asia competition barometer: petrochemicals and chemicals

TRANSCRIPT

Asia Competition BarometerPetrochemicals and chemicalsAn Economist Intelligence Unit report

Supported by

© The Economist Intelligence Unit Limited 2012 1

Asia Competition Barometer:Petrochemicals and chemicals

Contents

Preface 2

Executive summary 3

Asia’s growing importance for corporate performance and global competitiveness 5

Competition and profitability at Asian firms 8 Competition: Declining since 2008 8

Profitability:Slightoveralldecline 10

Commodity prices 12

Case study: Tata Chemicals 12

Positioning for success in Asia 13 Asiaremainsvitalbothasamarketandasaproductionsource 13

Evolvingsupplychainsandpartnerships 14

Case study: BASF 15

Outlook 16

Barometer methodology 17

© The Economist Intelligence Unit Limited 20122

Asia Competition Barometer:Petrochemicals and chemicals

SupportedbySingapore’sEconomicDevelopmentBoard(EDB),theEconomistIntelligenceUnithasdevelopedtheAsiaCompetitionBarometerwiththeaimofunderstandingthechangingmarketdynamicsinkeysectorsandassessingtheintensityofcompetitioninthem.Drawinguponcompany-leveldataonprofitabilityandotherindicators,theBarometerquantifiesthechangingdynamicsofcompetitivenessinAsiaforselectindustriesbetween2004and2009.

ThisreportfocusesontheBarometerfindingsforthepetrochemicalsandchemicalsmanufacturing(PeC)sector.Assessingauniverseofover550PeCcompaniesthatarepubliclylistedineightcountries—China,India,Indonesia,Malaysia,thePhilippines,Singapore,ThailandandVietnam—theBarometerexamineschangingprofitabilityandthecompetitionlandscapeforthesector.

Otherreportsinthisserieslookattheinformationtechnologyservices,pharmaceuticals,precisionengineering,andtransportandlogisticssectorsinAsia.

February2012

Preface

© The Economist Intelligence Unit Limited 2012 3

Asia Competition Barometer:Petrochemicals and chemicals

Executive summary

WhatdoestheemergenceofAsiaasamajorengineofglobaleconomicgrowthmeanforcompaniesoperatingintheregion?Asia’srobusteconomicoutlook—coupledwithdiminishedgrowthprospects

inmanyotherpartsoftheworld—hasattractednewinvestmentintothemarketbothfromregionalplayersandWesternmultinationals(MNCs).Asaresult,competitionintheregionisexpectedtointensify.Giventhedarkeningglobaleconomicoutlook,andtheexpectedimpactonsomeeconomiesandsectorsintheregion,growthandprofitabilitylookuncertaininthenearterm.Butoverthemediumtolongerterm,Asia’sstrongeconomicfundamentalswillensureconsistentgrowthacrossarangeofindustries.HowarecompaniespositioningthemselvestocapitaliseonAsia’sgrowthopportunitiesoverthenextfewyears?

TheAsiaCompetitionBarometerassessestheintensityofcompetitionandchangingmarketdynamicsinseveralkeysectors.Thisreportexaminesthepetrochemicalsandchemicalsmanufacturing(PeC)sector,whichincludes:basicchemicals,fertilisersandnitrogencompounds,plasticsandsyntheticrubberinprimaryforms,pesticidesandotheragrochemicalproducts,paints,varnishesandsimilarcoatings,printinginkandmastics,soapanddetergents,cleaningandpolishingpreparations,perfumesandtoiletpreparations,explosives,otherchemicalproductsandman-madefibres.

Amongthekeyfindingsofthisreportarethefollowing:

• Asia’s PeC sector has been expanding rapidly, in line with the region’s stellar economic growth.Severalbroadmacroeconomictrends,includingAsia’semergenceasaglobalmanufacturingpowerhouse,haveboosteddemandforPeCproductsandservicesintheregion,andwillcontinuetodoso.Inparticular,demandfromtheconsumergoods,agriculture,automotiveandconstructionsectorswilldrivetheregion’sPeCsector.Meanwhile,theincreasingglobalandregionalemphasisonsustainabledevelopmentandalternativeenergysourceswillcreatenewpotentialmarketsforPeCfirms.Theindustryisexpectedtogrowatacompoundannualgrowthrateof10.5%between2010and2015,bywhenitwillbeworthsomeUS$2.6trn,accordingtoDatamonitor,aresearchfirm.

© The Economist Intelligence Unit Limited 20124

Asia Competition Barometer:Petrochemicals and chemicals

• The number of players in Asia’s PeC sector has risen since 2004, though recent consolidation suggests that this growth may be moderating.Thenumberandsizeofpublicly-listedfirmsinthePeCsectorinAsiahasincreaseddramatically,from376firmsin2004to549in2009.TotalcombinedrevenuesmorethandoubledfromUS$113.2bntoUS$256.3bnduringtheperiod.However,withongoingconsolidationthegrowthinthenumberoffirmsmaybemoderating—from2008to2009,thenumberofpublicly-listedPeCcompaniesinAsiaactuallydeclinedfrom559to549.Meanwhile,inrecognitionofAsia’sincreasingimportancetotheglobalPeCsector,foreignMNCshavebeenbuildinguptheirpresenceintheregion.ThelatterareincreasinglyviewingAsianotonlyasakeymarketbutalsoavitalsourceofproduction.

• Competition has decreased marginally, and large players are growing stronger. Competition in the PeCindustrygrewslightlybetweentheyears2004and2007,largelyduetoaninfluxofnewplayersintothesector.However,between2007and2009thelargestfirmsintheindustrybegantosteadilyincreasetheirmarketshare,partlybyexploitingeconomiesofscale.Withongoingconsolidationintheindustryitseemslikelythatthebiggerfirms,withresourcestoinvestinresearchanddevelopment,andseekoutlower-costsourcesoffeedstockandenergy,willcontinuetogrowindominance.

• Despite a slight overall decline, profitability in the sector has remained relatively resilient.ProfitmarginsforthePeCindustryin2009havefallenslightlyrelativeto2004,andhavegenerallyfluctuatedbroadlyintandemwithglobaleconomicgrowth.Theaveragegrossmarginofpublicly-listedAsianfirmsdeclinedfrom21.5%in2007to18.4%in2008.Thiswaslargelyduetoaslowdownindemandamidtheglobaleconomicdownturn,andaspikeinthecostofrawmaterials,suchasoil,thatyear.Theaveragegrossmarginthenbouncedbacktoreach21.4%by2009.Thiswaspartlybecauseofindustryconsolidation—whenrevenuegrowthslowedasaresultofthecrisis,thesmallerplayerscouldnotkeeppacewithlargeMNCsandstate-ownedcompanies,whowereabletofurtherexploiteconomiesofscaleandgrowtheirmarketshare.Inthecomingyears,profitabilitywillbelargelydependentoninnovation,theabilitytotapintomarketsthatarerelativelyunderpenetrated,andaccesstoresources.

