achieving ukraine's a agricultural potential - oecd · agricultural potential stimulating...

TRANSCRIPT

THE WORLD BANK

Achieving Ukraine's Agricultural Potential

Stimulating Agricultural Growth And Improving Rural Life

Organization for Economic Co-operation and Development & the Environmentally and Socially Sustainable Development Unit, Europe and Central Asia Region, The World Bank

Achieving U

kraine’sAgricultural Potential

THE WORLD BANK

1818 H Street, NWWashington, DC 20433Telephone 202-473-1000Internet www.worldbank.orgEmail [email protected]

OECD2, rue André Pascal F-75775 Paris Cedex 16France

TH

E W

OR

LD

BA

NK

Achieving Ukraine’s Agricultural Potential

Stimulating Agricultural Growth and Improving Rural Life

Joint Publication by the Organization for Economic Co-operation and Development

and the Environmentally and Socially Sustainable Development Unit, Europe and Central Asia Region,

The World Bank

© 2004 The International Bank for Reconstruction and Development / The World Bank 1818 H Street, NWWashington, DC 20433Telephone 202-473-1000Internet www.worldbank.orgE-mail [email protected] in the United States of AmericaFirst Printing: June 2004

All rights reserved.

The Europe and Central Asia Environmentally and Socially Sustainable Development Unit(ECSSD) of the World Bank and the Organization for Economic Co-operation and De-velopment (OECD), distributes this working paper to disseminate findings of work inprogress and to encourage the exchange of ideas among Bank staff and all others interestedin development issues. This paper carries the names of the author(s) and should be usedand cited accordingly. The findings, interpretations, and conclusions expressed herein arethose of the author(s) and do not necessarily reflect the views of the Board of Executive Di-rectors of the World Bank or the governments they represent.

For submission of comments and suggestions, and additional information, including copiesof this report, please contact Iain Shuker at:

1818 H Street N.W.Washington, DC 20433, USAEmail: [email protected]

Cover photos by: Lidia Warring, IFC Ukraine and Yuriy Aleshin and Gennadiy Marychev, Ukraine

A C R O N Y M S A N D A B B R E V I A T I O N S xi

A B S T R A C T xiii

P R E F A C E A N D A C K N O W L E D G M E N T S xv

E X E C U T I V E S U M M A R Y xvii

C H A P T E R

1 Agricultural Sector Performance 1

2 Agricultural Policy Framework 13

3 Domestic Support Measures 23

4 Trade Policy and WTO Accession 51

5 Evaluation of Support to Ukrainian Agriculture 73

6 Land Reform and Farm Restructuring 83

7 Competitiveness and Structural Change in the Agroprocessing Sector 97

8 Rural Livelihoods and Rural Poverty—Assessment and Solutions 115

9 Rural Public Services Infrastructure 135

B I B L I O G R A P H Y 147

A N N E X

1 Commodity Specific Performance Indicators 153

2 Changes in the Tax System for Agricultural Enterprises, 1997-2001 165

3 OECD Indicators of Support to Agriculture: Definitions 167

4 Agricultural Policies and Support for Individual Commodities 171

5 Agroprocessing Sector 191

iii

Contents

LIST OF FIGURES

Figure E.1: Evolution of Producer Support (%PSE) in Ukraine and Selected Countries (1986-2001) xxi

Figure E.2: Dynamics of Gross Agricultural Output in 1990-2001 xxii

Figure E.3: FDI in the Food Industry xxiv

Figure E.4: Distribution of Total per Capita Monthly Income, 2001 (Q1-Q3) xxv

Figure E.5: Housing Amenities in Ukraine (2000) xxvi

Figure 1.1: The Role of Agriculture in the National Economy 2

Figure 1.2: Mineral Fertilizer Application Rates and Changes in Grain Yields 5

Figure 1.3: Major Trends in Physical Volume of Crop Production (1000 tons) 6

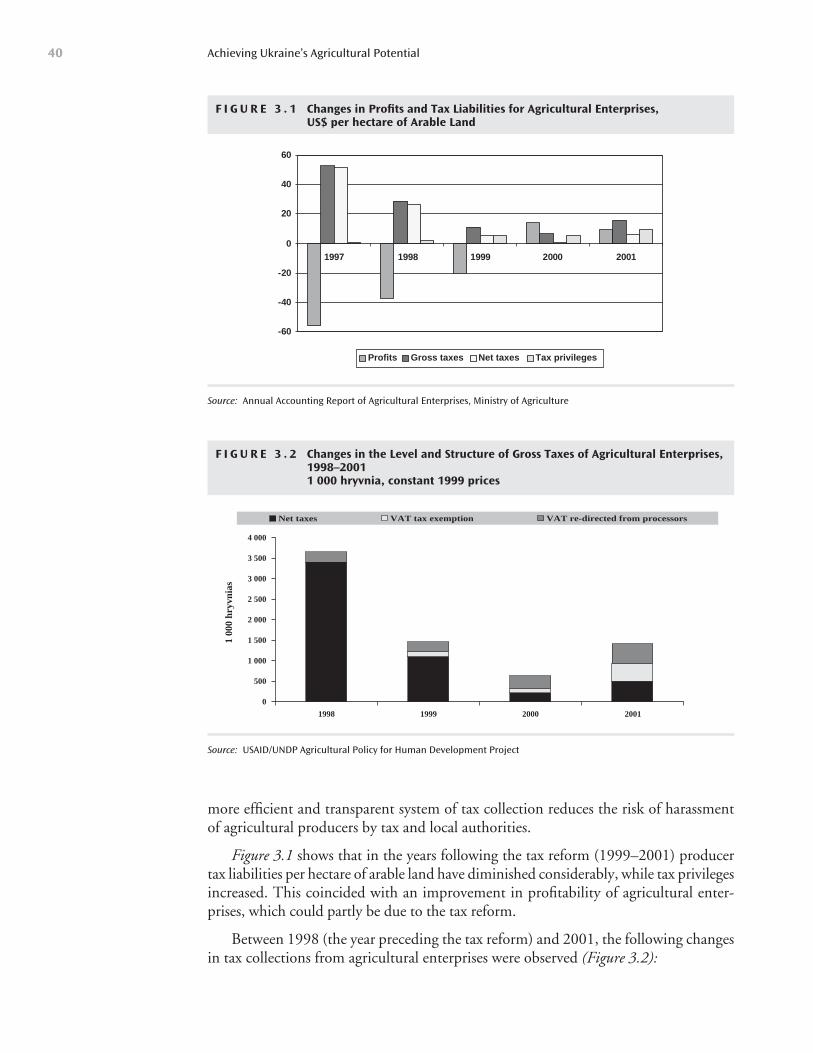

Figure 3.1: Changes in Profits and Tax Liabilities for Agricultural Enterprises 40

Figure 3.2: Changes in the Level and Structure of Gross Taxes of Agricultural Enterprises, 1998-2001 40

Figure 3.3: Composition of Direct Budgetary Transfers to the Agro-food Sector in 1992-2001 49

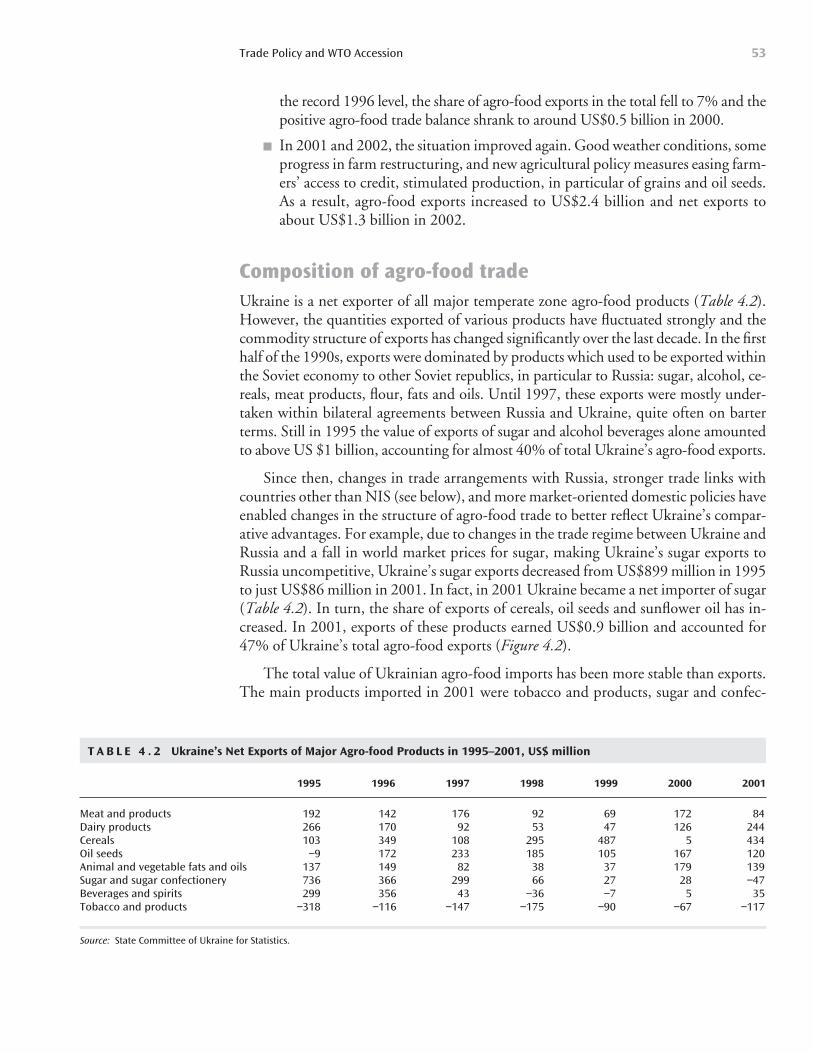

Figure 4.1: Agricultural Trade in Ukraine, 1994-2001 52

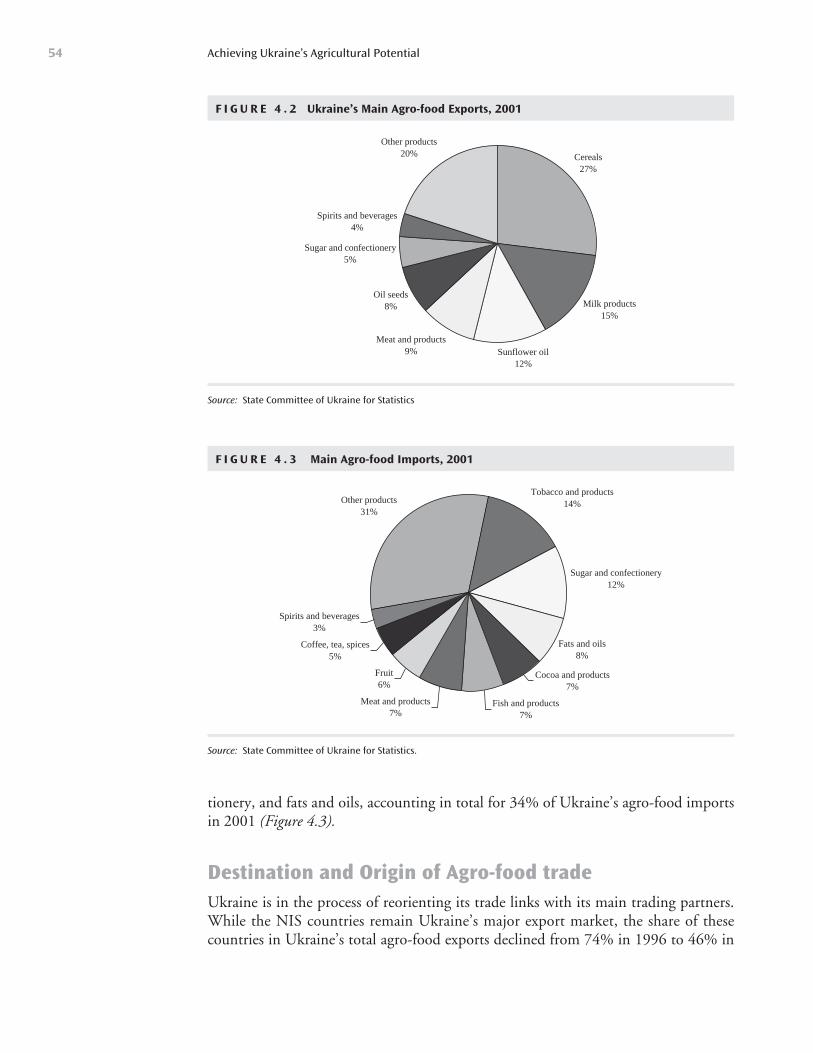

Figure 4.2: Ukraine’s Main Agro-food Exports, 2001 54

Figure 4.3: Ukraine’s Main Agro-food Imports, 2001 54

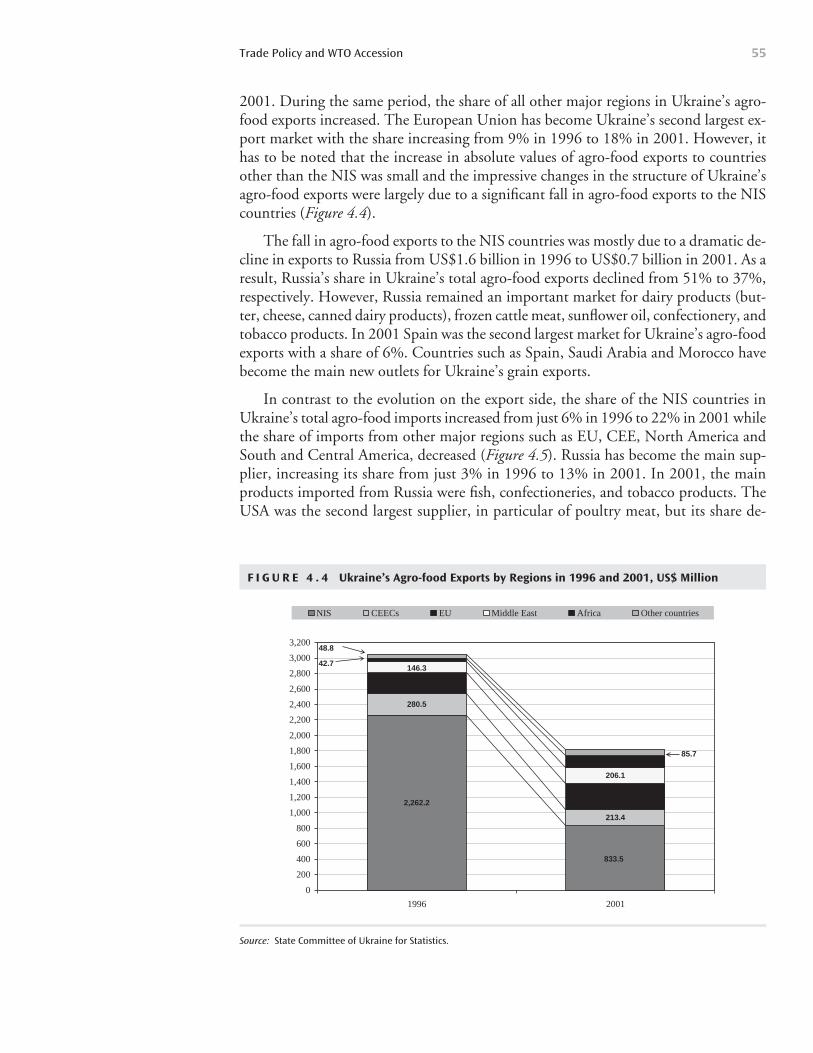

Figure 4.4: Ukraine’s Agro-food Exports by Regions in 1996 and 2001 55

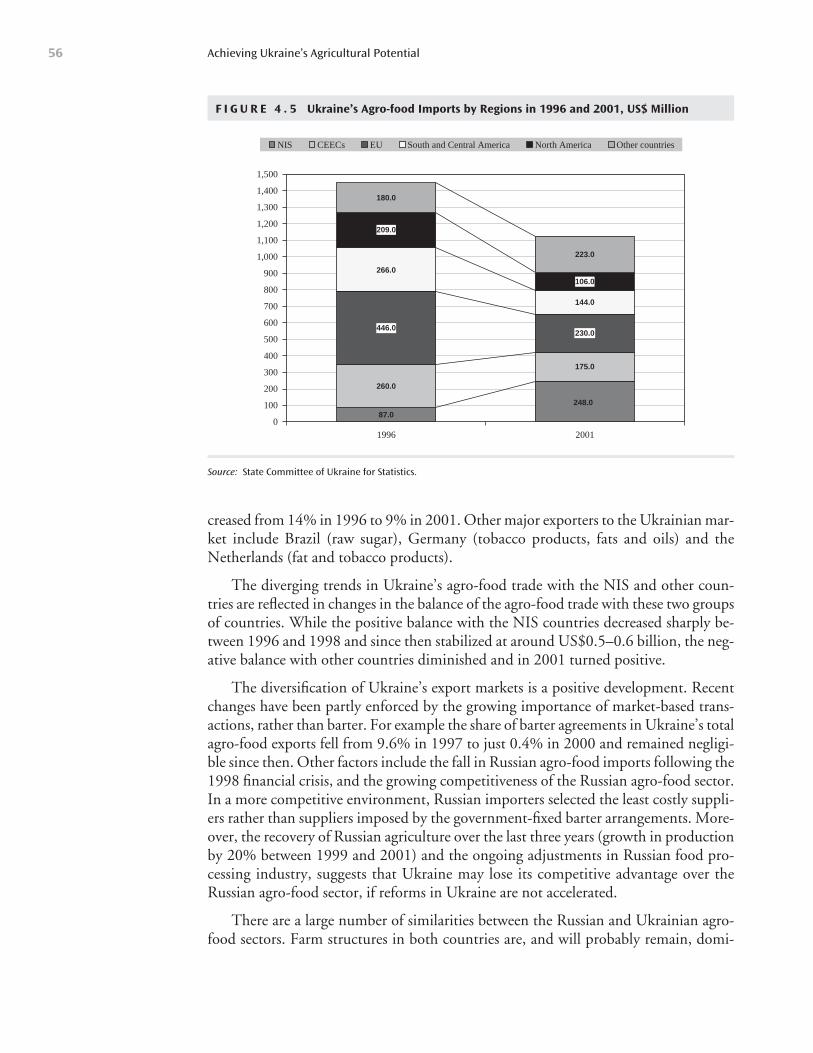

Figure 4.5: Ukraine’s Agro-food Imports by Regions in 1996 and 2001 56

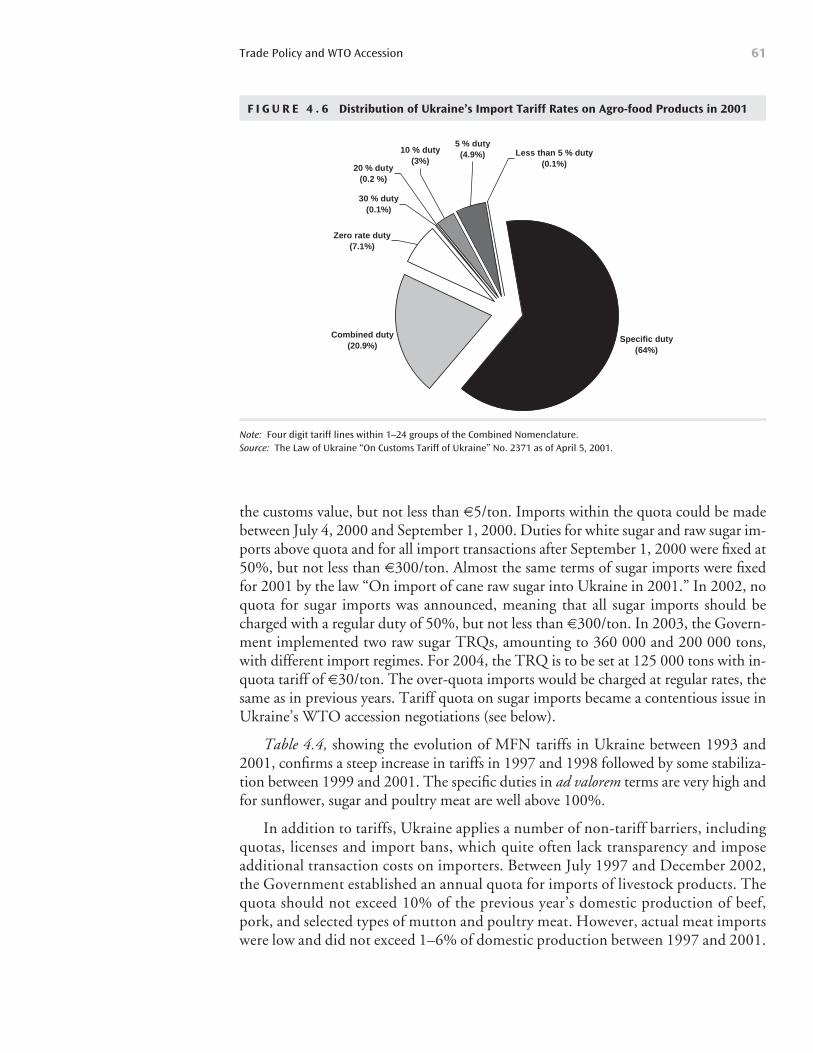

Figure 4.6: Distribution of Ukraine’s Import Tariff Rates on Agro-food Products in 2001 61

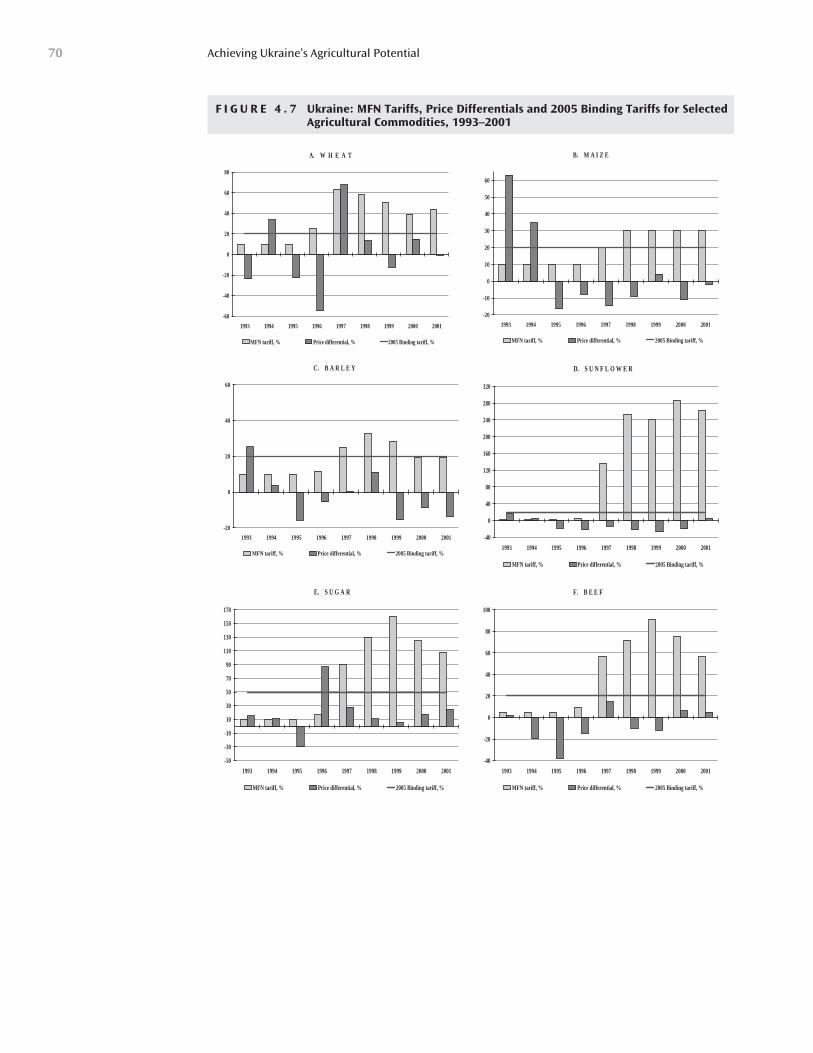

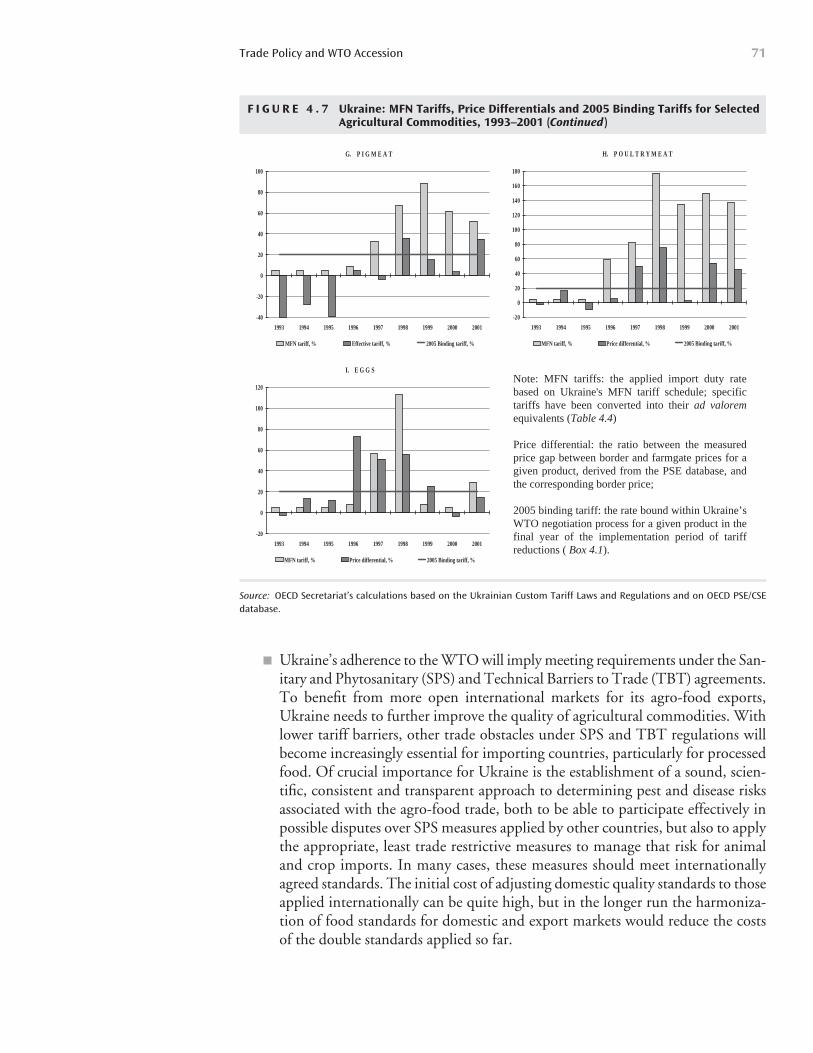

Figure 4.7: Ukraine: MFN Tariffs, Price Differentials and 2005 Binding Tariffs for Selected Agricultural Commodities, 1993-2001 70

Figure 5.1: Evolution of Producer Support (%PSE) in Ukraine and Selected Countries in 1986-2001 76

Figure 5.2: Percentage PSE by Country, EU and OECD Averages in 2000-2001 76

Figure 5.3: Evolution of Consumer Support (%CSE) in Ukraine and Selected Countries in 1986-2001 77

Figure 5.4: Composition of Producer Support Estimate, 1992-2001 78

Figure 5.5: Total Support Estimate in Ukraine and Selected Countries, 1999-2001 79

Figure 5.6: Ukrainian %PSE by Commodity in 2001 80

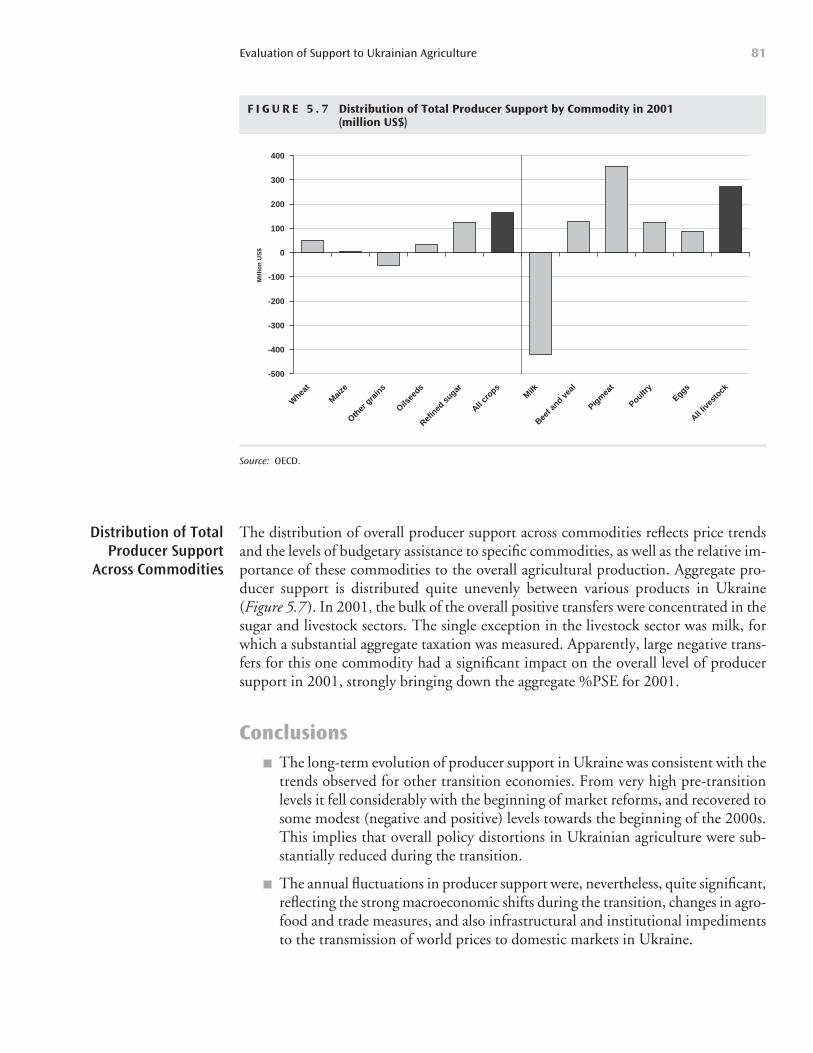

Figure 5.7: Distribution of Total Producer Support by Commodity in 2001 81

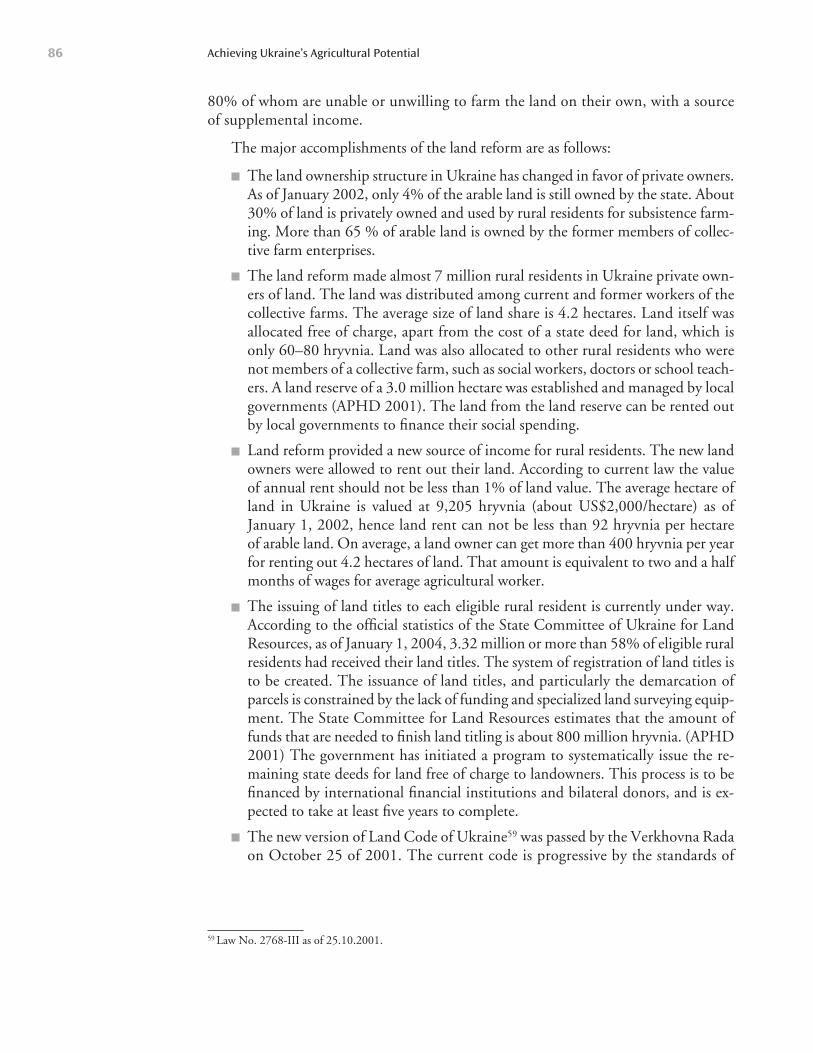

Figure 6.1: Length of Land Rental Agreements (years) in 2000 87

Contentsiv

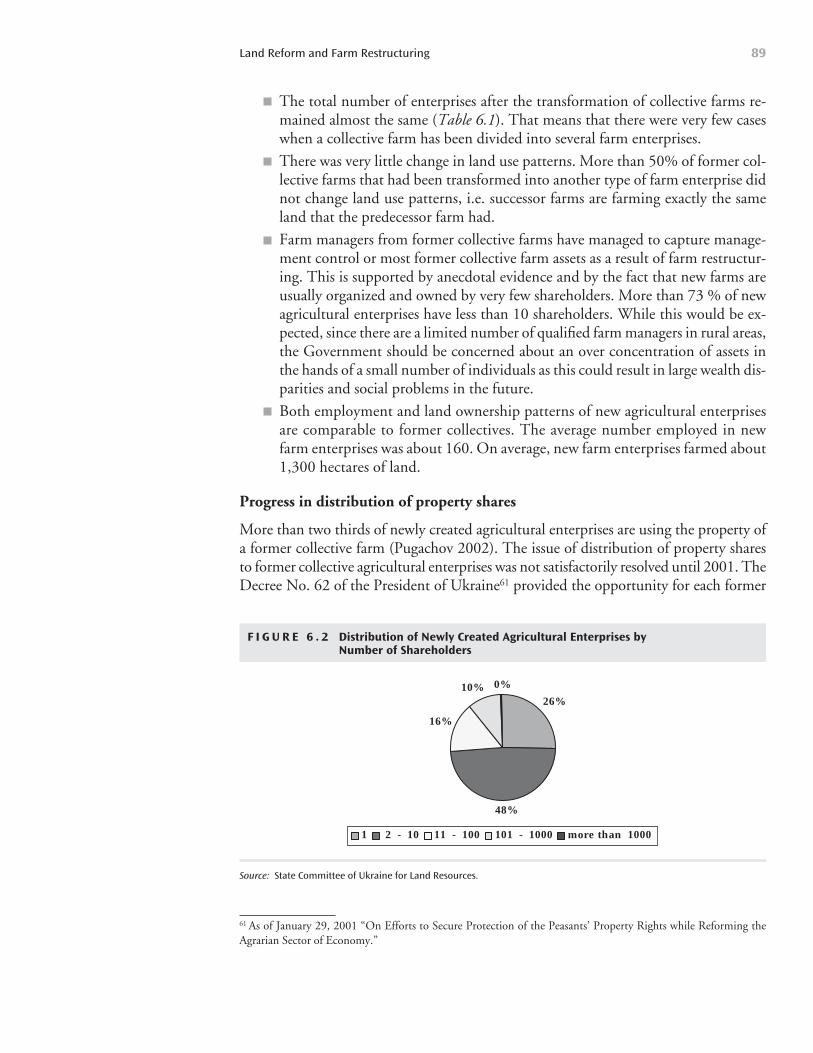

Figure 6.2: Distribution of Newly Created Agricultural Enterprises by Number of Shareholders 89

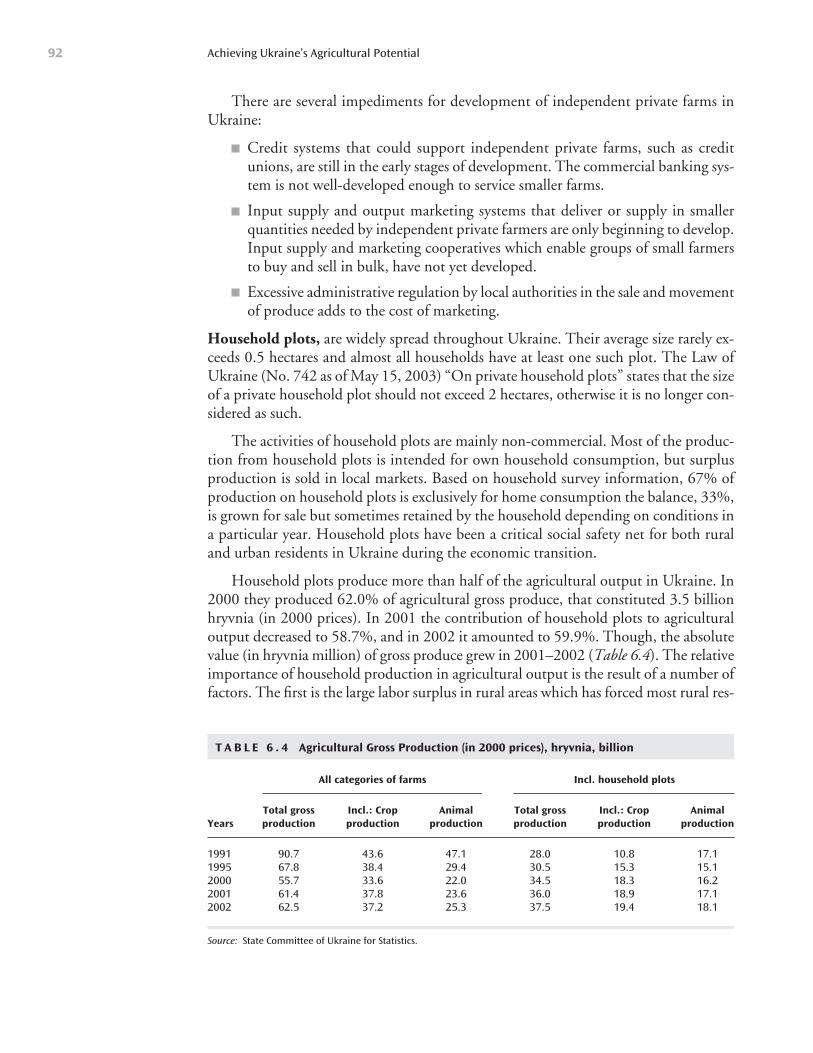

Figure 6.3: Profitability Indicators for Farm Enterprises 91

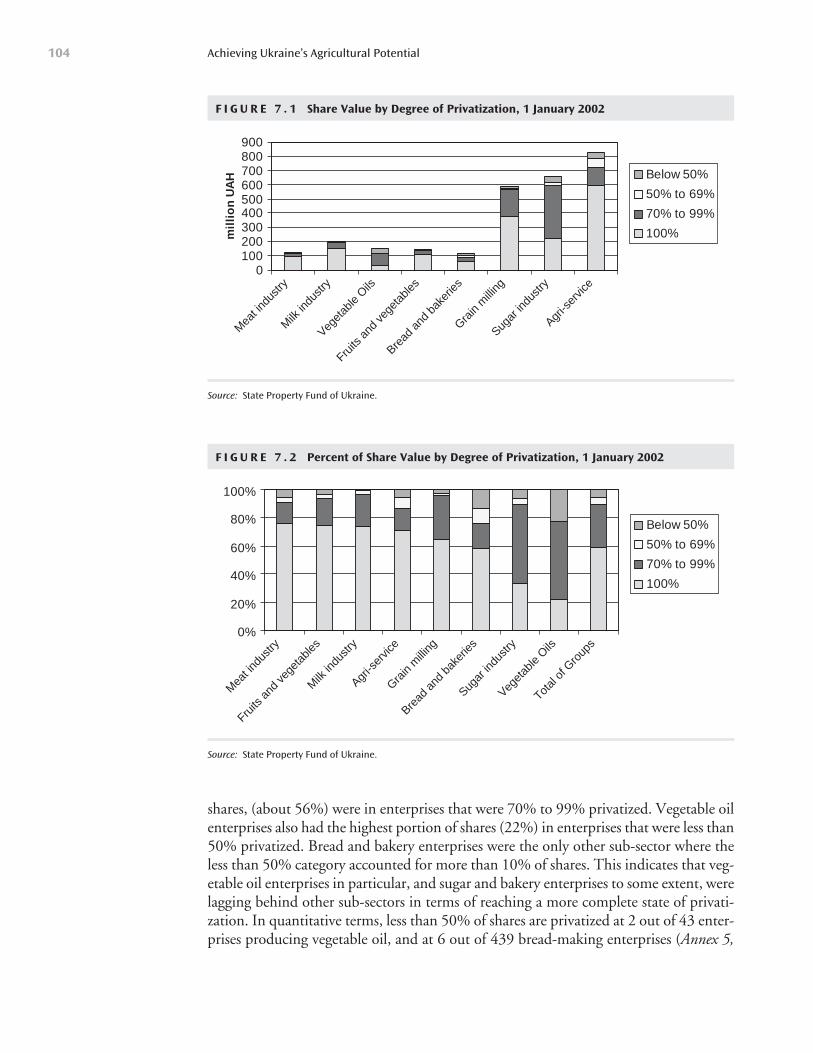

Figure 7.1: Share Value by Degree of Privatization, January 1, 2002 104

Figure 7.2: Percent of Share Value by Degree of Privatization, January 1, 2002 104

