*battelle - pacific northwest national laboratory · battelle memorial institute for the united...

TRANSCRIPT

PNNL-12115

ADOPTING A LONG VIEW TO ENERGY R&DAND GLOBAL CLIMATE CHANGE

JJ Dooley and PJ Runci

February 1999

Prepared forU.S. Department of Energyunder Contract DE-AC06-76RL0 1830

Pacific Northwest National LaboratoryOperated for the U.S. Department of Energyby Battelle Memorial Institute

*Battelle

DISCLAIMER

This report was prepared as an account of work sponsored by an agency of the United States

Government. Neither the United States Government nor any agency thereof, nor BattelleMemorial Institute, nor any of their employees, makes any warranty, express or implied, orassumes any legal liability or responsibility for the accuracy, completeness, or usefulness ofany information, apparatus, product, or process disclosed, or represents that its use wouldnot infringe privately owned rights. Reference herein to any specific commercial product,process, or service by trade name, trademark, manufacturer, or otherwise does not necessarilyconstitute or imply its endorsement, recommendation, or favoring by the United StatesGovernment or any agency thereof, or Battelle Memorial Institute. The views and opinions ofauthors expressed herein do not necessarily state or reflect those of the United States Governmentor any agency thereof.

PACIFIC NORTHWEST NATIONAL LABORATORY

operated byBATTELLE MEMORIAL INSTITUTE

for theUNITED STATES DEPARTMENT OF ENERGY

under Contract DE-AC06- 76RL0 1830

DISCLAIMER

Portions of this document may be illegiblein electronic image products. Images areproduced from the best available originaldocument.

t

ABSTRACT: In this paper, we present findings indicative of important, ongoing changes in theenergy research and development (R&D) investment portfolios of major OECD nations. We seekto explain the drivers of these changes and discuss their implications for the world’s ability todeal with future R&D-intensive energy challenges, such as global climate change. We alsoconsider possible implications of changes in individual countries’ energy R&D portfolios forinternational energy R&D collaboration among OECD countries themselves, and between OECDand developing countries. We conclude that the level of investment in energy R&D in the OECDis likely insufficient to meet the energy R&D challenges of climate change. A long-term,strategic approach would aim to broaden both the amount of resources devoted to energy R&Dand the geographical scope of the global energy R&D infrastructure. A successful strategy willaccount for large-scale changes in demographics and energy use over the coming decades willdrive the development of indigenous energy R&D capabilities in developing countries.

KEY WORDS: Energy R&D, Global Climate Change, Energy Technologies.

For well over a decade, the world has enjoyed a period of cheap and abundant energy supplies.Since the oil shocks of the 1970s, a combination of factors, including technological advances,discoveries of new petroleum resources, improved energy productivity, and the creation of i%turesmarkets, has alleviated fears that the energy i%ture would necessarily be characterized by scarcityand high prices. The 1990-91 Persian Gulf War, which caused only a brief price spike oninternational energy markets, ultimately bolstered optimism concerning the world’s improvedadeptness at managing energy crises.

Amid the general energy optimism that has persisted since the mid- 1980s, governmentinvestments in energy research and development (R&D) have declined in many advancedindustrial countries. To a great extent, the reduction in government commitments to energy R&Dreflects the perception that energy has become a matter of lesser urgency, relative to other socialpriorities.

At the same time, an ideological shifl in the industrialized countries toward the deregulation ofkey industries, such as electric and gas utilities, has placed additional pressures on R&Dinvestments. With the introduction of competitive forces in the energy industries and theelimination of guaranteed returns, firms’ (in particular, electric and gas utilities’) R&Dinvestments have grown smaller. Remaining R&D resources gravitate more often to lower risk,market-oriented projects than to riskier projects with more distant payoffs!

Yet, while public and private sector energy R&D investments have declined, a major new energychallenge has appeared on the horizon that will demand significant and sustained commitments tothe development of new energy technologies. The long-term challenge of global climate change,and actions aimed at its mitigation, will require a transition to fuels and energy technologies thatemit less carbon dioxide and other greenhouse gases—substances whose rising concentrations inthe atmosphere are thought to be major contributors to global warming and related climaticchanges.2 In the shorter-term, the costs associated with the reduction of greenhouse gasemissions will depend critically on the technologies that become available for deployment in thefirst decades of the next century. The estimated costs of greenhouse gas reduction span manyorders of magnitude, with some scenarios showing costs approaching zero, assuming widelyavailable and widely deployed advanced energy technologies.3 The challenge is made greaterstill by projections that global energy use is expected to grow by 75°/0 by 2020 and that most ofthe new demand will be met with fossil fuels.

In December 1997, official delegations from over 150 countries met in Kyoto, Japan, where manyparticipating countries also signed an international treaty aimed at reducing global emissions ofcarbon dioxide. Under the Kyoto Protocol, the major industrialized countries agreed to reducetheir carbon emissions by 6-8?40from their 1990 levels within the period 2008-2012. Yet theKyoto Protocol has not been ratified by any major signatories and its prospects, in the UnitedStates especially, are dim. While governments of industrialized countries now view the climatechange issue with increasing seriousness, there is still insufficient urgency surrounding theproblem to precipitate major political action and new government commitments to energy R&D.

