barclays industrial select conference - lennox … 02 20 lii barclays presentation.pdflennox...

TRANSCRIPT

Barclays Industrial Select Conference February 2014

FORWARD-LOOKING STATEMENTS

This presentation contains forward-looking statements within the meaning of the Private

Securities Litigation Reform Act of 1995. These statements are subject to numerous risks and

uncertainties that could cause actual results to differ materially from such statements. Such

risks and uncertainties include, but are not limited to, the impact of higher raw material and

commodity prices, the impact of unfavorable weather, and the ability of the company to

execute its strategic plans. For more information concerning these and other risks and

uncertainties, see Lennox International’s Form 10-K and other publicly available filings with

the Securities and Exchange Commission. LII disclaims any intention or obligation to update

or revise any forward-looking statements, whether as a result of new information, future

events or otherwise.

Use of Non-GAAP Financial Measures A reconciliation of non-GAAP financial measures appearing in this presentation to financial

measures prepared in accordance with U.S. Generally Accepted Accounting Principles

(GAAP) is posted on the company’s website at www.lennoxinternational.com.

2

Who We Are

Businesses & Strategic Priorities

Financial Guidance

3

Lennox International

… is winning in the market place with investments in products & distribution

… is well positioned for margin expansion

… is participating in growth markets with significant pent-up demand

… is driving shareholder value with a disciplined use of free cash flow

4

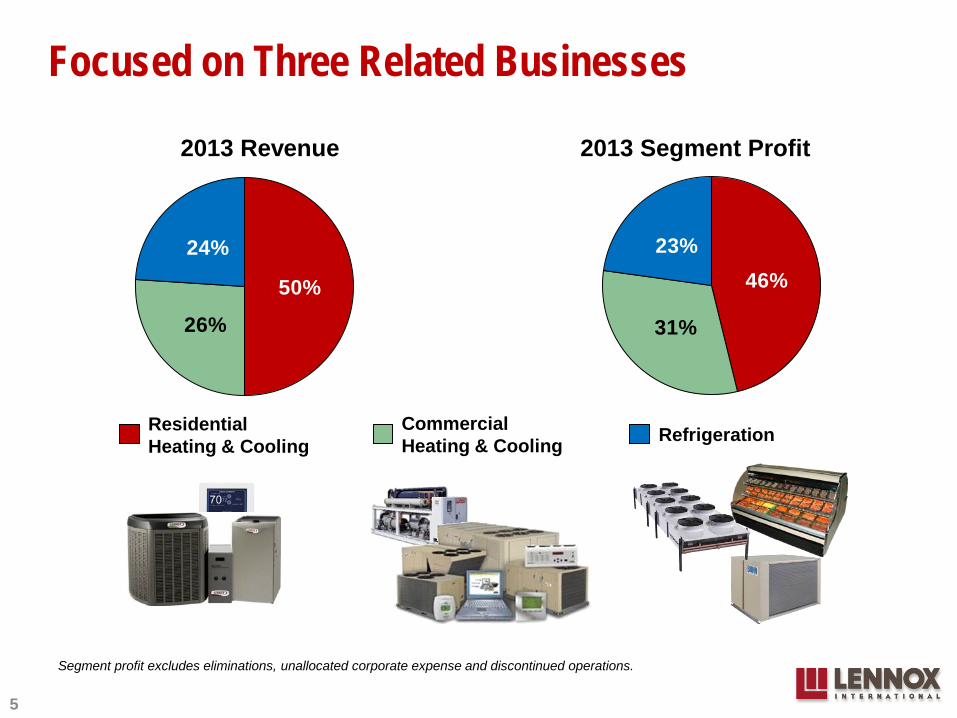

50%

26%

24%46%

31%

23%

Refrigeration Residential Heating & Cooling

Focused on Three Related Businesses

2013 Revenue 2013 Segment Profit

Commercial Heating & Cooling

Segment profit excludes eliminations, unallocated corporate expense and discontinued operations.

5

68%

32%

Business Mix

Customer

Residential Commercial

Based on 2013 total LII revenue excluding discontinued operations.

Americas Europe Asia Pacific

Geography

Replacement New Construction

End Market

85%

9%6%

50%50%

6

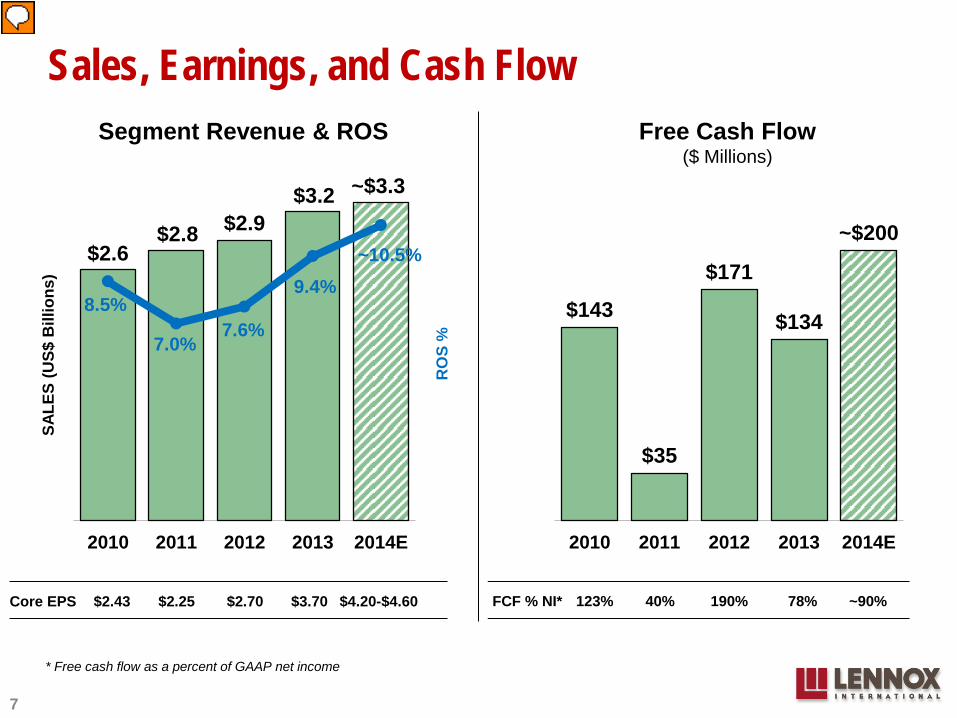

$143

$35

$171

$134

~$200

$0

$50

$100

$150

$200

$250

2010 2011 2012 2013 2014E

Sales, Earnings, and Cash Flow

Segment Revenue & ROS Free Cash Flow ($ Millions)

Core EPS $2.43 $2.25 $2.70 $3.70 $4.20-$4.60

* Free cash flow as a percent of GAAP net income

$2.6 $2.8 $2.9

$3.2 ~$3.3

8.5%

7.0% 7.6%

9.4% ~10.5%

0%

2%

4%

6%

8%

10%

12%

$0

$1

$2

$3

2010 2011 2012 2013 2014E

RO

S %

SALE

S (U

S$ B

illio

ns)

