balance sheet (translation) as of march 31, … · balance sheet (translation) as of march 31, 2011...

TRANSCRIPT

1

BALANCE SHEET (Translation) As of March 31, 2011

(Millions of yen) Account item Amount Account item Amount

ASSETS LIABILITIES

Current assets 971,205 Current liabilities 586,668 Cash and deposits 28,397 Notes payable-trade 3,939 Notes receivable-trade 23 Accounts payable-trade 25,354 Installment contract receivables 133,025 Short-term borrowings 50,975 Lease receivables 85,974 Current portion of bonds 2,000 Lease investment assets 502,844 Current portion of long-term debt 237,903 Loans receivables from customers 60,308 Commercial paper 190,958

Other loans receivables from customers 62,627 Payables under securitized lease receivables 19,090

Lease contract receivables 1,582 Lease payables 3,608 Other operating assets 7,914 Accounts payables 8,217 Advance on contracts 1,413 Accrued income taxes 3,630 Prepaid expenses 1,538 Accrued expenses 2,156

Accrued income 476 Advances received on lease contracts 11,370

Short-term loans receivables 89,773 Deposits received 7,666 Deferred tax assets 8,562 Deferred income 48

Other current assets 11,177 Unrealized gross profits on installment contracts 18,456

Allowance for doubtful receivables (24,435) Provision for bonuses 925 Other current liabilities 366

Fixed assets 160,183 Long-term liabilities 420,738 Tangible assets 14,581 Bonds 2,003 Property for lease and rent 13,372 Long-term debt 390,788

Property for lease and rent 13,461 Long-term payables under securitized lease receivables 16,350

Allowance for loss on disposal of property for lease and rent (89) Guarantee deposits received 6,723

Own-used assets 1,209 Long-term deferred income 31

Provision for employees’ retirement benefits 2,493

Intangible assets 5,017 Other long-term liabilities 2,347 Property for lease and rent 591

Property for lease and rent 594 Total liabilities 1,007,406

Allowance for loss on disposal of property for lease and rent (3) NET ASSETS

Goodwill 96 Stockholders’ equity 123,496 Software 3,982 Capital stock 32,000 Other intangible assets 347 Capital surplus 66,264

Legal capital surplus 30,000 Investments and other assets 140,584 Other capital surplus 36,264 Investment securities 13,687 Retained earnings 25,231 Investments in affiliated companies 25,750 Earned surplus reserve 412 Long-term loans receivables 89,596 Other retained earnings 24,819 Claims provable in bankruptcy, in

rehabilitation and other 4,895 Unappropriated 24,819

Long-term prepaid expenses 120 Valuation and translation adjustments 485

Long-term deferred tax assets 4,140 Net unrealized gain on available-for-sale securities 1,302

Long-term money deposited 2,115 Deferred gains (losses) on hedges (816) Other investments 4,829

Allowance for doubtful receivables (4,551) Total net assets 123,982

Total assets 1,131,388 Total liabilities and net assets 1,131,388

2

STATEMENT OF INCOME (Translation) For the year ended March 31, 2011

(Millions of yen) Account item Amount

Revenues Lease revenue 255,916 Installment sales 39,456 Finance revenue 4,919 Other revenue 7,245 307,538

Costs Cost of lease 224,269 Cost of installment sales 34,676 Cost of finance 563 Cost of other sales 5,928 Financing costs 6,537 271,976

Gross profit 35,562 Selling, general and administrative expenses 14,535

Operating income 21,026 Non-operating income

Interest and dividends received 2,658 Other 326 2,984

Non-operating expenses Interest expense 1,565 Other 185 1,751

Ordinary income 22,258 Special gains

Gain on sales of investment securities 4 Reversal of allowance for doubtful receivables 7,694 7,698

Special losses Loss on disposal of operating assets, etc. 18 Loss on disposal of fixed assets 8 Impairment loss 757 Loss on sales of investment securities 930 Loss on valuation of investment securities 1,547 Loss on sales of investments in affiliated

companies 238

Loss on liquidation of investments in affiliated companies 17

Loss on valuation of investments in affiliated companies 55

Loss on sales of golf club memberships 28 Loss on effect of adoption of accounting standard

for asset retirement obligations 182

Extra retirement payment 1,855 5,640 Income before income taxes 24,317

Income taxes-current 4,463 Income taxes-deferred 4,375

Net income 15,478

3

STATEMENT OF CHANGES IN NET ASSETS (Translation) For the year ended March 31, 2011

(Millions of yen)

Stockholders’ equity

Capital stock Capital surplus

Legal capital surplus Other capital surplus Total capital surplus

Balance at March 31, 2010 32,000 30,000 36,264 66,264

(Changes during the year)

Net income ─ Changes during the year for items other than stockholders’ equity (net)

─

Total of changes during the year ─ ─ ─ ─

Balance at March 31, 2011 32,000 30,000 36,264 66,264

Stockholders’ equity

Retained earnings Total stockholders’

equity Earned surplus reserve

Other retained earnings Total retained

earnings Unappropriated

Balance at March 31, 2010 412 9,340 9,753 108,018

(Changes during the year)

Net income 15,478 15,478 15,478 Changes during the year for items other than stockholders’ equity (net)

