brexit monitor the impact industry of brexit on the ... · pwc | brexit monitor - the impact of...

TRANSCRIPT

Agrifood industry

Brexit MonitorThe impact of Brexit on the AgriFood industry

PwC | Brexit Monitor - The impact of Brexit on the AgriFood industry | p.2

Agrifood industry

The impact of Brexit on the AgriFood industry

“Maintaining tariff-free access to the EU single market is a vital priority. It is where 75% of our food exports go, so all our farming and food businesses wish to achieve this outcome.” That is the opinion of 71 of the UK’s largest food companies, as published in the Times, calling on the UK Government to negotiate the “best possible access” for the UK to EU markets. The statement was signed by 71 leading food businesses that have a combined turnover of over £92 billion (approximately €110 billion) and employing over 925 000 people across the UK. Signatories included the heads of Sainsbury’s, Morrisons, Marks & Spencer and Weetabix.

The letter signals the impact of Brexit on the UK AgriFood industry. The consequences of Brexit for the European AgriFood industry will very much depend on the openness of trade between the EU and the UK post Brexit.

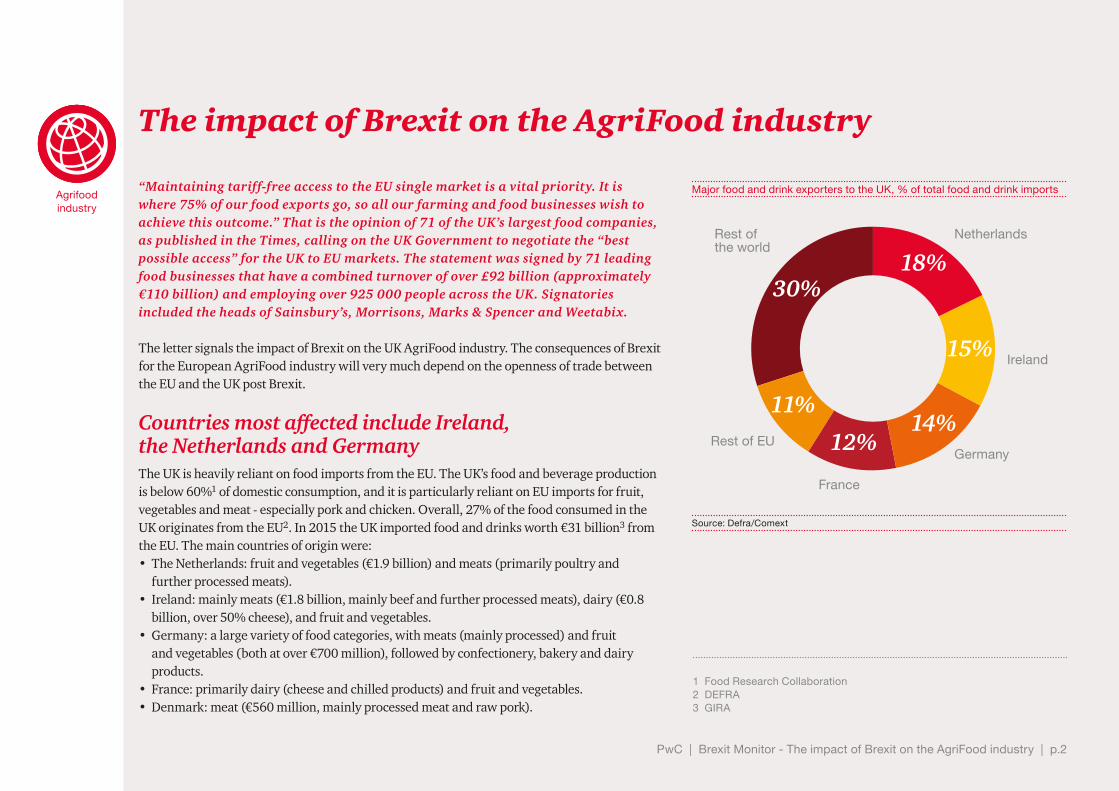

Countries most affected include Ireland, the Netherlands and GermanyThe UK is heavily reliant on food imports from the EU. The UK’s food and beverage production is below 60%1 of domestic consumption, and it is particularly reliant on EU imports for fruit, vegetables and meat - especially pork and chicken. Overall, 27% of the food consumed in the UK originates from the EU2. In 2015 the UK imported food and drinks worth €31 billion3 from the EU. The main countries of origin were: • The Netherlands: fruit and vegetables (€1.9 billion) and meats (primarily poultry and

