asset securitisation and long term financing in the power sector

TRANSCRIPT

Asset Securitisation&

Long Term Financing in the Power Sector

A presentationto

Nigerian Electricity Regulatory Commission25th of January, 2007

By

Mr. Sonnie AyereManaging Director / CEO

UBA GLOBAL MARKETS

Introduction

Debit Capital MarketsPrepared bySonnie Ayere

Introduction

What is Securitisation ?

l Securitisation is the raising of debt secured on the cashflow and/or collateral value of a selected pool of assets

l Securitisation debt is non-recourse to the originator, so that investors depend solely on the performance of the assets and are insulated from the financial condition of the originator

Debit Capital MarketsPrepared bySonnie Ayere

Introduction cont’

l Pure asset securitisation is generally achieved by legally and economically isolating the receivables / assets from the balance sheet of the originator

l This is achieved by what is commonly referred to as a “True Sale” of the assets or receivables

Range of Debt Markets &

Assets

Debit Capital MarketsPrepared bySonnie Ayere

Range of Debt Markets

Actively Tradedbonds

Commercial Paper

Non tradablePrivate Placements

Publicissue

TradablePrivate Placements

Illiquid Highly liquid

Debit Capital MarketsPrepared bySonnie Ayere

Range of Assets

l Generally, any asset that produces a certain level of predictable cashflow can be securitised

l Both short-term (e.g. trade credit ) and long-term (residential mortgages) can be securitised

Debit Capital MarketsPrepared bySonnie Ayere

Range of Assets cont’

l Examples of asset types that have been securitised

l Residential and Commercial Mortgages

l Auto / Equipment / Aircraft Leases

l Credit Card Receivables

l Auto and Consumer Loans

l Bank and Corporate Debt

l Trade Receivables

l Export and Domestic Corporate Receivables

l Air Ticket Receivables

l Workers Remittances

Typical Structure of a Securitisation

Debit Capital MarketsPrepared bySonnie Ayere

Typical Structure of a Securitisation

Subordinated or Mezzanine

Investor

SeniorInvestors

Sale & Service ofReceivables

Debt Service

Debt Service

PurchaseReceivables

Sell ABS

Retain Residual Interest (First Loss)

SPVSpecial Purpose Issuing Vehicle

Receivables Pool

Sr. ABS(AAA)

Mezz. ABS(BBB/BB)

Jr. ABS(Equity)

Sell ABS

Seller, Servicer

Receivables Pool

Assets Liabilities

Assets Liabilities

Debit Capital MarketsPrepared bySonnie Ayere

Key Elements of Securitisation

l In-depth knowledge of the assets

l Isolation / transfer of assets

l Servicing

l Credit Rating (Domestic or International)

l Legalese and Deal Documentation

l Placement

l Monitoring

Debit Capital MarketsPrepared bySonnie Ayere

Basic Transfer Mechanism

AccountsReceivable

Accounts Receivable

SPONSORING COMPANY

Sale or Assignment

ISSUES

ASSET-BACKED

SECURITIES

SPECIAL PURPOSE

VEHICLE

Debit Capital MarketsPrepared bySonnie Ayere

Methods of Asset Transfer

l Novation – An arrangement that involves the termination of the existing contract and the writing of a new one

l Sub-Participation Funded or Unfunded - Involves one party depositing monies which may only be repaid when the underlying assets pays or unfunded when the related loan is drawn or the the asset defaults

l Assignment – Full transfer of the assets to the assignee

Case Study

Debit Capital MarketsPrepared bySonnie Ayere

Case Study IPP Securitise its Receivables

l Some factors need to be in place before a securitisation can occur. Some of which are:-

– Corporate commitment

– Management depth

– Internal systems (servicing, and collection)

– Available and up to date information (company and collateral)

