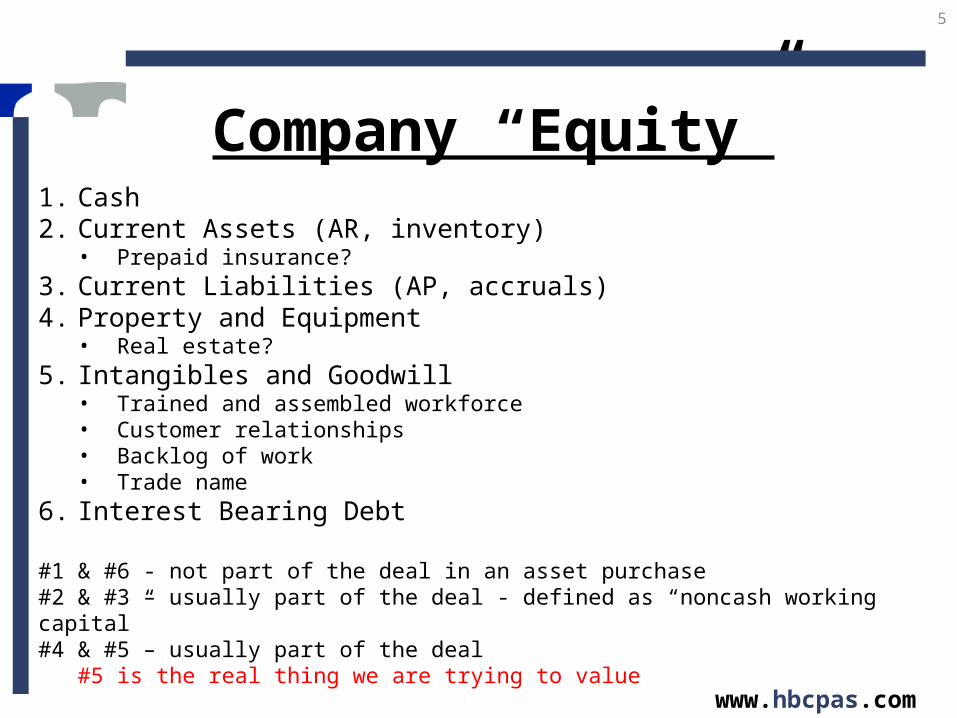

Company “Equity”1. Cash2. Current Assets (AR, inventory)

• Prepaid insurance?

3. Current Liabilities (AP, accruals)4. Property and Equipment

• Real estate?

5. Intangibles and Goodwill• Trained and assembled workforce• Customer relationships• Backlog of work• Trade name

6. Interest Bearing Debt

#1 & #6 - not part of the deal in an asset purchase#2 & #3 – usually part of the deal - defined as “noncash working capital”#4 & #5 – usually part of the deal