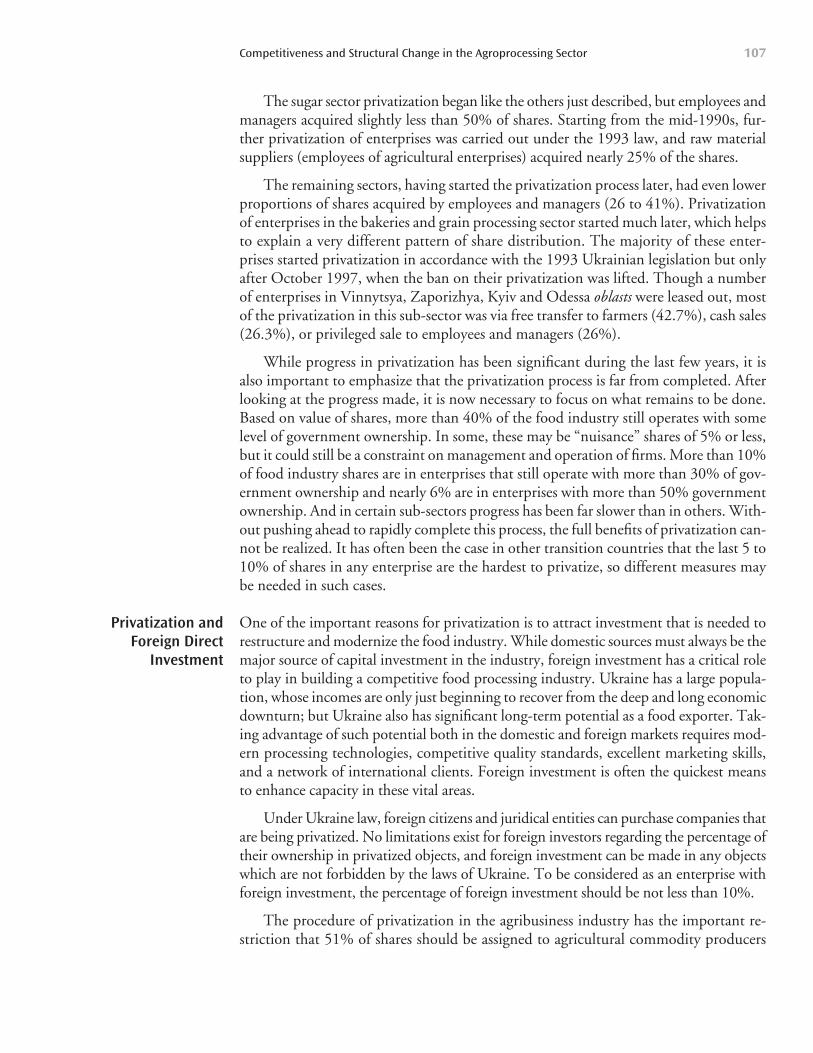

Figure 7.3: FDI in the Food Industry 108

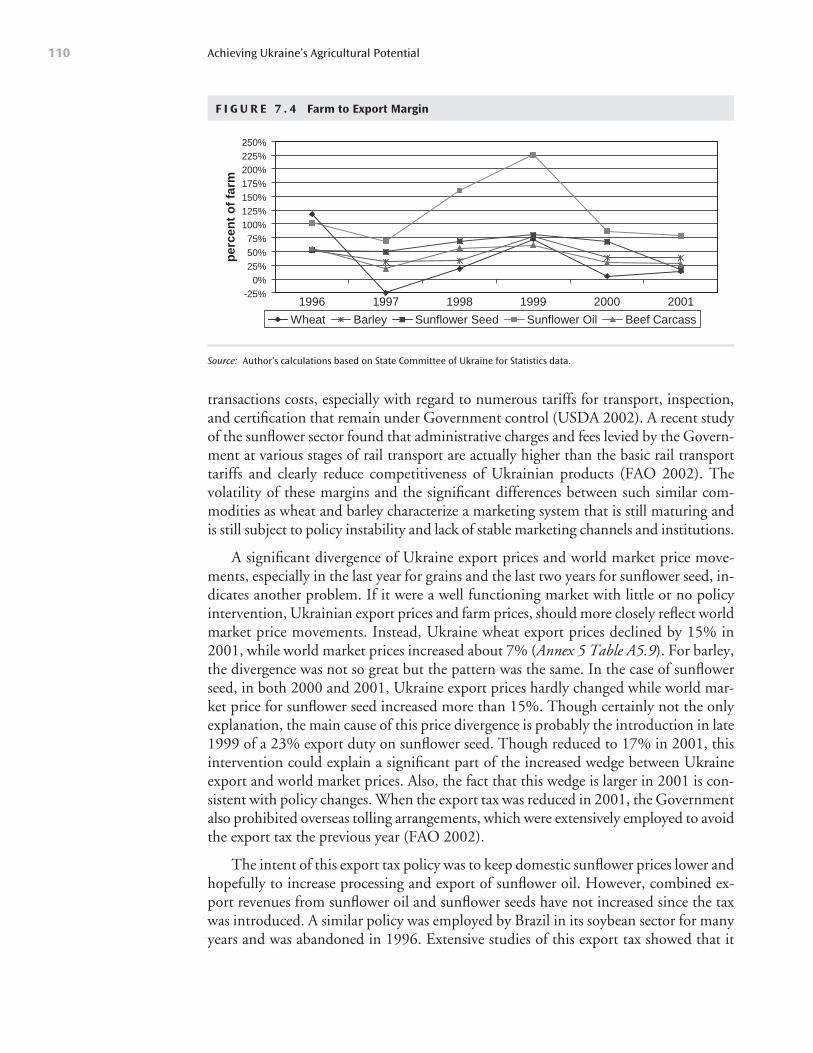

Figure 7.4: Farm to Export Margin 110

Figure 7.5: Farm to Retail Margins 111

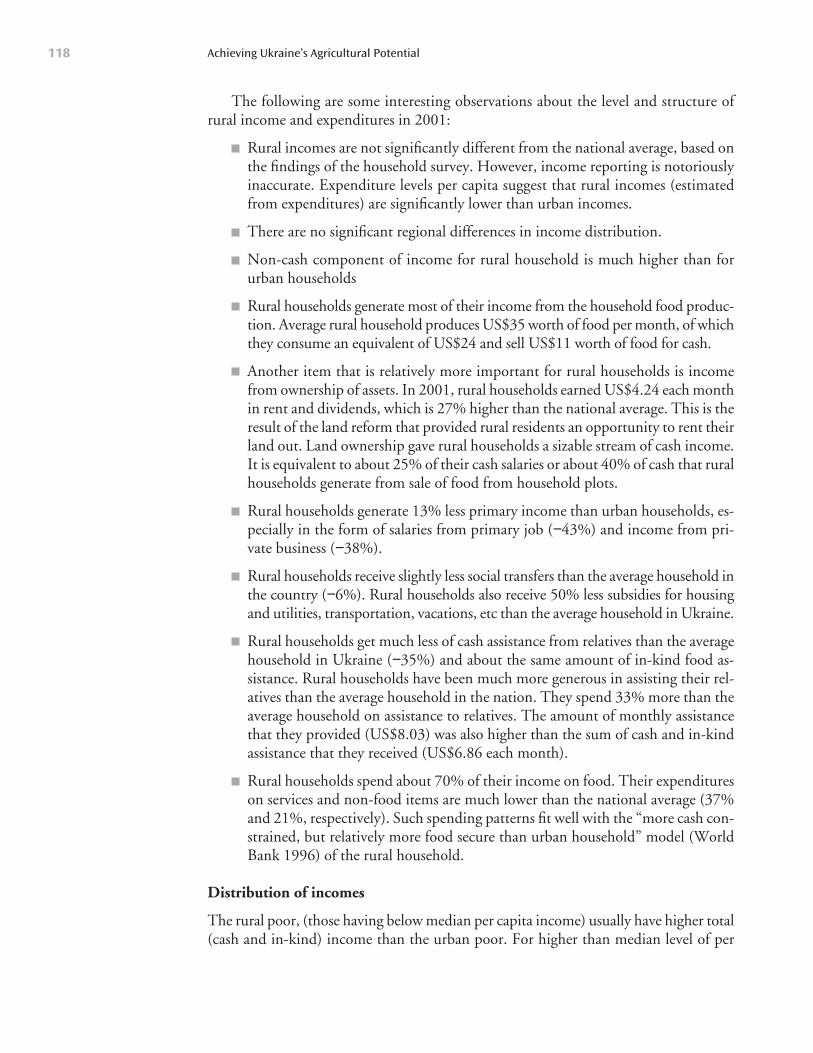

Figure 8.1: Distribution of Total per Capita Monthly Income, 2001 (Q1-Q3) 119

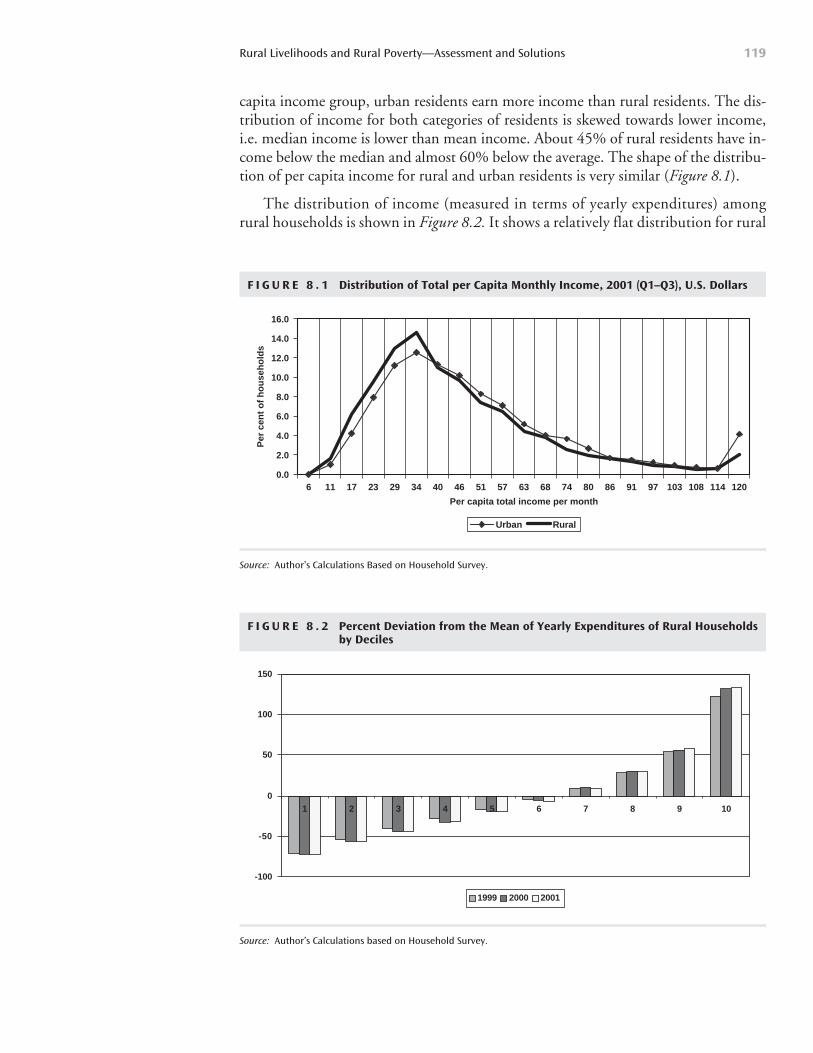

Figure 8.2: Percent Deviation from the Mean of Yearly Expenditures of Rural Households 119

Figure 8.3: Per Capita Food Consumption Trends 124

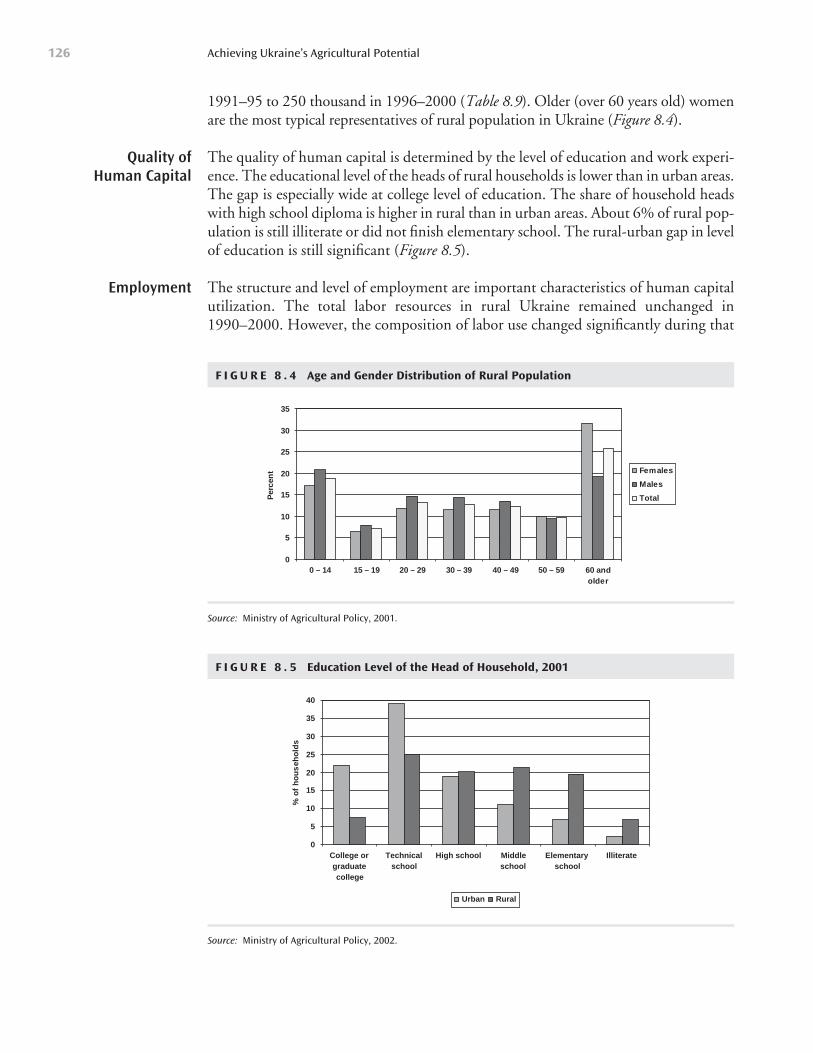

Figure 8.4: Age and Gender Distribution of Rural Population 126

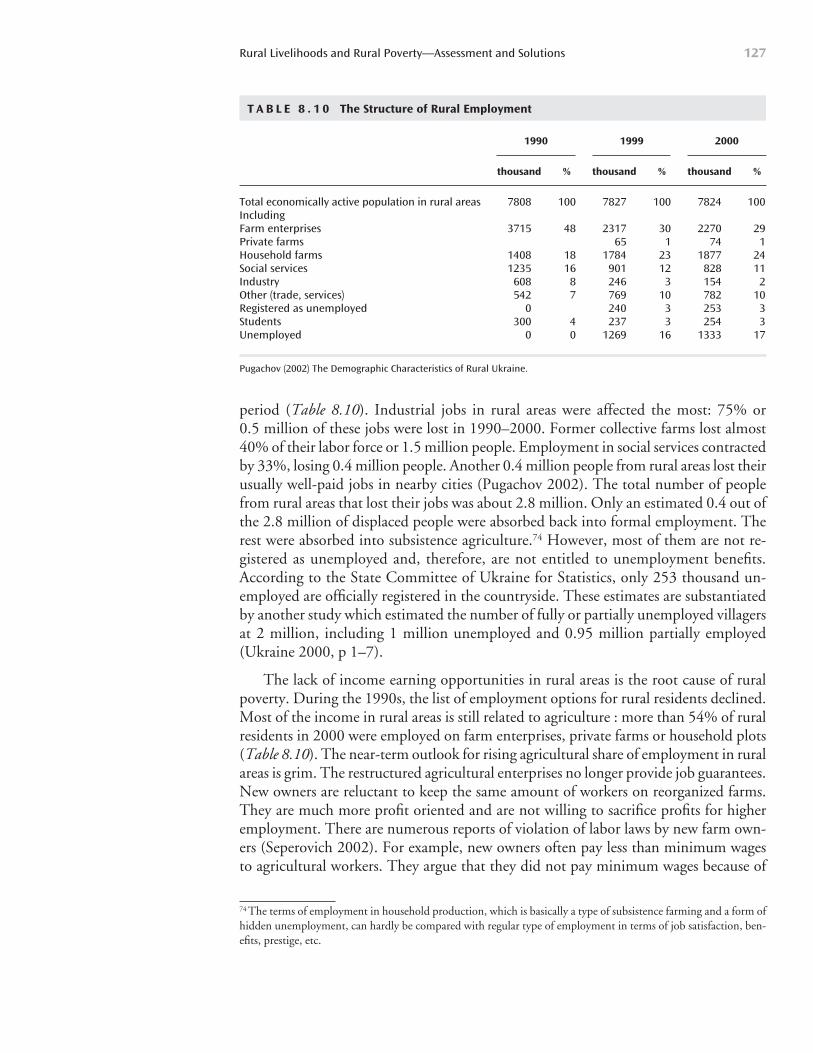

Figure 8.5: Education Level of the Head of Household, 2001 126

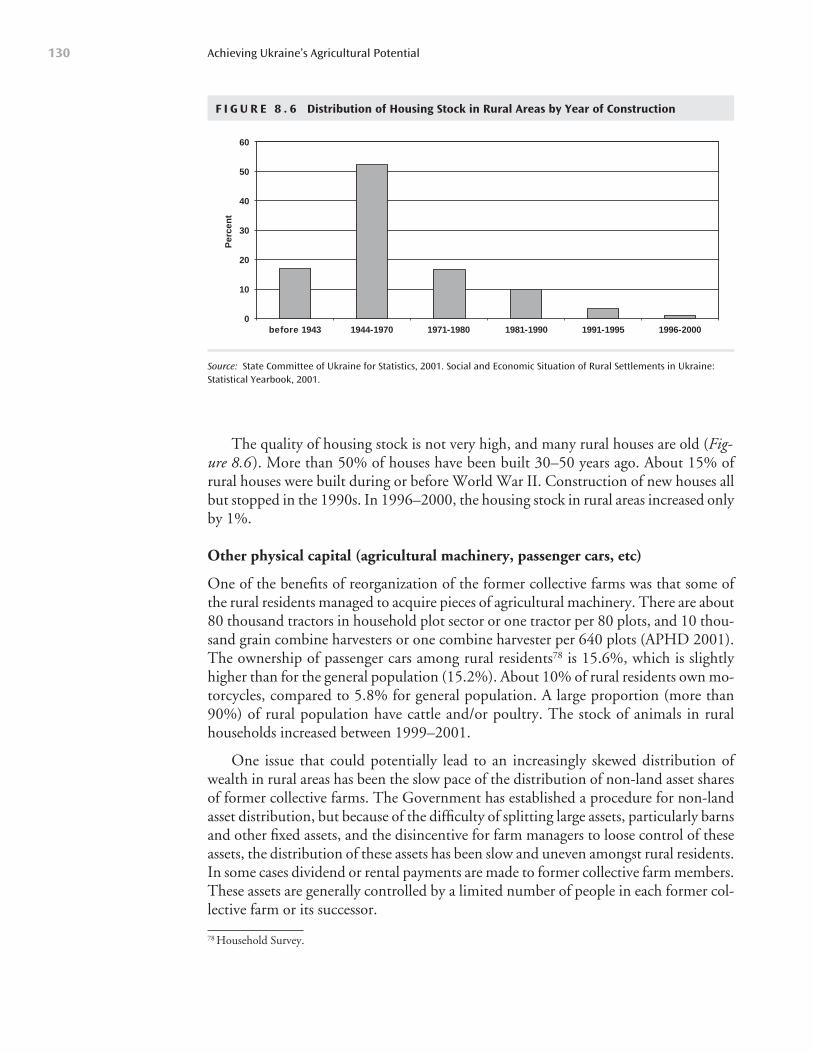

Figure 8.6: Distribution of Housing Stock in Rural Areas 130

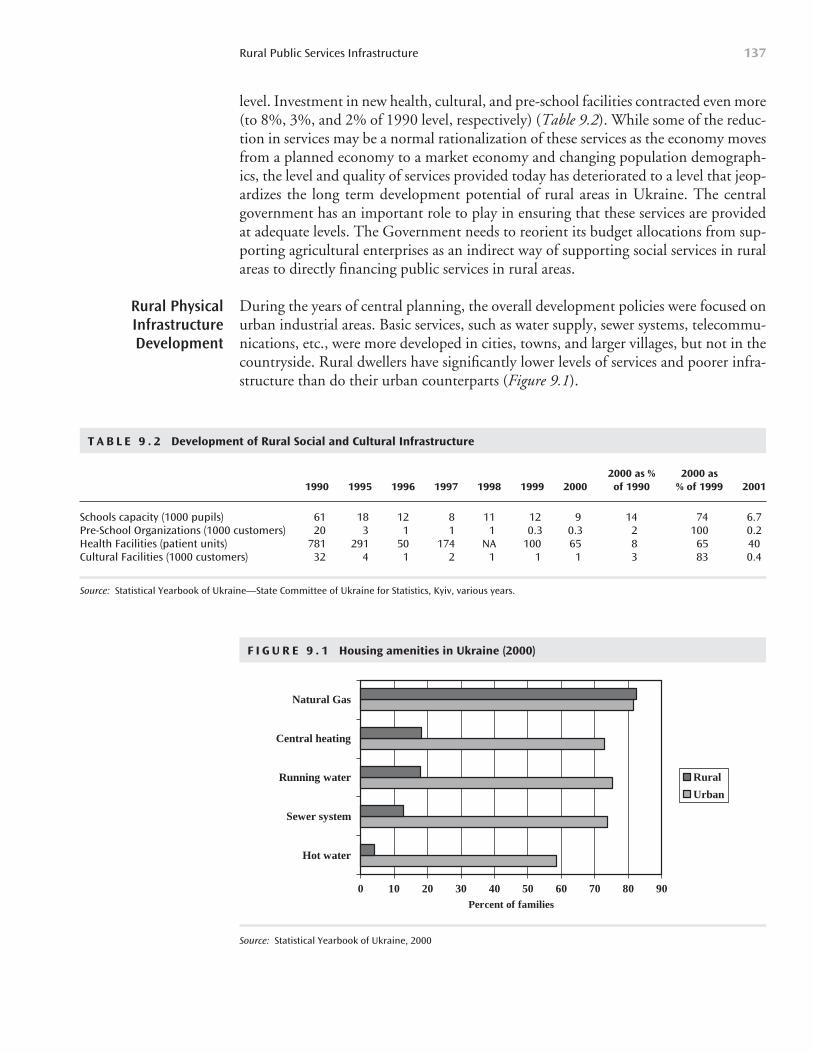

Figure 9.1: Housing Amenities in Ukraine 2000 137

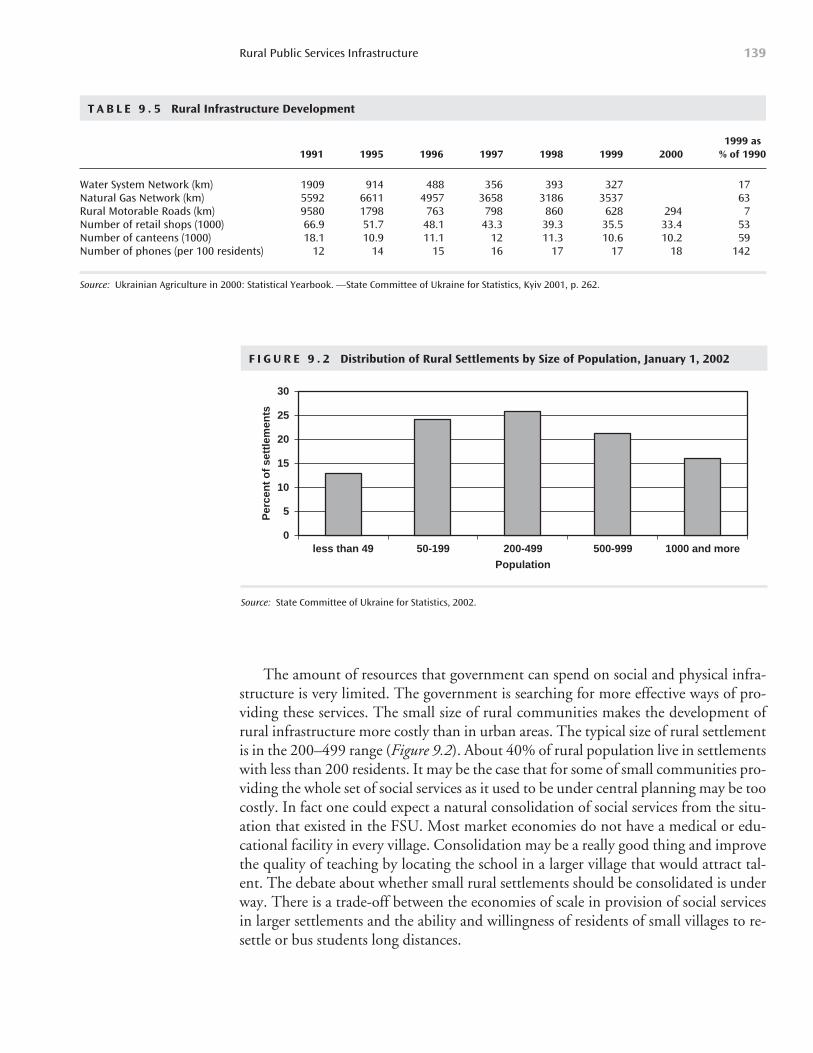

Figure 9.2: Distribution of Rural Settlements by Size of Population, January 1, 2002 139

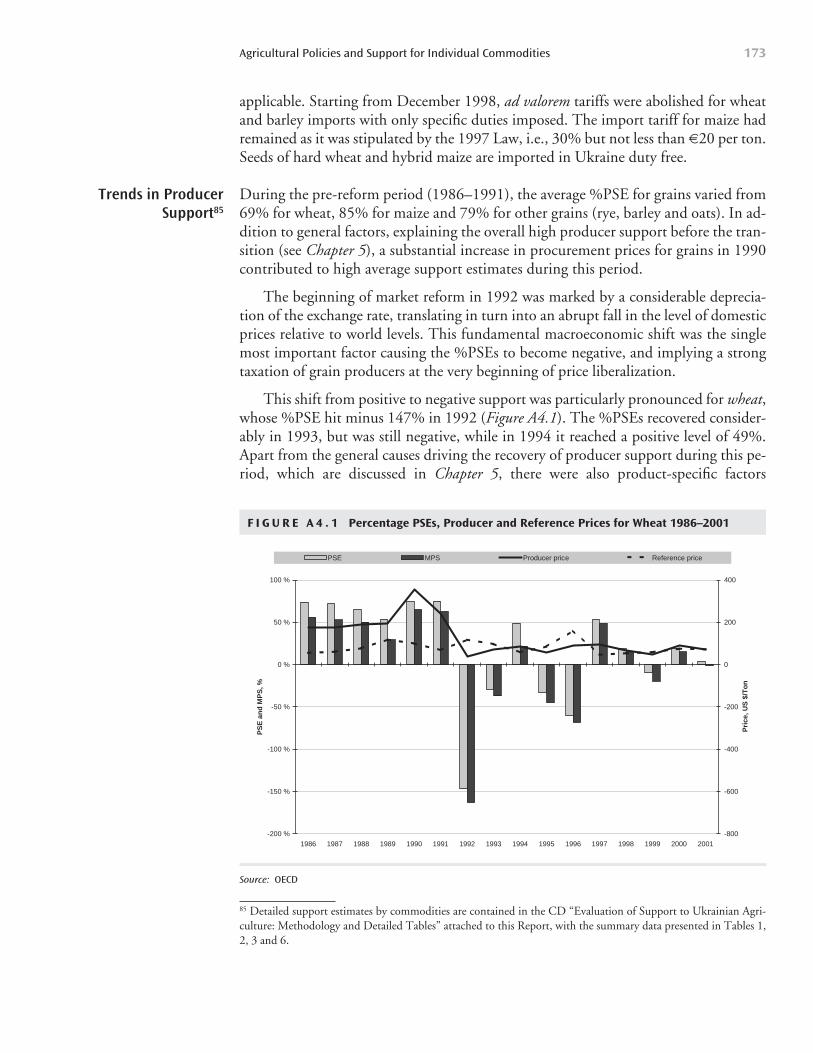

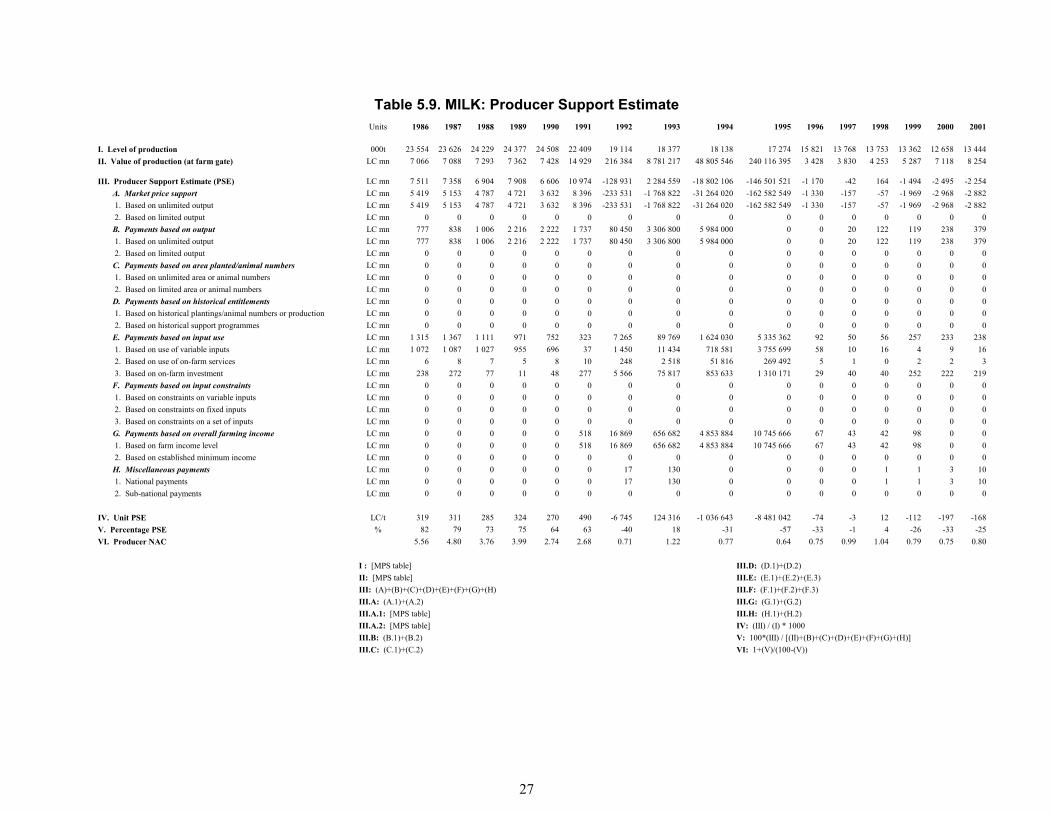

Figure A4.1: Percentage PSEs, Producer and Reference Prices for Wheat, 1986-2001 173

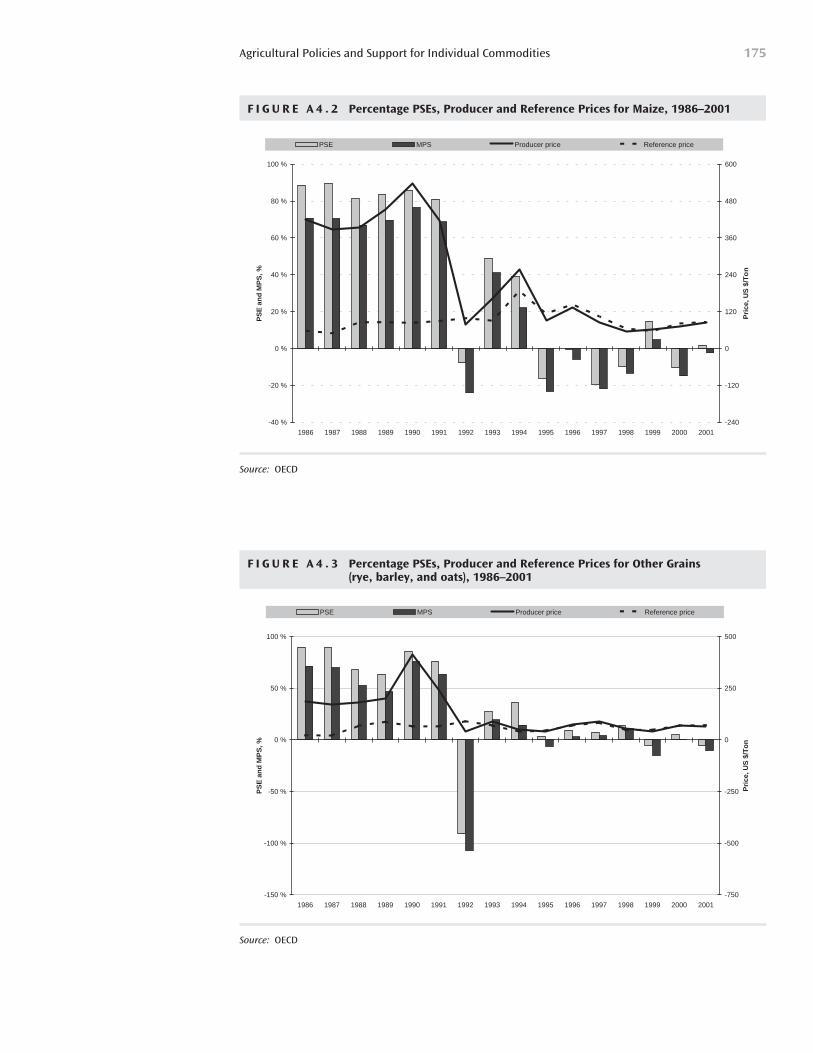

Figure A4.2: Percentage PSEs, Producer and Reference Prices for Maize, 1986-2001 175

Figure A4.3: Percentage PSEs, Producer and Reference Prices for Other Grains (rye, barley, and oats), 1986-2001 175

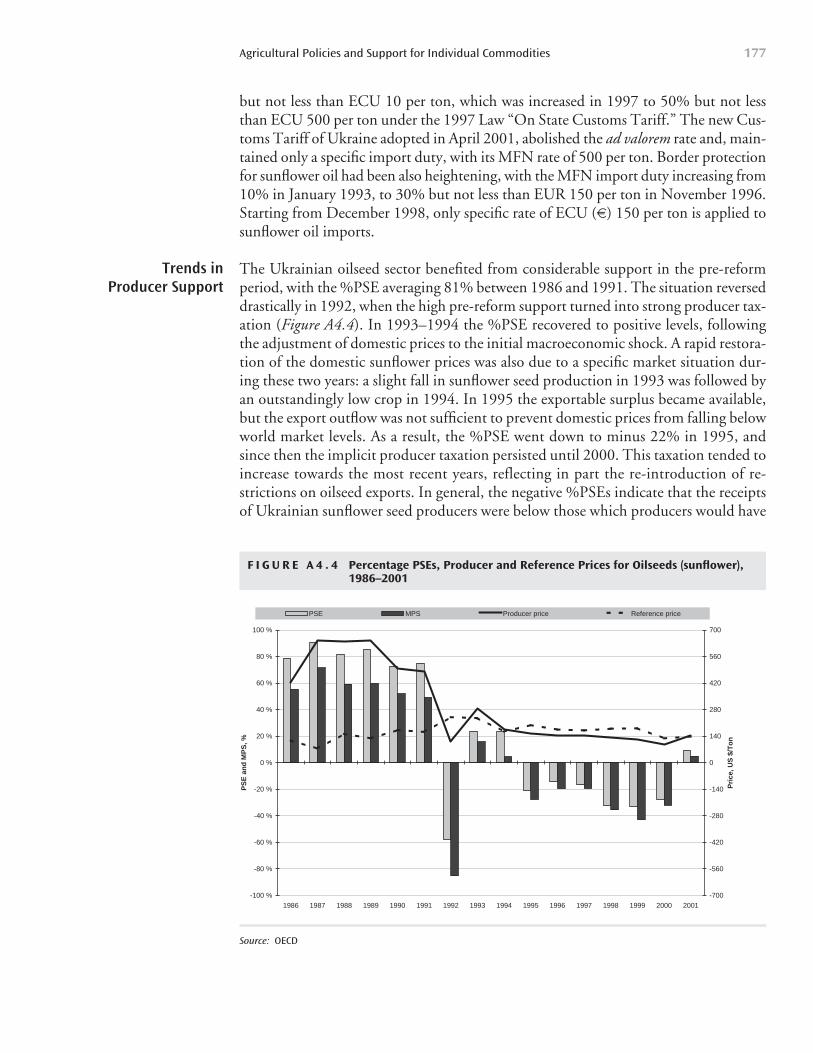

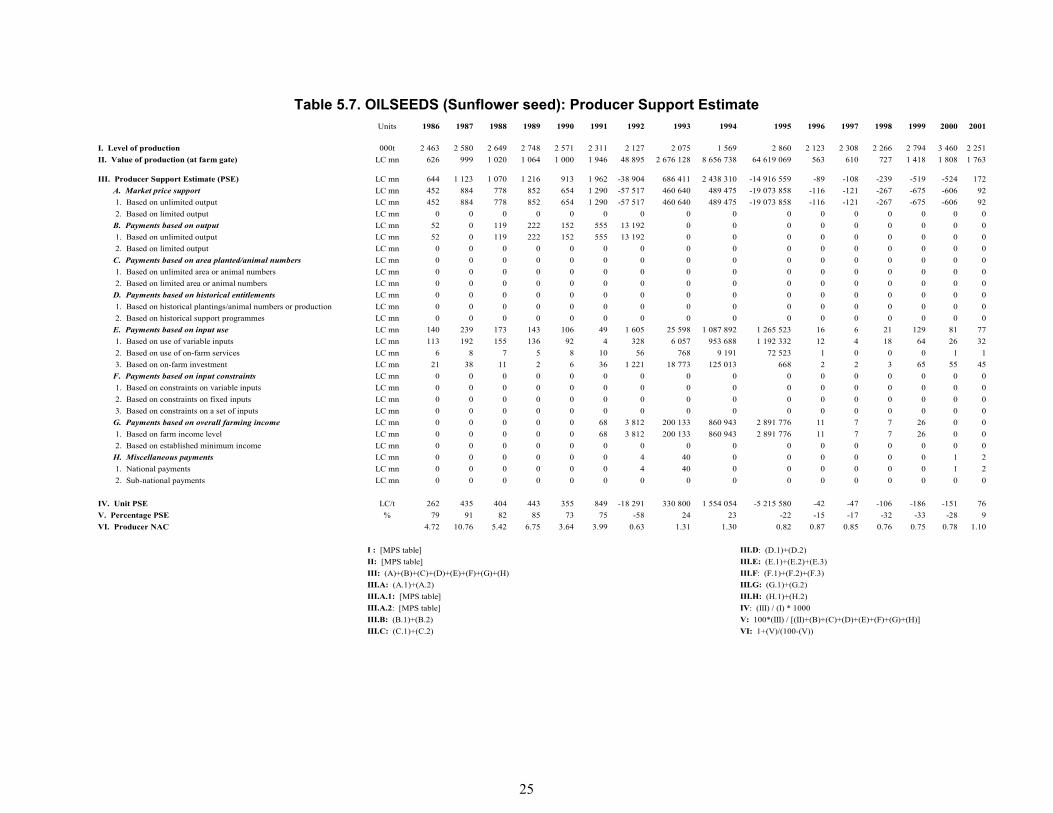

Figure A4.4: Percentage PSEs, Producer and Reference Prices for Oilseeds (sunflower), 1986-2001 177

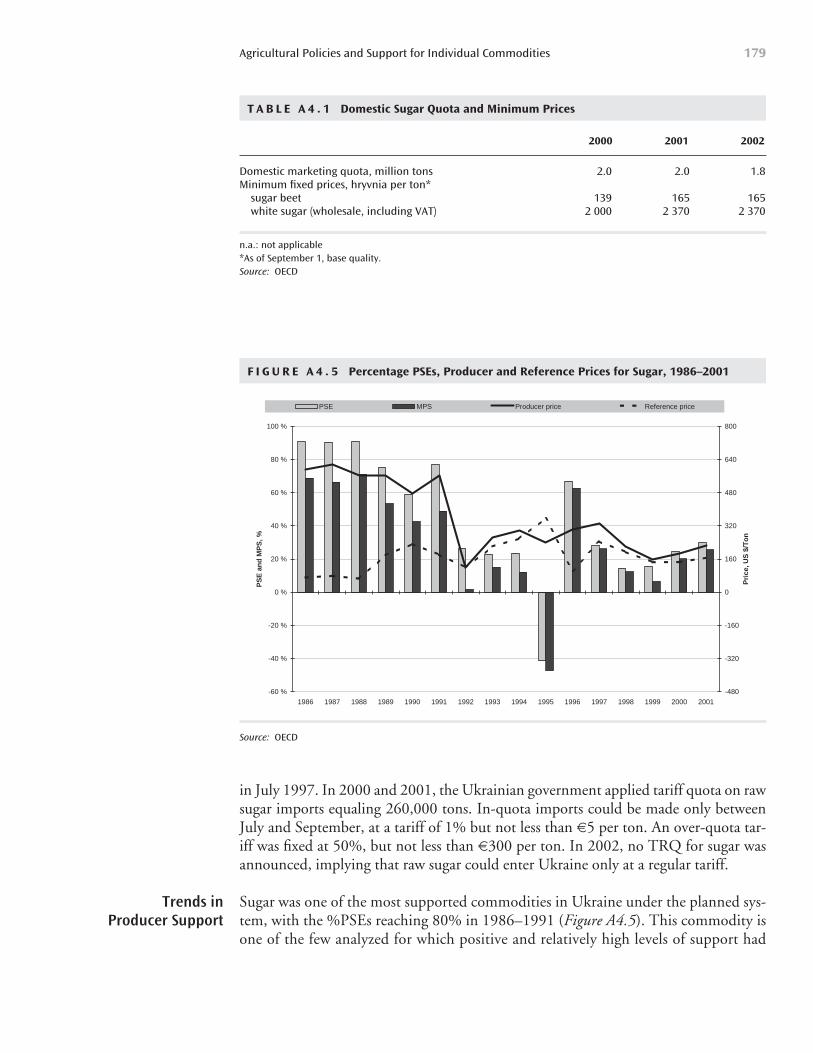

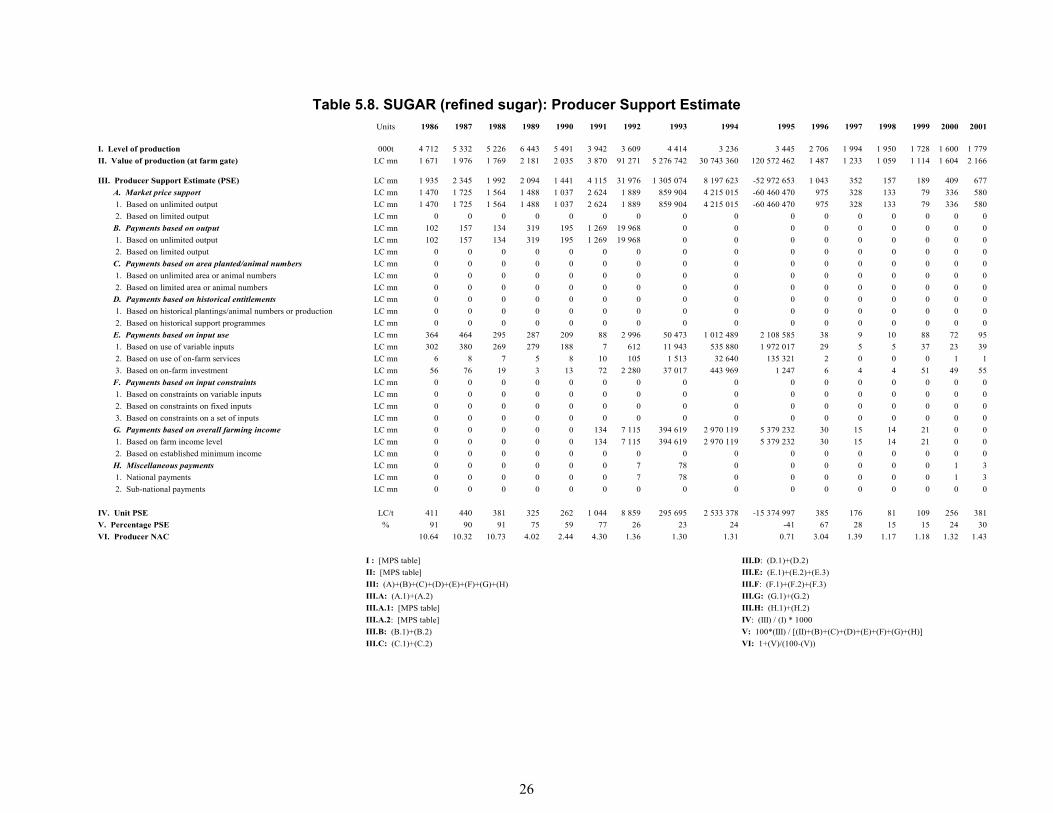

Figure A4.5: Percentage PSEs, Producer and Reference Prices for Sugar, 1986-2001 179

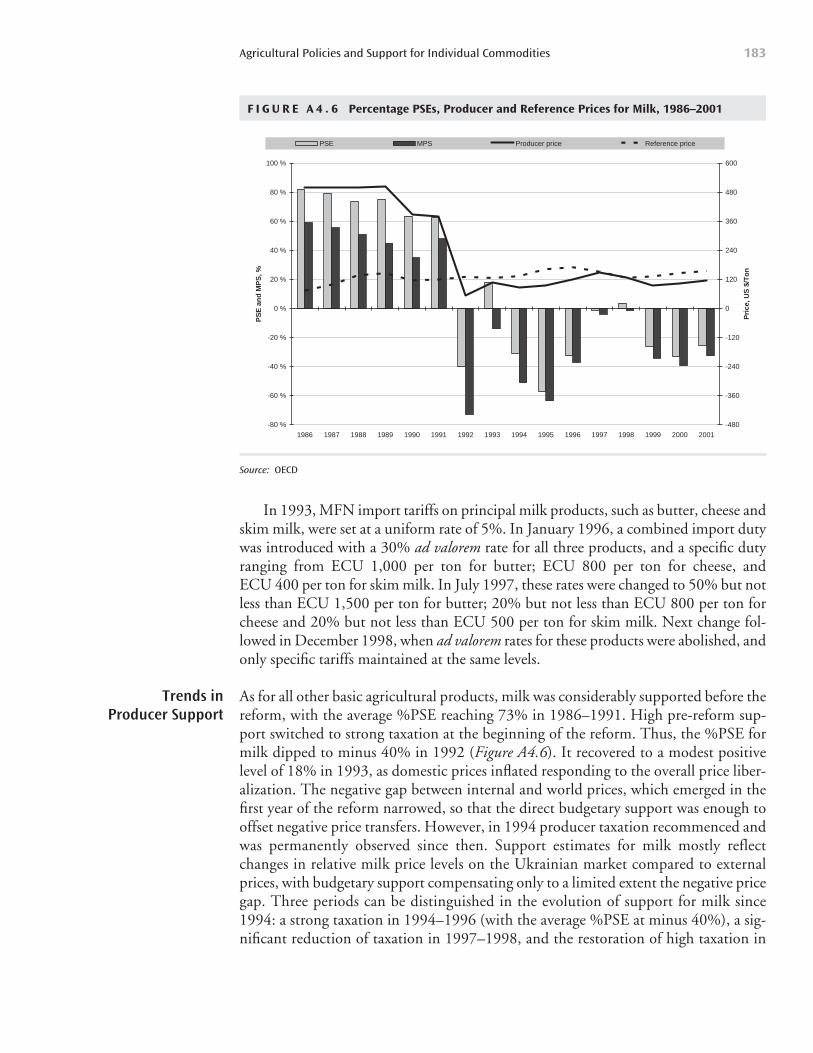

Figure A4.6: Percentage PSEs, Producer and Reference Prices for Milk, 1986-2001 183

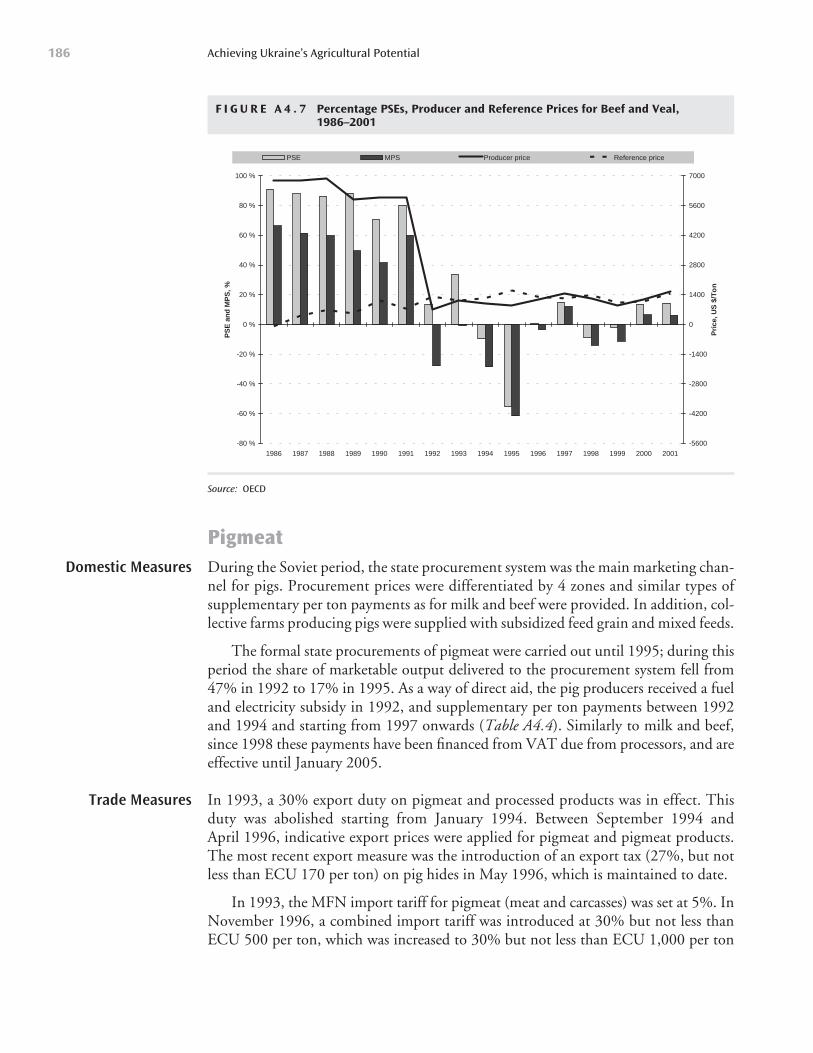

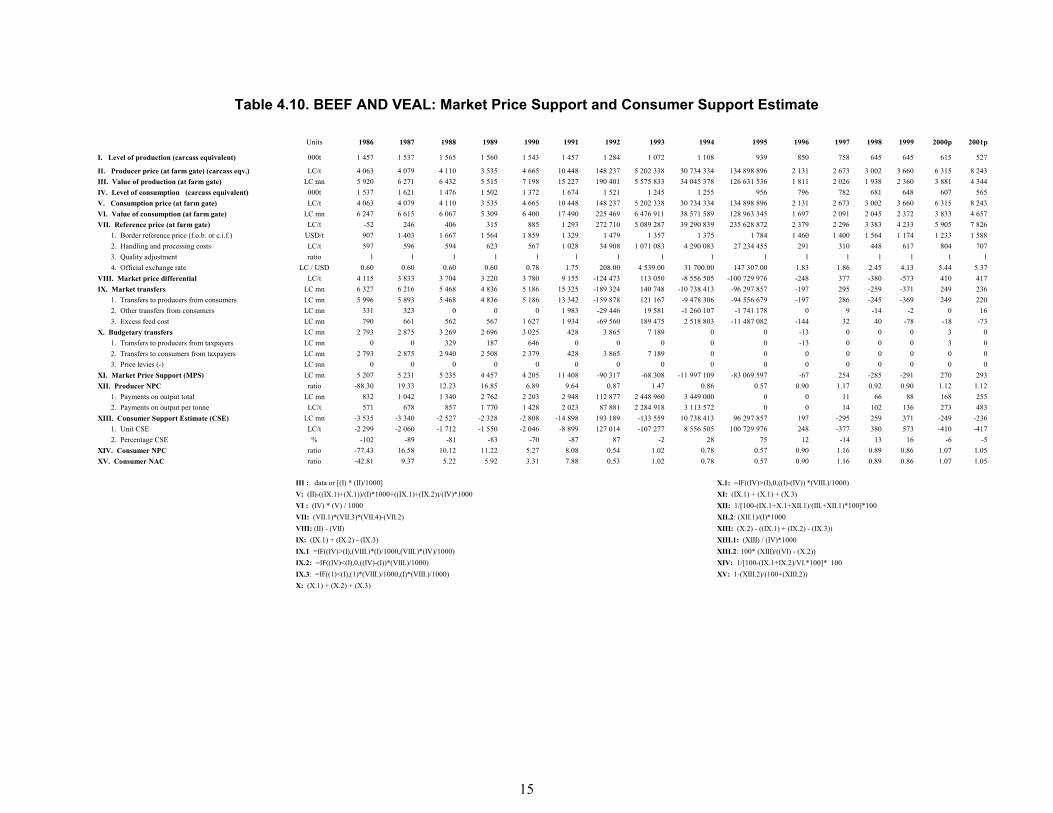

Figure A4.7: Percentage PSEs, Producer and Reference Prices for Beef and Veal, 1986-2001 186

