automotive transactions and trends 2016 · automotive value chain automotive sub-sector 7...

TRANSCRIPT

Automotive transactions and trends 2016Global automotive mergers and acquisitions review

Produced by Global Markets — EY Knowledge

ContentsExecutive summary 1

3Analysis by deal sizes

4Cross-border deals in 2016

6Transaction drivers for the automotive value chain

7Automotive sub-sector transaction trends and drivers

12Investing in mobility

13Capital and M&A outlook

14EY’s Capital Agenda — key considerations and implications

The global automotive industry is in a rapid state of change. An evolution of products and processes, people and places, software and services. The industry is likely to experience more change in the next decade than it has in the previous 50 years. Digitalization and innovation will drive this change. So too will relationships, whether they be with consumers or strategic partners. Success in this new age of automotive will rely heavily on the ability to adapt and adjust, quickly. To access the products, services and skillsets of tomorrow’s automotive industry today.

While organic growth remains important, automotive companies continue to utilize M&A as a strategic tool to access the critical talent, intellectual property and innovation necessary to prosper in the reshaping automotive landscape. Smaller, smarter deals are likely to drive transaction activities.

Traditional deal challenges remain, but many others have emerged in this new environment. As sector convergence increases, the integration of assets outside a company’s traditional core is far less straightforward, requiring customer-centric solutions. Additionally, the rise of nationalist politics adds a new layer of complexity to cross-border investment strategies and deal assessments.

Despite the challenges, automotive companies fully understand that improving their competitive edge requires a sharp focus on acquiring innovative assets that best position them for success in the new automotive ecosystem.

Mark ShortEY Global Automotive and Transportation Industry Leader, Transaction Advisory Services

M&A plays a key, strategic role in the reinvention of the automotive industry

1Automotive transactions and trends 2016 |

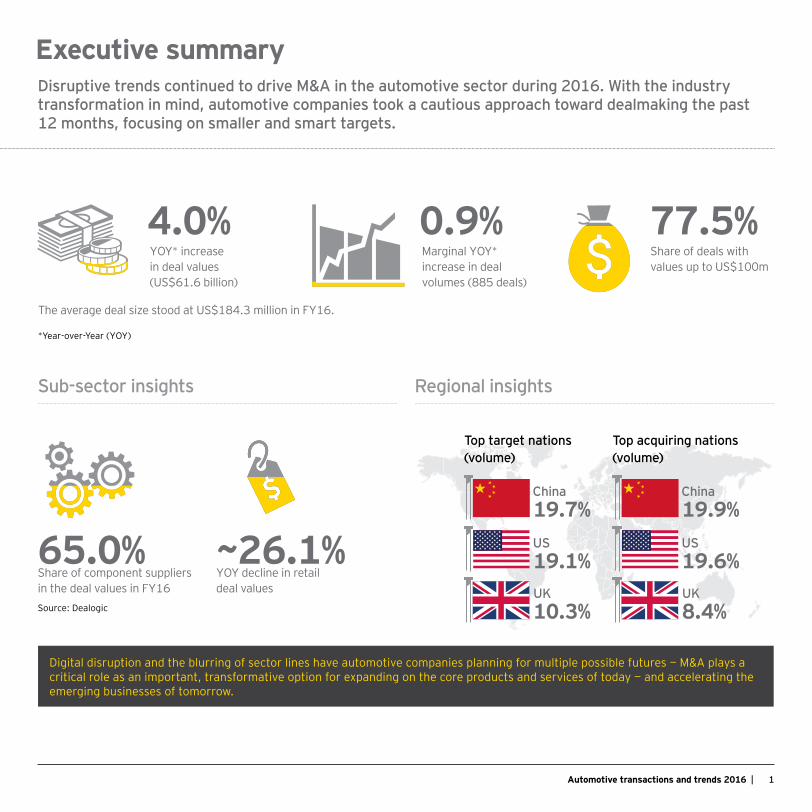

Executive summary

Sub-sector insights Regional insights

Share of component suppliers in the deal values in FY16

65.0%YOY decline in retail deal values

~26.1%

The average deal size stood at US$184.3 million in FY16.

