attracting and retaining key employees while protecting...

TRANSCRIPT

ATTRACTING AND RETAINING KEY EMPLOYEES

WHILE PROTECTING YOUR BUSINESS

Presented By

Robert M. HaleMarian A. Tse

H. David HenkenJoseph A. PiacquadDavid A. Elchoness

Sarah H. Minifie

Copyright 2000 Labor and Employment Department, ERISA/Employee BenefitsDepartment and the Private Equity Group of Goodwin, Procter & Hoar LLP. All rightsreserved, including the right to reproduce these materials or portions thereof, in any form,except for the inclusion of brief quotations in a review. All inquiries should be addressedto Labor & Employment Law Department, Goodwin, Procter & Hoar LLP, Exchange Place,Boston, MA 02109 or visit our website at www.gph.com to access seminar materialspresented today as well as materials from earlier seminars.

(i)i

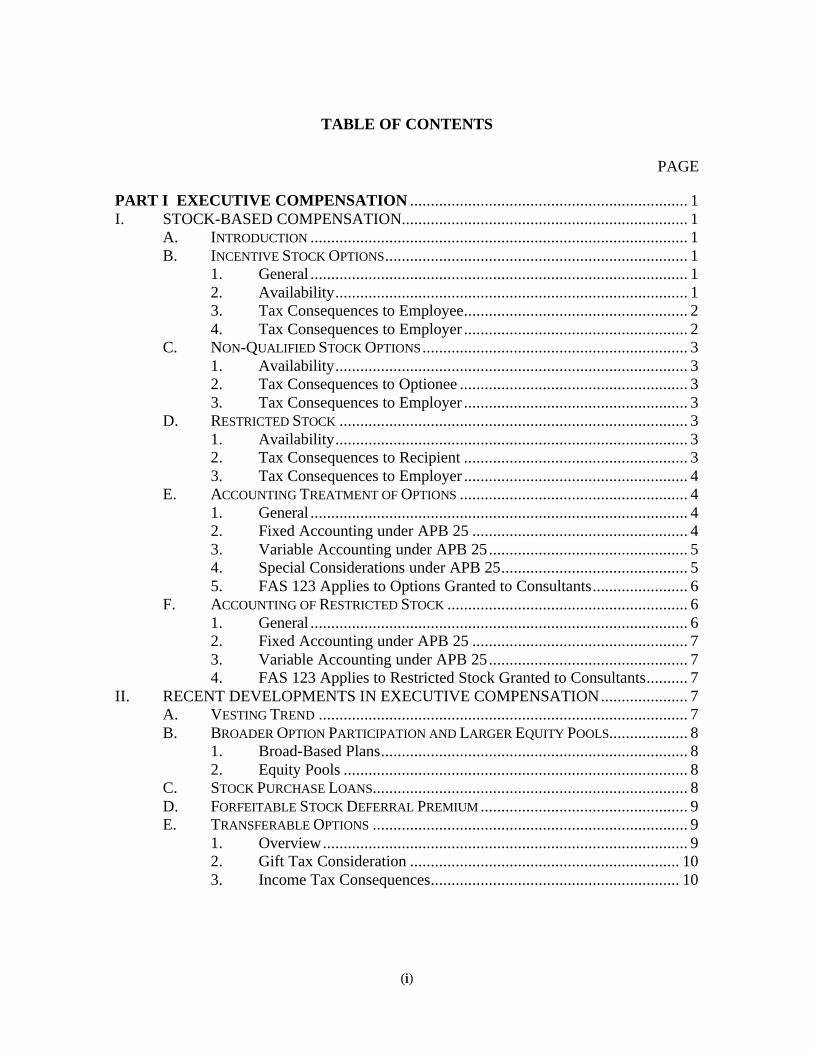

TABLE OF CONTENTS

PAGE

PART I EXECUTIVE COMPENSATION ................................................................... 1I. STOCK-BASED COMPENSATION..................................................................... 1

A. INTRODUCTION ........................................................................................... 1B. INCENTIVE STOCK OPTIONS......................................................................... 1

1. General ........................................................................................... 12. Availability..................................................................................... 13. Tax Consequences to Employee...................................................... 24. Tax Consequences to Employer ...................................................... 2

C. NON-QUALIFIED STOCK OPTIONS ................................................................ 31. Availability..................................................................................... 32. Tax Consequences to Optionee ....................................................... 33. Tax Consequences to Employer ...................................................... 3

D. RESTRICTED STOCK .................................................................................... 31. Availability..................................................................................... 32. Tax Consequences to Recipient ...................................................... 33. Tax Consequences to Employer ...................................................... 4

E. ACCOUNTING TREATMENT OF OPTIONS ....................................................... 41. General ........................................................................................... 42. Fixed Accounting under APB 25 .................................................... 43. Variable Accounting under APB 25................................................ 54. Special Considerations under APB 25............................................. 55. FAS 123 Applies to Options Granted to Consultants....................... 6

F. ACCOUNTING OF RESTRICTED STOCK .......................................................... 61. General ........................................................................................... 62. Fixed Accounting under APB 25 .................................................... 73. Variable Accounting under APB 25................................................ 74. FAS 123 Applies to Restricted Stock Granted to Consultants.......... 7

II. RECENT DEVELOPMENTS IN EXECUTIVE COMPENSATION..................... 7A. VESTING TREND ......................................................................................... 7B. BROADER OPTION PARTICIPATION AND LARGER EQUITY POOLS................... 8

1. Broad-Based Plans.......................................................................... 82. Equity Pools ................................................................................... 8

C. STOCK PURCHASE LOANS............................................................................ 8D. FORFEITABLE STOCK DEFERRAL PREMIUM .................................................. 9E. TRANSFERABLE OPTIONS ............................................................................ 9

1. Overview........................................................................................ 92. Gift Tax Consideration ................................................................. 103. Income Tax Consequences............................................................ 10

(i)ii

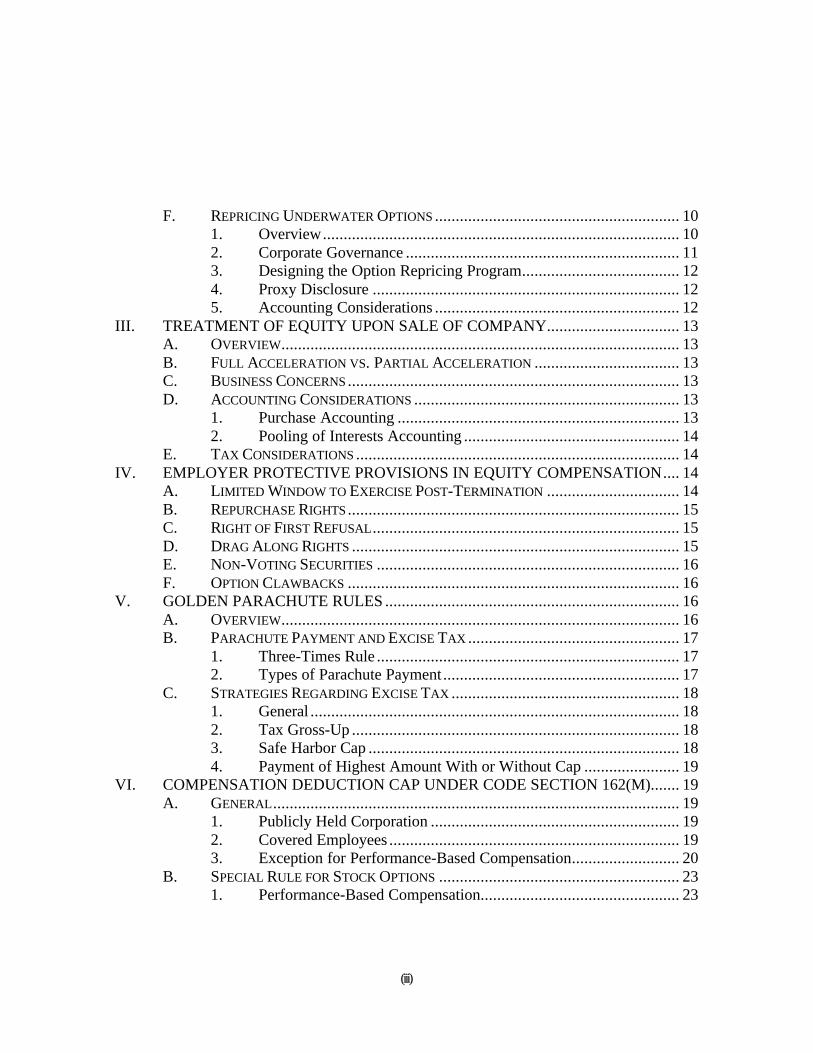

F. REPRICING UNDERWATER OPTIONS ........................................................... 101. Overview...................................................................................... 102. Corporate Governance .................................................................. 113. Designing the Option Repricing Program...................................... 124. Proxy Disclosure .......................................................................... 125. Accounting Considerations ........................................................... 12