─ ─

Total of changes during the year ─ 15,478 15,478 15,478

Balance at March 31, 2011 412 24,819 25,231 123,496

Valuation and translation adjustments

Net unrealized gain on

available-for-sale securities

Deferred gains (losses) on hedges

Total valuation and translation

adjustments Total net assets

Balance at March 31, 2010 1,848 (747) 1,100 109,118

(Changes during the year)

Net income ─ 15,478 Changes during the year for items other than stockholders’ equity (net)

(545) (69) (615) (615)

Total of changes during the year (545) (69) (615) 14,863

Balance at March 31, 2011 1,302 (816) 485 123,982

4

NOTES TO FINANCIAL STATEMENTS (Translation) For the year ended March 31, 2011 (Notes to Significant Accounting Policies) 1. Valuation basis and methods applied for assets

(1) Securities ① Trading securities………………………. At fair value based on market price etc., as of the

balance-sheet date. (The cost of securities sold is determined by the moving-average method.)

② Held-to-maturity debt securities…………. At amortized cost or accumulated cost ③ Investments in subsidiaries and affiliates. At cost determined by the moving-average method ④ Available-for-sale securities

Those with determinable fair values.......... At fair value based on market price etc., as of the balance-sheet date. (All valuation differences are reported as a component of net assets. The cost of securities sold is determined by the moving-average method.)

Those without determinable fair values..... At cost determined by the moving-average method (2) Derivative financial instruments......................... At fair value

2. Methods of depreciation and amortization applied for fixed assets

(1) Property for lease and rent

Property for lease and rent is depreciated under the straight-line method within the estimated lease and rent

period, assuming that useful lives are the same as the estimated lease and rent period, and that residual values

are the disposal price estimable at the end of the estimated lease and rent period.

In some of the property for lease and rent, tangible assets are depreciated under the declining-balance method.

However, buildings (excluding improvements) acquired on or after April 1, 1998 are depreciated under the

straight-line method. Intangible assets are amortized under the straight-line method.

(2) Other fixed assets

Of the other fixed assets, tangible assets are depreciated under the declining-balance method while intangible

assets are amortized under the straight-line method. However, buildings (excluding improvements) acquired on

or after April 1, 1998 are depreciated under the straight-line method.

Software of internal use is amortized under the straight-line method over internal useful lives (5 years).

3. Significant allowance and provisions

(1) Allowance for doubtful receivables

For general receivables, allowance for estimated uncollectible receivables is provided for at an adequate rate

calculated based on the probability of bankruptcy, while allowance for certain categories including seriously

doubtful receivables is provided for based on case-by-case collectability assessment.

(2) Allowance for loss on disposal of property for lease and rent

Allowance for estimated loss is provided for potential loss associated with disposal of property for lease and

rent.

(3) Provision for bonuses

Of the estimated amount of bonuses payable to employees in the following fiscal year, the portion attributable

to their service during current fiscal year has been set aside as provision for employees’ bonuses.

(4) Provision for employees’ retirement benefits

The Company provides for the estimated year-end liabilities for retirement benefits based on the projected

5

benefit obligations and plan assets at the balance sheet date.

Past service liabilities are recognized in each fiscal year as they arise. Actuarial differences are charged to

income on a straight-line basis, beginning from the year after they are recognized, over the then average

remaining years of service of employees (13 to 15 years).

4. Lease accounting

Accounting policy for revenues and costs from finance lease transactions

The Company adopts the method in which lease revenue and cost of lease are recorded at the time when lease

fees are collectible.

Accounting policy for revenues from operating lease transactions

The Company records lease revenues corresponding to the elapsed period of the lease contract term, on the

basis of the monthly lease fees collectible according to the lease contract for such contract term.

5. Accounting for installment contracts

The Company accounts for the full amount of contract as installment contract receivables upon delivery of

goods, and records installment sales and costs of installment sales as each payment becomes due.

Unrealized gross profits on installment contract receivables with installment payments becoming due at later

dates are deferred.

Meanwhile, for some of the installment contracts, amount equivalent to interest is allocated to each period as

installment sales.

6. Accounting treatment for financial expenses

Total assets are divided into assets based on sales transactions and other assets, where financial expenses

corresponding to the former are recorded as financing costs under the heading of operating expenses while

financial expenses corresponding to the latter are recorded as non-operating expense, based on the balance

proportion of such assets.

Financial expenses related to operating assets less corresponding interest received, etc. are recorded as

financing costs.

7. The method of hedge accounting

Gains or losses on derivatives are deferred until maturity of the hedged items. For interest rate swap, the

Company applies the exceptional method as far as it qualifies for the required rules.

In respect of blanket hedging of liabilities as stipulated in “Temporary Accounting and Auditing Treatment in

the Application of the Accounting Standard for Financial Instruments in Leasing Business (Report No. 19

issued by the Industrial Auditing Committee of the Japanese Institute of Certified Public Accountants on

November 14, 2000)”, gains or losses thereon are deferred until maturity of the hedged items.

8. Translation of foreign currency accounts

All monetary receivables and payables denominated in foreign currencies are translated into Japanese yen at the

spot exchange rates on the balance sheet date, and the foreign exchange gains and losses therefrom are

recognized in the statement of income.

6

9. Other significant matters that serve as the basis for preparing financial statements

(1) Accounting treatment for consumption taxes

Consumption tax and local consumption tax are accounted for by the tax exclusion method.

(2) Amortization of goodwill

Goodwill is amortized over five years under the straight-line method.

