building a “headquarters economy”: the geography of headquarters within beijing and its...

TRANSCRIPT

Cities 42 (2015) 1–12

Contents lists available at ScienceDirect

Cities

journal homepage: www.elsevier .com/locate /c i t ies

Building a ‘‘Headquarters Economy’’: The geography of headquarterswithin Beijing and its implications for urban restructuring

http://dx.doi.org/10.1016/j.cities.2014.08.0040264-2751/� 2014 Elsevier Ltd. All rights reserved.

⇑ Corresponding author. Cell: +86 (10)138 1043 8595.E-mail addresses: [email protected] (F. Pan), [email protected] (J. Guo),

[email protected] (H. Zhang), [email protected] (J. Liang).1 http://english.sohu.com/20051229/n227704100.shtml.

2 http://www.china-briefing.com/news/2012/03/15/chinas-headquartomy-a-new-path-to-industrial-upgradation.html.

3 http://www.chijihon.metro.tokyo.jp/ahq_project/english/news-even20130726.html.

Fenghua Pan a,⇑, Jie Guo b, Hua Zhang a, Jinshe Liang a

a School of Geography, Beijing Normal University, No. 19, XinJieKouWai St., HaiDian District, Beijing 100875, PR Chinab School of Government, Peking University, No. 5 Yiheyuan Road, HaiDian District, Beijing 100871, PR China

a r t i c l e i n f o a b s t r a c t

Article history:Received 8 December 2013Received in revised form 28 July 2014Accepted 20 August 2014

Keywords:HeadquartersHeadquarters economyLocationAgglomerationUrban structureBeijing

As command centers, headquarters (HQ) of large firms are crucial to the economy of cities where they arelocated. Since HQ of large firms play a key role in shaping the urban structure, it is important to inves-tigate the locational patterns of HQ within a city for both academic and policy considerations. Basedon a data set of publicly listed firms with HQ located in Beijing, we found that the spatial distributionof HQ is characterized by both agglomeration and dispersion. On the one hand, HQ are significantlyagglomerated at different geographical scales. Several clusters of HQ have been identified in our study.Moreover, a suburbanization of HQ trend has also emerged. The regression analysis shows that firm attri-butes, including sector, scale, ownership and year of going public, may explain the location pattern of HQ.We conclude by providing a detailed analysis of HQ distributions within Beijing that is being shaped byboth market and state forces; it also highlights the role of HQ location in urban restructuring. Theagglomeration of HQ is persistent and could be the results of the interplay between market and stateforces, among which the agglomeration economy as well as the urban planning are most important.The results could also shed some light on the development of a ‘‘HQ economy’’ and urban planning forother cities.

� 2014 Elsevier Ltd. All rights reserved.

Introduction

Headquarters (HQ) are in charge of some, if not all, of the stra-tegic functions of firms (Godfrey & Zhou, 1999; Rice & Lyons, 2010;Taylor & Csomós, 2012; Taylor et al., 2009; Tonts & Taylor, 2010).As command centers of firms, the HQ of large firms are crucial tothe economy of cities where they are located in many ways(Csomós, 2013; Godfrey & Zhou, 1999; Taylor & Csomós, 2012;Taylor et al., 2009; Testa, 2006). Firms tend to relocate their HQor regional HQ to other cities when they need to adapt to con-stantly changing economic situations (Holloway & Wheeler,1991; Klier, 2006). It has become a feasible strategy for cities toattract the HQ of large firms in order to advance their urban andregional economies (Klier & Testa, 2001; Testa, 2006).

The overall economic influence of HQ on the urban and regionaleconomy is often termed as ‘‘HQ economy’’,1 which has been widelyused and adopted by Chinese local governments in developing urbaneconomies (Chan & Poon, 2011). The entrepreneurial endeavour of

China’s governments (Wu, 2002) can also be observed in their effortsto build a ‘‘HQ economy’’ at the local level. Given the significant ben-efits that could be generated by the so-called ‘‘HQ economy’’, localgovernments tend to adopt preferential policies to attract HQ(Chan & Poon, 2011). Many cities such as Beijing, Shanghai andShenzhen have advanced their ‘‘HQ economy’’ strategy by attractingthe HQ of large firms or the regional HQ of foreign firms (G. Zhang,2013; Zhao, 2013). In addition, building a ‘‘HQ economy’’ is consid-ered as ‘‘a path towards industrial upgrading’’2 in China. This phe-nomenon could also be observed in developed countries. Forexample, Tokyo launched a special zone for Asian HQ in 2013.3

Moreover, HQ are sometimes seen as playing an important role notonly in shaping the overall spatial pattern of office buildings withina city but also in influencing the employment opportunities andresulting traffic flows. Attracting HQ could also be a key concern ofurban planning and urban development strategies.

Existing studies on the geography of HQ of large firms have paidlittle attention to their locations and agglomerations within a city.

ers-econ

ts/press/

2 F. Pan et al. / Cities 42 (2015) 1–12

Most of them have focused on the distribution of HQ among differ-ent cities (Bel & Fageda, 2008; Klier, 2006; Meyer & Green, 2003;Pan & Xia, 2014; Rice, 2010; Rice & Lyons, 2010; Tonts & Taylor,2011, 2010). Theoretical and empirical research suggests that HQare highly agglomerated in metropolitan areas in western coun-tries (Davis & Henderson, 2008; Henderson & Ono, 2008; Lovely,Rosenthal, & Sharma, 2005; Strauss-Kahn & Vives, 2009). Recentstudies on the geography of HQ of large firms among Chinese citiesfound that HQ are mostly concentrated in large cities such asBeijing, Shanghai and Shenzhen (Pan & Xia, 2014; Wu & Ning,2010). It is pointed out that HQ are highly agglomerated withinmetropolitan areas as well (Meyer & Green, 2003). However, thespatial patterns and underlying mechanisms of the HQ distribu-tions within a city have been underexplored. So is their interactionwithin a city’s evolving urban structure.

The rapid rise of both large firms and world cities in China hasimpacts both within and beyond the urban territory. Studying thedevelopment of the ‘‘HQ economy’’ is of central importance as therelocation of HQ often results in restructuring of metropolitanareas.

Of all the cities involved in building a ‘‘HQ economy’’ in China,Beijing has been the most successful. It has made great strides inpresenting itself as a world city (Wei & Yu, 2006). Among all themeans applied by the local government, attracting HQ of domesticlarge firms and regional HQ of multinational corporations (MNCs)turns out to be the most effective, because Beijing has an ‘‘informa-tion advantage’’ due to its administrative role (Wang, Zhao, Gu, &Chen, 2011; Zhao, 2003; Zhao, Cai, & Zhang, 2005; Zhao, Zhang,& Wang, 2004). Beijing, as the capital of China, has become theleading city and home of the HQ of large firms in China. In 2013,Beijing surpassed Tokyo to become the No. 1 city housing the mostHQ of Global Fortune 500 companies.4 The most centrally directedfirms by SASAC (State-owned Assets Supervision and AdministrationCommission) and the Minister of Finance are located in Beijing.Moreover, Beijing is also home to the largest number of HQ of pub-licly listed firms (Pan & Xia, 2014). Beijing has also attracted themost HQ of domestically publicly listed firms relocating from othercities in China (Pan, Xia, & Liu, 2013). The latest case is SANY Group,a publicly listed firm that moved its HQ from Changsha to Beijing.More recently, many multinational corporations have setup newregional HQ in Beijing or relocated their regional HQ to Beijing. Forinstance, the regional HQ of Benz in Great China relocated from HongKong to Beijing in 2012.5 Promoting the ‘‘HQ economy’’ has provedto be an important way for Beijing to improve its competitivenessand to build on its reputation as a world city in the global era. How-ever, after firms decide to locate their HQ in certain cities (e.g.,Beijing) over others, where to locate their HQ within the city is thequestion that needs to be addressed.