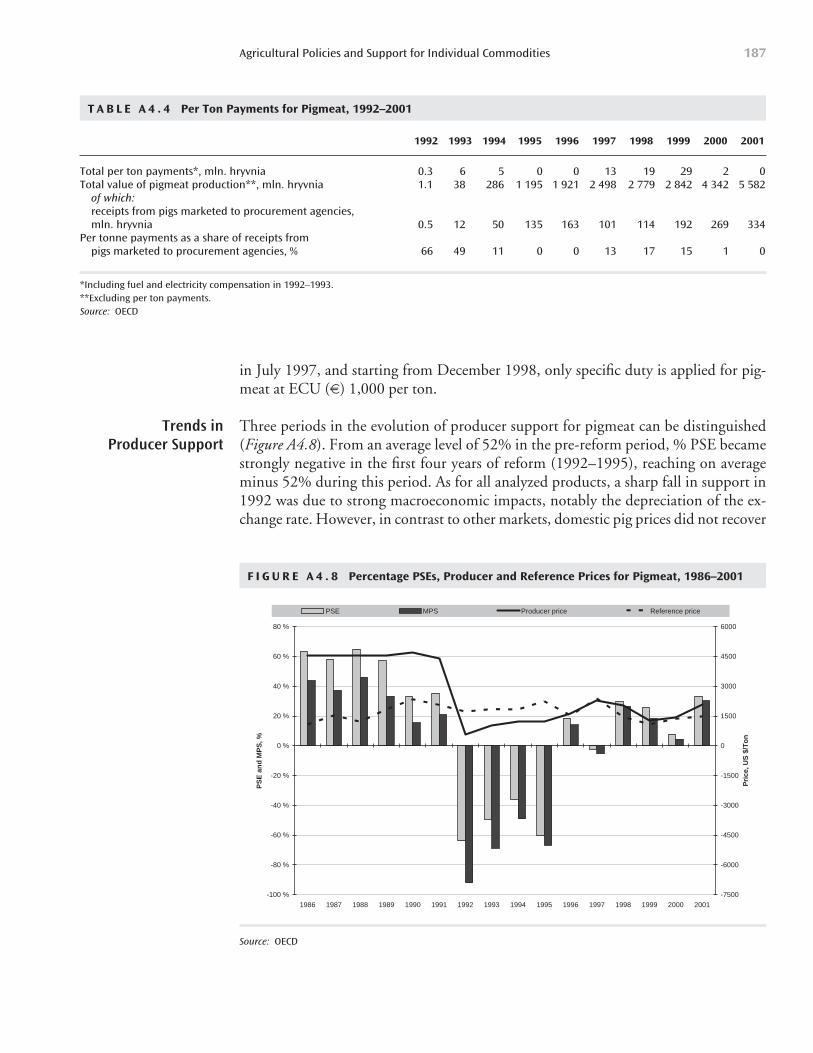

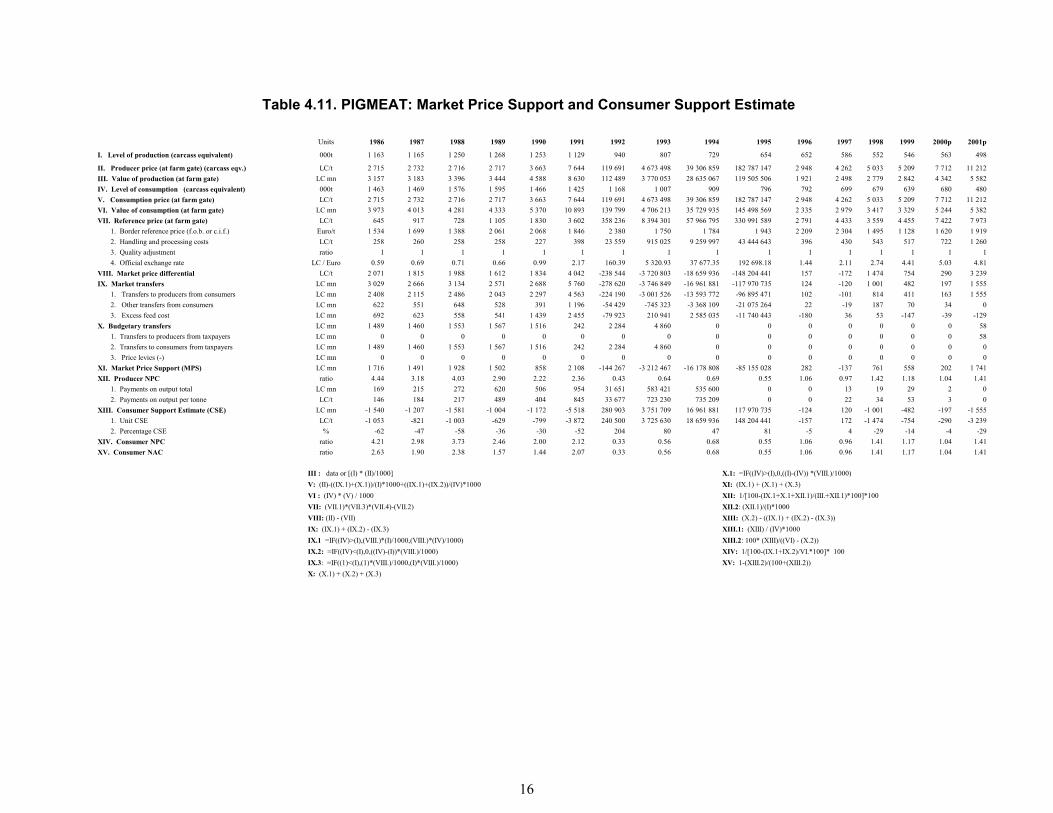

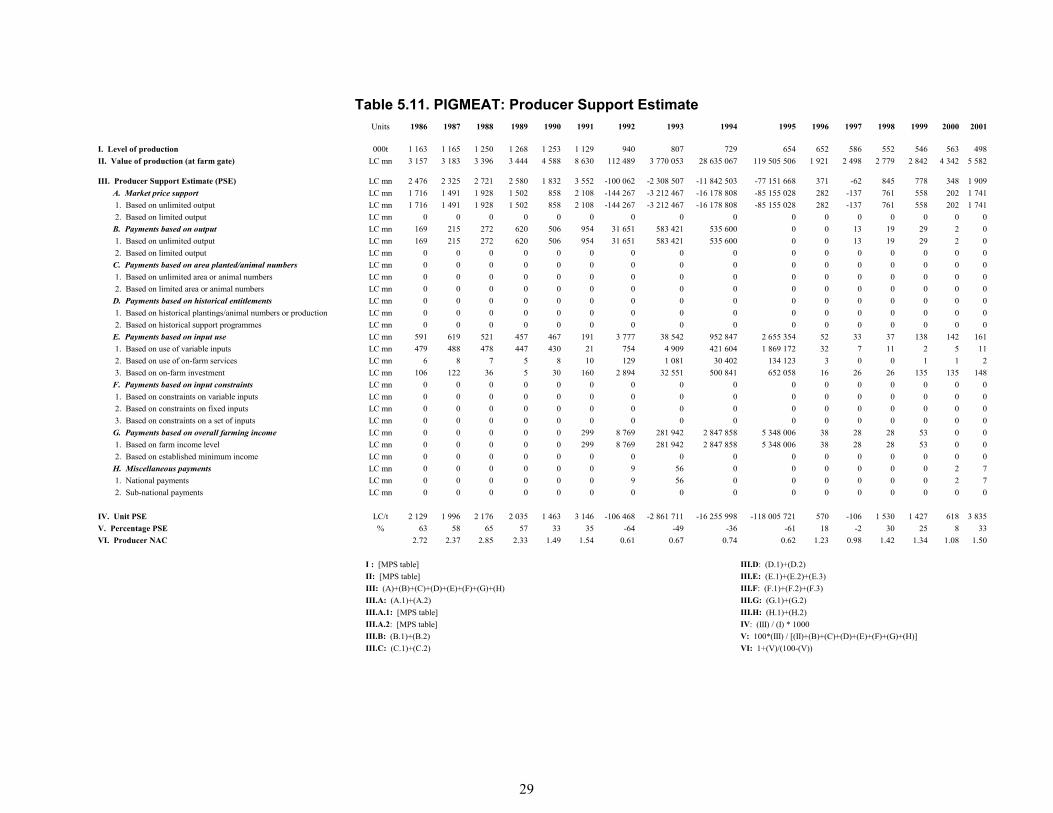

Figure A4.8: Percentage PSEs, Producer and Reference Prices for Pigmeat, 1986-2001 187

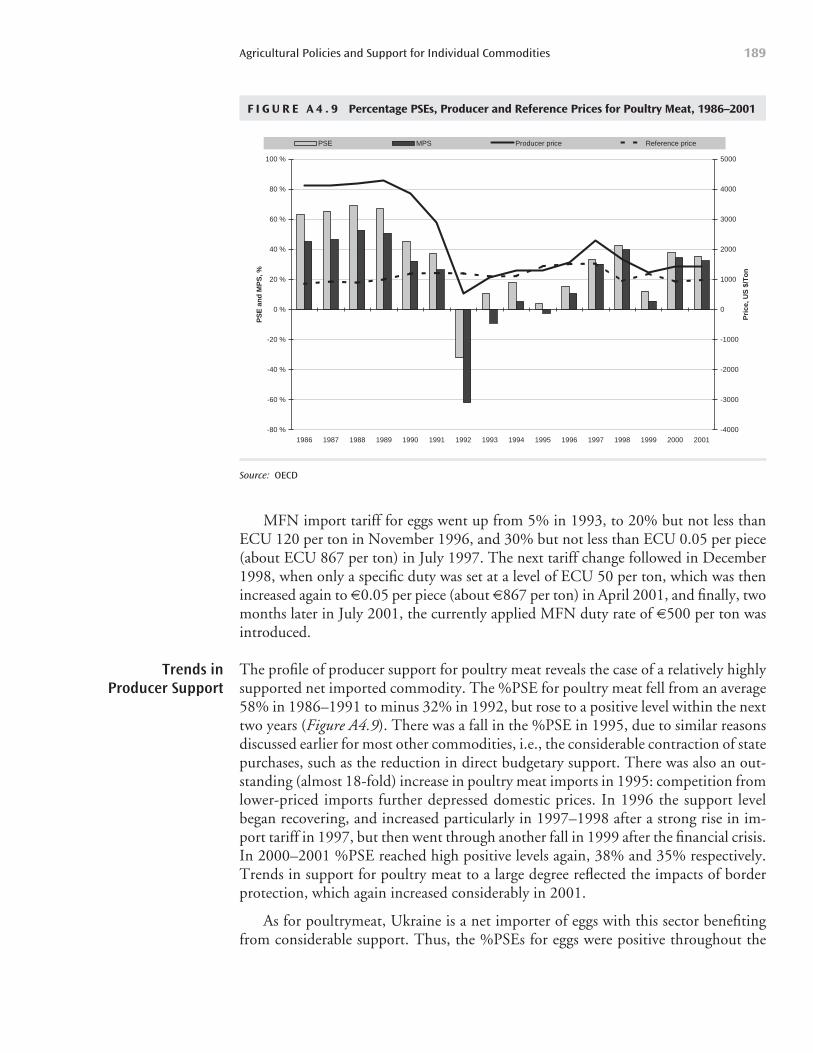

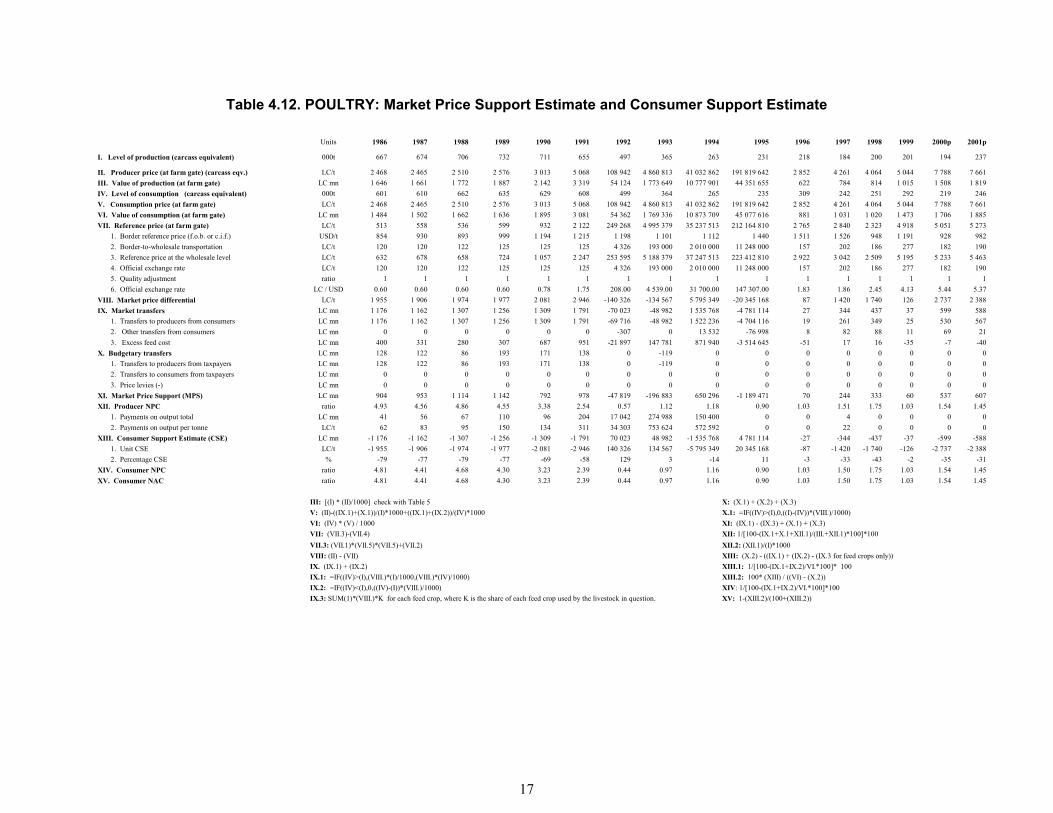

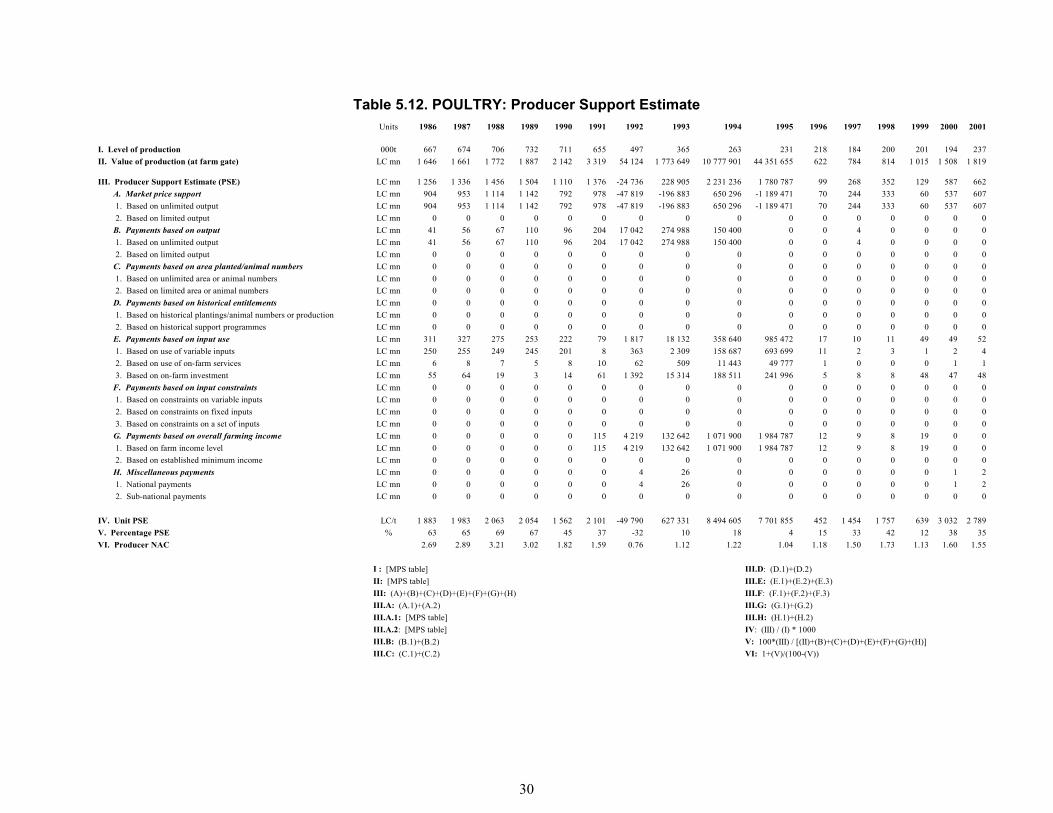

Figure A4.9: Percentage PSEs, Producer and Reference Prices for Poultry Meat,1986-2001 189

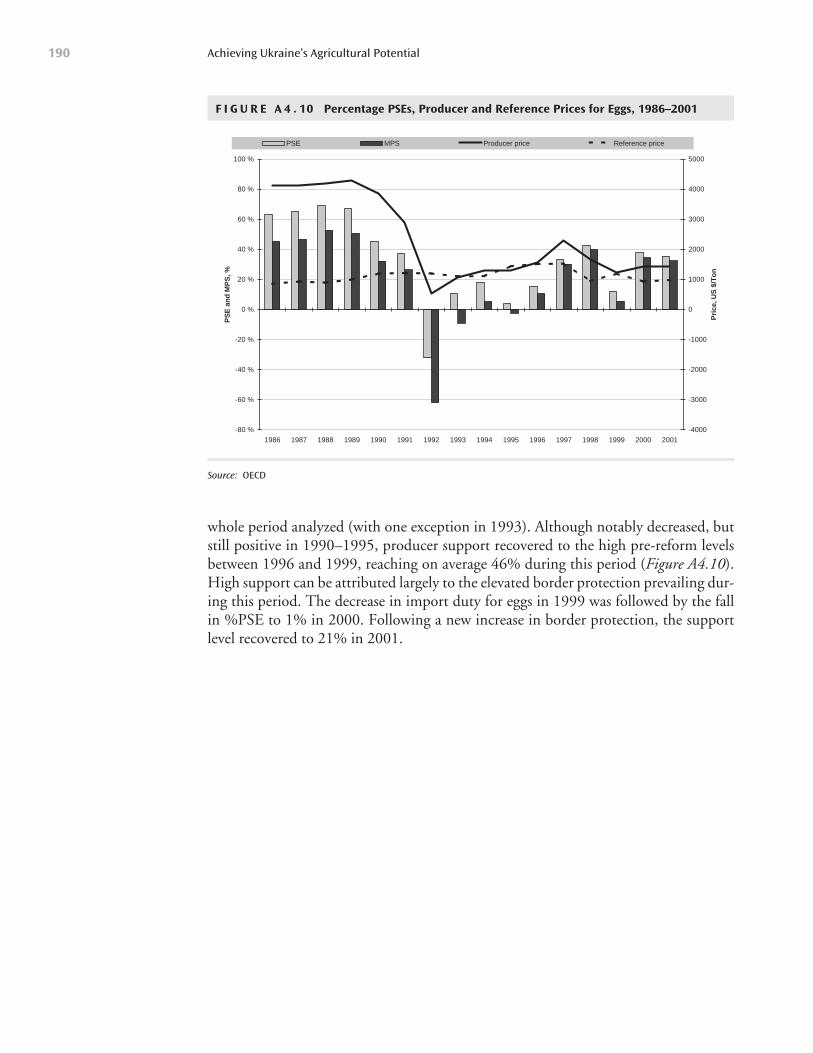

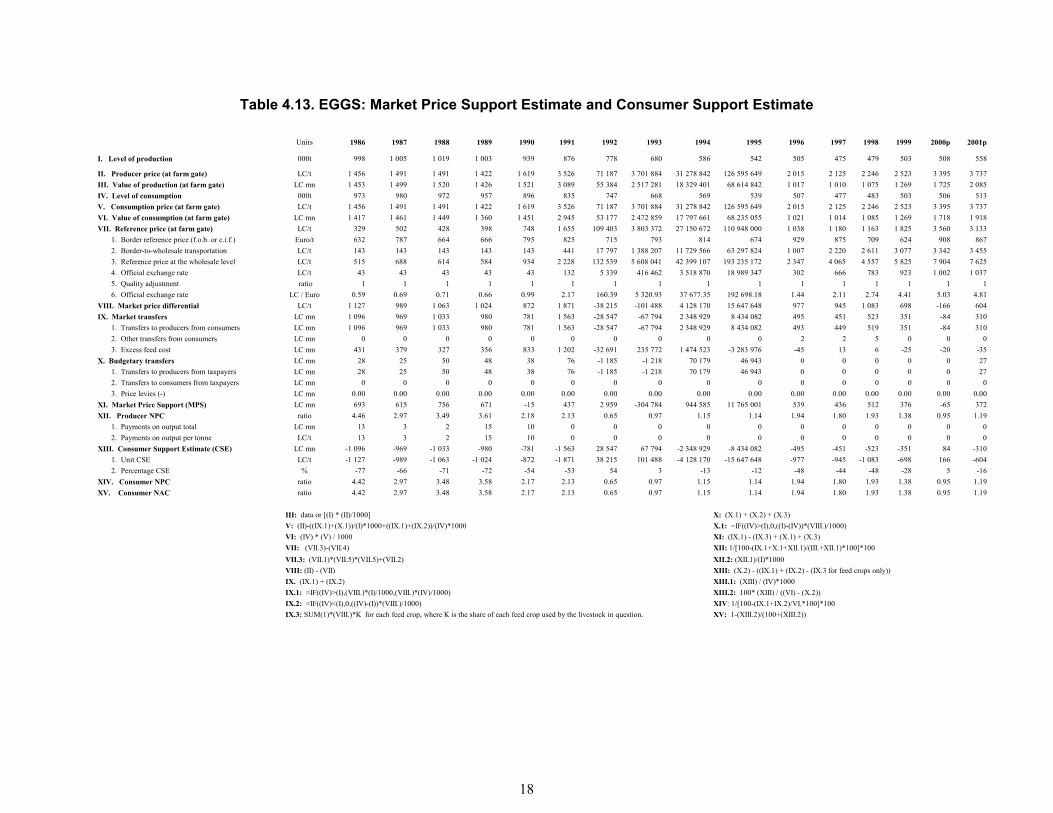

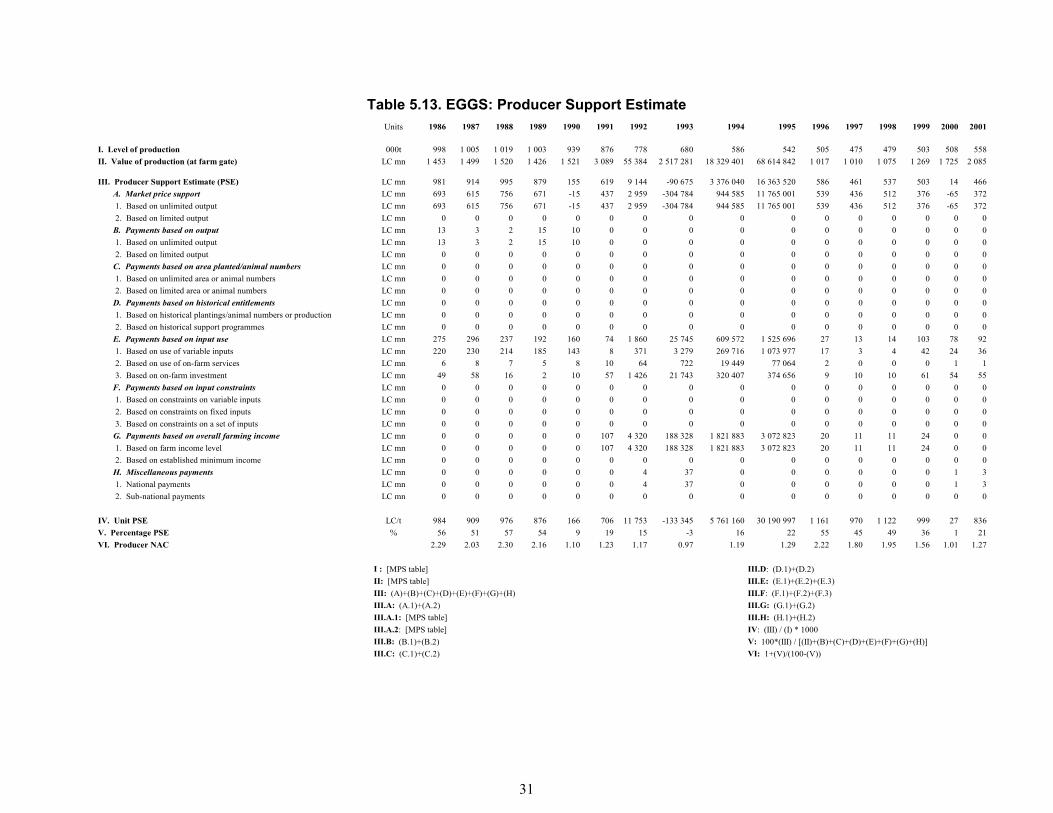

Figure A4.10: Percentage PSEs, Producer and Reference Prices for Eggs, 1986-2001 190

Contents v

LIST OF TABLES

Table 1.1: Comparison of Yields for Selected Commodities 2

Table 1.2: Position of Agriculture in the National Economy 3

Table 1.3: Agricultural Trade, 1992-2002 4

Table 1.4: Structure of Grain Production 6

Table 1.5: Grain Marketed by Market Participants 7

Table 1.6: Grain Balance 8

Table 1.7: Productivity Indicators for Sunflowers 9

Table 1.8: Profitability of Sunflower Production 9

Table 1.9: Major Indicators of Sunflower Sector 9

Table 1.10: Sugar Balance 10

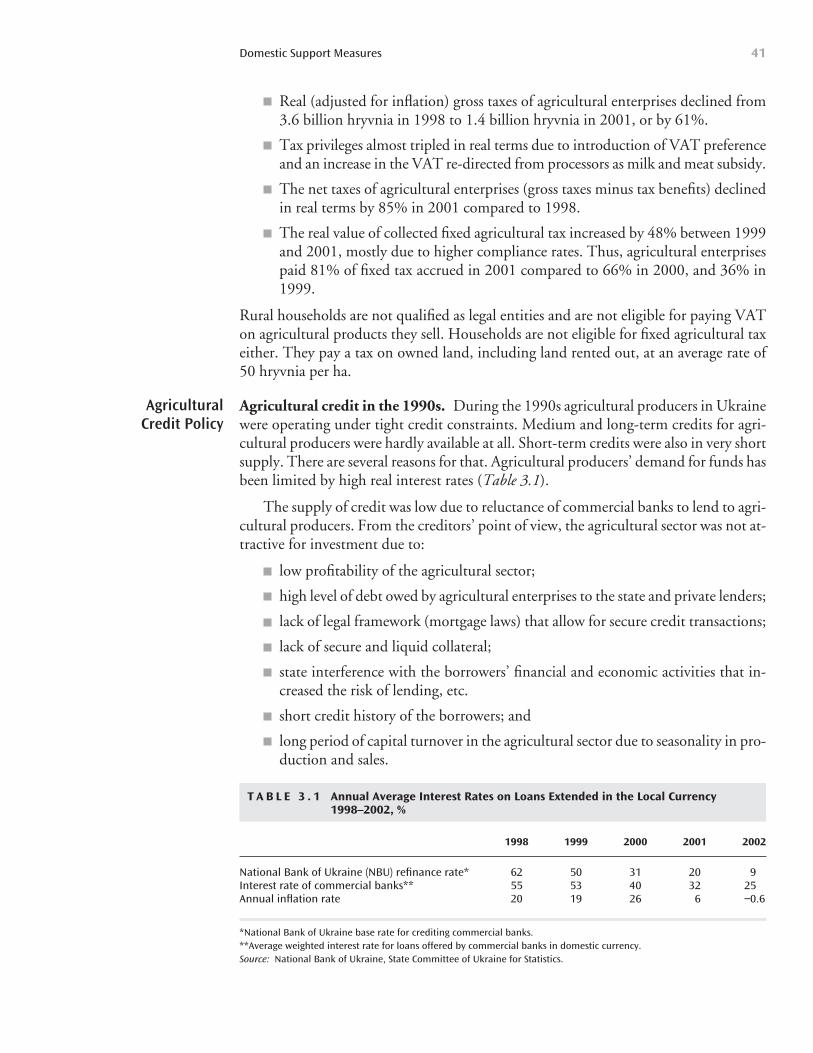

Table 3.1: Annual Average Interest Rates on Loans Extended in the Local Currency 1998-2002 41

Table 3.2: Average Nominal Commercial Interest Rate for Loans in 2000 and 2002 42

Table 3.3: Selected Indicators of Social Assistance to Low-Income Groups in Ukraine, 1995-2001 46

Table 3.4: Share of Household Money Expenditures Spent on Food, Food Price and Money Income Indices, 1990-2001 46

Table 3.5: Per Capita Consumption of Main Food Products in Ukraine in 1990-2001 46

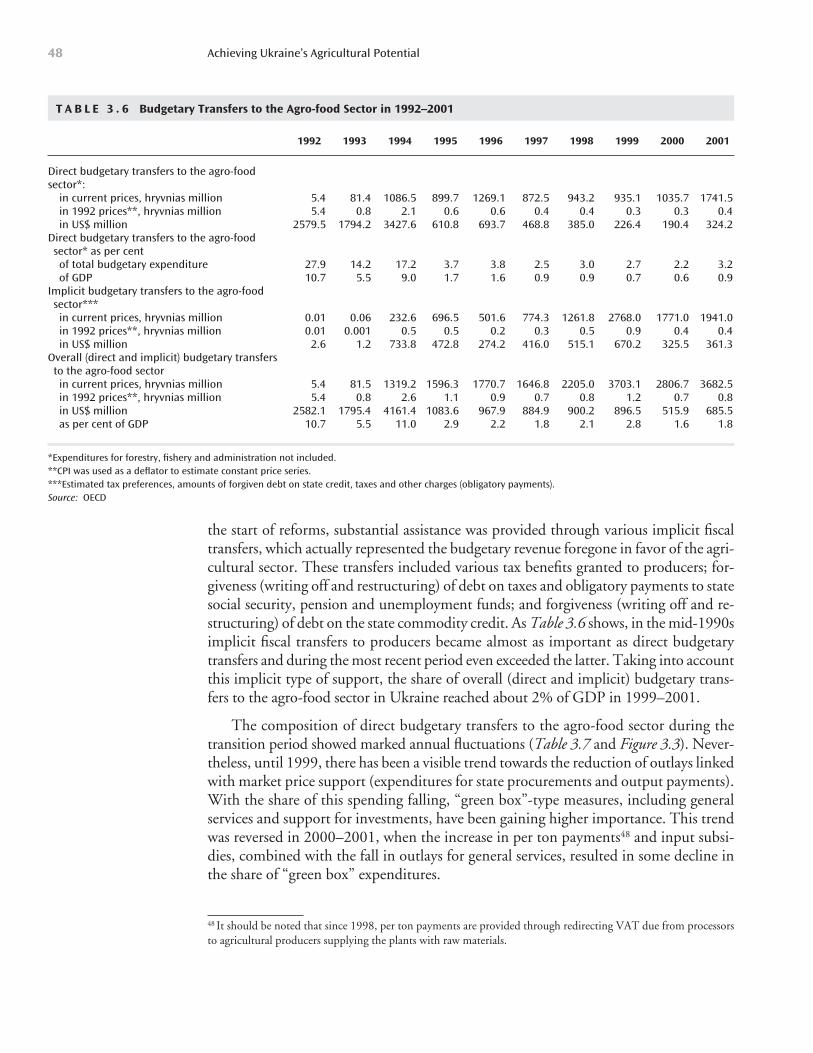

Table 3.6: Budgetary Transfers to the Agro-food Sector in 1992-2001 48

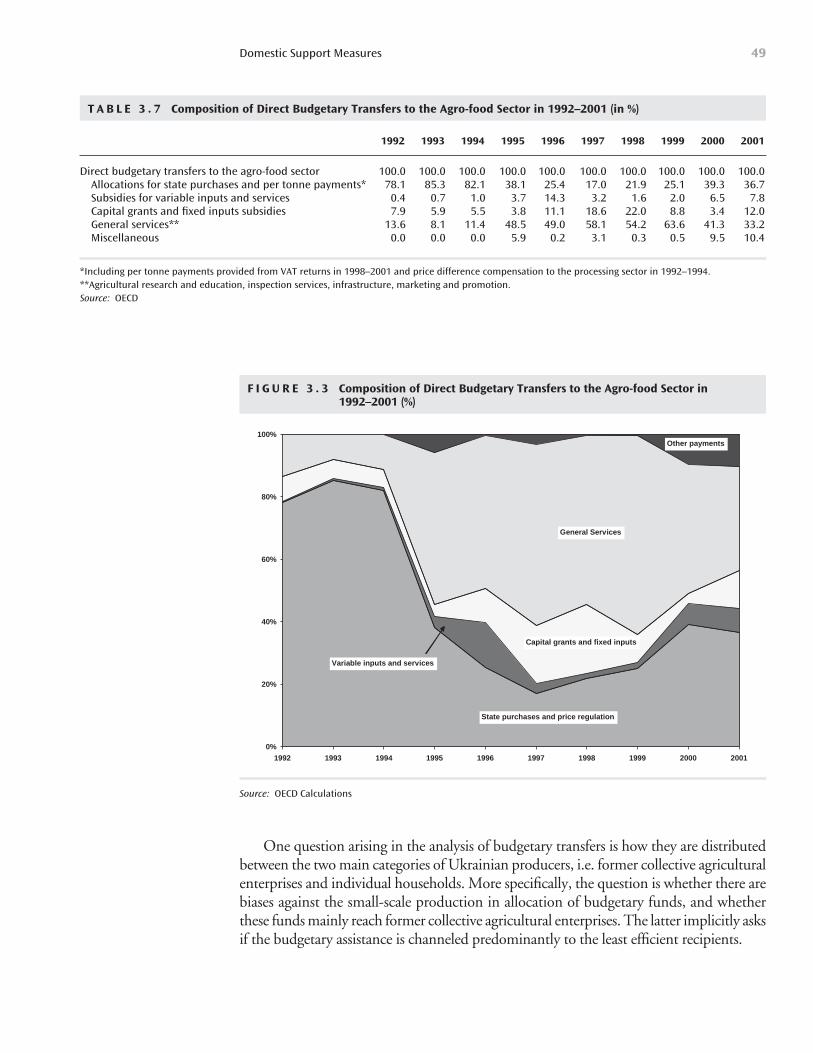

Table 3.7: Composition of Direct Budgetary Transfers to the Agro-food Sector in 1992-2001 49

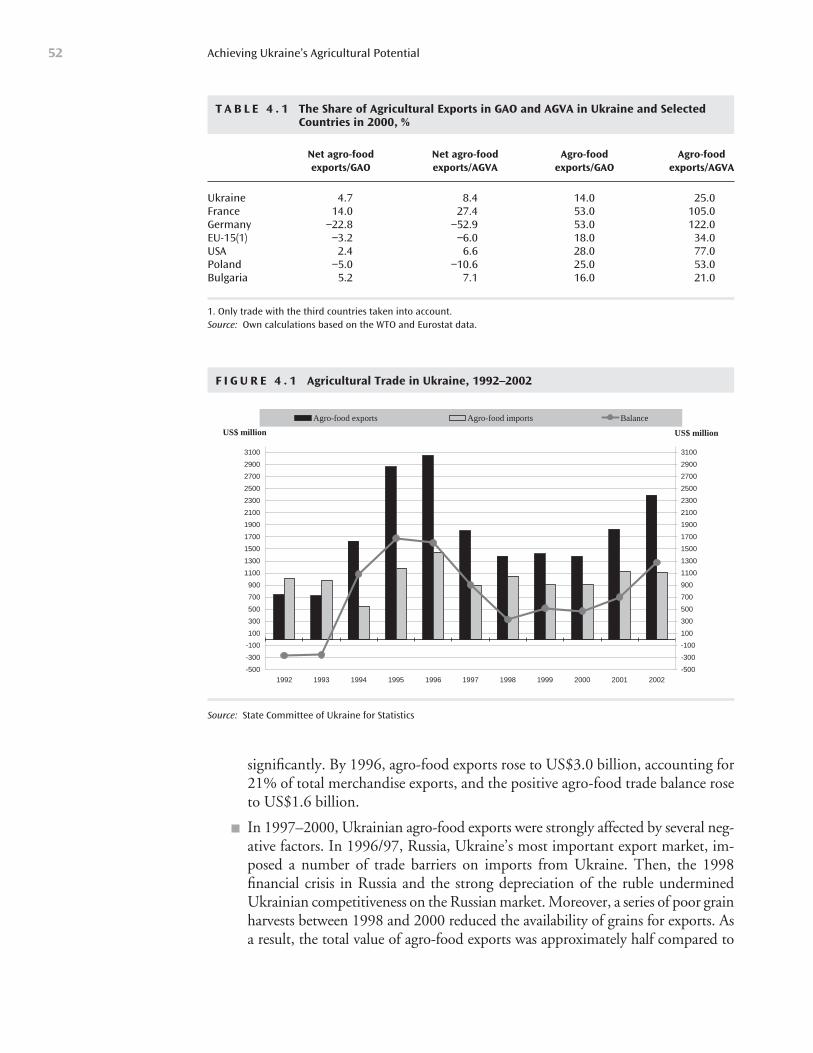

Table 4.1: The Share of Agricultural Exports in GAO and AGVA in Ukraine and Selected Countries in 2000 52

Table 4.2: Ukraine’s Net Exports of Major Agro-Food Products in 1995-2001 53

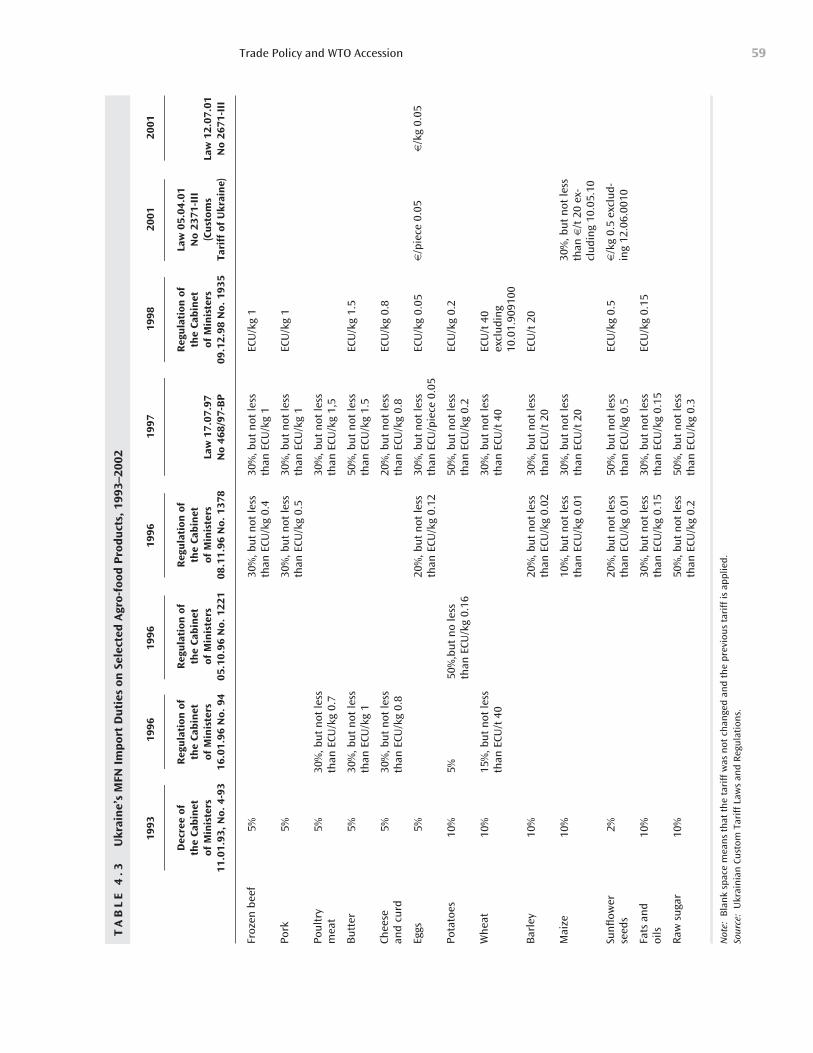

Table 4.3: Ukraine’s MFN Import Duties on Selected Agro-food products, 1993-2002 59

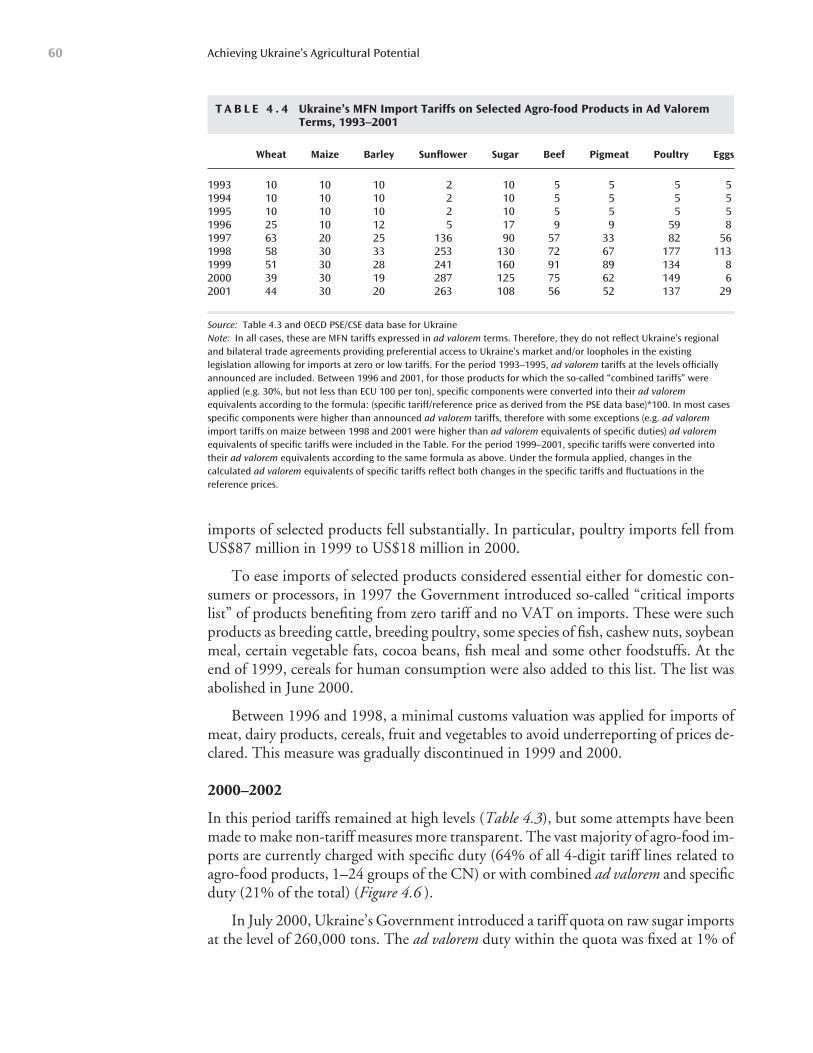

Table 4.4: Ukraine’s MFN Import Tariffs on Selected Agro-Food Products in Ad Valorem Terms, 1993-2001 60

