building a brand we love - nielsen.com · social media segmentation customer service usage and...

TRANSCRIPT

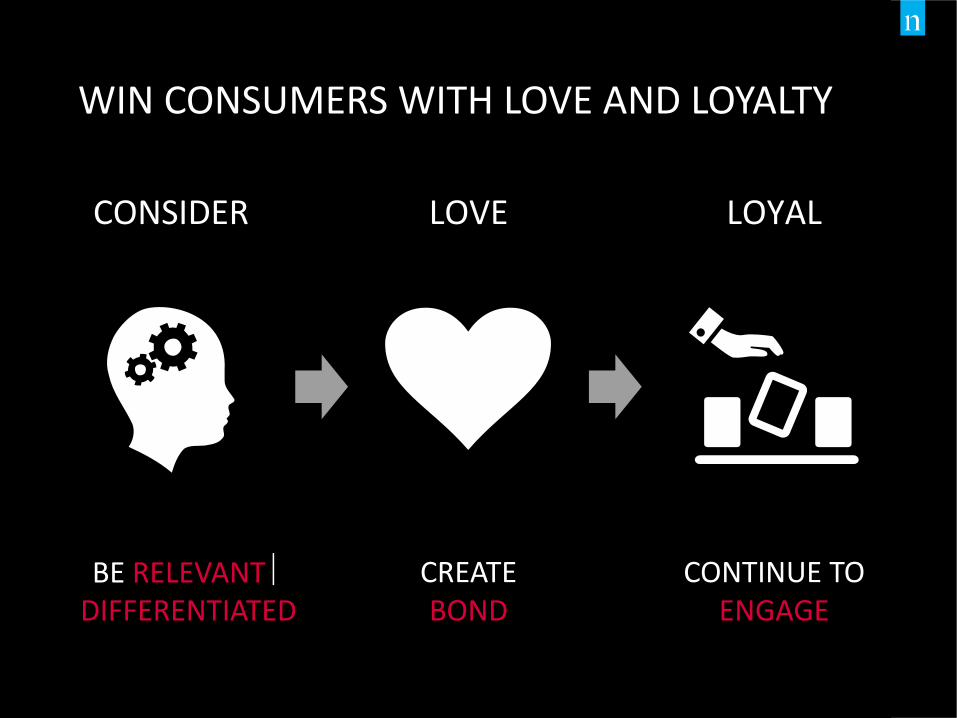

WINNING CONSUMERS’ HEARTS AND MINDS

BUILDING A BRAND WE LOVE

CONSIDER LOVE LOYAL

BE RELEVANT DIFFERENTIATED

CREATEBOND

CONTINUE TO ENGAGE

WIN CONSUMERS WITH LOVE AND LOYALTY

HOW WE INTERACT WITH BRANDS YESTERDAY IS DIFFERENT TODAY, EVOLVED TOMORROW

Every consumer is the same

Every consumer is different

Mass Marketing

Viral and Real-time Marketing

Single Screen Multiscreen

FROM TO

Store Retailing Online Shopping

TV Primetime Interactive and Embedded Advertising

HOW DO YOU STAND OUT IN YOUR CATEGORY?

DRIVE BRAND EQUITY AND BUSINESS PERFORMANCE

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

5

HEALTH CHECK

ACTIVATIONCATEGORIES

FORESIGHT

BRAND BUILDER

THAT’S WHERE WE COME INComplete diagnosis of a brand’s health, envision your future state and help you develop strategies for continued success and prosperity of your brand

RETAIL MANAGEMENT

HOMESCAN

SOCIAL MEDIA

SEGMENTATION

CUSTOMER SERVICE

USAGE AND ATTITUDE

MEDIA/BRAND EFFECT

PROGNOSIS

COMMUNICATIONS

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

6

HELP YOU SEE AROUND THE NEXT CORNER

MAKE YOUR AD WORK HARDER

PROVIDEBRAND FORESIGHT

LEVERAGE GROWTH & IDENTIFY VULNERABILITIES

ACTIVATE BRAND ACROSS TOUCH POINTS

CONNECT THE DOTS

360BRAND VIEW

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

7

LET’S DIVE INTO THE DETAILS

Deliver Brand Foresight

Making Your Ad Work Harder

Activate Brand Across Touch Points

360 Brand View

CAPTURE 360 BRAND VIEW

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

9

BRANDS DO NOT OPERATE IN ISOLATIONStart by evaluating your category health and identifying issues surrounding your brand

NEW CATEGORY

SHRINKING CATEGORYHas it affected your brand?

CATEGORY UNDER THREAT How do you defend?

WE HELP YOU MANAGE YOUR BRAND IN THE CATEGORY CONTEXT

GROWING CATEGORYHow do you leverage?

CATEGORY X

ALTERNATIVE Z

ALTERNATIVE Y

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

10

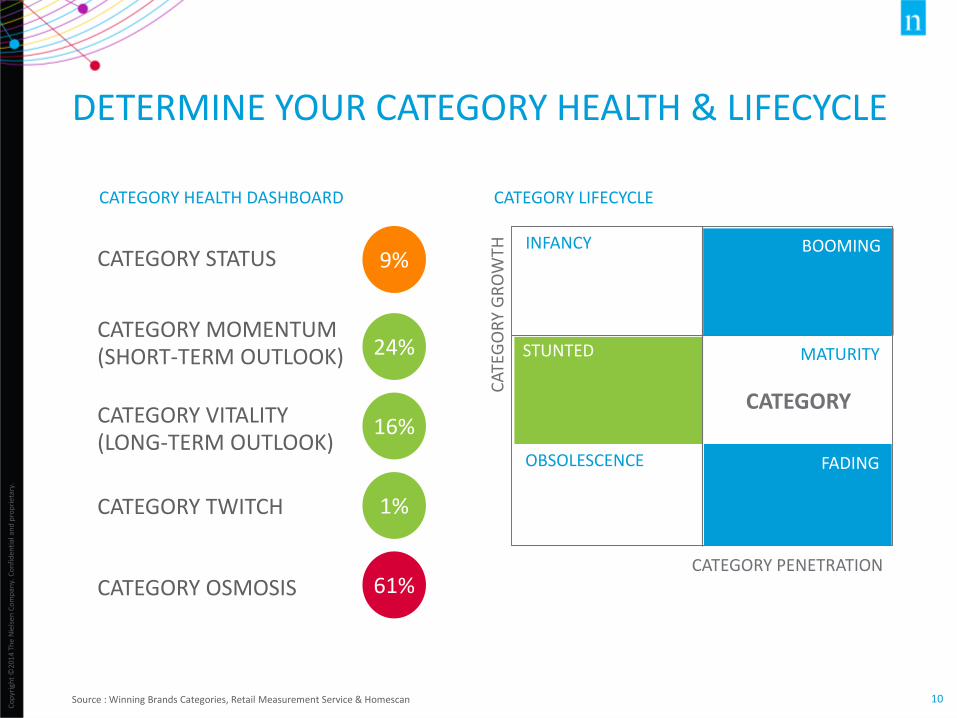

DETERMINE YOUR CATEGORY HEALTH & LIFECYCLE

Source : Winning Brands Categories, Retail Measurement Service & Homescan

CATEGORY STATUS

CATEGORY VITALITY (LONG-TERM OUTLOOK)

CATEGORY MOMENTUM (SHORT-TERM OUTLOOK)

