angel investing through equity crowdfunding websites (series: equity crowdfunding)

TRANSCRIPT

Angel Investing Through Equity Crowdfunding Websites

EQUITY CROWDFUNDING Premiere Date: February 23, 2017

This webinar is sponsored by: EisnerAmper

1

2

3

4

MODERATOR Christopher Cahill Lowis & Gellen LLP

PANELISTS Lynda Davey Avalon Securities Ltd. Swati Chaturvedi Propel (x) Richard Swart Next Gen Crowdfunding

MEET THE FACULTY

6

SERIES SPONSOR

7

ABOUT THIS WEBINAR

This webinar explores how angel inves8ng is dis8nct from other early-‐stage inves8ng, how an array of crowdfunding websites helps iden8fy opportuni8es to invest, and how they facilitate such inves8ng.

The panel also examines the phenomenon of online syndica8on and the impact it has had on the landscapes of angel inves8ng and crowdfunding.

8

ABOUT THIS SERIES This webinar series explores the purchase of ownership shares in private companies via crowdfunding websites. "Crowdfunding" for this series refers both to investments made in this way by accredited investors -‐-‐ given greater scope by Title II of the 2012 JOBS Act -‐-‐ and those made by any investor under Title III of the JOBS Act.

Episodes in the series address the modes of angel inves8ng in a company during its early stages, the opportuni8es and perils of crowdfunding real estate investments, the money-‐raising en8ty's perspec8ve, and a close look at crowdfunding op8ons under federal and state law.

Each episode is delivered in Plain English understandable to business owners and execu8ves without much background in these areas. Yet, each episode is proven to be valuable to seasoned professionals. As with all Financial Poise Webinars, each episode in the series brings you into engaging, some8mes humorous, conversa8ons designed to entertain as it teaches. And, as with all Financial Poise Webinars, each episode in the series is designed to be viewed independently of the other episodes, so that par8cipants will enhance their knowledge of this area whether they aTend one, some, or all of the episodes.

9

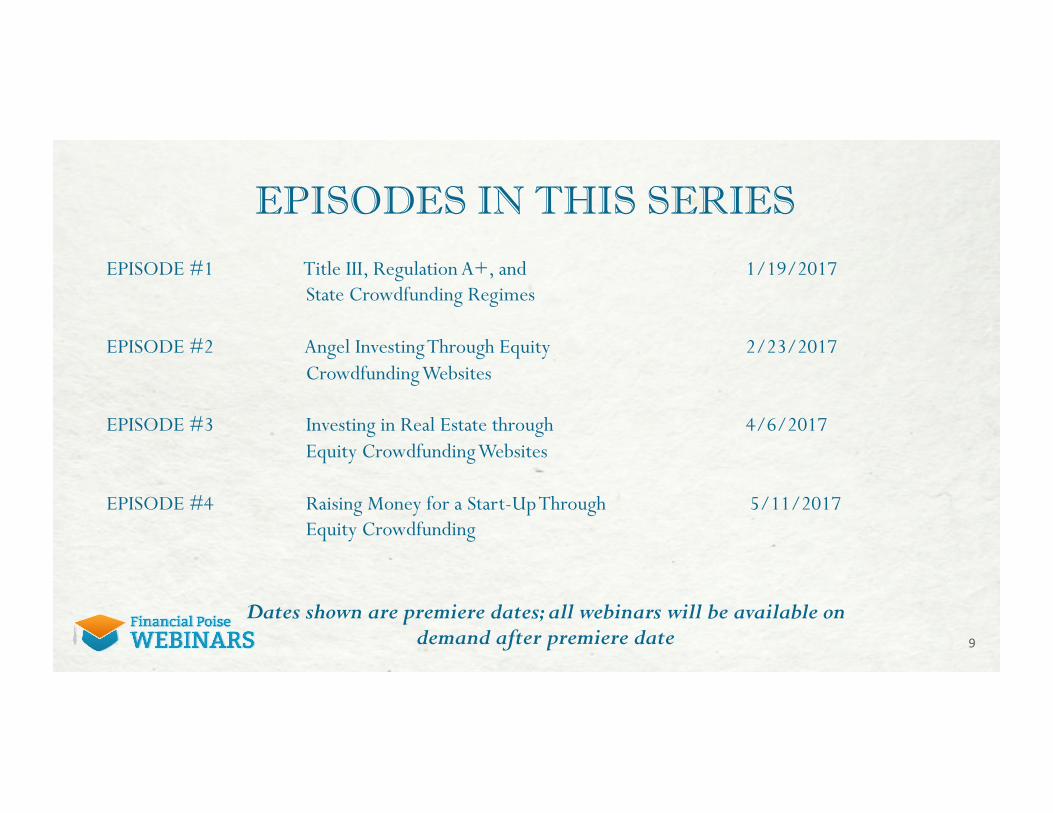

EPISODES IN THIS SERIES

Dates shown are premiere dates; all webinars will be available on demand after premiere date

EPISODE #1 Title III, Regulation A+, and 1/19/2017 State Crowdfunding Regimes

EPISODE #2 Angel Investing Through Equity 2/23/2017 Crowdfunding Websites

EPISODE #3 Investing in Real Estate through 4/6/2017 Equity Crowdfunding Websites

EPISODE #4 Raising Money for a Start-Up Through 5/11/2017 Equity Crowdfunding

EARLY FUNDERS – ANGELS AND NON-ANGELS

• Friends and Family • Angel Investors • Venture Capital • Regulation D offerings (Rules 506b and 506c) • Regulation CF crowdfunding

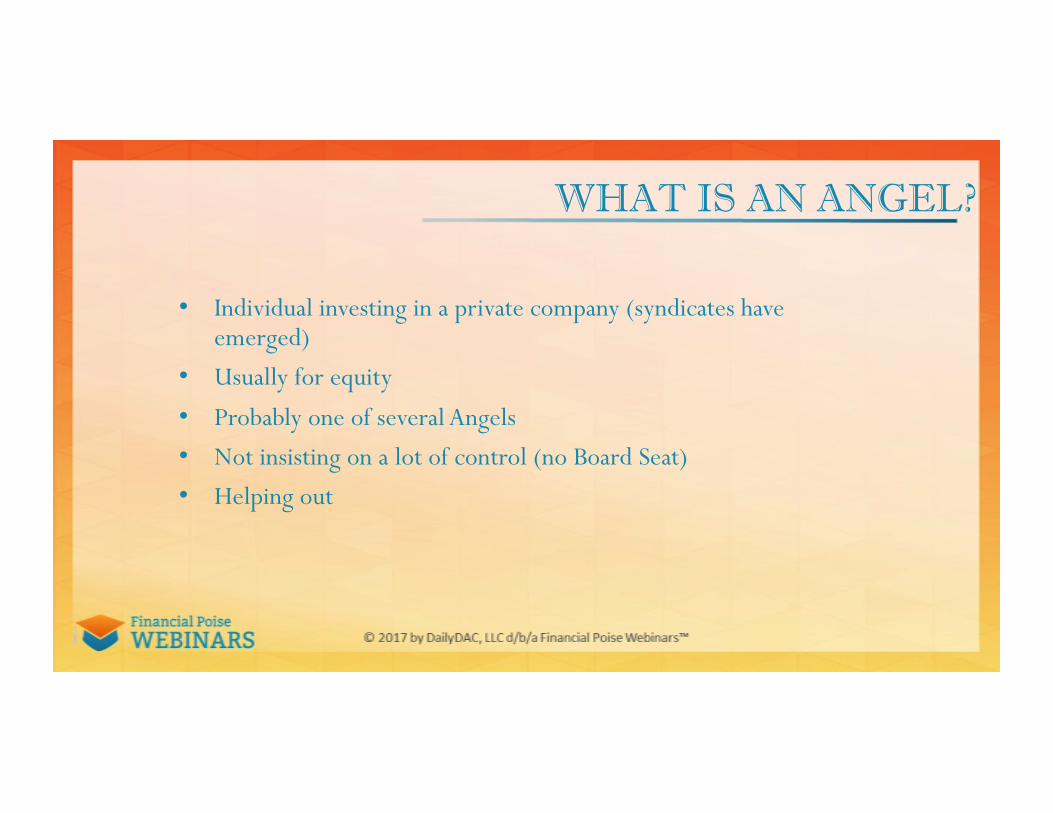

WHAT IS AN ANGEL?