7

FCF % NI* 123% 40% 190% 78% ~90%

Who We Are

Businesses & Strategic Priorities

Financial Guidance

8

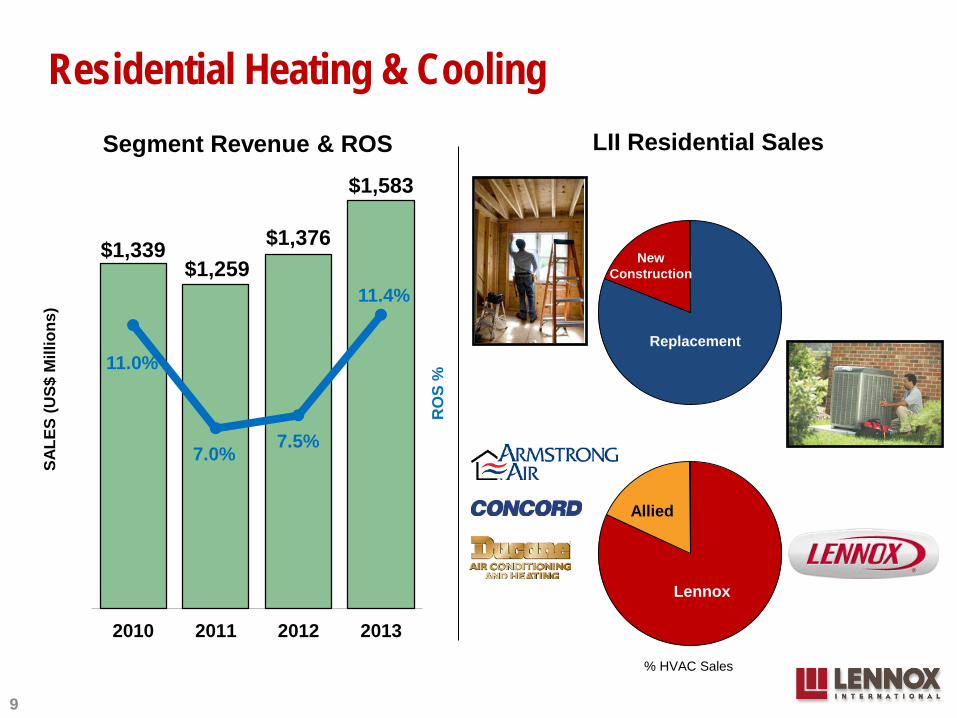

$1,339 $1,259

$1,376

$1,583

11.0%

7.0% 7.5%

11.4%

0%

2%

4%

6%

8%

10%

12%

14%

16%

$0

$1,500

2010 2011 2012 2013

RO

S %

SALE

S (U

S$ M

illio

ns)

Residential Heating & Cooling Segment Revenue & ROS

Replacement

NC

LII Residential Sales

Allied

Lennox

NC

Replacement

Allied

Lennox

% HVAC Sales

New Construction

Replacement

9

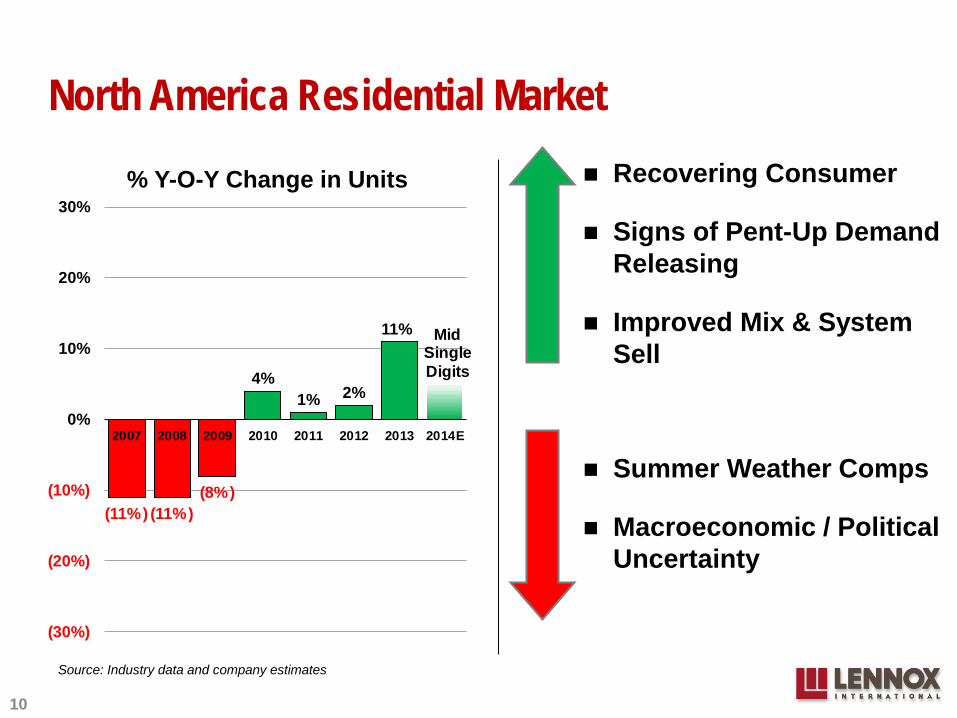

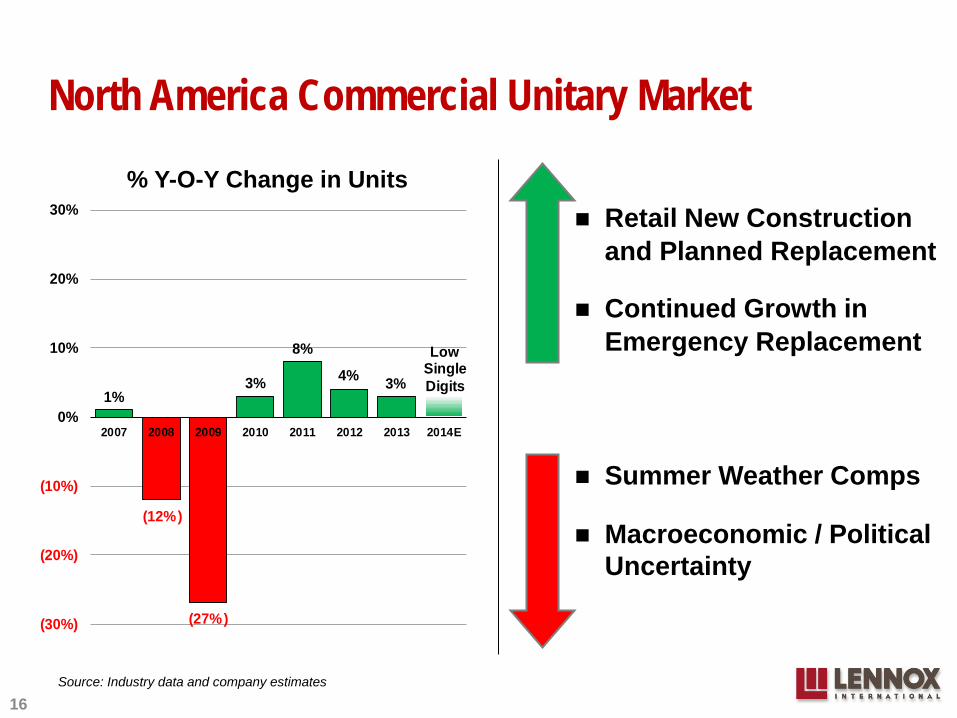

(11%) (11%)(8%)