CATEGORY TWITCH

CATEGORY OSMOSIS

9%

24%

16%

1%

61%CATEGORY PENETRATION

CA

TEG

OR

Y G

RO

WTH INFANCY

STUNTED

OBSOLESCENCE

BOOMING

MATURITY

FADING

CATEGORY

CATEGORY LIFECYCLECATEGORY HEALTH DASHBOARD

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

11

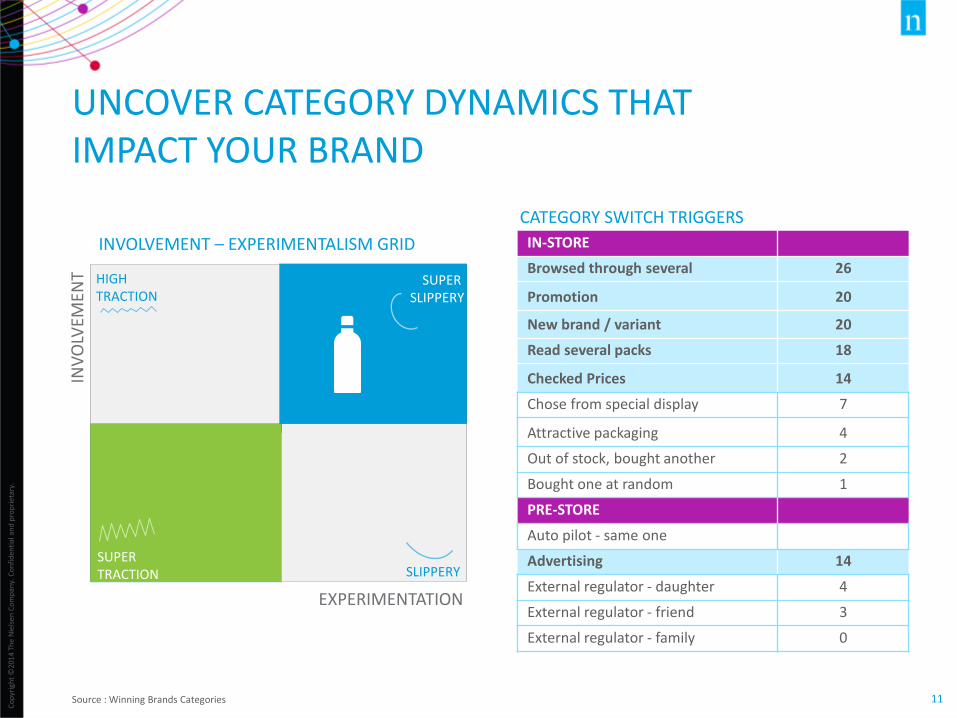

UNCOVER CATEGORY DYNAMICS THAT IMPACT YOUR BRAND

CATEGORY SWITCH TRIGGERS

IN-STORE

Browsed through several 26

Promotion 20

New brand / variant 20

Read several packs 18

Checked Prices 14

Chose from special display 7

Attractive packaging 4

Out of stock, bought another 2

Bought one at random 1

PRE-STORE

Auto pilot - same one

Advertising 14

External regulator - daughter 4

External regulator - friend 3

External regulator - family 0

SUPER TRACTION

SUPER SLIPPERY

SLIPPERY

HIGH TRACTION

EXPERIMENTATION

INV

OLV

EMEN

T

INVOLVEMENT – EXPERIMENTALISM GRID

Source : Winning Brands Categories

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

12

KEEP TABS OF YOUR BRAND HEALTHMeasure your brand’s ability to win consumers’ minds and hearts

CONSIDERATION

QUALITY

FAMILIARITY

AFFIRMATION

CONNECTION

PREFERENCE

BRAND STRENGTH

BRAND EQUITY

Source : Winning Brands Health Check

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

13

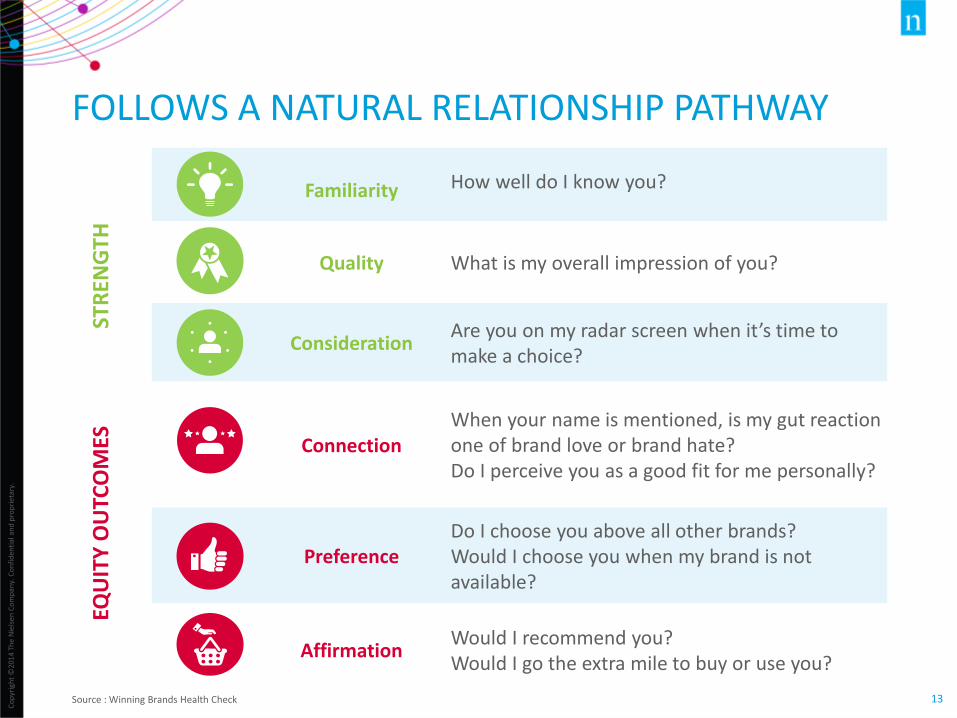

FOLLOWS A NATURAL RELATIONSHIP PATHWAY

Familiarity How well do I know you?

Quality What is my overall impression of you?

ConsiderationAre you on my radar screen when it’s time to make a choice?

ConnectionWhen your name is mentioned, is my gut reaction one of brand love or brand hate?Do I perceive you as a good fit for me personally?

PreferenceDo I choose you above all other brands?Would I choose you when my brand is not available?

AffirmationWould I recommend you?Would I go the extra mile to buy or use you?

STR

ENG

THEQ

UIT

Y O

UTC

OM

ES

Source : Winning Brands Health Check

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

14

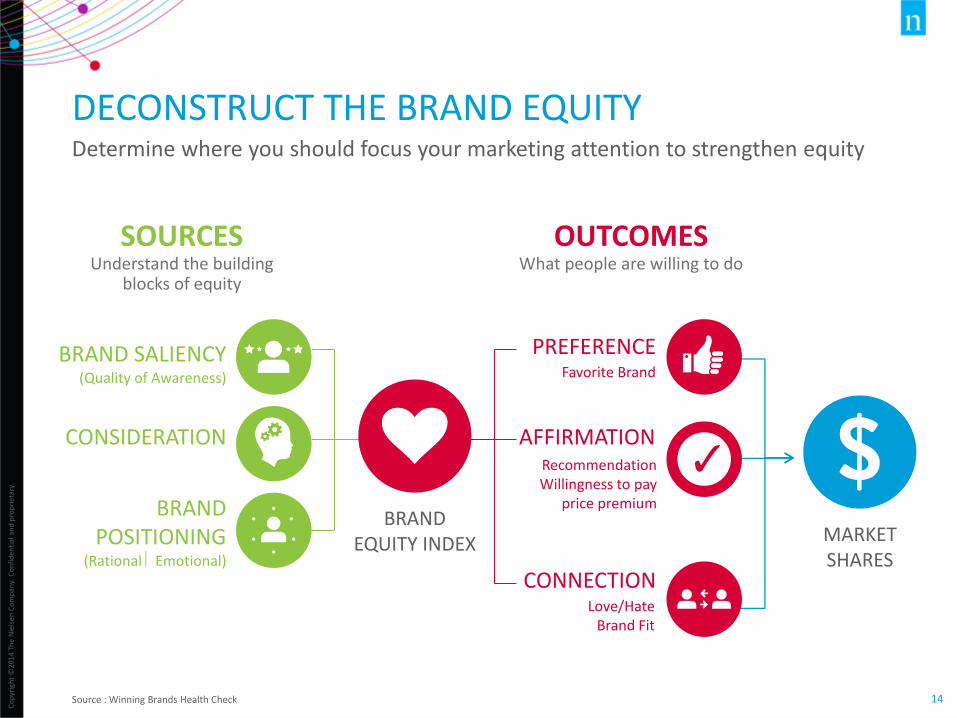

DECONSTRUCT THE BRAND EQUITYDetermine where you should focus your marketing attention to strengthen equity

