business intelligence & analytics cost accounting: a ... · business intelligence &...

TRANSCRIPT

Business Intelligence & Analytics Cost Accounting:

A Survey on the Perceptions of Stakeholders

Raphael Grytz

Paderborn University

Artus Krohn-Grimberghe

Paderborn University

Abstract

As data driven decision-making using business

intelligence and analytics (BI&A) becomes standard

in companies, the importance of mitigating the

accompanying growth in costs increases. Research

shows that increasing transparency to the granularity

of individual BI&A artefacts such as reports or

analytic applications is a necessary means, but in

practice the introduction of said systems is

cumbersome and adoption is slow. We address the

status quo of BI&A cost accounting for three types of

stakeholders: users, developers and managers. The

results show in which areas of application a strong

need for action exists and we identify major challenges

for further research are ahead. Our findings indicate

for example that managers at the same time regard

cost accounting for BI&A with a higher potential

benefit while they also believe they have already

established a higher degree of implementation in their

enterprises compared to the other stakeholder types.

We conclude that BI&A professionals have to consider

these different perceptions to run a successful

department and gain traction for BI&A cost

accounting.

1. Introduction

To compete successfully in the marketplace, it is

becoming increasingly important for an enterprise to

utilize the full potential of data-driven decision

support that Business Intelligence & Analytics

(BI&A) promises [24]. Chen et al. [5] define BI&A as

“the techniques, technologies, systems, practices,

methodologies, and applications that analyze critical

Business data to help an enterprise better understand

its business and market and make the timely decisions

it needs”. In most enterprises, an internal department

for BI&A, which in most cases is organized as a BI

Competency Center (BICC) [23], provides this

information through a company-specific BI&A

architecture and organization. Today, the benefits of

BI&A are undisputed and it has reached most

enterprises.

While current discussions in the field of BI&A are

dominated by potential benefits of big data [1, 19], the

costs of establishing and maintaining BI&A systems

are often overlooked. Due to complex architectures

[17], in addition to the high speed of innovation in

technology and methods [5], the costs of BI&A have

recently increased. The costs associated with such

systems need to be transparent to management to

allow for correct business decision-making [24]. This

is especially important during times of increased

global competition [12, 22].

We believe, this lack of cost transparency is a

significant driver for increasing BI&A costs. If

customers are not paying for BI&A resources, then

they have no interest in saving money for the

company. To increase consciousness, customers have

to pay the cost for services they demand. Payment

must then be charged without this billing

disproportionate costs. Besides being cheap and

efficient, such an accounting system is fair inasmuch

as service consumers have to pay for the costs they

cause [14]. Additionally, without such a system,

outlay cannot be priced reliably; this is true for the

company’s entire BI&A investments as well as

individual applications within the BI&A department.

Although companies are looking for new outsourcing

opportunities, e.g. delivering BI&A as a service [2,

15], without cost transparency any outsourcing

decisions with respect to specific parts of a BI&A

landscape cannot be evaluated. Furthermore, it is

difficult to locate potential for improving efficiency

and productivity, for planning the use of resources,

and for justifying it to management. With improved

cost transparency, a BI&A department can locate cost

savings and cost drivers.

The necessary cost transparency can be provided

by a BI&A cost accounting system. Such a system can

be used as a managerial instrument which delivers

information about value streams and for planning,

controlling and monitoring all tasks in the BI&A

organization [16, 20] in a fast, efficient, and data-

Proceedings of the 51st Hawaii International Conference on System Sciences | 2018

URI: http://hdl.handle.net/10125/49982ISBN: 978-0-9981331-1-9(CC BY-NC-ND 4.0)

Page 750

driven way. Current research on BI&A cost

accounting regarding management objectives and

design principles [10] shows the importance of this

topic on a managerial level as well as first realistic

implementation guidelines [14].

With an appropriate cost accounting system, it will

also become possible to calculate costs for both

individual BI&A artefacts and entire BI&A projects.

In addition, with the ability to calculate BI&A

applications, incoming BI&A demands could be

prioritized according to their expected benefit (value).

This would improve the efficiency (cost-benefit

perspective) of the whole BI&A department and

increase the productivity of BI&A resources. Aside

from the possibility of allowing make-or-buy

decisions or cost benchmarks to be made, improved

cost transparency would come one step closer to

performing a profitability analysis.

Even with the recent proposals, especially the one

from [14] becoming more feasible both from an

implementation and a consumption view, the

introduction of a BI&A related cost accounting in the

enterprise often fails or is not seen to be successful.

One of the reasons for less success in practice could be

the divergent perceptions of stakeholders regarding

information systems (IS) [28]. In particular, this is true

of the success of analytic information systems where

the perception of different stakeholders is identified as

a significant characteristic [27]. Yet there is not

sufficient study of whether, and to what extent, the

perceptions of stakeholders related to BI&A cost

accounting reveal differences regarding and negative

influence on the introduction of such a system.

Therefore, the core question of this paper is this: Are

there different perceptions of stakeholders affected

which could influence the success of a cost accounting

initiative for BI&A and, if so, how can these divergent

perceptions be identified? To close this research gap,

we carry out a descriptive-explorative survey in order

to collect required data and permit further analysis.

More precisely, we aim to examine the issue by

developing sensitivity for the different subjective

assessments of the potential benefits, the degree of

implementation, and the implementation challenges

regarding a BI&A cost accounting. We see our results

being used to assist BI&A professionals planning to

introduce cost accounting approaches for BI&A in

companies.