– Origination capacity

Debit Capital MarketsPrepared bySonnie Ayere

l Other factors necessary are :-

– Ability to legally assign receivables

– Enforceability of law

– Ability to perfect interest quickly - property

– At least a 5 year fixed rate government curve – the longer the better

– Electronic payment systems e.g. direct debits

Case Study IPP Securitise its Receivables

Debit Capital MarketsPrepared bySonnie Ayere

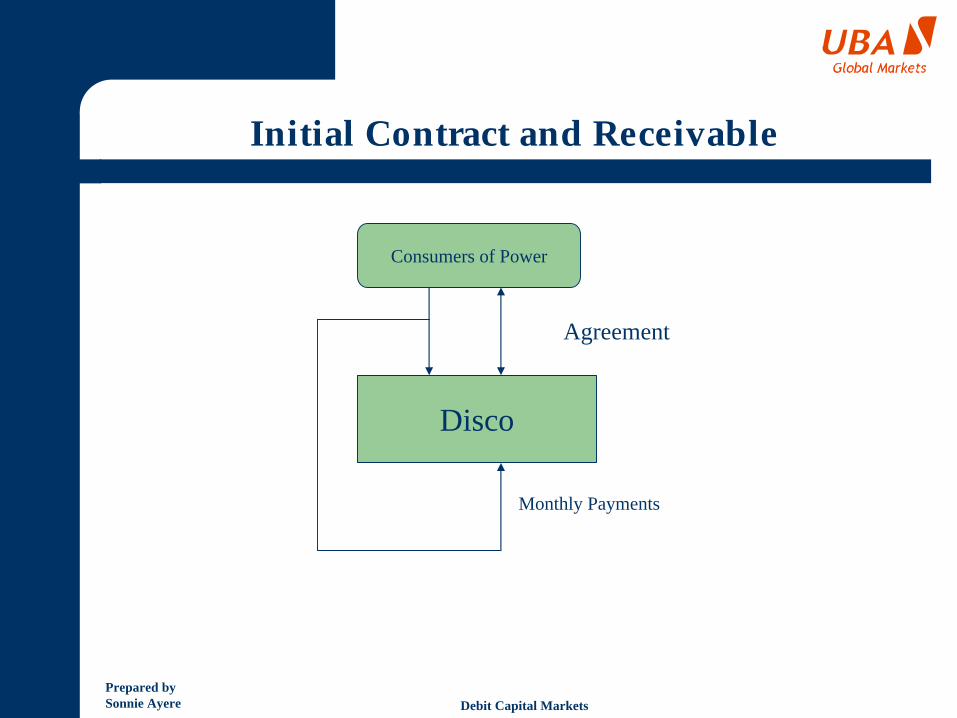

Initial Contract and Receivable

Consumers of Power

Disco

Agreement

Monthly Payments

Debit Capital MarketsPrepared bySonnie Ayere

Transfer of Receivables to SPV

Consumers

Disco

Monthly

Payments

ReceivablesFunding Trust

Investorsproceeds

Sale of monthly payments

proceeds

Asset Backed

Securities

Debit Capital MarketsPrepared bySonnie Ayere

Independent Trustee appointed & reallocation of cashflow

Consumers

Disco

Monthly Payments

ReceivablesFunding Trust - A

Investorsproceeds

Sale of

Receivables

proceeds

Asset Backed

Securities

Trustee

Principal &

Interest

Debit Capital MarketsPrepared bySonnie Ayere

Allocation of Excess Spread

Consumers

Disco

Principal &

Interest

ReceivablesFunding Trust - A

Investorsproceeds

Sale of

Receivables

proceeds

Asset Backed

Securities

Trustee

Principal &

Interest

Excess Spread + Servicing Fees

Debit Capital MarketsPrepared bySonnie Ayere

Introduction of Swap counter-party and Guarantor

Consumers

Disco

Principal &

Interest

ReceivablesFunding Trust - A

Investorsproceeds

Sale of Assets

proceeds

Asset Backed

Securities

Trustee

Principal &

Interest

Excess Spread + Servicing Fees

Swap Counter party

FinancialGuarantor

Debit Capital MarketsPrepared bySonnie Ayere

Other form of Credit Enhancement considered

Consumers

Disco

Principal &

Interest

ReceivablesFunding Trust - A

Investorsproceeds

Sale of

Receivables

proceeds

Asset Backed

Securities

Trustee

Principal &

Interest

Excess Spread + Servicing Fees

Swap Counter party

FinancialGuarantor

Debit Capital MarketsPrepared bySonnie Ayere

Use of Senior/subordinated Structure

Consumers

Disco

Principal &

Interest

ReceivablesFunding Trust - A

Investorsproceeds

Sale of

Receivables

proceeds

Asset Backed

Securities

Trustee

Principal &

Interest

Excess Spread + Servicing Fees

Swap Counter party

AAASenior

BBBMezzanine

Equity

Debit Capital MarketsPrepared bySonnie Ayere

Senior Subordinate Structure

l This is the most common kind of structure /credit enhancement for the following reasons :-