III. TREATMENT OF EQUITY UPON SALE OF COMPANY................................ 13A. OVERVIEW................................................................................................ 13B. FULL ACCELERATION VS. PARTIAL ACCELERATION ................................... 13C. BUSINESS CONCERNS ................................................................................ 13D. ACCOUNTING CONSIDERATIONS ................................................................ 13

1. Purchase Accounting .................................................................... 132. Pooling of Interests Accounting .................................................... 14

E. TAX CONSIDERATIONS .............................................................................. 14IV. EMPLOYER PROTECTIVE PROVISIONS IN EQUITY COMPENSATION.... 14

A. LIMITED WINDOW TO EXERCISE POST-TERMINATION ................................ 14B. REPURCHASE RIGHTS ................................................................................ 15C. RIGHT OF FIRST REFUSAL.......................................................................... 15D. DRAG ALONG RIGHTS ............................................................................... 15E. NON-VOTING SECURITIES ......................................................................... 16F. OPTION CLAWBACKS ................................................................................ 16

V. GOLDEN PARACHUTE RULES ....................................................................... 16A. OVERVIEW................................................................................................ 16B. PARACHUTE PAYMENT AND EXCISE TAX ................................................... 17

1. Three-Times Rule ......................................................................... 172. Types of Parachute Payment ......................................................... 17

C. STRATEGIES REGARDING EXCISE TAX ....................................................... 181. General ......................................................................................... 182. Tax Gross-Up ............................................................................... 183. Safe Harbor Cap ........................................................................... 184. Payment of Highest Amount With or Without Cap ....................... 19

VI. COMPENSATION DEDUCTION CAP UNDER CODE SECTION 162(M)....... 19A. GENERAL.................................................................................................. 19

1. Publicly Held Corporation ............................................................ 192. Covered Employees ...................................................................... 193. Exception for Performance-Based Compensation.......................... 20

B. SPECIAL RULE FOR STOCK OPTIONS .......................................................... 231. Performance-Based Compensation................................................ 23

(i)iii

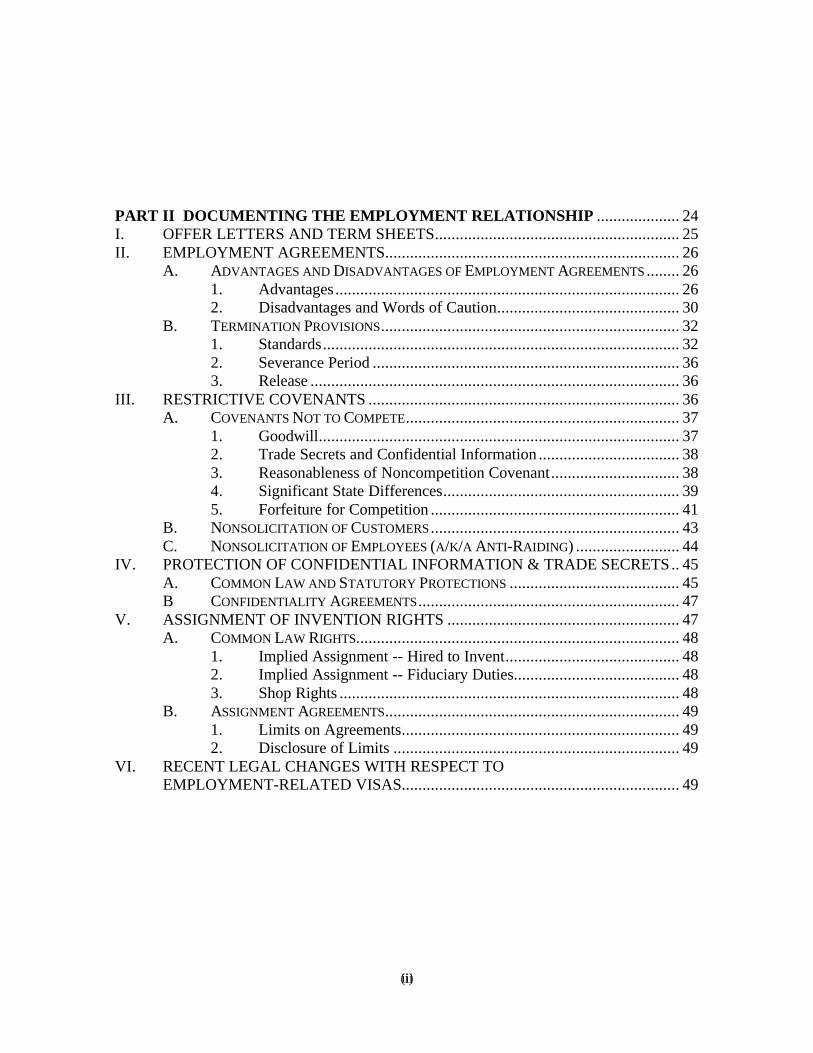

PART II DOCUMENTING THE EMPLOYMENT RELATIONSHIP .................... 24I. OFFER LETTERS AND TERM SHEETS........................................................... 25II. EMPLOYMENT AGREEMENTS....................................................................... 26

A. ADVANTAGES AND DISADVANTAGES OF EMPLOYMENT AGREEMENTS ........ 261. Advantages................................................................................... 262. Disadvantages and Words of Caution............................................ 30

B. TERMINATION PROVISIONS........................................................................ 321. Standards...................................................................................... 322. Severance Period .......................................................................... 363. Release ......................................................................................... 36

III. RESTRICTIVE COVENANTS ........................................................................... 36A. COVENANTS NOT TO COMPETE.................................................................. 37

1. Goodwill....................................................................................... 372. Trade Secrets and Confidential Information .................................. 383. Reasonableness of Noncompetition Covenant............................... 384. Significant State Differences......................................................... 395. Forfeiture for Competition ............................................................ 41

B. NONSOLICITATION OF CUSTOMERS ............................................................ 43C. NONSOLICITATION OF EMPLOYEES (A/K/A ANTI-RAIDING) ......................... 44

IV. PROTECTION OF CONFIDENTIAL INFORMATION & TRADE SECRETS.. 45A. COMMON LAW AND STATUTORY PROTECTIONS ......................................... 45B CONFIDENTIALITY AGREEMENTS............................................................... 47

V. ASSIGNMENT OF INVENTION RIGHTS ........................................................ 47A. COMMON LAW RIGHTS.............................................................................. 48

1. Implied Assignment -- Hired to Invent.......................................... 482. Implied Assignment -- Fiduciary Duties........................................ 483. Shop Rights .................................................................................. 48

B. ASSIGNMENT AGREEMENTS....................................................................... 491. Limits on Agreements................................................................... 492. Disclosure of Limits ..................................................................... 49

VI. RECENT LEGAL CHANGES WITH RESPECT TOEMPLOYMENT-RELATED VISAS................................................................... 49

ATTRACTING AND RETAINING KEY EMPLOYEESWHILE PROTECTING YOUR BUSINESS

PART I

EXECUTIVE COMPENSATION

I. STOCK-BASED COMPENSATION

A. Introduction

Companies often use stock-based compensation to incentivize their executives.The types of stock-based compensation most frequently used include stock options (bothincentive and non-qualified) and restricted stock. In the case of public companies, the useof stock-based compensation must take into account a myriad of laws and requirements,including securities law considerations (registration, Section 16, proxy disclosure), taxconsiderations (tax deductibility), accounting considerations (expense charges, dilution,etc.), stock exchange and NASDAQ requirements (shareholder approval), corporate lawconsiderations (fiduciary duty, conflict-of-interest) and shareholder relations (dilution,excessive compensation, option repricing). In order to satisfy the foregoing requirements,equity grants to executive employees of public companies are typically made under ashareholder-approved plan by a compensation committee comprised of independentdirectors.

B. Incentive Stock Options

1. General

A stock option is a right to buy stock in the future, generally at a fixedprice. There are two kinds of options, incentive stock options (“ISOs”) and non-qualified stock options (“NQOs”). ISOs are a creation of the tax code. If all thestatutory requirements are met the optionee will receive favorable tax treatment.NQOs do not provide any special tax treatment to the recipient.

2. Availability

ISOs may be granted only to employees. ISOs must be granted at fairmarket value or higher, and the maximum option term is ten years. In the case ofISOs granted to any 10 percent or greater shareholder, the exercise price must be atleast 110 percent of fair market value and the maximum option term is five years.The maximum amount of ISOs that can vest in the same calendar year for any

2

individual is limited to $100,000. This is determined by multiplying the fair marketvalue of the stock against the number of shares that are scheduled to vest in a year.Any option granted in excess of the $100,000 limitation, regardless of howdenominated, will be non-qualified.

