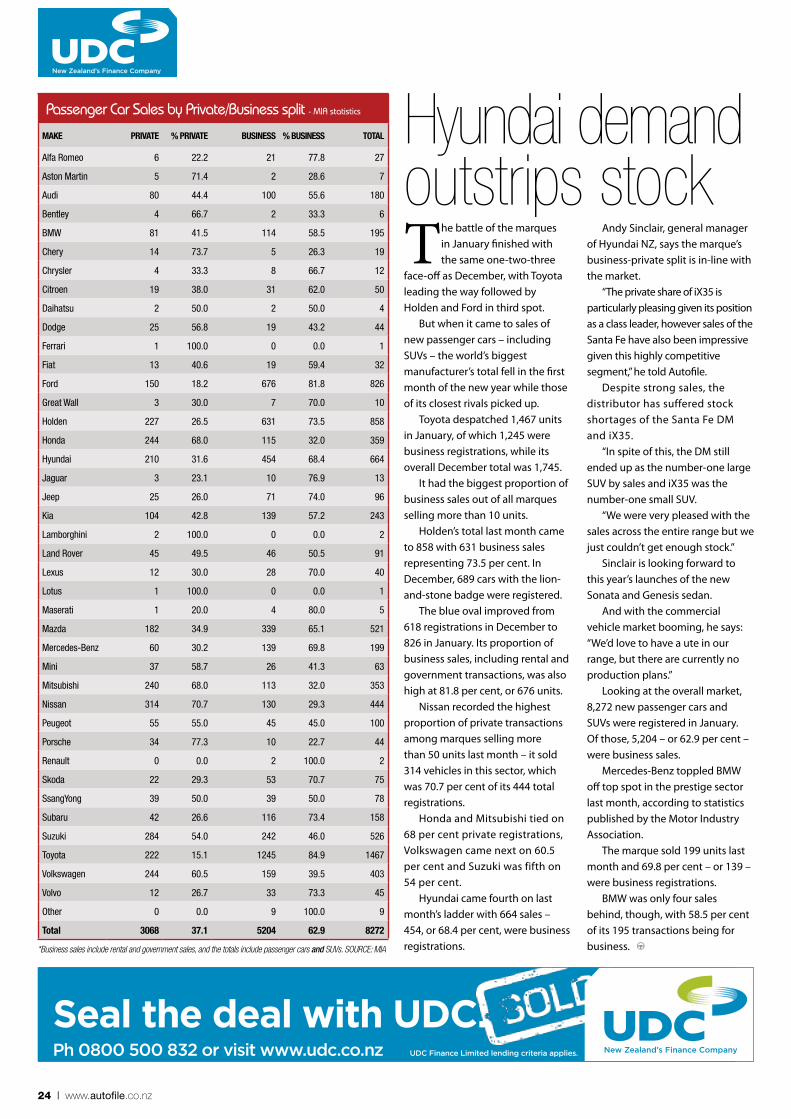

autofile: february 21

DESCRIPTION

The government is being urged to allow marques, dealers and lenders to keep spare car keys when finance is approved. In the second part of an investigation, Autofile reveals this long-established practice could be under threat in the loan-shark laws. The vehicle industry has provided Ports of Auckland with a massive boost, as profits jump by 70 per cent. CEO Tony Gibson told Autofile: “Having almost 100,000 units in the second half of 2013 is a sign the economy seems to be picking up.” The MTA has raised issues with the Commerce Commission about IAG wanting to buy out Lumley. “We’re concerned with the impact on collision repairers and labour rates,” says Dougal Morrison. And Malcolm Yorston, of the IMVIA, compares cheap imported toasters to some after-market car parts, such brake-disc pads. Find out why this reminds him of five-and-dime stores.TRANSCRIPT

Car dealers’ safety net may be bannedThe Financial Services

Federation (FSF) is urging the government to allow

motor vehicle manufacturers, traders and lenders to hold spare sets of car keys after finance is approved for purchases.

The long-established practice could be banned under the Credit Contracts and Financial Services Reform Bill, which the government describes as the biggest overhaul of the sector for a decade.

Most of the proposals are aimed at cracking down on

unscrupulous lenders, particularly in the lower end of the market.

But in its present form, the legislation will affect how finance companies and car dealers go about their business – as revealed in the previous issue of Autofile.

The FSF has also raised concerns with other parts of the bill and is calling for Craig Foss, Minister of Consumer Affairs, to address them.

The federation submits there’s nothing wrong in principle with lenders and registered motor vehicle dealers holding duplicate

sets of keys from day one of loans. “Doing so may facilitate

subsequent repossession to the benefit of all concerned in terms of cost savings,” says executive director Lyn McMorran. “The use of keys should be regulated, not the custody of them.”

The issue is particularly important with car finance because manufacturers typically hold duplicate keys for their vehicles with many having outlets that provide point-of-sale finance for new stock.

The FSF questions if one section [continued on page 4]

The trusted voice of the auto industry for more than 25 yearsIssue 3-2014

21 February 2014

In this issuep6 Trader’s view on WOFs

p9 IMVIA’s capital venture

p10 Kia Soul EV unveiled

p12 Spotlight on Hamilton

p15 MTA’s take on Lumley

p18 Buyer was ‘trying it on’

Specialised training to increase your sales

Find out more on Page 17

Vehicles boost profits at port

www.autofile.co.nz

New Zealand’s booming motor vehicle industry is providing Ports of

Auckland Ltd with a massive increase in business, as reflected in its half-yearly financial statement.

The company has announced a 70 per cent increase in profits for the six months up to December 31.

One of the port’s star

performers was the automotive sector, with motor vehicle imports increasing by 29.3 per cent to 99,710 units from 77,122.

Volumes of break-bulk – or general – cargo, which is non-containerised and includes cars, were up 41.9 per cent to 2.87m tonnes compared to 2.02m over the same timescale.

“The motor vehicle numbers we’ve been experiencing have been very good,” Tony Gibson, chief executive officer, told Autofile.

“Having almost 100,000 units coming through the port in the second half of 2013 is a good sign – the economy seems to be really picking up.”

[continued on page 8]

Retro Vehicle Enhancementwww.rve.co.nz

0800 RETRO 4 U

Driving Solutions

ACCESSORY BUNDLINGCREATE AN EXCLUSIVE MODEL FOR YOUR BRAND

MORE SALES MORE PROFIT

CUSTOMERS FOR LIFE

WWW.DEALERSHIPEDITIONS.CO.NZVIEW VIDEO

p10

From Gran Turismo to Chicago -

Toyota’s FT-1 PlayStation racer becomes reality

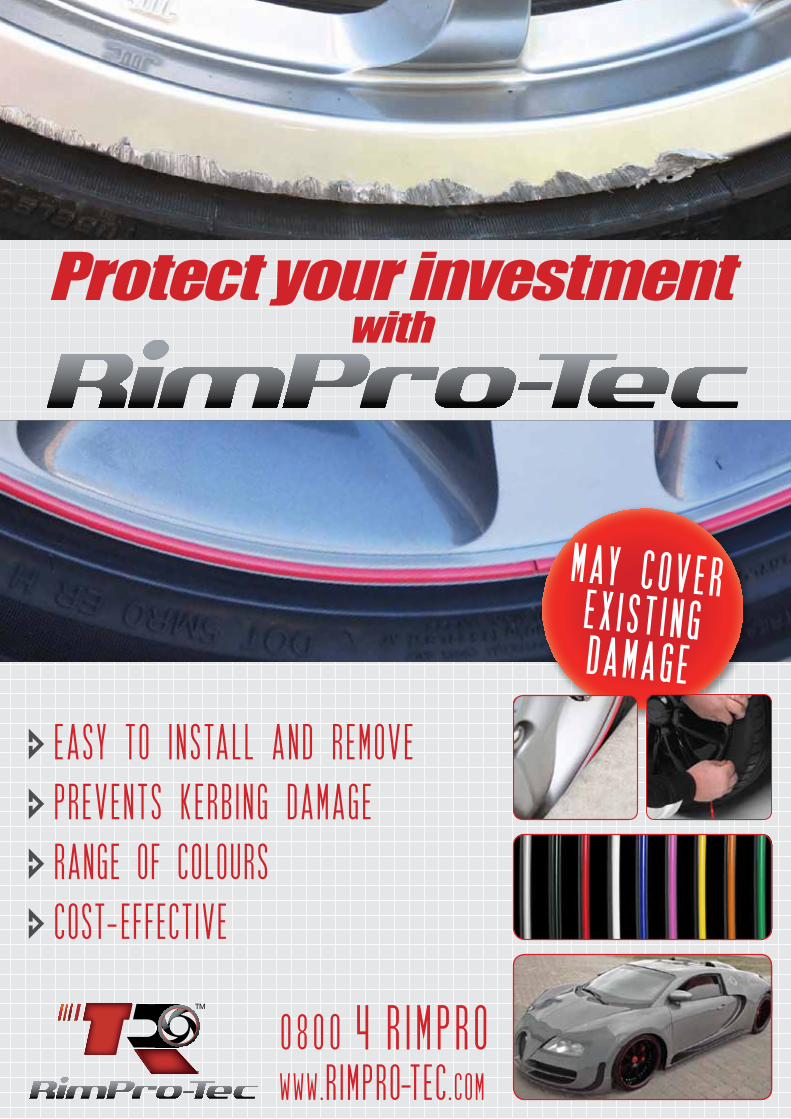

Protect your investmentwith

E A S Y T O I N S TA L L A N D R E M O V E

P R E V E N T S K E R B I N G D A M A G E R A N G E O F C O L O U R S C O S T-E F F E C T I V E

0 8 00 4 R I M P R OWWW.R I M P R O-T E C.C O M

M A Y C O V E R E X I S T I N G D A M A G E

www.autofile.co.nz | 3

editor’s note

Getting fuelled up in the futureIt’s often said that because

New Zealand no longer manufactures as much stuff as

it used to – such as motor vehicles – that this country is more of a technology taker than provider.