Our main contributions are:

• Divergent perceptions among users, developers,

and managers. Our findings confirm that there are

indeed substantial differences in the perception of

BI&A cost accounting and the implementation of

such systems among the three major stakeholder

groups (users, developers, managers) included in

the survey.

• Identification of the differences in perception for

single stakeholder groups. We note that

stakeholders have different priorities and

potentials regarding a BI&A cost accounting

system. For example users assessed the potential

benefit for continuous cancellation management

by cost evaluation as low. By contrast, developers

predict less potential benefit from outsourcing

opportunities, whereas managers assessed the

highest potential benefit for justification towards

management. If these different perceptions are not

considered during the planning process, the

introduction of the BI&A cost accounting system

is endangered.

• Selling the BI&A cost accounting to the

enterprise. The differences we found among the

stakeholder groups stipulate that selling the idea

of BI&A cost accounting works best when

building on the intrinsic motivation of the

managers while leveraging the more positive

attitude of the developers and users.

• Higher acceptance of BI&A cost accounting and

project success. We offer a definition and way of

prioritizing the needs for action and challenges

resulting from the implementation of a BI&A cost

accounting system. Proper prioritization aligned

with user needs helps increase acceptance and

thus project success.

• High potential among all stakeholder groups.

Last but not least, we can confirm that all

stakeholder groups see a high potential in the

establishment of a BI&A cost accounting system.

This also highlights the necessity of action to

implement a BI&A cost accounting system in

order to improve the cost transparency in BI&A

departments among the organizations surveyed.

With this research, we contribute to implementing

cost accounting for BI&A in companies and create a

foundation for further research to this topic.

The rest of this paper is organized as follows.

Section 2 describes the conceptual foundations for this

paper. In chapter 2.1, we present the current research

on BI&A cost accounting. The influence of the

stakeholder perspective on IS in general and BI&A in

particular will be dealt with in Section 2.2. Our

research concept is described in Section 3, above all

the research method used and a statistical description

of our sample. Section 4 holds the presentation of our

analysis and discussion of findings. The last section

concludes with an explanation of the limitations and

gives an outlook on future work.

Page 751

2. Conceptual foundation

In this section, we give a brief overview of the

current research on BI&A cost accounting.

Furthermore, we present relevant knowledge about the

influence of stakeholder perspectives on IS and BI&A

success.

2.1. A brief overview of the current research

on BI&A cost accounting

At present, increasing demands for BI&A continue

to challenge existing BI&A landscapes in companies.

From IS literature, it is clear that architectures,

organizations, and technologies must be adapted [19];

this, however, often results in an increase in costs. In

our experience, BI&A departments are under rising

cost pressure and must demonstrate efficiency,

productivity, and cost optimization on a day-by-day

basis. Consequently, these departments are forced to

try and justify a monolithic BI&A cost block to

management. Cost allocation systems to mitigate this

problem are identified in the literature [11, 18, 26].

However, usually few details are given: there are some

frameworks for summing up the total cost of BI&A

technology landscapes in companies e. g. by return on

investment (ROI) level [22, 30]; there are also some

other approaches proposing cost estimation based on

resource consumption [4, 21]. The paper by Brandl et

al. [4] introduces a method aimed at determining

usage-based cost allocation keys for customer-

oriented services based on their estimated resource

consumption. This can be achieved if every user

request is tracked across systems using a unique user

ID, resulting in detailed monitoring and metering of

users’ resource consumption. This approach only deals

about allocation keys without proposing a whole cost

accounting related to BI&A. Klesse [21] focuses on a

method of carrying out cost allocation for data

warehouse competency centers (DWH CC). Products

and services of the DWH CC are modeled as so-called

information products; for a modeled information

product, platform and process services must be

assigned in detail. Due to the fact that the resulting cost

accounting system is based on the information product

model, accounting can be carried out in a very detailed

fashion on the costs-by-cause principle, yet only for

the DWH layer.

What is missing is a detailed holistic BI&A cost

accounting approach. Seeing it from an IT perspective,

[3, 29] point out that IT costs allocation is necessary to

improve cost transparency and that this is a

challenging task with problems which remain

unresolved; this holds true for BI&A especially [14].

We concluded that, in literature to date, four principle

kinds of cost accounting for BI&A have been

discussed: 1. No allocation of costs is executed.

2. Costs are allocated using flat-rate distribution keys.

3. Costs are charged using a production-oriented

allocation base, e. g. CPU or memory utilization.

4. Costs are calculated using product-oriented

approaches which are too technical and overly detailed

in their current form. Although BI&A is driven by IT

[2, 5, 25], due to fundamental characteristics we

discussed in [14], such as developmental and

operational architecture, business domain, technical

and functional requirements, costs which appear for

BI&A must be treated differently when thinking about

a cost accounting. This makes it difficult to transfer

and apply existing cost accounting approaches to

BI&A.

Grytz and Krohn-Grimberghe created a BI&A

service-oriented cost allocation (BIASOCA) [14]

which quantifies and subsequently breaks down the

cost pool generated by BI&A in an understandable and

yet efficient way. BI&A services are defined through

the activities carried out by a BI&A department. The

definition of an accounting net and a cost model then

is used in combination with the mentioned BI&A

services to create a company-specific and

understandable service catalog. This work improves

cost transparency and enables internal processes for

invoicing BI&A service purchasers and consumers

within the organization in a fairer and more exact way.

2.2. Influence of the stakeholder perspective

on IS evaluation

There is no shortage of research on IS evaluation

which both forms the basis of varied academic activity

and is widely used in practice until today [6]. Early

research emphasizes the existence of differences

regarding the perspective from which the success or

efficiency of IS is evaluated within organizations [28].