(Change in Accounting Policies) Effective this fiscal year, the Company adopted the “Accounting Standard for Asset Retirement Obligations”

(Accounting Standards Board of Japan (ASBJ) Statement No. 18, issued on March 31, 2008) and the “Guidance

on Accounting Standard for Asset Retirement Obligations” (ASBJ Guidance No. 21, issued on March 31, 2008).

As a result, operating income and ordinary income decreased by ¥30 million, respectively, and income before

income taxes decreased by ¥213 million. (The Additional Information) Recording of allowance for doubtful receivables due to the effects of the Great East Japan Earthquake

In order to prepare for the risk of loan losses from operating receivables caused by the deteriorating financial

conditions of customers following the Great East Japan Earthquake, which struck on March 11, 2011, the

Company has recorded an allowance for doubtful receivables based on a reasonable estimate of the

uncollectible receivables.

7

(Notes to Balance Sheet) 1. Assets pledged as collateral and corresponding liabilities

(1) Assets pledged as collateral

(Millions of yen) Installment contract receivables 2,652 Lease receivables 374 Lease investment assets 34,459 Other loans receivables to customers 3,976 Property for lease and rent 44 Investment securities 9 Other investments 15 Total 41,530

(2) Liabilities corresponding to assets pledged as collateral

(Millions of yen) Current portion of long-term debt 97 Payables under securitized lease receivables 16,090 Long-term payables under securitized lease receivables 16,350 Other liabilities 531 Total 33,068

2. Accumulated depreciation of tangible assets

(Millions of yen) Property for lease and rent 22,803 Other tangible assets 1,283 Total 24,086

3. Contingent liabilities

Contingent liabilities for the subsidiaries’ borrowing liabilities etc. from financial institutions

(Millions of yen) Altair Lines S.A. 63,374 PT. Mitsui Leasing Capital Indonesia 23,389 JA MITSUI LEASING TATEMONO CO., LTD. 2,060 Mitsui Leasing Capital Corporation 1,725 Others 1,050 Total 91,599

4. Breakout of lease receivables and lease investment assets

(Millions of yen) Lease receivables Lease investment assets

Amount of receivables 108,630 525,899 Estimated residual value ─ 29,163 Amount equivalent to interest receivables 22,656 52,218 Total 85,974 502,844

8

5. Notes received as guarantees

(Millions of yen) Notes received for installment contract receivables 11,727 Notes received for lease receivables 20 Notes received for lease investment assets 4,133 Notes received for other loans receivables to customers 475

6. Operating lease contract receivables under the remaining lease terms

(Millions of yen) Notes received as guarantees 16 Other lease contract receivables 8,405 Total 8,422

7. Trade receivables due after one year

(Millions of yen) Installment contract receivables 85,484 Lease receivables 61,390 Lease investment assets 336,171 Loans receivables from customers 40,481 Other loans receivables from customers 37,154 Operating lease contract receivables under the remaining lease terms 5,459 Total 566,142

8. Receivables and payables with associated companies

(Millions of yen)

Short-term receivables 98,443

Long-term receivables 89,631

Short-term payables 61,853

Long-term payables 21,850

(Notes to Statement of Income) 1. Transactions with associated companies

(Millions of yen)

Amount of operating transactions

Revenues 3,307

Costs 772

Selling, general and administrative expenses 371

Amount of non-operating transactions 2,526

9

(Notes to Statement of Changes in Net Assets) 1. Number of issued and outstanding shares

Class of shares Number of shares at

the end of the previous fiscal year

Number of increased shares during the fiscal

year

Number of decreased shares during the fiscal

year

Number of shares at the end of the fiscal

year

Issued and outstanding shares

Ordinary shares 32,415,296 ─ ─ 32,415,296Class I classified shares 4,077,528 ─ ─ 4,077,528

Class II classified shares 33,448,582 ─ ─ 33,448,582

Class III classified shares 3,883,500 ─ ─ 3,883,500

Total 73,824,906 ─ ─ 73,824,906

(Notes to Income Taxes) Significant components of the Company’s deferred tax assets and liabilities

(Millions of yen) Deferred tax assets

Excess provision for allowance for doubtful receivables 13,184 Investment securities 1,289 Provision for employees’ retirement benefits 1,014 Investments in affiliated companies 907 Other 3,819 Subtotal 20,215 Less valuation allowance (5,409) Total deferred tax assets 14,805

Deferred tax liabilities Fair valuation difference of business combinations (914) Net unrealized gain on available-for-sale securities (770) Other (417) Total deferred tax liabilities (2,102)

Net deferred tax assets 12,702

(Notes to leased fixed assets) In addition to fixed assets stated in the balance sheet, the Company uses information equipments and vehicles

under lease contracts.

10

(Notes to Financial Instruments) 1. Matters relating to the status of financial instruments

(1) The Company’s policy in handling financial instruments The Company engages in its core business leasing and other financial service businesses including installment sales and loans to customers. To ensure constant financial liquidity to carry out these businesses, the Company raises funds by direct financing such as issuance of commercial paper and bonds as well as securitization of receivables, along with indirect financing including bank borrowing. Since the Company’s business involves holding of financial assets and liabilities exposed to interest rate volatility, it engages in derivative transactions as part of the comprehensive asset and liability management (ALM) in an effort to avoid unexpected losses due to the fluctuations of interest rate.