Source: Dealogic

YOY* increase in deal values (US$61.6 billion)

4.0% 0.9%Marginal YOY* increase in deal volumes (885 deals)

77.5%Share of deals with values up to US$100m

Disruptive trends continued to drive M&A in the automotive sector during 2016. With the industry transformation in mind, automotive companies took a cautious approach toward dealmaking the past 12 months, focusing on smaller and smart targets.

Top target nations (volume)

Top acquiring nations (volume)

19.1%US

China19.7%

UK10.3%

19.6%US

China19.9%

UK8.4%

Digital disruption and the blurring of sector lines have automotive companies planning for multiple possible futures — M&A plays a critical role as an important, transformative option for expanding on the core products and services of today — and accelerating the emerging businesses of tomorrow.

*Year-over-Year (YOY)

2 | Automotive transactions and trends 2016

Despite strong deal fundamentals and a healthy deal environment, the rate of automotive transactions moderated in 2016, likely caused by Brexit, the US presidential election and weakening economic growth in China, among other factors.

Overall completion rate for deals announced in last nine quarters

89.7%

Average deals closed in the announced quarter, during 4Q14 to 4Q16

77.1%

Deal completion scenario* in the last two years

Continued confidence in the M&A market**

*Based on deal volumes.** Insights from the latest Capital Confidence Barometer.Source: Dealogic and Capital Confidence Barometer

of automotive executives expect to pursue acquisitions in the next 12 months

58%of automotive executives have a positive level of confidence with regard to the number of acquisition opportunities

62%of automotive executives expect the M&A market to improve in next 12 months, while an additional 63% expect a stable M&A market

31%

Deals completed in the same quarter (%)Deals completed (%)

97.6% 97.8% 96.9%90.5%

75.2%

94.9% 93.9% 88.8%

71.6%83.0% 82.1% 77.2% 80.6%

72.8% 78.3% 73.7% 76.3%70.1%

4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16

Executive summary

The pace of investment in mobility, autonomous driving technologies and connected infotainment is accelerating. With the profit potential and growth opportunities within the new mobility landscape becoming more clear, both automotive and non-automotive companies are leveraging M&A or strategic partnerships to advance their market positioning, as evidenced by General Motors’ US$500 million Lyft investment and the US$8 billion Samsung-Harman international deal.

Middle-market transactions (those valued up to US$250m) continued to dominate acquisition plans. The number of upper-middle-market deals (those valued above US$250m and under US$1b) increased.

Deal volumes split by deal size, 4Q13–4Q16

•

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Transaction values in US$ million>250101–250<100

• Access to new customers, data

• Acquiring talent�• Access new

technologies and intellectual property

• Move into new geographical markets

83%

9%

9%

79%

8%

13%

89%

2%9%

80%

7%

12%

87%

6%8%

75%

10%

14%

82%

8%

10%

76%

15%

9%

77%

12%

11%

78%

7%

16%

82%

13%

5%

76%

16%

8%

75%

14%

10%

1Q144Q13 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16

Deal drivers

*Calculation based on deals with disclosed values.Source: Dealogic

Analysis by deal sizes

3

Tech companies such as Microsoft, Baidu, Alibaba, Google, IBM, Apple and CISCO, among others, are increasing collaboration with automotive players to develop next-generation technologies.

Automotive transactions and trends 2016 |

4 | Automotive transactions and trends 2016

Cross-border deals in 2016Cross-border acquisitions provide companies access to new markets, new business segments and new customers. However, these activities may be temporarily delayed due to recent events like the outcome of the US presidential election, Brexit and China’s new regulations on outbound foreign investment.

(73)

86%

(95)

74%

22%

4%

UK

74%

22%

4%

Domestic deals Outbound deals Inbound deals

(214)

US

19%

21%61%

(78)

Canada

19%

56%

24% 27%40%

33%

Germany

(72)

France

75%

13%

13% (200)

China

75%

12%

13%

75%

Japan

(68)

7%

40%53%

*The number in brackets represents the total number of deals in that country/region.Source: Dealogic

Where a company operates is as important as the segments in which it operates. Enterprises that undertake a robust portfolio review often move toward geographies that fill gaps or are ripe for disruption.