] JJ Dooley, “Unintended Consequences: Energy R&D in a Deregulated Market,” Energy PoIicy (June1998).1 See Intergovernmental Panel on Climate Change, IPCC Second Assessment: C[imate Change 1995, p 13.3JA Edmonds, JJ Dooley, and MA Wise, “Atmospheric Stabilization: The Role of Energy Technology,” inClimate Change PoIicy, Risk Prioritization, and US Economic Growth ( Washington, DC: AmericanCouncil for Capital Formation, June 1997).

Global Climate Change and Energy Technology: The Long View

In addition to the political and economic aspects of the Kyoto Protocol that have hindered itsadoption, questions concerning the agreement’s effectiveness in combatting climate change alsoloom large in the minds of politicians and scientists. Such questions arise from the fact that theclimate change problem is unfolding on a century-scale, yet the mitigative actions encompassedby the Kyoto Protocol are often viewed as a “quick fix” to be implemented over the short span ofthe coming decade. The short implementation schedule of the Kyoto Protocol essentially dictatesthat the world address climate change with those technologies currently available. Consequently,poor results could be purchased at high cost.

A more favorable, alternative approach to climate change would consider that continued advancesin the state of the art of energy technology, which are in large part a function of energy R&Dinvestment levels, will expand the problem’s solution set. Thus, the state of energy R&D willalso determine to a large extent the cost of attaining any stabilized “safe” atmosphericconcentration of greenhouse gases over the coming century.4 Based on this logic, sustainedenergy R&D investment must be viewed as a vital component of a century scale strategydesigned both to address the problem effectively and to minimize associated costs. Consideringalso that the majority of growth in world energy consumption expected in the next century willoccur in the developing world, an effective strategy must include provisions ensuring theparticipation of key developing states. Countries such as China, India, and Brazil should beencouraged and assisted to become future producers of energy R&D and energy technologies andought not be expected to remain contented consumers of Western expertise and hardwarethroughout the next century.

Moreover, the motivation for major developing countries to develop indigenous energy R&Dinfrastructures extends beyond climate change. Local environmental conditions, particularly airquality, is already a severe problem in many industrializing areas. The impetus for thedeployment of newer and cleaner energy technologies will also grow as the levels of industrialactivity and energy demand rise in developing countries.

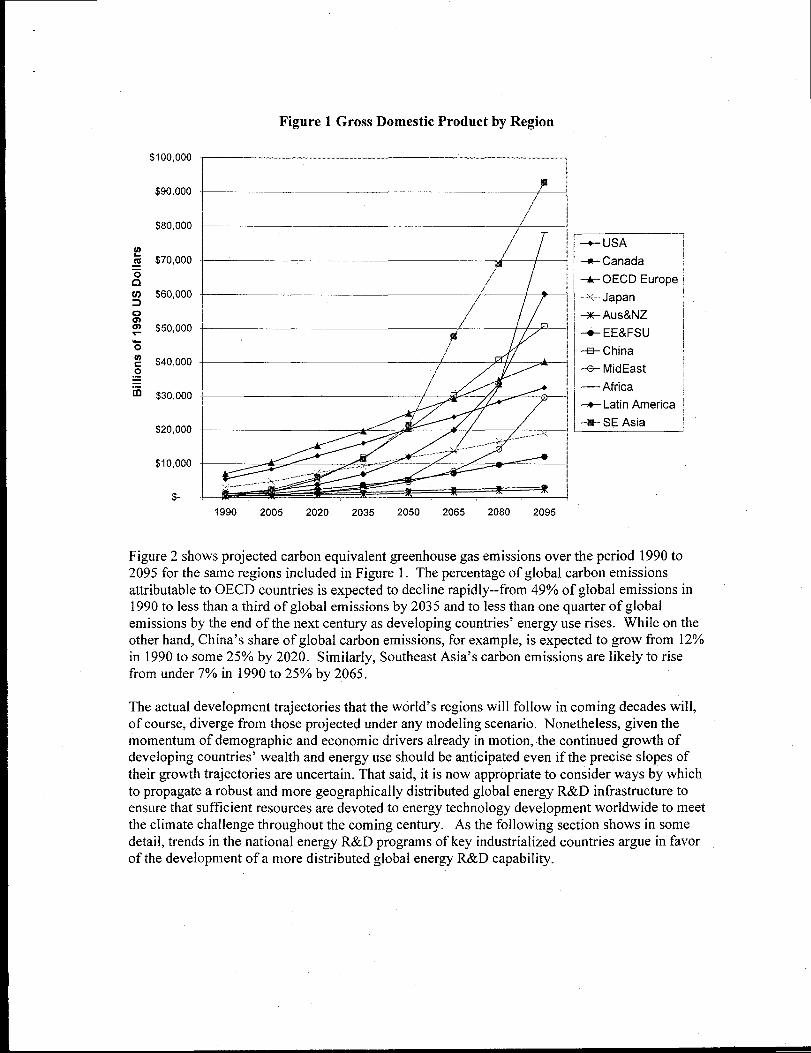

To understand the increasingly significant role of developing countries in strategies to addressclimate change, it is useful to consider some anticipated global energy and economic trends.Figure 1 shows regional projections of gross domestic product (GDP) for the period 1990-2095?Most recent data show, for example, that China’s economy is now less than half the size of theUnited States’ economy. Yet if China’s economic growth persist at its current rate, it will likelybecome one of the world’s largest economies towards the middle of the next century. By themiddle of the century, China might also be significantly wealthier when measured in terms ofGDP per capita. These figures also show that several other countries currently regarded as“developing,” and that currently lack an advanced and extensive technology R&D infrastructure,are likely to experience significant growth in wealth during the next century.