OUTCOMESWhat people are willing to do

SOURCESUnderstand the building

blocks of equity

BRAND SALIENCY(Quality of Awareness)

CONSIDERATION

BRAND POSITIONING

(Rational Emotional)

Love/HateBrand Fit

RecommendationWillingness to pay

price premium

Favorite Brand

PREFERENCE

AFFIRMATION

CONNECTION

BRAND EQUITY INDEX MARKET

SHARES

Source : Winning Brands Health Check

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

15

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0

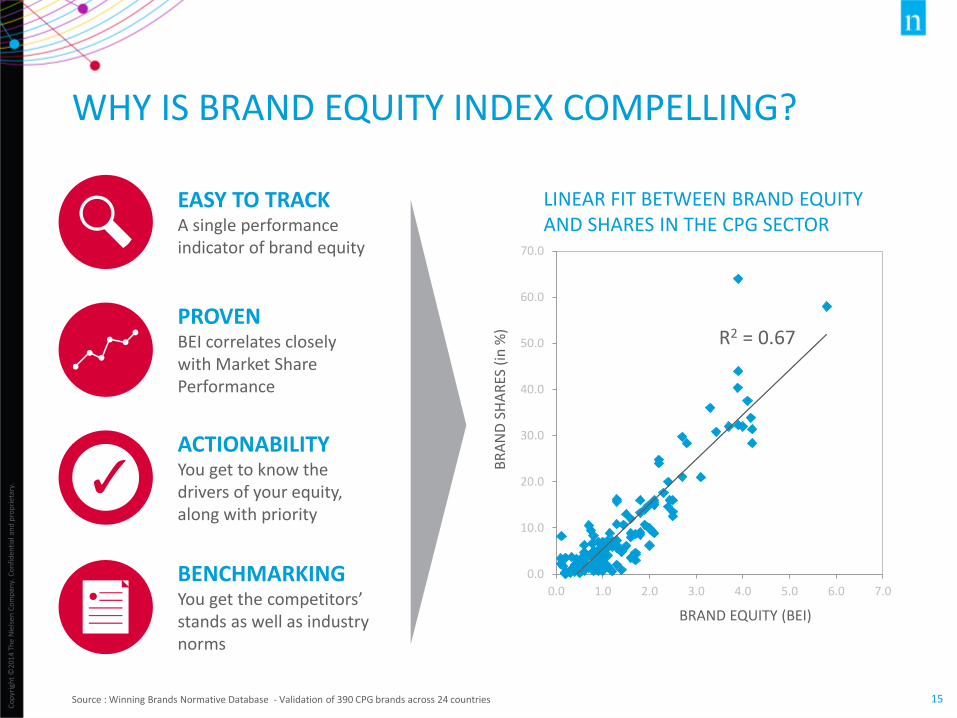

WHY IS BRAND EQUITY INDEX COMPELLING?

LINEAR FIT BETWEEN BRAND EQUITY AND SHARES IN THE CPG SECTOR

BRAND EQUITY (BEI)

BR

AN

D S

HA

RES

(in

%)

EASY TO TRACKA single performance indicator of brand equity

BENCHMARKINGYou get the competitors’ stands as well as industry norms

ACTIONABILITYYou get to know the drivers of your equity, along with priority

PROVENBEI correlates closely with Market Share Performance

Source : Winning Brands Normative Database - Validation of 390 CPG brands across 24 countries

R2 = 0.67

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

16

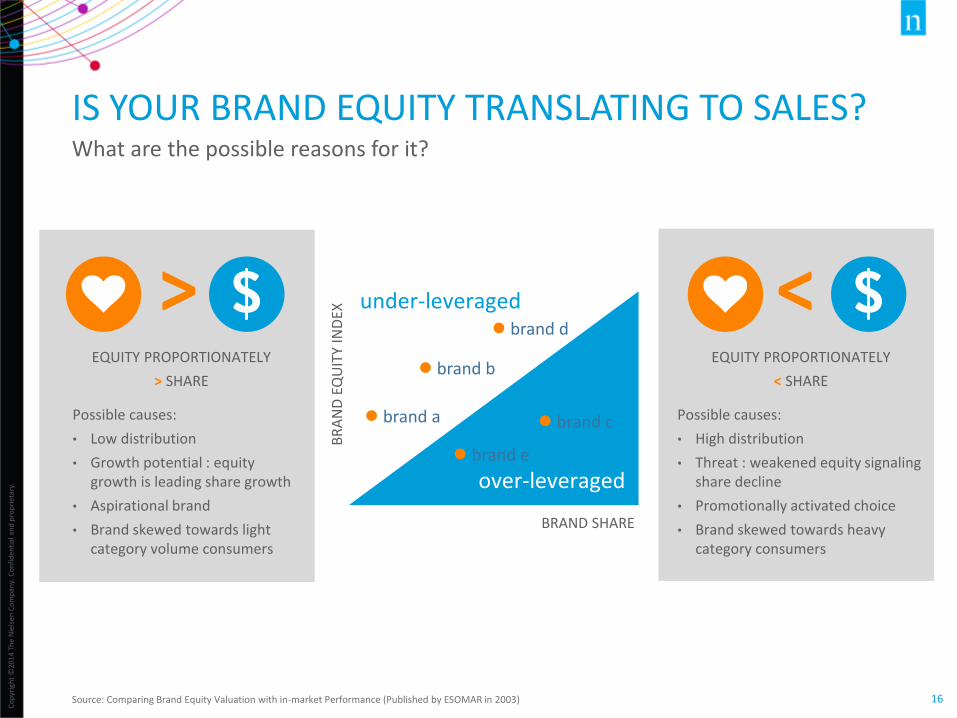

IS YOUR BRAND EQUITY TRANSLATING TO SALES?What are the possible reasons for it?

Source: Comparing Brand Equity Valuation with in-market Performance (Published by ESOMAR in 2003)

Possible causes:

• Low distribution

• Growth potential : equity growth is leading share growth

• Aspirational brand

• Brand skewed towards light category volume consumers

EQUITY PROPORTIONATELY

> SHARE

Possible causes:

• High distribution

• Threat : weakened equity signaling share decline

• Promotionally activated choice

• Brand skewed towards heavy category consumers

EQUITY PROPORTIONATELY

< SHARE

BRAND SHARE

BR

AN

D E

QU

ITY

IND

EX

under-leveraged

brand b

brand d

brand a brand c

brand e

over-leveraged

< >

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

17

40

41

31

46

85

93

41

6

36 22

WHERE IS YOUR BRAND LOSING ITS FRANCHISE?