• Access to resources has displaced low labour costs as the key driver of competitive advantage, disrupting traditional industry supply chains.Inasectorwithlittleproductdifferentiation,oneofthebiggestprofitabilitydriversispreferentialaccesstolow-costenergyandrawmaterialssuchasoil,naturalgas,water,metalsandminerals.IndustrysupplychainsarehencebeingreworkedtotapresourcesinplacessuchastheMiddleEast.Asaresult,thesectorisalsoseeinganincreasingnumberofpartnershipsbetweenMNCswithglobalnetworksandtechnologicalknow-how,andlocalplayers,includingstate-ownedfirms,withaccesstoresources.Followingsteeprisesin2010-11,theEIUexpectsthepricesofoilandnon-oilcommoditiestomoderatesomewhatin2012-16.Nevertheless,PeCfirmswillcontinuetocompetefiercelyforaccesstotheseresources,particularlygiventhesupplyconstraintsinmanycommoditymarkets.

© The Economist Intelligence Unit Limited 2012 5

Asia Competition Barometer:Petrochemicals and chemicals

Asia’s growing importance for corporate performance and global competitiveness

Overthepastdecade,Asiahasrapidlygrowninimportancetotheglobaleconomy.ItsshareofglobalGDP,measuredinpurchasing-powerparityterms,increasedfrom26.8%in2001to33.8%in2010.1

By2016,theEconomistIntelligenceUnit(EIU)expectsthisproportiontoriseto38.9%.ThereareseveralbroadtrendsthathavebeendrivingAsia’spetrochemicalsandchemicals

manufacturing(PeC)sector.2ThefirstisAsia’semergenceasaglobalmanufacturingpowerhouse.Overthepastdecade,Asia’sshareofglobalmanufacturingoutputhasincreaseddramatically,ledbyChina(seeFigure1).ThishasboosteddemandforPeCproductsthatareusedasrawmaterialsforthemanufactureofavarietyofgoods.

Thesecondtrend,whichishelpingtounderpinthefirst,relatestorisingprivateconsumptioninAsia,whichisboostingregionaldemandinanumberofsectors,fromautomobilesandconsumergoodstoconstruction,pharmaceuticalsandfood.DuetoAsia’srapideconomicgrowthoverthelastfewyears,theregionisnowhometoahugeandgrowingmiddleclass.TheAsianDevelopmentBank(ADB)estimates

1AsiahereincludesBangladesh,China,HongKong,Indonesia,India,Japan,SouthKorea,Malaysia,Myanmar,Philippines,Pakistan,Singapore,SriLanka,Thailand,Taiwan,andVietnam

2ThePeCsectorincludesthefollowingsub-segments:basicchemicals,fertilisersandnitrogencompounds,plasticsandsyntheticrubberinprimaryforms,pesticidesandotheragrochemicalproducts,paints,varnishesandsimilarcoatings,printinginkandmastics,soapanddetergents,cleaning and polishing preparations,perfumesandtoiletpreparations,explosives,otherchemicalproductsandman-madefibres.

Figure 1: Share of world manufacturing output(%, constant 2000 US$)

0

3

6

9

12

15

IndiaTaiwanSouth KoreaASEANChina

2000 2009

Note: ASEAN here comprises Indonesia, Malaysia, The Philippines, Singapore, Thailand and Vietnam

Source: UNIDO

© The Economist Intelligence Unit Limited 20126

Asia Competition Barometer:Petrochemicals and chemicals

thatbetween1990and2008developingAsia’smiddleclasspopulationmorethantripledfrom565mto1.9bn.Asashareofthetotalpopulation,itgrewfrom21%to56%overthatperiod.3

Thesenewconsumershavebeenspendingonproductssuchascarsandhouses,whichrelydirectlyonthePeCsectorforinputs.Asiahassomeofthefastestgrowingautomobilemarketsaswellassomeofthelargestautomobilemanufacturersintheworld.In2009,ChinaovertooktheUnitedStatesastheworld’sbiggestcarmarket.Between2011and2015,theEIUexpectsAsiatosee157.5mmorepassengervehiclesand54.7mmorecommercialvehiclesonitsroads.RisingvehiclesaleshaveadirectandnoticeableimpactonPeCsectorperformance,withalagofaboutsixmonths,accordingtoRamakrishnanMukundan,themanagingdirectorofTataChemicals,anIndianchemicalsmanufacturer.

Onaverage,theproductionofonecarrequiresabout155kgofpolymersandotherchemicals,valuedataboutUS$2,300.4Examplesofchemicalproductsusedinautomobilemanufacturingincludepolypropylene,polyethylene,polycarbonate,polyvinylchloride,polyesterfabric,adhesives,primers,powdercoatings,surfacecoatingmaterials,paintsandmetalhandlingandpolymeradhesives.Theyareusedinawholevarietyofwaysincludingdashboards(vents,gauges,dialsandpanelling),steeringwheels,seats(armrests,headrests,foam),coatingsfortheoutsideofthevehicle,tyres,andfoamforroofing,amongothers.

RisingincomesinAsiahavealsoledtoaboomintheregion’sconstructionsector,whichusesarangeofPeCinputs,includingcellulosics,whosemarketgrewby15%in2011.“Newconstructionismainlydrivenbyinfrastructureandhousingneedsofcountrieswithstrongmigrationmovementsofyoungpopulationsintourbaneconomiccentres,”TilmanKrauch,headofBASF’sconstructionchemicalsdivision,wasquotedassaying.5

Theworldmarketforconstructionchemicalsisexpectedtogrowatanannualaverageof5%perannumfromUS$30.7bnin2009toUS$39.2bnin2014,accordingtoSRIConsulting.6Chinawillaccountformuchofthisgrowth,withitsmarketexpandingbyanannualaverageof9%perannumfromUS$7.9bntoUS$12.1bnoverthatperiod.Tomeetthegrowingdemand,globalcompaniesareinvestinginAsia.AmericanfirmDowConstructionChemicals,forinstance,planstoexpanditscellulosicproductioncapacityinAsia.7

Intheareaofinfrastructure,manyAsianeconomies,despiteyearsofrapidgrowth,stillfacehugeinfrastructuredeficits.Asaresult,thereismuchpublicandprivatespendingonroads,ports,bridgesandotherinfrastructure,allofwhichrequirePeCinputsfortheirconstruction.