4 It is important to note that the Framework Convention on Climate Change is silent on what would be a“safe” atmospheric concentration for greenhouse gases and that these levels remain a subject of debate.The lower the “safe concentration” is judged to be the more difficult the challenge of climate changebecomes and the more critical advances in energy R&D will become.5 These data were generated from the “B2F” non-intervention scenario generated m a part of theIntergovernmental Panel on Climate Change, Working Group III’s forthcoming Special Report onEmissions Scenarios (SRES). B2F is a conservative growth scenario over the course of the next century.

$100,000

$90,000

$80,000

g $70,000

~()) $60,00030m: $50,000%g $40,000.-=“h $30,()()(3

$20,000

$10,000

$-

Figure 1 Gross Domestic Product by Region

/ //.$

/’/,/

/ - USA~_ ~ana~a

--k OECD Europe,.+<...J~p~n

I + Aus&NZ

~+ EE&FSU

I --5 China

~-e- MidEast

— Africa

+ Latin America

-w- SE Asia

1990 2005 2020 2035 2050 2065 2080 2095

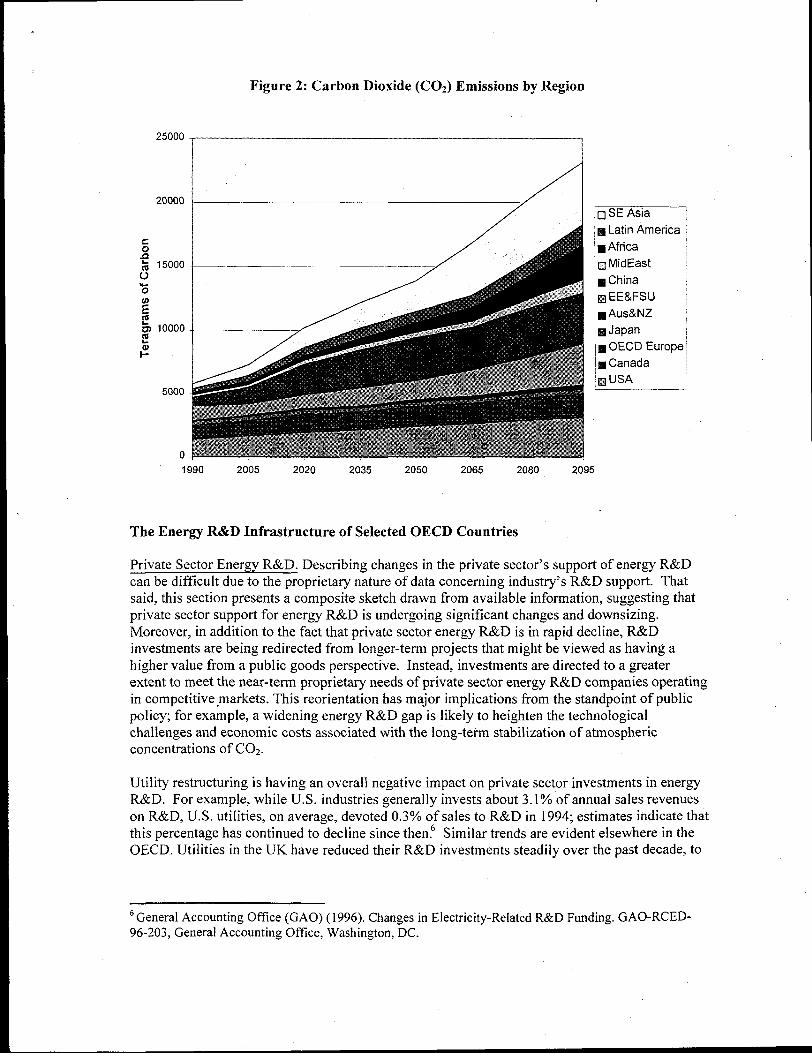

Figure 2 shows projected carbon equivalent greenhouse gas emissions over the period 1990 to2095 for the same regions included in Figure 1. The percentage of global carbon emissionsattributable to OECD countries is expected to decline rapidly--from 49°/0 of global emissions in1990 to less than a third of global emissions by 2035 and to less than one quarter of globalemissions by the end of the next century as developing countries’ energy use rises. While on theother hand, China’s share of global carbon emissions, for example, is expected to grow from 12°/0in 1990 to some 25°/0 by 2020. Similarly, Southeast Asia’s carbon emissions are likely to risefrom under 7% in 1990 to 25% by 2065.

The actual development trajectories that the world’s regions will follow in coming decades will,of course, diverge from those projected under any modeling scenario. Nonetheless, given themomentum of demographic and economic drivers already in motion, the continued growth ofdeveloping countries’ wealth and energy use should be anticipated even if the precise slopes oftheir growth trajectories are uncertain. That said, it is now appropriate to consider ways by whichto propagate a robust and more geographically distributed global energy R&D infrastructure toensure that sufficient resources are devoted to energy technology development worldwide to meetthe climate challenge throughout the coming century. As the following section shows in somedetail, trends in the national energy R&D programs of key industrialized countries argue in favorof the development of a more distributed global energy R&D capability.