China is playing an increasing role in Asia-Pacific M&A activity, with their volume increasing from 120 deals in FY14 to 200 deals in FY16. China’s outbound M&A activity surged in 2015 and 2016 with an increase in pace and deal size. In addition, some of the largest domestic deals within Asia-Pacific during FY16 were announced by China, followed by Australia and Japan.

5Automotive transactions and trends 2016 |

Domestic and cross-border deals both remained strong during FY16. While smaller deals dominated the M&A landscape by volume, deals valued above US$250 million contributed more than 75% share to the total deal value for the same period.

*Represent deals with disclosed values.Source: Dealogic

Bubble represents cumulative deal value in US$ billion *Deal value category in US$ million

*The size of the circle represents deal value in US$ billion

4.9

14.7

2.65.5

238 76

3516

30 12

Domestic Cross-border

31.6

1.7

>250100-250<100

Number of deals by value category*, FY16Deal volume split by deal type*, FY12–16

Cross-border deals in 2016

With global growth moderating and uneven, cross-border M&A strategies are driven by companies seeking pockets of growth abroad.

Steady cross-border acquisition activities highlight the increasing interconnectedness within the global economy.

27%

375 299 361 369 407

29% 23% 28% 26%

73% 71% 77% 72% 74%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015 2016

Cross-border Domestic

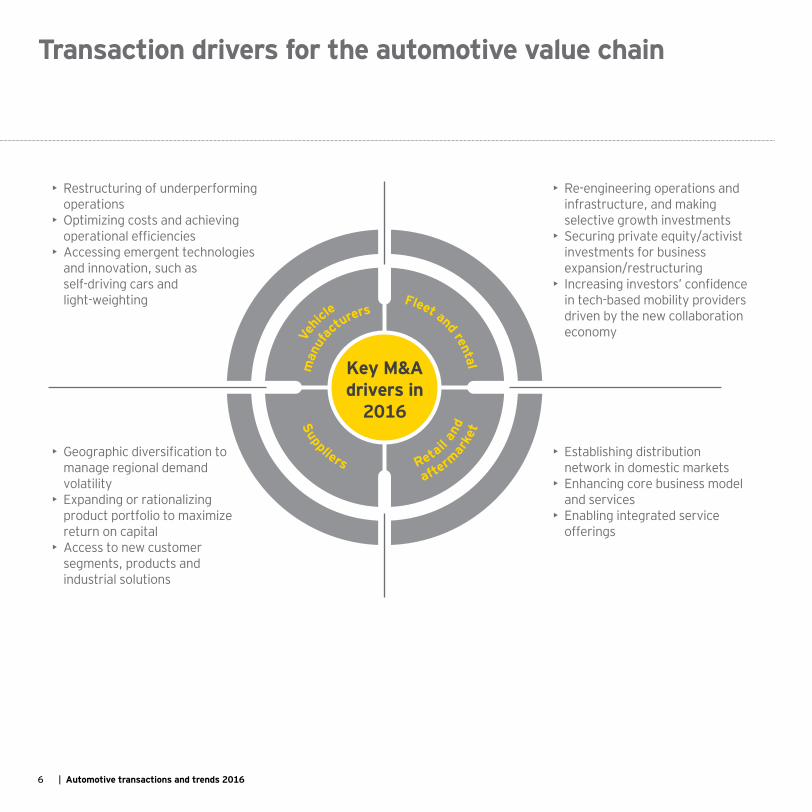

Key drivers for cross-border deals• Leverage cost base/economies of scale• Access strategic proprietary assets and low labor cost

• Gradual easing of FDI and related regulatory processes• Growing domestic demand for global products in emerging markets