4%1% 2%

11% MidSingle Digits

(30%)

(20%)

(10%)

0%

10%

20%

30%

2007 2008 2009 2010 2011 2012 2013 2014E

North America Residential Market

Source: Industry data and company estimates

% Y-O-Y Change in Units

10

Recovering Consumer

Signs of Pent-Up Demand Releasing

Improved Mix & System Sell

Summer Weather Comps

Macroeconomic / Political Uncertainty

icomfort Wi-Fi™

Continued Investment in Industry Leading Products

11

Residential – Industry Leading Products

Ultimate Comfort SystemTM

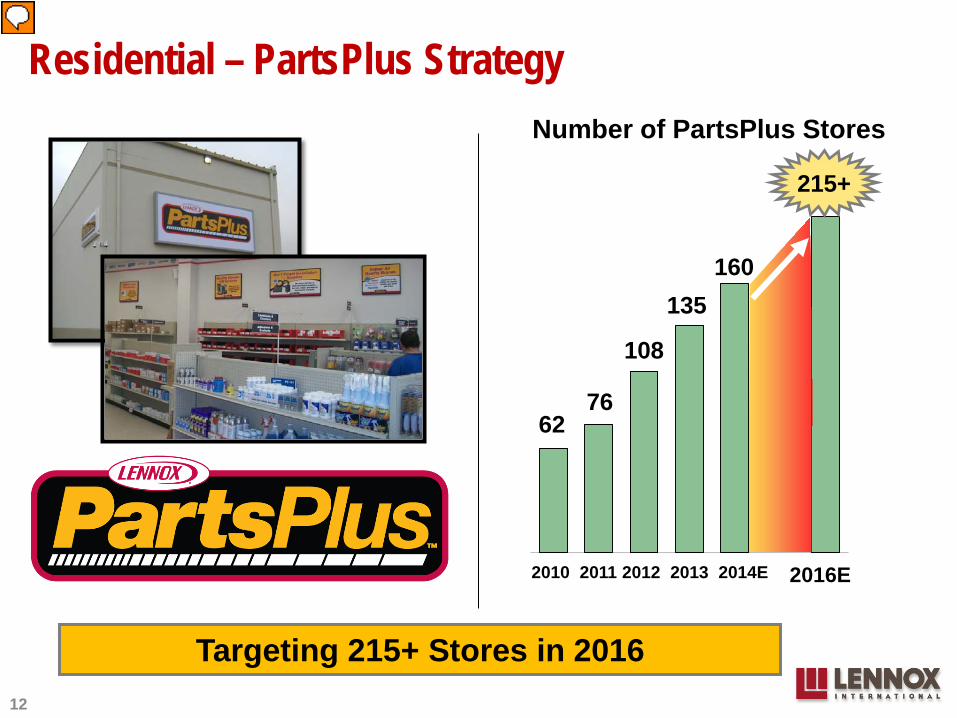

Number of PartsPlus Stores

62 76

108

135

200+

2010 2011 2012 2013 2014 2015TGT

Targeting 215+ Stores in 2016 12

Residential – PartsPlus Strategy

200+

2016E

215+

160

2010 2011 2012 2013 2014E

200

270

340

420460

2009 2010 2011 2012 2013

Saltillo Mexico Factory Units Sold (000s)

Saltillo Facility Exceeding Expectations 13

Residential – Manufacturing Strategy

Expanding Mexico Manufacturing Footprint

14

Residential – Manufacturing Strategy

$30M Investment

Furnace Production & Sheet Metal Fabrication

Start Production 2nd Half of 2014

$15M Annualized Savings by 2016

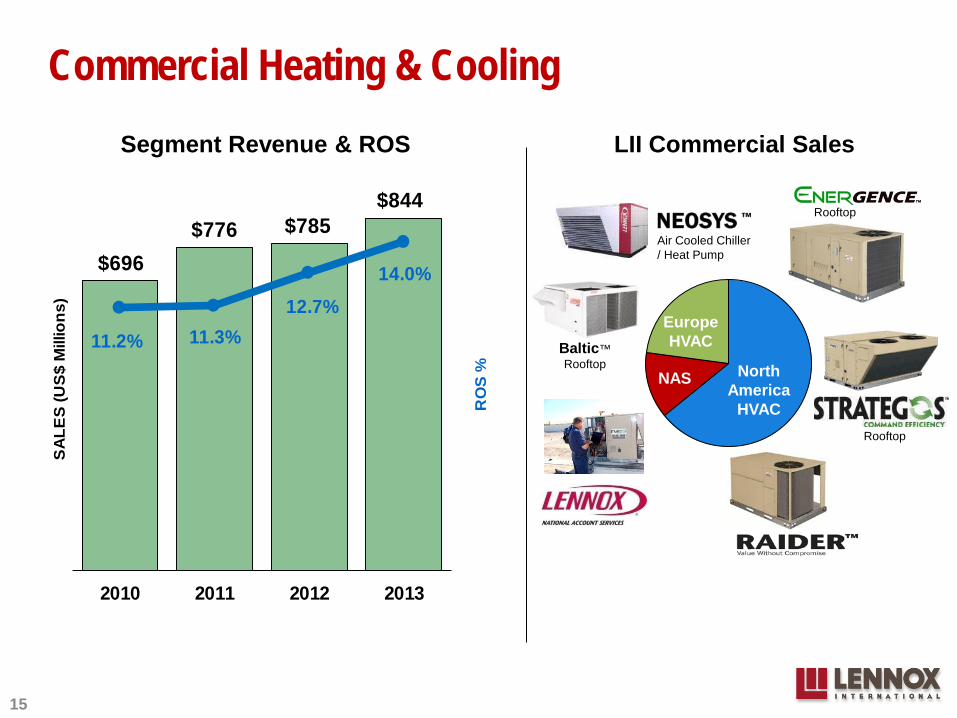

$696$776 $785

$844

11.2% 11.3%12.7%

14.0%

2010 2011 2012 2013

RO

S %

SA

LES

(US

$ M

illio

ns)

Commercial Heating & Cooling

North America

HVAC

Europe HVAC

Segment Revenue & ROS LII Commercial Sales

Rooftop

Baltic™ Rooftop

Rooftop

Air Cooled Chiller / Heat Pump

15

NAS

1%

(12%)

(27%)