3. Tax Consequences to Employee

There is no tax effect on the employee at the time of grant or vesting. Uponexercise of an ISO, there is no ordinary income to the employee, but the optionspread is taken into account in calculating the employee's alternative minimum tax.

(a) When the employee sells the underlying stock, if the sale ofthe underlying stock occurs more than two years from thedate of grant and more than one year from date of exercise,then the employee has long-term capital gains equal to thedifference between sale price and exercise price.

(b) When the employee sells the underlying stock, if the saleoccurs within two years from the date of grant or within oneyear from the date of exercise, the employee has(A) ordinary income equal to the spread (i.e., fair marketvalue less exercise price) that existed at exercise, plus (B)capital gains (long or short term depending on the holdingperiod of the underlying stock) equal to the differencebetween the sale price and fair market value of the stock atexercise. If the amount of sale is less than fair market valueof the stock at exercise, then the amount of ordinary incomeis limited to the difference between the sale price and theexercise price.

4. Tax Consequences to Employer

Subject to Section 162(m) of the Internal Revenue Code of 1986, asamended (the "Code"), the employer has a compensation deduction upon the sale ofthe underlying stock equal to the amount of ordinary income (if any) recognized bythe optionee if the holding period set forth in Section 3(a) above is not met. Theemployer has no compensation deduction if the holding period is met.

3

C. Non-Qualified Stock Options

1. Availability

NQOs can be granted to employees, outside directors and consultants.NQOs can be granted at or below fair market value. NQOs can be transferable tofamily members of the optionee.

2. Tax Consequences to Optionee

There is no tax consequence to optionee at the time of grant or vestingexcept in very unusual circumstances. At the time of exercise, the optionee hasordinary income equal to the excess of fair market value of the stock over theexercise price. This amount is also subject to Social Security taxes. Upon sale ofthe stock, the optionee receives capital gain or loss treatment, which may be longterm or short term, depending on the holding period of the stock. The optionee'sbasis is the exercise price plus the amount included in income upon exercise.

3. Tax Consequences to Employer

Subject to Code Section 162(m), the employer has a compensationdeduction upon option exercise equal to the amount of ordinary income recognizedby the optionee.

D. Restricted Stock

1. Availability

Restricted stock can be granted to employees, outside directors andconsultants. Except for payment of par value (a requirement of most statecorporate laws), the employer may grant the stock outright or require a purchaseprice at less than fair market value. To earn true ownership of the stock, therecipient is usually required to fulfill vesting conditions that may be based oncontinuing employment over a period of years and/or achievement of pre-established performance goals. Restricted stock can deliver more value to therecipient and therefore is less dilutive to stockholders. During the vesting period,the stock is considered outstanding, and the recipient can receive dividends andexercise voting rights.

2. Tax Consequences to Recipient

The recipient is taxed at ordinary income tax rates on the value of the stockat the time of vesting. Alternatively, the recipient may make a Section 83(b)

4

election within 30 days of grant to include in income the entire value of therestricted stock at the time of grant. Upon sale of stock, the recipient receivescapital gain or loss treatment, which may be long term or short term, depending onthe holding period.

Any dividends paid while the stock is unvested are taxed as compensationincome subject to withholding. Dividends paid with respect to vested stock aretaxed as dividends and no tax withholding is required.

3. Tax Consequences to Employer

Subject to Section 162(m) of the Code, the employer generally has acompensation deduction equal to the amount of ordinary income recognized by therecipient. The employer also has a compensation deduction equal to the amount ofdividends paid with respect to non-vested restricted stock.

E. Accounting Treatment of Options

1. General

Options are accounted for under either (i) APB 25, which applies to optionsgranted to employees and non-employee directors in their capacity as such or (ii)FAS 123, which applies to options granted to consultants and third parties otherthan employees and directors. Under APB 25, options receive fixed or variableaccounting, with variable accounting based on the intrinsic value of the option,which essentially means the spread. Under FAS 123, options are accounted forusing variable accounting based on fair value, which is determined using Black-Scholes or other valuation methodology.

2. Fixed Accounting under APB 25

(a) Generally, there is no compensation expense either at time ofgrant or upon vesting if the option grant is at fair marketvalue and vesting is time-based (i.e., fixed).

(b) If the option grant is below fair market value, the discount isa compensation expense; the discount amount is fixed anddetermined at grant date and amortized over the fixed vestingperiod.

(c) Options with performance-based vesting will still be subjectto fixed accounting if vesting will occur (even if theperformance hurdles are not met) at the end of a fixedperiod, typically five to seven years.

5

3. Variable Accounting under APB 25

(a) Variable accounting applies if the award is not fixed in somemanner; for example, if the price is not fixed or vesting isperformance-based (e.g., only vests if revenue targets areachieved and not on a date certain).

(b) Compensation expense is based on intrinsic value as opposedto FAS 123 fair value.

(c) Variable accounting always results in compensation expense.This is determined by marking to market every quarter untiloption is exercised, or in some instances, when awardbecomes fixed.

4. Special Considerations under APB 25

(a) Option repricing will result in variable accounting untiloption is exercised under APB 25.

(b) Any cancellation/regrant within six months will be deemedrepricing.

(c) Use of promissory note with below market interest rate topay exercise price will be deemed option repricing.

(d) Use of promissory note without full recourse to pay exerciseprice may raise similar issues and may be deemed repricing.

(e) Any modification to option terms (e.g., change in vesting,extension of post-termination exercise period, extension ofterm) can be considered a new grant for accounting purposesand will result in a new "measurement date." If on the newmeasurement date the exercise price is less than fair marketvalue of the stock, the discount will be a charge to earningsunder APB 25 fixed accounting.

(f) Business Combinations.

i. In a purchase accounting transaction when optionsare exchanged for options issued by the acquiringcompany:

6

(A) The fair value (i.e., Black-Scholes value) ofvested options (including options that vest onthe change in control) is included as part ofthe purchase price of the target.

(B) Unvested options also become part of thepurchase price in an amount equal to their fairvalue. However, if continued service isrequired for vesting after the date of theacquisition, then the "intrinsic value" of theunvested options, i.e., the spread at theacquisition date, is allocated to unearnedcompensation cost and expenses over theremaining vesting period. Any compensationcost determined by its intrinsic value isdeducted from the fair value of the unvestedoptions in determining the allocation to thepurchase price.

ii. In a pooling of interests transaction, if the exchangeof options does not increase the intrinsic value or theratio of exercise price to market value, then no newmeasurement date will be required.

5. FAS 123 Applies to Options Granted to Consultants

Fair value of options (determined on each vesting date) with respectto those options vesting as of such date will result in a charge to earnings.

(a) Fair value is determined using Black-Scholes or otherbinomial valuation method.

(b) Directors' grants can be subject to FAS 123 if granted forconsulting services.

F. Accounting of Restricted Stock

1. General

As with options, APB 25 applies only to restricted stock granted toemployees and non-employee directors.

7

2. Fixed Accounting under APB 25

If vesting is time-based and grantee pays full value, there is nocompensation charge.

(a) If vesting is time-based, but grantee pays less than full value,the discount is a compensation expense; this amount is fixedand amortized over vesting period.

(b) Restricted stock with performance-based vesting will besubject to fixed accounting if vesting will occur at the end ofa fixed period, typically five to seven years, even ifperformance goals are not met. This form of restricted stockis commonly known as TARSAPs.

3. Variable Accounting under APB 25

If vesting is performance-based, fair market value of stock at time ofvesting, less purchase price, must be charged to earnings; interim estimateswill likely be required.

4. FAS 123 Applies to Restricted Stock Granted to Consultants

(a) The fair market value of the stock, at each vesting date, lesspurchase price, will be a charge to earnings.

(b) Directors' grants can be subject to FAS 123 if granted forconsulting service.

II. RECENT DEVELOPMENTS IN EXECUTIVE COMPENSATION

A. Vesting Trend

The trend is towards faster vesting, over a period of three to four years, withvesting occurring initially at the end of 12 months from the date of grant, and then pro ratavesting on a monthly or quarterly basis thereafter.

8

B. Broader Option Participation and Larger Equity Pools

1. Broad-Based Plans

Increasingly, option plans are no longer reserved just for executives.In a recent survey prepared by Wordatwork, 80 percent of the companiesthat reported having a stock-based compensation plan offer stock options toa broad-based group of employees. Options are becoming the currency ofchoice and a large majority of employees in new economy companiesexpect equity grants to be part of the compensation package. In someinstances, companies grant options to every employee, including contractand part-time employees.