Given the leading position of HQ in shaping the urban structure,it is particularly necessary to analyze the geographical distributionof HQ from the urban planning perspective. As an emerging ‘‘globalcapital city’’ (Chubarov & Brooker, 2013), the urban structure ofBeijing has evolved from a monocentric model to polycentric one(Feng, Wang, & Zhou, 2009; Qin & Han, 2013). At the same time,Beijing is suffering from problems like the expansion of the centralbuilt-up area, traffic congestion, air pollution and other urbanissues. It is also struggling to achieve a compact development plan(Yang, Shen, Shen, & He, 2012). Since the local government hasbeen so eager to build a ‘‘HQ economy’’ zone, this will definitelyinfluence the city’s urban structure in the near future. In this paper,we will discuss how the geography of HQ within Beijing and theresulting urban structure have been interacting with each other.

4 http://news.xinhuanet.com/2012-07/18/c_112471530.htm.5 http://auto.jrj.com.cn/2012/10/31120014599862.shtml.

Based on a data set of publicly listing firms that have their HQlocated in Beijing, we found that the spatial distribution is bothagglomerated and dispersed. On the one hand, HQ are significantlyagglomerated at different geographical scales. There also emergeda polycentric form as several distinct clusters could be identified.The regression analysis discussed below reveals that specific firmattributes, including sector, scale, ownership and year of goingpublic, are crucial to explaining the location pattern of HQ.

The remainder of this paper is organized as follows. The nextsection proposes a conceptual framework for analyzing the HQlocation within a city in a transitional economy, followed by a dis-cussion of the data and the methodology. Section ‘The Geographyof HQ within Beijing: an example’ maps the HQ distribution withinBeijing, which is then followed by a regression analysis on factorsthat may influence HQ location. Section ‘Discussion’ discusses thefactors that have impacts over the spatial distribution of HQ cen-ters as well as the interaction of the HQ distribution and urbanstructure. The final section concludes the study.

HQ location within a city of a transitional economy

Most empirical and theoretical studies on location of HQ indeveloped economies have paid much attention on the role of mar-ket forces such as benefits and costs of a specific locational choiceof HQ (Bel & Fageda, 2008; Davis & Henderson, 2008; Henderson &Ono, 2008; Lovely et al., 2005), while the importance of the statefactors in determining HQ location have been largely overlooked.Institutional contexts have been considered critical in the distribu-tion of HQ of large firms within China’s urban system (Pan & Xia,2014). Specifically, the location of HQ of large firms within a cityin China could also be influenced by policy interventions and theunique institutional background.

Urban transformation in China has been shaped by the interplaybetween the state and market (Han, 2000; Zhang, 2003). In otherwords, the HQ locations of large firms within a city can be seenas the result of the coexistence of the state bureaucracy and marketforces in a transitional economy.

As economic liberalization deepened in China, the marketbecame increasingly important in China’s economic development(Naughton, 2011). One of the critical characteristics of China’surban transformation has been the land-centered urban develop-ment (Lin, 2007). With land use reform, one significant change inBeijing from late 1980s onwards was the emergence of the CentralBusiness District (Gaubatz, 1995), as well as the rapid increase inland prices in Chinese cities. Firms need to take into account landprice when choosing a HQ location, even state-owned firms. Landprice is particularly crucial in small and new firms’ decision-making process.

Agglomeration economies take place in the CBDs of the largermetropolitan areas (Drennan & Kelly, 2011), and are critical inexplaining HQ location and overall agglomeration within a city.On the one hand HQ may locate in the specific area to enjoy spe-cific regional advantages such as the high quality of infrastructure,diversified community, convenient living environment, presence ofhigh-end producer service, excellent university and research insti-tutes. On the other hand HQ tend to locate close to each other.Firms can obtain agglomeration economies not only by sharingcommon inputs and the same labor market but also by enjoyinginformation spillover (Duranton & Puga, 2004; Rosenthal &Strange, 2004; Davis & Henderson, 2008; Lovely et al., 2005).Admittedly, due to the growing cost of being in the CBDs anddevelopment of information and communication technology (ICT)some firms may move their HQ out of urban centers(Boiteux-Orain & Guillain, 2004).

F. Pan et al. / Cities 42 (2015) 1–12 3

In a transitional economy such as China, the state still plays aheavy-handed, if not dominant, role in economic development.China’s central government has substantial influence on the spatialconfiguration of urban development, while local governments areshown to be dominant in the formation of the world city (L.-Y.Zhang, 2013). Attracting the HQ of large firms is considered to bea feasible way to advancing economic growth and improving theimage of the city and even the country. Therefore, both the nationaland local governments are key actors shaping the spatial pattern ofHQ within Beijing.

First, the majority of large firms in China is state-owned (Pan &Xia, 2014). Large state-owned firms have preferential access tocheap land and also benefit from strong ties with both local andnational governments. Thus, the locational choice of HQ of state-owned firms could be influenced by factors simply beside marketforces. Second, urban planning plays a leading role in some areas.For instance, the Financial Street and CBD were first proposed inBeijing’s Master Plan as early as 1993, in which the two areas weredesignated to be national financial management center and theCentral Business District respectively. The HQ of large firms havebeen encouraged to locate within these two areas. Finally, theentrepreneurial nature of local government activities has alsogreatly influenced the urban transformation in China, due largelyto the power of local governments in disposing of urban rightsfor land use (Shin, 2009). In short, urban planning and other policytools are being used to build a ‘‘HQ economy’’. Government incen-tives are crucial in the location choice of large firms ‘HQ (Chan &Poon, 2011; Pan & Xia, 2014).

Data and methodology

Data

Our data are drawn from Wind6 which includes all firms listedon the Shanghai and Shenzhen Stock Exchanges. There were 227publicly listed firms whose headquarters were in Beijing at theend of 2011.7 Publicly listed firms are used for two reasons: (1) theyare often large and include almost all large firms in Beijing and (2)detailed information of these firms is available. The location of theHQ is identified by the firm’s office address in the dataset, which issimilar with the previous study (Pan & Xia, 2014). Due to the lackof full information of HQ of other types of large firms, such as firmslisted on overseas stock exchanges and multinational corporations,this paper only focuses on firms listed on domestic stock exchanges.

Measurement of agglomeration at varied geographical scales

We use the Kernel Density Function (KDF) to calculate theagglomeration of HQ in Beijing, which is a widely used methodto calculate the density of point features (Silverman, 1986). TheKernel Density Estimate (KDE) is a widely used non-parametricway to estimate the probability density function in spatial analy-sis; it has been incorporated into ArcGIS 10.0, which is used below.

The L function is used to calculate the agglomeration of pointsat any geographical scales, based on the KDF. The equation is asfollows:

LðrÞ ¼ffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiKðrÞ=p

p� r;

where K is the KDF and r is the search radius. When L(r) > 0, itmeans items, in this case firms, are agglomerated. When L(r) < 0,it means items are scattered (Besag, 1977; Ripley, 1977). Because

6 Wind (Wan De) is a financial service company based in China. The website of thecompany is as follows: http://www.wind.com.cn/.

7 The data is the latest one that the authors can have at hand.

it is not possible to estimate the significance of the results of L func-tion directly, a Monte Carlo Simulation is preferred.