3%

8%

4% 3%

Low Single Digits

(30%)

(20%)

(10%)

0%

10%

20%

30%

2007 2008 2009 2010 2011 2012 2013 2014E

North America Commercial Unitary Market

Source: Industry data and company estimates

% Y-O-Y Change in Units Retail New Construction

and Planned Replacement

Continued Growth in Emergency Replacement

Summer Weather Comps

Macroeconomic / Political Uncertainty

16

Commercial – Emergency Replacement Strategy

Significant Investment in Both Products & Distribution

17

75% Same Day Coverage

Commercial Distribution Points

18

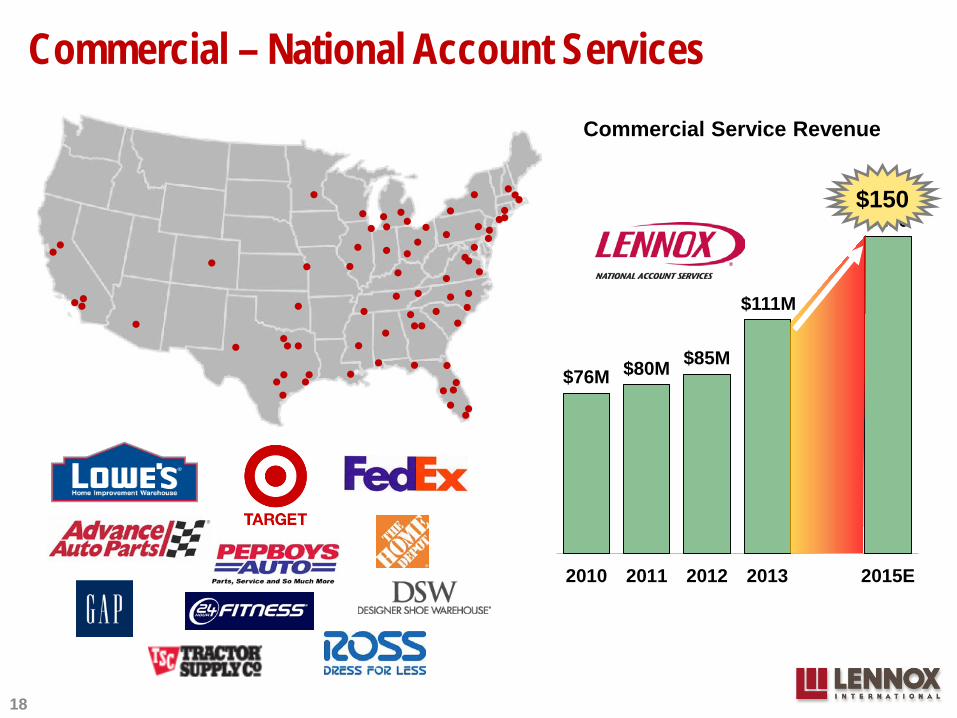

$76M $80M $85M

$111M

$150

2010 2011 2012 2013 2015E

$150

Commercial Service Revenue

Commercial – National Account Services

Leverage Lennox Company Owned Distribution Advantage

19

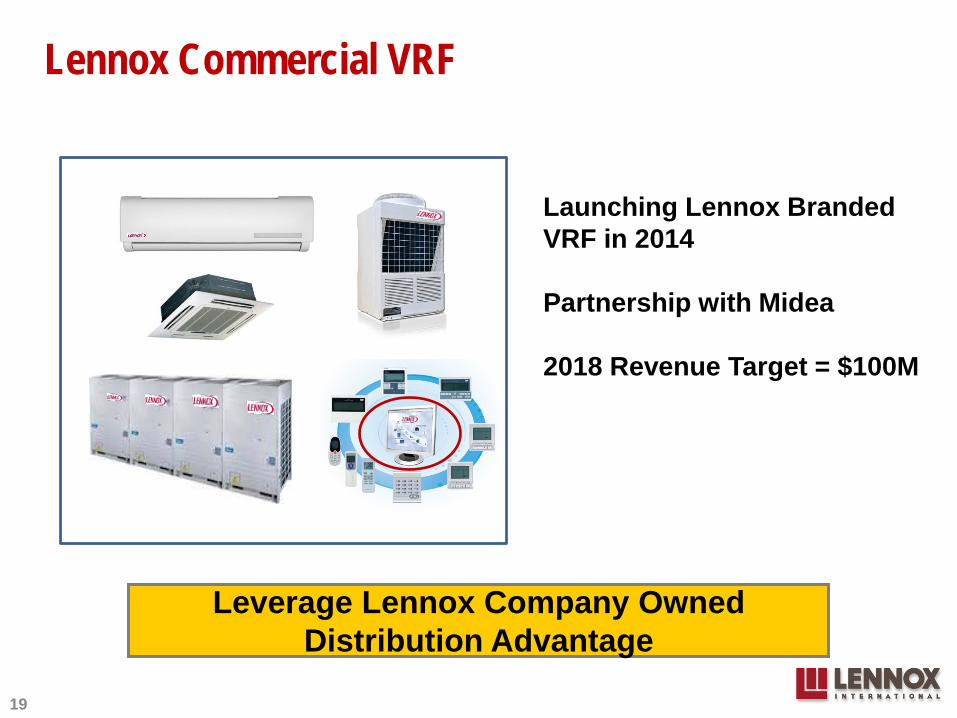

Lennox Commercial VRF

Launching Lennox Branded VRF in 2014

Partnership with Midea

2018 Revenue Target = $100M

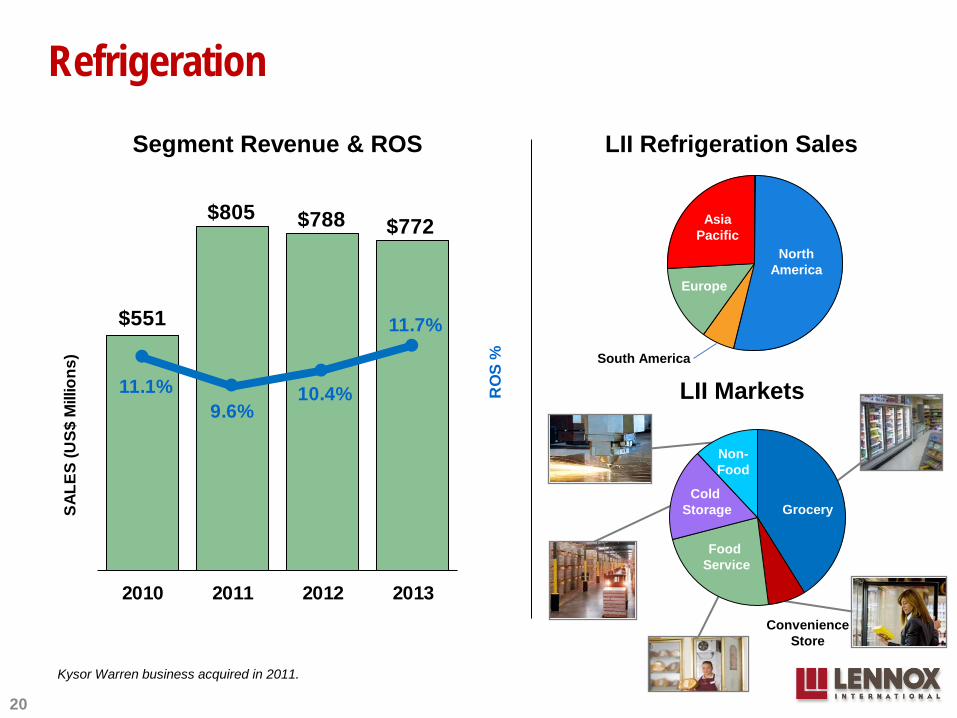

LII Markets

Food Service

Grocery

Convenience Store

Cold Storage

Non- Food

Refrigeration

Segment Revenue & ROS LII Refrigeration Sales

Asia Pacific

North America

Europe

20

Kysor Warren business acquired in 2011.

