balance sheet

DESCRIPTION

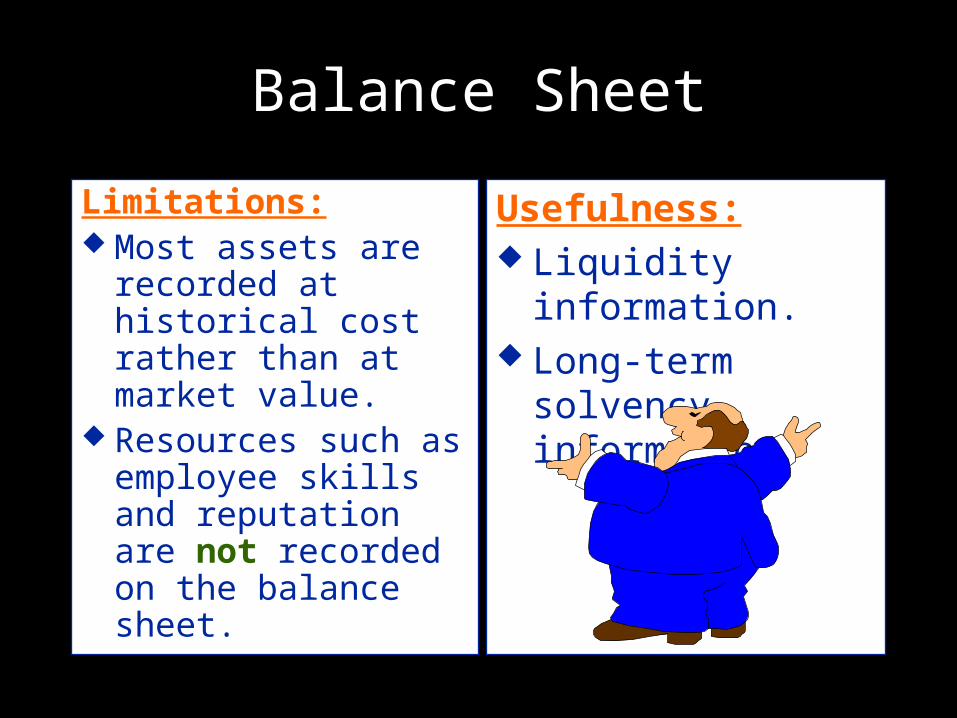

Limitations: Most assets are recorded at historical cost rather than at market value. Resources such as employee skills and reputation are not recorded on the balance sheet. Usefulness: Liquidity information. Long-term solvency information. Balance Sheet. Case 3-5. - PowerPoint PPT PresentationTRANSCRIPT

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

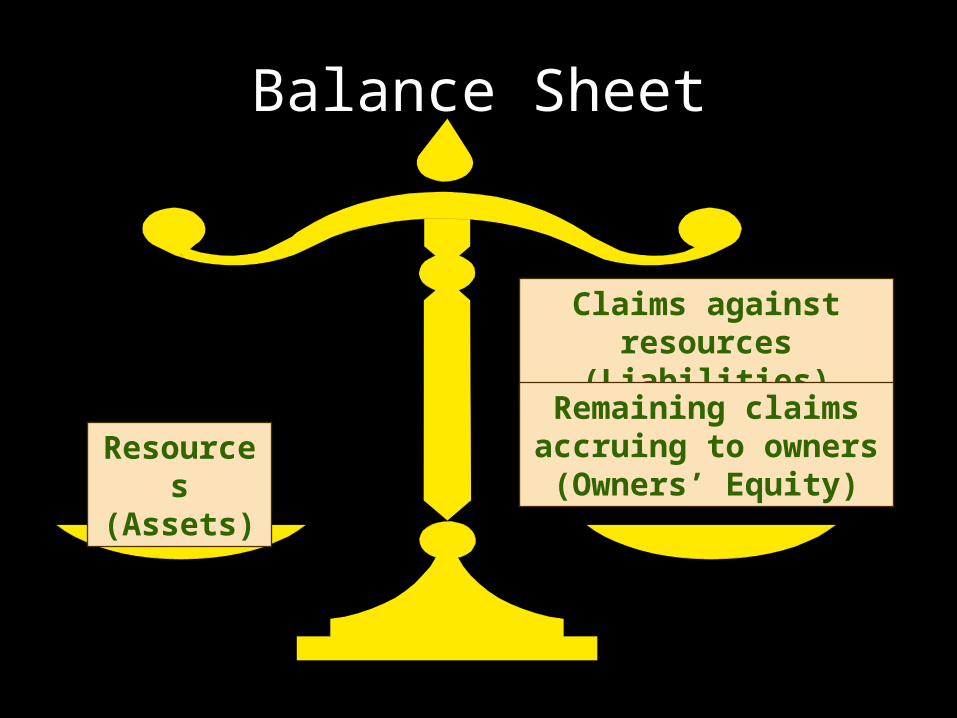

Balance Sheet

Limitations: Most assets are

recorded at historical cost rather than at market value.

Resources such as employee skills and reputation are not recorded on the balance sheet.

Usefulness: Liquidity information. Long-term solvency

information.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Case 3-5

Which items require further disclosure?

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Resources (Assets)

Claims against resources (Liabilities)

Remaining claims accruing to owners

(Owners’ Equity)

Balance Sheet

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

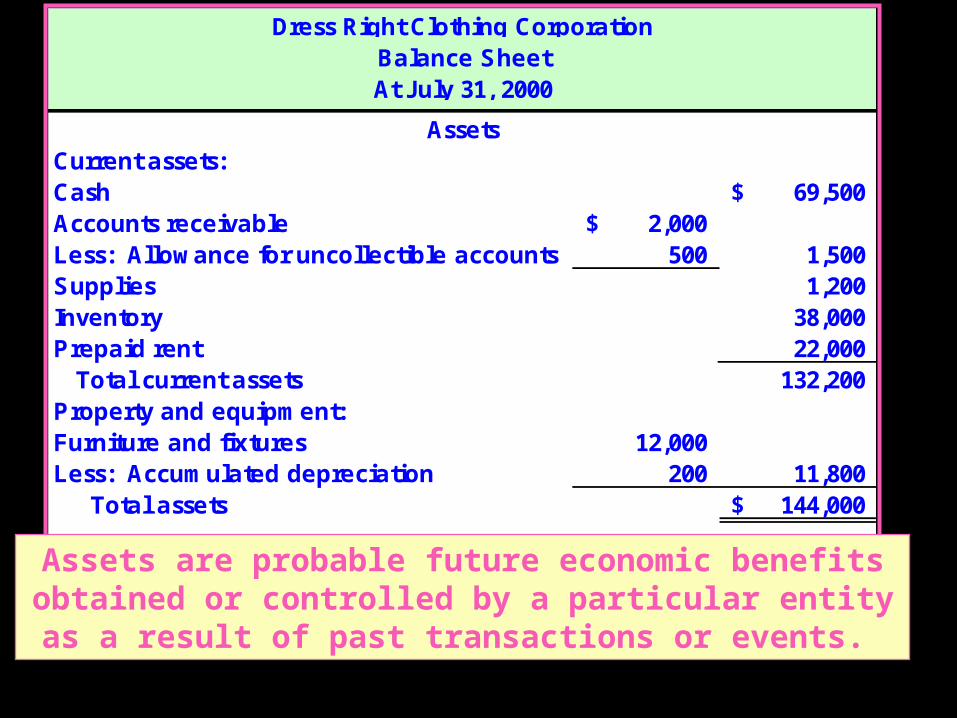

Current assets:Cash 69,500$ Accounts receivable 2,000$ Less: Allowance for uncollectible accounts 500 1,500 Supplies 1,200 Inventory 38,000 Prepaid rent 22,000 Total current assets 132,200 Property and equipment:Furniture and fixtures 12,000 Less: Accumulated depreciation 200 11,800 Total assets 144,000$

Dress Right Clothing CorporationBalance SheetAt July 31, 2000

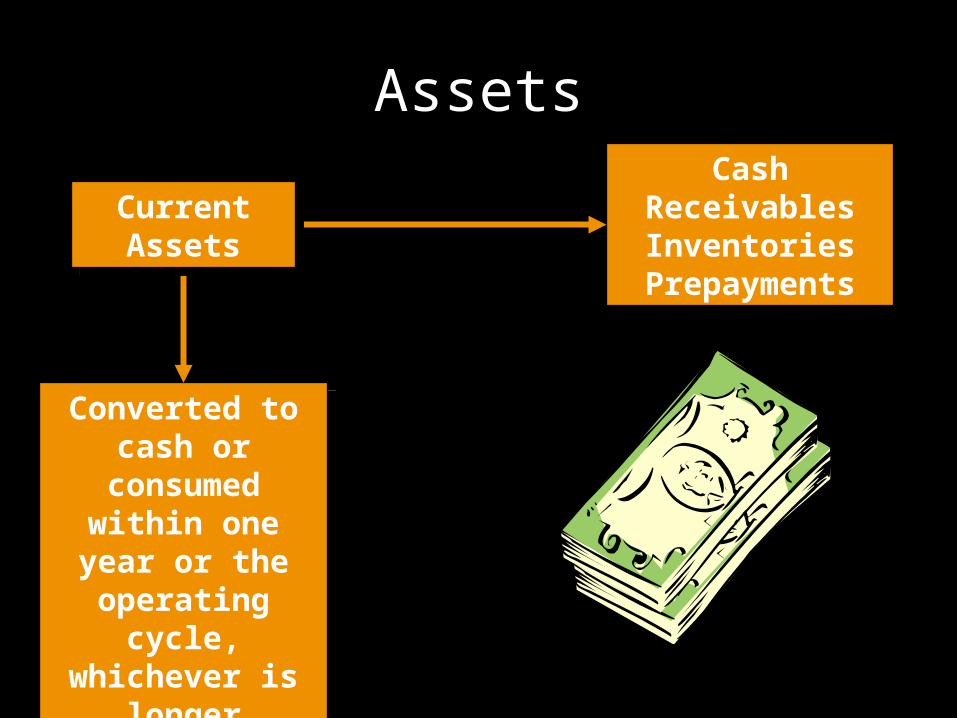

Assets

Assets are probable future economic benefits obtained or controlled by a particular entity as a result of past

