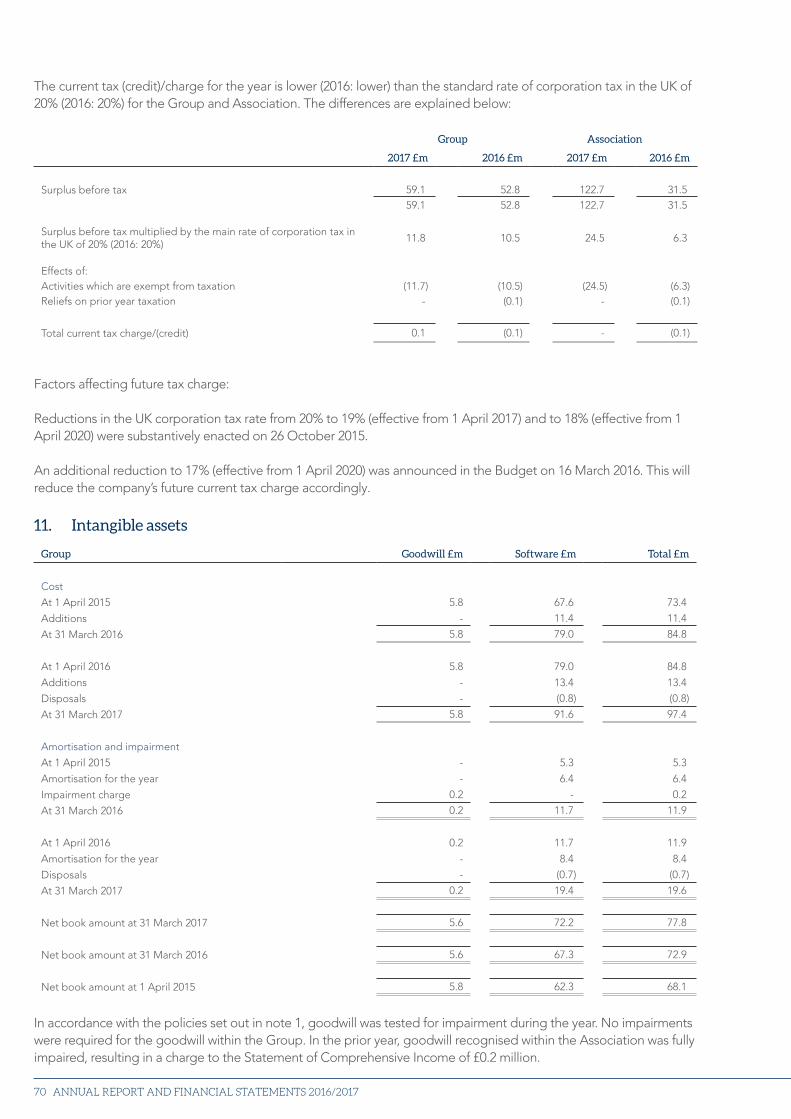

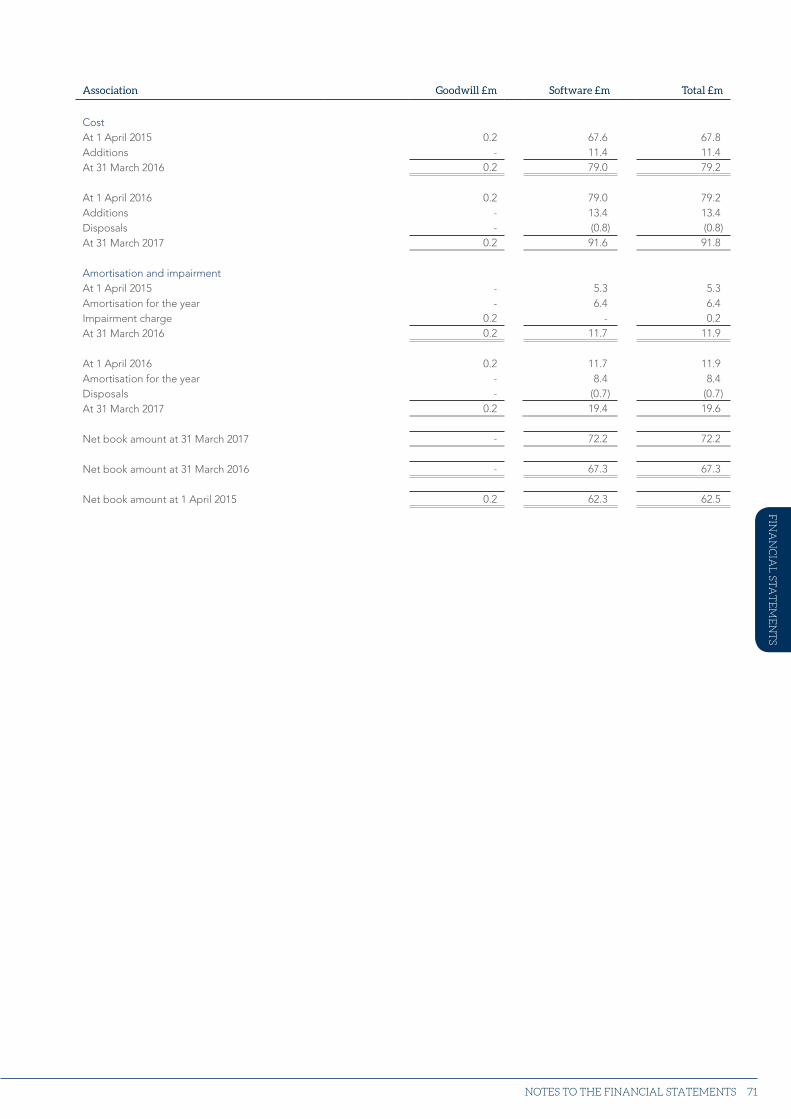

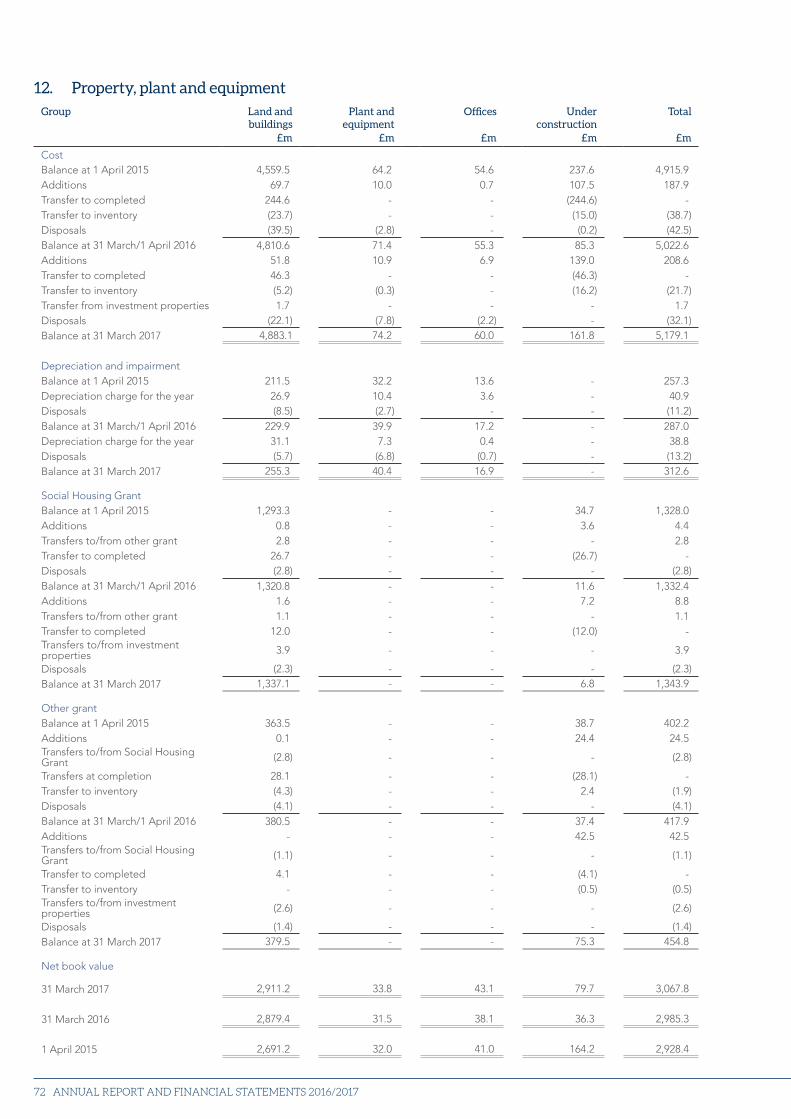

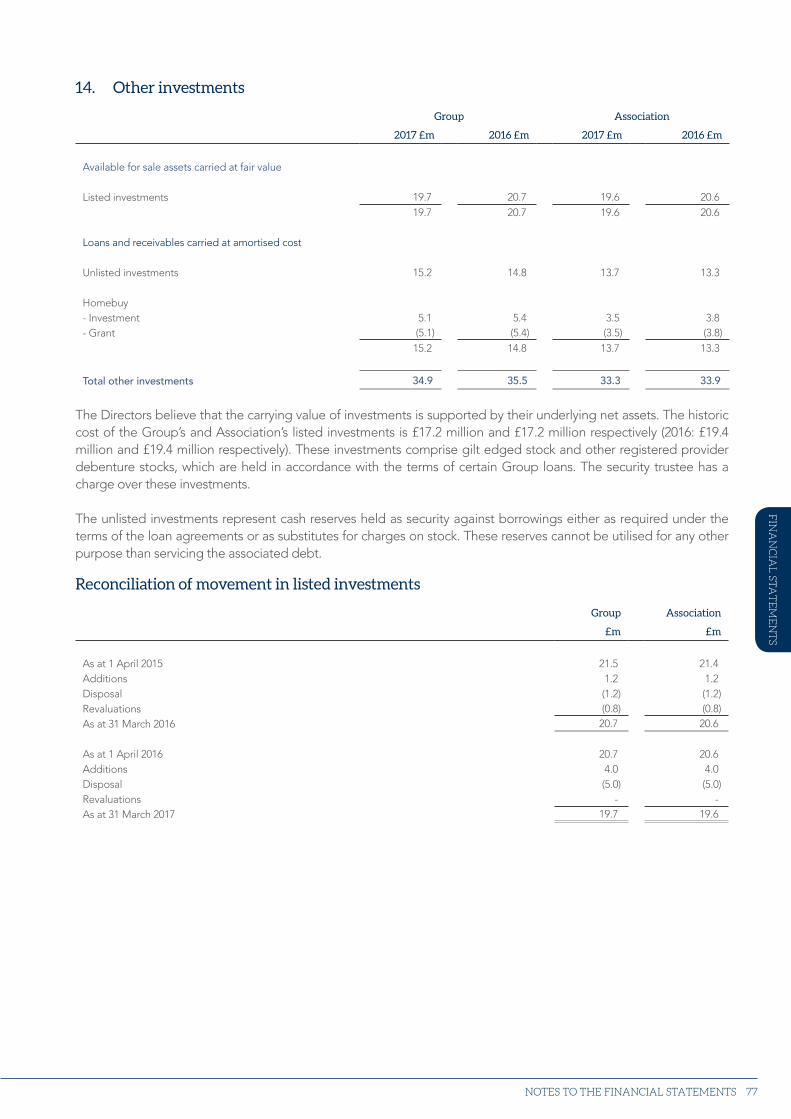

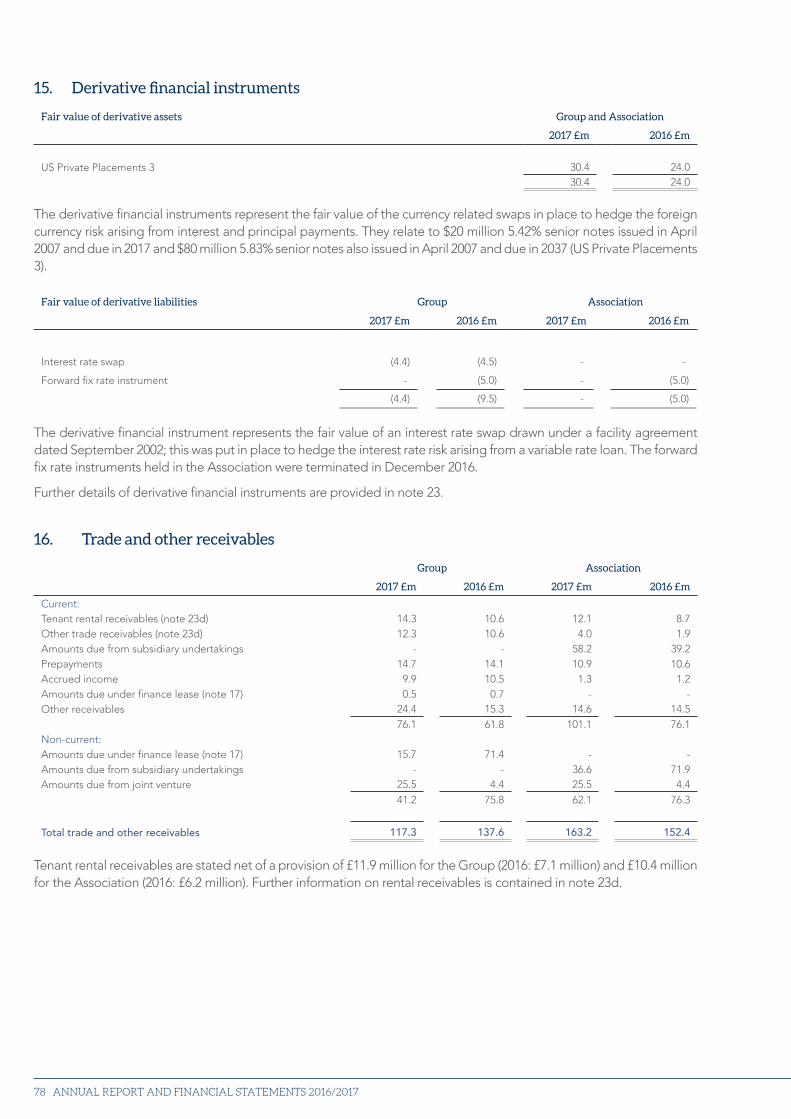

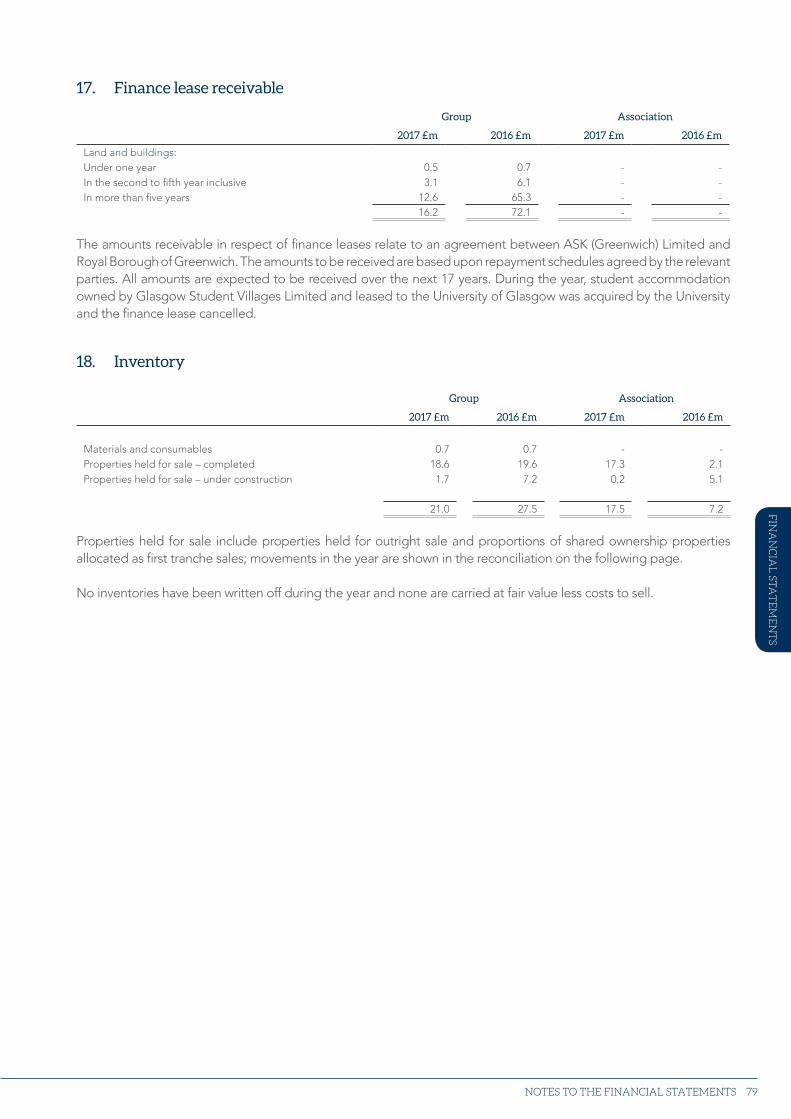

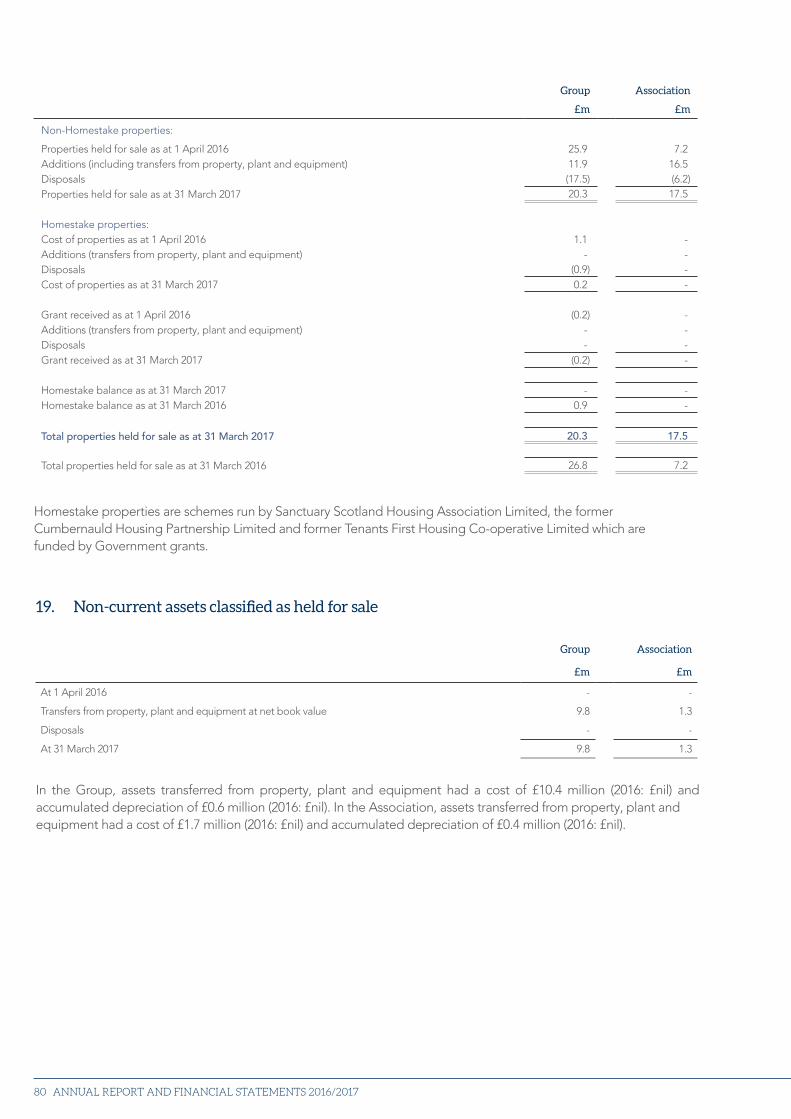

annual report and financial statements - sanctuary group · 6 annual report and financial...