$551

$805 $788 $772

11.1%9.6%

10.4%

11.7%

2010 2011 2012 2013

RO

S %

SALE

S (U

S$ M

illio

ns)

North America

South America

Asia Pacific

Europe

21

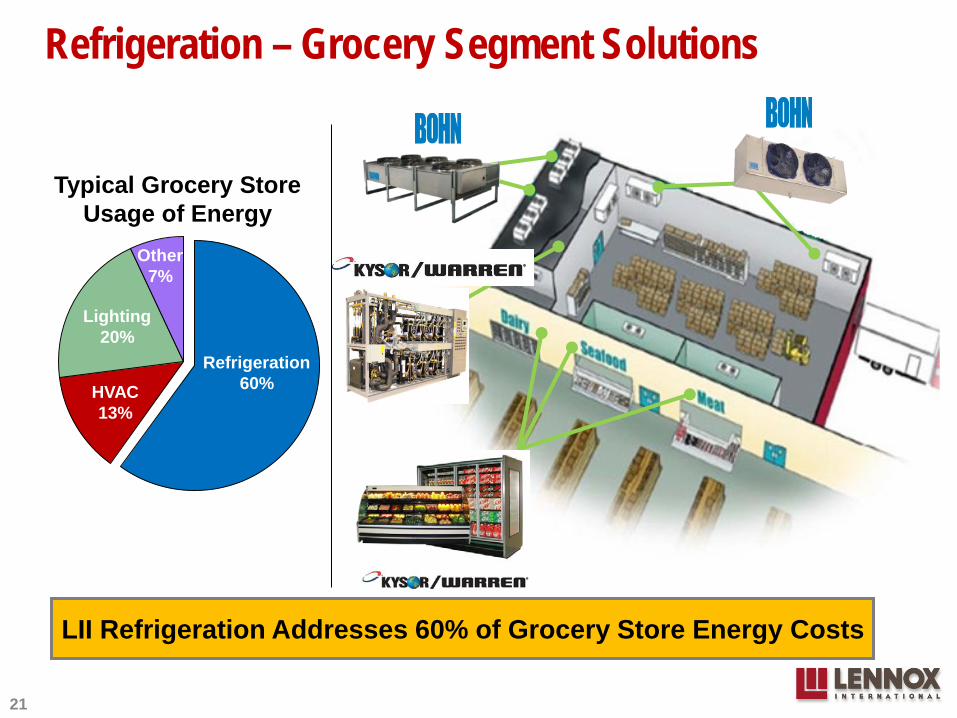

Refrigeration – Grocery Segment Solutions

Lighting

Refrigeration 60%

Lighting 20%

Other 7%

HVAC 13%

Typical Grocery Store Usage of Energy

LII Refrigeration Addresses 60% of Grocery Store Energy Costs

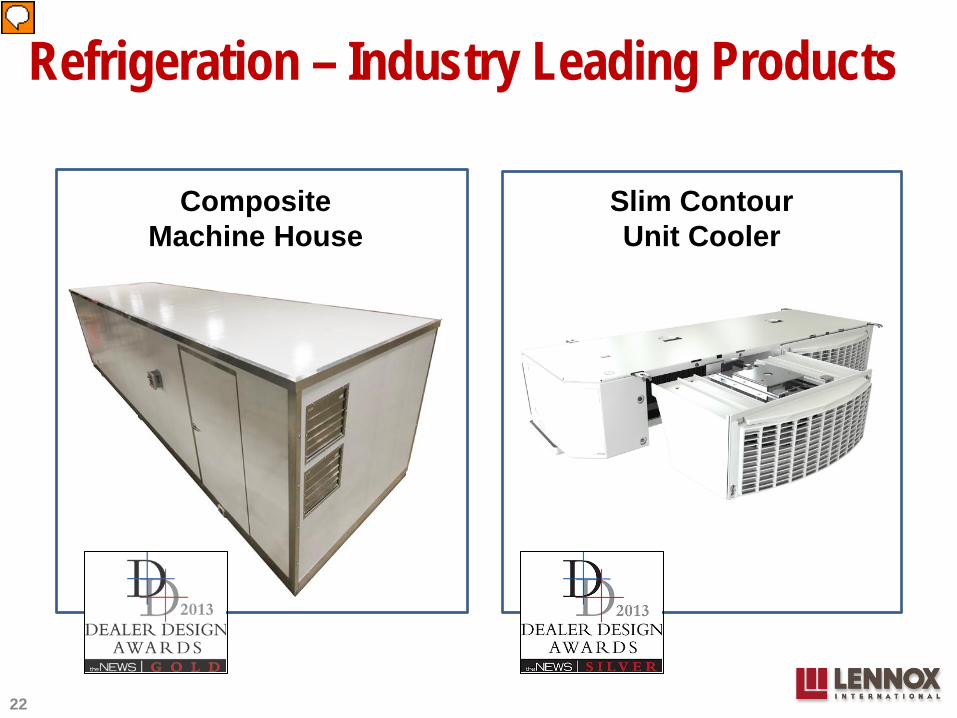

Refrigeration – Industry Leading Products

22

Composite Machine House

Slim Contour Unit Cooler

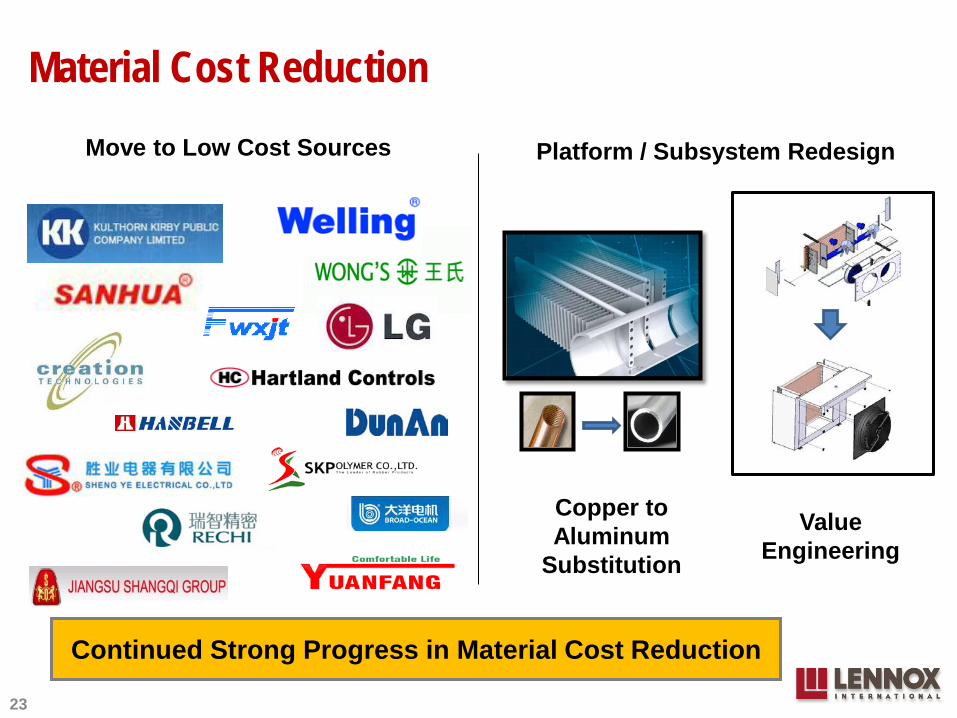

Platform / Subsystem Redesign

Value Engineering

Copper to Aluminum

Substitution

23

Move to Low Cost Sources

Material Cost Reduction

Continued Strong Progress in Material Cost Reduction

Who We Are

