application creep, grush, transport futures 20150917

TRANSCRIPT

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015 1

Bern Grush | John Niles | endofdriving.org

Environmentally Sustainable Deployment of Autonomous Vehicles

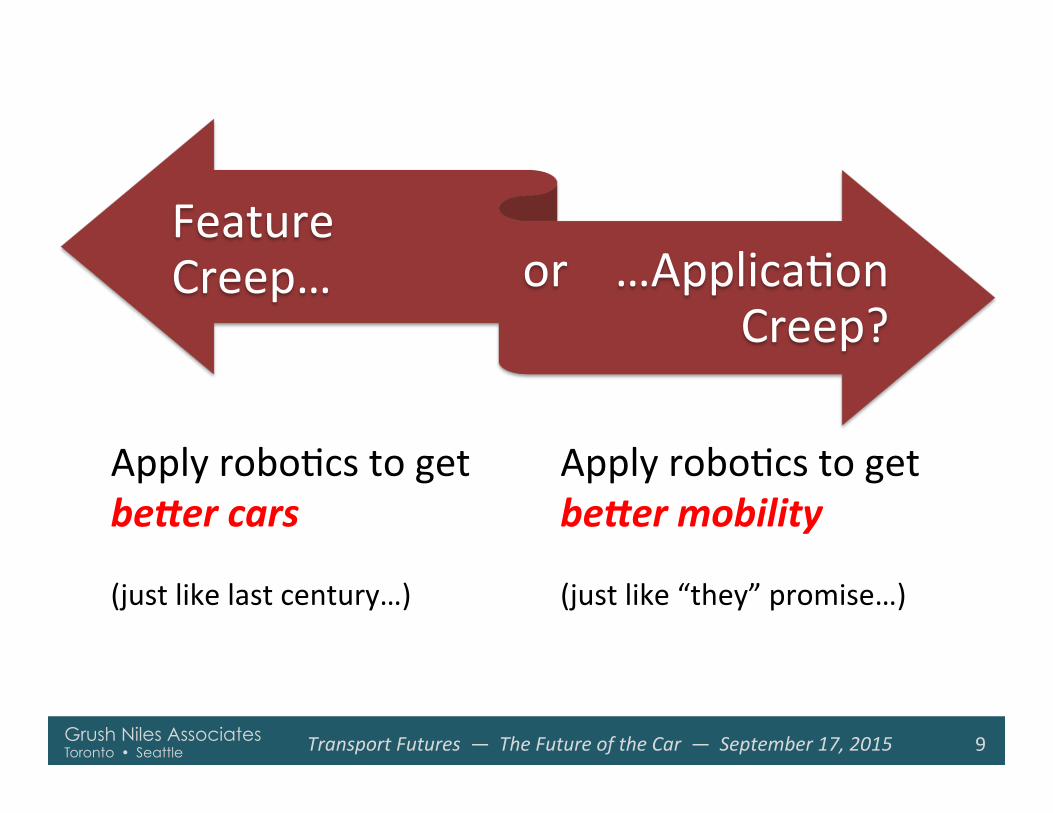

Feature Creep… or …ApplicaEon Creep?