(2) Details of financial instruments and their risks Financial assets held by the Company are primarily lease investment assets, installment contract receivables and loans to customers involving domestic clientele, all of which are exposed to credit risk associated with the event of default by customers. Bank borrowing and issuance of commercial papers and bonds are all exposed to liquidity risk involving difficulty in ensuring the procurement of sufficient fund via normal fund raising activities in the event of significant dysfunction of the financial/capital market. Furthermore, borrowing at variable interest rate is exposed to interest rate risk, which, however, is partially avoided by interest rate swap transactions. Lease, installment sales and loans transactions denominated in foreign currencies are exposed to exchange risk, which, however, is mitigated by foreign currency denominated borrowing. One area of the derivative transactions engaged by the Company is interest rate swap transactions deployed as hedging instruments as part of ALM in which interest rate risk associated with the hedged borrowing is subject to hedge accounting. Under hedge accounting, the Company compares the cumulative changes in cash flows of the hedged items against those of the hedging instruments, during the period from the start of the hedging until the time to determine the its effectiveness. This comparison serves as the basis to evaluate the effectiveness of hedging.

(3) Risk management system for financial instruments ① Management of credit risks

In accordance with the internal rules for credit risk management, the Company has developed and maintains credit management system in respect of its trade receivables, including credit assessment and management of credit limits and credit data on case-by-case basis, internal credit rating, application of ceiling system to avoid credit concentration risk, arrangement of guarantee and security, and response to questionable receivables.

② Management of market risks The Company manages interest rate risk on the basis of the comprehensive management of its assets and liabilities (ALM). Details of the methods and procedures of the risk management are set out under the Company’s Risk Management Policies, while analysis of information on the financial market trend and identification/confirmation of interest rate risk position, along with discussion/approval on the future policies for handling this type of risk are carried out by the Integrated ALM Committee. Exchange risk is managed on case-by-case basis. Furthermore, as quantitative analysis of the interest rate risk, the Company calculates the amount of impact on profit and loss by simulating the reasonably expected moving range of interest rate risk after the year-end; and assuming that all risk variables other than interest rates remain the same, calculations indicate that income before income taxes for the following fiscal year will decrease by ¥3,028 million based on the scenario where the benchmark interest rate increases 100 basis points (1%) as of March 31, 2011.

11

③ Management of liquidity risks concerning financing The Company engages in liquidity management of company-wide fund via the ALM, along with other measures including the maintenance of adequate balance of cash and deposits, diversification of fund-raising methods, establishment of commitment lines from a number of financial institutions and optimum mix of short-term and long-term financing in consideration of the market environment.

12

2. Matters relating to the fair value of financial instruments

Balance sheet amounts, fair values, and the differences as of March 31, 2011 are as follows: (Millions of yen)

Balance sheet amount Fair value Difference (1) Installment contract receivables 110,526 115,471 4,945

Installment contract receivables (*1) 114,568 Allowance for doubtful receivables (*2) (4,041)

(2) Lease receivables 85,019 86,871 1,851Lease receivables 85,974 Allowance for doubtful receivables (*2) (954)

(3) Lease investment assets 466,662 481,809 15,147Lease investment assets 502,844 Estimated residual value (*3) (29,163) Allowance for doubtful receivables (*2) (7,019)

(4) Loans receivables to customers 51,328 55,639 4,310Loans receivables to customers 60,308 Allowance for doubtful receivables (*2) (8,979)

(5) Other loans receivables to customers 60,592 61,176 584Other loans receivables to customers 62,627 Allowance for doubtful receivables (*2) (2,035)

(6) Short and long-term loans receivables 179,012 180,081 1,068Short-term loans receivables 89,773 Long-term loans receivables 89,596 Allowance for doubtful receivables (*2) (357)

(7) Claims provable in bankruptcy, in rehabilitation and other 641 641 -

Claims provable in bankruptcy, in rehabilitation and other 4,895 Allowance for doubtful receivables (*2) (4,254)

Total assets 953,783 981,691 27,908(1) Short-term borrowings 50,975 50,975 -(2) Commercial papers 190,958 190,958 -(3) Payables under securitized lease receivables

(*4) 3,000 3,000 -(4) Bonds (*5) 4,003 4,003 -(5) Long-term debt (*6) 628,691 630,138 1,446(6) Long-term payables under securitized lease

receivables (*7) 32,440 32,650 210Total liabilities 910,069 911,727 1,657Derivative transactions (*8)

1) Derivative transactions to which hedge accounting is not applied 67 67 -

2) Derivative transactions to which hedge accounting is applied (1,376) (1,376) -

Total derivative transactions (1,309) (1,309) -(*1) Deferred unrealized gross profits on installment contracts have been deducted from installment contract

receivables. (*2) Corresponding allowance for doubtful receivables has been deducted. (*3) Estimated residual value included in lease investment assets has been deducted. (*4) Long-term payables under securitized lease receivables scheduled to be repaid within one year as included

in payables under securitized lease receivables have been deducted. (*5) Current portion of bonds is included. (*6) Current portion of long-term debt is included. (*7) Long-term payables under securitized lease receivables scheduled to be repaid within one year as included

in payables under securitized lease receivables are included also in long-term payables under securitized lease receivables.

(*8) Actual receivables and payables derived from derivative transactions are represented by net amounts. Net payables are presented in parentheses.