TRANSCRIPT

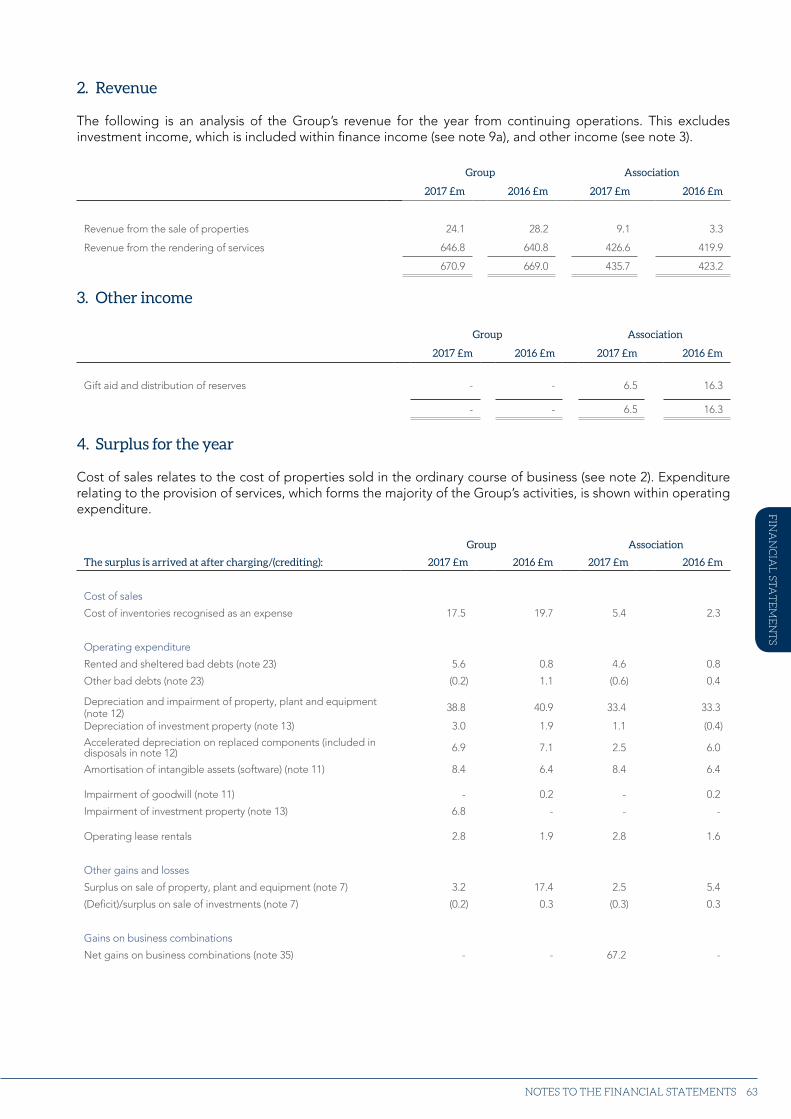

2 ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/2017

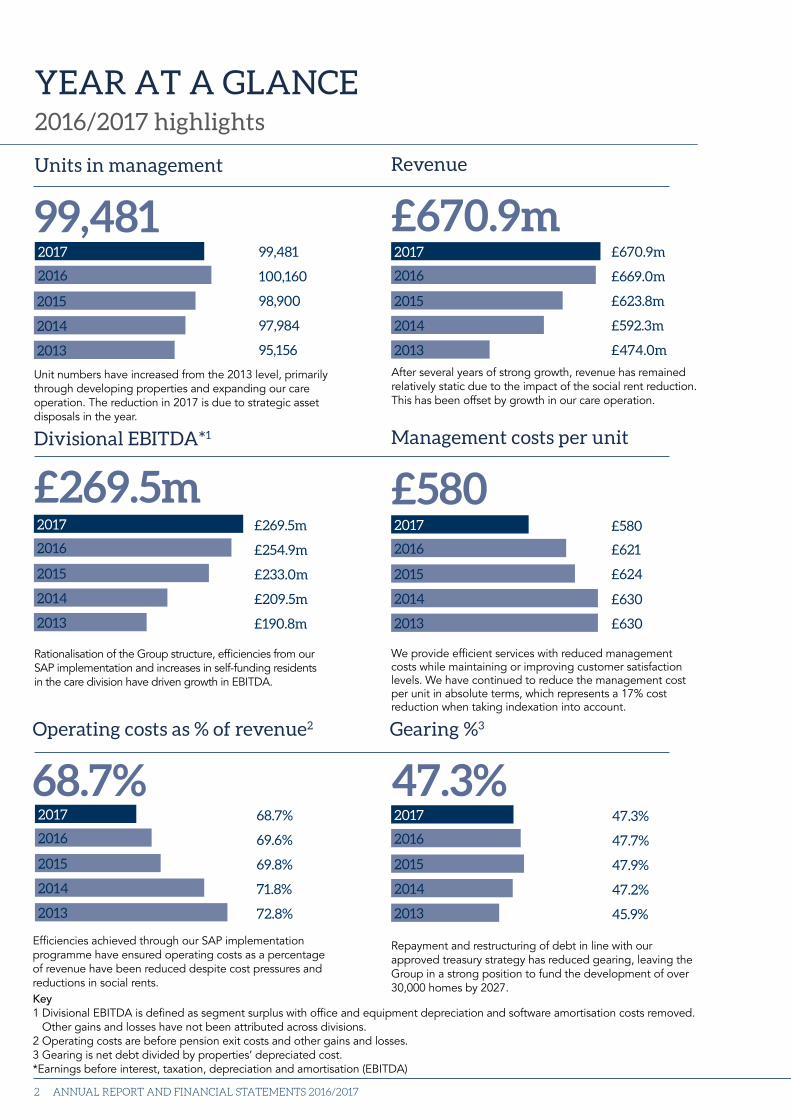

YEAR AT A GLANCE 2016/2017 highlights

68.7% 2017 68.7%

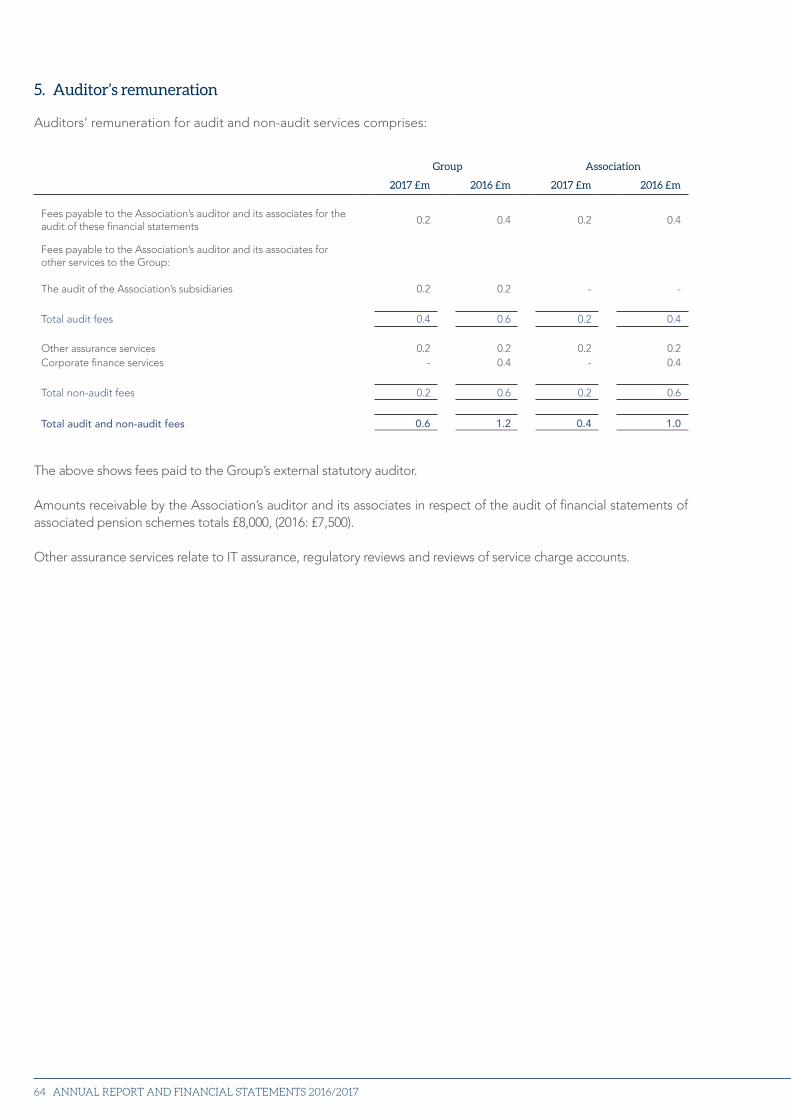

2016 69.6%

2015 69.8%

2014 71.8%

2013 72.8%

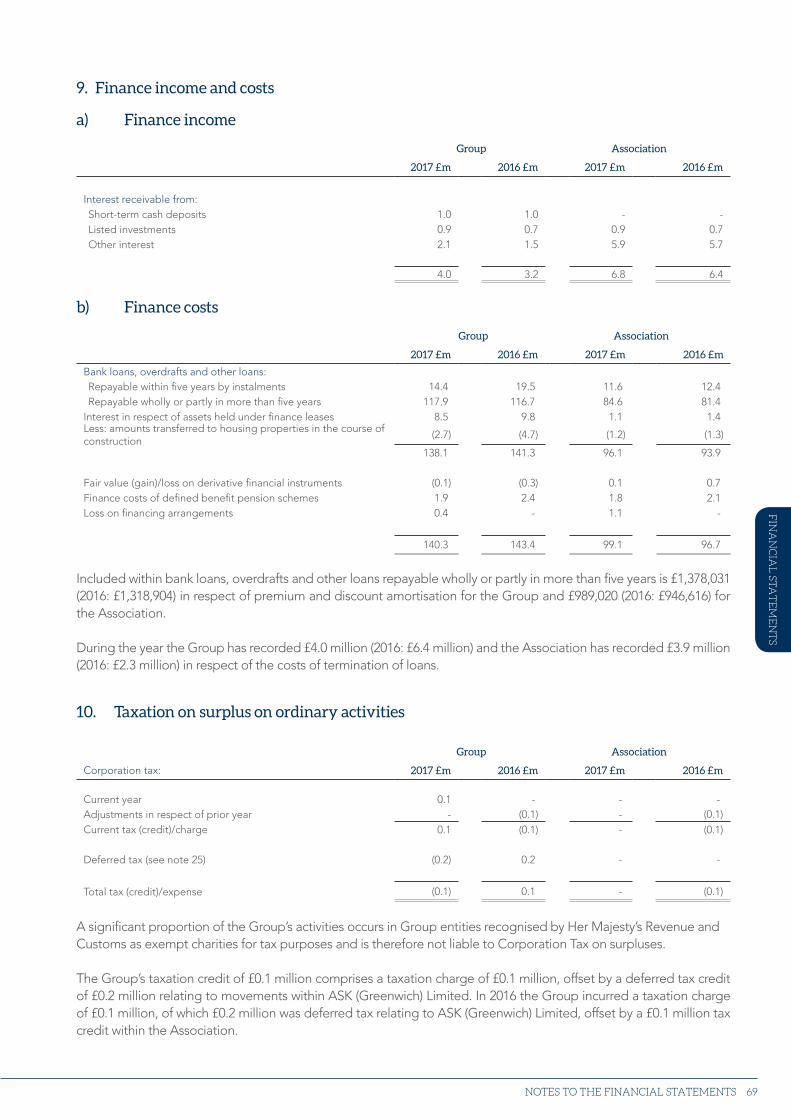

Efficiencies achieved through our SAP implementation programme have ensured operating costs as a percentage of revenue have been reduced despite cost pressures and reductions in social rents.

99,481 2017 99,481

2016 100,160

2015 98,900

2014 97,984

2013 95,156

Units in management

Unit numbers have increased from the 2013 level, primarily through developing properties and expanding our care operation. The reduction in 2017 is due to strategic asset disposals in the year.

Divisional EBITDA*1

£269.5m 2017 £269.5m

2016 £254.9m

2015 £233.0m

2014 £209.5m

2013 £190.8m

Rationalisation of the Group structure, efficiencies from our SAP implementation and increases in self-funding residents in the care division have driven growth in EBITDA.

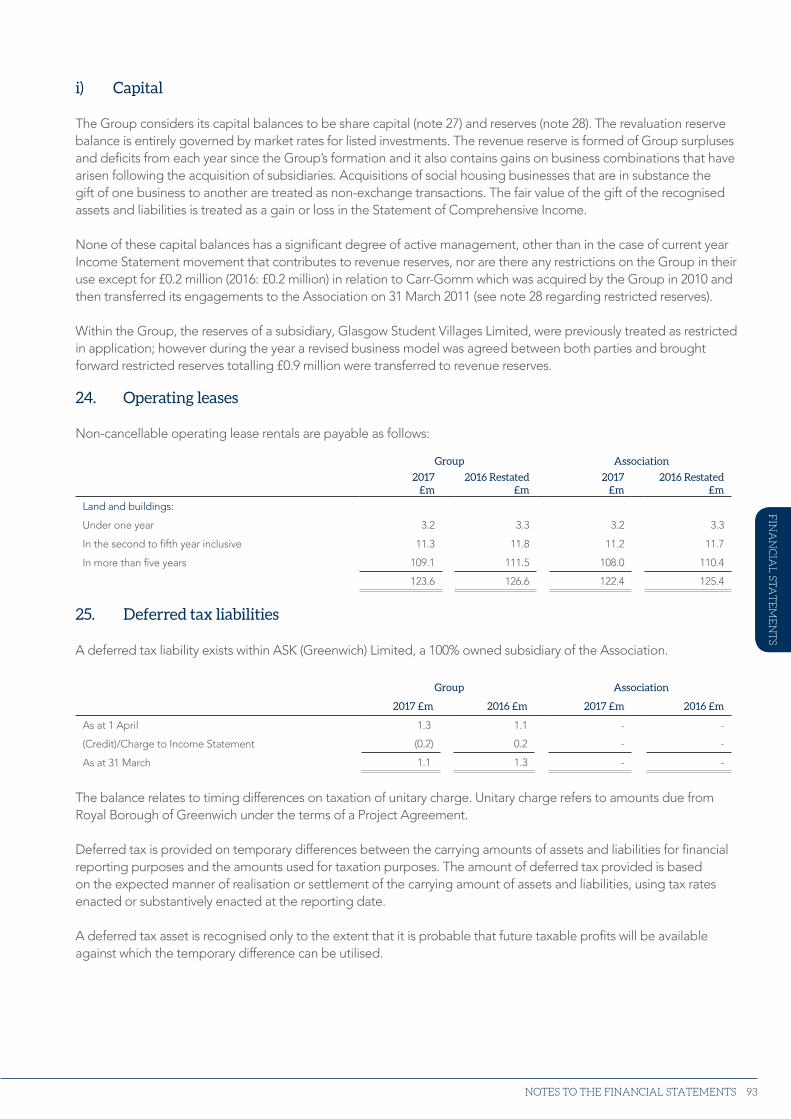

47.3% 2017 47.3%

2016 47.7%

2015 47.9%

2014 47.2%

2013 45.9%

Repayment and restructuring of debt in line with our approved treasury strategy has reduced gearing, leaving the Group in a strong position to fund the development of over 30,000 homes by 2027.

Revenue

£670.9m 2017 £670.9m

2016 £669.0m

2015 £623.8m

2014 £592.3m

2013 £474.0m

After several years of strong growth, revenue has remained relatively static due to the impact of the social rent reduction. This has been offset by growth in our care operation.