Asia’sgrowingfoodconsumptionisanotherdemandbooster.AccordingtoMrMukundan,agricultureandfarm-relatedchemicalsisthesegmentshowingthe“mostrobustgrowth”intermsofprofitability.“Themarginstructuresoffertilisercompanieshavebeeninkeepingwithfoodprices,”headds.

AthirdtrendthatwilldrivethePeCindustryisthegrowingemphasisonsustainabledevelopmentandalternativeenergysources.ChemicalproducerBASFsees“strongpotentialinsolutionsthatcontributetosustainabledevelopment,”saysAlbertHeuser,thefirm’spresidentformarketandbusinessdevelopmentinAsiaPacific.Forinstance,BASFestimatesthatby2020theglobalmarketforitswindpowerproducts—includingepoxysystems,corefoams,advancedcoatingsandhydraulicfluids—willbeworthsome€300m(US$390m).Muchofthissegment’sgrowthwillcomefromChina,whichisalreadytheworld’slargestwindpowermarket.

4“Globalchemicalindustryrecovers,butanautomotiveshifttoAsiawillposemorechallenges”,ICIS,March22nd2010

3“TheriseofAsia’smiddleclass”,AsianDevelopmentBank,2010

5“Urbanizationtrendboostsconstructionchemicalsmarket”,ICIS,July9th2010

6Citedin“ChemicalsandConstruction:BuildingaFutureTogether”,KPMG,June13th2011

7“DowplanstoexpandcellulosicproductioncapacityinAsia-Pacific”,Chemicals-technology.com,Dec12th2001

© The Economist Intelligence Unit Limited 2012 7

Asia Competition Barometer:Petrochemicals and chemicals

Thefourthtrendisgrowingdemandforpotablewater.Millionsofpeople,particularlyincountriessuchasIndia,donothaveaccesstosafedrinkingwater.MrHeuseridentifieswaterproductsandservicesasakeygrowthsegment.BASFbelievesitcancapturearound€800m(US$1bn)oftheestimated€20bn(US$26bn)globalwatertreatmentandpurificationmarket.

ForeignPeCfirmshavebeenoperatinginAsiaforseveraldecades.Recently,inrecognitionofAsia’sgrowingimportance,theyhavebeeninvestingheavilyintheregion.BetweenJanuary2004andDecember2011,fDiMarkets,aresearchhouse,recordedatotalof1,512projectsinAsia.MostofthoseinvestmentsoriginatedfromtheUS(24%oftheinvestmentprojects),Japan(24%)andGermany(15%).ThetopthreeinvestmentdestinationmarketswereChina(48%oftheinvestmentprojects),India(14%)andThailand(6%).Aboutone-thirdoftheseforeigninvestmentswerefocussedonproductionforregionalmarkets.

© The Economist Intelligence Unit Limited 20128

Asia Competition Barometer:Petrochemicals and chemicals

Competition and profitability at Asian firms

Thenumberandsizeofpublicly-listedfirmsinthePeCsectorinAsiahasincreaseddramatically,by46%between2004and2009,from376firmsto549.Overthesameperiod,thetotalcombinedrevenue

ofpublicly-listedPeCcompaniesmorethandoubledfromUS$113.2bntoUS$256.3bn;thesefirms’combinedtotalassetsrosefromUS$104.2bntoUS$254.2bn.

Competition: Declining since 2008WithmanycompaniesraisingtheirexpectationsofAsiatodelivergrowthandprofits,itisreasonabletoexpectcompetitionintensityintheregiontoincrease.TocapturethisintensitywehaveusedtheHerfindahl–HirschmanIndex(HHI),whichmeasuresthemarketconcentrationofanindustry’slargestfirms.HHIvaluescanrangefrom0(extremelyfragmentedmarket)to1.0(monopoly).Herewehavemultipliedthevaluesby100toachieveascaleconsistentwithprofitabilityindicators(seebelow).

TheHHIforAsia’sPeCindustryincreasedslightlyfrom8.27in2004to8.48in2009,signifyingthatthe50biggestfirmsintheBarometersawamarginalincreaseinconcentrationbetween2004and2009(seeFigure2).8

CompetitioninthePeCindustrygrewbetweentheyears2004and2007.TheHHIdroppedfrom8.27to7.52overthatperiod,signifyingthatthemarketshareofthe50biggestfirmsdeclined.Thisislargelybecauseofaninfluxofnewplayersintothesector—inthosetwoyears,157newAsiancompaniesenteredtheindustry,capturingmuchoftherapidlygrowingmarket.

However,between2007and2009,thelargestfirmsintheindustrybegantosteadilyincreasetheirconcentrationonceagain.TheHHIrosefrom7.52to8.48overthatperiod.Thisismostlybecauseoftheglobaleconomicslowdown’simpactonsmallerfirmsintheregion,andtheresultingindustryconsolidation.

ProfitabilityinthePeCsectorinAsiadeclinedsignificantlyin2008(seenextsectionformoredetails),hurtingsmallercompaniesinparticular.Largercompanies,whowereflushwithcashandhadgreater

8Ameasureofthesizeofcompanies in relation to the industry,andanindicatoroftheamountofcompetitionamongthem,theHHIisdefinedasthesumofthesquaresofthemarketsharesofthe50largestfirmsfromtheuniverseofover200listedcompaniesassessed.FormoreinformationontheBarometermethodology,pleaserefertothelastsectioninthisreport.

© The Economist Intelligence Unit Limited 2012 9

Asia Competition Barometer:Petrochemicals and chemicals

Figure 2: Herfindahl–Hirschman Index

7.0

7.5

8.0

8.5

9.0

200920082007200620052004

Source: Economist Intelligence Unit

2004 2005 2006 2007 2008 2009

Herfindahl—Hirschman Index (HHI) 8.27 7.90 7.65 7.52 7.54 8.48

flexibilitytoadjustproduction,werebetterabletoweatherthestorm.From2008to2009,thenumberofpublicly-listedPeCcompaniesinAsiaactuallydeclinedfrom559to549.

