beyond group lending p.v. viswanath. learning goals what are some problems with group lending? ...

TRANSCRIPT

BEYOND GROUP LENDING

P.V. Viswanath

Learning Goals

What are some problems with group lending? What can a model of individual loans with costly

debt collection tell us? Can progressive lending be used to resolve some of

the problems with individual lending? What is the role of hard and soft collateral? Why do many microlenders require public

repayments? What is the impact of competition? Is it good or

bad? Why do microlenders require very frequent payment

installments?

Problems with Group Lending

The essence of group lending is that it’s a way to transfer onto customers the responsibility for jobs usually undertaken by lenders – screening potential customers, monitoring their efforts and enforcing contracts. However, this has its costs. Need to find other borrowers in order to be eligible for a

loan Attending meetings can be costly, both in terms of time

and money, particularly in sparsely populated areas. Borrowers have to bear the risk of other borrowers’

default Further, in sparsely populated areas and urban areas,

borrowers might not have good information on each other

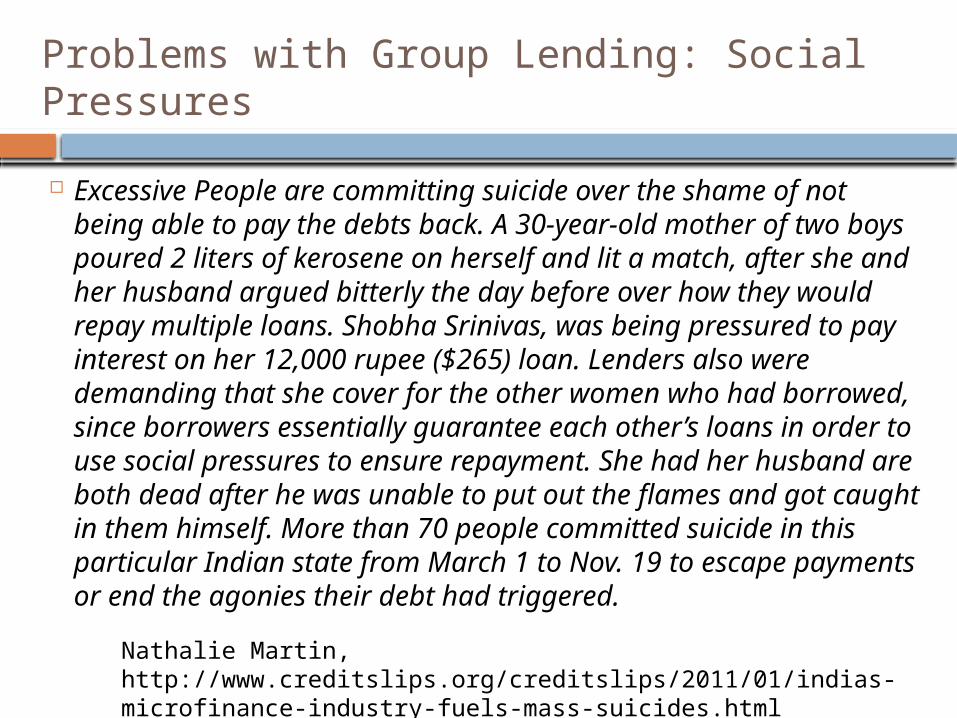

Problems with Group Lending: Social Pressures

Excessive People are committing suicide over the shame of not being able to pay the debts back. A 30-year-old mother of two boys poured 2 liters of kerosene on herself and lit a match, after she and her husband argued bitterly the day before over how they would repay multiple loans. Shobha Srinivas, was being pressured to pay interest on her 12,000 rupee ($265) loan. Lenders also were demanding that she cover for the other women who had borrowed, since borrowers essentially guarantee each other’s loans in order to use social pressures to ensure repayment. She had her husband are both dead after he was unable to put out the flames and got caught in them himself. More than 70 people committed suicide in this particular Indian state from March 1 to Nov. 19 to escape payments or end the agonies their debt had triggered.

Nathalie Martin, http://www.creditslips.org/creditslips/2011/01/indias-microfinance-industry-fuels-mass-suicides.html

Problems with Group Lending: Flexibility

Lack of flexibility – what happens if a borrower through no fault of her own has liquidity problems?

Grameen USA has not experience this problem, yet, but Sandy was a test case. Surprisingly, there were no defaults or delinquencies because of Hurricane Sandy.