Management costs per unit

£580 2017 £580

2016 £621

2015 £624

2014 £630

2013 £630

We provide efficient services with reduced management costs while maintaining or improving customer satisfaction levels. We have continued to reduce the management cost per unit in absolute terms, which represents a 17% cost reduction when taking indexation into account.

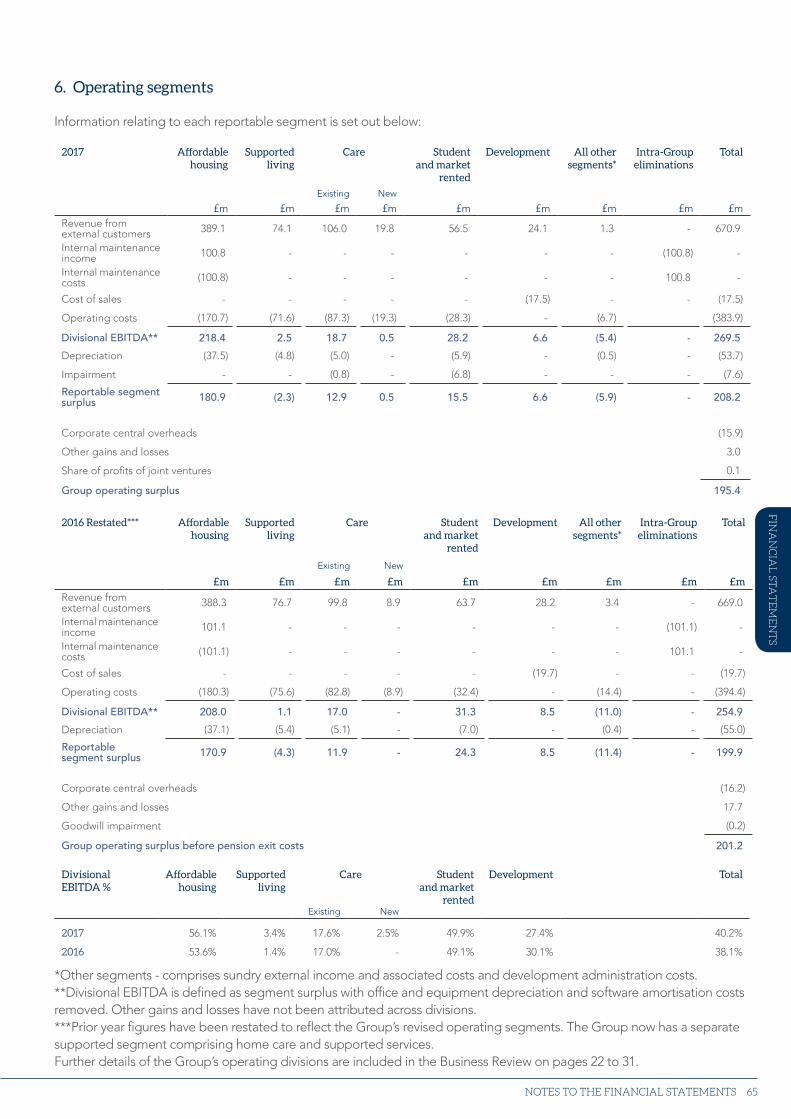

Key1 Divisional EBITDA is defined as segment surplus with office and e quipment depreciation and software amortisation costs removed.

Other gains and losses have not been attributed across divisions.2 Operating costs are before pension exit costs and other gains and losses.3 Gearing is net debt divided by properties’ depreciated cost.*Earnings before interest, taxation, depreciation and amortisation (EBITDA)

Operating costs as % of revenue2 Gearing %3

Strategic report Financial statem

ents

3

CONTENTS

STR

AT

EG

IC R

EP

OR

T

GO

VE

RN

AN

CE

F

INA

NC

IAL

STA

TE

ME

NT

SO

TH

ER

INF

OR

MA

TIO

N

CONTENTS

THE STRATEGIC REPORT OF THE BOARD AND OPERATING AND FINANCIAL REVIEW

GROUP CHAIR’S STATEMENT 4

GROUP CHIEF EXECUTIVE’S

STATEMENT

6

THE OPERATING STRUCTURE OF

OUR BUSINESS

8

OUR VALUES 9

SANCTUARY’S BUSINESS MODEL 10

VALUE FOR MONEY 12

BUSINESS STRATEGY 2017–2021 14

CHIEF FINANCIAL OFFICER’S REVIEW 16

BUSINESS REVIEW 22

GOVERNANCE

GROUP BOARD 32

STATUTORY, REGULATORY AND

OTHER INFORMATION

38

INTERNAL CONTROLS 40

VIABILITY STATEMENT 42

PRINCIPAL RISKS AND

UNCERTAINTIES

43

STATEMENT OF BOARD’S

RESPONSIBILITIES IN RESPECT OF

THE BOARD’S REPORT AND THE

FINANCIAL STATEMENTS

46

FINANCIAL STATEMENTS

INDEPENDENT AUDITOR’S

REPORT TO SANCTUARY

HOUSING ASSOCIATION

47

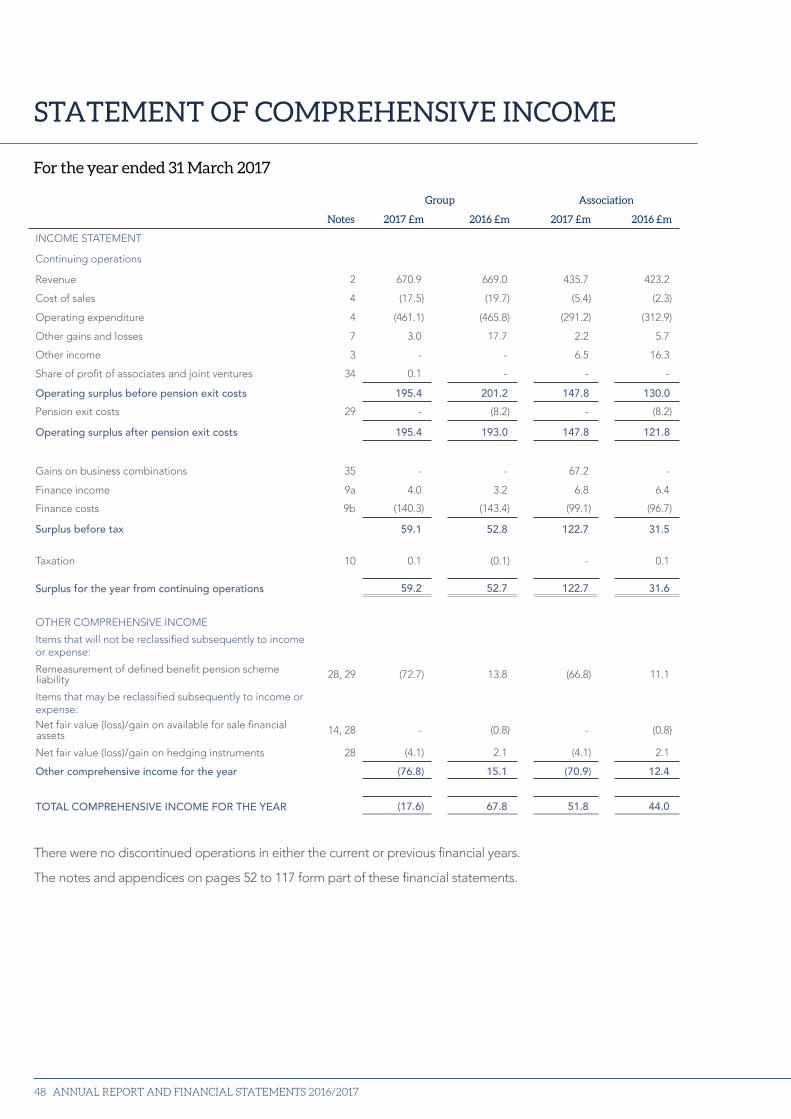

STATEMENT OF

COMPREHENSIVE INCOME

48

STATEMENT OF FINANCIAL

POSITION

49

STATEMENT OF CHANGES IN

EQUITY

50

STATEMENT OF CASH FLOWS 51

NOTES TO THE FINANCIAL

STATEMENTS

52

OTHER INFORMATION

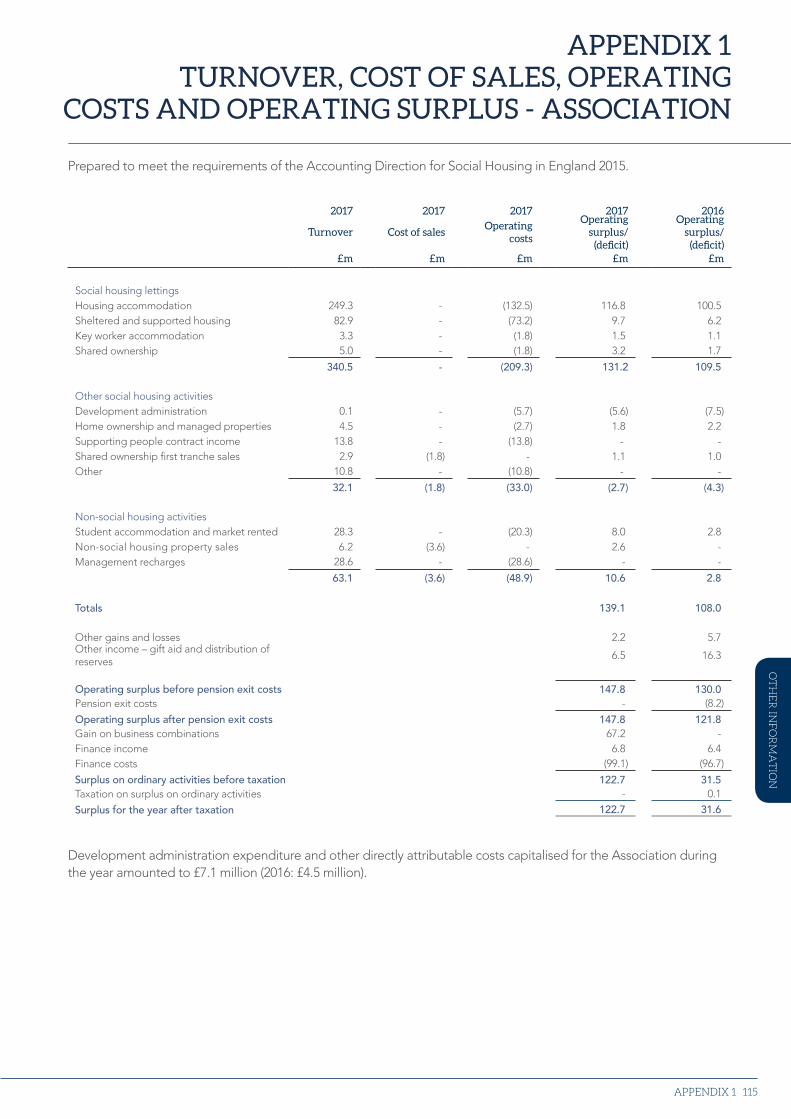

APPENDIX 1 TURNOVER, COST

OF SALES, OPERATING COSTS

AND OPERATING SURPLUS

114

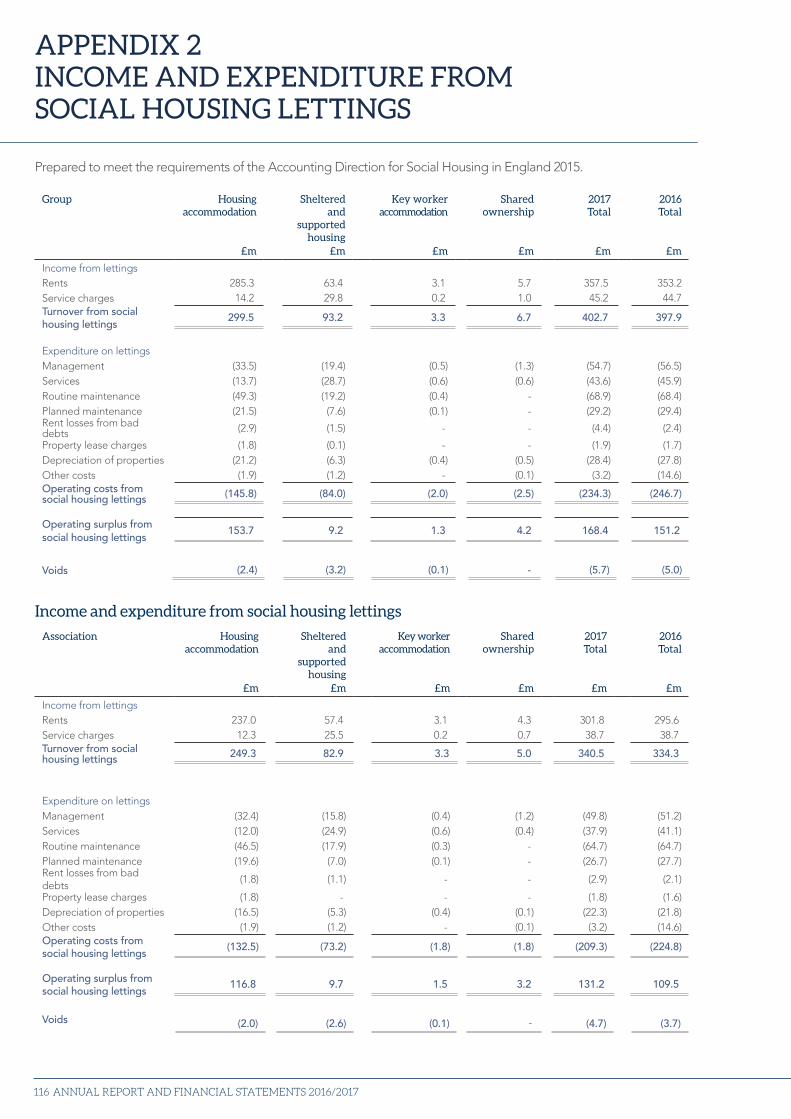

APPENDIX 2 INCOME AND

EXPENDITURE FROM SOCIAL

HOUSING LETTINGS

116

APPENDIX 3 FIVE-YEAR

SUMMARY NOTES117

ADVISORS AND OTHER

INFORMATION

118

Icon keyLinks to website

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/20174

GROUP CHAIR’S STATEMENT

“Sanctuary’s unique portfolio of accommodation and services means we are well placed to make a positive difference to a wide range of communities across the country.”

In a changing operating environment, Sanctuary remains committed to delivering high quality services, whilst leading the way in solving Britain’s housing crisis. As a result, we are developing over 30,000 new homes in England and Scotland by 2027, two-thirds of which will be affordable housing.

The past year has been focused on laying the foundations for our ambitious development programme and ensuring we continue to deliver services as efficiently as possible.

Sanctuary’s unique portfolio of accommodation and services means we are well placed to make a positive difference to a wide range of communities across the country.

Sanctuary is in the process of expanding its portfolio of care homes through a combination of construction and acquisition. As one of the largest providers of residential and nursing care in the UK, this will enable us to give a greater number of older people the care and support they want to live healthy and fulfilling lives.

None of our achievements would be possible without financial strength and uncompromising standards of governance. The confirmation of the Group’s financial ratings by Moody’s and Standard & Poor’s, and the Homes and Communities Agency’s G1/V1 rating, confirm external confidence in the Group’s business plan and governance.

We are mindful of the risks Sanctuary is facing, including the impact of welfare reform on our tenants, further reductions in social rents and uncertainty around Brexit. I am confident that we will be able to succeed in our mission and ensure Sanctuary’s continued growth as a sector-leading and sustainable business.

Our charitable objectives, of providing housing and care to those who are in need, remain the reason for our existence and are what motivate us every day. To that end, it is thanks to the commitment of our 11,000 staff that we can look to the future with optimism for our customers, stakeholders and investors.

Leading the way in solving Britain’s housing crisis

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/20174

Jonathan Lander Group Chair

Strategic report Financial statem

ents

5

“The past year has been focused on laying the foundations for our ambitious development programme and ensuring we continue to deliver services as efficiently as possible.”

5GROUP CHAIR’S STATEMENT 5

STR

AT

EG

IC R

EP

OR

T

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/20176

“Sanctuary is playing

an important role in

delivering high quality

social care to older

people and those who

need additional support.”

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/20176

Strategic report Financial statem

ents

7

GROUP CHIEF EXECUTIVE’S STATEMENT

GROUP CHIEF EXECUTIVE’S STATEMENT 7

STR

AT

EG

IC R

EP

OR

T

Demonstrating our values

“As Sanctuary approaches its 50th year, our charitable objectives remain as important as when we were set up.”

Sanctuary is developing over 30,000 homes by 2027, which will enable the Group to make a marked contribution to improving housing nationwide. The programme has been progressing apace and now has 5,000 homes in the pipeline, building up to a sustainable programme of 3,000 new homes each year from 2020.

The Group is proud to be developing notable and exciting schemes including the former Victoria Infirmary in Glasgow; contemporary, stylish apartments at The Quadrangle in Haringey; and family homes at Bullwood Hall in Rochford. As well as providing new homes, this programme will create a wide range of employment and training opportunities, enhancing theimpact of the investment. To supportthe delivery of the programme the Homes and Communities Agency has awarded Sanctuary almost £90 million of funding, the largest grant allocation in the sector.

Furthermore, Sanctuary is playing an important role in delivering high quality social care to older people and those who need additional support. Our 68 care homes hold one of the highest overall Care Quality Commission ratings for large providers in the sector with 85 per cent of our homes rated good or outstanding, while we continue to win contracts around the country, most recently in Redcar and Cleveland, to deliver support services. We have expanded our offering with a number of intermediate care contracts allowing people to leave hospital when they are ready and receive rehabilitative care before returning home.

