balance sheet considerations - elliott davis · balance sheet considerations obtaining favorable...

TRANSCRIPT

Balance Sheet Considerations

Obtaining Favorable Current Yield Mixed With the Potential for Future

Higher Interest Rates (Ugh!)

December 16, 2008 3.25 (The Current U.S. Prime Rate)

October 29, 2014: The FOMC has voted to keep the target range

for the fed funds rate at 0% - 0.25%. Therefore, the U.S. Prime Rate will continue at 3.25%. The next FOMC meeting

and decision on short-term rates will be on December 17TH, 2014.

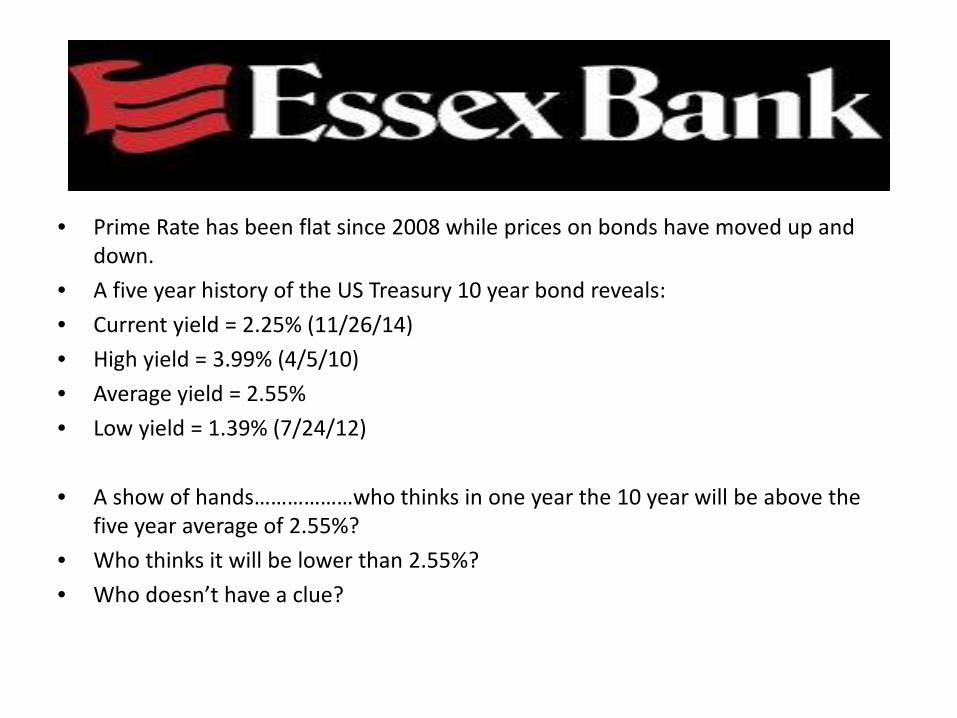

• Prime Rate has been flat since 2008 while prices on bonds have moved up and down.

• A five year history of the US Treasury 10 year bond reveals: • Current yield = 2.25% (11/26/14) • High yield = 3.99% (4/5/10) • Average yield = 2.55% • Low yield = 1.39% (7/24/12)

• A show of hands………………who thinks in one year the 10 year will be above the

five year average of 2.55%? • Who thinks it will be lower than 2.55%? • Who doesn’t have a clue?