Figure 2: Carbon Dioxide (C02) Emissions by Region

25000

20000

%

o

——- — 4❑ SE Asia

H Latin America

■ Africa

❑ MidEast

❑ China

❑ EE&FSU \

■ Aus&NZ ,H Japan ~

❑ OECD Europe \

H Canada :

H USA

1990 2005 2020 2035 2050 2065 2080 2095

The Energy R&D Infrastructure of Selected OECD Countries

Private Sector Energ y R&D. Describing changes in the private sector’s support of energy R&Dcan be difficult due to the proprietary nature of data concerning industry’s R&D support. Thatsaid, this section presents a composite sketch drawn from available information, suggesting thatprivate sector support for energy R&D is undergoing significant changes and downsizing.Moreover, in addition to the fact that private sector energy R&D is in rapid decline, R&Dinvestments are being redirected from longer-term projects that might be viewed as having ahigher value from a public goods perspective. Instead, investments are directed to a greaterextent to meet the near-term proprietary needs of private sector energy R&D companies operatingin competitive ,markets. This reorientation has major implications from the standpoint of publicpolicy; for example, a widening energy R&D gap is likely to heighten the technologicalchallenges and economic costs associated with the long-term stabilization of atmosphericconcentrations of C02.

Utility restructuring is having an overall negative impact on private sector investments in energyR&D. For example, while U.S. industries generally invests about 3.1’% of annual sales revenueson R&D, U.S. utilities, on average, devoted 0.3°/0 of sales to R&D in 1994; estimates indicate thatthis percentage has continued to decline since then.d Similar trends are evident elsewhere in theOECD. Utilities in the UK have reduced their R&D investments steadily over the past decade, to

s General Accounting OffIce (GAO) (1996). Changes in Electricity-Related R&I) Funding. GAO-RCED-96-203, General Accounting Office, Washington, DC.

a level that currently stands between O.10/o-0.30/0of sales.7 Dutch utilities are reducing their R&Dinvestments from 0.7°/0 to 0.6°/0 of sales, with further decreases expected, while Norwegianutilities currently invest approximately 0.3°A of sales in energy R&D!

In terms of society’s ability to stabilize atmospheric concentrations of COZ, it is important to notethat certain forms of energy R&D are experiencing a much larger share of the reductions. Arecent utility industry journal article noted that utilities with plans to sell off generation assets will“naturally pull their funding for R&D previously targeted to power production.’Q This shift awayfrom advanced power generation R&D can be seen in actions taken by utilities in many countries.

For example, utilities in Italy and the Netherlands are no longer sponsoring new, large-scaletechnology demonstration programs and have terminated ongoing demonstration projects foradvanced power system technologies, such as grid-connected photovoltaic systems, which cannot be justified strictly on economic grounds!” In the United States, Electric Power ResearchInstitute’s (EPRI) advanced power generation program (focusing on technologies such as fuelcells, coal gasification, advanced gas turbines, and renewable energy technologies) declined 66’%over a 3 year period.’1 EPRI’s renewable energy program, a subset of the advanced powergeneration program, saw its budget cut 45’XOin just two years!2

There is also mounting evidence that R&D time frames and perceptions of acceptable risk levelsfor energy R&D sponsored by utilities are contracting due to heightened competition. Forexample, the time-horizon for British utilities’ long-term R&D projects has contracted from five-to seven-years a decade ago, to less than three years now. It is estimated that in a fullycompetitive market R&D timeframes could be cut to one year for R&D sponsored by UKutilities.13 Under such circumstances: as one US utility research executive noted, the initiation ofadvanced power generation R&D programs (e.g., fuel cells) would not be feasible.ld

7 International Energy Agency, Energy Technology Policy Office (1996). Submission to the InternationalEnergy Agency’s Committee on Energy Research and Technology’s Round Table on Greater UtilityCompetition and Its Impact on Industry and Government Technology R&D Budgets and Priorities. Paris,France. 13 November.8 KEMA (The Netherlands) ( 1996). Summary of Corech/Eurelectric Discussion of R&D in a DeregulatedMarket October 11, 1996. Paper presented to the International Energy Agency’s Committee on EnergyResearch and Technology’s Round Table on Greater Utility Competition and Its Impact on Industry andGovernment Technology R&D Budgets and Priorities. Paris, France. 13 November.9 Jones, Cate. “R&D continues to brace for a difficult fiture.” Power. November/December 1998.10Italian submission (1 996). Paper and presentation to the International Energy Agency’s Committee onEnergy Research and Technology’s Round Table on Greater Utility Competition and Its Impact on Industryand Government Technology R&D Budgets and Priorities. Paris, France. 13 November.The Netherlands’ Economic Ministry. Greater Utility Competition in the Netherlands. Paper andpresentation to the International Energy Agency’s Committee on Energy Research andTechnology’s Round Table on Greater Utility Competition and Its Impact on Industry and GovernmentTechnology R&D Budgets and Priorities. Paris, France. 13 November.11 GAO, 1996.lZElectric Power Research Institute (EPRI). 1996. The Impact of Utilip industry Restructuring on

Research for the Pub[ic Good. BR- 107160. Electric Power Research Institute, Palo Alto, CA.15Walker, J.A. and Riley, F.D. (1996). Utility Competition’s Impact on Energy R&D in the UnitedKingdom. Paper and presentation to the International Energy Agency’s Committee on Energy Research andTechnology’s Round Table on Greater Utility Competition and Its Impact on Industry and GovernmentTechnology R&D Budgets and Priorities. Paris, France. 13 November.1“Jones 1998.