– Internal credit enhancement and therefore, generally speaking, the cheapest form of credit enhancement

– However, the ability to calculate the expected loss of each tranche and size the required credit enhancement is imperative

– The adviser and rating agency is usually responsible for this work

Debit Capital MarketsPrepared bySonnie Ayere

Typical Senior/Sub structure example

l As noted above, the cost of funding to the issuer is close to the interest rate of the AAA bond

Debit Capital MarketsPrepared bySonnie Ayere

Other types of Credit Enhancement

l Monoline Insurance

l Letters of Credit

l Reserve / Spread Account

l Cash Collateral Loan / Subordinated Loan

l Yield Supplement Account

Rating a Transaction

Debit Capital MarketsPrepared bySonnie Ayere

Rating the transaction

l Credit risk

l Liquidity risk

l Servicer performance risk

l Swap counter-party risk

l Guarantor risk

l Legal risk

l Sovereign risk

l Interest rate and currency risks

l Prepayment risk

Debit Capital MarketsPrepared bySonnie Ayere

How does the rating help

l Rating is an indication of the likelihood of credit losses on the securitised assets exceeding the available credit protection to the transaction structure

l Ratings are widely accepted by investors (and the agency must becertified by the regulators)

– To the investor, it creates efficiency, provides pricing benchmarks and carries highly condensed information

l Moodys, Standard and Poors and Fitch Ratings have global recognition

Benefits of Securitisation

Debit Capital MarketsPrepared bySonnie Ayere

Benefits of Securitisation

l The three main market constituents -

l Originator – Underlying Lender / owner of asset

l Investors - Buyers

l Underlying Borrowers – Obligors

l Others are -

l Credit Enhancement Provider

l Liquidity Facility Provider

l Servicer

l Trustee

Debit Capital MarketsPrepared bySonnie Ayere

Benefits to the Parties

Originator

1. Progressively cheaper and longer term funding

2. Diversification of funding sources

3. Timing Flexibility

4. Stable funding source

5. Improved credit risk management

6. Improved asset-liability management

7. Often improved operating efficiency

8. Increased Transparency

Debit Capital MarketsPrepared bySonnie Ayere

Benefits to the Parties cont’

Investor

1. Opportunity to invest in a risk that is much lower than that of the originator

2. Direct investment in the performance of the underlying asset

3. Generally, allows the investor to worry less about event risk

4. Asset Liability matching e.g. pension funds

5. Provides investors with different risk return opportunities e.g.senior or subordinated tranches

Debit Capital MarketsPrepared bySonnie Ayere

Benefits to Parties cont’

Underlying Borrower / Obligor

1. Cheaper, longer term funding

2. Increased flexible credit for consumers and corporations

3. Diversification of funding sources

4. Tapping into a new investor base.

Typical Regulatory Issues

Debit Capital MarketsPrepared bySonnie Ayere

Legal and Regulatory

l Legal

l Asset Transfer

l The Special Purpose Entity or Vehicle

l Bankruptcy Remoteness

l Regulation

l Taxation

Debit Capital MarketsPrepared bySonnie Ayere

Conditions for True Sale

l Transfer must be a true sale, or its legal equivalent. If originator is only pledging the assets to secure a debt, then it becomes a collaterised financing in which the originator would stay directly indebted to investor

l The assets must be owned by a special purpose entity, whose ownership of the sold assets will in all probability survive the bankruptcy of the originator/seller

l Actual ownership of the special purpose vehicle must be independent of the originator

Debit Capital MarketsPrepared bySonnie Ayere

Confirmation of a asset sale

l The treatment and form of the transaction

l The influence the seller has on the assets after the sale

l The extent and nature of benefits transferred via the sale

l The purchase price

l Notification (if necessary) to underlying borrowers when assets are sold

l Title ownership

Debit Capital MarketsPrepared bySonnie Ayere

The Special Purpose Vehicle

l Generally set up by the originator with ownership vested in a charitable trust

l Commonly set up in tax havens l Mauritiusl Cayman Islandsl Jersey

l Apart from legally isolating the assets it also helps to avoid double taxation and hence reduce the expenses (if any) of the trust

