acegas interim report q3 2010

TRANSCRIPT

8/3/2019 Acegas Interim Report Q3 2010

http://slidepdf.com/reader/full/acegas-interim-report-q3-2010 1/8

Acegas-Aps SpaVia del Teatro, 5

34121 TriesteCap.Soc.283.690.762.80 i.v.

Codice Fiscale e iscrizione n. 00930530324R.E.A.n. 111554 - CC.I.A.A. Trieste

P.IVA 00930530324www.acegas-aps.it

Investor Relations: Federico Trevisan Media Relations: Maurizio Stefani [email protected] [email protected]: +39-040-7793.368 [email protected]: +39-040-7793.233 Office PD: +39-049-8280.551

Office TS: +39-040-7793.534Fax PD: +39-049-8280.554Fax TS: +39-040-7793.295

Interim management report to 30 September2010 approved

Results for the period register a sharp improvement:• Net revenues: € 360.9 million (+ € 13.6 million, i.e. +3.9% vs. 9M09)• EBITDA: € 76.6 million (+ € 9.2 million, or +13.7%)• Group net profit: € 15.6 million (+ € 12.4 million, or +387%)

Trieste, 11 November 2010: Today the Board of Directors of AcegasAps, under the chairmanship of Massimo Paniccia, reviewed and approved the Group’s results for the first nine months of 2010 (9M10).

The AcegasAps Group’snet revenues increased by € 13.6 million (+3.9%), from € 347.4 million in9M09 to € 360.9 million in 9M10. This growth was supported by the significant increase in revenues inthe Services Division, up a total of € 7.9 million, related to the positive performance of subsidiarySinergie, thanks to the acquisition of new customers and the launch of new contracts (Padua Hospitals).Also posting significant growth were the Waste Management Division, with revenues up € 5.6 million,mainly owing to the launch of the third line of the waste-to-energy plant in Padua, and the IntegratedWater Management Division (+ € 5.0 million), which benefited from the 6% tariff increase in the Paduaarea, and, from June 2010, also in the Trieste area (around 28%). Finally, the Gas Division registered adecline in revenues of € 4.5 million. This was due to lower gas sales prices as a result of the trend in oilprices. EBITDAadvanced from € 67.4 million to € 76.6 million, an increase of 13.7%. The Integrated WaterManagement Divisionmade the most significant contribution to EBITDA growth, with an increase in itsEBITDA figure of € 4.2 million (+18.4%). Specifically, EBITDA of the Integrated Water ManagementDivision rose from € 23.0 million in 9M09 to € 27.2 million in 9M10. Contributions to this growth wereprovided by both the Padua area, with an average tariff increase of 6%, and the Trieste area, where from June 2010, the new tariff system was fully applied, resulting in an average tariff increase of around 28%.As regards volumes, the Integrated Water Management Division registered a slight fall in quantitiesdistributed, from 40.5 million cubic metres in 9M09 to 40.2 million in 9M10 (-0.8%).

The Waste Management Divisionclosed 9M10 with a rise of € 0.9 million, from € 26.0 million to €26.8 million. This was mainly the result of the coming on stream of the third line of the WTE plant inPadua, whose EBITDA advanced by € 3.7 million in 9M10 versus 9M09. Note too that this result wasaffected by the fact that from 1 January 2010, Green Certificates for the power generated by L2 of thePadua plant (12.8 GWh in the first nine months of last year) were no longer recognised, which had anegative impact of € 1.1 million on the figure. As regards the management of the WTE plant in Trieste, the 9M10 result was affected by a negativechange in EBITDA of € 0.6 million, corresponding to a positive CIP6 equalisation payment registered in2009 related to the previous year.In volume terms, waste-to—energy processing decreased slightly (163,000 tonnes in 9M10, down 1.9%versus 9M09), as did power generated (82 GWh, down 10.6%), owing to the work undertaken during the year to launch the third line of the Padua WTE plant, but also, more recently, owing to the decline inproduction at the Trieste plant due to breakdowns that limited activity.