In this regard, Sweden’s Vattenfall, the sixth largest utility in Europe, has completely reversed thecomposition of its R&D portfolio from 70°/0 “corporate R&D” (e.g., advanced power production)and 30°/0 in the firm’s “business units.” Seventy percent of R&D resources are now invested inthe near-term R&D needs at the “business unit” level.’5 Vattenfall is doing away with its central“longer-term corporate R&D” in much the same way as countless energy firms eliminated theircorporate R&D laboratories in the late 1980s and early 1990s in an attempt to adjust to thedemands of international economic liberalization. Energy R&D investments are moving“downstream,” closer to the consumer.

Utilities in deregulated markets are also directing more of their resources (including R&Dresources) to areas only tangentially related to energy. Utility companies are entering newbusinesses and reorienting R&D resources as well in areas such as telecommunications, homesecurity, and integrated home energy management systems in an effort to offer new services thatwill allow them to maintain a strong customer base in an increasingly competitive environment!bSimilarly, firms that are planning to acquire new assets in a liberalized energy market settingoften reduce their R&D expenditures to build cash reserves needed to finance such purchases!7

The reductions in the support for energy R&D that are underway in the utility sector are alsopresent in the oil and gas industry. The largest oil and gas companies in the U.S. (most of whichare large multinationals) have reduced their investments in R&D, by 43°/0 on average, throughoutthe 1990s.1s Several factors have contributed to this trend, including consolidation in the oil andgas industries; the opening of several major upstream areas around the world, and the moreextensive deployment of existing advanced exploration and production technologies!9 Theseoverlapping drivers have had a dampening effect on energy R&D in this industry. Since oil andgas prices are expected to remain stagnant or in decline in real terms for the foreseeable future,given slack demand and abundant supplies, firms have little incentive to expand their R&Defforts.

Public Sector Energy R&D. Currently, just nine OECD countries perform more than 95% of theworld’s public sector energy R&D and, consequently, nearly all of the world’s long-term energyR&D.20 Given the high concentration of energy R&D capabilities in such a small number ofindustrialized nations, it is not an exaggeration to say that this small country set is defining theworld’s future energy choices through its energy R&D investment decisions. It is also importantto note that between 1985-1995, these nine energy R&D intensive OECD countries each reducedtheir budgets for energy R&D on average by more than 20°A in real terms. In extreme cases, such

15KEMA 1996.16 See Jones 1998 and Dooley 1998.17Jones, 1998.‘8US Department of Energy, Energy Information Administration. Performance Profiles of Major Ener~

Producers, 1997. Washington, D.C. January21, 1999.19US Department of Energy, Energy Information Administration. Petro[ium 1996: Issues and Trends.

September 1997. Washington, D.C. DOE/EIA-06 15.‘o The countries are the United States, Japan, Germany, the Netherlands, United Kingdom, France, Italy,Canada, and Switzerland. The European Union, which is a major energy R&D sponsor, is also regarded asan individual “country” in this paper, although its energy R&D investments are not included among thoseof the nine countries listed here. Source: International Energy Agency, IE.4 Ener~ Technology R&D

Statistics: 1974-1995 (Paris: international Energy Agency, 1997).

as those of Germany, Italy, and the United Kingdom, budgets were slashed by 70°/0 or more overthe same period.21

The scale of these reductions in energy R&D funding and the commonality of the funding cutsacross countries make it worthwhile to examine the evolution of key countries’ energy R&Dportfolios and to seek to explain the overall downward trend. In this section, we presentpreliminary findings from a major research effort underway at the Pacific Northwest NationalLaboratory to better understand the composition of the energy R&D programs of thesecountries.2~ This ongoing research effort seeks to assess the adequacy of the industrializedworld’s energy R&D programs, particularly in the light of the significant energy technologychallenges that global climate change could soon pose. As of the end of 1998, in depth casestudies of the United States, Japan, the European Union, Germany, and the Netherlands are nearcompletion. In 1999, case studies for of Canada, France, Italy, Switzerland, and the UnitedKingdom will be completed thereby completing the survey of the major energy R&D intensivenations.

Overall public sector investment levels in energy R&D have declined over the past decade as thefollowing data show23:●

●

●

●

●

The US federal energy R&D program has fallen by 26?40over the period 1990-1997, a declineof more than $1.2 billion in real terms from the level in 1990.The Japanese government’s energy R&D program declined 8.6% over the past three years(1996-1998), a real decrease of $226 million. As a percentage of total public sector R&Deffort, energy R&D has fallen from 19.9°/0 in 1990 to 13.7’XOin 1998.The German energy R&D program has declined by71 % since 1990, a funding reduction of$1.04 billion.

