adaa ifrs digest compendium 2015 - abu dhabi · ifrs news, updates from adaa, iasb and the...

TRANSCRIPT

ADAA IFRS digest

compendium 2015

Highlights

January 2015

IASB Disclosure initiative, IAS 1, amendment removes ‘as a minimum’.

IAS 7 ED proposes reconciliation of opening and closing balances of assets and liabilities related to financing activities.

Status of a NIFRIC on IAS 40 rental of a Telecoms tower.

Investment entity amendment. And finally on the back page - Revenues and value an insight from ADAA’s Steven Ralls. February 2015

New revenue and leasing standards include disclosure objectives.

IFAC’s Year in Review calls for: Reform in government and public sector accounting. Reform of taxation systems. Integrated reporting and highlights the regulatory pressures impacting global accounting.

IFRS in Practice. Practical guides on IAS 7, IFRS 3 and IFRS 15 from BDO.

2015 Global Audit Committee survey from KPMG.

IAS 36 Impairment review tips from PWC. And finally on the back page – Addressing audit quality an insight from ADAA’s Steven Ralls.

March 2015

The complexity and length of financial reporting reflects an increasingly complex economic reality. If you want simple accounting don’t do complex transactions says Hans Hoogervorst.

Defining a lease.

IFRS 13 disclosure requirements publication from PWC.

Big data insight from EY.

Adopting IFRS 15 EY’s publication delves into the detail.

Debt current or non current?

What the Regulators think – IFIAR Global Survey. And finally on the back page – IFRS 15 Key considerations an insight from ADAA’s Muhammad Shabbir. April 2015

The essentials. The IASB highlights the principle to present fairly.

Poll of Polls from IFIAR. For three years getting fair value measurement wrong is top of the list.

Mind the GAAP. Hans Hoogervorst asserts there is bias in selection and presentation of other financial information.

‘I dream of a world where all values are fair.’ A sonnet from PWC. And finally on the back page – What the Regulators think an insight from ADAA’s Mahmoud Shahin. May 2015

The numbers do not tell the story. The numbers say you spent the cash. Compare your reporting to the IFRS Foundation’s Annual Report.

Why do more than you have to? The IAASB revises guidance for information presented in annual reports.

Impairment Transition Group. New IFRS 9 causes problems early! And finally on the back page – IFRS 9 careful planning for big changes ahead an insight from ADAA’s Muhammad Shabbir.

June 2015

‘A solid Conceptual Framework is essential because it shapes the decisions the IASB takes when developing standards.’

IASB’s Essentials publication provides a unique perspective into the issue of bank leverage.

State Owned Enterprises must institutionalize best practices in ownership and management. Publication from PWC.

The better the question. The better the answer. The better the world works. EMIA Fraud survey from EY.

And finally on the back page – IFRS 10 is a game changer an insight from ADAA’s Ahmed El Meleegy. August 2015

The accounting profession was probably responsible for the French revolution.

IASB Board member Steve Cooper says ‘if all your estimates are optimistic your financial statements won’t comply with IFRS.’

How creativity and complexity caused the 2008 Financial Crisis.

ESMA guidelines on Alternative Performance Measures. And finally on the back page – Optimizing capital structure an insight from ADAA’s Ahmed El Meleegy. September 2015

IAS 27 revised. The IASB reinstates equity accounting in separate financial statements.

The future of audit and assurance. Professional skepticism at the heart of the competence of our profession.

Integrated Reporting is not another reporting initiative. And finally on the back page – Arthur Andersen and the seven dwarfs an insight from ADAA’s Khulood Al Reyami. October 2015

Working in the public interest. What does it really mean?

Conceptual Framework. Where does it say in the standard I can’t do this?

Select auditing considerations for the 2015 audit cycle from the Center for Audit Quality. And finally on the back page – Future direction of IFRS an insight from ADAA’s Muhammad Shabbir.

November 2015

The objective of financial reporting is to provide financial information that is useful.

What kind of standards should the IASB write?

Trust in the profession is more fragile than ever says the ICAEW.

Integrated thinking or integrated reporting? And finally on the back page – What is the Regulator thinking an insight from ADAA’s Steven Ralls. December 2015

Coming soon changes to IFRS that will impact you!

Before IFRS there was no comparability.

Raising the bar in financial reporting.

Audit quality inconsistent across the Big Four firms. And finally on the back page – Fair value measurement an insight from ADAA’s Ahmed El Meleegy.

IFRS news, updates from ADAA, IASB and the Accounting Profession January 2015

WHAT’S NEW FROM THE IASB?

To boiler plate or not to boiler plate that is the question?

The IASB dreams of perfect disclosure.

IAS 1. Narrow scope but meaningful amendments!

IAS 7 Exposure Draft proposes a new reconciliation.

Applying the Consolidation Exception.

Amendments to IFRS 10, IFRS 12 and IAS 28.

No convergence on lease accounting After several years of trying, complete convergence on lease accounting has ultimately failed to materialize.

IAS 40. Accounting for a structure that lacks the physical characteristics of a building.

And finally on the back page Revenues and value an insight from ADAA’s Steven Ralls.

To boiler plate or not to boiler plate that is the question? The IASB dreams of perfect disclosure. It was June 2013 when Hans Hoogervorst delivered the IASB’s 10 point plan to break the boiler plate. 18 months on and the IASB is starting to deliver on its promise. The IASB’s Disclosure Initiative of agreed changes to IAS 1 is published. Effective 2016 and can be early adopted.

IAS 1: Described as a narrow scope amendment but actually it is quite a radical change. The words ‘as a minimum’ are deleted!! Those three words in IAS 1 affected the whole philosophy of preparing financial statements. If a standard said these are the disclosure requirements then that was it. It was far safer to leave immaterial disclosure in than to leave it out and risk being wrong.

There are three key areas to consider;

Information should not be obscured by aggregating or by providing immaterial information. Materiality applies to all parts of financial statements, even to specified disclosures required by a standard.

Line items to be presented in the statement of financial position and the statement of profit or loss and other comprehensive income can be disaggregated and aggregated as relevant. Guidance is provided on the use of subtotals.

The amendments clarify that understandability and comparability are key considerations when determining what should be in the notes and the order of them.

eIFRS users can access the IASB project page here. Not an eIFRS user? Access Deloitte’s IFRS in Focus here.

IAS 7 Exposure draft: proposes a new reconciliation. The IASB proposes that companies should provide a reconciliation of their opening and closing balances of liabilities and assets related to their financing activities. This will allow investors to clearly see movements in a reporting period that result from:

cash flows from financing activities;

the effects of mergers and acquisitions (e.g. obtaining or losing control of subsidiaries or other businesses); and

other non-cash changes (such as the effects of foreign exchange and changes in fair value).

The IASB believes the changes will address commonly cited investor concerns with debt disclosures enabling investors to better understand a company's financial position and liquidity and improve the transparency of a company's ability to use its funds.

Hans Hoogervorst says: “There is a real appetite for improving disclosure in financial reporting. While problems with disclosures cannot be solved by the IASB alone, we do have an important part to play. Today’s announcement shows that we intend to deliver on this challenge.” More details are available on IASB website here.

IAS 40. Accounting for a structure that lacks the physical characteristics of a building. An odd choice you may think! The rental of a telecoms tower was the example being considered by the IASB. It doesn’t have walls or a roof, but it can and is rented to tenants. The IFRIC referred the issue to the IASB whom after reviewing the research of the IASB staff decided there was limited diversity in practice and not to take deliberations further. So is that a NIFRIC or a NIASB? Read the IASB Update here.

Amendments to investment entities requirements Key points

A parent entity that is a subsidiary of an investment entity is exempt from presenting consolidated financial statements when the parent investment entity measures all of its subsidiaries at fair value.

Only a subsidiary that is not an investment entity itself and provides support services to the investment entity is consolidated. All other subsidiaries of an investment entity are measured at fair value.

A non investment entity parent can retain the fair value measurement applied by the investment entity associate, or joint venture to its interests in subsidiaries.

More details available on the IASB and EY websites.