• Individual investing in a private company (syndicates have emerged)

• Usually for equity • Probably one of several Angels • Not insisting on a lot of control (no Board Seat) • Helping out

ANGELS IN THE US - 2015

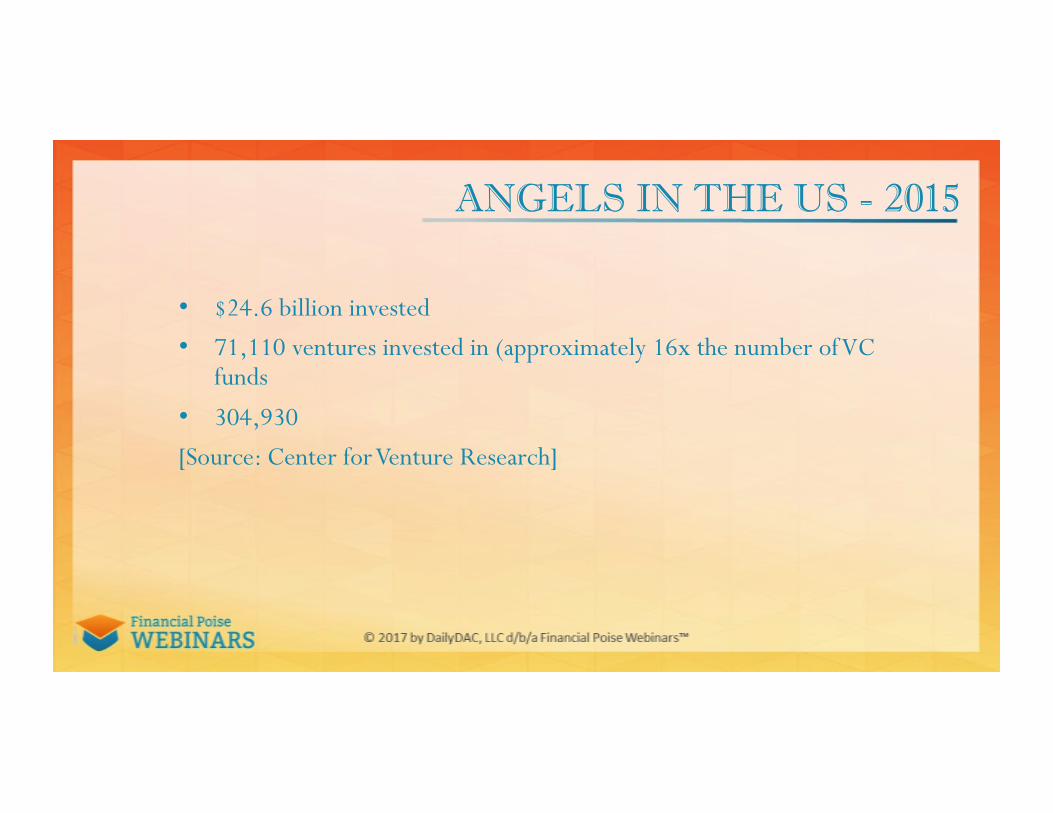

• $24.6 billion invested • 71,110 ventures invested in (approximately 16x the number of VC

funds • 304,930 [Source: Center for Venture Research]

WHAT DO ANGELS WANT?

• High growth and scalability • Thus software and tech, more than manufacturing • A market for the innovation, a moat against future competitors • Payoff (exit) in 5 to 10 years • To build their own brand to gain access to future deals

WHAT ANGELS LOOK FOR IN THE COMPANY

• Tangible assets? None or Few • Financial track record? Likely to be scant or nonexistent • Sales? Some • User or customer base? Existing, presumably growing • Scalable? It had better be, with ROI potential of at least 10x • Founding team: BINGO [per research by Shai Bernstein (Stanford) and Arthur Korteweg (USC)]

OTHER FACTORS RE: PRODUCT OR SERVICE OFFERED BY COMPANY

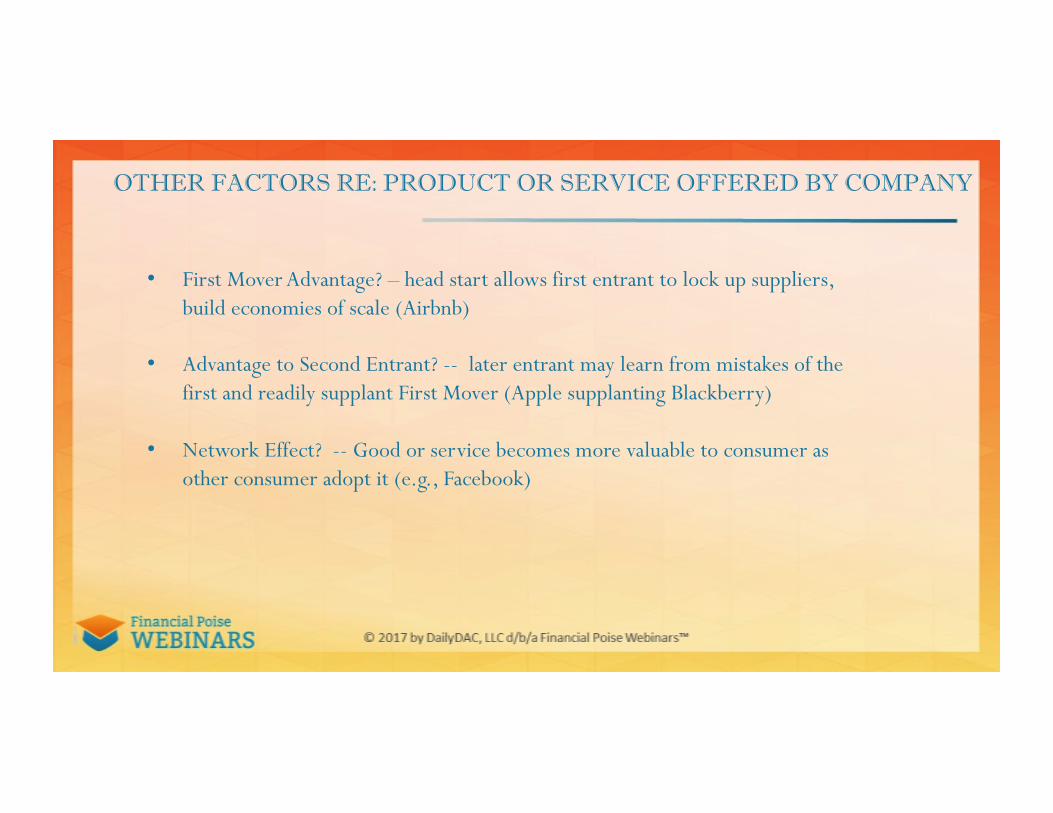

• First Mover Advantage? – head start allows first entrant to lock up suppliers, build economies of scale (Airbnb)

• Advantage to Second Entrant? -- later entrant may learn from mistakes of the first and readily supplant First Mover (Apple supplanting Blackberry)

• Network Effect? -- Good or service becomes more valuable to consumer as other consumer adopt it (e.g., Facebook)

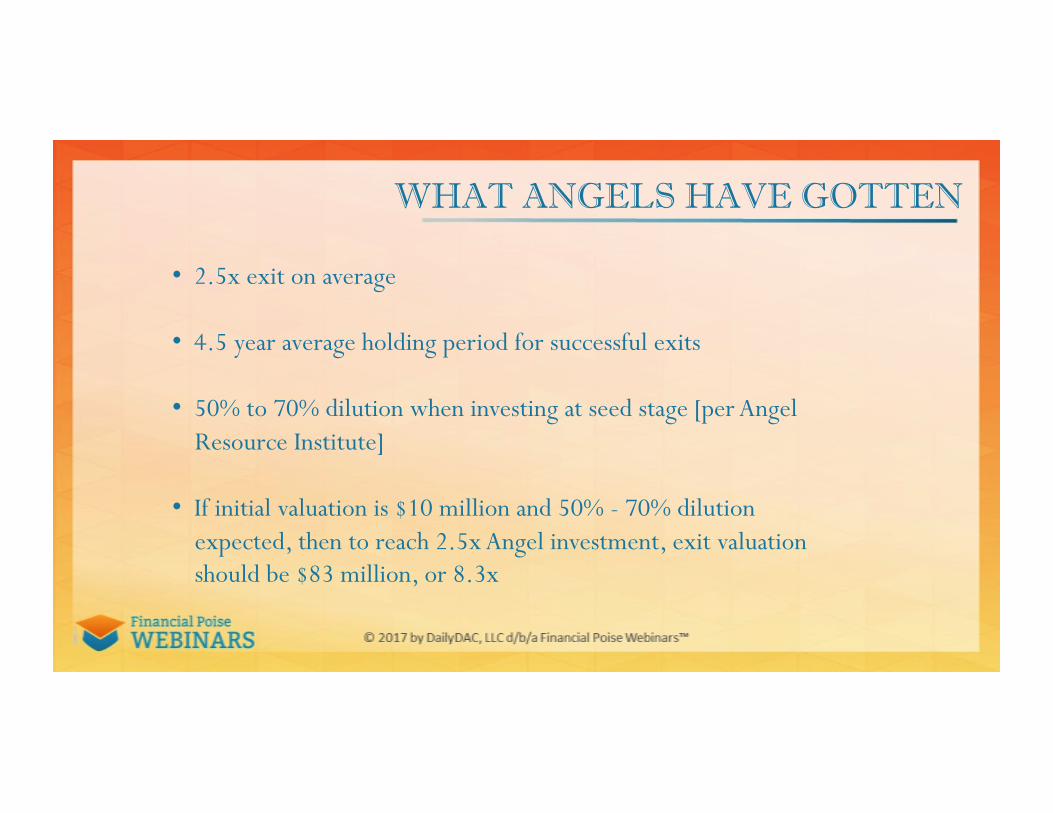

WHAT ANGELS HAVE GOTTEN

• 2.5x exit on average

• 4.5 year average holding period for successful exits

• 50% to 70% dilution when investing at seed stage [per Angel Resource Institute]