2. Equity Pools

The rate at which companies grant stock continues to increase. Thiscan be attributed to the cash-to-equity shift prevalent among new economycompanies, as well as the increased use of equity grants as a keyrecruitment and retention tool across a wide variety of industries for bothexecutives and professionals. According to a 1999 study of equity plans inthe 200 largest U.S. corporations prepared by Pearl Meyer & Partners Inc.,while the average equity pool for executive and employee incentive poolsstabilized at 13.2 percent in 1998, a number of companies have equity poolswell in excess of the average. In fact, 15 companies set aside more than 25percent of their outstanding shares for their employee stock plans. Of these,nine have allocations exceeding 30 percent, with five companies higher than40 percent and two of these higher than 50 percent. The diversifiedfinancial/brokerage sector, with an average equity pool of 32.91 percent,was by far the leader, followed by the technology sector at 20.68 percent.With new economy and start-up companies, which tend to be cash-poor,one should expect an even higher level of equity reserved in employee stockoption pools.

C. Stock Purchase Loans

Another trend is the increased use of stock purchase loans. Both old economycompanies, such as Kodak and Monsanto, and new economy companies, such as eBay andExcite@Home, have extended loans to key employees for use towards stock purchases. Insome instances, the underlying stock may be subject to risk of forfeiture. To encourageretention, sometimes these loans are forgiven if the employee remains employed for acertain period of time. By owning stock outright instead of just options, the key employeesenjoy both voting and dividend rights and are more aligned with the interest ofstockholders. There is also the added and not insignificant benefit of receiving capital

9

gains treatment on the stock price appreciation upon subsequent sale of the stock. Thedifferences in tax rates are quite significant (39.6 percent vs. 20 percent for federal taxes).In instances where the underlying stock is restricted, executives often file a Section 83(b)election to avoid recognition of income upon vesting of the restricted stock. Where therestricted stock is purchased for fair market value, albeit with the proceeds of a stockpurchase loan, no income would be recognized by the executives upon making the Section83(b) election.

Stock purchase loans should be structured very carefully to avoid tax andaccounting concerns. State corporate law and the Company's by-laws must also beexamined to ensure that stock purchase loans are properly authorized. In some instances,stock purchase loans that are secured by the stock may result in filings with the FederalReserve Bank.

D. Forfeitable Stock Deferral Premium

Another way that companies may encourage stock retention by executives is byoffering a deferred compensation program pursuant to which an executive could defer aportion of his cash bonus into deferred stock units that are credited to his account with apremium. This premium is forfeitable if the employee terminates employment prior to thevesting date for the premium. To illustrate this approach, assume an employee deferred$10,000 of cash bonuses into deferred stock units at a time when the stock price was $10and the company credited a 15 percent stock deferral premium. The employee would becredited with 1,000 units ($10,000/$10) plus 150 units (1,000 x 15%) for the premium. Ifthe employee subsequently terminates before the vesting date, the 1,000 units would bedistributed in shares and the 150 premium units would be forfeited. Such a programenables executives to acquire more stock on a tax-deferred basis.

E. Transferable Options

1. Overview

Transferring stock options to family members is a valuable estate-planning device for high net worth executives. Only non-qualified stockoptions can be transferred since incentive stock options are not transferableunder the tax laws. If the executive makes a completed gift of a stockoption to a family member, the gift will be subject to federal gift taxes at thetime of the gift based on the fair market value of the option at that time,subject to the potential availability of the $10,000 annual exclusion and/orthe unified credit. Since the value of the option could be less than the valueof the shares at the time of exercise, the individual could have transferredthe future increase in value to family members free of estate and gift taxes.

10

2. Gift Tax Consideration

In order to achieve the desirable tax consequences, it is importantthat the executive makes a completed gift of the stock options. For sometime, there had been some uncertainty as to whether a completed gift couldbe made with an option that was not currently exercisable. The InternalRevenue Service, in a recent revenue ruling, concluded that one cannotmake a competed gift of a stock option until it becomes exercisable. In theevent the option were to become exercisable in stages, each portion of theoption that becomes exercisable can be gifted on a separate basis. Rev. Rul.98-21.

In a recent revenue procedure, the Service also provided guidanceon the valuation of stock options for gift tax purposes. In Rev. Proc. 98-34,the Service stated that stock options must be valued by using a generallyrecognized option pricing model, such as the Black-Scholes method, thattakes into account the following factors: the option exercise price; theexpected life of the option; the current market price of the stock; theexpected volatility of the stock; the expected dividends on the stock; and therisk-free interest rate over the remaining option term. Further, a taxpayerthat wishes to rely on Rev. Proc. 98-34 may not apply a discount to thevaluation produced by the option pricing model to take into account factorssuch as the lack of transferability and risk of early termination of the optionupon termination of employment. It should be noted, however, that themethodology provided by a revenue procedure is simply a safe harbor.

3. Income Tax Consequences

At the time of option exercise by the family member, the executive(not the family member) will recognize ordinary income in an amount equalto the excess of the fair market value of the stock over the exercise price ofthe option (i.e., the option spread). The family member neverthelessreceives a basis in the shares received upon exercise equal to the exerciseprice paid plus the amount of income recognized by the executive. Theincome tax consequences of option exercises again result in transfer ofwealth to family members without the payment of gift or estate taxes.

F. Repricing Underwater Options

1. Overview

When a company's stock price drops below the exercise prices ofoptions, the options become "underwater" and have no perceived currentvalue to the employees. Many companies try to address employees'

11

dissatisfaction with "underwater" options by repricing the stock options.Repricing of stock options often results in increased scrutiny and criticismby institutional shareholders of a company's compensation program andpolicies. Shareholders may question whether repricing defeats the purposesof providing long-term incentive to employees by removing the risk to suchemployees of downward price movements in the company's stock. Somecritics compare repricing to changing the scoreboard or moving the goalposts halfway through a game. Institutional Shareholder Services, a proxyadvisory service in Bethesda, Maryland, that advises institutional investors,proclaims a zero tolerance for option repricing. Institutional ShareholderServices advises its institutional clients to vote against stock plan proposalsfor any company that has repriced stock options without shareholderapproval. Recently, the State of Wisconsin Investment Board has takensteps to persuade a number of companies in which it has a stake to seekshareholder approval of all option repricings, although such approval is nottypically required under state laws or stock exchanges rules. These policiesmay ignore the business realities faced by many companies; namely thatunderwater options do not have retention value to employees. SinceDecember 1998 when FASB announced that stock option repricing wouldresult in variable accounting, the use of option repricing has slowed downsignificantly. Instead of re-pricing when stock price drops below the optionstrike price, some companies, like Microsoft, who have a large pool ofreserved shares in their option plans, have made additional option grants toemployees to address morale and retention issues.

2. Corporate Governance

Shareholder approval is typically not required for option repricing,so long as the stock plan document gives the board, or the compensationcommittee, discretion to determine the option price, and there is noprohibition in the company's by-laws or the stock plan itself. Nevertheless,repricing of stock options has been the subject of shareholder litigation.Grounds for such lawsuits have included corporate waste, conflict ofinterest and breach of fiduciary duty. To avoid shareholder litigation overthis issue, compensation committees asked to approve repricing shouldcarefully deliberate and consider any proposed option program in order toavail themselves of the business judgment rule. In particular, compensationcommittees should consult legal, accounting and other professional adviceand should demonstrate their careful consideration of the issues throughwell-documented minutes, including well-reasoned justification for therepricing program, such as the need to keep the company's compensationprograms competitive and to avoid cherry picking by competitors. Tomitigate the risks of shareholder litigation, the compensation committeeshould also consider prohibiting outside directors and executives from

12

participating in the program and requiring additional consideration from theoption holders, such as restarting the vesting period over again.

3. Designing the Option Repricing Program

One way to reprice options is to simply amend the existing stockoptions to reduce the exercise price. Another method is through an optionexchange program. Under this method, employees are given an opportunityto surrender underwater options for new options at a lower exercise price,but for fewer shares. Very often, the exchange is made on a true economicbasis, by valuing the old and new options under an option-pricing model.Some companies require additional consideration such as extending thevesting period and/or imposing a "black-out" on option exercises for areasonable period following the repricing.

4. Proxy Disclosure

If option repricing benefits any of the named executive officers, thenthe company is required to disclose additional information in its proxystatement for the fiscal year in which the repricing occurs. This includes anexplanation by the compensation committee of the repricing program andthe basis therefor, as well as a repricing table that shows all option repricing(as well as exchanges) with respect to options held by executive officers(not just the named executive officers) in the last ten years.

5. Accounting Considerations

(a) Expense Charge. Companies that reprice options will besubject to variable accounting under APB 25 and arerequired to recognize as a compensation expense an amountequal to the difference between the new lower exercise priceand any future increase in stock price through the date theoption is exercised. This applies to both vested and unvestedoptions. Any option cancellation and re-grant within sixmonths is deemed to be option repricing for this purpose.