l Cost of set-up an SPV is low

Debit Capital MarketsPrepared bySonnie Ayere

Why Bankruptcy Remote

l Only assets in the SPV are available to protect and pay investors

l No need for protection from creditors

l All obligations are limited to those available from the assets

l No recourse to the originator

l The vehicle can only receive the assets as purchased and issue notes or certificates

l Hence, probability of Bankruptcy is remote

Debit Capital MarketsPrepared bySonnie Ayere

Regulation

l Bank Regulators will place a strong emphasis on the the amount of regulatory capital accorded to the transaction

l For instance, regulators in certain countries will insist that issuing bank hold 100% Risk Weighted Capital to Equity portion of the transaction *

l This will differ from country to country and will normally be defined by the securitisation laws of the country

l FASB 46 …? Consolidation of VIEs - Somewhat mitigated by QSPE under FAS 140

Debit Capital MarketsPrepared bySonnie Ayere

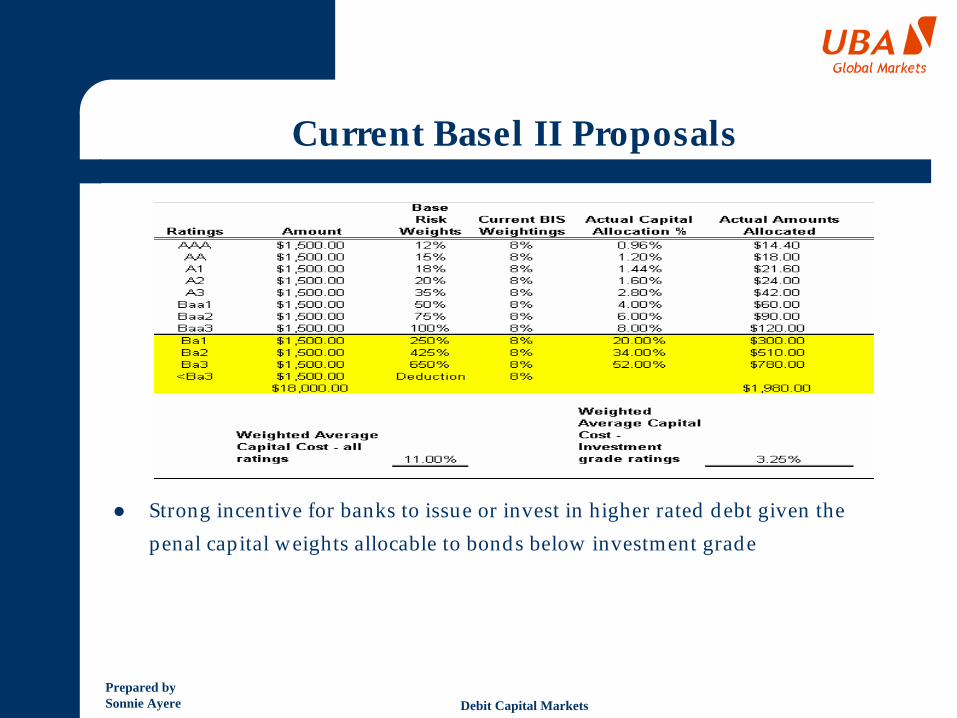

Current Basel II Proposals

l Strong incentive for banks to issue or invest in higher rated debt given the penal capital weights allocable to bonds below investment grade

Debit Capital MarketsPrepared bySonnie Ayere

SPV Taxation

l Generally speaking, the Special purpose Entities are carefully structured to ensure that its income is offset by its expenses so that little or no tax is incurred

l Tax incentives are however provided to special assets classes – e.g. most countries exempt the transfer of mortgages from Stamp Duty

Deal Structuring

Debit Capital MarketsPrepared bySonnie Ayere

Initial Deal Concept

l The structure of a transaction typically depends on the following :-

– Underlying asset class

– Investor preference

– Cost

Debit Capital MarketsPrepared bySonnie Ayere

Underlying Asset

l The way an asset pays is strongly correlated to the liabilities created

l For example, a lease is not an interest bearing asset but it can still be securitised

l Two things come about from securitising these assets

– Fixed rate bonds (internal or external swaps can be used to create a floating rate note)

– Leases are sold at discount to produce the expected yield

– Generally no excess spread

Debit Capital MarketsPrepared bySonnie Ayere

Investor Preference

l Investors have a strong influence on the deal structure by having a preference for :-

– Tenors required

– Rating required

– Spreads required

– Prepayments

– Whether bonds are fully amortising, soft bullets, etc.