No convergence on lease accounting After several years of trying, complete convergence on lease accounting has ultimately failed to materialize. The general perception (or is it the lobbyist’s view) is that the IASB favors a single lease model whereas FASB prefers a dual model with leases classified in a similar way to current leasing requirements. A standard on accounting for leases is expected towards the end of 2015.

Ian Mackintosh, Vice-Chairman of the IASB said; “Convergence was not a perfect process but it was a good one and we achieved a great deal. The similarities between the two sets of Standards are bigger than the differences.”

For more details and the results of IASB and FASB recent meeting see the lease project page and EY’s publication.

ADAA’s hot

topics

The IASB is

located in

Cannon

Street,

London

WHAT’S NEW THIS MONTH

WHAT’S NEW FROM THE ACCOUNTING PROFESSION?

And finally

please turn

the page

for ADAA’s

monthly

accounting

insight…

ADAA IFRS digest

IFRS news, updates from ADAA, IASB and the Accounting Profession January 2015

Revenue and value an insight from ADAA’s Steven Ralls

Happy New Year 2015.

The annual reporting race is underway. Regulators, Auditors and Accountants are lining up around the world. Who will win the reporting race this year?

We have had some new standards, some recently effective, some not effective for a couple of years but can be early adopted. Will they make a difference? To borrow a phrase from an economist - It depends!

2014 brought us some things we did not expect and certainly some things we didn’t budget for. ADX entered the year with ADI at 4,400 and it departs at about the same level. At one time it was up nearly 20% and then the oil price fall brought investor sentiment and with it ADI tumbling down. But no one invests in equities for the short term do they? An investment made in 2009 would have doubled in value by today. Whereas an investment made in 2006 would have lost a third! See ADX’s 10 year chart here. Hindsight is a wonderful thing and it is always easier to be clever after the event, so what can we learn?

Why the focus on ADX? It doesn’t have to be ADX we could have chosen any stock market. And equally we could have chosen a non listed entity to make our point. There may be many things that affect an entity’s valuation including things that the entity has no control over but there is also one thing that an entity does have control over that affects its valuation and that one thing is information about itself.

Controlling what information is released, how and when it is released and how it is presented impacts valuation. The Accountants Code of Ethics starts – “a distinguishing mark of the accountancy profession is its acceptance of the responsibility to act in the public interest.” It is clearly in the Public Interest to ensure that (as far as is possible) valuations are materially correct from the shareholder, investor, creditor, customer, employee’s perspective, It matters not whether the entity is listed or not. The Code of Ethics continues: “Therefore a professional accountant’s responsibility is not exclusively to satisfy the needs of an individual client or employer.” This means sometimes the Accountant, Auditor, Regulator may find themselves involved in some difficult conversations.

Shareholders naturally like to see management delivering steady improving performance and management targets being hit. It is human nature to embrace stability. We know from our ‘fight’ or ‘flight’ reaction to shocks that volatility is unnerving.

The ADTF met last week and revenue was the topic for discussion. Not so surprising perhaps given the new revenue standard. And also because we have been following the Tesco supermarket story. Economia article here.

All ADTF’s attendees have produced their IFRS 15 guides: BDO, Deloitte, EY, KPMG, PWC, and the IFRS Foundation has their slide deck from their Special Interest Session Revenue. And PWC’s Dave Walters provides a seasonal uptake on the standard (page 3) 'Santa's other present' All are very Informative publications and they certainly bring alive how much more complicated revenue transactions have become.

Complication of course brings with it judgement and judgement involves estimation. Estimates are by their nature wrong, so great care is required with estimates – ask your builder!

In May 2010 COSO published its findings looking at cases of fraudulent corporate reporting among US public companies for the ten year period 1998 to 2007. In 60% of all cases revenue was misstated. Revenue is a key number for investors. Revenue growth and growth ahead of the market is an indicator of the relative competiveness of an entity which helps to drive valuation.

A significant part of our ADTF discussion concerned payments received from a supplier. IFRS 15 clearly catches these payments in the supplier’s reporting because they are picked up in determining the transaction price with the customer. Paragraph 48 refers to variable payments, financing, non cash consideration and consideration payable to a customer. The test to pass in IFRS 15 is higher than the probable test in IAS 18. The test in IFRS 15 is highly probable. Thus when a supplier offers a consideration in the supply of goods or services that consideration is more often than not either recognised as a discount on supply or is deferred and recognised over the period of supply of product or service to the customer.

In the purchaser’s reporting there is no accounting standard to turn to for dealing with cash or non cash consideration receivables from inventory suppliers (why would there need to be you might ask?). However there is in IAS 16 for the acquisition of capital assets, it says link the contracts, unless they are obviously not linked.

The conceptual framework defines income and expenses and says that they are recognised by applying the matching basis. IAS 8 says management should apply judgement by applying other IFRS by analogy or looking to other GAAP. Presumably that means getting to a matched position. However this is where the accounting structuring specialist will start to find the gaps in the standards and when the infamous one liner pops out: “where does it say in the standard that I can’t do this?”

There are always two sides to a transaction so when suppliers made payments to Premier Foods branded by the UK press as a ‘pay to stay’ scheme, was it an investment by the supplier to grow their business with Premier, or was it just another discount? We have not seen a restatement of Premier Foods accounting so presumably they booked the payments as a discount. However, the day the news broke Premier’s share valuation fell 7%. Why? The company said the investment scheme was not understood and is being wound down. The financial press speculated it highlighted the burden of debt the Company was carrying. Either way shareholders lost value.

We enter a period where the falling oil price is hurting valuations for many, we have a change in the revenue standard, from which we may not know the outcome until post 31 December 2017. Revenue can be an area of significant judgement and estimation. Appropriate disclosure of changes in accounting and the impact of changes in assumptions on estimations will likely be a key area of investor and regulatory focus this reporting season.

We wish you a successful new year.

IFRS news, updates from ADAA, IASB and the Accounting Profession February 2015

WHAT’S NEW FROM THE IASB?

New and impactful. IASB reaches a critical decision on leases.

The Year in Review. A recap of IFAC viewpoints from 2014.

IFRS IN PRACTICE. BDO address the practical application of IFRS in their publications. IAS 8 requires entities to disclose the impact of the new revenue standard this year or to say that they don’t know. Do you really want to say you don’t know?

It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.’ Investor Update is all about revenue.

Tone at the Top. Key challenges in today’s economic environment.

Choosing prudence. Tips for impairment review of non-financial assets.

And on the back page addressing Audit Quality an insight from ADAA’s Steven Ralls.

New and impactful. The final lease standard should include a disclosure objective; to enable assessment of the amount, timing, and uncertainty of cash flows arising from leases. More from the IASB click here.

The Year in Review. A recap of IFAC viewpoints from 2014.

Strong calls for reform in the government and public sector. IPSASB emphasize the need for greater accountability, accrual based accounting and the adoption of IPSAS as indispensable steps towards meeting the long term needs of society.

Regulatory pressures and changes have global implications. CNCC provide insights into how regulatory changes by the European Commission will have costs and impacts on the global accounting profession. Global accounting standards and practices increases capital markets confidence promoting transparency, comparability, and consistency. EY CEO in “Déjà vu all over again,” urges the global community to refrain from slowing the momentum of global regulatory convergence.

The need for reform of taxation systems. Governments are

finding it difficult to sustain their tax bases, economies are stressed and taxpayers becoming increasingly mobile and sophisticated in arranging their tax affairs.

The need for Integrated Reporting. Financial information alone is not enough! All those charged with financial leadership are encouraged to embrace integrated reporting from the bottom up. Click here to view IFAC’s recap of 2014.

It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.’ IASB Investor Update reports all seem to be talking about revenue! The new standard aims to reduce current diversity in practice. A case in point is the sale of residential real estate in multi-unit developments. IFRIC 15 forced many developers to reverse their percentage of completion accounting interpretation of IAS 18 and recognise revenue on delivery of the unit to the customer. IFRS 15 has opened the door to a return to the percentage of completion method but there are specific and strict criteria that must be met in order to achieve it.