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

Policy Technology

Society

Planning & Deployment

Infrastructure Environment Urban livability Human health

Climate footprint

CriEcal links…

2

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

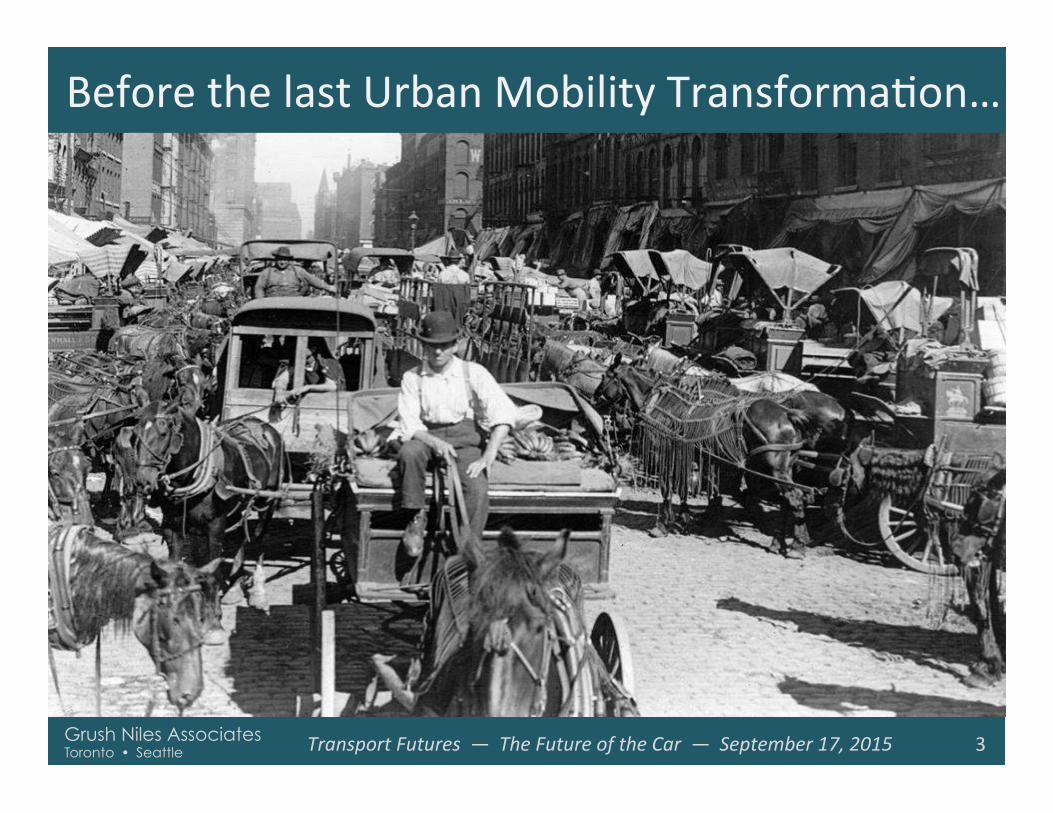

Before the last Urban Mobility TransformaEon…

3

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

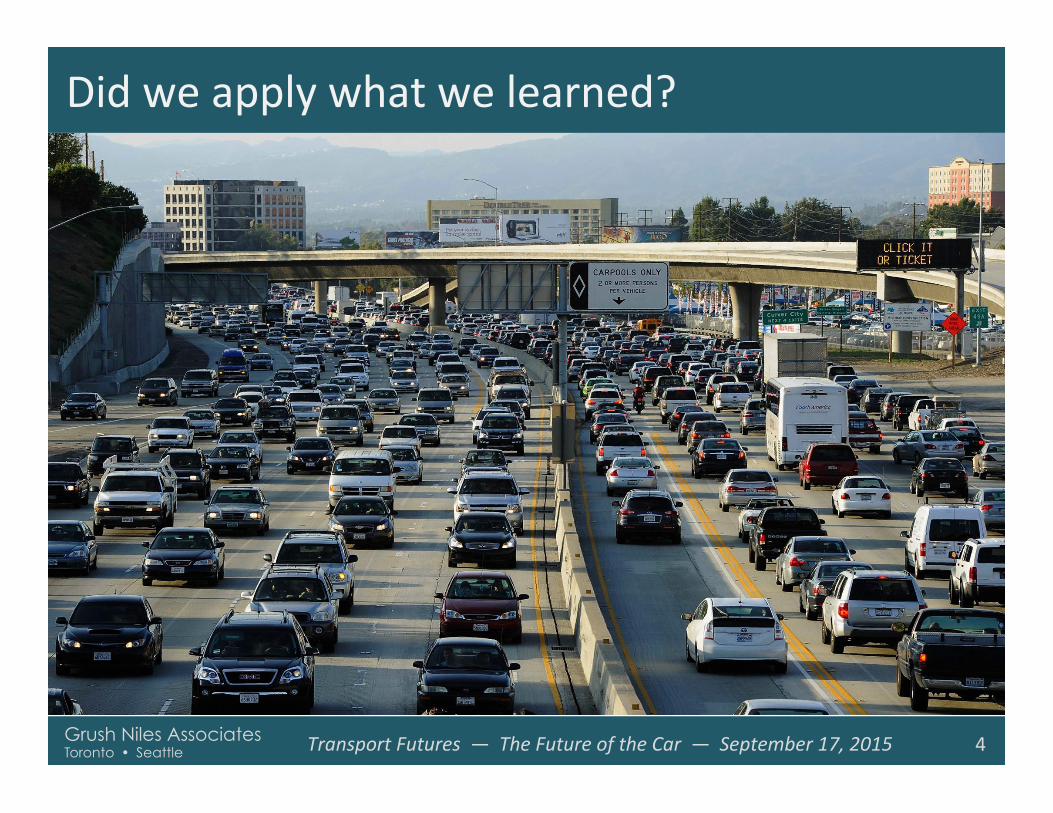

Did we apply what we learned?

4

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015 5

2010 One billion

motor vehicles

2050 Four billion

motor vehicles MANY COSTS • Vehicle Kilometers Traveled • Vehicles • Energy consumpEon • Carbon • Parking • Roads • FataliEes, injuries

KEY BENEFIT • Mobility

(Passenger Kilometers Traveled -‐ PKT)

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

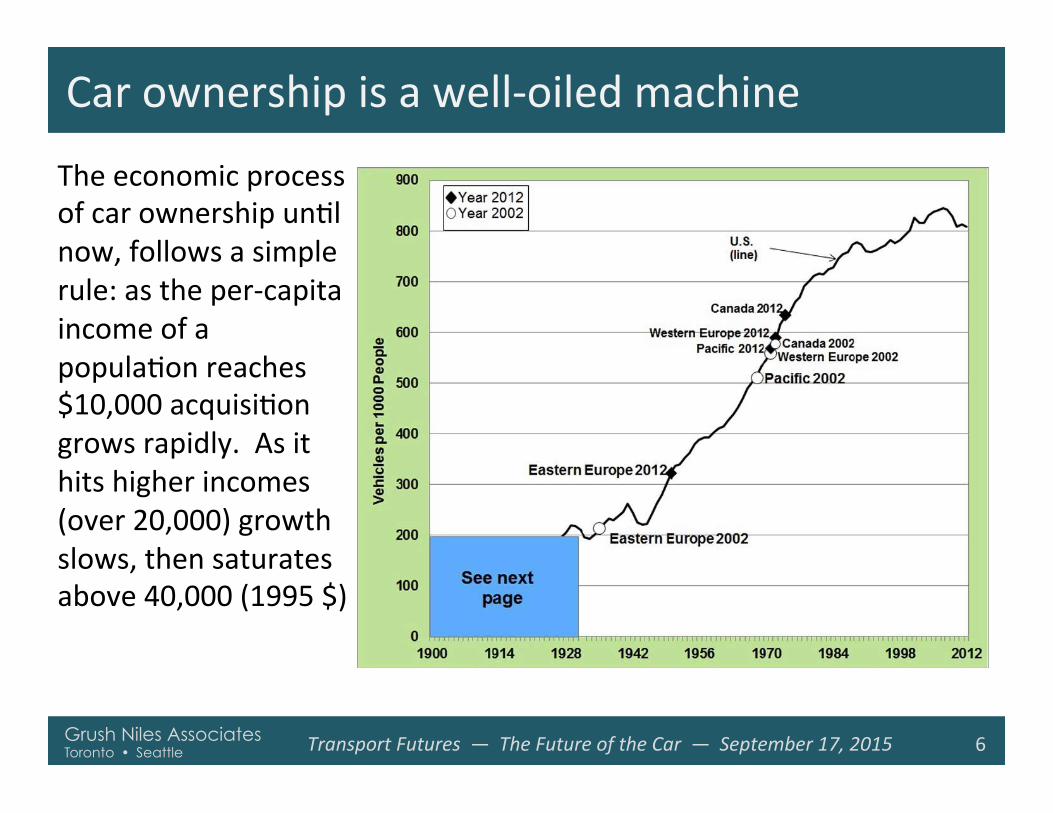

Car ownership is a well-‐oiled machine

6

The economic process of car ownership unEl now, follows a simple rule: as the per-‐capita income of a populaEon reaches $10,000 acquisiEon grows rapidly. As it hits higher incomes (over 20,000) growth slows, then saturates above 40,000 (1995 $)

