adoption of ifrs 15 - utilitywise plc · sustained growth record good customer experience 4 ifrs...

TRANSCRIPT

www.utilitywise.com

Adoption of IFRS 15

1

Brendan Flattery, CEORichard Laker, CFO31 July 2017

www.utilitywise.com

Brendan Flattery

@BPFlattery

2

www.utilitywise.com

Sustained Growth Record

Good Customer Experience

3

IFRS 15 adoption

DividendsTrading

update FY17

www.utilitywise.com

Sustained Growth Record

Good Customer Experience

4

IFRS 15 to be adopted on

1 August 2017

Early adoption to provide

shareholders with clarity

Year ended 31 July 2017 final year

pre-IFRS 15

www.utilitywise.com

Sustained Growth Record

Good Customer Experience

5

Detailed review of revenue accounting

policies

Technical advice from independent

accounting firm

Change in accounting policies on adoption –

earlier years restated

www.utilitywise.com

Sustained Growth Record

Good Customer Experience

6

Reduction in revenue and

profit

Increase in future secured revenue (order

book)

Reduction in accrued

revenue on balance sheet

www.utilitywise.com

Sustained Growth Record

Good Customer Experience

7

No change in commercial activities of

Group

No change in operating cash

flows of the Group

Close correlation

between profit and operating cash flow in

future

www.utilitywise.com

Richard Laker

@richardlaker76

8

www.utilitywise.com9

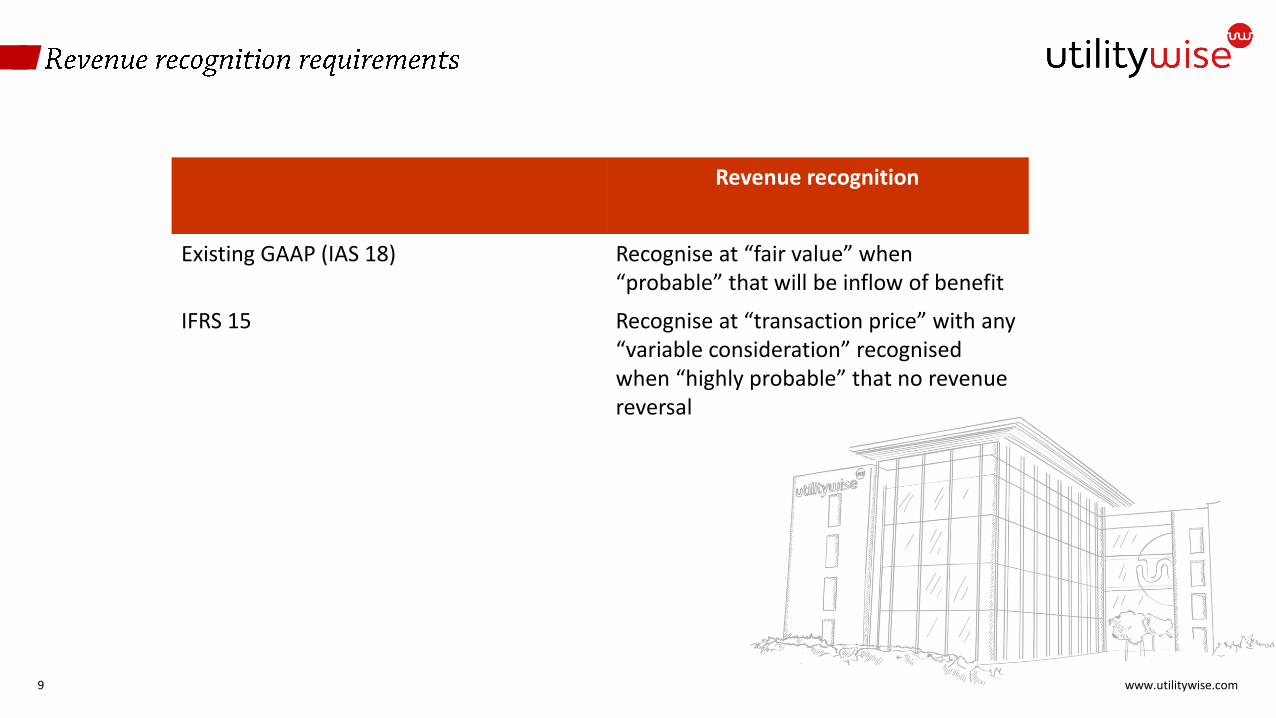

Revenue recognition

Existing GAAP (IAS 18) Recognise at “fair value” when“probable” that will be inflow of benefit

IFRS 15 Recognise at “transaction price” with any“variable consideration” recognised when “highly probable” that no revenue reversal

www.utilitywise.com10

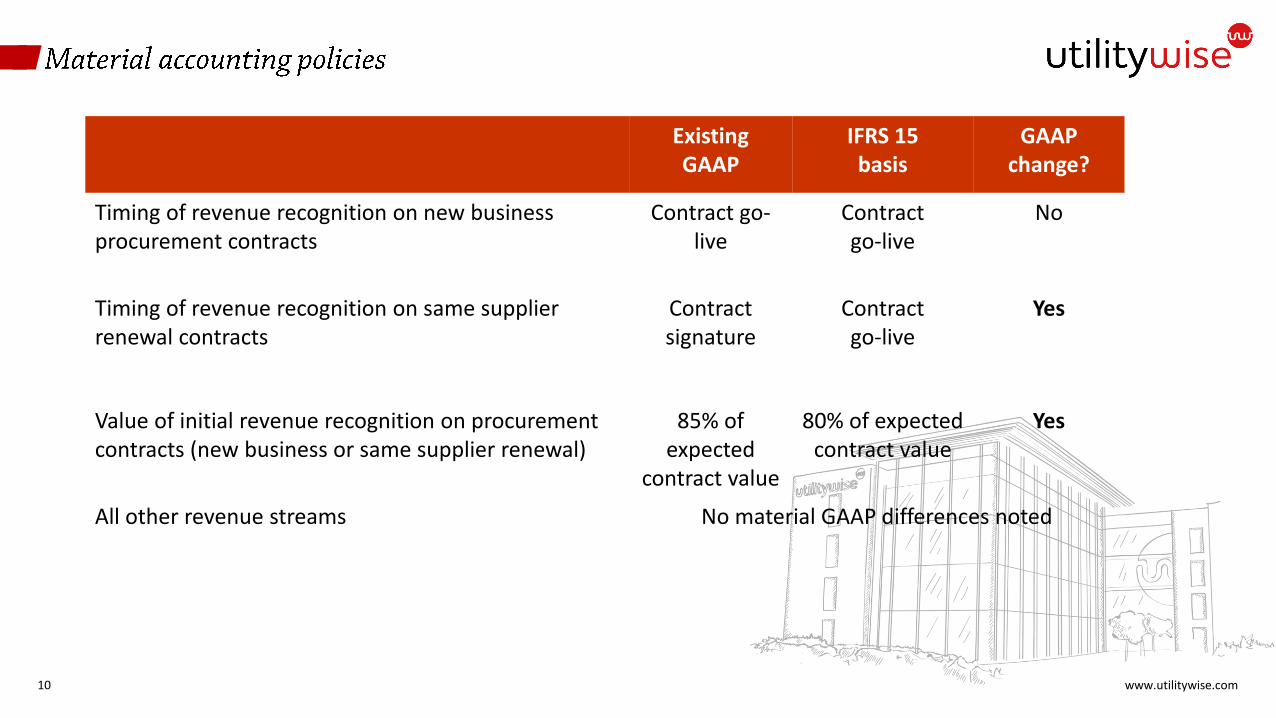

ExistingGAAP

IFRS 15basis

GAAPchange?