transactions or events.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

AssetsCash

ReceivablesInventories

Prepayments

CashReceivablesInventories

Prepayments

Converted to cash or

consumed within one year or the operating cycle,

whichever is longer

Converted to cash or

consumed within one year or the operating cycle,

whichever is longer

Current Assets

Current Assets

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

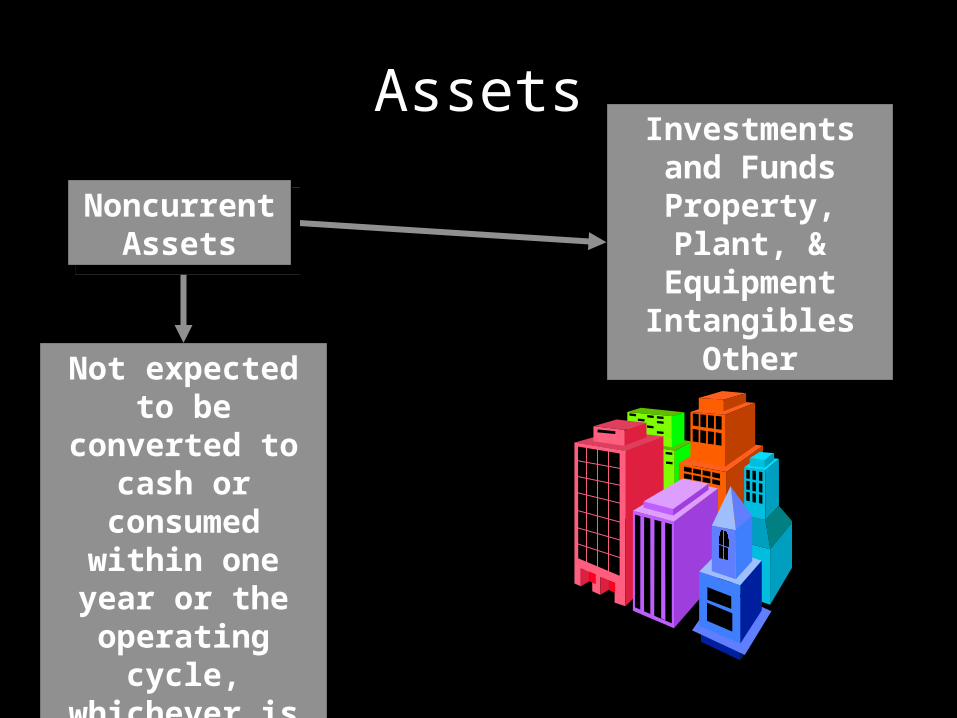

AssetsInvestments and

FundsProperty, Plant, &

EquipmentIntangibles

Other

Investments and Funds

Property, Plant, & EquipmentIntangibles

Other

Not expected to be converted to

cash or consumed within one year or the operating cycle,

whichever is longer

Not expected to be converted to

cash or consumed within one year or the operating cycle,

whichever is longer

Noncurrent Assets

Noncurrent Assets

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

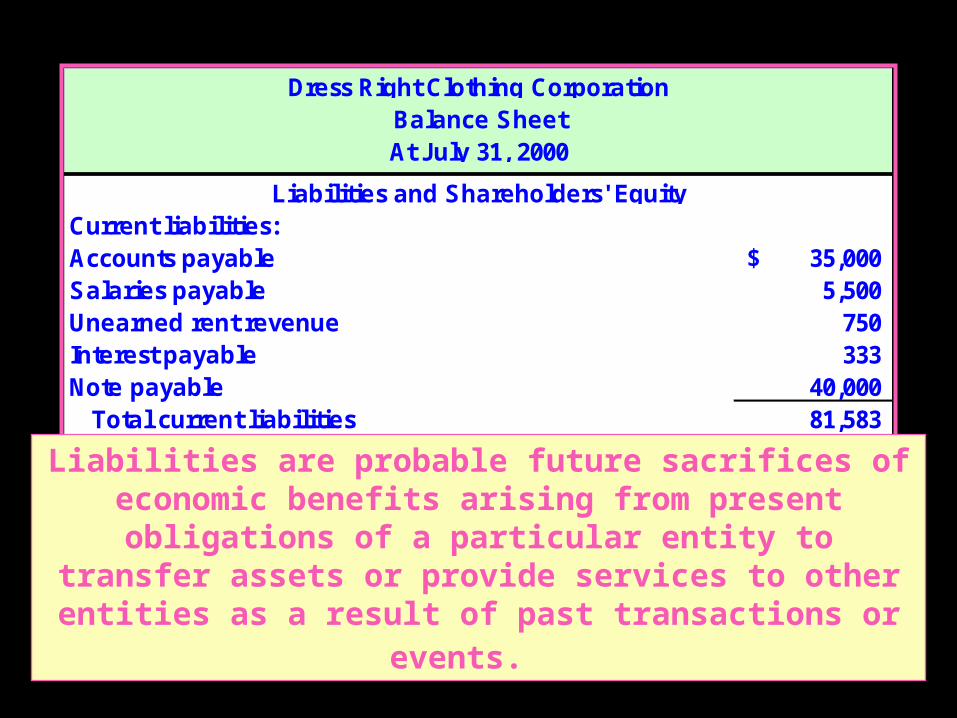

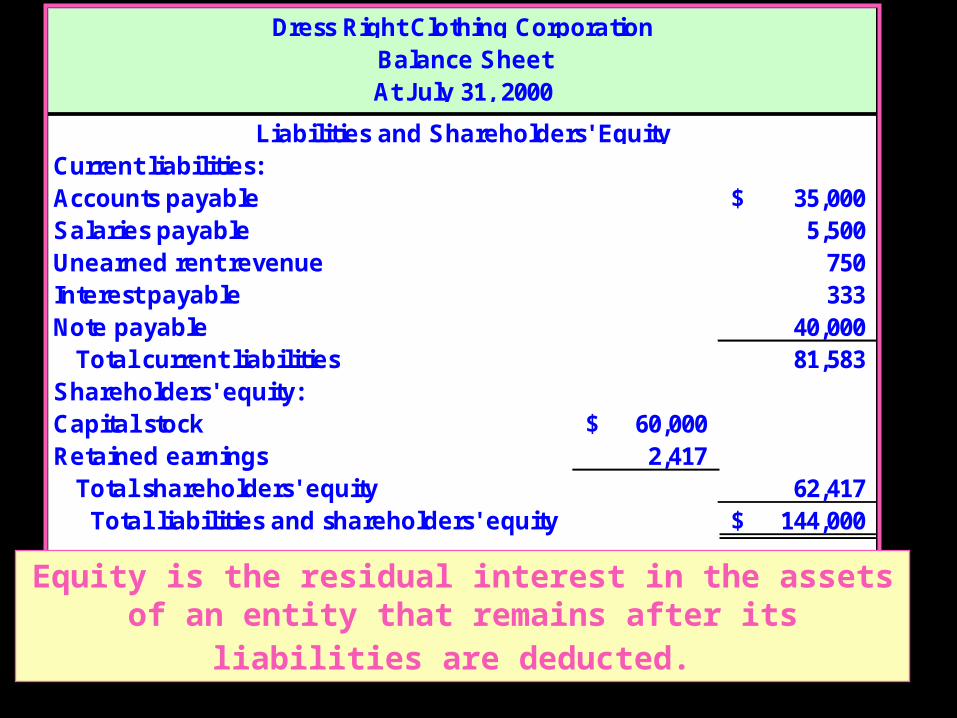

Current liabilities:Accounts payable 35,000$ Salaries payable 5,500 Unearned rent revenue 750 Interest payable 333 Note payable 40,000 Total current liabilities 81,583 Shareholders' equity:Capital stock 60,000$ Retained earnings 2,417 Total shareholders' equity 62,417 Total liabilities and shareholders' equity 144,000$

Dress Right Clothing CorporationBalance SheetAt July 31, 2000

Liabilities and Shareholders' Equity

Liabilities are probable future sacrifices of economic benefits arising from present obligations of a particular

entity to transfer assets or provide services to other entities as a result of past transactions or events.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

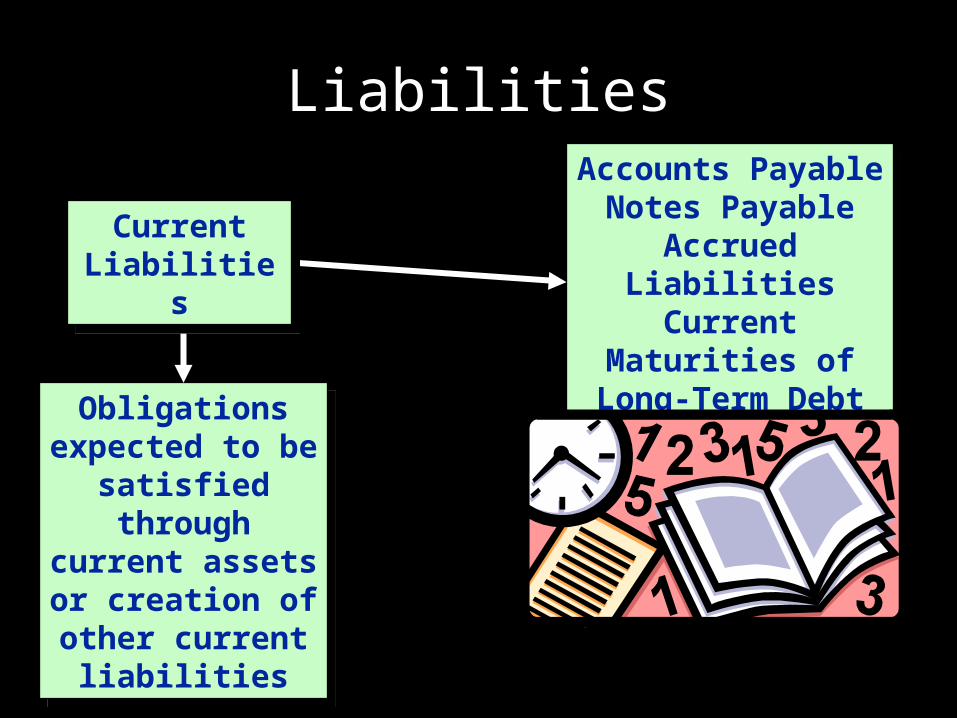

LiabilitiesAccounts Payable

Notes PayableAccrued LiabilitiesCurrent Maturities of Long-Term Debt

Accounts PayableNotes Payable

Accrued LiabilitiesCurrent Maturities of Long-Term Debt

Obligations expected to be

satisfied through current assets or creation of other current liabilities

Obligations expected to be

satisfied through current assets or creation of other current liabilities

Current Liabilities

Current Liabilities

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

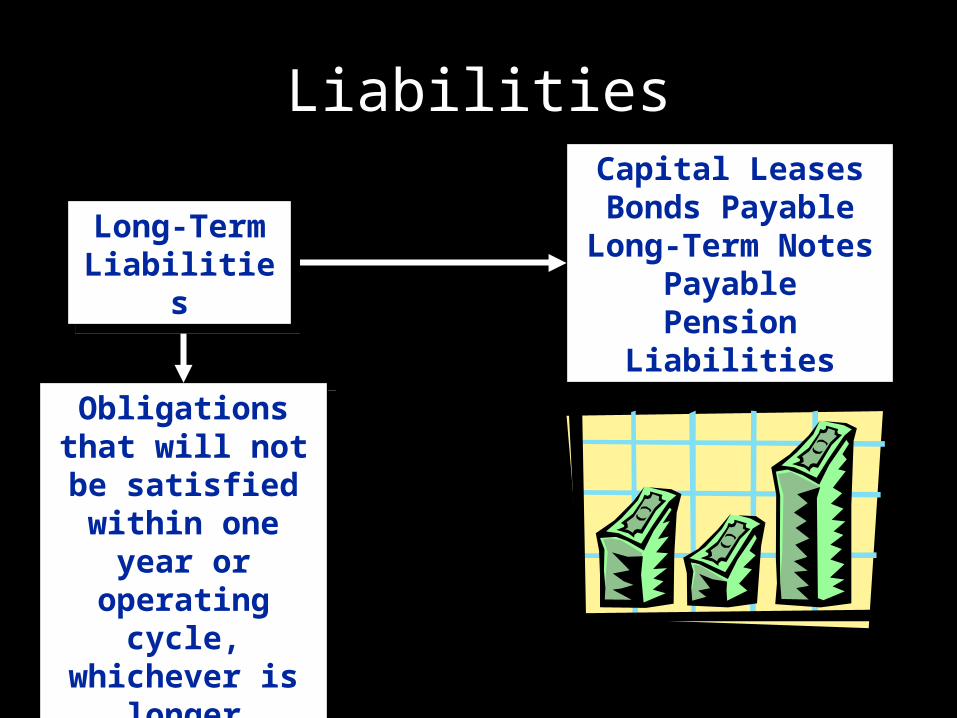

LiabilitiesCapital LeasesBonds Payable

Long-Term Notes Payable

Pension Liabilities

Capital LeasesBonds Payable

Long-Term Notes Payable

Pension Liabilities

Obligations that will not be

satisfied within one year or

operating cycle, whichever is

longer

Obligations that will not be

satisfied within one year or

operating cycle, whichever is

longer

Long-Term Liabilities

Long-Term Liabilities

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Current liabilities:Accounts payable 35,000$ Salaries payable 5,500 Unearned rent revenue 750 Interest payable 333 Note payable 40,000 Total current liabilities 81,583 Shareholders' equity:Capital stock 60,000$ Retained earnings 2,417 Total shareholders' equity 62,417 Total liabilities and shareholders' equity 144,000$

Dress Right Clothing CorporationBalance SheetAt July 31, 2000

Liabilities and Shareholders' Equity

Equity is the residual interest in the assets of an entity that remains after its liabilities are deducted.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

