bpo industry (including sa value proposition and ... in sa-3.pdf · 1 bpo industry (including sa...

TRANSCRIPT

1

BPO Industry (including SA Value Proposition and

International Perspective)

Mfanu Mfayela, BPeSA CEOMidrand, June 2007

2

Thinking Global

“Invest where you get maximum returns, source talent from where it is best available, produce where it is most cost-effective, and sell where the markets are, without being constrained by national boundaries.”

Narayan Murthy, Infosys

3

Outline

1. Business Process Outsourcing- Opportunity & Background Information

2. International Developments

3. SA Industry4. SA Value Proposition5. Q & A

4

Section I‘Business Process Outsourcing’

5

Potential Across the Value Chain

Source: NASSCOM-KPMG 2004

Finance and Accounts

Product Development

Human Resources Management

Technology Services

Inbo

und

Logi

stic

s

Man

ufac

turin

g / O

pera

tions

Out

boun

d Lo

gist

ics

Mar

ketin

g an

d S

ales

Cus

tom

er

Ser

vice

Human Resources• Payroll Processing• Recruitment and

selection support• HRIS

IT Services and Support• Custom development• Systems integration• Hosting / maintenance• Customer help desk /

support

Operations / logistics• Order tracking• Order / claims /

application processing• Payments processing

Sales / Marketing and Customer Service

• Tele-sales• Order Processing• Customer services and

Complaints• Help-desk

Finance and Accounting• Back-office• Accounts

payable/receivable• Financial reporting• Finance accounting• Revenue accounting

Research / Design and Development

• Clinical research• VLSI design• DSP chip design• Avionics research• Engineering design

services• Legal research

6

Global Delivery Locations

- Genpact, India • US, Mexico, Hungary, Romania and China

- IBM, US• South Africa, China, India, Malaysia, Australia, Costa

Rica and the Philippines

- ACS, US• China, India, Fiji and Ghana

- Virgin Mobile• UK, South Africa

7

Blurring of Onshore, Nearshore& Farshore Locations

- Automobile manufacturer in Europe with suppliers across the EU

- Outsourcing of accounts payable• Provider receives invoices from suppliers at a central

location in Spain• Invoices scanned and sent to facilities in India and the

Philippines for processing payment• Payment to suppliers facilitated by delivery centers in

Spain and the UK

8

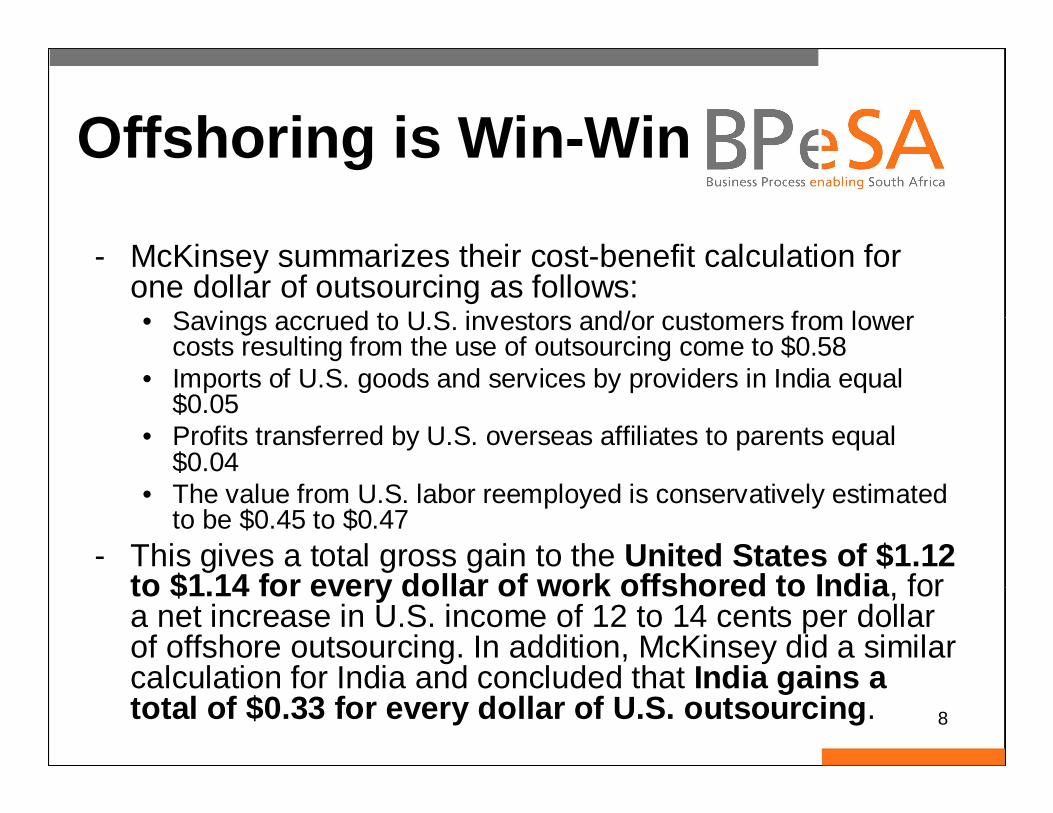

Offshoring is Win-Win

- McKinsey summarizes their cost-benefit calculation for one dollar of outsourcing as follows: • Savings accrued to U.S. investors and/or customers from lower

costs resulting from the use of outsourcing come to $0.58• Imports of U.S. goods and services by providers in India equal

$0.05• Profits transferred by U.S. overseas affiliates to parents equal

$0.04 • The value from U.S. labor reemployed is conservatively estimated

to be $0.45 to $0.47- This gives a total gross gain to the United States of $1.12

to $1.14 for every dollar of work offshored to Indi a, for a net increase in U.S. income of 12 to 14 cents per dollar of offshore outsourcing. In addition, McKinsey did a similar calculation for India and concluded that India gains a total of $0.33 for every dollar of U.S. outsourcing .