Businesses & Strategic Priorities

Financial Guidance

24

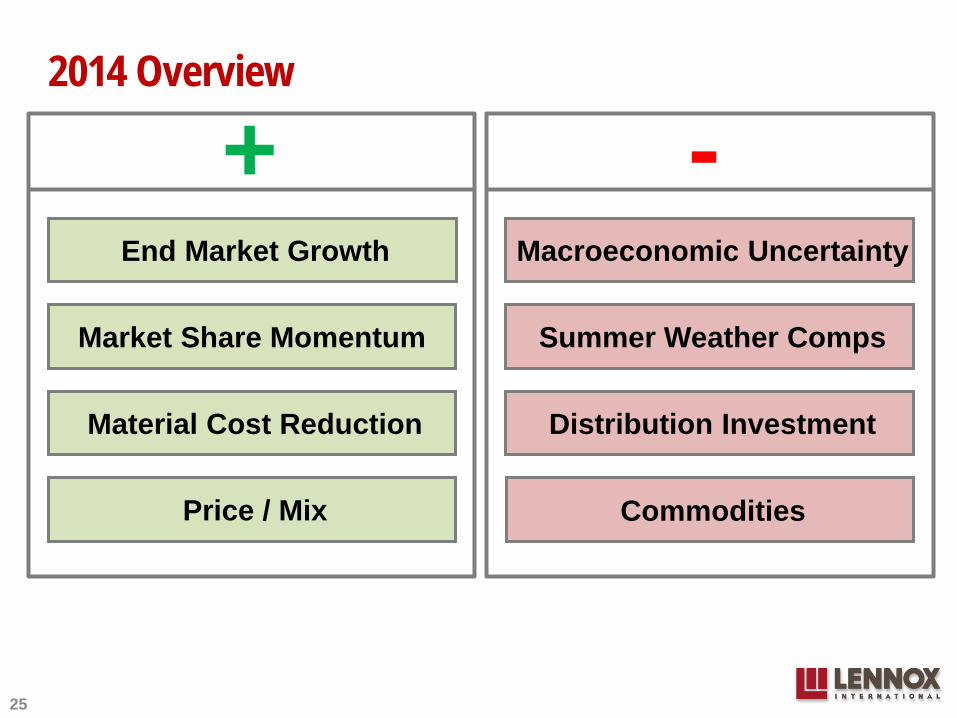

2014 Overview

+ - End Market Growth Macroeconomic Uncertainty

Market Share Momentum

Material Cost Reduction

Summer Weather Comps

Price / Mix

Distribution Investment

25

Commodities

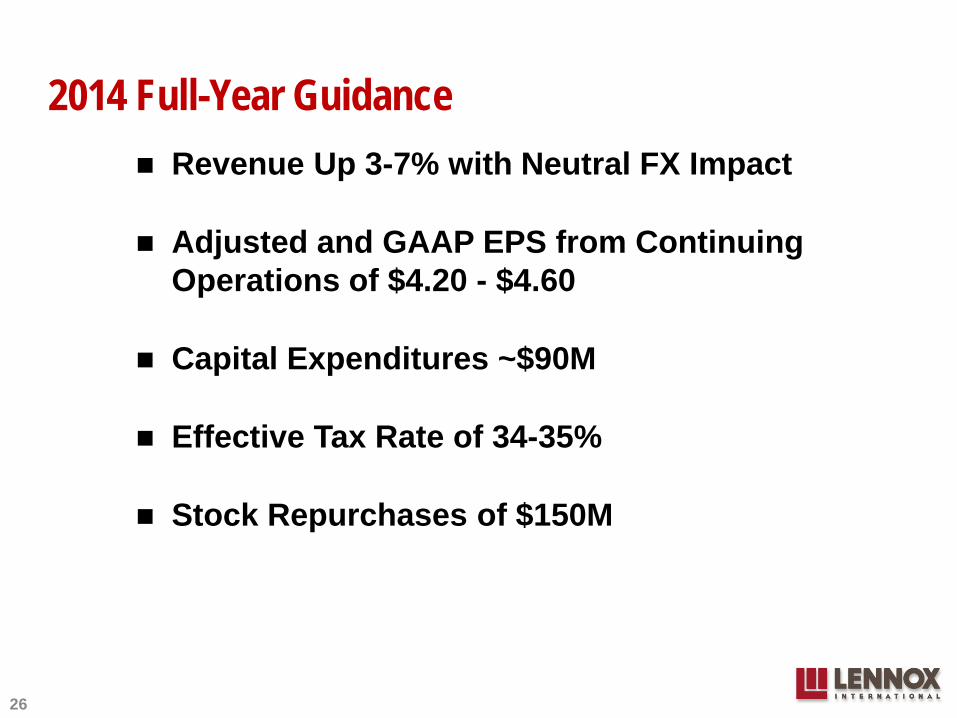

2014 Full-Year Guidance Revenue Up 3-7% with Neutral FX Impact

Adjusted and GAAP EPS from Continuing Operations of $4.20 - $4.60

Capital Expenditures ~$90M

Effective Tax Rate of 34-35%

Stock Repurchases of $150M

26

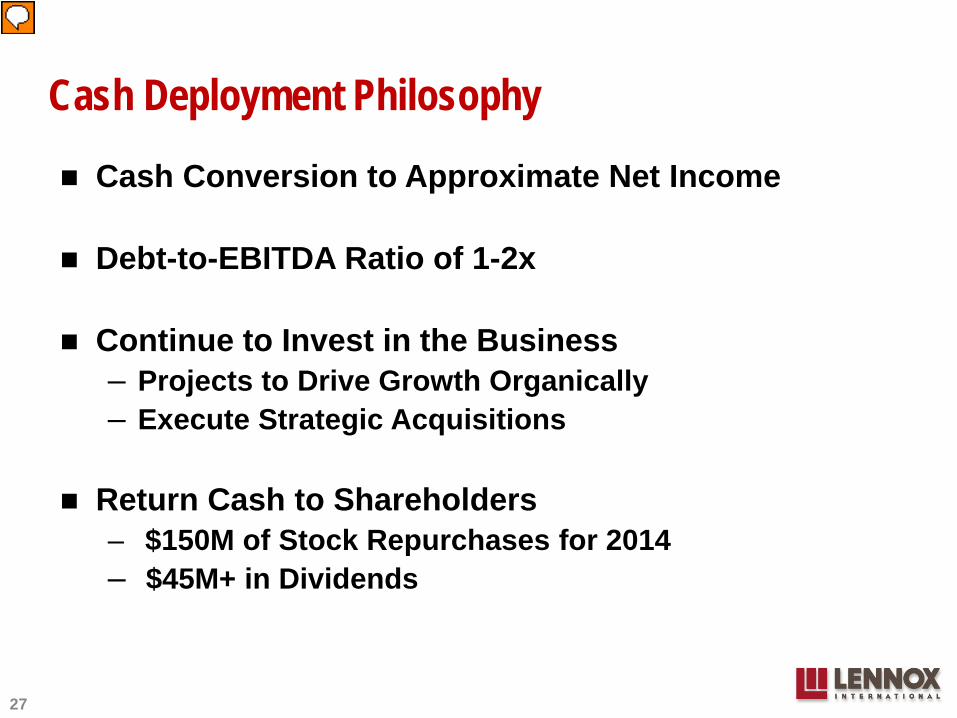

Cash Deployment Philosophy

Cash Conversion to Approximate Net Income

Debt-to-EBITDA Ratio of 1-2x

Continue to Invest in the Business – Projects to Drive Growth Organically – Execute Strategic Acquisitions