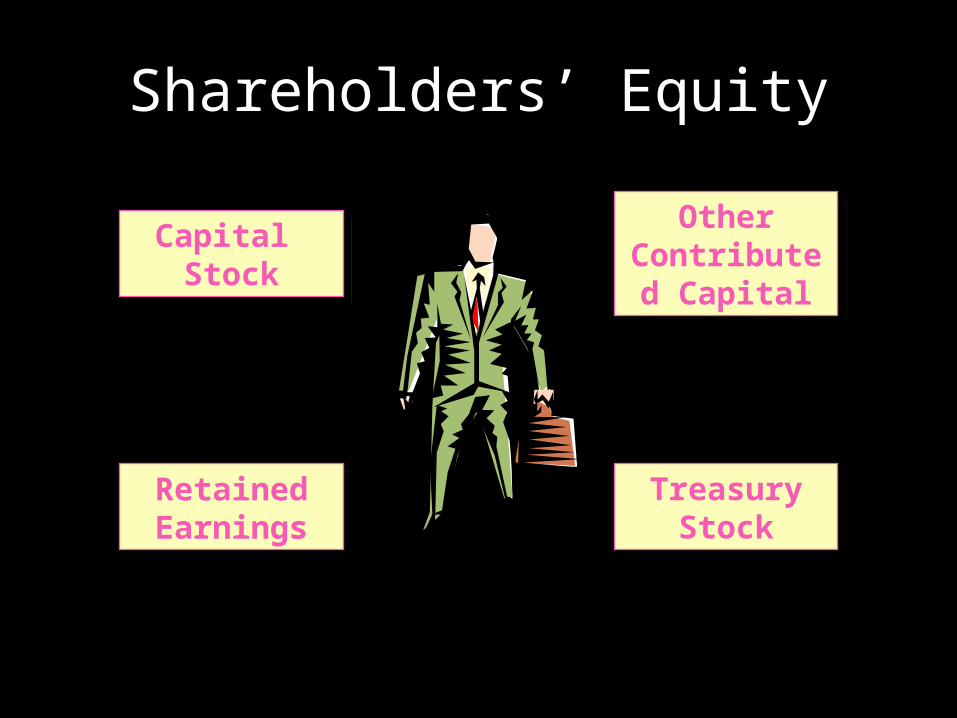

Shareholders’ Equity

Capital Stock

Capital Stock

Retained Earnings

Retained Earnings

Treasury Stock

Treasury Stock

Other Contributed

Capital

Other Contributed

Capital

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Some Examples

SEARS Balance SheetSears Footnotes

Kohl's Balance SheetKohl’s Footnotes

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

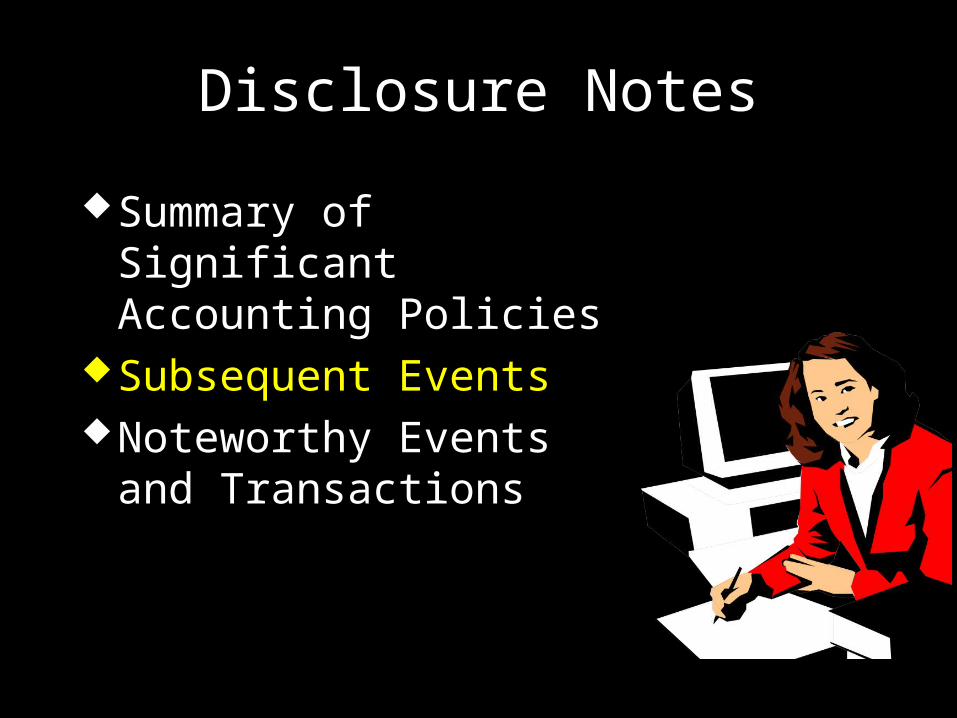

Disclosure Notes

Summary of Significant Accounting Policies

Subsequent EventsNoteworthy Events and

Transactions

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

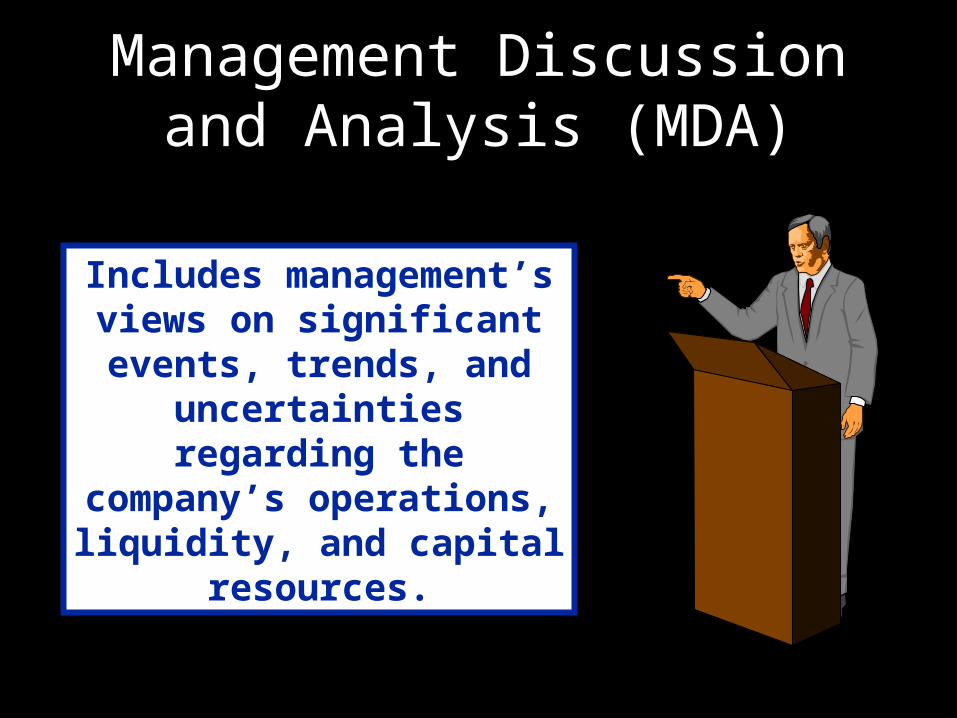

Management Discussion and Analysis (MDA)

Includes management’s views on significant events, trends, and

uncertainties regarding the company’s operations,

liquidity, and capital resources.

