alfredo ergas cfo -...

TRANSCRIPT

Alfredo ErgasCFO

» Who are we?

» What are we facing today?

» What do you think we should do in the future?

» What we are really doing and what we are committed to.

» What is our regulatory framework?

Total Customers: 11.9 millionTotal Sales: 61,610 GWh Total Assets: US$B 12,177

Colombia

Customers 2.2 MillionSales 11,441 GWhMarket Share 23%

Peru

Customers 1 MillionSales 5,201 GWhMarket Share 23%

Chile

Customers 1.5 MillionSales 12,923GWhMarket Share 44%

Argentina

Customers 2.2 MillionSales 15,833 GWhMarket Share 17%

Brazil

Customers 2.7 MillionSales 7,227 GWhMarket Share 6%

Customers 2.4 MillionSales 8,985 GWh

As of December 2007

Leading Distribution Company in South America

Total Capacity: 13,707 MWTotal Sales: 62,567 GWh Total Assets: US$B 10,842

ChileCapacity 4,779 MWProduction 18,773 GWhHydro 13,179 GWhThermo 5,591 GWh

Market Share 37%

ArgentinaCapacity 3,644 MWProduction 12,117 GWhHydro 3,696 GWhThermo 8,421 GWhMarket Share 15%

BrazilCapacity 987 MWProduction 3,954 GWhHydro 3,888 GWhThermo 66 GWh

Market Share 1%

PeruCapacity 1,468 MWProduction 7,654 GWhHydro 4,385 GWhThermo 3,270 GWh

Market Share 28%

ColombiaCapacity 2,829 MWProduction 11,942 GWhHydro 11,427 GWhThermo 515 GWh

Market Share 21%

Leading Generation Company in South America

As of December 2007

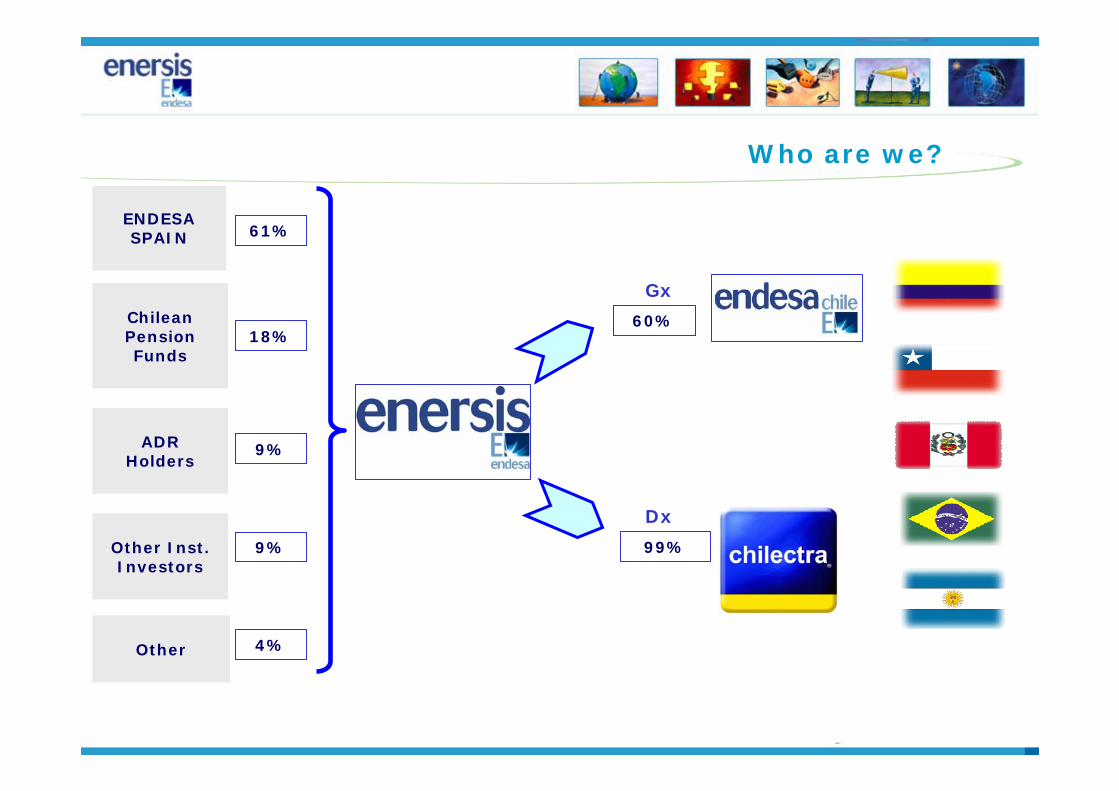

ENDESA SPAIN

ChileanPensionFunds

ADRHolders

Other

Gx

Other Inst. Investors

61%

18%

9%

9%

4%

Who are we?

