beyond transactions building a compelling retail...

TRANSCRIPT

Beyond transactionsBuilding a compelling retail experience An Economist Intelligence Unit white paperSponsored by SAP

Beyond transactionsBuilding a compelling retail experience

© Economist Intelligence Unit Limited 20091

Preface

Beyond transactions: Building a compelling retail experience is an Economist Intelligence Unit report sponsored by SAP. The Economist Intelligence Unit bears sole responsibility for this report. The Economist Intelligence Unit’s editorial team conducted the interviews and wrote the report. The fi ndings and views expressed in this report do not necessarily refl ect the views of the sponsor. Dan Armstrong was the editor of the report and Sylvia Helm as the author. Mike Kenny was responsible for layout and design. Our thanks are due to all of the executives who responded to the survey.

October 2009

© Economist Intelligence Unit Limited 2009

Beyond transactionsBuilding a compelling retail experience

2

Contents

Introduction 3

Key fi ndings 4

Conclusion 7

Appendix 1: Overall survey results 8

Appendix 2: Americas survey results 13

Appendix 3: Asia-Pacifi c survey results 18

Appendix 4: Europe Middle East and Africa survey results 23

Beyond transactionsBuilding a compelling retail experience

© Economist Intelligence Unit Limited 20093

Introduction

Global recession, the accompanying fall in demand and the proliferation of shopping choices have combined in the last year to make retailing a tough business in which to succeed. Shoppers can buy the same goods from any number of interchangeable sources, including competing chains and multiple web commerce sites. They can use their mobile phones to scan bar codes and instantly obtain a list of stores and website where the product is available and how much it costs at each. They can reject a retailer for any number of reasons: a price that may be only pennies higher than competitors, the level of convenience, the friendliness of the sales staff, even the store’s décor. When products are delivered to the door at a low price with a click of the mouse, there is no reason to even leave the house.

To differentiate in this environment, retailers need to provide something special—something informed by the qualities that the customer values. If it is not price, the key is customer experience. Regardless of channel, the retailer needs to provide a consistently enjoyable and convenient shopping experience, ensuring that everything—from the feel of the store or website to the return and exchange policy and the promotions extended to the customer—is carefully matched with the traits that the customer values.

In this diffi cult economy, retailers would be well-advised to focus on the elements within their control, especially building customer loyalty among the most valuable customers who account for the bulk of the revenues and profi ts. Getting these customers to keep coming back requires gathering information from customer transactions, sharing that information across customer-facing units, and ultimately measuring and taking actions based on the value of each customer.

About the survey

In September 2009, the Economist Intelligence Unit surveyed 89 executives of retail organisations on the challenges of getting customer-facing departments to work together more consistently and effectively.

Survey respondents spanned the globe, with 34% from the Asia-Pacifi c region, 32% from the Americas and 34% from EMEA. Respondents’ annual revenue ranged from less than US$500m to more than US$10bn. The level of seniority of respondents was high: 31% were C-level or board members and another 17% were VPs or heads of business units.

© Economist Intelligence Unit Limited 2009

Beyond transactionsBuilding a compelling retail experience

4

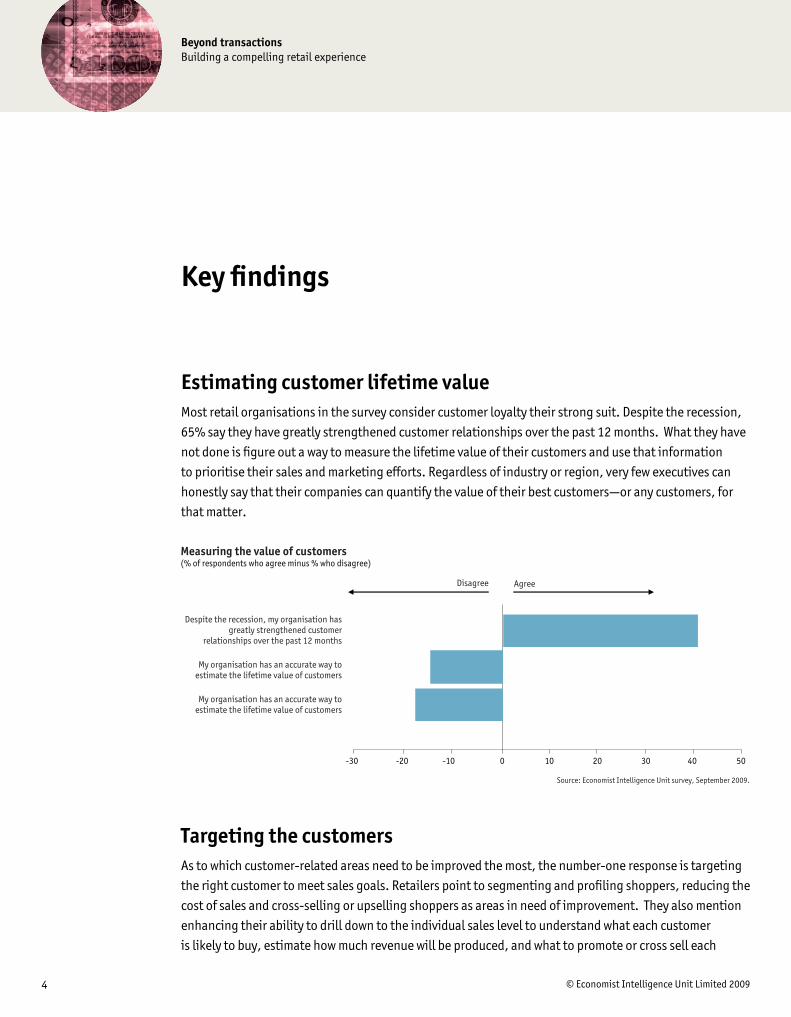

Estimating customer lifetime value Most retail organisations in the survey consider customer loyalty their strong suit. Despite the recession, 65% say they have greatly strengthened customer relationships over the past 12 months. What they have not done is fi gure out a way to measure the lifetime value of their customers and use that information to prioritise their sales and marketing efforts. Regardless of industry or region, very few executives can honestly say that their companies can quantify the value of their best customers—or any customers, for that matter.

Targeting the customersAs to which customer-related areas need to be improved the most, the number-one response is targeting the right customer to meet sales goals. Retailers point to segmenting and profi ling shoppers, reducing the cost of sales and cross-selling or upselling shoppers as areas in need of improvement. They also mention enhancing their ability to drill down to the individual sales level to understand what each customer is likely to buy, estimate how much revenue will be produced, and what to promote or cross sell each

Key fi ndings

Measuring the value of customers(% of respondents who agree minus % who disagree)

Source: Economist Intelligence Unit survey, September 2009.

Despite the recession, my organisation has greatly strengthened customer

relationships over the past 12 months

My organisation has an accurate way to estimate the lifetime value of customers

My organisation has an accurate way to estimate the lifetime value of customers

Disagree Agree

-30 -20 -10 0 10 20 30 40 50

Beyond transactionsBuilding a compelling retail experience

© Economist Intelligence Unit Limited 20095

customer. To do this, retailers have moved beyond traditional demographic criteria to frequency and size of purchases, lifestyle information and the last product bought.

For instance, the US women’s clothing retailer Coldwater Creek—which sells through retail stores, a web site and direct-mail catalogs—recently announced the launch of the “Onecreek” loyalty program aimed at the top 5% of the company’s active customers. It offers early peeks at new merchandise, a personal shopper, free shipping on returns and a gift on the customer’s birthday. Eligible customers are those who purchase three times as frequently and spend four times as much as an average customer. “The program is designed to improve retention and overall spend within this very important and profi table segment of our customer base,” said Dennis Pence, the company’s CEO, in a press release.

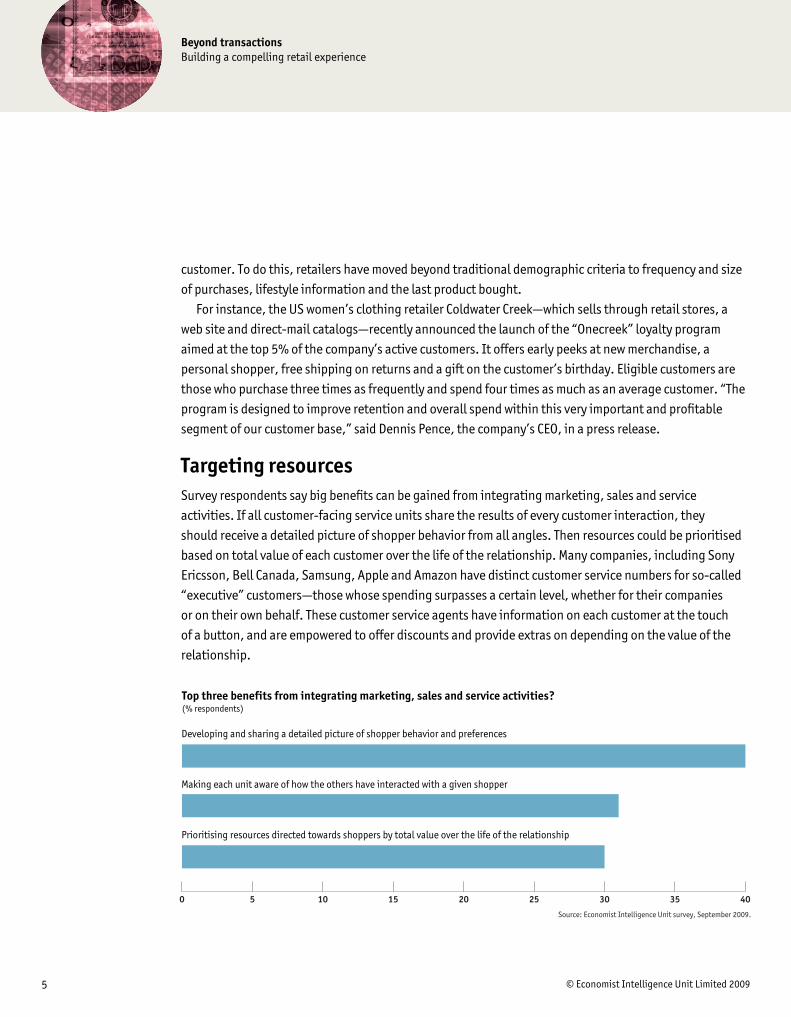

Targeting resourcesSurvey respondents say big benefi ts can be gained from integrating marketing, sales and service activities. If all customer-facing service units share the results of every customer interaction, they should receive a detailed picture of shopper behavior from all angles. Then resources could be prioritised based on total value of each customer over the life of the relationship. Many companies, including Sony Ericsson, Bell Canada, Samsung, Apple and Amazon have distinct customer service numbers for so-called “executive” customers—those whose spending surpasses a certain level, whether for their companies or on their own behalf. These customer service agents have information on each customer at the touch of a button, and are empowered to offer discounts and provide extras on depending on the value of the relationship.

0 5 10 15 20 25 30 35 40

Source: Economist Intelligence Unit survey, September 2009.

Developing and sharing a detailed picture of shopper behavior and preferences

Making each unit aware of how the others have interacted with a given shopper

Prioritising resources directed towards shoppers by total value over the life of the relationship

Top three benefits from integrating marketing, sales and service activities? (% respondents)

© Economist Intelligence Unit Limited 2009

Beyond transactionsBuilding a compelling retail experience

6

How the three regions differThe three regions surveyed—the Americas, Asia-Pacifi c and EMEA –all give themselves top marks for excellent customer service. All pride themselves on the loyalty of their customers. And all admit that their organisations cannot accurately measure the value of—or even identify, in many cases—their most profi table customers. The challenges faced in each region include the following.

Americas Reducing the cost of sales—necessary to keep margins low and prices competitive—is a top priority for Americas retail organisations. In the Americas, customer feedback tends to be fi ltered through the less expensive e-commerce channels, rather than from direct response feedback (as is the case in the two other regions).