#5 is the real thing we are trying to value www.hbcpas.com

6

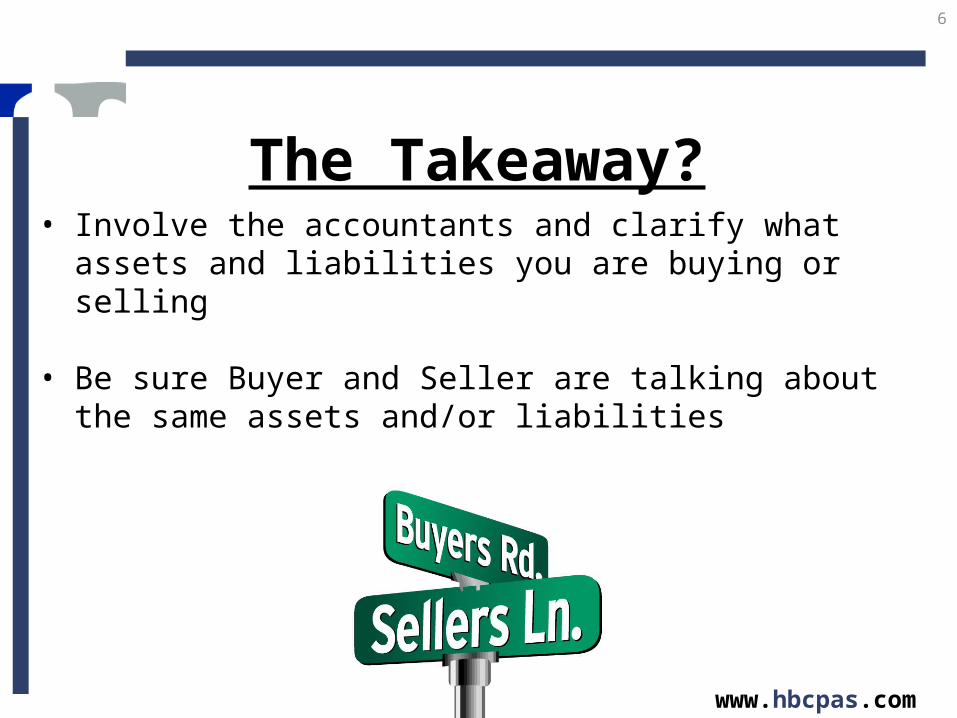

The Takeaway?• Involve the accountants and clarify what assets and liabilities

you are buying or selling

• Be sure Buyer and Seller are talking about the same assets and/or liabilities

www.hbcpas.com

7

What is a Business Valuation?• Giving an opinion as to the value of an ownership interest

(usually shares of stock) of a businesso Generally, all assets and liabilities of a company

(theoretical equity value)

• Fair Market Value – consider both sides – willing buyer and seller

www.hbcpas.com

8

The Business Valuation Process• Internal Company Information

• Economic and Industry Analysis

• Valuation Approacheso Asseto Incomeo Market

• Value Conclusion

www.hbcpas.com

9

The Business Valuation Process:Internal Company Information

• Review of past five years’ financials statements• Interviews with management• General investigation of major assets, liabilities and

business operations• Identifying strengths and weaknesses

www.hbcpas.com

10

The Business Valuation Process:Economic and Industry Analysis

• Primary purpose: Help quantify risks associated with the Company’s operations

• Identify key external factors (interest rates, inflation, competition, etc.) that may have a direct effect on the Company’s value

• Compare the Company to its industry (Benchmarking)

www.hbcpas.com

11

The Business Valuation Process:Valuation Approach – Asset

• Value the Company’s assets and liabilities at fair market value (FMV)

o Appraisals are usually obtained (real estate, equipment, etc.)o FMV of liabilities typically equals book value

• Evaluated as if the Company liquidated in an orderly fashion (Can set a floor for value)