13

(Note 1) Matters relating to the calculation method of fair value of financial instruments and derivative

transactions

Assets

(1) Installment contract receivables, (2) Lease receivables, (3) Lease investment assets, (4) Loans receivables to

customers, (5) Other loans receivables to customers and (6) Short and long-term loans receivables

Financial instruments based on variable interest rate reflect market rate at shorter intervals, thus their book

value approximate their fair value unless credit standing of the customers involved therein changes

significantly. Hence they are stated at book values. Meanwhile, financial instruments based on fixed interest

rate are calculated by discounting the sum of principal and interest using the hypothetical interest rate

assumed applicable to the new borrowing on similar conditions, by type of receivable, by grade of internal

rating and by term basis. On the other hand, doubtful receivables are calculated based on the estimated

amount recoverable through repossession or guarantee, in which their balance sheet amount less estimated

bad debt at the closing date are proximate to their fair value, and thus are stated as such.

(7) Claims provable in bankruptcy, in rehabilitation and other

Receivables from businesses under bankruptcy or rehabilitation process are calculated based on the estimated

amount recoverable through repossession or guarantee, in which their balance sheet amount at the closing

date less the currently estimated bad debt are proximate to their fair value, and thus stated as such.

Liabilities

(1) Short-term borrowings and (2) Commercial papers

Since these are settled in a short period and their book value proximate to their fair value, they are stated at

book values.

(3) Bonds

As the bonds issued by the Company are based on variable interest rate, reflecting market rate at short

intervals, while the Company’s credit standing has not changed significantly since their issuance, their book

value is deemed proximate to their fair value, and thus are stated as such.

(4) Long-term debt and (5) Long-term payables under securitized lease receivables

Of the long-term debt, those based on variable interest rate reflecting market rate at short intervals with the

Company’s credit standing remaining without significant change since the borrowing, are stated at their book

value which is believed to approximate their fair value. Meanwhile, those based on fixed interest rate are

stated at their fair value calculated by discounting the sum of their principal and interest (*) for each of

certain time periods within the term, using the hypothetical interest rate assumed applicable to the borrowing

on similar conditions as at the end of each such time period.

(*) For long-term borrowings applicable to the exceptional method for interest rate swap transactions

(See “Derivative transactions. ②” below), the sum of their principal and interest (calculated by the

rate applicable to such interest rate swap transactions)

14

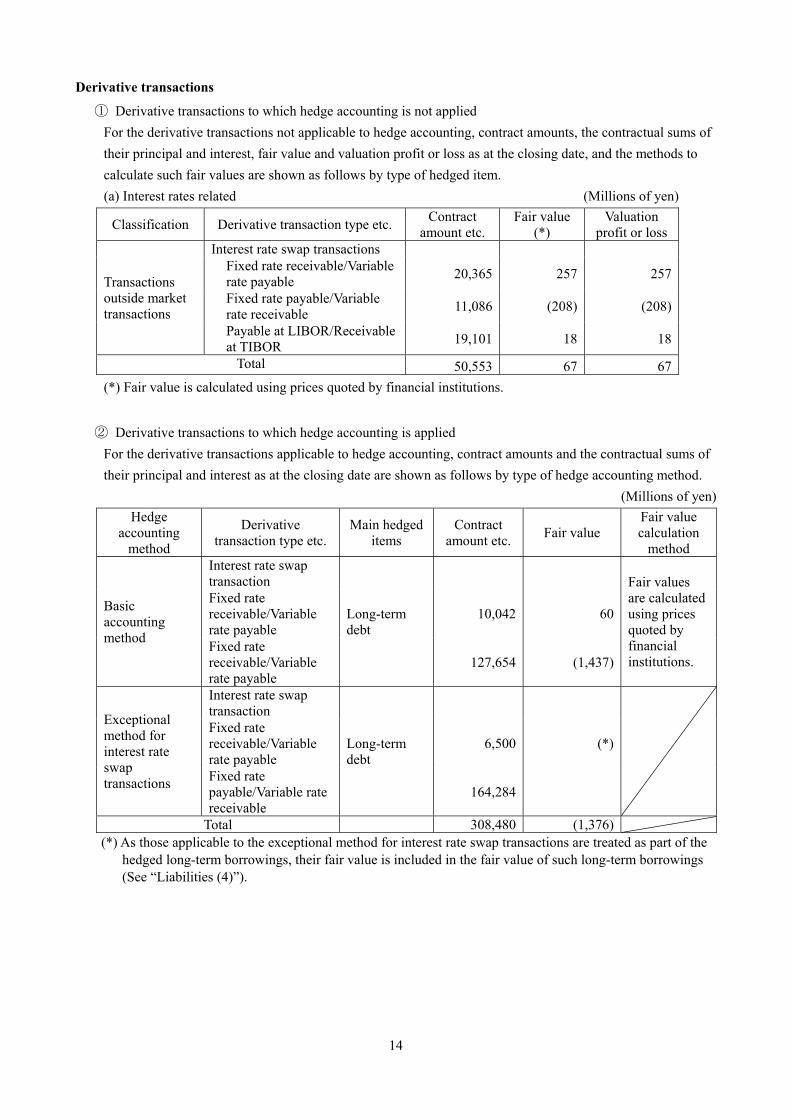

Derivative transactions

① Derivative transactions to which hedge accounting is not applied For the derivative transactions not applicable to hedge accounting, contract amounts, the contractual sums of their principal and interest, fair value and valuation profit or loss as at the closing date, and the methods to calculate such fair values are shown as follows by type of hedged item. (a) Interest rates related (Millions of yen)

Classification Derivative transaction type etc. Contract amount etc.