9

Estimated addressable market in global offshore IT industry 2005(UbSS$ billion)

150-18014-173-430-36

30-36

70-85

0

20

40

60

80

100

120

140

160

Traditional IT Application

development

and

maintenance

System

integration

Consulting

(including

network

consulting)

R&D sevices Total

2 31 5 10 30 11Current

Penetration %

Includes hw/sw maintenance,

network administration and

help desk

10

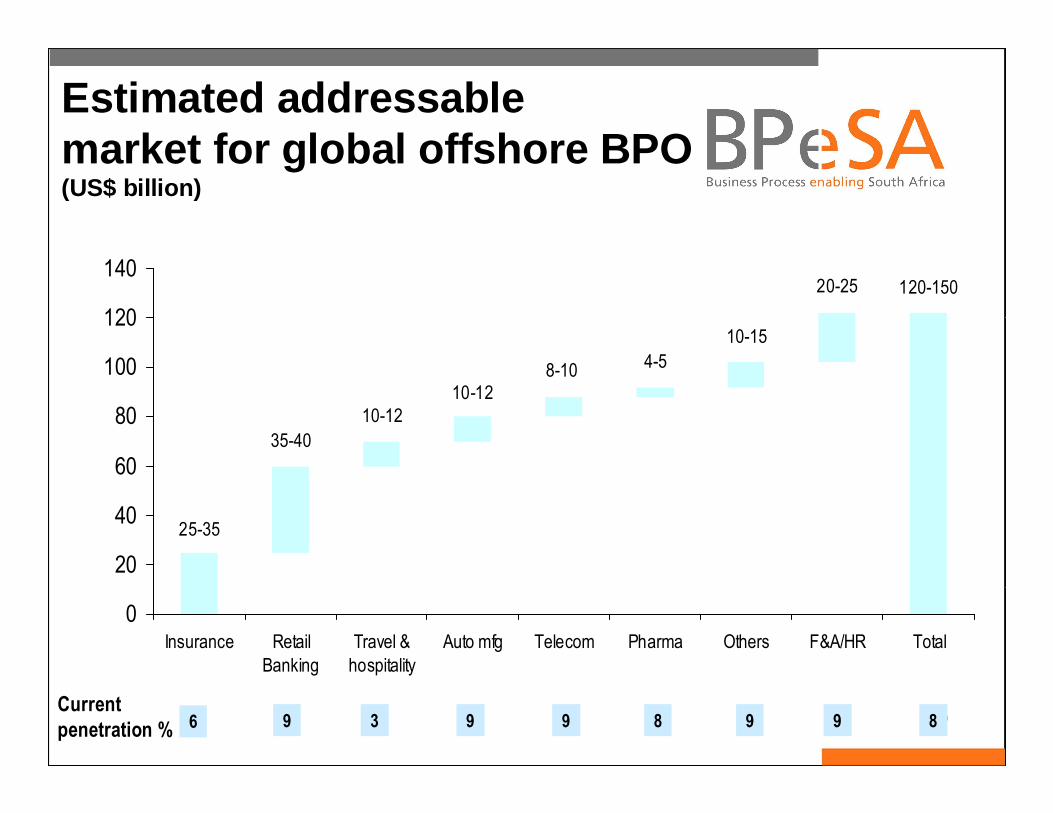

Estimated addressable market for global offshore BPO(US$ billion)