RECOMMENDERS(recommend the brand to others)

(prefer the brand over competitors)

(use brand most often)

(regularly use brand)

(regular use/will consider buying in future)

(have tried it)

(will not consider brand)

HIGHCOMMITMENT

LOW COMMITMENT

(top of mind, spont, total awareness)Achieving

brand saliency

Providingbrand relevance

Ensuringbrand performance

Ensuringemotional loyalty

NON-CONSIDERERS

AWARERS

CONSIDERERS

TRIALISTS

REGULARS

DEPENDABLES

PREFERERS

Source : Winning Brands Health Check

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

18

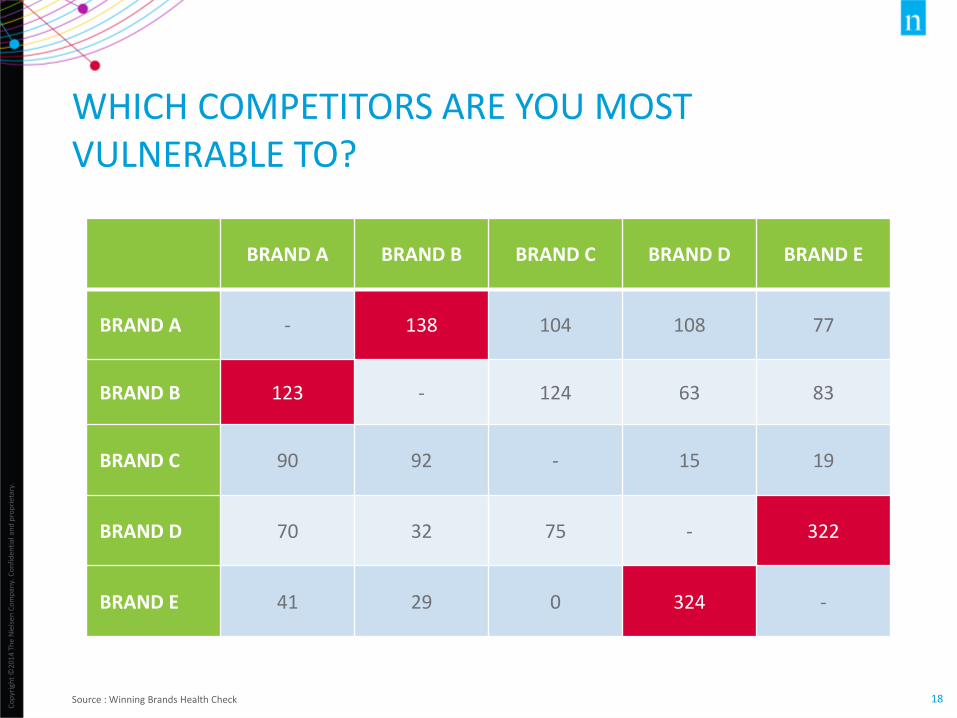

WHICH COMPETITORS ARE YOU MOST VULNERABLE TO?

BRAND A BRAND B BRAND C BRAND D BRAND E

BRAND A - 138 104 108 77

BRAND B 123 - 124 63 83

BRAND C 90 92 - 15 19

BRAND D 70 32 75 - 322

BRAND E 41 29 0 324 -

Source : Winning Brands Health Check

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

19

DEVELOP BRAND STRATEGIES FOR YOUR STATUREAre you a champion, challenger, niche, occasional, struggler or unfamiliar? What are the implications?

BRAND STATURE

BR

AN

D D

EPTH

BRAND SPAN

BRAND SPAN

• familiarity

• penetration

BRAND DEPTH

• emotive loyalty

• behavioral loyalty

CHAMPION

Maintain position through continual investment

CHALLENGER

Spread the good news while remaining true to proposition

NICHE

Reinforcing current strengths or broaden franchise

UNFAMILIAR

Establish both brand span and depth

STRUGGLER

Establish both brand span and depth

OCCASIONAL

Milk or renovate brand to drive loyalty

Source : Winning Brands Health Check & Homescan

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

20

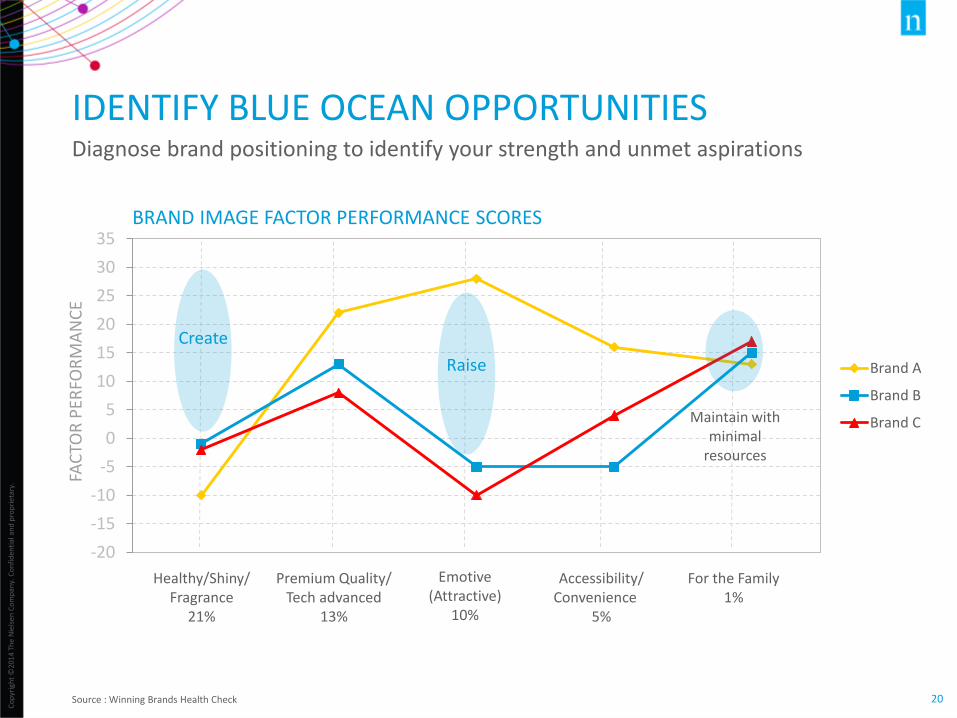

IDENTIFY BLUE OCEAN OPPORTUNITIESDiagnose brand positioning to identify your strength and unmet aspirations

-20

-15

-10

-5

0

5

10

15

20

25

30

35

Brand A

Brand B

Brand C

Healthy/Shiny/Fragrance

21%

Premium Quality/Tech advanced

13%

Accessibility/ Convenience

5%

Emotive(Attractive)