Asia-Pacifi c Asia-Pacifi c retail organisations get most of their customer feedback in stores, through retail sales staff, and at the point of sale. They are the lowest users of e-commerce, and call centers are used by only 17% of respondents.

EMEA Of all regions surveyed, EMEA retail organisations are the least able to gauge the lifetime value of customers. Most in need of improvement: profi ling, targeting, and cross selling or up selling existing customers. EMEA retailers use call centers the least and direct response (direct mail, e-mail) the most.

Beyond transactionsBuilding a compelling retail experience

© Economist Intelligence Unit Limited 20097

Few survey respondents say they can accurately measure the value of customers. Faced with challenges they cannot control—global economic trends, rapid shifts in product demand, commoditization of the retail channel—they have to focus on what they can control, working to understand the customer and provide a pleasant and convenient retail experience. Retailer organisations should consider how to:

l Do a better job of analysing the customer base and measuring the value of individual customers.

l Share and act on customer information in all customer-facing units, making sure to improve the weak links.

l Differentiate customers by products purchased, services used and revenues generated.

l Provide distinct service to high-value customers, building their trust, increasing their loyalty, and generating more revenues.

Conclusion

8 Economist Intelligence Unit 2009

Appendix 1Overall survey results

Beyond transactionsBuilding a compelling retail experience

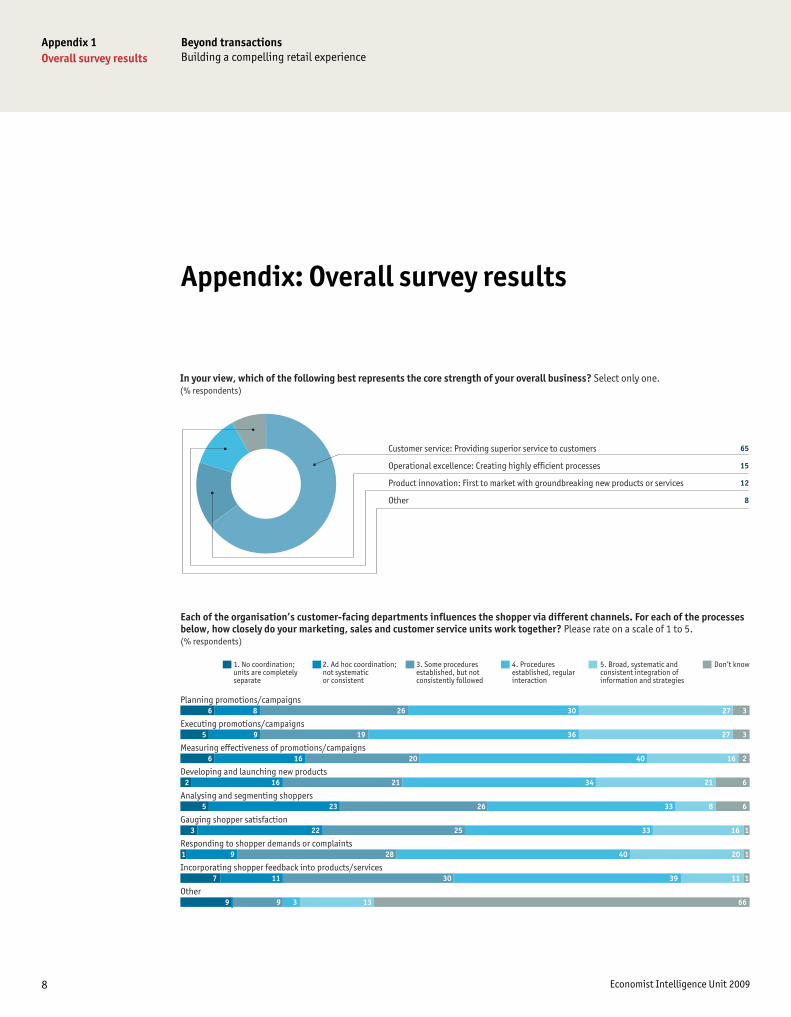

Appendix: Overall survey results

65

15

12

8

Customer service: Providing superior service to customers

Operational excellence: Creating highly efficient processes

Product innovation: First to market with groundbreaking new products or services

Other

In your view, which of the following best represents the core strength of your overall business? Select only one.(% respondents)

1. No coordination; 2. Ad hoc coordination; 3. Some procedures 4. Procedures 5. Broad, systematic and Don’t knowunits are completely not systematic established, but not established, regular consistent integration of separate or consistent consistently followed interaction information and strategies

Planning promotions/campaigns

Executing promotions/campaigns

Measuring effectiveness of promotions/campaigns

Developing and launching new products

Analysing and segmenting shoppers

Gauging shopper satisfaction

Responding to shopper demands or complaints

Incorporating shopper feedback into products/services

Other

Each of the organisation’s customer-facing departments influences the shopper via different channels. For each of the processes below, how closely do your marketing, sales and customer service units work together? Please rate on a scale of 1 to 5.(% respondents)

6 8 26 30 27 3

5 9 19 36 27 3

6 16 20 40 16 2

2 16 21 34 21 6

5 23 26 33 8 6

3 22 25 33 16 1

1 9 28 40 20 1

7 11 30 39 11 1

9 9 3 13 66

Appendix 1Overall survey results

Beyond transactionsBuilding a compelling retail experience

9 Economist Intelligence Unit 2009

Targeting the right shoppers to achieve sales volume and revenue objectives

Segmenting and profiling shoppers

Reducing the cost of sales

Cross-selling or upselling shoppers

Measuring/optimising effectiveness of marketing and promotional campaigns

Maximising repeat purchases and building loyalty among shoppers

Gathering shopper intelligence in the course of providing service

Measuring the satisfaction of shoppers

Generating promotions/campaigns

Involving shoppers in product/service development (eg, co-creation)

Building long-term relationships with store management

Ensuring that shopper complaints are resolved quickly

Creating effective collateral

Other

Don’t know

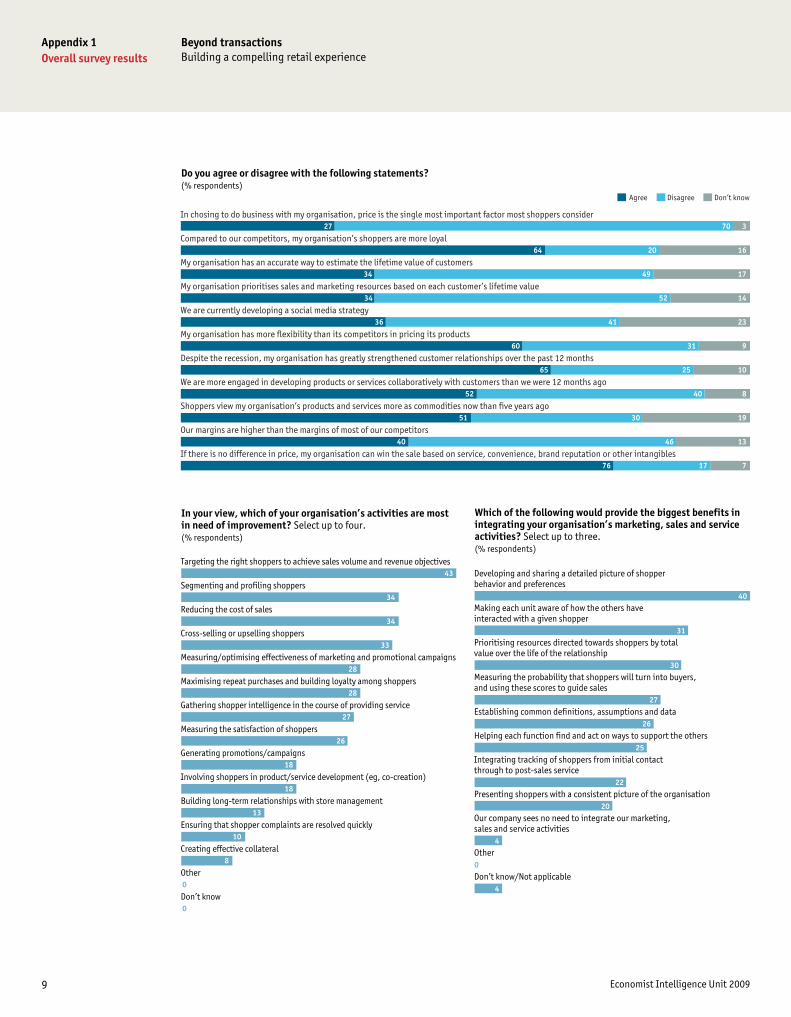

In your view, which of your organisation’s activities are most in need of improvement? Select up to four. (% respondents)

43

34

34

33

28

28

27

26

18

18

13

10

8

0

0

Developing and sharing a detailed picture of shopper behavior and preferences

Making each unit aware of how the others have interacted with a given shopper

Prioritising resources directed towards shoppers by total value over the life of the relationship

Measuring the probability that shoppers will turn into buyers, and using these scores to guide sales

Establishing common definitions, assumptions and data

Helping each function find and act on ways to support the others

Integrating tracking of shoppers from initial contact through to post-sales service

Presenting shoppers with a consistent picture of the organisation

Our company sees no need to integrate our marketing, sales and service activities

Other

Don’t know/Not applicable

Which of the following would provide the biggest benefits in integrating your organisation’s marketing, sales and service activities? Select up to three. (% respondents)

40

31

30

27

26

25

22

20

4

0

4

Do you agree or disagree with the following statements?(% respondents)

In chosing to do business with my organisation, price is the single most important factor most shoppers consider

Compared to our competitors, my organisation’s shoppers are more loyal

My organisation has an accurate way to estimate the lifetime value of customers

My organisation prioritises sales and marketing resources based on each customer’s lifetime value

We are currently developing a social media strategy

My organisation has more flexibility than its competitors in pricing its products

Despite the recession, my organisation has greatly strengthened customer relationships over the past 12 months

We are more engaged in developing products or services collaboratively with customers than we were 12 months ago

Shoppers view my organisation’s products and services more as commodities now than five years ago

Our margins are higher than the margins of most of our competitors

If there is no difference in price, my organisation can win the sale based on service, convenience, brand reputation or other intangibles

Agree Disagree Don’t know

27 70 3

64 20 16

34 49 17

34 52 14

36 41 23

60 31 9

65 25 10

52 40 8

51 30 19

40 46 13

76 17 7

10 Economist Intelligence Unit 2009

Appendix 1Overall survey results

Beyond transactionsBuilding a compelling retail experience

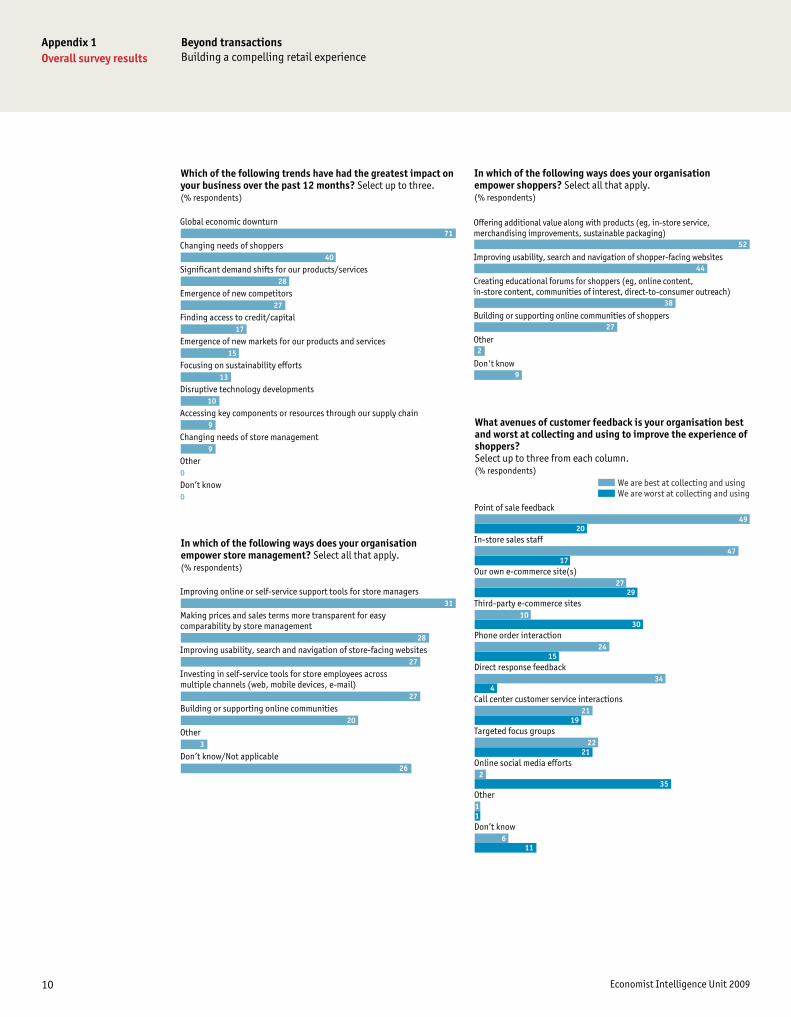

Global economic downturn

Changing needs of shoppers

Significant demand shifts for our products/services

Emergence of new competitors

Finding access to credit/capital

Emergence of new markets for our products and services

Focusing on sustainability efforts

Disruptive technology developments

Accessing key components or resources through our supply chain

Changing needs of store management

Other

Don’t know

Which of the following trends have had the greatest impact on your business over the past 12 months? Select up to three.(% respondents)