8/3/2019 Acegas Interim Report Q3 2010

http://slidepdf.com/reader/full/acegas-interim-report-q3-2010 2/8

Acegas-Aps SpaVia del Teatro, 5

34121 TriesteCap.Soc.283.690.762.80 i.v.

Codice Fiscale e iscrizione n. 00930530324R.E.A.n. 111554 - CC.I.A.A. Trieste

P.IVA 00930530324www.acegas-aps.it

Investor Relations: Federico Trevisan Media Relations: Maurizio Stefani [email protected] [email protected]: +39-040-7793.368 [email protected]: +39-040-7793.233 Office PD: +39-049-8280.551

Office TS: +39-040-7793.534Fax PD: +39-049-8280.554Fax TS: +39-040-7793.295

EBITDA of thePower Divisionrose by € 0.1 million, from € 8.8 million in 9M09 to € 8.9 million in

9M10. The bulk of this increase was due to greater sales activity (+ € 0.5 million), thanks to a moreprofitable customer portfolio and a more careful supply policy. Distribution (- € 0.2 million) andgeneration (- € 0.1 million) activities both registered slight falls. As regards volumes, generation at theElettrogorizia power plant increased by 9 GWh (+18.2%). Volumes of electricity distributed totalledalmost 600 GWh, corresponding to growth of 1.4% versus 9M09. Volumes of electricity sold rosesharply, from 588 GWh in 9M09 to 634 GWh in 9M10 (+7.8%).

EBITDA of theGas Divisionrose to € 24.0 million, ending the first nine months of 2010 with anincrease of € 2.1 million. Sales activities increased, with a positive change in EBITDA of € 0.8 million,while overhead costs advanced (+ € 0.4 million). EBITDA of distribution activities came out € 1.2 millionahead of the 9M09 figure, owing to the new tariff model that came into force in 2009. Volumes in 9M10registered significant growth, both in terms of distribution activities (336 million cubic metres, versus293 million in 9M09, +14.9%), and sales (296 million cubic metres in 9M10, versus 266 million in9M09, +11.3%). EBITDA of theServices Divisionincreased by € 1.3 million, from € 9.5 million to € 10.8 million. Note,within this business line, growth of subsidiary Sinergie, which expanded its customer portfolio andimproved its profitability. Sinergie closed the period with a rise in EBITDA of € 1.4 million, from € 6.5million in 9M09 to € 7.7 million in 9M10. Provisionscame in at a negative € 2.6 million, from a positive figure of € 0.8 million in 9M09, a periodmarked by the release of provisions for the dispute relating to the landfill site at Ponte San Nicolò.Provisions for disputes with third parties, employees (dispute with INPS) and for the management of waste in storage totalled € 2.6 million in the period under review. Depreciation, amortisation and write-downsincreased by € 3.3 million, from € 36.9 million to € 40.2million. Depreciation increased by € 2.8 million, from € 35.7 million to € 38.5 million. This rise relatesto the significant investment made over the last few years, particularly in the water and waste businesses.Provisions for the doubtful accounts fund totalled € 1.7 million (versus € 1.3 million in 9M09), and wereimplemented to bring the fund into line with the customer insolvency risk. The provisions to 30September 2010 are higher than for the same period of 2009 (€ 0.4 million), since analyses showedthat the existing fund needed to be increased, given the nature of the credit positions managed and thegreater risk inherent in certain positions.

EBITin 9M10 totalled € 33.8 million versus € 31.3 million in 9M09, an increase of € 2.5 million(+7.9%). The Group’s operating efficiency also improved, which had an impact on 9M10 results, leading to a 9.4% EBIT margin on sales, versus 9.0% in 9M09.

Financial chargesfell by € 6.0 million, from € 11.7 million in 9M09 to € 5.7 million in 9M10. Thismajor reduction was mainly due to the structure of the Group’s borrowings, 95% of which are variable-rate, and to the tangible decrease of base interest rates seen between the two periods. Note too that in9M09, this item was affected by non-recurring financial charges of € 4.0 million related to the clawbackof the tax moratorium.