That’s not to knock what is made here or belittle how high in the innovation stakes we come.

But perhaps more could be done to prepare us for new technology before it actually arrives on our wharves inside cars, or powering them.

Latest statistics from the Imported Motor Vehicle Industry Association (IMVIA) on what’s happening in Japan shouldn’t be underestimated.

The bottom line is that motorists in that country – the biggest source market for all vehicles crossing our border – are falling in love with hybrids.

Like it or not, the revolution there is in full swing and that will eventually impact on what can be sourced and brought over to be sold on yards here.

The IMVIA’s views are covered in-depth online at www.autofile.co.nz.

Among the news is the fact that Toyota is leading the charge by announcing it will introduce 15 more hybrids in Japan over the next two years to complement its existing fleet.

The two best-sellers there last year were the Aqua and Prius, with the two hybrids making up almost 16 per cent of over-1,000cc registrations.

And the hybrid version of the new Honda Fit accounted for more than 70 per cent of the model’s sales in four months.

The massive rise in the popularity of hybrids in Japan appears to be coming at the expense of some tried and tested models on dealers’ yards here.

There were notable month-on-

month drops in market share for the Nissan Cube and Mazda Demio – both due to be replaced shortly – and sales of Suzuki’s Swift are decreasing.

Another gem of information was that the Nissan’s Leaf was the only pure electric vehicle (EV) to show up in the Japanese charts. It notched up 13,021 registrations in 2013, with a number arriving on these shores.

EVs are continuing to find their feet in New Zealand and their uptake will be slower than hybrids but where Australia leads, surely we can try to follow.

The Leaf scored a sales and exposure goal last year when the Lord Mayor of Sydney took delivery of 10 of the small hatchbacks.

The council’s purchase marked the largest single order of Leafs in Australia at the time and they joined four Mitsubishi i-MiEVs.

They replaced a fleet of Toyota Prius petrol-electric hybrids because the use of zero-emission vehicles was seen as a wholesale gain in an urban environment.

Citizens can also make their own choices about what they drive because dozens of charging points have been installed in council car parks to overcome range anxiety.

It was also interesting to find out that EVs were a common thread at the IMVIA’s national executive meeting in Wellington, which was attended by cabinet members, government officials and representatives of motor vehicle industry associations.

Perhaps it’s time to realise that alternative ways of powering our cars are coming to New Zealand.

It’s already happening in other parts of the world – be that with hybrids, EVs or fuel-cell technology.

Darren RisbyEditor

Copyright: Published twice monthly by 4Media, PO Box 6222, Dunedin 9059 All statements made, although based on information believed to be accurate and reliable, cannot be guaranteed, and no liability can be accepted for any errors or omissions. Reproduction of autofile in whole or part, without written permission, whether by xerography or any other means, is strictly forbidden. All rights reserved.

Editor

darren risby [email protected] 021 137 5430

Journalist & onlinE producEr

cameron carpenter [email protected]

advErtising

Brian Mccutcheon [email protected] 021 455 775

dEsignEr

adrian payne [email protected]

Autofile is also available as an electronic copy via email. If you’d like to receive electronic copies please send an email with your name and organisation to: [email protected]. Back copies are also available on request.

Call Steve Owens now on 021 947 752

AUCKLAND

WELLINGTONNE LSON

KAWASAK I

NAGOYAOSAKA

RVessels arriving every two weeksRServicing Auckland, Wellington, Lyttelton

& Nelson with ‘Direct Port Calls’

w w w . d o l p h i n s h i p p i n g . c o . n z

Full PORT to DOOR service

Karla Sorensen Mob: 0276 796 981 Ph: 09 373 5881 Fx: 09 303 0072Email: [email protected]

JAPAN to

NEW ZEALAND

CALL ME NOW!

L YTT E L TON

4 | www.autofile.co.nz

At a glance The loan-shark law changes include lenders taking responsibility for the likely effect of their credit. They will only be able to provide loans to meet borrowers’ needs and repayments shouldn’t cause substantial hardship.

Companies may be banned for irresponsible lending and there will be tighter controls on misleading adverts.

Repossession will be banned unless specified in the paperwork, while agents and employees will be licensed.

[continued from page 1]

news

of the bill, which defines these proposals, is intended to prevent marques, dealers and financiers from holding duplicate keys.

“Our members submit the cost to replace modern motor vehicle keys is significant,” says McMorran.

“This cost would be passed onto consumers and is one which will often need to be incurred by lenders if the clause is enacted without change.”

The issue is flagged up elsewhere in the bill, which states lenders must not “hold” keys or similar access devices until the goods have been repossessed.

With regard to holding duplicate keys – particularly by car finance companies – the FSF says that seems undesirable because: It would prevent a debtor

voluntarily giving the lender

the keys at the start of the repossession process, which may be sensible for the borrower to do.

There’s nothing wrong with a financier holding a duplicate set after a contract has been signed because this can facilitate repossession to the benefit of everyone concerned.

The FSF wants the word “hold” replaced with “use” in the relevant parts of the legislation to overcome some of the issues.

DEVICES TO BE REGULATEDDisabling devices – including those fitted to vehicles – will be regulated under the bill.

Lenders may not activate one unless the borrower is in default, has been given reasonable notice

it will be activated and advised how to prevent this.

They must not be connected to, or used with, essential household goods and important documents, and devices will be defined by having functions that warn debtors repayments are overdue, prevent goods from being used and limit their use.

Their other functions include enabling creditors to locate goods and achieving beneficial outcomes for lenders.

While the FSF is sympathetic to disabling devices being regulated, McMorran says it’s “odd the regime being proposed is different to repossessions generally”.

GUIDELINES FOR LENDINGThe Credit Contracts and

Disabling devices under scrutinyAccess to goodsPart of the Credit Contracts

and Financial Services Law Reform Bill covers devices that disable goods.

“A contract may not provide for keys or other devices to be held by the creditor prior to repossession,” it states.

When a contract states the creditor has security over the goods, they

must be identified in the contract – and to what the device is

connected and what the right to activate it is.

Is your desk limiting your sales opportunities ? Use MotorWeb where and when it is convenient for you.

Our new mobile responsive website allows access from your smartphone while you are on the move.

Nothing to download or setup; just login to your MotorWeb account or scan the QR code at the base of this page. It’s that simple!

You will then be greeted by our login page with a handy ‘remember me’ function

Now you’re done!

ph 0800 668 679

Paying arrearsThe proposed legislation says creditors must give debtors time to remedy defaults.

“A creditor may repossess goods [for] which a repossession warning notice has been served unless the period for remedying the default has expired and the debtor has failed to remedy [it].”

This will also be the case if the debtor has returned the goods or reinstated the agreement by paying any arrears.

Financial Services Reform Bill will result in responsible lending principles being introduced.

The FSF already has a set of guidelines for its members, which

www.autofile.co.nz | 5

of responsible behaviour are prevented from preying on the vulnerable.

“Enforcement will need to be stepped up on the enactment of this bill.”

She adds there is some “horrendously irresponsible behaviour” in parts of the market, including unjustifiably high interest rates and fees charged by some providers.

The Motor Trade Association is supporting the submission made by the FSF, while three other areas of concern to car dealers have previously been highlighted by Autofile.

One issue is the bill defining

traders and point-of-sale retailers as lenders.

It also says dealers, by being classed as lenders, will have to publish loan terms, borrowing costs, and information on repayment waivers and extended warranties.

The proposals include lenders and traders being banned from charging commission on insurance if people have no

choice but to buy policies from one provider.

McMorran told Autofile: “The Commerce Committee is due to report back in March, so we will see what difference our submissions have made then.”

arrears or repossession action,” explains McMorran.

“This provides bad customers with the

ability to have the loan without paying for it. This disadvantages all consumers because good ones are paying for those who abuse the system.”

It is in financiers’ interests to help customers

through short-term hardship so loans are fully repaid.

“The provider secures payments by dealing with

hardship situations effectively for both parties,” she says.

“Repossession is a last resort. More often than not, it results in recovering less than the debt owed, leaving the borrower with a residual obligation.”

The FSF has entered into a memorandum of understanding with the NZ Federation of Family Budgeting Services.

This requires its members to refer on clients when they recognise borrowers may be under financial stress and heading towards hardship.