71

40

28

27

17

15

13

10

9

9

0

0

Improving online or self-service support tools for store managers

Making prices and sales terms more transparent for easy comparability by store management

Improving usability, search and navigation of store-facing websites

Investing in self-service tools for store employees across multiple channels (web, mobile devices, e-mail)

Building or supporting online communities

Other

Don’t know/Not applicable

In which of the following ways does your organisation empower store management? Select all that apply.(% respondents)

31

28

27

27

20

3

26

Offering additional value along with products (eg, in-store service, merchandising improvements, sustainable packaging)

Improving usability, search and navigation of shopper-facing websites

Creating educational forums for shoppers (eg, online content, in-store content, communities of interest, direct-to-consumer outreach)

Building or supporting online communities of shoppers

Other

Don't know

In which of the following ways does your organisation empower shoppers? Select all that apply. (% respondents)

52

44

38

27

2

9

Point of sale feedback

In-store sales staff

Our own e-commerce site(s)

Third-party e-commerce sites

Phone order interaction

Direct response feedback

Call center customer service interactions

Targeted focus groups

Online social media efforts

Other

Don’t know

What avenues of customer feedback is your organisation best and worst at collecting and using to improve the experience of shoppers? Select up to three from each column.(% respondents)

We are best at collecting and usingWe are worst at collecting and using

49 20

47 17

27 29

10 30

24 15

34 4

21 19

22 21

2 35

11

6 11

Appendix 1Overall survey results

Beyond transactionsBuilding a compelling retail experience

11 Economist Intelligence Unit 2009

Putting recommendations into action

Persuading shoppers to share experiences, both positive and negative

Persuading store employees to share feedback from shoppers, both positive and negative

Synthesising information from retail outlets into coherent recommendations

Distinguishing relevant from irrelevant shopper information

Monitoring the results of actions in terms of shopper behaviour and marketing metrics

Synthesising information from customer service into coherent recommendations

Dealing systematically with extremely high volumes of information from stores

Demonstrating to shoppers that their comments are being addressed

Synthesising information from online channels into coherent recommendations

Other

Don’t know

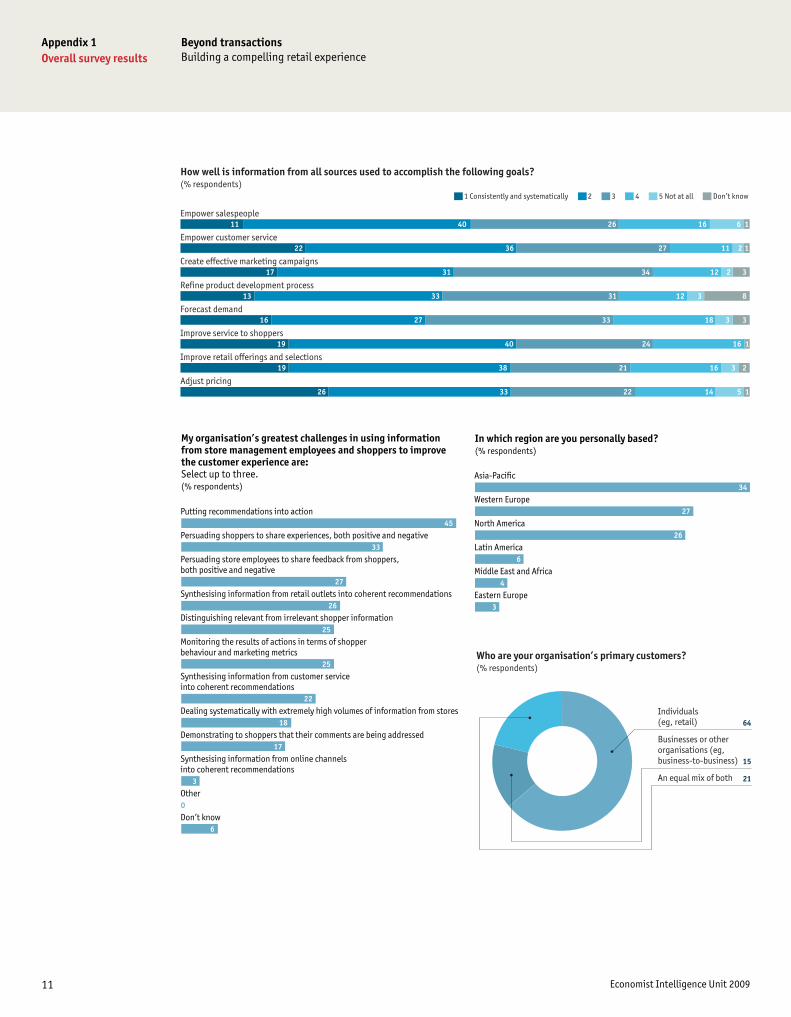

My organisation’s greatest challenges in using information from store management employees and shoppers to improve the customer experience are: Select up to three. (% respondents)

45

33

27

26

25

25

22

18

17

3

0

6

Asia-Pacific

Western Europe

North America

Latin America

Middle East and Africa

Eastern Europe

In which region are you personally based? (% respondents)

34

27

26

6

4

3

64

15

21

Individuals (eg, retail)

Businesses or other organisations (eg, business-to-business)

An equal mix of both

Who are your organisation’s primary customers?(% respondents)

1 Consistently and systematically 2 3 4 5 Not at all Don’t know

Empower salespeople

Empower customer service

Create effective marketing campaigns

Refine product development process

Forecast demand

Improve service to shoppers

Improve retail offerings and selections

Adjust pricing

How well is information from all sources used to accomplish the following goals?(% respondents)

11 40 26 16 6 1

22 36 27 11 2 1

17 31 34 12 2 3

13 33 31 12 3 8

16 27 33 18 3 3

19 40 24 16 1

19 38 21 16 3 2

26 33 22 14 5 1

12 Economist Intelligence Unit 2009

Appendix 1Overall survey results

Beyond transactionsBuilding a compelling retail experience

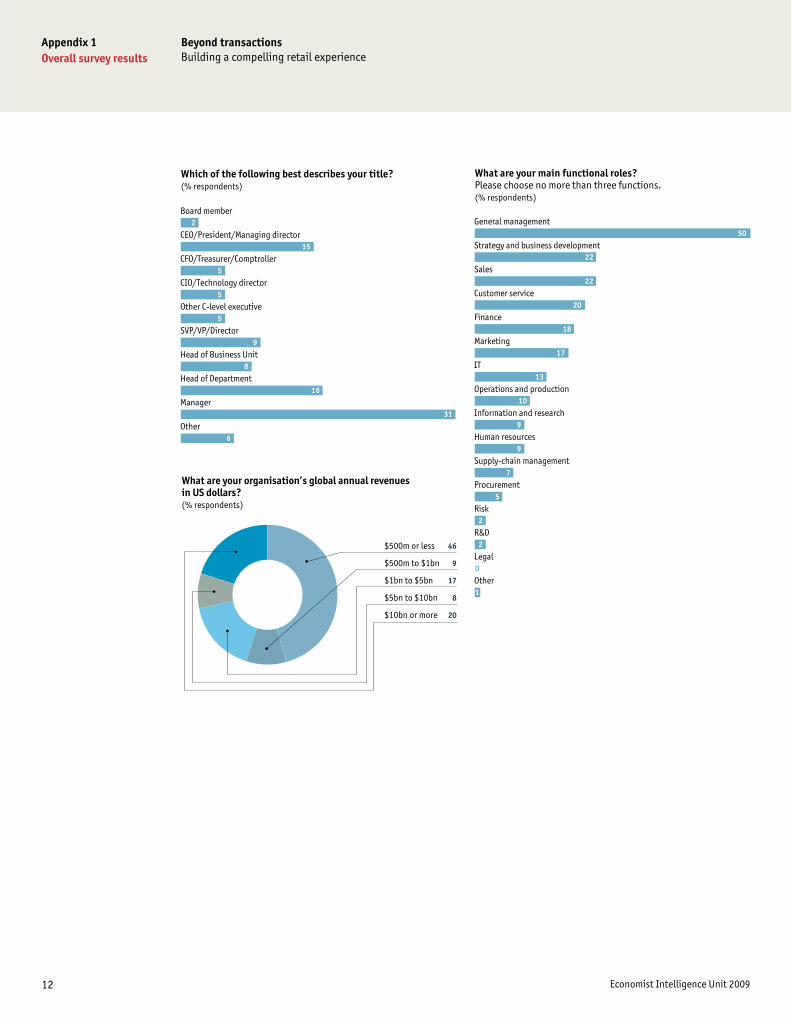

46

9

17

8

20

$500m or less

$500m to $1bn

$1bn to $5bn

$5bn to $10bn

$10bn or more

What are your organisation’s global annual revenues in US dollars? (% respondents)

General management

Strategy and business development

Sales

Customer service

Finance

Marketing

IT

Operations and production

Information and research

Human resources

Supply-chain management

Procurement

Risk

R&D

Legal

Other

What are your main functional roles? Please choose no more than three functions.(% respondents)

50

22

22

20

18

17

13

10

9

9

7

5

2

2

0

1

Board member

CEO/President/Managing director

CFO/Treasurer/Comptroller

CIO/Technology director

Other C-level executive

SVP/VP/Director

Head of Business Unit

Head of Department

Manager

Other

Which of the following best describes your title?(% respondents)