(b) Pooling of Interest Accounting. Option repricing within twoyears of a business combination could adversely affect theparties' ability to use the pooling of interest method toaccount for the combination.

13

III. TREATMENT OF EQUITY UPON SALE OF COMPANY

A. Overview

In designing stock option plans, it is important to consider whether the vesting ofunvested options will be accelerated upon a sale of the company. There is no one correctapproach that serves the needs of every company.

B. Full Acceleration vs. Partial Acceleration

Some stock option plans provide for full acceleration of unvested stock optionsupon a sale of the company. This is particularly prevalent among large public companies.Other stock option plans provide that if the options will be assumed by the acquiringcompany, the vesting of 50 percent of the unvested options will be accelerated upon thesale of the company. The remaining 50 percent will vest in their normal course, but in theevent the optionee is terminated by the acquiring company without "cause" within a periodof time after closing (typically varies from 12 to 18 months), the vesting of the remainingunvested options will be accelerated as well. A third approach provides for no accelerationupon sale, but full or partial acceleration of vesting if the optionee is terminated without"cause" within a certain period after closing. The second and third approaches aresometimes referred to as "double-trigger" approaches.

C. Business Concerns

Investors are generally not in favor of full acceleration because of concerns that itmight lower the value of their investment. Further, there is the added concern that theemployees who receive a "windfall" upon the sale of the company will have no incentiveto stay with the acquiring company post-acquisition. This could increase the cost of theacquisition as the acquiring company may be required to put in place additional incentivesto retain the key employees. The double-trigger approaches discussed above are viewed bysome investors as a more balanced approach which also provides protection for employeeswho are terminated without "cause" before the end of the vesting period. Employees, onthe other hand, for obvious reasons prefer full acceleration of stock options upon the saleof the company. Some companies may permit full acceleration in specific grants in orderto attract and retain high quality employees in a competitive market.

D. Accounting Considerations

1. Purchase Accounting

In a purchase accounting transaction when options are exchangedfor options issued by the acquiring company, vested options (includingoptions that vest on the sale of company) are treated as they have been inthe past. The "fair value" (i.e., Black-Scholes) of the substitute options is

14

included as part of the purchase price of the target. Unvested options alsobecome part of the purchase price in an amount equal to their "fair value."However, if continued service is required for vesting after the date of theacquisition, then the "intrinsic value" of the unvested options, i.e., thespread at the acquisition date, is allocated to unearned compensation costand expenses over the remaining vesting period. Any compensation costdetermined by its "intrinsic value" is deducted from the "fair value" of theunvested options in determining the allocation to the purchase price.

2. Pooling of Interests Accounting

If the exchange of options does not increase the intrinsic value or theratio of exercise price to market value, then the exchange of options will notresult in compensation expenses. In a transaction that is accounted for as apooling of interests, it is impermissible to change the vesting of options atthe time the transaction is negotiated or contemplated as that would beconsidered a change in equity position that would disqualify the use ofpooling.

E. Tax Considerations

Stock options or stock grants that vest upon a sale of the company are consideredparachute payments potentially subject to the golden parachute tax. In the case of a privatecompany, the golden parachute tax concerns can be avoided completely if the shareholders,upon full disclosure, approve the acceleration in vesting in connection with the saletransaction. See Section V.

IV. EMPLOYER PROTECTIVE PROVISIONS IN EQUITY COMPENSATION

There are a number of protection provisions that a properly represented employershould seek to have in their employee equity documentation. As indicated below, not allof these provisions are appropriate for public employers.

A. Limited Window to Exercise Post-Termination

If the employment is terminated with cause, stock options should provide that theoption held by an executive terminates immediately, and is no longer exercisable.Similarly, with respect to restricted stock, vesting should cease and a repurchase rightshould arise (See IVB). In all other cases, the option agreement should specify the post-termination exercise period. Typically, post-termination periods are 12 months in the caseof death or disability, and 90 days in the case of termination without cause. Someexecutives will try to negotiate extended post-termination exercise periods as long as theremaining exercise period in the original ten-year term.

15

B. Repurchase Rights

With respect to restricted stock, private companies should always consider havingrepurchase rights for unvested as well as vested stock. Unvested stock should always besubject to repurchase either at cost or fair market value, or the lower of cost or fair marketvalue. With respect to vested stock and stock issued upon exercise of vested options, someemployers retain a repurchase right at fair market value upon termination under allcircumstances until the employer goes public; other employers only retain a repurchaseright under limited circumstances, such as termination without cause or bankruptcy.

In general, public companies should only retain the repurchase right with respect tounvested stock, as the need to ensure that an employer’s securities remain only in a limitednumber of friendly hands is no longer present.

C. Right of First Refusal

As another means to ensure that securities remain only in relatively few friendlyhands, private company employers often have a right of first refusal or first offer withrespect to any proposed transfers by an executive. Generally, these provide that prior totransferring equity securities to an unaffiliated third party, an executive must first offer thesecurities for sale to the employer-issuer and/or perhaps other shareholders of the employeron the same terms as offered to the unaffiliated third party. Only after the executive hascomplied with the right of first refusal can the executive sell the securities to such a thirdparty. Even if an employer was not contemplating a right of first refusal, outside venturecapital investors are likely to insist on these types of provisions.1 Rights of first refusal(and co-sale rights) typically terminate once the employer has successfully completed anIPO.

D. Drag Along Rights

Private companies should also consider having a so-called “drag-along” or “take-along” right, which generally provides that a holder of the employer’s equity securities willbe contractually required to go along with major corporate transactions such as a sale ofthe company, regardless of the structure thereof, so long as the holders of a statedpercentage of the employer’s equity securities is in favor of the deal. This will preventindividual employee shareholders from interfering with a major corporate transaction by,for example, voting against the deal or exercising dissenters’ rights. Again, venture capitalinvestors typically insist on this type of provision.

1It would not be unusual for venture capital investors to insist on a co-sale right as well.

16

E. Non-Voting Securities

Another technique private employers should consider is issuing non-votingcommon stock to their employees. Generally, except as required by law, holders of non-voting common stock have very limited voting rights and, hence, will be less likely tointerfere with a major corporate transaction that has the backing of a stated percentage ofsecurity holders.

F. Option Clawbacks

To protect themselves from an employee who seeks to engage in post-terminationcompetition, employers may consider a “claw back” provision under which an employeewho violates a noncompetition agreement (see Section II.B. below) forfeits not only his orher stock and stock options but also any profit derived therefrom. At least one FederalCircuit court has recognized such a provision. International Business Machines Corp. v.Bajorek, 191 F.3d 1033 (9th Cir. 1999) (option agreement enforces where it included apromise that employee would return any profit (here, $928, 538.74) made from his or herstock option if he worked for a competitor within six months of their exercise). But seeLucente v. International Business Machines Corp., 99 Civ. 3987 (CM) (S.D.N.Y.October 19, 2000) (stock forfeiture provision invoked when former executive joinedcompetitor two years after his retirement was unreasonable as a matter of law).

V. GOLDEN PARACHUTE RULES

A. Overview

Sections 280G and 4999 of the Internal Revenue Service Code disallow a federalincome tax deduction to the employer corporation of an "excess parachute payment" andimpose a non-deductible excise tax equal to 20 percent of the "excess parachute payment"on the recipient of the payment.

The parachute tax rules generally apply to compensation payments to a disqualifiedindividual if the payments are contingent on a change in the ownership or effective controlof the employer corporation or in the change in ownership of a substantial portion of theassets of the employer corporation. The parachute tax rules do not apply to payments by Scorporations, or payments by closely-held corporations, if the shareholder approvalrequirements have been satisfied.

17

B. Parachute Payment and Excise Tax

1. Three-Times Rule

Code Section 280G(b)(2)(A) defines a "parachute payment" as any paymentin the nature of compensation that is made to a "disqualified individual" (i.e.,officer, shareholder or highly compensated employee), is contingent on a change incontrol of the employer corporation, and, together with all other payments, has apresent value that equals or exceeds three times the individual's "base amount" (i.e.,the average annual taxable compensation received by the disqualified individualover the most recent five years ending before the change in control). Compensationpaid pursuant to agreements entered into one year before a change in control ispresumed to be contingent on the change. If the present value of the parachutepayment equals or exceeds three times the individual's base amount, then theindividual must pay an excise tax equal to 20 percent of the excess of parachutepayment over the base amount. (Note, not three times the base amount.) Forexample, if an individual's base amount is $300,000 and the individual is entitled toreceive parachute payments with a present value of $1,000,000, he is liable for anexcise tax of $140,000 [.2 x ($1,000,000 - $300,000)]. The corporation's taxdeduction is limited to $300,000.

2. Types of Parachute Payment

(a) Severance payments which become payable because of atermination of employment in connection with a change incontrol are generally considered parachute payments.