Debit Capital MarketsPrepared bySonnie Ayere

Cost

l Issuers and their advisors will also consider the cost of one structure against another. For example :-

– Wrapping a deal by a Monoline may be less expensive than getting a Letter of Credit

– Overcollateralisation may prove more expensive than a senior/subordinated structure

Debit Capital MarketsPrepared bySonnie Ayere

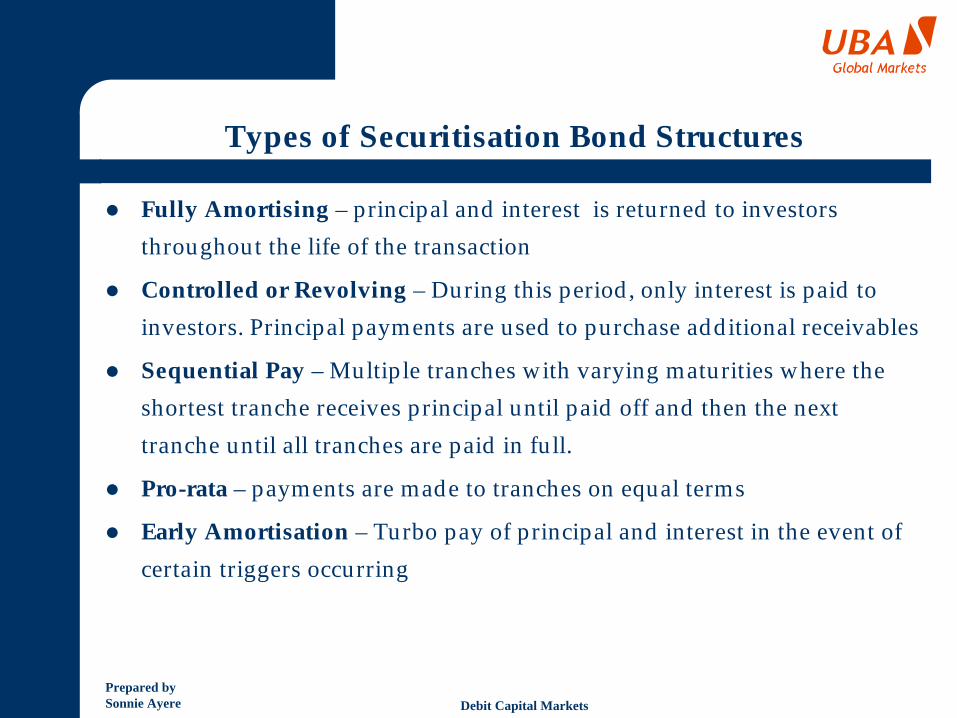

Types of Securitisation Bond Structures

l Fully Amortising – principal and interest is returned to investors throughout the life of the transaction

l Controlled or Revolving – During this period, only interest is paid to investors. Principal payments are used to purchase additional receivables

l Sequential Pay – Multiple tranches with varying maturities where the shortest tranche receives principal until paid off and then the next tranche until all tranches are paid in full.

l Pro-rata – payments are made to tranches on equal terms

l Early Amortisation – Turbo pay of principal and interest in the event of certain triggers occurring

Analytics

Debit Capital MarketsPrepared bySonnie Ayere

Analytical Concepts commonly used

l Loan-by-loan analysis

l Cash-flow modeling

l Stratification

l Monte Carlo Simulation

l Prepayment Modeling

l CBO Analysis: S&P’s CDO Model or Moody’s Binomial Expansion Method

Debit Capital MarketsPrepared bySonnie Ayere

Example of Expected Loss Calculation

Debit Capital MarketsPrepared bySonnie Ayere

Understanding the Prospectus

l Is the interest in loans perfected

l Title perfection triggers

l Set-off risk

l MIG Cover

l Basis Swap

l Compensating interest

l Definition of Interest and Principal

l Definition of Delinquencies and Charge-offs

l Any internal swap – How does it work

l Legal Nuances

l Any supplements

Trading Platforms

Debit Capital MarketsPrepared bySonnie Ayere

Trading

l MBS/ABS generally trade Over The Counter – ‘OTC’ as in most fixed income securities

l They trade similar to all other bonds however, the understanding of the underlying asset and structure is crucial

l Option Adjusted Spread ‘OAS’ – the ability to price the optionality in the bond due to step-ups etc is also crucial

l Trades are generally conducted by counter-parties using Bloomberg or other terminals