10%

For the Family1%

FAC

TOR

PER

FOR

MA

NC

E

Create

Maintain with minimal

resources

Raise

BRAND IMAGE FACTOR PERFORMANCE SCORES

Source : Winning Brands Health Check

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

21

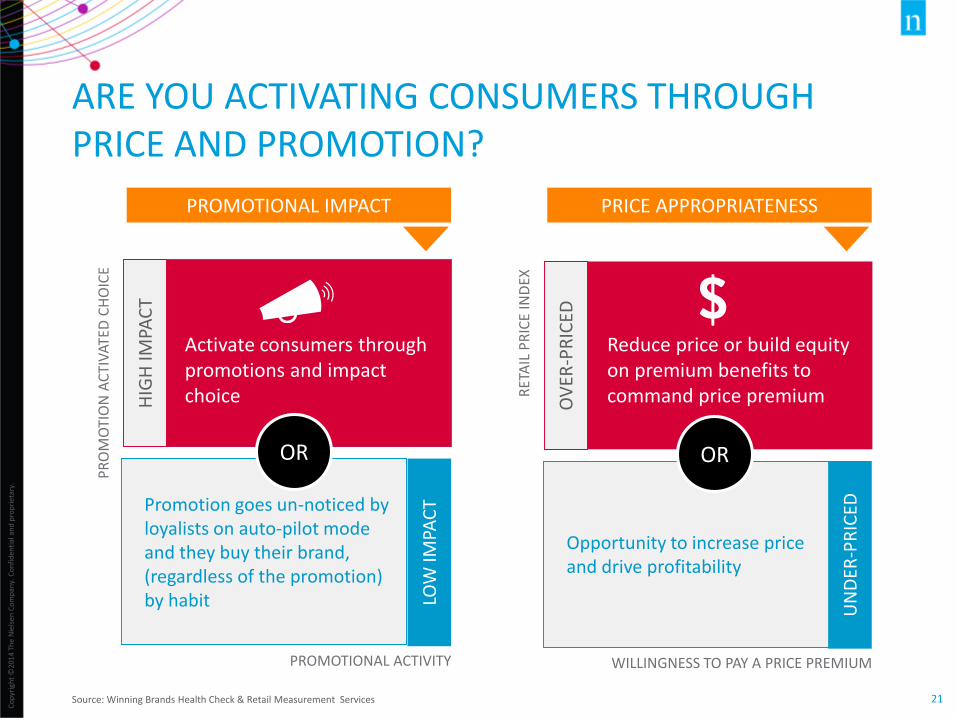

ARE YOU ACTIVATING CONSUMERS THROUGH PRICE AND PROMOTION?

Source: Winning Brands Health Check & Retail Measurement Services

PR

OM

OTI

ON

AC

TIV

ATED

CH

OIC

E

PROMOTIONAL ACTIVITY

HIG

H IM

PAC

T

Promotion goes un-noticed by loyalists on auto-pilot mode and they buy their brand, (regardless of the promotion) by habit LO

W IM

PAC

T

PROMOTIONAL IMPACT

OR

RET

AIL

PR

ICE

IND

EX

WILLINGNESS TO PAY A PRICE PREMIUM

OV

ER-P

RIC

EDOpportunity to increase price and drive profitability

UN

DER

-PR

ICED

PRICE APPROPRIATENESS

OR

Reduce price or build equity on premium benefits to command price premium

Activate consumers through promotions and impact choice

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

22Source: Winning Brands Brand Builder & Retail Measurement Services

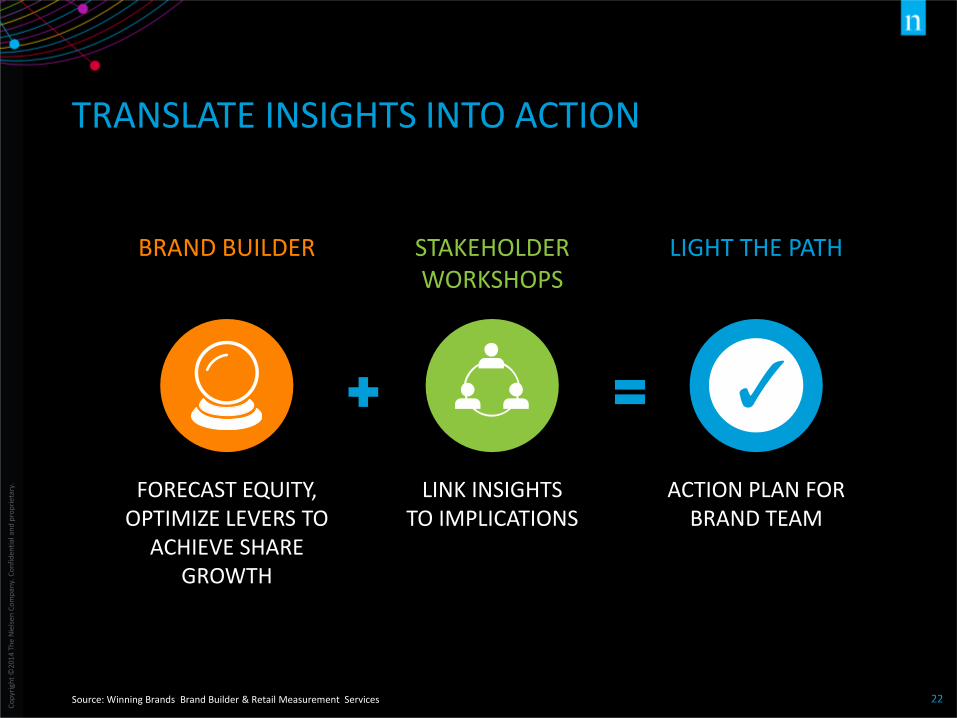

TRANSLATE INSIGHTS INTO ACTION

FORECAST EQUITY, OPTIMIZE LEVERS TO

ACHIEVE SHARE GROWTH

ACTION PLAN FOR BRAND TEAM

LINK INSIGHTS TO IMPLICATIONS

BRAND BUILDER STAKEHOLDER WORKSHOPS

LIGHT THE PATH

ACTIVATE BRAND ACROSS TOUCH POINTS

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

24

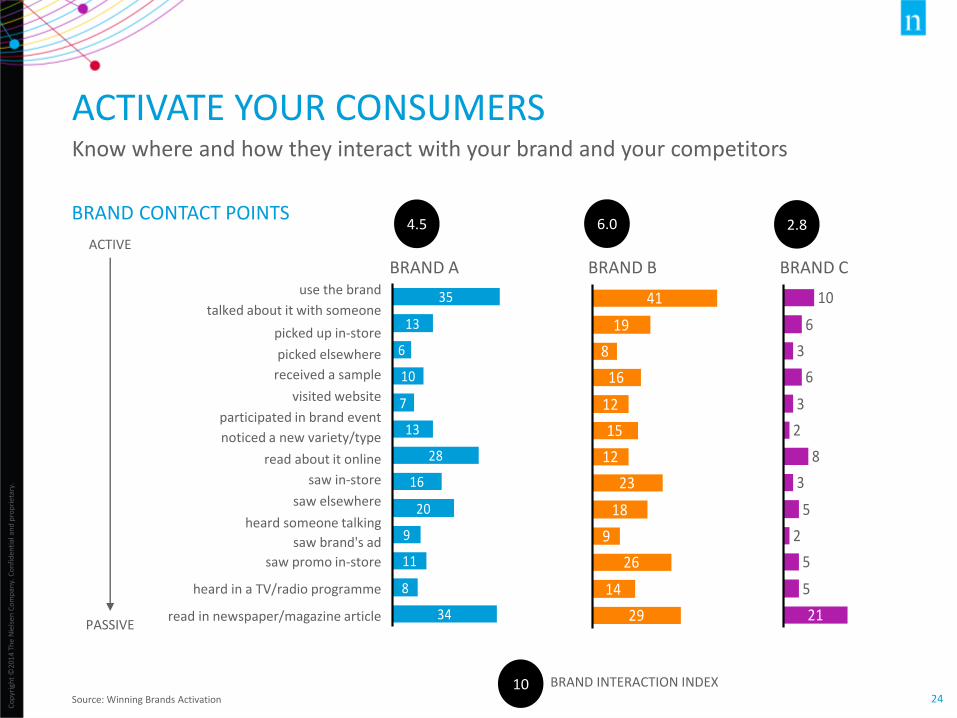

34

8

11

9

20

16

28

13

7

10

6

13

35use the brand

talked about it with someone

picked up in-store

picked elsewhere

received a sample

visited website

participated in brand event

noticed a new variety/type

read about it online

saw in-store

saw elsewhere

heard someone talking

saw brand's ad

saw promo in-store

heard in a TV/radio programme

read in newspaper/magazine article

ACTIVATE YOUR CONSUMERSKnow where and how they interact with your brand and your competitors

