accounting - holy cross high school – holy cross online

TRANSCRIPT

Directorate: Curriculum FET

ACCOUNTING

Teacher Training Companies

Module 1

Accounting Companies: Module 1

2

SECTION A: COMPANIES

Activity A.1

CONCEPTS AND ACCOUNTING EQUATION (70 marks; 45 minutes)

You are provided with information relating to Family Ltd in respect of the financial year ended 28 February 2015. The company has an authorised share capital of 4 000 000 ordinary shares.

At the start of the financial year the following balances, amongst others, appeared in the General Ledger: Ordinary share capital R8 000 000 (2 000 000 shares) Retained income R380 000 SARS (Income tax) R62 000 (Dr) Shareholders for dividends R440 000

REQUIRED:

A.1.1 Briefly explain the following concepts: Limited Liability Separation of ownership and control (4)

A.1.2 Analyse the transactions below according to the example provided. The bank account is favourable at all times. (66)

Example: Bought merchandise on credit from Stock Wholesalers, R2 000.

No. General ledger

Amount Effect on accounting equation

Account debit Account credit Assets Equity Liabilities

Eg. Trading stock Creditors’ control R2 000 + 0 +

Transactions: 1. On 4 March 2014, the company received a refund in respect of tax overpaid in respect of the

previous financial year.

2. On 15 March 2014, the shareholders were paid for the final dividends that were declared at the end of the previous financial year.

3. On 31 August 2014, interim dividends of 20 cents per share were paid in respect of this financial year.

4. On 1 September 2014, 500 000 new shares were issued at a price of R6,50 per share.

5. Two provisional tax payments of R480 000 were made during the year.

6. This company has three directors. According to her contract, the CEO is entitled to directors fees of R100 000 per month. The other two directors are entitled to R60 000 per month each. The fees for February 2015 are still to be paid.

7. On 31 December 2014 the directors decided to buy back 25 000 shares from a dissatisfied shareholder at a price of R3,00 above the average share price.

8. Final dividends of 45 cents per share were declared on 28 February 2015.

9. Net profit before tax amounted to R2 953 125. The income tax rate is 32% of the net profit.

Accounting Companies: Module 1

3

Activity A.2 Use the information to prepare the following accounts in the General ledger of Siyanda Ltd for the accounting period ended 30 September 2015.

Ordinary share capital

Retained income

SARS (Income tax)

Shareholders for dividends

Income tax

Ordinary share dividends

Appropriation account

INFORMATION: 1 Oct 2014 The following balances appeared in the ledger:

Ordinary share capital (1 600 000 shares) R6 400 000 Retained income 1 280 000 SARS (Income tax) 22 000 (Credit) Shareholders for dividends 280 000

1 Oct 2014 The company issued a further 900 000 ordinary shares at R6,00 each. The proceeds were received and duly deposited in the current account.

25 Oct 2014 The shareholders and SARS were paid the amounts due to them.

30 March 2015 The company paid provisional tax of R460 000 and interim dividends of 30 cents per share. All existing shareholders were eligible to receive dividends.

30 Sep 2015 At the end of the accounting period, the company made a second provisional tax payment of R360 000 and the directors declared a final dividends of 44 cents per share. This was applicable to all shareholders.

30 Sep 2015 The directors decided to buy back 200 000 shares from a shareholder at R5,60 per share. A cheque was issued to him.

30 Sep 2015 The net income before tax for the year ended 30 September 2015 was calculated at R2 600 000. Income tax is calculated at 30% of the net profit before tax.

Accounting Companies: Module 1

4

Activity A.3 (Exemplar: Question 6) INCOME STATEMENT, FIXED ASSETS AND STOCK (60 marks; 35 minutes)

A.3.1 KLOOF COMPUTERS (PTY) LTD

You are provided with information relating to Kloof Computers (Pty) Ltd for the year ended 30 June 2015.