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance Sheet

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

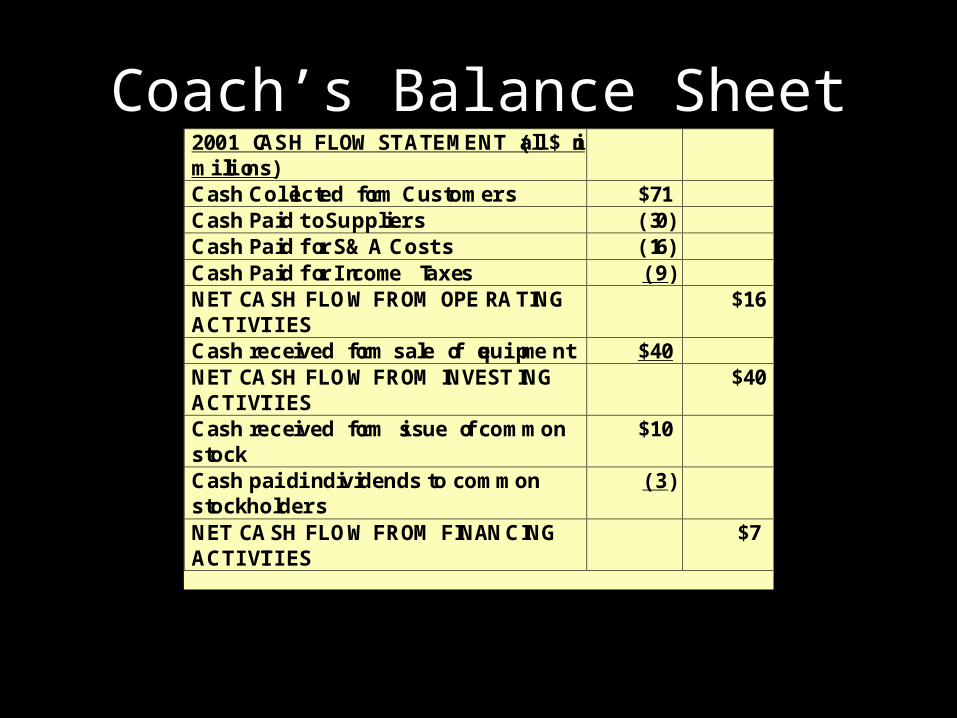

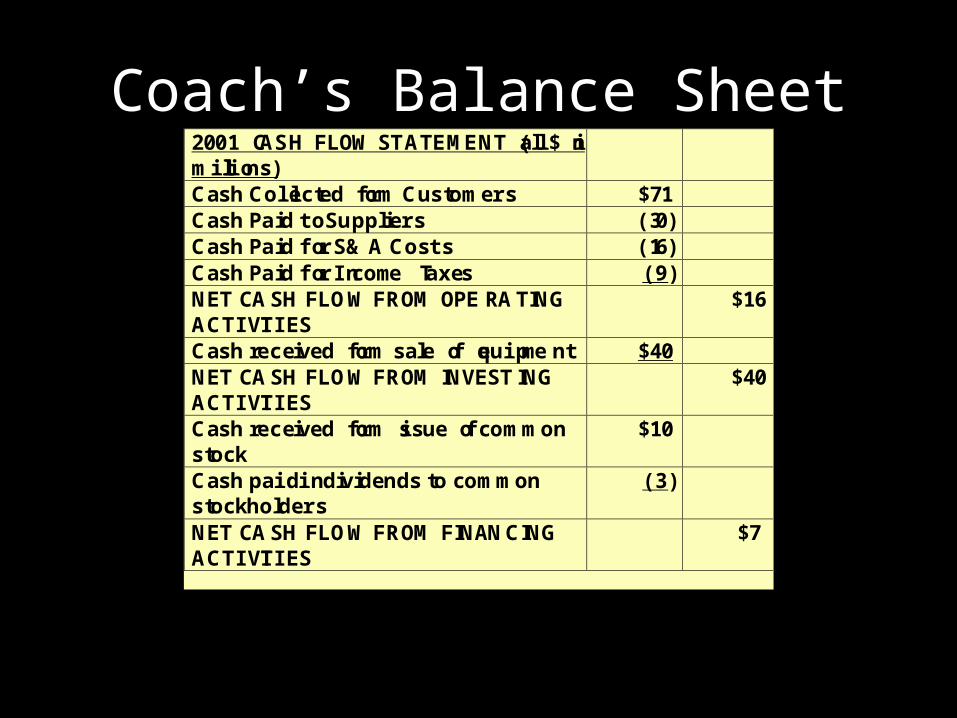

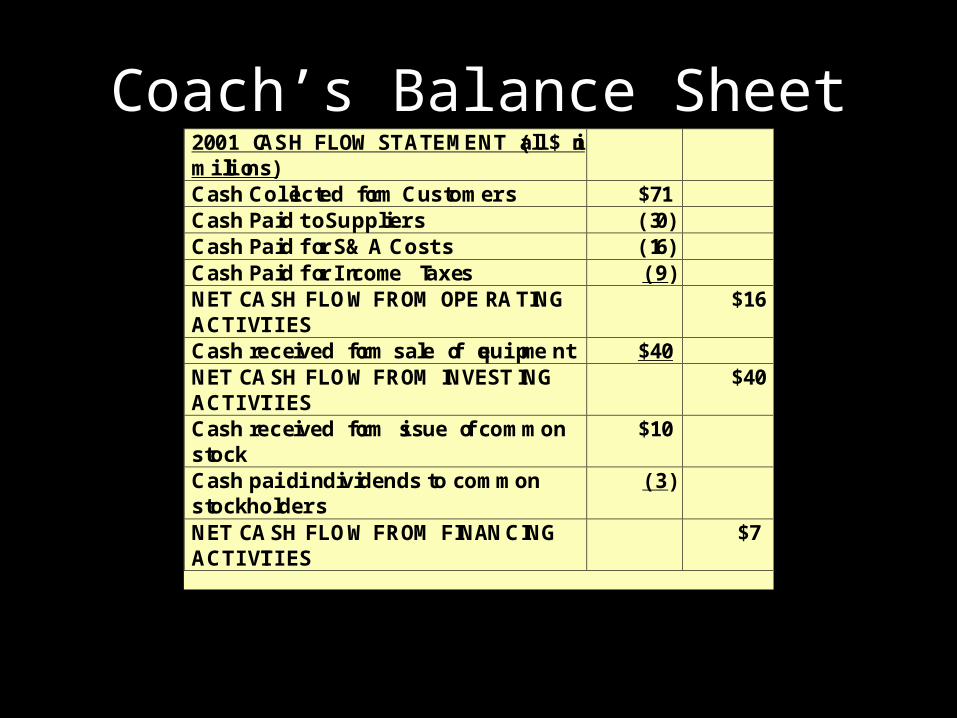

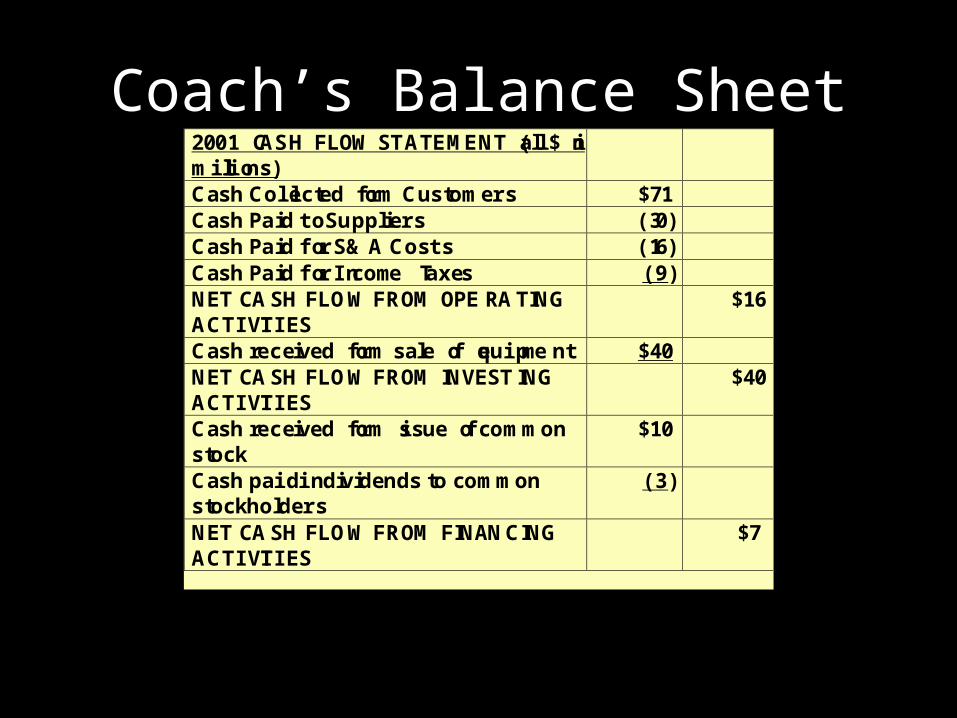

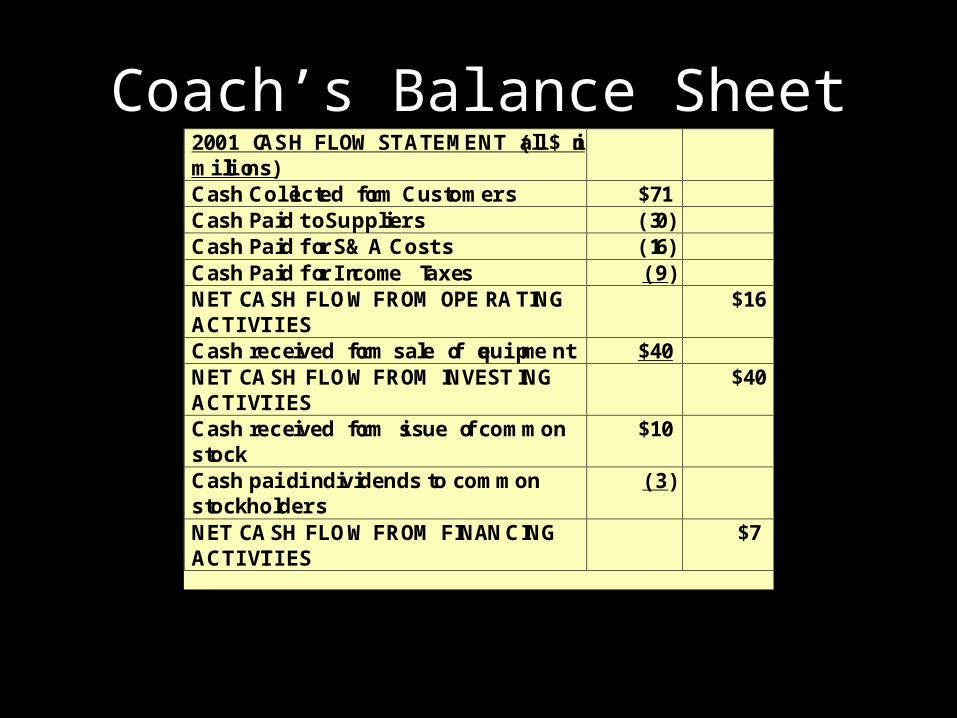

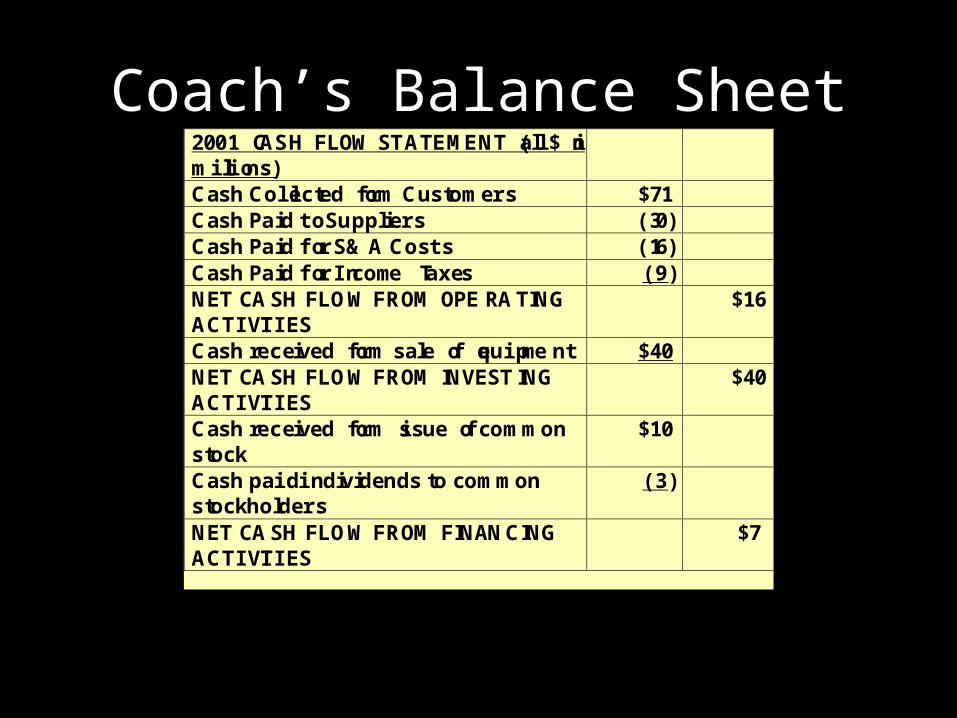

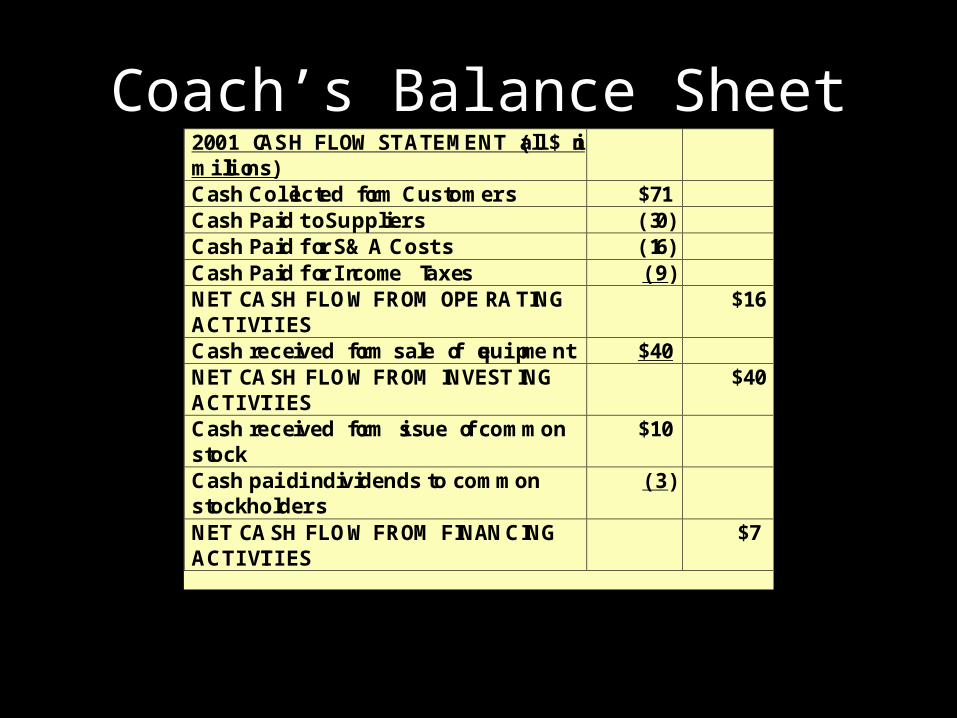

Coach’s Balance Sheet2001 CASH FLOW STATEMENT (all $ inmillions)Cash Collected from Customers $71Cash Paid to Suppliers (30)Cash Paid for S& A Costs (16)Cash Paid for Income Taxes (9)NET CASH FLOW FROM OPERATINGACTIVITIES

$16

Cash received from sale of equipment $40NET CASH FLOW FROM INVESTINGACTIVITIES

$40

Cash received from issue of commonstock

$10

Cash paid in dividends to commonstockholders

(3)