IASB member, Patrick Finnegan provides his views. To view the January 2015 edition click here.

IFRS IN PRACTICE. BDO address the practical application of IFRS in their publications:

New IFRS 15 ‘Revenue from Contracts with Customers’ has a single comprehensive framework to determine how much revenue is recognized, and when. The core principle is that a vendor recognizes revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the vendor expects to be entitled in exchange for the transfer. IFRS 15 introduces a disclosure objective together with significantly enhanced disclosure requirements. IAS 8 requires entities to disclose the impact of the new revenue standard this year or to say that they don’t know. Do you really want to say you don’t know?

IAS 7 Statement of Cash Flows. It is surprising how often the cash flow statement is wrongly presented. This publication helps you address: What is cash? How to deal with hedges. Non-cash items and more.

When is a business combination an asset purchase? This publication helps appraise the accounting, judgments, and difficulties in distinguishing asset acquisition transactions.

Click here to access the full publications.

Tone at the top. KPMG’s 2015 Global Audit Committee Survey reports the issues on the audit committee’s radar. Views on audit reforms are mixed and while confidence in audit quality continues to be strong there is still room for auditors to offer more insight. Audit committees’ views on whether the EU’s audit reforms including mandatory rotation will improve audit quality vary widely with the greatest skepticism in the US. Only 8% view the reforms positively! The greatest areas for external auditors to improve their performance are: offering insights and benchmarking on industry specific issues, helping the audit committee stay up to speed and sharing views on the quality of the financial management team. On internal audit, Audit committees are still looking for greater value. Click here to view KPMG’s 2015 Global Audit Committee Survey.

Choosing prudence. PWC highlight their 5 top tips for completing your impairment review for non-financial assets. Top tip 1: Cash flows must be reasonable and supportable. Forecast revenue, profitability and cash flow growth must be comparable to historical growth and industry peers. Key assumptions in the cash flows need to be disclosed. Sensitivity analysis is even more relevant when the markets are volatile. Click here for PWC’s next 4 tips.

ADAA’s hot

topics

The IASB is

located in

Cannon

Street,

London

WHAT’S NEW THIS MONTH

WHAT’S NEW FROM THE ACCOUNTING PROFESSION?

And finally

please turn

the page

for ADAA’s

monthly

accounting

insight…

ADAA IFRS digest

IFRS news, updates from ADAA, IASB and the Accounting Profession February 2015

Addressing audit quality an insight from ADAA’s Steven Ralls

We will deliver you an efficient, effective and robust audit

How many times have you heard that expression from your audit proposal team? How many times did you receive what you were promised?

You may think that a Regulator is not that much concerned in an efficient audit? Not so we say! Our work (normally) starts when the audit is finished and with so many 31 December year-ends and Whole of Government Accounts to work on, we are always keen to start as soon as we can. So we are interested in your audit being efficient, but we don’t want it to be efficient if it is not also effective and robust.

What makes for an efficient, effective and robust audit?

The answer may come as a surprise for the internet generation, who seem to believe the answer is in their laptop and for much of the audit that is where they will remain for most of their time. The answer is people. Good people make for an efficient, effective and robust audit. Good people in the audit client, good people in the audit team. Good people know what they are doing and why it needs to be done.

Auditors need evidence. Relevant, reliable evidence that is of sufficient quality and quantity. The audit client needs to make sure it is there and that the auditor can access it efficiently. But getting evidence efficiently does not make an audit effective and robust.

An effective and robust audit is one that achieves the Auditor’s objectives:

To discover what is right and provide assurance on that being right, and

To discover what is wrong and advise on how to put it right.

Naturally we all hope that nothing is wrong, but not all transactions are straight forward and systematic. Increasingly sophisticated trading and collaborative risk sharing business activities means management estimates and judgements are required to be made. Estimates are by their nature inherently wrong. So the question the auditor has to answer is how far wrong is it likely the estimate will be? Because if the answer is potentially materially wrong then the estimate will need adjusting, or the auditor will need to consider qualifying their audit opinion. Auditing management’s estimates and judgements is often not straightforward and requires the application of industry and technical accounting skills and experience and also negotiation and intellectual skills. These skills are acquired over time.

IFAC’s International Accounting Education Standards Board (IAESB) is not one that we hear from, or hear about too often. However, we have heard from them now! The IAESB has updated and reissued its eight International Education Standards. The project has taken several years to complete and was driven by the Financial Crisis. All professional accountants, Audit Committees, Heads of Internal Audit and CFOs, should be aware of their content and should be testing, auditing if you like, the interactions they have with professional accountants against the criteria in those standards.

What are the professional competencies required by the IAESB of an Audit Engagement Partner? IES 8 defines them. We could reprint them, but you can read them just as easily here. Perhaps what might be more interesting and more useful is a set of questions you could ask to assess the competencies of your Audit Engagement Partner?

Assessing the Competencies of your Audit Engagement Partner

Technical Competence - Audit

Did the partner lead the identification and assessment of the risks of material misstatement as part of an overall audit strategy? How was it different from last year? What new risks did they assess and why? What were you worried about, what audit work was done that addressed your worries? What specialists did they use? What extras did the specialists bring to the audit? Were the key audit matters they discussed with you and those charged with governance the ones you were expecting? Does the organisation feel that it has been audited? What weaknesses and potential improvements to controls did they report? And how did they document all this? Did they discuss the new audit report required by ISA 700 in 2016? Or did they tell you it’s for listed entities only and the old audit report is good enough for your Public Sector entity? But if it’s the new ‘gold standard’ for some entities should it not apply for all?

Technical Competence - Financial accounting and reporting

How did their IFRS knowledge compare to your finance team? Did they defer to their IFRS desk or did they have the answers to hand? Did they advise on IFRS disclosures your team missed? Or how to ‘cut the clutter’? Were the key audit matters included in the IAS 1.122-125 disclosures?

IES 8 includes six more competency areas including information technology and tax. These are two competencies often delegated to specialists. If they are, did you meet and understand the specialists’ conclusions. IES 8 includes four professional skills and three professional values, What evidence do you have that your audit partner promotes audit quality in all their activities with a focus on protecting the public interest? How many times have you disagreed with your audit partner’s conclusion? When you did disagree who changed their mind and why?

On Page 11 of IES 8 the diagram above is shown. A Professional Accountant is (must be) a member of an IFAC member body. Auditors and Regulators do not need to be, however they mostly are.

If the Professional Accountant already has a duty to protect the public interest why do we need either Auditors or Regulators? The answer is to be found in the 2008 Financial Crisis which few of us spotted. Since then, we professional accountants have all had to up our game. So perhaps the questions we suggest you ask of your Audit Engagement Partner are questions we should also ask of ourselves?

Professional Accountants

Engagement partner

Audit Firm

RegulatorIFAC

Member Body

IFRS news, updates from ADAA, IASB and the Accounting Profession March 2015

WHAT’S NEW FROM THE IASB?

The complexity and length of financial reporting reflects an increasingly complex economic reality.

Debt current or non-current? The IASB proposes changes to classifying a liability.

IFRS 13 disclosure requirements. Challenges with the fair value hierarchy.

Big Data! Concepts and challenges of mining Big Data.

Defining a lease, what’s the big deal? The battle for operating leases continues.

The new frontier. The IASB issued a number of consequential amendments to other IFRSs to address the interaction with IFRS 15.

What the Regulators think! IFIAR publishes third year of findings.

And finally on the back page IFRS 15 – key considerations an insight from ADAA’s Muhammad Shabbir.

The complexity and length of financial reporting reflects an increasingly complex economic reality. “IFRS has had a transformative effect on the quality and consistency of financial reporting around the world however we are not deaf to concerns about increasing complexity and disclosure overload in financial reporting” says Hans Hoogervorst. Derivatives, liabilities that are equity instruments, service concession arrangements that are not leases. If you want simple accounting then stop entering into more and more complex transactions. Impairment testing may be costly but it’s what investors want. Read more here.