MrMukundansaysthatbeforethe2008-09economicslowdown,severalfirmsmadebiginvestmentsbasedonhowtheyexpectedPeCsupplychainstoevolve.“Someofthesebetshavegonewrongduetoinsufficientdata,someduetoinactionandsomesimplybecauseofthewaythemarketsturned,”hesays.TataChemicalsusedthecrisistoexamineitscoststructures.ItdecidedtocloseamanufacturingplantintheNetherlands,andthenacquiredasaltbusinessintheUK.“Companiesthatsharpenedtheirfocusoncashcameoutwithbetterbalancesheets,”saysMrMukundan.Manyfirmswereabletobouncebackfromtherecessionas“alotofthebelt-tighteninghappenedfairlyquickly”.

MrMukundanbelievesthatsegmentsinthePeCsectorarebecomingmorecommoditisedandthe“spacetoaddanintangibleorservicecomponentisgettingshavedquickly”.Withtheexceptionofafewcleaningagents,mostPeCproductsareusedasrawmaterialsforthemanufactureofotherproducts.Asthereislittledifferentiationintheseproducts,economiesofscaleareimportant.

Figure 3: Top ten companies by turnover

Company Country of origin 2004 turnover (US$bn) 2009 turnover (US$bn)

Indian Oil Corporation India 30.02 56.62

RelianceIndustries India 15.14 47.6

ThaiOilPublicCompany Thailand 6.16 9.48

SinopecShanghaiPetrochemical China 5.88 7.21

MangaloreRefineryandPetrochemicals India 0.41 7.07

ShanghaiMaterialTrading China 1.3 6.91

ChennaiPetroleumCorporation India NA 5.6

IRPCPublicCompany Thailand 5.14 5.51

HindustanUnilever India 2.41 4.04

BangchakPetroleum Thailand 2.65 3.61

Note:ThesearethetenbiggestcompaniesbyturnoverthatwereanalysedintheBarometer,whichconsideredonlypubliclylistedfirmsineightcountries:China,India,Indonesia,Malaysia,thePhilippines,Singapore,ThailandandVietnam

© The Economist Intelligence Unit Limited 201210

Asia Competition Barometer:Petrochemicals and chemicals

Whenrevenuegrowthslowedasaresultofthecrisis,thesmallerplayerscouldnotkeeppacewithlargeMNCsandstate-ownedcompanies.Tocompeteintoday’sclimate,MrMukundansayscompaniesneedtofocusonbeingcost-competitiveandtoinvestininnovation.“Bothofthesearequitecriticalandcompaniesthatdobothoratleastoneoftheseareonesthathavetendedtogainmarketshare,”hesays.Thesmallerplayers,headds,havehadatoughtimeandonlyafewofthemhaveadaptedwellenough.Consolidationhasledtothecreationofevenlargerfirmswithmultiplecapabilities.

Thethreelargestcompaniesby2009turnover(seeFigure3)—IndianOilCorporation,RelianceIndustriesandThaiOilPublicCompany—togetheraccountforalmosthalfoftheindustry’scombinedrevenues.

MrHeuseratBASFsaysthatlargerfirmshave“aclearedge”overthecompetitionastheycanbuildontheirexistingglobalresearchanddevelopment(R&D)platforms.Nevertheless,rivalryamongthelargestPeCfirmsremainsextremelystrong,andcompetitionbetweenthemislikelytoincrease.

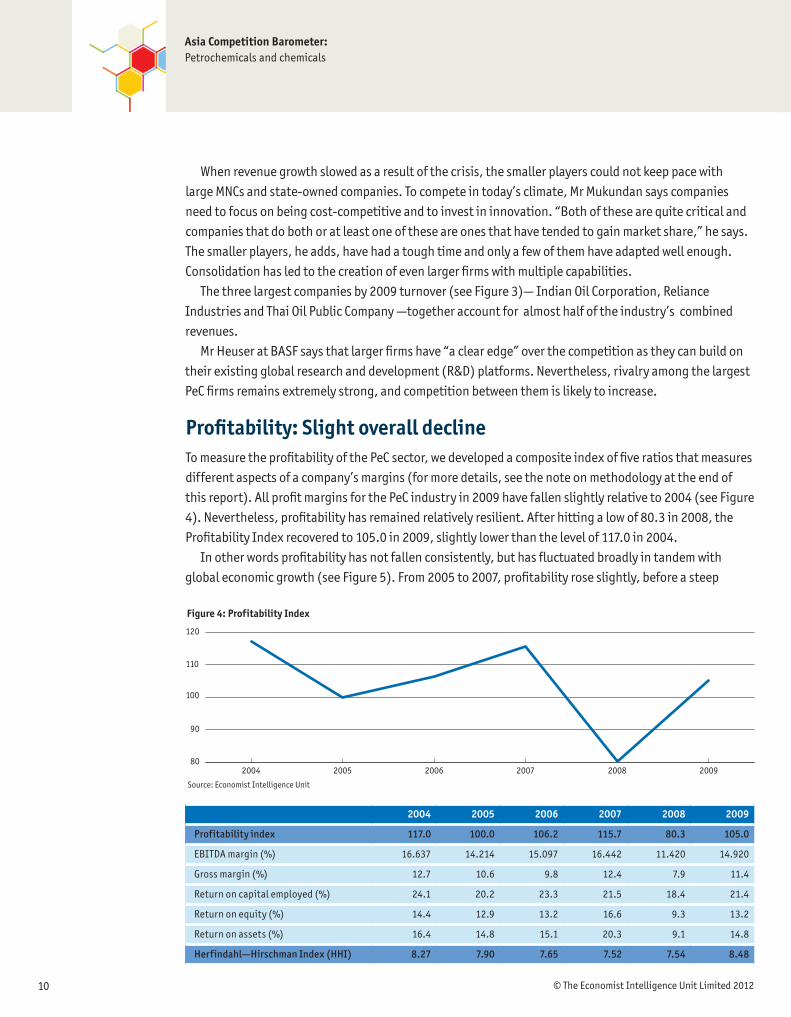

Profitability: Slight overall declineTomeasuretheprofitabilityofthePeCsector,wedevelopedacompositeindexoffiveratiosthatmeasuresdifferentaspectsofacompany’smargins(formoredetails,seethenoteonmethodologyattheendofthisreport).AllprofitmarginsforthePeCindustryin2009havefallenslightlyrelativeto2004(seeFigure4).Nevertheless,profitabilityhasremainedrelativelyresilient.Afterhittingalowof80.3in2008,theProfitabilityIndexrecoveredto105.0in2009,slightlylowerthanthelevelof117.0in2004.