The geography of HQ within Beijing: an example

Location of HQ within Beijing

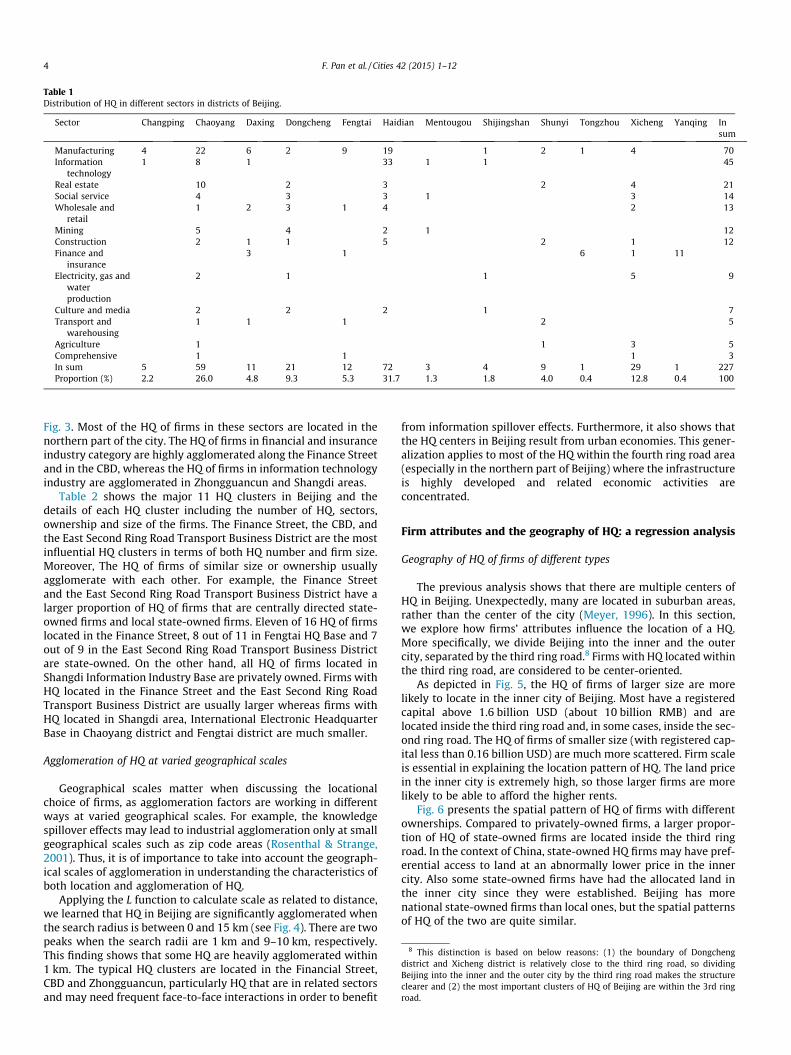

HQ are strongly concentrated at a district level. Table 1 showsthe distribution of HQ of publicly listed firms among different dis-tricts in Beijing. Haidian, Chaoyang and Xicheng are the top threedistricts in terms of number of HQ, together accounting for70.48% of the total.

The HQ of firms in the same sector tend to concentrate in a par-ticular district. For example, manufacturing firms are concentratedin Chaoyang and Haidian while information technology HQ areconcentrated in Haidian district. Nearly half of HQ of all firms inreal estate are located in Chaoyang district while those in financeand insurance are mostly in Xicheng and Dongcheng districts.

Fig. 1 shows the overall distribution of HQ of publicly listed firmsin Beijing. Three features stand out. First, there is a significant spa-tial bias for the location and agglomeration of HQ in Beijing. Alongthe South–North axis, there are more HQ in the northern part of Bei-jing divided by Chang’an Street and its extension. The most agglom-erated areas are in the northern part, except for Fengtai HQ Base. Onan East–West axis, the agglomeration patterns of HQ in the easternand western parts are similar.

Second, most HQ are located along the major urban transit lines.Almost 80% of the HQ are located within a 1 km buffer zone ofurban expressways. The clustering is more apparent in the agglom-erated area of HQ. For example, HQ are highly agglomerated in thearea along the north-second, third and fourth ring roads. In addi-tion, the HQ located outside of fifth ring road area are mostly alongradial highways. HQ are mostly close to urban expresswaysbecause they could benefit from access to information and commu-nication linkages, improve their efficiency, and take advantage ofother economic benefits (Daniels, 1975).

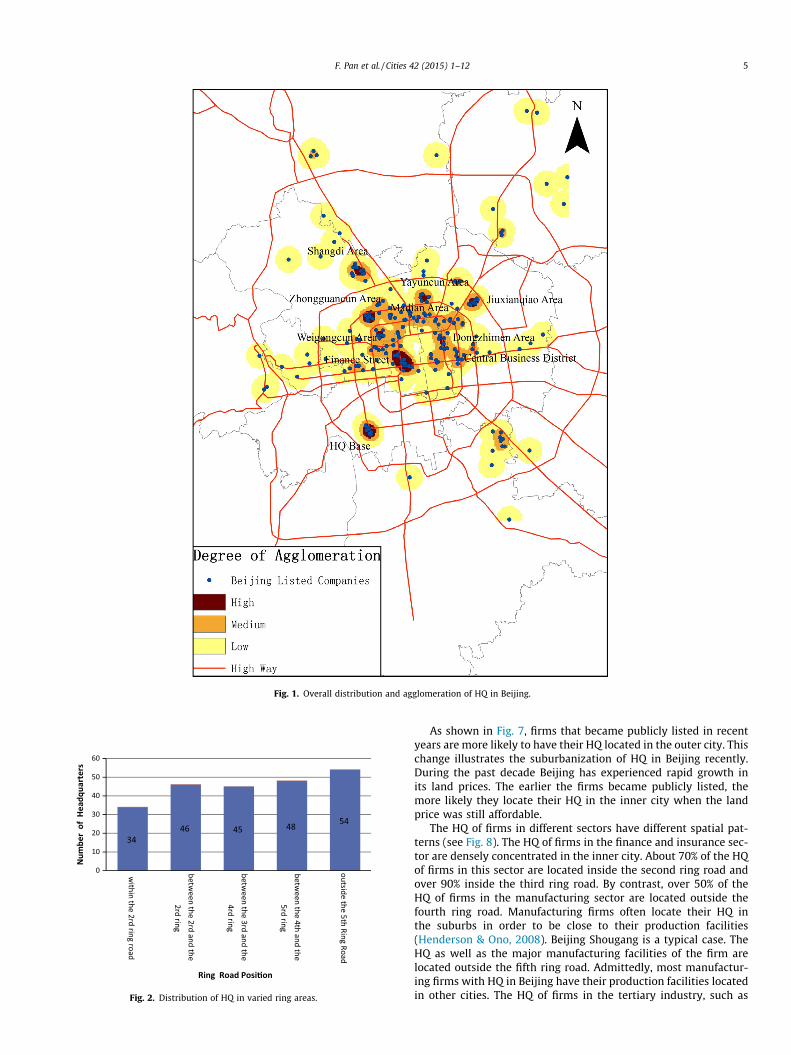

Third and finally, the distribution of HQ of large firms is charac-terized by both agglomeration and dispersion. The HQ are evenlydistributed among regions divided by the 2nd, 3rd, 4th and 5thring roads (see Fig. 2). Although the density of HQ along the 3rdring road area is the highest, the number of HQ outside of the5th ring road is the largest. This finding illustrates that there areseveral HQ clusters within the city.

Major HQ centers in the city

As noted, there are distinct clusters of HQ within Beijing, sug-gesting a polycentric spatial distribution of HQ. Fig. 1 depicts theagglomeration pattern of HQ in Beijing based on KDF analysis withinthe search radius of 2000 m. In general, the HQ are more agglomer-ated in the inner city than in suburban areas. The major HQ clustersare located in the Finance Street of Xicheng district, Dongzhimenarea of Dongcheng district, Central Business District (CBD), Yayun-cun and Jiuxianqiao areas in the Chaoyang district, Zhongguancun,Madian, Shangdi and Weigongcun areas in the Haidian district,HQ Base of the Fengtai district and the area near the internationalairport in Shunyi district. Although there are fewer HQ located inShijingshan and Fengtai districts, the HQ are highly agglomeratedwithin these two districts. For example, most of the HQ in Fengtaidistrict are located in the HQ Base.