Source: Winning Brands Activation

29

14

26

9

18

23

12

15

12

16

8

19

41

5

5

2

5

3

8

2

3

6

3

6

10

21

ACTIVE

PASSIVE

BRAND CONTACT POINTS

BRAND A BRAND B BRAND C

4.5 6.0 2.8

BRAND INTERACTION INDEX10

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

25

DETERMINE IF YOUR BRAND IS AGGRESSIVELY ACTIVATING THE MARKET

ADVERTISING ACTIVATIONINDEX

ADVERTISING EFFICIENCYINDEX

PROMOTIONAL ACTIVATION BRAND BUZZ INDEX BRAND CARDIO (% NEW SKUS)

BRAND A BRAND B BRAND C BRAND D BRAND E

BRAND ACTIVATION

Source: Winning Brands, Retail Measurement & Media Measurement

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

26

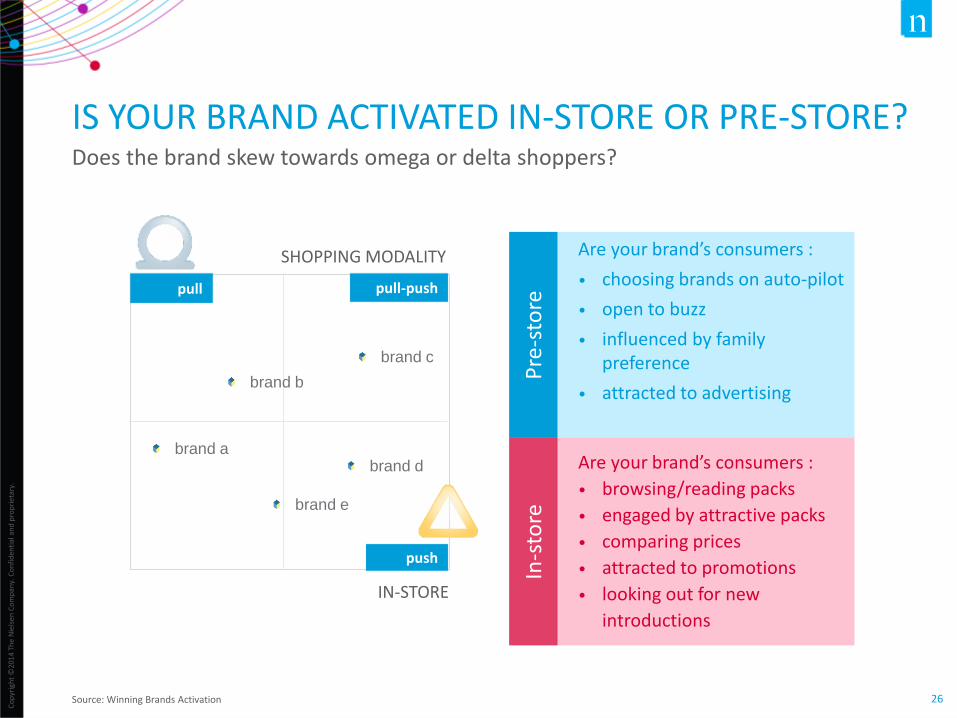

pull pull-push

push

IN-STORE

PR

E-ST

OR

E

Are your brand’s consumers :

• browsing/reading packs

• engaged by attractive packs

• comparing prices

• attracted to promotions

• looking out for new

introductions

Are your brand’s consumers :

• choosing brands on auto-pilot

• open to buzz

• influenced by family preference

• attracted to advertising

Pre

-sto

re

In-s

tore

brand b

brand c

brand d

brand e

brand a

SHOPPING MODALITY

IS YOUR BRAND ACTIVATED IN-STORE OR PRE-STORE?Does the brand skew towards omega or delta shoppers?

Source: Winning Brands Activation

MAKING YOUR AD WORK HARDER

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

28Source: Advertising Response Model

Advertising Response Modeling (ARM) models the effectiveness of individual advertising executions against TARPS

IS YOUR ADVERTISING PROVIDING THE ROI THAT YOU ARE LOOKING FOR?

=

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

29

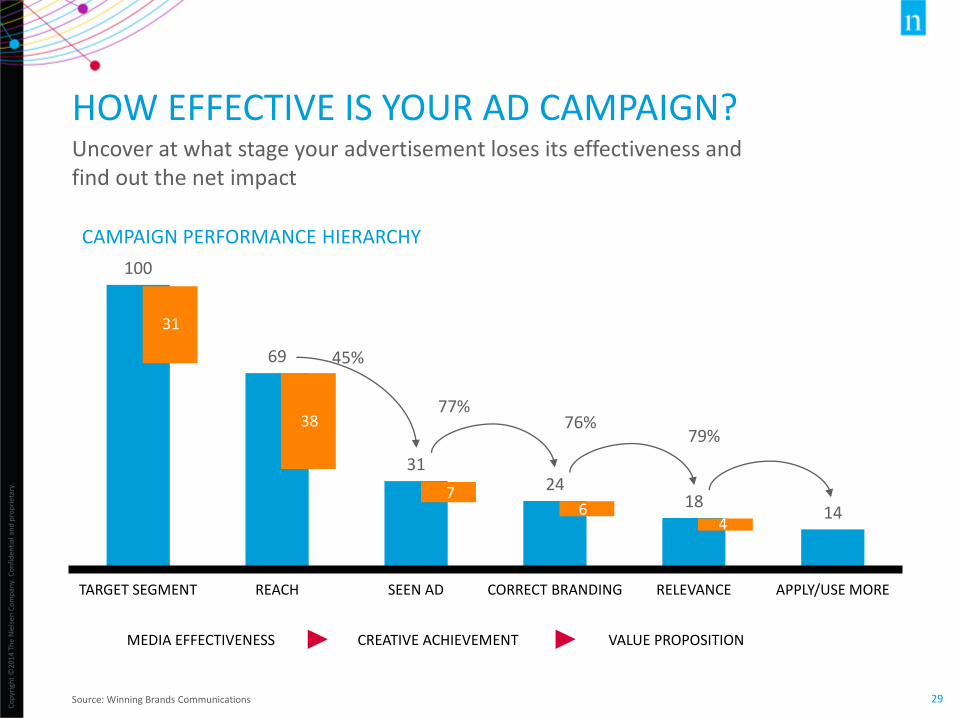

HOW EFFECTIVE IS YOUR AD CAMPAIGN? Uncover at what stage your advertisement loses its effectiveness and find out the net impact