Inotherwordsprofitabilityhasnotfallenconsistently,buthasfluctuatedbroadlyintandemwithglobaleconomicgrowth(seeFigure5).From2005to2007,profitabilityroseslightly,beforeasteep

Figure 4: Profitability Index

80

90

100

110

120

200920082007200620052004

Source: Economist Intelligence Unit

2004 2005 2006 2007 2008 2009

Profitability index 117.0 100.0 106.2 115.7 80.3 105.0

EBITDAmargin(%) 16.637 14.214 15.097 16.442 11.420 14.920

Grossmargin(%) 12.7 10.6 9.8 12.4 7.9 11.4

Returnoncapitalemployed(%) 24.1 20.2 23.3 21.5 18.4 21.4

Returnonequity(%) 14.4 12.9 13.2 16.6 9.3 13.2

Returnonassets(%) 16.4 14.8 15.1 20.3 9.1 14.8

Herfindahl—Hirschman Index (HHI) 8.27 7.90 7.65 7.52 7.54 8.48

© The Economist Intelligence Unit Limited 2012 11

Asia Competition Barometer:Petrochemicals and chemicals

declinebetween2007and2008,adirectreflectionofthegatheringfinancialstormattheendof2007thatdepressedglobaldemand.9Asmuchofthedevelopedworldenteredarecession,exportsofmanufacturedgoodsfromAsiatotheWestcontractedsharply.ThishadadirectimpactonprofitabilityinAsia’sPeCsector.

Rawmaterialcostswerealsoafactorinprofitability.WhileoverallrevenuesofthefirmsintheIndexincreasedin2008,thecostofrawmaterials,suchasoil,naturalgas,water,metalsandminerals,roseevenmore.Asiancompaniessawtheiraveragegrossprofitmarginfallfrom21.5%in2007to18.4%in2008.Thepriceofoilpeakedinmid-2008,theyearprofitabilityfellmost.MrMukundanatTataChemicalssaysthatthepricesofseveralotherinputs,suchasrockphosphate,ureaandammonia,allhitapeakin2008“astraderswereflippingtheseassetsinahurry”.

Profitabilitybouncedbackin2009asemergingAsia’seconomiesbegantogrowrapidlyagain.Asiaex-JapansawrealGDPgrowthof5.2%thatyear.Meanwhile,rawmaterialcostsdeclinedsharply.Finally,industryconsolidationwouldhaveimprovedtheallocationandaverageproductivityofassets,assomesmallerfirmsshut,andsomelargerfirmswereabletogrowtheirmarketshare.

Inthecomingyears,profitabilitywilllargelybedependentoninnovationandtheabilitytotapintomarketsthatarerelativelyunderpenetrated.Mostimportantly,accordingtoMrMukundan,istheneedforcompaniestosecureaccesstolow-costrawmaterialsandenergy.

TheEIUexpectsthepricesofoilandindustrialrawmaterialstomoderateoverthenextfewyears(seeBox:Commodityprices).

9ThecompositeProfitabilityIndexismadeupoffiveratios that each represents adifferentaspectofacompany’sprofitability.FormoreinformationontheBarometermethodology,pleaserefertothelastsectioninthisreport.

Figure 5: Global GDP(% real change p.a.)

-3

-2

-1

0

1

2

3

4

5

2016201520142013201220112010200920082007200620052004

Source: Economist Intelligence Unit

© The Economist Intelligence Unit Limited 201212

Asia Competition Barometer:Petrochemicals and chemicals

Commodity prices

Aftersharpfallsinthefinalquarterof2011,commoditypricesgenerallyhavehadastrongstartto2012,buoyedbydatareleasesshowingmorepositivegrowthtrendsinbothChinaandtheUSandsometentativesignsthattheeurozonedebtmarketswillavoidwidespreaddefaults.Oilprices,inparticular,havebeenstrongowingtosupplyconcernsrelatedtocivilunrestinNigeriaandtensionsbetweenIranandtheWest.Priceswillremainhostagetosentimentsurroundingtheoutcomeoftheeurozonecrisisandglobaleconomicprospectsinearly2012.Amarkeddeteriorationintheoutlookforthe

eurozonecouldbeexpectedtoleadtodramaticfallsincommodityprices,giventhatitwouldmostlikelyhavesevereconsequencesforglobalgrowth.

Onaverage,pricesareexpectedtobeweakerin2012,owingtoslowerconsumptiongrowthand,dependingonthecommodity,someimprovementonthesupplyfront.AstrongerUSdollarwillalsobenegativeforcommodityprices.However,looseglobalmonetaryconditionsandalossofconfidenceinsovereigncreditworthiness,whichisencouraginginvestorstoseekreturnsinrealassets,willoffersomesupporttoprices.Withglobaldemandsettostabilisein2015-16,commoditypricesareexpectedtonudgehigher.

Figure 6: Commodity price forecasts

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

OilpricesBrent;US$/b 72.71 97.66 61.86 79.63 111.01 110.00 103.63 108.25 104.00 110.00

Non-oilcommodities*%changeinUS$prices 20.8 12.2 -22.4 24.0 26.3 -12.2 -1.9 -3.6 3.4 2.8

*IndexincludesBeverages,Grains,Oilseeds,Sugar,Metals,FibresandRubber

Source:TheEconomistIntelligenceUnit,Feb10th2012

Case study: Tata Chemicals

Tata Chemicals: Competing to secure raw materials and energyTataChemicals,oneofIndia’slargestchemicalcompanies,sawits

annualrevenuesquadruplefromUS$674min2004toUS$2.9bnin2008,beforefallingslightlytoUS$2.1bnin2009,duringtheglobaleconomicdownturn.

“WeareveryfortunatethatourhomemarketisAsia,”saysRamakrishnanMukundan,thefirm’smanagingdirector.“Ifyoulookatthepastandtheimmediatefuture,thebulkofprofitgrowthandthebulkofnewsegmentgrowthintermsofproductsarehappeninginAsia.”EventhoughEuropeandNorthAmericacontinuetoleadinafewmanufacturingsegments,suchashigh-endpharmaceuticals,MrMukundanbelievesthatAsiaisclosingthegap,drivenpartlybyrapiddevelopmentsintheregion’sregulatoryframeworks.