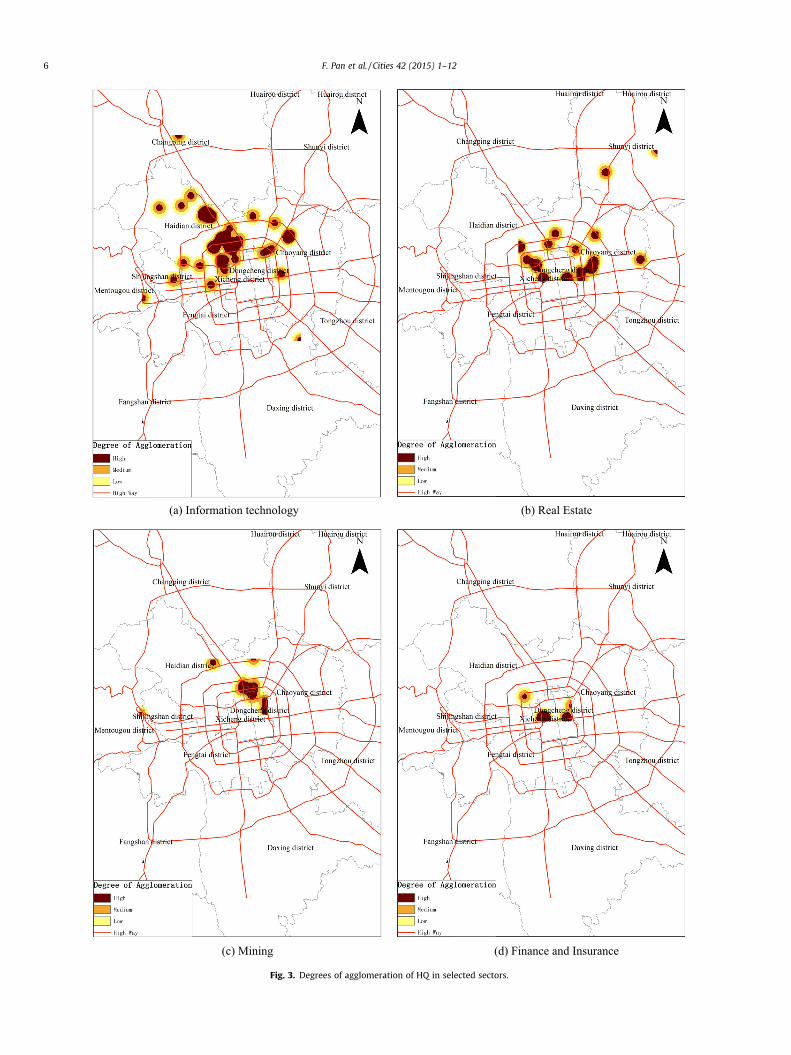

The spatial patterns of HQ in different industries are varied, andHQ of firms in the same industry tend to locate close to each other.Based on the results of KDF analysis, the agglomeration patterns offour sectors, including information technology, real estate, miningindustry and the finance and insurance industry, are shown in

Table 1Distribution of HQ in different sectors in districts of Beijing.

Sector Changping Chaoyang Daxing Dongcheng Fengtai Haidian Mentougou Shijingshan Shunyi Tongzhou Xicheng Yanqing Insum

Manufacturing 4 22 6 2 9 19 1 2 1 4 70Information

technology1 8 1 33 1 1 45

Real estate 10 2 3 2 4 21Social service 4 3 3 1 3 14Wholesale and

retail1 2 3 1 4 2 13

Mining 5 4 2 1 12Construction 2 1 1 5 2 1 12Finance and

insurance3 1 6 1 11

Electricity, gas andwaterproduction

2 1 1 5 9

Culture and media 2 2 2 1 7Transport and

warehousing1 1 1 2 5

Agriculture 1 1 3 5Comprehensive 1 1 1 3In sum 5 59 11 21 12 72 3 4 9 1 29 1 227Proportion (%) 2.2 26.0 4.8 9.3 5.3 31.7 1.3 1.8 4.0 0.4 12.8 0.4 100

8 This distinction is based on below reasons: (1) the boundary of Dongchengdistrict and Xicheng district is relatively close to the third ring road, so dividingBeijing into the inner and the outer city by the third ring road makes the structureclearer and (2) the most important clusters of HQ of Beijing are within the 3rd ringroad.

4 F. Pan et al. / Cities 42 (2015) 1–12

Fig. 3. Most of the HQ of firms in these sectors are located in thenorthern part of the city. The HQ of firms in financial and insuranceindustry category are highly agglomerated along the Finance Streetand in the CBD, whereas the HQ of firms in information technologyindustry are agglomerated in Zhongguancun and Shangdi areas.

Table 2 shows the major 11 HQ clusters in Beijing and thedetails of each HQ cluster including the number of HQ, sectors,ownership and size of the firms. The Finance Street, the CBD, andthe East Second Ring Road Transport Business District are the mostinfluential HQ clusters in terms of both HQ number and firm size.Moreover, The HQ of firms of similar size or ownership usuallyagglomerate with each other. For example, the Finance Streetand the East Second Ring Road Transport Business District have alarger proportion of HQ of firms that are centrally directed state-owned firms and local state-owned firms. Eleven of 16 HQ of firmslocated in the Finance Street, 8 out of 11 in Fengtai HQ Base and 7out of 9 in the East Second Ring Road Transport Business Districtare state-owned. On the other hand, all HQ of firms located inShangdi Information Industry Base are privately owned. Firms withHQ located in the Finance Street and the East Second Ring RoadTransport Business District are usually larger whereas firms withHQ located in Shangdi area, International Electronic HeadquarterBase in Chaoyang district and Fengtai district are much smaller.

Agglomeration of HQ at varied geographical scales

Geographical scales matter when discussing the locationalchoice of firms, as agglomeration factors are working in differentways at varied geographical scales. For example, the knowledgespillover effects may lead to industrial agglomeration only at smallgeographical scales such as zip code areas (Rosenthal & Strange,2001). Thus, it is of importance to take into account the geograph-ical scales of agglomeration in understanding the characteristics ofboth location and agglomeration of HQ.

Applying the L function to calculate scale as related to distance,we learned that HQ in Beijing are significantly agglomerated whenthe search radius is between 0 and 15 km (see Fig. 4). There are twopeaks when the search radii are 1 km and 9–10 km, respectively.This finding shows that some HQ are heavily agglomerated within1 km. The typical HQ clusters are located in the Financial Street,CBD and Zhongguancun, particularly HQ that are in related sectorsand may need frequent face-to-face interactions in order to benefit

from information spillover effects. Furthermore, it also shows thatthe HQ centers in Beijing result from urban economies. This gener-alization applies to most of the HQ within the fourth ring road area(especially in the northern part of Beijing) where the infrastructureis highly developed and related economic activities areconcentrated.

Firm attributes and the geography of HQ: a regression analysis

Geography of HQ of firms of different types

The previous analysis shows that there are multiple centers ofHQ in Beijing. Unexpectedly, many are located in suburban areas,rather than the center of the city (Meyer, 1996). In this section,we explore how firms’ attributes influence the location of a HQ.More specifically, we divide Beijing into the inner and the outercity, separated by the third ring road.8 Firms with HQ located withinthe third ring road, are considered to be center-oriented.

As depicted in Fig. 5, the HQ of firms of larger size are morelikely to locate in the inner city of Beijing. Most have a registeredcapital above 1.6 billion USD (about 10 billion RMB) and arelocated inside the third ring road and, in some cases, inside the sec-ond ring road. The HQ of firms of smaller size (with registered cap-ital less than 0.16 billion USD) are much more scattered. Firm scaleis essential in explaining the location pattern of HQ. The land pricein the inner city is extremely high, so those larger firms are morelikely to be able to afford the higher rents.

Fig. 6 presents the spatial pattern of HQ of firms with differentownerships. Compared to privately-owned firms, a larger propor-tion of HQ of state-owned firms are located inside the third ringroad. In the context of China, state-owned HQ firms may have pref-erential access to land at an abnormally lower price in the innercity. Also some state-owned firms have had the allocated land inthe inner city since they were established. Beijing has morenational state-owned firms than local ones, but the spatial patternsof HQ of the two are quite similar.

Fig. 1. Overall distribution and agglomeration of HQ in Beijing.