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

Car ownership is a well-‐oiled machine

7

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

Middle-‐class-‐centric opEmism From Wikipedia…

• [A new beginning…] – Full AV prototype here – Available 2020 – Reduce world vehicles count to Eny fracEon

– Children chauffeured – No more DUI – Lives saved

• No one keeps their car • Tap a smart phone and a perfect* ride shows up:

– robo-‐taxi – robo-‐bus – robo-‐limo – robo-‐Segway

8

…roboAc UberizaAon of transit

* Tailoring

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015 9

Feature Creep… or …ApplicaEon

Creep?

Apply roboEcs to get be#er cars (just like last century…)

Apply roboEcs to get be#er mobility (just like “they” promise…)

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

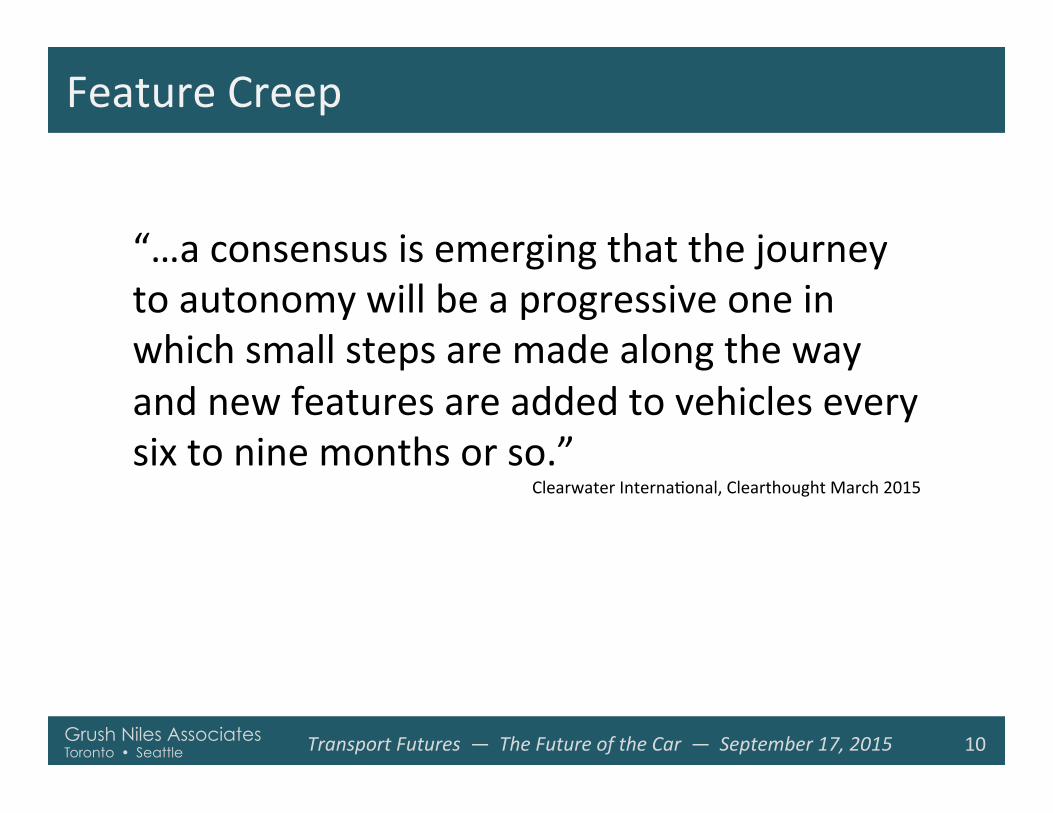

“…a consensus is emerging that the journey to autonomy will be a progressive one in which small steps are made along the way and new features are added to vehicles every six to nine months or so.”

Clearwater InternaEonal, Clearthought March 2015

Feature Creep

10

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

Feature creep: beker cars

• Focus on technology • Incremental improvements • Replace the old fleet with a new fleet • More cars sold è new model lust • More household vehicles • More infrastructure • Increased policy complexity • Insure growth projecEons to 4 billion vehicles • High-‐end trickle-‐down è wealthy consumers subsidize creep • Growing transportaEon inequity • Creep toward SAE level 5 (Body-‐out) è 2050? or later • A long legacy of pre-‐roboEc vehicles on the road