25-35

35-40

10-12

10-128-10 4-5

10-15

20-25 120-150

0

20

40

60

80

100

120

140

Insurance Retail

Banking

Travel &

hospitality

Auto mfg Telecom Pharma Others F&A/HR Total

6 9 3 9 9 9 9 88Current

penetration %

11

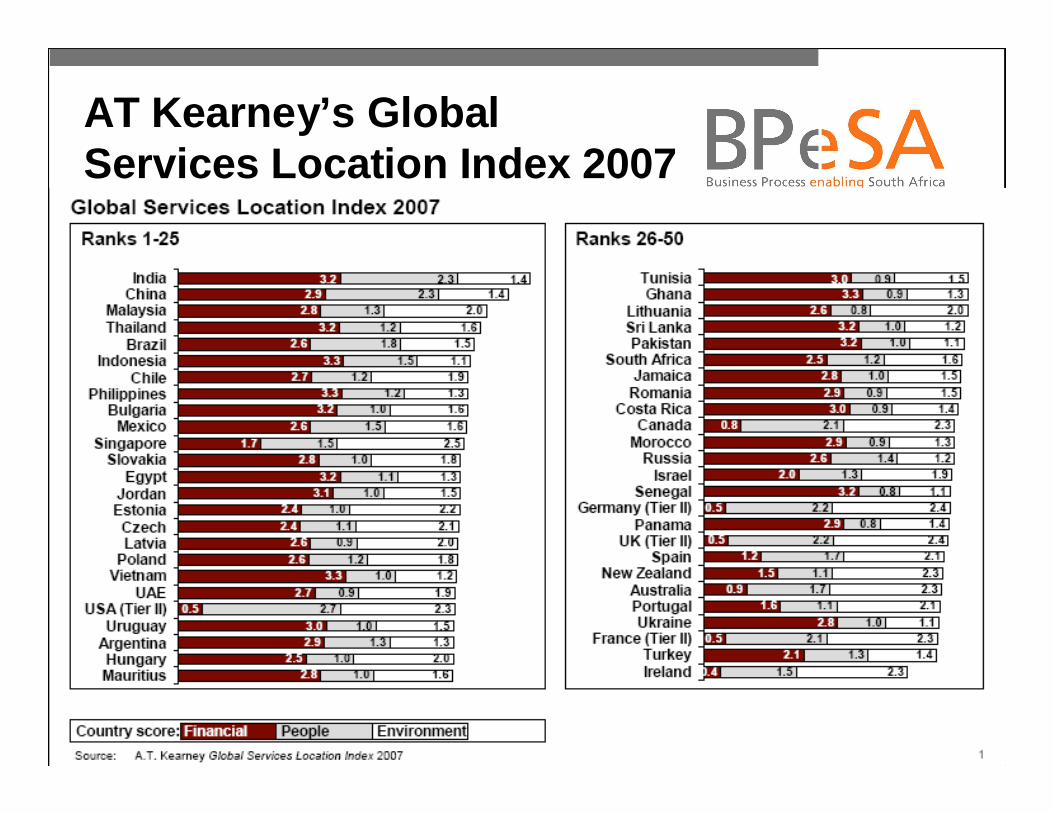

AT Kearney’s Global Services Location Index 2007

12

India’s IT/ITES Performance ($ billion)

23.6

30.3

5.3

7.2

17.8

FY 2006

31.3

39.7

6.5

9.5

23.7

FY 2007E

22.616.7Total

17.712.9Exports

3.92.9Engineering Services, R&D, Software Products

5.23.4ITES-BPO

13.510.4IT services

FY 2005FY 2004Sector

13

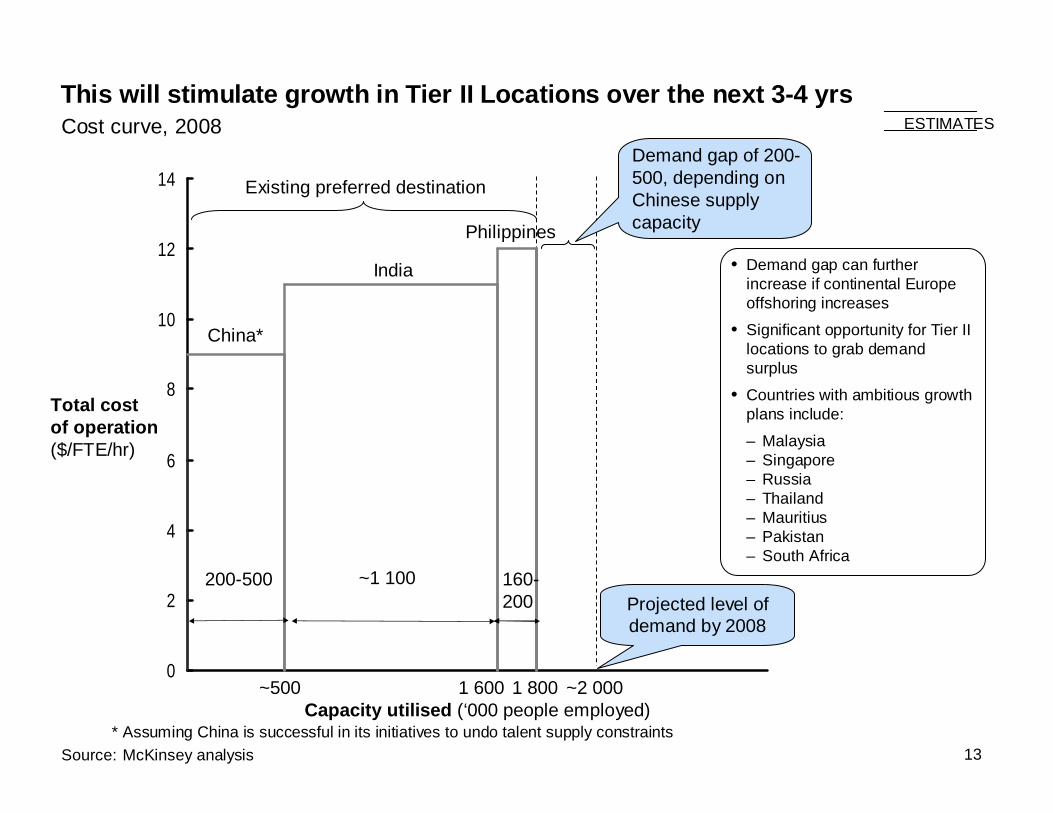

This will stimulate growth in Tier II Locations ove r the next 3-4 yrs Cost curve, 2008

* Assuming China is successful in its initiatives to undo talent supply constraintsSource: McKinsey analysis

ESTIMATES

0

2

4

6

8

10

12

14

Total cost of operation ($/FTE/hr)

Capacity utilised (‘000 people employed)

China*

India

Philippines

Existing preferred destination

~2 0001 600 1 800

• Demand gap can further increase if continental Europe offshoring increases

• Significant opportunity for Tier II locations to grab demand surplus

• Countries with ambitious growth plans include:

– Malaysia– Singapore– Russia– Thailand– Mauritius– Pakistan– South Africa

~1 100200-500 160-200

~500

Demand gap of 200-500, depending on Chinese supply capacity

Projected level of demand by 2008

14

Section II‘International Developments’

15

What’s Happening Out there???- USA

• ‘Legislation’ is the Driver (Rest of the World to Follow)� Do Not Call List� Speed to Answer

• Technology Development� Work from home� Nth Tier Cities (Competing with Offshore Locations)

• Innovation

- Rest of the World• Quality• Efficiency• Technology Development• New Markets; Australia

16

Section III‘SA Industry’

17

Key Factors for a Successful Industry

Infrastructure Talent PoolGovernment

policies

Promotion Smart marketingSuccess stories

18

Business Process enabling SA

- National industry association representing the interests that aims to provide a national coordinated service & address key challenges incl. policy advocacy, etc.