3446 45 48 54

0

10

20

30

40

50

60

within the 2rd ring road

between the 2rd and the

2rd ring

between the 3rd and the

4rd ring

between the 4th and the

5rd ring

outside the 5th Ring Road

Num

ber

of H

eadq

uart

ers

Ring Road Posi�on

Fig. 2. Distribution of HQ in varied ring areas.

F. Pan et al. / Cities 42 (2015) 1–12 5

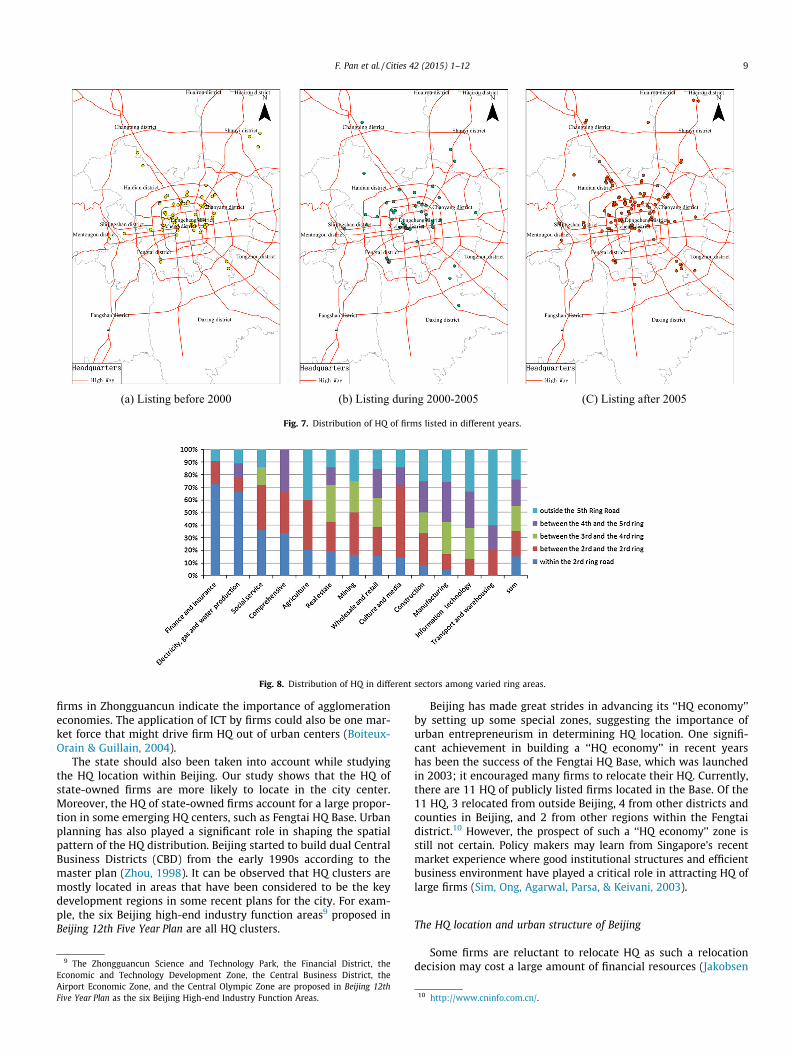

As shown in Fig. 7, firms that became publicly listed in recentyears are more likely to have their HQ located in the outer city. Thischange illustrates the suburbanization of HQ in Beijing recently.During the past decade Beijing has experienced rapid growth inits land prices. The earlier the firms became publicly listed, themore likely they locate their HQ in the inner city when the landprice was still affordable.

The HQ of firms in different sectors have different spatial pat-terns (see Fig. 8). The HQ of firms in the finance and insurance sec-tor are densely concentrated in the inner city. About 70% of the HQof firms in this sector are located inside the second ring road andover 90% inside the third ring road. By contrast, over 50% of theHQ of firms in the manufacturing sector are located outside thefourth ring road. Manufacturing firms often locate their HQ inthe suburbs in order to be close to their production facilities(Henderson & Ono, 2008). Beijing Shougang is a typical case. TheHQ as well as the major manufacturing facilities of the firm arelocated outside the fifth ring road. Admittedly, most manufactur-ing firms with HQ in Beijing have their production facilities locatedin other cities. The HQ of firms in the tertiary industry, such as

(a) Information technology (b) Real Estate

(c) Mining (d) Finance and Insurance

Fig. 3. Degrees of agglomeration of HQ in selected sectors.

6 F. Pan et al. / Cities 42 (2015) 1–12

Table 2Major HQ clusters in Beijing.

HQ clusters Amountof HQ

Sector Ownership Size

1 Finance Street 16 Finance and Insurance 6, Manufacturing 3, Electricity, gas andwater production 2

State-owned 7, localstate-owned 4, private 5

Small 6,medium 2,large 8

2 CBD 10 Real estate 3, Social service 2, Manufacturing 2, Transport andwarehousing 1, Comprehensive 1, Information technology 1

State-owned 4, private 6 Small 5,medium 5

3 Zhongguancun area 16 Information technology 6, Manufacturing 5, Real estate 3 State-owned 8, localstate-owned 1, private 7

Small 6,medium 8,large 2

4 Yizhuang Economic andTechnology Development Zone

10 Manufacturing 7, Information technology 1, Wholesale and Retail 1,Transport and warehousing 1

State-owned 2, localstate-owned 2, private 6

Small 6,medium 3,large 1

5 East Second Ring Road TransportBusiness District

9 Mining 3, Social service 3, Finance and Insurance 1, Construction 1,Culture and media 1

State-owned 7, private 2 Medium 3,large 6

6 Shangdi Information Technologyarea

11 Information technology 7, Manufacturing 3, Mining 1 Private 11 Small 9,medium 2

7 Fengtai Headquarters Base 11 Manufacturing 8, Transport and warehousing 1, Wholesale andRetail 1, Comprehensive 1

State-owned 8, private 3 Small 7,medium 2,large 2

8 Yayuncun Area (including theCentral Olympic Zone)

8 Manufacturing 5, Wholesale and retail 1, Real estate 1, Electricity,gas and water production 1

State-owned 3, localstate-owned 1, private 4

Small 5,medium 2,large 1

9 International ElectronicHeadquarter Base in Chaoyangdistrict

8 Information technology 3, Manufacturing 3, Real estate 1, Cultureand media 1

State-owned 1, localstate-owned 3, private 4

Small 6,medium 2

10 Wangjing InternationalTechnological Business District

5 Manufacturing 2, Construction 2, Information technology 1 State-owned 3, private 2 Small 2,medium 1,large 2

11 Airport Economic Zone 4 Transport and warehousing 2, Real estate 1, Manufacturing 1 State-owned 2, localstate-owned 1, private 1

Small 2,medium 1,large 1

Fig. 4. Degree of agglomeration of HQ at different geographical scales.

F. Pan et al. / Cities 42 (2015) 1–12 7

media and cultural industry and social services, are mainly locatedin the inner city. Exceptions are firms in the transport and ware-housing and information technology industry. Over 80% of HQ inthese two sectors are located outside the third ring road. The HQof firms in the information technology industry are inclined to beclose to top research institutes and universities, which are mostlylocated outside the fourth ring road in Beijing. While the HQ offirms in the transport and warehousing industry are more likelyto be located in the outer city, because they need larger spaceand to be close to transport nodes.