8/3/2019 Acegas Interim Report Q3 2010

http://slidepdf.com/reader/full/acegas-interim-report-q3-2010 3/8

Acegas-Aps SpaVia del Teatro, 5

34121 TriesteCap.Soc.283.690.762.80 i.v.

Codice Fiscale e iscrizione n. 00930530324R.E.A.n. 111554 - CC.I.A.A. Trieste

P.IVA 00930530324www.acegas-aps.it

Investor Relations: Federico Trevisan Media Relations: Maurizio Stefani [email protected] [email protected]: +39-040-7793.368 [email protected]: +39-040-7793.233 Office PD: +39-049-8280.551

Office TS: +39-040-7793.534Fax PD: +39-049-8280.554Fax TS: +39-040-7793.295

Income taxes fell by € 2.8 million, from € 15.6 million to € 12.8 million. 9M09 was negatively affectedby the contingent liabilities relating to the payment of IRPEG taxes calculated on the years of the tax

moratorium from 1997 to 1999 totalling € 5.9 million. Stripping out this phenomenon, the tax ratewould have been down compared to that recorded in the same period of 2009 (51.3% in 2009 versus45.2% in 2010).

Net profitcame in at € 15.6 million, compared with € 3.2 million in 9M09, an increase of € 12.4million. Without the non-recurring impact of the tax moratorium, growth in net profit in 9M10 wouldhave been € 3.5 million (+28.8%) against the same period last year.

As regardsinvestments, Group capital expenditure totalled € 65 million in 9M10, versus € 89 million in9M09. Investments therefore fell by € 24 million in 9M10, mainly owing to the lower rate of investmentin the Padua WTE plant, which came on stream in May 2010.

Thenet financial positionrose from € 407.4 million as of 31 December 2009 to € 451.2 million as of 30 September 2010. In absolute terms, this is an increase of € 43.8 million.

Events after 30 September 2010 The Group launched a company restructuring with a view to integrating the activities conducted by someof its minor subsidiaries. In this regard, it decided to put Ricicla Srl into liquidation (an operation that willbe completed by the end of the current year) and to fully demerge Nestenergia Spa in favour of subsidiaries Sinergie Spa and Nestambiente Spa. Iniziative Ambientali Srl, a full subsidiary of AcegasApsSpa operating in environmental services, was also established.

Business outlookThe approval of the new rates for the Integrated Water Management Division in Trieste, determinedaccording to the “Normalised Method” and in force from 22 June, has led to sustained revenues growthin the Trieste area: the effect on revenues of reaching the maximum annual increase threshold allowedby the tariff method (“tariff limit”) is approximately € 0.6 million/month, also valid for the fourth quarter of 2010. In the Padua area, activities continue to determine the 2007-2009 tariff rebalancing by the BacchiglioneAATO (Optimum Territorial Area Authority).Finally, through appropriate synergies between Group Divisions and Companies, the Group is assessing the possibility of optimising the disposal process for biological sludge resulting from purification plants,partly by industrialising the incineration process for this by-product (firstly on an experimental basis) atthe Company’s WTE plants.

8/3/2019 Acegas Interim Report Q3 2010

http://slidepdf.com/reader/full/acegas-interim-report-q3-2010 4/8

Acegas-Aps SpaVia del Teatro, 5

34121 TriesteCap.Soc.283.690.762.80 i.v.

Codice Fiscale e iscrizione n. 00930530324R.E.A.n. 111554 - CC.I.A.A. Trieste

P.IVA 00930530324www.acegas-aps.it

Investor Relations: Federico Trevisan Media Relations: Maurizio Stefani [email protected] [email protected]: +39-040-7793.368 [email protected]: +39-040-7793.233 Office PD: +39-049-8280.551

Office TS: +39-040-7793.534Fax PD: +39-049-8280.554Fax TS: +39-040-7793.295

Declaration of the Corporate Financial Reporting ManagerThe Corporate Financial Reporting Manager, Massimo Forliti, herewith declares that the financial disclosure contained in this press release matches documentary evidence, corporate books, and accounting records .

The following pages show the income statement, balance sheet, net financial position and cash flow statement of the AcegasAps Group.