Return Cash to Shareholders – $150M of Stock Repurchases for 2014 – $45M+ in Dividends

27

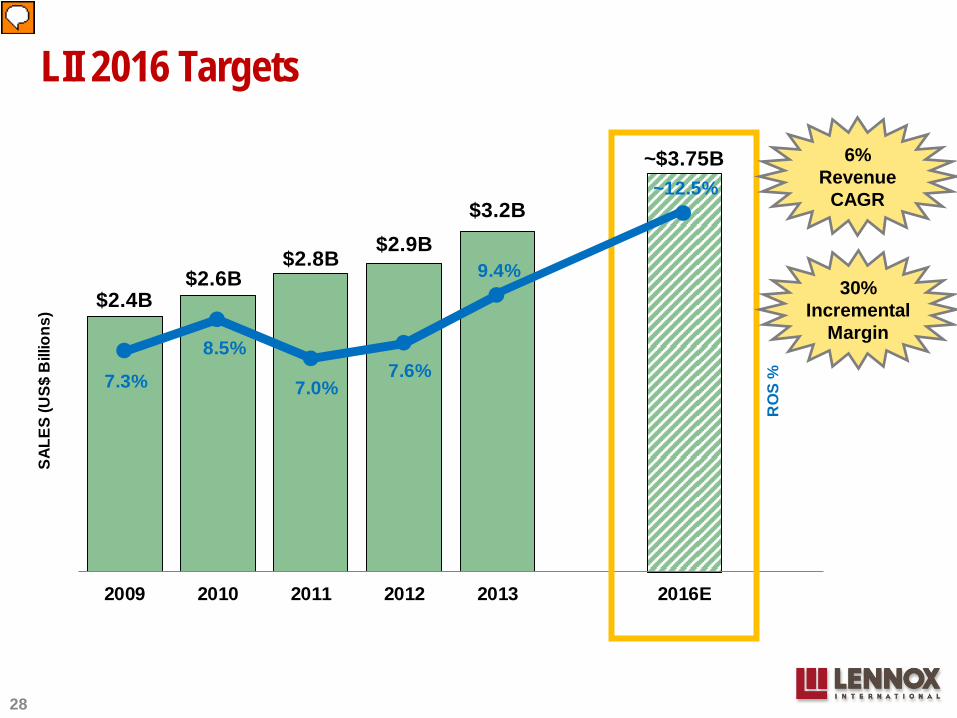

$2.4B$2.6B

$2.8B$2.9B

$3.2B

~$3.75B

7.3%

8.5%

7.0%7.6%

9.4%

~12.5%

2009 2010 2011 2012 2013 2016E

RO

S %

SALE

S (U

S$ B

illio

ns)

LII 2016 Targets

30% Incremental

Margin

28

6% Revenue

CAGR

Lennox International

… is winning in the market place with investments in products & distribution

… is well positioned for margin expansion

… is participating in growth markets with significant pent-up demand

… is driving shareholder value with a disciplined use of free cash flow

29

30

GAAP / Non-GAAP Reconciliations

31

32

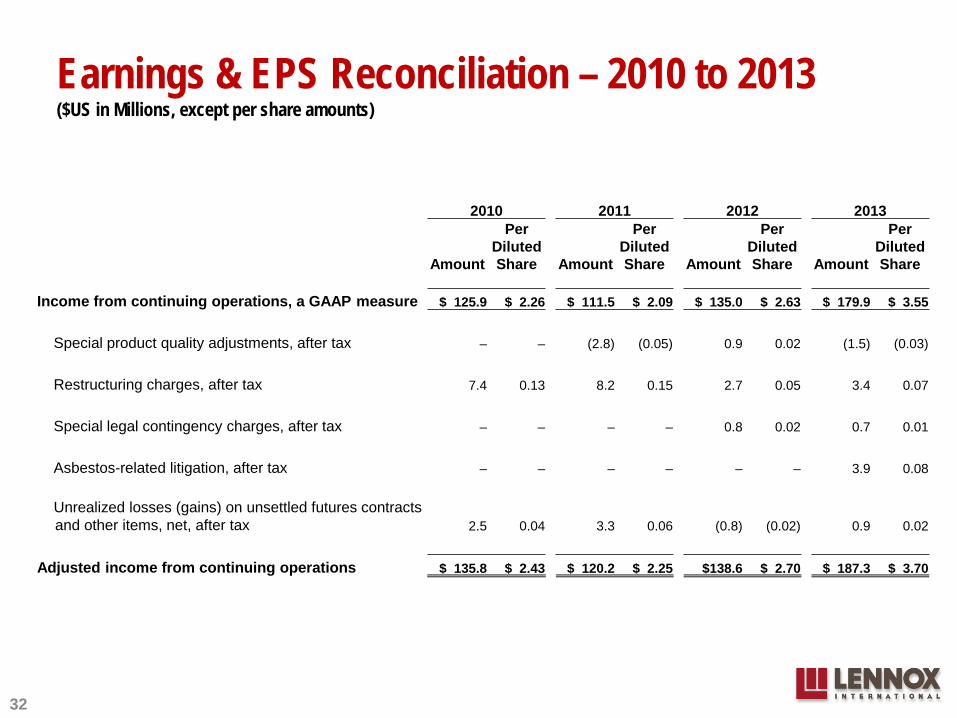

Earnings & EPS Reconciliation – 2010 to 2013 ($US in Millions, except per share amounts)