Fair value (*)

Valuation profit or loss

Transactions outside market transactions

Interest rate swap transactions Fixed rate receivable/Variable rate payable 20,365 257 257

Fixed rate payable/Variable rate receivable 11,086 (208) (208)

Payable at LIBOR/Receivable at TIBOR 19,101 18 18

Total 50,553 67 67(*) Fair value is calculated using prices quoted by financial institutions.

② Derivative transactions to which hedge accounting is applied

For the derivative transactions applicable to hedge accounting, contract amounts and the contractual sums of their principal and interest as at the closing date are shown as follows by type of hedge accounting method.

(Millions of yen) Hedge

accounting method

Derivative transaction type etc.

Main hedged items

Contract amount etc. Fair value

Fair value calculation

method

Basic accounting method

Interest rate swap transaction

Long-term debt

Fair values are calculated using prices quoted by financial institutions.

Fixed rate receivable/Variable rate payable

10,042 60

Fixed rate receivable/Variable rate payable

127,654 (1,437)

Exceptional method for interest rate swap transactions

Interest rate swap transaction

Long-term debt

Fixed rate receivable/Variable rate payable

6,500 (*)

Fixed rate payable/Variable rate receivable

164,284

Total 308,480 (1,376) (*) As those applicable to the exceptional method for interest rate swap transactions are treated as part of the

hedged long-term borrowings, their fair value is included in the fair value of such long-term borrowings (See “Liabilities (4)”).

15

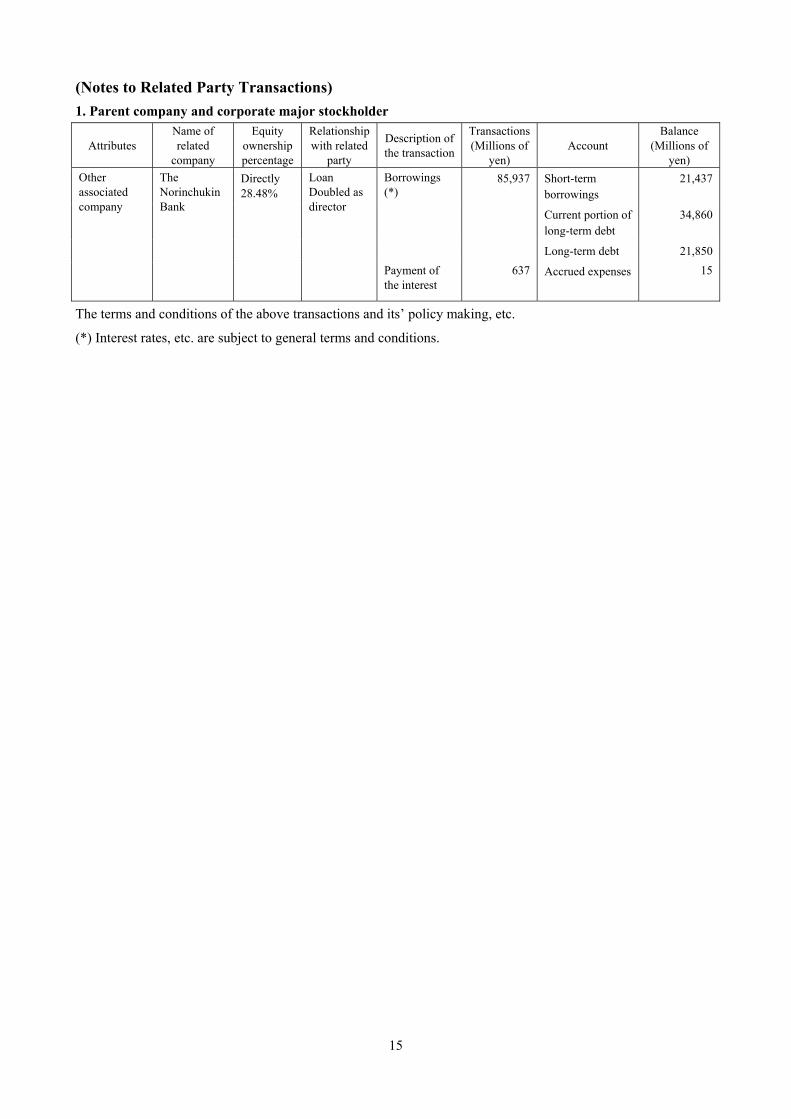

(Notes to Related Party Transactions) 1. Parent company and corporate major stockholder

Attributes Name of related

company

Equity ownership percentage

Relationship with related

party

Description of the transaction

Transactions(Millions of

yen) Account

Balance (Millions of

yen) Other associated company

The Norinchukin Bank

Directly 28.48%

Loan Doubled as director

Borrowings (*)

85,937

Short-term borrowings

21,437

Current portion of long-term debt

34,860

Long-term debt 21,850Payment of the interest

637 Accrued expenses

15

The terms and conditions of the above transactions and its’ policy making, etc.

(*) Interest rates, etc. are subject to general terms and conditions.