• If initial valuation is $10 million and 50% - 70% dilution expected, then to reach 2.5x Angel investment, exit valuation should be $83 million, or 8.3x

ANGEL BATTING AVERAGE

• Lower than baseball batting averages • Many losers, but high returns from winners • Likely need for future investments rounds • Angels diversify their bets, and bet with funds they can afford to

lose

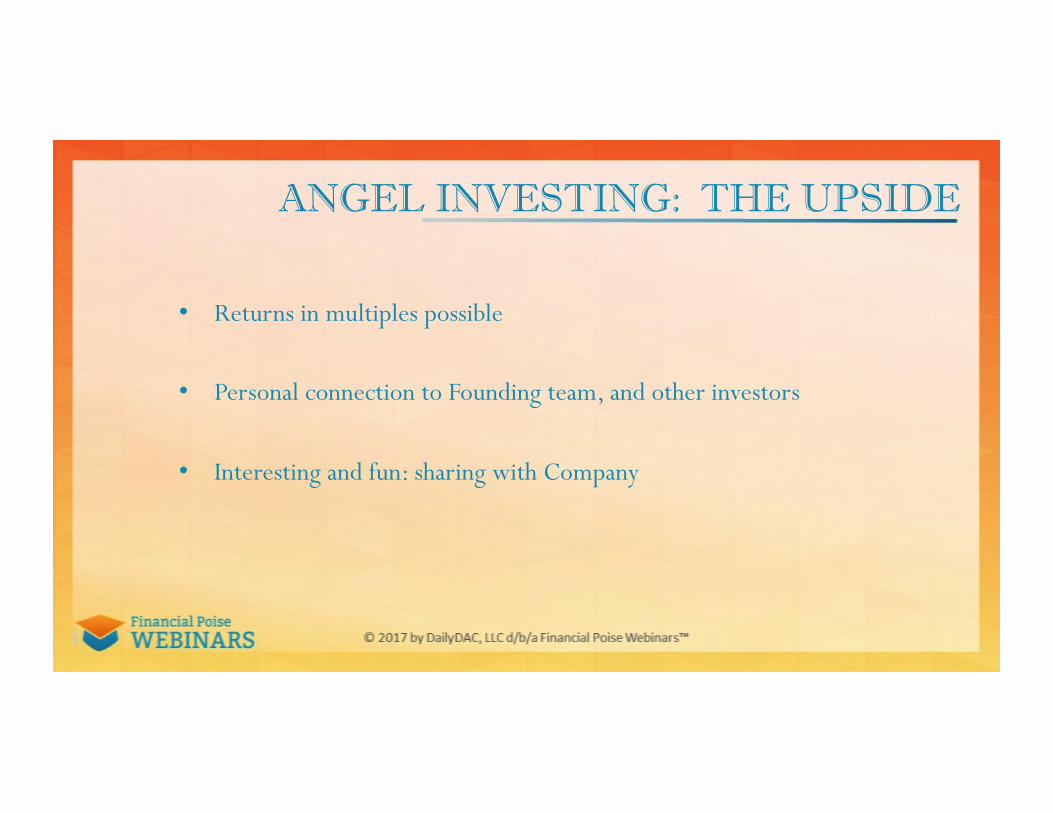

ANGEL INVESTING: THE UPSIDE

• Returns in multiples possible

• Personal connection to Founding team, and other investors

• Interesting and fun: sharing with Company

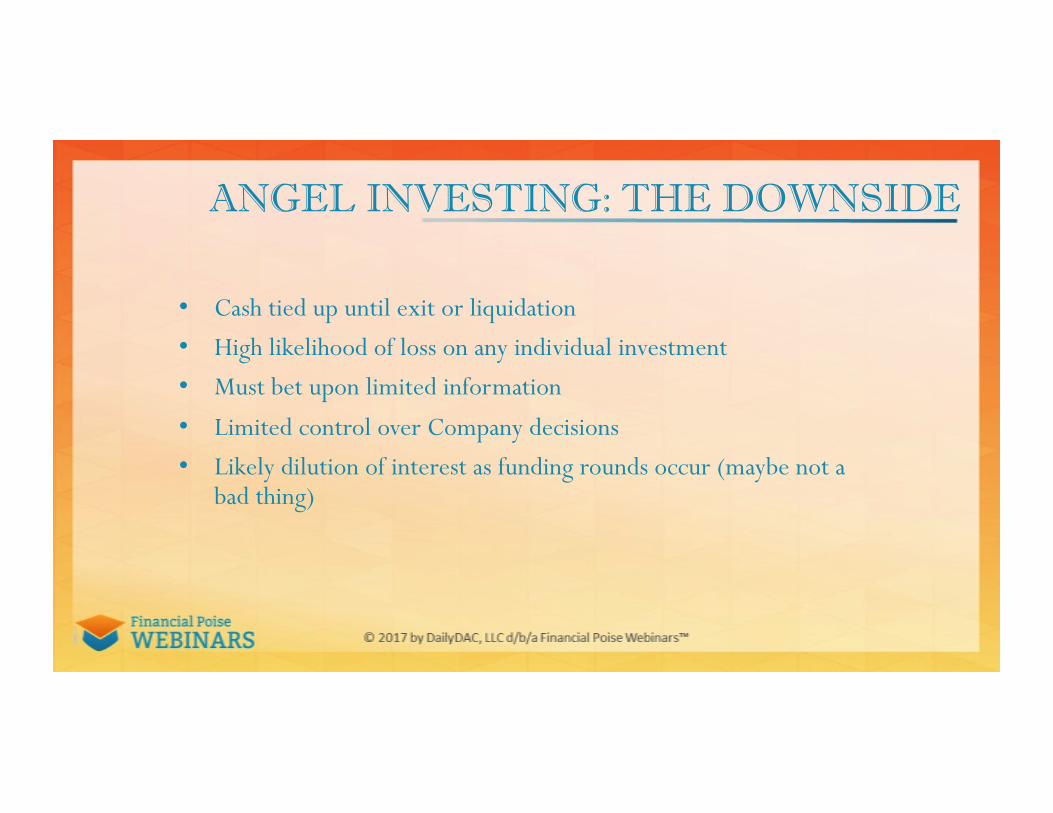

ANGEL INVESTING: THE DOWNSIDE

• Cash tied up until exit or liquidation • High likelihood of loss on any individual investment • Must bet upon limited information • Limited control over Company decisions • Likely dilution of interest as funding rounds occur (maybe not a

bad thing)

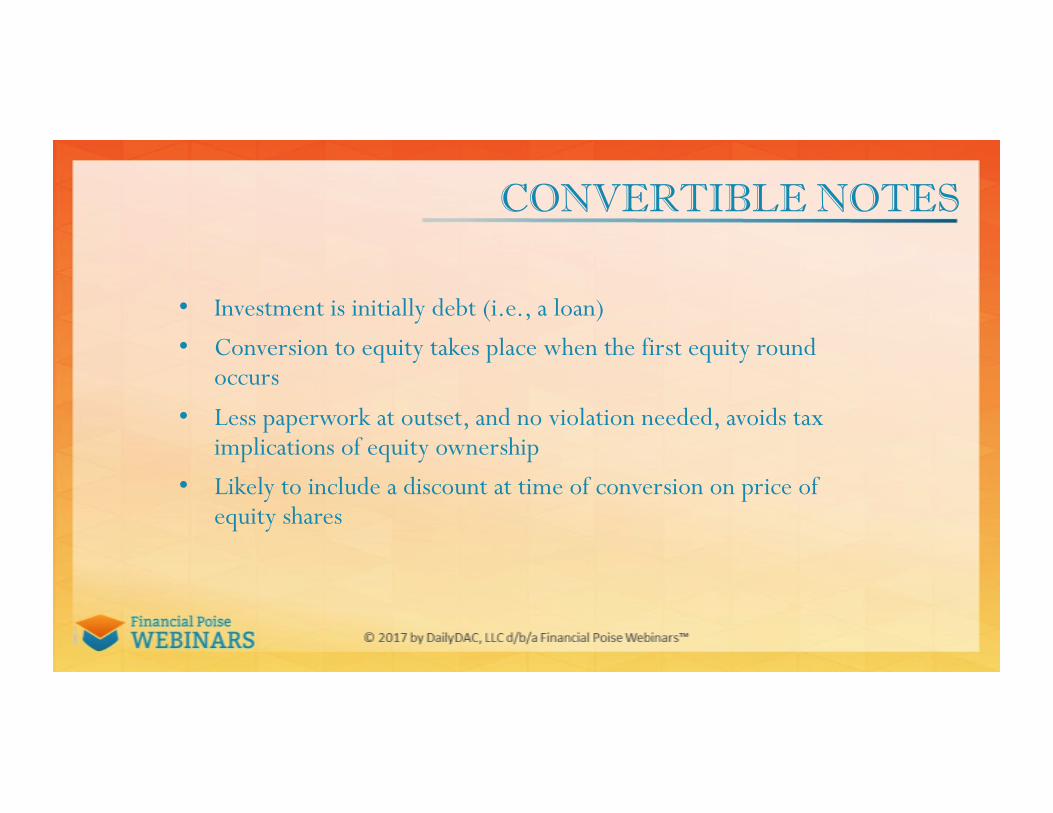

CONVERTIBLE NOTES

• Investment is initially debt (i.e., a loan) • Conversion to equity takes place when the first equity round