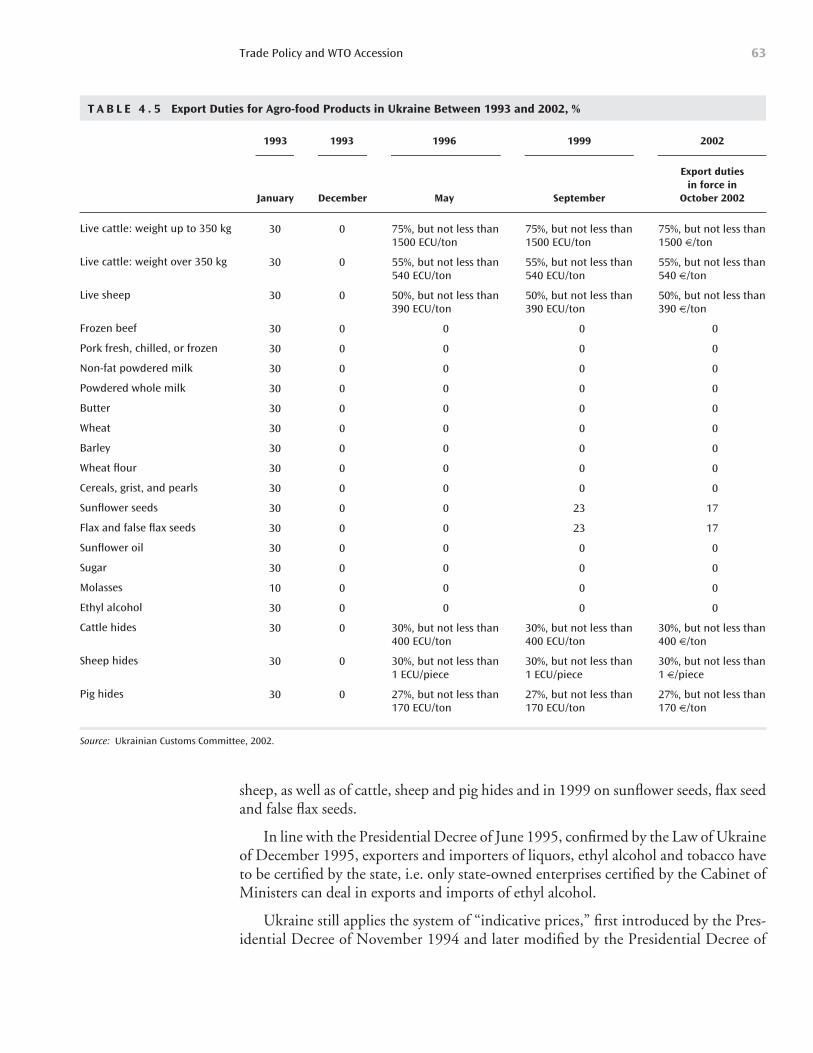

Table 4.5: Export Duties for Agro-food Products in Ukraine between 1993 and 2002 63

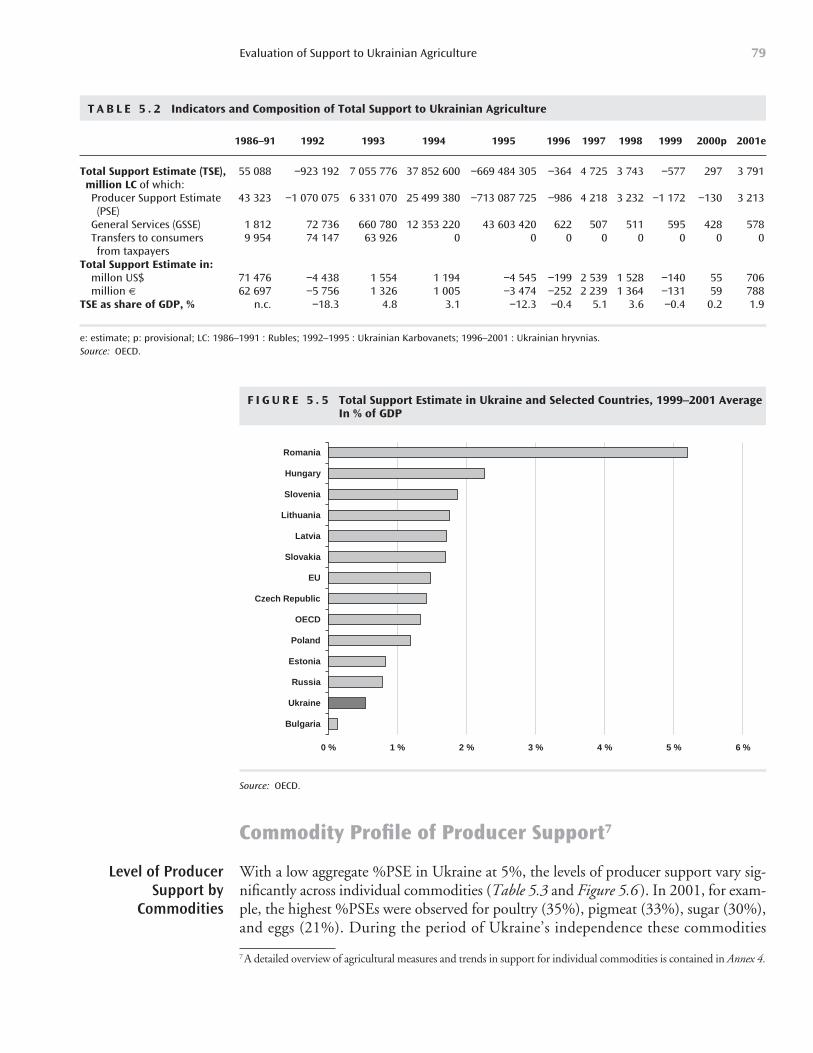

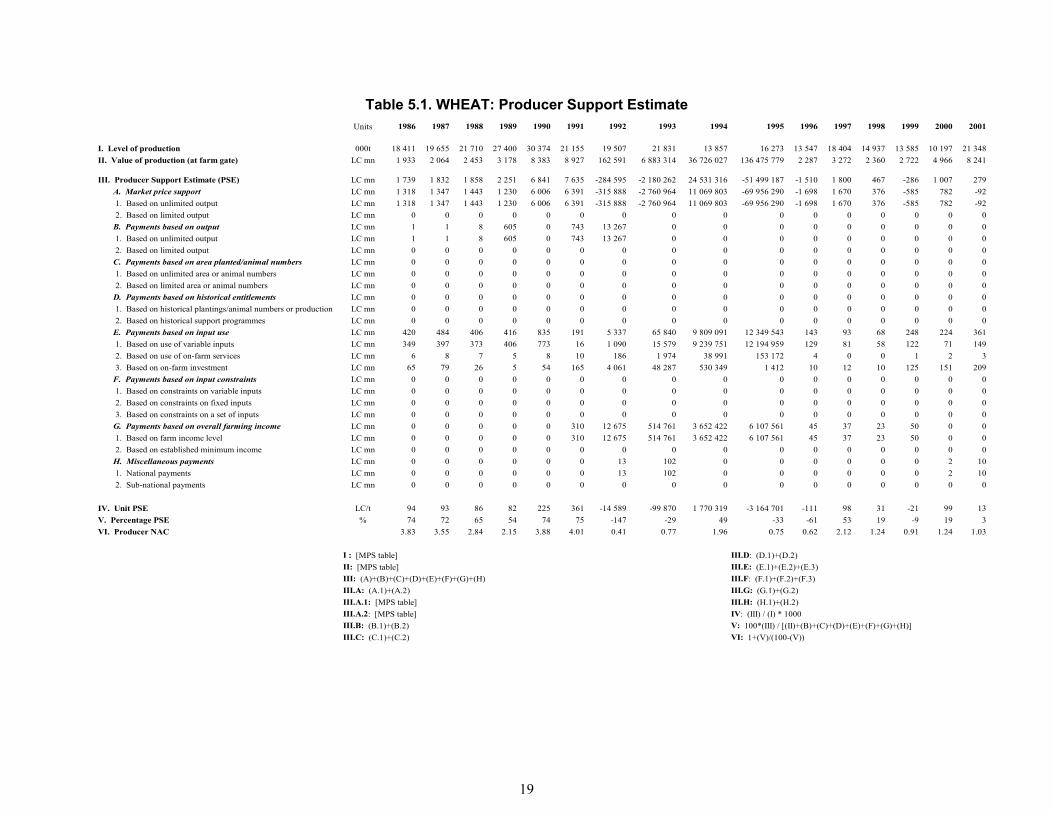

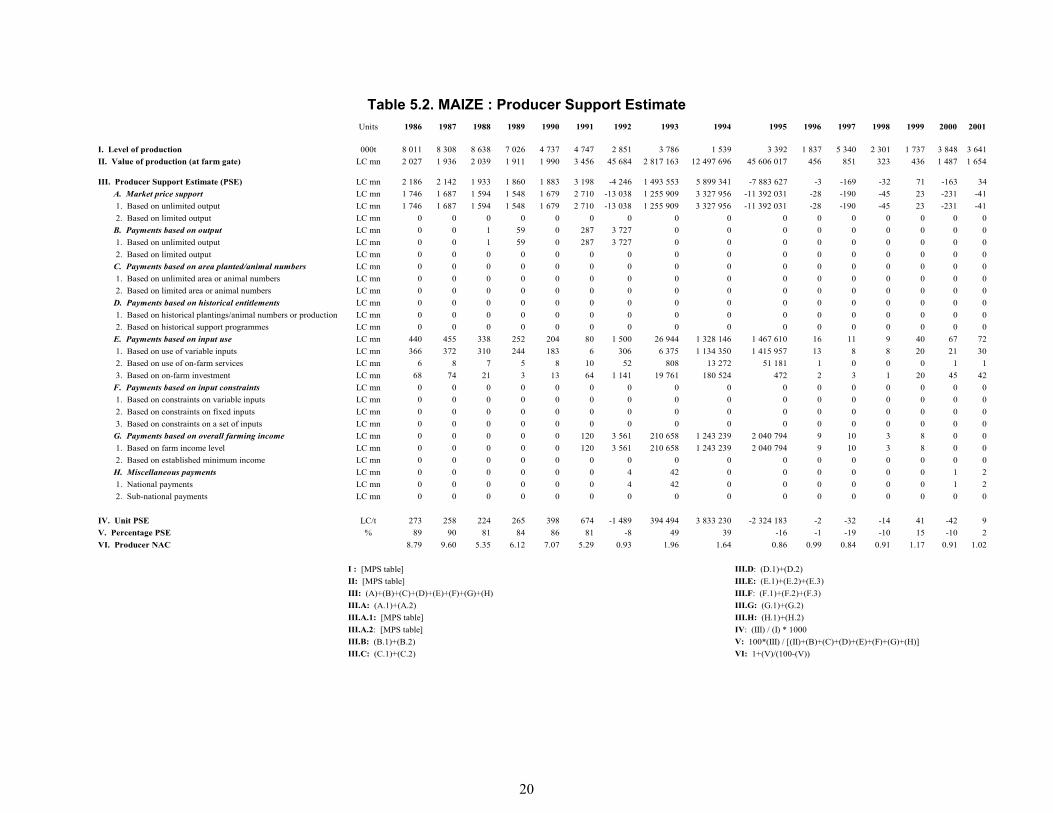

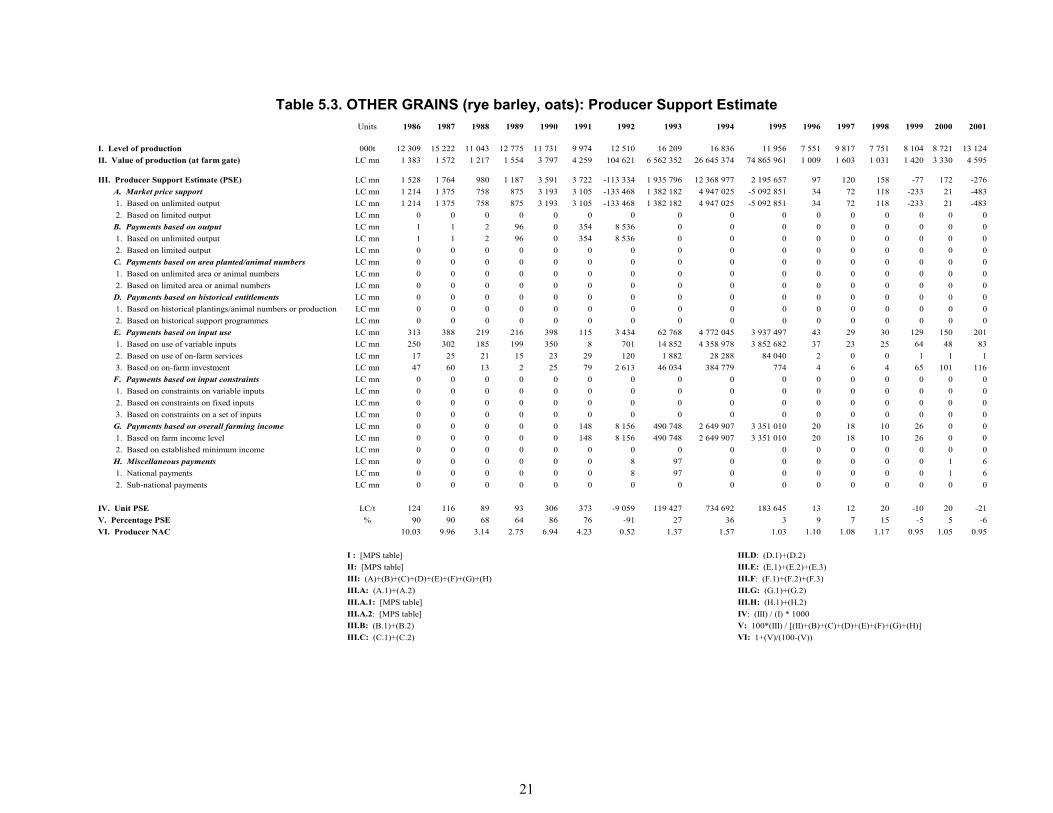

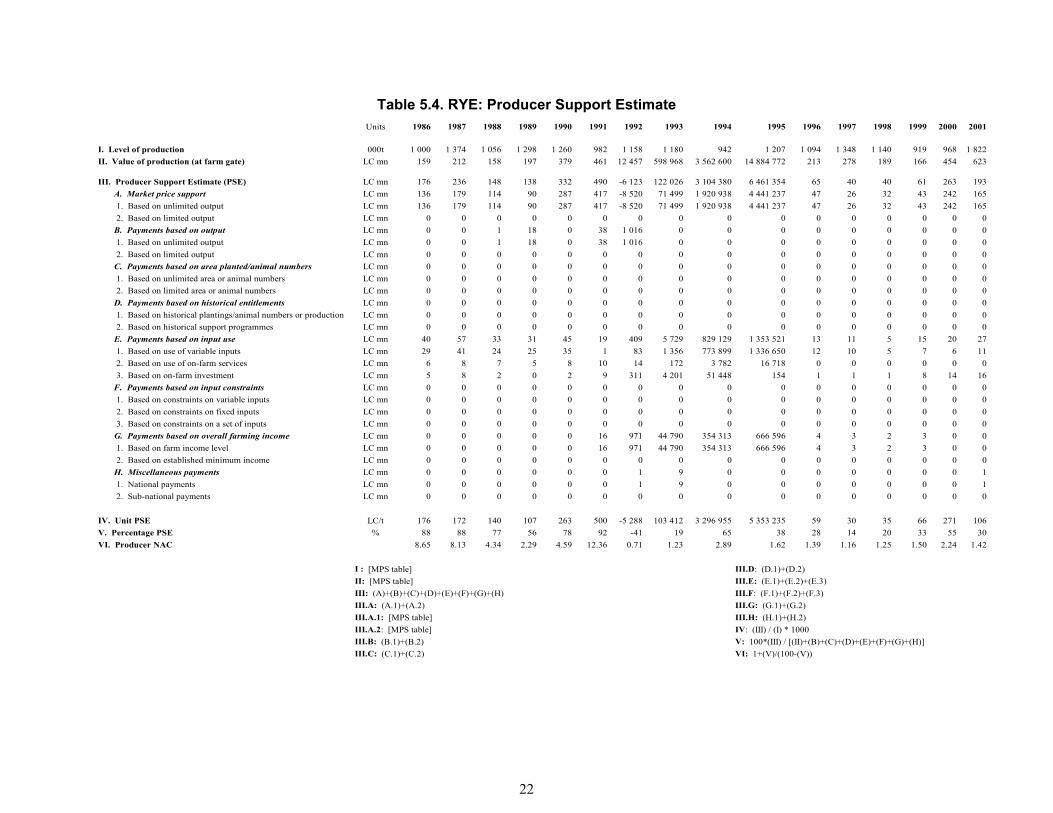

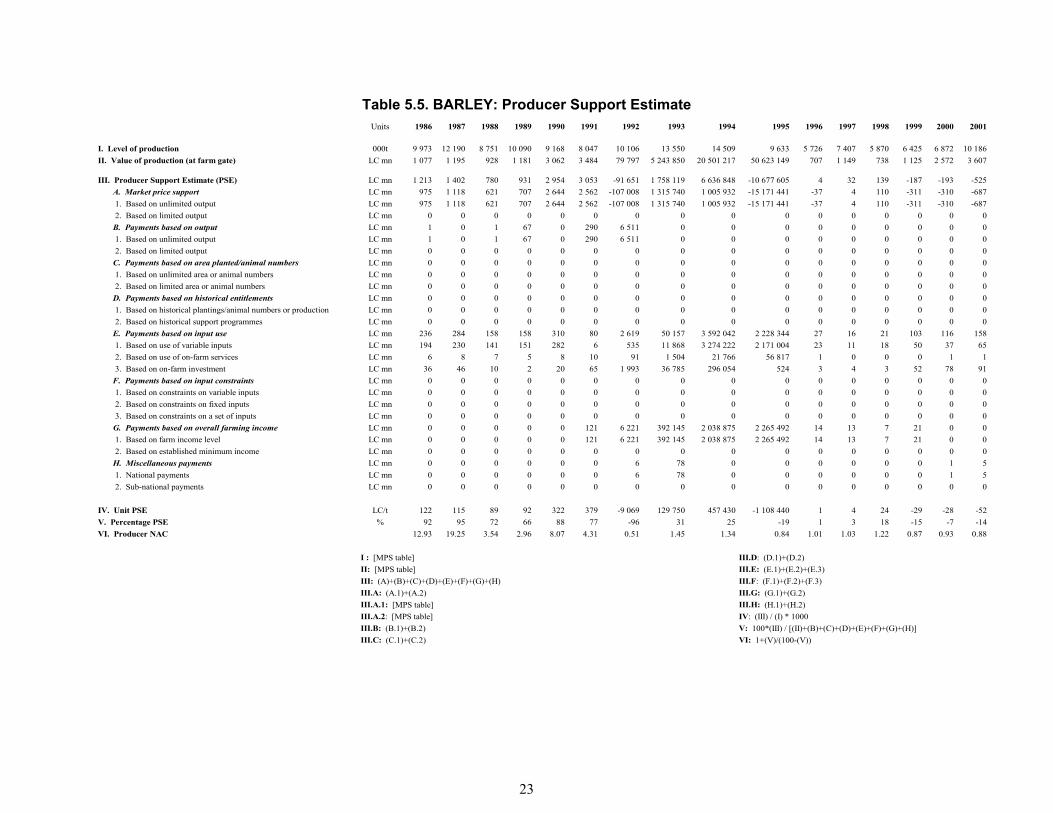

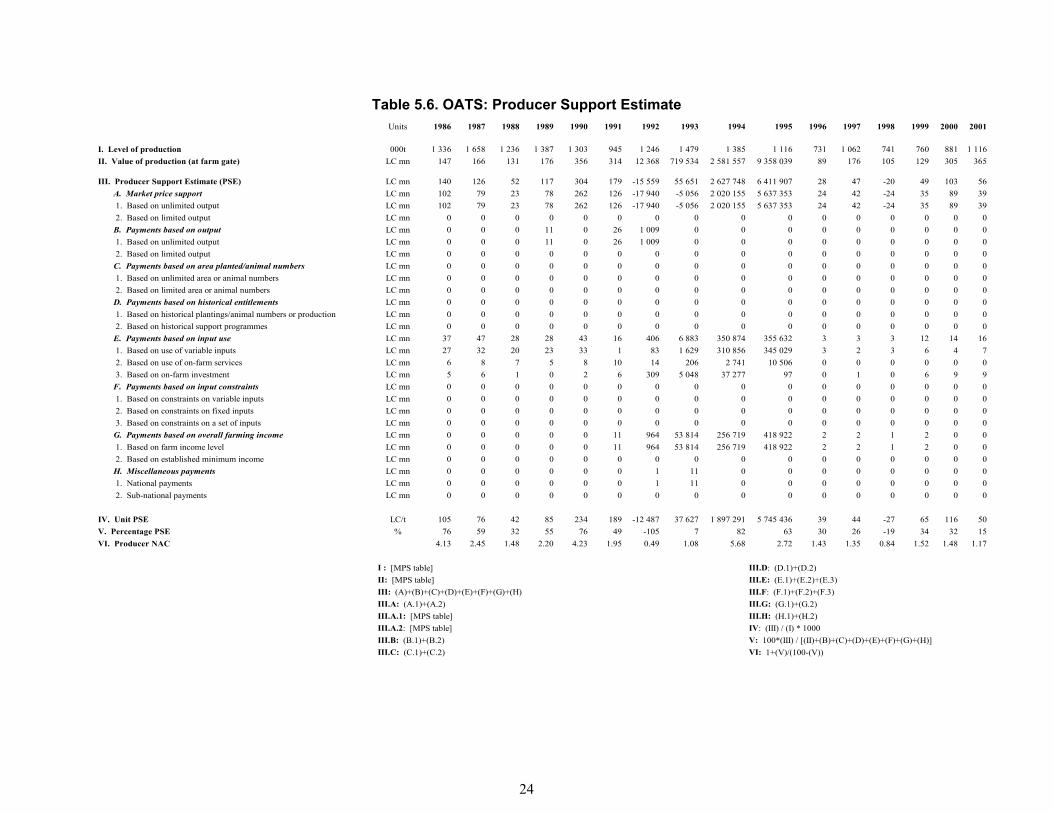

Table 5.1: Aggregate %PSEs and %CSEs for Ukraine 74

Table 5.2: Indicators and Composition of Total Support to Ukrainian Agriculture 79

Contentsvi

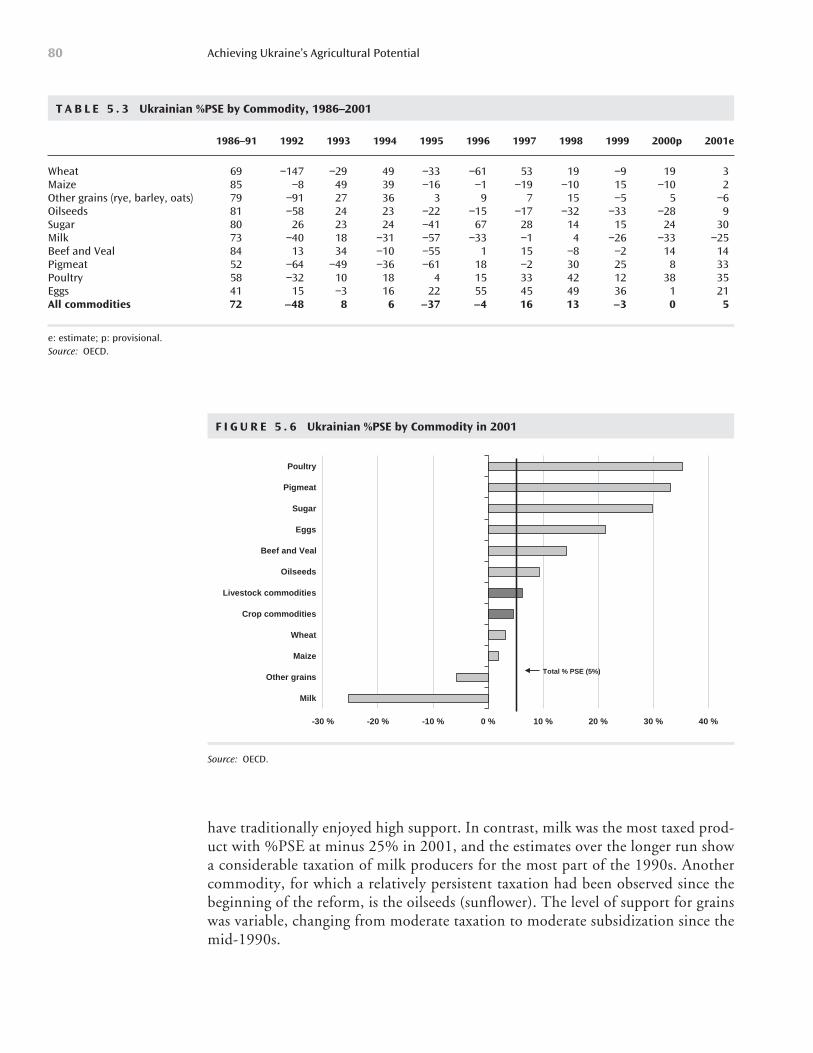

Table 5.3: Ukrainian %PSE by Commodity, 1986-2001 80

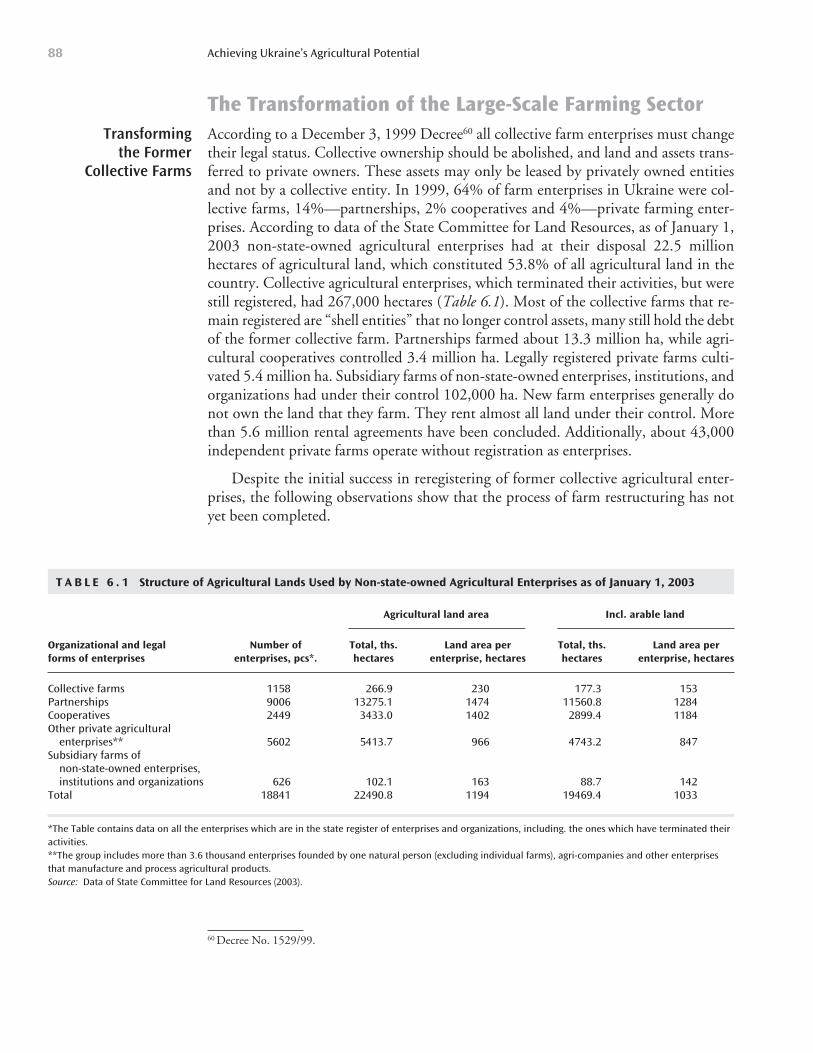

Table 6.1: Structure of Agricultural Lands Used by Non-state-owned Agricultural Enterprises as of January 1, 2003 88

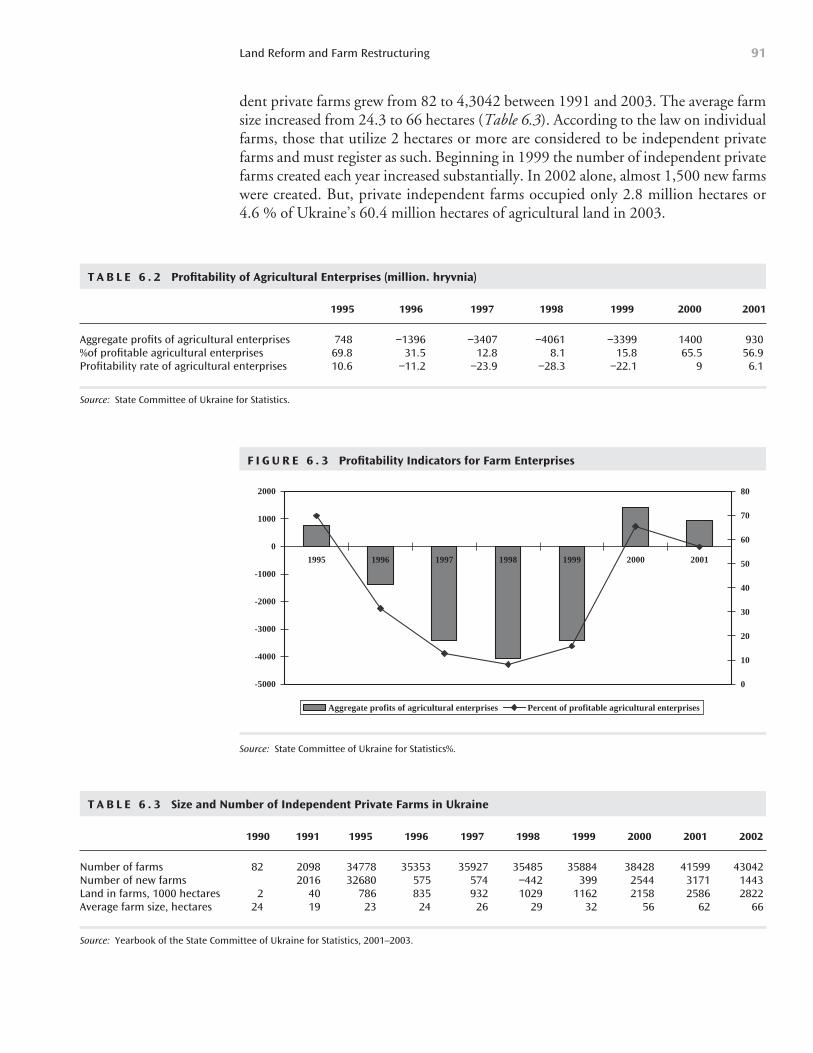

Table 6.2: Profitability of Agricultural Enterprises 91

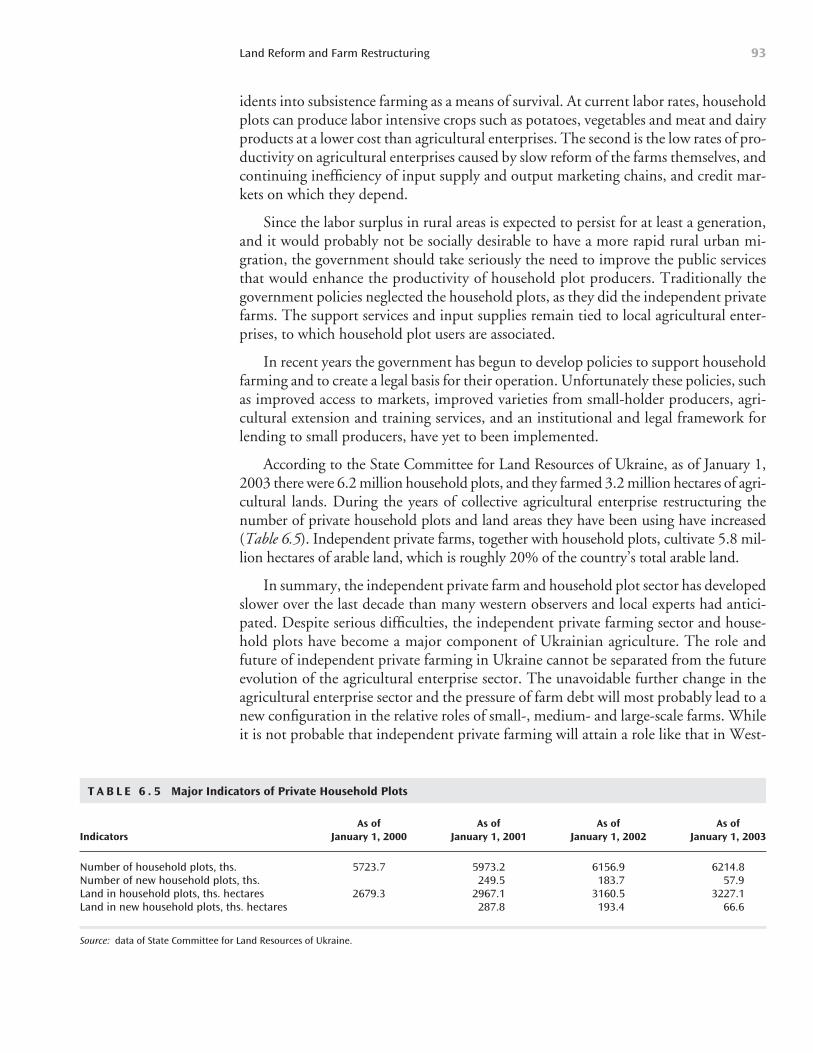

Table 6.3: Size and Number of Independent Private Farms in Ukraine 91

Table 6.4: Agricultural Gross Production 92

Table 6.5: Major Indicators of Private Household Plots 93

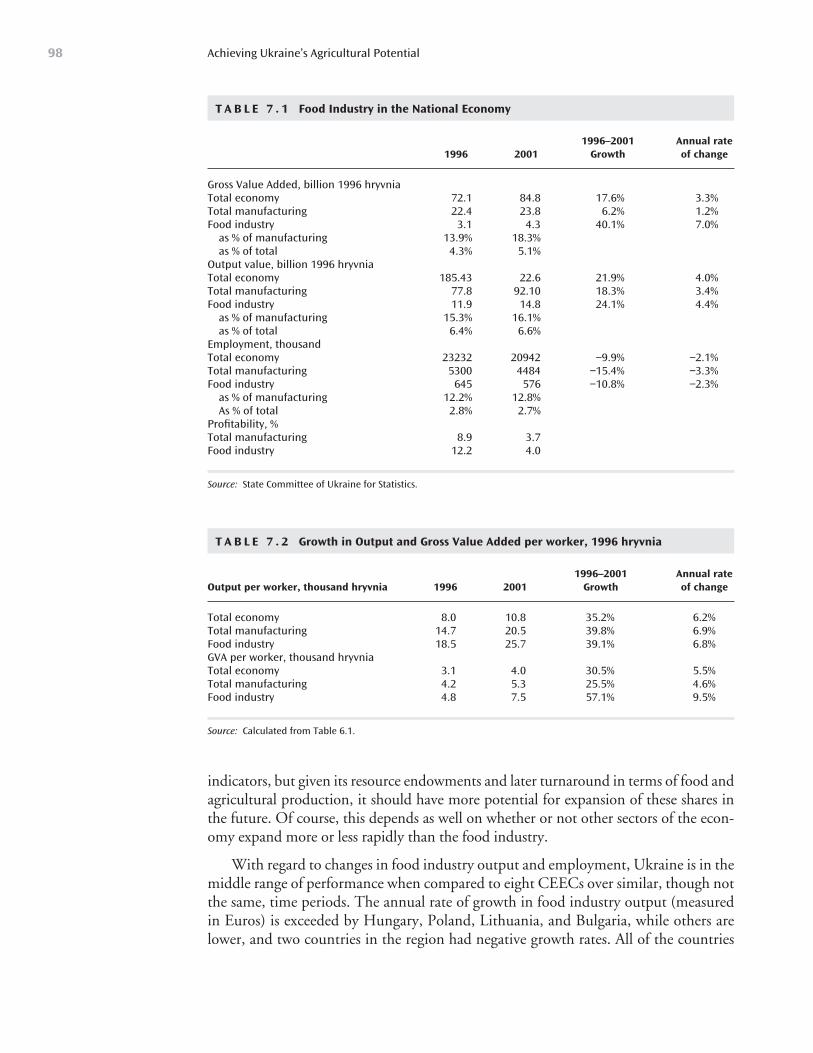

Table 7.1: Food Industry in the National Economy 98

Table 7.2: Growth in Output and Gross Value Added per worker, 1996 98

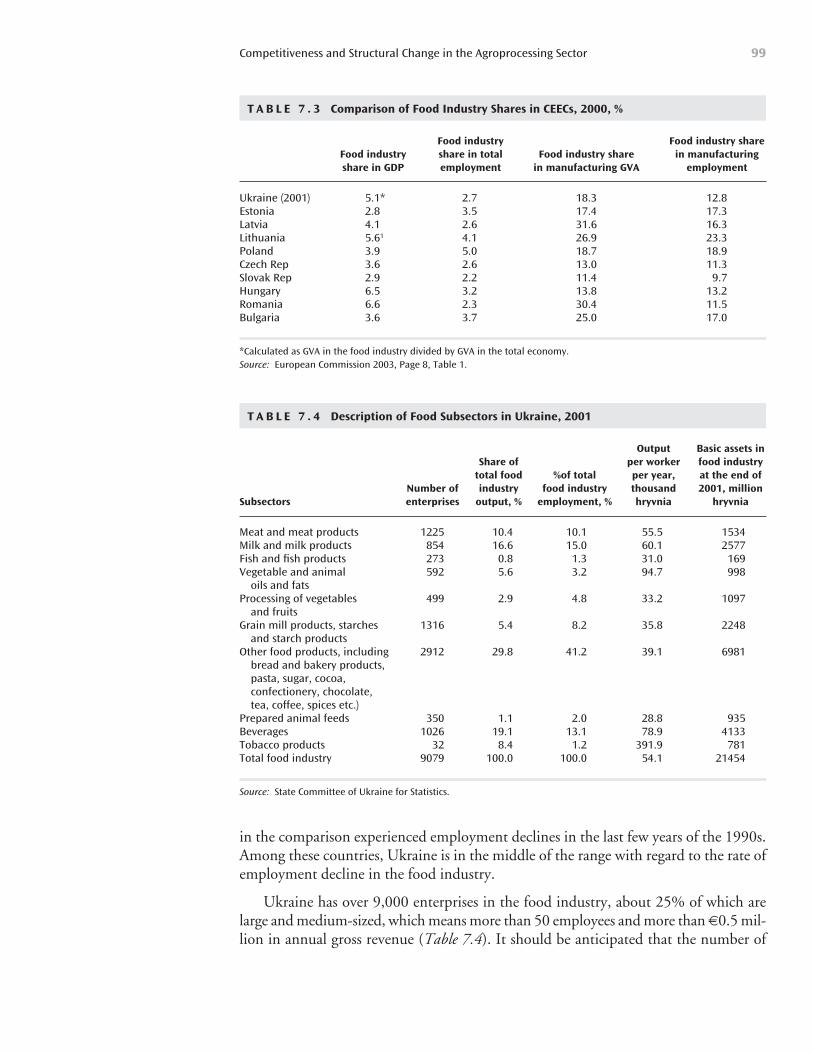

Table 7.3: Comparison of Food Industry Shares in CEECs, 2000 99

Table 7.4: Description of Food Subsectors in Ukraine, 2001 99

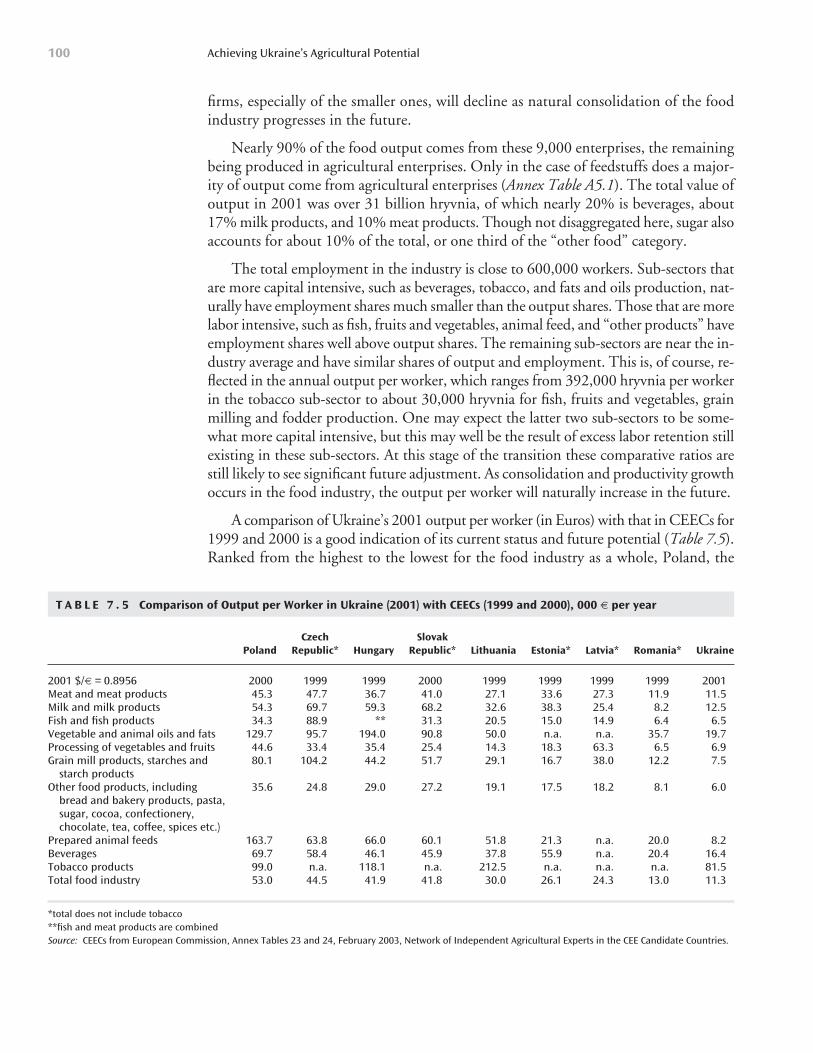

Table 7.5: Comparison of Output per Worker in Ukraine (2001) with CEECs (1999 and 2000) 100

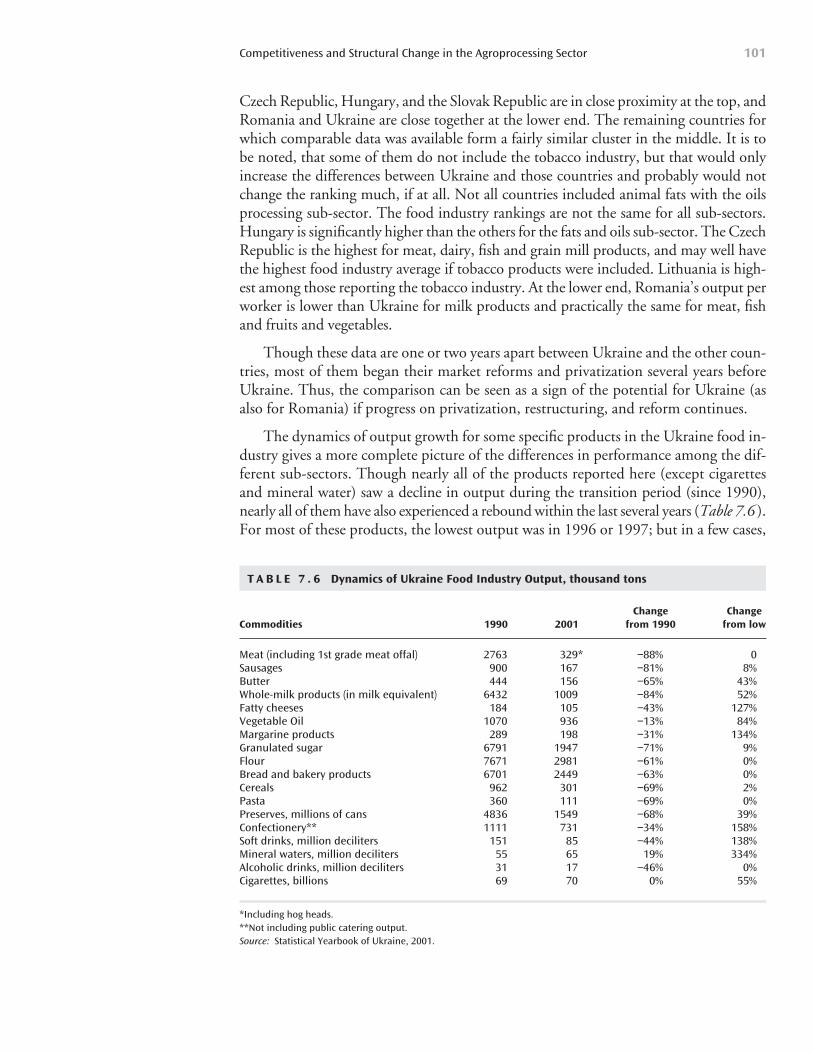

Table 7.6: Dynamics of Ukraine Food Industry Output 101

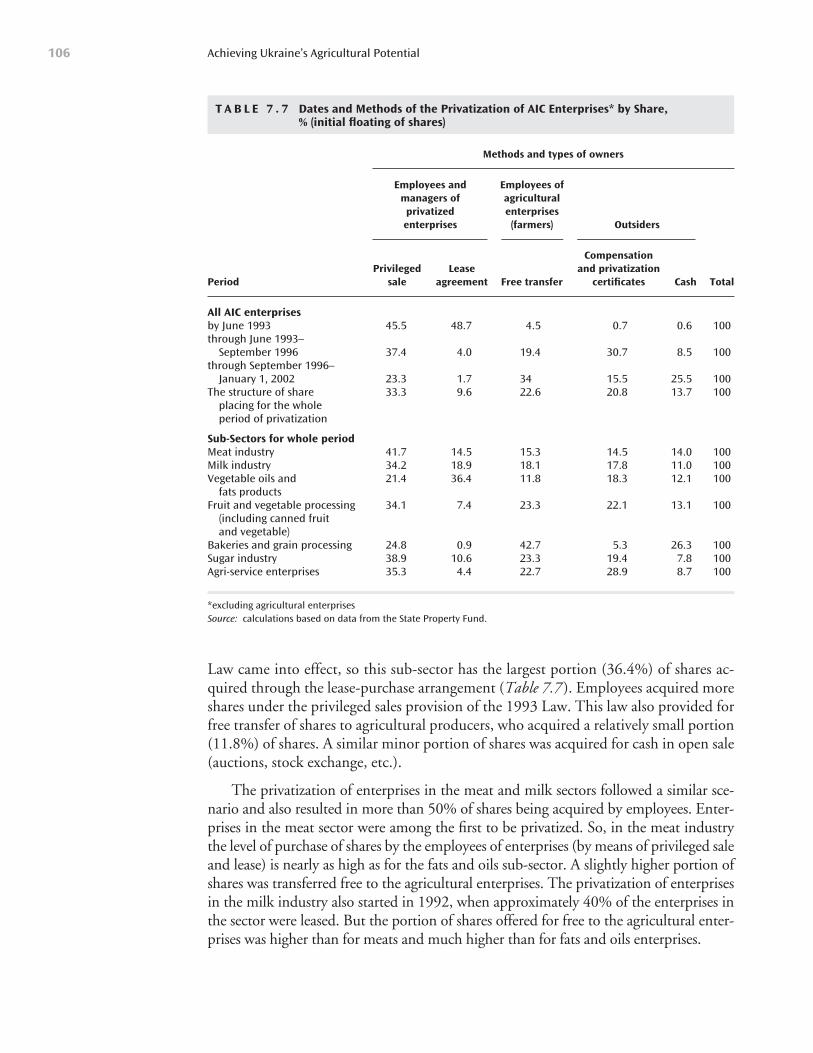

Table 7.7: Dates and Methods of the Privatization of AIC Enterprises by Share 106