11

20th Century in 21st Century clothing

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

Feature Creep

12

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

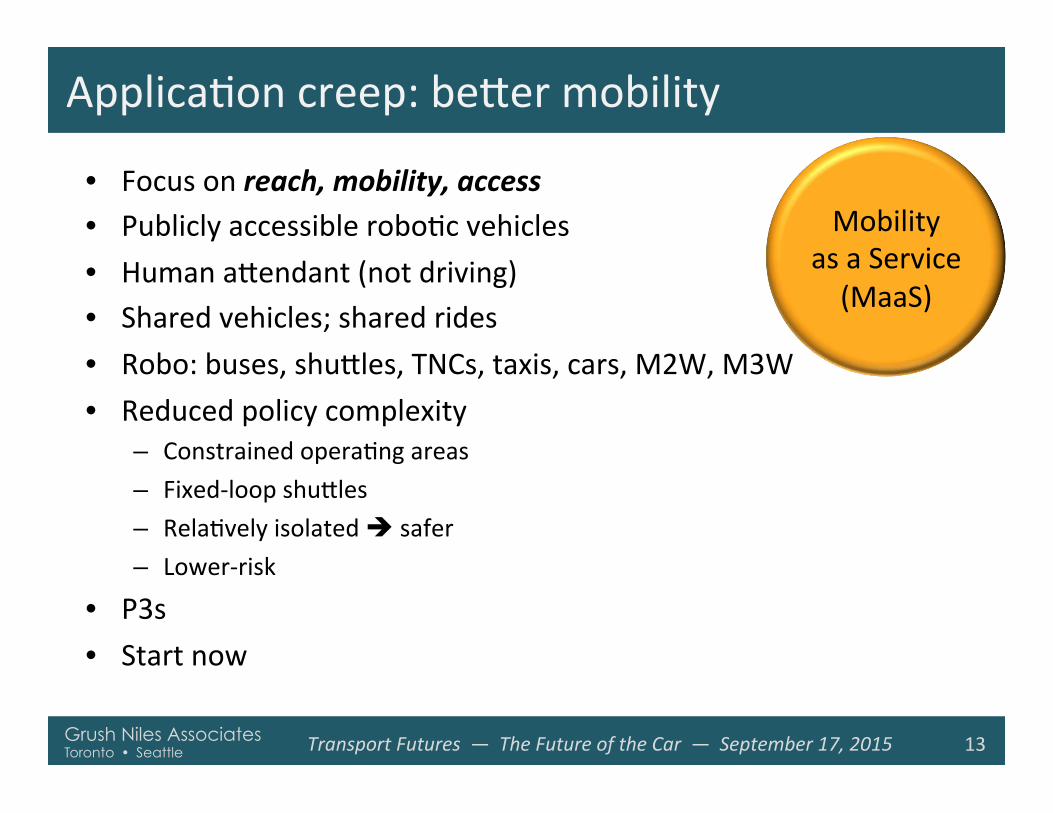

ApplicaEon creep: beker mobility

• Focus on reach, mobility, access • Publicly accessible roboEc vehicles • Human akendant (not driving) • Shared vehicles; shared rides • Robo: buses, shukles, TNCs, taxis, cars, M2W, M3W • Reduced policy complexity

– Constrained operaEng areas – Fixed-‐loop shukles – RelaEvely isolated è safer – Lower-‐risk

• P3s • Start now

13

Mobility as a Service (MaaS)

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

ApplicaEon Creep: EU

14

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

ApplicaEon Creep: Canada

15

Driverless Electric Shu>le Buses to be Studied for Use at Zibi September 1, 2015 Okawa, Ontario, Canada – Windmill Developments and the Canadian Automated Vehicles Centre of Excellence (CAVCOE) have teamed up to conduct a feasibility and planning study for the demonstraEon, trial and deployment of fully-‐automated, electric shukle-‐buses at Zibi.

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

Creep Levels

Feature Creep Levels of AUTOMATION*

1. Driver Assistance 2. ParEal AutomaEon 3. CondiEonal AutomaEon 4. High AutomaEon 5. Full AutomaEon

– No human drivers

ApplicaHon Creep Levels of REACH*

1. Route 2. Small area 3. Large area 4. Regional 5. NaEonal, InternaEonal

– No human drivers

16

* SAE J3016 * Under development at GNA

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

ApplicaEon Creep DefiniEons: Levels of Reach

17

Lvl Name DefiniHon Tailoring Network/Reach PKT

1 Loop (started)

Vehicles on limited, repeHHve, fixed-‐route, fixed schedule routes of short duraEon, under 30 mins, under 10 km, under 20kph

Likle or none: Vans, minibuses

Shukle: parking, shopping, urban tourist <1%

2

Small Area (2025)

Vehicles operaEng on most/all roadways/routes in a constrained area. Vehicles self-‐opEmize routes depending on combinaEon of schedule performance and user-‐demand responds to individuals calling for service by origin and desEnaEon

Modest: vehicles from 2 to 8 passengers; shukles, taxis, TNCs, minibuses; modest opEmizaEon of vehicle assignment. Start of P3s.

Campus: corporate, university, military, reErement community. First-‐mile and last mile to/from train staEons or transit hubs. Under 50km2

3%

3 Large Area (2035)

Same as Level 2, plus vehicles operaEng on most/all roadways/routes in an urban subarea/district

Full: vehicles from 2 to 30 passengers. At least 3 compeEng fleets; at least 2/3 are P3s.

Borough, suburban or exurban area, CBD, Island. Under 500km2

15%

4 Regional (2045)

As level 3, plus anywhere, any distance, public roads

Full: vehicles from 1 to 100+ passengers; Majority P3s

Megaregion. Under 5000km2 40%

5 NaEonal (2055)

As level 4, plus any mapped private roadways Full; Majority P3s NaEonal, InternaEonal 80%

© Grush Niles, 2015

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

Vehicle PopulaEon

18

Four billion vehicles… or …One billion

vehicles?

Feature creep will encourage worldwide car ownership growth to over 0.4 per capita è Now at 0.12 per capita

ApplicaEon creep enables this to stay at 0.1 per capita. è 80% of PKT in shared vehicles

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

AutomoEve Manufacturing

Feature Creep • More vehicles

– Household use – Less tailoring – Long road life

• High-‐opEon vehicles – Personal/household

sales

• More – Features – Turnover – Resales

ApplicaHon Creep • More vehicles

– Public use – More tailoring – Short road life

• Simpler vehicles – Service/maintenance

opEmizaEon

• More – Wearables – Carryables – Portables

19

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

Parking

20

Parked 95% of Eme… or …Parked 50%

of Eme?