Timing of revenue recognition on new business procurement contracts

Contract go-live

Contract go-live

No

Timing of revenue recognition on same supplier renewal contracts

Contract signature

Contract go-live

Yes

Value of initial revenue recognition on procurement contracts (new business or same supplier renewal)

85% of expected

contract value

80% of expected contract value

Yes

All other revenue streams No material GAAP differences noted

www.utilitywise.com11

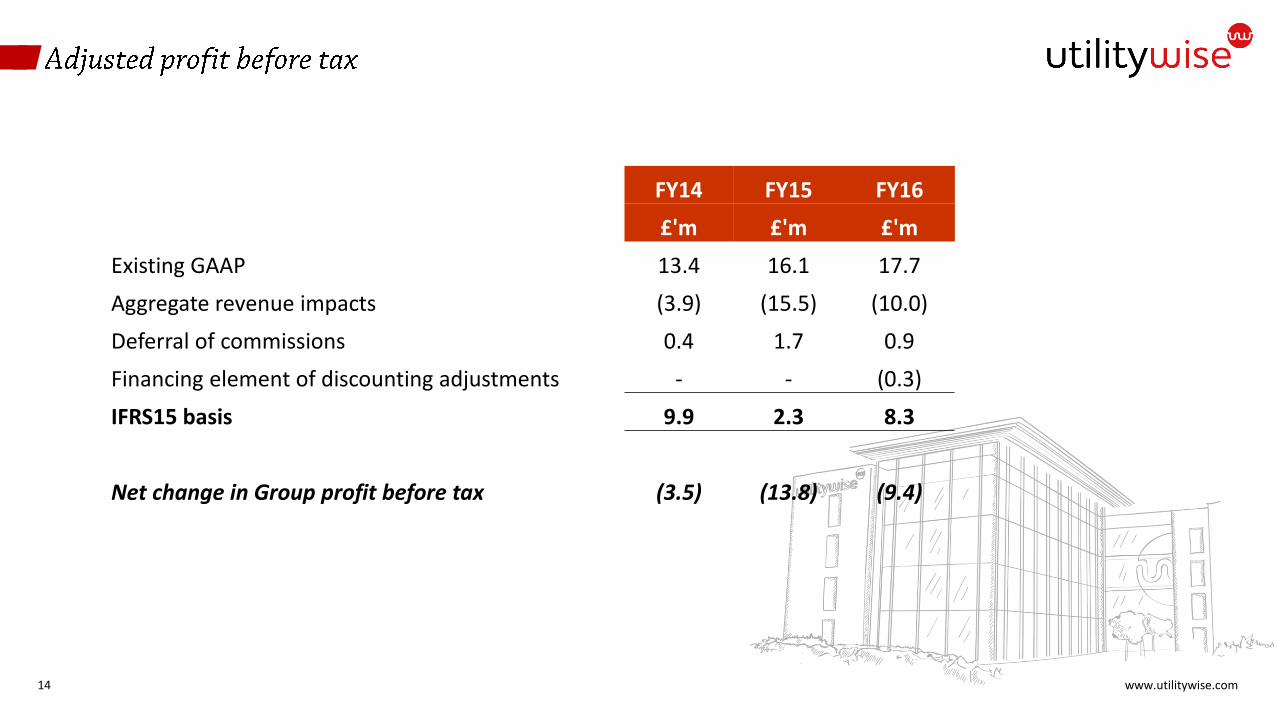

FY14 FY15 FY16

£'m £'m £'m

Existing GAAP 48.9 68.9 84.4

Recognition of renewals on contract start (2.9) (14.0) (7.4) (24.3)

Initial recognition at 80% (1.7) (1.9) (2.6) (6.2)