‘PREYING ON VULNERABLE’On one hand, the government says its loan-shark laws will better protect borrowers from lenders, especially at the lower end of the market.

On the other, FSF members – which provide finance, investment, banking and insurance services to more than one million Kiwis – already take compliance seriously.

“They abhor irresponsible behaviour in the sector to which they frequently bear witness,” says McMorran.

“The FSF believes enforcement is key to ensuring firms that don’t adhere to high standards

“FSF members abhor irresponsible behaviour in the sector to which they frequently bear witness.” – Lyn McMorran

detail what responsible behaviour entails, and the principles in the bill largely match up with them.

But the federation says lenders being required to help borrowers be aware of the “full” implications of contracts could create issues by being too broad and onerous for the financier.

The FSF would like the period for developing the code after the legislation is passed to be one year – not two – to give lenders clarity.

The federation and its members have also offered to help government officials to develop it.

SYSTEM OPEN TO ABUSEUnder the Credit Contracts and Consumer Finance Act as it stands, borrowers are unable to lodge hardship applications when in default but that’s set to change.

The FSF warns New Zealand must avoid replicating Australia’s system, which is abused.

“If borrowers in Australia claim hardship, lenders must suspend

At a glance The loan-shark law changes include lenders taking responsibility for the likely effect of their credit. They will only be able to provide loans to meet borrowers’ needs and repayments shouldn’t cause substantial hardship.

Companies may be banned for irresponsible lending and there will be tighter controls on misleading adverts.

Repossession will be banned unless specified in the paperwork, while agents and employees will be licensed.

news

RELIABILITYFirst choice for NZ dealers for 20 years

EXPERIENCEOur buyers are knowledgeable about NZ dealers requirements

CHOICE100,000 vehicles per week available through our auction search engine

STOCK READY FOR SHIPPINGExtensive range of pre-purchased stock available for shipping NOW

PEACE OF MINDAll vehicles Ramp Inspected before departure

TRUE DEALER WHOLESALEFixed fee includes all Japan side: transport, documents and taxes

STRICTLY DEALER ONLY Heiwa Auto never sell or export vehicles to private buyers

WITH YOUR CURRENT VEHICLE SUPPLIER

WHAT YOU GET WITH

ARE Y

OUHAPPY?

www.heiwa-auto.co.nzReece McKerrow Ph: 021 988 727 Greg Bardsley Ph: 0279 363 595

Access to goodsPart of the Credit Contracts

and Financial Services Law Reform Bill covers devices that disable goods.

“A contract may not provide for keys or other devices to be held by the creditor prior to repossession,” it states.

When a contract states the creditor has security over the goods, they

must be identified in the contract – and to what the device is

connected and what the right to activate it is.

Paying arrearsThe proposed legislation says creditors must give debtors time to remedy defaults.

“A creditor may repossess goods [for] which a repossession warning notice has been served unless the period for remedying the default has expired and the debtor has failed to remedy [it].”

This will also be the case if the debtor has returned the goods or reinstated the agreement by paying any arrears.

6 | www.autofile.co.nz

newsnews

WE TRANSPORT

• MOTOR VEHICLES

• FARM TRACTORS

• MACHINERY

• AGRICULTURAL EQUIPMENT

• CONSTRUCTION EQUIPMENT

• PLEASURE CRAFT

• CONTAINERS

OTHER SERVICES

• VEHICLE STORAGE

• VEHICLE DISTRIBUTION MANAGEMENT

• HANDLING OF RARE AND RACE CARS

• FILMING PROJECTS

• ENCLOSED TRANSPORTERS

• M.A.F & CUSTOMS FACILITIES

• SECURITY & CONFIDENTIALITY

p: 0800 4 JEFFSe: vehicles: [email protected] pleasure craft: [email protected]: www.jeffs.co.nz

Vehicles revenue boost profitsstatement would have included extra revenue of $4.2m with no significant profit change.

The company describes the cost of the buy-out as “modest” and “a clean purchase at an attractive multiple”, with “earnings accretive, funded from cash”.

It says MotorWeb is strategically aligned with its customers, the industry and for data giving it an opportunity to “strengthen connectivity”, and grow revenue and earnings in a growing market.

Its addition has been positive for earnings before interest, taxes, depreciation and amortisation, but it has increased Trade Me’s expenses and reduced margins.

Trade Me Motors’ total revenue was up by 16 per cent year-on-year, which was led by dealer

revenue and premium uptake.Listing volumes grew by 1.8

per cent and it’s expected this will remain flat. Direct listings rose by 0.8 per cent and those placed by dealers increased by 3.5 per cent.

Details about Trade Me’s acquisition of MotorWeb have been published in

its half-year financial report.Overall, it shows revenue

increasing by seven per cent year-on-year to $85.7 million, while net profits went up by two per cent to $38m.

Jon Macdonald, chief executive officer, says the classifieds division, which includes vehicles, performed well in the six months to December 31 with revenue growth of 17 per cent.

Trade Me Motors has been strengthened by acquiring MotorWeb, the vehicle information authority.

“MotorWeb is an excellent fit given its great reputation and strong expertise in data,” says Macdonald.

“There’s a lot of potential around broadening and deepening products we provide

for buyers and sellers of vehicles.”MotorWeb was acquired through

a combination of asset and share purchases on December 20.

Trade Me paid $19.5m for its assets, which included goodwill of $11.7m, software valued at $7.8m and $71,000 worth of

property, plant and equipment.MotorWeb has had no significant

impact on revenue or profit, but had the takeover happened at the start of the reporting period, Trade Me’s consolidated income

I write in reference to the story in the February 10, 2014, issue of Autofile headlined “traders responsible for WOFs”.

The issue of warrants of fitness covered in this article has previously been subject to appeal in the district court.

The applicant (end user/buyer) claimed the respondent (dealer) was responsible for a seat-belt standards error. A new WOF had been issued and the seat belt had an incorrect standard.

The respondent lost at the Motor Vehicle Disputes Tribunal but appealed. The argument given was the dealer was no different to any person or organisation presenting a vehicle for a WOF.

He argued he was entitled to rely on the WOF-issuing agent to correctly test the subject vehicle and pass or fail it.

The act merely requires the WOF must be properly issued and be no

older than 28 days at the time of sale. A seller complies if the vehicle is presented for inspection by a properly authorised inspection centre.

The responsibility for a poor and incorrect inspection lies technically with the NZTA in the first instance, and then the issuing agent and inspector. The district court judge agreed and the appeal was successful. This precedent is common sense really – the inspection is technical and the inspection manual is a significant document with strict training, audit and equipment criteria.

Any person presenting a vehicle for a WOF at a properly authorised centre must be able to rely on the inspection carried out.

The tribunal referee in this matter covered by Autofile, in my view, has overstepped his jurisdiction.Arthur Murray, Hatchback Autos, Kelston, Auckland

Decision ‘oversteps’ jurisdiction

Email your letters, news and views to [email protected]. Please include your full name and daytime contact details.

Letter to the editor

“There’s a lot of potential around broadening and deepening products we provide for buyers and sellers of vehicles.” – Jon Macdonald, Trade Me

www.autofile.co.nz | 7

news

Yield in the motors division increased from ongoing premium products and dealer price increases.

Dealer yield jumped by 23.3 per cent compared to a direct yield rise of 9.2 per cent.

When it came to premium spend, the average spend per dealer was $288 a month, a year-on-year increase of 38 per cent.

Macdonald says this part of the business delivered innovation with improvements to selling processes, DealerBase, the boats category and new premium products.

Future growth levers include product enhancements – sell process and data – yield opportunities with premium products and people with account management and technology, while there has been some promotional and trade spend.

Overall, Trade Me’s expenses were up by 19 per cent year-on-year.

“This is a hefty increase, but it’s necessary for us to properly convert on the opportunities and position the business for the longer term,” says Macdonald.

The main contributors to the increase were people and marketing, with about 350 staff now employed.

“Trade Me has embarked on a period of reinvestment in the business with slow growth in short-term earnings as costs rise faster than revenue. We are convinced this is the right approach.”

More than half of website visits in January came from mobile devices and Macdonald expects strong growth to continue.

“We’ve put an enormous amount of work into making Trade Me a great experience across tablets and smart phones,” he says.

“E-commerce trends, the migration of advertising revenue to online and growth in online retail are in our favour.

“We expect stronger profit growth as we roll out products, phase in yield improvements in classifieds and increase activity in general items.

“However, we expect to talk about mobile less rather than more as it becomes completely ingrained in the business, rather

than separate to our websites.”Trade Me intends to pay a

dividend of 7.6 cents per share, which it says is consistent with its policy of having payments based on about 80 per cent of net profit after tax.

FLEET BOOST FOR TURNERSTurners Auctions has beaten its own profits forecast and, in doing so, now accounts for about 10 per cent of New Zealand’s used vehicle market.

Net profit rose by 14 per cent to $4.8 million in its 2013 financial year – better than its November estimate of about 10 per cent – while revenue went up by the same proportion to $89.2m.

Revenue from Turners’ higher margin fleet division surged by 30 per cent to $46.9m, but auction revenues fell by one per cent to $36.3m.