Often, these perspectives are classified by stakeholder

types. Common types are end user (consumer), IT

personnel, management, and external stakeholders

[13]. The research on IS evaluation is also applied to

BI&A when it comes to success models where there

is, as a minimum, differentiation by end-user-side and

BI&A department-side [7, 27]. However, in literature

to date, there is a common understanding of how

strongly the different stakeholder perspectives

influence IS evaluation [28]. Referring to our research

question in Section 1, the extant research on IS

evaluation suggests that different stakeholder types in

companies come to different assessments regarding

BI&A cost accounting initiatives.

Page 752

3. Research concept

The aim of this paper is to determine a way of

producing practice-based estimates on the potential

benefits and the degree of implementation for specific

application areas of cost accounting for BI&A.

Beyond this, this study focuses on the current

challenges for practical implementation of cost

accounting for BI&A. With the results of this paper,

we are able to show need for action and identify

barriers to new and further development of cost

accounting for BI&A. The next two subsections sum

up the research method used and detail the

demographic structure of our sample.

3.1. Research method

The underlying data used for this study was

collected by a quantitative-empirical survey using a

standardized online questionnaire. This survey

includes all items which are used to answer our

research question. The survey structure is based on

investigations carried out by Dinter et al. [8]. The

questionnaire consists of three parts: a general section

about the respondent and the organization with their

BI&A environment, general questions about BI&A-

related cost accounting, and a part regarding

challenges and the use of BI&A cost accounting. The

survey items were readjusted so that they fit to the

underlying topic of BI&A cost accounting.

A short introduction to the term BI&A cost

accounting was given to ensure a common

understanding. Consultants or academics were then

asked to respond from the point of view of the

customer they know best. Prior work by Dinter et al.

[8] suggests to consider the BI life cycle of [9], for

structuring the questions related to investigated

application areas into BI&A development/ operation,

BI usage, and an organizational dimension. Table 1

gives an overview of the structure with investigated

application areas. These application areas were

assessed by a five-point Likert scale. The respondents

were asked to assess the potential benefits

(5=“essential”, 4=“high benefit”, 3=“nice to have”,

2=“low benefit”, 1=“no benefit”) and the degree of

implementation (5=“implemented”,

4=“implementing”, 3=“planned”, 2=“initiative

failed”, 1=“no entry”) of the mentioned application

areas.

Table 1. Application areas of BI&A cost

accounting

Another perspective we intend to examine are the

implementation challenges of BI&A cost accounting.

Table 2 gives an overview of the relevant items. The

respondents also rate the efforts for this challenges on

a five-point scale (1=“insignificant”, 2=“low”,

3=“moderate”, 4=“huge”, 5=“insurmountable”).

Table 2. Implementation challenges of BI&A

cost accounting

The questionnaire developed was evaluated by

experts from industry and university on content,

structure, and language. After this pre-test, feedback

was considered and the structure was redesigned for

better readability. The online questionnaire was sent at

Page 753

first to 1,202 German TDWI members (The Data

Warehousing Institute) at the end of 2016.

Additionally, this survey was posted in groups for

business intelligence on XING.com. To gain a better

result from practice, BI&A departments from five

large companies where asked to participate in the

survey. After two months, this procedure was

repeated. The online survey platform was configured

so that each attendee could only participate once.

3.2. Structure of the sample

As we were focussing on BI&A cost accounting,

our target group were BI&A stakeholders. We

estimate that there was a total of about 3000 recipients

for this survey; precisely 251 BI&A stakeholders took

part. Given this approximation of our potential

attendees, we can assume a response rate of about

11.9%. From this percentage, we collected 59

complete answer records. Table 3 presents an

overview of our sample by company size and BI&A

experience.

To answer our research question, we considered

the following three stakeholder types: BI&A user,

BI&A developer, and BI&A manager. External

stakeholders are not included in this survey because

we are looking at the internal structure of BI&A

organizations. Table 3 shows our sample divided by

the three different stakeholder roles into BI&A users

with 21 participants (35.6%), BI&A developers with

24 participants (40.7%), and BI&A managers with 14

participants (23.7%). We can classify our population

as experienced, with 61.0% having “6 to 10 years”

behind them in the area. BI&A users above all

classified themselves as less experienced, with up to 5

years (23.7%).

In terms of the BI&A organization, 49.2% deal

with 100 to 999 BI&A users. 25.4% of the participants

are in companies with 1,000 and above 9,999 BI&A

users. Another interesting point is the heterogeneity of

the BI&A landscape: 44.1% are working with 3 up to

5 BI&A vendors. 18.6% are served by one sole vendor

and 15.3% use two. This corresponds to 47.5% of

BI&A organizations employing a “best of breed”

approach; another 40.7% prefer to work with one

single BI&A suite.

Looking at the company size, the majority of the

respondents are working in large companies with more

than 1,000 employees (83.0%); the remaining part

work in medium-sized companies. 50.9% of these

companies are in the production industry; the next

greater part are IT software companies (10.2%).

Another 38.9% is more or less spread over other

categories of companies, with bank and financial

service providers (6.8%) and energy supply/ trading

(5.1%) as the largest groups.

Our survey points out that BI&A cost accounting

is important (47.3%) and indispensable for 11.9% of

the participants (cp. Table 4). Another 25.5% rated

BI&A cost accounting as “nice to have”. Beside this,

more than the half of our population (54.2%) have no

form of cost accounting in their BI&A organization.