Our continued focus on cost-effective services has seen us launch our sector-leading enterprise-wide information technology system. We now use the SAP system to manage housing and maintenance operations, on top of our existing use of it for human resources, finance and recruitment. This has led to improved and streamlined processes and will mean we can operate even more efficiently.

As Sanctuary approaches its 50th year, our charitable objectives remain as important as when we were set up. Throughout that time, we have demonstrated our values of ambition, diversity, integrity, quality and sustainability. Our people share those values and it is thanks to them that we are able to make a difference to customers and society as a whole.

David Bennett Group Chief Executive

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/20178

Development We take our role in meeting the UK’s housing shortage seriously and we are building more homes than ever before. Our significant development programme will include homes built by our own in-house construction team. Ultimately, we want to build the majority of our new homes, creating training and employment opportunities for our customers along the way.

Affordable housing We believe everyone should be able to live in a decent home, where they feel safe and secure. We provide a range of high quality affordable homes and support services across England and Scotland, reflecting the needs and aspirations of our customers and delivering services at a competitive cost. We also provide in-house maintenance and reinvestment services across our portfolio of properties.

CareWe are a leading provider of care for older people, with 68 welcoming homes operated by highly trained staff. We are committed to keeping kindness at the heart of our care. We help our residents live dignified and fulfilling lives in places where they can explore their passions, learn new things and build lasting friendships. Our well-equipped care homes provide a range of long and short-term care and support, including residential, nursing, intermediate, respite, end-of-life, and specialist dementia care.

Supported livingWe provide a range of housing where specialist, tailored support is offered alongside accommodation. This includes support for people with learning and physical disabilities, young people, homelessness and people with mental health problems. We also provide care in people’s homes in our extra care schemes.

Student and market rentedWe provide a range of commercial services. These include working with universities and NHS trusts to provide accommodation and facilities management services for students and key workers, managing a portfolio of direct-let student accommodation, as well as overseeing a diverse portfolio of commercial and market rent properties.

Sanctuary Group is structured into five operations, all supported by our Group shared service centre. We have structured our business in this way to ensure the operating efficiency of each operation is clearly visible and transparent to our customers, stakeholders and funders.

THE OPERATING STRUCTURE OF OUR BUSINESS

Strategic report Financial statem

ents

9

At the core of our business are Sanctuary’s values. These represent the way we conduct ourselves and how we do business.

OUR VALUES

OUR values

our mission

To remain a market leader in the provision of high quality housing, nursing and residential care, and

community services.

AMBITION

qualityWe focus on delivering positive outcomesfor our customers.We have high standards; providing efficient and effective services.

sustainabilityWe continue to build a sustainable business model for our people and our customers.We deliver services ourselves wherever possible.

diversityWe respect and value the diversity of our people. We are committed to fair access to services for all of our customers.

We invest in and care for our people and communities.We seek opportunities to grow our business.

integrityWe act with honesty and integrity in all that we do. We’ll do the right thing, even if it’s not the easy thing.

OUR VALUES 9

STR

AT

EG

IC R

EP

OR

T

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201710

Building new homes

£117m

£18m

£4m

£139m

Investing in existing homes

£69m

£47m

£23m

£139m

Providing services and community investment

£312m

HOW IT IS USED TO MEET OUR OBJECTIVES

ECONOMY

Raising funds

Repaying debt

£50m

Raising capital

£250m

-£128m -£128m

-£12

8m

-£128m

R

aisi

ng

capi

tal

R

epayin

g deb

t

=£590m

Businessactivities

Affordable housing

£389m

Care

£126m

Student and market rented £57m

Development

£24m

Supportedliving

£74m

£670m £670m

£670

m

£670m

Government funding

£48m £48m

£48m

£48m

G

ran

t rec

eiv

able

£48m

Grant receivab

le £48m

INCOMING RESOURCES

SANCTUARY’S BUSINESS MODEL

VALUE FOR MONEY =

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201710

£310.5m

£1.5m

Strategic report Financial statem

ents

11

Building new homes

New social homes

Shared ownership properties

New care homes

Investing in existing homes

Capital repairs and maintenance

Routine maintenance

Planned maintenance

Providing services and community investment

Provision of housing and care services Community investment

HOW IT IS USED TO MEET OUR OBJECTIVES

EFFECTIVENESS

Service

83% resident satisfaction with services

85% care home CQC compliance

V1/G1 rating from HCA

Economic

£92m reinvested into our properties

456 housing units completed

£1.5m procurement savings in the year

Social and environmental

61,690 people benefited from our community projects

£1.5m invested in communities

7,014 residents supported through projects promoting access to employment

EFFICIENCY EFFECTIVENESSECONOMY

SANCTUARY’S BUSINESS MODEL 1111

STR

AT

EG

IC R

EP

OR

T

£117m

£18m

£139m

£69m

£47m

£139m

£312m£310.5m

£1.5m

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201712

ECONOMYAchieving the best value

from our inputs, that is, where items were purchased did we

get them for the best possible value?

EFFICIENCYMaximising the outputs for a given level of inputs, that is, how good are we at creating

the output?

EFFECTIVENESSEnsuring the outputs deliver the desired

outcome, that is, was what we delivered at the correct standard and did

it achieve the desired outcome? We measure

effectiveness through the service, economic, and

social and environmental benefits created.

+

Our full Value for Money document is included within our Value Report, which can be found at: www.sanctuary-group.co.uk/about-us/publications

VALUE FOR MONEY

Our Group Board has responsibility for setting Value for Money objectives and for

monitoring progress. Objectives are set in the business plan and are reflected in

operational plans and budgets. Key performance indicators and management accounts

reports are monitored by our Executive Committee and Group Board against operational

plans and budgets. A balanced scorecard and performance reports are presented to our

Group Board.

At Sanctuary, we work to the principles of the three Es – Economy, Efficiency and

Effectiveness – while focusing on delivering service, economic, and social and

environmental benefits. We believe that to achieve and provide Value for Money we

must balance these in achieving our objectives.

Strategic report Financial statem

ents

13VALUE FOR MONEY

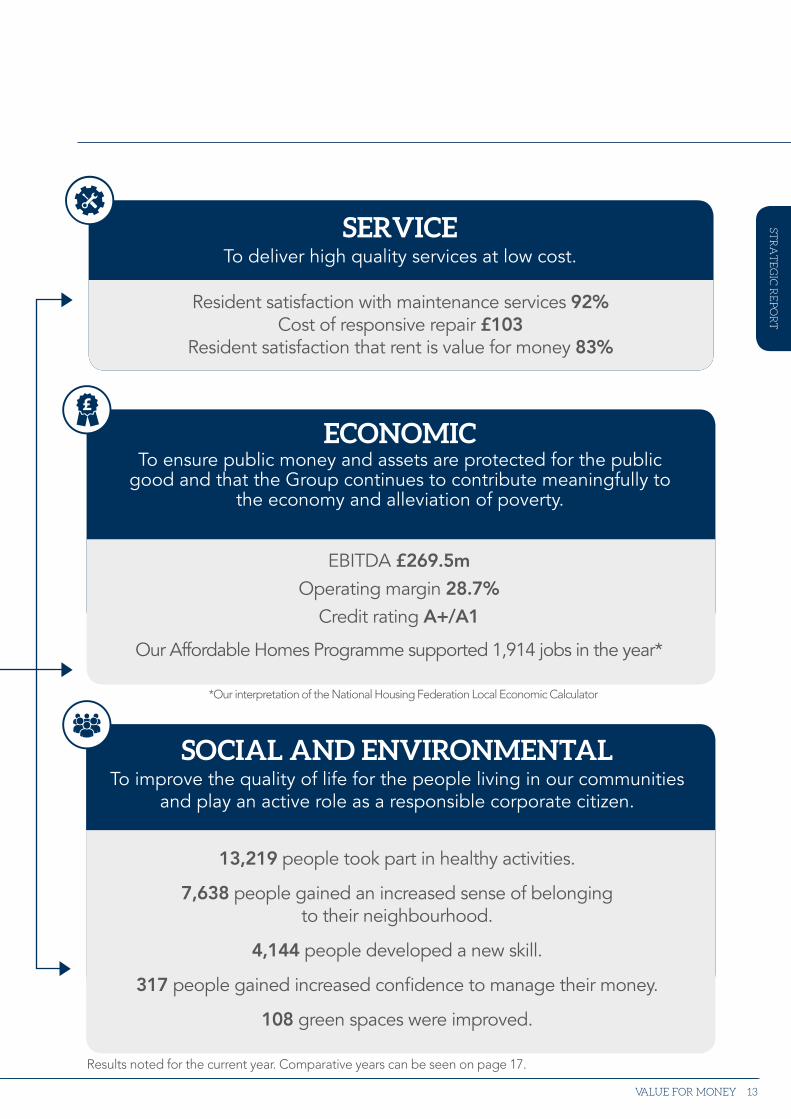

SERVICETo deliver high quality services at low cost.

SOCIAL AND ENVIRONMENTALTo improve the quality of life for the people living in our communities

and play an active role as a responsible corporate citizen.

Resident satisfaction with maintenance services 92% Cost of responsive repair £103

Resident satisfaction that rent is value for money 83%

ECONOMICTo ensure public money and assets are protected for the public

good and that the Group continues to contribute meaningfully to the economy and alleviation of poverty.

EBITDA £269.5m

Operating margin 28.7%

Credit rating A+/A1

Our Affordable Homes Programme supported 1,914 jobs in the year*

13,219 people took part in healthy activities.

7,638 people gained an increased sense of belonging to their neighbourhood.

4,144 people developed a new skill.

317 people gained increased confidence to manage their money.

108 green spaces were improved.

STR

AT

EG

IC R

EP

OR

T

*Our interpretation of the National Housing Federation Local Economic Calculator

Results noted for the current year. Comparative years can be seen on page 17.

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201714

BUSINESS STRATEGY 2017–2021

The opportunities and challenges facing the UK’s housing sector have never been greater. The EU referendum, increasing demographic pressure on housing and social care, deregulation, the impact of welfare reform, and rent reduction have contributed to a shifting landscape for social landlords. Organisations will need strength and flexibility to thrive in this new environment.

Sanctuary has that strength and flexibility, combined with a bold ambition to play a key part in solving the UK’s housing shortage. We recognise that now is a time for action and that the country needs organisations which are going to step up to dramatically increase housing supply while looking at new ways to deliver a range of tenures. Our strategy, as set out in the Group Business Plan, will do just that.

Our plan includes:

• building new homes – we are developing over 30,000 new homes by 2027. These will be a mixture of shared ownership, rent and properties for outright sale as well as care homes.

• providing cost-effective services – we provide efficient services with reduced management costs while maintaining or improving customer satisfaction levels.

• achieving high quality standards – we will make sure operations across the Group’s diverse range of activities meet the high service expectations of customers and regulators.

The Group has a well-earned reputation as a financially robust and well governed organisation. As a consequence of our careful financial management, public investment has been protected and we have been able to create capacity to subsidise the delivery of social housing, build new homes for those aspiring to own, part own or rent, and for Sanctuary to be an important stakeholder in the communities we serve.

We will reinforce that reputation by utilising our resources to develop new housing for rent and for sale while:

• maintaining and improving key performance ratios;

• proactively managing a range of risks from sales risk through to welfare reform; and

• ensuring access to competitively priced credit.

The full Group Business Plan can be found on the Group website at www.sanctuary-group.co.uk/about-us/publications

Strategic report Financial statem

ents

15

Our development strategy

Our development programme is focused on enabling people to own their own home while providing high quality, affordable rent options for those who cannot, or do not want to, buy. Sanctuary, as one of the biggest developers of new homes in the sector, has invested around £1 billion in developing properties in the last six years.

We are committed to a new housing development programme delivering over 30,000 units by 2027, including 2,700 social rented units which will be built without grant and funded out of surplus.

As well as outright sale, our development programme will provide affordable home ownership, through the Help to Buy and shared equity products. Our shared ownership properties will be sold through our new brand Sanctuary Homes, while homes for outright sale will be sold through the new Beech Grove Homes brand. New websites will be established for each of the development brands, enabling innovative digital marketing.

Funding our development strategy

In order to achieve our objective to build over 30,000 units by 2027, the Group will use the following resources:

• Surpluses generated by our core operations are used to fund on-going development and reinvestment into our properties to provide the best possible standards for our tenants and residents.

• Property sales, by selling homes either fully or through shared ownership, generate profit which will be reinvested in more development.

• We have bid for and won almost £90 million of grant funding which will be receivable from the Homes and Communities Agency to build 2,265 affordable homes under the 2016–2021 Affordable Homes Programme, taking the largest share of the £1.3 billion allocation.

• We have entered into three joint ventures with one of the UK’s largest house building and construction groups, Galliford Try plc, in order to develop over 600 properties at three sites, including a significant element of affordable housing.

• Debt funding which is available to the Group due to our strong financial position. Our credit ratings of A1 from Moody’s and A+ from Standard & Poor’s, together with G1 and V1 governance and viability ratings from the Homes and Communities Agency, allow us to access funding at competitive rates of interest.

• Working with a specialist development company to deliver new care homes.

• We already have in place cash and facilities to fund development for over one year.

BUSINESS STRATEGY 2017–2021

STR

AT

EG

IC R

EP

OR

T

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201716

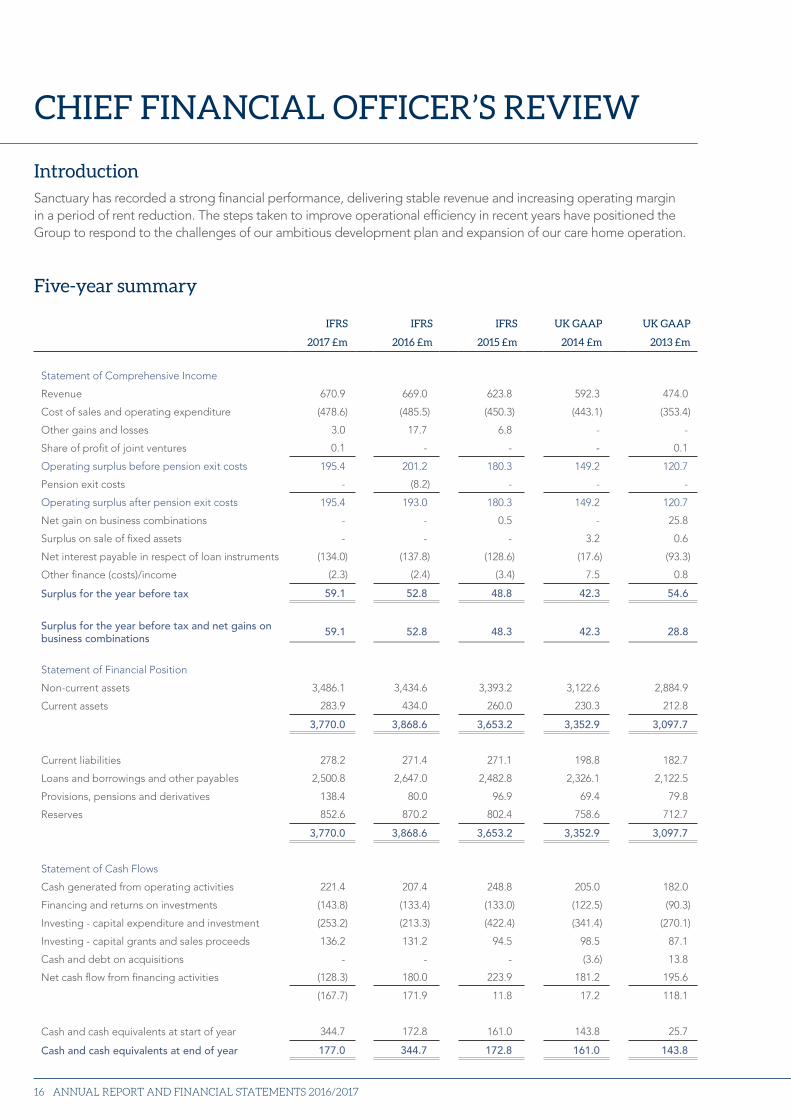

CHIEF FINANCIAL OFFICER’S REVIEW

IntroductionSanctuary has recorded a strong financial performance, delivering stable revenue and increasing operating margin in a period of rent reduction. The steps taken to improve operational efficiency in recent years have positioned the Group to respond to the challenges of our ambitious development plan and expansion of our care home operation.