MrMukundanbelievesthatcompetitioninthePeCsectorhaschangedwithgreaterconsolidationinthemarket.“Ithasledtothecreationoflargerfirmsthathavemultiplecapabilities,”saysMrMukundan.“Firmswithmarketaccesshavebeenacquiringormerging

withfirmsthathaveaccesstolowercostsintheformofcheaperenergyoraccesstorawmaterials.”Assuch,PeCfirmsarelookingtopartnerwithothercompaniesthathavecomplementaryskillsorcompetitiveadvantages.

Overthenextfewyears,MrMukundanexpectsPeCfirmstocompeteacrossthreedimensions.“Thefirstisalargefocusonsustainability.Thesecondissueisinnovation.Thethirdishowcompaniescanimplementthefirsttwoinordertoharnesswhatisreferredtoasthemarketatthebottomofthepyramid,”hesays,referringtoemergingmarketsinAsia,LatinAmericaandAfrica.Inthisregard,Asiancompanieshaveanadvantageas“theyhaveatouchandfeel”ofthismarket.MrMukundanbelievesthesethreefactorswillbethekeydriversofprofitability.

However,MrMukundanstressesthatunderlyingthethreedimensionsofcompetitiveness—innovation,sustainabilityanduntappedmarkets—ispreferentialaccesstoenergyandfeedstock.“Firmshavetoreachoutandgetthatadvantage,”hesays,pointingoutthattheseinputcostarbitrageopportunitieshavegrownoverthelastfewyears.

© The Economist Intelligence Unit Limited 2012 13

Asia Competition Barometer:Petrochemicals and chemicals

Positioning for success in Asia

Asia remains vital both as a market and as a production source

Giventhelong-termstructuralproblemsinmanyWesternmarketsandemergingAsia’slargelybullisheconomicfundamentals,theshiftintradeandinvestmentfromtheWesttoAsiawillcontinue.The

EIUestimatesthatby2016theeightAsiancountriesinthisstudyalonewillaccountfor28.9%ofglobalGDP(measuredinpurchasing-powerparityterms),upfrom23.2%in2010.

Growingregionaldemandforarangeofproducts,fromautomobilestohouses,willdriveAsia’sPeCsector.Itisexpectedtogrowatacompoundannualgrowthrateof10.5%between2010and2015,bywhenitwillbeworthsomeUS$2.6trn,accordingtoDatamonitor,aresearchfirm.China’smarketalonewillaccountforaboutUS$1.4bn.

GlobalPeCfirmsareincreasinglyviewingAsianotonlyasakeymarketbutalsoavitalsourceofproduction.BASFestimatesthatemergingmarketswillberesponsiblefor54%ofglobalchemicalproduction(excludingpharmaceuticals)by2015andalmost60%by2020,withChinaaloneaccountingfor30%ofglobalproductioninthatyear(seeFigure7).

ThekeyquestionforforeignplayersishowtheywillpositionthemselvesinAsianmarketstotakeadvantageofthisglobalshiftinthechemicalindustry.ThereareanumberoflargeAsianlocalcompaniesalreadyactiveinthisspace;severalofthem,suchasOilandNaturalGasCorporation(ONGC)andIndianOilCorporationinIndia,PetronasinMalaysia,andChinaPetroleumandPetrochemicalCorporation(Sinopec),ChinaNationalOilOffshoreCorporation(CNOOC)and

Figure 7: Global chemical production (excluding pharma)(Trillion $, real 2005)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2020201520101995

Thereof China

Emerging marketsDeveloped markets*World

~1.3

~2.1

~3.1

~3.2% p.a.

~4.0% p.a.

* BASF definition: Developed markets include EU15, Norway, Switzerland, North Amercia, Japan, Australia, New Zealand.

Source: BASF

~40% ~45%

~1.4~1.2

1.01.10.9

0.4 ~60%

~1.8

© The Economist Intelligence Unit Limited 201214

Asia Competition Barometer:Petrochemicals and chemicals

PetroChina,arestate-ownedenterprises.Theirlocalknowledgeandclosegovernmenttiesofferthemanadvantageagainstforeigncompetition.

ChinesePeCfirms,forinstance,havebeenabletosecuresuppliesofcrudeinplacessuchasAfricalargelybecauseoftheirgovernment’sfinancialandpoliticalbacking.Similarly,PetronasenjoysavirtualmonopolyinMalaysia.IthastherightstoallofMalaysia’shydrocarbonreserves.

Facedwiththesechallenges,privatesectorPeCfirmshaveforyearsbeenenteringintopartnershipswiththesestate-backedincumbents,offeringthemskillsandtechnologyinreturnforaccesstorawmaterials.Ashydrocarbonreservesdwindle,andastheseprivatesectorfirmsfindithardertosecuretherawmaterialstheyneed,thesepartnershipsarelikelytogrowinnumberandscope.

Evolving supply chains and partnershipsThescrambleforaccesstorawmaterialsandenergyisalreadyhavinganimpactonsupplychains.Thesespecificinputpricedifferentialsfaroutweighanyadditionallabourcosts.Forinstance,MiddleEasterncompaniesproducingfertilisernowhaveacrucialcompetitiveadvantagebecauseoftheiraccesstocheapnaturalgasintheregion.

Moreover,itisnolongeramatterofAsianstate-ownedenterprisesteamingwithlargelyWesternMNCs.Asiancompaniesarelookingoutsidetheregion.

TataChemicals,whichhasmanufacturingfacilitiesinAsia,Europe,NorthAmericaandAfrica,hasitslargestproductioncentreintheUS—energycoststherearerelativelylow,andthecountryhastheworld’slargestdepositsoftrona,whichisusedintheproductionofsodaash.

Logisticsarealsoevidentlymoreimportantthanlowcosts.InAsia,globalfirmsareestablishingkeyproductionsitesnotonlyclosetofeedstocksources,butalsoatlocationswhichprovidegoodaccessandconnectivitytorawmaterialsanddestinationmarkets.Forexample,ExxonMobil,anAmericanoilandgasfirm,willthisyearcompletetheconstructionofitslargestintegratedchemicalandrefiningsiteinSingapore.Similarly,Lanxess,aGermanchemicalscompany,recentlymoveditsbutylrubberglobalheadquartersfromSwitzerlandtoSingapore.

Thisraceforaccesstorawmaterialsandenergypartlyexplainstheincreasingnumberofpartnershipsinvolvingstate-ownedPeCfirms.OneofthelargestprojectsisRoyalDutchShell’sUS$4.3bnintegratedrefineryandpetrochemicalsjointventurewithCNOOCinGuangdongthatwassetupinApril2006.10 AnotherisBASF’sNanjing-basedUS$2.9bnjointventurewithSinopecthatbeganoperationsin2005.BASFalsohasajointventurewithPetronasinKuantan,Malaysia.ThesetwofacilitiesareBASF’slargestproductionsitesinAsia.