28.8% are using a product-oriented allocation whereas

3.4% allocate their costs over a production-oriented

allocation. But another aspect shows that 23.7% of the

participants are planning or are currently in an

implementation stage of their cost accounting

initiative.

Table 4. Importance of BI&A cost accounting

Table 3. Overview of sample structure

Page 754

4. Empirical analysis and discussion of

findings of cost accounting for BI&A

Evaluating our results in a three-stage process, we

will highlight the most remarkable findings. In Section

4.1, we present the results of our survey by discussing

the potential benefits in relation to the degree of

implementation for the BI&A cost accounting

application areas. The findings will be discussed for

each BI&A stakeholder perspective. We will then

combine these perspectives and analyze the potential

benefits and the degree of implementation separately.

The challenges for practical implementation and

refinement of a BI&A cost accounting are then

described in Section 4.2. In the last section, we present

a summary assessment of our findings.

4.1. Evaluation of the potential benefits and

degree of implementation

To aid comprehensibility, the single application

areas from Table 1 are abbreviated in the same order

according to BI&A development/operation from A1 to

A3, BI&A usage from B1 to B4, and BI&A

organization from C1 to C6. Furthermore, we select

graphical diagrams to visualize differences and

similarities. The relation between the potential

benefits and degree of implementation could be

interpreted as an indicator for desired “need for

action” for the single application areas [8].

Figure 1 presents the results as mean ratings of

how BI&A users assessed the potential benefits and

degree of implementation for each area of application.

It is obvious that BI&A users identify higher potential

in those application areas where they benefit from

directly or the opposite. At first, the high potential

benefit in B2 (overall, partial project calculation), C1

(sensitization of customers for and economical usage

of BI&A) and C2 (increase of BI&A understanding)

means that we may assume that the users are willing

to improve understanding in BI&A organization to

prevent inefficiencies. On the other hand, they see less

potential in A3 of deleting uneconomical BI&A

applications. Maybe the risk of losing necessary

applications is considered to high? Nevertheless, they

asses other areas with high potential (A2:

identification of cost drivers, B4: improvement to plan

BI&A resources, C4: allowing make-or-buy). From

the low degree of implementation, we can conclude

that from a BI&A user perspective, the whole topic of

BI&A cost accounting in relation to the potential

benefits creates both high potential and pronounced

need for improvements.

Figure 1. BI&A users

Looking at the BI&A developer perspective in

Figure 2, we can begin by highlighting the lower

potential benefit assessed for allowing outsourcing

comparisons (C5). This may be explained by

developers being unwilling to make themselves

superfluous. Another obvious point is their low

estimation of potential benefits for improvement in

planning the users’ BI&A demands (B3). This can be

explained by less involvement in this topic from an

“end-user view”. Furthermore, developers confirm

most potential benefits, especially for the BI&A usage

category, e.g. in improving planning of BI&A

resource consumption (B4) or prioritizing order

management by ROI (B1).

Figure 2. BI&A developers

Another high potential is increasing awareness of

BI&A usage (C1) with BI&A cost accounting.

However, we can observe a homogenous course of

both potential benefits and degrees of implementation

with an assessment gap as shown in the BI&A user

perspective. This emphasizes the need for action in all

application areas and gives further evidence for the

need of a BI&A cost accounting.