Personal Vehicles Use increasing percentage of urban real-‐estate…

Shared vehicles Shrinking percentage è opportunity to manage differently

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

CongesEon

Feature Creep Bias: owning

• More SOVs • Likle or no tailoring* • Plus-‐sized vehicles

* right-‐sizing of vehicle for purpose

ApplicaHon Creep Bias: sharing

• More HOVs • Enables high tailoring • Reduce vehicle size/weight per PKT

21

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

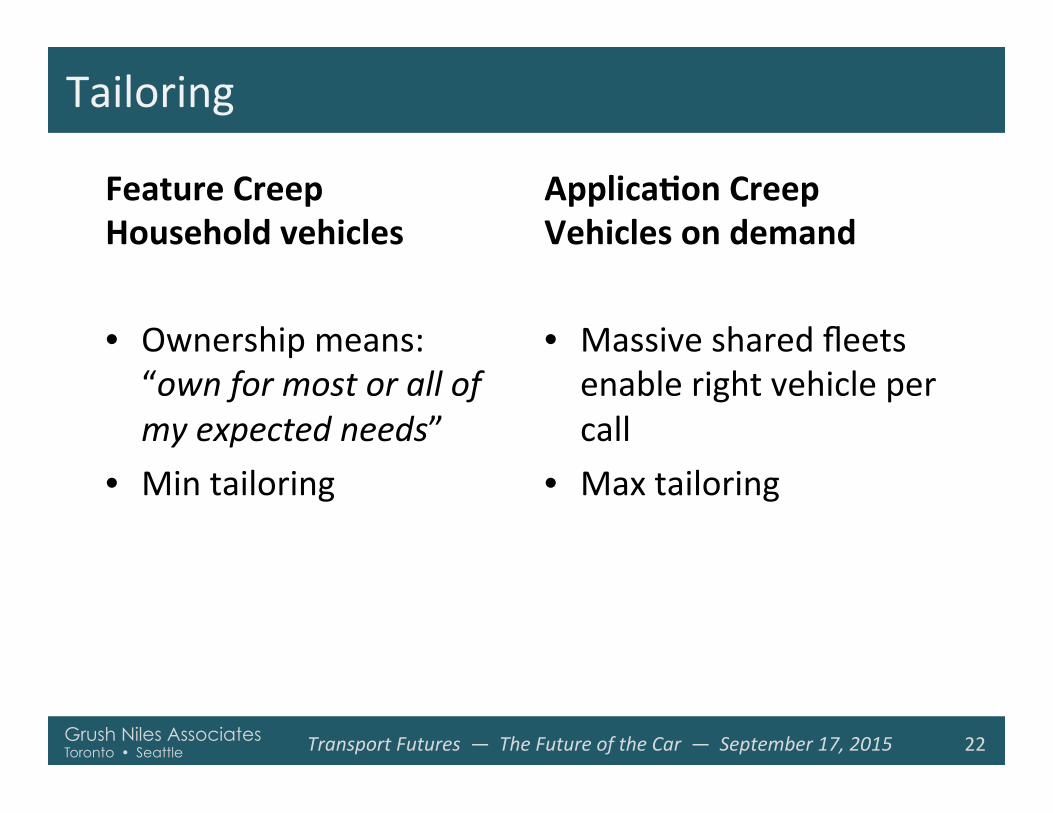

Tailoring

Feature Creep Household vehicles • Ownership means: “own for most or all of my expected needs”

• Min tailoring

ApplicaHon Creep Vehicles on demand

• Massive shared fleets enable right vehicle per call

• Max tailoring

22

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

Energy

• OpEmizing managed fleets provide greater opportuniEes/incenEves to control: – Energy type – Energy waste – Energy distribuEon/storage

23

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

Accident risk

Feature Creep

• Mixed driver-‐in/driver-‐out, 2020-‐2050

• Mixing L2, L3, L4, L4.5 means higher risks for distracted driving!

ApplicaHon Creep

• IsolaEon of driver-‐in/driver-‐out reduces risk

• Removes distracEon circumstances

24

“AlerAng a driver to retake control during an emergency [is] one of the biggest safety challenges for manufacturers of parAally automated cars, industry officials and scienAsts said.”

hXp://www.scmp.com/news/arAcle/1855591/race-‐automaAon-‐google-‐and-‐carmakers-‐take-‐different-‐roads-‐pursuing-‐self-‐drive

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

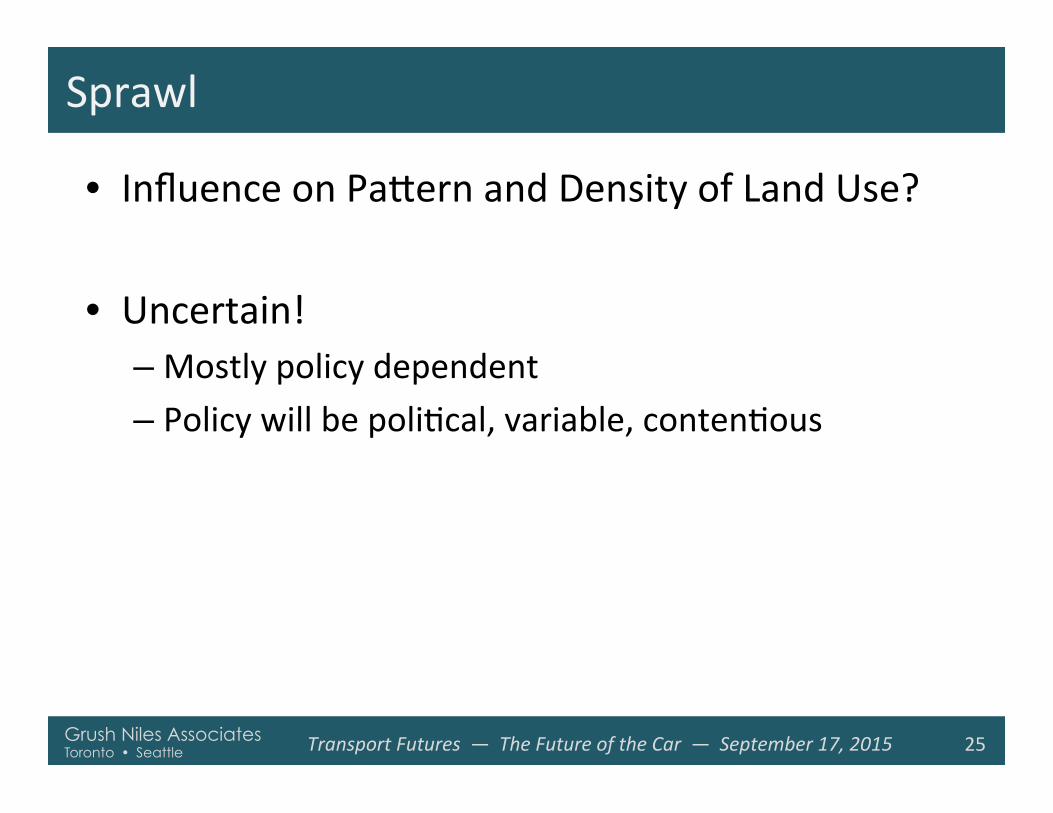

Sprawl

• Influence on Pakern and Density of Land Use?