16

2. Affiliates, etc.

Attributes Name of related

company

Equity ownership percentage

Relationship with related

party

Description of the transaction

Transactions(Millions of

yen) Account

Balance (Millions of

yen) Subsidiary JA Mitsui

Leasing Auto, Ltd.

Directly 100%

Loan Doubled as director

Loan (*1) 178,180

Short-term loans receivables

23,670

Long-term loans receivables

7,330

Receipt of the interest

350 Accrued income 11

Subsidiary Nishi-Nippon Sogo Lease Co., Ltd.

Directly 85.10%

Loan Doubled as director

Loan (*1) 174,600 Short-term loans receivables

16,966

Long-term loans receivables

6,001

Receipt of the interest

158 Accrued income 29

Subsidiary Altair Lines S.A.

Directly 100%

Loan

Loan (*1) 48,502 Short-term loans receivables

8,902

Long-term loans receivables

44,787

Receipt of the interest

586 Accrued income 27

Guarantee of liability

Guarantee of liabilities (*2)

63,374 ─ ─

Receipt of the guarantee fee

99 Accrued income 44

Subsidiary Michinoku Lease Co., Ltd.

Directly 95.00%

Loan Doubled as director

Loan (*1) 141,705 Short-term loans receivables

10,655

Receipt of the interest

87 Accrued income 1

Subsidiary Kinki Sogo Leasing Co., Ltd.

Directly 94.04%

Loan Doubled as director

Loan (*1)

76,250 Short-term loans receivables

6,648

Long-term loans receivables

3,869

Receipt of the interest

66 Accrued income 17

Subsidiary Unite Co., Ltd.

Directly 77.77%

Loan Doubled as director

Loan (*1)

26,950 Short-term loans receivables

2,150

Long-term loans receivables

2,500

Receipt of the interest

59 ─ ─

Subsidiary Mitsui CM Leasing, Ltd.

Directly 100%

Loan Doubled as director

Loan (*1) 44,601 Short-term loans receivables

5,950

Receipt of the interest

15 ─ ─

Subsidiary JA MITSUI LEASING TATEMONO CO., LTD.

Directly 100%

Loan Doubled as director

Loan (*1)

25,700 Short-term loans receivables

13,700

Long-term loans receivables

24,000

Receipt of the interest

495 Accrued income 11

Subsidiary PT. Mitsui Leasing Capital Indonesia

Directly 85.00% Indirectly 14.99%

Guarantee of liability Doubled as director

Guarantee of liabilities (*2)

23,389 ─ ─

Receipt of the guarantee fee

27 Accrued income 8

The terms and conditions of the above transactions and its’ policy making, etc.

17

(*1) The terms and conditions of the loans are on an arm’s-length basis. No collateral is received from the

borrower.

(*2) The guarantees of liabilities are for borrowings from financial institutions.

18

(Notes to Per Share Information) 1. Net assets per share of ordinary shares ¥1,951.86

2. Net income per share of ordinary shares ¥209.66

(Notes to Impairment Loss) Impairment loss has been recorded on the following assets for this fiscal year.

Name and location Usage Type Impairment loss amounts

Kashiwa dormitory (Kashiwa-City, Chiba Prefecture) Company housing Land and building, etc. ¥509 million

Urawa dormitory (Saitama-City, Saitama Prefecture) Company housing Land and building, etc. ¥248 million

Although the Company had previously grouped company dormitories into common assets, upon determining the

policy of disposal by sale, it has decreased the book value of the fixed assets to the recoverable amount and

recorded said amount of decrease as an impairment loss under special losses. The recoverable amount has been

measured on the basis of the net selling price, which was calculated by a real estate appraiser based on the real

estate appraisal standard. (Notes to Asset Retirement Obligations) Asset retirement obligations recorded in the balance sheet

a. Outline of the relevant asset retirement obligations

Asset retirement obligations are recorded where restoration is required in the lease contract for the Head

Office and the fixed-term land leasehold contracts of a portion of the Company’s business assets.

b. Calculation method for the amount of the relevant asset retirement obligations

In calculating the amount of asset retirement obligations recorded under liabilities, the estimated period of

use of 15 to 20 years has been assumed, and the JGB distribution yield corresponding to the estimated

period of use has been used as the discount rate (mainly 2.16%).

c. Increase or decrease of relevant asset retirement obligations during this fiscal year

Balance at beginning of year (Note) ¥438 million

Reconciliation associated with passage of time ¥9 million

Balance at end of year ¥447 million

(Note) This balance at the beginning of year is a result of the adoption of the “Accounting Standard for Asset

Retirement Obligations” (ASBJ Statement No.18, issued on March 31, 2008) and the “Guidance on

Accounting Standard for Asset Retirement Obligations” (ASBJ Guidance No.21, issued on March 31,

2008), effective this fiscal year.

19

(Translation)

Audit Report by the Board of Corporate Auditors Certified Copy

Audit Report

The board of corporate auditors, following deliberations on the reports made by each corporate auditor concerning the audit of performance of duties by directors of the Company for the 3rd fiscal year from April 1, 2010 to March 31, 2011, has prepared this Audit Report, and hereby reports as follows: 1. Auditing Method Used by Each Corporate Auditor and the Board of Corporate Auditors and Details Thereof

The board of corporate auditors established auditing policies, assignment of duties and other relevant matters, and received reports from each corporate auditor regarding the progress and results of audits, as well as received reports from the directors, other relevant personnel and the independent auditors regarding the performance of their duties, and sought explanations as necessary.