Five-year summary

IFRS IFRS IFRS UK GAAP UK GAAP

2017 £m 2016 £m 2015 £m 2014 £m 2013 £m

Statement of Comprehensive Income

Revenue 670.9 669.0 623.8 592.3 474.0

Cost of sales and operating expenditure (478.6) (485.5) (450.3) (443.1) (353.4)

Other gains and losses 3.0 17.7 6.8 - -

Share of profit of joint ventures 0.1 - - - 0.1

Operating surplus before pension exit costs 195.4 201.2 180.3 149.2 120.7

Pension exit costs - (8.2) - - -

Operating surplus after pension exit costs 195.4 193.0 180.3 149.2 120.7

Net gain on business combinations - - 0.5 - 25.8

Surplus on sale of fixed assets - - - 3.2 0.6

Net interest payable in respect of loan instruments (134.0) (137.8) (128.6) (17.6) (93.3)

Other finance (costs)/income (2.3) (2.4) (3.4) 7.5 0.8

Surplus for the year before tax 59.1 52.8 48.8 42.3 54.6

Surplus for the year before tax and net gains on business combinations

59.1 52.8 48.3 42.3 28.8

Statement of Financial Position

Non-current assets 3,486.1 3,434.6 3,393.2 3,122.6 2,884.9

Current assets 283.9 434.0 260.0 230.3 212.8

3,770.0 3,868.6 3,653.2 3,352.9 3,097.7

Current liabilities 278.2 271.4 271.1 198.8 182.7

Loans and borrowings and other payables 2,500.8 2,647.0 2,482.8 2,326.1 2,122.5

Provisions, pensions and derivatives 138.4 80.0 96.9 69.4 79.8

Reserves 852.6 870.2 802.4 758.6 712.7

3,770.0 3,868.6 3,653.2 3,352.9 3,097.7

Statement of Cash Flows

Cash generated from operating activities 221.4 207.4 248.8 205.0 182.0

Financing and returns on investments (143.8) (133.4) (133.0) (122.5) (90.3)

Investing - capital expenditure and investment (253.2) (213.3) (422.4) (341.4) (270.1)

Investing - capital grants and sales proceeds 136.2 131.2 94.5 98.5 87.1

Cash and debt on acquisitions - - - (3.6) 13.8

Net cash flow from financing activities (128.3) 180.0 223.9 181.2 195.6

(167.7) 171.9 11.8 17.2 118.1

Cash and cash equivalents at start of year 344.7 172.8 161.0 143.8 25.7

Cash and cash equivalents at end of year 177.0 344.7 172.8 161.0 143.8

Strategic report Financial statem

ents

17

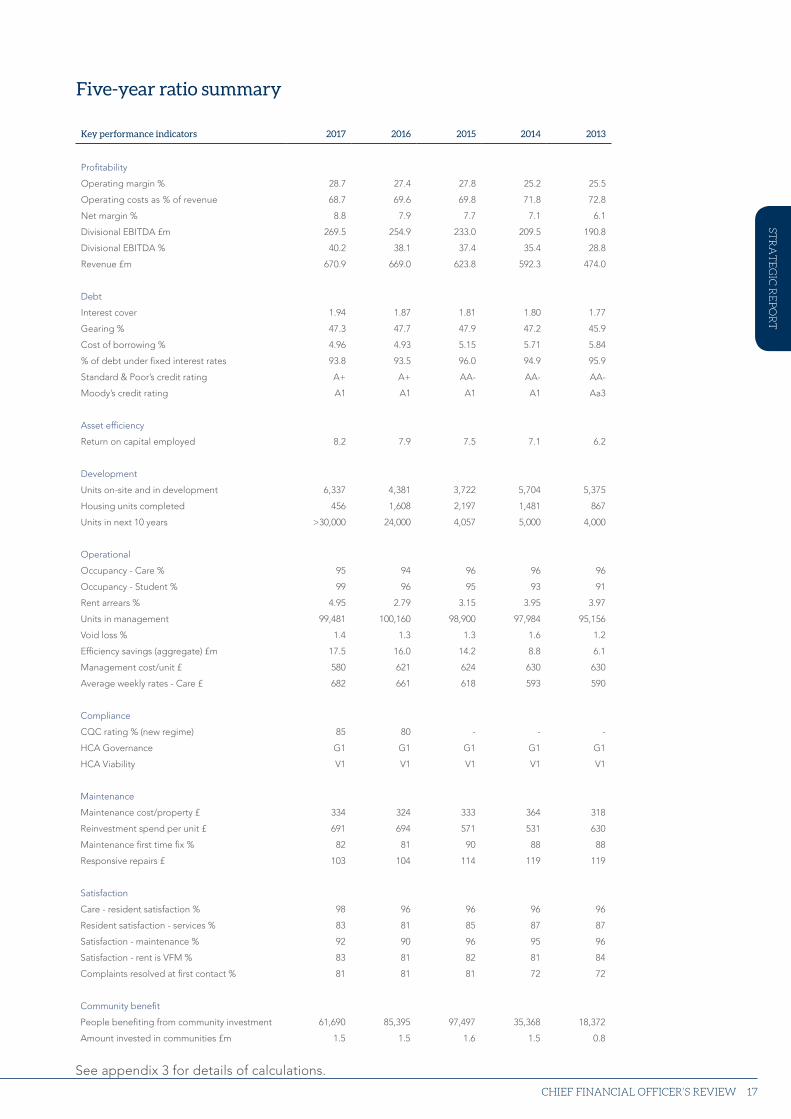

Five-year ratio summary

CHIEF FINANCIAL OFFICER’S REVIEW

Key performance indicators 2017 2016 2015 2014 2013

Profitability

Operating margin % 28.7 27.4 27.8 25.2 25.5

Operating costs as % of revenue 68.7 69.6 69.8 71.8 72.8

Net margin % 8.8 7.9 7.7 7.1 6.1

Divisional EBITDA £m 269.5 254.9 233.0 209.5 190.8

Divisional EBITDA % 40.2 38.1 37.4 35.4 28.8

Revenue £m 670.9 669.0 623.8 592.3 474.0

Debt

Interest cover 1.94 1.87 1.81 1.80 1.77

Gearing % 47.3 47.7 47.9 47.2 45.9

Cost of borrowing % 4.96 4.93 5.15 5.71 5.84

% of debt under fixed interest rates 93.8 93.5 96.0 94.9 95.9

Standard & Poor’s credit rating A+ A+ AA- AA- AA-

Moody’s credit rating A1 A1 A1 A1 Aa3

Asset efficiency

Return on capital employed 8.2 7.9 7.5 7.1 6.2

Development

Units on-site and in development 6,337 4,381 3,722 5,704 5,375

Housing units completed 456 1,608 2,197 1,481 867

Units in next 10 years >30,000 24,000 4,057 5,000 4,000

Operational

Occupancy - Care % 95 94 96 96 96

Occupancy - Student % 99 96 95 93 91

Rent arrears % 4.95 2.79 3.15 3.95 3.97

Units in management 99,481 100,160 98,900 97,984 95,156

Void loss % 1.4 1.3 1.3 1.6 1.2

Efficiency savings (aggregate) £m 17.5 16.0 14.2 8.8 6.1

Management cost/unit £ 580 621 624 630 630

Average weekly rates - Care £ 682 661 618 593 590

Compliance

CQC rating % (new regime) 85 80 - - -

HCA Governance G1 G1 G1 G1 G1

HCA Viability V1 V1 V1 V1 V1

Maintenance

Maintenance cost/property £ 334 324 333 364 318

Reinvestment spend per unit £ 691 694 571 531 630

Maintenance first time fix % 82 81 90 88 88

Responsive repairs £ 103 104 114 119 119

Satisfaction

Care - resident satisfaction % 98 96 96 96 96

Resident satisfaction - services % 83 81 85 87 87

Satisfaction - maintenance % 92 90 96 95 96

Satisfaction - rent is VFM % 83 81 82 81 84

Complaints resolved at first contact % 81 81 81 72 72

Community benefit

People benefiting from community investment 61,690 85,395 97,497 35,368 18,372

Amount invested in communities £m 1.5 1.5 1.6 1.5 0.8

STR

AT

EG

IC R

EP

OR

T

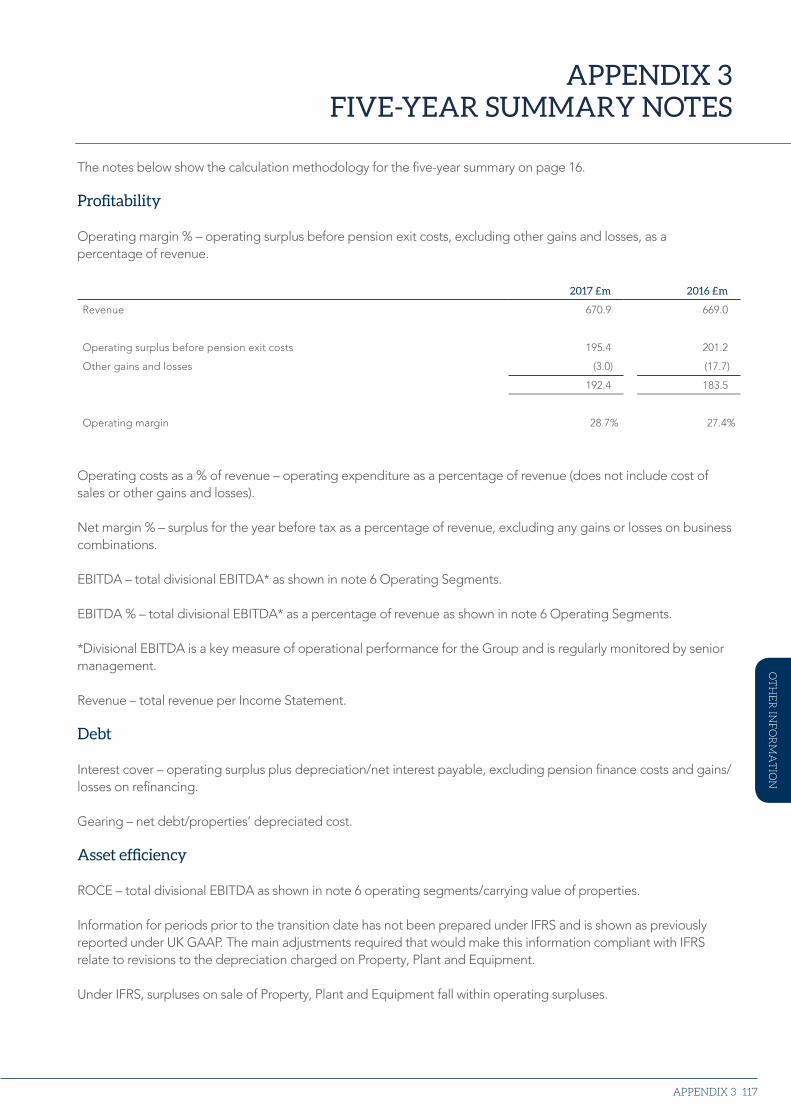

See appendix 3 for details of calculations.

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201718

Operational growth and efficiency

Group revenue was £670.9 million for the year, of which £646.8 million was attributable to operations and £24.1 million was attributable to property sales. Realising efficiency gains from our enterprise-wide SAP system, OneSanctuary, and increasing numbers of self-funders in our care operation have reduced the impact of changes in the housing and care sectors.

Operating surplus before other gains and losses has increased by £8.9 million to £192.4 million, an operating margin of 28.7%. EBITDA has increased by £14.6 million to £269.5 million.

Investment in our assets

Growth in housing properties includes: construction costs of £139.0 million; reinvestment spend on components of £68.7 million and planned maintenance of £22.5 million. Grant funding of £48.1 million has been received in the year for the development of new homes.

Cash collection and generation

The cash position of the Group is strong, with sufficient cash in hand and facilities to fund operations and capital expenditure throughout the next financial year and beyond.

The Group generated £221.4 million of cash from operating activities, an increase of £14.0 million on the prior year. At 31 March 2017, the Group had a cash balance of £177.0 million and had £176.0 million of undrawn facilities available.

Debt repayment profile and cost of capital

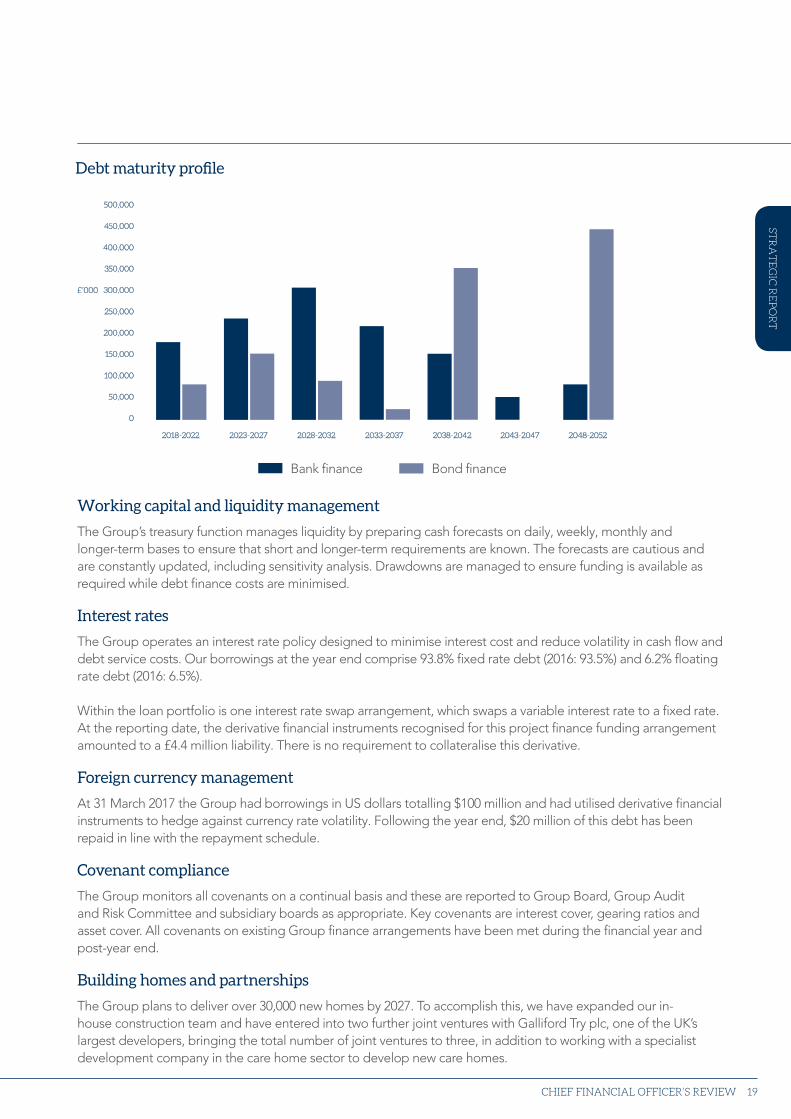

Net interest payable in respect of loan instruments has fallen by £3.8 million to £134.0 million as a result of restructuring the financing of one of the student properties and the repayment of certain loan facilities. Overall, the Group cost of borrowing for the year has increased to 4.96% from 4.93%, while interest cover has increased from 1.87 to 1.94. The Group has reduced its exposure to volatility of inherited financial derivatives by redeeming a forward starting derivative during the year. The weighted average duration of drawn debt across the Group is 20.3 years. Our funding strategy is designed to ensure refinancing requirements are manageable and planned.

The Group has a refinancing risk of 10.93% (£282.7 million) of existing drawn loans in the next five years. The Group is confident it can both refinance existing loans and finance the current business plan commitments. The Group anticipates funding this through a mix of fixed and variable interest rate facilities, cash generated from property sales, operating activities and Government grant.

During the year the Group has agreed £75 million of revolving credit facilities. This form of funding has been put in place to reflect the expected cash flows from our development and sales programme; ensuring flexible funding at cost-effective rates.

Capital finance and treasury

At 31 March 2017 the Group had total borrowings of £2,585.7 million, analysed as follows:

2017 £m 2016 £m

Bank loans and mortgages 1,153.7 1,273.8Senior secured notes and debenture stock 1,285.2 1,282.3Finance leases 146.8 150.4

2,585.7 2,706.5

Strategic report Financial statem

ents

19

Working capital and liquidity management

The Group’s treasury function manages liquidity by preparing cash forecasts on daily, weekly, monthly and longer-term bases to ensure that short and longer-term requirements are known. The forecasts are cautious and are constantly updated, including sensitivity analysis. Drawdowns are managed to ensure funding is available as required while debt finance costs are minimised.

Interest rates

The Group operates an interest rate policy designed to minimise interest cost and reduce volatility in cash flow and debt service costs. Our borrowings at the year end comprise 93.8% fixed rate debt (2016: 93.5%) and 6.2% floating rate debt (2016: 6.5%).

Within the loan portfolio is one interest rate swap arrangement, which swaps a variable interest rate to a fixed rate. At the reporting date, the derivative financial instruments recognised for this project finance funding arrangement amounted to a £4.4 million liability. There is no requirement to collateralise this derivative.

Foreign currency management

At 31 March 2017 the Group had borrowings in US dollars totalling $100 million and had utilised derivative financial instruments to hedge against currency rate volatility. Following the year end, $20 million of this debt has been repaid in line with the repayment schedule.

Covenant compliance

The Group monitors all covenants on a continual basis and these are reported to Group Board, Group Audit and Risk Committee and subsidiary boards as appropriate. Key covenants are interest cover, gearing ratios and asset cover. All covenants on existing Group finance arrangements have been met during the financial year and post-year end.

Building homes and partnerships

The Group plans to deliver over 30,000 new homes by 2027. To accomplish this, we have expanded our in-house construction team and have entered into two further joint ventures with Galliford Try plc, one of the UK’s largest developers, bringing the total number of joint ventures to three, in addition to working with a specialist development company in the care home sector to develop new care homes.