2

15

5

5

5

9

8

16

31

6

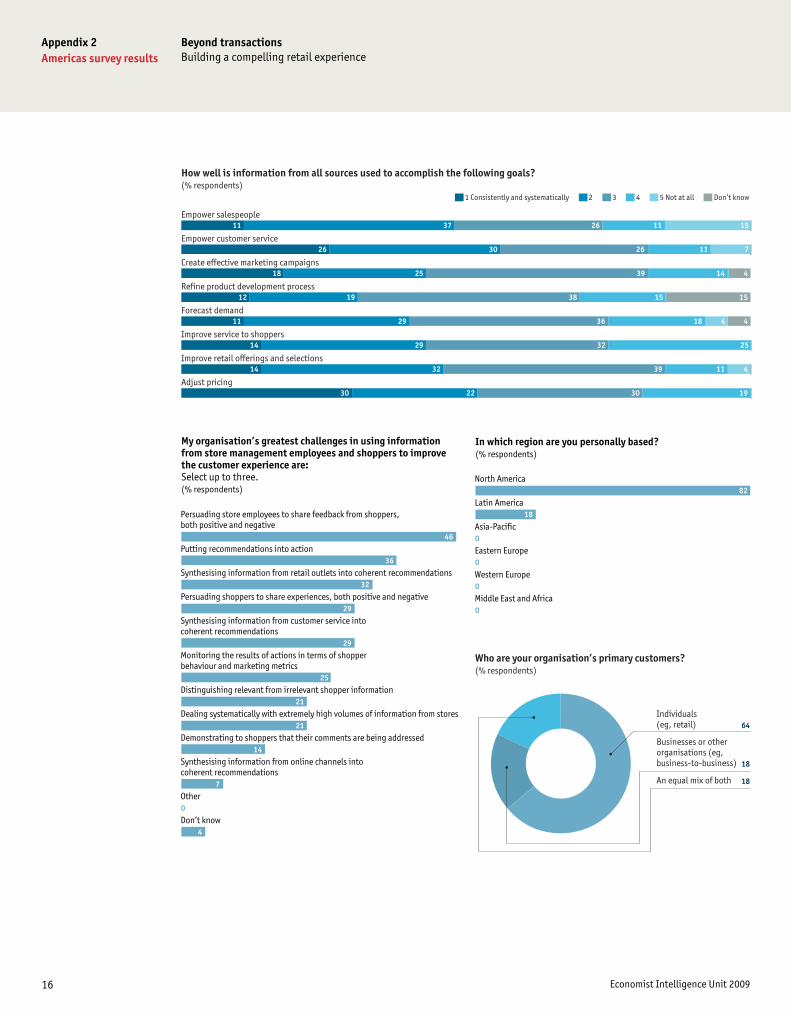

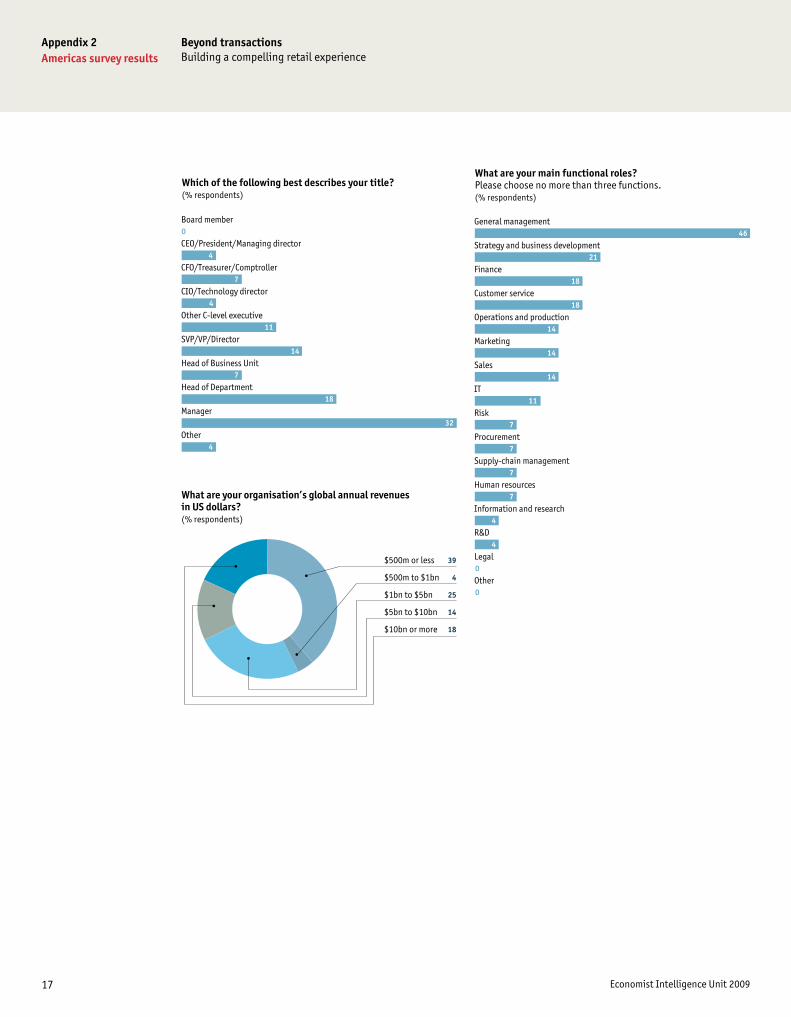

Appendix 2Americas survey results

Beyond transactionsBuilding a compelling retail experience

13 Economist Intelligence Unit 2009

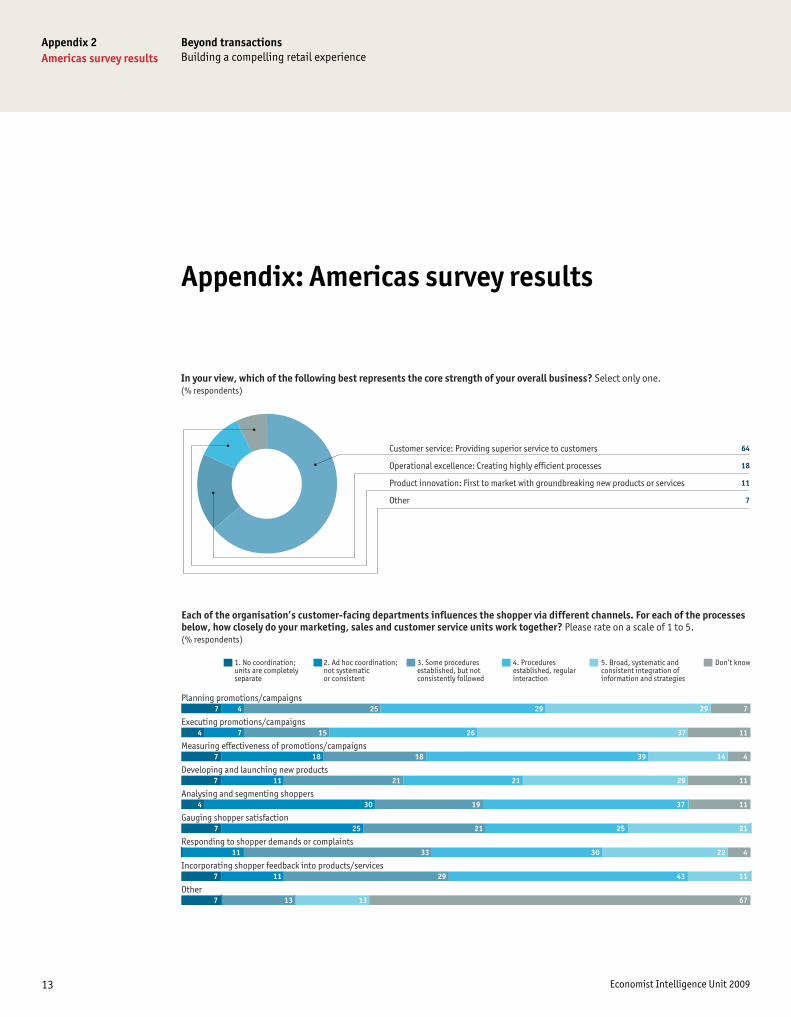

Appendix: Americas survey results

64

18

11

7

Customer service: Providing superior service to customers

Operational excellence: Creating highly efficient processes

Product innovation: First to market with groundbreaking new products or services

Other

In your view, which of the following best represents the core strength of your overall business? Select only one.(% respondents)

1. No coordination; 2. Ad hoc coordination; 3. Some procedures 4. Procedures 5. Broad, systematic and Don’t knowunits are completely not systematic established, but not established, regular consistent integration of separate or consistent consistently followed interaction information and strategies

Planning promotions/campaigns

Executing promotions/campaigns

Measuring effectiveness of promotions/campaigns

Developing and launching new products

Analysing and segmenting shoppers

Gauging shopper satisfaction

Responding to shopper demands or complaints

Incorporating shopper feedback into products/services

Other

Each of the organisation’s customer-facing departments influences the shopper via different channels. For each of the processes below, how closely do your marketing, sales and customer service units work together? Please rate on a scale of 1 to 5.(% respondents)

7 4 25 29 29 7

4 7 15 26 37 11

7 18 18 39 14 4

7 11 21 21 29 11

4 30 19 37 11

7 25 21 25 21 0

11 33 30 22 4

7 11 29 43 11 0

7 13 13 67

14 Economist Intelligence Unit 2009

Appendix 2Americas survey results

Beyond transactionsBuilding a compelling retail experience

Targeting the right shoppers to achieve sales volume and revenue objectives

Reducing the cost of sales

Measuring/optimising effectiveness of marketing and promotional campaigns

Gathering shopper intelligence in the course of providing service

Segmenting and profiling shoppers

Maximising repeat purchases and building loyalty among shoppers

Cross-selling or upselling shoppers

Measuring the satisfaction of shoppers

Involving shoppers in product/service development (eg, co-creation)

Generating promotions/campaigns

Creating effective collateral

Ensuring that shopper complaints are resolved quickly

Building long-term relationships with store management

Other

Don’t know

In your view, which of your organisation’s activities are most in need of improvement? Select up to four. (% respondents)

46

43

39

29

25

25

18

18

14

11

11

11

7

0

0

Developing and sharing a detailed picture of shopper behavior and preferences

Helping each function find and act on ways to support the others

Prioritising resources directed towards shoppers by total value over the life of the relationship

Making each unit aware of how the others have interacted with a given shopper

Establishing common definitions, assumptions and data

Integrating tracking of shoppers from initial contact through to post-sales service

Measuring the probability that shoppers will turn into buyers, and using these scores to guide sales

Presenting shoppers with a consistent picture of the organisation

Our company sees no need to integrate our marketing, sales and service activities

Other

Don’t know/Not applicable

Which of the following would provide the biggest benefits in integrating your organisation’s marketing, sales and service activities? Select up to three. (% respondents)

39

32

32

29

25

25

25

21

4

0

4

Do you agree or disagree with the following statements?(% respondents)

In chosing to do business with my organisation, price is the single most important factor most shoppers consider

Compared to our competitors, my organisation’s shoppers are more loyal

My organisation has an accurate way to estimate the lifetime value of customers

My organisation prioritises sales and marketing resources based on each customer’s lifetime value

We are currently developing a social media strategy

My organisation has more flexibility than its competitors in pricing its products

Despite the recession, my organisation has greatly strengthened customer relationships over the past 12 months

We are more engaged in developing products or services collaboratively with customers than we were 12 months ago

Shoppers view my organisation’s products and services more as commodities now than five years ago

Our margins are higher than the margins of most of our competitors

If there is no difference in price, my organisation can win the sale based on service, convenience, brand reputation or other intangibles