Debt current or non-current? The IASB proposes changes to IAS 1 classifying a liability, particularly debt when coming up for renewal. Classification should be based on the entity’s rights existing at the end of the reporting period. The link between the settlement of a liability and the outflow of resources should be clear. Link to IASB here.

Defining a lease, what’s the big deal? It may be more than a decade since Sir David Tweedie’s legendary quote ‘one day I would like to fly in an airplane that is actually in the airline’s balance sheet’ but the IASB continues to press on with its leasing project. The IASB believes a customer leasing assets should recognize assets and liabilities arising from the leases, including those leases that are currently off balance sheet today. With plans to issue a new leasing standard before the end of 2015, the IASB has a long way to go, but is a step closer by agreeing on the definition of lease. A lease is defined as a contract that conveys to the customer the right to use an asset for a period of time in exchange for consideration.

A lease exists, when a customer controls the right to use an identified item - which is when the customer has the exclusive use of an item for a period of time; and can decide how to use it.

The new standard will bring significant change to the accounting for leases, which is perhaps why the leasing industry is being so vocal about it. Read more here on the IASB’s lease project page, and click here to access the summary presentation.

IFRS 13 disclosure requirements. Challenges arise with the fair value hierarchy of IFRS 13 because there are different, in other words more onerous, disclosure requirements for level 3 than level 2, and level 2 than level 1. It is of no surprise that level 3 is a diminutive category.

PWC’s publication provides clarification and guidance on:

The meaning of observable and unobservable inputs;

Key differences between level 1 and level 2 inputs; and

When an unobservable input is significant enough to make the whole fair value measurement level 3. For example investment property valued using an income approach.

Read more here.

Big Data! In this new age, we are presented with a massive amount of information in both our personal and our professional lives. Acquiring the ability to draw insights from the data around us is a key skill. Click here to view EY’s insight to the key concepts and challenges in mining big data.

The new frontier. EY’s publication expands the implications of adopting IFRS 15 past the revenue consequences. One key consideration is the sale of non-financial assets. IFRS 15 amends IASs 16, 38 and 40 to use the conditions of IFRS 15 for the recognition and measurement of gains and losses arising from the sale of non-financial assets that are not an output of an entity’s ordinary activities.

The new standard affects the disclosure of advertising costs resulting from an exchange of rights. IFRS 15 replaces SIC-31 and does not specifically address such transactions. However, IFRS 15 requires that an arrangement has commercial substance in order to be considered a contract with a customer. As for service concession arrangements, IFRIC 12 will refer to IFRS 15 and entities will have to identify the performance obligations in each contract in accordance with the requirements of IFRS 15. Fees, interest and dividends are excluded from the scope of IFRS 15. When it comes to onerous contracts, IFRS 15 replaces IAS 11 and contains no specific requirements to address contracts with customers that are, or become, onerous. Click here to view the discussion in depth.

What the Regulators think! IFIAR publishes its third year of findings. Fair value measurement, ITGC’s and revenue recognition are the top three failings finds the International body of Audit Regulators. IFIAR Global Survey.

ADAA’s hot

topics

The IASB is

located in

Cannon

Street,

London

WHAT’S NEW FROM THE ACCOUNTING PROFESSION?

And finally

please turn

the page

for ADAA’s

monthly

accounting

insight…

WHAT’S NEW THIS MONTH

IFRS news, updates from ADAA, IASB and the Accounting Profession March 2015

IFRS 15 – key considerations, an insight from ADAA’s Muhammad Shabbir

After a very long wait the new revenue standard was issued last year and if you are keeping up with your CPE then doubtless you will have read it and concluded the changes to revenue recognition principles and disclosures are significant. It’s not a short standard either at 87 pages plus 175 pages of Basis of Conclusions and 82 pages of Illustrative Examples!

The new model at a glance

The core principle of IFRS 15 is to recognize revenue to depict the transfer of goods or services to customers in amounts that reflect the consideration (that is, payment) expected in exchange for those goods or services.

The Standard provides a single, principles based five-step model to be applied to all contracts with customers to determine whether, how much, and when revenue is recognized.

To recognize revenue an entity applies the five-step model consistently to contract(s) with similar characteristics and in similar circumstances. Performance obligation is the new accounting catch phrase. Delivering a performance obligation results in revenue. So understanding a performance obligation is vital. We covered the model in our July 2014 IFRS digest issue.

Key considerations in the application of the 5 step model

IFRS 15 provides detailed guidance in applying the standard in certain areas. In particular:

Contract costs

Costs of obtaining a contract are capitalized when such costs are incremental to obtaining a contract (e.g. sales commissions) and are expected to be recovered. When the amortization period for the asset is one year or less, the entity is not required to capitalize the incremental costs to obtain a contract. Costs that will be incurred regardless of whether the contract is obtained are expensed as they are incurred, unless they meet the criteria to be capitalized as fulfilment costs.

Costs of fulfilling a contract are capitalized when they relate directly to a contract, generate or enhance resources that will be used to satisfy performance obligations, and are expected to be recovered.

Capitalized costs are amortized in a manner consistent with the pattern of transfer of goods or services to which the capitalised costs relate. Accordingly, it is possible that the amortisation period may extend beyond the original contract term with the customer.

Accounting for a contract modification

A contract modification is a change in the scope or price (or both) of a contract that is approved by the parties to the contract. If a contract is modified, it must be determined if the modification creates a new contract or if it is to be accounted for as part of the existing contract. A contract modification is treated as a separate contract (prospective treatment) if it results in a promise to deliver additional goods or services which are distinct and the added goods or services are priced commensurate with their standalone selling prices.

Where the modification results in a promise to deliver additional goods or services that are distinct but, are not priced commensurate with their standalone selling prices; the modification is accounted for as a termination of existing contract and creation of a new contract (prospective treatment).

If the contract modification does not involve a promise to deliver additional goods or services which are distinct, it should be accounted for as part of the original contract and would require a retrospective (cumulative catch-up adjustment).

Warranties

Accounting impact depends on the nature of warranty:

Warranties that provide a service to the customer in addition to assurance that the delivered product is as specified in the contract (service-type warranties).

Warranties that promise the customer that the delivered product is as specified in the contract (assurance-type warranties).

When the customer can choose whether or not to purchase the warranty, or the warranty is a service-type warranty, it is accounted for as a distinct performance obligation. Assurance-type warranties are not accounted for as a distinct performance obligation; they are subject to the provisions of IAS 37 i.e. continue to account under existing guidance.

Sale with a right of return

When an entity provides its customers with a right to return a transferred product, it does not represent a separate performance obligation. Instead, the entity is making an uncertain number of sales. Until the right of return expires, the entity is not certain how many sales will fail. Accordingly, the entity does not recognise revenue for sales that are expected to fail as a result of the customer exercising its right to return. An entity recognises the amount of expected returns as a refund liability, representing its obligation to return the customer’s consideration. The potential for customer returns is considered when an entity estimates the revenue because potential returns are a component of variable consideration.

Concluding thought

If you are an IFRS reporter then IFRS 15 will almost certainly be applicable to you. There is a large amount of guidance available on a range of special topics of interest, like guidance on customers’ unexercised rights (e.g. unclaimed loyalty points), licensing, principal versus agent considerations, non-refundable upfront fees, customer acceptance, consignment and bill-and-hold arrangements, to name just a few. IFRS 15 also includes extensive disclosure requirements. An early assessment is key to successfully managing its implementation.

A wide range of comprehensive, technical and industry specific guidance is available in the links below, and this publication from EY is useful for Audit Committee members in fulfilling the entrusted responsibility of overseeing the financial reporting process.

Publication links: KPMG EY Deloitte PwC BDO.

IFRS news, updates from ADAA, IASB and the Accounting Profession April 2015

WHAT’S NEW FROM THE IASB?

The Essentials. A must read for IFRS Reporters. In this issue the IASB highlights the principle to present fairly.

Poll of polls from IFIAR. For three years getting fair value measurement wrong tops the list of Regulators’ findings.

IFRIC Update. If Joint arrangements or significant asset disposals feature in your accounting you must click here.