• Aim to develop & grow industry to become a significant contributor to GDP, through attracting foreign direct investment & creating sustainable job creation

• Aim to strengthen & improve sector, ensure and promote SA as a destination of choice investors

19

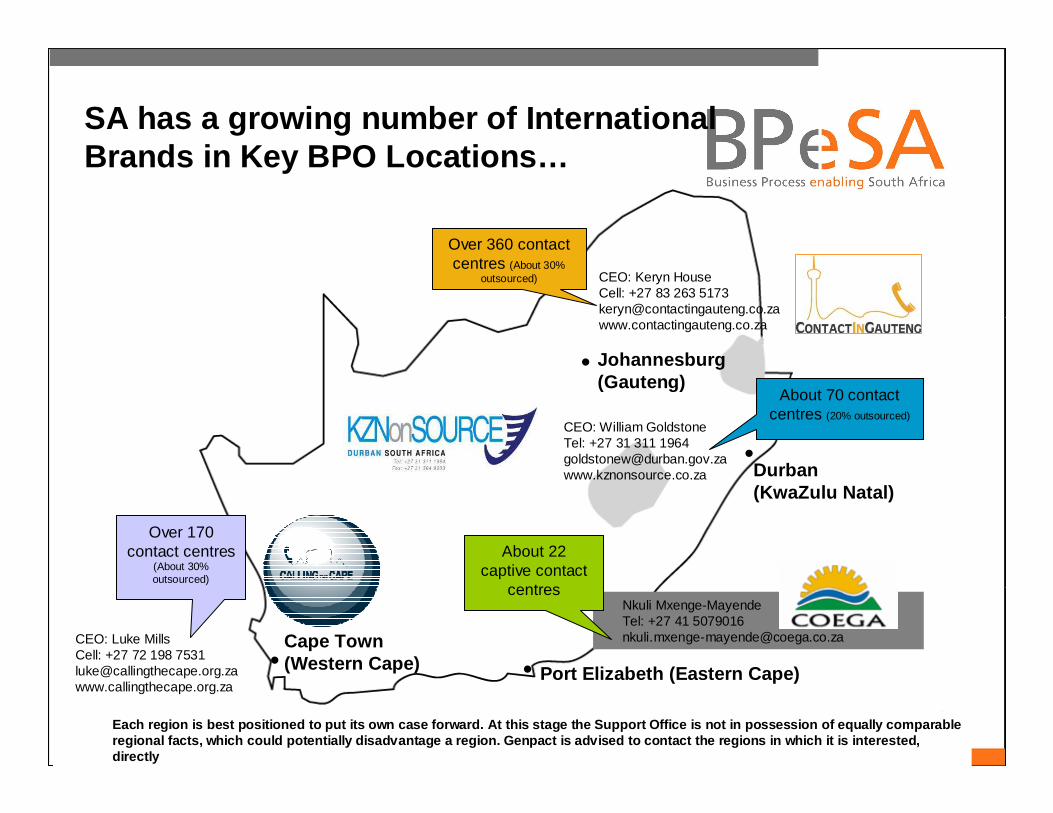

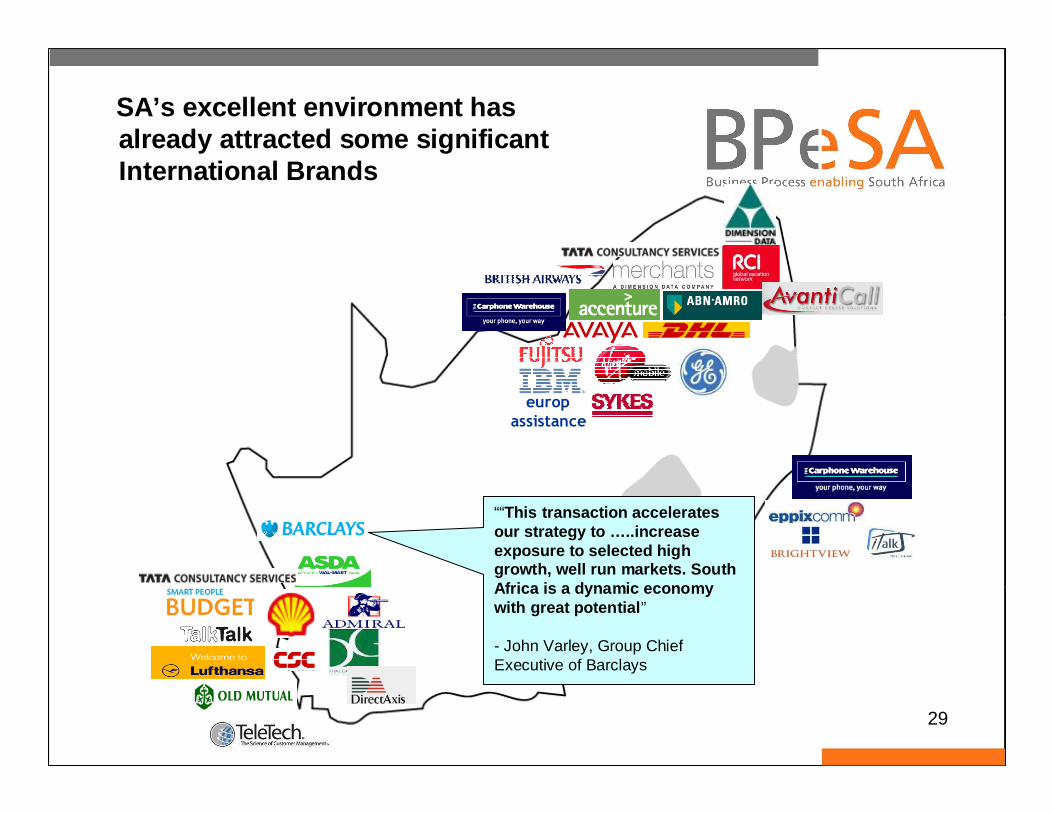

SA has a growing number of International Brands in Key BPO Locations…

Cape Town (Western Cape)

Johannesburg(Gauteng)

Durban (KwaZulu Natal)

Port Elizabeth (Eastern Cape)

•

• •

•

Over 360 contact centres (About 30%

outsourced)

Over 170 contact centres

(About 30% outsourced)

About 70 contact centres (20% outsourced)

Nkuli Mxenge-MayendeTel: +27 41 [email protected]

Each region is best positioned to put its own case forward. At this stage the Support Office is not in possession of equally comparable regional facts, which could potentially disadvantag e a region. Genpact is advised to contact the regio ns in which it is interested, directly

CEO: William GoldstoneTel: +27 31 311 [email protected]

CEO: Luke MillsCell: +27 72 198 [email protected]

CEO: Keryn HouseCell: +27 83 263 [email protected]

About 22 captive contact

centres

20

Realising Opportunity

- BPeSA formed strategic partnership with dti and Business Trust designed to realise its objectives• Has taken a non-traditional, development role as

industry is being born

- Urgent focus on getting Government support to enable this development

- Need to achieve partnership with Government at national level, similar to successes already achieved at regional level

21

SA (Renewed) Foundation

- Government & SACCCOM recognise that:• Need to leverage strengths &