This is not only a problem in equity, but also one of efficiency.

In the corporate world, this is taken care of through restructuring. The US Bankruptcy code is essentially a debtor-friendly system, for this very reason.

Grameen II has a basic loan with weekly repayments, but also a Flexible Loan with easier terms spread over a longer period; this is a sort of workout procedure.

Problems with Delegation of Control

There can be collusion between borrowers, undermining the whole rationale for groups.

From Hussan-Bano Burki, “Unraveling the Delinquency Problem in Punjab-Pakistan.

Group leaders and activists get an opportunity to turn into commission agents primarily because the MF staff, lending through solidarity groups, tend to delegate significant portion of their client selection responsibility to group leaders or activists. Having a de facto power to accept or reject a potential borrower in a group, the group leader has the power to provide or refuse access to financial services to potential clients. This power allows group leaders to charge commission from borrowers for access into a group.

… …often, the group leader had accessed more loans from an [MFI] than

the [MFI] had record of by borrowing through a “dummy” or “ghost” borrower. In some cases the group leader and the “ghost” borrower had subdivided the loan amount and thus the repayment responsibility as well.

Solutions to group lending problems

Progressive Lending –promising larger and larger loans for groups and individuals in good standing.

Repayment Schedules with weekly or monthly installments (as opposed to daily payments in earlier group lending contracts).

Public repayments – e.g. the use of shaming (this has its own problems)

The targeting of women (is this a solution or refusal to address a problem?)

Weakening or eliminating of joint liability.

Group loans versus individual loans Relative to group-lenders, individual loan lenders

are slightly more self-reliant as proxied by the percentage of their financial costs covered and

Charge lower interest rates and fees Does this mean that individual lending is better? However, individual lenders

Serve better-off clients, as reflected by average loan size

Serve a smaller population of women So it is still important to look at whether and how

individual lending can be used to solve group lending problems in target populations.

Progressive Lending

Microlenders can give incentives to borrowers by threatening to exclude defaulting borrowers from future access to loans.

Ever-larger loans to good customers can turn startup businesses into steady enterprises.

This can only work if the microlender is the sole source of fund.

In a study by Aleem (1990), moneylenders elicited loan repayments by Developing repeated relationships with borrowers Making sure that existing borrowers do not contract new

loans.

The economics of non-financing threats

Assume that there are two periods of production and that an investment project requires $1.

At the end of each period, the borrower can generate a gross return y > $1, calculated before repayment of the loan with interest, provided that her current project is financed by the bank.

At the repayment stage, the borrower may decide to default strategically by not repaying the loan.

In order to deter the borrower from doing this, the bank can extend a second period loan contingent upon full repayment of the first-period obligations.

The borrower’s penalty for defaulting after the first period is that she will not be able to invest in the second period.

The model: details

Suppose the borrower defaults on the first period loan. The expected payoff will be y + dvy, where d is the discount factor, and v is the probability of being refinanced by the bank despite having defaulted.

The reason v is not automatically zero is that the borrower may be able to get funding from another bank, which leads to a greater likelihood of default. This is possible if there are no credit bureaus.

Assume further that the borrower needs the bank to go ahead with the second project even if she pockets the proceeds of the first period realization. (This doesn’t make sense because if each project requires an investment of $1, the proceeds from the first investment should be sufficient to fund the second project – but we will see later how progressive lending can resolve this issue.)

If the borrower decides to repay the first period loan, her payoff is y – R + dy, where R is the gross interest rate. For simplicity, assume that in the second period, there will be no repayment.

The borrower’s problem

Of course, in a finite-period game, it makes sense to default in the second period. However, in reality, the borrower might become large enough that it would make sense for the borrower to invoke the legal system. Alternatively, banks might not provide her with a loan with defaults in her background. (Of course, this is another way of saying that the game is really an infinite one.)

Clearly, the borrower will repay in period 1 if y + dvy < y – R + dy. This requires that R < dy (1-v). Note, here, that R is decreasing in v; i.e. the greater the chance that the borrower will have access to the bank after default, the lower the interest rate that the lender can charge to forestall default. Hence in equilibrium, the bank will want to set v=0, i.e. the incentive compatible condition is R < dy.

Costly Collection and Microlending Failures

We have interpreted d as the discount factor accounting for the borrower’s time preference. However, if we simply interpret dy as the value at time 1 of the expected time 2 payoff from a second project, d could also incorporate the likelihood of the band having sufficient funds to lend to the entrepreneur in the second period.