In conformity with the corporate auditors’ auditing standard policies established by the board of corporate auditors, and in accordance with the auditing policies, assignment of duties and other relevant matters, each corporate auditor endeavored to gather information and to create an improved environment for auditing through close communication with the directors, employees including those working in the Internal Audit Department and other relevant personnel. Each corporate auditor also attended meetings of the board of directors and other important meetings, received reports from the directors, employees and other relevant personnel regarding the performance of their duties, sought explanations as necessary, inspected documents involving important resolutions, and examined the operations and financial position of the Company at the Head Office and other principal offices of the Company. Also, each corporate auditor monitored and verified the content and the status of the resolution of the board of directors to establish the systems provided by Article 100, Section 1 and 3 of the Ordinance for Enforcement of the Companies Act and the systems established pursuant to such resolution (the “Internal Control System”), which are necessary to establish the systems to ensure directors carry out their duties described in the business report in accordance with laws and regulations and the Company’s Articles of Incorporation and other systems to ensure appropriateness of the Company’s business.

As for the subsidiaries of the Company, each corporate auditor endeavored to keep communication and shared information with the directors, corporate auditors and other related personnel of the subsidiaries, and received reports from the subsidiaries regarding their businesses as necessary.

Based on the foregoing method, the corporate auditors examined the business report for the fiscal year. Furthermore, the corporate auditors monitored and verified whether the independent auditors maintained its

independence and implemented appropriate audits, as well as received reports from the independent auditors regarding the performance of its duties and sought explanations as necessary. Each corporate auditor was notified by the independent auditors that it has established a “system to ensure that duties of independent auditors are being conducted properly” (matters prescribed in each item of Article 131 of the Corporate Accounting Regulations) and that the system is developed and implemented in accordance with the “Quality Control Standards for Audit” (Business Accounting Council, October 28, 2005) and other applicable standards, and sought explanation as necessary.

Based on the foregoing method, the corporate auditors reviewed the financial statements for the fiscal year (balance sheet, statement of operations, statement of changes in net assets and the related notes) and supplementary schedules thereto.

20

2. Audit Results (1) Audit Results on the Business Report, etc. 1) In our opinion, the business report fairly represents the Company’s condition in conformity with the applicable

laws and regulations as well as the Articles of Incorporation of the Company. 2) We have found no evidence of misconduct or material facts in violation of the applicable laws and regulations,

nor of any violation with respect to the Articles of Incorporation of the Company, related to performance of duties by the directors.

3) In our opinion, the status of the operation and maintenance of the Internal Control System is appropriate. We have found no issues to be mentioned on the contents of the business report and the directors’ performance of their duties with respect to the Internal Control System.

(2) Results of Audit of the Financial Statements and Supplementary Schedules

In our opinion, the method and the results of the audit used and conducted by Deloitte Touche Tohmatsu LLC, the independent auditors are appropriate.

May 25, 2011 The board of corporate auditors of JA Mitsui Leasing, Ltd.

Standing corporate auditor Takuo Shirakawa (Seal) Standing corporate auditor Hideyuki Nebashi (Seal) Standing corporate auditor Akihiko Onozawa (Seal) Corporate auditor Katsuhisa Kiyozuka (Seal)

(Note) Takuo Shirakawa and Hideyuki Nebashi, standing corporate auditors, and Katsuhisa Kiyozuka, corporate

auditor, are the outside corporate auditors as set forth in Article 2, Item 16 and Article 335, Section 3 of the Companies Act.

(TRANSLATION)

INDEPENDENT AUDITORS' REPORT

May 19, 2011

To the Board of Directors of JA MITSUI LEASING, Ltd.:

Deloitte Touche Tohmatsu LLC

Designated Unlimited Liability Partner,Engagement Partner,Certified Public Accountant:

Tomomitsu Umezu

Designated Unlimited Liability Partner,Engagement Partner,Certified Public Accountant:

Yasunori Kusaka

Designated Unlimited Liability Partner, Engagement Partner, Certified Public Accountant:

Haruhiko Ohno

Pursuant to the first item, second paragraph of Article 436 of the Companies Act, we have audited the financial statements, namely, the balance sheet as of March 31, 2011 of JA MITSUI LEASING, Ltd.(the ”Company”), and the related statements of operations and changes in net assets, and the related notes for the 3rd fiscal year from April 1, 2010 to March 31, 2011, and the accompanying supplemental schedules . These financial statements and the accompanying supplemental schedules are the responsibility of the Company's management. Our responsibility is to express an opinion on these financial statements and the accompanying supplemental schedules based on our audit.

We conducted our audit in accordance with auditing standards generally accepted in Japan. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and the accompanying supplemental schedules are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and the accompanying supplemental schedules. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statements and the accompanying supplemental schedules presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements and the accompanying supplemental schedules referred to above present fairly, in all material respects, the financial position of the Company as of March 31, 2011, and the results of its operations for the year then ended in conformity with accounting principles generally accepted

in Japan.

Our firm and the engagement partners do not have any financial interest in the Company for which disclosure is required under the provisions of the Certified Public Accountants Act.

The above represents a translation, for convenience only, of the original report issued in the Japanese language and "the accompanying supplemental schedules" referred to in this report are not included in the attached financial documents.