minimise duplication• Support & cooperate with each other• Need to build strong partnership &

meaningful co-operation which is essential to positioning & promoting SA as a leading offshore destination

22

Section IV‘South Africa – Alive with

Possibilities’

23

SA Value Proposition- A unique opportunity to improve its service offerin g and delivery to existing and

prospective customers• Distinctive strengths in key industries and service lines• A large quality talent pool• A sound regulatory environment including financial service regulation and protection of

data privacy and intellectual property

- An attractive social, economic and political climat e to extend its global footprint and thereby reduce its location risk• A stable, open investment environment• World class infrastructure• Attractive lifestyle• Competitive costs for key inputs• A growing number of international brands that have capitalised on and enrich the

operating environment

- Expanded Government assistance to enhance South Afr ica’s offering and support investors• BPO sector support programme as part of AsgiSA• A new incentives regime• Targeted talent development programme• Commitment to addressing concerns about security• A support facility to assist investors

24

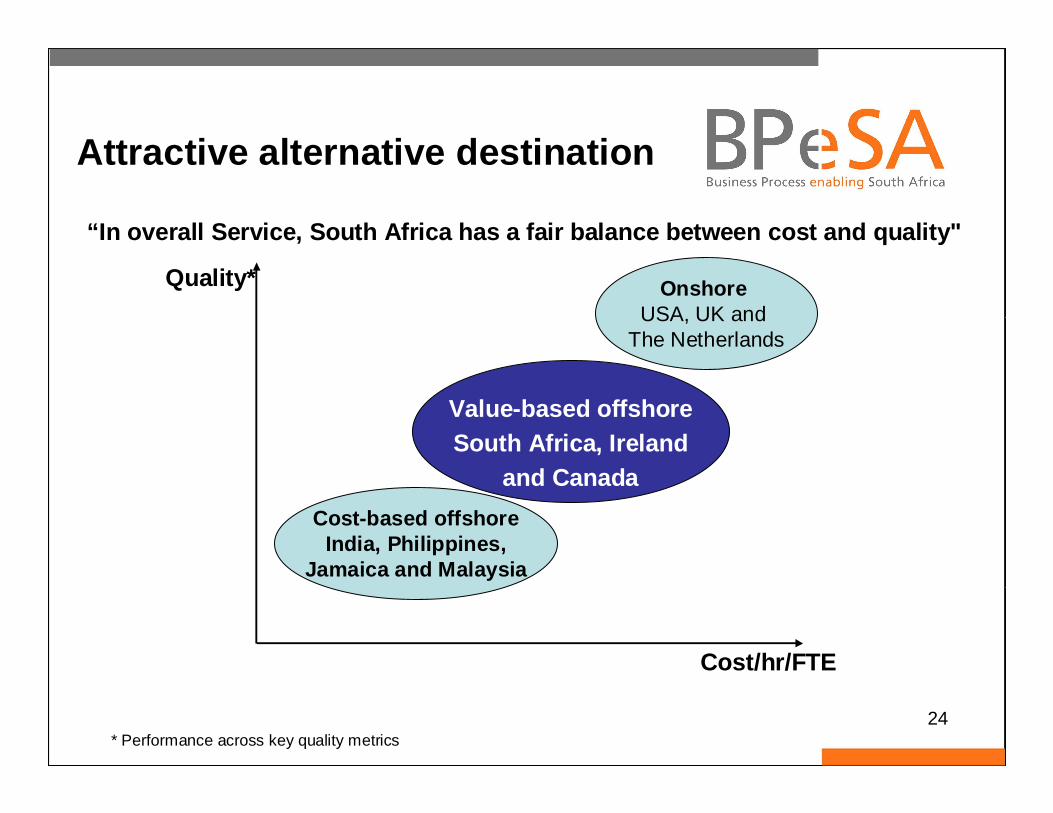

Attractive alternative destination

Quality*

Cost/hr/FTE

Onshore USA, UK and

The Netherlands

Value-based offshoreSouth Africa, Ireland

and Canada

Cost-based offshore India, Philippines,

Jamaica and Malaysia

“In overall Service, South Africa has a fair balanc e between cost and quality"

* Performance across key quality metrics

25

What are the SA Industry Standards?