occurs • Less paperwork at outset, and no violation needed, avoids tax

implications of equity ownership • Likely to include a discount at time of conversion on price of

equity shares

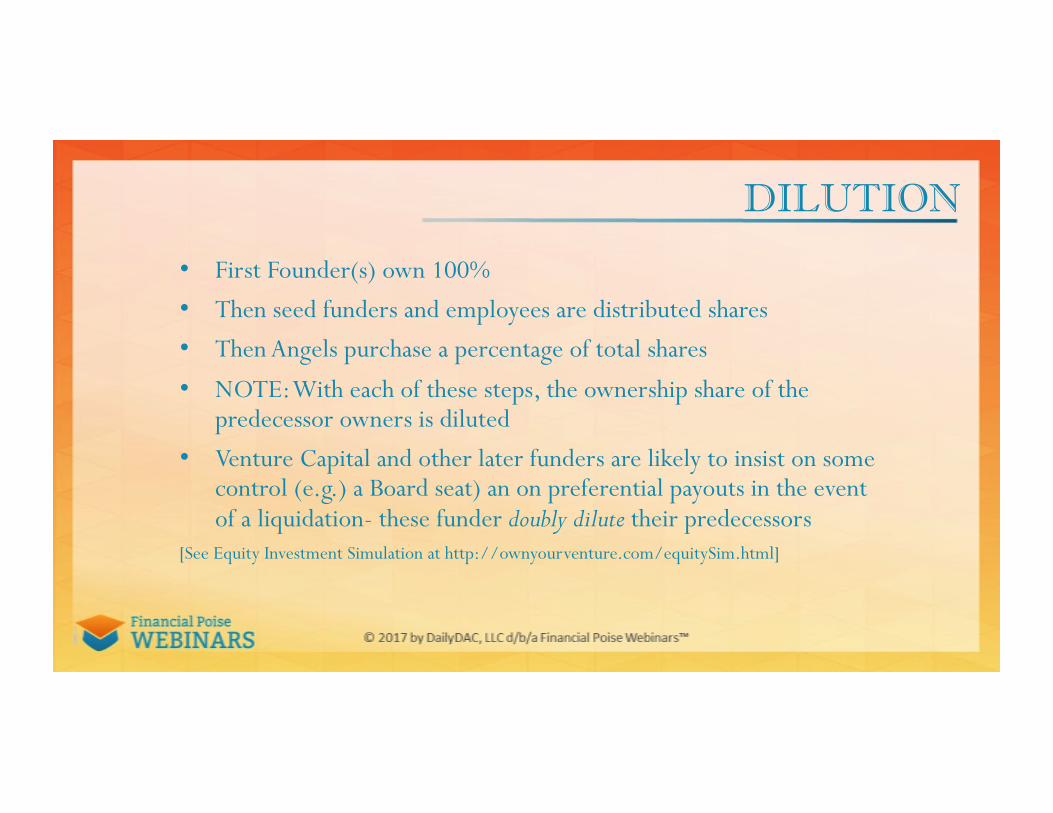

DILUTION

• First Founder(s) own 100% • Then seed funders and employees are distributed shares • Then Angels purchase a percentage of total shares • NOTE: With each of these steps, the ownership share of the

predecessor owners is diluted • Venture Capital and other later funders are likely to insist on some

control (e.g.) a Board seat) an on preferential payouts in the event of a liquidation- these funder doubly dilute their predecessors

[See Equity Investment Simulation at http://ownyourventure.com/equitySim.html]

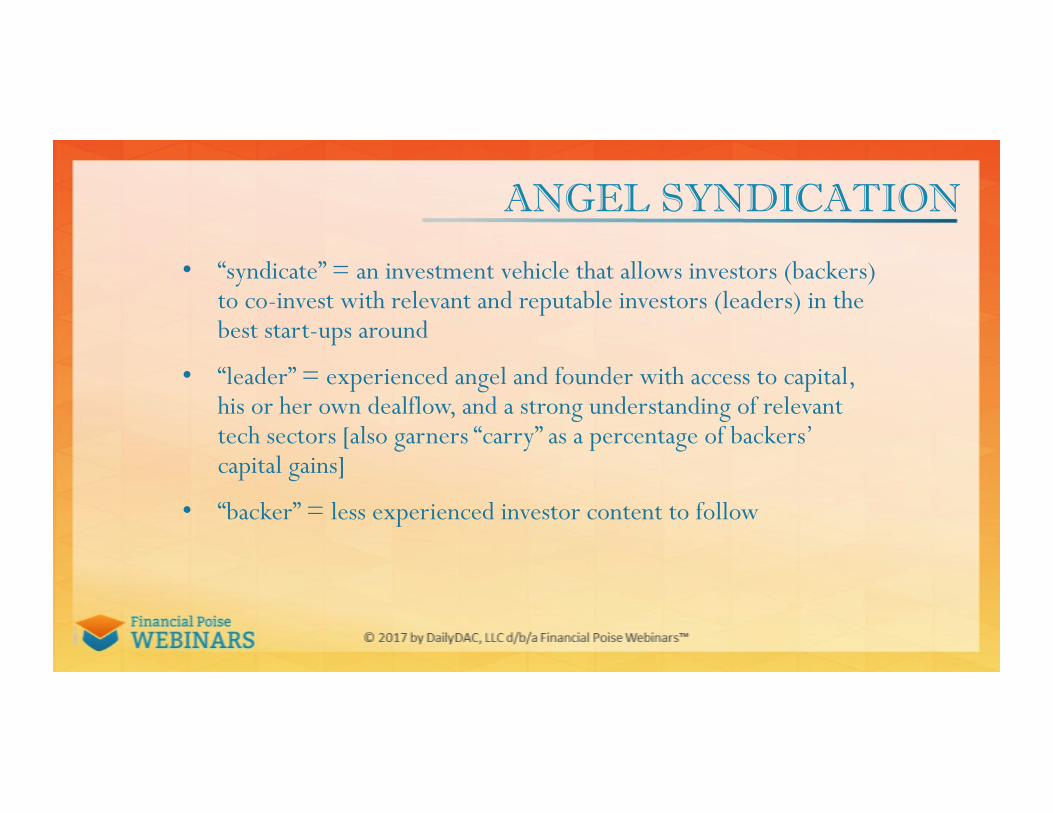

ANGEL SYNDICATION

• “syndicate” = an investment vehicle that allows investors (backers) to co-invest with relevant and reputable investors (leaders) in the best start-ups around

• “leader” = experienced angel and founder with access to capital, his or her own dealflow, and a strong understanding of relevant tech sectors [also garners “carry” as a percentage of backers’ capital gains]