REQUIRED:

A.3.1.1 Refer to Additional Information 5. Calculate the profit/loss on the disposal of the Office Computer sold on 31 March 2015. (6)

A.3.1.2 Refer to Additional Information 6. Calculate the value of stock on hand of: Hypa Computers, according to the Specific Identification method

ABX Printers, according to the FIFO method

Silvo Printing paper, according to the Weighted Average method.

(3) (5) (5)

A.3.1.3 Prepare the Income Statement for the year ended 30 June 2015. (32)

INFORMATION:

(a) Items extracted from the pre-adjustment Trial Balance on 30 June 2015:

Balance Sheet accounts section Debit Credit

Land & buildings 930 000

Equipment 510 100

Accumulated depreciation on equipment 231 000

Trading stock 281 000

Loan from Highway Lenders (13% p.a.) 300 000

SARS (Provisional tax) 194 000

Debtors control 32 000

Provision for bad debts 2 000

Nominal accounts section

Sales 3 700 000

Cost of sales 2 100 000

Staff costs (salaries, wages & commission) 180 000

Directors’ fees 120 000

Commission income 36 000

Interest on loan 29 000

Sundry expenses (including packing materials) 45 000

Asset disposal 7 000

(b) Adjustments and additional information:

1. Commission income of R2 350 is owed to the business.

2. Packing materials of R1 700 are on hand at the end of the year. Packing materials are included in Sundry expenses.

3. One of the two directors has been paid his fees for 6 months. The fees were increased by 10% half-way through the financial year. Provide for fees owing. Both directors earn the same annual fees.

Accounting Companies: Module 1

5

4. Interest at 13% p.a. is owed on the loan. This interest is not capitalised. The loan was taken out several years ago. A payment of R100 000 was made on 31 December 2014. This has been properly recorded.

5. Equipment comprises:

Cost on 30 June 2015

Accumulated depreciation

on 1 July 2014

Depreciation rate

General equipment 418 000 183 000

20% on diminishing balance method

Office computers 92 100 48 000 33⅓% on cost

R 510 100 R231 000

Note: One of the office computers was sold on 31 March 2015. The selling price was credited to the Asset Disposal account but no other entry has been made. The cost price of this computer was R18 600 and the accumulated depreciation at the beginning of the year was R9 400.

Depreciation is to be written off at the rates reflected above.

6. The business uses the perpetual inventory system. Stock records show:

Item Valuation method Stock on hand on 30 June 2015

Value on 30 June 2015

Hypa Laptops Specific identification: R10 500 each

20 computers ?

ABX printers FIFO 46 printers ?

Silvo Printing paper

Weighted average 600 reams ?

Note : Two of the Hypa Laptops included in the stock figures above were donated to Bonlo Primary School and Bonlo High School. No entry has been made for these donations.

The following information relates to trading stock of printers and paper:

ABX printers Silvo Printing paper

Quantity Price Total Quantity Price Total

Opening stock

20 R700 R14 000 1 200 R33 R39 600

PURCHASES 204 R153 040 5 400 R206 800

Aug 2014 100 R730 R73 000 1 600 R40 R64 000

Jan 2015 70 R750 R52 500 2 000 R30 R60 000

May 2015 34 R810 R27 540 1 800 R46 R82 800

SUBTOTAL 224 R167 040 6 600 R246 400

Sales 178 R1 500 R267 000 6 000 R65 R390 000

Closing stock

46 ? 600 ?

7. The income tax assessment for the year reflected that the business owed SARS an amount of R37 000 on 30 June 2015.

Accounting Companies: Module 1

6

A.3.2 PROBLEM-SOLVING

To try and increase their sales of laptops, the directors of Kloof Computers (Pty) Ltd decided to employ three newly qualified salespersons on a trial period for one month. These salespersons would not be restricted to working at the shop premises. They were employed to visit potential customers who might be interested in the laptops and printers. The salespersons would each be paid a:

fixed basic monthly salary of R7 000

10% commission on sales made by them

travel allowance of R2,00 per kilometres travelled in their personal cars. The business normally makes a gross profit of R6 000 per laptop (cost price R10 500, selling price R16 500). The salespersons are allowed to offer a maximum trade discount of R500 per laptop to help them secure a sale if necessary. At the end of the one month trial period, you are provided with the figures below.