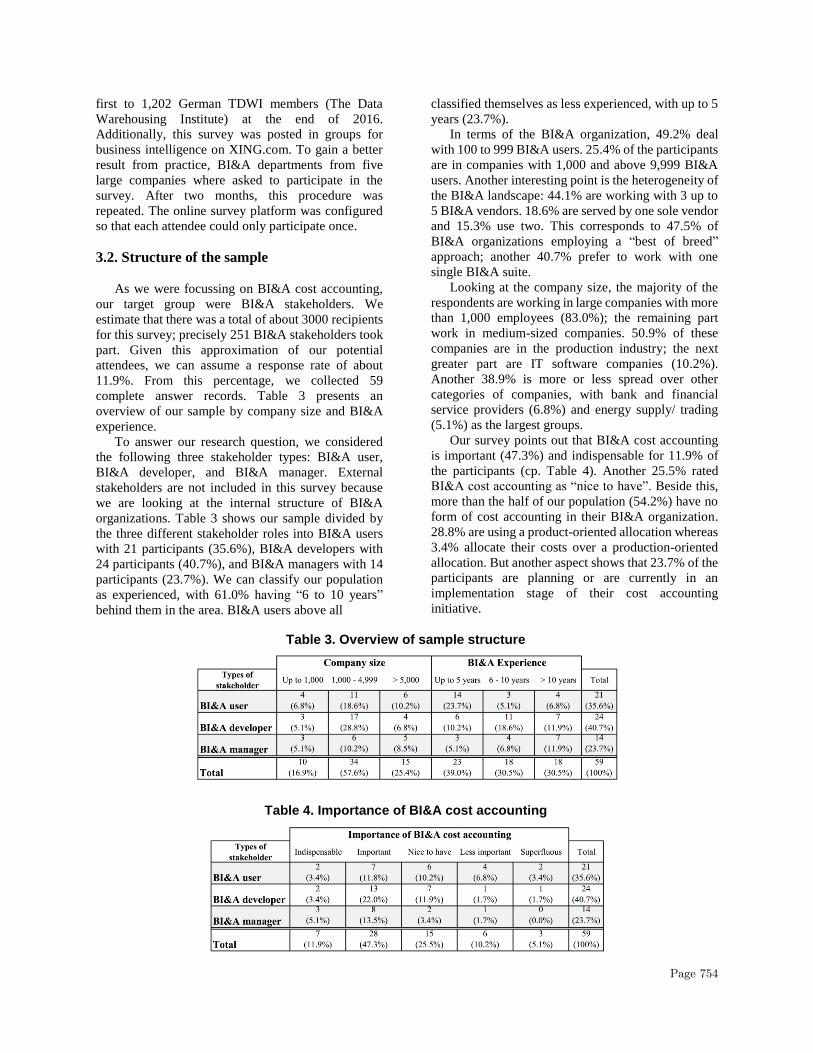

Not surprisingly, BI&A mangers in Figure 3 see

the most potential benefits in being able to justify their

BI&A organization to management (C3). Another

remarkable area is the high potential in sensitizing

BI&A users to economical BI&A usage (C1) and

increasing BI&A acceptance (C2). In comparison to

those high ratings, cancellation management (A3) has

Page 755

the lowest ratings. This contradicts with (C1) because,

by deleting uneconomical BI&A applications,

resources would be freed up, especially in the BI&A

operations area. Nevertheless, BI&A managers see

high potential in prioritizing order management (B1),

doing project calculations (B2), and executing service

management with internal cost allocation (A1).

Looking at the high degree of implementation assessed

in these three areas B1, B2, A1 and C3, we are of the

opinion that these areas represent the BI&A mangers’

daily business and that they are therefore most able to

achieve results here. The most pressing need for action

is situated in allowing make-or-buy decisions (C4),

outsourcing comparisons (C5), and allowing cost

benchmarks (C6) because it is here that the gap

between assessed potential benefits and the degree of

implementation is the highest. Once more, this is

evidence for the high potential of BI&A cost

accounting to improve the current situation in BI&A

departments e.g. by creating cost transparency and

allowing the invoicing of BI&A costs to customers.

Figure 3. BI&A managers

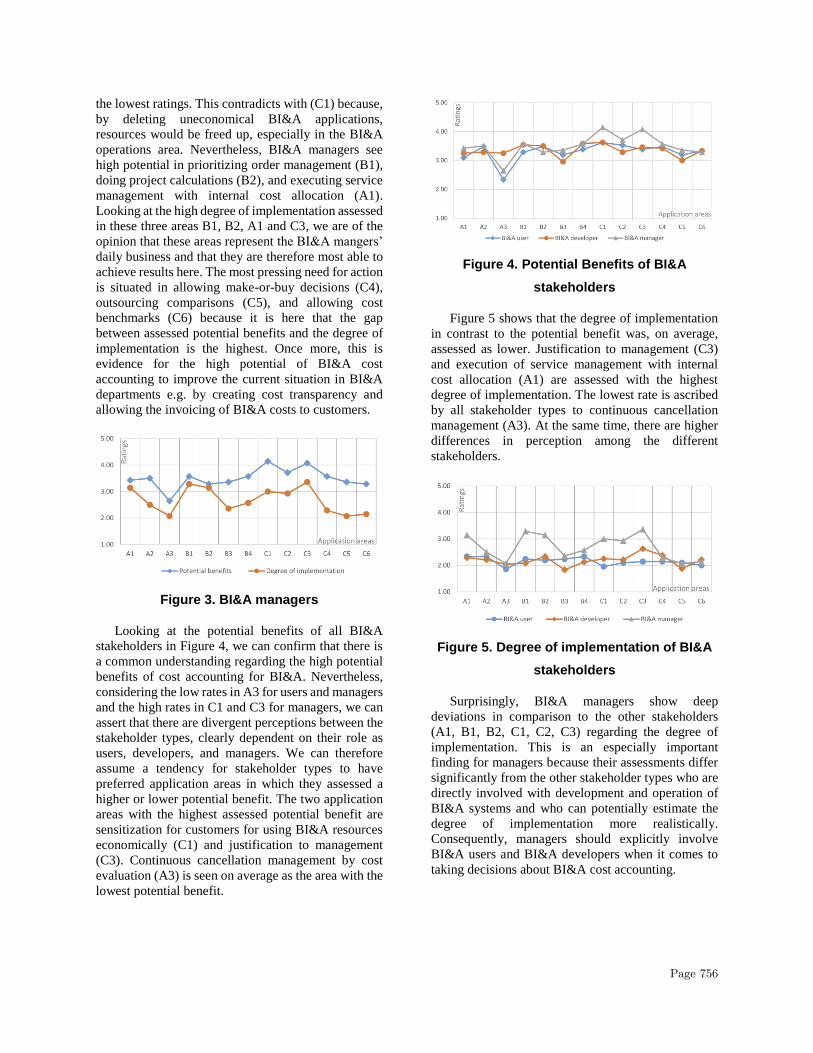

Looking at the potential benefits of all BI&A

stakeholders in Figure 4, we can confirm that there is

a common understanding regarding the high potential

benefits of cost accounting for BI&A. Nevertheless,

considering the low rates in A3 for users and managers

and the high rates in C1 and C3 for managers, we can

assert that there are divergent perceptions between the

stakeholder types, clearly dependent on their role as

users, developers, and managers. We can therefore

assume a tendency for stakeholder types to have

preferred application areas in which they assessed a

higher or lower potential benefit. The two application

areas with the highest assessed potential benefit are

sensitization for customers for using BI&A resources

economically (C1) and justification to management

(C3). Continuous cancellation management by cost

evaluation (A3) is seen on average as the area with the

lowest potential benefit.