8/3/2019 Acegas Interim Report Q3 2010

http://slidepdf.com/reader/full/acegas-interim-report-q3-2010 5/8

Acegas-Aps SpaVia del Teatro, 5

34121 TriesteCap.Soc.283.690.762.80 i.v.

Codice Fiscale e iscrizione n. 00930530324R.E.A.n. 111554 - CC.I.A.A. Trieste

P.IVA 00930530324www.acegas-aps.it

Investor Relations: Federico Trevisan Media Relations: Maurizio Stefani [email protected] [email protected]: +39-040-7793.368 [email protected]: +39-040-7793.233 Office PD: +39-049-8280.551

Office TS: +39-040-7793.534Fax PD: +39-049-8280.554Fax TS: +39-040-7793.295

€ /000

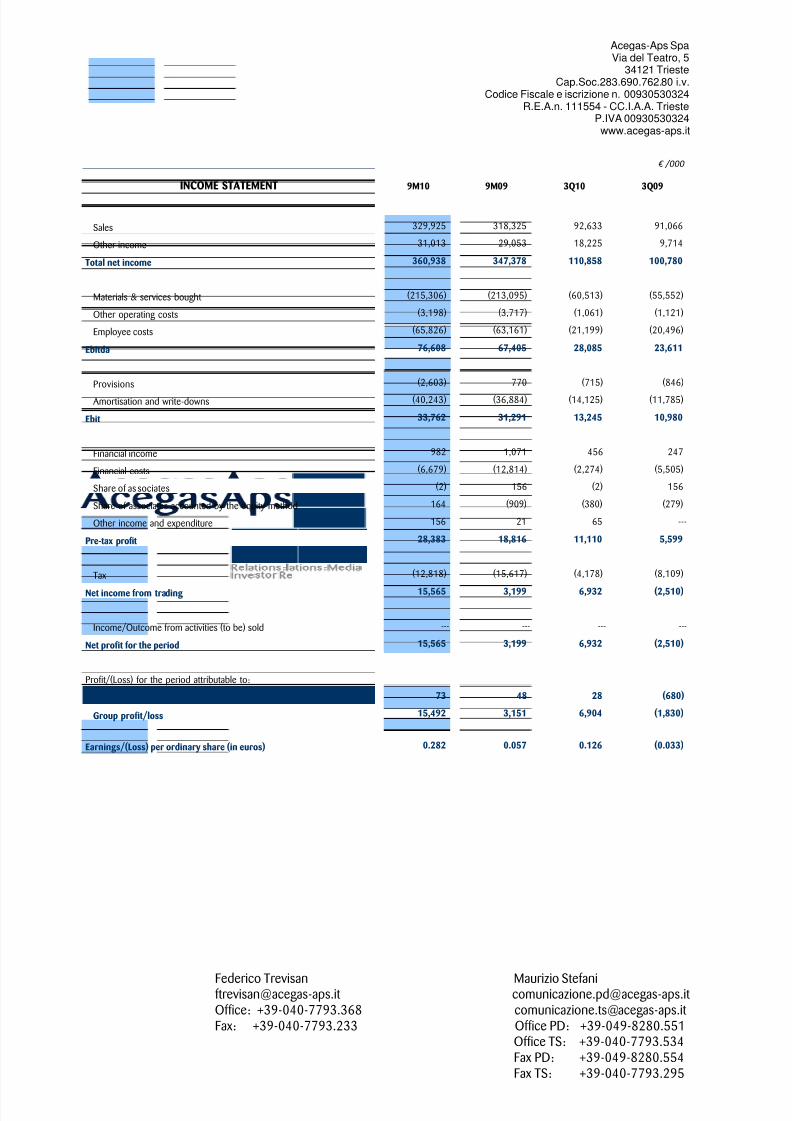

INCOME STATEMENT 9M10 9M09 3Q10 3Q09

Sales 329,925 318,325 92,633 91,066

Other income 31,013 29,053 18,225 9,714

Total net income 360,938 347,378 110,858 100,780

Materials & services bought (215,306) (213,095) (60,513) (55,552)

Other operating costs (3,198) (3,717) (1,061) (1,121)

Employee costs (65,826) (63,161) (21,199) (20,496)

Ebitda 76,608 67,405 28,085 23,611

Provisions (2,603) 770 (715) (846)

Amortisation and write-downs (40,243) (36,884) (14,125) (11,785)

