basic estimation techniques

DESCRIPTION

Basic Estimation Techniques. The relationships we theoretically develop in the text can be estimated statistically using regression analysis, Regression analysis is a method used to determine the coefficients of a a functional relationship. For example, if demand is P = a+bQ - PowerPoint PPT PresentationTRANSCRIPT

5.1

Basic Estimation Techniques The relationships we theoretically develop

in the text can be estimated statistically using regression analysis,

Regression analysis is a method used to determine the coefficients of a a functional relationship.

For example, if demand is P = a+bQ

We need to estimate a and b.

5.2

Ordinary Least Squares(OLS) Means to determine regression equation that

“best” fits data Goal is to select the line(proper intercept &

slope) that minimizes the sum of the squared vertical deviations

Minimize ei2 which is equivalent to

minimizing (Yi -(Y-hat)i)2

5.3

Standard Error of the Estimate Measures variability

about the regression equation

Labeled SEE If SEE = 0 all points

are on line and fit is perfect

)1(2

knei

5.4

Standard Error of the Slope Measures theoretical

variability in estimated slope - different datasets(samples) would yield different slopes

n

i

XX

SEESE

1

21

)()(

5.5

Variability in the Dependent Variable

The sum of squares of Y about its mean value is representative of the total variation in Y

2

1

)( YYTSSn

ii

5.6

Variability in the Dependent Variable

The sum of squares of Y about the regression line(Y-hat) is representative of the “unexplained” or residual variation in Y

n

ii YYRSS

1

2)ˆ(

5.7

Variability in the Dependent Variable

The sum of squares of Y-hat about Y-bar is representative of the “explained” variation in Y

n

ii YYESS

1

2)ˆ(

5.8

Variability in the Dependent Variable

Note, TSS = ESS + RSS If all data points are on the regression line,

RSS=0 and TSS=ESS If the regression line is horizontal, slope =

0, ESS=0 and TSS=RSS The better the fit of the regression line to

the data, the smaller is RSS

5.9

Describing Overall Fit - R2

The coefficient of determination is the ratio of the “explained” sum of squares to the total sum of squares

n

ii

n

ii

YY

e

TSSRSS

TSSESSR

1

2

1

2

2

)(11

5.10

Coefficient of Determination R2 yields the percentage of variability in Y

that is explained by the regression equation It ranges between 0 and 1 What is true if R2 = 1? What is true if R2 = 0?

5.11

Statistical Inference Drawing conclusions about the population

based on sample information. Hypothesis Testing

– which independent variables are significant?– Is the model significant?

Estimation - point versus interval– what is the rate of change in Y per X?– what is the expected value of Y based on X

5.12

Errors in Hypotheses Testing Type I error - rejecting the null hypothesis

when it is true Type II error - accepting the null hypothesis

when it is false Will never eliminate the possibility of error

- but can control their likelihood

5.13

Structuring the Null and Alternative Hypotheses

The null hypothesis is often the reverse of what theory or logic suggest the researcher believes; it is structured to allow the data to contradict it. In the model on the effect of price on quantity demanded, the researcher would expect price to inversely impact amount purchased. Thus, the null might be that price does not effect quantity demanded or it effects it in a positive direction.

5.14

Structuring the Null and Alternative Hypotheses

Model: QA=B0+B1PA+B2Inc+B3PB+

– QA = quantity demanded of good A

– PA = price of good A

– Inc = Income

– PB = price of good B

H0: B1 0

HA: B1 < 0 Law of Demand expectation

5.15

H0 : 1 = 0

Do Not Reject RejectReject

/2/2

5.16

H0 : 1 0

RejectDo Not Reject

5.17

H0 : 1 0

Do Not RejectReject

5.18

The t-Test for the Slope We can test the significance of an

independent variable by testing the following

H0 : k = 0 k = 1,2,….K

HA : k 0

Note if k = 0 a change in the kth independent variable has no impact on Y

5.19

The t-Test for the Slope The test statistic is

)ˆ(

ˆ0

k

Hkk SEt

5.20

T-Test Decision Rule The critical t-value, tc, is the value that

defines the boundary line separating the rejection from the do not reject region.