Figure 4. Potential Benefits of BI&A

stakeholders

Figure 5 shows that the degree of implementation

in contrast to the potential benefit was, on average,

assessed as lower. Justification to management (C3)

and execution of service management with internal

cost allocation (A1) are assessed with the highest

degree of implementation. The lowest rate is ascribed

by all stakeholder types to continuous cancellation

management (A3). At the same time, there are higher

differences in perception among the different

stakeholders.

Figure 5. Degree of implementation of BI&A

stakeholders

Surprisingly, BI&A managers show deep

deviations in comparison to the other stakeholders

(A1, B1, B2, C1, C2, C3) regarding the degree of

implementation. This is an especially important

finding for managers because their assessments differ

significantly from the other stakeholder types who are

directly involved with development and operation of

BI&A systems and who can potentially estimate the

degree of implementation more realistically.

Consequently, managers should explicitly involve

BI&A users and BI&A developers when it comes to

taking decisions about BI&A cost accounting.

Page 756

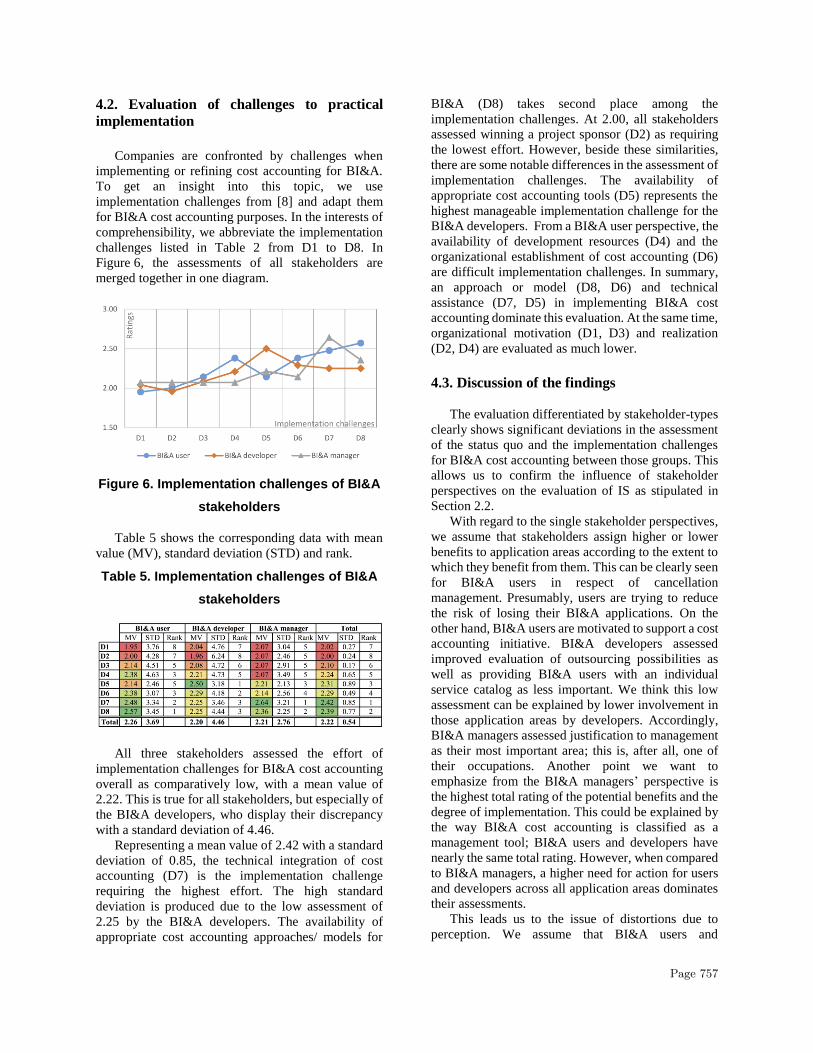

4.2. Evaluation of challenges to practical

implementation

Companies are confronted by challenges when

implementing or refining cost accounting for BI&A.

To get an insight into this topic, we use

implementation challenges from [8] and adapt them

for BI&A cost accounting purposes. In the interests of

comprehensibility, we abbreviate the implementation

challenges listed in Table 2 from D1 to D8. In

Figure 6, the assessments of all stakeholders are

merged together in one diagram.

Figure 6. Implementation challenges of BI&A

stakeholders

Table 5 shows the corresponding data with mean

value (MV), standard deviation (STD) and rank.

Table 5. Implementation challenges of BI&A

stakeholders

All three stakeholders assessed the effort of

implementation challenges for BI&A cost accounting

overall as comparatively low, with a mean value of

2.22. This is true for all stakeholders, but especially of

the BI&A developers, who display their discrepancy

with a standard deviation of 4.46.

Representing a mean value of 2.42 with a standard

deviation of 0.85, the technical integration of cost

accounting (D7) is the implementation challenge

requiring the highest effort. The high standard

deviation is produced due to the low assessment of

2.25 by the BI&A developers. The availability of

appropriate cost accounting approaches/ models for

BI&A (D8) takes second place among the

implementation challenges. At 2.00, all stakeholders

assessed winning a project sponsor (D2) as requiring

the lowest effort. However, beside these similarities,

there are some notable differences in the assessment of

implementation challenges. The availability of

appropriate cost accounting tools (D5) represents the

highest manageable implementation challenge for the

BI&A developers. From a BI&A user perspective, the

availability of development resources (D4) and the

organizational establishment of cost accounting (D6)

are difficult implementation challenges. In summary,

an approach or model (D8, D6) and technical

assistance (D7, D5) in implementing BI&A cost

accounting dominate this evaluation. At the same time,

organizational motivation (D1, D3) and realization

(D2, D4) are evaluated as much lower.