Source: Winning Brands Communications

1418

2431

69

100

APPLY/USE MORERELEVANCECORRECT BRANDINGSEEN ADREACHTARGET SEGMENT

CAMPAIGN PERFORMANCE HIERARCHY

MEDIA EFFECTIVENESS CREATIVE ACHIEVEMENT VALUE PROPOSITION

79%

45%

77%76%

31

38

67

4

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

30

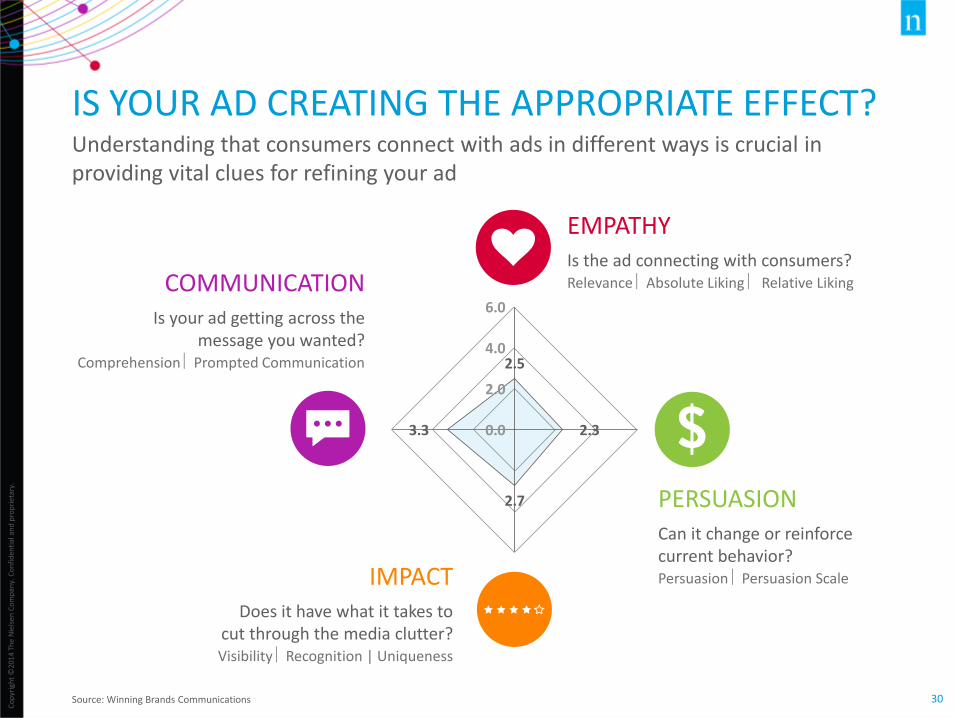

2.5

2.3

2.7

3.3 0.0

2.0

4.0

6.0

EMPATHYIs the ad connecting with consumers?Relevance Absolute Liking Relative Liking

PERSUASIONCan it change or reinforce current behavior?Persuasion Persuasion Scale

COMMUNICATIONIs your ad getting across the

message you wanted?Comprehension Prompted Communication

IS YOUR AD CREATING THE APPROPRIATE EFFECT?Understanding that consumers connect with ads in different ways is crucial in providing vital clues for refining your ad

IMPACTDoes it have what it takes to

cut through the media clutter?Visibility Recognition | Uniqueness

Source: Winning Brands Communications

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

31

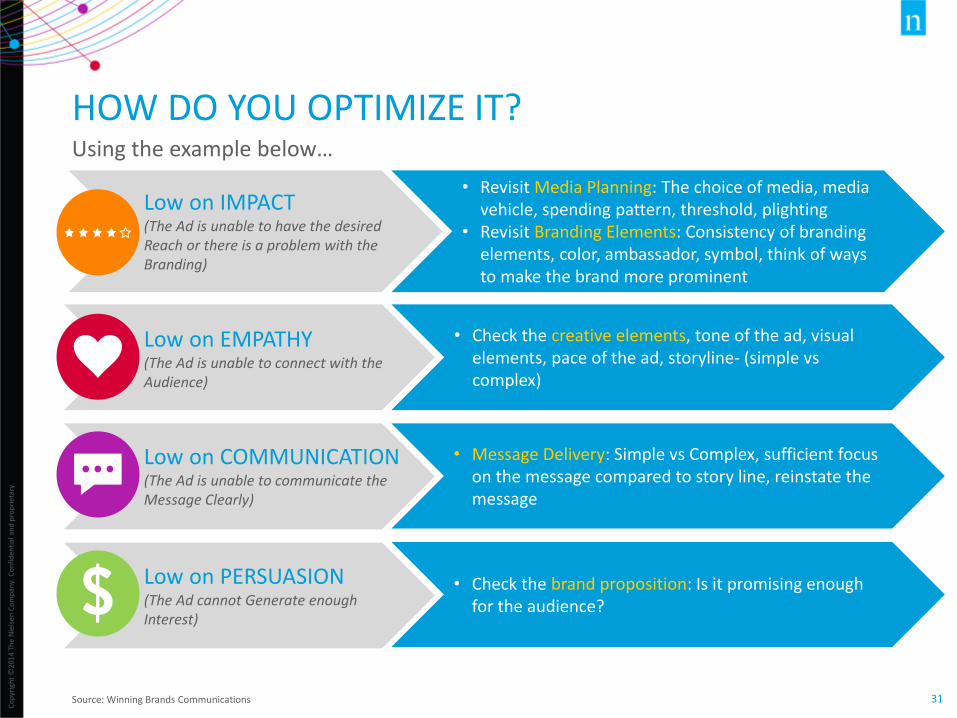

HOW DO YOU OPTIMIZE IT?Using the example below…

Low on IMPACT(The Ad is unable to have the desired Reach or there is a problem with the Branding)

Low on EMPATHY(The Ad is unable to connect with the Audience)

Low on COMMUNICATION(The Ad is unable to communicate the Message Clearly)

Low on PERSUASION(The Ad cannot Generate enough Interest)

• Revisit Media Planning: The choice of media, media vehicle, spending pattern, threshold, plighting

• Revisit Branding Elements: Consistency of branding elements, color, ambassador, symbol, think of ways to make the brand more prominent

• Check the creative elements, tone of the ad, visual elements, pace of the ad, storyline- (simple vs complex)

• Message Delivery: Simple vs Complex, sufficient focus on the message compared to story line, reinstate the message

• Check the brand proposition: Is it promising enough for the audience?

Source: Winning Brands Communications

DELIVER BRAND FORESIGHT

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

33

DEFEND

BRAND C

BRAND A

BRAND B

BRAND E

BRAND D

0

20

40

60

80

100

120

140

160

0 20 40 60 80 100 120 140 160 180 200 220

BRAND C

BRAND A

BRAND BBRAND E

BRAND D

0.0

1.0

2.0

3.0

4.0

5.0

0 20 40 60 80 100 120 140 160 180 200 220

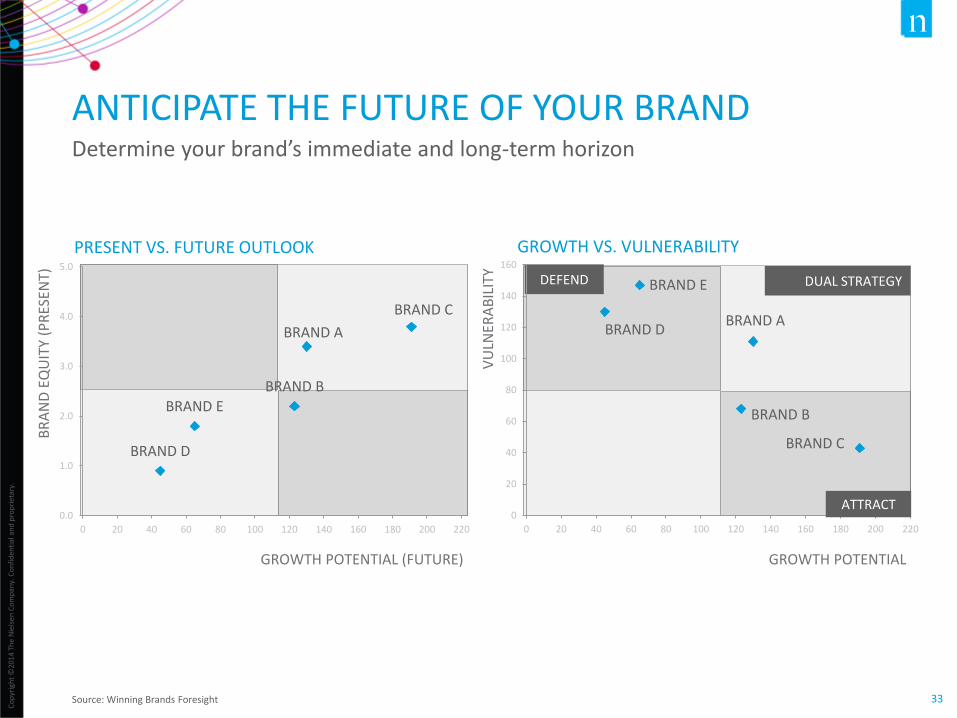

ANTICIPATE THE FUTURE OF YOUR BRANDDetermine your brand’s immediate and long-term horizon