Agree Disagree Don’t know

36 61 4

63 15 22

41 37 22

26 56 19

44 30 26

61 21 18

59 30 11

50 43 7

44 30 26

43 46 11

74 19 7

Appendix 2Americas survey results

Beyond transactionsBuilding a compelling retail experience

15 Economist Intelligence Unit 2009

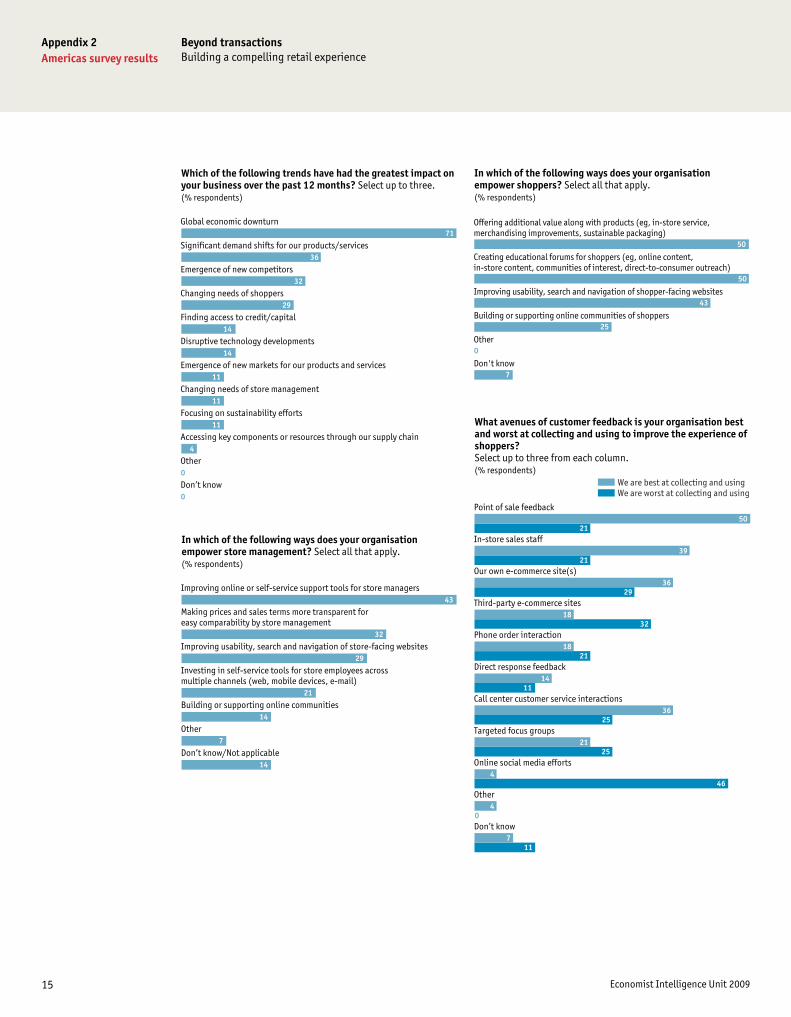

Global economic downturn

Significant demand shifts for our products/services

Emergence of new competitors

Changing needs of shoppers

Finding access to credit/capital

Disruptive technology developments

Emergence of new markets for our products and services

Changing needs of store management

Focusing on sustainability efforts

Accessing key components or resources through our supply chain

Other

Don’t know

Which of the following trends have had the greatest impact on your business over the past 12 months? Select up to three.(% respondents)

71

36

32

29

14

14

11

11

11

4

0

0

Improving online or self-service support tools for store managers

Making prices and sales terms more transparent for easy comparability by store management

Improving usability, search and navigation of store-facing websites

Investing in self-service tools for store employees across multiple channels (web, mobile devices, e-mail)

Building or supporting online communities

Other

Don’t know/Not applicable

In which of the following ways does your organisation empower store management? Select all that apply.(% respondents)

43

32

29

21

14

7

14

Offering additional value along with products (eg, in-store service, merchandising improvements, sustainable packaging)

Creating educational forums for shoppers (eg, online content, in-store content, communities of interest, direct-to-consumer outreach)

Improving usability, search and navigation of shopper-facing websites

Building or supporting online communities of shoppers

Other

Don't know

In which of the following ways does your organisation empower shoppers? Select all that apply. (% respondents)

50

50

43

25

0

7

Point of sale feedback

In-store sales staff

Our own e-commerce site(s)

Third-party e-commerce sites

Phone order interaction

Direct response feedback

Call center customer service interactions

Targeted focus groups

Online social media efforts

Other

Don’t know

What avenues of customer feedback is your organisation best and worst at collecting and using to improve the experience of shoppers? Select up to three from each column.(% respondents)

We are best at collecting and usingWe are worst at collecting and using

50 21

39 21

36 29

18 32

18 21

14 11

36 25

21 25

4 46

40

7 11

16 Economist Intelligence Unit 2009

Appendix 2Americas survey results

Beyond transactionsBuilding a compelling retail experience

Persuading store employees to share feedback from shoppers, both positive and negative

Putting recommendations into action

Synthesising information from retail outlets into coherent recommendations

Persuading shoppers to share experiences, both positive and negative

Synthesising information from customer service into coherent recommendations

Monitoring the results of actions in terms of shopper behaviour and marketing metrics

Distinguishing relevant from irrelevant shopper information

Dealing systematically with extremely high volumes of information from stores

Demonstrating to shoppers that their comments are being addressed

Synthesising information from online channels into coherent recommendations

Other

Don’t know

My organisation’s greatest challenges in using information from store management employees and shoppers to improve the customer experience are: Select up to three. (% respondents)

46

36

32

29

29

25

21

21

14

7

0

4

North America

Latin America

Asia-Pacific

Eastern Europe

Western Europe

Middle East and Africa

In which region are you personally based? (% respondents)

82

18

0

0

0

0

64

18

18

Individuals (eg, retail)

Businesses or other organisations (eg, business-to-business)

An equal mix of both

Who are your organisation’s primary customers?(% respondents)

1 Consistently and systematically 2 3 4 5 Not at all Don’t know

Empower salespeople

Empower customer service

Create effective marketing campaigns

Refine product development process

Forecast demand

Improve service to shoppers

Improve retail offerings and selections

Adjust pricing

How well is information from all sources used to accomplish the following goals?(% respondents)

11 37 26 11 15

26 30 26 11 7

18 25 39 14 4

12 19 38 15 15

11 29 36 18 4 4

14 29 32 25

14 32 39 11 4

30 22 30 19

Appendix 2Americas survey results

Beyond transactionsBuilding a compelling retail experience

17 Economist Intelligence Unit 2009

Board member

CEO/President/Managing director

CFO/Treasurer/Comptroller

CIO/Technology director

Other C-level executive

SVP/VP/Director

Head of Business Unit

Head of Department

Manager

Other

Which of the following best describes your title?(% respondents)

0

4

7

4

11

14

7

18

32

4

39

4

25

14

18

$500m or less

$500m to $1bn

$1bn to $5bn

$5bn to $10bn

$10bn or more

What are your organisation’s global annual revenues in US dollars? (% respondents)

General management

Strategy and business development

Finance

Customer service

Operations and production

Marketing

Sales

IT

Risk

Procurement

Supply-chain management

Human resources

Information and research

R&D

Legal

Other

What are your main functional roles? Please choose no more than three functions.(% respondents)

46

21

18

18

14

14

14

11

7

7

7

7

4

4

0

0

18 Economist Intelligence Unit 2009

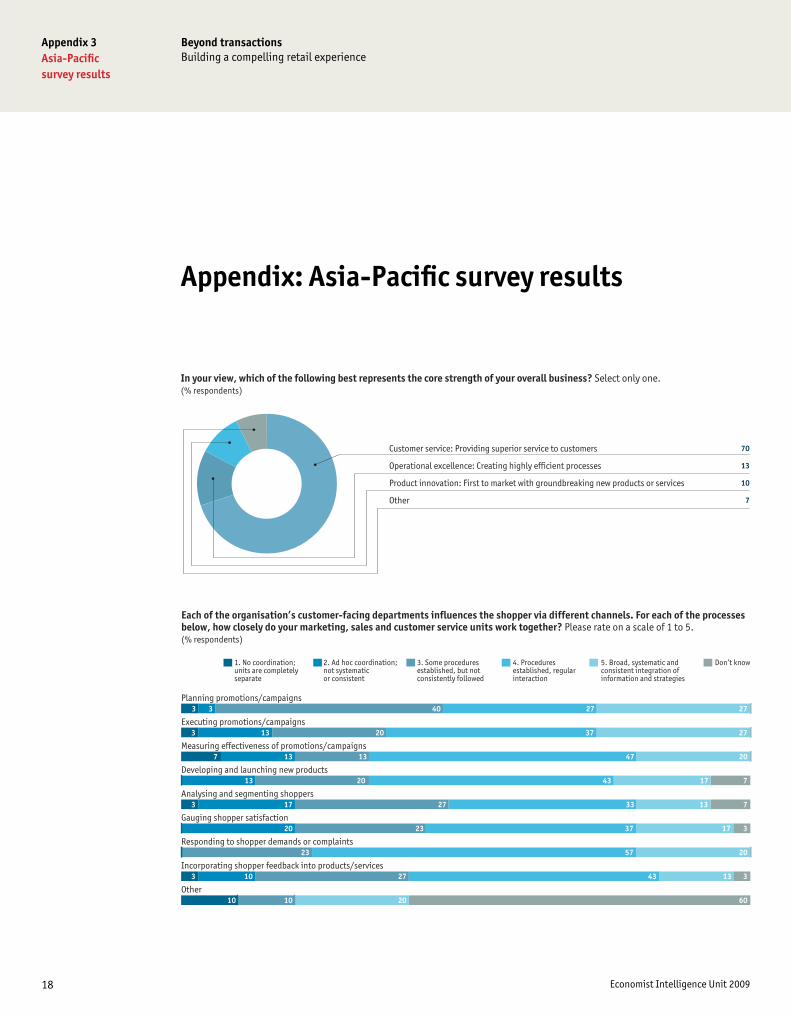

Appendix 3Asia-Pacifi c survey results

Beyond transactionsBuilding a compelling retail experience

Appendix: Asia-Pacifi c survey results

70

13

10

7

Customer service: Providing superior service to customers

Operational excellence: Creating highly efficient processes

Product innovation: First to market with groundbreaking new products or services

Other

In your view, which of the following best represents the core strength of your overall business? Select only one.(% respondents)

1. No coordination; 2. Ad hoc coordination; 3. Some procedures 4. Procedures 5. Broad, systematic and Don’t knowunits are completely not systematic established, but not established, regular consistent integration of separate or consistent consistently followed interaction information and strategies

Planning promotions/campaigns

Executing promotions/campaigns

Measuring effectiveness of promotions/campaigns

Developing and launching new products

Analysing and segmenting shoppers

Gauging shopper satisfaction

Responding to shopper demands or complaints

Incorporating shopper feedback into products/services

Other

Each of the organisation’s customer-facing departments influences the shopper via different channels. For each of the processes below, how closely do your marketing, sales and customer service units work together? Please rate on a scale of 1 to 5.(% respondents)

3 3 40 27 27 0

3 13 20 37 27 0

7 13 13 47 20 0

13 20 43 17 7

3 17 27 33 13 7

20 23 37 17 3

23 57 20 0

3 10 27 43 13 3

10 10 20 60

19 Economist Intelligence Unit 2009

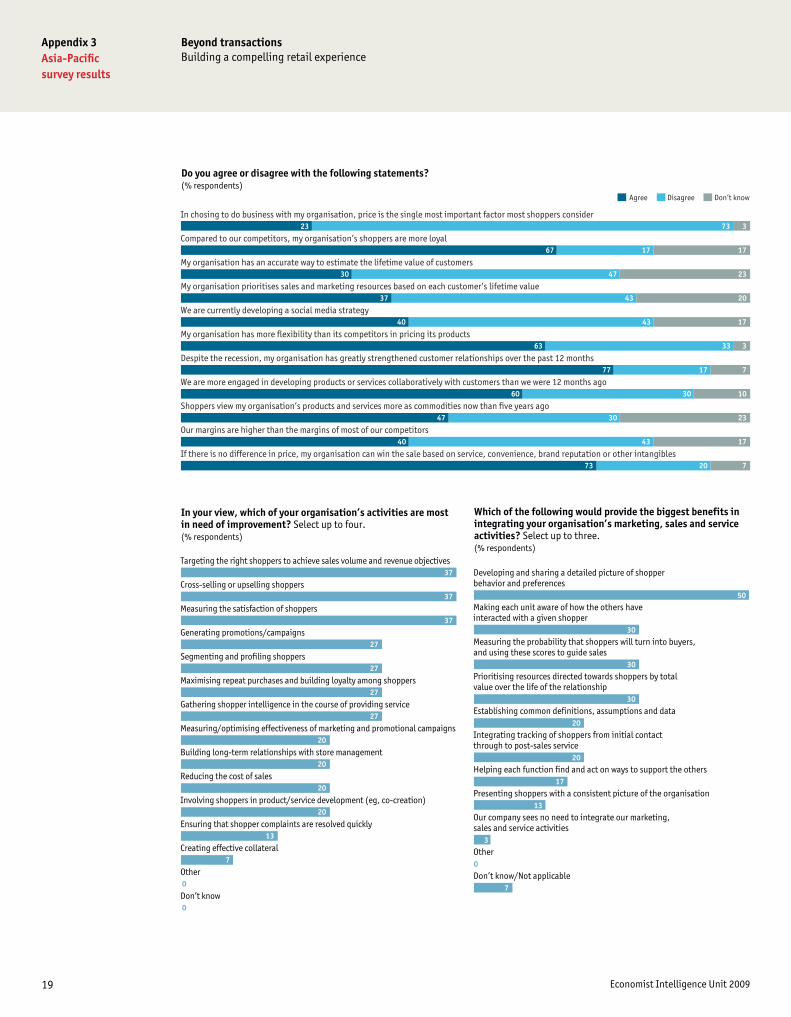

Appendix 3Asia-Pacifi c survey results

Beyond transactionsBuilding a compelling retail experience

Targeting the right shoppers to achieve sales volume and revenue objectives

Cross-selling or upselling shoppers

Measuring the satisfaction of shoppers

Generating promotions/campaigns

Segmenting and profiling shoppers

Maximising repeat purchases and building loyalty among shoppers

Gathering shopper intelligence in the course of providing service

Measuring/optimising effectiveness of marketing and promotional campaigns

Building long-term relationships with store management

Reducing the cost of sales

Involving shoppers in product/service development (eg, co-creation)