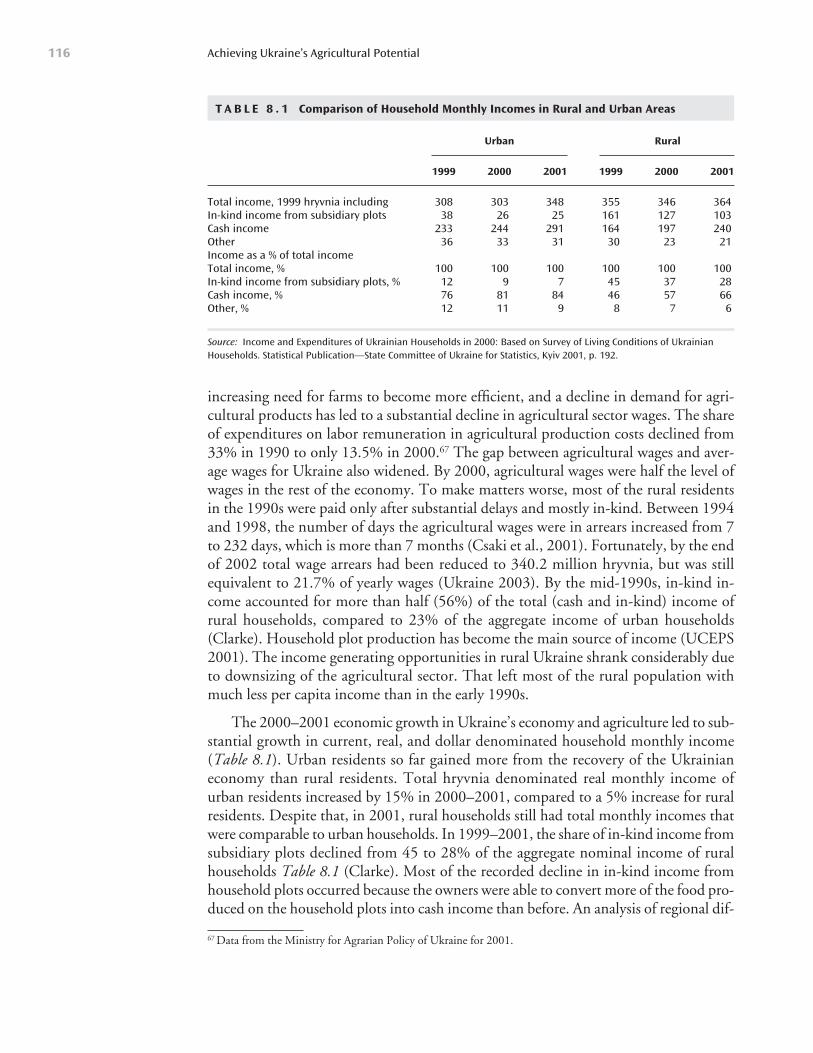

Table 8.1: Comparison of Household Monthly Incomes in Rural and Urban Areas 116

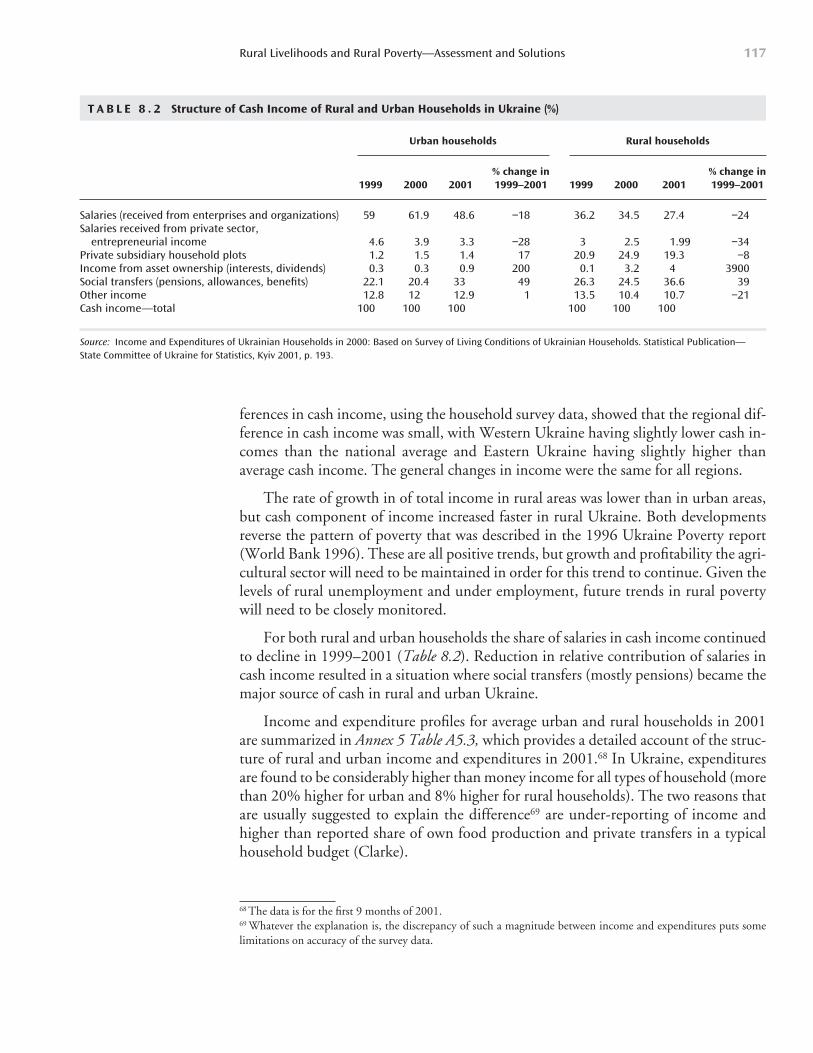

Table 8.2: Structure of Cash Income of Rural and Urban households in Ukraine 117

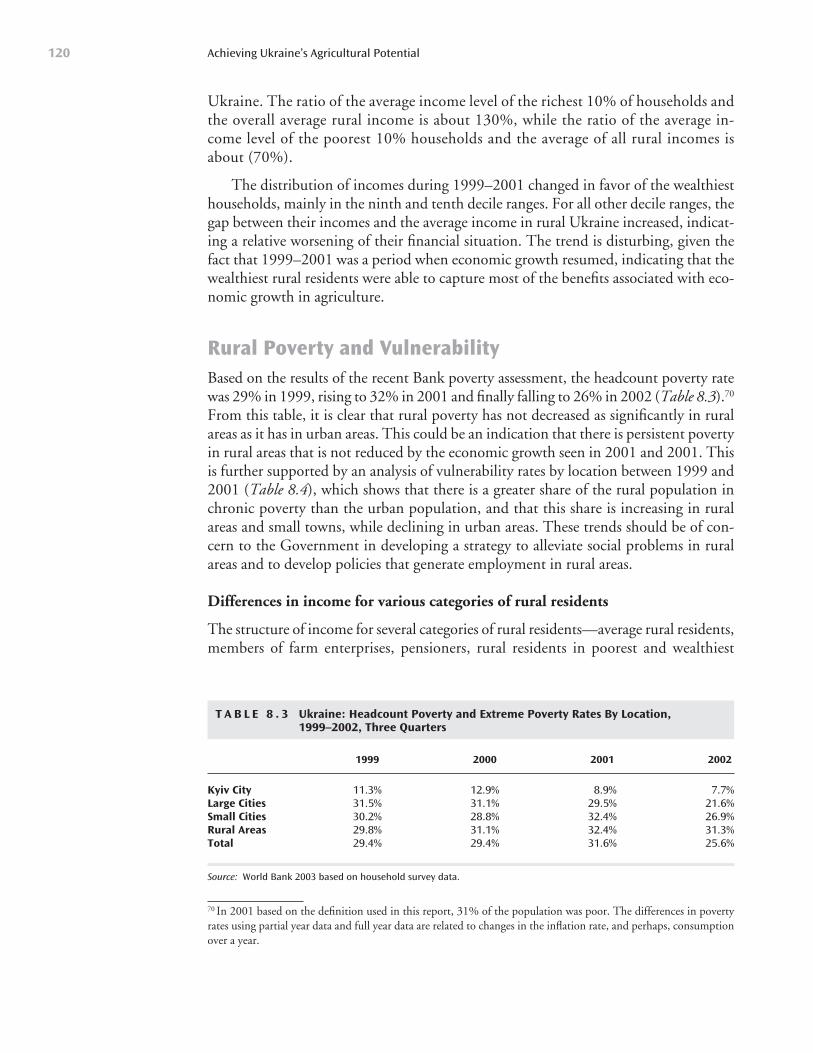

Table 8.3: Ukraine: Headcount Poverty and Extreme Poverty RatesBy Location, 1999-2002 Three Quarters 120

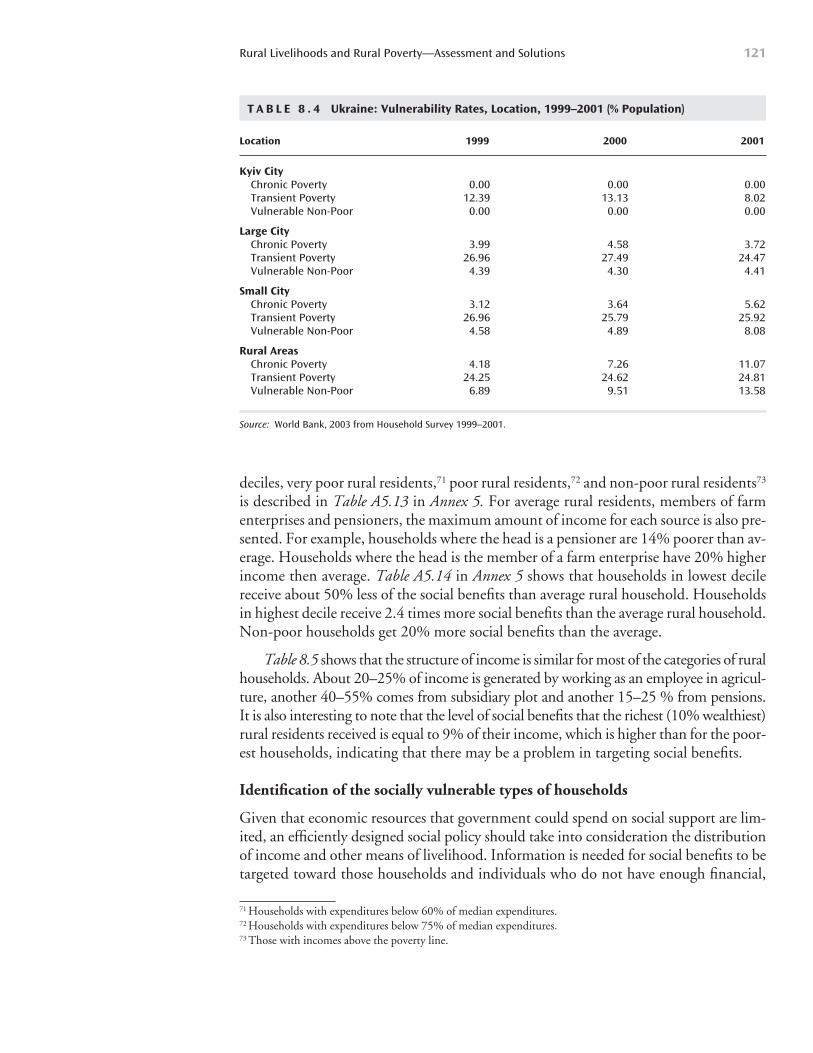

Table 8.4: Ukraine: Vulnerability Rates, Location, 1999-2001 121

Table 8.5: Structure of Income for Different Categoriesof Rural Residents in 2001 122

Table 8.6: Poverty Quotient Change Over Time for Very Poor Households, in Rural Areas 123

Table 8.7: Food Consumption in Urban and Rural Households in 2000 124

Table 8.8: Demographic Information about Rural Population, January 1 of each year 125

Table 8.9: The Balance of Rural Population 125

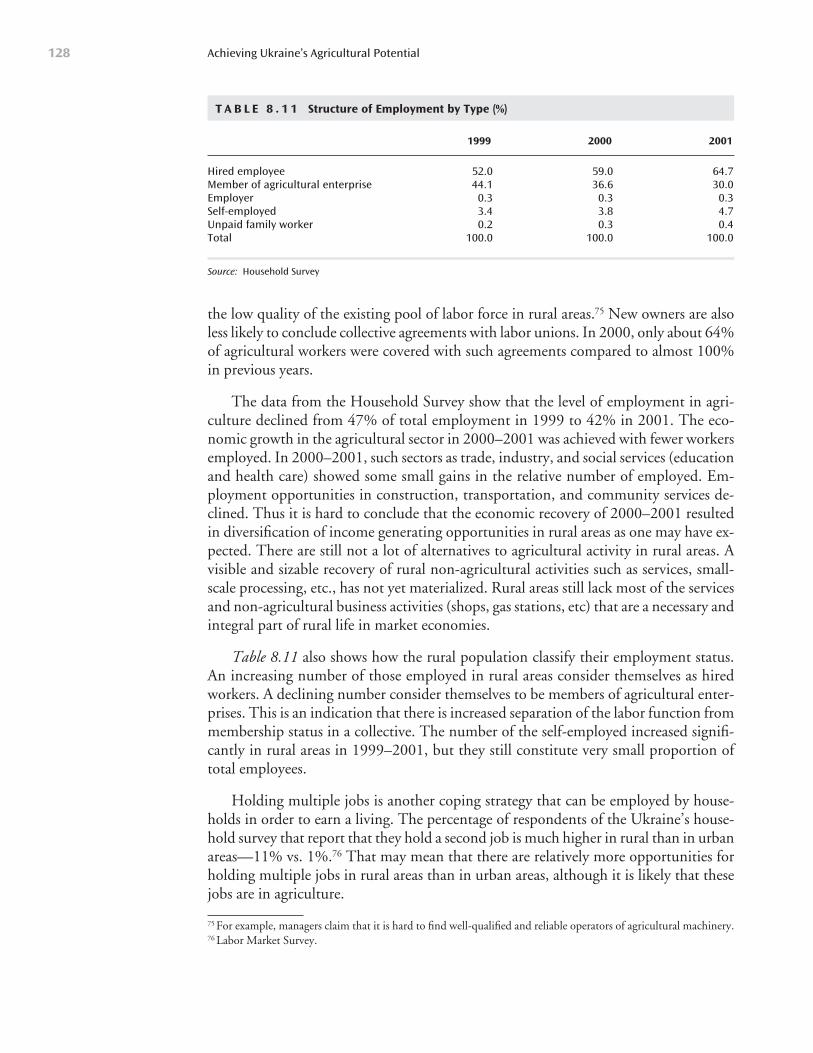

Table 8.10: The Structure of Rural Employment 127

Table 8.11: Structure of Employment by Type 128

Table 8.12: Ownership of Rural Housing 129

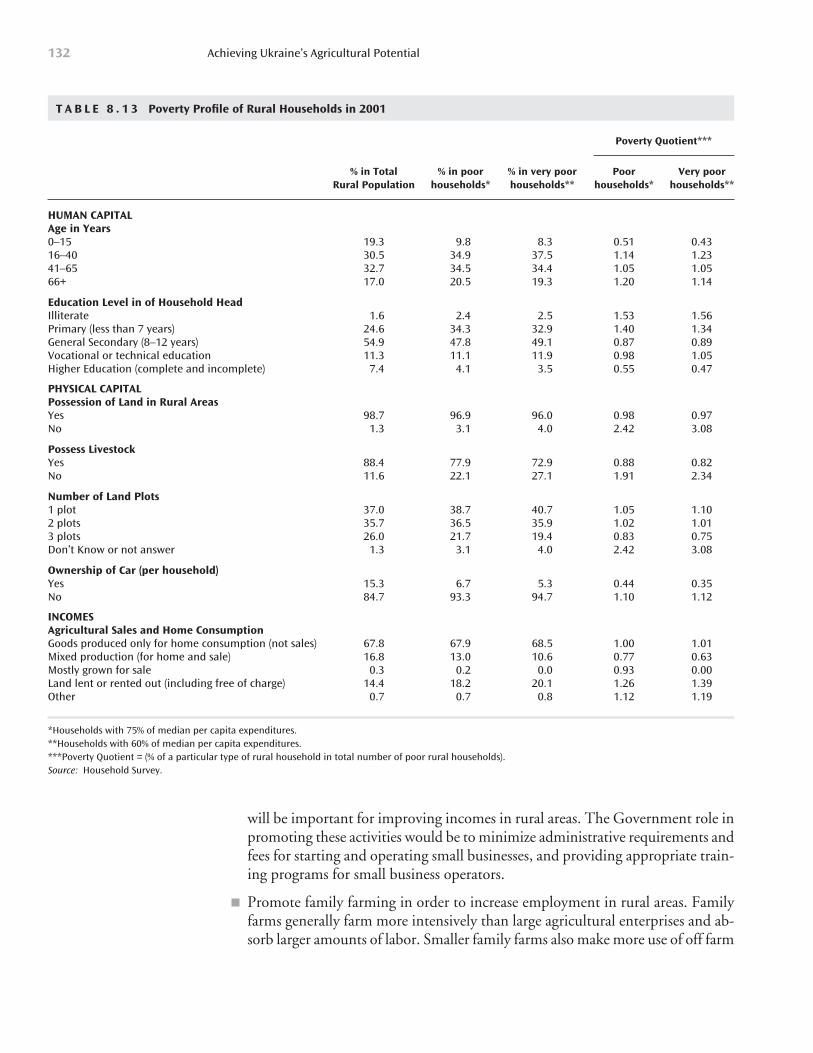

Table 8.13: Poverty Profile of Rural Households in 2001 132

Contents vii

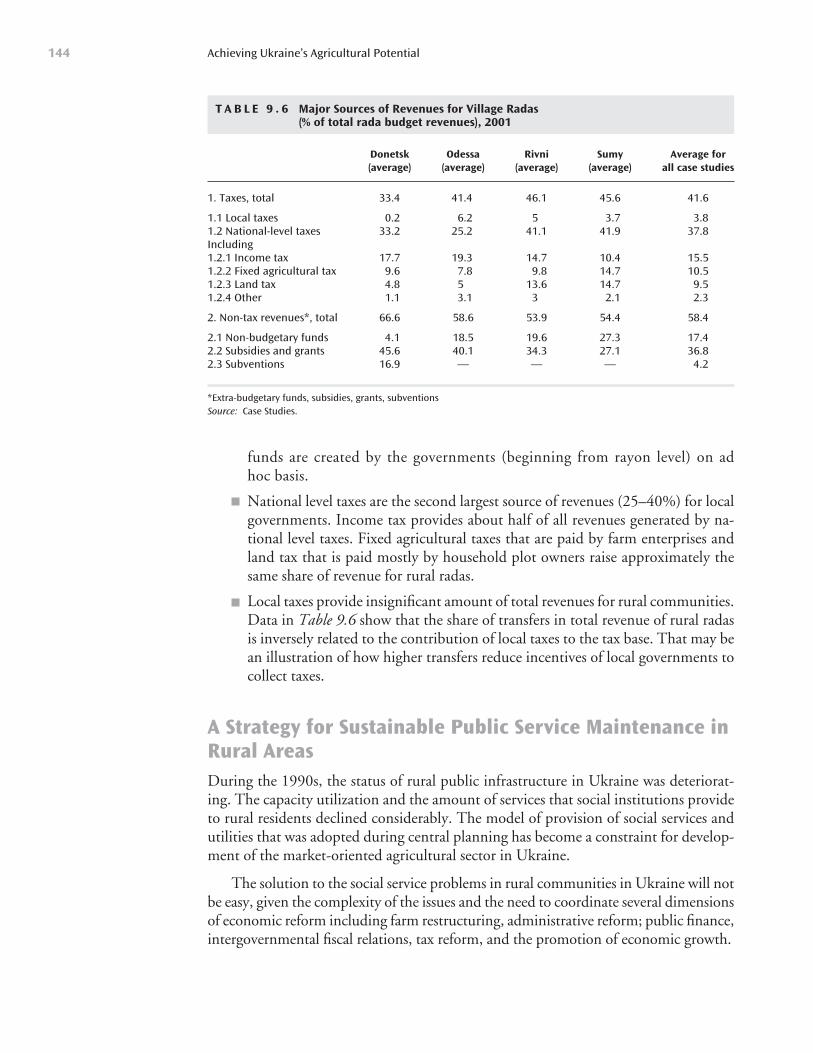

Table 9.1: Social Infrastructure in Rural Areas 136

Table 9.2: Development of Rural Social and Cultural Infrastructure 137

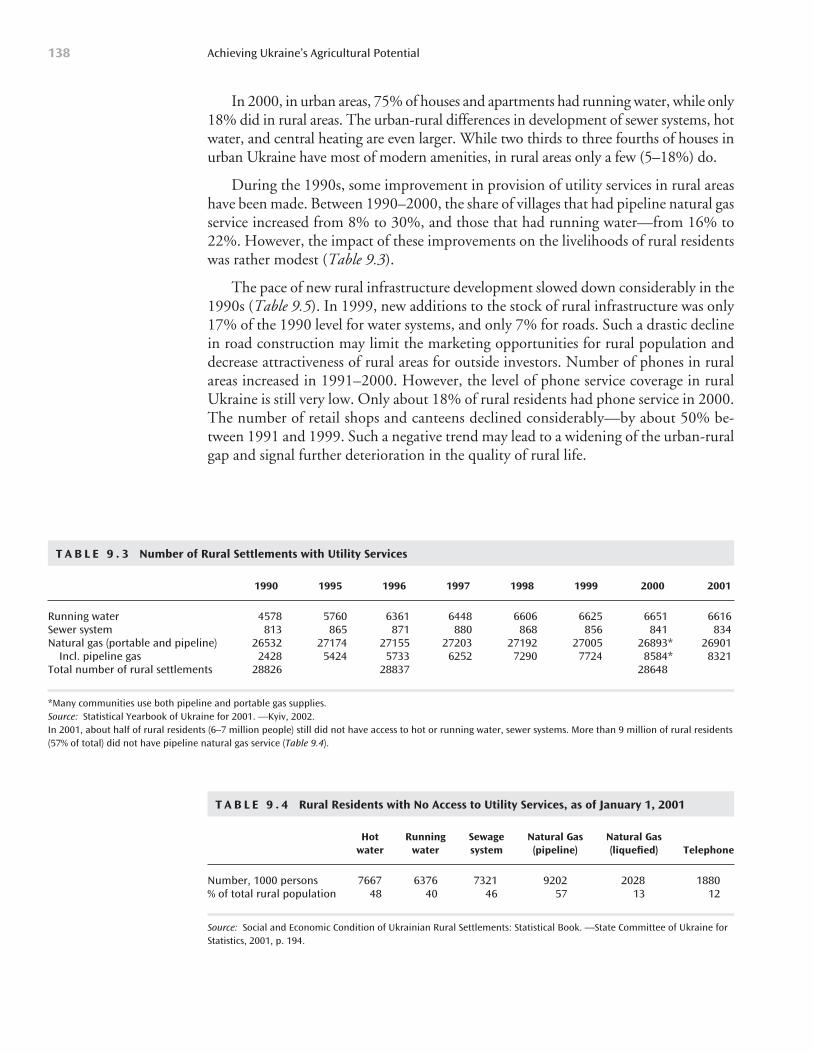

Table 9.3: Number of Rural Settlements with Utility Services 138

Table 9.4: Rural Residents with No Access to Utility Services, as of January 1, 2001 138

Table 9.5: Rural Infrastructure Development 139

Table 9.6: Major Sources of Revenues for Village Radas 144

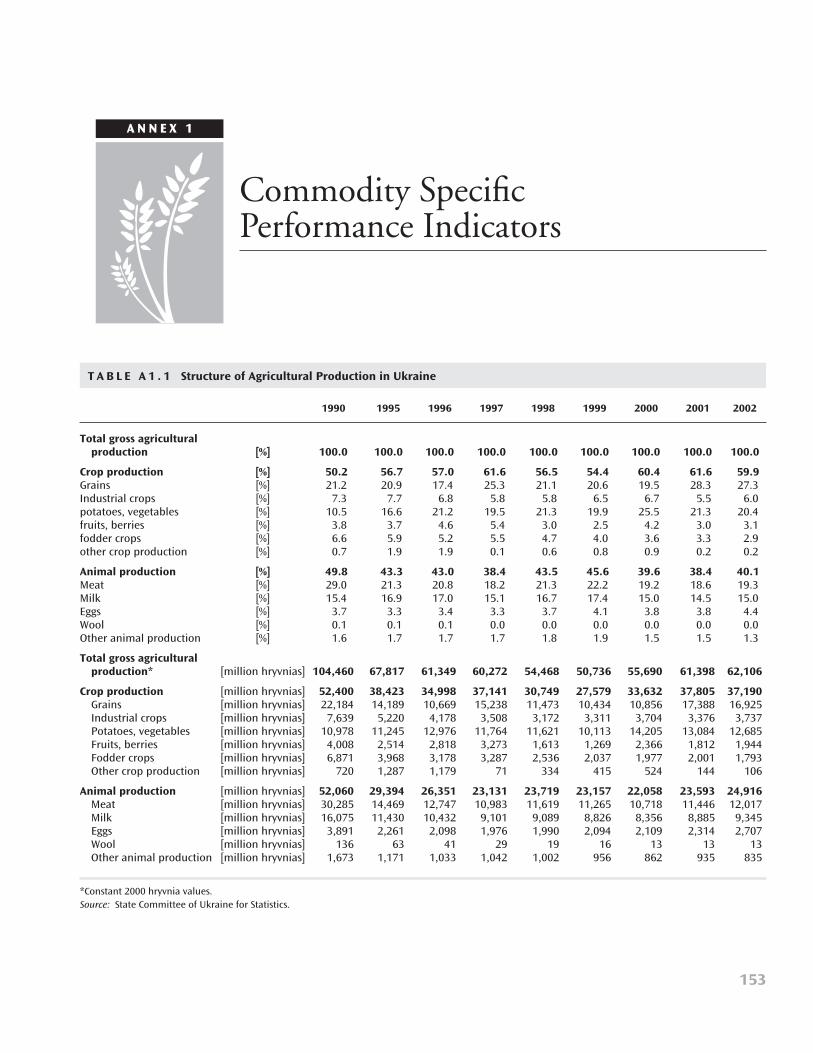

Table A1.1: Structure of Agricultural Production in Ukraine 153

Table A1.2: Structure of Gross Sales of Farm Enterprises 154

Table A1.3: Volume and Structure of Grain Production in Ukraine 154

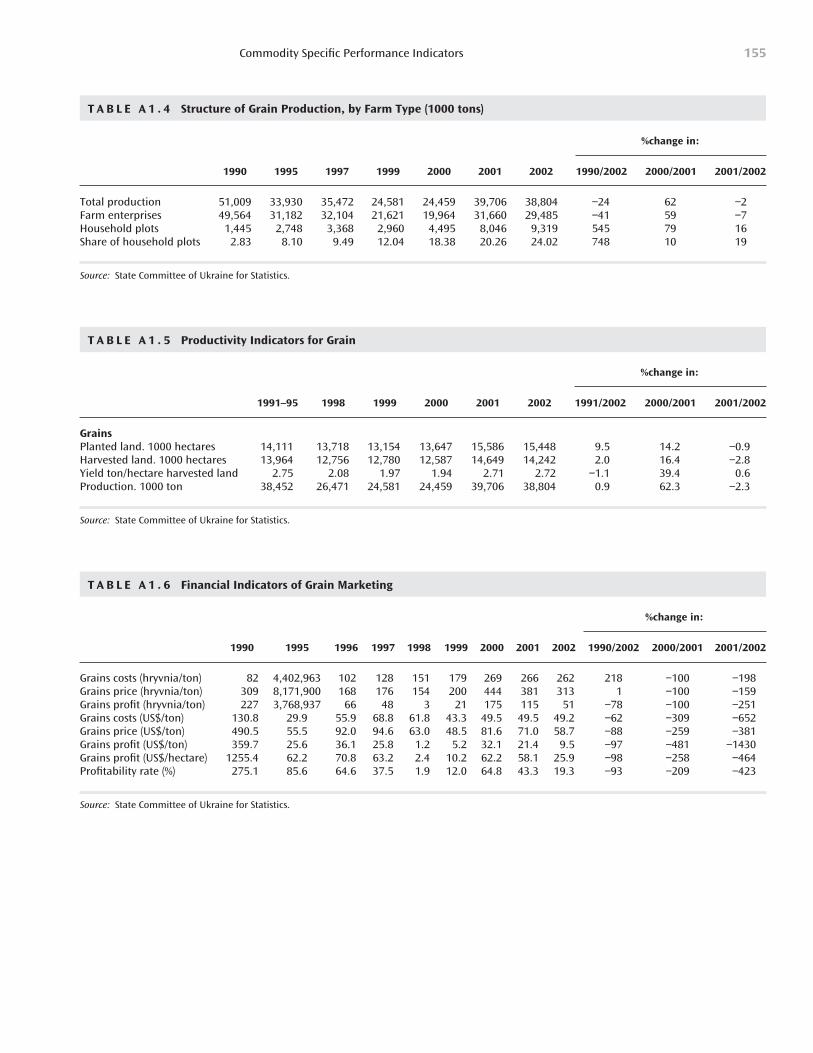

Table A1.4: Structure of Grain Production 155

Table A1.5: Productivity Indicators for Grain 155

Table A1.6: Financial Indicators of Grain Marketing 155

Table A1.7: Grain Produced and Marketed 156

Table A1.8: Grain Balance 157

Table A1.9: Major Indicators of Sunflower Sector 157

Table A1.10: Profitability of Sunflower Production 158

Table A1.11: Productivity of Sugarbeet Production 158

Table A1.12: Profitability of Sugarbeet Production 158

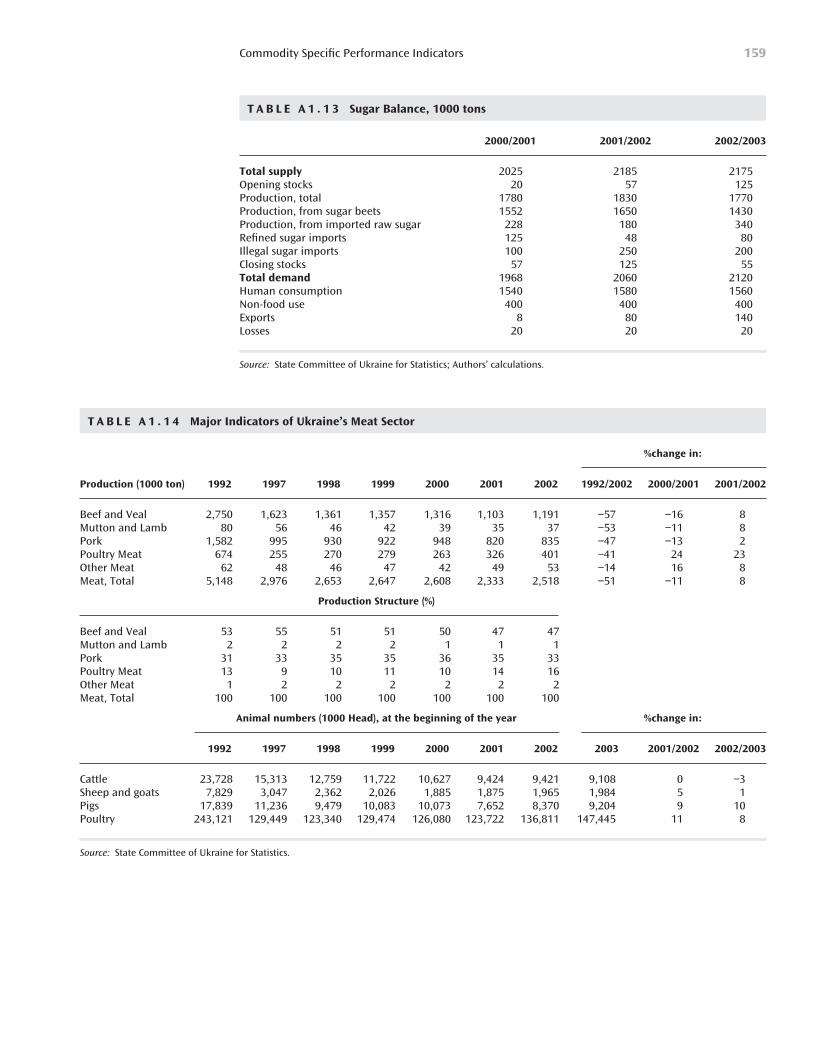

Table A1.13: Sugar Balance 159

Table A1.14: Major Indicators of Ukraine's Meat Sector 159

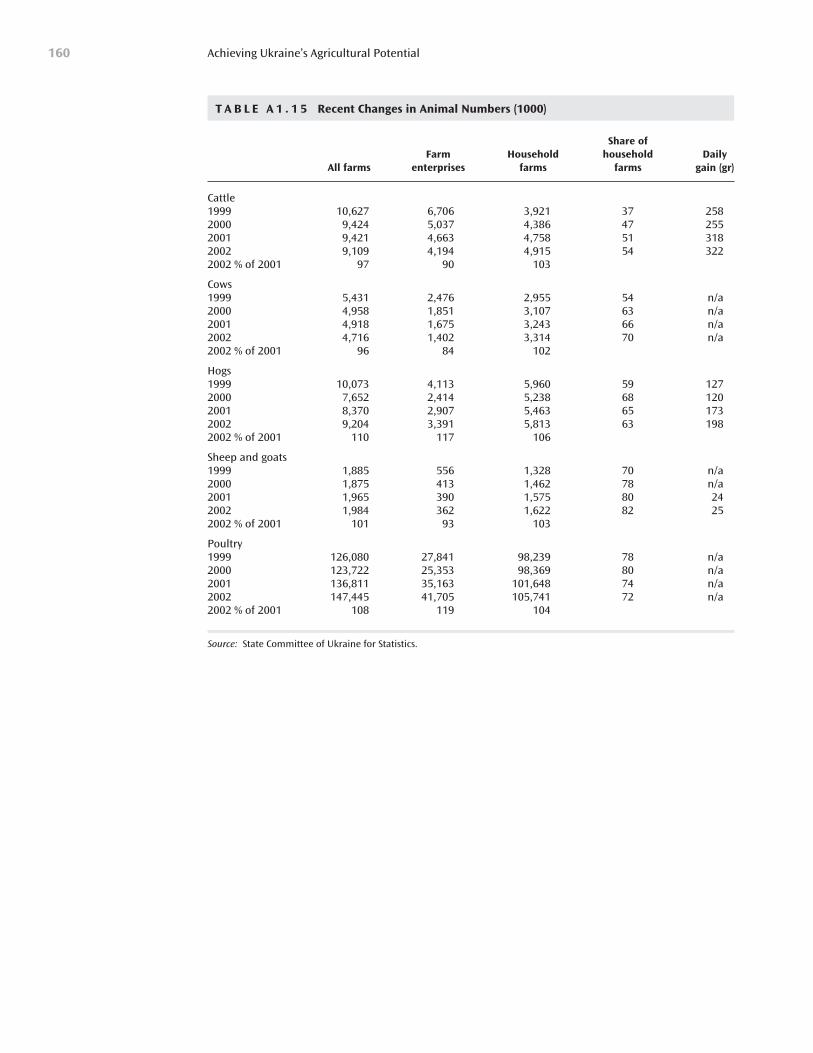

Table A1.15: Recent Changes in Animal Numbers 160

Table A1.16: Meat Marketing and Profitability Indicators 161

Table A1.17: Meat Marketing Indicators, by Type of Marketing Agent 161

Table A1.18: Meat Balance 162

Table A1.19: Milk Sector: Production and Profitability Trends 162

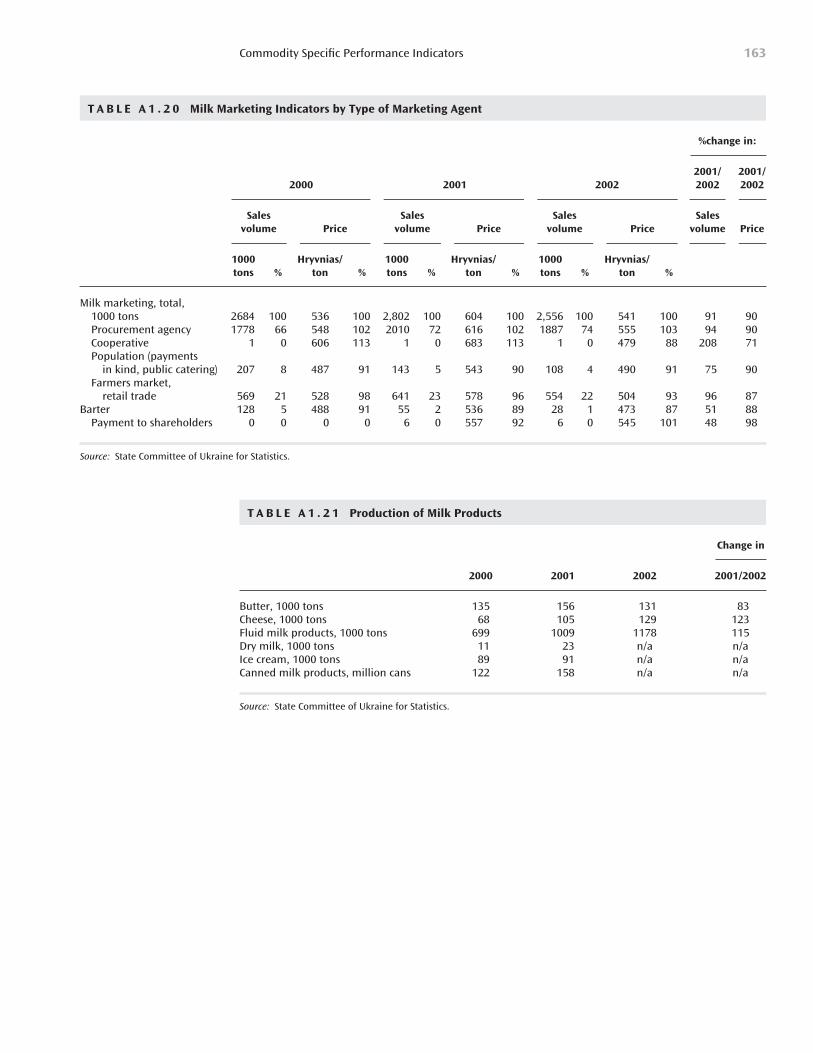

Table A1.20: Milk Marketing Indicators by Type of Marketing Agent 163

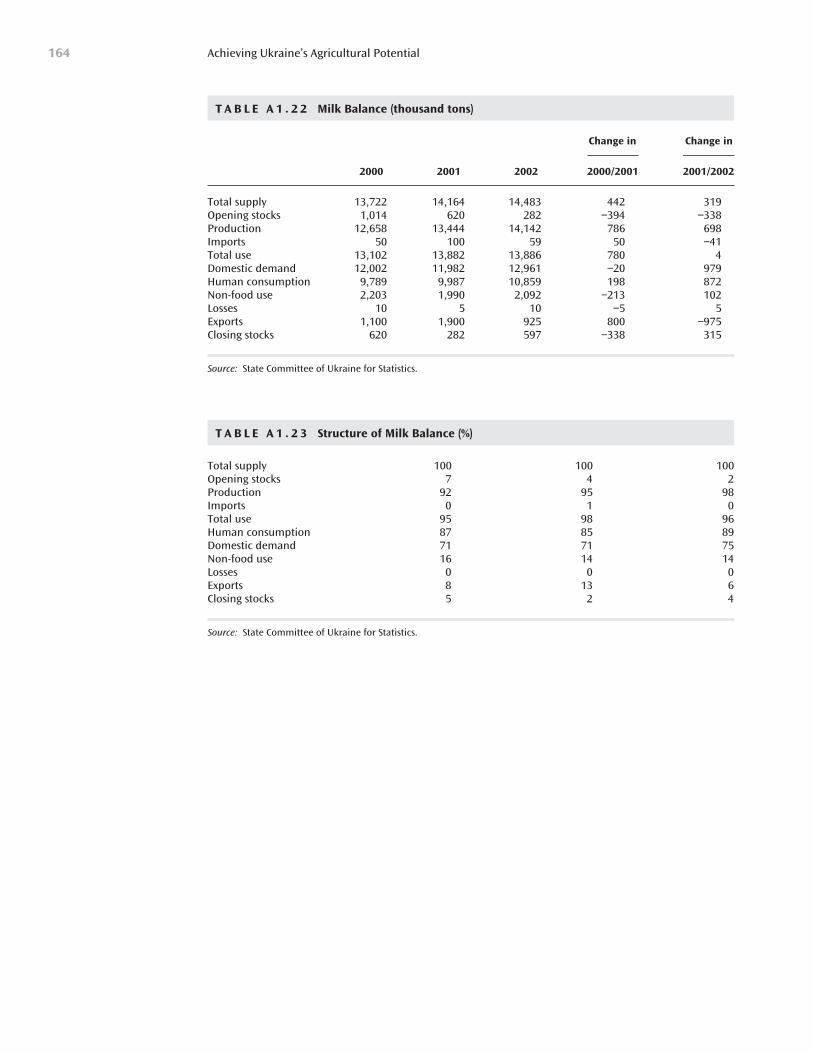

Table A1.21: Production of Milk Products 163

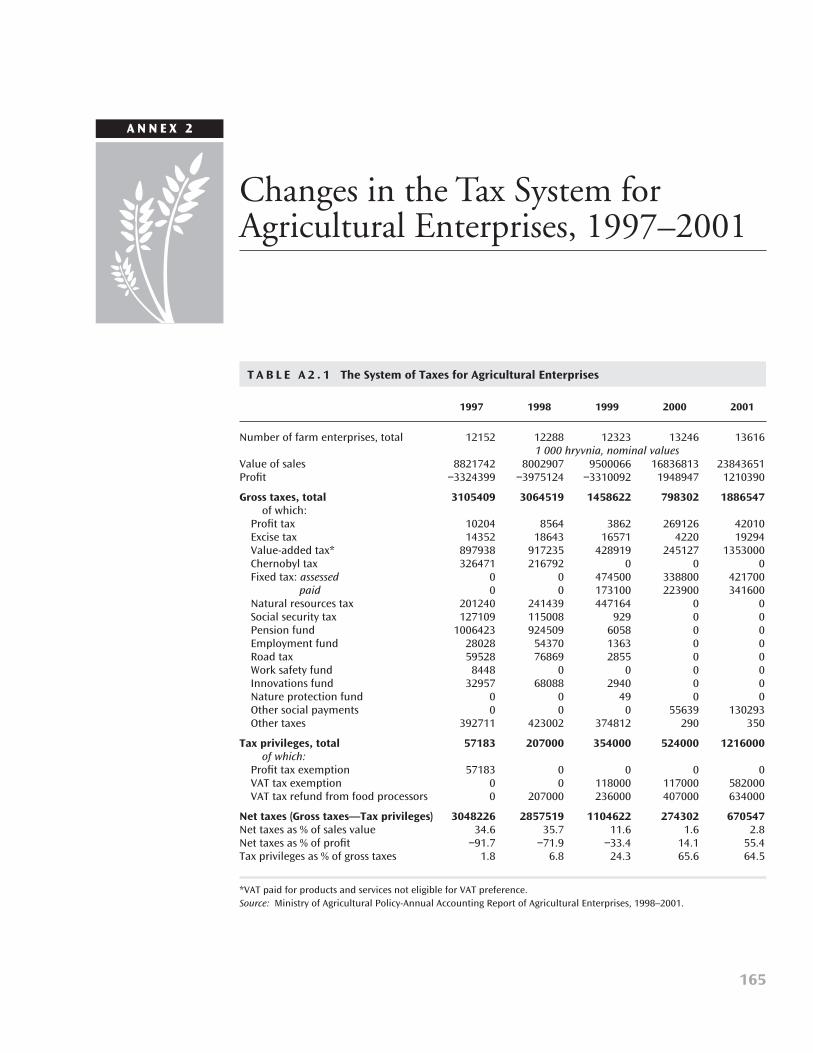

Table A1.22: Milk Balance 164

Table A1.23: Structure of Milk Balance 164

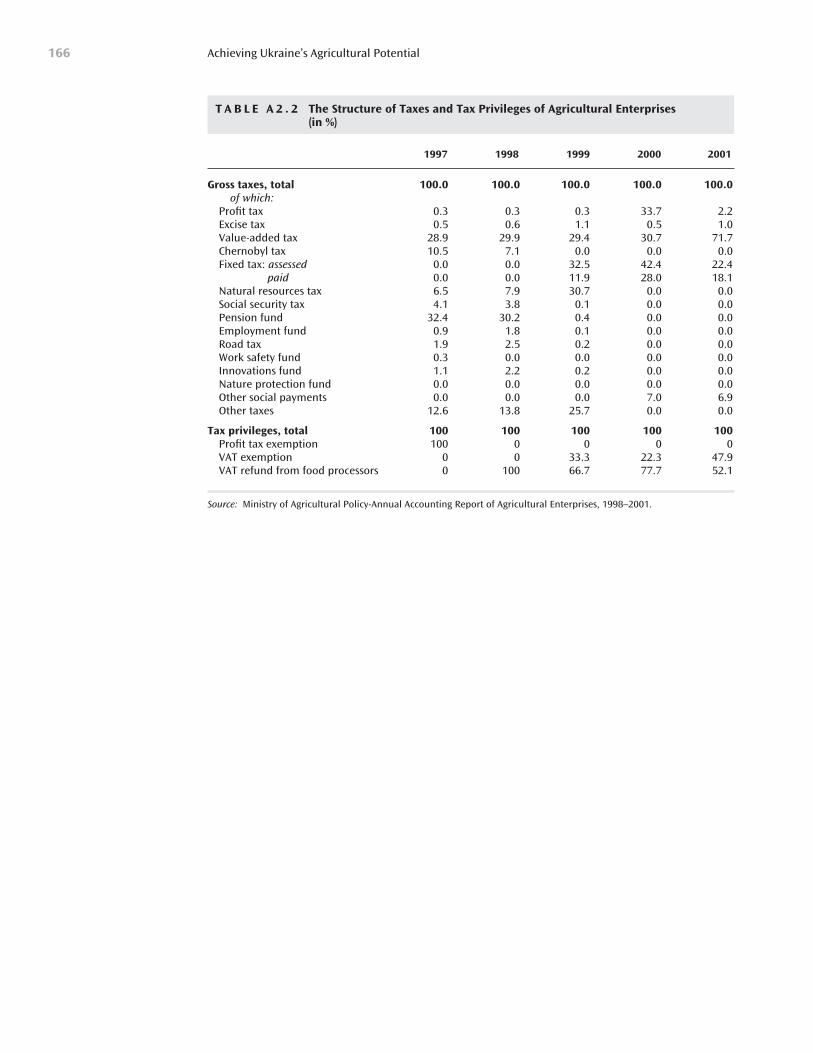

Table A2.1: The System of Taxes for Agricultural Enterprises 165

Table A2.2: The Structure of Taxes and Tax Privileges of Agricultural Enterprises 166