Discounting adjustments 0.7 0.4 -

IFRS15 basis 45.0 53.4 74.5

Net change in Group revenue (3.9) (15.5) (10.0)

www.utilitywise.com12

85% 85% to 80%

basis 80% basis

Financial year ended £'m £’m £'m

31 July 2017 11.0 (0.6) 10.4

31 July 2018 6.5 (0.4) 6.1

31 July 2019 3.5 (0.2) 3.3

31 July 2020 2.1 (0.1) 2.0

1 August 2020 or later 1.2 (0.1) 1.1

24.3 (1.4) 22.9

• Will give final position as at 31 July 2017 in trading update on 24 August 2017

www.utilitywise.com

Sustained Growth Record

Good Customer Experience

13

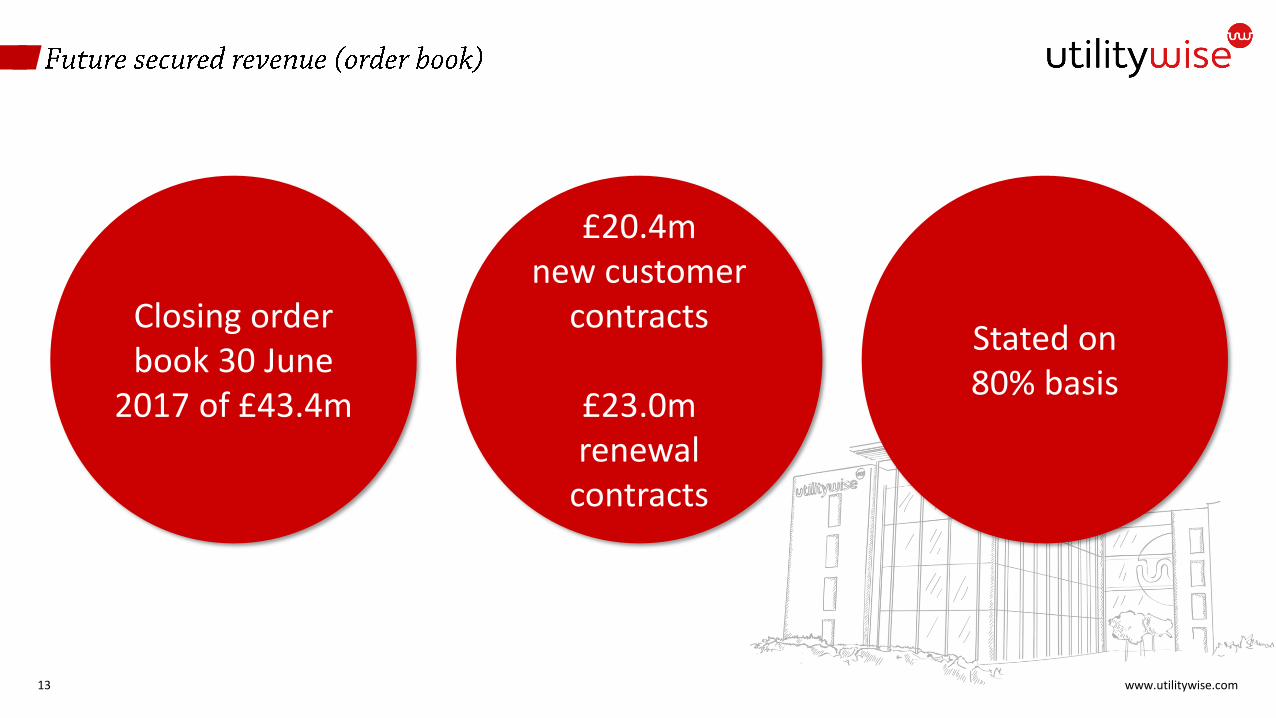

Closing order book 30 June

2017 of £43.4m

£20.4m new customer

contracts

£23.0m renewal

contracts

Stated on 80% basis

www.utilitywise.com14

FY14 FY15 FY16

£'m £'m £'m

Existing GAAP 13.4 16.1 17.7

Aggregate revenue impacts (3.9) (15.5) (10.0)