CHIEF FINANCIAL OFFICER’S REVIEW

STR

AT

EG

IC R

EP

OR

T

Debt maturity profile

500,000

450,000

400,000

350,000

300,000

250,000

200,000

150,000

100,000

50,000

0

2018-2022 2023-2027 2028-2032 2033-2037 2038-2042 2043-2047 2048-2052

£’000

Bank finance Bond finance

20 ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/2017

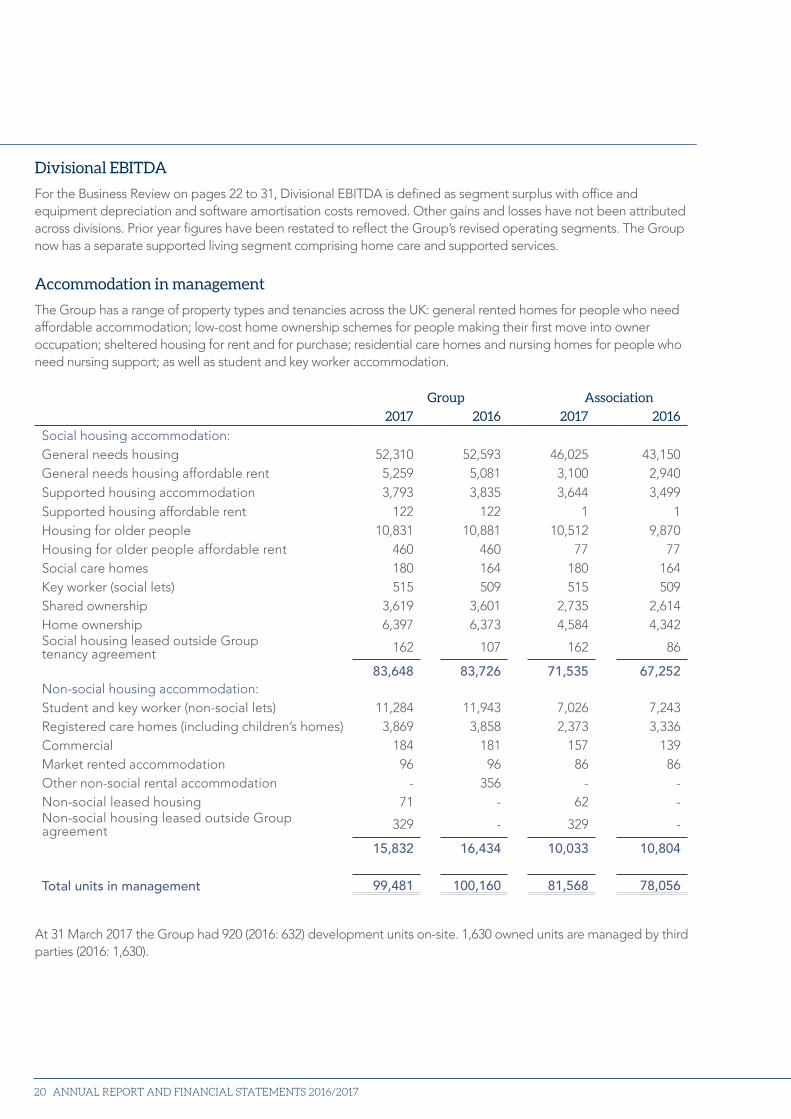

Divisional EBITDA

For the Business Review on pages 22 to 31, Divisional EBITDA is defined as segment surplus with office and equipment depreciation and software amortisation costs removed. Other gains and losses have not been attributed across divisions. Prior year figures have been restated to reflect the Group’s revised operating segments. The Group now has a separate supported living segment comprising home care and supported services.

Accommodation in management

The Group has a range of property types and tenancies across the UK: general rented homes for people who need affordable accommodation; low-cost home ownership schemes for people making their first move into owner occupation; sheltered housing for rent and for purchase; residential care homes and nursing homes for people who need nursing support; as well as student and key worker accommodation.

Group Association

2017 2016 2017 2016

Social housing accommodation:General needs housing 52,310 52,593 46,025 43,150General needs housing affordable rent 5,259 5,081 3,100 2,940Supported housing accommodation 3,793 3,835 3,644 3,499Supported housing affordable rent 122 122 1 1Housing for older people 10,831 10,881 10,512 9,870Housing for older people affordable rent 460 460 77 77Social care homes 180 164 180 164Key worker (social lets) 515 509 515 509Shared ownership 3,619 3,601 2,735 2,614Home ownership 6,397 6,373 4,584 4,342Social housing leased outside Group tenancy agreement 162 107 162 86

83,648 83,726 71,535 67,252Non-social housing accommodation: Student and key worker (non-social lets) 11,284 11,943 7,026 7,243Registered care homes (including children’s homes) 3,869 3,858 2,373 3,336Commercial 184 181 157 139Market rented accommodation 96 96 86 86Other non-social rental accommodation - 356 - -Non-social leased housing 71 - 62 -Non-social housing leased outside Groupagreement 329 - 329 -

15,832 16,434 10,033 10,804

Total units in management 99,481 100,160 81,568 78,056

At 31 March 2017 the Group had 920 (2016: 632) development units on-site. 1,630 owned units are managed by third parties (2016: 1,630).

Strategic report Financial statem

ents

21CHIEF FINANCIAL OFFICER’S REVIEW 21

STR

AT

EG

IC R

EP

OR

T

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201722

BUSINESS REVIEW Affordable housing – divisional review

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201722

Strategic report Financial statem

ents

23

Performance Revenue has remained stable in the affordable housing division. During the year, as a result of the Welfare Reform and Work Act 2016, a one per cent rent reduction has been applied to properties in England, subject to certain exceptions. This reduction applies only to rental income and not service charge income. Properties in Scotland are not included in the rent reduction and extra care properties are exempt from the changes in the current year.

EBITDA has increased due to efficiencies being realised from the implementation of our OneSanctuary enterprise-wide SAP system and the further consolidation of our housing operation, achieving an EBITDA percentage of 56.1%.

During the year Sanctuary Maintenance has further expanded the services that it offers to the Group, now providing 87% of gas repairs and servicing to our Scottish operation and maintenance services to our student business. This delivers greater value for money and better service for our customers. The average cost of a responsive repair is £103 for internally delivered works and £173 where external contractors are used. Customer satisfaction with repairs has increased from 90% in 2016 to 92% in the year.

The implementation of the SAP system in the maintenance operation which occurred at the end of the year will generate further efficiencies. Effectiveness of the service has been improved this year with increased levels of repairs being completed first time at 82%.

The average cost of managing a property has fallen to £580 from £621 in 2016.

Future targets and objectivesTo mitigate the effect of the Government’s rent reduction policy, there will be a continuing focus on cost management. The objective now is to maximise the efficiencies from the OneSanctuary programme through optimisation of the system, and providing a seamless customer service centre using state-of-the-art technology.

Planned Government changes to Local Housing Allowances, Housing Benefit and Universal Credit will present further challenges to the Group’s income base. The Group’s community investment activity will be aligned with these changes and a dedicated support function will be provided to tenants to offer additional guidance and advice during these challenging times.

The maintenance service will continue to roll-out in-house delivery of repairs and servicing, delivering a high quality, sustainable service which will support the future growth aspirations of the Group. A Maintenance Review programme is being implemented, delivering savings and other associated benefits to achieve a ‘smarter maintenance’ service, ensuring greater customer benefits and efficiencies. Our continued investment in technology will support operational improvements and efficiency through increased customer self-service, integrated materials management and electronic support planning.

AFFORDABLE HOUSING - DIVISIONAL REVIEW

2017 2016

Affordable housing

Revenue (£m) 389.1 388.3

Divisional EBITDA (£m) 218.4 208.0

Divisional EBITDA (%) 56.1 53.6

Capital investment (£m) 61.7 42.2

Units in management at the year end 79,012 79,153

Management costs per unit (£) 580 621

23

STR

AT

EG

IC R

EP

OR

T

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201724

BUSINESS REVIEW Supported living – divisional review

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201724

Strategic report Financial statem

ents

25SUPPORTED LIVING - DIVISIONAL REVIEW 25

*After provision for loss making contracts

Performance This division includes our supported living, home care and Sanctuary365 operations. A review of organisational structures, terms and conditions and consolidation of management across the Sanctuary Supported Living, Sanctuary Home Care and Sanctuary365 operations has brought consistency of quality and working practices across our services. Developments in our information technology systems have supported the continuous review of performance against consistent metrics. This greater focus on efficiency and margins has driven increased profitability across the operation.

Sanctuary Supported Living continues to win new contracts across the country, as well as extending existing contracts that we currently service. New contracts secured in the year include delivering mental health support in Redcar and Cleveland. The Group remains committed to supporting the vulnerable in society by providing a high quality and efficient service. Resulting efficiencies have compensated for increased costs from the introduction of the National Living Wage.

During the year Sanctuary Home Care has consolidated its operation. It has negotiated variations in contracts or ensured a smooth withdrawal and handover to new service providers where arrangements have not been financially viable. The level of agency staff expenditure has been significantly reduced during the year, improving margins achieved on contracts. This has contributed to an increase in EBITDA from £1.1 million in 2016 to £2.5 million in 2017.

Sanctuary365 has retained its accreditation as a platinum provider of telecare services by the Telecare Services Association and has continued to work with our supported living and extra care operations, growing the service provided to the Group’s existing customers by 10% during the year.

Future targets and objectivesSanctuary Supported Living will further develop internal expertise to embed best practice, identify market opportunities, and develop innovative products and services. Service models and working practices will be reviewed across all supported living services to ensure best practice models are shared, economies of scale realised and consistent engagement and service delivery models adopted. We will proactively respond to changes in the legislative frameworks which impact upon supported housing and the delivery of personal care services, and maximise the opportunities presented by these changes.

Sanctuary Home Care will continue its strategic review of domiciliary care contracts to ensure they are viable and that quality service provision can be offered at affordable rates.

The number of hours provided by our home care operation at Sanctuary-owned extra care schemes will be increased to generate efficiencies. This will be achieved while continuing to maintain good Care Quality Commission (CQC) ratings.

2017 2016

Supported living

Revenue (£m) 74.1 76.7

Divisional EBITDA (£m) 2.5 1.1

Divisional EBITDA (%) 3.4 1.4

Capital investment (£m) 9.0 6.5

Units in management at the year end 4,408 4,391

STR

AT

EG

IC R

EP

OR

T

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201726

BUSINESS REVIEW Care – divisional review

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201726

Strategic report Financial statem

ents

27CARE - DIVISIONAL REVIEW 27

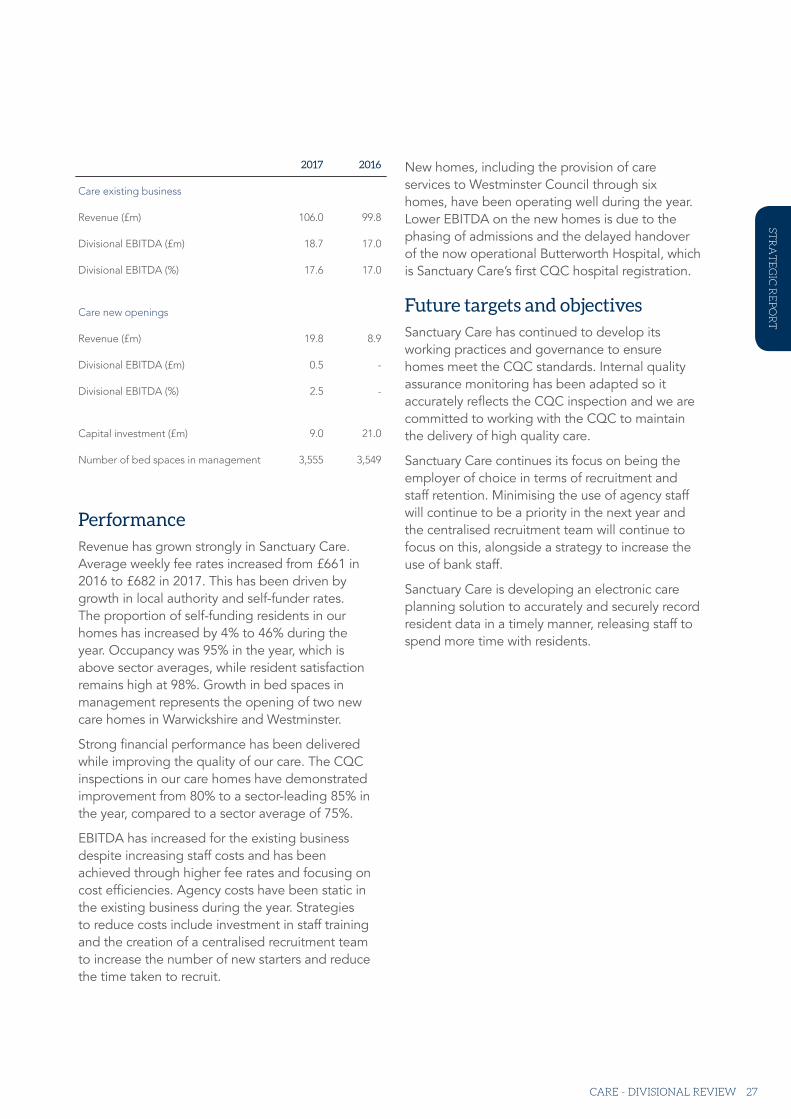

Performance Revenue has grown strongly in Sanctuary Care. Average weekly fee rates increased from £661 in 2016 to £682 in 2017. This has been driven by growth in local authority and self-funder rates. The proportion of self-funding residents in our homes has increased by 4% to 46% during the year. Occupancy was 95% in the year, which is above sector averages, while resident satisfaction remains high at 98%. Growth in bed spaces in management represents the opening of two new care homes in Warwickshire and Westminster.

Strong financial performance has been delivered while improving the quality of our care. The CQC inspections in our care homes have demonstrated improvement from 80% to a sector-leading 85% in the year, compared to a sector average of 75%.

EBITDA has increased for the existing business despite increasing staff costs and has been achieved through higher fee rates and focusing on cost efficiencies. Agency costs have been static in the existing business during the year. Strategies to reduce costs include investment in staff training and the creation of a centralised recruitment team to increase the number of new starters and reduce the time taken to recruit.

New homes, including the provision of care services to Westminster Council through six homes, have been operating well during the year. Lower EBITDA on the new homes is due to the phasing of admissions and the delayed handover of the now operational Butterworth Hospital, which is Sanctuary Care’s first CQC hospital registration.

Future targets and objectivesSanctuary Care has continued to develop its working practices and governance to ensure homes meet the CQC standards. Internal quality assurance monitoring has been adapted so it accurately reflects the CQC inspection and we are committed to working with the CQC to maintain the delivery of high quality care.

Sanctuary Care continues its focus on being the employer of choice in terms of recruitment and staff retention. Minimising the use of agency staff will continue to be a priority in the next year and the centralised recruitment team will continue to focus on this, alongside a strategy to increase the use of bank staff.

Sanctuary Care is developing an electronic care planning solution to accurately and securely record resident data in a timely manner, releasing staff to spend more time with residents.

2017 2016

Care existing business

Revenue (£m) 106.0 99.8

Divisional EBITDA (£m) 18.7 17.0

Divisional EBITDA (%) 17.6 17.0

Care new openings

Revenue (£m) 19.8 8.9

Divisional EBITDA (£m) 0.5 -

Divisional EBITDA (%) 2.5 -

Capital investment (£m) 9.0 21.0

Number of bed spaces in management 3,555 3,549

STR

AT

EG

IC R

EP

OR

T

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201728

BUSINESS REVIEW Student and market rented – divisional review

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201728

Strategic report Financial statem

ents

29STUDENT AND MARKET RENTED - DIVISIONAL REVIEW 29

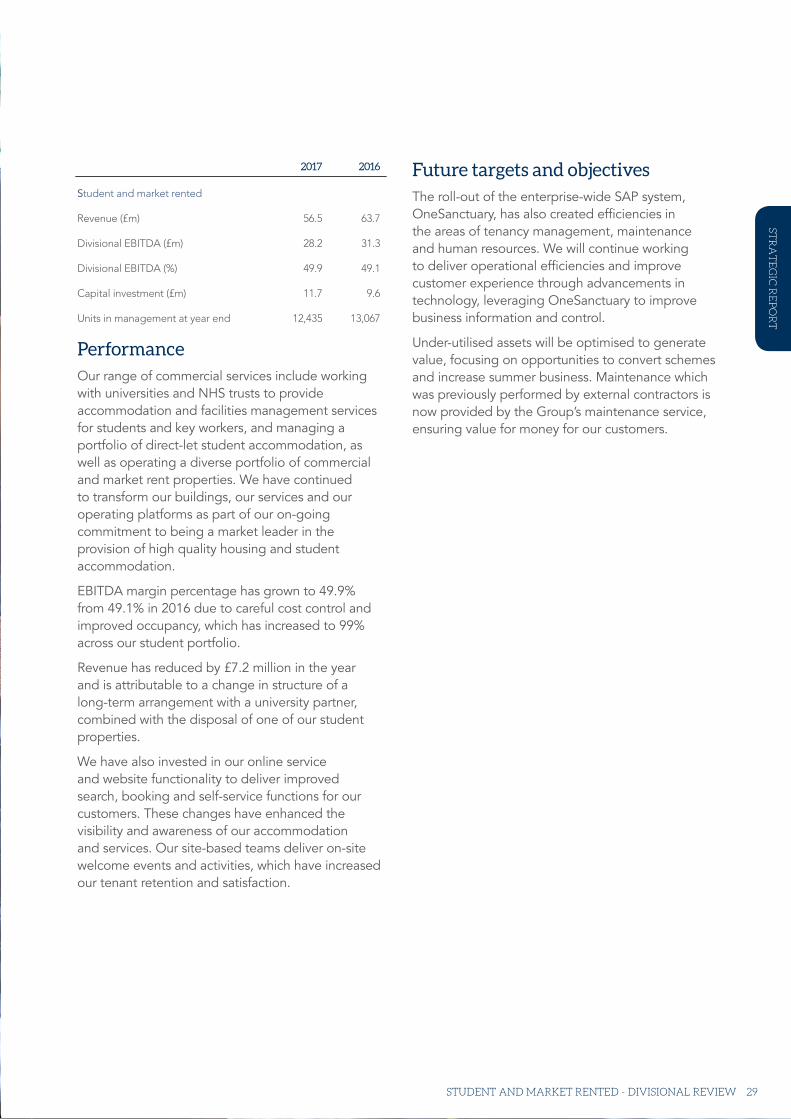

Performance Our range of commercial services include working with universities and NHS trusts to provide accommodation and facilities management services for students and key workers, and managing a portfolio of direct-let student accommodation, as well as operating a diverse portfolio of commercial and market rent properties. We have continued to transform our buildings, our services and our operating platforms as part of our on-going commitment to being a market leader in the provision of high quality housing and student accommodation.