99%

60%

Dx

Operating Income

Millions Ch$

11%

2007 Results

1,131,631

1,255,567

1,060,000

1,080,000

1,100,000

1,120,000

1,140,000

1,160,000

1,180,000

1,200,000

1,220,000

1,240,000

1,260,000

1,280,000

2006 2007

2007 Results

Millions Ch$

Non-Operating Income

27.3%

Effect BT64 year 2006

Effect BT64 year 2007

Gas Atacama provision

(439,029)

(558,859)(600,000)

(500,000)

(400,000)

(300,000)

(200,000)

(100,000)

-2006 2007

Millions Ch$

Net Income and Homogeneous Terms

13.3%

38.7%307.122

166.287

Net Income, as of December 2007

188,376

-

50,000

100,000

150,000

200,000

250,000

300,000

2006 2007

Fin. Debt / Equity

EBITDA / Fin. Expenses

2005 2006 2007

135%

3.3 4.8

128% 116%

4.0

ENERSIS

Fin. Debt / EBITDA 3.0 2.02.5

Financial Results

Source: Enersis

(*) As of December 31st, 2007

2003US$ 4,475

millionShare: $ 86

2004US$ 5,557

millionShare: $ 94

2005US$ 7,177

millionShare: $ 111

2006US$ 10,448

millionShare: $ 170

2007US$ 10,504

millionShare: $ 160

CAGR*: 17%

Strong Profits for our Shareholders

Apr 30, 2008US$ 12,243

millionShare: Ch$ 173

Positive Perception of Rating Agencies

Date: 07-03-2007Date: 07-05-2007 Date: 12-14-2006

BBB-

BBB

Ba1

Baa3

BBB-

BBB AA- AA-

A+A+

Date: 07-06-2007 Date: 07-20-2007

Domestic MarketInternational Market

…DUE TO A OF GROWTH INCREASING SCENARIO, GREATER FINANCIAL FLEXIBILITY AND FEWER REGULATORY UNCERTANTIES

» Who are we?

» What are we facing today?

» What do you think we should do in the future?

» What we are really doing and what are we committed to.

» What is our regulatory framework?

Generation Distribution & Supply

Transmission End User

PRICE REGULATION

Long term contracting w/ distribution companies for regulated customers

Free bilateral contracting with eligible customers

Short-term markets covering variable cost

Regulated operation of distribution networks

Guaranteed access where suppliers exist (Colombia)

Prices based on investment and capital costs plus recovery of energy costs

Guaranteed access at regulated prices, based on investment and capital costs

Investor selection through competitive bidding

New project definition through technical studies

DISTRIBUTION AND SUPPLY BUSINESS

Wholesale energy costs

Supply costsInvestment

and O&M costs

Competitive bidding for long term contracts

Stabilized spot price

Competitive bidding for long term contracts

Competitive bidding for long term contracts

Competitive bidding for long term contracts and spot price

Optimal NRV and O&M costs for a model company

Under

Optimal NRV and O&M costs for a model company

O&M model company, depreciation costs, amortized NRV

NRV at regulated infrastructure prices, O&M costs

Included in distribution

Included in distribution

Included in distribution

Included in distribution

Optimal customer administration costs

Wholesale Energy Costs

Supply CostsInvestment

and O&M Costs

Competitive bidding for long-term contracts

Stabilized spot price

Competitive bidding for long-term contracts

Competitive bidding for long-term contracts

Competitive bidding for long-term contracts and spot price

Optimal NRV and O&M costs for a model company

Under review

Optimal NRV and O&M costs for a model company

O&M model company, depreciation costs, amortized NRV

NRV at regulated infrastructure prices, O&M costs

Included in distribution

Included in distribution

Included in distribution

Included in distribution

Optimal customer administration costs

ENERGY AND POWER PURCHASES

- Pass Through of auction prices

- Purchases through spot market or through public auctions.Pass through:

- Weighted average cost of own purchase prices and market prices for the last 12 months.

- Energy purchases at bidding process for the regulated customers demand. Distributor may include free customers demand in the regulated auctions

Auction prices are passed on to final tariffs at close to +/-3% band of.

- Energy purchases at bidding processes for the regulated customers demand. For the free customers demand, bilateral contracting or auctions- Pass Through of auction prices

2. Energy: Average marginal cost of energy.3. Power: Costs of reserve and ancillary services.

- all the distributors needs are covered together. Pass-Through

Energy and Power Purchases

Colombia

Brasil

Argentina

Chile

Perú

- Energy and power purchases made at seasonal price- Pass Through to final tariffs at seasonal prices.

Seasonal Price:1. Calculated every 3 months with a 3-year operation simulation.