6 | Automotive transactions and trends 2016

• Restructuring of underperforming operations

• Optimizing costs and achieving operational efficiencies

• Accessing emergent technologies and innovation, such as self-driving cars and light-weighting

• Re-engineering operations and infrastructure, and making selective growth investments

• Securing private equity/activist investments for business expansion/restructuring

• Increasing investors’ confidence in tech-based mobility providers driven by the new collaboration economy

• Establishing distribution network in domestic markets

• Enhancing core business model and services

• Enabling integrated service offerings

• Geographic diversification to manage regional demand volatility

• Expanding or rationalizing product portfolio to maximize return on capital

• Access to new customer segments, products and industrial solutions

Key M&Adrivers in

2016

Fleet and rental

Retail an

d

afterm

arke

tSuppliers

Vehic

lem

anuf

acturers

Transaction drivers for the automotive value chain

Automotive sub-sector transaction trends and drivers

8 | Automotive transactions and trends 2016

4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16

Deal value (US$m) No. of deals

969

14,868

6741,654

3071,491

3,901 1,903 2,269

5,871 3,3702,296

1,237

17

35

2118

2621 21

2732

24 21

1724

2016 deals weredriven by autonomous driving, connectivity

and alternate powertrain technologies. OEMs continue

to accelerate the paceof their engagementwith tech companies,both large and small.

Deal values increased by ~28%

YOY to reach US$12.3 billion

Deal volumes decline by 16% YOY

China, Japanand US were the largest acquirer countries, with a

combined 91% share in deal value and

56% share indeal volume

Fleet and rental

Retail an

d

afterm

arke

tSuppliers

Vehic

le

man

ufac

turers

Key M&Adrivers in

1H16

Source: Dealogic*The Porsche-Scania deal contributed more than 60% to the total deal value during 1Q14.

Vehicle manufacturers (OEMs) transactions

M&Astrategyoutlook

Operational restructuring tounlock capital for expansion

Access to future mobility

solutions/services, autonomous driving

and connectivity technologies

Energy/powertrain, parking and rentals/

marketplaces

Deal indicatorsShare of the top five deals in FY16 in total deal values

68% Completion rate of deals announced in 2H16 based on deal volumes

76% Completion rate of deals announced in 4Q16 based on deal volumes

70%

The growing number of autonomous driving, connectivity and powertrain technologies acquisitions highlights the importance of leadership positioning among passenger vehicle manufacturers in the burgeoning mobility landscape.

9Automotive transactions and trends 2016 |

China, the US and Japan emerged as the largest acquirer countries, with 83% share in deal value

Deal values declined by 4% YOY to US$31.8 billion, while deal volumes increased by 3% YOY

China, the US and Germany were the largest target nations, accounting for more than 53% share by deal volume

Parts and equipment (supplier) transactions

2016 deals were driven by self-driving revolution, control of multipart modules and interior business consolidation

Fleet and rental

Retail an

d

afterm

arke

tSuppliers

Vehic

le

man

ufac

turers

Key M&Adrivers in

1H16

4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16

Deal value (US$m) No. of deals

4,609

7,771 8,917

16,600

1,606

15,255

5,695 6,976

5,182

7,236

4,397 4,478

15,740

84

112

89 111100 100

111

88

82

96 94

110

91

Source: Dealogic

M&Astrategyoutlook

To keep up with advances

in self-driving cars, infotainment

and powertrains

Wave of consolidation and access to the all-

important interface between driver

and vehicle

Gaining access to new safety

and electronics technologies

Deal indicatorsShare of the top five deals in FY16 in total deal values

45% Completion rate of deals announced in 2H16 based on deal volumes

72% Completion rate of deals announced in 4Q16 based on deal volumes

63%

With Samsung’s acquisition of Harman, a “new market entrant” booked the largest deal in the supplier space.