REQUIRED:

Explain one problem relating to each salesperson. Provide figures to support your explanations.

What advice would you offer the directors in respect of the plan to employ these salespersons?

(6)

(3)

INFORMATION:

Name of salesperson: Gugu Manny Jim

Number of laptops drawn from stock at beginning of month

20 20 20

Number of laptops sold for cash 9 16 11

Number of laptops returned to stock at end of month

11 4 8

Discounts allowed to customers R0 R8 000 R5 000

Cash from sales deposited by each salesperson into the bank account

R148 500 R207 000 R176 500

Gross profit earned before discounts and other expenses

R54 000 R96 000 R66 000

Basic salary R7 000 R7 000 R7 000

Commission paid to each salesperson R14 850 R25 600 R17 650

Travel allowance claimed (R2,00 per km) R3 000 R1 000 R1 000

60

Accounting Companies: Module 1

7

Activity A.4 (Adapted from November 2013: Question 3) COMPANY FINANCIAL STATEMENTS AND AUDIT REPORT (75 marks; 45 minutes) A.4.1 Give ONE word/term for each of the following descriptions by choosing a

word/term from the list below. Write only the word/term next to the question number in the ANSWER BOOK.

current asset; non-current asset; income; expense; current liability; non-current liability

A.4.1.1 Profit on the sale of an asset is a/an ...

A.4.1.2 The portion of a loan that will have to be repaid within a year is a/an ...

A.4.1.3 Consumable stores on hand are a/an ...

A.4.1.4 Interest on a bank overdraft is a/an ... (4) A.4.2 SELATI LIMITED You are provided with information for the financial year ended 30 June 2015. REQUIRED:

A.4.2.1 Complete the Income Statement. (54)

A.4.2.2 Prepare the note for Retained Income. (11) INFORMATION:

EXTRACT FROM THE TRIAL BALANCE ON 30 JUNE 2015:

Balance Sheet Accounts Section R

Ordinary share capital 5 605 000

Retained income (1 July 2014) 735 000

Trading stock 1 534 000

Debtors' control 521 300

Provision for bad debts 22 000

Creditors' control 471 800

Loan: Puma Bank 630 000

Bank (Dr) 129 400

SARS: Income tax (Dr) 260 000

Pension fund 15 800

Unemployment Insurance Fund (UIF) 2 300

Fixed deposit: Sharp Bank 450 000

Accounting Companies: Module 1

8

Nominal Accounts Section R

Sales ?

Cost of sales 8 200 000

Salaries and wages 788 000

Directors' fees 1 840 000

Audit fees 88 000

Employer's contribution (Pension and UIF) 81 000

Bank charges 31 000

Sundry expenses 89 730

Bad debts 12 100

Rent income 69 160

Interest on fixed deposit 27 000

Repairs and maintenance 125 600

Packing material 43 900

Ordinary share dividends (interim) ?

ADJUSTMENTS AND ADDITIONAL INFORMATION: 1. The auditors are owed a further R7 500. 2. Goods are sold at a mark-up of 60% on cost price. The company held discounted

cash sales during the year to clear excess stock. The total of trade discount given to customers was R702 000.

3. Packing material to the value of R41 000 was used during the year ended

30 June 2015. 4. Interest on the bank overdraft, R2 800, is included in the bank charges. 5. No entries have been made for stock stolen at the beginning of June 2015. The

insurance company has informed Selati Ltd that they have transferred R32 000 into the business' bank account in respect of the insurance claim. Selati Ltd bears 20% of any stock loss.