So since R is decreasing in d, we see that the interest rate that the bank can charge and still have the borrower repay is even lower if borrowers believe that the bank will not be able to make future loans. This shows why it is important for the bank to maintain an impression of stability.

In any case, if R must be less than dy to elicit repayment, the bank cannot break even! So what can it do?

Progressive Lending

One answer is progressive lending. If successive loans are larger, then clearly, interest rates

can be higher because servicing costs are lower for larger loans. Assume, for now, that the cost of capital per dollar of loan is constant.

Now, suppose the bank increases the size of its loans by a factor l . Assume, however, that we have constant returns to scale.

Now, by not repaying, the borrower suffers a loss of l dy, which is larger than dy. The restriction, now, is y + dl vy < y – R + dl y, i.e. R < l dy(1-v) or with v=0, R < l dy. Hence interest rates can be raised, relative to the constant loan size case. Let the interest rate, in this case, be R’ > R.

How Progressive Lending Helps Earlier, we assumed that the borrower could not invest in period 2 if

she defaulted on the first loan. However, if she defaults, she would have access to the returns from the first loan! So let us assume that the borrower can keep part of the principal from the first period even in case of default. Suppose f percent of the proceeds can be reinvested in the second period. Assume, once more, that v=0.

In this case, if the loan is repaid, the return for the borrower is y-R’ + l dy. If she does not repay, then the payoff is y(1- f) + fdy2. When f = 0, the payoff is simply y because the borrower can invest nothing in the second period; now if f > 0, the borrower gets to keep y(1- f) from the first period returns, and invest fy instead of 0. The return, therefore on this investment in period 2, will be (fy)y or fy2. After discounting this amount, we get y(1- f) + fdy2. Hence, there will be no default if y-R’ + l dy > y(1- f) + fdy2. Simplifying, we get R’ < l dy + (1-dy)fy, which is smaller than the previous R’, as we would expect, as long as dy >1. That is, having f > 0, is not helpful to the bank.

Note at this point, that R’ is increasing in l . Furthermore, R’ is decreasing in f, under the same assumption.

The eventual need for collateral Let’s look again at the condition as to when the borrower would

not default: y-R’ + l dy > y(1- f) + fdy2. Suppose now, that in case of default, the borrower would hold back f = R’/y; i.e. the amount fy that she reinvests is exactly equal to R’, the amount that she would have had to repay to the bank. In this case, substituting for in the inequality above, we get y-R’ + ldy > y(1- R’/y) + (R’/y) dy2. Cancelling, we get the condition l > R’.

That is, if we can assume that the defaulter will act in a reasonable manner to use the defaulted funds, default can be forestalled by ensuring that the factor of increase of funds is greater than the interest rate. This makes sense, because then the borrower gets a net influx of funds.

The only issue is whether it makes sense for the bank to make such loans, since there’s going to be default at some point. This makes sense if at some point, there will be collateral that will make it not worthwhile for the borrower to default.