(b) Stock grants that vest or stock options that becomeexercisable as a result of a change in control are alsoconsidered parachute payments. However, if the payment iscertain (i.e., would have been paid sometime in the future ifthe individual had remained employed) but the timing ofreceipt is accelerated due to the change in control, only aportion of the payment is treated as contingent on thechange. The proposed regulations include a formula fordetermining the value of the portion to be treated ascontingent. Prop. Reg. § 1.280G, Q/A - 24(c).

(c) If a disqualified individual receives benefits continuationfollowing a termination of employment in connection with achange in control, the value of the benefits continuation arelikely to be considered parachute payments.

18

(d) Any amount that one can establish as reasonablecompensation for personal services to be rendered on or afterthe change in control is not considered a parachute payment.Payments to a disqualified person for not competing againstthe employer corporation after the change in control maycome under this exception if the amounts are reasonable.

(e) Payments from tax-qualified plans are not consideredparachute payments.

C. Strategies Regarding Excise Tax

1. General

There are three approaches that corporations generally take with regard tothe golden parachute tax: (a) tax gross-up; (b) safe harbor cap; and (c) payment ofhighest amount with or without cap.

2. Tax Gross-Up

In order to protect the executive from the punitive nature of the excise tax,many corporations provide the executive with a "gross-up" payment to ensure thatthe executive receives the after-tax benefits he or she would have received had thepayments not been subject to the excise tax. In particular, the gross-up paymentwould be equal to the sum of (a) the excise tax on the parachute payments, and (b)the federal, state, local, employment tax and excise tax on the gross-up payment.The gross-up payment can be very costly to the employer. At today's tax rates, thegross-up payment can be close to three times the amount of the excise tax. Inaddition, the corporation would not be entitled to a tax deduction with respect to theexcess of the parachute payments, including the gross-up payment, over theexecutive's base amount.

3. Safe Harbor Cap

Under this approach, the corporation and executive agree in advance thatthe parachute payments (including severance payments) payable upon a change incontrol would be limited to three times the executive's base amount less $1.00. Forexample, assume that the executive's base amount is $200,000, and that theparachute value of the executive's options that accelerated upon the change incontrol is $150,000. Under the safe harbor cap approach, the maximum severancepayments cannot exceed $449,999 [(3 x $200,000 -- $150,000 - $1)]. This safeharbor cap could lead to disappointment to the executive because in manyinstances, given the magnitude of today's equity grants for executives, the

19

acceleration of vesting may cause all or a substantial portion of the executive's safeharbor to be used up prior to the payment of any severance benefits.

4. Payment of Highest Amount With or Without Cap

Another approach that some corporations take is to impose the safe harborcap only if the executive's net after-tax benefit is greater by applying the cap than ifthe cap is not applied. A variation of this approach is to impose the cap only if theamount to be eliminated as a result of the cap is less than a certain percentage (e.g.,110 percent) of the present value of all taxes imposed on the eliminated amount.These approaches are less costly to the corporation than the gross-up approach andwill provide for larger after-tax dollars to the executive. For example, assume thatthe executive's safe harbor is $900,000 and that the contractual payments wouldhave been $1,500,000 prior to any cutback. Further assume a maximum combinedtax bracket of 65 percent (including the excise tax) and 45 percent (excluding theexcise tax). With the cap, the executive would have received $495,000 on an after-tax basis ($900,000 x .55). Without the cap, the executive would have received$585,000 on an after-tax basis ($1,200,000 (i.e., the amount of the payment inexcess of the base amount) x .35 + $300,000 (i.e., the base amount) x .55). In thisinstance, the executive would be better off without the cap than if the cap hadapplied.

VI. COMPENSATION DEDUCTION CAP UNDER CODE SECTION 162(m)

A. General

Under Code Section 162(m), subject to certain exceptions, a "publicly heldcorporation" is denied a deduction for remuneration paid to a "covered employee" forservices performed by such employee to the extent the remuneration exceeds $1 million forthe taxable year.

1. Publicly Held Corporation

A "publicly held corporation" is defined as "any corporation issuingany class of common equity securities required to be registered underSection 12 of the Securities Exchange Act of 1934." Code § 162(m)(2).

2. Covered Employees

Under Code Section 162(m), an individual is a "covered employee"if the individual is employed on the last day of the company's tax year andhe or she is either the chief executive officer or any other individual whosecompensation must be reported to shareholders under the Securities

20

Exchange Act of 1934 Act by reason of being among the four highest paidofficers.

3. Exception for Performance-Based Compensation

Code Section 162(m) excludes performance-based compensationfrom the $1 million deduction limit. Such compensation must satisfy thefollowing four requirements:

(a) Performance Goals. The compensation is paid solely onaccount of the attainment of one or more pre-establishedobjective performance goals. See Treas. Reg. § 1.162-27(e)(2)(i)-(ii).

i. The goal must be established by the compensationcommittee not later than 90 days after thecommencement of the performance period (or withinthe first 25 percent of the period if the period is lessthan one year).

ii. The performance goal must be objective such that athird party having knowledge of the relevant factscould determine whether the goal is met.

iii. The compensation committee does not have thediscretion to increase the compensation due uponattainment of the goal, but may retain negativediscretion to reduce the compensation.

iv. The performance goal can be based on one or morebusiness criteria that apply to the business unit, orcorporation as a whole. Examples of business criteriainclude stock price, earnings per share, return onequity, market share, sales, etc.

v. If the executive would receive part or all of thecompensation even if the performance goal is notattained, the compensation does not qualify for theperformance-based exception.

(b) Goals Must Be Determined by Compensation Committee.The performance goals must be established by acompensation committee comprised solely of two or more"outside directors." See Treas. Reg. § 1.162-27(e)(3).

21

i. To qualify as an "outside director," a director

(A) must not be a current employee of the publiccompany;

(B) must not be a former employee of the publiccompany who receives compensation for priorservices (other than benefits under a tax-qualified retirement plan);

(C) must not have served as an officer of thepublic company; and

(D) must not receive remuneration from thepublic company, directly or indirectly, in anycapacity other than as a director. For thispurpose, "remuneration" includes:

i) any amount paid to an entity in whichthe director has more than a 50 percentbeneficial interest;

ii) amounts, other than de minimisremuneration, paid by the publiccompany to an entity in which thedirector has more than 5 percentbeneficial interest; and

iii) amounts, other than de minimisremuneration, paid by the publiccompany to an entity by which thedirector is employed or self-employed.

To qualify under the de minimis exception,the remuneration must be $60,000 or less ifpaid for personal services and may not exceed5 percent of the gross revenues of the entityfor the taxable year ending with or within thepreceding taxable year of the public company.

ii. Although the regulations provide that thecompensation committee must be comprised solely oftwo or more outside directors, the Service has ruled

22

that a compensation committee with directors who donot so qualify as outside directors can still qualify asa committee of outside directors under Code Section162(m) so long as all the directors who do not soqualify abstain or recuse themselves, and there are atleast two remaining directors who qualify as outsidedirectors. PLR 9811029.

(c) Shareholder Approval Required. The material terms of theperformance goal under which the compensation is to bepaid must be disclosed to and approved by the shareholdersbefore the compensation is paid. Treas. Reg. § 1.162-27(e)(4).

i. The shareholders must be made aware of the materialterms of the compensation, including the class ofeligible employees, the description of the businesscriteria on which the performance goal is based andeither the maximum amount of the compensation thatwould be paid or the formula used to calculate theamount.

ii. The specific targets do not have to be disclosed to theshareholders.

iii. If the compensation committee has authority tochange the targets under a performance goal, theshareholders must reapprove the performance goalsevery five years.

iv. The shareholder approval requirement is satisfiedonly if the material terms of the performance goal areapproved by the shareholders, in a separate vote inwhich a majority of the votes cast (includingabstentions, to the extent abstentions are counted asvoting under applicable state laws) on the issue arecast in favor of approval.

(d) Certification. Prior to payment, the compensation committeemust certify in writing that the performance goals were infact satisfied. Code Section 162(m)(4)(C)(iii). For thispurpose, the approved minutes of the compensationcommittee are satisfactory.

23

B. Special Rule for Stock Options

1. Performance-Based Compensation

Stock options will be considered qualified performance-based compensationif the grant is made by a compensation committee comprised solely of two or moreoutside directors, the plan specifies a limitation on the number of options that maybe granted to any individual during a specified period and the amount ofcompensation attributable to the option is based solely on an increase in the valueof the stock after the date of grant.

(a) The individual limit on the number of options need not bethe same for each employee.

(b) Under the regulations, if an outstanding option is repriced, itis deemed canceled with a new option issued in its place.The canceled option counts against the particular employee'soption share limit under the plan.