The Standards cover Inbound and Outbound Contact Centres, Back-Office Processing Operations and are a QA framework of:

- management principles

- practices and

- processes

These require that specific ‘performance metrics’are measured

Source: BPO&O Sector Support Programme: QA workstream - October 2005 to date

26

What are the Industry Standards designed to do?

The QA framework provides the highest probability of success resulting in:

- Higher customer satisfaction- High levels of staff efficiency- High quality and service standards- Increased revenue- Reduced cost of waste- Management of business risk

Source: BPO&O Sector Support Programme: QA workstream - October 2005 to date

27

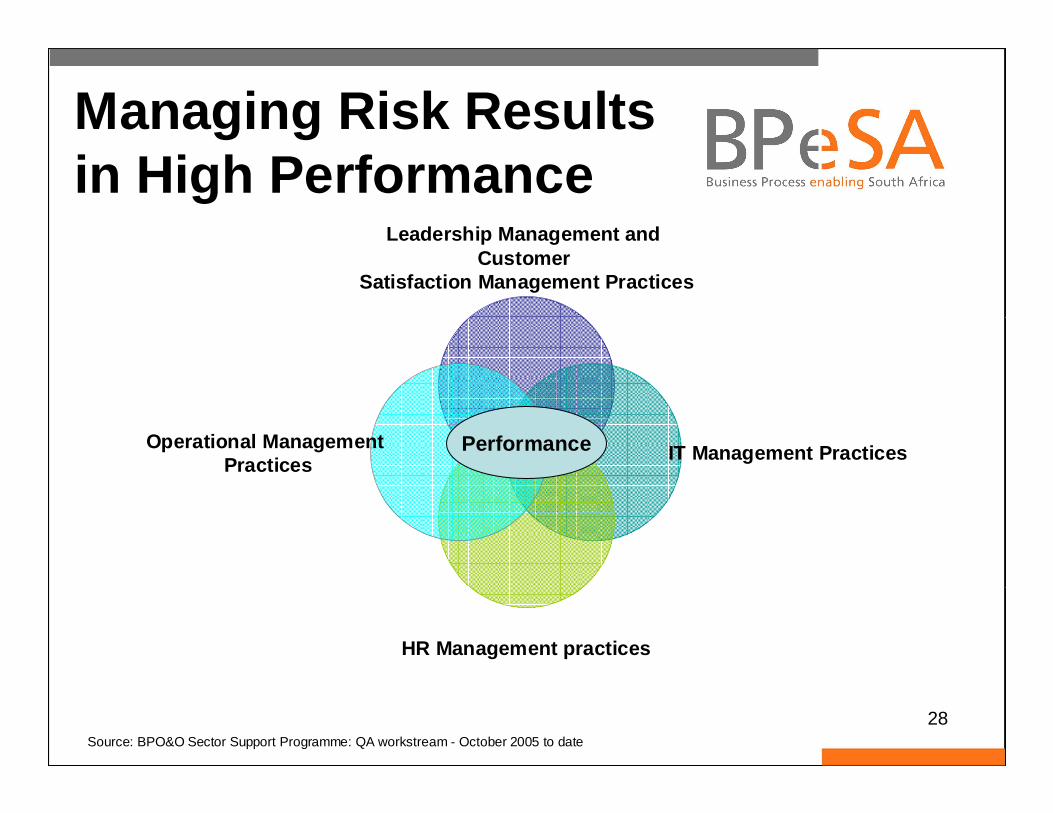

Four Categories exist in the Standards

1. Leadership and Customer Satisfaction Management Practices

2. Operational Management Practices3. Human Resource Management Practices4. Technical Resource Management Practices

- There are a number of requirements within each item that are required to be met from an approach, process and performance metric perspective

- They manage the areas of dependency so that business efficiencies and customers’ experiences are successfully managed

- They widen the accountability in the business, rather than focusing on the silo’s of the contact centre and the back-office

Source: BPO&O Sector Support Programme: QA workstream - October 2005 to date

28

Managing Risk Resultsin High Performance

Leadership Management and Customer

Satisfaction Management Practices

IT Management Practices

HR Management practices

Operational ManagementPractices

Performance

Source: BPO&O Sector Support Programme: QA workstream - October 2005 to date

29

SA’s excellent environment has already attracted some significant International Brands

europ

assistance

““This transaction accelerates our strategy to …..increase exposure to selected high growth, well run markets. South Africa is a dynamic economy with great potential ”