Contentsviii

Table A4.1.: Domestic Sugar Quota and Minimum Prices 179

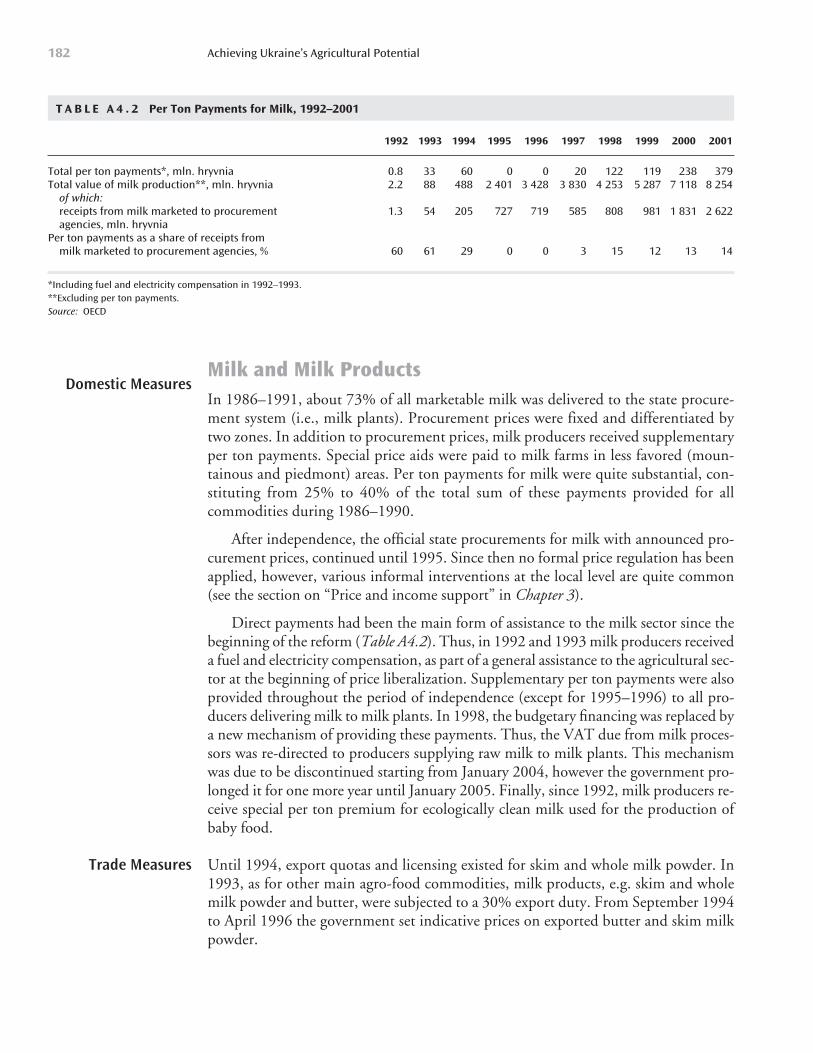

Table A4.2: Per Ton Payments for Milk, 1992-2001 182

Table A4.3: Per Ton Payments for Cattle, 1992-2001 185

Table A4.4: Per Ton Payments for Pigmeat, 1992-2001 187

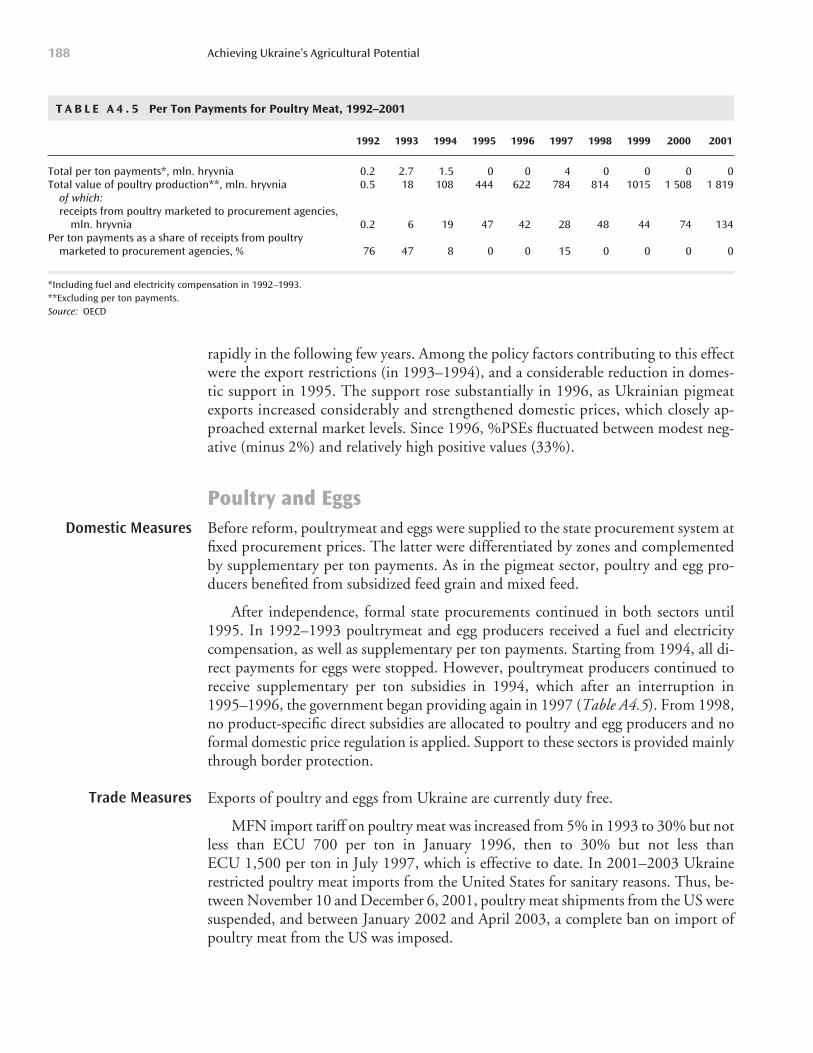

Table A4.5: Per Ton Payments for Poultry Meat, 1992-2001 188

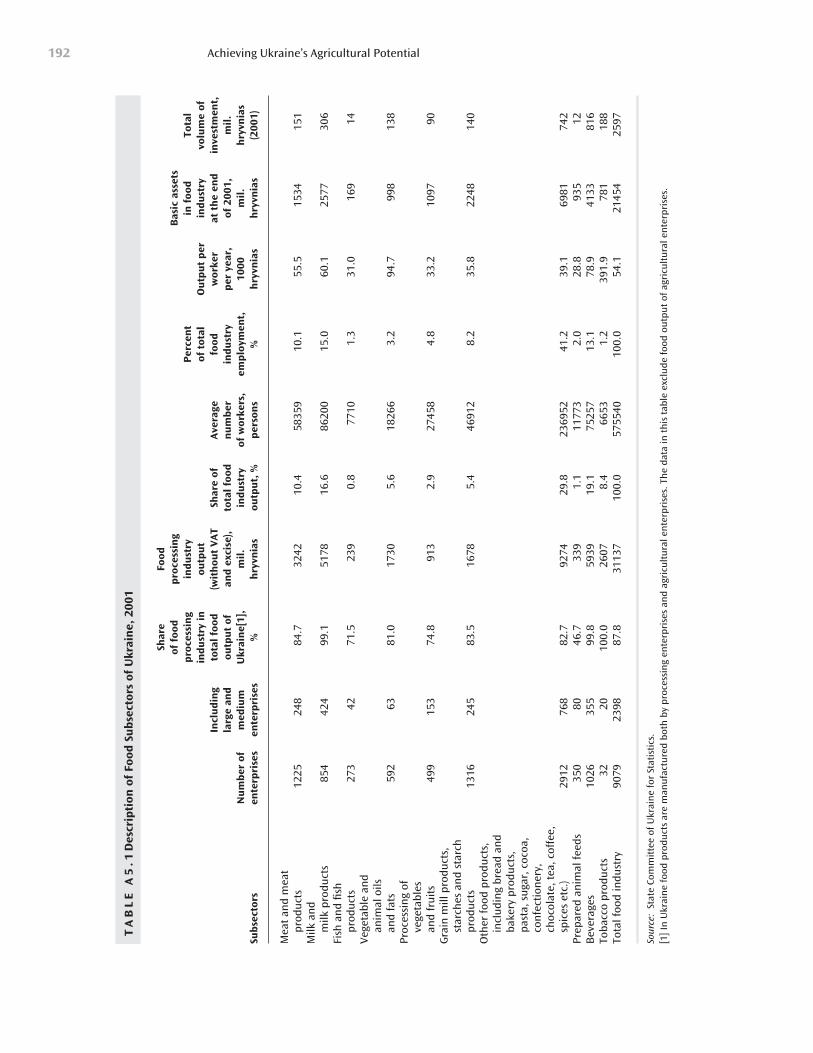

Table A5.1: Description of Food Subsectors of Ukraine, 2001 192

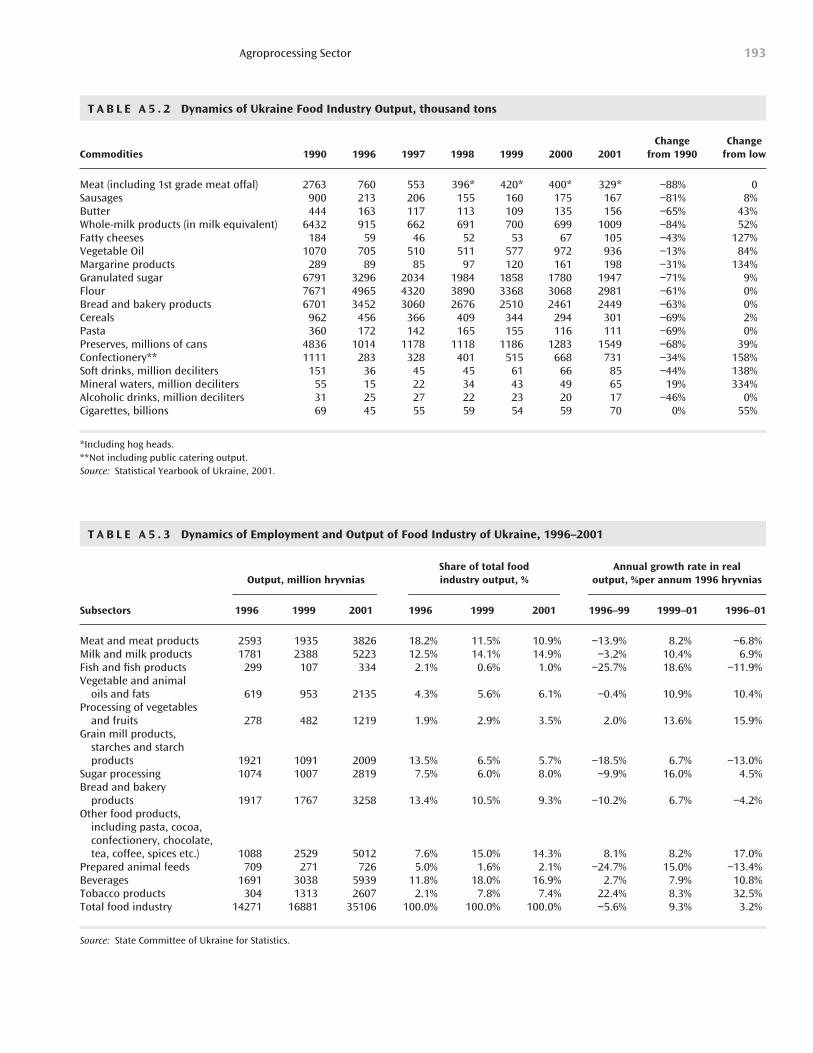

Table A5.2: Dynamics of Ukraine Food Industry Output 193

Table A5.3: Dynamics of Employment and Output of Food Industry of Ukraine, 1996-2001 193

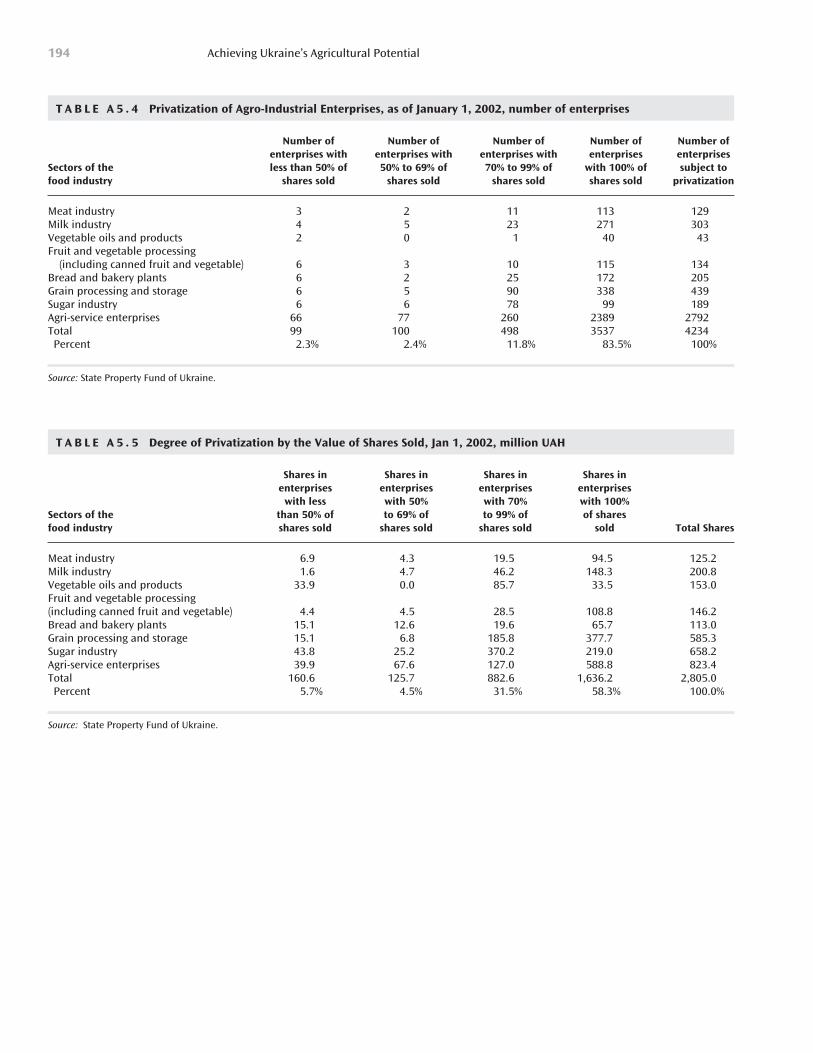

Table A5.4: Privatization of Agro-Industrial Enterprises, as of January 1, 2002 194

Table A5.5: Degree of Privatization by the Value of Shares Sold, Jan 1, 2002 194

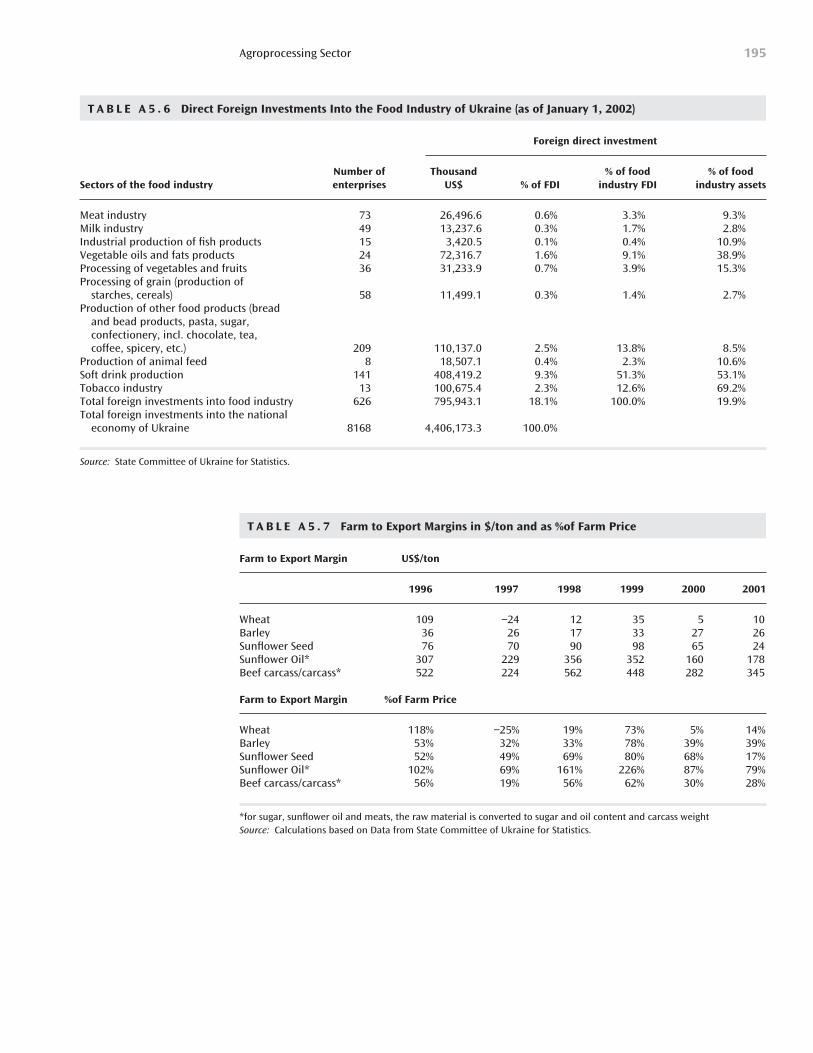

Table A5.6: Direct Foreign Investments Into the Food Industry of Ukraine (as of January 1, 2002) 195

Table A5.7: Farm to Export Margins in $/ton and as % of Farm Price 195

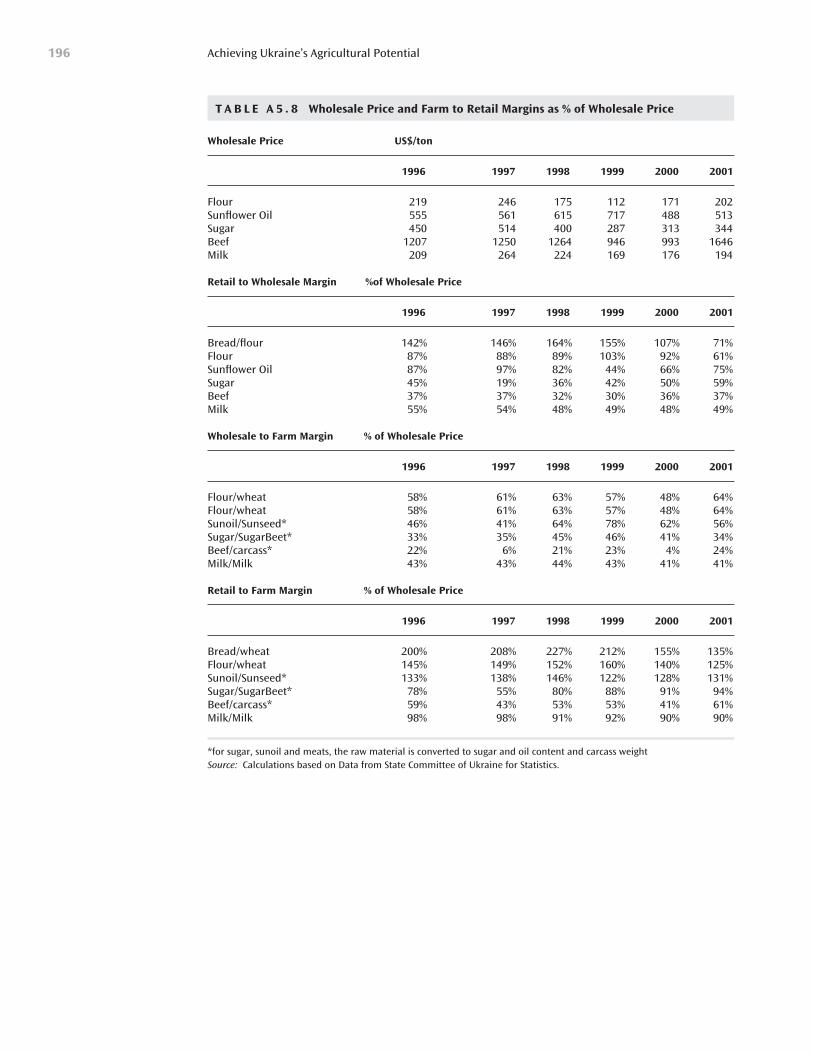

Table A5.8: Wholesale Price and Farm to Retail Margins as % of Wholesale Price 196

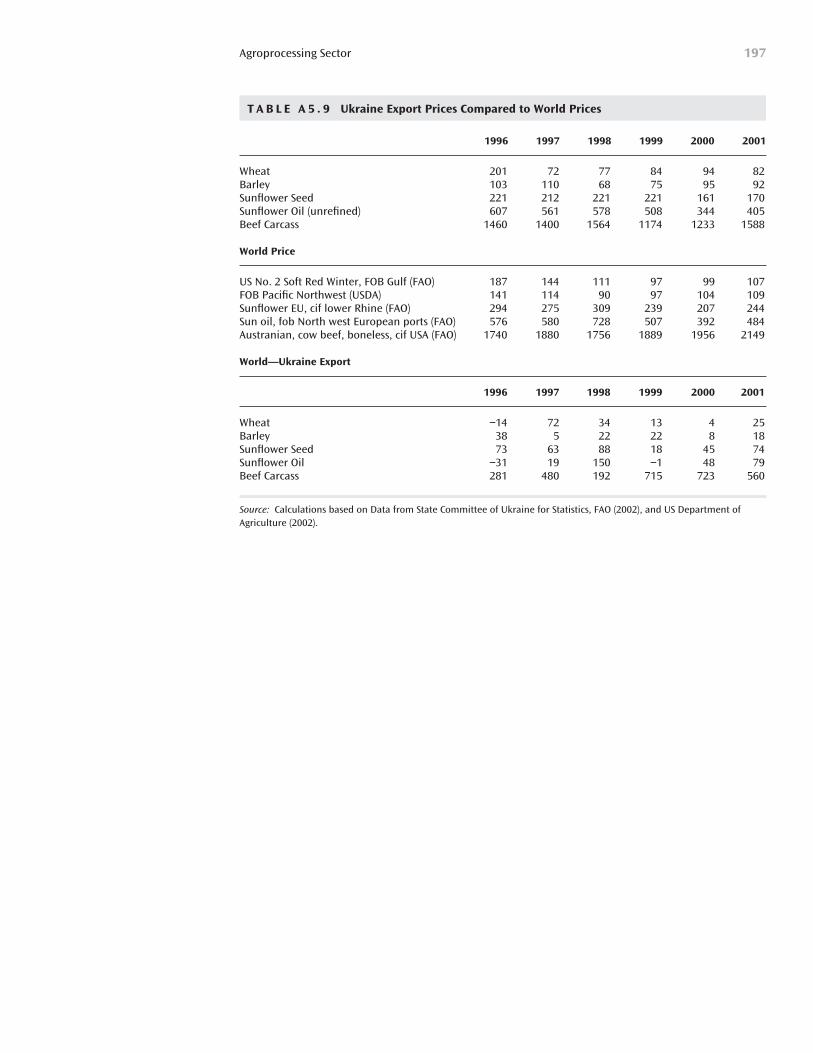

Table A5.9: Ukraine Export Prices Compared to World Prices 197

LIST OF BOXES

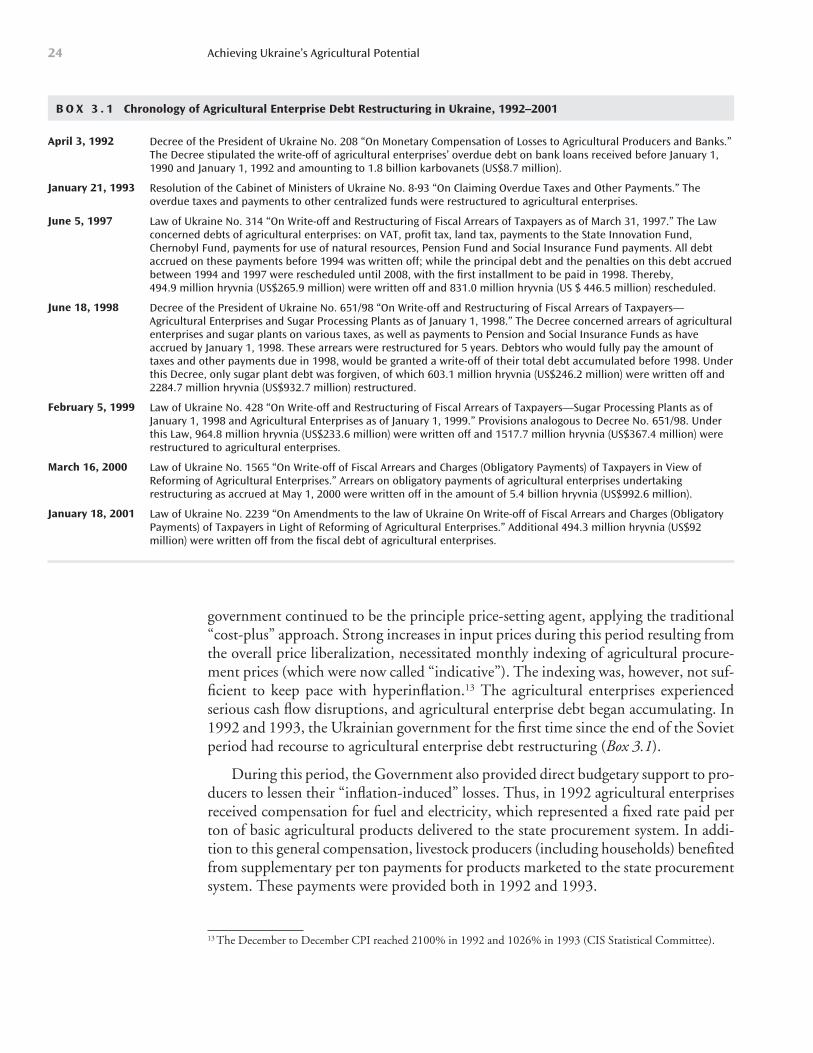

Box 3.1: Chronology of Agricultural Enterprise Debt Restructuring in Ukraine, 1992-2001 24

Box 3.2: Regional Resources of Agro-food Products: An Unclear Concept and Ambiguous Practices 26

Box 4.1: Ukraine's Progress in the Negotiation Process on Agriculture, November 2003 68

Contents ix

AMS Aggregate Measurement of Support

ARD Agency for Rural Development

BSE Bovine Spongiform Encephalitis

CAE Collective Agricultural Enterprises

CAM Common Agricultural Market (of the CIS)

CAP Common Agricultural Policy (of the European Union)

CEE Central and Eastern Europe

CEEC Central and Eastern European Countries

CEFTA Central Europe Free Trade Agreement

CIF Customs, Insurance and Freight

CIS Commonwealth of Independent States

CMO Common Market Organization

CN Combined Nomenclature

CSE Consumer Support Estimate

ECU European Currency Unit

EU European Union

FTA Free Trade Area

FDI Foreign Direct Investment

FMD Foot and Mouth Disease

GAO Gross Agricultural Output

GATT General Agreement on Tariffs and Trade

GDP Gross Domestic Product

GOU Government of Ukraine

GSP Generalized System of Preferences

xi

Acronyms and Abbreviations

GSSP General Services Support Estimate

GUAM Georgia, Ukraine, Azerbaijan, Moldova

GUUAM Georgia, Ukraine, Uzbekistan, Azerbaijan, Moldova

GVA Gross Value Added

HTU Higher Territorial Unit

IFI International Financial Institution

MFN Most Favored Nation

MPS Market Price Support

NBU National Bank of Ukraine

NIS Newly Independent States

OECD Organization for Economic Cooperation and Development

PCA Partnership and Cooperation Agreement (between Ukraine and the EU)

PSE Producer Support Estimate

SPS Sanitary and Phytosanitary (measures)

TBT Technical Barriers to Trade

TRQ Tariff Rate Quota

TSE Total Support Estimate

TRIPS Trade Related International Property Rights

UAH Hryvnia

UNDP United Nations Development Program

USAID United States Agency for International Development

USDA United States Department of Agriculture

VAT Value Added Tax

WTO World Trade Organization

Acronyms and Abbreviationsxii

This study provides a review of the food and agricultural sector in Ukraine. Itassesses the current status of the food and agricultural sector with special ref-erence to the agricultural policy regime and the form and level of government

support to the sector. The paper reviews the sector’s readiness to compete on openglobal markets for food and agricultural products. Given the importance and sensitiv-ity of the food and agriculture sector in the country, the report highlights a number ofcritical issues for the Ukrainian government to address. The report goes beyond the nar-rower focus of the agricultural policies and reviews the status of current rural physicaland social infrastructure and issues of rural poverty.

The Executive Summary highlights policy recommendations for Ukrainian policy-makers, while the individual chapters provide technical analysis on key policy issues.

xiii

Abstract

This study was prepared as a joint undertaking of the World Bank, the OECDand the Government of Ukraine. The study outlines a forward-looking policyagenda, assesses the development and current status of agricultural policies and

institutions and presents for the first time internationally comparable estimates of supportto the Ukrainian agricultural sector based on Producer and Consumer Support Estimates(PSE/CSE) developed by OECD. Going beyond the boundaries of the agricultural sec-tor, the report also encompasses the entire rural space surrounding agriculture, includingrural physical and social infrastructure and the extent of rural poverty.

The study was managed and compiled by Iain Shuker (World Bank, ECSSD), withthe support of Csaba Csaki (World Bank, ARD). At the OECD, Andrzej Kwiecinskiand Olga Melyukhina (Directorate for Food, Agriculture and Fisheries) prepared thesections concerned with the agricultural and trade policies and provided estimates ofthe level of support to the Ukrainian agricultural sector. The study is the result ofefforts by a large team of Ukrainian and international experts. On the Ukrainian side,Mykola Pugachov, Natalya Seperovich, Inna Chapko, and Iryna Kobuta from theUNDP Agricultural Policy for Human Development Project (funded by USAID), werethe major contributors, together with Sergey Sotnikov, a World Bank consultant, whoalso coordinated the work in Kyiv. From the Ministry of Agricultural Policy of Ukraine,Mykola Bezugly and Vitaly Drobot coordinated the activities under this study andprovided valuable inputs. Willi Meyers, a World Bank consultant, was responsible forthe agri-business section. Oleksandr Sikachin, Vitaliy Zhigadlo, and OleksandrYaroslavsky from the UNDP Agricultural Policy for Human Development Project, andFlorence Mauclert, a World Bank and OECD consultant also provided analytical sup-port, while Oleksandr Shevtsov and Volodymyr Artiushin coordinated the inputs of theUNDP Agricultural Policy for Human Development Project. Aleksander Kaliberda ofthe World Bank’s Kyiv office provided overall support to the project. Editorial assis-tance was provided by Alan Zuschlag and Sonali Wijayanandana (World Bank,ECSSD). The OECD contribution to the study was made possible through voluntarycontributions from Finland and Poland.

xv

Preface and Acknowledgments

Stimulating efficiency-driven agricultural output growth, developing more off-farm employment, and improving rural public services are the critical factors inthe recovery of the Ukrainian agricultural and rural economies. Ukraine’s agri-

cultural sector experienced one of the most severe and prolonged economic declines ofany economy in the Former Soviet Union or Eastern Europe. Fortunately, in recentyears, output in the sector has begun to stabilize. Building on the significant progressmade since 1999 in land reform, more stable trade policy, and a discontinuation ofhighly distortive commodity credit programs, the agricultural sector in Ukraine ispoised for a period of improved efficiency and growth. One of the consequences of thisefficiency-driven growth, however, will be a continued decline in formal farm employ-ment. Implementing strategies for absorbing surplus labor in rural areas and improvingthe quality of services for rural residents will be crucial to the economic and politicalsuccess of the agricultural reform program.

Stimulating agricultural growth and productivity. Efficiency driven growth in agri-cultural GDP is a priority for Ukraine. Agricultural GDP declined by 51% between1991 and 1999, recovered by 10 % per year in both 2000 and 2001, increased by 1.2%in 2002 and declined again by 18% in 2003. This economic decline has been one ofthe most severe and prolonged in Eastern Europe and the former Soviet Union. Someof this decline was the result of a collapse in the general economy, but this recession wasmade deeper and longer than in other transition economies by slow and inconsistentpolicy reforms for most of the 1990s. Post 1999, improvements in land reform and agri-cultural enterprise1 restructuring and discontinuation of the highly distortive state com-modity credit program have provided a base for making agriculture more efficient and

xvii

Executive Summary

1 The terminology used to describe different categories of farms will follow the standard Ukrainian legal definitionof farm categories. Household plots are parcels of land that are owned by private individuals and may not exceed 2 hectares. Independent private farms are owned by private individuals and are larger than 2 hectares. Agriculturalenterprises are farming enterprises (generally large farms) that are owned by legal entities such as cooperatives, part-nerships, collective farms, joint stock companies or are owned by private individuals. Individual owners may electto register their holdings as either agricultural enterprises or as independent private farms.

thus stimulating growth. Future reforms required to stimulate growth are outlined inmore detail below, but the key will be to avoid ad hoc government interference in agri-cultural markets, such as administrative limits on prices and profit margins and restric-tions on grain movement, and to avoid the sudden reversals in policy seen in the 1990sand more recently in 2003.

Provision of a good environment for job creation and improving public services. For-mal employment positions for rural residents declined by 30% between 1990 and 2000.As the agriculture sector becomes more efficient the number of such positions in the agri-cultural sector will decline even further. Most of the surplus labor has thus far been ab-sorbed into subsistence farming on individual land plots. However, with about 25% ofUkraine’s labor force based in rural areas, subsistence farming is not a sustainable long-term solution. Off-farm job creation and improved public services in rural areas are neededto prevent increased rural poverty and large-scale urban migration, together with their as-sociated social problems.

Simultaneous implementation of an agricultural growth strategy and a rural devel-opment strategy is important. The need for an agricultural growth strategy based onimproving the efficiency of the agriculture sector is clear. Without it the sector willcontinue to stagnate. However, it is important to mitigate the effects of reduced ruralemployment opportunities that will result from improved efficiency in the agriculturalsector through programs that develop off-farm employment and provide public servicesin rural areas. Without medium-term improvements in the quality of rural life, theagricultural reform program may loose credibility and political support.

Stimulating Agricultural Growth and ProductivityA stable macroeconomy and growing incomes will help the agricultural sector.Macroeconomic instability caused huge problems for the agriculture sector in the1990s, making the sequencing of agricultural reforms extremely difficult. Declining de-mand for agricultural products, a period of high inflation between 1991 and 1993, cur-rency appreciation between 1995 and 1998 followed by rapid depreciation in 1998, allmade agricultural economic reforms in the 1990s more difficult.

Fortunately, real incomes have begun to increase, and inflation and exchange rateshave stabilized, which improves the prospects for the agricultural sector. But, real in-terest rates on loan funds remain high due to political risk and structural inefficienciesin the banking and property rights systems. Lead times required for agricultural pro-duction and investments are longer term than in most other industries, making low realand nominal interest rates critical for its development.

Maintaining macroeconomic stability and improving the efficiency of the bankingand property rights systems should be the top priority for the policy makers concernedwith development of the agricultural sector.

Promote a stable and predictable, market oriented policy environment. Sharp agri-cultural policy reversals exacerbated the economic decline of the agricultural sector in

Executive Summaryxviii

1990s. Some of these ad hoc policy changes were an attempt to compensate for theabove mentioned macro policy distortions, but in many cases they were misguided at-tempts to prop up inefficient farms, input supply chains or agro-processors, or to main-tain parts of a centrally planned system in the context of a market economy. This createda high-risk investment climate in the agriculture sector. As a result farm managers, in-vestors, banks, input suppliers and traders avoided making new investments in the agri-cultural sector or charged high margins to compensate for the risk.

An example of a detrimental policy reversal was the introduction of the “state com-modity credit” program in 1996. This program resulted in restrictions on grain move-ments after some progress in market liberalization between 1994 and 1995, andreintroduced the direct government participation in commercial input supply and grainmarkets. This caused the private sector to significantly reduce the supply of inputs andcredit to the sector, resulting in further declines in grain production. Government in-terference in grain markets in 2003 has again added risk for input supply, credit andagricultural marketing companies, causing them to reduce supplies and charge highermargins, thus reducing the efficiency of the agricultural sector.

In order to increase investor confidence in the agricultural sector, the Ministry ofAgriculture should prepare a clearly articulated medium-term agricultural policy frame-work and then systematically implement this policy. Ad hoc reversals in policy, such asthe reintroduction of price and grain movement controls in the 2003 season, or in theperiod 1996 to 1999, should be avoided, as they create additional uncertainty in theagricultural sector and increase risk for producers, investors and lenders. The policyorientation should shift away from intervening in markets and instead support thedevelopment of market infrastructure and market institutions. If market interventionsare necessary, they should be rule based and transparent to all market participants. Sucha strategy would be the most efficient for the reduction of transactions costs and insta-bility on agricultural markets and ultimately, for a sustained agricultural growth.

Trade policy keeps improving, but there are some notable exceptions. Relative toother countries with similar agricultural capacity, Ukrainian agricultural exports are low.For example, in 2000 the ratio of food exports to Gross Agricultural Output for Ukrainewas 14%, compared to 25% for Poland and 53% for France and Germany. GivenUkraine’s agricultural resources, trade policy has critical importance for future agriculturalgrowth.

Ukraine has made significant progress in agricultural trade policy since the early1990s, moving exports from largely barter based bilateral agreements with countries ofthe NIS, to a more diversified set of export destinations based on private market trans-actions. Export quotas that were used in the early 1990s have largely been removed, butthe use of “indicative prices” and export taxes remains a restriction for a few selectedproducts, such as sunflower and live animals.

Imports of agricultural products, on the other hand, are still restricted by a largenumber of tariff and non-tariff barriers. Statutory tariffs increased sharply between 1997and 1999 followed by a period of stabilization in 2000 and 2001. The specific duties inad valorem terms for sunflower, sugar and poultry were all above 100% in 2001. Even

Executive Summary xix

wheat had an import tariff rate of 44%. Ukraine also applies a number of non-tariffbarriers, including quotas licenses and import bans which quite often lack transparencyand are expensive by international norms. The State Committee for Standardization ofUkraine imposes numerous (often unnecessary) technical standards and certificationrequirements on many imports. The Committee also fails to recognize foreign productcertificates even if issued in accordance with international standards.

Ukrainian accession to WTO is vitally important for agricultural trade. It willimprove the constancy, transparency, and predictability of trade relations and adherenceto multilateral rules and disciplines. This will provide a more stable framework fordomestic and foreign agents, thus reducing risk and encouraging investment. Transportcosts would also be reduced due to the guaranteed freedom of transit through theterritory of WTO member states. It will also mean that, with binding tariffs for almostall agricultural products fixed at no more than 20%, there will be a substantial drop inborder protection. However, as demonstrated in more detail in the paper, this is expectedto have very little downward pressure on domestic prices for crops where Ukraine is a netexporter. It will reduce domestic price fluctuations for agricultural products that switchbetween net export and net import positions. Commodities where Ukraine is a netimporter and does not have a cost advantage in production, such as sugar, could experi-ence downward pressure on prices. In order for Ukraine to gain the full advantage ofWTO accession, it is important that Ukraine establish a sound scientific, consistent, andtransparent approach to determining pest and disease risks associated with agro-foodtrade, both to be able to participate effectively in Sanitary and Phytosanitary measures incooperation with other countries, but also to apply appropriate, least trade restrictivemeasures to manage that risk for crop and animal imports. This is a difficult andexpensive undertaking and will require the adoption of international standards and thecommitment of public funds to regulation and testing facilities.