Finance revenue rose by 10 per cent to $6m with more people buying cars using consumer finance via the BuyNow service, which boosted its loan book by 20 per cent to $25.6m, while CashNow posted a 56 per cent rise in sales to 7,444.

“There was more focus on end-of-life and damaged vehicles, which accounted for six per cent of 2013’s purchases, but there was an increase in the cost of sales with stock levels growing,” says Todd Hunter, chief executive officer.

“There was a 61 per cent increase in purchases of imported vehicles in 2013 as demand recovered.

“Auction revenues were in line with the previous year, with operating profit impacted by IT investment and one‐off restructure costs.

“Growth in car, truck and machinery revenue offset a drop in damaged vehicle sales.”

Hunter says about 1.3 million used vehicles are sold every year, and Turners is aiming to grow its market share by creating more channels to source and sell them.

“The fleet business will be grown through CashNow to target running and end-of-life vehicles, and improve sales conversion.”

He says BuyNow is a “one-on-one method of sale, which

increases our opportunity to sell add‐on finance and insurance”.

Nine per cent of Turners’ total vehicle sales were through this channel during the 2013 financial year compared to five per cent in 2012.

The company is regularly selling more than 1,000 items per week on Trade Me, while its revamped website was launched in April and is optimised for smart devices and is delivering growth in user traffic – unique browsers in 2013 were up 22 per cent to 1.9m.

With the changing environment, Turners predicts more mobile devices be used to access the web, rising infrastructure costs, vendors pushing for higher yields and a fleet that continues to age exacerbated by emissions regulations.

As first reported online at www.autofile.co.nz, the company’s second half-year was better than the first six months for a final dividend of nine cents per cent and a financial year pay-out of 16 cents.

a fresh approachto dealer finance

we’re in this together

www.MyFinance.co.nz 0800 385 385

Todd Hunter, CEO of Turners Auctions

8 | www.autofile.co.nz

Trans Future 5 Voyage 72

osaka 10 Feb, Nagoya 11 Feb, kawasaki 15 Feb,auckland 5 Mar, lyttelton 7 Mar, wellington 9 Mar, Nelson 10 Mar

Trans Future 6 Voyage 69

osaka 24 Feb, Nagoya 25 Feb, kawasaki 1 Mar,auckland 20 Mar, lyttelton 22 Mar, wellington 24 Mar, Nelson 25 Mar

Morning Miracle Voyage 7

osaka 16 Feb, Nagoya 17 Feb, kawasaki 18 Feb,auckland 8 Mar

news

depreciation, rose by just 4.6 per cent to $56.8m despite the lift in freight volumes and the record number of containers handled in the six months to December 31.

Gibson says: “Productivity has improved since we started restructuring in 2011, which has enabled us to take advantage of an improving economy and Auckland’s growth.”

Since 2011, the company has reorganised its management structure, improved container handling and technology, and 60 per cent of stevedores are now working a flexible shift and roster system.

“Looking ahead, we’re focusing on developing our leaders, increasing opportunities for women and investing in the training,” he adds.

“This year has started well with volumes holding up. As as a result, we recently announced investment to support growth – a larger tug to handle bigger ships and two straddle carriers for rising container numbers.”

Gibson says there’s pressure on ports to become more efficient because supply and demand imbalances are driving down freight rates and hurting big shipping companies.

The port’s next development will be introducing a new terminal management system in July.

This will create a platform for the later introduction of new technology, such as optical recognition to identify containers at crane level and at the port’s gate.

The company has implemented a master-plan to cope with rising freight demand, including cars.

This has involved consolidating the handling of containers to the east at the Fergusson terminal and turning Bledisloe into a multi-purpose terminal.

Bledisloe is now used extensively for all kinds of break-bulk, including cars and other vehicles – plus the occasional container ship.

“This has given us much better flexibility and has meant we are better able to cope with the relentless increase in vehicle numbers,” explains Gibson.

“Captain Cook Wharf was our main berth for roll-on, roll-off vessels and used for car storage, along with Marsden Wharf, but this is now complimented by the more frequent use of berths at Bledisloe and Jellicoe.”

The port’s unaudited net

[continued from page 1]

Master-plan to cope with carsThree roll-on, roll-off vessels discharging cars at Ports of Auckland at, from left, Captain Cook, Bledisloe and Jellicoe wharves

profit after tax increased to $26.4 million for the second half of 2013 compared to $15.5m in the same period of 2012 – as first reported

online at www.autofile.co.nz.The half-year results will see an

interim dividend of $20.94m going to Auckland Council Investments Ltd, which compares to $11.56m for the same period of 2012.

It aims to provide 12 per cent return on equity and Gibson says it isn’t far off that target, but he doesn’t expect this financial year’s second half to be as strong as the first.

Earnings before interest and taxes for port operations went up 47.1 per cent to $40.4m.

Total container volumes increased by 15.1 per cent to 476,333 20-foot equivalent units from 413,884, full import containers were 19.9 per cent higher and full exports rose by 12.9 per cent.

Operating costs, excluding

“We are now better able to cope with the relentless increase in vehicle numbers.” – Tony Gibson

Automotive Holdings Group (AHG), which owns dealerships in Auckland,

made record profits in the last six months of 2013.

Its half-yearly profit was A$38.4 million (NZ$41.59m), which was up 1.3 per cent on the same period in 2012 and came on the back of A$2.32 billion in revenue.

Revenue from vehicle retail operations increased by A$1.916b,

with profits rising by 11 per cent to A$68m.

Managing director Bronte Howson says: “We will continue to explore other opportunities that meet our growth and financial criteria.”

AMG owns the John Andrew and North Harbour Ford and Mazda franchises in Auckland, and last year acquired Manukau’s Davie Motors Holden, which is now also a Nissan dealership.

Growth to be explored

www.autofile.co.nz | 9

The future roll-out of electric vehicles (EVs) was one of the “common

threads” discussed at an Imported Motor Vehicle Industry Association (IMVIA) two-day meeting attended by politicians, government officials and automotive organisations.

Michael Woodhouse, the Associate Minister of Transport, Social Development Minister Paula Bennett and Julie Anne Genter, the Greens’ transport spokesperson, were among those who met with the association’s six-strong national executive in Wellington earlier this month.

“We had very high expectations of the benefits of moving the national executive meeting to the capital and those were exceeded,” says David Vinsen, chief executive of the IMVIA.

“It was all about relationships, structures and how everything operates. It was a chance for people and organisations to understand each other’s differences and where they’re at on different issues.

“We also discussed how to handle those differences and deal with them, while acknowledging the fact we agree to disagree.”

The subject of EVs was on the agenda over the two days.

“EVs were one common thread and we had lively discussions about them,” Vinsen told Autofile.

“This covered what the general issues are – such as safety, market share, power, logistics and infrastructure – and the fact the government’s revenues are likely to go down due to lower fuel sales.”

However, Vinsen believes the introduction of EVs and vehicles with other alternative fuel sources will happen “by default”

news

Industry issues on the agenda

planned and their view of the industry,” explains Vinsen.

“There was also an exchange of views and it was a chance to build relationships.”

Other attendees were David Crawford, CEO of the Motor Industry Association, Mike Noon, the AA’s general manager of motoring affairs and senior policy analyst Mark Stockdale, and Motor Trade Association president David Storey and CEO Rob MacGregor.

“It was a constructive meeting,” says Vinsen. “It was a good indication of how the motor vehicle industry has evolved, how the IMVIA has developed and how relationships have matured.”

The association’s executive and Vinsen spent February 11 and 12 in the capital – and it was the first time in about 12 years they had met in Wellington.

“At the moment, we have two-monthly national executive meetings and they roughly rotate between Auckland and Christchurch,” he says.

“Overall, it was very useful for all parties. I hope we will look to do this more frequently than every 12 years in the future.”

AND OUR DEALERS AGREE!

WE TAKE PRIDE IN CALLING OURSELVES YOUR SOLID FINANCE PARTNERPhone Kim Dwyer

on 021 595 124 Freephone 0800 808 058

or visit avantifi nance.co.nz

+ Fast approval+ Experienced lenders

+ Consistent criteria

Around the table, from left, are the IMVIA’s Frank Willett, David Vinsen, Alistair Sheard, Lloyd Wilson, Graeme Macdonald and Nick Owens

in New Zealand and “we will be constrained by what’s available in Japan”.

The Ministry of Transport’s chief executive officer, Martin Matthews, Leo Mortimer, manager of land transport safety, and Lee McKenzie, team leader on the electronic stability control project, attended.

Geoff Dangerfield, CEO of the NZTA, and its national manager of direction Leigh Mitchell also went along, as did Terry Collins, general manager of products of the Energy Efficiency and Conservation Authority.

“In regards to people from the government, it was about discussing what they had

“It was a good indication of how the motor vehicle industry has evolved and how relationships have matured.”