- John Varley, Group Chief Executive of Barclays

30

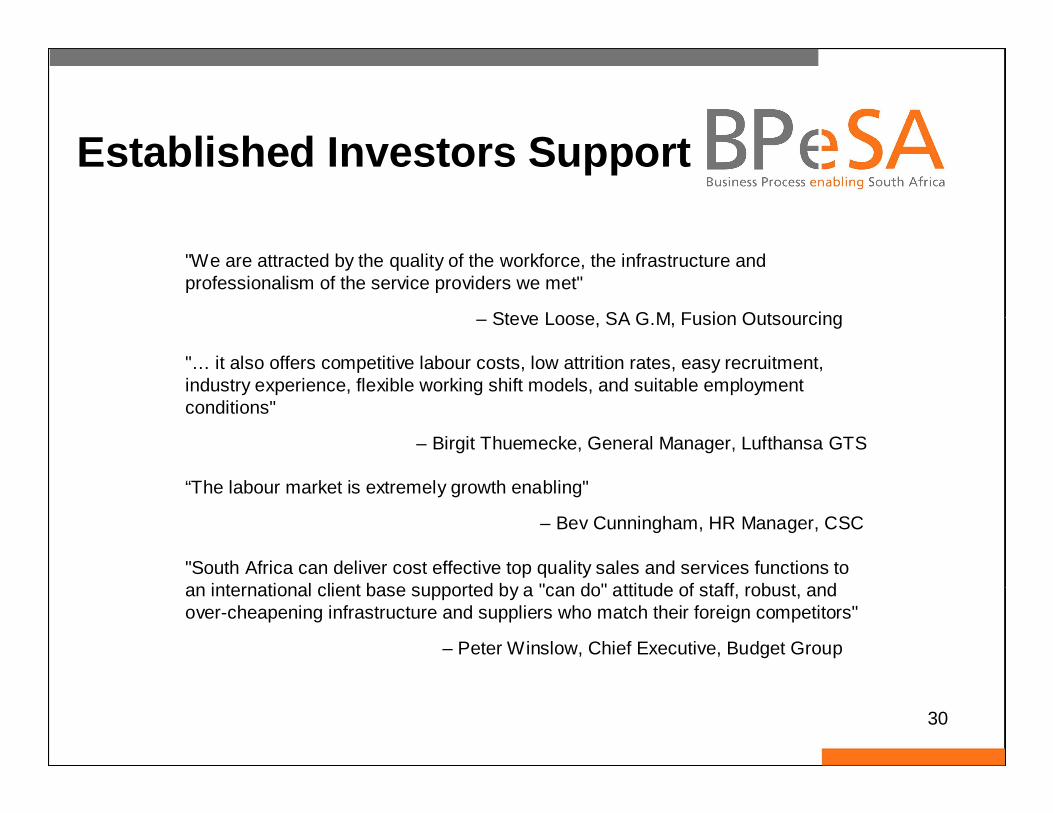

Established Investors Support

"We are attracted by the quality of the workforce, the infrastructure and professionalism of the service providers we met"

– Steve Loose, SA G.M, Fusion Outsourcing

"… it also offers competitive labour costs, low attrition rates, easy recruitment, industry experience, flexible working shift models, and suitable employment conditions"

– Birgit Thuemecke, General Manager, Lufthansa GTS

“The labour market is extremely growth enabling"

– Bev Cunningham, HR Manager, CSC

"South Africa can deliver cost effective top quality sales and services functions to an international client base supported by a "can do" attitude of staff, robust, and over-cheapening infrastructure and suppliers who match their foreign competitors"

– Peter Winslow, Chief Executive, Budget Group

32

“Case studies, challenges, and learnings"