4.3. Discussion of the findings

The evaluation differentiated by stakeholder-types

clearly shows significant deviations in the assessment

of the status quo and the implementation challenges

for BI&A cost accounting between those groups. This

allows us to confirm the influence of stakeholder

perspectives on the evaluation of IS as stipulated in

Section 2.2.

With regard to the single stakeholder perspectives,

we assume that stakeholders assign higher or lower

benefits to application areas according to the extent to

which they benefit from them. This can be clearly seen

for BI&A users in respect of cancellation

management. Presumably, users are trying to reduce

the risk of losing their BI&A applications. On the

other hand, BI&A users are motivated to support a cost

accounting initiative. BI&A developers assessed

improved evaluation of outsourcing possibilities as

well as providing BI&A users with an individual

service catalog as less important. We think this low

assessment can be explained by lower involvement in

those application areas by developers. Accordingly,

BI&A managers assessed justification to management

as their most important area; this is, after all, one of

their occupations. Another point we want to

emphasize from the BI&A managers’ perspective is

the highest total rating of the potential benefits and the

degree of implementation. This could be explained by

the way BI&A cost accounting is classified as a

management tool; BI&A users and developers have

nearly the same total rating. However, when compared

to BI&A managers, a higher need for action for users

and developers across all application areas dominates

their assessments.

This leads us to the issue of distortions due to

perception. We assume that BI&A users and

Page 757

developers are closer to the action and therefore in a

position to assess BI&A cost accounting

implementation more realistically than BI&A

mangers. Especially when looking at the degree of

implementation, deviations are visible due to varying

degrees of involvement in the application areas. The

different perceptions might cause suboptimal results

when it comes to designing or implementing BI&A

cost accounting. The rather low level of conviction

among BI&A users and developers we found could

lead to inaccurate BI&A cost accounting because they

may have to estimate efforts for BI&A projects which

are forwarded to customers. Furthermore, the risk of

accepting by these two perspectives after

implementation increases when there is no common

understanding about the use and benefits of BI&A cost

accounting and may further negatively affect

companies’ BI&A systems. Therefore, BI&A

managers should explicitly involve BI&A users and

developers in the process with regard to development,

implementation or refinement of BI&A cost

accounting initiatives.

These differences in perception are also visible in

the assessment of implementation challenges.

However, there is a common understanding about the

importance of a suitable approach and technical

assistance when implementing a BI&A cost

accounting.

One major implementation challenge we identify

in this study is the gap in BI&A cost accounting

approaches or models. To improve this situation, we

recommend reading further research results, for

example on introducing BI&A service-oriented cost

accounting in [14].

Through the findings of our survey, we conclude

the following:

• divergent perceptions among users, developers

and managers which can lead to less acceptance

and less success when introducing BI&A cost

accounting,

• users want to protect their BI&A applications,

developers try not to be superfluous whereas

managers need a cost accounting system most for

justification,

• the chance of selling a BI&A cost accounting

system in enterprises increases when

concentrating on managers because of their high

belief in the use and utility of a cost accounting

function,

• higher acceptance of BI&A cost accounting and

project success can be achieved when considering

the defined and prioritized needs for action and

implementation challenges.

From our analysis, we can conclude that there is

high potential for establishing BI&A cost accounting

and that companies in our population have a

pronounced need for action of which they are, at the

very least, well aware.

5. Limitations and further work

There are limitations to this paper: primarily,

interpreting the results of the analysis of the

differences in perception among stakeholders

regarding the development or refinement of BI&A

cost accounting. On the one hand, there are restrictions

to the underlying research concept; on the other hand,

there are limitations relating to the number of cases in

the sample collection. The available data set is not

representative and is therefore not suitable for

generalizing our findings. To achieve this, more

studies are needed.

With the data set available, further research is

conceivable by analyzing more questions. It may be

possible to take the amount of BI&A users, the

heterogeneity of the BI&A system landscape, or the

amount of employees working in a BI&A department

into account. From so doing, we expect a deeper

understanding about cost accounting usage. Our future

aim is to implement appropriate BI&A cost accounting

approaches to evaluate how stakeholder perceptions

are affected.

A useful contribution could be expected when

stakeholders are made to consider the most promising

application areas for them when implementing or

improving their BI&A cost accounting and to take the

resulting order of implementation challenges into

account.

7. References

[1] Baars, H., C. Felden, P. Gluchowski, A. Hilbert, H.-G.

Kemper, and S. Olbrich, "Shaping the Next Incarnation of

Business Intelligence", Business & Information Systems

Engineering, 6(1), 2014, pp. 11–16.

[2] Baars, H. and H.-G. Kemper, "Business intelligence in

the cloud?", PACIS 2010 Proceedings, 2010.

[3] Berghout, E. and D. Remenyi, "The Eleven Years of the

European Conference on IT Evaluation: Retrospectives and

Perspectives for Possible Future Research", Electronic

Journal of Information Systems Evaluation, 8(2), 2005,

pp. 81–98.

[4] Brandl, R., M. Bichler, and M. Strobel, "Cost

accounting for shared IT infrastructures",

Wirtschaftsinformatik, 49(2), 2007, pp. 83–94.

Page 758

[5] Chen, H., R.H.L. Chiang, and V.C. Storey, "Business

Intelligence and Analytics: From Big Data to Big Impact",

MIS quarterly, 36(4), 2012, pp. 1165–1188.