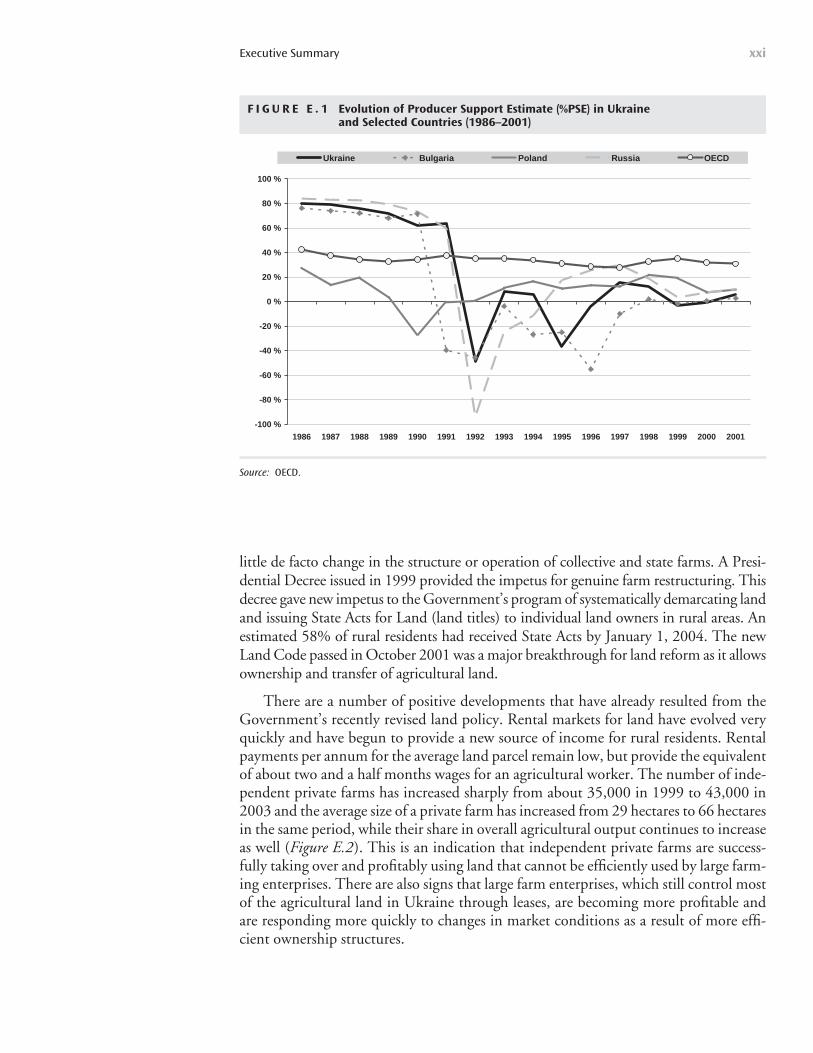

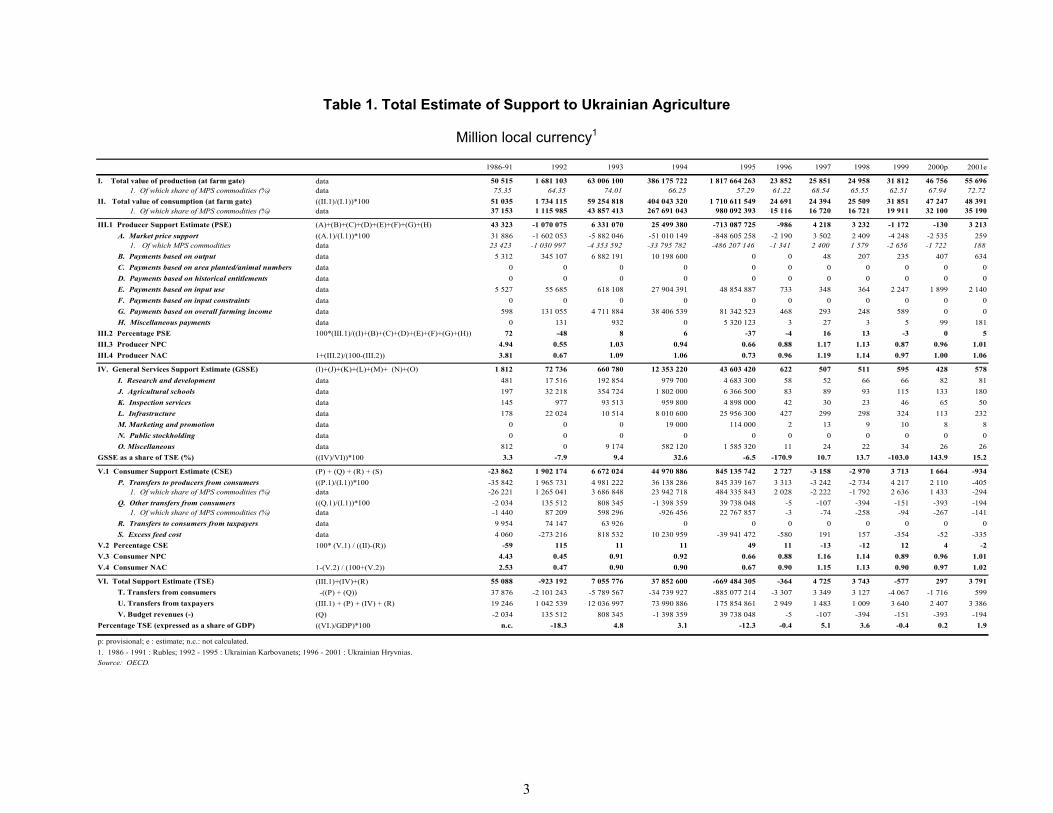

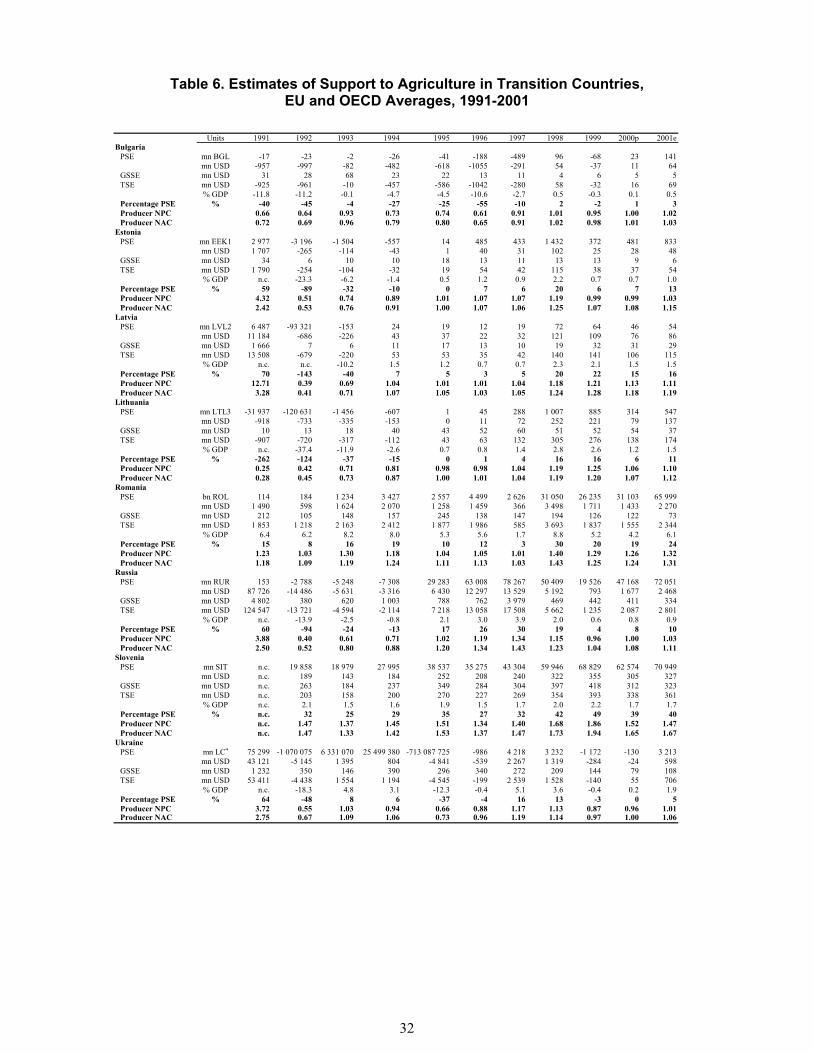

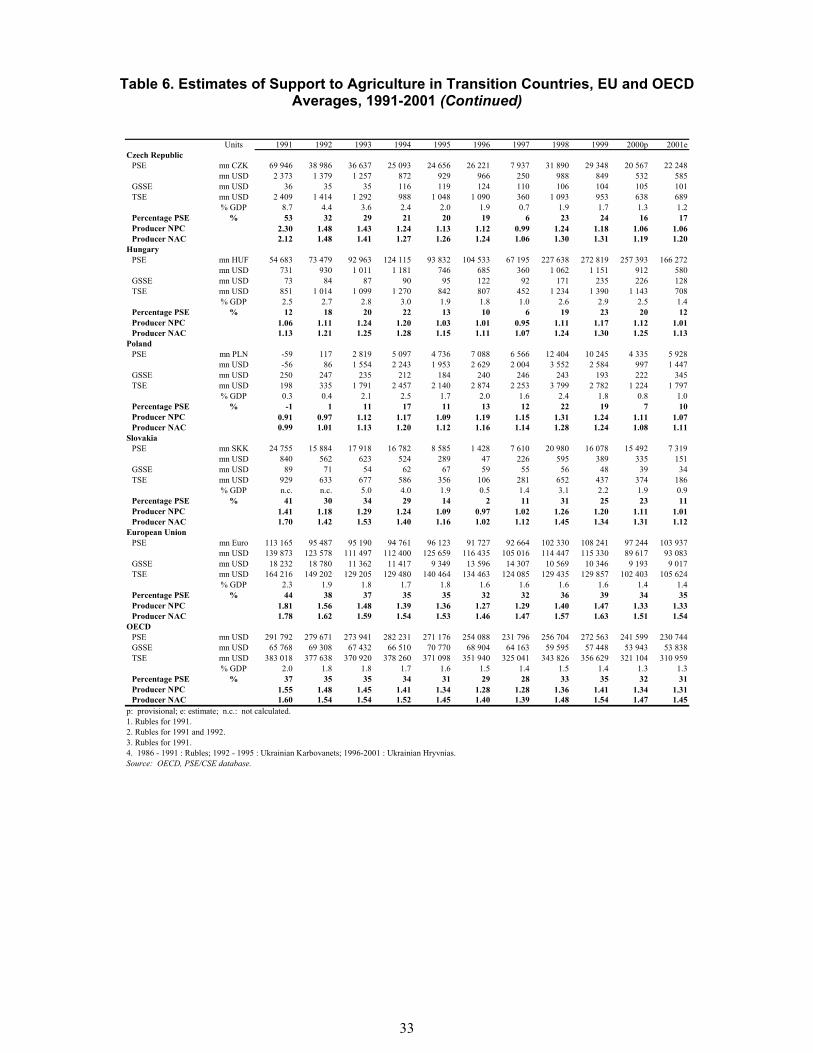

Aggregate support to Ukrainian agriculture has stabilized at moderate levels, how-ever, distortions in individual commodity sectors are significant. Producer SupportEstimate (PSE) was very high prior to the start of market reforms in 1992, followed by aperiod of strong producer taxation. By the late 1990s the support had recovered and sta-bilized at a relatively low level, meaning a significant reduction in overall policy distor-tions in the course of the transition. The PSE of 5% is currently one of the lowest amongthe transition countries analyzed (Figure E.1).

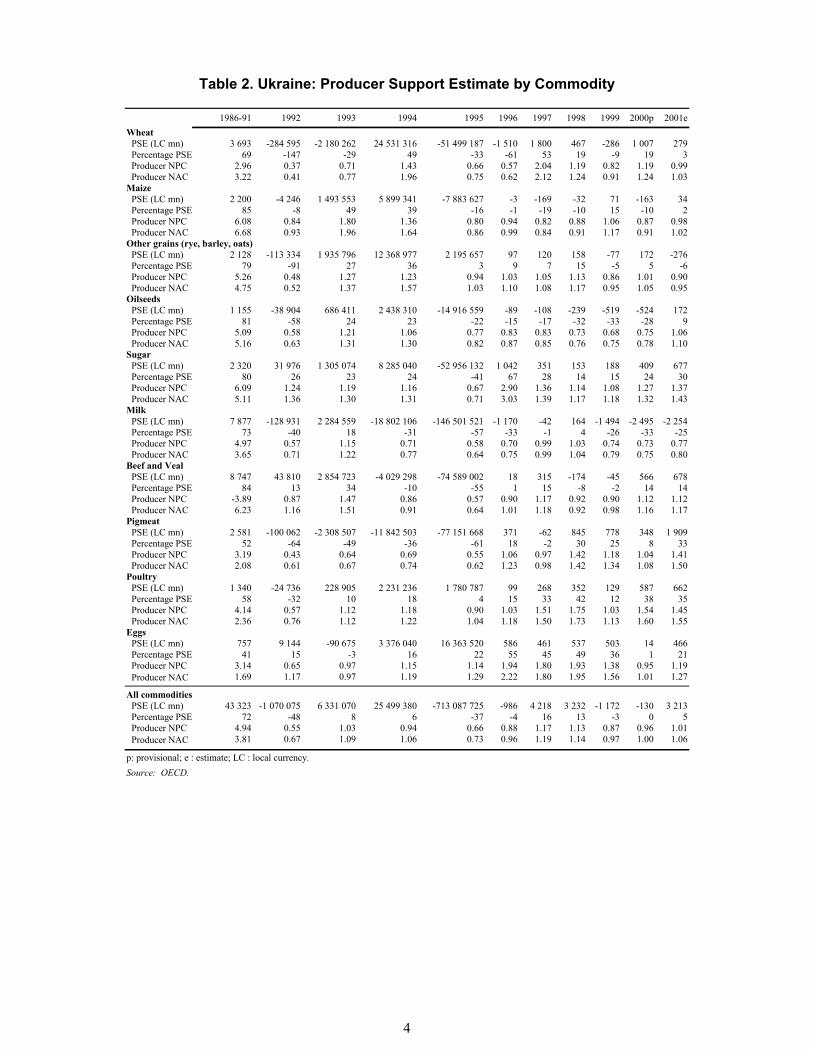

The aggregate low level of producer support, however, disguises the strong varia-tions across commodities, with relatively high support for poultry (35%), pigmeat(33%), eggs (21%) and sugar (30%), and a strong taxation of milk (-25%). This islargely the result of persistent price distortions in these sectors arising from Governmentpolicies, but also infrastructural and institutional weaknesses of Ukrainian agriculturalmarkets. The Government will need to adopt policies reducing market price distortions,particularly in these specific sectors.

The land reform and farm restructuring program is gaining momentum. The landreform program began in March 1991 but made very slow progress until 1999. Duringthis period land was transferred from state to collective ownership, which resulted in very

Executive Summaryxx

little de facto change in the structure or operation of collective and state farms. A Presi-dential Decree issued in 1999 provided the impetus for genuine farm restructuring. Thisdecree gave new impetus to the Government’s program of systematically demarcating landand issuing State Acts for Land (land titles) to individual land owners in rural areas. Anestimated 58% of rural residents had received State Acts by January 1, 2004. The newLand Code passed in October 2001 was a major breakthrough for land reform as it allowsownership and transfer of agricultural land.

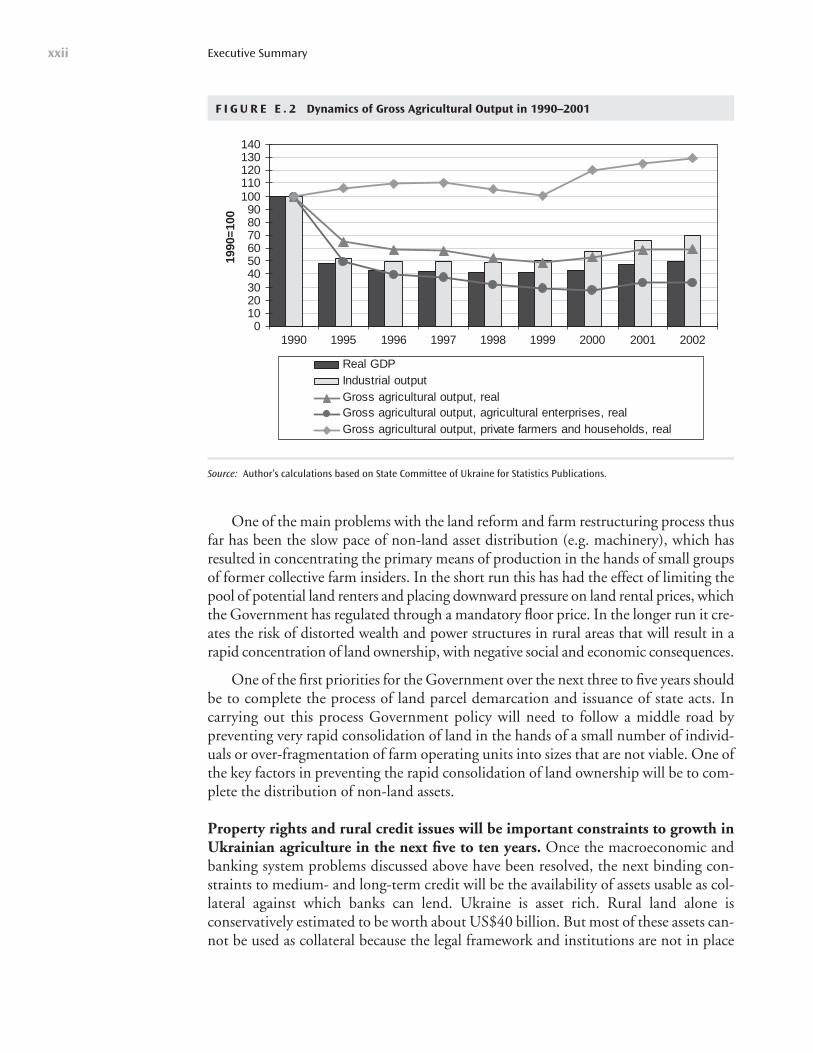

There are a number of positive developments that have already resulted from theGovernment’s recently revised land policy. Rental markets for land have evolved veryquickly and have begun to provide a new source of income for rural residents. Rentalpayments per annum for the average land parcel remain low, but provide the equivalentof about two and a half months wages for an agricultural worker. The number of inde-pendent private farms has increased sharply from about 35,000 in 1999 to 43,000 in2003 and the average size of a private farm has increased from 29 hectares to 66 hectaresin the same period, while their share in overall agricultural output continues to increaseas well (Figure E.2). This is an indication that independent private farms are success-fully taking over and profitably using land that cannot be efficiently used by large farm-ing enterprises. There are also signs that large farm enterprises, which still control mostof the agricultural land in Ukraine through leases, are becoming more profitable andare responding more quickly to changes in market conditions as a result of more effi-cient ownership structures.

Executive Summary xxi

F I G U R E E . 1 Evolution of Producer Support Estimate (%PSE) in Ukraine and Selected Countries (1986–2001)

-100 %

-80 %

-60 %

-40 %

-20 %

0 %

20 %

40 %

60 %

80 %

100 %

1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Ukraine Bulgaria Poland Russia OECD

Source: OECD.

One of the main problems with the land reform and farm restructuring process thusfar has been the slow pace of non-land asset distribution (e.g. machinery), which hasresulted in concentrating the primary means of production in the hands of small groupsof former collective farm insiders. In the short run this has had the effect of limiting thepool of potential land renters and placing downward pressure on land rental prices, whichthe Government has regulated through a mandatory floor price. In the longer run it cre-ates the risk of distorted wealth and power structures in rural areas that will result in arapid concentration of land ownership, with negative social and economic consequences.

One of the first priorities for the Government over the next three to five years shouldbe to complete the process of land parcel demarcation and issuance of state acts. Incarrying out this process Government policy will need to follow a middle road bypreventing very rapid consolidation of land in the hands of a small number of individ-uals or over-fragmentation of farm operating units into sizes that are not viable. One ofthe key factors in preventing the rapid consolidation of land ownership will be to com-plete the distribution of non-land assets.

Property rights and rural credit issues will be important constraints to growth inUkrainian agriculture in the next five to ten years. Once the macroeconomic andbanking system problems discussed above have been resolved, the next binding con-straints to medium- and long-term credit will be the availability of assets usable as col-lateral against which banks can lend. Ukraine is asset rich. Rural land alone isconservatively estimated to be worth about US$40 billion. But most of these assets can-not be used as collateral because the legal framework and institutions are not in place

Executive Summaryxxii

F I G U R E E . 2 Dynamics of Gross Agricultural Output in 1990–2001

0102030405060708090

100110120130140

1990 1995 1996 1997 1998 1999 2000 2001 2002

1990

=10

0

Real GDPIndustrial outputGross agricultural output, realGross agricultural output, agricultural enterprises, realGross agricultural output, private farmers and households, real

Source: Author’s calculations based on State Committee of Ukraine for Statistics Publications.

to support their use in this regard. These assets are considered to be “dead” for creditpurposes. The key to making these assets available as collateral is to develop the legaland regulatory framework for property rights.

The Government and Parliament are currently working on legislation on securedtransactions, a movable property rights registry, a cadastre and title registry, mortgage law,and improved banking laws. There is a rudimentary registry for movable assets whichneeds to be further developed to be efficient. The development of a unified property reg-istry system, to be financed by international donors and International Financial Institu-tions (IFIs), is planned for the next two years, and when installed, will provide a guaranteeof ownership rights and record mortgages and other liens on properties. These laws andinstitutions will make the use of collateral possible. A functioning property rights systemis a precondition for increased medium- and long-term credit to agriculture. The soonerthese laws and institutions are in place, the sooner efficient medium- and long-term creditmarkets will begin to develop.

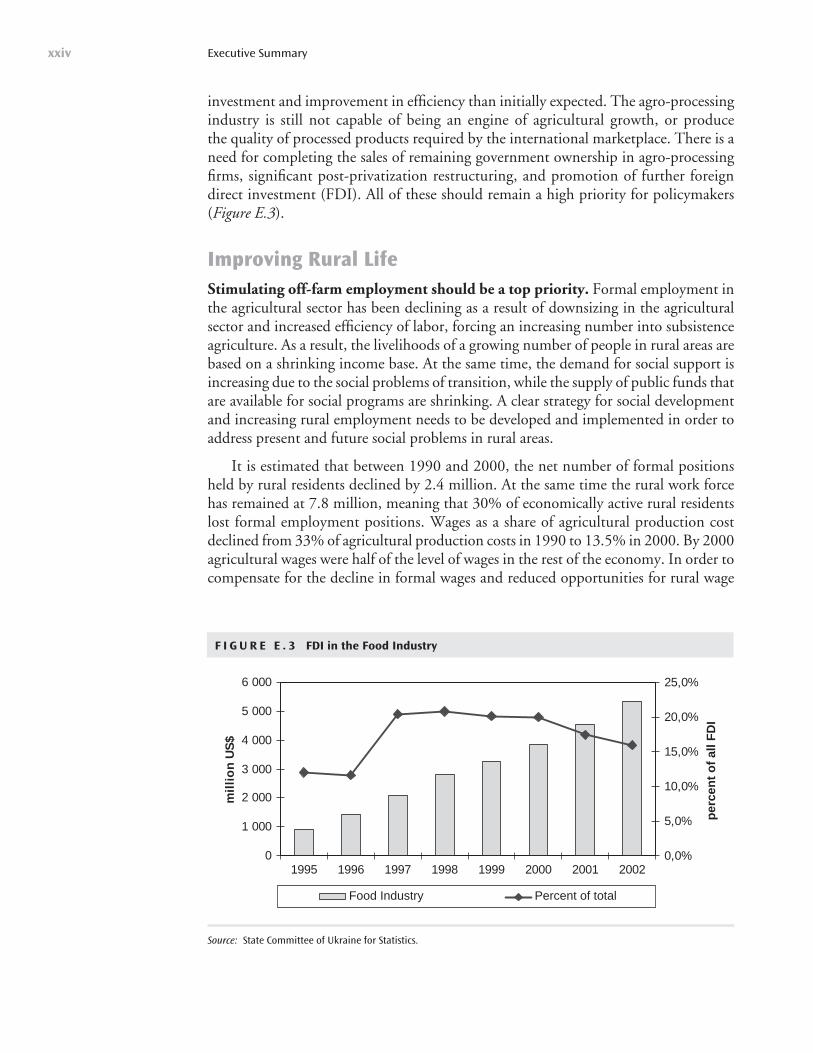

Agroprocessing privatization is increasing the efficiency of processing and mar-keting. An agro-processing industry which is capable of producing internationally com-petitive food products is an essential pre-condition for utilizing Ukraine’s significantagricultural potential. The privatization of Ukraine’s agro-processing sector is alreadyquite advanced. This has begun to show positive results in some industries by increasingefficiency and reducing margins. With real output and real gross value added (GVA) inthe food industry growing from 25% and 40% between 1996 to 2001 (4.4% to 7.0% perannum), respectively, and employment in the sector declining by 10% (2.3% per annum),the output and GVA per worker increased by 40% and 57%, respectively. This increasein GVA per worker in the food sector was significantly larger than for the economy as awhole, or for the manufacturing sector as a whole.

In the commodity marketing sector, margins for farm-to-export markets for five ofthe top six export products have declined over time. One of the factors that seems to havecontributed to the improvement of efficiency in the farm to export marketing is the entryof private intermediaries who can better manage and coordinate the flow of goods. A rea-sonable explanation for the observed improvements is that as more of the storage, han-dling, and processing facilities for grains and oilseeds have been privatized, the newownership, including foreign investors, has been able to improve the efficiency of thesemarketing channels. However, it is clear that there remains substantial potential for fur-ther reduction of transactions costs, especially with regard to numerous tariffs for trans-port, inspection, and certification that remain under Government control. A recentstudy of the sunflower sector found that administrative charges and fees levied by theGovernment at various stages of rail transport are actually higher than the basic rail trans-port tariffs and clearly reduce competitiveness of Ukrainian products. The volatility ofthese margins and the significant differences between such similar commodities as wheatand barley characterize a marketing system that is still maturing and is still subject to pol-icy instability and lack of stable marketing channels and institutions.

Despite all the progress made in the agribusiness sector, many of the new ownersdo not have the financial resources for technological improvements and have made less

Executive Summary xxiii

investment and improvement in efficiency than initially expected. The agro-processingindustry is still not capable of being an engine of agricultural growth, or produce the quality of processed products required by the international marketplace. There is aneed for completing the sales of remaining government ownership in agro-processingfirms, significant post-privatization restructuring, and promotion of further foreigndirect investment (FDI). All of these should remain a high priority for policymakers (Figure E.3).

Improving Rural LifeStimulating off-farm employment should be a top priority. Formal employment inthe agricultural sector has been declining as a result of downsizing in the agriculturalsector and increased efficiency of labor, forcing an increasing number into subsistenceagriculture. As a result, the livelihoods of a growing number of people in rural areas arebased on a shrinking income base. At the same time, the demand for social support isincreasing due to the social problems of transition, while the supply of public funds thatare available for social programs are shrinking. A clear strategy for social developmentand increasing rural employment needs to be developed and implemented in order toaddress present and future social problems in rural areas.

It is estimated that between 1990 and 2000, the net number of formal positionsheld by rural residents declined by 2.4 million. At the same time the rural work forcehas remained at 7.8 million, meaning that 30% of economically active rural residentslost formal employment positions. Wages as a share of agricultural production costdeclined from 33% of agricultural production costs in 1990 to 13.5% in 2000. By 2000agricultural wages were half of the level of wages in the rest of the economy. In order tocompensate for the decline in formal wages and reduced opportunities for rural wage

Executive Summaryxxiv

F I G U R E E . 3 FDI in the Food Industry

0

1 000

2 000

3 000

4 000

5 000

6 000

1995 1996 1997 1998 1999 2000 2001 2002

mil

lio

n U

S$

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

per

cen

t o

f al

l FD

I

Food Industry Percent of total

Source: State Committee of Ukraine for Statistics.

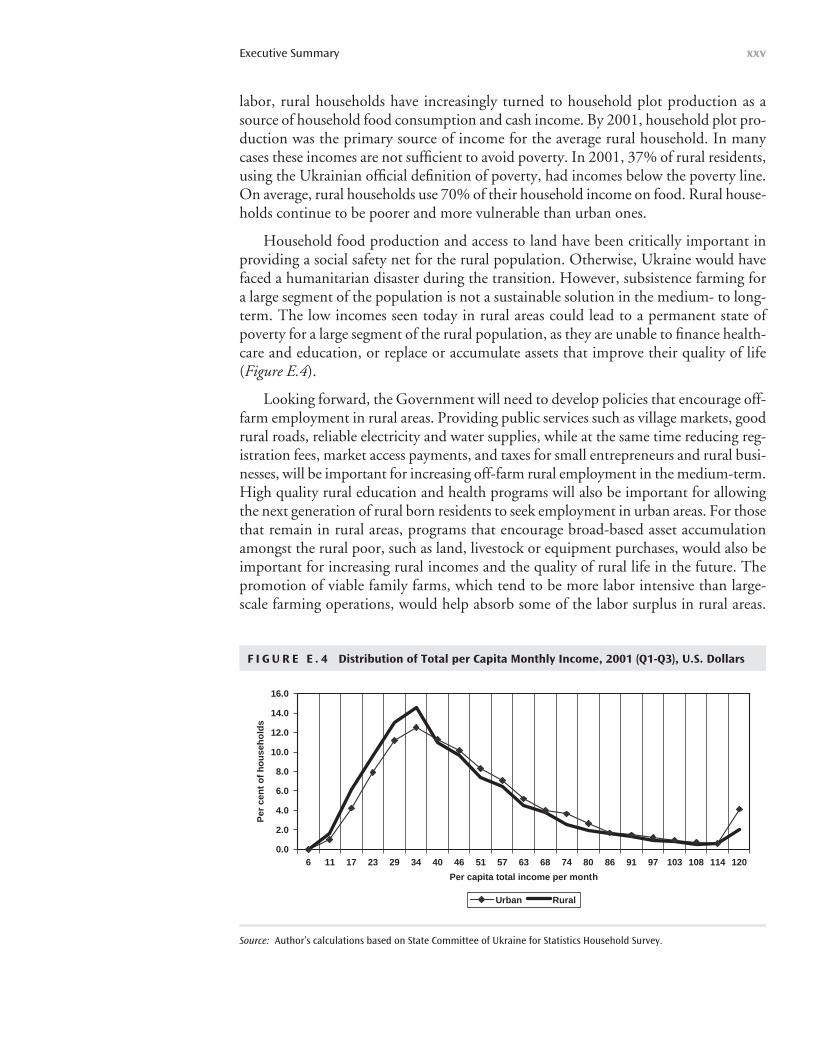

labor, rural households have increasingly turned to household plot production as asource of household food consumption and cash income. By 2001, household plot pro-duction was the primary source of income for the average rural household. In manycases these incomes are not sufficient to avoid poverty. In 2001, 37% of rural residents,using the Ukrainian official definition of poverty, had incomes below the poverty line.On average, rural households use 70% of their household income on food. Rural house-holds continue to be poorer and more vulnerable than urban ones.

Household food production and access to land have been critically important inproviding a social safety net for the rural population. Otherwise, Ukraine would havefaced a humanitarian disaster during the transition. However, subsistence farming fora large segment of the population is not a sustainable solution in the medium- to long-term. The low incomes seen today in rural areas could lead to a permanent state ofpoverty for a large segment of the rural population, as they are unable to finance health-care and education, or replace or accumulate assets that improve their quality of life(Figure E.4).

Looking forward, the Government will need to develop policies that encourage off-farm employment in rural areas. Providing public services such as village markets, goodrural roads, reliable electricity and water supplies, while at the same time reducing reg-istration fees, market access payments, and taxes for small entrepreneurs and rural busi-nesses, will be important for increasing off-farm rural employment in the medium-term.High quality rural education and health programs will also be important for allowingthe next generation of rural born residents to seek employment in urban areas. For thosethat remain in rural areas, programs that encourage broad-based asset accumulationamongst the rural poor, such as land, livestock or equipment purchases, would also beimportant for increasing rural incomes and the quality of rural life in the future. Thepromotion of viable family farms, which tend to be more labor intensive than large-scale farming operations, would help absorb some of the labor surplus in rural areas.

Executive Summary xxv

F I G U R E E . 4 Distribution of Total per Capita Monthly Income, 2001 (Q1-Q3), U.S. Dollars

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

6 11 17 23 29 34 40 46 51 57 63 68 74 80 86 91 97 103 108 114 120

Per capita total income per month

Per

cen

t o

f h

ou

seh

old

s

Urban Rural

Source: Author’s calculations based on State Committee of Ukraine for Statistics Household Survey.

Smaller farms also make more use of local services such as repair shops, input supplyservices, and marketing services.

The Government has a well conceived program to transfer social assets from for-mer collective farms to local administrations, but has no clear strategy for manag-ing or financing these services from the budget. By January 2002, which is six yearsfrom the start of the program to transfer assets, 48% of kindergartens, 50% of housing,54% of clubs, 58% of utility networks, and 64% of medical institutions, and 67% ofschools had been formally transferred to local administrations. Many of these facilitiesare under-funded, run down, or abandoned and those that continue to operate are stillbeing supported by farm enterprises because the state budgets for these activities are in-adequate. For example, in 2001, the State Budget earmarked only 55.2 million hryvniafor the maintenance of social assets in rural areas, which is far short of the funding lev-els required.

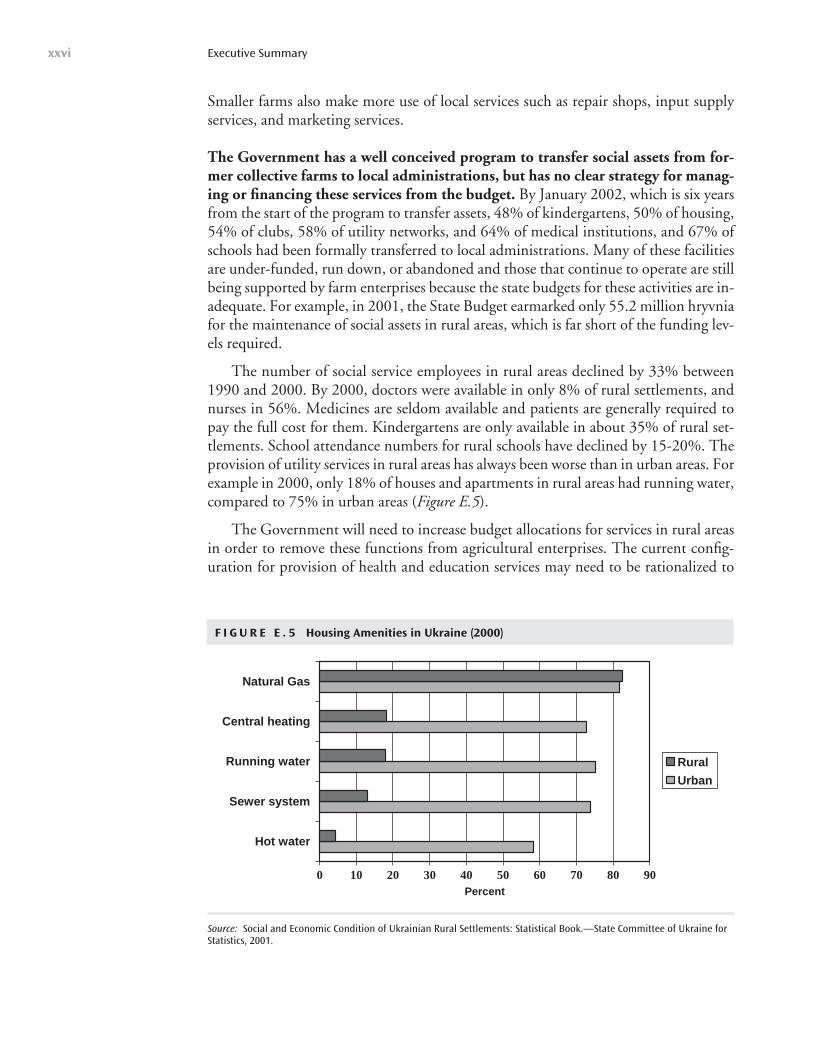

The number of social service employees in rural areas declined by 33% between1990 and 2000. By 2000, doctors were available in only 8% of rural settlements, andnurses in 56%. Medicines are seldom available and patients are generally required topay the full cost for them. Kindergartens are only available in about 35% of rural set-tlements. School attendance numbers for rural schools have declined by 15-20%. Theprovision of utility services in rural areas has always been worse than in urban areas. Forexample in 2000, only 18% of houses and apartments in rural areas had running water,compared to 75% in urban areas (Figure E.5).

The Government will need to increase budget allocations for services in rural areasin order to remove these functions from agricultural enterprises. The current config-uration for provision of health and education services may need to be rationalized to

Executive Summaryxxvi

F I G U R E E . 5 Housing Amenities in Ukraine (2000)

0 10 20 30 40 50 60 70 80 90

Hot water

Sewer system

Running water

Central heating

Natural Gas

Percent

Rural

Urban

Source: Social and Economic Condition of Ukrainian Rural Settlements: Statistical Book.—State Committee of Ukraine forStatistics, 2001.

provide these services more effectively. To achieve this, a comprehensive strategy forproviding health care and education services in rural areas will be needed, keeping inmind that the rural population is likely to decline significantly over time. This may re-quire further concentration of medical facilities, and fewer higher quality schools. Forthose services for which there could be cost recovery, such as gas supply, water supply,and other utilities, a combination of block grants and increased tax revenues will allowvillage administrations to better develop and manage these utility services. Other ser-vices that were provided by agricultural enterprises, such as shops, barbers and repairfacilities could be transferred to the private sector, and many of these functions prob-ably already have been transferred. The key role for government and local administra-tions in ensuring that these services are provided is to ensure a business environmentthat makes it possible for them operate cost effectively.

Executive Summary xxvii

Ukraine is endowed with rich natural resources (soil, climate, and water) that arehighly suitable for agricultural use. The country has over 40 million hectaresof agricultural land, of which about 80% (or 33 million hectares) is arable, and

of this amount, more than 50% consists of deep black chernozem soils. For that reasonalone, agriculture has the potential to become an important “driving force” for the Ukrain-ian economy. However, the agricultural sector2 went into a steep decline in the 1990s.The situation showed signs of changing in 2000 when, after ten years of disappointingperformance, the Ukrainian agricultural sector output grew by 10% per year for two yearsin a row, then maintained these output levels in 2002 by growing 1.2%. Adverse weatherconditions in 2003 resulted in a decline in agricultural GDP by an 18% (estimated).

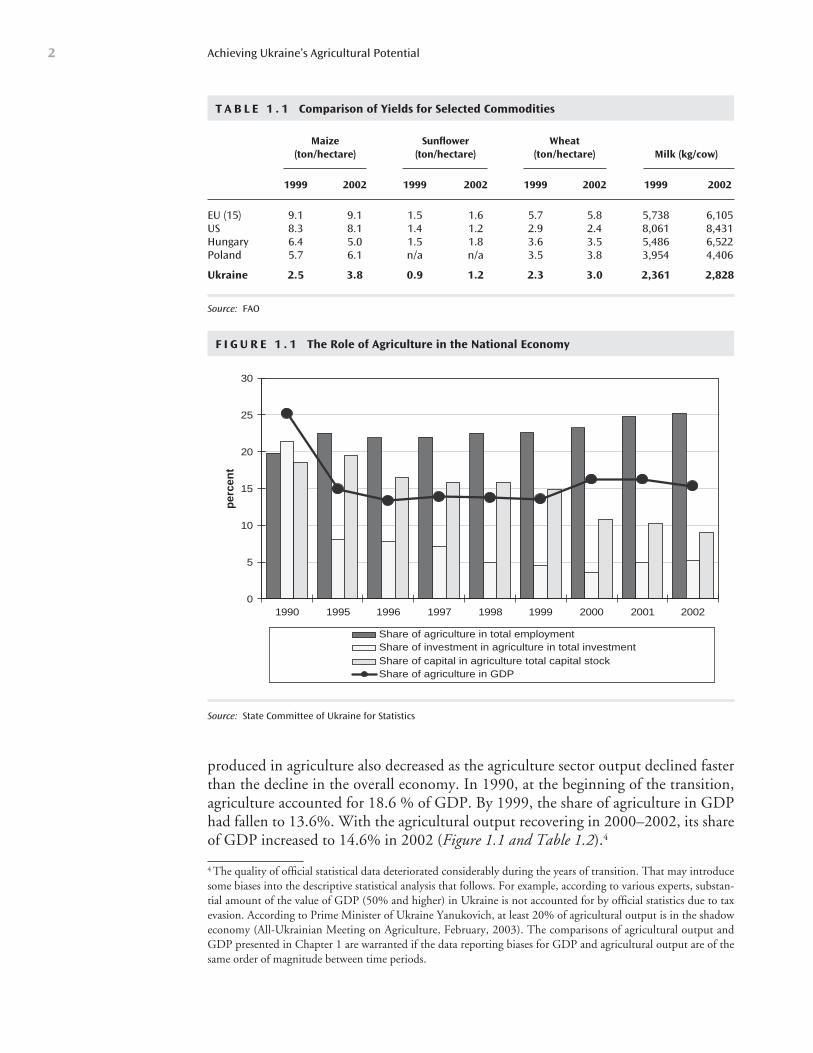

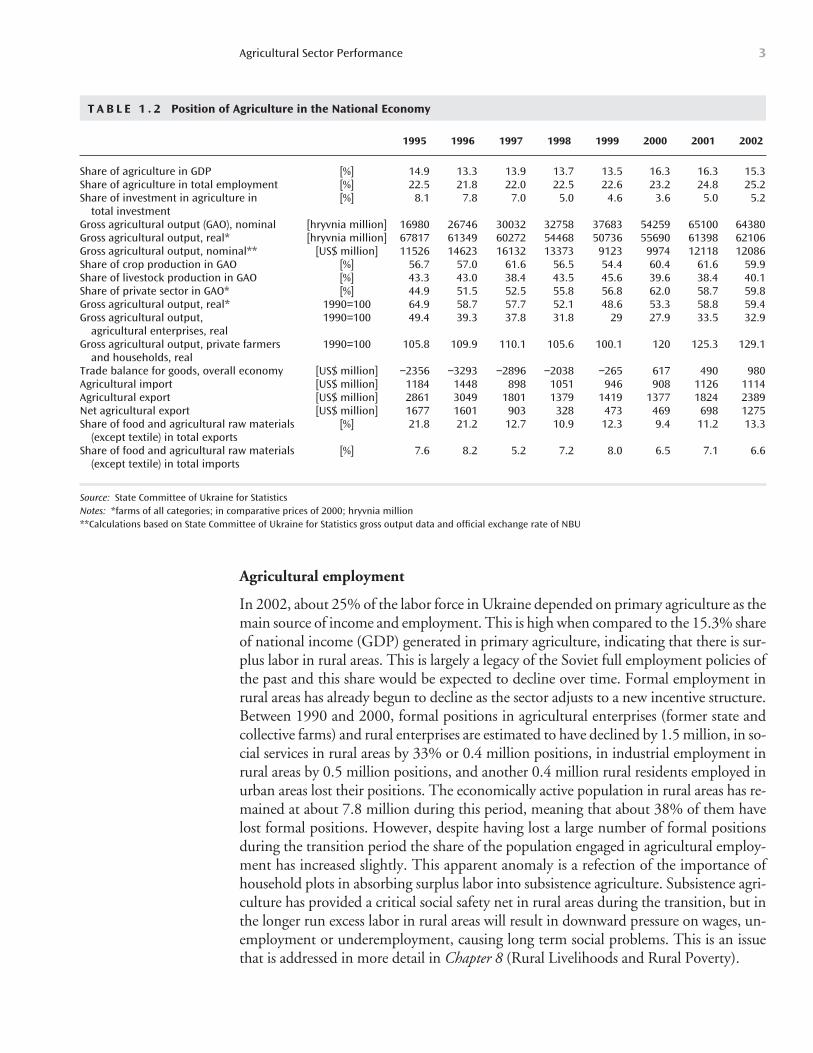

Role of Agriculture in the National EconomyAgriculture is an important sector of the Ukrainian economy. It makes up a significant pro-portion of GDP, is a major employer and has the potential to be a significant export earner.During the transition, it has also served an important role as a social safety net by absorb-ing surplus labor into subsistence farming, and preventing a major social upheaval by slow-ing the pace of urban-rural migration seen in similar economic collapses. On the whole,however, Ukraine’s agricultural potential is significantly underutilized (Table 1.1).

Agricultural output

The economic transition process has been difficult for the sector. Between 1990 and1999, output of the primary agricultural sector3 in Ukraine declined by 51% beforerecovering slightly in 2000–2002. The share of the Gross Domestic Product (GDP)

1

Agricultural Sector Performance

2 The agricultural sector is defined as primary agriculture, i.e., it does not include agribusiness.3 Gross agricultural output and agricultural contribution to GDP are different concepts. Gross agricultural outputis a value of all commodities produced in agriculture, i.e., it includes the value of commodities, such as feedstuffs,that are produced and consumed in agriculture. Hence, calculation of gross agricultural output involves doublecounting of some commodities. Agricultural GDP gives a measure of net contribution of agriculture to nationaleconomy.

C H A P T E R 1

produced in agriculture also decreased as the agriculture sector output declined fasterthan the decline in the overall economy. In 1990, at the beginning of the transition,agriculture accounted for 18.6 % of GDP. By 1999, the share of agriculture in GDPhad fallen to 13.6%. With the agricultural output recovering in 2000–2002, its shareof GDP increased to 14.6% in 2002 (Figure 1.1 and Table 1.2).4

Achieving Ukraine’s Agricultural Potential2

T A B L E 1 . 1 Comparison of Yields for Selected Commodities

Maize Sunflower Wheat(ton/hectare) (ton/hectare) (ton/hectare) Milk (kg/cow)

1999 2002 1999 2002 1999 2002 1999 2002

EU (15) 9.1 9.1 1.5 1.6 5.7 5.8 5,738 6,105US 8.3 8.1 1.4 1.2 2.9 2.4 8,061 8,431Hungary 6.4 5.0 1.5 1.8 3.6 3.5 5,486 6,522Poland 5.7 6.1 n/a n/a 3.5 3.8 3,954 4,406

Ukraine 2.5 3.8 0.9 1.2 2.3 3.0 2,361 2,828

Source: FAO

F I G U R E 1 . 1 The Role of Agriculture in the National Economy

0

5

10

15

20

25

30

1990 1995 1996 1997 1998 1999 2000 2001 2002

per

cen

t

Share of agriculture in total employmentShare of investment in agriculture in total investmentShare of capital in agriculture total capital stockShare of agriculture in GDP

Source: State Committee of Ukraine for Statistics

4 The quality of official statistical data deteriorated considerably during the years of transition. That may introducesome biases into the descriptive statistical analysis that follows. For example, according to various experts, substan-tial amount of the value of GDP (50% and higher) in Ukraine is not accounted for by official statistics due to taxevasion. According to Prime Minister of Ukraine Yanukovich, at least 20% of agricultural output is in the shadoweconomy (All-Ukrainian Meeting on Agriculture, February, 2003). The comparisons of agricultural output andGDP presented in Chapter 1 are warranted if the data reporting biases for GDP and agricultural output are of thesame order of magnitude between time periods.

Agricultural Sector Performance 3

T A B L E 1 . 2 Position of Agriculture in the National Economy

1995 1996 1997 1998 1999 2000 2001 2002

Share of agriculture in GDP [%] 14.9 13.3 13.9 13.7 13.5 16.3 16.3 15.3Share of agriculture in total employment [%] 22.5 21.8 22.0 22.5 22.6 23.2 24.8 25.2Share of investment in agriculture in [%] 8.1 7.8 7.0 5.0 4.6 3.6 5.0 5.2

total investmentGross agricultural output (GAO), nominal [hryvnia million] 16980 26746 30032 32758 37683 54259 65100 64380Gross agricultural output, real* [hryvnia million] 67817 61349 60272 54468 50736 55690 61398 62106Gross agricultural output, nominal** [US$ million] 11526 14623 16132 13373 9123 9974 12118 12086Share of crop production in GAO [%] 56.7 57.0 61.6 56.5 54.4 60.4 61.6 59.9Share of livestock production in GAO [%] 43.3 43.0 38.4 43.5 45.6 39.6 38.4 40.1Share of private sector in GAO* [%] 44.9 51.5 52.5 55.8 56.8 62.0 58.7 59.8Gross agricultural output, real* 1990=100 64.9 58.7 57.7 52.1 48.6 53.3 58.8 59.4Gross agricultural output, 1990=100 49.4 39.3 37.8 31.8 29 27.9 33.5 32.9

agricultural enterprises, realGross agricultural output, private farmers 1990=100 105.8 109.9 110.1 105.6 100.1 120 125.3 129.1

and households, realTrade balance for goods, overall economy [US$ million] −2356 −3293 −2896 −2038 −265 617 490 980Agricultural import [US$ million] 1184 1448 898 1051 946 908 1126 1114Agricultural export [US$ million] 2861 3049 1801 1379 1419 1377 1824 2389Net agricultural export [US$ million] 1677 1601 903 328 473 469 698 1275Share of food and agricultural raw materials [%] 21.8 21.2 12.7 10.9 12.3 9.4 11.2 13.3

(except textile) in total exportsShare of food and agricultural raw materials [%] 7.6 8.2 5.2 7.2 8.0 6.5 7.1 6.6

(except textile) in total imports

Source: State Committee of Ukraine for StatisticsNotes: *farms of all categories; in comparative prices of 2000; hryvnia million**Calculations based on State Committee of Ukraine for Statistics gross output data and official exchange rate of NBU

Agricultural employment

In 2002, about 25% of the labor force in Ukraine depended on primary agriculture as themain source of income and employment. This is high when compared to the 15.3% shareof national income (GDP) generated in primary agriculture, indicating that there is sur-plus labor in rural areas. This is largely a legacy of the Soviet full employment policies ofthe past and this share would be expected to decline over time. Formal employment inrural areas has already begun to decline as the sector adjusts to a new incentive structure.Between 1990 and 2000, formal positions in agricultural enterprises (former state andcollective farms) and rural enterprises are estimated to have declined by 1.5 million, in so-cial services in rural areas by 33% or 0.4 million positions, in industrial employment inrural areas by 0.5 million positions, and another 0.4 million rural residents employed inurban areas lost their positions. The economically active population in rural areas has re-mained at about 7.8 million during this period, meaning that about 38% of them havelost formal positions. However, despite having lost a large number of formal positionsduring the transition period the share of the population engaged in agricultural employ-ment has increased slightly. This apparent anomaly is a refection of the importance ofhousehold plots in absorbing surplus labor into subsistence agriculture. Subsistence agri-culture has provided a critical social safety net in rural areas during the transition, but inthe longer run excess labor in rural areas will result in downward pressure on wages, un-employment or underemployment, causing long term social problems. This is an issuethat is addressed in more detail in Chapter 8 (Rural Livelihoods and Rural Poverty).

Agricultural trade

During the 1990s, the importance of agricultural sector as an export revenue earner forUkraine declined in both absolute and relative terms. The share of agriculture in totalexports is considerably lower than other countries with similar agricultural export po-tential (Table 1.3). Relative to other countries with similar agricultural capacity, agri-cultural exports are low. For example, in 2000 the ratio of food exports to GrossAgricultural Output for Ukraine was 14% compared to 25% for Poland and 53% forFrance and Germany. Given Ukraine’s agricultural resources, trade policy has criticalimportance for future agricultural growth.