- Pass Through of auction prices

- Purchases through spot market or through public auctions.Pass through:

- Weighted average cost of own purchase prices and market prices

- Energy purchases at bidding process for the regulated customerscustomers demand in the regulated auctions

-3% band of real demand.

- Energy purchases at bidding processes for the regulated customers demand. For the free customers demand, bilateral contracting or auctions- Pass Through of auction prices

2. Energy: Average marginal cost of energy.3. Power: Costs of reserve and ancillary services.

- Energy purchases through auctions organized by ANEEL in whichPass-Through

Energy and Power Purchases

Colombia

Brazil

Argentina

Chile

Peru

- Energy and power purchases made at - Pass Through to final tariffs .

Seasonal Price:

REGULATORY AND POLITICAL STRUCTURE

End User Tariff =

Generation + Transmission + VAD

Distribution Added Value (VAD) =

Optimal [NRV @ 10% + O&M costs]

GENERATION

TRANSMISSION DISTRIBUTION

End User Tariff =

Generation + Transmission + VAD

Distribution Added Value (VAD) =

Optimal [NRV @ 10% + O&M costs]

GENERATION

TRANSMISSION DISTRIBUTION

» Who are we?

» What are we facing today?

» What do you think we should do in the future?

» What we are really doing and what we are committed to.

» What is our regulatory framework?

» Price of oil is US$62/barrel

» Average natural gas coming from Argentina: 16 million cubic meters daily

» Good hydrology

» Reservoirs at normal levels

» US dollar exchange rate of $532.4

» 2.9% Inflation

2006 2007

Energy Scenario

2007 2008

» Price of oil is US$91/barrel

» Average natural gas coming from Argentina: 7 million cubic meters daily

» Low hydrology

» Reservoirs at low levels

» US dollar exchange rate of $489.9

» 7.8% Inflation

» Price of oil is US$116/barrel

» Average natural gas coming from Argentina: 8 million of cubic meters daily

» Low hydrology

» Reservoirs at low levels

» US dollar exchange rate of $437.7

» 8.1% Inflation

GDP Forecasts*

* Latin American Consensus Forecasts, March 2008

What we can expect in terms of demand?

4.2%

6.9% 7.0%

4.6%

5.4%

4.7%4.4%

5.0%5.0%

6.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Chile Argentina Peru Brazil Colombia

2008 2009

» Who are we?

» What are we facing today?

» What do you think we should do in the future?

» What we are really doing and what we are committed to.

» What is our regulatory framework?

What do you think about…

» What is your view of the energy situation in the region?» How would you address the energy scenario in the region?

» What do you think about the use of our FCF?» Should we make more investments?» Should we pay more dividends?» Should we prepay debts?

» What do you think about our assets?» Should we keep the current level?» Should we develop further any specific country?» Should we venture into other countries?

» Who are we?

» What are we facing today?

» What do you think we should do in the future?

» What we are really doing and what we are committed to.

» What is our regulatory framework?

What can we do with our FCF?…

Free Cash Flow

Investments Dividends Debt

» Increase generation capacity

» Expansion of grids and distribution assets

» Strong prevention maintenance investment

Our Answer: 2008 – 2012 Investment Plan

US$ 10 billion

US$ 4.4 billion

in Distribution

US$ 5.6 billion

in Generation

We invest around US$ 900 billion yearly to

keep our service standards in line with international levels.

12 millioncurrent customers

» We decrease the number of shortages per year;

» We decrease the duration of shortages;

» We significantly enhance the reliability of our grids;

Investing in quality of service

+

In order to enhance our ratios:

And efficiently serve a growing customer base:

Annual incorporationof 400,000 new

customers

• 377 MW Installed Capacity• Combined Cycle Thermal Plant

• 32 MW Installed Capacity• Run of the river Hydro Plant

• 18 MW Installed Capacity• Wind Farm Power Station

We help increase the energy supply

• 2,750 MW Hydro Plant• Investments under study• Operation: 2012-2020

2007 *70%

US$ 259 billion

2006 70%

US$ 368 billion

200562%

US$ 64 billion

2007

Div. Yield: 3.4%Payout: 70% Div: $ 5.4 per share

200450%

US$ 24 billion

(*) As of December 2007

Increased Dividend

Capturing expansion opportunities

The Action Plan consists of:

» Our concession areas total approximately 202,000 Km2 in distribution.

» We serve 12 million customers.

We invest more than US$ 900

billion

We have been able to maintain our grids and incorporate more than

400,000 new customers annually.

Equivalent to purchasing a new midsize distribution company.

As a result of our constant concern

» We have decreased the number of shortages per year.

» We have decreased the duration of shortages.

» We have significantly enhanced the availability of our plants.

Taking Advantage of our Customer Base