• Not necessarily what Seller would realize in aftertax sale proceeds

www.hbcpas.com

12

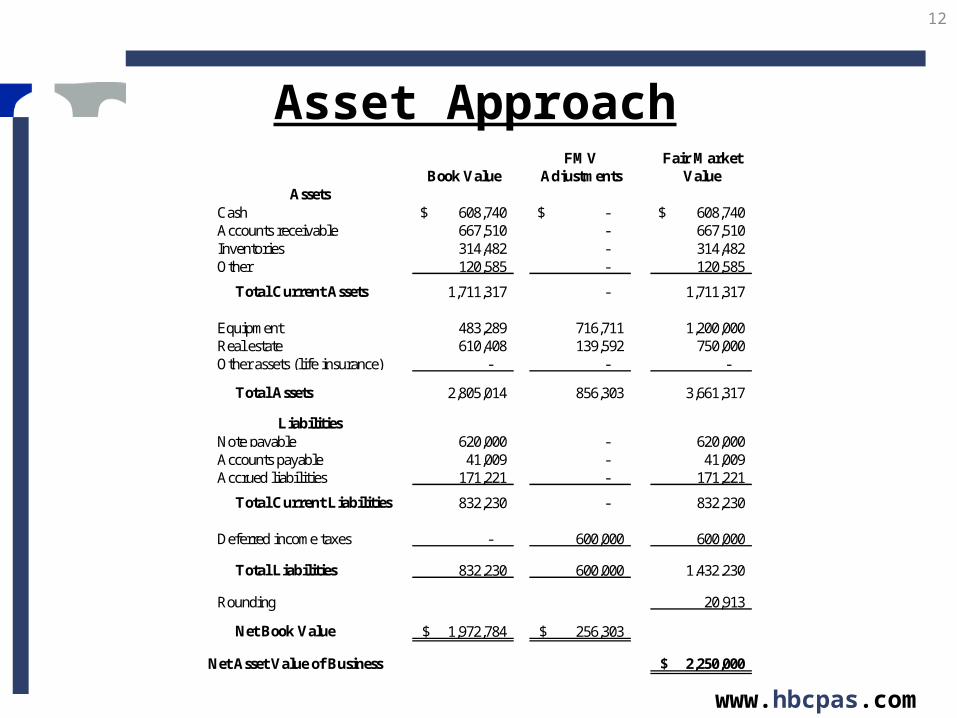

Asset Approach

www.hbcpas.com

FMV Fair MarketBook Value Adjustments Value

Cash 608,740$ -$ 608,740$ Accounts receivable 667,510 - 667,510 Inventories 314,482 - 314,482 Other 120,585 - 120,585

Total Current Assets 1,711,317 - 1,711,317

Equipment 483,289 716,711 1,200,000 Real estate 610,408 139,592 750,000 Other assets (life insurance) - - -

Total Assets 2,805,014 856,303 3,661,317

Note payable 620,000 - 620,000 Accounts payable 41,009 - 41,009 Accrued liabilities 171,221 - 171,221

Total Current Liabilities 832,230 - 832,230

Deferred income taxes - 600,000 600,000

Total Liabilities 832,230 600,000 1,432,230

Rounding 20,913

Net Book Value 1,972,784$ 256,303$

Net Asset Value of Business 2,250,000$

Liabilities

Assets

13

The Business Valuation Process:Valuation Approach – Income

• Value today = future cash flow discounted at the opportunity cost of capital

• Economic vs. Accounting Income: Normalization Adjustments

o Officer’s salaryo Rento Charitable contributionso Extraordinary items

www.hbcpas.com

14

Income Approach • Just because profits are reported correctly in

accordance with accounting standards does not indicate it reflects economic reality

• If I am a buyer, what cash flow will be available for me to pay back the debt incurred on the purchase?

• Future cash flow is discounted back to the present at a determined discount rate• Discount rate reflects the risk of the future cash flow

• Example: Picking up a quarter that is two feet away from you vs. a $100 bill that is across a busy city street. Risk! www.hbcpas.com