(c) If the exercise price of the option is no less than the fairmarket value of the stock on the date of grant, then theoption is considered performance-based under theregulations. In such a case, any compensation attributable tothe option is based solely on an increase in the value of thestock after the date of grant.

(d) Compensation that is tied solely to an increase in stock price,such as options, does not require written certification by thecompensation committee.

(e) Generally, with discounted stock options, the executive mayreceive compensation even if the stock declines in value (i.e.,the exercise price is less than the stock's fair market value atgrant, the stock drops in value but the executive still realizesa gain so long as the stock does not fall below the exerciseprice). Thus, discounted options are not deemedperformance-based compensation because the executive canrealize a gain that is not based solely on an increase in thevalue of the stock after the date of grant. However, if thegrant or the vesting of a discounted stock option is basedsolely on the attainment of an objective performance goalthat has received shareholder approval, then the resultingcompensation is qualified performance-based compensation.

24

PART II

DOCUMENTING THE EMPLOYMENT RELATIONSHIP

The extent to which terms and conditions of the employment relationship should bedocumented at the outset of employment is a delicate issue in which a number ofcompeting concerns should be considered.

For example, certain terms and conditions (e.g., noncompetition covenants,assignment of work-related inventions, etc.) must be documented if the employer expectsto have an agreement that is binding upon the employee. Other matters (e.g., stock optionsand restricted stock grants, incentive compensation plans, etc.) should be documented sothat there is no confusion regarding the parties’ respective rights and obligations. Themeans by which these terms are documented vary. For example, restrictive covenantsfrequently are embodied in stand-alone contracts. Likewise, the terms of equity grantsfrequently are (and should be) embodied in stand-alone agreements supplemented by theterms of underlying equity plans.

Other terms and conditions of employment (e.g., base salary, duties and reportingrelationships, frequency of annual reviews, etc.) do not need to be documented in a formalcommunication between the employer and employee, but frequently are. These terms maybe set forth in offer letters, term sheets or employment contracts. These documents alsooften are used, in lieu of standard agreements, to describe other matters, such as the termsof equity grants or the scope of restrictive covenants. Properly worded offer letters, forexample, can and do describe clearly the terms of employment.

Carefully documenting the relationship between employer and employee also mayhelp attract and retain employees. For example, new employees may find security in adocumented relationship. Existing employees with written agreements are more likely tounderstand their rights and obligations and accordingly may be less likely to lookelsewhere for employment.

Problems often arise, however, when employers attempt to document the terms ofemployment. Frequently encountered problems include, but are not limited to: (i) creatingconflicts among documents (e.g., an offer letter that describes terms of an equity grant thatare inconsistent with the terms of the equity plan); (ii) altering the employment relationshipfrom at-will to employment for a term; (iii) creating ambiguous terms (e.g., is an incentivebonus earned ratably?); (iv) promising benefits the employer is not yet ready or able toimplement; and (v) guaranteeing an employee that he or she will have a certain reportingrelationship (e.g., “you will report to the CEO”) or specific responsibilities (e.g., “you willbe responsible for world wide sales and marketing”). In some cases, these problems canlead to legal liability. In other cases, they can lead to significant morale or humanresources problems. In either case, these types of problems can have a detrimental effect

25

on the specific employee at issue, other employees in the workforce and, as the use ofemployer-specific chat rooms becomes more prevalent, potential recruits.

The following sections discuss in more detail some of the benefits and commonlyrecurring pitfalls of documenting the employment relationship.

I. OFFER LETTERS AND TERM SHEETS

At the recruiting stage, employers often use term sheets or offer letters to conveythe offered terms of employment. Frequently, employers ask a potential employee toindicate his or her acceptance of the offer by signing and returning the document. Manyemployers fail to recognize, however, that offer letters and term sheets can constitute or beevidence of contractual commitments that can be accepted expressly (i.e., when thecandidate executes the document) or implicitly through performance (i.e., when thecandidate begins working or leaves his or her other job in reliance on the offered terms).

If documents such as offer letters or term sheets are going to be used at therecruitment stage, an employer either should recognize that it may be creating a contractand draft with the care accorded other contracts or should take steps to avoid creatingcontractual commitments.

The language of offer letters and terms sheets sometimes may result in alteration ofthe employment relationship from at-will to employment for a term. This problem caneasily be avoided by a clear at-will disclaimer. Other steps also can be taken to avoid suchan unintended result. For example, offer letters should describe compensation in monthlyor weekly, rather than annual, terms because references to time may be construed tosupport the claim of a promise for employment of a certain duration. See Venizi v.Mahoney & Wright Insurance Agency, Inc., 40 Mass. App. Ct. 218, 225 (1996). Inaddition, offer letters should avoid representations concerning the timing of salaryincreases or performance reviews, since such representations may give rise to claims thatthe employee has a contract at least until the date of the salary increase or performancereview. See, e.g., Frederich v. Conagra, Inc., 713 F. Supp. 41, 46 (D. Mass. 1989).

When drafting term sheets or offer letters, it is important to keep in mind otherdocuments an employee may be asked to sign, especially documents that are to be signedcontemporaneously with acceptance of the offer of employment. To the extent that offerletters or term sheets refer to terms or conditions of employment that are embodied in otherdocuments, care should be taken to refer to those other documents as controlling. Thisprecaution should avoid creating confusion or, in the worst case, modifying the terms ofthose other documents. For example, an offer letter may promise unconditionally that acandidate will receive stock options upon commencement of employment, but theunderlying stock plan requires execution of a noncompetition agreement as a condition to agrant of options. Not surprisingly, the employee may balk at executing the noncompetitionwhen it is presented to him or her a month later.

26

Many of these same concerns arise when an employer engages in a bidding war toretain its own employees who are being recruited by other employer.

The key point for an employer is to treat offer letters with the same care andconsideration as it would in preparing or negotiating any other contract. An employershould not make commitments it is not prepared or able to fulfill.

II. EMPLOYMENT AGREEMENTS

Employment agreements are used to document many critical aspects of theemployment relationship, most frequently with respect to senior executives or other keypersonnel. As with any other contract a company may enter into, precision, accuracy andattention to detail are important in any such effort. A carefully crafted employmentagreement can clearly delineate an employer’s and employee’s respective rights, duties andobligations. Such agreements can anticipate and provide for future occurrences, such asthe consequences of any breach of the agreement and provide for a mutually agreeableforum in which to resolve disputes. A poorly drafted employment agreement, however,may fail to memorialize adequately all aspects of the parties’ agreed upon intentions.Indeed, a poorly drafted employment agreement may result in terms or conditions beingimposed by a court that were not intended by one or both parties to the agreement.

A. Advantages and Disadvantages of Employment Agreements

1. Advantages

The advantages of using an employment agreement todocument the employment relationship are numerous, provided thatsuch agreements are drafted accurately and precisely. Agreementsthat contain omissions, inconsistencies or ambiguities invariablylead to disputes. Of course, such disputes are exactly what theagreement was meant to prevent.

(a) Negotiate at Optimum Time. The start of an employmentrelationship is probably the most opportune time to negotiatean employment agreement. Among other reasons, theparties’ relationship at that time will most likely be amicable.

(b) Nature of the Relationship. In most jurisdictions,employment is presumed to be at-will (i.e., terminable byeither party at any time and for any lawful reason or noreason). If an employer intends to maintain an at-willrelationship, identifying employment as “at-will” in theemployment agreement is advisable. A statement that

27

employment is “at-will” signed by the employee may rebut aclaim of employment for a particular term. See Novosel v.Sears, Roebuck, 495 F. Supp. 344 (E.D. Mich. 1980). Onthe other hand, failure to do so may create unintendedguarantees of employment for a certain duration or that isterminable only for “cause.” Goldhor v. Hampshire College,25 Mass. Ct. App. 716, 721 (1988). If employment for adefinite term is intended, including that specific term in awritten contract provides evidence of commitment on thepart of both the employer and the employee.

(c) Compensation. In this tight job market, compensationremains a key method of attracting, incentivizing, andretaining key employees. Defining compensation, such assalary, bonus or other incentive compensation as well as anyequity rights in an employment agreement clearly informsthe employee how performance will be rewarded and mayassist in preventing disputes related to compensationobligations.

(d) Capacity. Spelling out an employee’s duties, responsibilitiesand functions confirms the employee’s understanding of thearrangement he or she is entering into and establishes theemployer’s expectations. Careful drafting is requiredbecause an inadvertent gap in an otherwise comprehensivedescription may become a subject for a dispute. To preventthis possibility, the employer should consider broadlyworded descriptions that reserve the employer’s discretion todefine or alter job duties over time.