10 | Automotive transactions and trends 2016

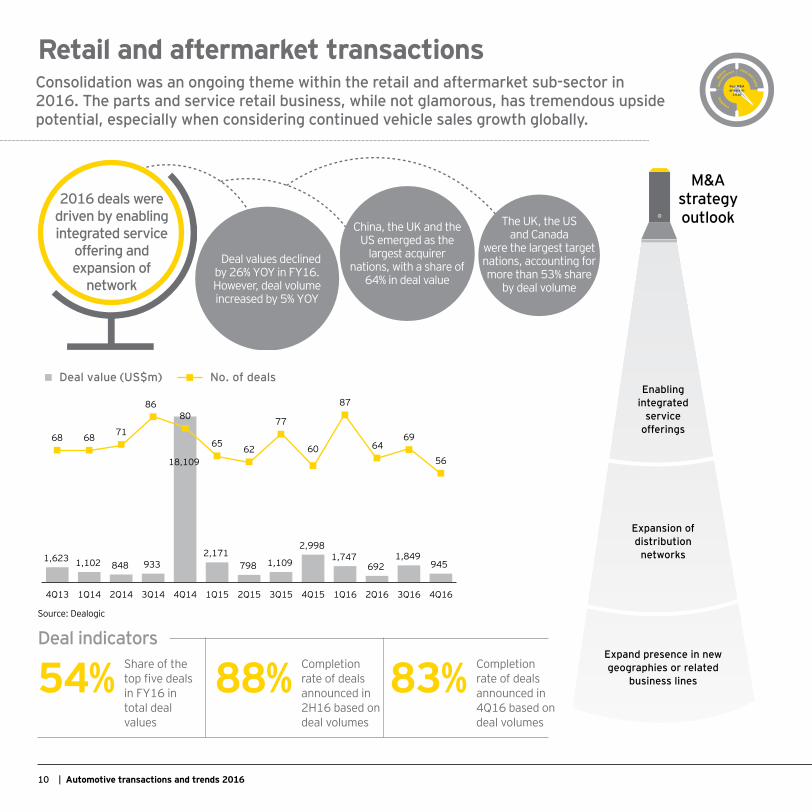

4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16

Deal value (US$m) No. of deals

1,623 1,102 848 933

18,109

2,171 798 1,109

2,998 1,747

692 1,849

945

68 68 71

8680

65 62

77

60

87

64 69

56

Fleet and rental

Retail an

d

afterm

arke

tSuppliers

Vehic

le

man

ufac

turers

Key M&Adrivers in

1H16

The UK, the USand Canada

were the largest target nations, accounting for more than 53% share

by deal volume

China, the UK and the US emerged as the

largest acquirer nations, with a share of

64% in deal value

Deal values declined by 26% YOY in FY16. However, deal volume increased by 5% YOY

2016 deals were driven by enabling integrated service

offering and expansion of

network

Source: Dealogic

M&Astrategyoutlook

Enabling integrated

service offerings

Expansion of distribution

networks

Expand presence in new geographies or related

business lines

Retail and aftermarket transactions

Deal indicatorsShare of the top five deals in FY16 in total deal values

54% Completion rate of deals announced in 2H16 based on deal volumes

88% Completion rate of deals announced in 4Q16 based on deal volumes

83%

Consolidation was an ongoing theme within the retail and aftermarket sub-sector in 2016. The parts and service retail business, while not glamorous, has tremendous upside potential, especially when considering continued vehicle sales growth globally.