Ebit 33,762 31,291 13,245 10,980

Financial income 982 1,071 456 247

Financial costs (6,679) (12,814) (2,274) (5,505)

Share of as sociates (2) 156 (2) 156

Share of associates accounted by the equity method 164 (909) (380) (279)

Other income and expenditure 156 21 65 ---

Pre-tax profit 28,383 18,816 11,110 5,599

Tax (12,818) (15,617) (4,178) (8,109)

Net income from trading 15,565 3,199 6,932 (2,510)

Income/Outcome from activities (to be) sold --- --- --- ---

Net profit for the period 15,565 3,199 6,932 (2,510)

Profit/(Loss) for the period attributable to:

Minorities 73 48 28 (680)

Group profit/loss 15,492 3,151 6,904 (1,830)

Earnings/(Loss) per ordinary share (in euros) 0.282 0.057 0.126 (0.033)

8/3/2019 Acegas Interim Report Q3 2010

http://slidepdf.com/reader/full/acegas-interim-report-q3-2010 6/8

Acegas-Aps SpaVia del Teatro, 5

34121 TriesteCap.Soc.283.690.762.80 i.v.

Codice Fiscale e iscrizione n. 00930530324R.E.A.n. 111554 - CC.I.A.A. Trieste

P.IVA 00930530324www.acegas-aps.it

Investor Relations: Federico Trevisan Media Relations: Maurizio Stefani [email protected] [email protected]: +39-040-7793.368 [email protected]: +39-040-7793.233 Office PD: +39-049-8280.551