Similarly,inNovember2011,nationally-ownedKuwaitPetroleumCorporationandChina’sSinopecstartedbuildinganRMB59bn(US$9.3bn)jointrefiningandpetrochemicalcomplexinGuangdong.11 The projectincludesarefineryandaone-milliontonneayearethylenecrackingunitandisexpectedtocomeonstreamin2015.ThistypifiesthekindofpartnershipMrMukundanspeaksof:KuwaitneedsasteadyoutletforitsoilandSinopecneedsareliablesupplyofoilinordertomanufacturepetrochemicalstomeetChina’sgrowingdemand.

10“ChemicalsinChina:Thenextdecade”,KPMG,Sep1st2006.

11“Sinopec,KPCstartbuilding$9.3blnpetrochemproject”,Reuters,Nov17th2011.

© The Economist Intelligence Unit Limited 2012 15

Asia Competition Barometer:Petrochemicals and chemicals

Case study: BASF

BASF: Deepening its presence in AsiaAtBASF,theworld’slargestchemicalproducerbyturnover,Asia

revenuesreached€12.5bn(US$16.3bn)in2010,orabout21%ofthecompany’sglobalsales.AlbertHeuser,thefirm’spresidentofmarketandbusinessdevelopmentinAsiaPacific,saysthatinthefirstthreequartersof2011,BASF’ssalesincreasedacrossallsegmentsofitsbusinessinAsiaPacific.Chinaaloneaccountedforsalesof€5.8bn(US$7.5bn)in2010,makingitthethirdlargestmarketforBASFglobally,afterGermanyandtheUS.

“Wetargetregionalgrowthofaround8%perannuminAsiaPacificbetween2010and2020,”MrHeusersays.By2020,BASFexpectsAsiatoaccountfor25%ofitsglobalsales.Asiaisincreasinglyimportantnotmerelyasamarket,butalsoforproduction—BASFforecaststhatemergingmarketswillcontributeabout60%oftotalglobalchemicalproductionby2020.

MrHeusersaysthatBASFisstrivingtodevelopitsportfoliotowards“moremarketdrivenandinnovativebusinesses”.Forinstance,overthepastseveralyears,thecompanyhasmadeacquisitionsthatbuilditscapacitiesinengineeringplastics,electronicchemicals,catalysts,water-basedcoatings,pigmentsandplasticadditives.Thecompanyhassimultaneouslydivestedbusinessesinpharmaceuticals,fibres,printingsystems,polyolefins,agrogenericsandvitaminspremix.

HeaddsthatacrossAsia,theadoptionofnewtechnologiesisessential.Forinstance,thecompanyrecentlycompletedthesecond

phaseofits“highly-integrated,highlyenergy-efficient”productioncomplexinNanjingwhichservesmultipleindustriessuchasagriculture,construction,electronics,pharmaceutical,automotiveandchemicalmanufacturing.Furthermore,BASF’sconstructionchemicalsdivisionismovingtostrengthenitsfocuson“thirdgenerationtechnology”fortheconcreteadmixturemarketinChina.

“Atthesametimewearelookingfornewwaystotakeadvantageofthedevelopmentoftheregionfromanoperationalstandpoint,”MrHeusersays.BASFhassetupanengineeringandtechnicalprocurementofficeinShanghai,whichrepresentsanimportantpartofthefirm’sglobalengineeringandprocurementnetwork.TheofficeprovidesprojectmanagementandexecutionservicesforprojectsinAsia,andengineeringandtechnicalprocurementservicesfornon-Asianprojects.

Thereisaneedtoensurecoststructuresarecompetitive,saysMrHeuser,andBASFisdoingthisthroughefficiencymeasuressuchasfixedcostsavings,capacityincreasesandbettersourcing.“TheintensityofcompetitionhasincreasedintheAsiaPacificregion,withnewcapacitycomingonstreamfrommultinationalcompanies,state-ownedandprivatecompaniesthroughouttheregion,”saysMrHeuser.“Localcompetitorsareimprovingtheircapabilities,butthisvarieswidelyfromproducttoproduct.”

Inordertomaintainitsprofitabilityoverthenextfewyears,MrHeuserwantsBASFtomovedownstreamtowardscustomerindustriessothatby2020theshareofitssalesofclassicalchemicalswillbecloserto30%,whilecustomisedproducts,functionalisedmaterialsandsolutionswillreacharound70%.

© The Economist Intelligence Unit Limited 201216

Asia Competition Barometer:Petrochemicals and chemicals

Outlook

ThePeCmarketinAsiahasgrownsteadilyoverthepastfewyears.Giventheregion’sbullishlong-termgrowthoutlook,thistrendlookslikelytocontinue.Inparticular,demandfromtheconsumergoods,

agriculture,automotiveandconstructionsectorswilldrivetheregion’sPeCsector.Meanwhile,theincreasingglobalandregionalemphasisonsustainabledevelopmentandalternativeenergysourceswillcreatenewpotentialmarketsforPeCfirms.Moreover,AsiahasalsobecomeanimportantregionforPeCproduction.

Fortheindustryasawhole,afterasharpdipinprofitabilityin2008—duetoaslowdownindemandamidtheglobaleconomicdownturncrisis,coupledwithhigherinputcosts—marginshaverisentoneartheirsix-yearpeak.Inparticular,bigcompanieshavebeenabletoexploiteconomiesofscaleandgrowrapidly,bothorganicallyandthroughmergersandacquisitions.Withongoingconsolidationintheindustry,itseemslikelythatthebiggerfirms,withadequateresourcestoinvestinR&D,willcontinuetogrowtheirmarketshare.

MrHeuseratBASFsayscompetitioninAsiawillcontinuetoincreaseasallregionalplayersviewtheregion—andespeciallyChina—asakeymarket,“meaningthatmanagementattentionishighandresourcesaremadeavailable”.However,hebelievesthatbecausePeCsectorcompetitivenessiscloselytiedtotherateandqualityofinnovation,internationalcompaniesenjoythebenefitsofaglobalresearchanddevelopmentnetwork.Accordingtohim,suchfirmshaveadistinctadvantageiftheycantailorthebenefitsofsuchaninternationalnetworktotheneedsoflocalcustomers.Inrecognitionofthis,BASFisinvestingheavilyinR&DinAsia,includingsubstantiallyincreasingitsR&Dheadcount.