NET CASH FLOW FROM FINANCINGACTIVITIES

$7

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance Sheet

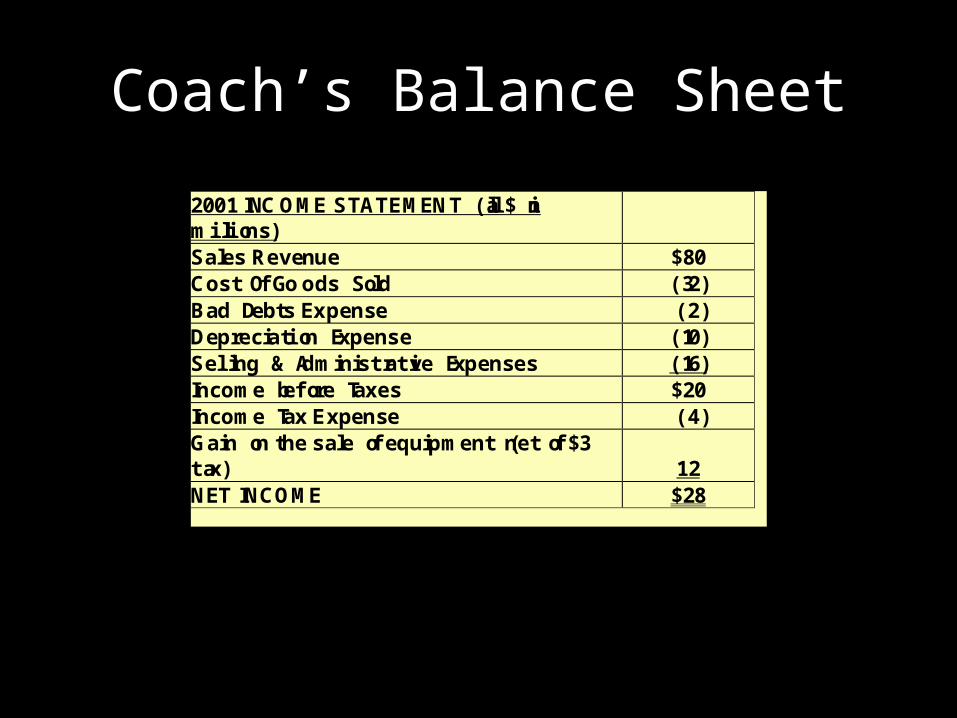

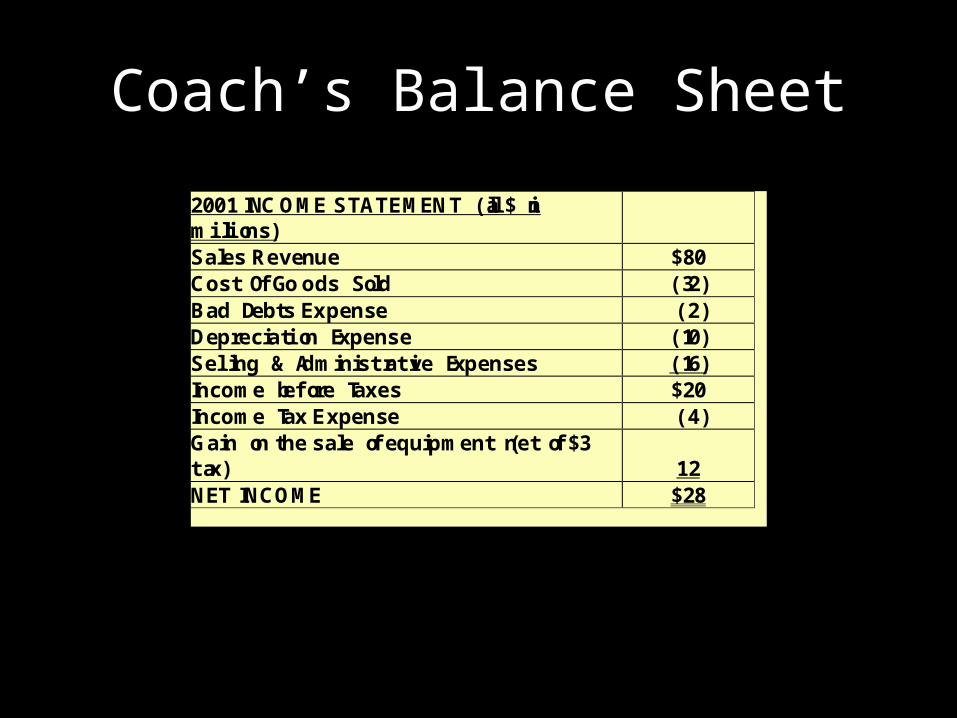

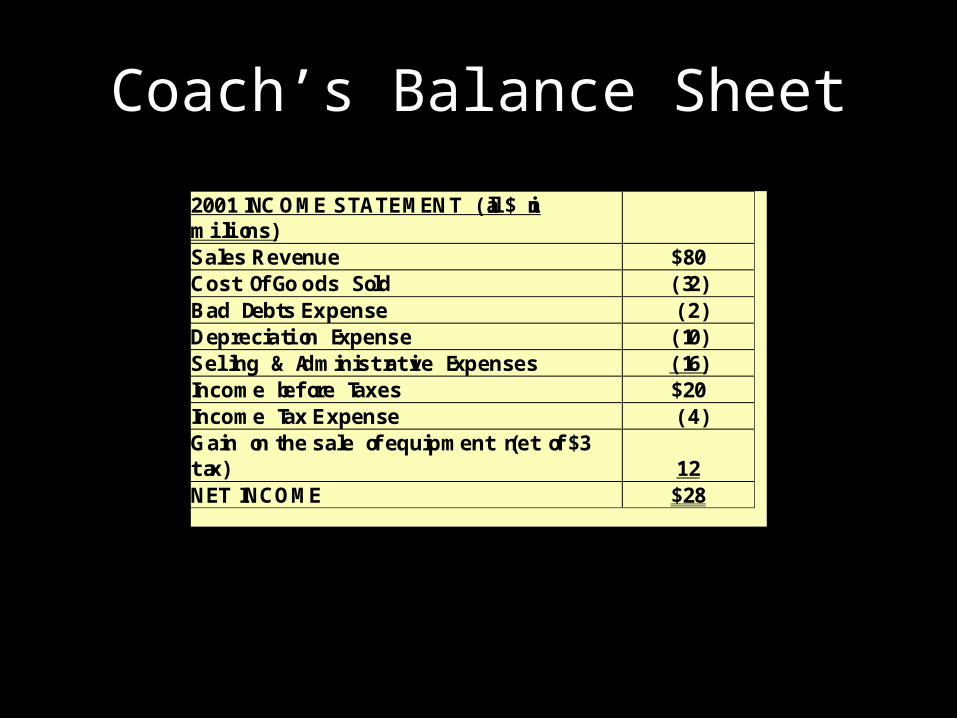

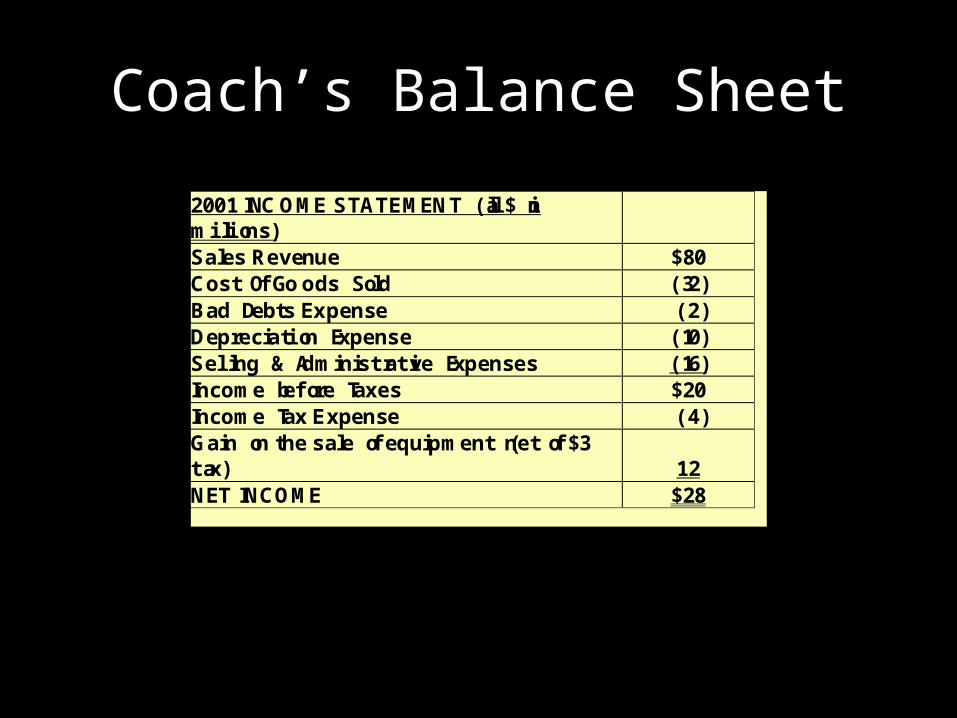

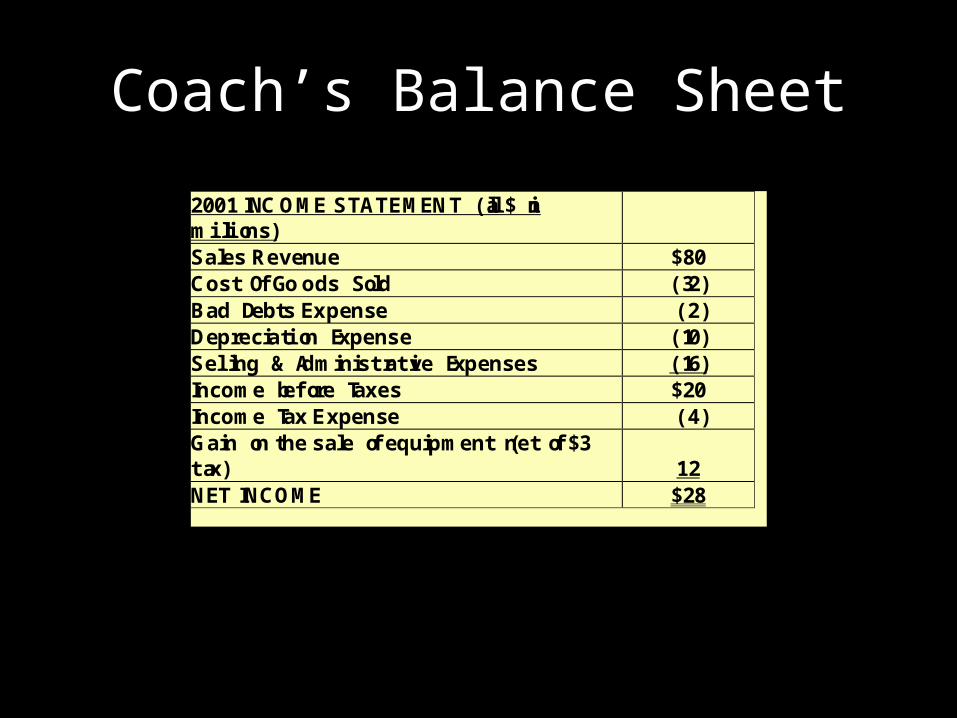

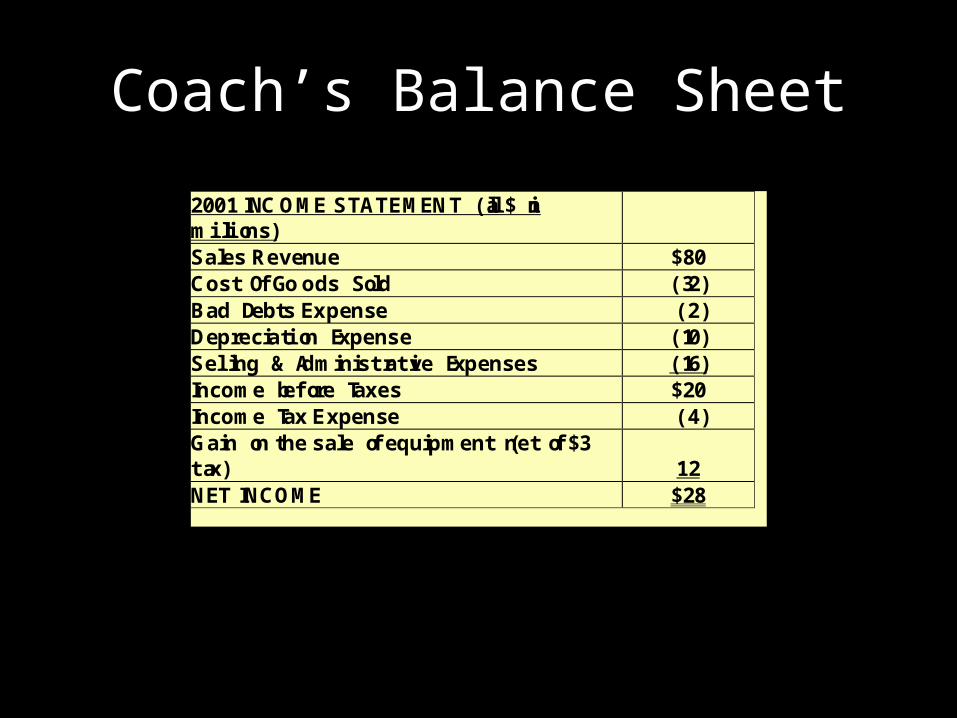

2001 INCOME STATEMENT (all $ inmillions)Sales Revenue $80Cost Of Goods Sold (32)Bad Debts Expense (2)Depreciation Expense (10)Selling & Administrative Expenses (16)Income before Taxes $20Income Tax Expense (4)Gain on the sale of equipment (net of $3tax) 12NET INCOME $28