15

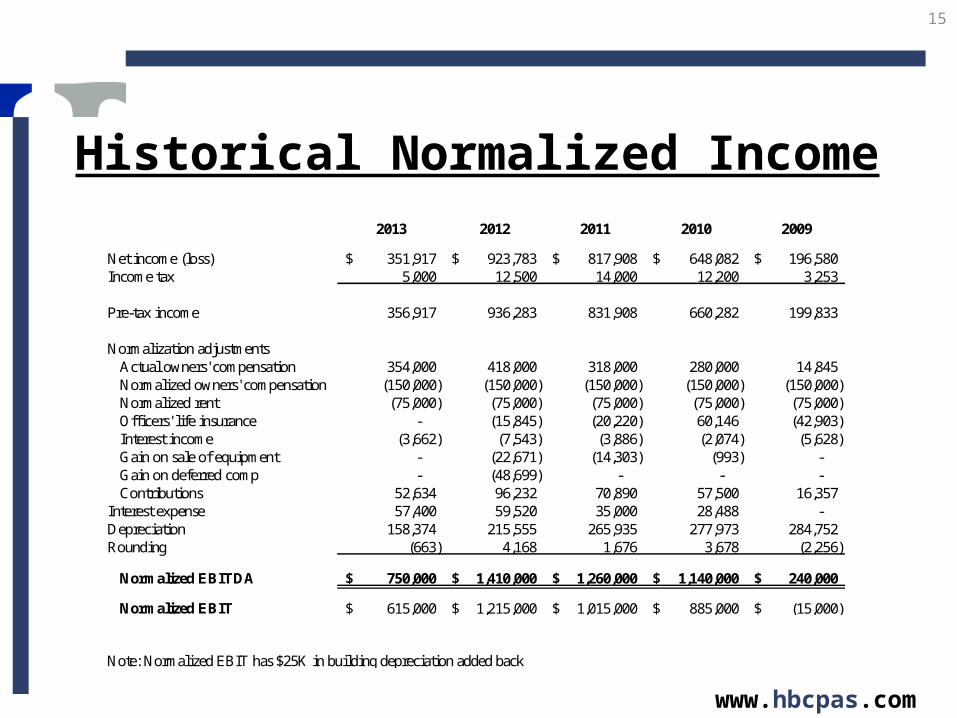

Historical Normalized Income

www.hbcpas.com

2013 2012 2011 2010 2009

Net income (loss) 351,917$ 923,783$ 817,908$ 648,082$ 196,580$ Income tax 5,000 12,500 14,000 12,200 3,253

Pre-tax income 356,917 936,283 831,908 660,282 199,833

Normalization adjustmentsActual owners' compensation 354,000 418,000 318,000 280,000 14,845 Normalized owners' compensation (150,000) (150,000) (150,000) (150,000) (150,000) Normalized rent (75,000) (75,000) (75,000) (75,000) (75,000) Officers' life insurance - (15,845) (20,220) 60,146 (42,903) Interest income (3,662) (7,543) (3,886) (2,074) (5,628) Gain on sale of equipment - (22,671) (14,303) (993) - Gain on deferred comp - (48,699) - - - Contributions 52,634 96,232 70,890 57,500 16,357

Interest expense 57,400 59,520 35,000 28,488 - Depreciation 158,374 215,555 265,935 277,973 284,752 Rounding (663) 4,168 1,676 3,678 (2,256)

