accelerated financial closing with sap

TRANSCRIPT

Bonn � Boston

James Fisher, Elizabeth Milne, and Birgit Starmanns

Accelerated Financial Closing with SAP®

446.book Seite 3 Donnerstag, 3. Oktober 2013 7:31 19

Contents at a Glance

1 Introduction to the Financial Close .......................................... 25

2 Creating an Action Plan for Improving Your Financial Close .... 41

3 Information Management ......................................................... 61

4 The General Ledger and Subledger Close ................................. 77

5 The Financial Close in Controlling ............................................ 103

6 Entity Close Management ........................................................ 131

7 Enhanced Internal Controls for Better Compliance .................. 141

8 Intercompany Reconciliation .................................................... 157

9 Financial Consolidation ............................................................ 169

10 Disclosure Management and XBRL Filings ............................... 213

11 Financial Reporting ................................................................... 245

12 The Future of Finance and Its Impact on the Financial Close .................................................................... 259

13 Conclusion ................................................................................ 277

446.book Seite 5 Donnerstag, 3. Oktober 2013 7:31 19

7

Contents

Foreword ......................................................................................................... 15Preface ............................................................................................................. 19Acknowledgments ............................................................................................ 23

1 Introduction to the Financial Close ........................................... 25

1.1 The Business Case for a Fast High-Quality Close .............................. 261.1.1 Internal and External Stakeholders ..................................... 271.1.2 Regulatory Drivers for the Accelerated Financial Close ....... 271.1.3 Benefits of the Accelerated Financial Close ......................... 29

1.2 Components of the Financial Close ................................................. 321.3 How Fast Is Fast? ............................................................................ 331.4 Barriers to a Fast, High-Quality Close Process ................................. 36

1.4.1 Compliance-Related Pressures ............................................ 371.4.2 Data Quality/Collection Errors ............................................ 381.4.3 Intercompany Reconciliation .............................................. 381.4.4 Poor Performance from Consolidation Applications ............ 381.4.5 Lack of Process Automation ............................................... 391.4.6 Weak Audit Trails .............................................................. 39

1.5 Summary ........................................................................................ 40

2 Creating an Action Plan for Improving Your Financial Close ..... 41

2.1 Vision, Benchmarking, and Sponsorship .......................................... 422.1.1 Perform “As-Is” Review ...................................................... 432.1.2 Define Vision and Benefits ................................................. 442.1.3 Sponsorship ....................................................................... 46

2.2 Quick Wins ..................................................................................... 482.2.1 Creating a Close Scorecard ................................................. 502.2.2 Peer-to-Peer Intercompany Reconciliation ......................... 512.2.3 Right-First-Time Close ........................................................ 532.2.4 XBRL Publishing ................................................................. 53

2.3 Big Wins ......................................................................................... 542.3.1 Standard Chart of Accounts ................................................ 552.3.2 Common Single Instance of SAP ERP .................................. 55

446.book Seite 7 Donnerstag, 3. Oktober 2013 7:31 19

Contents

8

2.3.3 Reporting and Disclosure Framework ................................. 562.3.4 Corporate and Entity Close ................................................. 56

2.4 Continuous Improvements .............................................................. 572.5 Summary ........................................................................................ 59

3 Information Management .......................................................... 61

3.1 Defining Data and Information ....................................................... 633.2 Master Data Management .............................................................. 64

3.2.1 Management of Financial Master Data in SAP Business Suite ......................................................... 65

3.3 Transactional Data Management .................................................... 673.3.1 Extracting Data from ERP Systems with SAP Rapid Marts ... 673.3.2 SAP Financial Information Management ............................. 68

3.4 Summary ........................................................................................ 75

4 The General Ledger and Subledger Close .................................. 77

4.1 SAP ERP Financials Concepts .......................................................... 774.1.1 The Organizational Hierarchy ............................................. 784.1.2 The Document Principle ..................................................... 794.1.3 Customer Story: Cargojet Income Fund Soars to

New Heights with Greater Financial Visibility ..................... 814.2 The General Ledger Close ............................................................... 83

4.2.1 Posting Periods .................................................................. 834.2.2 Period-End Journal Entries ................................................. 844.2.3 Foreign Currency Valuation ................................................ 854.2.4 The Year-End Close ............................................................ 864.2.5 Customer Story: Continental’s Smooth Transition

with the SAP General Ledger Migration Service ................. 874.3 The Accounts Payable and Accounts Receivable Close .................... 88