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

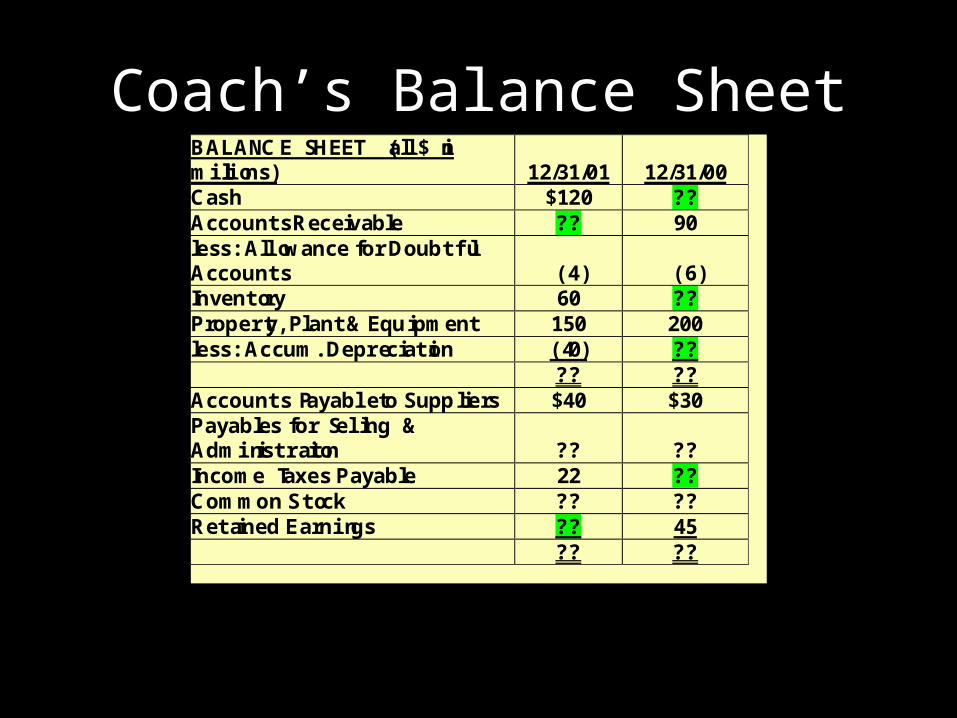

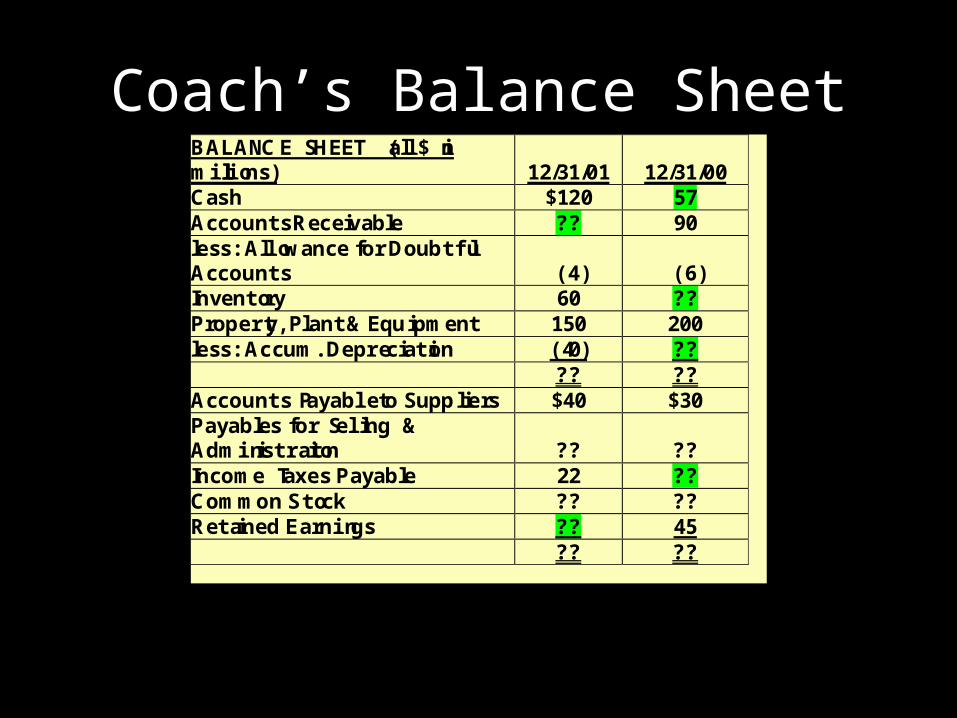

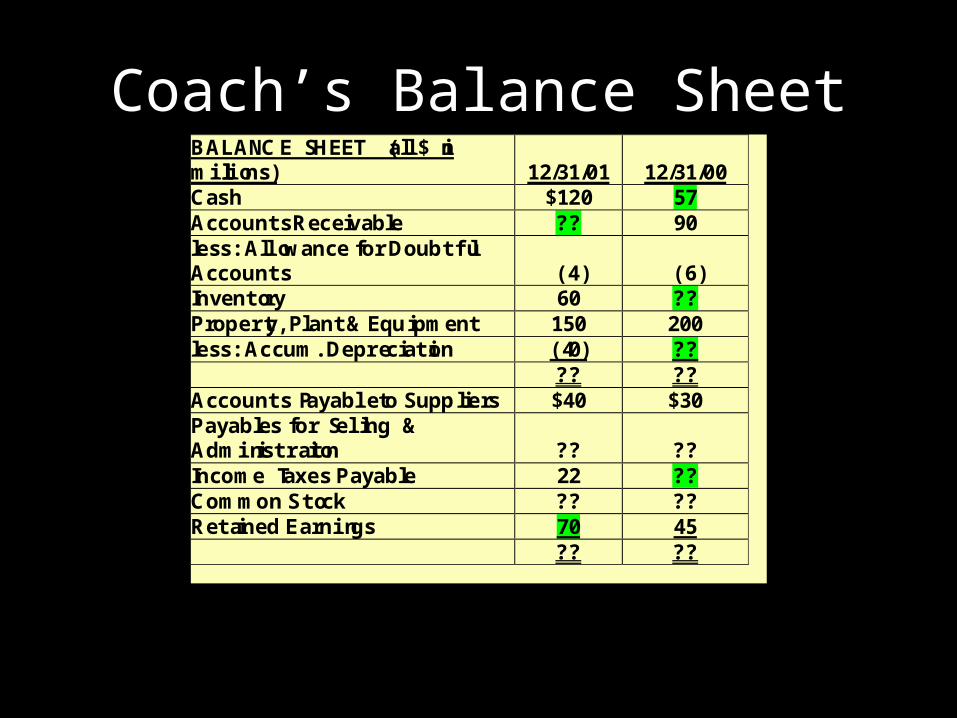

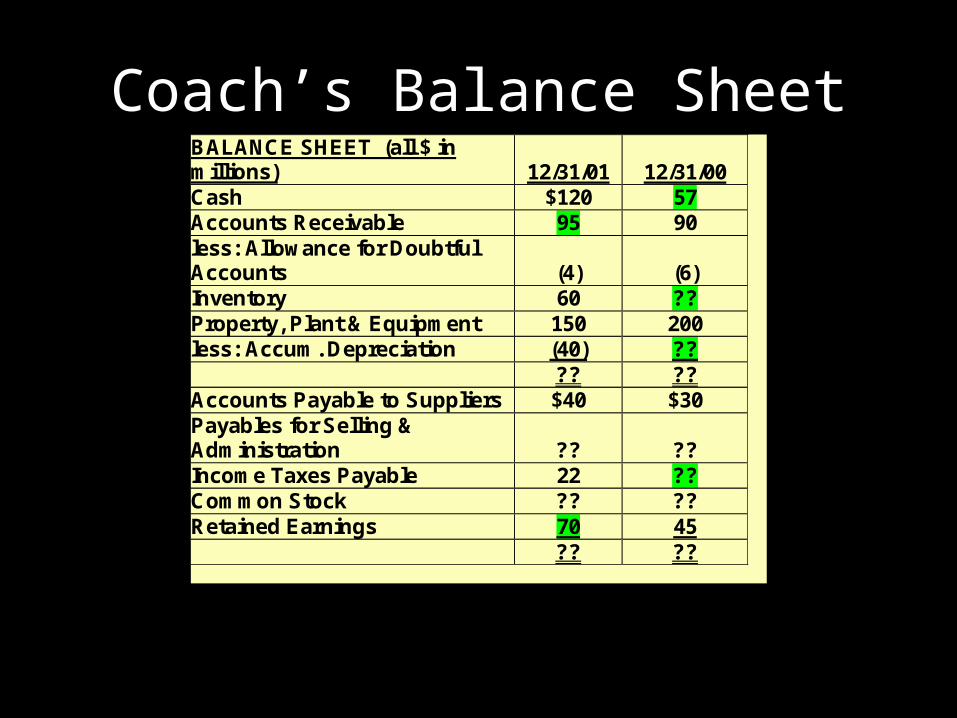

Coach’s Balance SheetBALANCE SHEET (all $ inmillions) 12/31/01 12/31/00Cash $120 ??Accounts Receivable ?? 90less: Allowance for DoubtfulAccounts (4) (6)Inventory 60 ??Property, Plant & Equipment 150 200less: Accum. Depreciation (40) ??

?? ??Accounts Payable to Suppliers $40 $30Payables for Selling &Administration ?? ??Income Taxes Payable 22 ??Common Stock ?? ??Retained Earnings ?? 45

?? ??

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance Sheet2001 CASH FLOW STATEMENT (all $ inmillions)Cash Collected from Customers $71Cash Paid to Suppliers (30)Cash Paid for S& A Costs (16)Cash Paid for Income Taxes (9)NET CASH FLOW FROM OPERATINGACTIVITIES

$16

Cash received from sale of equipment $40NET CASH FLOW FROM INVESTINGACTIVITIES

$40

Cash received from issue of commonstock

$10

Cash paid in dividends to commonstockholders

(3)

NET CASH FLOW FROM FINANCINGACTIVITIES

$7

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance Sheet

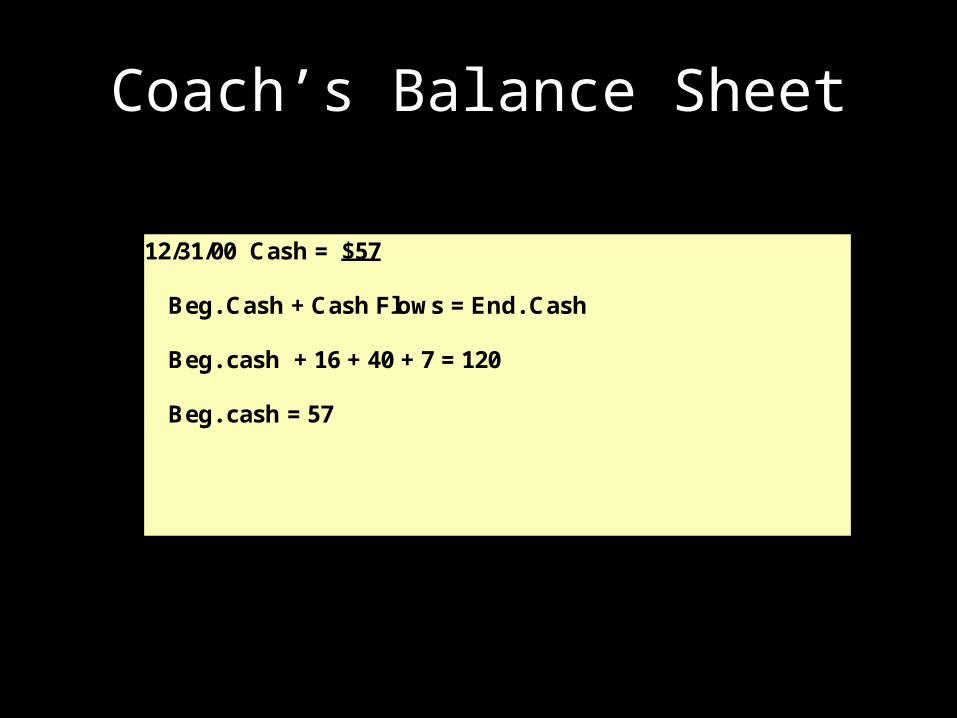

12/31/00 Cash = $57 Beg. Cash + Cash Flows = End. Cash Beg. cash + 16 + 40 + 7 = 120 Beg. cash = 57

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance SheetBALANCE SHEET (all $ inmillions) 12/31/01 12/31/00Cash $120 57Accounts Receivable ?? 90less: Allowance for DoubtfulAccounts (4) (6)Inventory 60 ??Property, Plant & Equipment 150 200less: Accum. Depreciation (40) ??

?? ??Accounts Payable to Suppliers $40 $30Payables for Selling &Administration ?? ??Income Taxes Payable 22 ??Common Stock ?? ??Retained Earnings ?? 45

?? ??

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance Sheet

2001 INCOME STATEMENT (all $ inmillions)Sales Revenue $80Cost Of Goods Sold (32)Bad Debts Expense (2)Depreciation Expense (10)Selling & Administrative Expenses (16)Income before Taxes $20Income Tax Expense (4)Gain on the sale of equipment (net of $3tax) 12NET INCOME $28

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance Sheet2001 CASH FLOW STATEMENT (all $ inmillions)Cash Collected from Customers $71Cash Paid to Suppliers (30)Cash Paid for S& A Costs (16)Cash Paid for Income Taxes (9)NET CASH FLOW FROM OPERATINGACTIVITIES

$16

Cash received from sale of equipment $40NET CASH FLOW FROM INVESTINGACTIVITIES

$40

Cash received from issue of commonstock

$10

Cash paid in dividends to commonstockholders

(3)

NET CASH FLOW FROM FINANCINGACTIVITIES

$7

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance Sheet

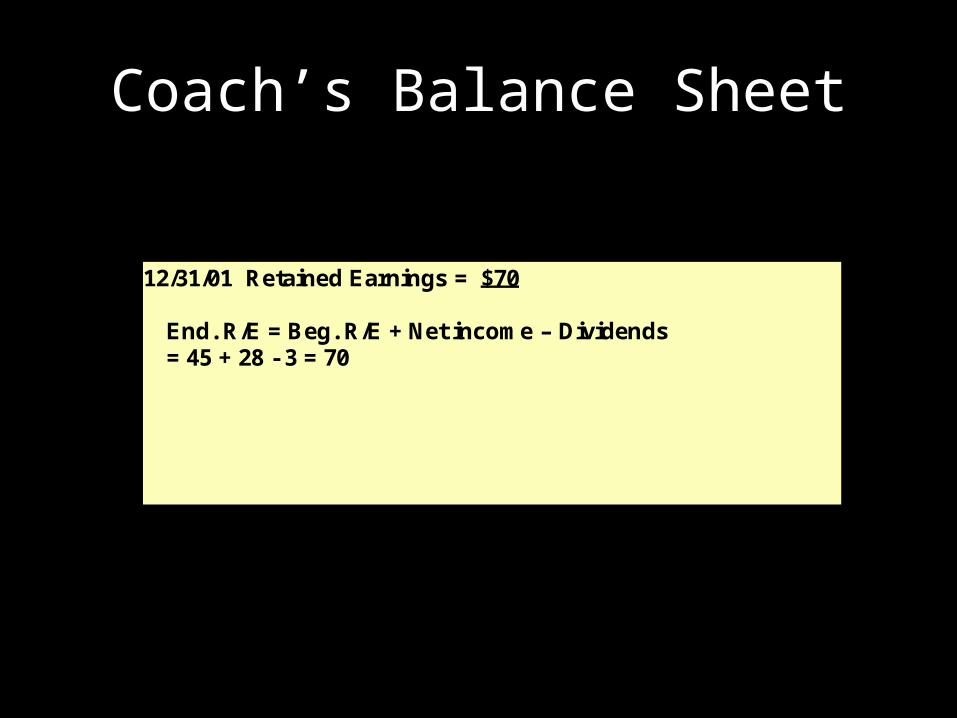

12/31/01 Retained Earnings = $70 End. R/E = Beg. R/E + Net income – Dividends = 45 + 28 - 3 = 70

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance SheetBALANCE SHEET (all $ inmillions) 12/31/01 12/31/00Cash $120 57Accounts Receivable ?? 90less: Allowance for DoubtfulAccounts (4) (6)Inventory 60 ??Property, Plant & Equipment 150 200less: Accum. Depreciation (40) ??

?? ??Accounts Payable to Suppliers $40 $30Payables for Selling &Administration ?? ??Income Taxes Payable 22 ??Common Stock ?? ??Retained Earnings 70 45

?? ??