Regression and results

A logistic regression model is used to test the importance offirms’ attributes in determining their HQ’s location. The dependentvariable is a dummy which is assigned to be 1 if the HQ is located

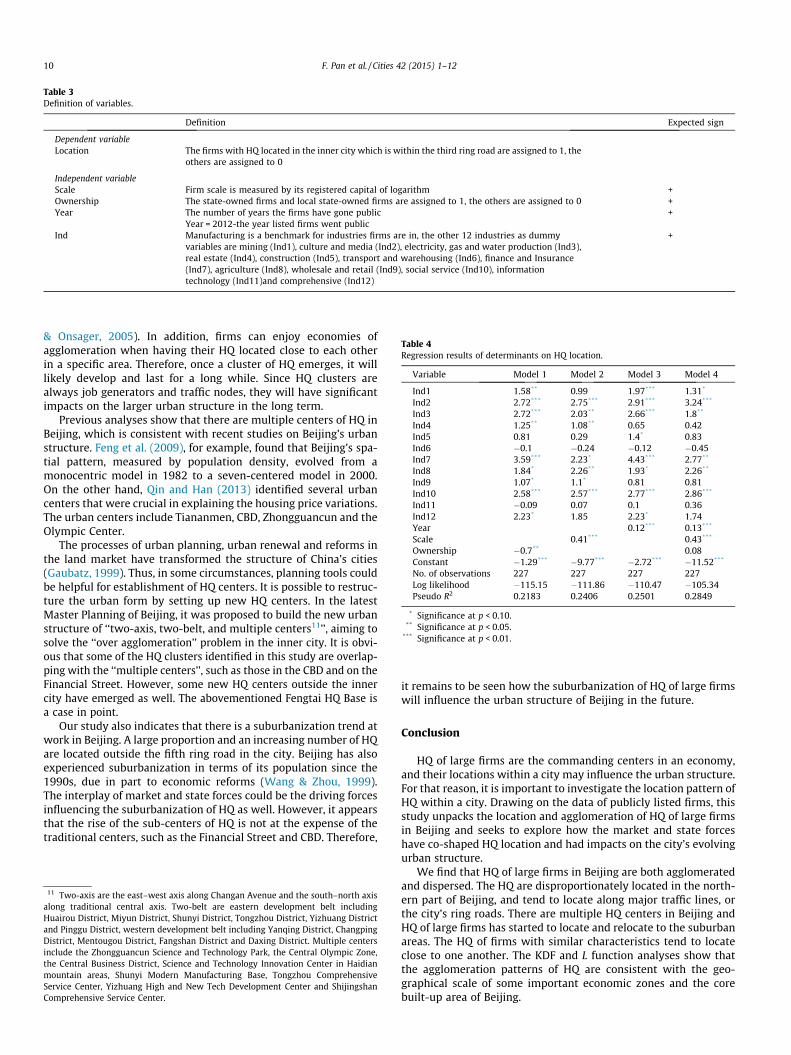

in the inner city, otherwise it is 0. The definitions of all variablesare presented in Table 3.

Due to the high correlation between Scale, Ownership and Year,model 1, model 2 and model 3 include only one of these three vari-ables and model 4 includes all of them. The results of the regressionsare shown in Table 4; they are consistent with previous analysis.The results indicate that the HQ of firms in most sectors are inclinedto locate in the inner city compared to those of the manufacturingsector. The HQ of firms in the service sectors, such as the cultureand media industry, finance and insurance and social service, areespecially center-oriented (the coefficients of Ind are all positiveand statistically significant). In addition, agriculture and gas andwater production firms are also significantly center-oriented.

After controlling the sector of the firms, the scale and public list-ing year of firms have a significant impact over the HQ location. Theresults show that firms of larger size and being publicly listing

(a) Below 0.16 billion USD(1 billion RMB)

(b) Between0.16 and 1.6 billion USD(1 and 10 billion RMB)

(C) Above 1.6 billion USD(10 billion RMB)

Fig. 5. Distribution of HQ of firms with different size (measured by registered capital). (The exchange rate in the end of 2011 was 6.3009 Yuan RMB per US Dollar, which isapplied in the calculation.)

(a) Local State-owned (b) National State-owned (C) Others

Fig. 6. Distribution of HQ of firms of different ownership.

8 F. Pan et al. / Cities 42 (2015) 1–12

earlier are more likely to locate their HQ within the inner city. Whenall three variables are included in the regression (see model 4), thecoefficients of Scale and Year remain statistically significant. Thesign of Ownership is not as expected after controlling other factors.

Discussion

The interplay between the market and state forces in determining HQlocation

Our findings confirm that the HQ locations within Beijing haveresulted from an interplay between the market and state forces.Market forces play critical roles in determining these locations.

The regression results show that smaller firms and newer firmsare more likely to locate farther from the urban centers, indicatingthat land price influences HQ location. HQ are also attracted byspecific regional resources. Partly due to its atmosphere of innova-tion and high level concentration of talents, Zhongguancun hasbecome one of the major HQ clusters of firms in the informationtechnology sector. Another example is in Beijing’s CBD. Being adja-cent to the embassy district of Beijing, it attracted many multina-tional corporations and high-end producer service companies. Thebusiness atmosphere in this area, shaped by global actors(Melchert Saguas Presas, 2004), is crucial for attracting the HQ ofdomestic firms. In addition, the agglomeration of HQ of financialfirms on the Financial Street and of HQ of information technology

(a) Listing before 2000 (b) Listing during 2000-2005 (C) Listing after 2005

Fig. 7. Distribution of HQ of firms listed in different years.

Fig. 8. Distribution of HQ in different sectors among varied ring areas.

F. Pan et al. / Cities 42 (2015) 1–12 9

firms in Zhongguancun indicate the importance of agglomerationeconomies. The application of ICT by firms could also be one mar-ket force that might drive firm HQ out of urban centers (Boiteux-Orain & Guillain, 2004).

The state should also been taken into account while studyingthe HQ location within Beijing. Our study shows that the HQ ofstate-owned firms are more likely to locate in the city center.Moreover, the HQ of state-owned firms account for a large propor-tion in some emerging HQ centers, such as Fengtai HQ Base. Urbanplanning has also played a significant role in shaping the spatialpattern of the HQ distribution. Beijing started to build dual CentralBusiness Districts (CBD) from the early 1990s according to themaster plan (Zhou, 1998). It can be observed that HQ clusters aremostly located in areas that have been considered to be the keydevelopment regions in some recent plans for the city. For exam-ple, the six Beijing high-end industry function areas9 proposed inBeijing 12th Five Year Plan are all HQ clusters.

9 The Zhongguancun Science and Technology Park, the Financial District, theEconomic and Technology Development Zone, the Central Business District, theAirport Economic Zone, and the Central Olympic Zone are proposed in Beijing 12thFive Year Plan as the six Beijing High-end Industry Function Areas.

Beijing has made great strides in advancing its ‘‘HQ economy’’by setting up some special zones, suggesting the importance ofurban entrepreneurism in determining HQ location. One signifi-cant achievement in building a ‘‘HQ economy’’ in recent yearshas been the success of the Fengtai HQ Base, which was launchedin 2003; it encouraged many firms to relocate their HQ. Currently,there are 11 HQ of publicly listed firms located in the Base. Of the11 HQ, 3 relocated from outside Beijing, 4 from other districts andcounties in Beijing, and 2 from other regions within the Fengtaidistrict.10 However, the prospect of such a ‘‘HQ economy’’ zone isstill not certain. Policy makers may learn from Singapore’s recentmarket experience where good institutional structures and efficientbusiness environment have played a critical role in attracting HQ oflarge firms (Sim, Ong, Agarwal, Parsa, & Keivani, 2003).

The HQ location and urban structure of Beijing

Some firms are reluctant to relocate HQ as such a relocationdecision may cost a large amount of financial resources (Jakobsen

10 http://www.cninfo.com.cn/.

Table 3Definition of variables.

Definition Expected sign

Dependent variableLocation The firms with HQ located in the inner city which is within the third ring road are assigned to 1, the

others are assigned to 0

Independent variableScale Firm scale is measured by its registered capital of logarithm +Ownership The state-owned firms and local state-owned firms are assigned to 1, the others are assigned to 0 +Year The number of years the firms have gone public +

Year = 2012-the year listed firms went publicInd Manufacturing is a benchmark for industries firms are in, the other 12 industries as dummy

variables are mining (Ind1), culture and media (Ind2), electricity, gas and water production (Ind3),real estate (Ind4), construction (Ind5), transport and warehousing (Ind6), finance and Insurance(Ind7), agriculture (Ind8), wholesale and retail (Ind9), social service (Ind10), informationtechnology (Ind11)and comprehensive (Ind12)

+

Table 4Regression results of determinants on HQ location.