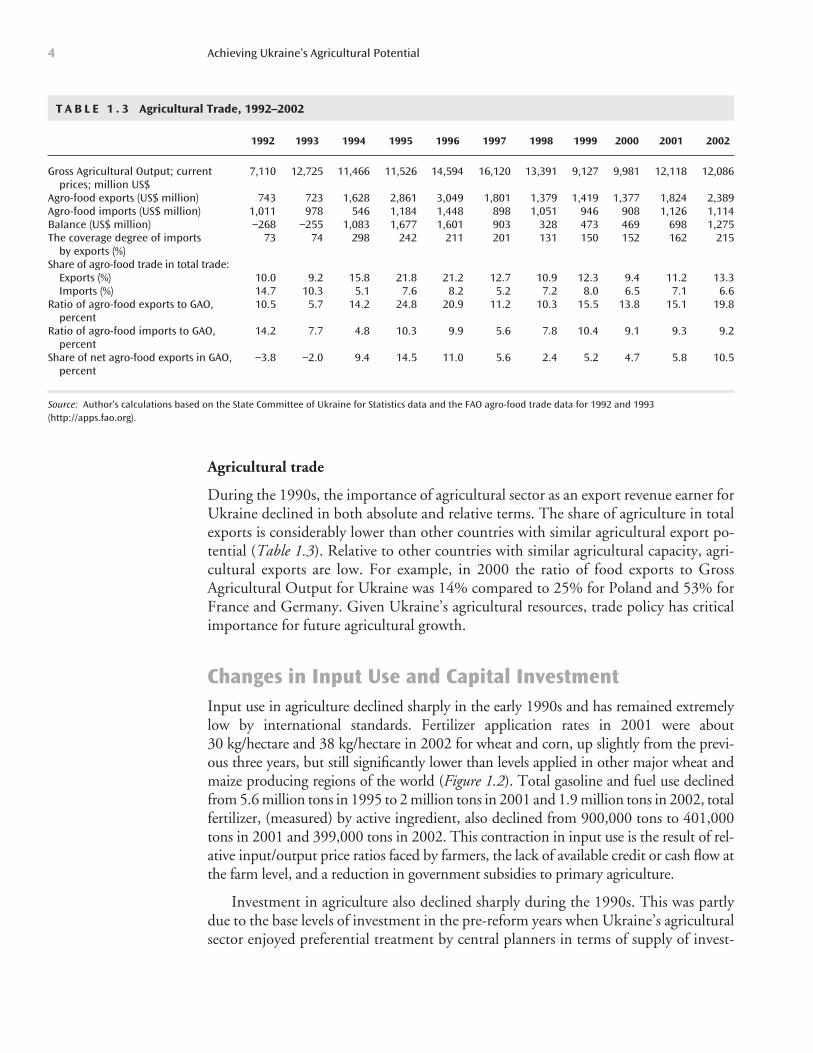

Changes in Input Use and Capital InvestmentInput use in agriculture declined sharply in the early 1990s and has remained extremelylow by international standards. Fertilizer application rates in 2001 were about30 kg/hectare and 38 kg/hectare in 2002 for wheat and corn, up slightly from the previ-ous three years, but still significantly lower than levels applied in other major wheat andmaize producing regions of the world (Figure 1.2). Total gasoline and fuel use declinedfrom 5.6 million tons in 1995 to 2 million tons in 2001 and 1.9 million tons in 2002, totalfertilizer, (measured) by active ingredient, also declined from 900,000 tons to 401,000tons in 2001 and 399,000 tons in 2002. This contraction in input use is the result of rel-ative input/output price ratios faced by farmers, the lack of available credit or cash flow atthe farm level, and a reduction in government subsidies to primary agriculture.

Investment in agriculture also declined sharply during the 1990s. This was partlydue to the base levels of investment in the pre-reform years when Ukraine’s agriculturalsector enjoyed preferential treatment by central planners in terms of supply of invest-

Achieving Ukraine’s Agricultural Potential4

T A B L E 1 . 3 Agricultural Trade, 1992–2002

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Gross Agricultural Output; current 7,110 12,725 11,466 11,526 14,594 16,120 13,391 9,127 9,981 12,118 12,086prices; million US$

Agro-food exports (US$ million) 743 723 1,628 2,861 3,049 1,801 1,379 1,419 1,377 1,824 2,389Agro-food imports (US$ million) 1,011 978 546 1,184 1,448 898 1,051 946 908 1,126 1,114Balance (US$ million) −268 −255 1,083 1,677 1,601 903 328 473 469 698 1,275The coverage degree of imports 73 74 298 242 211 201 131 150 152 162 215

by exports (%)Share of agro-food trade in total trade:

Exports (%) 10.0 9.2 15.8 21.8 21.2 12.7 10.9 12.3 9.4 11.2 13.3Imports (%) 14.7 10.3 5.1 7.6 8.2 5.2 7.2 8.0 6.5 7.1 6.6

Ratio of agro-food exports to GAO, 10.5 5.7 14.2 24.8 20.9 11.2 10.3 15.5 13.8 15.1 19.8percent

Ratio of agro-food imports to GAO, 14.2 7.7 4.8 10.3 9.9 5.6 7.8 10.4 9.1 9.3 9.2percent

Share of net agro-food exports in GAO, −3.8 −2.0 9.4 14.5 11.0 5.6 2.4 5.2 4.7 5.8 10.5percent

Source: Author’s calculations based on the State Committee of Ukraine for Statistics data and the FAO agro-food trade data for 1992 and 1993(http://apps.fao.org).

ment resources and working capital (Figure 1.1). However, the decline was made sharperand longer by the bad investment climate for agriculture during most of the 1990s (Fig-ure 1.1). The share of investment in primary agriculture of the total investment in thenational economy declined from 21.3% in 1990 to 2.1% in 2002 (Table 1.2).

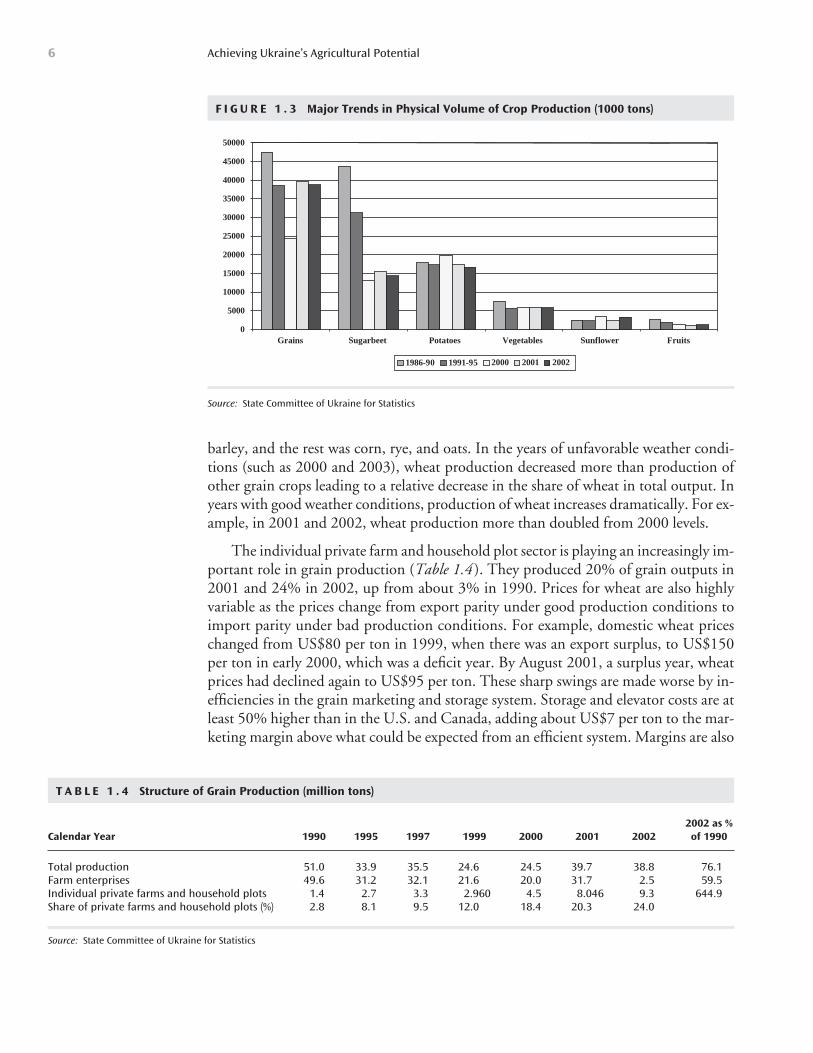

Commodity Specific Performance IndicatorsThe most significant change in agricultural output was the very sharp decline in live-stock production from about one-half to one-third of the total value of agricultural out-put. The main reason for this change was sharp decline in demand for animal productsprecipitated by a more than 60% drop in real per capita income in Ukraine between1990 and 2000. Demand for animal products decreased significantly more than forother food products because of its higher income elasticity. Grain production also de-clined sharply as the demand for feed grain declined, and farmgate prices for grains fellto levels that caused producers to move to low input/low output production methods.Grain production recovered in 2000–2002 levels as a result of several factors discussedin more detail in Chapter 2. Sugarbeet production also declined as domestic sugar pro-duction adjusted to increased competition from imports. The production of potatoes,vegetables, and sunflower was relatively stable during the 1990s. Potatoes and vegeta-bles were being produced primarily by private farmers or on household plots using laborintensive methods of production. Sunflower production levels were driven by profitableexport markets for the crop. Figure 1.3 shows the major trends in crop production vol-umes. More detailed information on commodity production is provided in Annex 1.

Trends in volume and structure of grain production

Between 1992 and 2000 grain production in Ukraine decreased by about one-third. In2001, it rebounded almost to the record level of the 1993 crop harvest. The structure ofgrain production was remarkably stable: about 55% of grain produced was wheat, 25%

Agricultural Sector Performance 5

F I G U R E 1 . 2 Mineral Fertilizer Application Rates and Changes in Grain Yields

0

50

100

150

200

250

300

1990 1997 1998 1999 2000 2001 2002

0

5

10

15

20

25

30

35

40

45

Winter and spring wheat - NPKapplied (kg/hectare) Corn - NPK applied (kg/hectare)

Wheat yields, 100 kg/hectare (right scale)

Corn yields, 100 kg/hectare (right scale)

Source: State Committee of Ukraine for Statistics

Trends in GrainProduction and

Marketing

barley, and the rest was corn, rye, and oats. In the years of unfavorable weather condi-tions (such as 2000 and 2003), wheat production decreased more than production ofother grain crops leading to a relative decrease in the share of wheat in total output. Inyears with good weather conditions, production of wheat increases dramatically. For ex-ample, in 2001 and 2002, wheat production more than doubled from 2000 levels.

The individual private farm and household plot sector is playing an increasingly im-portant role in grain production (Table 1.4 ). They produced 20% of grain outputs in2001 and 24% in 2002, up from about 3% in 1990. Prices for wheat are also highlyvariable as the prices change from export parity under good production conditions toimport parity under bad production conditions. For example, domestic wheat priceschanged from US$80 per ton in 1999, when there was an export surplus, to US$150per ton in early 2000, which was a deficit year. By August 2001, a surplus year, wheatprices had declined again to US$95 per ton. These sharp swings are made worse by in-efficiencies in the grain marketing and storage system. Storage and elevator costs are atleast 50% higher than in the U.S. and Canada, adding about US$7 per ton to the mar-keting margin above what could be expected from an efficient system. Margins are also

Achieving Ukraine’s Agricultural Potential6

F I G U R E 1 . 3 Major Trends in Physical Volume of Crop Production (1000 tons)

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

Grains Sugarbeet Potatoes Vegetables Sunflower Fruits

1986-90 1991-95 2000 2001 2002

Source: State Committee of Ukraine for Statistics

T A B L E 1 . 4 Structure of Grain Production (million tons)

2002 as % Calendar Year 1990 1995 1997 1999 2000 2001 2002 of 1990

Total production 51.0 33.9 35.5 24.6 24.5 39.7 38.8 76.1Farm enterprises 49.6 31.2 32.1 21.6 20.0 31.7 2.5 59.5Individual private farms and household plots 1.4 2.7 3.3 2.960 4.5 8.046 9.3 644.9Share of private farms and household plots (%) 2.8 8.1 9.5 12.0 18.4 20.3 24.0

Source: State Committee of Ukraine for Statistics

higher as a result of the high risk of ad hoc Government interventions in deficit yearsand high levels of business risk. High marketing margins result in lower farmgate prices.

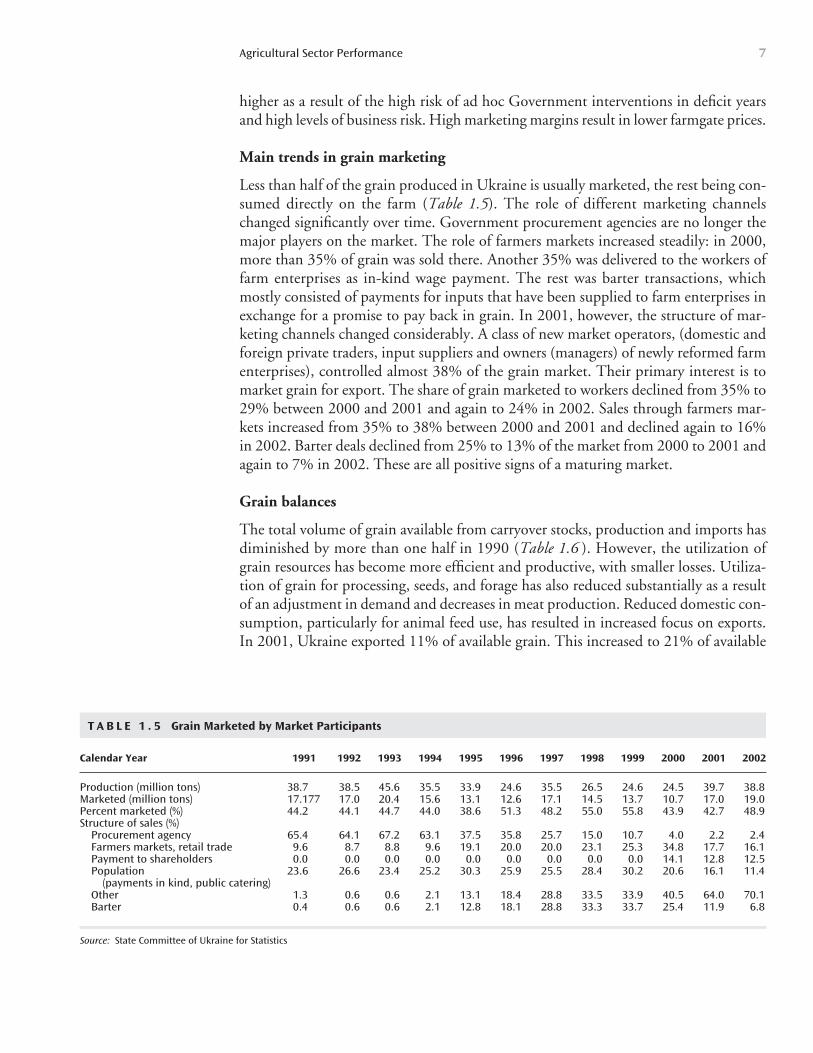

Main trends in grain marketing

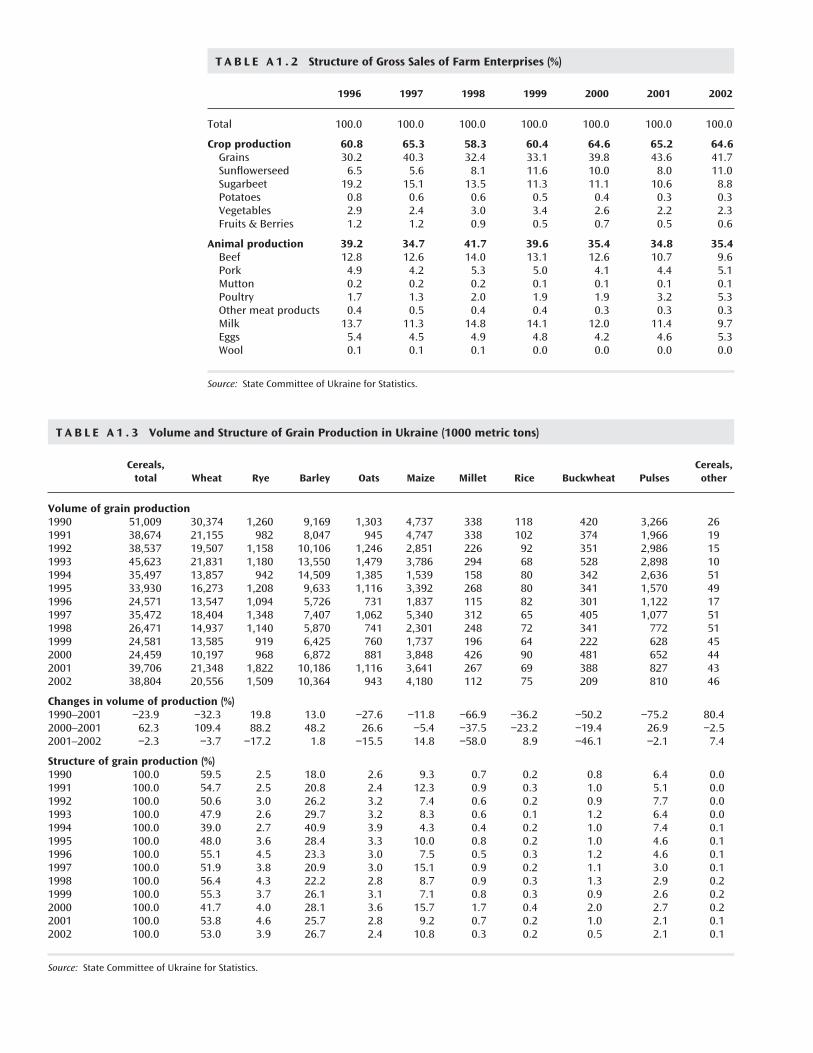

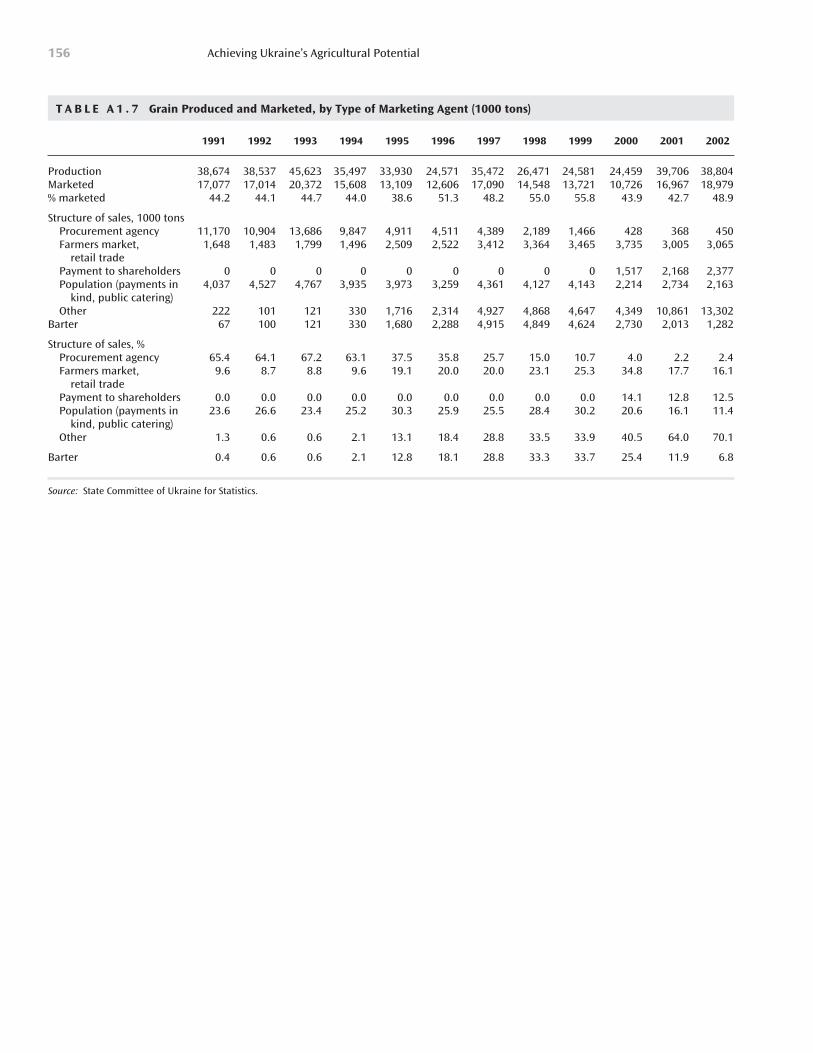

Less than half of the grain produced in Ukraine is usually marketed, the rest being con-sumed directly on the farm (Table 1.5). The role of different marketing channelschanged significantly over time. Government procurement agencies are no longer themajor players on the market. The role of farmers markets increased steadily: in 2000,more than 35% of grain was sold there. Another 35% was delivered to the workers offarm enterprises as in-kind wage payment. The rest was barter transactions, whichmostly consisted of payments for inputs that have been supplied to farm enterprises inexchange for a promise to pay back in grain. In 2001, however, the structure of mar-keting channels changed considerably. A class of new market operators, (domestic andforeign private traders, input suppliers and owners (managers) of newly reformed farmenterprises), controlled almost 38% of the grain market. Their primary interest is tomarket grain for export. The share of grain marketed to workers declined from 35% to29% between 2000 and 2001 and again to 24% in 2002. Sales through farmers mar-kets increased from 35% to 38% between 2000 and 2001 and declined again to 16%in 2002. Barter deals declined from 25% to 13% of the market from 2000 to 2001 andagain to 7% in 2002. These are all positive signs of a maturing market.

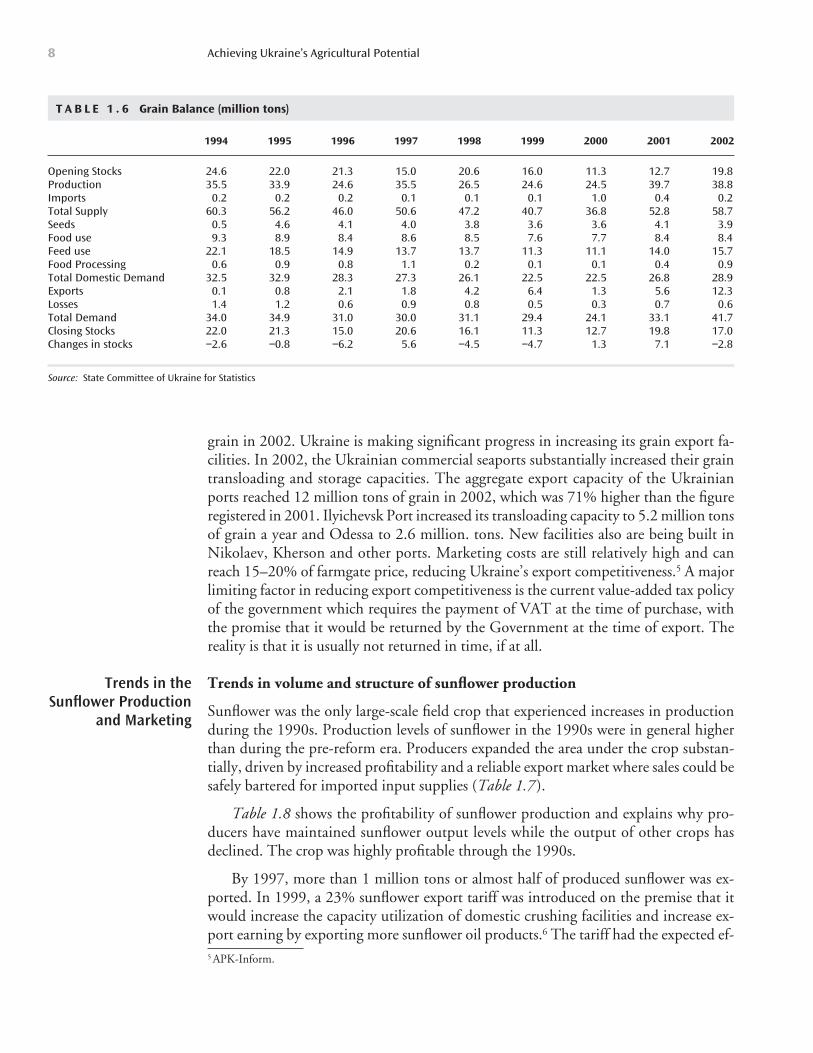

Grain balances

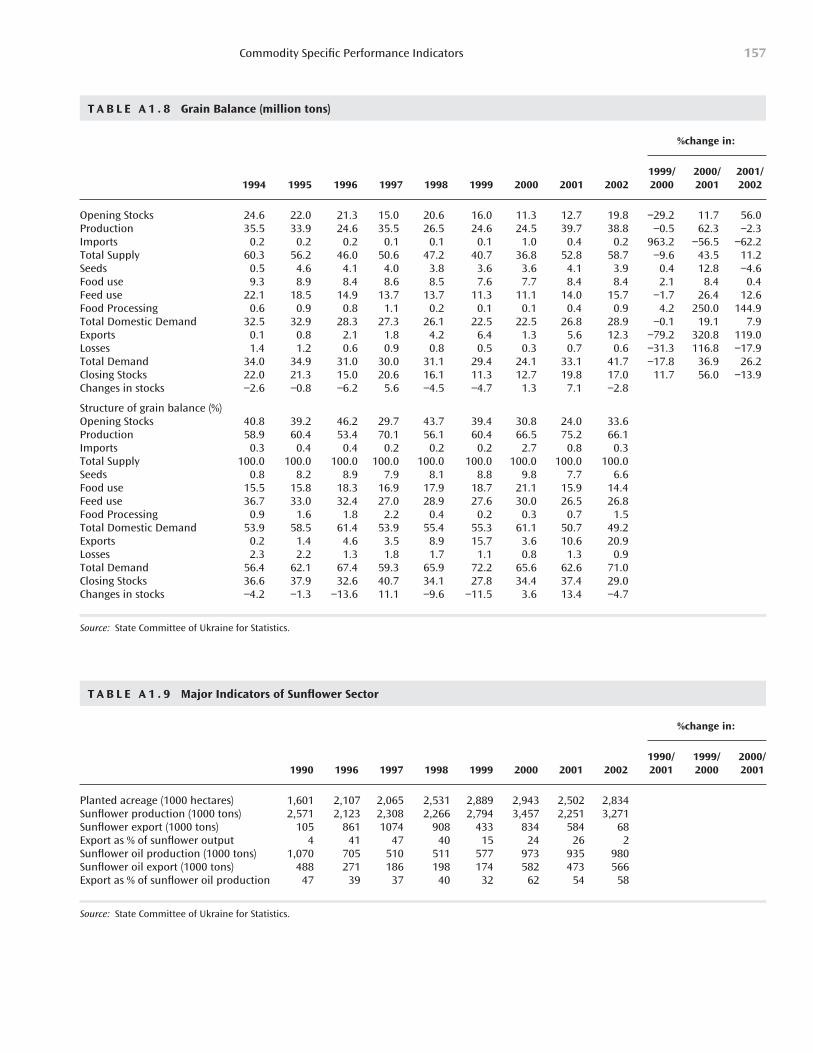

The total volume of grain available from carryover stocks, production and imports hasdiminished by more than one half in 1990 (Table 1.6 ). However, the utilization ofgrain resources has become more efficient and productive, with smaller losses. Utiliza-tion of grain for processing, seeds, and forage has also reduced substantially as a resultof an adjustment in demand and decreases in meat production. Reduced domestic con-sumption, particularly for animal feed use, has resulted in increased focus on exports.In 2001, Ukraine exported 11% of available grain. This increased to 21% of available

Agricultural Sector Performance 7

T A B L E 1 . 5 Grain Marketed by Market Participants

Calendar Year 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Production (million tons) 38.7 38.5 45.6 35.5 33.9 24.6 35.5 26.5 24.6 24.5 39.7 38.8Marketed (million tons) 17.177 17.0 20.4 15.6 13.1 12.6 17.1 14.5 13.7 10.7 17.0 19.0Percent marketed (%) 44.2 44.1 44.7 44.0 38.6 51.3 48.2 55.0 55.8 43.9 42.7 48.9Structure of sales (%)

Procurement agency 65.4 64.1 67.2 63.1 37.5 35.8 25.7 15.0 10.7 4.0 2.2 2.4Farmers markets, retail trade 9.6 8.7 8.8 9.6 19.1 20.0 20.0 23.1 25.3 34.8 17.7 16.1Payment to shareholders 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 14.1 12.8 12.5Population 23.6 26.6 23.4 25.2 30.3 25.9 25.5 28.4 30.2 20.6 16.1 11.4

(payments in kind, public catering)Other 1.3 0.6 0.6 2.1 13.1 18.4 28.8 33.5 33.9 40.5 64.0 70.1Barter 0.4 0.6 0.6 2.1 12.8 18.1 28.8 33.3 33.7 25.4 11.9 6.8

Source: State Committee of Ukraine for Statistics

grain in 2002. Ukraine is making significant progress in increasing its grain export fa-cilities. In 2002, the Ukrainian commercial seaports substantially increased their graintransloading and storage capacities. The aggregate export capacity of the Ukrainianports reached 12 million tons of grain in 2002, which was 71% higher than the figureregistered in 2001. Ilyichevsk Port increased its transloading capacity to 5.2 million tonsof grain a year and Odessa to 2.6 million. tons. New facilities also are being built inNikolaev, Kherson and other ports. Marketing costs are still relatively high and canreach 15–20% of farmgate price, reducing Ukraine’s export competitiveness.5 A majorlimiting factor in reducing export competitiveness is the current value-added tax policyof the government which requires the payment of VAT at the time of purchase, withthe promise that it would be returned by the Government at the time of export. Thereality is that it is usually not returned in time, if at all.

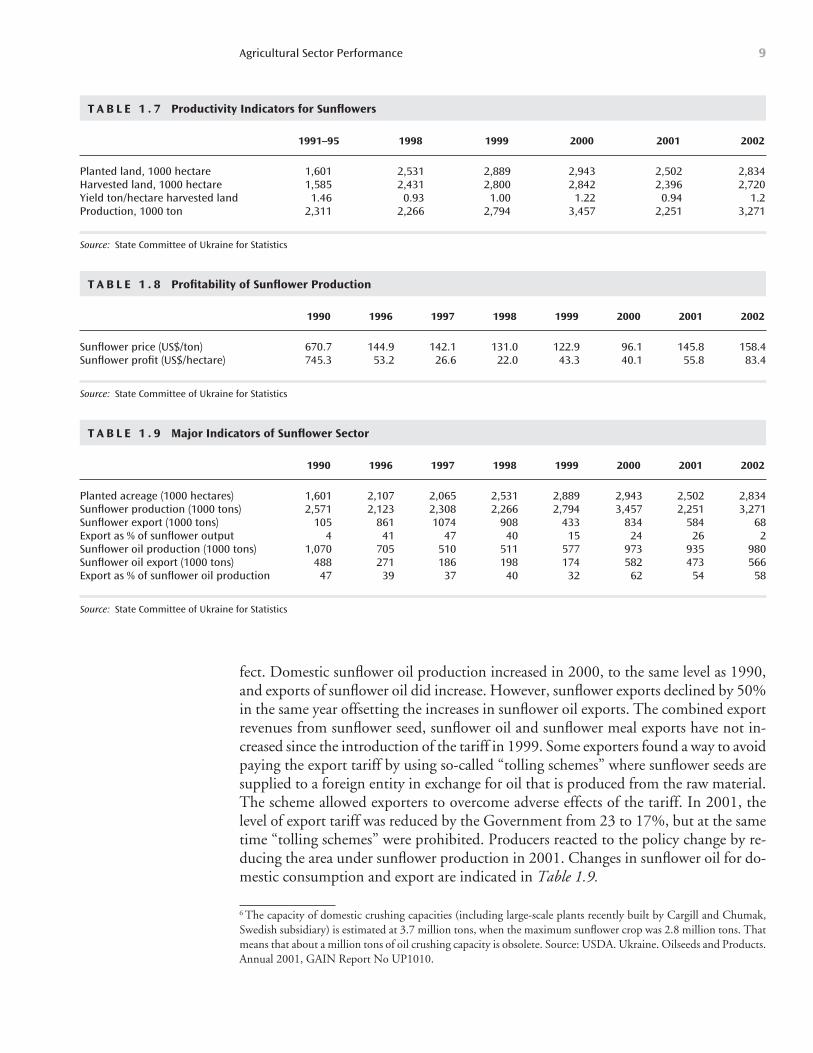

Trends in volume and structure of sunflower production

Sunflower was the only large-scale field crop that experienced increases in productionduring the 1990s. Production levels of sunflower in the 1990s were in general higherthan during the pre-reform era. Producers expanded the area under the crop substan-tially, driven by increased profitability and a reliable export market where sales could besafely bartered for imported input supplies (Table 1.7 ).

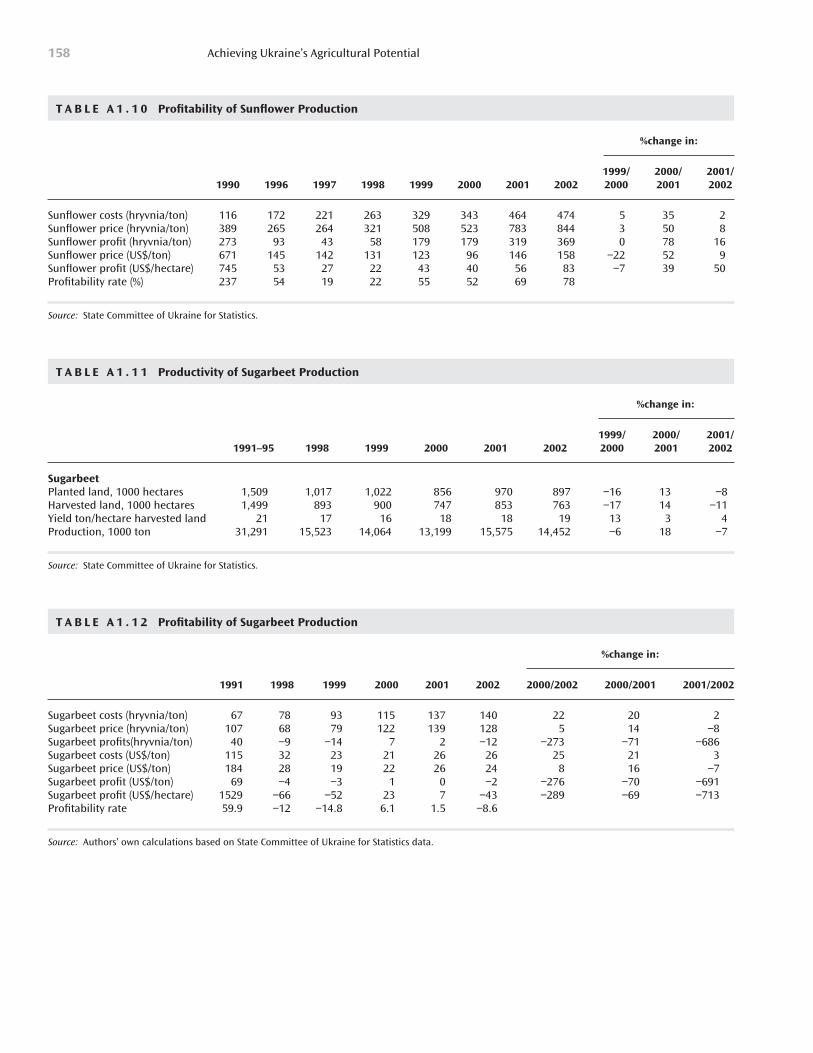

Table 1.8 shows the profitability of sunflower production and explains why pro-ducers have maintained sunflower output levels while the output of other crops hasdeclined. The crop was highly profitable through the 1990s.

By 1997, more than 1 million tons or almost half of produced sunflower was ex-ported. In 1999, a 23% sunflower export tariff was introduced on the premise that itwould increase the capacity utilization of domestic crushing facilities and increase ex-port earning by exporting more sunflower oil products.6 The tariff had the expected ef-

Achieving Ukraine’s Agricultural Potential8

T A B L E 1 . 6 Grain Balance (million tons)

1994 1995 1996 1997 1998 1999 2000 2001 2002

Opening Stocks 24.6 22.0 21.3 15.0 20.6 16.0 11.3 12.7 19.8Production 35.5 33.9 24.6 35.5 26.5 24.6 24.5 39.7 38.8Imports 0.2 0.2 0.2 0.1 0.1 0.1 1.0 0.4 0.2Total Supply 60.3 56.2 46.0 50.6 47.2 40.7 36.8 52.8 58.7Seeds 0.5 4.6 4.1 4.0 3.8 3.6 3.6 4.1 3.9Food use 9.3 8.9 8.4 8.6 8.5 7.6 7.7 8.4 8.4Feed use 22.1 18.5 14.9 13.7 13.7 11.3 11.1 14.0 15.7Food Processing 0.6 0.9 0.8 1.1 0.2 0.1 0.1 0.4 0.9Total Domestic Demand 32.5 32.9 28.3 27.3 26.1 22.5 22.5 26.8 28.9Exports 0.1 0.8 2.1 1.8 4.2 6.4 1.3 5.6 12.3Losses 1.4 1.2 0.6 0.9 0.8 0.5 0.3 0.7 0.6Total Demand 34.0 34.9 31.0 30.0 31.1 29.4 24.1 33.1 41.7Closing Stocks 22.0 21.3 15.0 20.6 16.1 11.3 12.7 19.8 17.0Changes in stocks −2.6 −0.8 −6.2 5.6 −4.5 −4.7 1.3 7.1 −2.8

Source: State Committee of Ukraine for Statistics

5 APK-Inform.

Trends in theSunflower Production

and Marketing

Agricultural Sector Performance 9

T A B L E 1 . 7 Productivity Indicators for Sunflowers

1991–95 1998 1999 2000 2001 2002

Planted land, 1000 hectare 1,601 2,531 2,889 2,943 2,502 2,834Harvested land, 1000 hectare 1,585 2,431 2,800 2,842 2,396 2,720Yield ton/hectare harvested land 1.46 0.93 1.00 1.22 0.94 1.2Production, 1000 ton 2,311 2,266 2,794 3,457 2,251 3,271

Source: State Committee of Ukraine for Statistics

T A B L E 1 . 8 Profitability of Sunflower Production

1990 1996 1997 1998 1999 2000 2001 2002

Sunflower price (US$/ton) 670.7 144.9 142.1 131.0 122.9 96.1 145.8 158.4Sunflower profit (US$/hectare) 745.3 53.2 26.6 22.0 43.3 40.1 55.8 83.4

Source: State Committee of Ukraine for Statistics

fect. Domestic sunflower oil production increased in 2000, to the same level as 1990,and exports of sunflower oil did increase. However, sunflower exports declined by 50%in the same year offsetting the increases in sunflower oil exports. The combined exportrevenues from sunflower seed, sunflower oil and sunflower meal exports have not in-creased since the introduction of the tariff in 1999. Some exporters found a way to avoidpaying the export tariff by using so-called “tolling schemes” where sunflower seeds aresupplied to a foreign entity in exchange for oil that is produced from the raw material.The scheme allowed exporters to overcome adverse effects of the tariff. In 2001, thelevel of export tariff was reduced by the Government from 23 to 17%, but at the sametime “tolling schemes” were prohibited. Producers reacted to the policy change by re-ducing the area under sunflower production in 2001. Changes in sunflower oil for do-mestic consumption and export are indicated in Table 1.9.

6 The capacity of domestic crushing capacities (including large-scale plants recently built by Cargill and Chumak,Swedish subsidiary) is estimated at 3.7 million tons, when the maximum sunflower crop was 2.8 million tons. Thatmeans that about a million tons of oil crushing capacity is obsolete. Source: USDA. Ukraine. Oilseeds and Products.Annual 2001, GAIN Report No UP1010.

T A B L E 1 . 9 Major Indicators of Sunflower Sector

1990 1996 1997 1998 1999 2000 2001 2002

Planted acreage (1000 hectares) 1,601 2,107 2,065 2,531 2,889 2,943 2,502 2,834Sunflower production (1000 tons) 2,571 2,123 2,308 2,266 2,794 3,457 2,251 3,271Sunflower export (1000 tons) 105 861 1074 908 433 834 584 68Export as % of sunflower output 4 41 47 40 15 24 26 2Sunflower oil production (1000 tons) 1,070 705 510 511 577 973 935 980Sunflower oil export (1000 tons) 488 271 186 198 174 582 473 566Export as % of sunflower oil production 47 39 37 40 32 62 54 58

Source: State Committee of Ukraine for Statistics

Potatoes and vegetables are almost exclusively produced by the household sector. In2000, 98.6% of the total potato crop and 80% of the vegetable crop was produced onhousehold plots. Production levels of these commodities have been stable, and evenincreasing slightly during the 1990s. The sown area for potatoes is between 1.5 and1.6 million hectares. Average total annual production of potatoes for Ukraine is be-tween 10–12 million tons, of which 6–7 million tons are consumed as food and 4–5million tons are used as seed. Most potatoes and vegetables are consumed by the house-holds that produce them, with the surplus being sold in local markets.

Throughout the transition period, meat sector in Ukraine has undergone a long andpainful adjustment. Reduced demand for meat as a result of the reduced purchasingpower of the population, resulted in a decline in the total value of meat products pro-duced by 65% between 1990 and 2000. During this period, the production of animal

Achieving Ukraine’s Agricultural Potential10

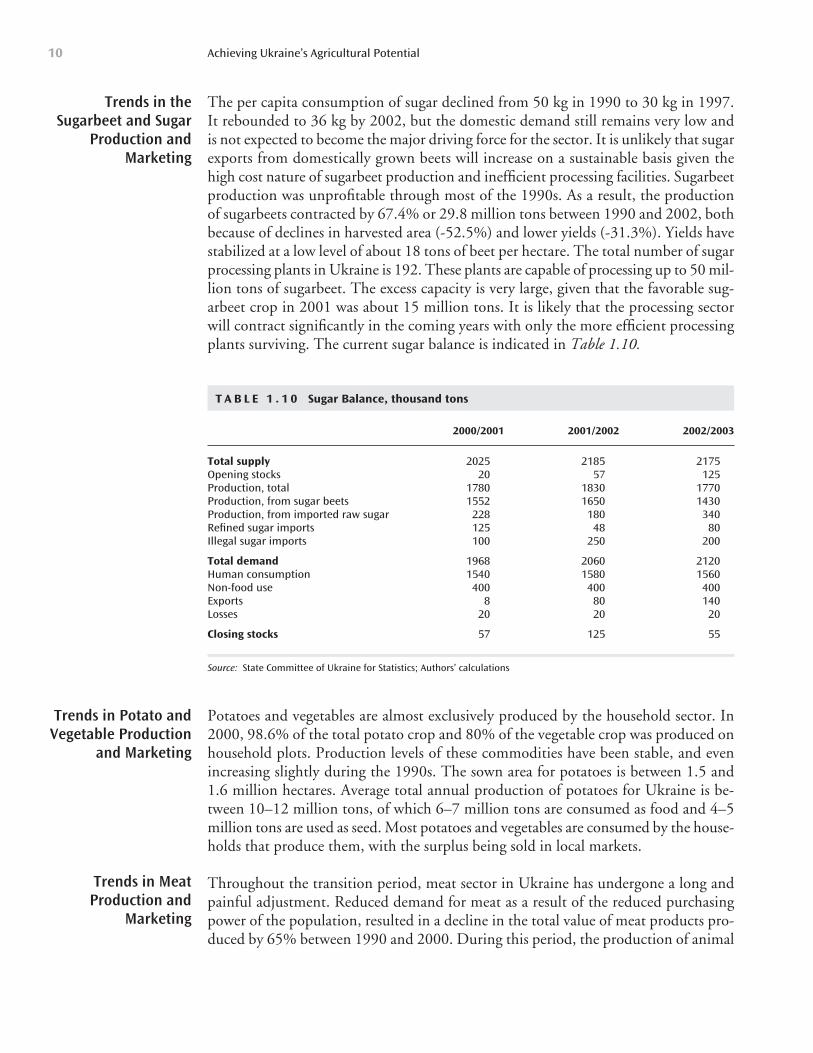

T A B L E 1 . 1 0 Sugar Balance, thousand tons

2000/2001 2001/2002 2002/2003

Total supply 2025 2185 2175Opening stocks 20 57 125Production, total 1780 1830 1770Production, from sugar beets 1552 1650 1430Production, from imported raw sugar 228 180 340Refined sugar imports 125 48 80Illegal sugar imports 100 250 200

Total demand 1968 2060 2120Human consumption 1540 1580 1560Non-food use 400 400 400Exports 8 80 140Losses 20 20 20

Closing stocks 57 125 55

Source: State Committee of Ukraine for Statistics; Authors’ calculations

Trends in Potato andVegetable Production

and Marketing

Trends in MeatProduction and

Marketing

Trends in theSugarbeet and Sugar

Production andMarketing

The per capita consumption of sugar declined from 50 kg in 1990 to 30 kg in 1997.It rebounded to 36 kg by 2002, but the domestic demand still remains very low andis not expected to become the major driving force for the sector. It is unlikely that sugarexports from domestically grown beets will increase on a sustainable basis given thehigh cost nature of sugarbeet production and inefficient processing facilities. Sugarbeetproduction was unprofitable through most of the 1990s. As a result, the productionof sugarbeets contracted by 67.4% or 29.8 million tons between 1990 and 2002, bothbecause of declines in harvested area (-52.5%) and lower yields (-31.3%). Yields havestabilized at a low level of about 18 tons of beet per hectare. The total number of sugarprocessing plants in Ukraine is 192. These plants are capable of processing up to 50 mil-lion tons of sugarbeet. The excess capacity is very large, given that the favorable sug-arbeet crop in 2001 was about 15 million tons. It is likely that the processing sectorwill contract significantly in the coming years with only the more efficient processingplants surviving. The current sugar balance is indicated in Table 1.10.

products, with the exception of eggs and poultry remained unprofitable. During thisperiod of decline, meat production also shifted in favor of pork and away from beefand mutton. In 2001, meat production experienced its first turnaround in a decade.The gross value of animal production increased by 5.3% in 2001 and again by 5.6%in 2002, mainly as a result of increased prices. Meat production makes up about 20%of agricultural output (CASE 2002).

Animal efficiency indicators in the individual private farm and household sectors arestill much higher than in farm enterprises. For example, the weight gains of cattle in thehousehold sector are in the range of 580–750 grams per day, compared to only 318 gramsa day in farm enterprises. In hog production, the weight gains are 320–380 grams a dayin individual private farm and household sectors compared to 173 grams a day in farmenterprises. According to the Ukrainian Institute of Agrarian Economics, in order toreach a breakeven point in profits, average weight gains should be at least 400 grams perday in cattle production and about 200 grams per day in pork production. As of today,the daily gains in agricultural enterprises are still 2 to 2.4 times lower than the mini-mum level of efficiency that is needed for them to become profitable.

According to official statistics, the household sector marketed 34% of total meatand meat products they produced in 2002. The household sector sold about 40% ofproduce to processing and purchasing enterprises.