6. A physical stocktaking on 30 June 2015 reflected that stock to the value of

R1 475 500 was on hand. 7. An amount of R1 700 received from M Mpoani had been credited to the

Debtors' Control Account in June 2015. The account of M Mpoani was written off as a bad debt during May 2015. The provision for bad debts must be adjusted to 4% of outstanding debtors.

Adjustment 8 on next page.

Accounting Companies: Module 1

9

8. One employee was omitted from the Salaries Journal for June 2015. His salary details are:

Deductions Employer's Contribution Net salary

2 020 1 610 4 980

9. EZ Builders was paid R105 000 for the construction of a storeroom (R80 000)

and repairs to paving (R25 000). The entire amount was debited to Land and Buildings in error.

10. The loan statement from Puma Bank on 30 June 2015 reflected:

Balance at beginning of financial year R1 470 000

Repayments during the year 840 000

Interest capitalised ?

Balance at end of financial year 750 000

11. Rent income for July 2015 has already been received. The monthly rent was

increased by 10% on 1 May 2015. 12. Depreciation is the missing figure in the Income Statement. 13. Net profit and tax:

After taking all adjustments into account, the correct net profit after tax is R588 000.

The income tax rate is 30% of net income before tax. 14. Shares:

The ordinary share capital on 1 July 2014 consisted of 1 500 000 ordinary shares which were issued at R2,60 per share.

500 000 shares were issued on 1 January 2015 at R4,00 per share. This was properly recorded.

On 28 February 2015 the shareholders repurchased 100 000 shares from the estate of a deceased shareholder at a price of R4,50 per share. This has not yet been recorded.

15. Dividends:

Interim dividends of 14 cents per share were declared and paid on 31 December 2014.

Final dividends of 10 cents per share were declared on 30 June 2015.

Accounting Companies: Module 1

10

A.4.3 AUDIT REPORT

EXTRACT FROM THE REPORT OF THE INDEPENDENT AUDITORS We have audited the annual financial statements of Selati Ltd for the year ended 30 June 2015. These financial statements are the responsibility of the company's directors. Basis for Disclaimer of Opinion During the course of our audit we established that bonuses paid to directors amounting to R1,5m had not been authorised by the Remuneration Committee. Furthermore, no documentation is available for sundry expenses of R75 000. Audit Opinion Because of the significance of the matter described above, we have not been able to obtain sufficient audit evidence to provide a basis for an audit opinion. Accordingly, we do not express an opinion on the financial statements of Selati Ltd for the year ended 30 June 2015. Morley and Associates, Chartered Accountants (SA)

REQUIRED: As a shareholder, why would you be concerned about this audit report? Explain.

State THREE points. (6)

75

Accounting Companies: Module 1

11

Activity A.5 (Source: New Era Study Guide) (45 marks; 25 minutes) You are provided with extracts from the financial statements of Slimtreads Ltd at the end of February 2015, together with comparative figures for 2014 and some additional information. Extracts from the Income Statement of Slimtreads Ltd for the year ended 28 February 2015

2015

Sales 12 105 000

Depreciation 453 000

Interest on loan 252 000

Net profit before tax ?