EBITDA margin percentage has grown to 49.9% from 49.1% in 2016 due to careful cost control and improved occupancy, which has increased to 99% across our student portfolio.

Revenue has reduced by £7.2 million in the year and is attributable to a change in structure of a long-term arrangement with a university partner, combined with the disposal of one of our student properties.

We have also invested in our online service and website functionality to deliver improved search, booking and self-service functions for our customers. These changes have enhanced the visibility and awareness of our accommodation and services. Our site-based teams deliver on-site welcome events and activities, which have increased our tenant retention and satisfaction.

Future targets and objectivesThe roll-out of the enterprise-wide SAP system, OneSanctuary, has also created efficiencies in the areas of tenancy management, maintenance and human resources. We will continue working to deliver operational efficiencies and improve customer experience through advancements in technology, leveraging OneSanctuary to improve business information and control.

Under-utilised assets will be optimised to generate value, focusing on opportunities to convert schemes and increase summer business. Maintenance which was previously performed by external contractors is now provided by the Group’s maintenance service, ensuring value for money for our customers.

2017 2016

Student and market rented

Revenue (£m) 56.5 63.7

Divisional EBITDA (£m) 28.2 31.3

Divisional EBITDA (%) 49.9 49.1

Capital investment (£m) 11.7 9.6

Units in management at year end 12,435 13,067

STR

AT

EG

IC R

EP

OR

T

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201730

BUSINESS REVIEW Development – divisional review

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201730

Strategic report Financial statem

ents

31DEVELOPMENT - DIVISIONAL REVIEW 31

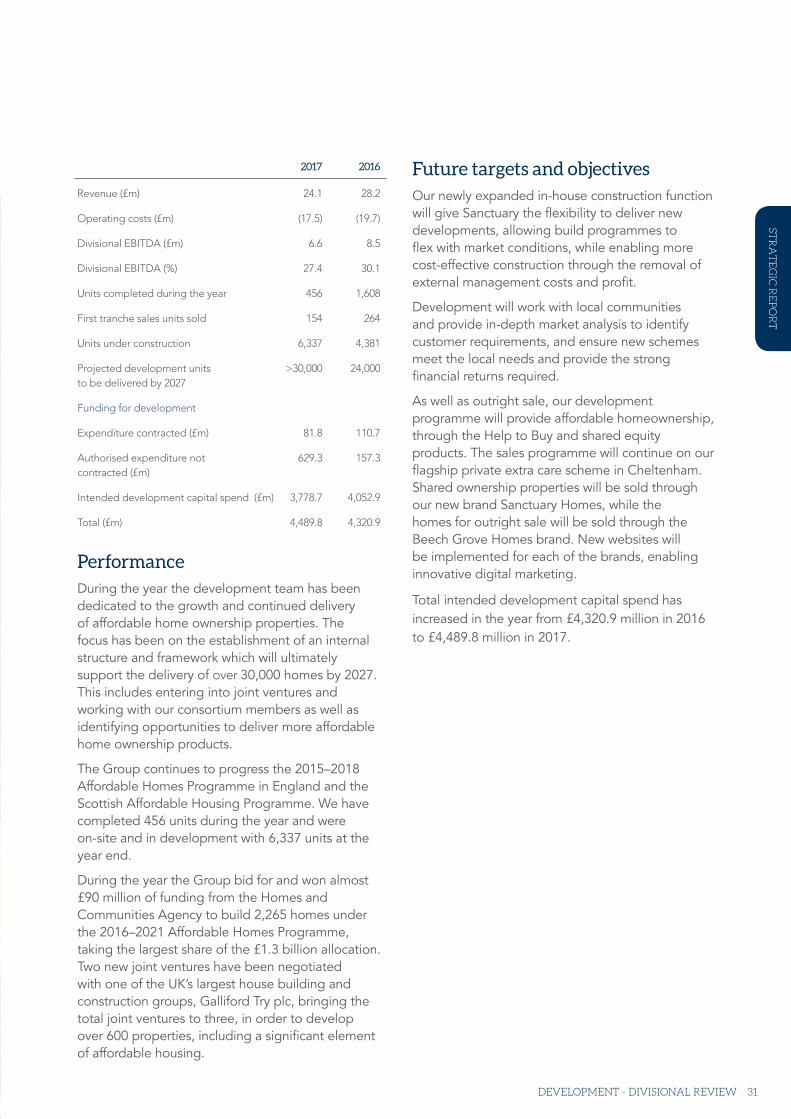

Performance During the year the development team has been dedicated to the growth and continued delivery of affordable home ownership properties. The focus has been on the establishment of an internal structure and framework which will ultimately support the delivery of over 30,000 homes by 2027. This includes entering into joint ventures and working with our consortium members as well as identifying opportunities to deliver more affordable home ownership products.

The Group continues to progress the 2015–2018 Affordable Homes Programme in England and the Scottish Affordable Housing Programme. We have completed 456 units during the year and were on-site and in development with 6,337 units at the year end.

During the year the Group bid for and won almost £90 million of funding from the Homes and Communities Agency to build 2,265 homes under the 2016–2021 Affordable Homes Programme, taking the largest share of the £1.3 billion allocation. Two new joint ventures have been negotiated with one of the UK’s largest house building and construction groups, Galliford Try plc, bringing the total joint ventures to three, in order to develop over 600 properties, including a significant element of affordable housing.

Future targets and objectivesOur newly expanded in-house construction function will give Sanctuary the flexibility to deliver new developments, allowing build programmes to flex with market conditions, while enabling more cost-effective construction through the removal of external management costs and profit.

Development will work with local communities and provide in-depth market analysis to identify customer requirements, and ensure new schemes meet the local needs and provide the strong financial returns required.

As well as outright sale, our development programme will provide affordable homeownership, through the Help to Buy and shared equity products. The sales programme will continue on our flagship private extra care scheme in Cheltenham. Shared ownership properties will be sold through our new brand Sanctuary Homes, while the homes for outright sale will be sold through the Beech Grove Homes brand. New websites will be implemented for each of the brands, enabling innovative digital marketing.

Total intended development capital spend has increased in the year from £4,320.9 million in 2016 to £4,489.8 million in 2017.

2017 2016

Revenue (£m) 24.1 28.2

Operating costs (£m) (17.5) (19.7)

Divisional EBITDA (£m) 6.6 8.5

Divisional EBITDA (%) 27.4 30.1

Units completed during the year 456 1,608

First tranche sales units sold 154 264

Units under construction 6,337 4,381

Projected development units >30,000 24,000 to be delivered by 2027

Funding for development

Expenditure contracted (£m) 81.8 110.7

Authorised expenditure not 629.3 157.3 contracted (£m)

Intended development capital spend (£m) 3,778.7 4,052.9

Total (£m) 4,489.8 4,320.9

STR

AT

EG

IC R

EP

OR

T

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201732

GROUP BOARD

Jonathan Lander BSc (Hons), FCA

1

Robert McComb MSc

3

Liz Meek CBE, BA (Hons)

4

David Bennett CBE, FCA, CCMI

2

Sanctuary has a group structure, in which Sanctuary Housing Association (the Association) is the parent company. The Association was established on 5 May 1969 and is a Registered Society. The Group is governed by the Board of the Association (the Board) which comprises up to seven non-executive members, the Group Chief Executive, and up to three co-opted members.

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201732

Elwyn Roberts MA, FCA

5

Strategic report Financial statem

ents

33

The role of the Group BoardThe Board’s primary role is to define strategy and ensure compliance with the Group’s values and objectives. It agrees the strategic direction of the organisation and makes sure that policies and plans are in place to achieve those objectives. It also establishes and oversees a framework of delegation and systems of control, ensuring that good governance practices are embedded across the Group operations.

Craig Moule BSc (Hons)

9

Dr GarethTuckwell Dip. Pall. Med (Univ of Wales), MRCGP

7

Thelma Stober BA (Hons) Law, CEDR Accredited Mediator

6Denise Plumpton BSc (Hons), CERTIoD

8

Elwyn Roberts MA, FCA

5

GROUP BOARD 33

GO

VE

RN

AN

CE

5

34 ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/2017

Jonathan Lander BSc (Hons), FCA Group Chair, Chair of Nominations Committee and Chair of Succession Planning CommitteeJonathan Lander retired as a senior partner at PricewaterhouseCoopers LLP (PwC) in 2008, having been with the organisation for over 30 years. At PwC Jonathan was lead assurance engagement partner to public companies, large private and private equity backed companies and businesses with overseas ownership, as well as being a Midlands Leadership team member responsible for strategy, marketing, communications and business development.

1

David Bennett CBE, FCA, CCMI Group Chief ExecutiveDavid Bennett is a chartered accountant and has extensive experience in the housing association sector. He has been the Group Chief Executive of Sanctuary since 1992. Prior to joining Sanctuary in 1990, he held senior finance positions in the commercial sector. David was appointed Commander of the Order of the British Empire (CBE) in 2015 for services to social housing.

2

Robert McComb MSc Group Vice Chair and Chair of Remuneration CommitteeRobert McComb is a retired investment banker with experience in treasury, structured and asset finance, and debt capital markets. Prior to retiring from Dresdner Kleinwort in 2007, Robert was treasurer of the bank’s $36 billion structured credit fund, issuing bonds to investors worldwide. He was a senior member of the bank’s structured finance group, with specific responsibility for structured finance in France.

Since retiring, Robert has been a non-executive chair of a venture capital funded hospitality business and a board member of a small north London housing association. He continues to take a close interest in the financial markets.

3

Liz Meek CBE, BA (Hons) Chair of Group Housing Committee Liz Meek is chair of Twining Enterprise, a provider of employment support for people with mental health problems, and a trustee of a London think-tank – the Centre for London. She is also involved with work to improve services for people with schizophrenia and for ex-offenders.

Until 31 March 2011, Liz was Regional Director at the Government office for the North West based in Manchester and Liverpool with responsibility for delivering projects and programmes for 11 Whitehall departments. Her long civil service career has involved specialisation in urban regeneration, combating social exclusion and worklessness, as well as housing association policy and the delivery of European funding streams.

4

Elwyn Roberts MA, FCA Chair of Group Audit and Risk Committee Elwyn Roberts is an engineering graduate and qualified as a Chartered Accountant with Deloitte Haskins and Sells in Cardiff. He became a partner in the audit and assurance business of PwC in 1990 and retired from the organisation in December 2011.

While at PwC, Elwyn was involved in developing the firm’s housing association portfolio in Wales and the South West. He also advised a range of organisations in the charity sector, including the Aberfan Disaster Fund, and was appointed to the Charity Commission’s national working party for the development of the 2000 SORP (accounting guidance for charities) in 1999.

During his time with PwC in Birmingham, Elwyn was responsible for developing and leading the firm’s Risk Assurance practice in the Midlands. Focusing on governance, risk and control, he advised clients in both the private and public sector on corporate governance and risk management.

5

Strategic report Financial statem

ents

35GROUP BOARD

Thelma Stober BA (Hons) Law, CEDR Accredited Mediator Thelma Stober is a Senior Public Sector Solicitor and Mediator. She is currently the Corporate Legal Adviser to the Local Government Association and its associated companies, where she delivers legal advice and company secretarial support on all aspects of law relating to public, administrative, constitutional, company, commercial, local Government and corporate governance. Thelma is also a Lay Member of Herts Valley Clinical Commissioning Group and chair of its Primary Care Co-Commissioning Committee.

Prior to her present role, Thelma was Director of Corporate Law and Governance and Board Secretary at the Equality and Human Rights Commission and, before that, Director of Legal and Procurement and Monitoring Officer at the Greater London Authority and the London Development Agency.

6

Dr Gareth Tuckwell Dip. Pall. Med (Univ of Wales), MRCGP

Gareth Tuckwell brings many years of experience in clinical leadership, care delivery and clinical governance to the Group. Gareth was Chief Executive Officer of Burrswood Hospital, Kent, from 2007 for a five-year term, Clinical Director of Hospice in the Weald from 2003 to 2007, and Regional Director of Macmillan Cancer Support from 2000 to 2003.

Gareth was a Trustee of Macmillan Cancer Support from 2003 to 2013 and a Trustee and subsequently chairman of Friends of Vellore (UK) from 2011 to 2016. Gareth was also Medical Director of Burrswood Hospital from 1986 to 1999.

He is a Vice-President of Phyllis Tuckwell Hospice Care and, from 2017, is Chair of The M.E. Trust.

Denise Plumpton BSc (Hons), CERTIoDDenise Plumpton is currently Vice-Chair at Birmingham South Central Clinical Commissioning Group and a Non-Executive Advisor to Centro (Network West Midlands) for their Smart Ticketing Programme. Denise is also an active member of the Greater Birmingham Chamber of Commerce.

Since 2010 Denise has worked as an Independent Strategic Consultant advising and directing companies to improve their performance, in particular focusing on developing and delivering strategy, and enhancing customer service and process efficiency. Prior to this, Denise was Director of Information at the Highways Agency; IT Director at Sendo Group; Group IT Director at TNT UK & Ireland; and Chief Information Officer/Director for Powergen Plc.

7

GO

VE

RN

AN

CE

8

Craig Moule BSc (Hons)

Chief Financial Officer and Co-opted Board MemberCraig Moule joined Sanctuary in 1989 from Coopers & Lybrand. He is responsible for finance and resources including financial strategy, treasury and risk, information systems, business information, procurement, asset management, governance and legal services, and the shared service centre.

Craig manages Sanctuary’s relationships with investors, bankers, internal and external auditors, and the rating agencies Standard & Poor’s and Moody’s Investors Service. In addition Craig leads on negotiations of complex commercial deals including raising private finance.

9

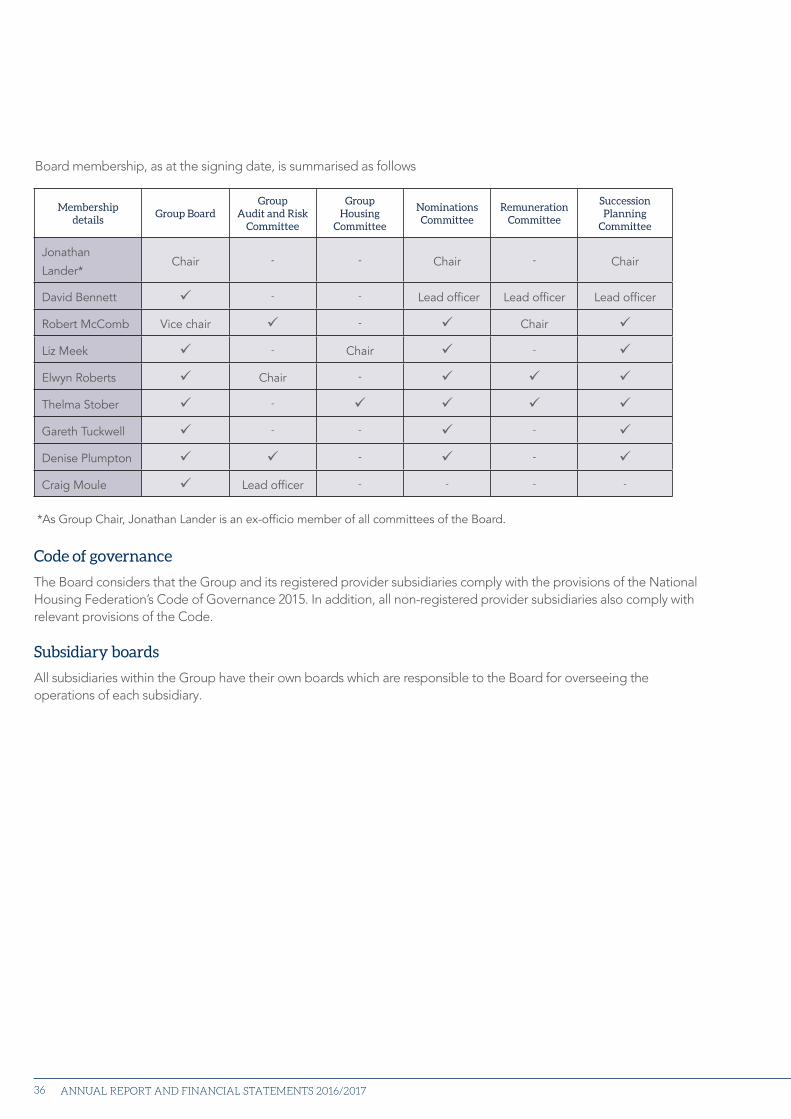

Membership details

Group BoardGroup

Audit and Risk Committee

Group Housing

Committee

Nominations Committee

Remuneration Committee

Succession Planning

Committee

Jonathan

Lander*Chair - - Chair - Chair

David Bennett - - Lead officer Lead officer Lead officer

Robert McComb Vice chair - Chair

Liz Meek - Chair -

Elwyn Roberts Chair -

Thelma Stober -

Gareth Tuckwell - - -

Denise Plumpton - -

Craig Moule Lead officer - - - -

*As Group Chair, Jonathan Lander is an ex-officio member of all committees of the Board.

Board membership, as at the signing date, is summarised as follows

Code of governance

The Board considers that the Group and its registered provider subsidiaries comply with the provisions of the National Housing Federation’s Code of Governance 2015. In addition, all non-registered provider subsidiaries also comply with relevant provisions of the Code.

Subsidiary boards

All subsidiaries within the Group have their own boards which are responsible to the Board for overseeing the operations of each subsidiary.