• “backer” = less experienced investor content to follow

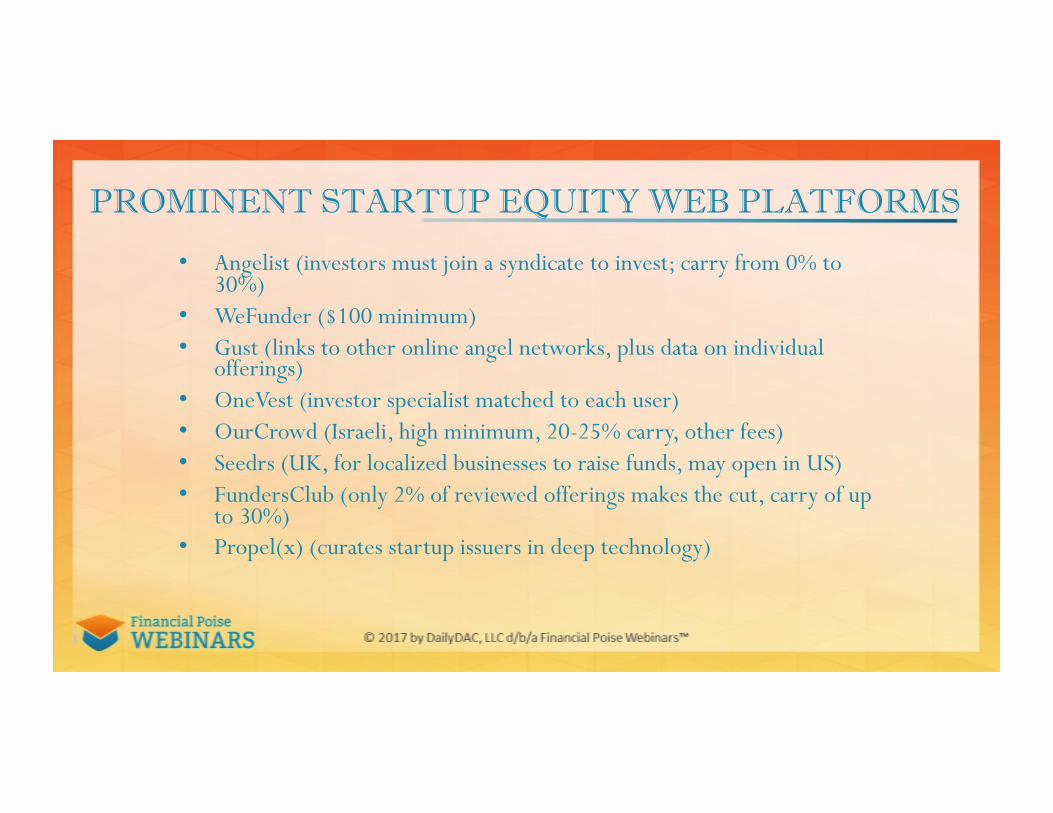

PROMINENT STARTUP EQUITY WEB PLATFORMS

• Angelist (investors must join a syndicate to invest; carry from 0% to 30%)

• WeFunder ($100 minimum) • Gust (links to other online angel networks, plus data on individual

offerings) • OneVest (investor specialist matched to each user) • OurCrowd (Israeli, high minimum, 20-25% carry, other fees) • Seedrs (UK, for localized businesses to raise funds, may open in US) • FundersClub (only 2% of reviewed offerings makes the cut, carry of up

to 30%) • Propel(x) (curates startup issuers in deep technology)

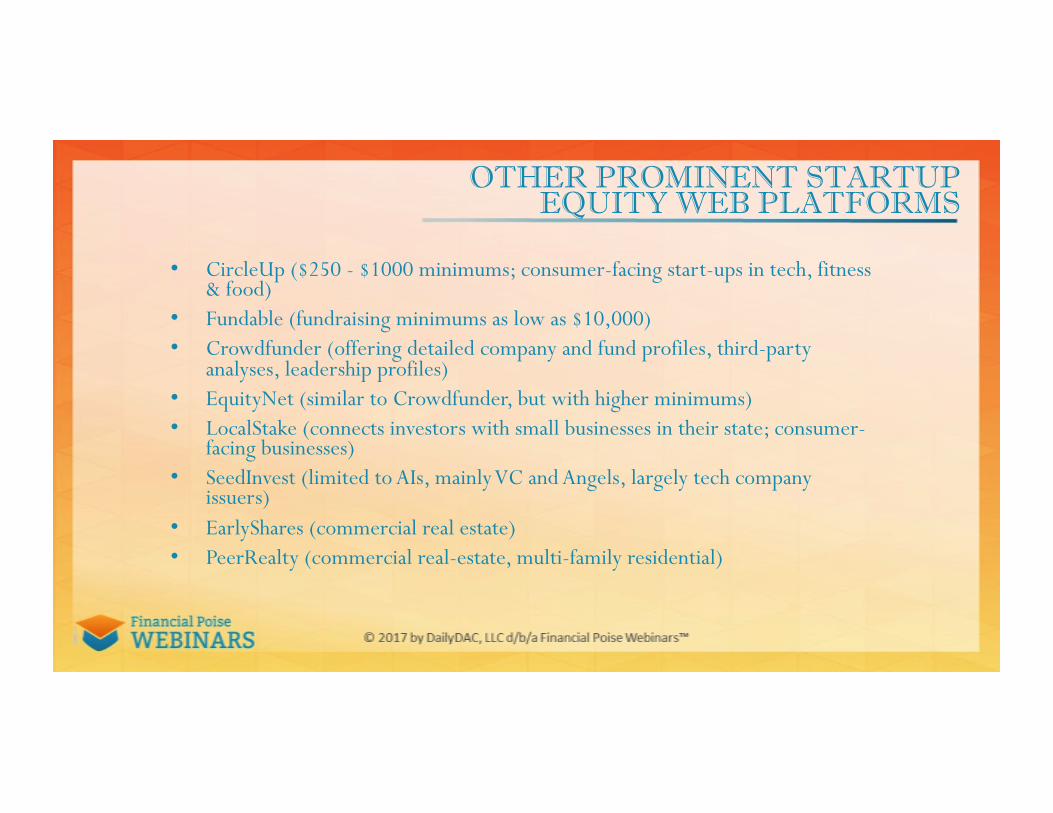

OTHER PROMINENT STARTUP EQUITY WEB PLATFORMS

• CircleUp ($250 - $1000 minimums; consumer-facing start-ups in tech, fitness & food)

• Fundable (fundraising minimums as low as $10,000) • Crowdfunder (offering detailed company and fund profiles, third-party

analyses, leadership profiles) • EquityNet (similar to Crowdfunder, but with higher minimums) • LocalStake (connects investors with small businesses in their state; consumer-

facing businesses) • SeedInvest (limited to AIs, mainly VC and Angels, largely tech company

issuers) • EarlyShares (commercial real estate) • PeerRealty (commercial real-estate, multi-family residential)

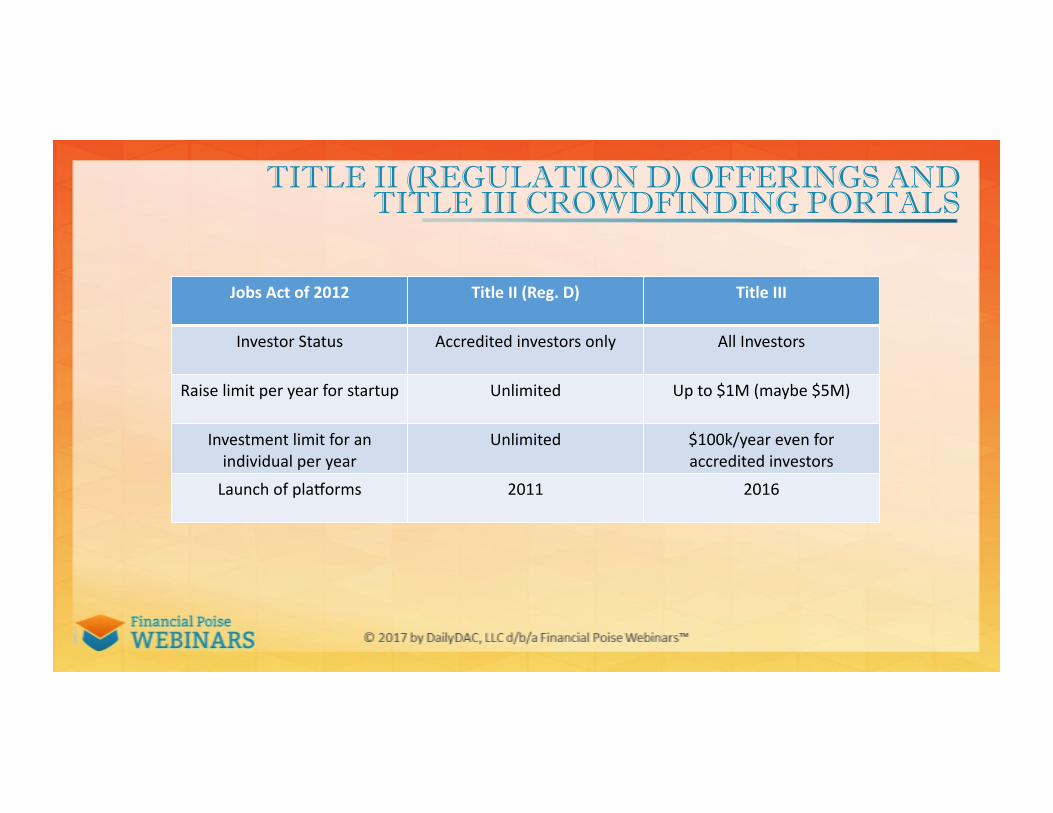

TITLE II (REGULATION D) OFFERINGS AND TITLE III CROWDFINDING PORTALS

Jobs Act of 2012 Title II (Reg. D) Title III

Investor Status Accredited investors only All Investors

Raise limit per year for startup Unlimited Up to $1M (maybe $5M)