Income tax 393 000

Net profit after tax 917 000

Extracts from the Balance Sheet of Slimtreads Ltd as at 28 February 2015

2015 2014

ASSETS 2 764 500 2 374 000

Non-current assets 2 631 200 2 274 000

Fixed assets 133 300 100 000

Fixed deposit

Current assets 2 548 000 1 088 000

Inventories 254 000 272 000

Trade and other receivables (see notes) 1 638 000 770 000

Cash and cash equivalents 656 000 46 000

TOTAL ASSETS 5 312 500 3 462 000

SHAREHOLDERS’ EQUITY AND LIABILITIES

Shareholders’ equity (c) 1 652 000

Ordinary share capital (see notes) (d) 1 378 000

Retained income (e) 273 500

Non-current liabilities 1 800 000 1 000 000

Loan from North West Bank (18% p.a.) 1 800 000 1 000 000

Current liabilities 810 000

Trade and other payables (see notes) (f) 810 000

TOTAL EQUITY AND LIABILITIES (g) 3 462 000

Accounting Companies: Module 1

12

Extracts from the notes to the financial statements of Slimtreads Ltd

2015 2014

Ordinary share capital

675 000 shares in issue at beginning of year 1 378 500 1 378 500

375 000 new shares issued on 1 March 2014 900 000 0

40 000 shares repurchased on 28 February 2015 (a) 0

? shares in issue at end of year (b) 1 378 500

2015 2014

Trade and other receivables

Trade debtors 1 592000 770 000

SARS (Income tax) 46 000 0

1 638 000 770 000

2015 2014

Trade and other payables

Trade creditors ? 692 500

SARS (Income tax) 0 95 000

Shareholders for dividends 157 500 22 500

? 810 000

ADDITIONAL INFORMATION

1. The current ratio on 28 February 2015 was 4 : 1.

2. During the year a vehicle was bought for R970 000 and old equipment was sold at book value.

3. The extra shares were sold on 1 March 2014.

4. On 1 March 2014, 375 000 new shares were issued.

5. On 28 February 2015, 40 000 shares were repurchased at R2,50 each. The necessary payment was made.

REQUIRED:

A.5.1 Balance sheet and notes:

(i) Complete the Retained income note to the Balance Sheet on 28 February 2015. (10) (ii) Calculate the figures denoted by (a) and (b) in the Note for Ordinary Share

Capital. (4) (iii) Calculate the figures denoted by (c) to (g) in the Balance Sheet. (6)

A.5.2 Complete the following notes to the Cash Flow Statement on 28 February 2015.

(i) Reconciliation between profit before tax and cash generated from operations. (16) (ii) The amount paid for income tax. (4) (iii) Cash proceeds from the sale of equipment (5)

45

Accounting Companies: Module 1

13

Activity A.6 (Taken from March 2015, Question 3) (75 marks; 45 minutes)

A.6.1 Choose a description from COLUMN B that matches a term/concept in COLUMN A. Write only the letter (A–E) next to the question number (A.6.1.1–A.6.1.5) in the ANSWER BOOK.

COLUMN A COLUMN B

A.6.1.1

A.6.1.2

A.6.1.3

A.6.1.4

A.6.1.5

Companies and Intellectual Property Commission

Director

IFRS

Limited liability

Independent auditor

A

B

C

D E

guidelines for the preparation of financial statements to ensure consistency

responsible for maintaining records and control of new and existing companies

the business is responsible for its own debts and the liability of owners is limited to the amounts they invested

responsible for expressing an opinion on the financial statements of a company an elected member of the board responsible for running the business and implementing policy

(5)

A.6.2 Bargain Traders Ltd is a public company listed on the JSE. The business has an authorised share capital of 1 000 000 ordinary shares.

REQUIRED:

A.6.2.1 Prepare the following notes to the Balance Sheet:

(a) Ordinary share capital (7) (b) Retained income (10) (c) Trade and other receivables (10)

A.6.2.2 Complete the Balance Sheet on 30 June 2015. Where notes are not required, show ALL workings in brackets to earn part marks. (28)

A.6.2.3 Calculate the net asset value (NAV) per share on 30 June 2015. (3)

A.6.2.4 Comment on the price offered for the shares that were repurchased. Quote relevant financial indicators (actual figures/ratios/ percentages) to support your comment. (3)

Accounting Companies: Module 1

14

A.6.2.5 The CEO (chief executive officer), Kyle Mason, has convinced the company to repurchase a further 90 000 shares from other shareholders during the next financial year on 31 August 2015. Kyle Mason currently owns 315 000 shares which represents 45% of the issued shares.

Calculate Kyle Mason's percentage shareholding after the proposed share buy-back on 31 August 2015. (3)

As a shareholder, explain your concern regarding the proposed repurchase of shares. Provide TWO questions you would ask the directors at the annual general meeting. (6)

INFORMATION:

A. Issued share capital comprised 850 000 ordinary shares on 1 July 2014.

B. The following was extracted from the books on 30 June 2015:

Fixed/Tangible assets (carrying value) ?