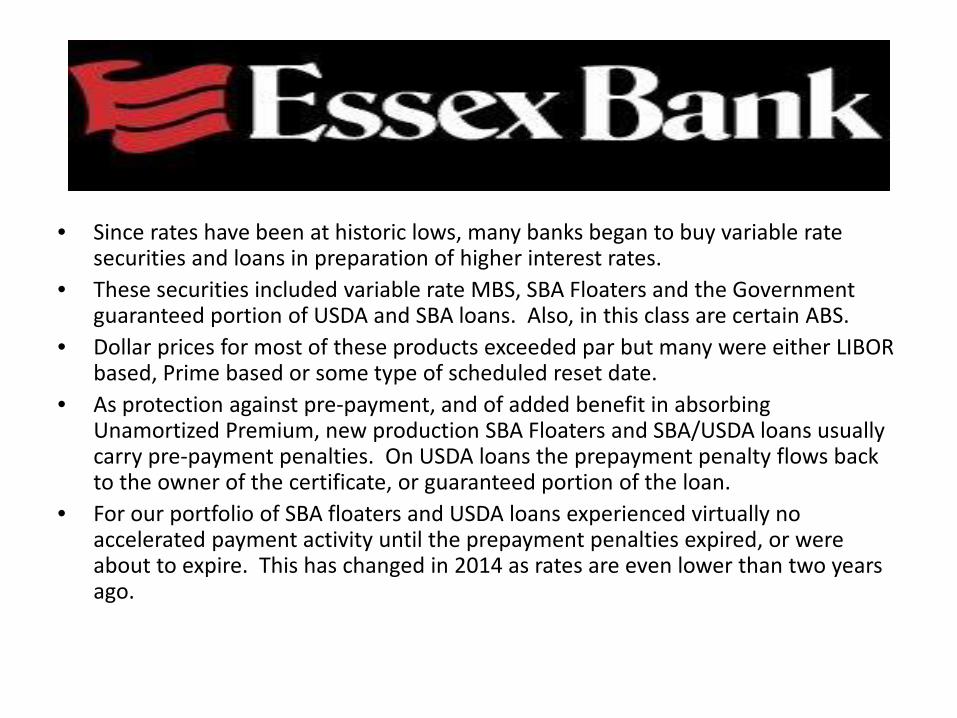

• Since rates have been at historic lows, many banks began to buy variable rate securities and loans in preparation of higher interest rates.

• These securities included variable rate MBS, SBA Floaters and the Government guaranteed portion of USDA and SBA loans. Also, in this class are certain ABS.

• Dollar prices for most of these products exceeded par but many were either LIBOR based, Prime based or some type of scheduled reset date.

• As protection against pre-payment, and of added benefit in absorbing Unamortized Premium, new production SBA Floaters and SBA/USDA loans usually carry pre-payment penalties. On USDA loans the prepayment penalty flows back to the owner of the certificate, or guaranteed portion of the loan.

• For our portfolio of SBA floaters and USDA loans experienced virtually no accelerated payment activity until the prepayment penalties expired, or were about to expire. This has changed in 2014 as rates are even lower than two years ago.

• Bottom line – amortizing product (loan or security) that is purchased above par needs to be monitored on an individual Cusip basis.

• Examine 1 month, 3 month, 12 month and life CPR. Examine the book price, coupon, whether or not the prepayment penalties are in place, number of loans in the pool and where rates and spreads are in relation to when you purchased the product.

• In many cases being proactive will result in a gain on sale and an attractive reinvestment without appreciable extension and may be better than eating premium.

• Conundrum – Prime rate has been unchanged for six years. The 10 year UST is trading near the five year average. Amortizing product with any yield at purchase was purchased above par, prepayment incentive is now gone on seasoned product and could be refinanced by the borrower at a better rate, exposing you to unamortized premium risk.

• Do we sell and put new production on? Are we sure rates are going up? How do we insulate for higher rates and get some yield today. Variable rate new production is in demand and yields are worse than three years ago.

• September 28, 2014 - Financial Times reporting on the 16th annual Geneva Report predicts interest rates across the world will have to stay low for a “very, very long” time to enable households, companies and governments to service their debts and avoid another crash.

• The report documents the continued rapid rise of public sector debt in rich countries and private debt in emerging markets, especially China.

• It warns of a “Poisonous combination of high and rising global debt and slowing nominal GDP driven by both slowing real growth and falling inflation.”

• The total burden of world debt, private and public, has risen from160 per cent of national income in 2001 to almost 200 percent after the crisis struck in 2009 and 215 percent in 2013.

• The report’s authors expect interest rates to stay lower than market expectations because the rise in debt means that borrowers would be unable to withstand faster rate rises.

• The authors worry that since asset prices have risen alongside the growth in debt, so balance sheets don’t look stretched, asset prices may see a reversal, causing a credit squeeze.

• Recent actions on our balance sheet have included proactively monitoring and when prudent, selling USDA loans (to fund core loan growth) and SBA Floaters that have been faster payers.

• The SBA proceeds have been redeployed into longer term (10 – 15 years) Municipal securities (of the Tax-Exempt Bank Qualified variety) at yields that average around 4.50%.

• To avoid the OCI mark in higher rates we have placed most of these in the Held-to-Maturity designation.

• So what about higher rates? If you are replacing variable rate product with fixed rate product wouldn’t you feel comfortable with some type of hedge?