Investment limit for an individual per year

Unlimited $100k/year even for accredited investors

Launch of pla_orms 2011 2016

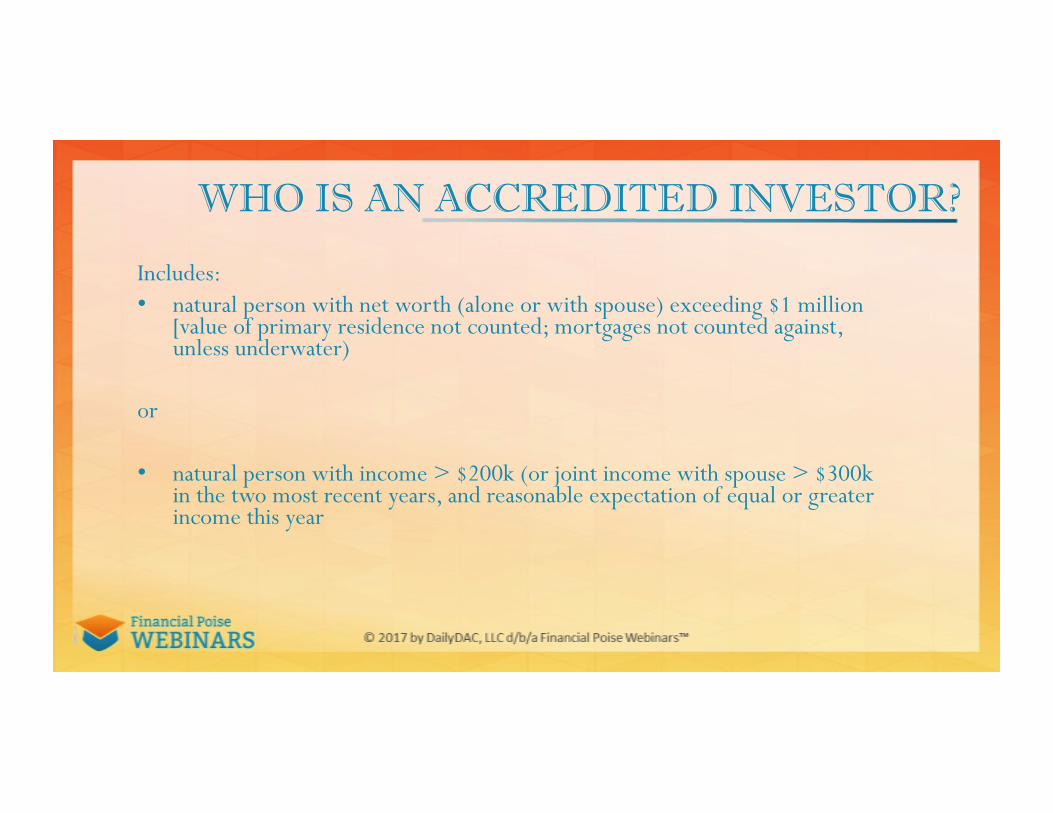

WHO IS AN ACCREDITED INVESTOR?

Includes: • natural person with net worth (alone or with spouse) exceeding $1 million

[value of primary residence not counted; mortgages not counted against, unless underwater)

or

• natural person with income > $200k (or joint income with spouse > $300k in the two most recent years, and reasonable expectation of equal or greater income this year

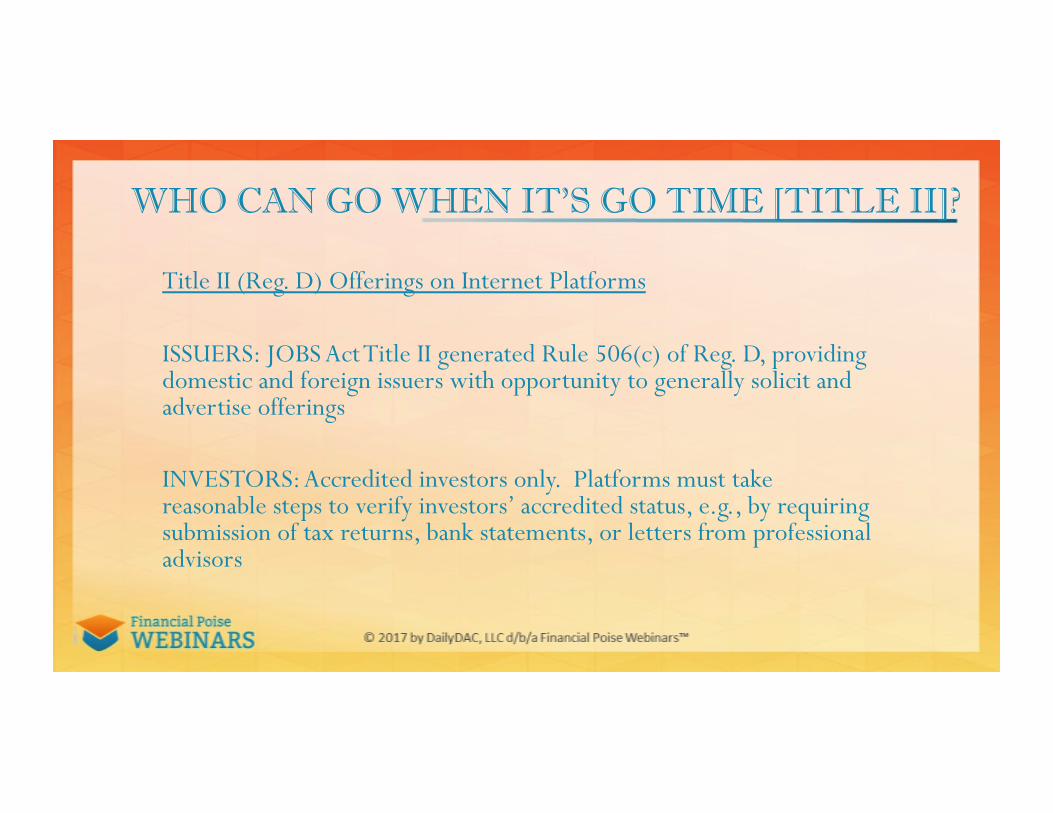

WHO CAN GO WHEN IT’S GO TIME [TITLE II]?

Title II (Reg. D) Offerings on Internet Platforms

ISSUERS: JOBS Act Title II generated Rule 506(c) of Reg. D, providing domestic and foreign issuers with opportunity to generally solicit and advertise offerings

INVESTORS: Accredited investors only. Platforms must take reasonable steps to verify investors’ accredited status, e.g., by requiring submission of tax returns, bank statements, or letters from professional advisors

TITLE II, REGULATION D, RULE 506(C) OFFERING

• May now generally solicit their offerings outside of the platform

• Issuers are not required to use an intermediary, like a broker-dealer

• No issuer or investor dollar limits

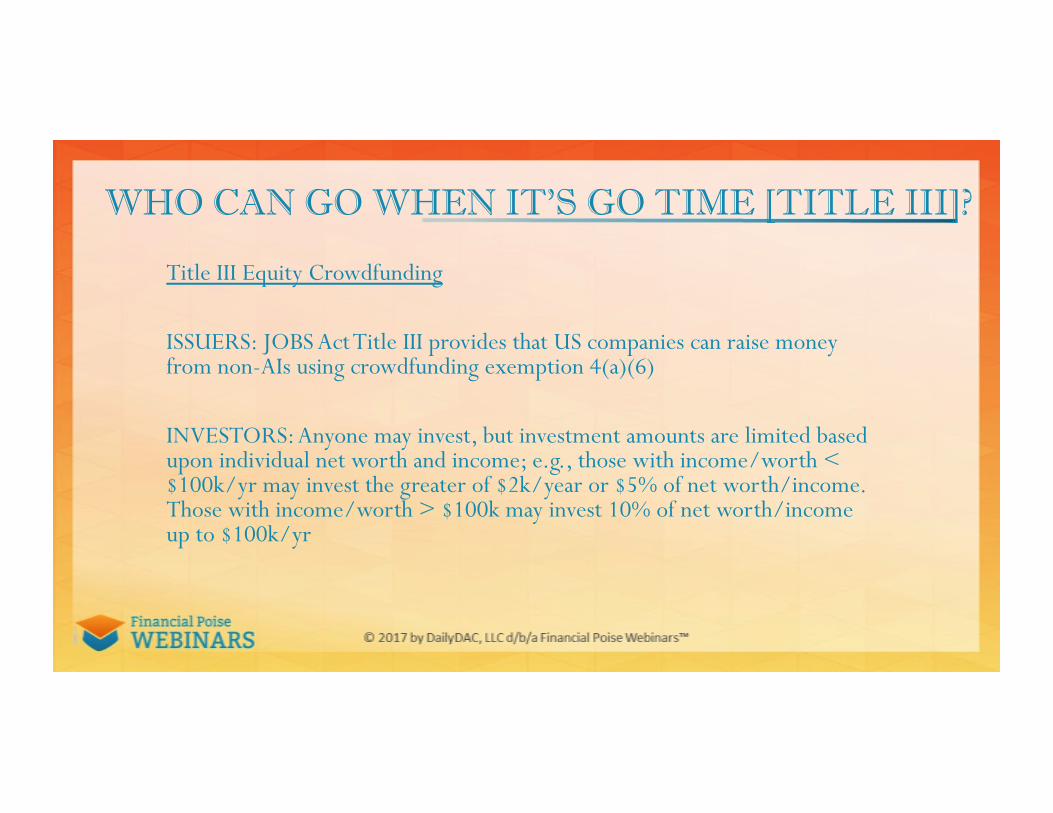

WHO CAN GO WHEN IT’S GO TIME [TITLE III]?