Fixed deposit: Swan Bank 120 000

Ordinary share capital (850 000 shares) 5 737 500

Retained income (1 July 2014) 181 900

Bank 351 200

Loan: Drake Bank 295 000

Trading stock 355 700

Net trade debtors (after deducting provision for bad debts dated 1 July 2014) 118 370

Creditors' control 197 000

SARS: Income tax (provisional payments) 320 900

Dividends on ordinary shares (interim dividends) 315 000

C. No entries have been made for the repurchase of shares. On 1 October 2014 the business bought back 150 000 ordinary shares from certain shareholders. Although the market price of the shares was R9,25, they accepted R7,40 for each share. These shareholders were not entitled to interim dividends.

D. The following adjustments have not yet been taken into account: Insurance included an annual policy of R29 832 paid for on

1 December 2014.

The provision for bad debts must be increased by R6 100.

Unused packing material was counted to be R9 500. A debtor with a credit balance of R11 700 is to be transferred to the

Creditors' Ledger.

The bank reconciliation reflected a post-dated cheque for R33 000 dated 31 August 2015.

The statement received from Drake Bank in respect of the loan reflected interest capitalised of R31 200. Monthly repayments are R10 800 including interest. These repayments will end in 2018.

On 30 June 2015, a final dividend of 40 cents per share was declared.

E. Net profit after tax, after taking into account the adjustments above, was calculated as R813 600. The income tax rate is 28% of net profit before tax.