(e) Damages. In light of the amicable nature at the start of mostemployment relationships, the issue of damages should bebroached with the employee at that time. Specifically,provisions may be negotiated to establish the rights of eitherparty in the event of a breach by the other. For example, theparties may agree to liquidated damages in the event theemployee breaches obligations to the employer. In the caseof employment for a term, the parties may negotiate damagesif either party terminates employment without cause or goodreason. The parties should be able to reach agreement onthese issues more easily prior to the onset of any dispute.

28

(f) Noncompetition, Nonsolicitation and NondisclosureAgreements. In the new economy, employers have becomeincreasingly vigilant about preventing the disclosure ofconfidential information to their competitors. Similarly,employers have an increased interest in keeping a workforceintact. Accordingly, employers should consider includingrestrictive covenants, such as noncompetition agreements,nonsolicitation of customers, nonsolicitation of employees,and nondisclosure provisions in their employmentagreements. Of course, as discussed above, for obviousreasons, these provisions should be negotiated prior to thecommencement of the employment relationship. In additionto practical concerns, some courts hold that restrictivecovenants entered into after the start of employment may notbe enforceable without new consideration. Compare IkonOffice Solutions, Inc. v. Belanger, 1999 WL 508689(D. Mass.) (continued employment insufficient to support anoncompetition agreement) with Zellner v. Stephen D.Conrad, M.D., P.C., 183 A.D.2d 250 (N.Y. 2d Dept. 1992)(enforcing agreement entered into during employmentwithout additional consideration); Reynolds & ReynoldsCo. v. Tart, 955 F. Supp. 547,553 (W.D.N.C. 1997)(same);Midwest Sports Mktg. Inc. v. Bradsby of Can. Ltd., 552N.W. 2d 254 (Minn. Ct. App. 1996)(same). Because somestate laws generally prohibit certain restrictive covenants,care should be taken when presenting any employee with aproposed agreement containing such terms. See, e.g., Cal.Bus. and Professions Code § 1600 (generally prohibitingrestraints of trade, such as noncompetition provision);see also discussion below in Section II.B.

(g) Breach of Fiduciary Duty. Employment agreements andother documents that contain explicit termination provisionsmay help protect employers from breach of fiduciary dutyclaims. By way of background, in Massachusetts, allshareholders in a close corporation, but particularly a“controlling group” or a majority shareholder, owe eachother a duty of “utmost good faith and loyalty.” Donahue v.Rodd Electrotype Co. of New England, 367 Mass. 578, 592(1974). Accordingly, Massachusetts courts generally requirethat employers have a legitimate business reason forterminating an employee who is also a minority shareholder

29

in a close corporation. Wilkes v. Springside Nursing Home,370 Mass. 842, 850 (1976).

Complying with an employment agreement and purchasing aminority shareholder’s stock at a “fair price” may insulate amajority shareholder from a fiduciary duty claim eventhough the employer/majority shareholder lacked a“legitimate business reason” for terminating the minorityshareholder’s employment. Merola v. Exergen Corp., 423Mass. 461, 465 (1996.) “Questions of good faith and loyaltywith respect to rights on termination or stock purchase do notarise when all the stockholders in advance enter intoagreements concerning termination of employment and forthe purchase of stock of a withdrawing or a deceasedshareholder.” Blank v. Chelmsford Ob/Gyn, P.C. 420 Mass.404, 408 (1995) (where employment contract permittedemployment to be terminated by either party on six monthsnotice, and there is no allegation that the defendants weredenying the plaintiff his or her contractual rights or futurecompensation for past services.); see Donahue, 367 Mass. at599, n.24.

(h) Alternative Dispute Resolution. Including alternativedispute resolution provisions in employment agreementsmay also be useful. Many employers find such provisions,which typically require both the employer and employee tosubmit all employment disputes to arbitration, to be efficientand cost effective. While many courts have enforced suchprovisions in the employment context, see, e.g., Gilmer v.Interstate/Johnson Lane Corporations, 500 U.S. 20 (1991);Seus v. John Nuveen & Co., 146 F.3d 175, 179, 182-83 (3dCir. 1998); Mugnano-Bornstein v. Cromwell, 42 Mass. App.Ct. 347 (1997), the United States Supreme Court has yet todecide whether arbitration clauses included in “contracts ofemployment” (as opposed to other types of documents) areenforceable. It is expected to do so in its current term.Circuit City Stores v. Adams, 194 F.3d 1070 (9th Cir. 1999),cert. granted, 120 S.Ct. 2004, 164 L.Ed. 2d 955 (2000).

The Federal Arbitration Act (“FAA”) generally requirescourts to enforce arbitration agreement, but excludes from itsscope arbitration agreements in “contracts of employment ofseamen, railroad employees, or any other class of workersengaged in foreign or interstate commerce.” 9 U.S.C. § 1.

30

Many courts have construed this exclusion to apply only tocontracts of workers actually engaged in moving goods ininterstate commerce, e.g., truck drivers and seamen. E.g.,Tenney Engineering, Inc. v. United Elec. Radio & Mach.Workers, 207 F.2d 450 (3d Cir. 1953) (en banc). The NinthCircuit, however, has held this exclusion applies to any typeof employment agreement. E.g., Circuit City Stores v.Adams, supra (exclusion applies to arbitration agreemententered into in connection with employment application as acondition of at-will employment); Circuit City Stores Inc. v.Ahmed, 195 F.3d 1131 (9th Cir. 1999) (exclusion applies toarbitration agreement in any document employer intends tobe binding on employee). In Circuit City Stores v. Adams,the Supreme Court will decide whether a mandatoryarbitration provision in a contract of employment isenforceable in light of the particular wording the of FAA.However, the Supreme Court will not consider what types ofdocuments constitute “contracts of employment.” Thus, ifthe Supreme Court endorses the Ninth Circuit’s expansiveview of the scope of Section One of the FAA, it will remainunclear whether employees will remain free to usearbitration agreements in other types of documents withemployees such as stock option agreements.

2. Disadvantages and Words of Caution

The following are disadvantages and risks associated withdocumenting the employment relationship.

(a) Ambiguity and Implied Terms. Careful drafting ofemployment agreements is required to avoid ambiguity andthe possibility that a court will imply terms that the employerdid not intend. However, oral assurances also may createbinding obligations on an employer either under a contracttheory or through an employee’s reliance on such assurances.See Nelson v. Energy Exch. Corp., 727 F. Supp. 59,62 (D.Mass. 1989) (salesman may sue for commissions promisedbut not paid).

(b) Breach of the Implied Covenant of Good Faith and FairDealing. Employers must be mindful of the claim known as“breach of good faith and fair dealing.” Employers must actin good faith so as not to deprive the employees of “the fruitsof [a] contract.” Fortune v. National Cash Register Co., 373

31

Mass. 96, 103 (1977) (bad faith includes terminating acommissioned employee on the brink of sale, deprivation ofthe portion of any commission, and forfeiture of benefitsalmost earned by the rendering of financial services);Gram v. Liberty Mutual Insurance Co., 384 Mass. 659, 672(1981) (breach of good faith and fair dealing whereterminated employee’s “loss of compensation is so clearlyrelated to an employee’s past service.”). Failing to preciselydefine contractual rights and obligations may make anemployer more susceptible to such claims when terminatingemployees.

The implied covenant of good faith and fair dealing isbreached if an employer terminates an at-will employee inbad faith or other than for good cause resulting in theemployee’s loss of identifiable future compensationreflective of past services. See, e.g., Fortune, 373 Mass. at104-05 (employer cannot terminate employee in bad faith todeprive her of earned but not yet payable compensation);Gram, 384 Mass. at 670 (employer cannot terminate anemployee without good cause, i.e., for reasons which are“bad, unjust and unkind” and contrary to the employee’s“reasonable expectations” and, as a result, deprive theemployee of compensation she has earned but not yetreceived).

Bonus programs, commission incentive programs and equitygrants are all susceptible to breach of the implied covenantclaims. The key question posed is when is a bonus,commission or equity grant “earned”? To the extent poordrafting leaves these questions less than clearly answered, anemployer essentially invites a court to fill in the gaps throughapplication of the implied covenant of good faith and fairdealing. Equity vesting illustrates this issue. When anemployee is terminated shortly before a vesting date, anissue can arise as to whether the employee has “earned” or“virtually earned” vesting. Courts have not dealt with thisquestion uniformly. For example, the First Circuit hasreasoned that a vesting schedule “audibly delineates betweenpart and future services” and, accordingly, already vestedstock corresponds with past services. Sergeant v. Tenaska,Inc., 108 F.3d 5, 9 (1st Cir. 1997). However, in Thompsonv. Sundance Publishing, Inc., Mass. Super., C.A. No. 95-02748 (Dec. 15, 1997), the Superior Court found that an

32

employee was entitled to one year’s worth of vesting whenhe was terminated approximately three weeks prior to anannual vesting date.