Double Indemnity. PWC IFRS fair value specialist presents five videos on key matters for IFRS 13 and IAS 36.

I dream of a world where all values are fair.

Tick the box, or Value add? What is your approach? Some of you may feel accounting is complex enough.

Sustainability Disclosures. The Sustainability Accounting Standards Board (SASB) has published five provisional standards.

Mind the GAAP. The IASB has no objection to the use of non-GAAP measures and understands the insight such measures provide.

Accounting for revenue is changing.

Operating leasing days are numbered.

And on the back page What the Regulators Think…

The Essentials. A must read for IFRS Reporters. Aims to increase awareness and enhance insight analyzing financial statements. Structuring specialists beware! In the month we publish our illustrative financial statements the IASB reminds us the principle of reporting is providing a true understanding of the financial performance of the entity. If more lines are needed to disclose material events, add them. If line items are not material, amalgamate them. If your accounting judgment is a fine one, disclose how fine it really is. More here.

Poll of polls from IFIAR. For three years getting fair value measurement wrong tops the list of Regulators’ findings. Sir David Tweedie now Chairman of the International Valuation Standards Council (IVSC), identifies a loophole in the valuation standard: “What IFRS 13 does is say this is how you do a fair value but it doesn't go into the detail.” If you ask a valuation specialist in American, France, UK, UAE to value an asset you get four different answers and with some financial assets the differences are materially large. With Sir David chairing the IVSC this is going to change. Click here for the summary and in full here.

IFRIC Update. If Joint arrangements or significant asset disposals feature in your accounting you must click here.

Tick the box, or Value add? What is your approach? Some of you may feel accounting is complex enough and achieving compliance is itself a laudable goal. But this is not the view of others IFAC reports in the run up to the annual meeting in Davos, 3 Professors call for the accounting profession to develop standards and reporting requirements to deal with the number one risk threatening global stability – lack of water. 92% of water is used by agriculture, 3% by households and 5% by industry. More on the IFAC knowledge gateway.

Sustainability Disclosures. The Sustainability Accounting Standards Board (SASB) has published five provisional standards for the Resource Transformation sector - manufacturing, chemical, aerospace, defence, electrical, containers and packing. 90% of investors identify environmental, social and governance disclosures key to investment decisions. Article here. SASB website www.sasb.org.

Mind the GAAP. The IASB has no objection to the use of non-GAAP measures and understands the insight such measures provide. But Hans Hoogervorst asserts there is bias in selection and presentation. He quotes Warren Buffet “When CEOs tout EBITDA as a valuation guide, wire them up for a polygraph test.” Access the speech here.

Double Indemnity. PWC IFRS fair value specialist presents five videos on key matters for IFRS 13 and IAS 36 fair value cash flow models. The key matters to consider are encapsulated in their highly amusing sonnet below. Click here to view the video series and PWC news here.

I dream of a world where all values are fair.

Robust, objective not just floating in the air.

Based on cash flows with realistic growth.

Supportable, maintainable, in fact a bit of both.

Risk reflected in the discount rate.

Not too low or you will miss-state.

Don’t forget you must disclose.

Or you and your Regulator will come to blows.

Let me leave you with a parting fact.

As in valuation tis hard to be exact.

Always cross check to market figures.

Then twill stand up to your reviewers’ rigor.

Accounting for revenue is changing. The impact on food, drink and consumer goods companies from KPMG. Their conclusion is revenue (and profit) will be deferred. We saw this previously with IFRIC 15’s impact on Construction companies and we disagree with KPMG. Our view is IAS 8.12 would already result in the accounting now proposed. IFRS may have less guidance than US GAAP but if IFRS is silent and US GAAP is not, is the default conclusion of a qualified CPA not to follow US GAAP? More here.

Operating leasing days are numbered. It’s only taken 20 years to get here and we may not see the final standard until the end of 2015. But before Expo arrives in Dubai, Sir David will get his wish “to finally fly in an aircraft that is in the airline’s balance sheet.” So why all the fuss? Why is operating lease accounting so appealing to management? Simple, if you are focused on short term profit. Interest expense is higher in the earlier years of a finance lease which combined with straight-line depreciation of lease assets results in a total lease expense that is higher than operating lease expense in the first half of the lease term. So more operating profit means more profit now, less in the future. Next time management judgement falls on the cusp of operating lease keep that observation in mind. PWC news here.

ADAA’s hot

topics

The IASB is

located in

Cannon

Street,

London

WHAT’S NEW FROM THE ACCOUNTING PROFESSION?

WHAT’S NEW THIS MONTH

And finally

please turn

the page for

ADAA’s

monthly

accounting

insight…

IFRS news, updates from ADAA, IASB and the Accounting Profession April 2015

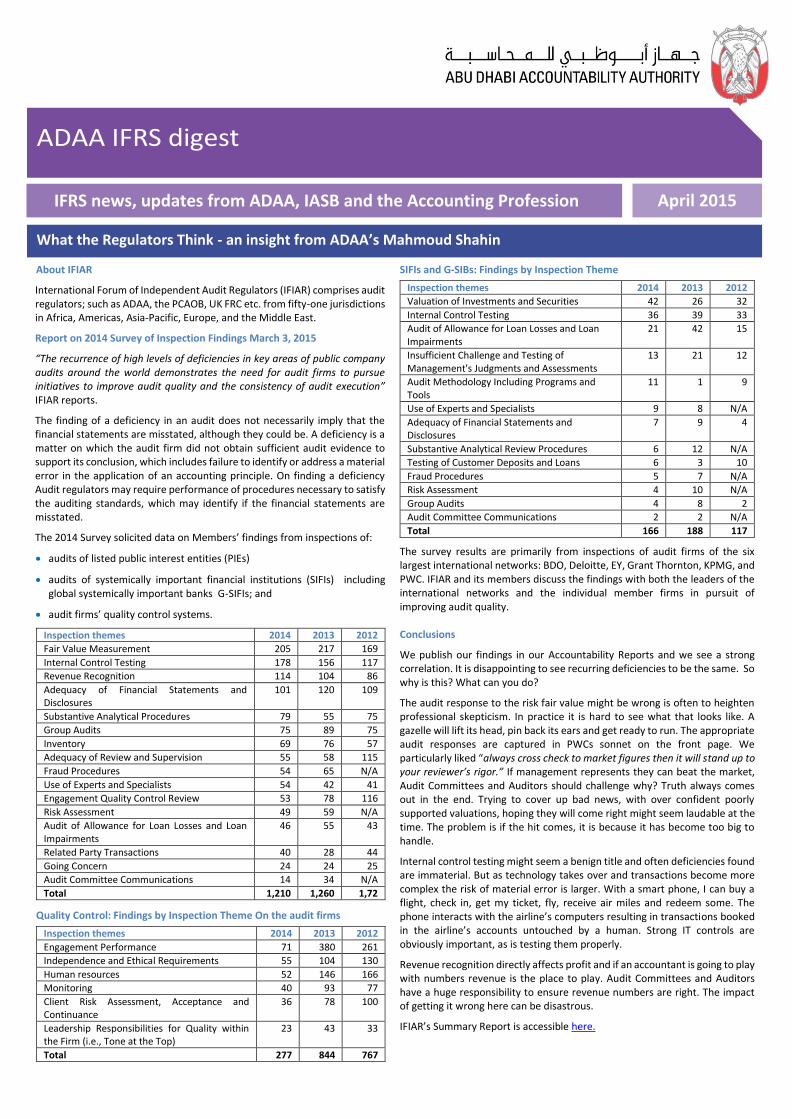

What the Regulators Think - an insight from ADAA’s Mahmoud Shahin

About IFIAR

International Forum of Independent Audit Regulators (IFIAR) comprises audit regulators; such as ADAA, the PCAOB, UK FRC etc. from fifty-one jurisdictions in Africa, Americas, Asia-Pacific, Europe, and the Middle East.

Report on 2014 Survey of Inspection Findings March 3, 2015

“The recurrence of high levels of deficiencies in key areas of public company audits around the world demonstrates the need for audit firms to pursue initiatives to improve audit quality and the consistency of audit execution” IFIAR reports.