Deferral of commissions 0.4 1.7 0.9

Financing element of discounting adjustments - - (0.3)

IFRS15 basis 9.9 2.3 8.3

Net change in Group profit before tax (3.5) (13.8) (9.4)

www.utilitywise.com15

FY14 FY15 FY16

£‘m £‘m £‘m

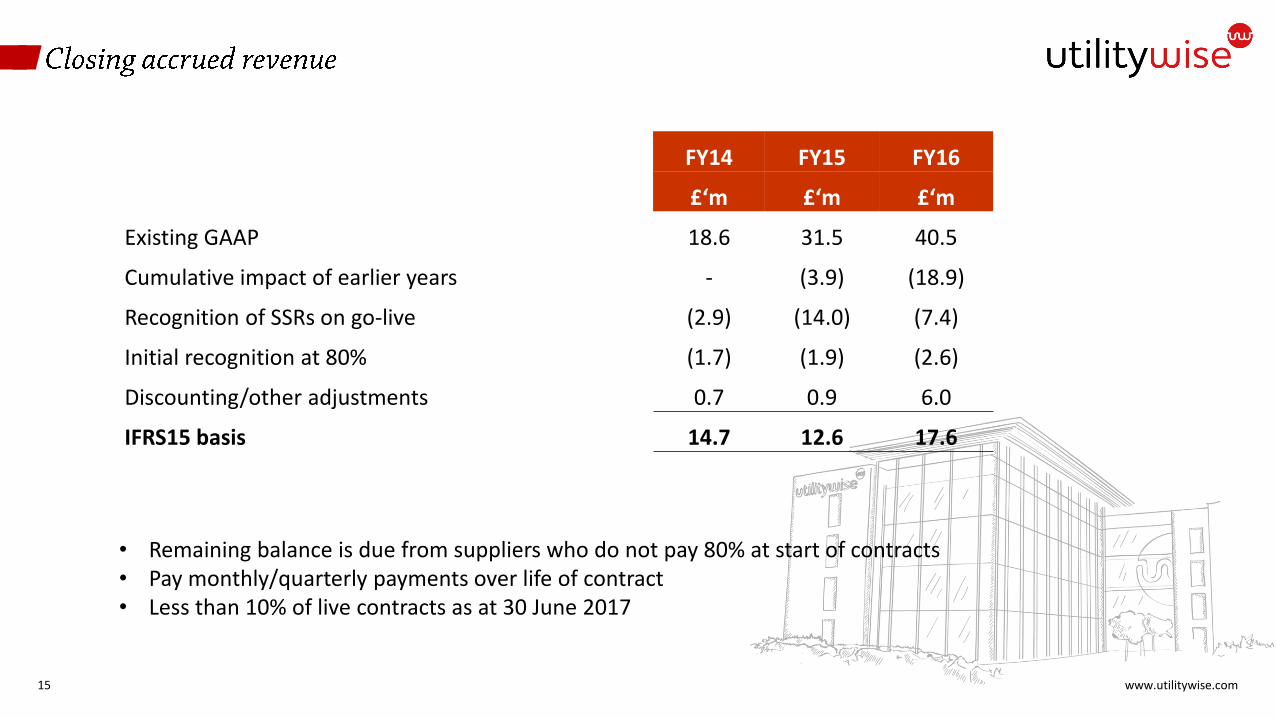

Existing GAAP 18.6 31.5 40.5

Cumulative impact of earlier years - (3.9) (18.9)

Recognition of SSRs on go-live (2.9) (14.0) (7.4)

Initial recognition at 80% (1.7) (1.9) (2.6)

Discounting/other adjustments 0.7 0.9 6.0

IFRS15 basis 14.7 12.6 17.6

• Remaining balance is due from suppliers who do not pay 80% at start of contracts• Pay monthly/quarterly payments over life of contract• Less than 10% of live contracts as at 30 June 2017