Ensuring that shopper complaints are resolved quickly

Creating effective collateral

Other

Don’t know

In your view, which of your organisation’s activities are most in need of improvement? Select up to four. (% respondents)

37

37

37

27

27

27

27

20

20

20

20

13

7

0

0

Developing and sharing a detailed picture of shopper behavior and preferences

Making each unit aware of how the others have interacted with a given shopper

Measuring the probability that shoppers will turn into buyers, and using these scores to guide sales

Prioritising resources directed towards shoppers by total value over the life of the relationship

Establishing common definitions, assumptions and data

Integrating tracking of shoppers from initial contact through to post-sales service

Helping each function find and act on ways to support the others

Presenting shoppers with a consistent picture of the organisation

Our company sees no need to integrate our marketing, sales and service activities

Other

Don’t know/Not applicable

Which of the following would provide the biggest benefits in integrating your organisation’s marketing, sales and service activities? Select up to three. (% respondents)

50

30

30

30

20

20

17

13

3

0

7

Do you agree or disagree with the following statements?(% respondents)

In chosing to do business with my organisation, price is the single most important factor most shoppers consider

Compared to our competitors, my organisation’s shoppers are more loyal

My organisation has an accurate way to estimate the lifetime value of customers

My organisation prioritises sales and marketing resources based on each customer’s lifetime value

We are currently developing a social media strategy

My organisation has more flexibility than its competitors in pricing its products

Despite the recession, my organisation has greatly strengthened customer relationships over the past 12 months

We are more engaged in developing products or services collaboratively with customers than we were 12 months ago

Shoppers view my organisation’s products and services more as commodities now than five years ago

Our margins are higher than the margins of most of our competitors

If there is no difference in price, my organisation can win the sale based on service, convenience, brand reputation or other intangibles

Agree Disagree Don’t know

23 73 3

67 17 17

30 47 23

37 43 20

40 43 17

63 33 3

77 17 7

60 30 10

47 30 23

40 43 17

73 20 7

20 Economist Intelligence Unit 2009

Appendix 3Asia-Pacifi c survey results

Beyond transactionsBuilding a compelling retail experience

Global economic downturn

Changing needs of shoppers

Emergence of new markets for our products and services

Significant demand shifts for our products/services

Emergence of new competitors

Focusing on sustainability efforts

Accessing key components or resources through our supply chain

Finding access to credit/capital

Disruptive technology developments

Changing needs of store management

Other

Don’t know

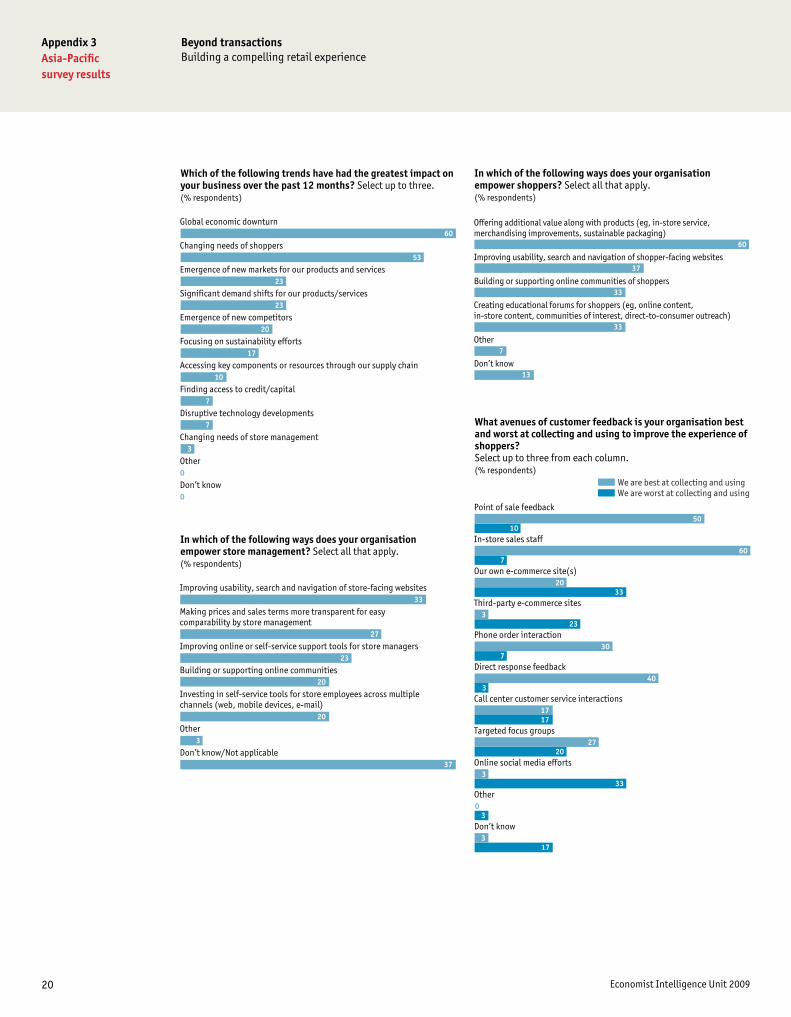

Which of the following trends have had the greatest impact on your business over the past 12 months? Select up to three.(% respondents)

60

53

23

23

20

17

10

7

7

3

0

0

Improving usability, search and navigation of store-facing websites

Making prices and sales terms more transparent for easy comparability by store management

Improving online or self-service support tools for store managers

Building or supporting online communities

Investing in self-service tools for store employees across multiple channels (web, mobile devices, e-mail)

Other

Don’t know/Not applicable

In which of the following ways does your organisation empower store management? Select all that apply.(% respondents)

33

27

23

20

20

3

37

Offering additional value along with products (eg, in-store service, merchandising improvements, sustainable packaging)

Improving usability, search and navigation of shopper-facing websites

Building or supporting online communities of shoppers

Creating educational forums for shoppers (eg, online content, in-store content, communities of interest, direct-to-consumer outreach)

Other

Don’t know

In which of the following ways does your organisation empower shoppers? Select all that apply. (% respondents)

60

37

33

33

7

13

Point of sale feedback

In-store sales staff

Our own e-commerce site(s)

Third-party e-commerce sites

Phone order interaction

Direct response feedback

Call center customer service interactions

Targeted focus groups

Online social media efforts

Other

Don’t know

What avenues of customer feedback is your organisation best and worst at collecting and using to improve the experience of shoppers? Select up to three from each column.(% respondents)

We are best at collecting and usingWe are worst at collecting and using

50 10

60 7

20 33

3 23

30 7

40 3

17 17

27 20

3 33

0 3

3 17

21 Economist Intelligence Unit 2009

Appendix 3Asia-Pacifi c survey results

Beyond transactionsBuilding a compelling retail experience

Putting recommendations into action

Persuading shoppers to share experiences, both positive and negative

Monitoring the results of actions in terms of shopper behaviour and marketing metrics

Synthesising information from retail outlets into coherent recommendations

Dealing systematically with extremely high volumes of information from stores

Demonstrating to shoppers that their comments are being addressed

Persuading store employees to share feedback from shoppers, both positive and negative

Distinguishing relevant from irrelevant shopper information

Synthesising information from customer service into coherent recommendations

Synthesising information from online channels intocoherent recommendations

Other

Don’t know

My organisation’s greatest challenges in using information from store management employees and shoppers to improve the customer experience are: Select up to three. (% respondents)

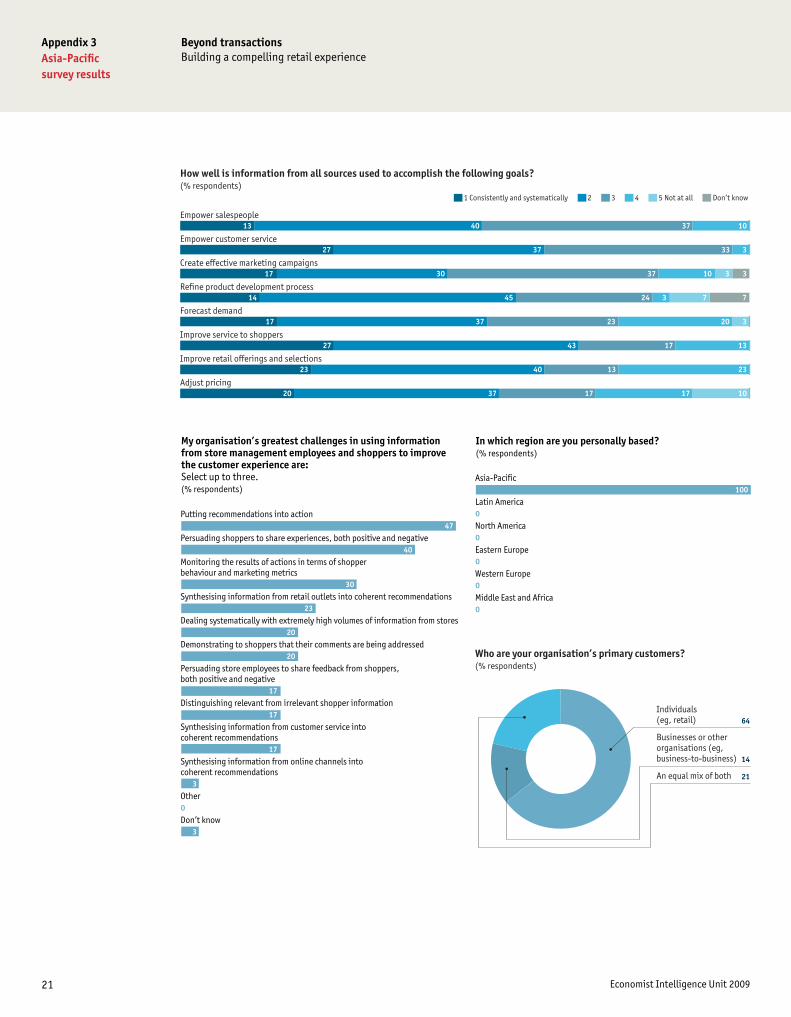

47

40

30

23

20

20

17

17

17

3

0

3

Asia-Pacific

Latin America

North America

Eastern Europe

Western Europe

Middle East and Africa

In which region are you personally based? (% respondents)

100

0

0

0

0

0

64

14

21

Individuals (eg, retail)

Businesses or other organisations (eg, business-to-business)

An equal mix of both

Who are your organisation’s primary customers?(% respondents)