PerhapsthegreatestimperativeforPeCfirmsoverthenextfewyearsistheneedtosecureaccesstolow-costrawmaterialsandenergy.Asaresult,thesectorisseeinganincreasingnumberofpartnershipsbetweenMNCswithglobalnetworksandtechnologicalknow-how,andlocalplayers,includingstate-ownedfirms,withaccesstoresources—anothertrendthatwillfavourlargercompanies.

Withenergyandfeedstockpricearbitragelikelytodetermineprofitabilityandcompetitiveness,companiesofallnationalitieswillbeforcedtoexpandintonewmarkets.AccordingtoMrMukundan,“Allofushavetorealignourselves.”GlobalPeCfirmsthatareabletoadapttotheseevolvingindustrytrendswillbebestplacedtoboosttop-andbottom-linegrowth.

© The Economist Intelligence Unit Limited 2012 17

Asia Competition Barometer:Petrochemicals and chemicals

Barometer methodology

Toassesstheintensityofcompetitionandunderstandthechangingmarketdynamicsinkeysectors,theEconomistIntelligenceUnithasdevelopedtheAsiaCompetitionBarometer.Drawinguponcompany-

leveldataonprofitabilityandotherindicators,theBarometerquantifiesthechangingdynamicsofcompetitivenessinAsiaforselectindustriesbetween2004and2009.

Assessingauniverseofover550publicly-listedpetrochemicalandchemicalcompaniesacrosseightcountries—China,India,Indonesia,Malaysia,thePhilippines,Singapore,ThailandandVietnam—theBarometerexamineschangingprofitabilityandthecompetitionlandscapefortheT&Lsector.

How do we define the petrochemicals and chemicals manufacturing sector? Thepetrochemicalsandchemicalsmanufacturing(PeC)sectorincludesthefollowingsub-segments:

basicchemicals,fertilisersandnitrogencompounds,plasticsandsyntheticrubberinprimaryforms,pesticidesandotheragrochemicalproducts,paints,varnishesandsimilarcoatings,printinginkandmastics,soapanddetergents,cleaningandpolishingpreparations,perfumesandtoiletpreparations,explosives,otherchemicalproductsandman-madefibres.

Methodology TheBarometerhastwodimensions:profitabilityandmarketconcentration.

Profitability IndexToassesstheaggregateprofitabilityofthePeCmanufacturingsectorinAsia,theEconomistIntelligenceUnitdevelopedacompositeindexoffiveratiosthateachrepresentadifferentaspectofacompany’sprofitability:

• EBITDA margin (%):Ameasureofacompany’soperatingprofitability.Itisequaltoearningsbeforeinterest,tax,depreciationandamortisation(EBITDA)dividedbytotalrevenue.BecauseEBITDAexcludesdepreciationandamortisation,EBITDAmarginprovidesaclearerviewofacompany’scoreprofitability.Anincreaseincompetitionmayputpressureonanindustry’sprofitmargins.

© The Economist Intelligence Unit Limited 201218

Asia Competition Barometer:Petrochemicals and chemicals

• Gross margin (%):Whenusedasamarketmeasureofcompetition,grossmarginmeasurestheprofitabilityconsideringonlythecostsofgoodssold.Thehigherthepercentage,themorethecompanyretainsoneachdollarofsalestoserviceitsothercostsandobligations.Anincreaseincompetitiontendstoreducefirms’abilitytoincreasepricesandtherebyincreaseitsgrossmargin.

• Return on capital employed (%):Ameasureoftheefficiencyandprofitabilityofacompany’scapitalinvestments.Returnoncapitalemployedalsoindicateswhetherthecompanyisearningsufficientrevenuesandprofitsinordertomakethebestuseofitscapitalassets.Anincreaseincompetitionmayrequirefirmstoemployadditionalcapitaltomaintainprofitability.

• Return on equity (%):Ameasureoftherateofreturnontheshareholders’equity.Itmeasuresafirm’sefficiencyatgeneratingprofitsfromeveryunitofshareholders’equity.Returnonequityshowshowwellacompanyusesshareholderfundstogenerateearningsgrowth.Ariseincompetitiontendstoputpressureonreturnsonshareholderfunds.

• Return on assets (%):Ameasureofhowprofitableacompany’sassetsareingeneratingrevenue,orhowprofitableacompanyisrelativetoitsassets.Returnonassetsdeterminesacompany’sabilitytoutiliseitsassetsefficientlyandeffectively.Highercompetitiontendstoputpressureonfirms’abilitytomaintainreturnonassets.

Weaggregatedcompany-leveldataforover550publicly-quotedPeCcompaniesandexaminedtheirprofitabilityratios.Toenableobservationoftrendsovertime,acompositeProfitabilityIndexwasdeveloped(whereyear2005=100).EBITDAandgrossmarginaregivenahigherweightingintheindexastheyspeakdirectlytobottomlineprofitability,whilethereturnoncapitalemployed,returnonequityandreturnonassetsratiosspeaktohowacompanymakeuseofitsvariousresourcestodrivereturn(i.eefficiency/productivity).

Profitability indicator Weight in Profitability Index

EBITDAmargin(%) 35%

Grossmargin(%) 35%

Returnoncapitalemployed(%) 10%

Returnonequity(%) 10%

Returnonassets(%) 10%

Market concentration Toassessmarketconcentration,theEconomistIntelligenceUnitcalculatedtheHerfindahl-HirschmannIndex(HHI)forthePeCsectorinAsiafrom2004to2009.Ameasureofthesizeofcompaniesinrelationtotheindustry,andanindicatoroftheamountofcompetitionamongthem,theHHIisdefinedasthesumofthesquaresofthemarketsharesofthe50largestfirmsfromtheuniverseofover550listedcompaniesassessed.12HHIvaluescanrangefrom0to1.0,movingfromanextremelyfragmentedmarket(0)toamonopoly(1).HHIvalueshavebeenmultipliedby100toachieveascaleconsistentwithprofitabilityindicators.ArisingHHIindexgenerallyindicatesfallingmarketcompetition,whileafallintheHHIsuggeststhatcompetitionisincreasing.

12Orsummedforallthefirmsin the case that there are fewerthan50.

Whilst every effort has been taken to verify the accuracy of this information, neither The Economist Intelligence Unit Ltd. nor the sponsor of this report can accept any responsibility or liability for reliance by any person on this report or any of the information, opinions or conclusions set out herein.