The finding of a deficiency in an audit does not necessarily imply that the financial statements are misstated, although they could be. A deficiency is a matter on which the audit firm did not obtain sufficient audit evidence to support its conclusion, which includes failure to identify or address a material error in the application of an accounting principle. On finding a deficiency Audit regulators may require performance of procedures necessary to satisfy the auditing standards, which may identify if the financial statements are misstated.

The 2014 Survey solicited data on Members’ findings from inspections of:

audits of listed public interest entities (PIEs)

audits of systemically important financial institutions (SIFIs) including global systemically important banks G-SIFIs; and

audit firms’ quality control systems.

Inspection themes 2014 2013 2012

Fair Value Measurement 205 217 169

Internal Control Testing 178 156 117

Revenue Recognition 114 104 86

Adequacy of Financial Statements and Disclosures

101 120 109

Substantive Analytical Procedures 79 55 75

Group Audits 75 89 75

Inventory 69 76 57

Adequacy of Review and Supervision 55 58 115

Fraud Procedures 54 65 N/A

Use of Experts and Specialists 54 42 41

Engagement Quality Control Review 53 78 116

Risk Assessment 49 59 N/A

Audit of Allowance for Loan Losses and Loan Impairments

46 55 43

Related Party Transactions 40 28 44

Going Concern 24 24 25

Audit Committee Communications 14 34 N/A

Total 1,210 1,260 1,72

Quality Control: Findings by Inspection Theme On the audit firms

Inspection themes 2014 2013 2012

Engagement Performance 71 380 261

Independence and Ethical Requirements 55 104 130

Human resources 52 146 166

Monitoring 40 93 77

Client Risk Assessment, Acceptance and Continuance

36 78 100

Leadership Responsibilities for Quality within the Firm (i.e., Tone at the Top)

23 43 33

Total 277 844 767

SIFIs and G-SIBs: Findings by Inspection Theme

Inspection themes 2014 2013 2012

Valuation of Investments and Securities 42 26 32

Internal Control Testing 36 39 33

Audit of Allowance for Loan Losses and Loan Impairments

21 42 15

Insufficient Challenge and Testing of Management's Judgments and Assessments

13 21 12

Audit Methodology Including Programs and Tools

11 1 9

Use of Experts and Specialists 9 8 N/A

Adequacy of Financial Statements and Disclosures

7 9 4

Substantive Analytical Review Procedures 6 12 N/A

Testing of Customer Deposits and Loans 6 3 10

Fraud Procedures 5 7 N/A

Risk Assessment 4 10 N/A

Group Audits 4 8 2

Audit Committee Communications 2 2 N/A

Total 166 188 117

The survey results are primarily from inspections of audit firms of the six largest international networks: BDO, Deloitte, EY, Grant Thornton, KPMG, and PWC. IFIAR and its members discuss the findings with both the leaders of the international networks and the individual member firms in pursuit of improving audit quality. Conclusions

We publish our findings in our Accountability Reports and we see a strong correlation. It is disappointing to see recurring deficiencies to be the same. So why is this? What can you do?

The audit response to the risk fair value might be wrong is often to heighten professional skepticism. In practice it is hard to see what that looks like. A gazelle will lift its head, pin back its ears and get ready to run. The appropriate audit responses are captured in PWCs sonnet on the front page. We particularly liked “always cross check to market figures then it will stand up to your reviewer’s rigor.” If management represents they can beat the market, Audit Committees and Auditors should challenge why? Truth always comes out in the end. Trying to cover up bad news, with over confident poorly supported valuations, hoping they will come right might seem laudable at the time. The problem is if the hit comes, it is because it has become too big to handle.

Internal control testing might seem a benign title and often deficiencies found are immaterial. But as technology takes over and transactions become more complex the risk of material error is larger. With a smart phone, I can buy a flight, check in, get my ticket, fly, receive air miles and redeem some. The phone interacts with the airline’s computers resulting in transactions booked in the airline’s accounts untouched by a human. Strong IT controls are obviously important, as is testing them properly.

Revenue recognition directly affects profit and if an accountant is going to play with numbers revenue is the place to play. Audit Committees and Auditors have a huge responsibility to ensure revenue numbers are right. The impact of getting it wrong here can be disastrous.

IFIAR’s Summary Report is accessible here.

IFRS news, updates from ADAA, IASB and the Accounting Profession May 2015

WHAT’S NEW FROM THE IASB?

Efficiency, comparability, communication, performance. Four reasons Japan chooses IFRS.

Why do more than you have to? IAASB revises guidance for information presented in annual reports.

Risk in review. “We are not afraid to work out and work through problems.

Pensions are not dull. IFRIC 14 is confused.

IFRS 15 delayed by the IASB to 2017. Tentative decision.

Leasing, Structured Entities and Joint Arrangements if you have any of these you need to stay up to date with IFRIC.

Impairment Transition Group. New IFRS 9 causes problems early!

And on the back page addressing IFRS 9: Careful planning for big changes ahead - an insight from ADAA’s Muhammad Shabbir.

Efficiency, comparability, communication, performance. Four reasons Japan chooses IFRS. IFRS is mandated in Abu Dhabi. Analysts compare listed companies published information and the value they attribute is reflected in the share price. But what if you are not listed? What if you are unique? The IFRS Foundation publishes its’ Annual Report. Only ten of the sixty pages are required by IFRS, so why fifty more? The answer, particularly if you are a not for profit or public sector entity, is the numbers do not tell the story. The numbers say you spent the cash. They don’t say what value it was!

Unsurprisingly the European Commission is the largest financial supporter of the IASB, next is the USA, the large four audit firms and Japan. Is it right that the standard setters are financially supported by the firms that opine on the standards they write?

Why do more than you have to? IAASB revises guidance for information presented in annual reports. These contain

more narrative and qualitative information than in the past. Such as description of business model and risk exposure. Users attach increasing importance to this information as they look to inform their analysis and understanding. Click here for ISA 720 to understand what your auditor must do.

IFRS 15 delayed by the IASB to 2018. Tentative decision allows more time to understand the collectability considerations investigated by the joint Transition Resource Group, as well as keeping the implementation date with FASB aligned. More here.

Leasing, Structured Entities and Joint Arrangements if you have any of these you need to stay up to date with IFRIC’s deliberations on changes to the accounting here.

We were asked the question! When diversity in practice occurs and IFRIC is asked to opine and it results in a change to a standard being announced. Can you still apply the old (technically discredited) accounting up to the change implementation date? Our answer - Technically, yes! Ethically no!

Risk in review. “We are not afraid to work out and work through problems. We understand companies and economies run through cycles and you better be prepared to live through a down turn and weather the storm. Part of our job is to make sure people understand the choices in the harsh light of day, there are really no free risks. If you create the right risk framework, promote transparency, have strong domain expertise, the right culture, and strong governance, the decisions will take care of themselves.” Ryan Zanin CRO GE Capital. PWC survey executive summary here full report here.

Pensions are not dull. IFRIC 14 is confused. In a defined benefit plan the employer accounts for the obligation to pay benefits. In a defined contribution plan the employer accounts for the obligation to pay contributions. But in certain circumstances IFRIC 14 requires an employer to account for the obligation to pay contributions to a defined benefit plan. In other words it treats it like an onerous contract. More here.

Impairment Transition Group. New IFRS 9 causes problems early!

What is the maximum period for measuring expected credit losses when a contract can be extended at the option of the borrower and the lender?

Most IFRS reporters prepare their provisioning position well before the year end to achieve a hard close. When must that provisioning be updated?

When are lease arrangements and store cards scoped in?

Is collateral included in the assessment of credit risk for guaranteed debt instruments?

What is the maximum period to consider when measuring expected credit losses,

No consensus on the appropriate period for revolving credit facilities. Half thought a shorter period when credit risk mitigation is significant and half favoured the historical behavioural life of the asset.

To find the answers click here to access EY’s coverage of the topic.