36 ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/2017

Strategic report Financial statem

ents

37

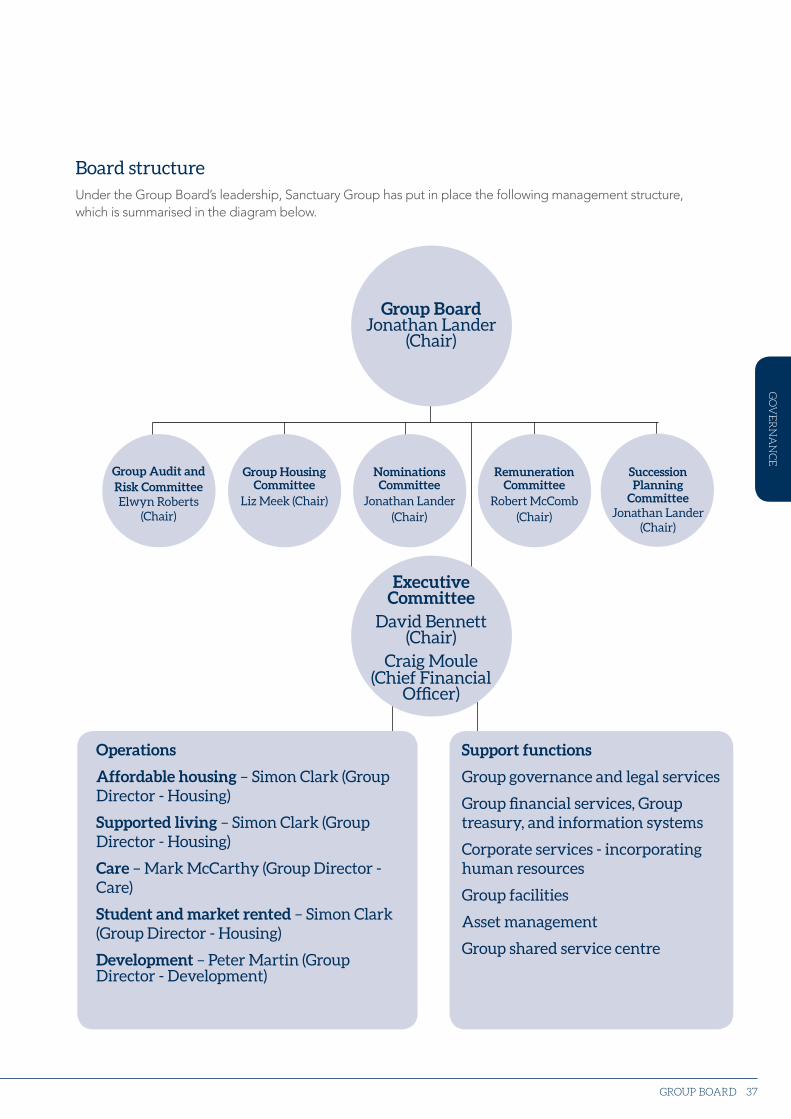

Board structureUnder the Group Board’s leadership, Sanctuary Group has put in place the following management structure, which is summarised in the diagram below.

Operations

Affordable housing – Simon Clark (Group Director - Housing)

Supported living – Simon Clark (Group Director - Housing)

Care – Mark McCarthy (Group Director - Care)

Student and market rented – Simon Clark (Group Director - Housing)

Development – Peter Martin (Group Director - Development)

Support functions

Group governance and legal services

Group financial services, Group treasury, and information systems

Corporate services - incorporating human resources

Group facilities

Asset management

Group shared service centre

Executive Committee

David Bennett (Chair)

Craig Moule (Chief Financial

Officer)

Group Housing Committee

Liz Meek (Chair)

Group Audit and Risk Committee Elwyn Roberts

(Chair)

Nominations Committee

Jonathan Lander (Chair)

Remuneration Committee

Robert McComb (Chair)

Succession Planning

Committee Jonathan Lander

(Chair)

Group Board Jonathan Lander

(Chair)

GROUP BOARD

GO

VE

RN

AN

CE

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201738

STATUTORY, REGULATORY AND OTHER INFORMATION

Executive management

The Board delegates day-to-day management of activities to the Group Chief Executive, David Bennett, who is responsible for ensuring that the organisation has appropriate executive arrangements in place to meet Group objectives and targets, and that those arrangements reflect the complex needs of the business, including financial performance, capital investment, compliance, growth and business planning. To this end the Group has an Executive Committee, chaired by David Bennett, which considers and approves strategic matters affecting the Group (either implementation of strategy direction by the Board or determination of recommendations to the Board); and a Capital Committee, also chaired by David Bennett, which is responsible for monitoring performance and approving capital projects in furtherance of the Group Business Plan agreed by the Group Board.

Audit

KPMG provides external audit services and PwC performs internal audit services. The Group Audit and Risk Committee has approved a policy in relation to the nature of non-audit work undertaken by PwC and KPMG. Where such work is expected to be in excess of a specified amount, the Chair of the Group Audit and Risk Committee must approve the work. Below that amount, the Chief Financial Officer has authority to approve such work once he is satisfied that PwC or KPMG are the most appropriate providers. There is an annual review of the provision of, and fees for, non-audit services as part of the Group Audit and Risk Committee’s review of the services provided by PwC and KPMG.

Group financial statements

The financial statements for the Group consist of the financial results of the Association and its subsidiary undertakings, which have been consolidated in accordance with the relevant financial reporting standards.

Rent

The Group has various different types of social housing tenancies, the rents for which are set in accordance with the regulatory frameworks for social housing in England and Scotland.

Health and safety

It is the clear intention of the Group to ensure, as far as reasonably practicable, the health, safety and welfare at work of all its employees. The Group undertakes to comply, as a minimum, with the provisions of the Health and Safety at Work Act 1974 and other relevant legislation to meet the objective of achieving the highest possible standards.

Political and charitable donations

The Group made no donations to political organisations (2016: none). The Group made donations to charitable organisations of £11,800 (2016: £17,070).

Employee involvement

It is Group policy to involve all employees in matters affecting them. At a formal level this takes place through the Staff Council, where management consult with elected staff representatives. At an operational level, a team briefing system is in place to keep all employees updated on core Group business issues.

Strategic report Financial statem

ents

39

Ethical business

The Group is committed to conducting its business in an ethical and responsible manner. This involves making decisions which take into account not only economic considerations but also social and environmental impacts. It means running Group operations efficiently, investing in the communities where the Group works, providing training and employment opportunities, and ensuring that Group operations are run in an environmentally-friendly manner.

Slavery and human trafficking statement

The Group is committed to achieving greater clarity and understanding of our supply chains in order to seek out and deal with any evidence of slavery and human trafficking. The Group recognises that no supply chain can be considered entirely free from the potential for slavery or human trafficking to occur and we are endeavouring to take further steps to understand high risk areas, communicate our approach and take positive action. The Group’s full statement can be found on the Group website at https://www.sanctuary-group.co.uk.

Equality and diversity

The Group aims to be an open and inclusive organisation, where diversity is promoted and discrimination eliminated. Our single equality scheme – ‘Fairness for All’ – outlines the commitment to ensuring that our services and operations meet the needs of all customers. It ensures that equality, diversity and human rights are integrated into the way the Group plans, develops and delivers services, covering internal functions as an employer and external operations as a provider of housing, care and commercial services. The Group operates an Equality and Diversity Working Group, which ensures that the requirements set out by the scheme are embedded across the Group’s operations. The Working Group is chaired by Nathan Warren, Group Director - Commercial.

Directors’ and Officers’ liability insurance

The Group has maintained Directors’ and Officers’ liability insurance throughout the year and up to the date of approval of the financial statements.

Events after the reporting period

On 19 June 2017 the Association purchased 100 per cent of the ordinary share capital of Embrace Care Ltd (Embrace), the parent of a group of companies that own and manage 35 care homes and a supported living scheme. The acquisition enables the Group to further fulfil its charitable objectives of providing housing and care services to those who need it. The locations of Embrace’s homes, which are in Scotland and the North of England, allow the Group to expand its care offering into a wider geographical area. This transaction will be treated as a business combination under IFRS 3 and full details of the financial effects will be included in the next set of financial statements.

STATUTORY, REGULATORY AND OTHER INFORMATION

GO

VE

RN

AN

CE

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201740

The Board is ultimately responsible for ensuring that the Group maintains a system of internal control that is appropriate to the various business environments in which it operates. Internal control systems are designed to meet the particular needs of the Group and the risks to which it is exposed. The controls by their nature can provide reasonable but not absolute assurance against material misstatement or loss.

The Board has established key procedures to provide internal control and there are clear lines of responsibility for the creation and maintenance of the procedures through the Executive Committee of the Group. These controls are designed to give reasonable assurance with respect to:

• the reliability of financial information used within the Group or for publication;

• the maintenance of proper accounting records; and

• the safeguarding of assets against unauthorised use or disposition.

Major business risks are identified through a system of continuous monitoring. The financial control framework includes the following key features:

• The Board being directly responsible for strategic risk management.

• The adoption of formal policies and procedures including documentation of key systems and rules relating to a delegation of authorities which allows the monitoring of controls and restricts the unauthorised use of the Group’s assets.

• Experienced and suitably qualified staff being responsible for important business functions. Annual appraisal procedures have been established to maintain standards of performance.

• Executives to monitor the key business risks and financial objectives allowing the Group to progress towards its financial plans set for the year and the medium-term. Regular management accounts are prepared promptly providing relevant, reliable and up-to-date financial and other information including significant variances from budgets which are investigated as necessary.

• All significant new initiatives, major commitments and investment projects are subject to formal authorisation procedures.

• The Group Audit and Risk Committee reviews reports from management, PwC (internal auditors) and KPMG (external auditors) to provide reasonable assurance that control procedures are in place and are being followed. The Group Audit and Risk Committee receives an annual report on internal controls from the Executive Directors. The Group Audit and Risk Committee makes regular reports to the Board. The Group follows formal procedures for instituting appropriate action to correct weaknesses identified in the above reporting.

During the year the Group migrated its housing, assets and maintenance systems to SAP, the Group’s new information technology system, known internally as OneSanctuary. The Group Board and Group Audit and Risk Committee are satisfied that since the transfers the system of internal control is appropriate to the various business environments in which it operates.

On behalf of the Board, the Group Audit and Risk Committee has reviewed the effectiveness of the systems of internal control in existence in the Group for the year ended 31 March 2017 and is not aware of any material changes at the date of signing the financial statements.

INTERNAL CONTROLS

Strategic report Financial statem

ents

41

Arrangements for managing the risk of fraud

The Group has robust arrangements in place for managing the risks of fraud. These include:

• prevention – the Group seeks to generate a strong anti-fraud culture supported by appropriate controls over operational and employment systems.

• detection – the Group has implemented comprehensive systems and procedures to detect evidence of fraud and to facilitate and encourage the reporting of fraud.

• investigation – the Group follows a comprehensive Group policy on fraud investigation and reporting.

• insurance – the Group has appropriate insurance cover in place to mitigate the potential financial losses associated with fraud.

Going concern

The Board has a reasonable expectation that the Group has adequate resources to continue in operational existence for a period of at least 12 months. Accordingly, it continues to adopt the going concern basis in preparing the Group and Association’s financial statements.

INTERNAL CONTROLS

GO

VE

RN

AN

CE

ANNUAL REPORT AND FINANCIAL STATEMENTS 2016/201742

VIABILITY STATEMENT

During the year the Board has assessed the viability of the Group over a four-year period. This assessment has been made through the business planning process which takes account of both the Group’s current position and its principal risks, which are detailed on pages 43 to 45.

The Board has determined that a four-year period is an appropriate period over which to provide its viability statement. While the Board believes that the Group will be viable over a much longer period, as demonstrated by the thirty-year forecast that is performed annually, a four-year period has been chosen as it has a much greater degree of certainty and provides an appropriate longer-term outlook.

The business planning process includes the Group’s most recent budgets, operational plans and a review of external factors. The operational plans provide long-term direction and are reviewed on at least an annual basis. The base strategy is tested through rigorous sensitivity analysis and stress testing using a series of robust downside financial scenarios which result in a financial impact. The testing also identifies the principal risks that may adversely impact the Group which include operational, political, business, liquidity, market and credit risk. The results of the testing ensure potential mitigating actions are appropriately developed.

Due to the inherent uncertainty involved in all business planning, it is not possible for the review to consider every risk that the Group may face. However, the Board considers that the stress testing performed includes all known risks and therefore provides strong assurance of the Group’s financial viability. These risks include the expected impact of welfare reform on our tenants, further reductions in social rents and uncertainty around Brexit, as discussed in the Group Chair’s Statement on page 4.

Also key is the maintenance of a Group-wide assets and liabilities register and risk management processes that flow through to all of the Group’s subsidiaries and operations.

The Board has therefore concluded, based on the extent of the business planning process and strong financial position, that there is a reasonable expectation the Group and the Association have adequate resources and will continue to operate and meet their liabilities as they fall due over the period of their assessment.

The Board can also confirm that it has complied with the Governance and Financial Viability Standard set out by the Homes and Communities Agency.

During the year the Homes and Communities Agency confirmed the G1 and V1 governance and financial viability ratings.

Strategic report Financial statem

ents

43

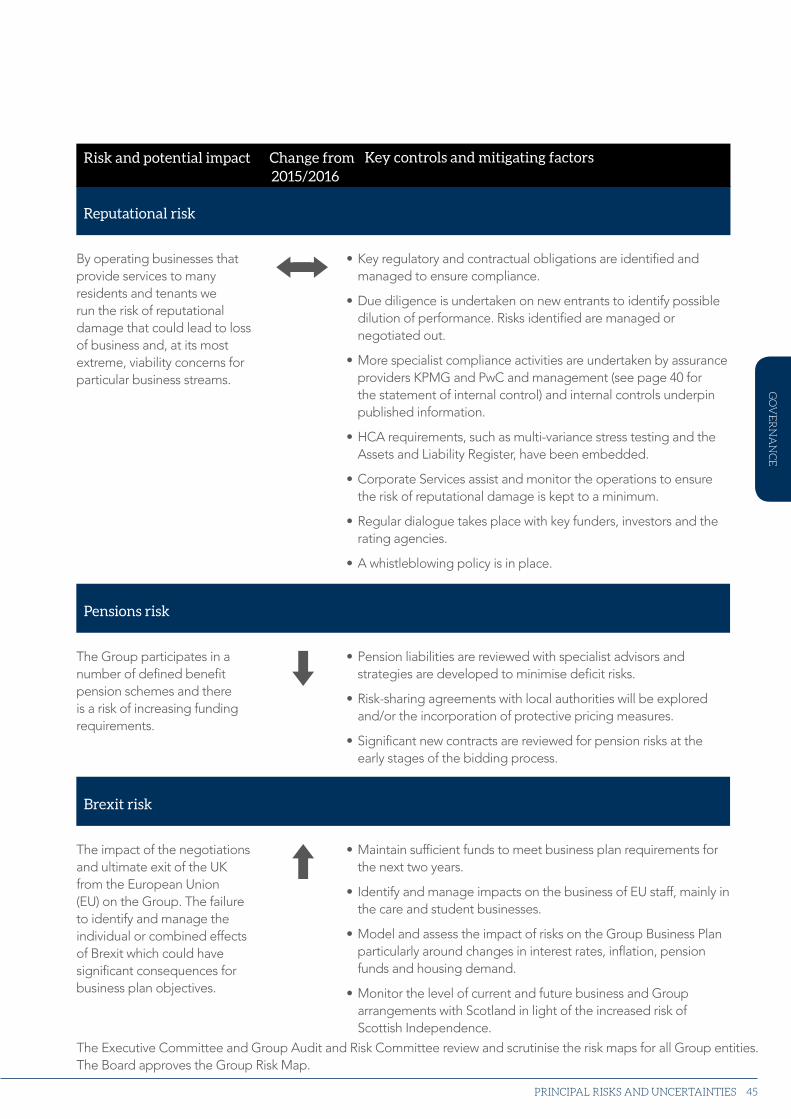

PRINCIPAL RISKS AND UNCERTAINTIES

The Group operates a comprehensive risk mapping process as part of its annual business planning cycle, which is monitored at each Board meeting. Furthermore, each report provided at Group and subsidiary board meetings must reference the relevant risks addressed on the appropriate risk map.

The principal risks affecting the Group are set out below, along with their movement in the year and examples of key controls and mitigating factors.

Risk and potential impact Change from Key controls and mitigating factors

Government policy, legislation and regulation

Failure to comply with or react to regulations and Government announcements, for example around welfare reform and rent reduction, leading to reputation damage and financial impacts such as cash flow deterioration.

• Income services support to our tenants has been increased.

• Joint working with Government agencies and participation in a pilot to assess the impact of welfare changes.

• Number of self-funders in our care homes to increase to mitigate the New Living Wage cost pressures.

• Updated financial projections have been prepared incorporating a revised growth strategy.

Funding and financial viability

Gearing constraints can limit the Group’s capacity for further borrowing.

Downgrades to the sector’s credit ratings may increase the cost of future borrowing.

Failure to obtain funding could undermine the Group’s long-term growth plans.

• The Group retains high credit quality and ratings enabling access to financial markets. The Group provides regulators with key treasury reports, long-term business plans and sensitivity scenarios.

• Quarterly financial updates for lenders are published on our website and relationships with existing and potential funders are maintained to promote our activities and identify further funding sources.

• Development programmes have capital requirement limits and commitments are monitored against total liquidity.

• Committed developments are forward-funded via bond issues and bank facilities.

• Available funding in place including shorter-term Revolving Credit Facilities to manage a more variable cash flow requirement for the 30,000 plus unit development plan to 2027.

• Longer-term projections and multi-variance stress testing are updated regularly.

• Unencumbered assets are monitored on a continual programme to support future funding requirements.

• Cash flows, covenant compliance and future funding requirements are monitored, incorporating multi-variant sensitivity analyses to assess the impact of cumulating risks.

• Annual funding strategy is approved by the Group Board at the same time as long-term projections are updated.

2015/2016