33

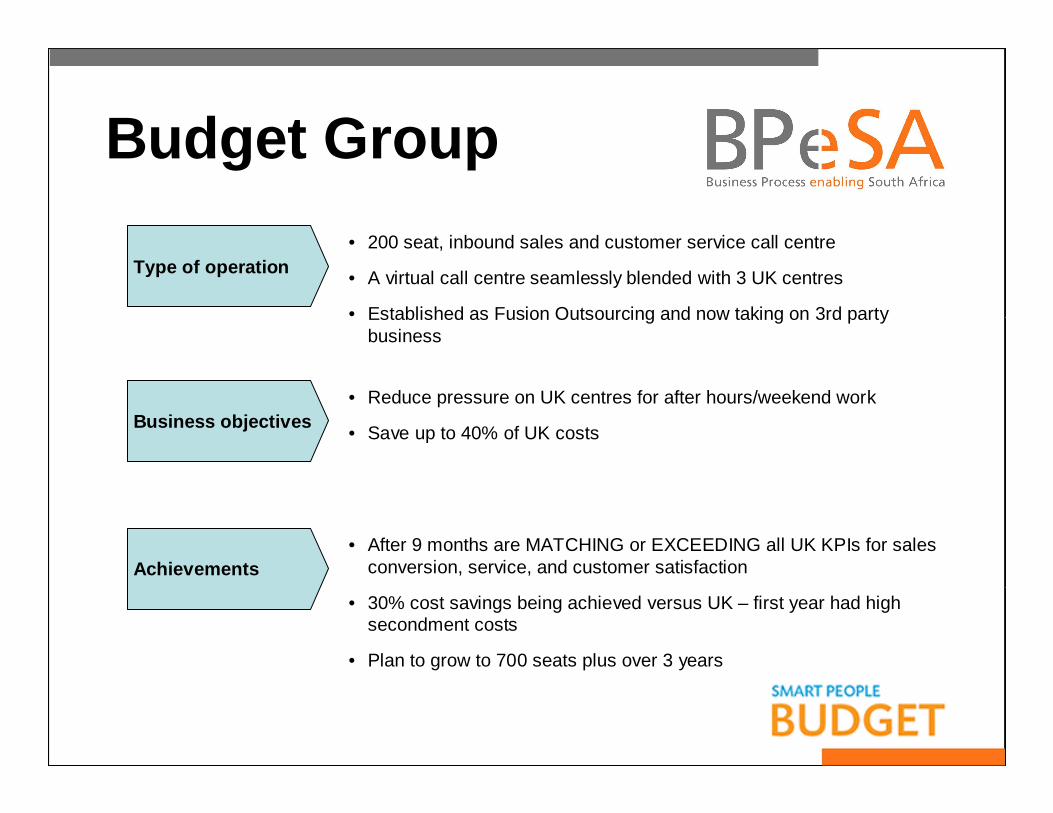

Budget Group

• 200 seat, inbound sales and customer service call centre

• A virtual call centre seamlessly blended with 3 UK centres

• Established as Fusion Outsourcing and now taking on 3rd party business

• After 9 months are MATCHING or EXCEEDING all UK KPIs for sales conversion, service, and customer satisfaction

• 30% cost savings being achieved versus UK – first year had high secondment costs

• Plan to grow to 700 seats plus over 3 years

• Reduce pressure on UK centres for after hours/weekend work

• Save up to 40% of UK costs

Type of operation

Business objectives

Achievements

34

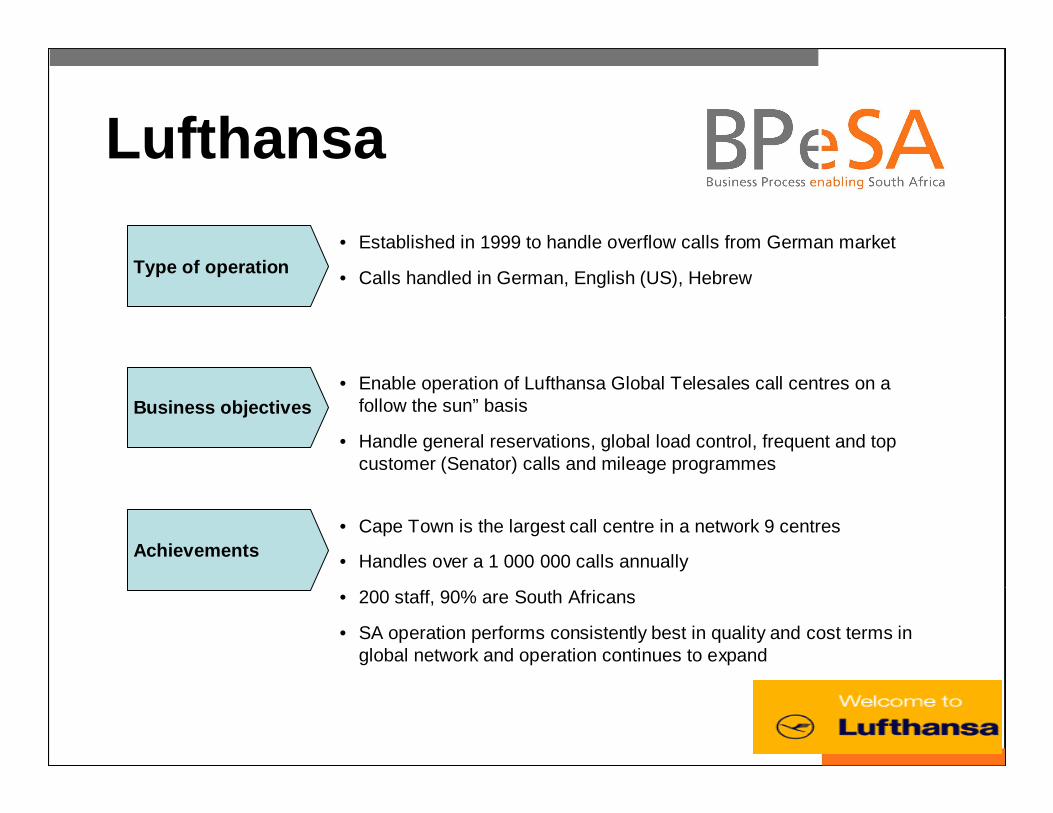

Lufthansa

• Established in 1999 to handle overflow calls from German market

• Calls handled in German, English (US), Hebrew

• Enable operation of Lufthansa Global Telesales call centres on afollow the sun” basis

• Handle general reservations, global load control, frequent and top customer (Senator) calls and mileage programmes

• Cape Town is the largest call centre in a network 9 centres

• Handles over a 1 000 000 calls annually

• 200 staff, 90% are South Africans

• SA operation performs consistently best in quality and cost terms in global network and operation continues to expand

Type of operation

Business objectives

Achievements

35

CSC

• Set up, March 2003, is a back office annual life and pensions

administration facility for US and UK clients

• Uses automated workflow distribution (AWD)

• Plan to grow to 1 000 people by 2008

• Compliment facilities in India and US to enable 24/7 operations

• SA operation exceeds India and US productivity standards in terms of policies per hour/error rates

• Value of a three country global BPO operation proven by ability to reroute work during emergencies

Type of operation

Business objectives

Achievements

36

ABSA

• Contact centre with 1 600 seats, handling up to 42 lines of business

• As an independent commercial division of the ABSA Group offers services to other divisions at market rates as well as services 3rd parties

• Division has made a significant contribution to group profits (US$8.8m) as well its customer and employee satisfaction ratings

• Services provide to US-based corporate, TransUnion have delivered the following value to the client

• Reduction of unit cost per call from $24 to $7

• Consistent achievement of all 9 service and quality targets

• Increase in IT captures from 97% to 99.95%

Type of operation

Achievements