Normalized EBITDA 750,000$ 1,410,000$ 1,260,000$ 1,140,000$ 240,000$

Normalized EBIT 615,000$ 1,215,000$ 1,015,000$ 885,000$ (15,000)$

Note: Normalized EBIT has $25K in building depreciation added back

16

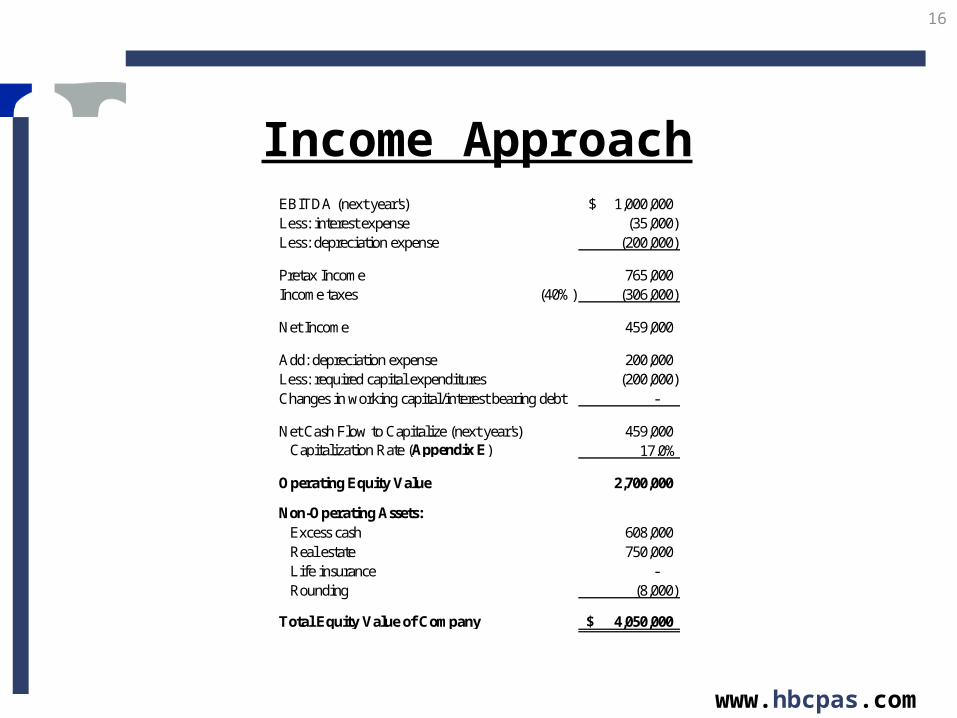

Income Approach

www.hbcpas.com

EBITDA (next year's) 1,000,000$ Less: interest expense (35,000) Less: depreciation expense (200,000)

Pretax Income 765,000 Income taxes (40%) (306,000)

Net Income 459,000

Add: depreciation expense 200,000 Less: required capital expenditures (200,000) Changes in working capital/interest bearing debt -

Net Cash Flow to Capitalize (next year's) 459,000 Capitalization Rate (Appendix E) 17.0%

Operating Equity Value 2,700,000

Non-Operating Assets: Excess cash 608,000 Real estate 750,000 Life insurance - Rounding (8,000)

Total Equity Value of Company 4,050,000$

17

The Business Valuation Process:Valuation Approach – Market

• The stock market can provide objective evidence of value

• Search for similar companies and determine valuation multiples

• Common Multiples:o Revenueso Net income – aka “P/E multiple”o EBITDA (Earnings before Interest, Taxes, Depreciation and Amortization)o EBIT

www.hbcpas.com

18

Market Approach • Private broker reporting databases of nonpublic

companies

• Difficult to see how truly comparable they are – but can prove useful in certain industries

• Key is to know what is included in the “price” reported by the broker (possibility of errors)