Title III Equity Crowdfunding

ISSUERS: JOBS Act Title III provides that US companies can raise money from non-AIs using crowdfunding exemption 4(a)(6)

INVESTORS: Anyone may invest, but investment amounts are limited based upon individual net worth and income; e.g., those with income/worth < $100k/yr may invest the greater of $2k/year or $5% of net worth/income. Those with income/worth > $100k may invest 10% of net worth/income up to $100k/yr

TITLE III EQUITY CROWDFUNDING

• Creates new exemption: Section 4(a)(6) of the Securities Act of 1933

• Issuers permitted to raise $1 million per year from both accredited investors and non-accredited investors

• Crowdfunding issuers must use a registered broker or registered funding portals

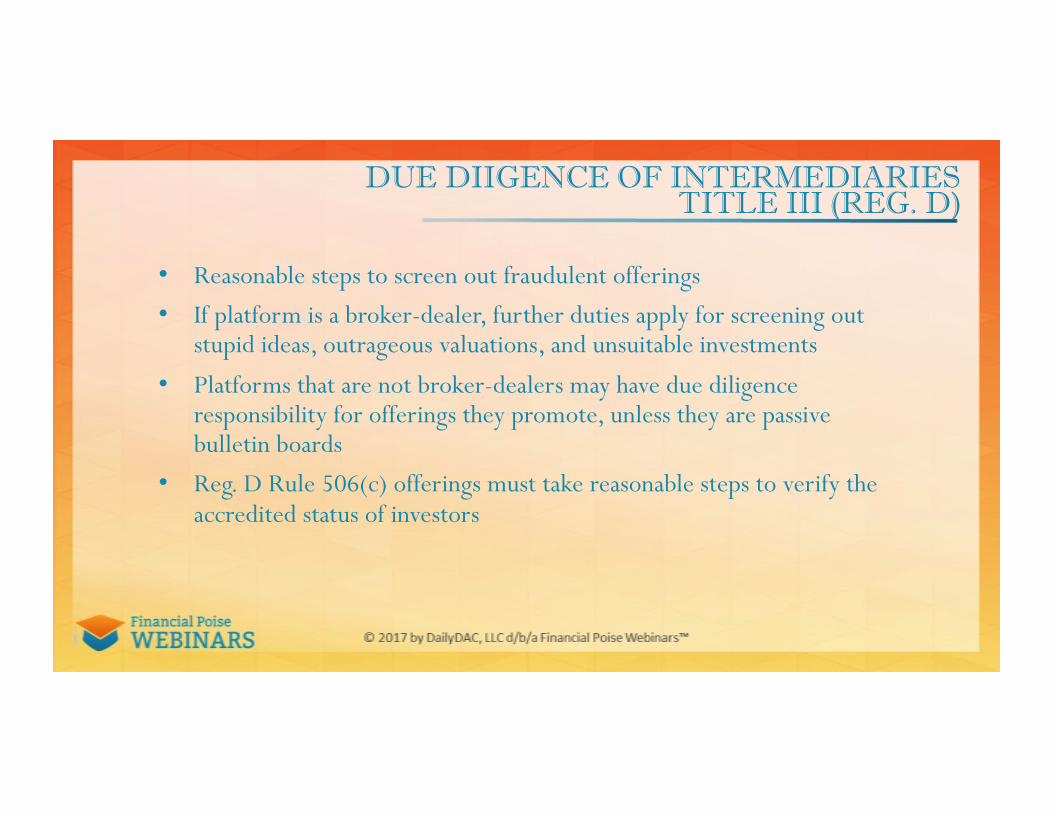

DUE DIIGENCE OF INTERMEDIARIES TITLE III (REG. D)

• Reasonable steps to screen out fraudulent offerings • If platform is a broker-dealer, further duties apply for screening out

stupid ideas, outrageous valuations, and unsuitable investments • Platforms that are not broker-dealers may have due diligence

responsibility for offerings they promote, unless they are passive bulletin boards

• Reg. D Rule 506(c) offerings must take reasonable steps to verify the accredited status of investors

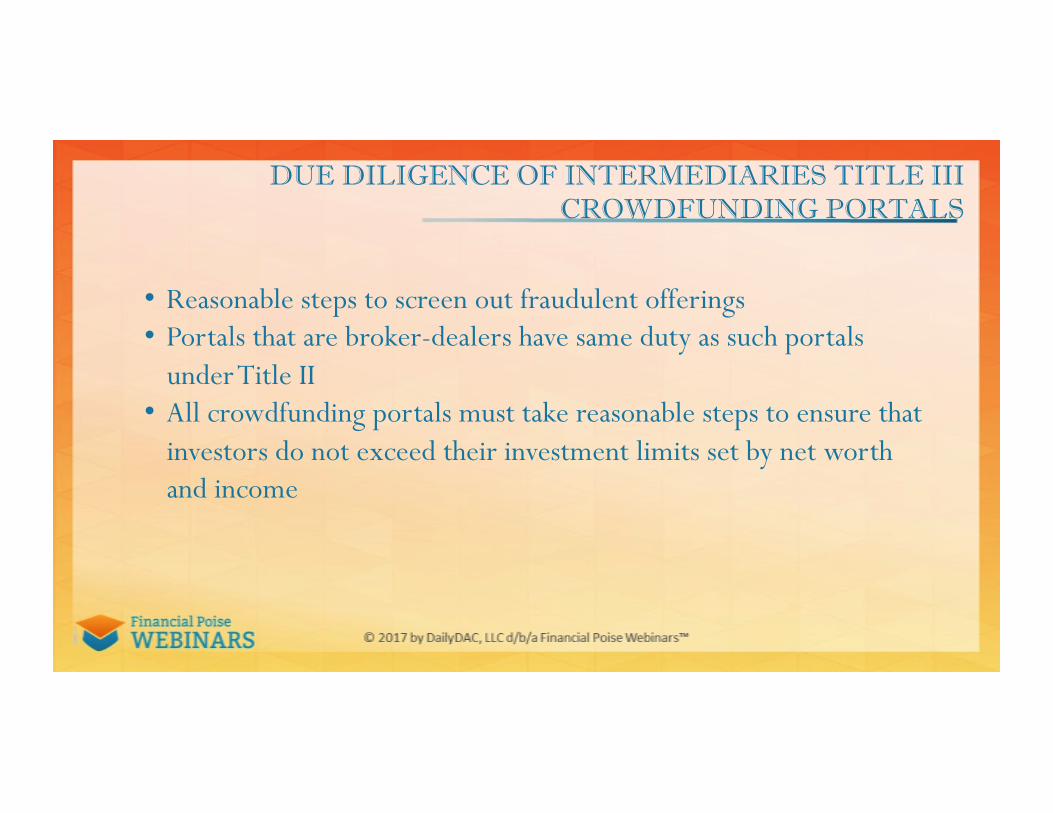

DUE DILIGENCE OF INTERMEDIARIES TITLE III CROWDFUNDING PORTALS

• Reasonable steps to screen out fraudulent offerings • Portals that are broker-dealers have same duty as such portals

under Title II • All crowdfunding portals must take reasonable steps to ensure that