Debit Capital MarketsPrepared bySonnie Ayere

How does UBA Global get involved

l Structuring mandates

l Advisory mandates

l Advising and structuring credit and liquidity enhancement

Examples of infrastructure transactions globally

Debit Capital MarketsPrepared bySonnie Ayere

Universidad Diego Portales Chile

• 1,000,000 UF ($23 mm in inflation indexed Chilean pesos) eight-year bond secured by UDP’s future tuition receipts and backed by a 30% partial guarantee from IFC;

• Rated AA- by local affiliates of Moody’s, S&P, and Fitch;

• The bond, which was oversubscribed, was bought by domestic institutional investors including pension funds, insurance companies, and mutual funds. The issue priced tight to expectations, yielding 240 basis points over the Chilean Treasury;

• The transaction represented the first future flow securitization in Chile, and the first future flow for a university in Latin America.

Debit Capital MarketsPrepared bySonnie Ayere

Partial Credit Guarantee – Bharti Mobile (India)

•Bharti Mobile, which operates cellular licenses in India, is a part of of BhartiEnterprises, one of India’s leading telecom conglomerates.

•As Bharti’s revenues are in Indian rupee, the management placed an importance on raising long-term rupee financing in order to best match the company’s assets and liabilities.

•IFC offered a partial guarantee on three different tranches with tenors of five, eight, and ten years respectively in order to reach the widest audience of investors.

•The transaction was IFC’s second partial guarantee of a bond issue in India and opened the door for other borrowers to raise long-term local currency financing.

•Structured as three different offerings with tenors of five, eight, and 10 years respectively;

•Total issue size of Indian Rupees 2.1 billion ($45 million);•Rated AA+ by Indian affiliates of S&P and Moody’s;•Placement to domestic mutual funds, banks, life insurance companies, and other

institutional investors;•Well received by market with significant oversubscription.

Debit Capital MarketsPrepared bySonnie Ayere

BANCO DAVIVIENDA COLOMBIA

• UVR 1 billion ($50 million equivalent in inflation indexed Colombian pesos) 10 year non-call five, subordinated step-up bond;

• 30% guarantee by IFC;

• Rated AA+ by local affiliate of Fitch;

• Placed within 1 day to domestic institutional investors;

• First-ever bond issue in Colombia to qualify as Tier 2 capital under the newly issued guidelines.

Debit Capital MarketsPrepared bySonnie Ayere

Triple A Example

• Securities: COP$ 180 billion (US$63 million equivalent) 10-year bond issue, amortizing over last 5 years

• Guarantee: IFC Guarantee equal to greater of (i) 25% of principal or (ii) 5 coupon payments

• Rating: 3-notch rating increase from AA- to AAA

• Other enhancements: (a) Company revenues managed by Trustee, (b) Reserve account contributed by Sponsor

• Placement: Subscribed in 4 hours by over 15 institutional investors

• Pricing: Priced at IPC + 8.5% (120 bps > Gov.)

Thank You

Debit Capital MarketsPrepared bySonnie Ayere

Sonnie Ayere - BiographyMr. Sonnie Ayere Mr. Sonnie Ayere

Mr. Ayere has over 14 years continuous years of solid Corporate Mr. Ayere has over 14 years continuous years of solid Corporate and Structured Finance, Banking and Asset Management and Structured Finance, Banking and Asset Management experience working with HSBC, Royal Bank of Scotland (formerly, experience working with HSBC, Royal Bank of Scotland (formerly, NatWestNatWest), Sumitomo Mitsui Bank, Bank of Montreal ), Sumitomo Mitsui Bank, Bank of Montreal Nesbitt Burns in London and the International Finance CorporatioNesbitt Burns in London and the International Finance Corporation (The World Bank Group). n (The World Bank Group).