Office TS: +39-040-7793.534Fax PD: +39-049-8280.554Fax TS: +39-040-7793.295

€ /000

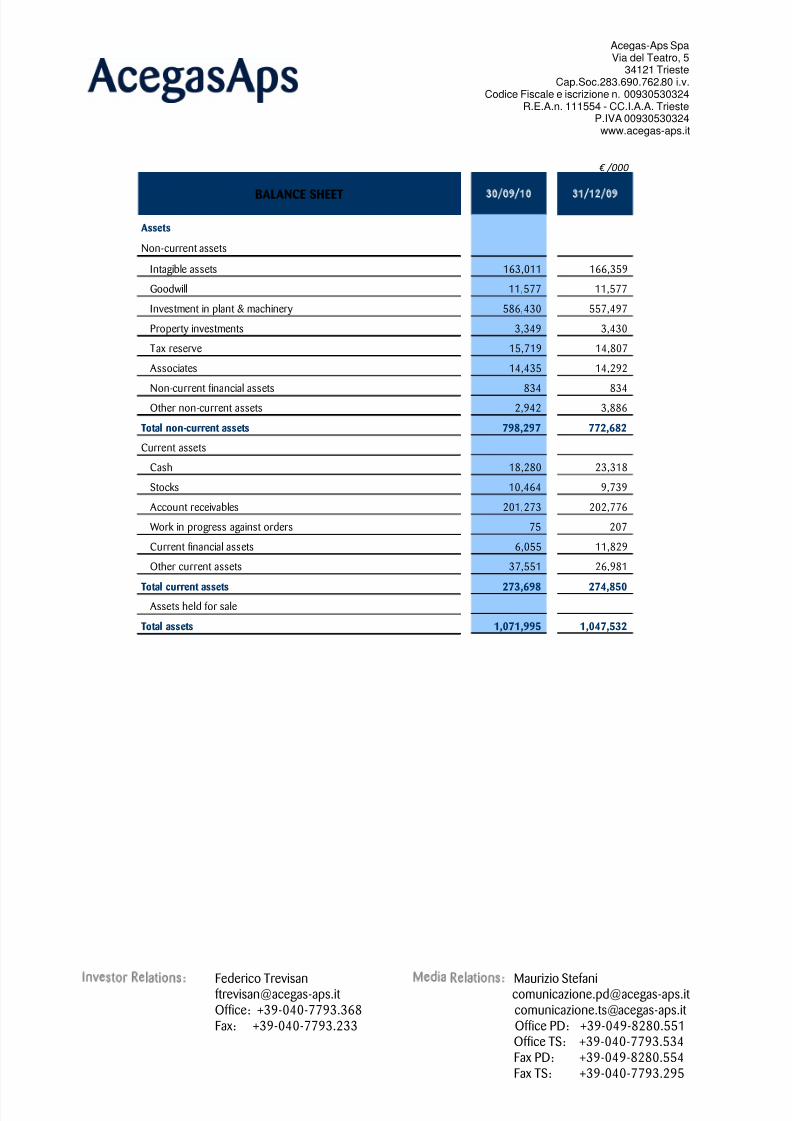

BALANCE SHEET 30/09/10 31/12/09

Assets

Non-current assets

Intagible assets 163,011 166,359

Goodwill 11,577 11,577

Investment in plant & machinery 586,430 557,497

Property investments 3,349 3,430

Tax reserve 15,719 14,807

Associates 14,435 14,292

Non-current financial assets 834 834Other non-current assets 2,942 3,886

Total non-current assets 798,297 772,682

Current assets

Cash 18,280 23,318

Stocks 10,464 9,739

Account receivables 201,273 202,776

Work in progress against orders 75 207

Current financial assets 6,055 11,829

Other current assets 37,551 26,981

Total current assets 273,698 274,850Assets held for sale

Total assets 1,071,995 1,047,532

8/3/2019 Acegas Interim Report Q3 2010

http://slidepdf.com/reader/full/acegas-interim-report-q3-2010 7/8

Acegas-Aps SpaVia del Teatro, 5

34121 TriesteCap.Soc.283.690.762.80 i.v.

Codice Fiscale e iscrizione n. 00930530324R.E.A.n. 111554 - CC.I.A.A. Trieste

P.IVA 00930530324www.acegas-aps.it

Investor Relations: Federico Trevisan Media Relations: Maurizio Stefani [email protected] [email protected]: +39-040-7793.368 [email protected]: +39-040-7793.233 Office PD: +39-049-8280.551

Office TS: +39-040-7793.534Fax PD: +39-049-8280.554Fax TS: +39-040-7793.295

€ /000

BALANCE SHEET 30/09/10 31/12/09

Liabilities

Net assets

Share capital 283,691 283,691

Share premium reserve 6,643 6,643

Other reserves 46,748 46,393

Profit/Loss carried forward 2,382 (3,022)

Profit/Loss for the period 15,492 10,743

Group net assets 354,956 344,448

Minorities 460 392Total net assets 355,416 344,840

Non-current liabilities

Employee funds 26,601 26,969

Provisions 16,067 17,067

Medium/Long term financing 287,093 257,405

Non-current financial liabilities 11,551 12,610

Liability for deferred tax 13,774 1,469

Other non-current liabilities 32,566 30,906Total non-current liabilities 387,652 346,426

Current liabilities

Account payables 106,547 122,147

Short-term financing 131,994 142,704

Share of current financing 31,478 22,926

Current financial liabilities 10,718 5,348

Tax liabilities 20,197 32,113

Other current liabilities 27,993 31,028

Total current liabilities 328,927 356,266

Total liabilities 1,071,995 1,047,532

8/3/2019 Acegas Interim Report Q3 2010

http://slidepdf.com/reader/full/acegas-interim-report-q3-2010 8/8

Acegas-Aps SpaVia del Teatro, 5

34121 TriesteCap.Soc.283.690.762.80 i.v.

Codice Fiscale e iscrizione n. 00930530324R.E.A.n. 111554 - CC.I.A.A. Trieste

P.IVA 00930530324www.acegas-aps.it

Investor Relations: Federico Trevisan Media Relations: Maurizio Stefani [email protected] [email protected]: +39-040-7793.368 [email protected]: +39-040-7793.233 Office PD: +39-049-8280.551