EU-sponsored energy R&D has declined by 13% since 1984; as a fraction of the EUFramework Programme budget, energy R&D’s share has declined from 47% to 189’0over thesame period.The Netherlands’ public energy R&D support declined by 28% in real terms from 1985 to1995. Support for energy R&D has recovered somewhat between 1996-1997

The trends in overall public budgets for energy R&D tell an incomplete story, however. Figure 3shows the energy R&D portfolios of the five countries mentioned above by program area. Thecomposition of these portfolios is, in many respects, as important as the overall funding levels indetermining the range of future technological options?4

2i International Energy Agency, IEA Energy Technology R&D Statistics: 1974-199.5 (Paris: InternationalEnergy Agency, 1997).22This analysis was prepared using data obtained directly from country sources and avoiding data fromthird party sources such as the Paris-based International Energy Agency (IEA). The use of official countrysource data facilitated more accurate and more detailed analysis of energy R&D trends. The use of countrysource data also enabled the conversion of all currencies into constant 1995 purchasing power parity (PPP)US dollars.2SThese data are tlom JJ Dooley, PJ Runci, and EEM Luiten, “Energy R&D in the Industrialized World:Retrenchment and Refocusing,” Pacific Northwest National Laboratory Technical Report No. PNNL-1206 I (December 1998). This report summarizes the progress of this research program in 1998.

‘4 The residual “Other” category in Figure 3 deserves explanation. For the US, this category amounts tonearly half of the US total energy R&D effort and largely comprises the “basic energy sciences” researchprograms supported by the US Department of Energy’s Office of Science (formerly the Office of EnergyResearch). These US programs explore fundamental aspects of the science that underpin energytechnologies. In the other countries this “Other Energy R&D’ category accounts for programs focusing onsystems and policy analysis. as well as some basic research, electric power transmission, distribution, and

Figure 3 shows that national governments have sharply different priorities with regard to energyR&D technology investment areas. For example, Japan devotes 66% of ail public sector energyR&D expenditures to nuclear fission programs, while the United States and the Netherlandsdevote a continually declining share-currently less than 8Yo--of their energy R&D resources tofission .25Furthermore, although all of these nations have energy policies that place a very highpriority on developing and deploying renewable energy and energy efficient technologies as away of increasing their energy security and protecting the environment, only the Dutchgovernment invests the majority of its energy R&D resources in these technology areas.An important observation that arises from this side-by-side analysis of public energy R&Dexpenditures is the large variance in the scale of government programs, from the United States’and Japan’s expenditures of more than $2 billion each, to the Netherlands’ $137 millionexpenditure. In fact, Japan’s fission energy R&D budget alone is larger than the sum of theNetherlands, EU, and German total energy R&D budgets.

Significant changes are also occurring in the major energy R&D program areas: fossil energy,energy efflc iency, renewable energy, and nuclear energy.

Fossil Energy R&D –Fossil energy R&D programs in industrialized countries no longer focus, asthey did a decade or more ago, on research to locate and characterize new fossil energy resourcesand to develop new methods of cheaply extracting these resources. To a large extent, fossilenergy R&D programs are also moving away from the development of “clean coal technology”programs designed to improve the efficiency and cleanliness of fossil fuel combustion. Thebeginning of a potentially significant transition in fossil energy research programs is nowdiscernible, wherein programs are seeking to develop zero carbon dioxide emitting fossil fueltechnologies. Amid this transition, technologies that are receiving increasing emphasis includem’ethods to “decarbonize” fossil fuels, programs to develop fuel cells capable of making use ofthe resulting hydrogen-rich fuel streams, and methods to sequester carbon dioxide. Anothernoteworthy trend is the expansion of fossil fuel research efforts to investigate the potential fordeveloping new, plentiful, and relatively clean hydrocarbon resources such as methane hydratesand coal bed methane reservoirs. Although these non-conventional fossil energy R&D programsare currently small, their emergence signals an expansion of the concept of fossil fuels and anexpectation of the continued viability of fossil fuels, even under greenhouse gas constraints, wellinto the next century. The Netherlands and Japan, for example, have had long-standing researchprograms examining the efficacy of new fossil energy technologies such as carbon sequestration.Of the industrialized countries surveyed, Japan is the largest supporter of these advanced fossilenergy research programs (e.g., carbon sequestration, methane hydrates).2G

Renewable Energy R&D – In recent years, the focus of industrialized countries’ renewable energyR&D programs has become ever more concentrated in the area of solar photovoltaics. Windenergy technology research also receives significant support although it appears that the primaryobjective of wind energy R&D programs is on technology deployment and commercialization,

storage R&D programs. Other nations do not seem to fund these “basic energy sciences” on a scalecomparable to that of the United States.‘5 At this point in this research effort, these comparisons are rough estimates. This research project is stillcollecting and standardizing the data from country sources. For example, the US “fission energy R&D”program might not include US funds for research covered in the other nation’s fission R&D programs suchas those used for the geologic disposition of radioactive waste.‘6 Monastersky, Richard. “The Ice that Bums: Can methane hydrates fuel the 2 I’t century?” Science News.November 14, 1998

Figure 3: Public Sector Energy R&D Portfolios

United States$2,259

9%

12%

50?4

147.

10%

European Union$533

‘%0

Germany (1996)$431

sg~o

Japan (1997)$2,511

5Y.