He began his structured finance career in 1997 when he joined thHe began his structured finance career in 1997 when he joined the structured finance / securitization team of Sumitomo Mitsui e structured finance / securitization team of Sumitomo Mitsui Bank, London. He was part of the team that structured the first Bank, London. He was part of the team that structured the first ever Japanese deever Japanese de--linked Balance Sheet linked Balance Sheet CollaterisedCollaterised Loan Loan Obligation Obligation securitisationsecuritisation –– GBP1.4bn Aurora Funding. He was also responsible for managing tGBP1.4bn Aurora Funding. He was also responsible for managing the bankhe bank’’s fixed income portfolio s fixed income portfolio in ABS investments in other asset classes for the bankin ABS investments in other asset classes for the bank’’s own balance sheet. s own balance sheet.

Following this, he joined BMOFollowing this, he joined BMO--Nesbitt Burns (the investment banking arm of the Bank of MontreaNesbitt Burns (the investment banking arm of the Bank of Montreal) London in 1998 as part of the l) London in 1998 as part of the team responsible for setting up a US$20bn Fixed Income Structureteam responsible for setting up a US$20bn Fixed Income Structured Investment Vehicle (d Investment Vehicle (““SIVSIV””), with a US$2bn Capital Note ), with a US$2bn Capital Note Program which launched in 1999. He was involved in the companyProgram which launched in 1999. He was involved in the company’’s set up, compiling aspects of its procedures manual, s set up, compiling aspects of its procedures manual, system evaluation and testing and subsequently responsible for asystem evaluation and testing and subsequently responsible for analyzing and investing / trading in various ABS/MBS and nalyzing and investing / trading in various ABS/MBS and other asset classes other asset classes –– bank subordinated debt and other corporate debt plus the onbank subordinated debt and other corporate debt plus the on--going credit monitoring of the portfolio. going credit monitoring of the portfolio.

He joined the Global Structured Finance Group of the InternationHe joined the Global Structured Finance Group of the International Finance Corporation (The World Bank Group) in Washington al Finance Corporation (The World Bank Group) in Washington DC in 2001 where he was responsible for originating structured fDC in 2001 where he was responsible for originating structured finance and securitization transactions globally, notable inance and securitization transactions globally, notable transactions include transactions include IFCIFC’’ss role as structuring investor in South Africa Home Loans first Rrole as structuring investor in South Africa Home Loans first Residential Mortgage Backed ZAR 1bn esidential Mortgage Backed ZAR 1bn Offering and structuring securities backed by ContractsOffering and structuring securities backed by Contracts--toto--sale in the Philippines. Mr. Ayere assumed the role of Structuresale in the Philippines. Mr. Ayere assumed the role of Structured d Finance Specialist for SubFinance Specialist for Sub--Saharan Africa in July 2002 and to date has been responsible forSaharan Africa in July 2002 and to date has been responsible for developing structured finance and developing structured finance and securitization transactions and developing debt capital market isecuritization transactions and developing debt capital market instruments for the bank and its clients across the continent. Innstruments for the bank and its clients across the continent. InSeptember, 2004 he also became coSeptember, 2004 he also became co--head / sector lead for financial markets business development fohead / sector lead for financial markets business development for Subr Sub--Saharan Africa. Saharan Africa. Here, he was responsible for generating financial market investmHere, he was responsible for generating financial market investments across the region to includes US$ lines of credit to new ents across the region to includes US$ lines of credit to new and existing IFC relationship banks. He pioneered and existing IFC relationship banks. He pioneered IFCIFC’’ss interest in developing the Nigerian bond market and was a princinterest in developing the Nigerian bond market and was a principal ipal adviser to the DMO on the development of the market. He is a memadviser to the DMO on the development of the market. He is a member of the Nigerian Bond Steering Committee.ber of the Nigerian Bond Steering Committee.

He joined UBA Group as Managing Director/CEO of UBA GLOBAL MARKEHe joined UBA Group as Managing Director/CEO of UBA GLOBAL MARKETS, the combined investment banking subsidiary of TS, the combined investment banking subsidiary of the bank group in August, 2005. the bank group in August, 2005.

Mr. Ayere obtained an MA (Mr. Ayere obtained an MA (HonsHons.) in Financial Economics from the University of Dundee .) in Financial Economics from the University of Dundee –– Scotland. He is an Alumni of City Scotland. He is an Alumni of City University Business School London (MBA) and London Business SchoUniversity Business School London (MBA) and London Business School (Corporate Finance Program).ol (Corporate Finance Program).