www.hbcpas.com

19

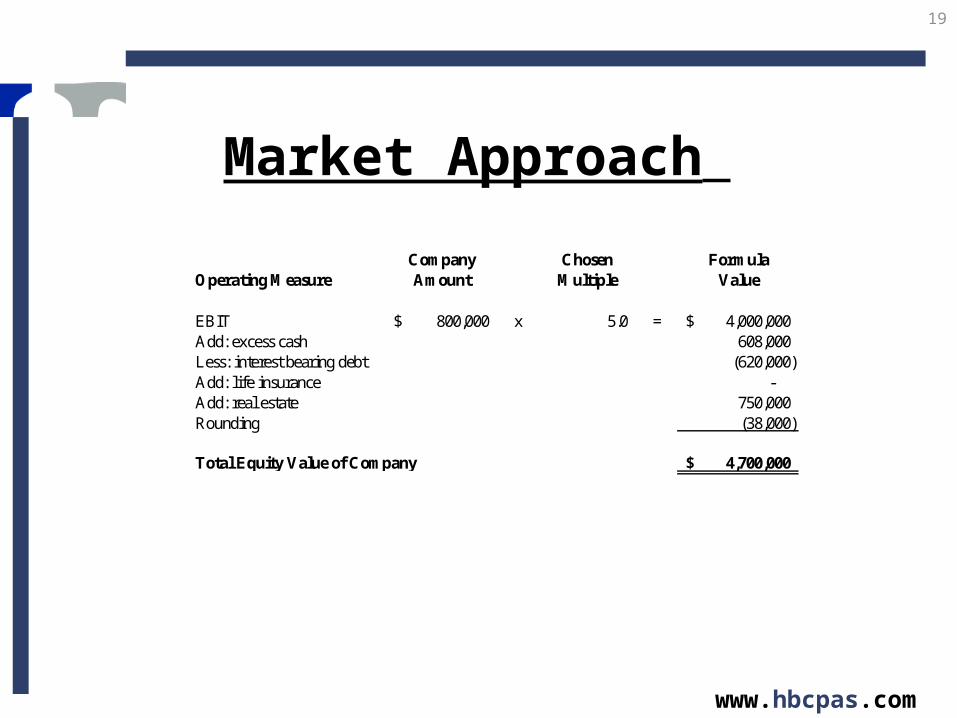

Market Approach

www.hbcpas.com

Company Chosen FormulaOperating Measure Amount Multiple Value

EBIT 800,000$ x 5.0 = 4,000,000$ Add: excess cash 608,000 Less: interest bearing debt (620,000) Add: life insurance - Add: real estate 750,000 Rounding (38,000)

Total Equity Value of Company 4,700,000$

20

The Business Valuation Process:Value Conclusion

• Reconcile the different approaches

• Sanity checks/Rules of thumb

• Decide on value

www.hbcpas.com

21

Value Conclusion

www.hbcpas.com

Weighted

Method Equity Value Weighting Value

Asset Approach 2,250,000$ 0% -$ Income Approach 4,050,000 75% 3,037,500$ Market Approach 4,700,000 25% 1,175,000

100% 4,212,500 Rounding (12,500)

Total Equity Value 4,200,000$

22

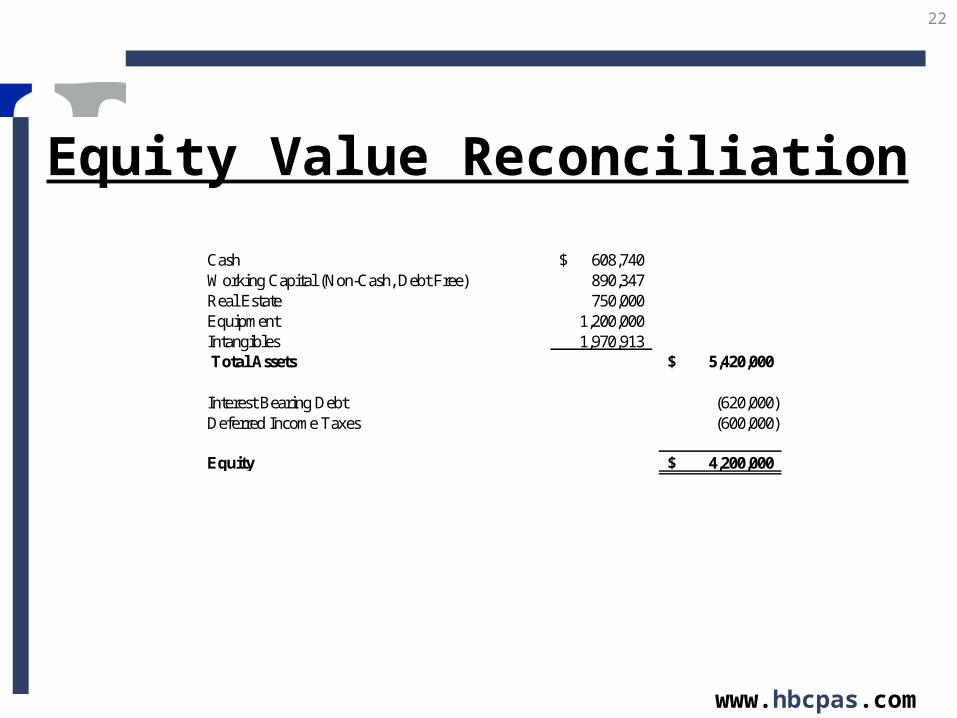

Equity Value Reconciliation

www.hbcpas.com

Cash 608,740$ Working Capital (Non-Cash, Debt Free) 890,347 Real Estate 750,000 Equipment 1,200,000 Intangibles 1,970,913 Total Assets 5,420,000$

Interest Bearing Debt (620,000) Deferred Income Taxes (600,000)

Equity 4,200,000$

23

Maximize Your Business Value• Clean up as much personal expenses as you can

o Be sure you are running it like a business

• Look to sell or distribute non-operating assets (considering income tax ramifications). Excess cash – not protected from creditors/lawsuits.