– David Vinsen, IMVIA

Michael Woodhouse Associate Minister of Transport

Julie Anne Genter Greens’ transport spokesperson

Terry CollinsEECA’s general manager of products

Paula BennettSocial Development Minister

Martin MatthewsCEO of the Ministry of Transport

Geoff DangerfieldCEO of the NZTA

Rob MacGregorMTA CEO

David CrawfordCEO of the MIA

new cars

Toyota’s FT-1 concept

From electric to ‘heart pounding’The Kia Soul EV – the Korean

manufacturer’s first mass-market electric car – has

been unveiled to the world.It’s scheduled to go on sale in

the third quarter of 2014 in the US, with Europe following. It will cost about NZ$50,000 in the UK with the marque here putting its hands up for the model.

The EV, which made its debut at Chicago Motor Show, uses a 27kWh lithium-ion polymer battery with an energy density of 200Wh/kg. It should yield a fully charged range of about 130-160km of real-world driving.

Kia’s regenerative braking system captures up to 12 per cent of its kinetic energy, which feeds into the battery while coasting and braking.

The car plugs into 120 and 240-volt charging points, with times varying from 24 hours for a depleted battery on a 120-volt outlet to less than five hours with 240 volts. An 80 per cent charge can be achieved in 33 minutes with a 50kW-output charger.

The Soul EV has an 81.4kW electric motor. The liquid-cooled AC synchronous permanent magnet motor delivers power to the front wheels through a single-speed constant-ratio gear reduction unit.

Acceleration from 0-100kph should take less than 12 seconds with the top speed limited to about 145kph. It has a virtual-engine sound system that sends out audible alerts below 19kph and when reversing.

The platform accepts battery packs

under the rear seats, which means little of the Soul’s 354-litre boot space has been sacrificed. This does, however, create a weight penalty of about 200kg over standard cars.

The EV gets its own design of 16-inch alloys with super-low rolling resistance tyres with 10 per cent less resistance than standard ones.

The cabin has environmentally friendly materials. Bio-based plastics derived from cellulose and sugar cane are used in many places, such as the door panels, seat trim, roof pillars and carpeting.

Another major attraction in Chicago was Toyota’s racing-car inspired FT-1 concept. It was first devised by Calty Design Research in the PlayStation game Gran Turismo.

It has what the marque calls a “function sculpting” design language shaped by the wind into a “muscle-body form”. At higher speeds, a retractable rear wing tilts forward for extra downforce.

The front-engine rear-wheel-drive configuration locates the cockpit rearward for better weight distribution, which helps create sports-car proportions.

The wraparound windshield and side glass openings are nods from Toyota’s 2000GT of 1967 to the Celica, Supra, MR2 and 86. There’s an F1-inspired steering wheel, while a delta-shaped display zone surrounds and integrates the driver.

The FT-1 follows global president Akio Toyoda’s directive for more emotional car designs displaying energy, passion and “waku-doki” – “a palpable heart-pounding sense of excitement”.

Meanwhile, Subaru chose Chicago to unveil its 2015 Legacy. It’s the same size externally as the 2014 model, but is the roomiest yet with the largest passenger compartment in the mid-size segment.

All-wheel-drive and the flat 2.5-litre four-cylinder and 3.6-litre six-cylinder engines return. But the marque has improved fuel economy with active front-grille shutters, better aerodynamics and continuously variable automatic transmissions.

Handling is aided by a faster ratio steering and electronic torque vectoring that applies the brake to the inside front wheel in turns.

SPEED IN MOTOR CITYBMW chose the show in Detroit to

launch some new models, including the M3 sedan and M4 coupé.

Compared with predecessors, they deliver better performance with a high-revving, straight six-cylinder engine with M TwinPower Turbo technology for 317kW/431hp.

Their suspensions and drivetrains are precision tuned to the engine’s performance characteristics, while lighter weight is achieved with a one-piece driveshaft made of carbon-fibre reinforced plastic to reduce rotating mass for better acceleration.

From a V12 S Class to a winged Smart car, Mercedes-Benz was determined not to be outdone and unveiled its “pure” all-electric model.

First shown in 2012, the B Class was heralded as a “no compromises” luxury EV that didn’t sacrifice seating or space.

Back then, the B Class Electric Drive’s 134hp motor was said to deliver a 200km range and

Kia’s Soul EV

10 | www.autofile.co.nz

www.autofile.co.nz | 11

configuration apparently gives the 200 a “distinctive and recognisable look coming and going”.

COMING UP IN GENEVAThe diesel variant of the Jeep Cherokee with its nine-speed automatic transmission will make its world premiere at next month’s Geneva Motor Show.

The turbo-diesel is available in two versions offering a choice of

170 or 140hp outputs with 350Nm of torque.

The 170hp version of the two-litre engine is coupled with the nine-speed automatic gearbox, while the 140hp unit has a six-speed manual.

Both two-litre versions have stop-start technology to improve fuel efficiency and reduce emissions.

Available in two and four-wheel-drive, the new Cherokee is the first mid-size SUV to have

recharging times of about an hour with a supercharger.

It aims to occupy the space between Nissan’s Leaf and the pricier Tesla Model S.

The all-new all-wheel-drive 2015 Chrysler 200 revealed the marque’s fresh styling “face”.

The mid-size sedan has a nine-speed automatic transmission with the option of a 3.6-litre Pentastar V6 engine or standard 2.4-litre MultiAir2 Tigershark.

The grille and headlamps are integrated for the first time and the updated Chrysler badge has an emphasis on the wing.

The exterior lighting

Toyota New Zealand will continue to source the Camry and Aurion from

Toyota Motor Corporation Australia (TMCA) until 2017, which is when the marque will call time on making cars across the ditch.

The company imported 1,352 Camrys and 455 Aurions from Australia last year, with the two models accounting for about 11 per cent of Toyota’s 16,182 passenger vehicle sales here during 2013.

“Future mid-size sedans will continue to be supplied from a source to be determined,” says Alistair Davis, chief executive of Toyota NZ.

Alternative source markets for the Camry and Aurion have yet to be identified and it’s against company policy “to discuss future model planning four years ahead”, adds Davis, who is also a non-executive board member of TMCA.

However, he says stock-holding policies here will not be reviewed, while there will be no effect on the supply of parts for and the

servicing of Toyotas made in Australian and sold here pre- and post-manufacturing there.

Toyota’s exit for car making across the Tasman will result in about 2,500 people losing their jobs, with the decision coming after Holden and Ford announced they were also pulling the plug over the next three years.

Its AU$330 million Altona engine plant, which was commissioned last year, will close while its specialist technical and design centre in Melbourne, which supports Toyota’s global operations, may be scaled back.

The company puts its exit down to the unfavourable Aussie dollar making exports unviable, high manufacturing costs and low economies of scale for production.

Meanwhile, Ford may cut its line rate at Broadmeadows, Victoria, to 80 units a day in June as it realigns production to the dwindling demand for its Australian-built vehicles.

Supply to be unaffected

rear-axle disconnect. This reduces friction and energy loss when four-by-four capability isn’t needed.

Inside, the seven-inch full-colour instrument cluster allows the driver to have a customised experience for receiving information and vehicle feedback.

Standard safety features include seven airbags, electronic stability control with roll-over mitigation, and ABS with on and off-road calibration.

Options include forward collision warning-plus, park assist, adaptive cruise control-plus, blind-spot monitoring and rear cross-path detection.

If you have a proven sale record then we want you.

We are looking for someone who has shown they can succeed in sales. That person must have good communication skills, be customer orientated and be able to find a solution to customer needs.

In return we will provide a good base salary, company car plus competitive commission structure, but the sky is the limit. And best of all you’ll get to live in sunny Nelson!

Bowater Hyundai is a leading Nelson business who has been in business for 65 years. We need to increase our sales team, could that person be you?

If this sounds interesting then email me your CV today [email protected]

new cars

Mercedes-Benz’s B Class Electric Drive

Subaru’s 2015 LegacyThe 2015 Chrysler 200

12 | www.autofile.co.nz

There’s a perception of Hamilton being a “cow-bell town” but dairying

is only one aspect of the region’s economy, which includes food and high-tech manufacturing, forestry and wood production.

Waikato Chamber of Commerce also says it’s the most important mineral-producing area in New Zealand – and these sectors combined account for 8.5 per cent of the country’s gross domestic product.

Sandra Perry, chief executive officer, says: “The manufacturing and engineering sectors continue to grow, particularly larger companies that have secured new contracts.”

She says the business community’s general sentiments are positive and optimistic after a tough couple of years.

“We have a population younger than the national average and we’re well-positioned as a region to support the business and housing overflow from Auckland.”

Waikato is, however, the country’s largest dairying region and as Fonterra boosted its pay-outs last

year, car sales drove up as well. New car sales totalled 5,258

last year. This was a 13 per cent increase on 2012, putting it ahead of the rest of the country by six per cent on average.

There were 6,052 used imports sold, up by 27 per cent on 2012 and one per cent above the national average.

“The high sales have been instigated by the rural sector,” says Andrew Unternährer, general sales manager of Ebbett Prestige, Hamilton.

“There’s a renewed confidence in the building sector. It had been quiet for the past few years, but it seems to have come right.”

He believes Auckland’s rising property prices may benefit Waikato because housing there is more affordable.

“It’s becoming a more desirable place to live and there’s potential for a large amount of growth.”