1 Consistently and systematically 2 3 4 5 Not at all Don’t know

Empower salespeople

Empower customer service

Create effective marketing campaigns

Refine product development process

Forecast demand

Improve service to shoppers

Improve retail offerings and selections

Adjust pricing

How well is information from all sources used to accomplish the following goals?(% respondents)

13 40 37 10

27 37 33 3

17 30 37 10 3 3

14 45 24 3 7 7

17 37 23 20 3 0

27 43 17 13

23 40 13 23

20 37 17 17 10 0

22 Economist Intelligence Unit 2009

Appendix 3Asia-Pacifi c survey results

Beyond transactionsBuilding a compelling retail experience

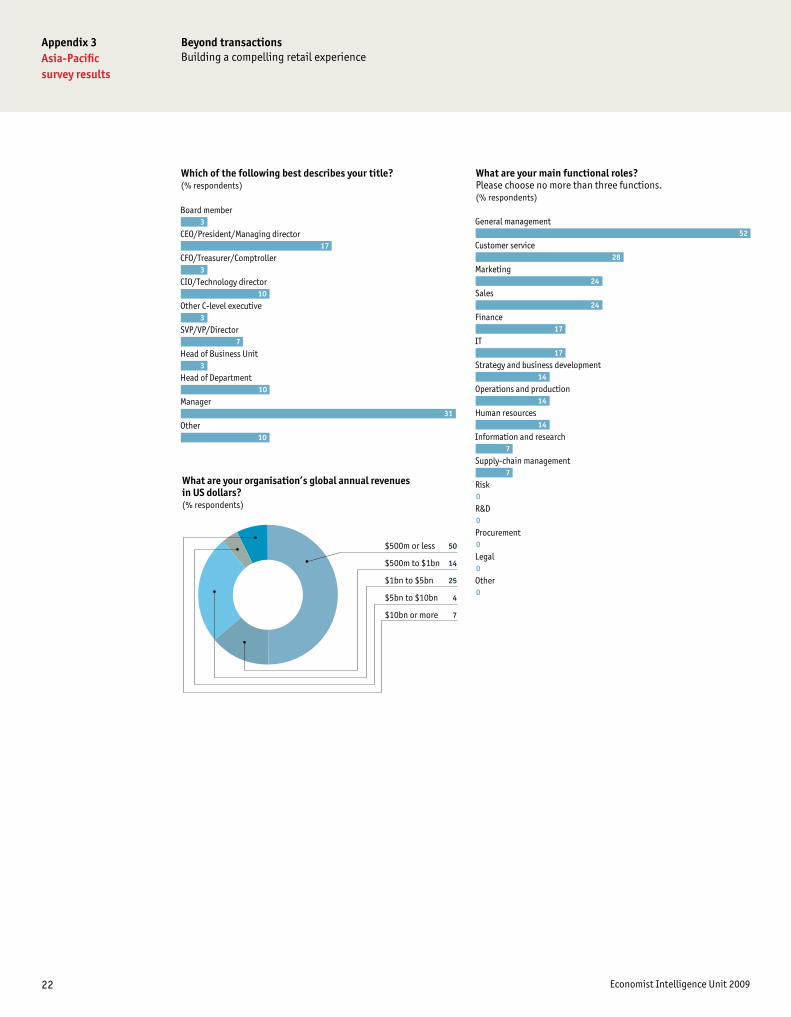

50

14

25

4

7

$500m or less

$500m to $1bn

$1bn to $5bn

$5bn to $10bn

$10bn or more

What are your organisation’s global annual revenues in US dollars? (% respondents)

General management

Customer service

Marketing

Sales

Finance

IT

Strategy and business development

Operations and production

Human resources

Information and research

Supply-chain management

Risk

R&D

Procurement

Legal

Other

What are your main functional roles? Please choose no more than three functions.(% respondents)

52

28

24

24

17

17

14

14

14

7

7

0

0

0

0

0

Board member

CEO/President/Managing director

CFO/Treasurer/Comptroller

CIO/Technology director

Other C-level executive

SVP/VP/Director

Head of Business Unit

Head of Department

Manager

Other

Which of the following best describes your title?(% respondents)

3

17

3

10

3

7

3

10

31

10

23 Economist Intelligence Unit 2009

Appendix 4EMEA survey results

Beyond transactionsBuilding a compelling retail experience

Appendix: Europe Middle East and Africa survey results

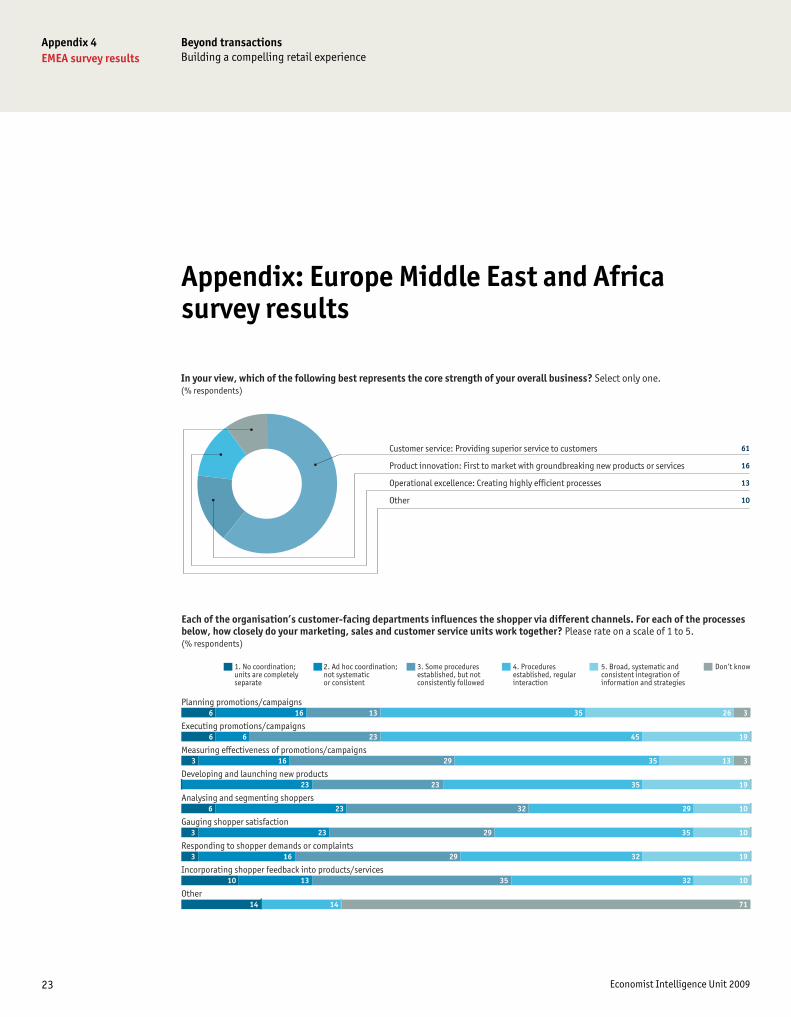

61

16

13

10

Customer service: Providing superior service to customers

Product innovation: First to market with groundbreaking new products or services

Operational excellence: Creating highly efficient processes

Other

In your view, which of the following best represents the core strength of your overall business? Select only one.(% respondents)

1. No coordination; 2. Ad hoc coordination; 3. Some procedures 4. Procedures 5. Broad, systematic and Don’t knowunits are completely not systematic established, but not established, regular consistent integration of separate or consistent consistently followed interaction information and strategies

Planning promotions/campaigns

Executing promotions/campaigns

Measuring effectiveness of promotions/campaigns

Developing and launching new products

Analysing and segmenting shoppers

Gauging shopper satisfaction

Responding to shopper demands or complaints

Incorporating shopper feedback into products/services

Other

Each of the organisation’s customer-facing departments influences the shopper via different channels. For each of the processes below, how closely do your marketing, sales and customer service units work together? Please rate on a scale of 1 to 5.(% respondents)

6 16 13 35 26 3

6 6 23 45 19 0

3 16 29 35 13 3

23 23 35 19 0

6 23 32 29 10 0

3 23 29 35 10 0

3 16 29 32 19 0

10 13 35 32 10 0

14 14 71

24 Economist Intelligence Unit 2009

Appendix 4EMEA survey results

Beyond transactionsBuilding a compelling retail experience

Segmenting and profiling shoppers

Targeting the right shoppers to achieve sales volume and revenue objectives

Cross-selling or upselling shoppers

Reducing the cost of sales

Maximising repeat purchases and building loyalty among shoppers

Measuring/optimising effectiveness of marketing and promotional campaigns

Gathering shopper intelligence in the course of providing service

Measuring the satisfaction of shoppers

Involving shoppers in product/service development (eg, co-creation)

Generating promotions/campaigns

Building long-term relationships with store management

Creating effective collateral

Ensuring that shopper complaints are resolved quickly

Other

Don’t know

In your view, which of your organisation’s activities are most in need of improvement? Select up to four. (% respondents)

48

45

42

39

32

26

26

23

19

16

13

6

6

0

0

Making each unit aware of how the others have interacted with a given shopper

Establishing common definitions, assumptions and data

Developing and sharing a detailed picture of shopper behavior and preferences

Prioritising resources directed towards shoppers by total value over the life of the relationship

Presenting shoppers with a consistent picture of the organisation

Helping each function find and act on ways to support the others

Measuring the probability that shoppers will turn into buyers, and using these scores to guide sales

Integrating tracking of shoppers from initial contact through to post-sales service

Our company sees no need to integrate our marketing, sales and service activities

Other

Don’t know/Not applicable

Which of the following would provide the biggest benefits in integrating your organisation’s marketing, sales and service activities? Select up to three. (% respondents)

35

32

32

29

26

26

26

23

6

0

3

Do you agree or disagree with the following statements?(% respondents)

In chosing to do business with my organisation, price is the single most important factor most shoppers consider

Compared to our competitors, my organisation’s shoppers are more loyal

My organisation has an accurate way to estimate the lifetime value of customers

My organisation prioritises sales and marketing resources based on each customer’s lifetime value

We are currently developing a social media strategy

My organisation has more flexibility than its competitors in pricing its products

Despite the recession, my organisation has greatly strengthened customer relationships over the past 12 months

We are more engaged in developing products or services collaboratively with customers than we were 12 months ago

Shoppers view my organisation’s products and services more as commodities now than five years ago

Our margins are higher than the margins of most of our competitors

If there is no difference in price, my organisation can win the sale based on service, convenience, brand reputation or other intangibles