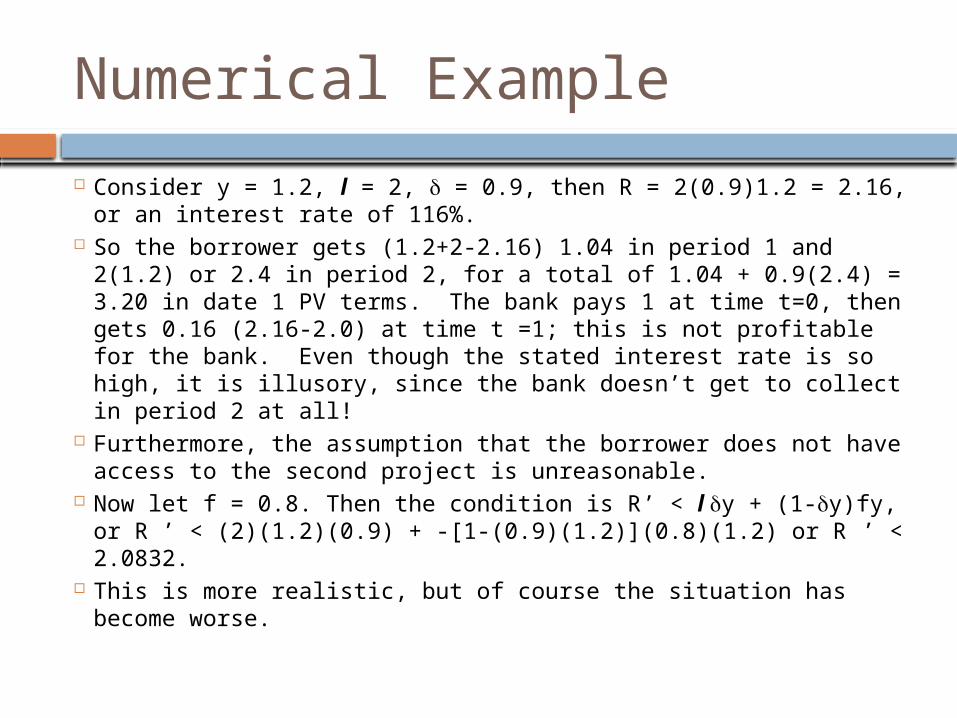

Numerical Example

Consider y = 1.2, l = 2, d = 0.9, then R = 2(0.9)1.2 = 2.16, or an interest rate of 116%.

So the borrower gets (1.2+2-2.16) 1.04 in period 1 and 2(1.2) or 2.4 in period 2, for a total of 1.04 + 0.9(2.4) = 3.20 in date 1 PV terms. The bank pays 1 at time t=0, then gets 0.16 (2.16-2.0) at time t =1; this is not profitable for the bank. Even though the stated interest rate is so high, it is illusory, since the bank doesn’t get to collect in period 2 at all!

Furthermore, the assumption that the borrower does not have access to the second project is unreasonable.

Now let f = 0.8. Then the condition is R’ < l dy + (1-dy)fy, or R ’ < (2)(1.2)(0.9) + -[1-(0.9)(1.2)](0.8)(1.2) or R ’ < 2.0832.

This is more realistic, but of course the situation has become worse.

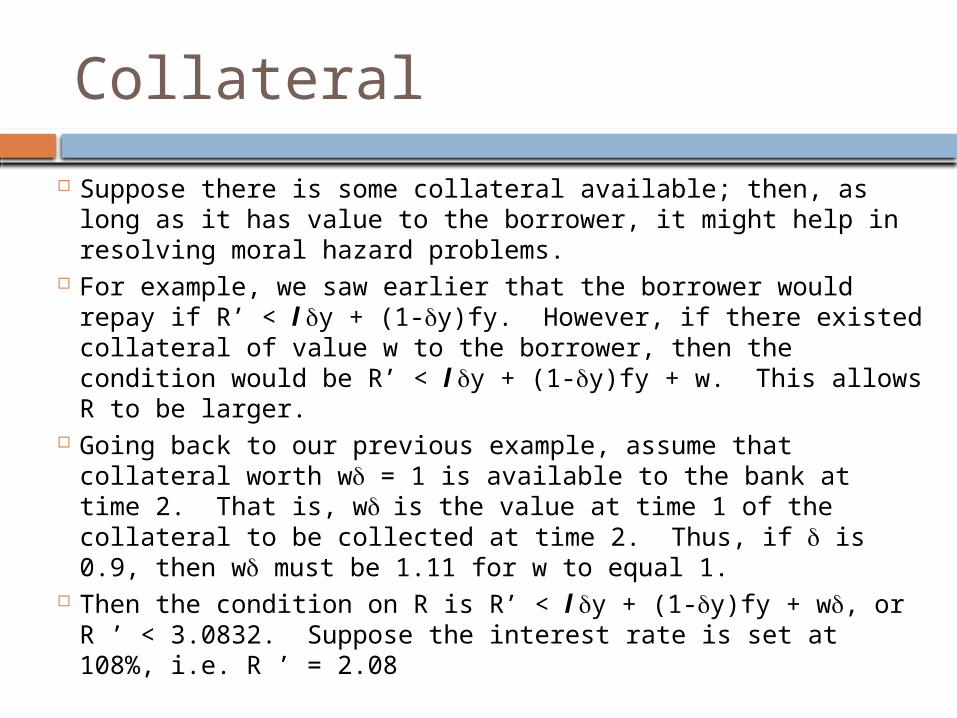

Collateral

Suppose there is some collateral available; then, as long as it has value to the borrower, it might help in resolving moral hazard problems.

For example, we saw earlier that the borrower would repay if R’ < l dy + (1-dy)fy. However, if there existed collateral of value w to the borrower, then the condition would be R’ < l dy + (1-dy)fy + w. This allows R to be larger.