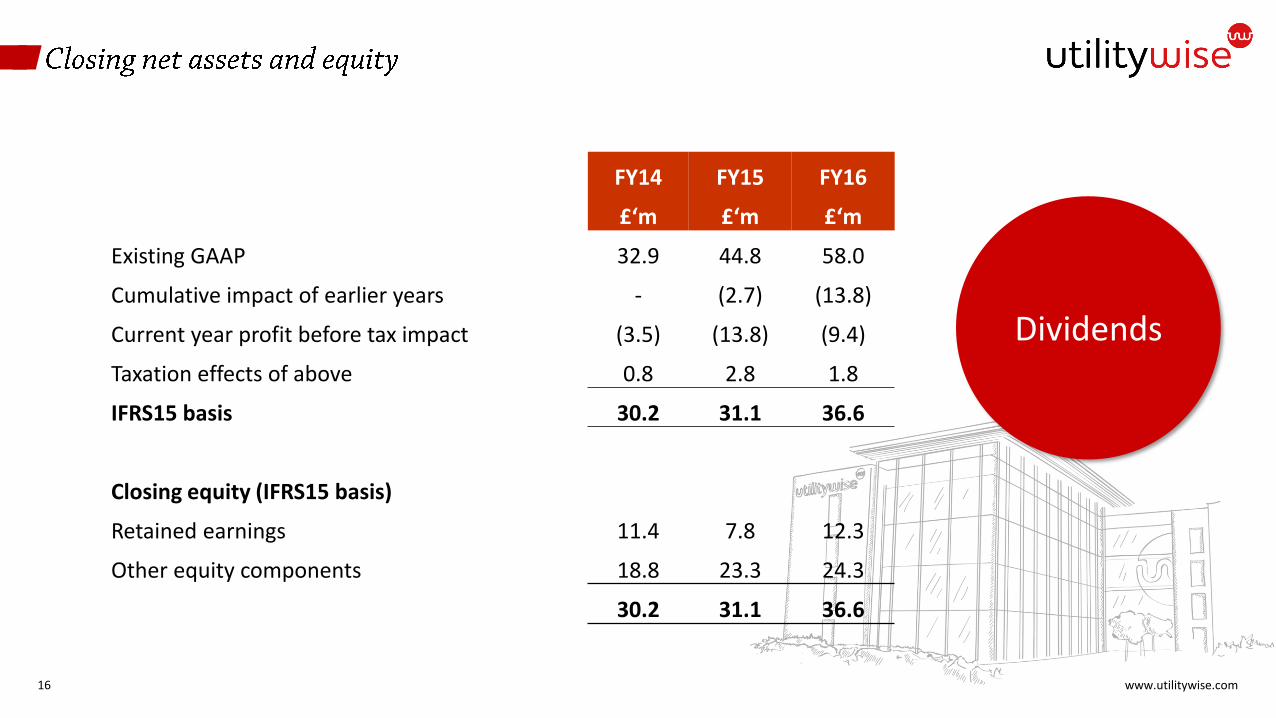

www.utilitywise.com16

FY14 FY15 FY16

£‘m £‘m £‘m

Existing GAAP 32.9 44.8 58.0

Cumulative impact of earlier years - (2.7) (13.8)

Current year profit before tax impact (3.5) (13.8) (9.4)

Taxation effects of above 0.8 2.8 1.8

IFRS15 basis 30.2 31.1 36.6

Closing equity (IFRS15 basis)