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance Sheet2001 CASH FLOW STATEMENT (all $ inmillions)Cash Collected from Customers $71Cash Paid to Suppliers (30)Cash Paid for S& A Costs (16)Cash Paid for Income Taxes (9)NET CASH FLOW FROM OPERATINGACTIVITIES

$16

Cash received from sale of equipment $40NET CASH FLOW FROM INVESTINGACTIVITIES

$40

Cash received from issue of commonstock

$10

Cash paid in dividends to commonstockholders

(3)

NET CASH FLOW FROM FINANCINGACTIVITIES

$7

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance Sheet

2001 INCOME STATEMENT (all $ inmillions)Sales Revenue $80Cost Of Goods Sold (32)Bad Debts Expense (2)Depreciation Expense (10)Selling & Administrative Expenses (16)Income before Taxes $20Income Tax Expense (4)Gain on the sale of equipment (net of $3tax) 12NET INCOME $28

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance Sheet

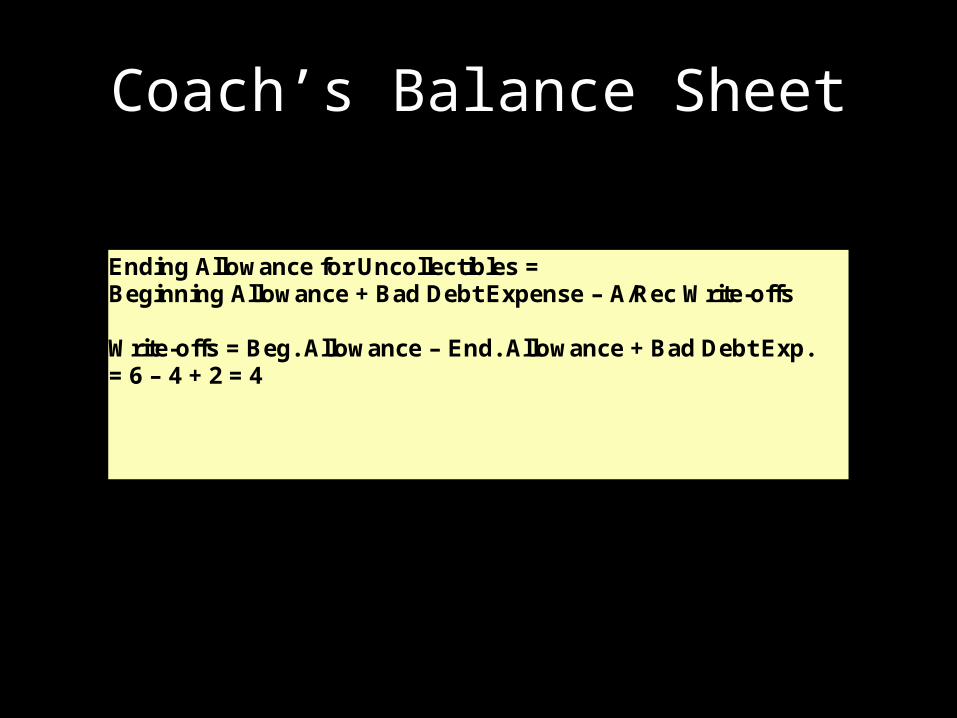

Ending Allowance for Uncollectibles = Beginning Allowance + Bad Debt Expense – A/Rec Write-offs Write-offs = Beg. Allowance – End. Allowance + Bad Debt Exp. = 6 – 4 + 2 = 4

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

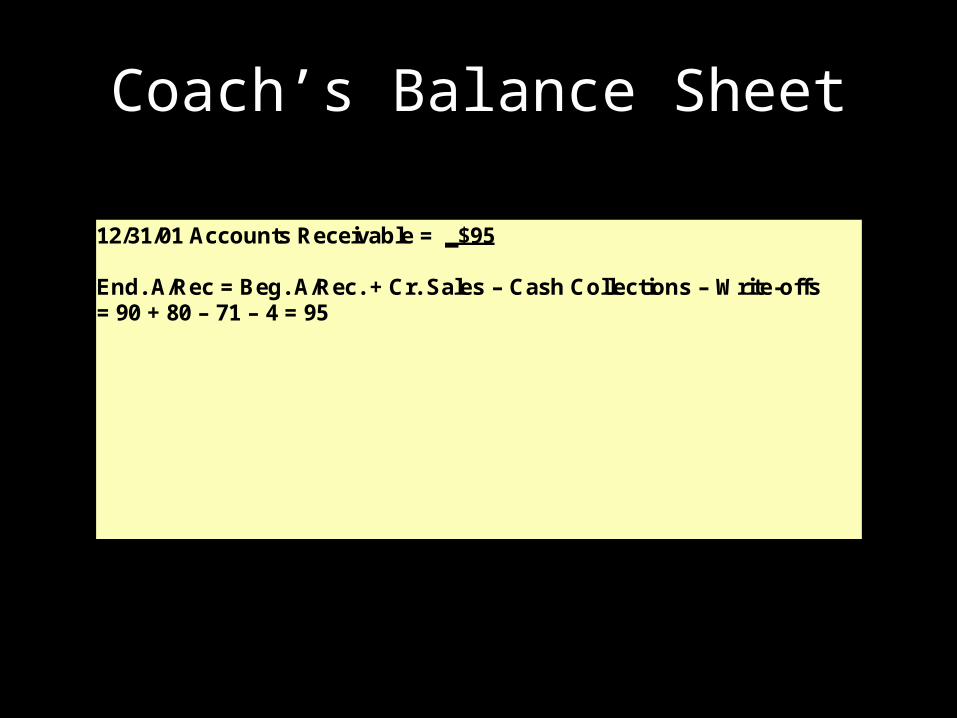

Coach’s Balance Sheet

12/31/01 Accounts Receivable = _$95 End. A/Rec = Beg. A/Rec. + Cr. Sales – Cash Collections – Write-offs = 90 + 80 – 71 – 4 = 95

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance SheetBALANCE SHEET (all $ in millions) 12/31/01 12/31/00 Cash $120 57 Accounts Receivable 95 90 less: Allowance for Doubtful Accounts (4) (6) Inventory 60 ?? Property, Plant & Equipment 150 200 less: Accum. Depreciation (40) ?? ?? ?? Accounts Payable to Suppliers $40 $30 Payables for Selling & Administration ?? ?? Income Taxes Payable 22 ?? Common Stock ?? ?? Retained Earnings 70 45 ?? ??

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance Sheet2001 CASH FLOW STATEMENT (all $ inmillions)Cash Collected from Customers $71Cash Paid to Suppliers (30)Cash Paid for S& A Costs (16)Cash Paid for Income Taxes (9)NET CASH FLOW FROM OPERATINGACTIVITIES

$16

Cash received from sale of equipment $40NET CASH FLOW FROM INVESTINGACTIVITIES

$40

Cash received from issue of commonstock

$10

Cash paid in dividends to commonstockholders

(3)

NET CASH FLOW FROM FINANCINGACTIVITIES

$7

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance Sheet

2001 INCOME STATEMENT (all $ inmillions)Sales Revenue $80Cost Of Goods Sold (32)Bad Debts Expense (2)Depreciation Expense (10)Selling & Administrative Expenses (16)Income before Taxes $20Income Tax Expense (4)Gain on the sale of equipment (net of $3tax) 12NET INCOME $28

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

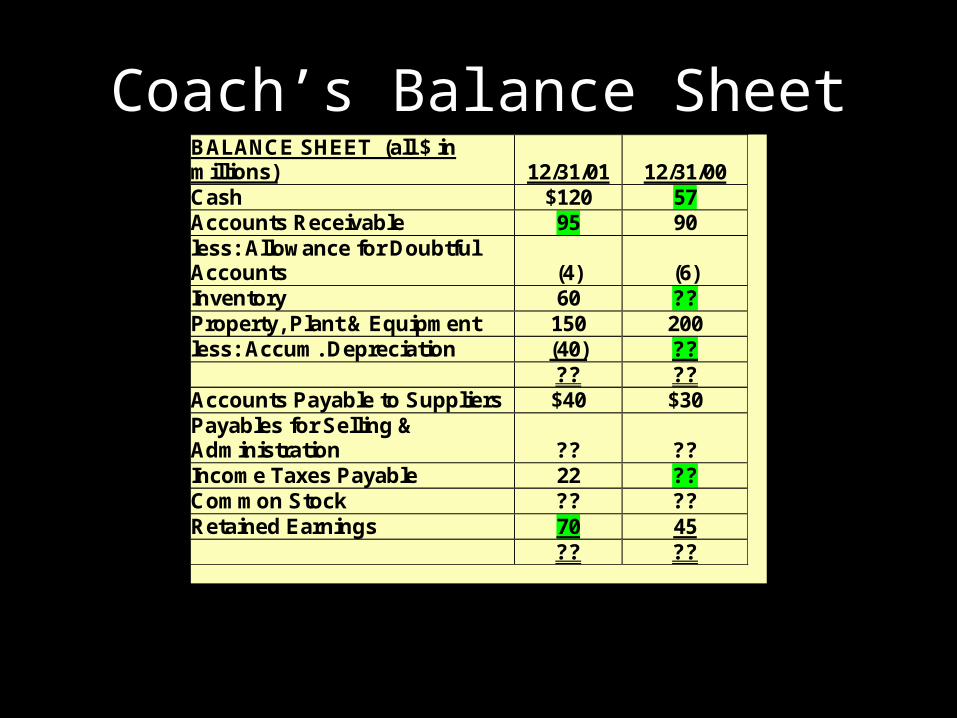

Coach’s Balance SheetBALANCE SHEET (all $ in millions) 12/31/01 12/31/00 Cash $120 57 Accounts Receivable 95 90 less: Allowance for Doubtful Accounts (4) (6) Inventory 60 ?? Property, Plant & Equipment 150 200 less: Accum. Depreciation (40) ?? ?? ?? Accounts Payable to Suppliers $40 $30 Payables for Selling & Administration ?? ?? Income Taxes Payable 22 ?? Common Stock ?? ?? Retained Earnings 70 45 ?? ??

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

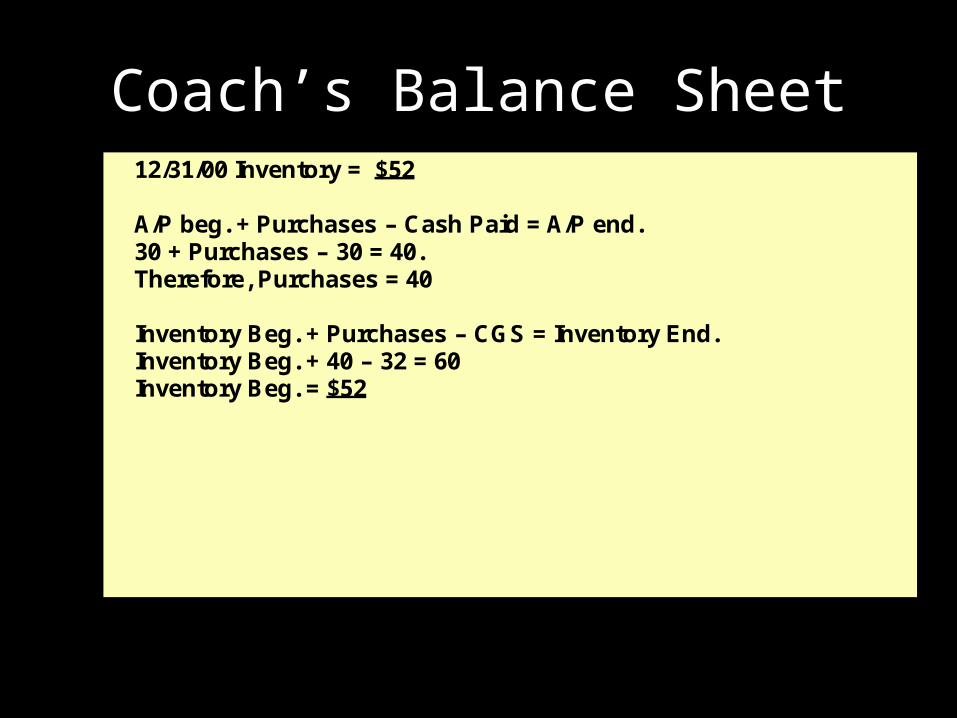

Coach’s Balance Sheet12/31/00 Inventory = $52 A/P beg. + Purchases – Cash Paid = A/P end. 30 + Purchases – 30 = 40. Therefore, Purchases = 40 Inventory Beg. + Purchases – CGS = Inventory End. Inventory Beg. + 40 – 32 = 60 Inventory Beg. = $52