further processed meats). • Ireland: mainly meats (€1.8 billion, mainly beef and further processed meats), dairy (€0.8

billion, over 50% cheese), and fruit and vegetables. • Germany: a large variety of food categories, with meats (mainly processed) and fruit

and vegetables (both at over €700 million), followed by confectionery, bakery and dairy products.

• France: primarily dairy (cheese and chilled products) and fruit and vegetables. • Denmark: meat (€560 million, mainly processed meat and raw pork).

1 Food Research Collaboration2 DEFRA3 GIRA

Major food and drink exporters to the UK, % of total food and drink imports

18%

15%

14%12%

11%

30%

NetherlandsRest of the world

Ireland

Germany

France

Rest of EU

Source: Defra/Comext

PwC | Brexit Monitor - The impact of Brexit on the AgriFood industry | p.3

Agrifood industry

The UK exports the majority of its AgriFood products to the EU. In total, 52%4 of the UK’s total AgriFood exports goes to only four countries: Ireland, France, the Netherlands and Germany.

On the exports side, Scotch whisky is the biggest UK AgriFood export product, accounting for 25%5 of the UK’s food and drinks exports, with sales of £4 billion (approximately €5 billion) in 2015. Overall, 40% of all exported Scotch whisky goes to the EU. However, as the EU has set whisky tariffs at zero for all markets, the costs for importers from the EU would not rise post Brexit. On the other hand, if the UK loses

access to the markets with which the EU has negotiated Free Trade Agreements, whisky importers from key markets such as South Africa, South Korea and Peru may face higher costs.

Top 10 countries importing food and drink from UK (in GBP billion)

Source: Food and Drink Federation

0 0,5 1,0 1,5 2,0 2,5 3,0 3,5

Ireland

France

Netherlands

Germany

Spain

United States

Belgium

Italy

China

Denmark

4 Food and Drink association, PwC analysis5 DEFRA, Scotch Whisky Association

PwC | Brexit Monitor - The impact of Brexit on the AgriFood industry | p.4

Agrifood industry

well as the potential costs of complying with two different regulatory regimes.

If trade barriers increase, regions will become more dependent on local production. In areas with low production, prices may increase, while high production regions might suffer from decreasing prices, making it difficult for the producers. This makes it even more important to be innovative in order to be able to ask premium prices.

Trade costs may riseUnless the EU and the UK agree on a trade deal that allows continued tariff-free trade, trade tariffs on AgriFood products will be imposed. Tariffs on agricultural produce tend to be among the highest in international trade. The EU and other countries generally agree a two-tier tariff structure on agricultural products, in which duties are lowered or waived on fixed quantities. Anything above these quotas is charged at the normal tariff. These Tariff Rate Quotas (TRQs) are often designed to allow the import of seasonal products when domestic production is slow. As dairy, meat and sugar tariffs are generally the highest, and vegetables are imported to the UK in large quantities, EU suppliers of these products may face the largest increase in tariffs.

Some food manufacturers have highly integrated supply chains - sourcing, processing and selling products in different countries. If facilities in the UK are part of their supply chain, companies may face increased tariffs and double taxation issues post Brexit. You can read more on the consequences for transfer pricing in issue 11 of the PwC Europe Brexit Monitor.

However, non-tariff trade costs between the UK and the EU may be just as an important factor post Brexit. Those transaction costs will increase once the UK leaves the UK. For example, under the Common Agricultural Policy (CAP) import licenses are required in order to import

certain agricultural products originating from outside the EU. This is the case for example with products such as beef and veal, pork, poultry, cereals, seeds, milk and other dairy products and sugar. Depending on the final trade deal between the EU and the UK, these rules may also apply to the UK following Brexit. Other trading costs may be associated with the re-introduction of customs controls, such as rules of origin checks, documentation and physical border checks, as

PwC | Brexit Monitor - The impact of Brexit on the AgriFood industry | p.5

Agrifood industry

The UK’s food and drink industry is very reliant on EU workers. In the UK, more than 250 0006 EU citizens are employed in the AgriFood industry, including the food and beverage services industries. Almost 120 000 of them work in the manufacturing of food products, and more than 70 000 in horticulture. For UK-based food producers and processors, Brexit may make it harder to recruit as restrictions on migration come into effect.