8

9%

67%

❑ Fusion

■ Fission

■ Fossil

❑ Energy Conservation

❑ Renewable Energy

Renewable Energy & Energy❑ Efficiency (Germany only)

❑ Other

The Netherlands$137

5%

rather than on the development of new systems and components that would fundamentally

improve the efficiency or economics of wind power systems. Interestingly, Japan continues todevote significant resources to renewable energy technology programs that no longer receivefunding from other industrialized countries such as wavelocean power and waste-to-energysystems. Also, the Japanese government funds a relatively large amount of geothermal researchgiven the abundance of geothermally active sites in Japan. Perhaps the most significant trend in

.

renewable energy research is the relatively flat budgets of these programs throughout the courseof the 1990s, a decade that saw increasing rhetoric from national governments pledging to dotheir best to reduce carbon dioxide emissions through, in part, the increased use of renewableenergy systems.

Energy E#iciency –Funding for energy efficiency programs has experienced the most consistentgrowth of all technology areas. In the United States, for example, public energy efficiency R&Dhas increased by 53% since 1990. Similarly, while Germany’s consolidated energy efficiencyand renewable R&D budget has grown only slightly over the past decade, its percentage of thetotal energy R&D budget has grown since 1985 from 9% to 39’Yo. The Netherlands’ efficiencyprograms have also grown steadily, now accounting for some 38% of the Dutch public energyR&D budget. Industrial energy efficiency programs appear to be receiving preference for R&Dfunds over buildings or transportation-related energy efficiency programs. This preference forindustrial energy efficiency R&D likely reflects both a desire to improve competitiveness and toprotect the environment.27

Nuclear Energy R&D – The future of nuclear energy and related technologies is in a period ofuncertainty in many countries. Many nations are decidedly shifting an ever-larger share of theirfission energy R&D programs away from the development of new reactors and components tofocus on research activities concerned with the nuclear fuel cycle, waste disposal, and reactordecommissioning. In Germany and the United States, for example, the fission research budgetshave fallen in real terms by more than 90% over the past decade. With respect to fusion research,Congress’ withdrawal of support for U.S. participation in the International ThermonuclearExperimental Reactor (ITER) project and the change in focus of the domestic program from“fusion energy technology development” to “fusion energy sciences” indicates that thecommercial availability of fusion energy is still on the distant horizon.

With regard to future energy R&D scenarios, it is important to note that despite major differencesacross countries in political culture and choices of policy instruments, countries share anassumption that greater energy efficiency will carry them a significant part of the way towardrealizing major carbon emissions reductions in the future. For example in the United States, somehave argued that major emissions reductions could be achieved at no cost through the aggressivedeployment of new energy efficiency technologies and the creation of an international carbonpermit trading regime.2s This policy trend raises questions about the prospects for futuregovernment support for new, advanced energy technology programs that will be needed tostabilize atmospheric C02 concentration over the next century.

There is also mounting evidence that the ongoing deregulation of the energy industries in manycountries is exerting downward pressure on energy R&D activities, particularly in the privatesector.29 While deregulation often leads to positive outcomes such as lower energy prices andmore choice for consumers, the competitive dynamics it introduces also heightens managers’ and

‘7 See Bundesministerium fur Bildung, Wissenschaft, Forschung, und technologies, 4. Programm

Energieforschung und Energietechno[ogien (Born: BMBF, 1997), p. 10; European Commission, ECResearch Funding (Luxembourg: Office for Official Publications of the European Communities, 1996),p.15.2%Interlaboratory Working Group. 1997. Scenarios of U.S. Carbon Redllctions: potential Impacts of

Energy –Efficient and Low-Carbon Technologies by 2010 and Beyond (Berkeley, CA: Lawrence BerkeleyNational Laboratory and Oak Ridge, TN: Oak Ridge National Laboratory), LBNL-40533 and ORNL-444,September (URL address: http: //www.oml.gov/ORNL/Energy_Eff/CON444), Executive Summary.‘9 Dooley, 1998.

shareholders’ sensitivity to short-term market performance indicators. The pressures on privatesector energy firms to reduce costs increasingly compel them to reduce their levels of R&Dexpenditure and to focus their remaining R&D investments on shorter-term, product-orientedprojects. By “privatizing” the governance of the energy industries through deregulation,governments redefine the roles of the public and private sectors in providing energy services tothe public. Although privatization may bring higher levels of economic efficiency in the energyindustries, those gains may compromise the ability to take a long view with regard to the energyfuture and to invest accordingly in energy R&D.

We conclude this overview. of trends within the energy R&D programs of the leading energyR&D intensive industrialized nations with the following summary points:

In stark contrast to overall national R&D (combined public and private sector R&D in allareas) which has flourished over the past decade, national energy R&D efforts have notexperienced significant growth over the past decade. In the nations surveyed, the dominanttrend has been toward significant reductions in publicly and privately funded energy R&D.For the public sector, energy R&D as a percent of total public sector R&D and as a percent ofgross domestic product has also been in decline in all of these nations. Where data areavailable, it is evident that private sector energy R&D investment is also in decline.Budgetary pressures, energy deregulation, and the perceived lack of an “energy crisis” arelikely to dampen government energy R&D budgets for the foreseeable future. In the absenceof major shifts in the world energy outlook, government energy R&D investments appearunlikely to be restructured and expanded in a way that is optimal for developing thetechnologies needed in the middle to long term to avoid global climate change.The current turmoil in private sector energy R&D programs brought about in large measureby the push to deregulate the energy industries will continue to place down~ard pressure onprivate sector investments in longer term energy R&D.Public energy R&D is evolving in important ways from the perspective of climate change.Research programs aimed at the development of fuel cells, hydrogen infrastructuretechnologies, and carbon capture and disposal technologies represent a small but growingpercentage of government energy R&D investment.There is an increasing gap between governments’ aspirations to curb carbon dioxideemissions, as express~~ in policy s~-tements, and th~ir funding commitments to energy R&D.Many countries appear to have adopted a de facto policy of relying on the further deploymentof existing energy efficiency technologies, fuel switching and emissions trading as theprimary means of reducing carbon dioxide emissions. While these efforts are important andnecessary, the y are, in and of themselves, insufficient to address the climate changeproblem.30