• Uncertain! – Mostly policy dependent – Policy will be poliEcal, variable, contenEous

25

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

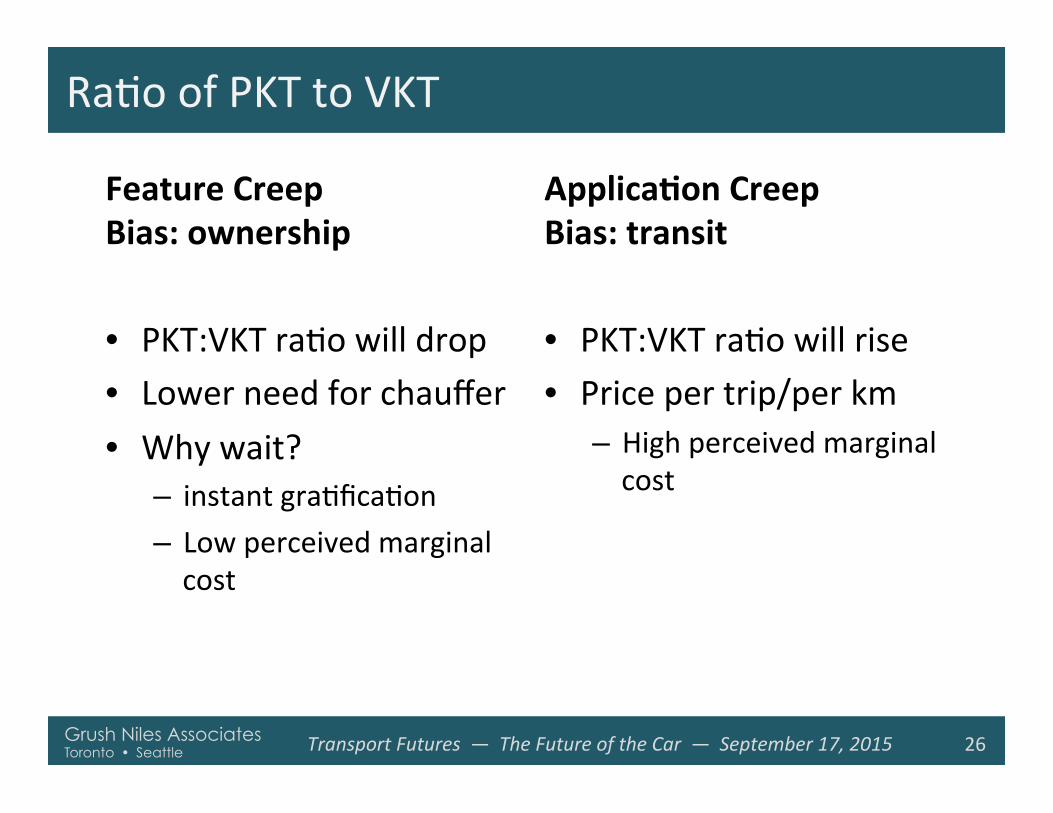

RaEo of PKT to VKT

Feature Creep Bias: ownership

• PKT:VKT raEo will drop • Lower need for chauffer • Why wait?