Source: Winning Brands Foresight

BR

AN

D E

QU

ITYI

ND

EX (

PR

ESEN

T)

GROWTH POTENTIAL (FUTURE)

PRESENT VS. FUTURE OUTLOOK

VU

LNER

AB

ILIT

Y

GROWTH POTENTIAL

GROWTH VS. VULNERABILITY

ATTRACT

DUAL STRATEGY

BR

AN

D E

QU

ITY

(PR

ESEN

T)

VU

LNER

AB

ILIT

Y

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

34

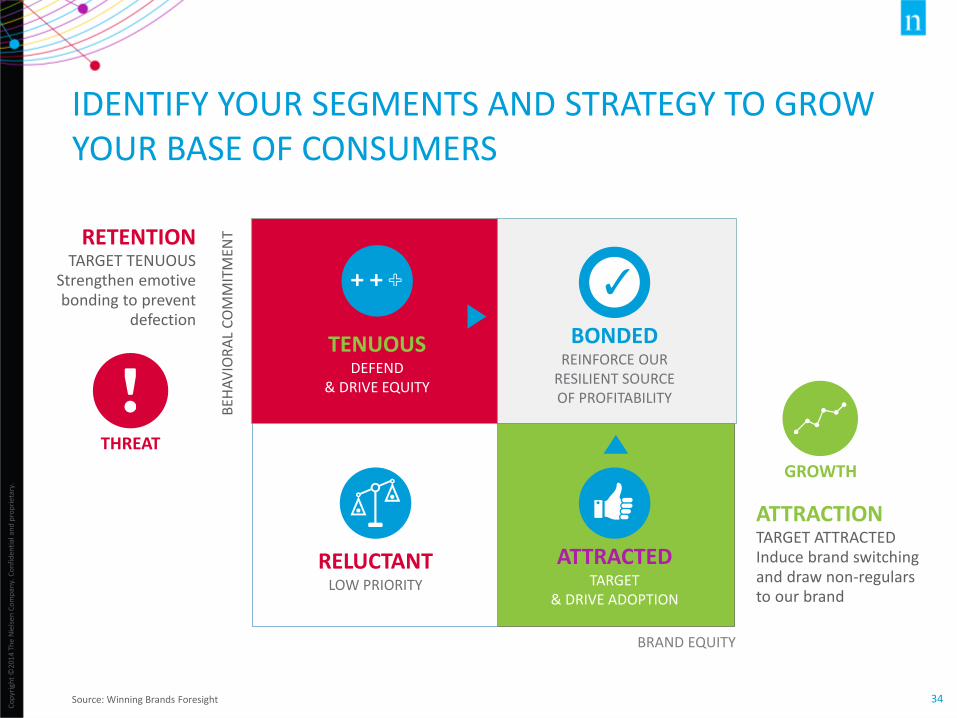

IDENTIFY YOUR SEGMENTS AND STRATEGY TO GROW YOUR BASE OF CONSUMERS

Source: Winning Brands Foresight

BEH

AV

IOR

AL

CO

MM

ITM

ENT

BRAND EQUITY

RELUCTANTLOW PRIORITY

BONDEDREINFORCE OUR

RESILIENT SOURCE OF PROFITABILITY

ATTRACTEDTARGET

& DRIVE ADOPTION

TENUOUSDEFEND

& DRIVE EQUITY

RETENTIONTARGET TENUOUS

Strengthen emotive bonding to prevent

defection

THREAT

ATTRACTIONTARGET ATTRACTEDInduce brand switching and draw non-regulars to our brand

GROWTH

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

35

Category Relationship

Brand Salience

Brand Meaning

Competitive Focus

Shopping Modality

Targeting

STRATEGIC

PLAN STRATEGY TO DRIVE GROWTH/DEFEND

Should the brand be driving its quality of awareness?

How should the brand be positioned?

What competitive brands should you focus on to prevent defection or induce switching?

How will you reach your consumers? What is their demographic, lifestyle and media profile?

What activates purchase for your target consumers? What in-store or pre-store drivers should you focus on?

What is their relationship with the category?

TACTICAL

Source: Winning Brands Foresight

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

36

WHO ARE THEY• Demographics• Geography• Life stage• Lifestyles

WHAT THEY DO• Activities & Interests• Travel & Tourism• Sports• Music

WHAT PRODUCTS ARE USED/CONSUMED• Personal care/Beauty• Food products• Household products• Technology products• Banking products• Automotive

WHERE THEY SHOP• Shopping habits• Supermarkets • Retail outlets

HOW TO REACH THEM• Media usage• Mass media – TV, Radio,

Newspapers, Magazines• Pay TV, Cinema• Internet• Outdoor• Direct Mail

GROW SEGMENTS, IMPROVE BRAND PERFORMANCEREACH CONSUMERS WHO ARE ATTRACTED TO BRAND

WHAT THEY THINK• Attitudes towards advertising,

career, fashion, finance, food cooking, health, travel, technology, products, general issues

• Corporate social responsibility

Source: Winning Brands Foresight & CMV

WHY CLIENTS LIKE US

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

38

DELIVERING UNIQUE PARTNERSHIP BENEFITS TO YOU

LATEST TRENDS AND

INSIGHTS

CONNECT THE DOTS AND

ACTIVATE INSIGHTS

BRAND HEALTH MANAGEMENT AND

CONSULTANCY

VALIDATED MEASURES & NORMS TO ANTICIPATE

MARKET CHANGES

INDUSTRY AND SUBJECT MATTER EXPERT TO

PROVIDE ISSUE-FOCUSED ACTIONS

About 20,000 CPG norms in 65 countries Supported 564 clients

in 73 markets across 213 categories

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

39

OUR RELATIONSHIPS WHEN IT COMES TO BRAND HEALTH TRACKING

Co

pyr

igh

t ©

2014

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

40

The Americas Europe/Middle East/Africa Asia/Pacific

AustriaBelgiumCzech Rep.DenmarkFinlandFranceGermanyGreeceHungaryIrelandItalyLuxembourgNetherlandsNorwayPolandPortugalSlovakiaSloveniaSpainSweden Switzerland

TurkeyYugoslaviaUKAfghanistanAlbaniaArmeniaAzerbaijanBelarusBosniaBulgariaCroatiaCyprusEstoniaGeorgiaKazakhstanKyrgyzstanLatviaLithuaniaMacedoniaMoldova

MongoliaPakistanRomaniaRussiaSerbiaTajikistan TurkmenistaUzbekistanUkraine

BahrainIsraelJordanKuwaitLebanonOmanQatarSaudi ArabiaSyriaU.A.E.Yemen

AustraliaChinaHong KongIndiaIndonesia JapanSouth Korea MalaysiaMyanmar New ZealandPhilippinesSingaporeTaiwanThailand Vietnam

CanadaU.S.A.

Costa RicaEl SalvadorGuatemalaHondurasNicaraguaPanama

ArgentinaBrazilChileColombiaEcuadorMexicoPeruPuerto Rico

AlgeriaEgyptEthiopiaMoroccoNigeriaSouth AfricaTanzaniaTunisiaUganda

DRIVING SMARTER, FASTER DECISIONS THE WORLD OVER