[6] Delone, W.H. and E.R. McLean, "The DeLone and

McLean Model of Information Systems Success: A Ten-

Year Update", Journal of Management Information

Systems, 19(4), 2003, pp. 9–30.

[7] Dinter, B., "The Maturing of a Business Intelligence

Maturity Model", in Proceedings of the American

Conference on Information Systems (AMCIS’2011). 2011:

Detroit, Michigan, USA.

[8] Dinter, B., P. Gluchowski, and C. Schieder, "A

Stakeholder Lens on Metadata Management in Business

Intelligence and Big Data - Results of an Empirical

Investigation Rico", in 21st Americas Conference on

Information Systems, AMCIS 2015, Puerto Rico. 2015.

[9] Dinter, B., C. Schieder, and P. Gluchowski, "Towards a

Life Cycle Oriented Business Intelligence Success Model

Competitiveness. 17th Americas Conference on

Information Systems, AMCIS 2011", in A Renaissance of

Information Technology for Sustainability and Global

Competitiveness. 17th Americas Conference on

Information Systems, AMCIS 2011, Detroit, Michigan,

USA, V. Sambamurthy and M. Tanniru, Editors. 2011.

[10] Epple, J., S. Bischoff, and S. Aier, "Management

Objectives and Design Principles for the Cost Allocation of

Business Intelligence", in PACIS. 2015.

[11] Gansor, T. and A. Totok, Von der Strategie zum

Business Intelligence Competency Center (BICC):

Konzeption, Betrieb, Praxis, 2nd edn., dpunkt.verlag;

TDWI Europe, Heidelberg, 2015.

[12] Gibson, M., D. Arnott, and I. Jagielska, "Evaluating

the Intangible Benefits of Business Intelligence: Review &

Research Agenda", Decision Support in an Uncertain and

Complex World: The IFIP TC8/WG8.3 International

Conference 2004, 2004, pp. 295–305.

[13] Grover, V., S.R. Jeong, and A.H. Segars, "Information

systems effectiveness: The construct space and patters of

application", Information & Management, 31(4), 1996,

pp. 177–191.

[14] Grytz, R. and A. Krohn-Grimberghe, "Service-

oriented Cost Allocation for Business Intelligence and

Analytics: Who pays for BI&A?", in Proceedings of the

50th Hawaii International Conference on System Sciences.

2017.

[15] Hagerty, J., R.L. Sallam, and J. Richardson, "Magic

quadrant for business intelligence platforms", 2012.

[16] Hamel, F., T.P. Herz, F. Uebernickel, and W. Brenner,

"State of the art: Managing costs and performance of

Information Technology", AMCIS 2010 Proceedings(Paper

516), 2010.

[17] Horakh, T.A., H. Baars, and H.-G. Kemper,

"Mastering Business Intelligence Complexity-A Service-

Based Approach as a Prerequisite for BI Governance",

AMCIS 2008 Proceedings, 2008, p. 333.

[18] Kaisler, S., F. Armour, and A. Espinosa, "Introduction

to Big Data and Analytics: Concepts, Methods, Techniques,

and Application Minitrack", in Proceedings of the 50th

Hawaii International Conference on System Sciences.

2017.

[19] Kaisler, S., F. Armour, J.A. Espinosa, and W. Money,

"Big Data: Issues and Challenges Moving Forward", in

2013 46th Hawaii International Conference on System

Sciences, 2013 46th Hawaii International Conference on

System Sciences (HICSS), Wailea, HI, USA, 07.01.2013 -

10.01.2013. 2013. IEEE.

[20] Kaplan, R.S. and R. Cooper, Cost & effect: Using

integrated cost systems to drive profitability and

performance, 9th edn., Harvard Business School Press,

Boston, Mass., 2005.

[21] Klesse, M., "Methode zur Gestaltung einer

Leistungsverrechnung für DWH Competence Center", in

Active Enterprise Intelligence™, J. Töpfer and R. Winter,

Editors. 2008. Springer Berlin Heidelberg.

[22] Lönnqvist, A. and V. Pirttimäki, "The Measurement of

Business Intelligence", Information Systems Management,

23(1), 2006, pp. 32–40.

[23] Miller, G.J., D. Bräutigam, and S.V. Gerlach, Business

intelligence competency centers: A team approach to

maximizing competitive advantage, John Wiley & Sons,

Hoboken, N.J, 2006.

[24] Moss, L.T. and S. Atre, Business intelligence

roadmap: The complete project lifecycle for decision-

support applications, Addison-Wesley, Boston, MA, 2003.

[25] Negash, S., "Business intelligence", The

Communications of the Association for Information

Systems, 13(1), 2004, p. 54.

[26] Schieder, C. and P. Gluchowski, "Towards a

consolidated research model for understanding business

intelligence success", in ECIS. 2011.

[27] Seddon, P.B., D. Constantinidis, T. Tamm, and H.

Dod, "How does business analytics contribute to business

value?", Information Systems Journal, 27(3), 2017,

pp. 237–269.

[28] Seddon, P.B., S. Staples, R. Patnayakuni, and M.

Bowtell, "Dimensions of Information Systems Success",

Commun. AIS, 2(3es), 1999.

[29] van Maanen, H. and E. Berghout, "Cost management

of IT beyond cost of ownership models: a state of the art

overview of the Dutch financial services industry",

Evaluation and Program Planning, 25(2), 2002, pp. 167–

173.

[30] Wu, J., "Calculating the ROI for Business Intelligence

Projects", 2000 (http://www.information-

management.com/news/2487-1.html, 14-06-2017).

Page 759