Going back to our previous example, assume that collateral worth wd = 1 is available to the bank at time 2. That is, w d is the value at time 1 of the collateral to be collected at time 2. Thus, if d is 0.9, then wd must be 1.11 for w to equal 1.

Then the condition on R is R’ < l dy + (1-dy)fy + wd, or R ’ < 3.0832. Suppose the interest rate is set at 108%, i.e. R ’ = 2.08

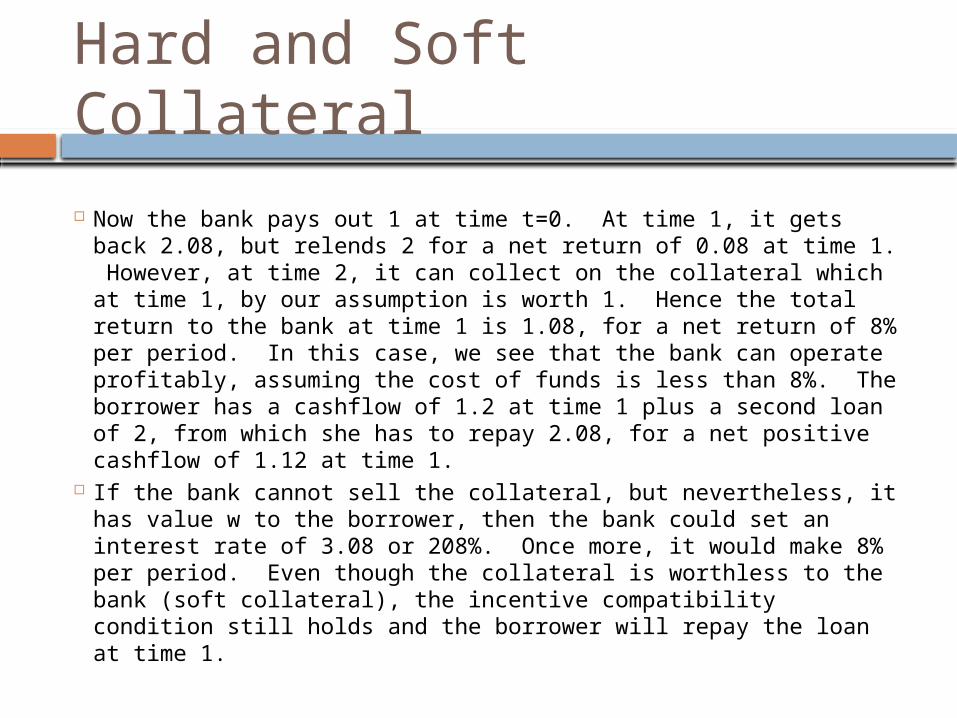

Hard and Soft Collateral

Now the bank pays out 1 at time t=0. At time 1, it gets back 2.08, but relends 2 for a net return of 0.08 at time 1. However, at time 2, it can collect on the collateral which at time 1, by our assumption is worth 1. Hence the total return to the bank at time 1 is 1.08, for a net return of 8% per period. In this case, we see that the bank can operate profitably, assuming the cost of funds is less than 8%. The borrower has a cashflow of 1.2 at time 1 plus a second loan of 2, from which she has to repay 2.08, for a net positive cashflow of 1.12 at time 1.

If the bank cannot sell the collateral, but nevertheless, it has value w to the borrower, then the bank could set an interest rate of 3.08 or 208%. Once more, it would make 8% per period. Even though the collateral is worthless to the bank (soft collateral), the incentive compatibility condition still holds and the borrower will repay the loan at time 1.