The region’s population grew by six per cent since 2006 according to the 2013 census, taking its head count up 22,815 to 403,638.

Unternährer has also seen Hamilton transition into a

More than a cow-bell town

market with bigger dealerships.“I don’t think we’ll see the

days of a large number of smaller dealerships again,” he says. “Economies of scale mean larger groups are more viable, while big margins have gone.”

Grant Chapman, of 4Guys Autobarn, told Autofile: “There are tonnes of developments going on in Hamilton, such as the new velodrome and the national cycleway coming through here.”

“We have the farming industry and we’re a go-to city. We get a lot of people from the surrounding towns coming in.”

Euan Means, dealer principal at

Ingham Hyundai, says business has tripled since 2012 and he’s hoping to top that by 20 per cent in 2014.

“I’ve been in Hamilton for a year and the big driver is all dealers do an exceptionally good job,” he says. “I’ve never heard of a customer having a bad experience with another dealer here.”

Means believes low house prices make it more affordable for younger families to go out and purchase a new car.

“There’s a young population that has more disposable income. If I had to guess, our customers are 20 years younger than the clients I had in Taranaki.”

regional report

Vehicle sales in city - Jan 2013 to Jan 2014

USeD CarS New CarS USeD CoMMS New CoMMS

Jan ‘13 443 429 36 232

Feb ‘13 483 412 31 166

Mar ‘13 514 498 30 247

Apr ‘13 448 414 29 217

May ‘13 502 433 45 284

Jun ‘13 484 516 35 340

Jul ‘13 583 474 44 287

Aug ‘13 509 429 36 248

Sept ‘13 460 465 24 267

Oct ‘13 495 424 31 274

Nov ‘13 546 441 37 240

Dec ‘13 585 323 30 172

Jan ‘14 655 565 29 215

12 month total 6264 5394 401 2957

NZ sales - past 12 months 101044 83341 6292 31188

% of national sales 6.2% 6.5% 6.4% 9.5%

Increase on Jan 2013 33% 8% -29% 23%

Job opportunitiesMary-Anne Martin, pictured, a business manager with the Motor Trade Association, says repairers in the Waikato generally have busy workshops at the moment.

“Some are busier than others. Those not doing so well could probably look at their pricing structures.”

Martin says collision repairers are facing uncertainty as they prepare for changes from insurers that could hurt their businesses.

“Some are also expressing concern about where the future technicians are coming from. They are reiterating too few young people are coming into the trade.”

Overall, the Waikato has a lower educational attainment than the rest of the country with some communities experiencing high levels of social deprivation, a report on its economy shows.

Used car sales for Hamilton - Jan 2013 to Jan 2014

TraDer To PUblIC

PUblIC To PUblIC

PUblIC To TraDer

ToTalTraDer To

PUblIC %PUblIC To PUblIC %

PUblIC To TraDer %

Jan ‘13 1131 2854 1285 5270

Feb ‘13 1077 2934 1263 5274 20.4% 55.6% 23.9%

Mar ‘13 1129 2977 1277 5383 21.0% 55.3% 23.7%

Apr ‘13 1295 2898 1361 5554 23.3% 52.2% 24.5%

May ‘13 1210 3271 1503 5984 20.2% 54.7% 25.1%

Jun ‘13 1036 2931 1241 5208 19.9% 56.3% 23.8%

Jul ‘13 1356 3347 1602 6305 21.5% 53.1% 25.4%

Aug ‘13 1223 3208 1514 5945 20.6% 54.0% 25.5%

Sept ‘13 1184 2832 1425 5441 21.8% 52.0% 26.2%

Oct ‘13 1251 2953 1527 5731 21.8% 51.5% 26.6%

Nov ‘13 1091 3088 1378 5557 19.6% 55.6% 24.8%

Dec ‘13 1035 2886 1321 5242 19.7% 55.1% 25.2%

Jan ‘14 1203 2911 1366 5480 22.0% 53.1% 24.9%

annual total 14090 36236 16778 67104 21.0% 54.0% 25.0%

Increase on Jan 2013 6.4% 2.0% 6.3% 4.0%

National YTD average

18.8% 56.6% 24.6%

Shaune Carruthers, of Waikato Toyota in Te Awamutu, with a happy customer and her new 86

www.autofile.co.nz | 13

Reliable fortnightly vehicle logistics

service JAPAN to NZ

PORT TO PORT / DOOR TO DOOR

to Auckland, Christchurch, Wellington, and Nelson

Full MPI inspection service from Kawasaki,

Osaka, and Nagoya

+ Marine Insurance available

Torhild Mellow 021 2253749 or 09 918 [email protected]

Anna Raina09 918 1305 [email protected]

FOR EFFICIENT CUSTOMER FOCUSED SERVICE CONTACT NYK

SSUUNN PPHHOOEENNIIXX CCOO..,,LLTTDD..

F R E E P H O N E 0 8 0 0 8 0 8 2 6 2

buy utes, they also buy SUVs for their families.”

His dealership shares a Toyota stand with its other dealers in the region and they work towards achieving a combined sales target.

Neil Waka, of Holden New Zealand, points out the event is one of the year’s biggest selling

STACKING UP THE NUMBERSThe national proportion of new passenger cars sold in Hamilton over the past 12 months was 6.47 per cent, with the region accounting for less than five per cent of the national population.

New commercials made up 9.48 per cent of national sales over the same period.

Private vehicle sales were 2.56 per cent less than the national average, which indicates Hamiltonians are more supportive of dealers.

And there were 2.16 per cent more trade-ins, while sales from traders were 0.4 per cent more than the rest of the country on average.

Overall, the city accounted for 2,742 new commercial sales in the past 12 months, while there were 372 used commercial registrations.

Those statistics are reinforced by the Navara being Jim Wright Nissan’s strongest performer, for example.

“We’re expecting a new model in the last quarter,” says managing director Jim Wright.

“It’s nowhere near in time for Fieldays but that would only be a

problem if it wasn’t performing so well, with the Navara outselling the Hilux in January.

“And when the rural sector is strong, Hamilton thrives.”

Even with the strong dairy boom, some farmers are cautious in case there’s a drought over the coming months, according to Shaune Carruthers, manager of

Waikato Toyota’s Te Awamutu branch.

“Farmers aren’t spending like they used to and we’re also getting a bit of stick from the competition,” he says. “The Ford Ranger isn’t a big competitor in this area, but Holden’s Colorado is.

“Most farmers have a three-year-old ute, which is still pretty reliable.”

In June, marques attend Fieldays at Mystery Creek, which is essential for developing leads and sales.

It’s the largest exhibition of its kind in Australasia, with more than 120,000

people going along over four days – and every manufacturer is there competing for a slice of the rural market.

Carruthers is hoping for a sales boost then. “The new Highlander is coming up. Even though farmers

periods for commercial vehicles.“Holden achieved about 25

actual sales at Fieldays in 2013 and received more than 50 leads,” he told Autofile.

“Rosetown Holden in Te Awamutu, which helps co-ordinate our side of the show, is the main recipient.”

regional report

What’s in a name?The Waikato Times says The Tron comes from a UFM competition in 1998. The station wanted “Hamiltron – city of the future” to replace the motto “Hamilton – where it’s happening”.

The Tron is believed to have been inspired by the movie of the same name.

Waikato generates more power than any other region, while 403,638 people live there and 168,800 are Hamiltonians.

“We’re well-positioned to support the overflow from Auckland.” – Sandra Perry, Waikato Chamber of Commerce

To adverTise here, conTacT:

Vehicles wanted

[email protected] 021 455 775

dealers Buying now

NewS in briefInternational winner has market limitationsA Kia has been voted international car of the year at Detroit Motor Show for the second time – the Cadenza, pictured, is a luxury model that sits above the mid-to-large Optima that won last year.

While the Optima is sold worldwide and has been face-lifted for New Zealand, the Cadenza is only available in selective left-hand-drive markets and was introduced to the US last year.

The fact you can’t buy it here hasn’t put the brakes on Kia Motors NZ’s party. “Winning the award shows Kia is coming of age,” says general manager Todd McDonald. “You don’t win prizes for coming second.”

Models to have form of power in mind from startNissan has refused to rule out an electric version of the next-generation Qashqai. Guillaume Cartier, sales and marketing boss in Europe, says such a model wouldn’t be “for now” suggesting it may become a reality.

An electric Qashqai could build on the Leaf’s technology, which was further developed with the NV200 EV.

Cartier says Nissan’s electric-vehicle line-up will grow but technology won’t be retrofitted. New models will be designed with electric propulsion in mind.

More industry news online at www.autofile.co.nzAlfa Romeo’s 4C was named 2013’s most beautiful car at the International Automobile Festival in France. It took out 41 per cent of the votes, ahead of the BMW Series 4 with 25 per cent.

Hyundai’s fourth-quarter profits increased by 13 per cent to about NZ$2.3 billion thanks to higher overseas sales, but earnings for the whole of 2013 dropped.

New truck sales in Japan last year jumped by 102 per cent to 801,975. Mini-sized trucks were the most popular on 422,820 sales.

World’s biggest marque enters electric marketIt was only a matter of time before Toyota entered the electric vehicle (EV) market – and it has done so with the Ranz.