Retained earnings 11.4 7.8 12.3

Other equity components 18.8 23.3 24.3

30.2 31.1 36.6

Dividends

www.utilitywise.com

Sustained Growth Record

Good Customer Experience

17

Corporate tax impact

Banking covenants

Non-procurement

revenue

www.utilitywise.com

Brendan Flattery

@BPFlattery

18

www.utilitywise.com

Sustained Growth Record

Good Customer Experience

19

Expected negative retained

earnings at 1 August 2017 on

adoption of IFRS 15

No final dividend in

respect of FY17

Intention to reinstate

dividends as soon as

sufficient distributable

reserves (FY18)

www.utilitywise.com

Sustained Growth Record

Good Customer Experience

20

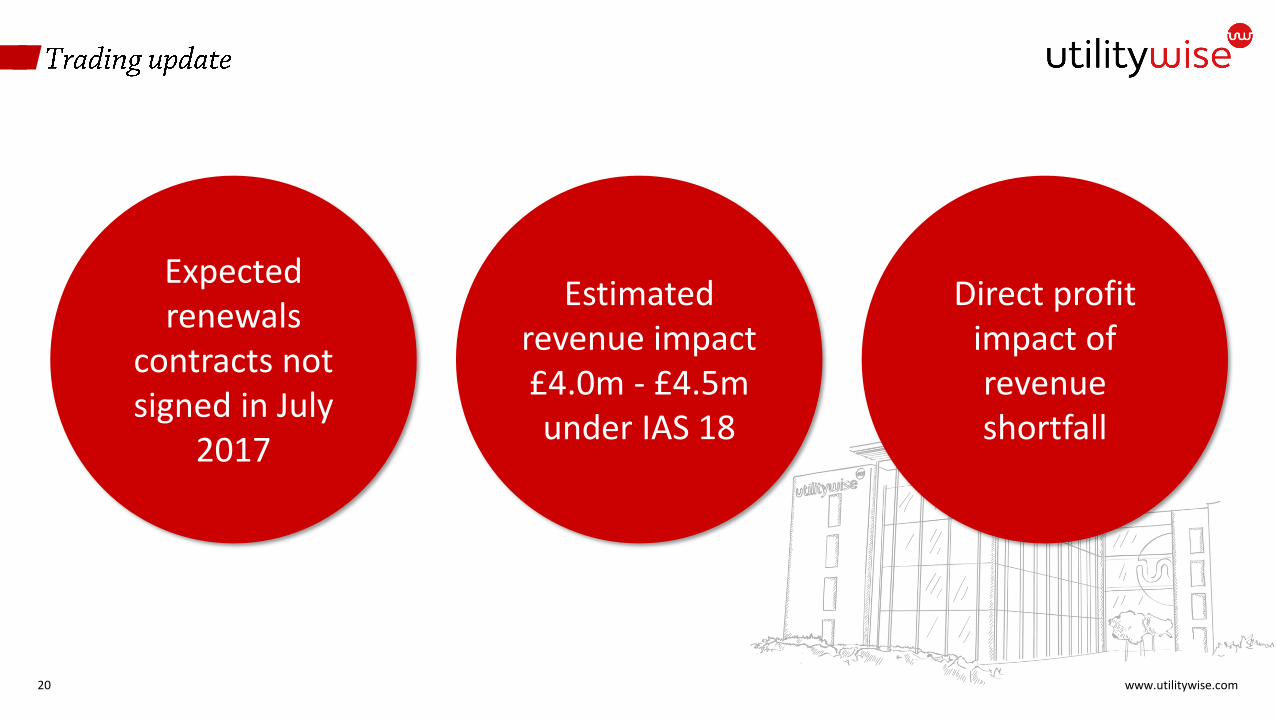

Expected renewals

contracts not signed in July

2017

Estimated revenue impact £4.0m - £4.5m under IAS 18

Direct profit impact of revenue shortfall

www.utilitywise.com

Sustained Growth Record

Good Customer Experience

21

Renewals contract revenue

recognised on signature under

IAS 18

Renewals contract revenue

recognised on contract go-live under IFRS 15

No material impact on FY17

on IFRS 15 basis

www.utilitywise.com

Sustained Growth Record

Good Customer Experience

22

Early adoption of IFRS 15 to

bring clarity to investors

Close correlation

between profit and cash flow going forward

Intention to re-instate

dividends as soon as possible

www.utilitywise.com23

Q&A