– instant graEficaEon – Low perceived marginal cost

ApplicaHon Creep Bias: transit

• PKT:VKT raEo will rise • Price per trip/per km

– High perceived marginal cost

26

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

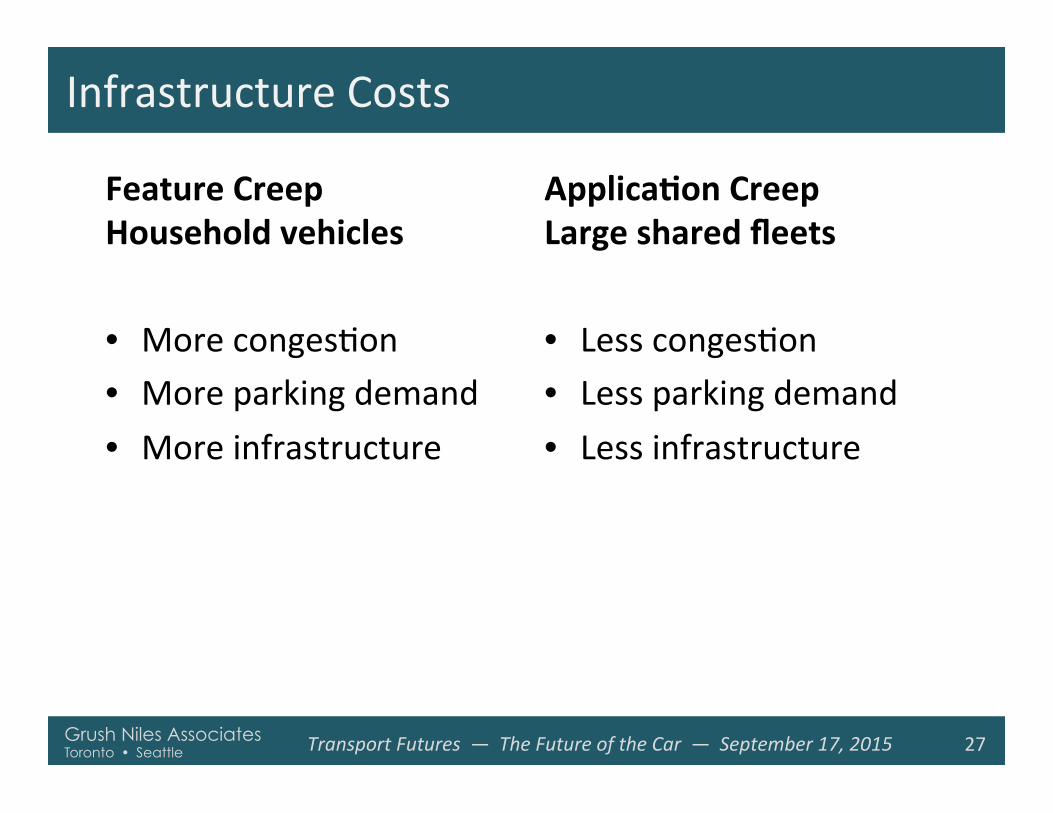

Infrastructure Costs

Feature Creep Household vehicles

• More congesEon • More parking demand • More infrastructure

ApplicaHon Creep Large shared fleets

• Less congesEon • Less parking demand • Less infrastructure

27

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

Transit jobs

Feature Creep Bias: ownership

• Reduce transit demand • Now 5 – 8% of PKT • Job loss

ApplicaHon Creep Bias: shared fleets

• Increase transit demand • Target 50 -‐ 80% of PKT • Job gains

28

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

Transit Subsidy

Feature Creep Bias: ownership

• Lower transit use • High cost per shared transit PKT

ApplicaHon Creep Bias: shared fleets

• Massive tailored fleets • High farebox recovery • Enable P3 involvement

29

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

TransportaEon equity

Feature Creep Bias: ownership

• Private vehicles are a high expense for lower income families

• Dominant ownership ensures lower equity for non-‐owners

ApplicaHon Creep Bias: transit

• Lower income families depend more owen on transit

• Shared transit fleets enables greater equity

30

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

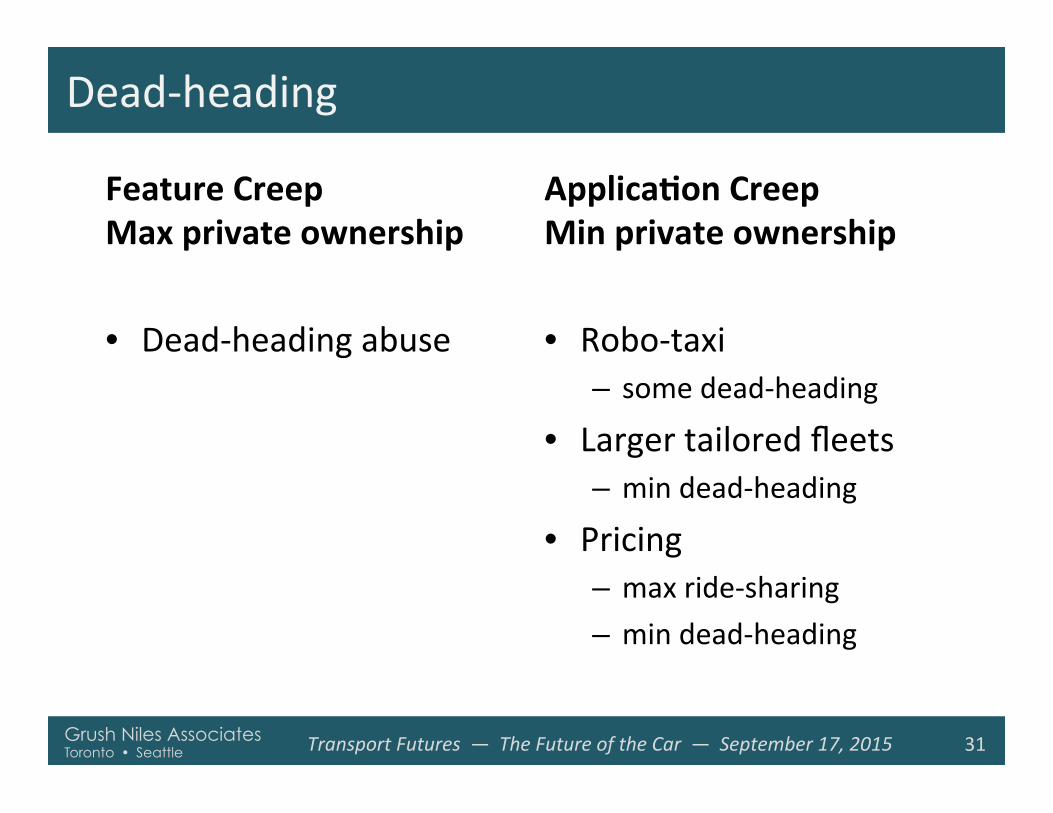

Dead-‐heading

Feature Creep Max private ownership

• Dead-‐heading abuse

ApplicaHon Creep Min private ownership