Based on the previous Corolla EX, it’s part of a sub-brand of the FAW-Toyota joint venture that’s focusing on making cheap EVs. Its 95hp electric motor will have a Chinese government-approved top speed of 120kph and a range of about 100km.

The first Ranz will be going on sale in Shanghai in April. Pricing is expected to be about NZ$21,500 and other markets may be considered in the future.

Dealers advised to ensure fuel labels are correctThe Energy Efficiency and Conservation Authority will be carrying out surveys during 2014.

If officials are checking heat-pump or refrigerator retailers in an area, it’s likely they will also visit car dealers, so the Imported Motor Vehicle Industry Association advises it’s a good time to check all stock has up-to-date fuel-economy labels.

ALWAYS BUYING GOOD NZ NEW VEHICLES

Call Guy Walker 021 992 048

VEHICLES WANTED

Simon O’Reilly 021 31 9992 [email protected] www.armstrongprestige.com I I I

ALL PORSCHE, LAND ROVERS, RANGE ROVERS, JAGUARS AND VOLVO MODELS

Contact Gareth 021660180 [email protected] www.317.co.nz

Buying: Vans, Utes, Light Trucks. Nationwide.

Brett Harris 029 293 1232 [email protected] www.farmerautovillage.co.nz

VWAudi

WE PURCHASE NZ NEW CARS AND COMMERCIALS FOR ALL OUR FRANCHISES

miles motor groupPAUL CURiN 0274 333 303 [email protected]

Mercedes BenzVolkswagen

BMwaudi

lexusKia

toyotanissanchryslerJeep dodge

VEHICLES WANTED

We are always looking to purchase late model NZ NEW CARS AND COMMERCIALS

www.autofile.co.nz | 15

news

The Commerce Commission is calling for submissions on IAG wanting to acquire 100

per cent of the shares in Lumley.A preliminary issues statement

details existing and potential competition matters it considers will be important in deciding whether or not to grant clearance.

Underwriting levels are under the spotlight, while a decision will be based on the Commerce Act and made by March 28.

The Motor Trade Association has already met with the commission to highlight issues.

“We’re concerned with the impact on collision repairers and a squeeze on labour rates, in particular for non-approved repairers,” says Dougal Morrison, advocacy and training manager.

“IAG is reviewing approved repairers and since it took over AMI

level,” it says. “We will also consider the impact on the distribution of intermediaries.”

The takeover involves overlapping products, so categories will be considered. These include private and commercial vehicles, commercial property and liability.

Because of an overlap in vehicle products, auto-glass and windscreen and collision repair services will be considered.

Buyers being able to switch providers if the merged entity raises prices will be probed, as will IAG being strengthened to decrease competition in windscreen and collision repairs.

IAG’s direct insurance brands are State and AMI, while NZI is intermediated.

It also owns DriveRight, which provides mechanical breakdown insurance. It’s no longer taking on new

there’s been a decrease in loss ratio over the past five years. This means it isn’t paying out as much but the cost of labour has hardly moved.”

Morrison adds the takeover may affect premiums and car dealers offering products such as mechanical warranties.

Lyn McMorran, executive director of the Financial Services Federation, which represents many automotive lenders, says the feeling among members is that Lumley’s pretty small.

“It doesn’t have a huge market share and most of its vehicle insurance is through Westpac so it shouldn’t make a great deal of difference.”

The commission will assess whether the merger is likely to result in a substantial lessening of competition.

“The acquisition would result in aggregation at underwriting

mechanical breakdown, guaranteed asset protection and payment protection insurance business.

Although DriveRight has accepted no new clients since November 1, existing policies will continue until their documented inclusion.

IAG also owns Swann Insurance, which provides classic car and motorbike and financial insurance protection, and runs Harley-Davidson Insurance Services.

Lumley has three divisions – broker, business solutions and finance – as well as general and professional liability, commercial vehicle products and a fleet management system.

The commission’s preliminary report is online at www.comcom.govt.nz. Submissions can be emailed to [email protected] with IAG/Lumley in the subject line or posted to PO Box 2351, Wellington 6140, by 4pm on February 21.

Call for views on takeover

Toyota has issued a precautionary recall on 1,003 Priuses sold new

here and made between March 2009 and February 2014.

Potential malfunctions with their electronic control units can be caused by high operating environment temperatures.

They can be damaged if increased thermal stress occurs, which would result in warning lights coming on.

In most cases, the cars would enter fail-safe mode. In limited instances, the entire system could switch off.

There have been no reported failures related to the problem here and it would be unlikely to happen because Kiwi conditions

mean engines generally don’t reach temperatures where this could be an issue.

A free software upgrade will fix the fault and take about one hour, while used imports brought to the marque’s attention will receive the work if needed.

The recall affects almost two million units worldwide. Toyota is aware of more than 400 cases of the problem, including 90 in North America and 300 in Japan, but no accidents have been reported.

The marque has also instructed dealers in North America to stop selling six models with heated seats because their fabric fails to comply with US standards, but none sold here are affected.

Control unit recall

Toyota's Prius

16 | www.autofile.co.nz

Five and dime in disguise

The IMVIa Technical report is proudly brought to you by leading certifi cation service provider, VINZ

from the trade and for the trade

foisted on us. This time it’s coming from different low-wage source markets, such as China, Sri Lanka and other developing countries.

I’m not talking about vehicles made in those places because manufacturers must meet strict standards.

For example, Kiwis buy toasters from major chains at low prices. When they pack up, they get replacements then moan about the junk they’re being sold.

The same can be said about some after-market car parts. You can buy brake-disc pads for ridiculously low prices, but later find they have to be replaced many times within the distance a quality set would last.

A lot of people are screwing down prices of car parts until the quality is lacking

When I was growing up in the 1950s, the cars we were driving

were referred to as “Brit sh*t” and “Yank tanks”.

The products on the shelves of Woolworths and McKenzies were – in the main – called “Jap crap”, while in the 1960s the first Japanese motorbikes and cars were talked about in the same vernacular.

But were these derogatory terms warranted? In many cases they were.

We had shocking vehicles on the road sourced from UK and US manufacturers, and we had rubbish being sold to the consumer from – as Americans called them – five-and-dime stores.

Are things any better today? I believe they are. We have a much better fleet that meets international safety and environmental standards, and it’s far more durable and better built than 1940s-60s vehicles.

Consumer goods from Japan are now recognised as world class and leaders in their fields.

My gripe is we still have cheap, mass-produced junk being

tech report

places, they look for the cheapest price – where quality is low – instead of paying a few more dollars.

A product sold for $25 today may retail for $35 and be of much better quality and durability had the distribution chain paid another $1 to the manufacturer for a better product.

Are we doing so-called “China Incorporated” and other developing economies a dis-service? I believe we are because we complain about “Chinese junk” as we complained about “Jap crap” in the 1950s and ‘60s.

If we vote with our feet and buy better quality items, retailers will ask themselves why products aren’t selling.

They will realise consumers want better products and change supply arrangements to ensure they are available.

Will this be cost-effective? Yes it will because there will be less waste and fewer replacement costs because products will be more durable.

China Incorporated, as Japan Incorporated did, will come to realise quality will be increasingly required by developed nations – as is in the car industry where requirements are standards based.

I’m not knocking Chinese manufacturing because top-quality products are coming from there in the electronic and other fields.

But when we will realise we can change product quality on retailers’ shelves? As soon as we decide we can make a difference, the sooner change will come.

– all for a few dollars.This market has a real

effect on the fleet’s safety – cheap brake pads wear out faster and increase the chance of in-service failure.

Dealers should bear in mind the quality of parts put in their vehicles – they need to pass

warrants of fitness and be fit for purpose so they comply with safety and consumer protection laws.

But is buying cheap, sub-standard parts cost-effective? No. The cost of parts and labour for replacements exceeds using a quality product in the first place.

Can we change this? Of course we can. When distribution chains buy products from China and other

JEVIC NZ 09 966 1779 www.jevic.co.nzNew Zealand

Japan

Singaporenngnngin

Specialists in Pre Shipment Inspections Full Border Inspections Biosecurity Inspections

Structural Inspections Odometer Verification

Pre Export Appraisal Vehicle History Reports

JEVIC Authorised NZTA Border Inspection Agency

MALCOLM YORSTONIMVIA membership and

technical services manager

A postcard view, above, of a FW Woolworth Co shop in the 1930s, while its first

five-and-dime store opened in New York in 1878. A poster, right, from Australian-owned Woolworths in Levin around 1949.

www.autofile.co.nz | 17

The automotive industry is highly competitive, and

reaching sales targets is often challenging and sometimes impossible to achieve month after month and year after year.

While there are effective sales and marketing initiatives to achieve targets, they don’t always support long-term strategies.

Without long-term strategies, dealers may face added pressures and challenges, ranging from unattainable sales targets to decreasing levels of employee satisfaction, performance and retention.

Niche industry provider, Protecta Insurance, has worked with a range of dealers over the past 30 years and has seen clients with similar strengths and weaknesses.