• Yes. Therefore we just entered into an interest rate swap to hedge the roll over of short-term fixed rate FHLB advances for a 5 year period.

• $ 30 million 5 year swap where bank pays fixed rate of 1.69% and receives 3 month LIBOR, which will reset on a quarterly basis.

• We will roll the 3 month advance every quarter on the same day that 3 month LIBOR resets on the floating leg of the swap. The receive floating leg will cancel out with the pay fixed rate on the 3 month advance, effectively fixing the rate on the funding at 1.69%.

• Because the swap is designated as a cash flow hedge, its quarterly market value changes get booked in OCI. The potential increases in swap market value, in a rising rate environment, should partially protect book value against securities unrealized losses booked into OCI.

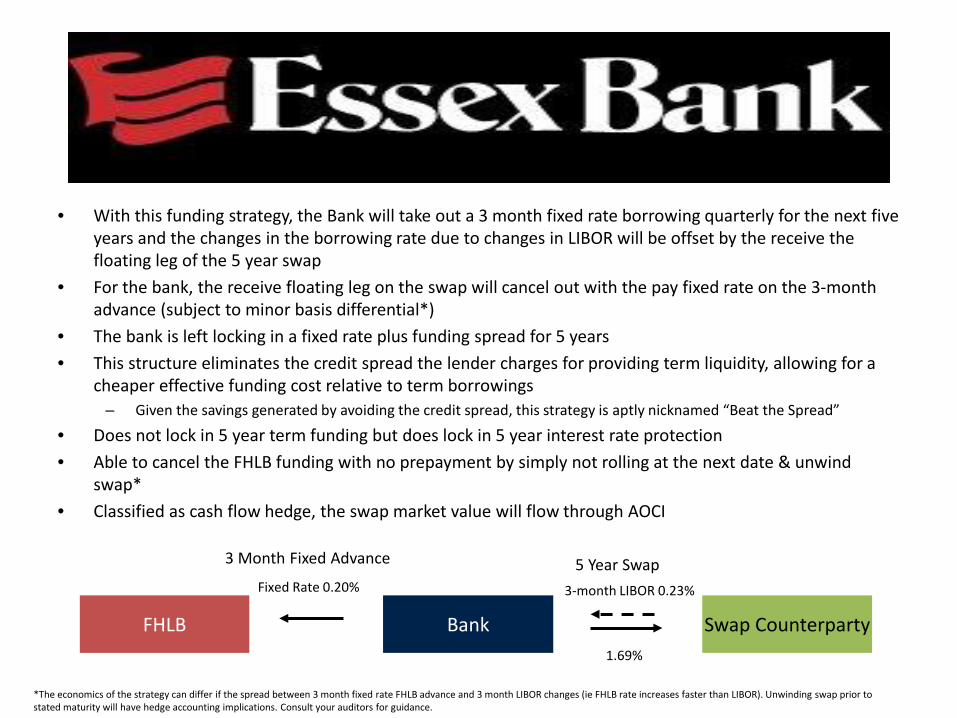

• With this funding strategy, the Bank will take out a 3 month fixed rate borrowing quarterly for the next five years and the changes in the borrowing rate due to changes in LIBOR will be offset by the receive the floating leg of the 5 year swap

• For the bank, the receive floating leg on the swap will cancel out with the pay fixed rate on the 3-month advance (subject to minor basis differential*)

• The bank is left locking in a fixed rate plus funding spread for 5 years • This structure eliminates the credit spread the lender charges for providing term liquidity, allowing for a

cheaper effective funding cost relative to term borrowings – Given the savings generated by avoiding the credit spread, this strategy is aptly nicknamed “Beat the Spread”

• Does not lock in 5 year term funding but does lock in 5 year interest rate protection • Able to cancel the FHLB funding with no prepayment by simply not rolling at the next date & unwind

swap* • Classified as cash flow hedge, the swap market value will flow through AOCI

*The economics of the strategy can differ if the spread between 3 month fixed rate FHLB advance and 3 month LIBOR changes (ie FHLB rate increases faster than LIBOR). Unwinding swap prior to stated maturity will have hedge accounting implications. Consult your auditors for guidance.

FHLB Bank Swap Counterparty

3 Month Fixed Advance 5 Year Swap Fixed Rate 0.20%

1.69%

3-month LIBOR 0.23%