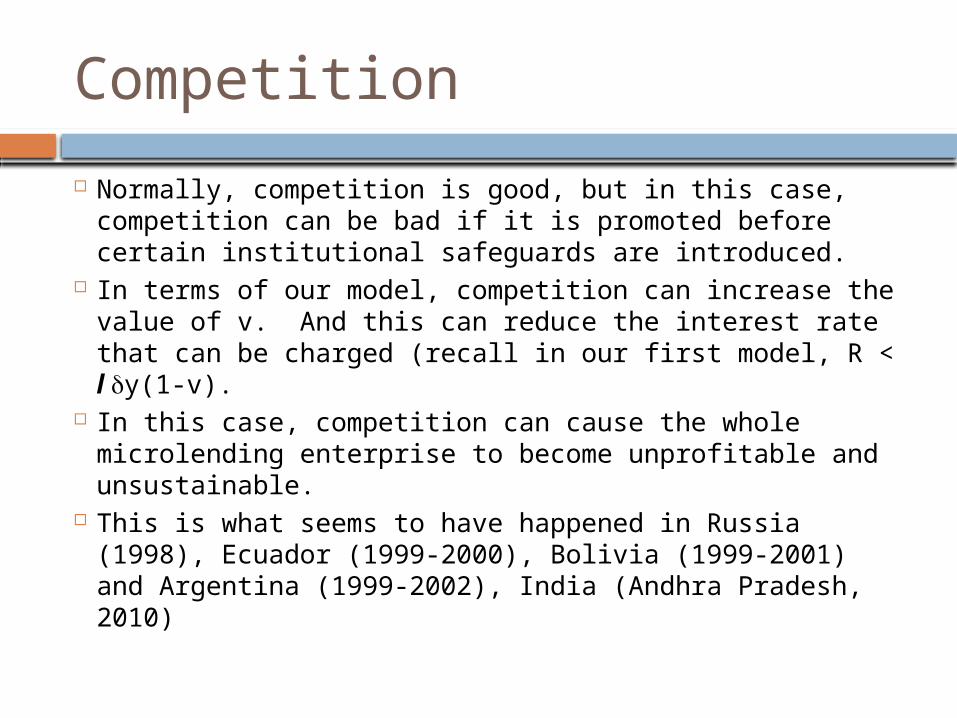

Competition

Normally, competition is good, but in this case, competition can be bad if it is promoted before certain institutional safeguards are introduced.

In terms of our model, competition can increase the value of v. And this can reduce the interest rate that can be charged (recall in our first model, R < l dy(1-v).

In this case, competition can cause the whole microlending enterprise to become unprofitable and unsustainable.

This is what seems to have happened in Russia (1998), Ecuador (1999-2000), Bolivia (1999-2001) and Argentina (1999-2002), India (Andhra Pradesh, 2010)

Competition and Efficiency

Vogelgesang (2003, World Development 31: 2085-2114) looked at competition and loan repayment performance for Caja Los Andes. He found that competition is related with multiple loan taking and higher levels of borrower indebtedness. Although higher levels of borrowing does lead to higher default, still, the probability of timely repayment is high in areas where there is high competition and high supply of microfinance services.

A recent study looked at data from 362 MFIs in 73 countries for the period 1995-2009. They found that intense competition is, overall, negatively associated with performance of MFIs.

“As a number of competing MFIs increase in a market, which makes information sharing between them challenging, borrowers may engage in multiple borrowing which increases the debt level of clients and the probability of default. This in turn can make worse off borrowers with a single lender since this behaviour will create an externality by inciting MFIs to respond to multiple borrowing by adjusting interest rates upward.”

Esubalew Assefa, Niels Hermes and Aljar Meesters, “Competition and Performance of Microfinance Institutions,” 2010

Solutions to problems from competition

Designing ways that makes sure MFIs do not compromise lower lending standards for increased market share.

Credit Bureaus: Designing ways that promote information sharing between MFIs, so that a borrower that defaults on one MFI loan could not turn to another MFI in the neighborhood and be granted a loan

Promoting financial literacy among clients may help them in their borrowing decisions, which in turn may limit multiple loan-taking.

Frequent Repayment Installments

Repayments in microfinance usually start immediately after the loan is disbursed.

Even though there is a mismatch between the repayment frequency and the borrower’s cashflow, there are some advantages: It provides an early warning system of potential default. It helps the lender select less risky clients – the only way to make

payments even before the business starts paying off is if the borrower has access to other sources of capital

Reduces incentives for borrowers to use cashflows for other non-productive purposes, in the absence of savings facilities

Regular repayments are difficult to impose in areas with highly seasonal occupations, such as agriculture. Everybody (not just the borrower) is exposed to this schedule of cashflows; there is nobody to borrow from, in order to make initial payments.

Making Payments Public

Social stigma can be used as an inducement to repay.

Meeting a cluster of borrowers simultaneously can reduce collection costs.

Group meetings can facilitate financial education

Group meetings can elicit information about errant borrowers.

On the other hand, this may increase tension among individual borrowers or create incentives to collude.

Questions

Is there a difference between Bangladesh and New York?

Between New York and Omaha? What are the specific features of

Grameen USA microfinance loans that reduce the problems of individual lending?