Agree Disagree Don’t know

23 74 3

61 29 10

32 61 6

39 58 3

26 48 26

55 39 6

58 29 13

45 48 6

61 29 10

39 48 13

81 13 6

25 Economist Intelligence Unit 2009

Appendix 4EMEA survey results

Beyond transactionsBuilding a compelling retail experience

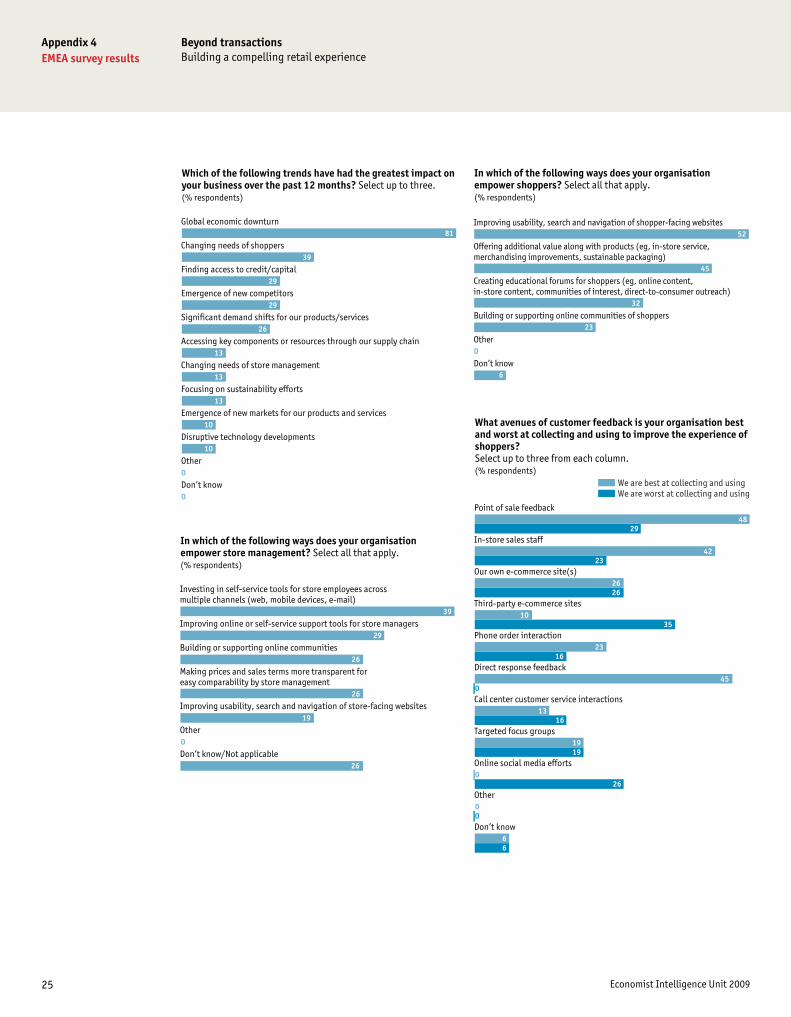

Global economic downturn

Changing needs of shoppers

Finding access to credit/capital

Emergence of new competitors

Significant demand shifts for our products/services

Accessing key components or resources through our supply chain

Changing needs of store management

Focusing on sustainability efforts

Emergence of new markets for our products and services

Disruptive technology developments

Other

Don’t know

Which of the following trends have had the greatest impact on your business over the past 12 months? Select up to three.(% respondents)

81

39

29

29

26

13

13

13

10

10

0

0

Investing in self-service tools for store employees across multiple channels (web, mobile devices, e-mail)

Improving online or self-service support tools for store managers

Building or supporting online communities

Making prices and sales terms more transparent for easy comparability by store management

Improving usability, search and navigation of store-facing websites

Other

Don’t know/Not applicable

In which of the following ways does your organisation empower store management? Select all that apply.(% respondents)

39

29

26

26

19

0

26

Improving usability, search and navigation of shopper-facing websites

Offering additional value along with products (eg, in-store service, merchandising improvements, sustainable packaging)

Creating educational forums for shoppers (eg, online content, in-store content, communities of interest, direct-to-consumer outreach)

Building or supporting online communities of shoppers

Other

Don’t know

In which of the following ways does your organisation empower shoppers? Select all that apply. (% respondents)

52

45

32

23

0

6

Point of sale feedback

In-store sales staff

Our own e-commerce site(s)

Third-party e-commerce sites

Phone order interaction

Direct response feedback

Call center customer service interactions

Targeted focus groups

Online social media efforts

Other

Don’t know

What avenues of customer feedback is your organisation best and worst at collecting and using to improve the experience of shoppers? Select up to three from each column.(% respondents)

We are best at collecting and usingWe are worst at collecting and using

48 29

42 23

26 26

10 35

23 16

450

13 16

19 19

0 26

00

6 6

26 Economist Intelligence Unit 2009

Appendix 4EMEA survey results

Beyond transactionsBuilding a compelling retail experience

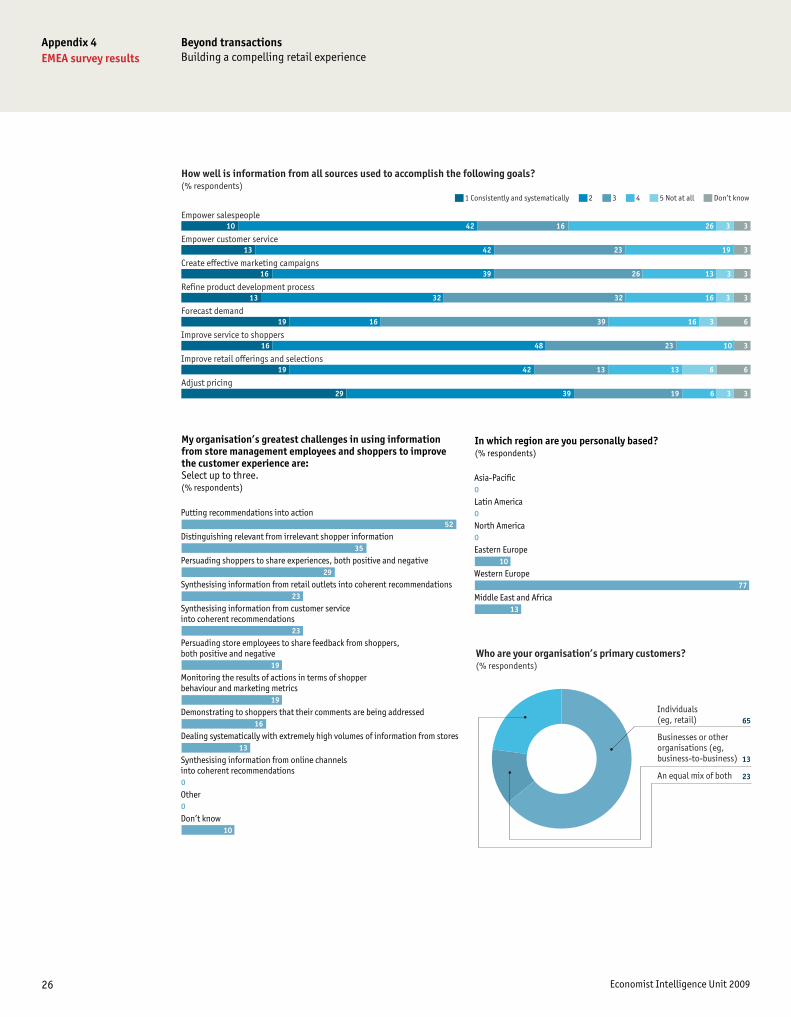

Putting recommendations into action

Distinguishing relevant from irrelevant shopper information

Persuading shoppers to share experiences, both positive and negative

Synthesising information from retail outlets into coherent recommendations

Synthesising information from customer service into coherent recommendations

Persuading store employees to share feedback from shoppers, both positive and negative

Monitoring the results of actions in terms of shopper behaviour and marketing metrics

Demonstrating to shoppers that their comments are being addressed

Dealing systematically with extremely high volumes of information from stores

Synthesising information from online channels into coherent recommendations

Other

Don’t know

My organisation’s greatest challenges in using information from store management employees and shoppers to improve the customer experience are: Select up to three. (% respondents)

52

35

29

23

23

19

19

16

13

0

0

10

Asia-Pacific

Latin America

North America

Eastern Europe

Western Europe

Middle East and Africa

In which region are you personally based? (% respondents)

0

0

0

10

77

13

65

13

23

Individuals (eg, retail)

Businesses or other organisations (eg, business-to-business)

An equal mix of both

Who are your organisation’s primary customers?(% respondents)

1 Consistently and systematically 2 3 4 5 Not at all Don’t know

Empower salespeople

Empower customer service

Create effective marketing campaigns

Refine product development process

Forecast demand

Improve service to shoppers

Improve retail offerings and selections

Adjust pricing

How well is information from all sources used to accomplish the following goals?(% respondents)

10 42 16 26 3 3

13 42 23 19 3

16 39 26 13 3 3

13 32 32 16 3 3

19 16 39 16 3 6

16 48 23 10 3

19 42 13 13 6 6

29 39 19 6 3 3

27 Economist Intelligence Unit 2009

Appendix 4EMEA survey results

Beyond transactionsBuilding a compelling retail experience

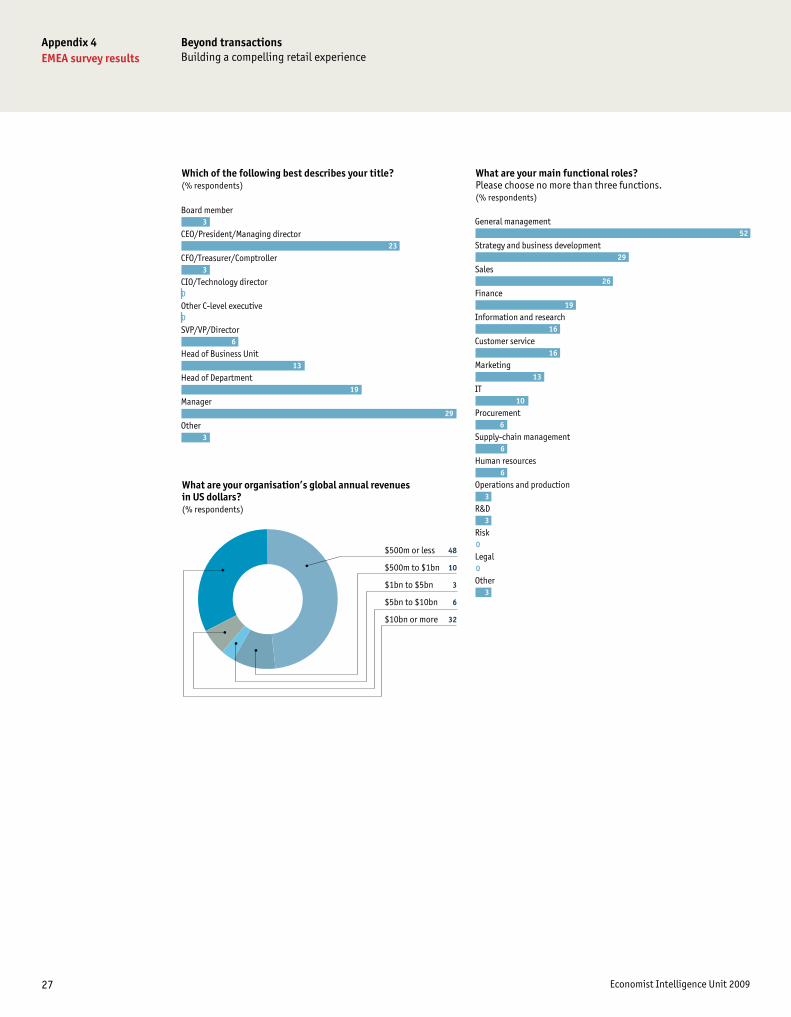

Board member

CEO/President/Managing director

CFO/Treasurer/Comptroller

CIO/Technology director

Other C-level executive

SVP/VP/Director

Head of Business Unit

Head of Department

Manager

Other

Which of the following best describes your title?(% respondents)

3

23

3

0

0

6

13

19

29

3

48

10

3

6

32

$500m or less

$500m to $1bn

$1bn to $5bn

$5bn to $10bn

$10bn or more

What are your organisation’s global annual revenues in US dollars? (% respondents)

General management

Strategy and business development

Sales

Finance

Information and research

Customer service

Marketing

IT

Procurement

Supply-chain management

Human resources

Operations and production

R&D

Risk

Legal

Other

What are your main functional roles? Please choose no more than three functions.(% respondents)

52

29

26

19

16

16

13

10

6

6

6

3

3

0

0

3

28

Whilst every effort has been taken to verify the accuracy of this information, neither The Economist Intelligence Unit Ltd. nor the sponsors of this report can accept any responsibility or liability for reliance by any person on this white paper or any of the information, opinions or conclusions set out in the white paper. Co

ver i

mag

e: S

hutt

erst

ock

LONDON26 Red Lion SquareLondon WC1R 4HQUnited KingdomTel: (44.20) 7576 8000Fax: (44.20) 7576 8476E-mail: [email protected]

NEW YORK111 West 57th StreetNew York NY 10019United StatesTel: (1.212) 554 0600Fax: (1.212) 586 1181/2E-mail: [email protected]

HONG KONG6001, Central Plaza18 Harbour RoadWanchai Hong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]