75

Accounting Companies: Module 1

15

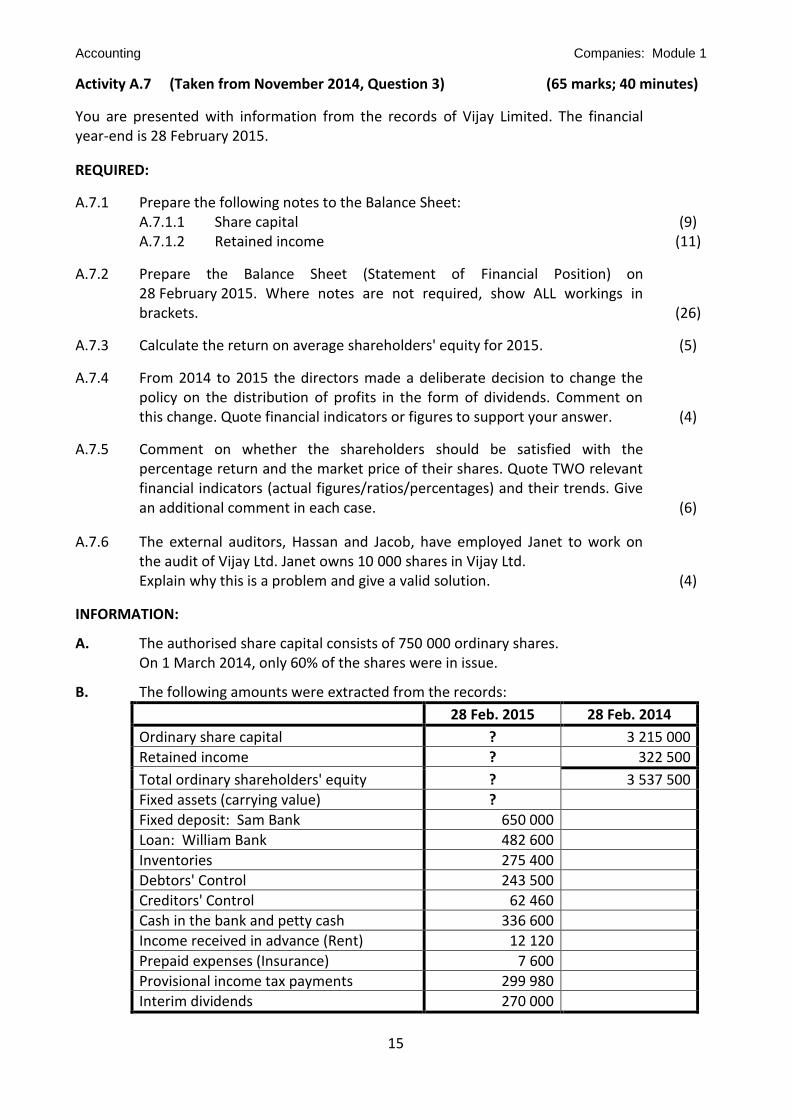

Activity A.7 (Taken from November 2014, Question 3) (65 marks; 40 minutes)

You are presented with information from the records of Vijay Limited. The financial year-end is 28 February 2015.

REQUIRED:

A.7.1 Prepare the following notes to the Balance Sheet: A.7.1.1 Share capital (9) A.7.1.2 Retained income (11)

A.7.2 Prepare the Balance Sheet (Statement of Financial Position) on 28 February 2015. Where notes are not required, show ALL workings in brackets. (26)

A.7.3 Calculate the return on average shareholders' equity for 2015. (5)

A.7.4 From 2014 to 2015 the directors made a deliberate decision to change the policy on the distribution of profits in the form of dividends. Comment on this change. Quote financial indicators or figures to support your answer. (4)

A.7.5 Comment on whether the shareholders should be satisfied with the percentage return and the market price of their shares. Quote TWO relevant financial indicators (actual figures/ratios/percentages) and their trends. Give an additional comment in each case. (6)

A.7.6 The external auditors, Hassan and Jacob, have employed Janet to work on the audit of Vijay Ltd. Janet owns 10 000 shares in Vijay Ltd.

Explain why this is a problem and give a valid solution. (4)

INFORMATION:

A. The authorised share capital consists of 750 000 ordinary shares. On 1 March 2014, only 60% of the shares were in issue.

B. The following amounts were extracted from the records:

28 Feb. 2015 28 Feb. 2014

Ordinary share capital ? 3 215 000

Retained income ? 322 500

Total ordinary shareholders' equity ? 3 537 500

Fixed assets (carrying value) ?

Fixed deposit: Sam Bank 650 000

Loan: William Bank 482 600

Inventories 275 400

Debtors' Control 243 500

Creditors' Control 62 460

Cash in the bank and petty cash 336 600

Income received in advance (Rent) 12 120

Prepaid expenses (Insurance) 7 600

Provisional income tax payments 299 980

Interim dividends 270 000

Accounting Companies: Module 1

16

C. On 1 November 2014, the company issued a further 80 000 shares at R9,50 per share. D. On 28 February 2015, the directors decided to repurchase 75 000 ordinary shares

from the estate of a shareholder who had died. This shareholder had originally purchased his shares on the JSE at various times and at different prices. A repurchase price of R10,40 was accepted as being a fair price.

E. On 27 February 2015, a final dividend of 40 cents per share was declared.

All shares, including the new shares issued and repurchased, qualify for final dividends.

F. The loan statement from William Bank received on 28 February 2015 reflected

interest capitalised at R81 400. This was not recorded in the books. The business expects to settle 20% of the outstanding balance in the next financial year.

G. After all the above adjustments were taken into account the net profit before tax was

calculated to be R1 161 000. The income tax is calculated at 30% of net income before tax.

H. Financial indicators on 28 February: 2015 2014

Earnings per share (EPS) 170 cents 82 cents

Dividends per share (DPS) 100 cents 82 cents

Net asset value (NAV) 846 cents 786 cents

Return on shareholders' equity (ROSHE) ? 18,3%

I. Additional information: 2015 2014

Market price of Vijay Ltd shares on JSE 1 032 cents 1 060 cents

Interest rate on alternative investments 9% 9%

65