11Automotive transactions and trends 2016 |

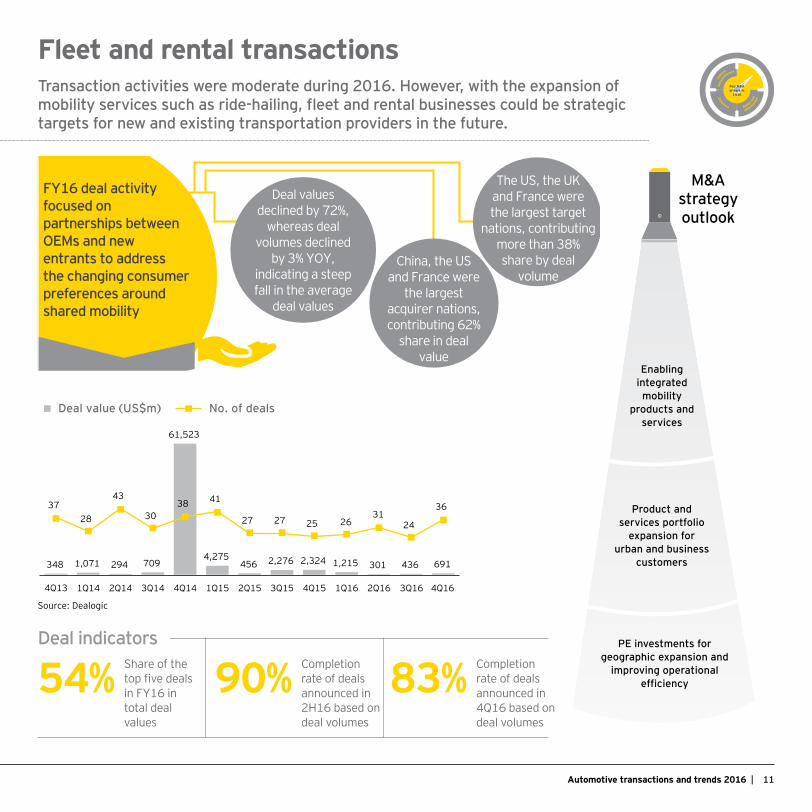

Deal value (US$m) No. of deals

4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16

348 1,071 294 709

61,523

4,275 456 2,276 2,324 1,215 301 436 691

3728

43

3038 41

27 27 25 26 31

24

36

Fleet and rental

Retail an

d

afterm

arke

tSuppliers

Vehic

le

man

ufac

turers

Key M&Adrivers in

1H16

FY16 deal activity focused on partnerships between OEMs and new entrants to address the changing consumer preferences around shared mobility

Deal values declined by 72%,

whereas deal volumes declined

by 3% YOY, indicating a steep fall in the average

deal values

China, the US and France were

the largest acquirer nations, contributing 62%

share in deal value

The US, the UKand France werethe largest target

nations, contributing more than 38% share by deal

volume

Source: Dealogic

M&Astrategyoutlook

Enabling integrated mobility

products and services

Product and services portfolio

expansion for urban and business

customers

PE investments for geographic expansion and

improving operational efficiency

Fleet and rental transactions

Deal indicatorsShare of the top five deals in FY16 in total deal values

54% Completion rate of deals announced in 2H16 based on deal volumes

90% Completion rate of deals announced in 4Q16 based on deal volumes

83%

Transaction activities were moderate during 2016. However, with the expansion of mobility services such as ride-hailing, fleet and rental businesses could be strategic targets for new and existing transportation providers in the future.

12 | Automotive transactions and trends 2016

Investing in mobilityAutomotive companies are seeking leadership positions in the fast-evolving transportation landscape; M&A, strategic partnerships, collaboration complement in-house initiatives.

Active acquirers: OEMs, suppliers and technology companies

• Audi, BMW (venture arm BMW i ventures), and Daimler have the highest number of acquisitions and collaborations among traditional automotive companies.

• Samsung, Siemens and Didi are leading non-automotive investors in mobility. Advancements in autonomous driving, connected vehicle, infotainment and GPS/mapping solutions are driving supplier investment activities.

• Recent high-value deals: Samsung-Harman (US$8 billion), Siemens-Mentor Graphics (US$4.5 billion) and the Uber-Otto acquisition (US$680 million).

• OEMs and suppliers have been actively increasing investments in technology start-ups, particularly in the US, where OEMs are in an ongoing battle (among themselves and other tech giants – Apple, Google, etc.) for new talent, IP and breakthrough technologies.

• Germany is also an active region, with Daimler, Volkswagen, BMW, as well as large tier-1 suppliers, seeking innovation and talent.

• China has a growing presence in mobility M&A activities, including the blockbuster Uber-Didi merger (resulting in a ride-hailing service valued at US$35 billion).