The UK is currently a major net contributor to the EU budget. It is currently the third largest contributor to the EU budget, adding €18.2 billion7 to the EU budget, or 12% of its total. Of these €18.2 billion, €3.2 billion is a contribution to the Common Agricultural Policy (CAP). Filling this gap in the EU budget would require either expenditure reductions or larger contributions by the remaining member states following Brexit.

Given the importance of European markets for UK food producers, it is likely that the UK will choose to mirror EU regulation on food safety and food quality, food ingredient labelling, animal health and welfare protection and other relevant regulations also after Brexit.

EU employment in UK AgriFood may be threatened

Common Agricultural Policy and other regulations

A Christmas Treat?

Brexit may re-open the debate about the definition of chocolate. For many years, EU rules prevented products low in cocoa fats from being marketed as chocolate. UK based confectionary producers may choose to change the contents of their candy bars in favour of less expensive “chocolate”.

6 Food and Drink Federation7 Capreform.eu

PwC | Brexit Monitor - The impact of Brexit on the AgriFood industry | p.6

Agrifood industry

Consumer prices may riseIn the short term, currency swings and the depreciation of the pound sterling have the potential to push up input prices for UK firms. The lower pound is likely to increase raw material costs for food manufacturers in the UK, but it will also put pressure on EU manufacturers who export to the UK. These price increases will likely be passed on to consumers.

In the longer term, increased non-tariff barriers and possibly the introduction of tariffs may increase costs for both AgriFood producers and importers, leading to higher consumer prices. Not only UK consumers may suffer from increasing prices. In Ireland, for example, where a high proportion of supermarket groceries are sourced from the UK, consumer food prices could be expected to rise due to these increased trading costs.

If the costs of labour also rise due to legislation changes, combined with increasing import costs and the devaluation of the pound, there will be additional pressure on prices. This price pressure will impact the most vulnerable in society as food takes a larger portion of their income. If prices for fruit and vegetables rise too much, it will impact sales.

PwC | Brexit Monitor - The impact of Brexit on the AgriFood industry | p.7

Agrifood industry

The takeawayIn the short term, currency swings and the depreciation of the pound sterling will have the most immediate effect on the AgriFood industry. Companies should consider how to position their company to take advantage of a weak British pound. Where possible, companies could hedge against weak sterling and look for investment opportunities that provide good value now, and would benefit the company in the long run.

Consumer sentiment in the UK may deteriorate over the next two years. Companies should consider prioritizing sales and marketing strategies that are successful during times of weak consumer confidence, and to look at how savings can be made across supply chains where possible. Carefully considering which costs may be passed on to customers is recommended.

After assessing the significance of Brexit to their business - in both the UK and the EU, companies should consider scenario planning of possible outcomes and reactions.

Anticipating future developments will be very important. Companies should stay informed of EU-UK negotiations and trade deal scenarios. Brexit is a process with many moving parts. The only way to assess the effect is to stay informed of events, progress and particularly of political positions coming from Brussels and from Westminster. Companies should also engage other stakeholders in the industry to influence governments in protecting the industry’s interests.

This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors. © 2016 PricewaterhouseCoopers B.V. (KvK 34180289). All rights reserved.

PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details. At PwC in the Netherlands, over 4,200 people work together from 12 offices. PwC Netherlands helps organisations and individuals create the value they’re looking for. We’re a member of the PwC network of firms in 157 countries with more than 195,000 people. We’re committed to delivering quality in assurance, tax and advisory services. Tell us what matters to you and find out more by visiting us at www.pwc.nl.

Peter HoijtinkAgriFood Leader PwCT: +31 (0) 88 792 30 90 M: +31 (0)6 42 01 93 83 E: [email protected]

Contact

Jan Willem VelthuijsenChief Economist, PwCT: +31 (0)88 792 75 58M: +31 (0)6 2248 3293E: [email protected]