Variable Model 1 Model 2 Model 3 Model 4

Ind1 1.58** 0.99 1.97*** 1.31*

Ind2 2.72*** 2.75*** 2.91*** 3.24***

Ind3 2.72*** 2.03** 2.66*** 1.8**

Ind4 1.25** 1.08** 0.65 0.42Ind5 0.81 0.29 1.4* 0.83Ind6 �0.1 �0.24 �0.12 �0.45Ind7 3.59*** 2.23* 4.43*** 2.77**

Ind8 1.84* 2.26** 1.93* 2.26**

Ind9 1.07* 1.1* 0.81 0.81Ind10 2.58*** 2.57*** 2.77*** 2.86***

Ind11 �0.09 0.07 0.1 0.36Ind12 2.23* 1.85 2.23* 1.74Year 0.12*** 0.13***

Scale 0.41*** 0.43***

Ownership �0.7** 0.08Constant �1.29*** �9.77*** �2.72*** �11.52***

No. of observations 227 227 227 227Log likelihood �115.15 �111.86 �110.47 �105.34Pseudo R2 0.2183 0.2406 0.2501 0.2849

* Significance at p < 0.10.** Significance at p < 0.05.

*** Significance at p < 0.01.

10 F. Pan et al. / Cities 42 (2015) 1–12

& Onsager, 2005). In addition, firms can enjoy economies ofagglomeration when having their HQ located close to each otherin a specific area. Therefore, once a cluster of HQ emerges, it willlikely develop and last for a long while. Since HQ clusters arealways job generators and traffic nodes, they will have significantimpacts on the larger urban structure in the long term.

Previous analyses show that there are multiple centers of HQ inBeijing, which is consistent with recent studies on Beijing’s urbanstructure. Feng et al. (2009), for example, found that Beijing’s spa-tial pattern, measured by population density, evolved from amonocentric model in 1982 to a seven-centered model in 2000.On the other hand, Qin and Han (2013) identified several urbancenters that were crucial in explaining the housing price variations.The urban centers include Tiananmen, CBD, Zhongguancun and theOlympic Center.

The processes of urban planning, urban renewal and reforms inthe land market have transformed the structure of China’s cities(Gaubatz, 1999). Thus, in some circumstances, planning tools couldbe helpful for establishment of HQ centers. It is possible to restruc-ture the urban form by setting up new HQ centers. In the latestMaster Planning of Beijing, it was proposed to build the new urbanstructure of ‘‘two-axis, two-belt, and multiple centers11’’, aiming tosolve the ‘‘over agglomeration’’ problem in the inner city. It is obvi-ous that some of the HQ clusters identified in this study are overlap-ping with the ‘‘multiple centers’’, such as those in the CBD and on theFinancial Street. However, some new HQ centers outside the innercity have emerged as well. The abovementioned Fengtai HQ Base isa case in point.

Our study also indicates that there is a suburbanization trend atwork in Beijing. A large proportion and an increasing number of HQare located outside the fifth ring road in the city. Beijing has alsoexperienced suburbanization in terms of its population since the1990s, due in part to economic reforms (Wang & Zhou, 1999).The interplay of market and state forces could be the driving forcesinfluencing the suburbanization of HQ as well. However, it appearsthat the rise of the sub-centers of HQ is not at the expense of thetraditional centers, such as the Financial Street and CBD. Therefore,

11 Two-axis are the east–west axis along Changan Avenue and the south–north axisalong traditional central axis. Two-belt are eastern development belt includingHuairou District, Miyun District, Shunyi District, Tongzhou District, Yizhuang Districtand Pinggu District, western development belt including Yanqing District, ChangpingDistrict, Mentougou District, Fangshan District and Daxing District. Multiple centersinclude the Zhongguancun Science and Technology Park, the Central Olympic Zone,the Central Business District, Science and Technology Innovation Center in Haidianmountain areas, Shunyi Modern Manufacturing Base, Tongzhou ComprehensiveService Center, Yizhuang High and New Tech Development Center and ShijingshanComprehensive Service Center.

it remains to be seen how the suburbanization of HQ of large firmswill influence the urban structure of Beijing in the future.

Conclusion

HQ of large firms are the commanding centers in an economy,and their locations within a city may influence the urban structure.For that reason, it is important to investigate the location pattern ofHQ within a city. Drawing on the data of publicly listed firms, thisstudy unpacks the location and agglomeration of HQ of large firmsin Beijing and seeks to explore how the market and state forceshave co-shaped HQ location and had impacts on the city’s evolvingurban structure.

We find that HQ of large firms in Beijing are both agglomeratedand dispersed. The HQ are disproportionately located in the north-ern part of Beijing, and tend to locate along major traffic lines, orthe city’s ring roads. There are multiple HQ centers in Beijing andHQ of large firms has started to locate and relocate to the suburbanareas. The HQ of firms with similar characteristics tend to locateclose to one another. The KDF and L function analyses show thatthe agglomeration patterns of HQ are consistent with the geo-graphical scale of some important economic zones and the corebuilt-up area of Beijing.

F. Pan et al. / Cities 42 (2015) 1–12 11

Specific attributes of firms may also influence the location pat-tern of HQ. Based on mapping and logistic regression analysis, wefind that firms that are larger, state-owned and listed in earlieryears are more likely to be city-center-oriented. Also the HQ offirms in the finance, insurance and other services are more likelyto locate in the inner city, while those in the manufacturing andinformation technology sectors would locate in the outer city.

This paper has provided a preliminary research in understand-ing the geography of HQ of large firms within an emerging worldcity in a transitional economy. The agglomeration of HQ is persis-tent and take place due partly to the interplay between the marketand state forces, among which agglomeration economies andurban planning are the most important. Given the importance ofHQ of large firms in shaping urban structure, it is possible to applyplanning tools to direct the future location choices of HQ and alsoto help solve the challenges facing the city’s future. This study alsosheds some light on how to advance the ‘‘HQ economy’’ for othercities in which market power might play a more important rolein HQ location decision.

Funding

This research was funded by the National Science Foundation ofChina [No. 41201107], the Fundamental Research Funds for theCentral Universities [No. 2012LYB36] and the Key Laboratory ofRegional Sustainable Development Modeling, Institute of Geo-graphical Sciences and Natural Resources Research, Chinese Acad-emy of Sciences.

Acknowledgments

We thank the editor and three anonymous reviewers for theirconstructive comments and suggestions on earlier versions of thismanuscript. We also thank Prof. Stan Brunn and Dr. Shengjun Zhufor their helpful suggestions.

References

Bel, G., & Fageda, X. (2008). Getting there fast: Globalization, intercontinental flightsand location of headquarters. Journal of Economic Geography, 8, 471–495.

Besag, J. (1977). Comments on Ripley’s paper. Journal of the Royal Statistical SocietySeries B – Statistics in Society, 39, 193–195.

Boiteux-Orain, C., & Guillain, R. (2004). Changes in the intrametropolitan location ofproducer services in Île-De-France (1978–1997): Do information technologiespromote a more dispersed spatial pattern? Urban Geography, 25, 550–578.

Chan, C.-P., & Poon, W.-K. (2011). The Chinese local administrative measures forbuilding up the ‘Headquarter Economy’: A comparison between Pudong andShenzhen. Journal of Contemporary China, 21, 149–167.

Chubarov, I., & Brooker, D. (2013). Multiple pathways to global city formation: Afunctional approach and review of recent evidence in China. Cities, 35, 181–189.

Csomós, G. (2013). The command and control centers of the United States (2006/2012): An analysis of industry sectors influencing the position of cities.Geoforum, 50, 241–251.