Office TS: +39-040-7793.534Fax PD: +39-049-8280.554Fax TS: +39-040-7793.295

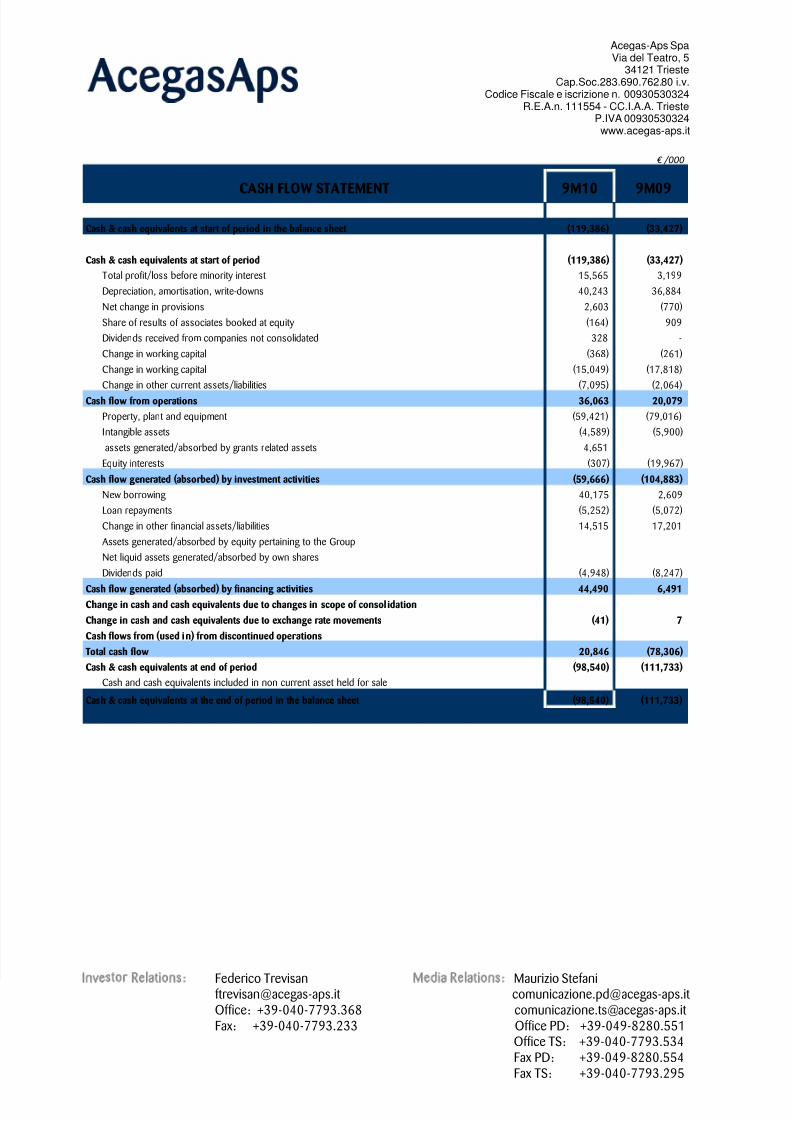

€ /000

CASH FLOW STATEMENT 9M10 9M09Cash & cash equivalents at start of period in the balance sheet (119,386) (33,427)

Cash & cash equivalents at start of period (119,386) (33,427)Total profit/loss before minority interest 15,565 3,199Depreciation, amortisation, write-downs 40,243 36,884Net change in provisions 2,603 (770)Share of results of associates booked at equity (164) 909Dividends received from companies not consolidated 328 -Change in working capital (368) (261)Change in working capital (15,049) (17,818)Change in other current assets/liabilities (7,095) (2,064)

Cash flow from operations 36,063 20,079Property, plant and equipment (59,421) (79,016)Intangible assets (4,589) (5,900)assets generated/absorbed by grants related assets 4,651Equity interests (307) (19,967)

Cash flow generated (absorbed) by investment activities (59,666) (104,883)New borrowing 40,175 2,609Loan repayments (5,252) (5,072)Change in other financial assets/liabilities 14,515 17,201Assets generated/absorbed by equity pertaining to the GroupNet liquid assets generated/absorbed by own sharesDividends paid (4,948) (8,247)

Cash flow generated (absorbed) by financing activities 44,490 6,491Change in cash and cash equivalents due to changes in scope of consolidationChange in cash and cash equivalents due to exchange rate movements (41) 7Cash flows from (used in) from discontinued operationsTotal cash flow 20,846 (78,306)Cash & cash equivalents at end of period (98,540) (111,733)

Cash and cash equivalents included in non current asset held for saleCash & cash equivalents at the end of period in the balance sheet (98,540) (111,733)