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

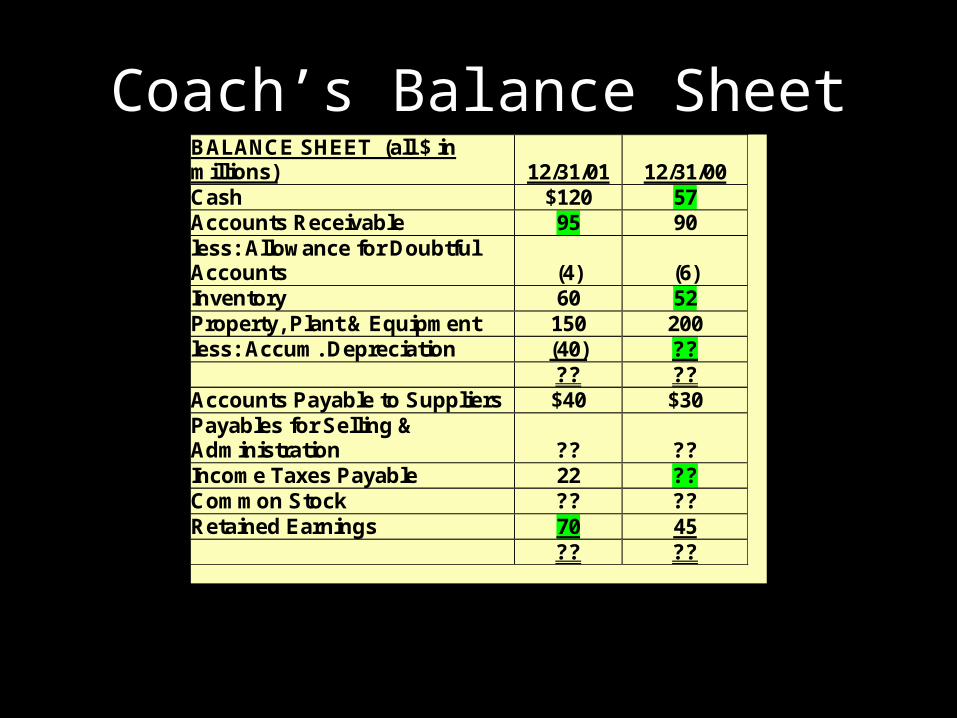

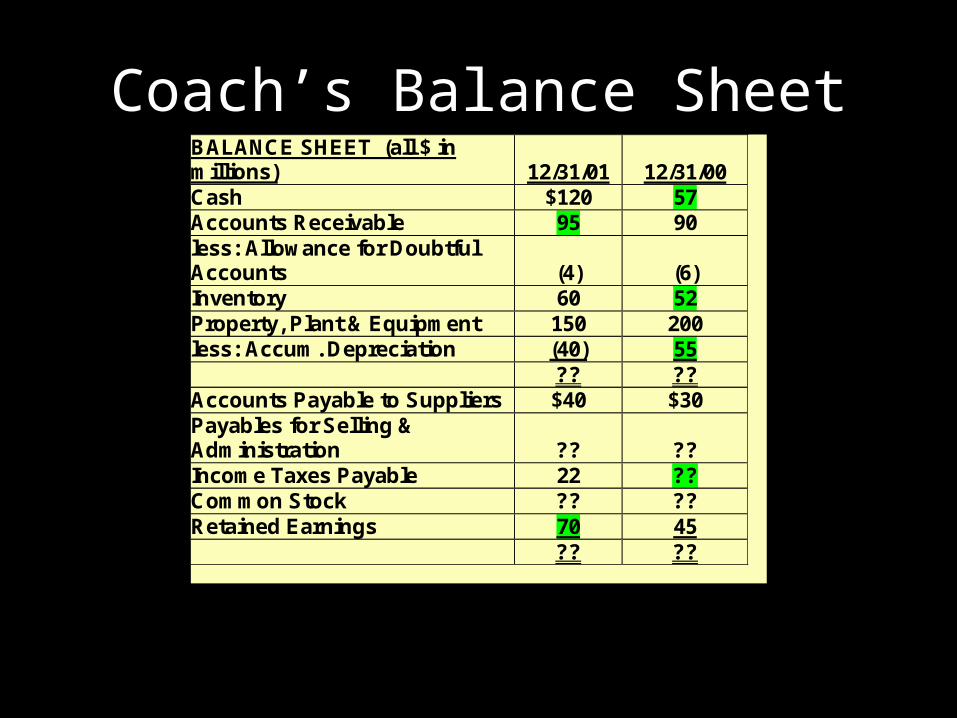

Coach’s Balance SheetBALANCE SHEET (all $ in millions) 12/31/01 12/31/00 Cash $120 57 Accounts Receivable 95 90 less: Allowance for Doubtful Accounts (4) (6) Inventory 60 52 Property, Plant & Equipment 150 200 less: Accum. Depreciation (40) ?? ?? ?? Accounts Payable to Suppliers $40 $30 Payables for Selling & Administration ?? ?? Income Taxes Payable 22 ?? Common Stock ?? ?? Retained Earnings 70 45 ?? ??

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance Sheet2001 CASH FLOW STATEMENT (all $ inmillions)Cash Collected from Customers $71Cash Paid to Suppliers (30)Cash Paid for S& A Costs (16)Cash Paid for Income Taxes (9)NET CASH FLOW FROM OPERATINGACTIVITIES

$16

Cash received from sale of equipment $40NET CASH FLOW FROM INVESTINGACTIVITIES

$40

Cash received from issue of commonstock

$10

Cash paid in dividends to commonstockholders

(3)

NET CASH FLOW FROM FINANCINGACTIVITIES

$7

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance Sheet

2001 INCOME STATEMENT (all $ inmillions)Sales Revenue $80Cost Of Goods Sold (32)Bad Debts Expense (2)Depreciation Expense (10)Selling & Administrative Expenses (16)Income before Taxes $20Income Tax Expense (4)Gain on the sale of equipment (net of $3tax) 12NET INCOME $28

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

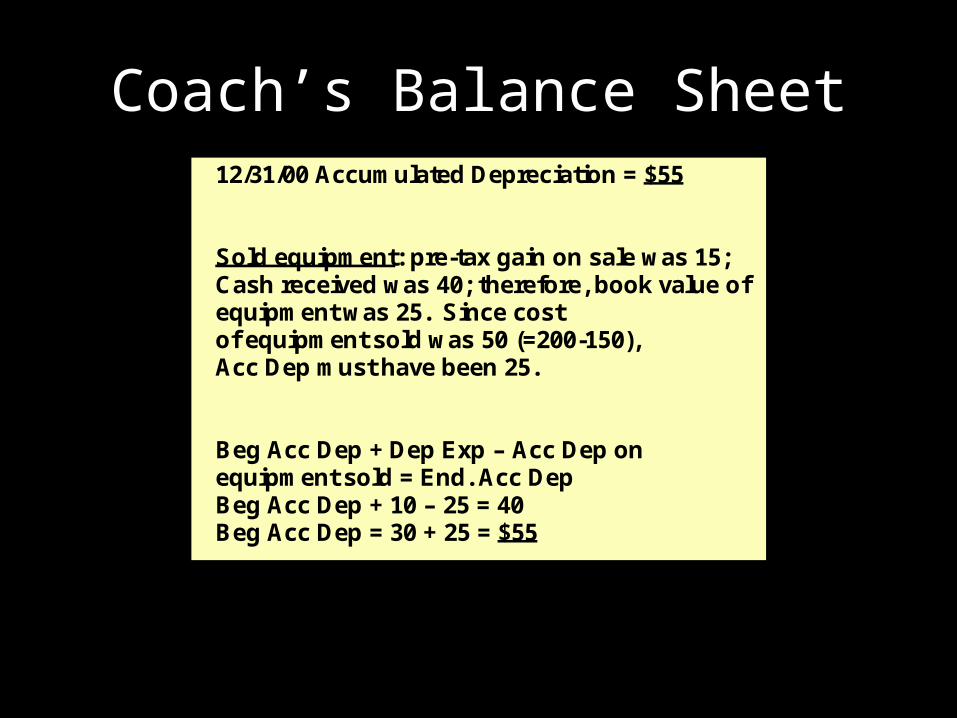

Coach’s Balance Sheet12/31/00 Accumulated Depreciation = $55 Sold equipment: pre-tax gain on sale was 15; Cash received was 40; therefore, book value of equipment was 25. Since cost of equipment sold was 50 (=200-150), Acc Dep must have been 25. Beg Acc Dep + Dep Exp – Acc Dep on equipment sold = End. Acc Dep Beg Acc Dep + 10 – 25 = 40 Beg Acc Dep = 30 + 25 = $55

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance SheetBALANCE SHEET (all $ in millions) 12/31/01 12/31/00 Cash $120 57 Accounts Receivable 95 90 less: Allowance for Doubtful Accounts (4) (6) Inventory 60 52 Property, Plant & Equipment 150 200 less: Accum. Depreciation (40) 55 ?? ?? Accounts Payable to Suppliers $40 $30 Payables for Selling & Administration ?? ?? Income Taxes Payable 22 ?? Common Stock ?? ?? Retained Earnings 70 45 ?? ??

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance Sheet2001 CASH FLOW STATEMENT (all $ inmillions)Cash Collected from Customers $71Cash Paid to Suppliers (30)Cash Paid for S& A Costs (16)Cash Paid for Income Taxes (9)NET CASH FLOW FROM OPERATINGACTIVITIES

$16

Cash received from sale of equipment $40NET CASH FLOW FROM INVESTINGACTIVITIES

$40

Cash received from issue of commonstock

$10

Cash paid in dividends to commonstockholders

(3)

NET CASH FLOW FROM FINANCINGACTIVITIES

$7

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance Sheet

2001 INCOME STATEMENT (all $ inmillions)Sales Revenue $80Cost Of Goods Sold (32)Bad Debts Expense (2)Depreciation Expense (10)Selling & Administrative Expenses (16)Income before Taxes $20Income Tax Expense (4)Gain on the sale of equipment (net of $3tax) 12NET INCOME $28

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

Coach’s Balance Sheet

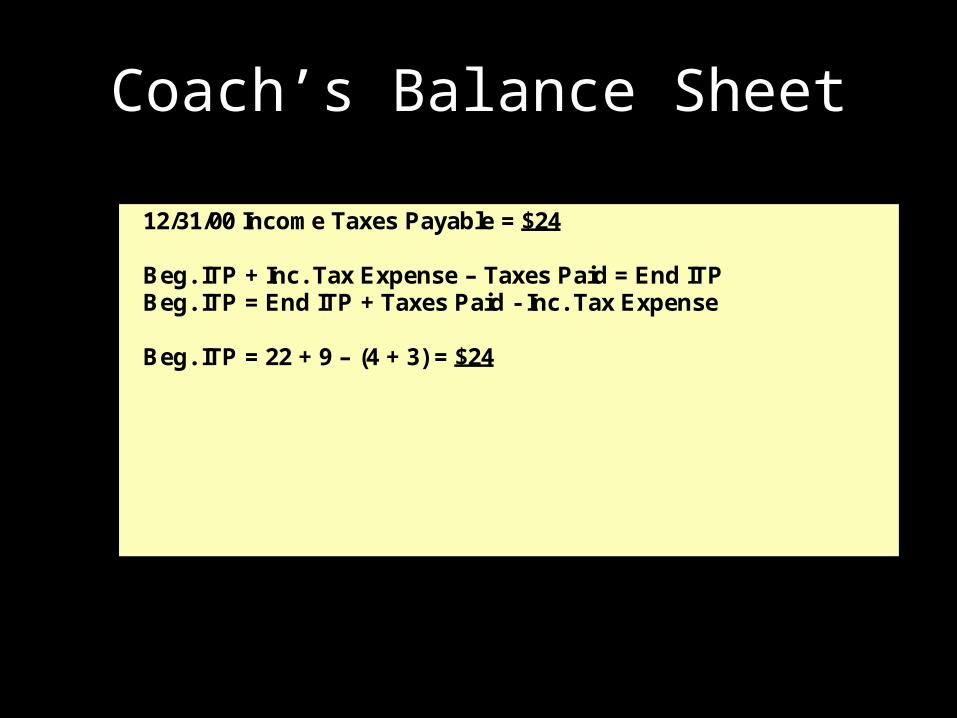

12/31/00 Income Taxes Payable = $24 Beg. ITP + Inc. Tax Expense – Taxes Paid = End ITP Beg. ITP = End ITP + Taxes Paid - Inc. Tax Expense Beg. ITP = 22 + 9 – (4 + 3) = $24

© The McGraw-Hill Companies, Inc., 2001Irwin/McGraw-Hill

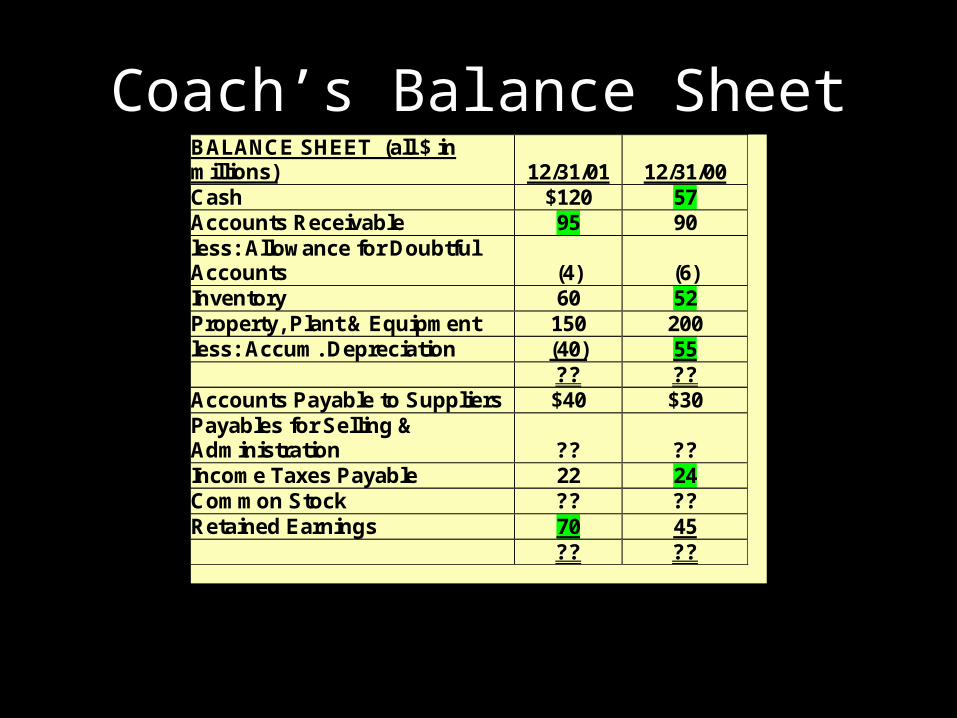

Coach’s Balance SheetBALANCE SHEET (all $ in millions) 12/31/01 12/31/00 Cash $120 57 Accounts Receivable 95 90 less: Allowance for Doubtful Accounts (4) (6) Inventory 60 52 Property, Plant & Equipment 150 200 less: Accum. Depreciation (40) 55 ?? ?? Accounts Payable to Suppliers $40 $30 Payables for Selling & Administration ?? ?? Income Taxes Payable 22 24 Common Stock ?? ?? Retained Earnings 70 45 ?? ??