ADAA’s hot

topics

The IASB is

located in

Cannon

Street,

London

WHAT’S NEW FROM THE ACCOUNTING PROFESSION?

WHAT’S NEW THIS MONTH

And finally

please turn

the page

for ADAA’s

monthly

accounting

insight…

IFRS news, updates from ADAA, IASB and the Accounting Profession May 2015

IFRS 9 - Careful planning for big changes ahead - an insight from ADAA’s Muhammad Shabbir

1 January 2018, seems a date far in the future? Not really according to Deloitte’s IFRS 9 readiness survey! Some entities will require three years to implement IFRS 9 and some may not be ready in time.

After almost a ten year process, multifaceted, globally drawn out, multiple phased (or should that be fazed?). A hugely prolonged process of exposition, discussion and deliberation and redeliberation. Finally new IAS 39 is born.

The background. Call it a consequence of the financial crisis or part of the IASB’s long term strategic plan, either way IFRS 9 replaces old IAS 39. A standard that was perceived by many as difficult to understand, difficult to apply, difficult to interpret and full of ‘rules’ (it was and it wasn’t). IAS 39 was never really an IASB standard in the first place. Dear old IASC the forerunner to the IASB needed a financial instrument standard to complete the suite of 30 they had agreed with IOSCO would form IAS. Having run out of time in 1999 they cut and paste from US GAAP. A neat solution at the time and we have lived with the consequences ever since.

There has been a systematic approach to IFRS 9 to complete the easy bits quickly and take more time for the harder bits.

Phase 1 – Classification and measurement.

Phase 2 – Impairment

Phase 3 – Hedge Accounting

All phases were added together in a single integrated final standard issued 2014.

The main measurement and presentation requirements? IFRS 9 is built on a logical, single classification and measurement approach to reflect the business model in which financial instruments are managed and their cash flow characteristics. This principle based approach replaces the existing rule based classification and measurement approach.

All financial instruments are initially measured at fair value, plus or minus, in the case of a financial asset or financial liability not at fair value through profit or loss, transaction costs.

Financial assets. Existing IAS 39 categories of held to maturity, loans & receivables and available for sale may sound familiar but they are gone for good. IFRS 9 divides all financial assets into two; those measured at amortized cost, and those measured at fair value. Key points to remember are;

A financial asset is classified and measured at amortized cost if it is held within a business model whose objective is to collect contractual cash flows, rather than to sell the instrument prior to its contractual maturity to realize its fair value changes (Business model test), and the contractual terms of the financial asset give rise to cash flows that are solely payments of principal and interest (Cash flow characteristics test).

A financial asset is classified and measured at fair value through other comprehensive income (FVOCI) if it meets the cash flow characteristics test and is held in a business model whose objective is achieved by both collecting contractual cash flows and selling financial assets.

All other financial assets are classified and measured at fair value through profit or loss (FVTPL).

You may also, at initial recognition, designate a financial asset as FVTPL if doing so eliminates or significantly reduces an accounting mismatch that would otherwise arise. The decision to designate a financial asset as FVTPL is irrevocable. Similarly, if an equity investment is not held for trading, an entity can make an irrevocable election at initial recognition to measure it at FVTOCI with only dividend income recognized in the income statement.

Financial liabilities. No change from existing basic measurement and classification requirements. Categories are FVTPL and amortized cost. Financial liabilities held for trading are measured at FVTPL, and all other financial liabilities are measured at amortized cost unless the FV option is applied. The designation as FVTPL at initial recognition is irrevocable.

Hedging. The new model introduced under IFRS 9 provides a more principle based approach that aligns hedge accounting more closely with risk management. Key points to remember are;

Fair value, cash flow and net investment in a foreign operation still remains as the principal types of hedging relationship.

No more “bright lines” for assessing hedge effectiveness. The highly effective (80% to 125%) threshold is replaced with new requirements focusing on the need for an economic relationship between the hedged item and hedging instrument, a requirement for credit risk not to dominate the value changes resulting from that economic relationship, and a hedge ratio that reflects the relationship between the quantities of the hedged item and hedging instrument actually used for risk management purposes.

IFRS 9 has retained the periodic effectiveness assessment criterion (at least, at each reporting date, or when circumstances change). However, the effectiveness test is only a forward-looking test (i.e., no retrospective test is required).

Voluntary de-designation of a hedging relationship is allowed under IAS 39, however, under IFRS 9 an entity cannot de-designate and thereby discontinue a hedging relationship unless the risk management objective for such relationship changes.

Ability to designate specifically identifiable and reliably measurable risk components of non-financial items as hedged items.

More flexibility in hedging groups of dissimilar items.

Impairment. Many things have been said about the incurred loss model delaying booking of losses, IFRS 9 uses an expected-loss model. Some say this is semantics and the difference is a question of the quality of evidence? A loss is a loss. The problem banks have is recognition is a painful business and it is the last thing they (rightly) wish to do. However economies go in cycles, booms lead to busts and loans made in boom times will inevitably for some lead to loss in a downturn. IFRS 9 might be perceived as a return to smoothing. Loss provisions are to reflect a probability-weighted outcome, time value of money and reasonable and supportable information.

Own credit. Gains arising from the buyback of own debt is not recognised in profit or loss.

A final thought. The accounting profession seems to believe the new disclosures, measurement and presentation principles and expected loss model may require significant changes to current systems and processes we believe banks already have this information. More here from Deloitte PWC EY KPMG.

IFRS news, updates from ADAA, IASB and the Accounting Profession June 2015

WHAT’S NEW FROM THE IASB?

It ain’t broke, but it’s due for an update. Hans Hoogervorst is clearly fed up with some accounting practitioners by their interpretation of the IASB’s IFRS.

What do Etihad and the United Kingdom’s Royal Mail have in common? State Owned Enterprises are they catalysts for public value creation?

And on the back page IFRS 10 is a game changer an insight from ADAA’s Ahmed El Meleegy

The mystic of offsetting revealed. The IASB Essentials publication provides an insight into bank leverage.

Too big to fail. Decisions reached on amendments to IFRS 15.

New age of regulation. Creation of a globally connected platform.

Fraud and corruption – the easy option for growth? We like EY’s new strap line – The better the question. The better the answer. The better the world works.

It ain’t broke, but it’s due for an update. Hans Hoogervorst, says; “A solid Conceptual Framework is essential because it shapes the decisions the IASB takes when developing Standards.”

The Conceptual Framework helps IFRS users to understand the IFRS accounting standards to ensure their correct application and in doing so promotes transparency and accountability of financial reporting.

Clearly the IASB are fed up with the ‘where in the accounting standard does it say I can’t do this’ somewhat myopic approach by some practitioners in interpreting their standards. Consistent high quality application of IFRS is what underpins the benefits it brings. Playing with the numbers should be left in the playground. The IASB’s proposed amendments and the view of Hans’ are here. And click here for the project in more detail.

The mystic of offsetting revealed. The IASB’s Essentials provides a unique perspective into the issue of bank leverage comparing different reporting frameworks. In solving the riddle the IASB provides guidance to offsetting in IAS 32.42, and disclosure requirements in IFRS 7.13A. More here.

Too big to fail. The IASB propose amendments to IFRS 15 for principal or agent considerations. More here

New age of regulation. IFRS Taxonomy is a guide to help market regulators accurately, clearly and consistently identify information that must be prepared in accordance with IFRS. The Taxonomy is applied to electronic filings of IFRS financial information (e.g. electronic submissions of IFRS financial statements). Click here for the IASB’s synopsis and here for the project resources and materials.

What do Etihad and the United Kingdom’s Royal Mail have in common? The economic reality is that at different times Government must step in. Fannie Mae, Freddy Mac, AIG, RBS, Lloyds are just a few examples. But whatever the motivation the future SOE needs to be much more actively owned and managed argues PWC. The SOE’s advantage is in furthering social outcomes, providing physical infrastructure, and creating stability in times of crisis. Nevertheless, the burning question is do SOEs add value to society, now and for the future? Corruption, bribery, political and income instability, mistrust, and inefficiency are major hindrances to SOEs creation of social value. To overcome these challenges, SOEs must institutionalise best practices in ownership and management. PWC identify the 4 Cs: Clarity, Capacity, Capability and Commitment to integrity as four key tests for Board of Directors and Executive Management teams. To pass the tests SOEs must be role models for good reporting practices: Adopt integrated reporting, avoid aggressive accounting and ‘pushing the envelope’ accounting tricks. Transparency and accountability are paramount. Timely and reliable reporting of performance and activities and proper challenge by external auditors are prerequisites for building trust.