investors do not exceed their investment limits set by net worth and income

ABOUT THE FACULTY

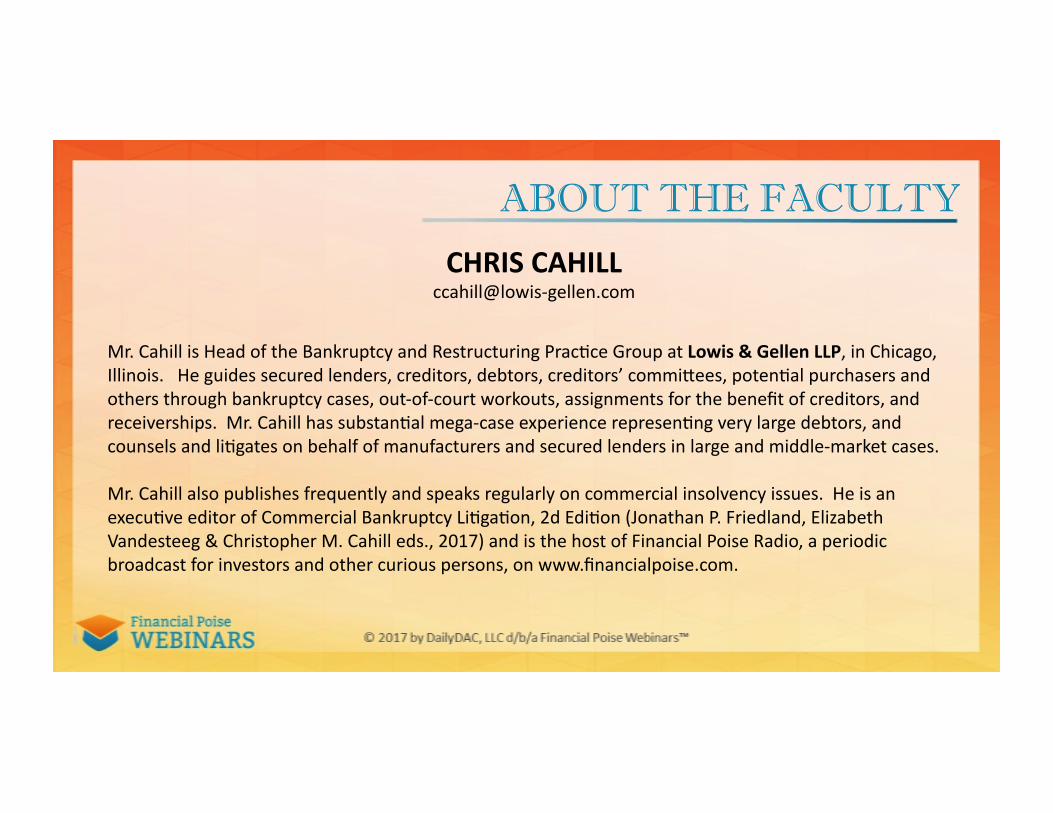

CHRIS CAHILL ccahill@lowis-‐gellen.com

Mr. Cahill is Head of the Bankruptcy and Restructuring Prac8ce Group at Lowis & Gellen LLP, in Chicago, Illinois. He guides secured lenders, creditors, debtors, creditors’ commiTees, poten8al purchasers and others through bankruptcy cases, out-‐of-‐court workouts, assignments for the benefit of creditors, and receiverships. Mr. Cahill has substan8al mega-‐case experience represen8ng very large debtors, and counsels and li8gates on behalf of manufacturers and secured lenders in large and middle-‐market cases.

Mr. Cahill also publishes frequently and speaks regularly on commercial insolvency issues. He is an execu8ve editor of Commercial Bankruptcy Li8ga8on, 2d Edi8on (Jonathan P. Friedland, Elizabeth Vandesteeg & Christopher M. Cahill eds., 2017) and is the host of Financial Poise Radio, a periodic broadcast for investors and other curious persons, on www.financialpoise.com.

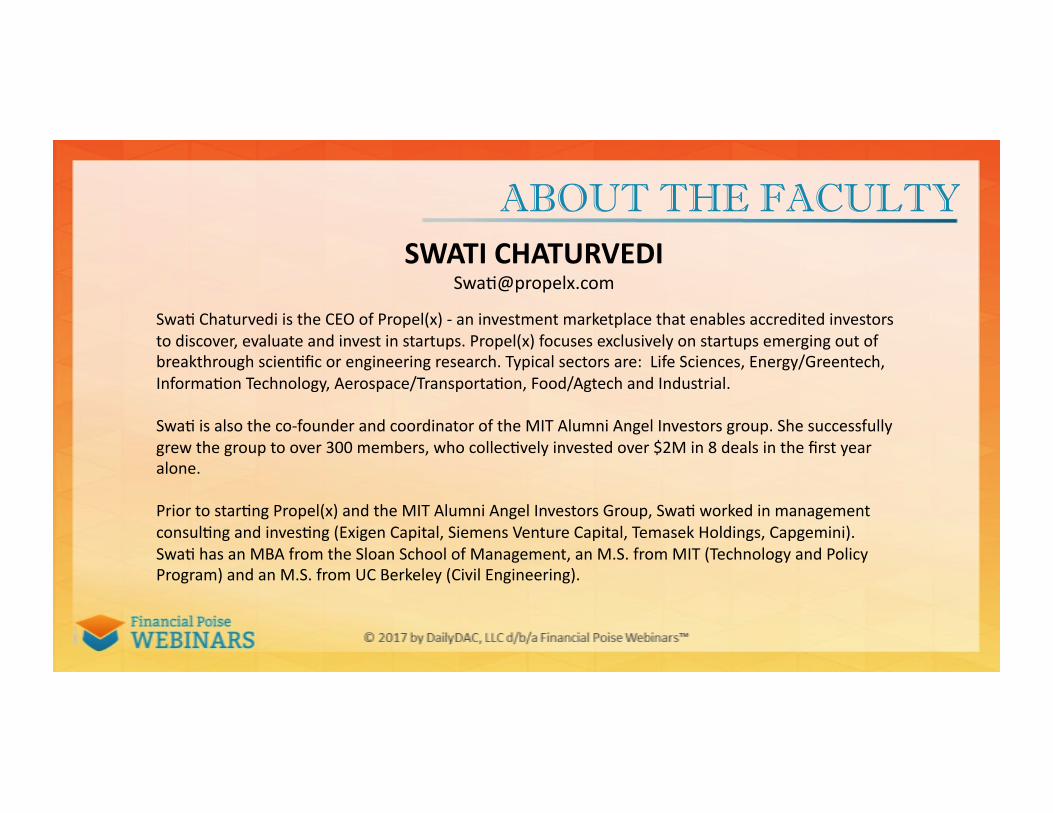

ABOUT THE FACULTY SWATI CHATURVEDI

Swa8 Chaturvedi is the CEO of Propel(x) -‐ an investment marketplace that enables accredited investors to discover, evaluate and invest in startups. Propel(x) focuses exclusively on startups emerging out of breakthrough scien8fic or engineering research. Typical sectors are: Life Sciences, Energy/Greentech, Informa8on Technology, Aerospace/Transporta8on, Food/Agtech and Industrial.

Swa8 is also the co-‐founder and coordinator of the MIT Alumni Angel Investors group. She successfully grew the group to over 300 members, who collec8vely invested over $2M in 8 deals in the first year alone.

Prior to star8ng Propel(x) and the MIT Alumni Angel Investors Group, Swa8 worked in management consul8ng and inves8ng (Exigen Capital, Siemens Venture Capital, Temasek Holdings, Capgemini). Swa8 has an MBA from the Sloan School of Management, an M.S. from MIT (Technology and Policy Program) and an M.S. from UC Berkeley (Civil Engineering).

ABOUT THE FACULTY LYNDA DAVEY

Lynda Davey is the Chairman and Founder of Avalon SecuriKes Ltd, one of the few woman-‐owned FINRA and SEC registered broker dealers. Ms. Davey's finance career spans 30 years of advising, financing and inves8ng in public and private companies. She serves as Co-‐Chief Execu8ve Officer of Avalon Net Worth. Ms. Davey brings broad exper8se to her clients, having assisted them strategically posi8on their companies for success by focusing on balanced capitaliza8on, developing and implemen8ng strategic growth plans and op8mally structuring transac8ons. Since 1992, Avalon has provided bulge bracket investment banking assistance to mid-‐market clients. The firm cul8vates long term rela8onships with high caliber business owners and senior execu8ves by assis8ng them with both short-‐term and long-‐term needs including financing for business expansions, balance sheet recapitaliza8ons, acquisi8ons and liquidity events.

Prior to founding Avalon, Ms. Davey worked at Salomon Brothers on public offerings, dives8tures, acquisi8ons and private placements for clients in a variety of industries. She was also President of Tribeca Corp, a merchant bank with large equity investments in public consumer companies and private buyouts. Before commencing her finance career Ms. Davey prac8ced as a registered architect.

ABOUT THE FACULTY

RICHARD SWART [email protected]

Dr. Richard Swart is the Chief Strategy Officer of NextGen Crowdfunding. With more than 20 years of experience in the industry, he also serves as a member of the University of Cambridge’s Alterna8ve Financing Industry Board. Richard is also a founding board member of the Crowdfunding Professional Associa8on (CfPA) and the Crowdfunding Intermediary Regulatory Advocates (CIFRA). Addi8onally, he advises the Bill and Melinda Gates Founda8on and works with several other prominent founda8ons, think tanks, funds and corpora8ons.

37

38