While some of these weaknesses are indicative of industry, there are many that aren’t and they could be prevented through long-term strategies.

In response to industry challenges, Protecta could see clients needed more from their insurance provider so the company shifted its focus from selling products to selling service and expertise.

It achieved this by taking a proactive approach to helping clients achieve sales targets.

Stephen Glading, managing director of Protecta Insurance, says: “Selling competitively priced products has never been a challenge for us and possibly not for other insurance providers either.

“We know the industry well because we have been working in it for a long time. We wanted to be able to show greater value to our clients, so we diversified our business to include specialist finance and insurance [F&I] training.”

Protecta’s F&I training is facilitated by Erin Mills, who has extensive experience working in

the business manager’s seat for some of Australasia’s largest dealers.

Her understanding of what makes a great business manager and having a great sales team are paying dividends for Protecta’s dealers.

Mills says: “It’s rewarding for me to be

able to continue working alongside an industry I built my career in and to share my 20 years’ worth of skills, experience and passion.

“Clients are growing more and more aware of our F&I training and we’re finding an increasing demand from dealers to consult with them on their sales capability and how we can assist.”

Protecta’s intensive one-day workshops are also benefiting clients by increasing product knowledge – and building individual and team confidence in a practical and interactive way.

“Most dealerships face similar, if not the same, challenges,” explains Mills. “Without industry experience and a deep understanding, I wouldn’t be able to deliver results-focused F&I training to strengthen long-term sales functions.

“I believe the critical attributes of business managers are high degrees of motivation, and the ability to build and maintain productive relationships with their teams.

“Sales teams and business managers need to be working in unison to optimise every sales opportunity. These are the kinds of areas our workshops also cover.

“I recommend dealers who think they may be able to strengthen their workforce through specialist F&I training to get in touch with me today to see how I may be able to assist.”

For more details, call Erin Mills at Protecta on 021-807-148 or email [email protected].

Specialist training is helping our motor dealers to achieve

longer term sales targets.

We’re raising the bar...

contact: erin Mills from Protecta insurance

Phone: 021 807 148 email: [email protected]

Find out more today.

Specialist training delivers dividends

f & i stats

13%

12%

18%

11%

38%

29%

40%

13%

49%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% 55%

Fina

nce

Paym

ent

prot

ectio

n GA

P In

sura

nce

MBI

New

Used

Best result $ 1,362Worst result $ 464

PROTECTA Nationwide F & I resultsJanuary 2014

ERiN MiLLSBusiness development

manager, Protecta insurance NZ Ltd

18 | www.autofile.co.nz

BackgroundScott Harvey bought a 1999 Mitsubishi Chariot for $7,999 – funded by swapping a 2004 Holden Barina – from Orange Autos Ltd on May 24 last year.

On July 8, he traded in the Mitsubishi for a 2006 Suzuki SX4 and a purchase price of $12,000.

The buyer rejected the Suzuki after its transmission failed and claimed he also rejected the Mitsubishi.

The trader said Harvey wasn’t entitled to a refund on either vehicle because he didn’t reject the Chariot and the SX4 was repaired.

The caseHarvey paid for the Mitsubishi through swapping and trading in his Barina. The vehicle offer and sale agreement (VOSA) recorded the swap’s value at $7,999 and the Chariot had 129,975km on its clock.

Within a few days, the Mitsubishi started shuddering and Harvey didn’t know what was wrong with it. The car shuddered at 70-80kph but the problem worsened and became evident at other speeds.

Harvey took the Chariot back to the trader and said he no longer wanted it. The dealer denied telling him it didn’t “do” refunds.

Carl Loader, the trader’s manager, said the value given to the Mitsubishi was $6,500 – $1,500 less than on the original VOSA.

The Suzuki’s total price was $12,000 and its odometer was on 81,831km when sold.

Harvey didn’t pay attention to the Mitsubishi’s recorded trade-in value because he was focusing on the money he needed to secure the Suzuki.

About three weeks after Harvey bought the SX4, its transmission

failed causing the car to go into limp mode.

On July 30, Loader told Harvey he would fix it. Harvey told him he wanted a refund and for the car to be returned.

Loader said that under the Consumer Guarantees Act (CGA) he had the right to repair it within a reasonable time.

The next day, Harvey texted Loader asking to be kept informed of what repairs were needed.

He wanted to know the extent of the damage and consider what remedy he might be entitled to. Loader refused his request to arrange an independent inspection.

Loader emailed Harvey on August 5 to say the transmission had been stripped, parts were coming and the work would take about eight hours.

A second-hand transmission was located in Wanganui that day and shipped to Autoshop Ltd to be fitted.

Harvey contacted Ryan Gerard at Autoshop and found out that parts referred to in Loader’s email included the transmission.

The same day Harvey wrote to Loader rejecting the Suzuki claiming it was a substantial failure of the CGA’s guarantee of acceptable quality.

The trader didn’t accept Harvey was entitled to reject the car because he collected the Suzuki and continued to pay its insurance.

Harvey said he did this to ensure it was safe until the application was determined, there had been some use of the car and its November 9 odometer reading was 83,340km.

Loader disputed Harvey rejected the Chariot and decided to

trade out of the Mitsubishi. In regard to the Suzuki,

Loader said the trader had met its CGA responsibilities by repairing the car in a reasonable time and Harvey wasn’t entitled to reject it because it was repairable.

Autoshop charged the dealer $639 to remove, strip and inspect the transmission, fit the second-hand one and refill it.

The replacement transmission from Wanganui Auto Wreckers cost $1,748. All of the repairs came to $2,387.

Ryan Gerard, who carried out the work, said this included a trade discount and the alternative was to rebuild the transmission, which would have cost about $3,000.

He said a bearing inside it had failed causing metal filings to be distributed throughout it.

The likely cause of the Suzuki losing drive was the filings getting into the valve body causing the valves controlling fluid pressure to the clutch packs to stick.

Loader said the Mitsubishi needed only a minor repair, with a knock sensor replaced for $265.

The ruling The Mitsubishi was 14 years old with 129,975km on the clock when sold for $7,999. Its failed knock sensor was repaired at minimal cost.

In most cases, such a fault wouldn’t fail the guarantee of acceptable quality but given it occurred within a week of purchase, the tribunal ruled it did.

The Suzuki was seven years old and had 81,831km on the clock when sold for $12,000. Within a month, the transmission needed replacing.

The tribunal ruled it failed

The case: The buyer rejected

a Suzuki SX4 after its transmission

failed and also claimed to reject

a Mitsubishi Chariot. The dealer said the customer didn’t reject the

Chariot and the SX4 was repaired.

The decision: The tribunal

ruled the purchaser had no right

rejecting the Chariot because there was no failure to fix the problem. But he was entitled to reject the Suzuki because its issues were substantial.

At: The Motor Vehicle Disputes

Tribunal, Christchurch.

the CGA guarantee because no reasonable buyer would regard as acceptable a car that needed repairs amounting to about 20 per cent of its price a month later.

It found the knock sensor failure wasn’t substantial. It wasn’t persuaded a reasonable buyer would have decided not to purchase the Mitsubishi with full knowledge of this problem.

But the Suzuki’s failure was significant and the tribunal was satisfied a reasonable purchaser – acquainted with the failure’s nature and extent – wouldn’t have bought it.

Harvey asked the trader to fix the Mitsubishi and didn’t have the right to reject it because there was no failure to repair.

There was no evidence Harvey asked for it to be repaired and nor was the failure substantial, which would have entitled him to reject.

However, Harvey was entitled to reject the Suzuki because of the transmission failure. He did this promptly once he knew what the problem was and the tribunal ruled this rejection was lawful.

Orders The rejection of the Suzuki was upheld and the trader was ordered to pay $12,000 to Harvey, who was to return the car after payment. The Mitsubishi’s rejection was dismissed.

Dealer’s repairs on vehicle defeats one out of two rejection applications

disputes

5500

6000

6500

7000

7500

8000

8500

9000

9500

10000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013

2012

17%

12%

13%

9%

41%

14%

22%

16%

43%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% 55%

Fina

nce

Paym

ent

prot

ectio

n GA

P In

sura

nce

MBI

New

Used

Whangarei Auckland Hamilton Thames Tauranga Rotorua Gisborne Napier New Plymouth Wanganui Palmerston North Masterton Wellington Nelson Blenheim Greymouth Whangarei Auckland Hamilton Thames Tauranga Rotorua Gisborne

Napier New Plymouth Wanganui Palmerston North Masterton Wellington Nelson Blenheim Greymouth Westport Christchurch Timaru Oamaru Dunedin

Invercargill Whangarei Auckland Hamilton Thames Tauranga Rotorua Gisborne Napier New Plymouth

Wanganui Palmerston North Masterton Wellington Nelson Blenheim Greymouth Whangarei Auckland Hamilton Thames Tauranga Rotorua

Ar

ou

n d t h e c ou nt

ry

20 | www.autofile.co.nz

0800 7000 44autoport.netwww.

UK, Japanese and local vehicles.Finance available.

The TRUSTED online wholesale trading site.

PHONE 0800 ARMACUP (276 2287) or 09 303 3314EMAIL [email protected]

www.armacup.com