• Robo-‐taxi – some dead-‐heading

• Larger tailored fleets – min dead-‐heading

• Pricing – max ride-‐sharing – min dead-‐heading

31

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

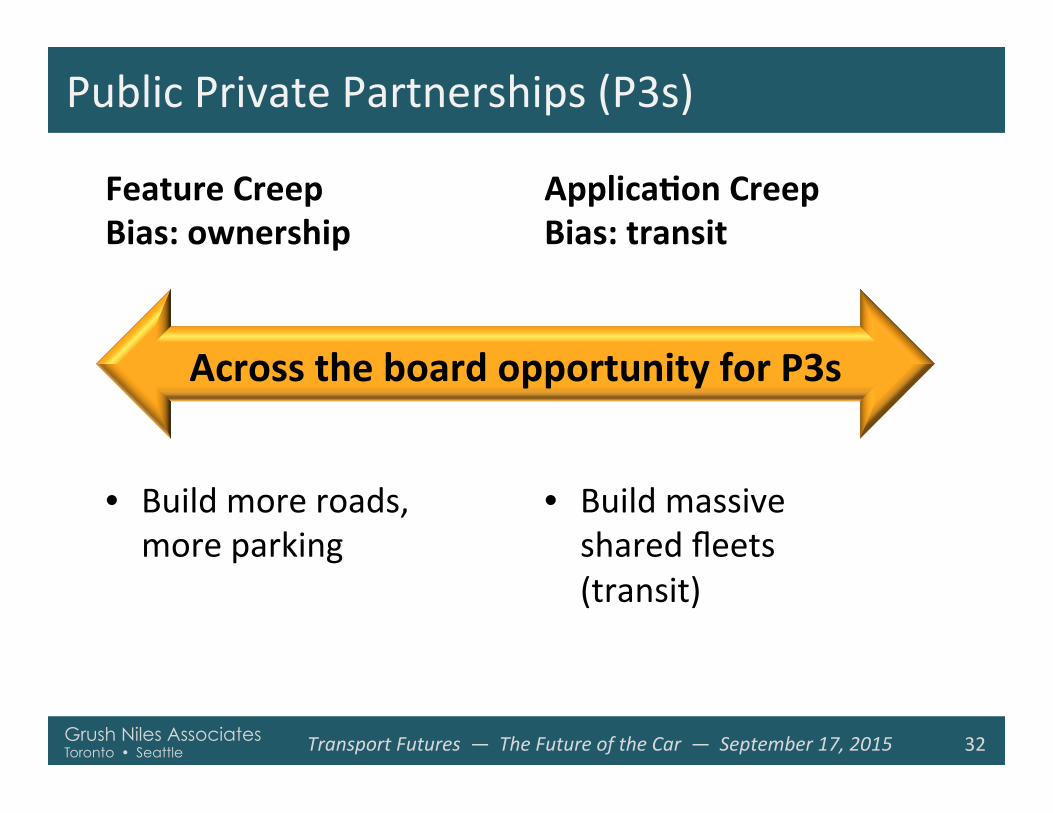

Public Private Partnerships (P3s)

Feature Creep Bias: ownership

• Build more roads, more parking

ApplicaHon Creep Bias: transit

• Build massive shared fleets (transit)

32

Across the board opportunity for P3s

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

Policy Complexity

Feature Creep

• Driver-‐in/Driver-‐out mix from 2030?-‐2050

• Motor vehicle regulaEon

ApplicaHon Creep

• P3s bring policy challenges

• Transit vehicle regulaEon

33

Complexity either way

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

How soon to the “Final Jump”?

Feature Creep Household vehicles

• Discon@nuity at L5 • Technology deployed slowly due to mix of driver/no-‐driver

• L5 likely delayed

ApplicaHon Creep Large shared fleets

• Steady ramp toward L5 • Technology deployed sooner due to Eered use-‐constraints

• L5 acceleraEon enabled

34

Grush Niles Associates Toronto � Seattle Transport Futures — The Future of the Car — September 17, 2015

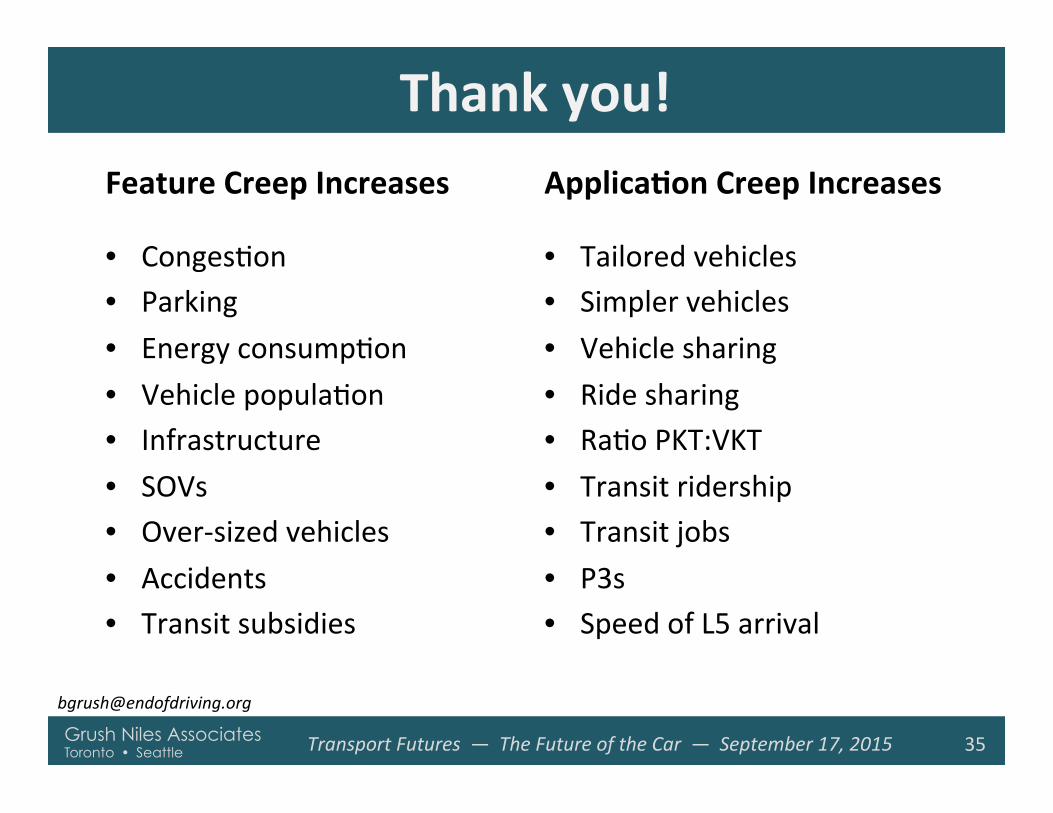

Thank you! Feature Creep Increases

• CongesEon • Parking • Energy consumpEon • Vehicle populaEon • Infrastructure • SOVs • Over-‐sized vehicles • Accidents • Transit subsidies

ApplicaHon Creep Increases

• Tailored vehicles • Simpler vehicles • Vehicle sharing • Ride sharing • RaEo PKT:VKT • Transit ridership • Transit jobs • P3s • Speed of L5 arrival

35