Conclusions

The small group of OECD nations that fund the vast majority of the world’s energy R&D aredefining the world’s future energy technology choices. Unless additional countries mountsignificant efforts to develop energy R&D programs, the energy research currently underway inthe OECD will define the energy technology solutions with which the world will be equipped inthe next century to address climate change. Considering the long lead times between initialinvestments in the development of new technologies and the availability of new technologies forcommercial deployment, those technologies that exist today and that are already in the R&D

30National Laboratory Directors, Technolo~ Opportunities to Reduce U.S. Greenhouse Gas Emissions

(October 1997), p. xiii.

,“pipeline” are those that will be available over the next few decades to meet global energychallenges. Declining energy R&D budgets in leading industrialized nations bespeak anarrowing range of future technological options.

That said, energy technology programs that could have significant impacts in addressing climatechange are starting to emerge. For example, the beginning of a potentially significant transition infossil energy research programs is now discernible, wherein programs are seeking to develop zerocarbon dioxide emitting fossil fuel technologies. Key technologies that are beginning to receivebudget preference include methods to “decarbonize” fossil fuels, fuel cells, and methods todispose of or sequester carbon dioxide wastes. The total amount of resources committed to thesetechnology areas is currently small, however.

The observed changes in the makeup of national energy R&D portfolios have major implicationsfor three additional aspects of energy technology development as it relates to efforts to meet thechallenge of climate change. Each of these is discussed below.

The scale of the world’s energy R&D enterprise is contracting. The challenge posed by climatechange demands continuing advancements in energy technologies over the course of the nextcentury. The continuing reductions in the scale of national energy R&D programs and theapparent shift to shorter term research suggests that the world is entering the next century withfewer energy R&D options than would be the case had more robust and sustained energy R&Dfunding levels been maintained. The drastic reductions that have taken place in key countriessuch as Germany and the United Kingdom have seriously stunted the research capabilities ofthese countries to carry out energy supply R&Don a scale that is “commensurate in scope andscale with the challenges and opportunities of the twenty-first century.’a’

Collaborative R&D between and among OECD countries is constrained by shrinking publicener~ R&D investments. In an era of greater fiscal discipline and shrinking governmentspending, public-private and international R&D cost sharing is increasingly popular among policymakers in major industrialized countries. The Japanese fast breeder reactor program and theInternational Thermonuclear Experimental Reactor (ITER) are examples of energy technologyareas where international collaboration and cost-sharing have succeeded in sustaining “bigscience” projects. Yet, in countries such as the U. S., the U. K., and Germany, deep energy R&Dbudget cuts may be having the opposite effect. As both public and private sector energy R&Dbudgets contract, pressure often intensifies to focus remaining resources “downstream” onshorter-term, applied research aimed at the development of commercial technologies rather thanon longer-term and basic research. The proprietary nature of the downsteam end of thetechnology innovation process imposes disincentives for international collaboration. Sinceresponding to climate change will require both new energy technologies and internationalcollaboration to that end, the shrinking of government R&D budgets may inflict double damagesby precluding both of these.

CoIIaborative R&D between OECD and developing countries is constrained by shrinking public

energy R&D investments. In the absence of a significant change in the current incentive structureand in the scale of OECD countries’ energy R&D efforts, it is unlikely that collaborative energyR&D programs involving OECD and developing countries will expand substantially. While theenergy technology imperatives of climate change argue in favor of long-term collaboration and

3[ Holdren, John, et. al. 1997. FederaI Energy Research and Development for the Challenges of the

Twenty--rst Century. Report of the Energy Research and Development Panel of the President’s Committeeof Advisors on Science and Technology. September 30, 1997. Washington, D.C.

capacity-building between OECD and developing countries, the shorter-term imperatives of themarket currently appear to be taking precedence.

The challenge is for industrialized countries to do more than deploy existing energy technologiesand transfer turnkey energy systems to the developing world. Meaningful response to climatechange demands that today’s energy R&D performing nations adopt the long view, embarking onefforts to engage major developing countries as partners in the climate change solution.Although shorter-term incentives will tempt OECD countries to regard major developingcountries as future markets for energy technology exports, the danger of this approach is that itmay contain the seed of its own destruction. Economic, political, and security considerations arelikely to prompt developing countries to avoid deepening dependence on imported energytechnologies. The alternatives for these countries will be either to continue to grow using currentgeneration energy technologies, or to attain a higher level of technological self-sufficiency.

‘ Global environmental well-being argues in favor of efforts to extend the world’s energy R&Dcapabilities by helping developing countries to become significant contributors of energytechnology.

,

*