2010 2011 2012 2013

Amount

Per Diluted Share Amount

Per Diluted Share Amount

Per Diluted Share Amount

Per Diluted Share

Income from continuing operations, a GAAP measure $ 125.9 $ 2.26 $ 111.5 $ 2.09 $ 135.0 $ 2.63 $ 179.9 $ 3.55

Special product quality adjustments, after tax – – (2.8) (0.05) 0.9 0.02 (1.5) (0.03)

Restructuring charges, after tax 7.4 0.13 8.2 0.15 2.7 0.05 3.4 0.07

Special legal contingency charges, after tax – – – – 0.8 0.02 0.7 0.01

Asbestos-related litigation, after tax – – – – – – 3.9 0.08

Unrealized losses (gains) on unsettled futures contracts and other items, net, after tax 2.5 0.04 3.3 0.06 (0.8) (0.02) 0.9 0.02

Adjusted income from continuing operations $ 135.8 $ 2.43 $ 120.2 $ 2.25 $138.6 $ 2.70 $ 187.3 $ 3.70

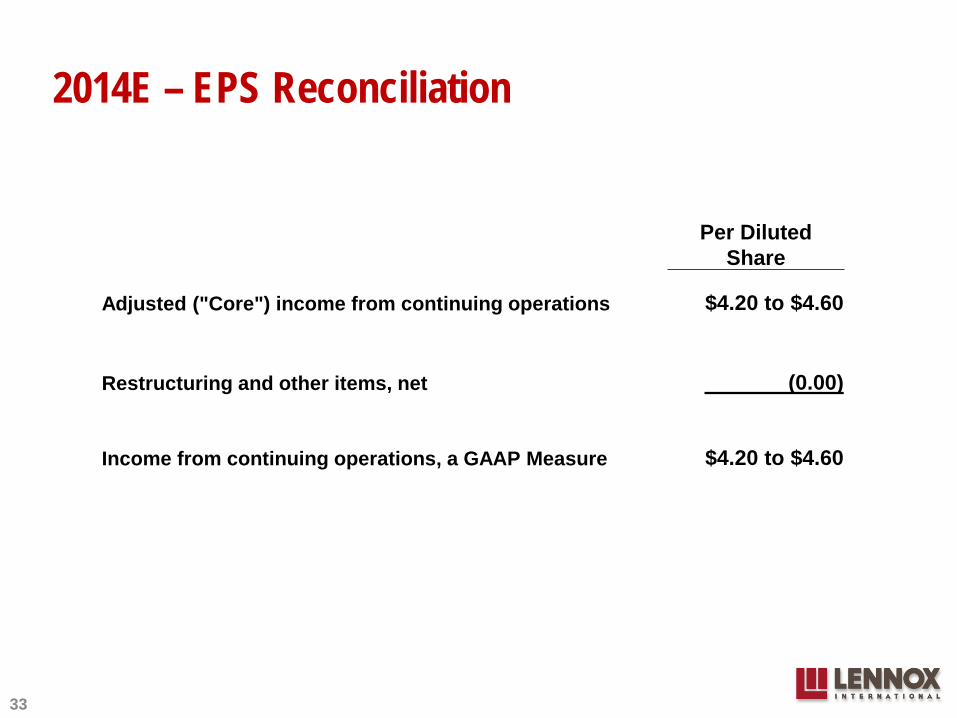

2014E – EPS Reconciliation

33

Per Diluted Share

Adjusted ("Core") income from continuing operations $4.20 to $4.60

Restructuring and other items, net (0.00)

Income from continuing operations, a GAAP Measure $4.20 to $4.60

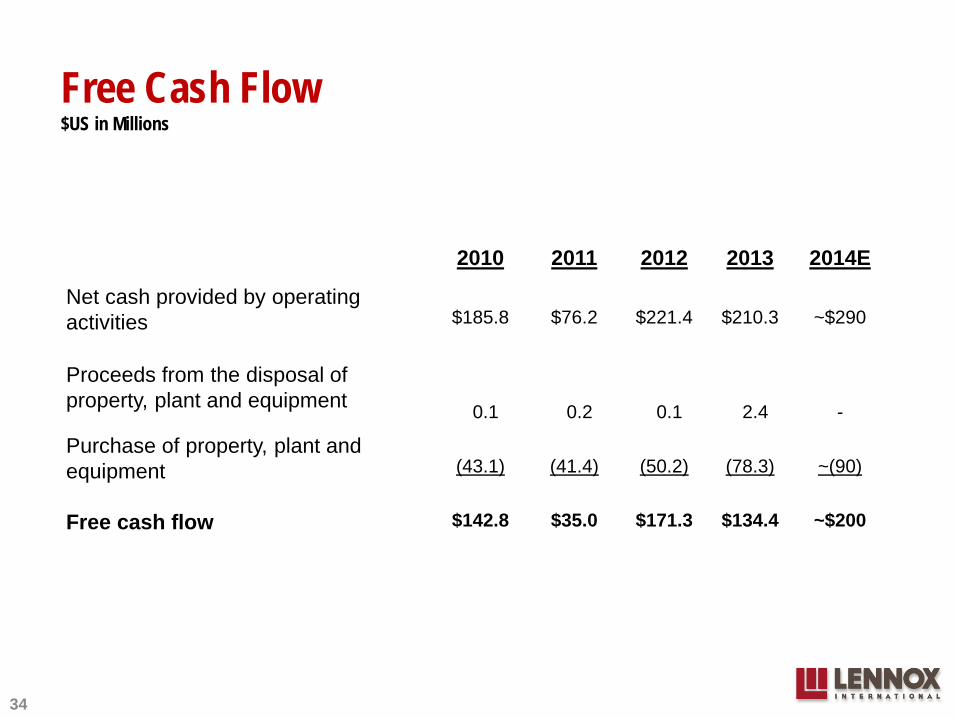

Free Cash Flow $US in Millions

34

2010

2011

2012

2013

2014E

Net cash provided by operating activities

$185.8

$76.2

$221.4

$210.3

~$290

Proceeds from the disposal of property, plant and equipment 0.1 0.2 0.1 2.4 -

Purchase of property, plant and equipment

(43.1)

(41.4)

(50.2)

(78.3)

~(90)

Free cash flow $142.8 $35.0 $171.3 $134.4 ~$200