Daniels, P. W. (1975). Office location: An urban and regional study. London: Bell.Davis, J. C., & Henderson, J. V. (2008). The agglomeration of headquarters. Regional

Science and Urban Economics, 38, 445–460.Drennan, M. P., & Kelly, H. F. (2011). Measuring urban agglomeration economies

with office rents. Journal of Economic Geography, 11, 481–507.Duranton, G., & Puga, D. (2004). Micro-foundations of urban agglomeration

economies. Handbook of regional and urban economics (pp. 2063–2117).Feng, J., Wang, F., & Zhou, Y. (2009). The spatial restructuring of population in

metropolitan Beijing: Toward polycentricity in the post-reform era. UrbanGeography, 30, 779–802.

Gaubatz, P. (1995). Changing Beijing. Geographical Review, 85, 79–96.Gaubatz, P. (1999). China’s urban transformation: Patterns and processes of

morphological change in Beijing, Shanghai and Guangzhou. Urban Studies, 36,1495–1521.

Godfrey, B. J., & Zhou, Y. (1999). Ranking world cities: Multinational corporationsand the global urban hierarchy. Urban Geography, 20, 268–281.

Han, S. S. (2000). Shanghai between state and market in urban transformation.Urban Studies, 37, 2091–2112.

Henderson, J. V., & Ono, Y. (2008). Where do manufacturing firms locate theirheadquarters? Journal of Urban Economics, 63, 431–450.

Holloway, S. R., & Wheeler, J. O. (1991). Corporate headquarters relocation andchanges in metropolitan corporate dominance, 1980–1987. EconomicGeography, 67, 54–74.

Jakobsen, S. E., & Onsager, K. (2005). Head office location: Agglomeration, clusters orflow nodes? Urban Studies, 42, 1517–1535.

Klier, T. H. (2006). Where the headquarters are: Location patterns of large publiccompanies, 1990–2000. Economic Development Quarterly, 20, 117–128.

Klier, T. H., & Testa, W. (2001). Headquarters wanted: Principals only need apply.Chicago Fed Letter, 1–4.

Lin, G. C. S. (2007). Reproducing spaces of Chinese urbanisation: New city-based andland-centred urban transformation. Urban Studies, 44, 1827–1855.

Lovely, M. E., Rosenthal, S. S., & Sharma, S. (2005). Information, agglomeration, andthe headquarters of U.S. exporters. Regional Science and Urban Economics, 35,167–191.

Melchert Saguas Presas, L. (2004). Transnational urban spaces and urbanenvironmental reforms: Analyzing Beijing’s environmental restructuring inthe light of globalization. Cities, 21, 321–328.

Meyer, S. P. (1996). Canadian multinational headquarters: The importance ofToronto’s inner city. Great Lakes Geographer, 3, 1–12.

Meyer, S., & Green, M. (2003). Headquarters in Canada: An analysis of spatialpatterns. Urban Geography, 24, 232–252.

Naughton, B. (2011). China’s economic policy today: The new state activism.Eurasian Geography and Economics, 52, 313–329.

Pan, F., & Xia, Y. (2014). Location and agglomeration of headquarters of publiclylisted firms within China’s urban system. Urban Geography, 1–23.

Pan, F., Xia, Y., & Liu, Z. (2013). The relocation of headquarters of public listed firmsin China: A regional perspective study. Acta Geographica Sinica, 68, 449–463.

Qin, B., & Han, S. S. (2013). Emerging polycentricity in Beijing: Evidence fromhousing price variations, 2001–2005. Urban Studies, 50, 2006–2023.

Rice, M. (2010). The urban geography of subsidiary headquarters in North America:Explorations by sector and Foreign Linkage. Urban Geography, 31, 595–622.

Rice, M. D., & Lyons, D. I. (2010). Geographies of corporate decision-making andcontrol: Development, applications, and future directions in headquarterslocation research. Geography Compass, 4, 320–334.

Ripley, B. D. (1977). Modelling spatial patterns. Journal of the Royal Statistical Society.Series B (Methodological), 172–212.

Rosenthal, S. S., & Strange, W. C. (2004). Evidence on the nature and sources ofagglomeration economies. Handbook of regional and urban economics (pp. 2119–2171).

Rosenthal, S. S., & Strange, W. C. (2001). The determinants of agglomeration. Journalof Urban Economics, 50, 191–229.

Shin, H. B. (2009). Residential redevelopment and the entrepreneurial local state:The implications of Beijing’s shifting emphasis on urban redevelopmentpolicies. Urban Studies, 46, 2815–2839.

Silverman, B. W. (1986). Density estimation for statistics and data analysis. New York:Chapman and Hall.

Sim, L.-L., Ong, S.-E., Agarwal, A., Parsa, A., & Keivani, R. (2003). Singapore’scompetitiveness as a global city: Development strategy, institutions andbusiness environment. Cities, 20, 115–127.

Strauss-Kahn, V., & Vives, X. (2009). Why and where do headquarters move?Regional Science and Urban Economics, 39, 168–186.

Taylor, P. J., & Csomós, G. (2012). Cities as control and command centres: Analysisand interpretation. Cities, 29, 408–411.

Taylor, P. J., Ni, P., Derudder, B., Hoyler, M., Huang, J., Lu, F., Pain, K., Witlox, F., Yang,X., & Bassens, D. (2009). The way we were: Command-and-control centres inthe global space-economy on the eve of the 2008 geo-economic transition.Environment and Planning A, 41, 7–12.

Testa, W. A. (2006). Headquarters research and implications for local development.Economic Development Quarterly, 20, 111–116.

Tonts, M., & Taylor, M. (2010). Corporate location, concentration and performance:Large company headquarters in the Australian urban system. Urban Studies, 47,2641–2664.

Tonts, M., & Taylor, M. (2011). The shifting geography of corporate headquarters inAustralia: A longitudinal analysis. Regional Studies, 1–16.

Wang, D. T., Zhao, S. X., Gu, F. F., & Chen, W. Y. (2011). Power or market? Locationdeterminants of multinational headquarters in China. Environment and PlanningA, 43, 2364–2383.

Wang, F., & Zhou, Y. (1999). Modelling urban population densities in Beijing 1982–1990: Suburbanisation and its causes. Urban Studies, 36, 271–287.

Wei, Y. D., & Yu, D. (2006). State policy and the globalization of Beijing: Emergingthemes. Habitat International, 30, 377–395.

Wu, F. (2002). China’s changing urban governance in the transition towards a moremarket-oriented economy. Urban Studies, 39, 1071–1093.

Wu, Q., & Ning, Y. (2010). Headquarter locations of top 500 enterprises of Chinesemanufacturing industries. Acta Geographica Sinica, 65, 139–152.

Yang, J., Shen, Q., Shen, J., & He, C. (2012). Transport impacts of clustereddevelopment in Beijing: Compact development versus overconcentration.Urban Studies, 49, 1315–1331.

Zhang, L.-Y. (2003). Economic development in Shanghai and the role of the state.Urban Studies, 40, 1549–1572.

Zhang, G. (2013). Research on the development strategy of the capital. Beijing: ChinaPopulation Publishing House.

12 F. Pan et al. / Cities 42 (2015) 1–12

Zhang, L.-Y. (2013). Dynamics and constraints of state-led global city formation inemerging economies: The case of Shanghai. Urban Studies.

Zhao, S. X. B. (2003). Spatial restructuring of financial centers in Mainland China andHong Kong: A geography of finance perspective. Urban Affairs Review, 38,535–571.

Zhao, S. X. B. (2013). Information exchange, headquarters economy and financialcenters development: Shanghai, Beijing and Hong Kong. Journal of ContemporaryChina, 1–22.

Zhao, S. X. B., Cai, J., & Zhang, L. (2005). Asymmetric information as a keydeterminant for locational choice of MNC headquarters and the development offinancial centers: A case for China. China Economic Review, 16, 308–331.

Zhao, S. X. B., Zhang, L., & Wang, D. T. (2004). Determining factors of thedevelopment of a national financial center: The case of China. Geoforum, 35,577–592.

Zhou, Y. U. (1998). Beijing and the development of dual central business districts.Geographical Review, 88, 429–436.