• Know/Tell your storyo Why would a buyer be interested in you? Processes/structure has

value.o Have good answers to tough questions (customer concentration).

• All key management positions filled by someone other than the owner. Succession plan in place.

www.hbcpas.com

24

Working Capital• Working capital is critically important in the operation of a

business and often implicit in determining a company’s value

• Example: 2 businesses are both generating $500,000 in net profit in the manufacturing industry• Company A needs $1 million of noncash working capital to operate• Company B needs $1.5 million of noncash working capital to operate• Why would this be?• Which Company is more attractive?

www.hbcpas.com

25

Working Capital• Manage your business to minimize your investment in these

noncash assetso Ultimately, this may increase your sales price

• KEY POINT: If you can show your business needs less cash to operate, Buyer will be willing to pay you more

www.hbcpas.com

26

Manufacturing• Generally higher multiples observed vs. other industries• How capital intensive is your business? Future capital

expenditures needed to support future projections.• Working capital

• AR – customer payment terms. The shorter the payment period, the less cash tied up in the business and the higher the return on assets.

• Inventory – inventory turnover.

• Real estate – does it have separate value from business?• Proprietary products with dealer or customer network vs.

something closer to a job shop which work is rebid every few years

• Production capabilitieswww.hbcpas.com

27

Manufacturing Multiples: Manufacturing vs. Other Industries

www.hbcpas.com

28

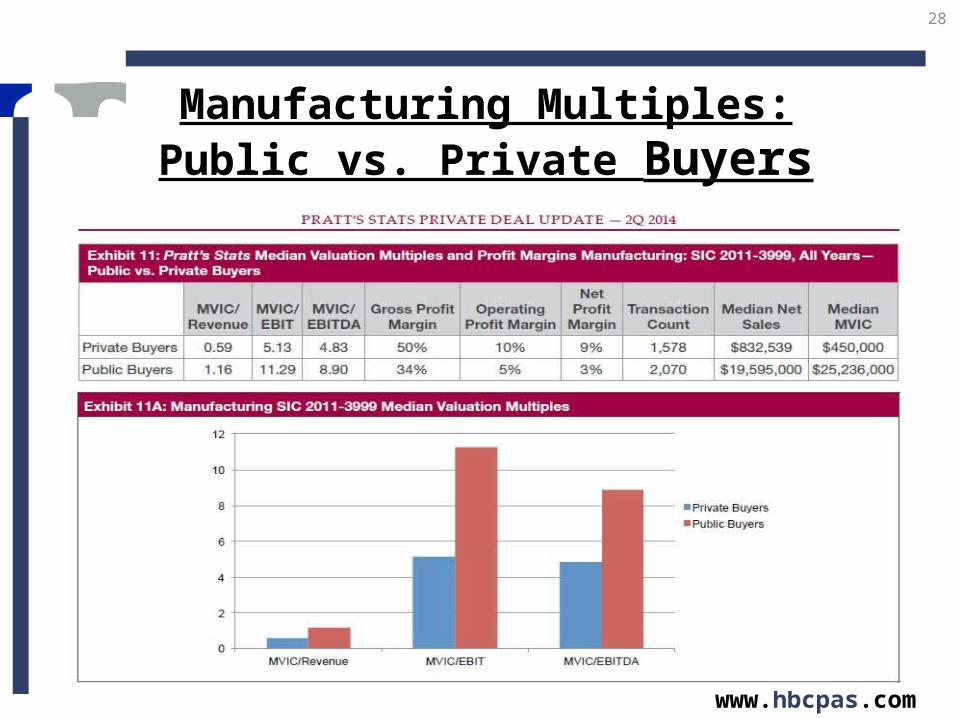

Manufacturing Multiples: Public vs. Private Buyers

www.hbcpas.com

29

Questions?

Glen E. BirnbaumCPA, CVA, ABV, AM

www.hbcpas.com309·694·4251