Fraud and corruption – the easy option for growth? We like EY’s new strap line – The better the question. The better the answer. The better the world works. Simple, neat and straightforward. If we ask the right questions, we get the right answers. People doing the right things for the right reasons have no reason to hide. What is alarming is that:

60% of those surveyed feel corruption is widespread.

Nearly 40% agree that companies report their financial performance better than it is.

A significant minority considered offering cash payments and gifts as justifiable.

14% say booking revenue from rebates with suppliers early can be justified.

27% say negotiating retrospective rebates with suppliers can be justified.

Reporting financial performance better than it is, is fraud. Offering improperly cash or gifts for favours are corrupt acts as FIFA is discovering. Tesco and Rolls Royce found to their shareholders cost that transactions with suppliers do not generate revenue. Negotiating with suppliers to obtain better terms is fine but transactions with them go through cost of sales. And be careful of when they are recognised. Read more in EY’s EMIA Fraud Survey 2015.

ADAA’s hot

topics

The IASB is

located in

Cannon

Street,

London

WHAT’S NEW FROM THE ACCOUNTING PROFESSION?

WHAT’S NEW THIS MONTH

And finally

please turn

the page

for ADAA’s

monthly

accounting

insight…

IFRS news, updates from ADAA, IASB and the Accounting Profession June 2015

IFRS 10 is a game changer an insight from ADAA’s Ahmed El Meleegy

Power arises from rights.

No, no it’s not a typo we meant to say it twice. Why do parents have the right and the power to make life changing decisions for their children? Why do government have the right and power to make life changing decisions for their citizens? Because they have the right (legal, emotional, financial) and the power to enforce it.

Understanding what rights you have is essential to understanding the power you have. IFRS 10 Appendix B.47 states: “When assessing control, an investor considers its potential voting rights as well as potential voting rights held by other parties, to determine whether it has power. Potential voting rights are rights to obtain voting rights of an investee, such as those arising from convertible instruments or options, including forward contracts.”

This paragraph explains the meaning of potential voting rights but the word we really need to consider is the word considers. The Oxford English dictionary defines considers as; think carefully about (something), typically before making a decision.

This paper considers what should be thought about before deciding if potential voting rights have an effect on control.

There are three key points to address:

Whether the potential voting rights are substantive.

The purpose and design of the instrument that includes the potential voting rights, and the purpose and design of any other involvement the investor has with the investee.

Other voting or decision rights the investor holds and whether those rights give the investor other decision making rights relating to the investee’s relevant activities.

How substantive are potential voting rights?

This could be determined through assessing Exercise price, Financial ability Exercise period

Exercise price or conversion price— One of the most significant changes between IFRS 10 and IAS 27 in evaluating whether an option can give power is that the exercise price (or conversion price) can and should be considered, because it might represent a barrier to exercise:

Deeply-out-of-the-money. Because it does not make economic sense to exercise them, generally these would not be considered substantive. However, this is not a forgone conclusion.

Out-of-the-money (but not deeply). Judgement is required to assess whether the cost of paying more than market value is worth the potential benefit of exercise, including the exposures to variable returns that are associated with exercising the option. Companies are more often than not purchased at a premium to their market capitalisation. So great care is required in this assessment.

In–the-money (and at market options). Normally these are considered substantive. For an at market option, consideration is given as to whether the option conveys rights that differ from those available to third parties in an open market.

Financial ability — The financial ability of an investor to pay the exercise price should be considered when evaluating whether an option is substantive, because there may be an ‘economic barrier,’ as contemplated

by IFRS 10. This was previously prohibited under IAS 27.

Exercise period — To have power, an investor must have existing rights that provide a current ability to direct an investee’s relevant activities. This implies an option be currently exercisable to give power. However, under IFRS 10, an option can give an investor the current ability to direct an investee’s relevant activities even when it is not currently exercisable, unlike in IAS 27. This is because the term ’current‘ is used more broadly in IFRS 10 than in IAS 27. Although ’current‘ often means ’as of today‘ or ’this instant‘ in practice, the IASB’s use of the term in IFRS 10 broadly refers to the ability to make decisions about an investee’s relevant activities when they need to be made. This is a huge clarification and means that where a significant minority stake is being acquired, perhaps because the acquiree requires urgent funding, the control issue needs to be carefully considered.

Purpose and design.

When assessing an instrument’s purpose and design, an investor should consider the instrument’s terms and conditions, including the apparent expectations, motives and reasons for agreeing to those terms and conditions. If the terms are such that the holder of the potential voting rights could not conceivably be expected to exercise them, they are disregarded.

Other voting or decision rights.

After considering current and potential voting rights an investor may conclude it has power over an investee. However, this might not be true if a third party has potential voting rights exercisable or convertible when the decisions about the relevant activities need to be made, which would have the effect of diluting the investor’s power. Hence, when performing the control assessment it is necessary to consider all potential voting rights in the investee held by other parties.

The Abu Dhabi Technical Forum chaired by ADAA discussed the issue in the following example:

Entity A is the largest shareholder of Entity B with 29% of the shares. The next two largest shareholders hold 12% and 5% of the shares. No other shareholders hold more than 1%. The shares are listed.

On 20 May 2014 Entity A subscribes for 75% of a fresh issue of perpetual convertible bonds. If converted Entity A holds a majority of the shares and voting rights. The bonds have no set conversion date and Entity A has declared that it will only exercise its conversion rights in certain defined circumstances.

Question: Does Entity A have a controlling interest in Entity B?

The Answer: Yes Entity A has control by virtue of the conversion rights in the perpetual bonds meaning it can achieve a majority voting position. The example does not say what the certain defined circumstances are that would cause Entity A to convert the bonds however it must obviously be circumstances in which it needs to protect its investment by having the power to direct its returns.

Read more in EY Publication: Challenges in adopting and applying IFRS 10 and PWC Publication: In Depth A look at current financial reporting issues.

IFRS news, updates from ADAA, IASB and the Accounting Profession August 2015

WHAT’S NEW FROM THE IASB?

The Reckoning. Financial accountability and the rise and fall of nations. Hans Hoogervorst, Chair, IASB adds to our must read list.

I believe it is very important that management do not prepare financial statements with an optimistic bias. Choosing estimates that are constantly at the optimistic end of the range of plausible values is unlikely to result in financial statements that faithfully represent that business says Steve Cooper, Board member, IASB.

How the creativity and complexity of financial systems caused the Financial crisis of 2008. Lord Turner’s Tommaso Padoa-Schioppa Memorial lecture provides insightful observations to what really went wrong. These are complex at times but well worth persevering with.

ESMA Guidelines on Alternative Performance Measures. Disclosure of non IFRS measures can distort financial reports and mislead users.

And on the back page addressing Optimizing capital structure - an insight from ADAA’s Ahmed El Meleegy.

The Reckoning. Financial accountability and the rise and fall of nations. Addressing Paris, Hans refers to Louis XVI’s attempt in 1781 to improve the credit worthiness of France (and the amount he could borrow) by publishing accounts of the state finances. Sadly for Louis ‘the law of unintended consequences’ resulted in the Comte Rendu exposing the cost of the Royal Court was more than half the cost of the military!! The public furor from the accounts means our profession is probably responsible for the French revolution. The Conceptual Framework may seem dull but measurement is not. Historic cost or fair value? More here.

I believe it is very important that management do not prepare financial statements with an optimistic bias. Choosing estimates that are constantly at the optimistic end of the range of plausible values is unlikely to result in financial statements that faithfully represent that business says Steve Cooper, Board member, IASB. Like a bad game of