Top target nations: US, China, Germany

Since 2012, more than US$22 billion in deals have been finalized in the automotive-mobility space

Rapid growth in autonomous and connected vehicle technologies has yielded investments of US$14 billion in the last five years

When considering deals by region, the US has been the most active market, with deal values reaching over US$15 billion*

The US had the highest number of deals, 27, with a lot of American automotive players investing in start-ups working in the autonomous and connected tech space

*US$8 billion attributed to Samsung-Harman deal

13Automotive transactions and trends 2016 |

Capital and M&A outlookInsights from the Automotive Capital Confidence Barometer

Digital and innovation drive M&A market

Digitalization and sector convergence are

likely prominent boardroom focus

points

Global economic confidence challenged

by volatility in currencies, commodities

and other capital markets

Acquiring talents and access to new

customers, data fuel cross-sector M&A

M&A strategy focused on cross-border

acquisitions

Respondents view the economy as either stable or modestly improving

70%

34%

Respondents indicating the impact of digital technology on business model as most prominent boardroom discussion point

34%

Respondents indicating sector convergence/increased competition from other sectors as2nd most prominent boardroom discussion point

Respondents cited geopolitical instability as the greatestbusiness risk

49%

Respondents cited acquiring talent as the main driver for acquisition outside of automotive sector

55%

Respondents cited access to new customers, details and databases as drivers for acquisition outside of automotive sector �

31%

Respondents planningacquisitions outsidetheir immediate region

42%

Respondents planningdomestic or intra-regional acquisitions in the next12 months

58%

1 2 3 4

14 | Automotive transactions and trends 2016

The CapitalAgenda

Raisin

g Investing

Preserving Optimizi

ng

What is the best way for your company to grow and is it aligned to core business?

How can you improve the performance of your assets?

What steps can you take to maximize your portfolio’s performance?

• Assess investment opportunities and risks associated with new segments and business models

• Use need-based and strategic alliances, JVs and acquisition to gain technology and geographic coverage

• Build flexibility in emerging market investments

Do you have the right capital structure to meet your strategic priorities?

• Improve information flows to support enhanced visibility of liquidity and cash risks

• Enhance business modeling and cash forecasting systems and capabilities

• Maintain a dynamic business and product portfolio assessment process to support liquidity needs

• Evaluate effectiveness of currency and raw material hedging strategies

EY’s Capital Agenda — key considerations and implications

• Integrate government incentives, direct loans and guarantees in capital-raising strategies

• Refinance debt, equity and other obligations

• Execute “loan-to-own strategies” providing opportunities to raise capital

• Balance cost reduction with sustainable process change

• Institutionalize and integrate working capital initiatives

• Divest carefully — implement risk management process around divestiture cycle to maximize cash benefits

• Benchmark leading-class performance and pursue targeted change

For a conversation about your capital strategy, please contact us:

Acknowledgements

Special thanks to EY Knowledge automotive analysts Joe Sebestyen and Sudarshan Vyas for the analysis and compilation of this study

Randall Miller Global Automotive and Transportation Industry Leader +1 313 628 8642 [email protected]

Mark Short Global Automotive and Transportation Industry Leader, Transaction Advisory Services +1 313 628 8760 [email protected]

Jim Carter Americas Automotive and Transportation Industry Leader, Transaction Advisory Services +1 313 628 8690 [email protected]

Constantin Gall GSA Automotive and Transportation Leader, Transaction Advisory Services +49 711 988114878 [email protected]

Tony Tsang Far East and Oceania Automotive Industry Leader, Transaction Advisory Services +86 21 2228 2358 [email protected]

Peter Wesp Japan Automotive Leader, Transaction Advisory Services +49 6196 996 27282 [email protected]

Anil Valsan Global Automotive and Transportation Lead Analyst +44 20 7951 6879 [email protected]

Regan Grant Global Automotive and Transportation Marketing Leader +1 313 628 8974 [email protected]

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2017 EYGM Limited. All Rights Reserved.

EYG no. 01182-174Gbl

BMC Agency GA 0665_09923

ED None.

In line with EY’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.

ey.com