For a 2-tailed test if |tk| > tc, reject the null; otherwise do not reject

For a 1-tailed test if |tk| > tc and if tc has the sign implied by HA, reject the null; otherwise do not reject

5.21

F-Test and ANOVA F-Test is used to test the overall

significance of the regression or model Analysis of Variance = ANOVA ANOVA is based on the components of the

variation in Y previously discussed - TSS, ESS, and RSS

5.22

ANOVA Table

Source Sum of Sq df Mean Sq

Explain ESS K ESS/K

Residual RSS n-K-1 RSS/(n-K-1)

Total TSS n-1

5.23

F-Statistic

)1/(/

KnRSSKESSF

)1/()(

/)ˆ(2

2

KnYYKYY

Fi

i

5.24

Hypotheses for F-Test

H0: 1= 2=…..= K=0

HA: H0 is not true

Note the null suggests that all slopes are simultaneously zero and that the model would NOT be significant, ie. no independent variables are significant

5.25

Decision Rule for F-Test If F > Fc, reject the null that the model is

insignificant. Note this likely to be good news - your model appears “good”

Otherwise do not reject

5.26

Regression StatisticsMultiple R 0.954779929R Square 0.911604712Adjusted R Square 0.901205266Standard Error 13.29712264Observations 20

ANOVAdf SS MS F Significance F

Regression 2 30998.57408 15499.28704 87.65897183 1.10827E-09Residual 17 3005.829001 176.8134706Total 19 34004.40308

Coefficients Standard Error t Stat P-value Lower 95%Intercept -74.13868247 34.61202288 -2.141992183 0.046968174 -147.1637695N 11.32035941 0.952579754 11.88389671 1.16743E-09 9.310588995C 0.011554953 0.004032508 2.865451029 0.010718486 0.003047094

Illustration 5.3 page174-75

5.27

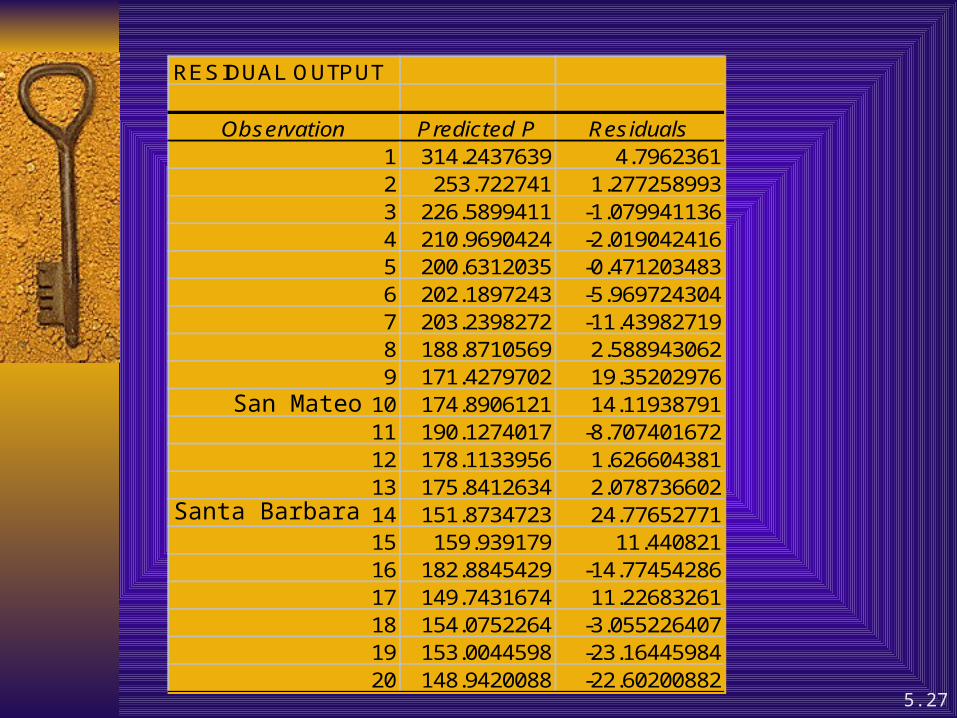

RESIDUAL OUTPUT

Observation Predicted P Residuals1 314.2437639 4.79623612 253.722741 1.2772589933 226.5899411 -1.0799411364 210.9690424 -2.0190424165 200.6312035 -0.4712034836 202.1897243 -5.9697243047 203.2398272 -11.439827198 188.8710569 2.5889430629 171.4279702 19.35202976

10 174.8906121 14.1193879111 190.1274017 -8.70740167212 178.1133956 1.62660438113 175.8412634 2.07873660214 151.8734723 24.7765277115 159.939179 11.44082116 182.8845429 -14.7745428617 149.7431674 11.2268326118 154.0752264 -3.05522640719 153.0044598 -23.1644598420 148.9420088 -22.60200882

San Mateo

Santa Barbara

5.28

Log_linear Model Constant percentage change in dependent

variable in response to a 1 percent change in an independent variable

no change in direction

cbZaXY

5.29

Double-Log Model Taking logs of the exponential equation

yields (note this is linear in the logs)

)(ln)(lnlnln ZcXbaY

5.30

Elasticity for Double Log Model The elasticity of Y with respect to X or Z

for a double- log model is merely the regression coefficient or b-hat or c-hat

Thus, in a double-log model the elasticities are constant and are merely equal to the estimated regression coefficients(partial slopes).