4.3.1 Reconciliation of Payables and Receivables Accounts ......... 894.3.2 Valuation of Payables and Receivables Accounts ................ 894.3.3 Collections and Dispute Management ................................ 904.3.4 Travel Management ........................................................... 91

4.4 Asset Accounting Close .................................................................. 914.4.1 Posting Depreciation .......................................................... 914.4.2 Assets Under Construction ................................................. 924.4.3 Year-End ............................................................................ 93

446.book Seite 8 Donnerstag, 3. Oktober 2013 7:31 19

Contents

9

4.5 Inventory Management .................................................................. 944.5.1 GR/IR Reconciliation .......................................................... 954.5.2 Work in Process ................................................................. 954.5.3 Inventory Valuation ........................................................... 964.5.4 Posting Periods .................................................................. 974.5.5 Customer Story: ConAgra Foods Improves Financial

Business Processes with In-Memory Computing ................. 984.6 Reporting ....................................................................................... 100

4.6.1 Customer Story: KazStroyService Group Streamlines and Consolidates Business Processes .................................. 101

4.7 Summary ........................................................................................ 102

5 The Financial Close in Controlling ............................................. 103

5.1 Cost Element Accounting ................................................................ 1055.1.1 Primary Cost Elements ....................................................... 1065.1.2 Secondary Cost Elements ................................................... 1075.1.3 Integration between Operations and Controlling ................ 1085.1.4 Customer Story: Korea Exchange Bank Benefits from

Standardized Business Processes ........................................ 1095.2 Cost Centers ................................................................................... 110

5.2.1 Accruals ............................................................................. 1105.2.2 Basis for Cost Center Allocations ........................................ 1115.2.3 Cost Elements .................................................................... 1115.2.4 Activity Types .................................................................... 1115.2.5 Statistical Key Figures ........................................................ 1125.2.6 Allocations ......................................................................... 1125.2.7 Variances ........................................................................... 113

5.3 Internal Orders ............................................................................... 1155.4 Project Systems .............................................................................. 1165.5 Product Costing .............................................................................. 119

5.5.1 Work in Process ................................................................. 1215.5.2 Variances ........................................................................... 1215.5.3 Customer Story: Qingdao TKS Sealing Industry

Achieves Transparent Reporting ......................................... 1235.5.4 The Material Ledger ........................................................... 124

5.6 Profitability Analysis ....................................................................... 1245.6.1 Customer Story: Promivi, a Leader in Animal Nutrition,

Utilizes SAP HANA and Gains Profitability and Growth Insight ................................................................... 126

446.book Seite 9 Donnerstag, 3. Oktober 2013 7:31 19

Contents

10

5.7 Profit Centers ................................................................................. 1275.8 Year-End Closing ............................................................................ 1285.9 Reconciliation Between the FI and CO Modules ............................. 1295.10 Summary ........................................................................................ 129

6 Entity Close Management .......................................................... 131

6.1 Plan and Prepare the Entity Close ................................................... 1326.2 Execute the Entity Close ................................................................. 1346.3 Customer Story: Dow Chemicals’ Faster, Less Costly Financial

Close Process with SAP Solutions .................................................... 1366.4 Monitor the Entity Close ................................................................ 1376.5 Summary ........................................................................................ 139

7 Enhanced Internal Controls for Better Compliance ................... 141

7.1 Access Risk Management ................................................................ 1447.1.1 Segregation of Duties ......................................................... 1467.1.2 Customer Story: Infosys Treats Governance and

Compliance Strategically with SAP Access Control .............. 1477.2 Identifying Controls across a Business Process ................................. 148

7.2.1 Control Monitoring and Remediation ................................. 1487.2.2 Customer Story: REC Silicon, Inc. Leverages Enhanced

Process Controls ................................................................ 1507.3 Audit Management ........................................................................ 1517.4 GRC Analytics ................................................................................. 1537.5 Summary ........................................................................................ 156

8 Intercompany Reconciliation ..................................................... 157

8.1 Defining Intercompany Reconciliation ............................................ 1578.2 SAP Solutions for Intercompany Reconciliation ............................... 158

8.2.1 One Source System ............................................................ 1598.2.2 Multiple Intercompany Source Systems .............................. 1608.2.3 Leveraging Consolidation Systems for Intercompany

Reconciliation .................................................................... 1618.3 Managing the Intercompany Process .............................................. 161

8.3.1 Traditional Intercompany Reconciliation Process ................ 1618.3.2 Peer-to-Peer Intercompany Reconciliation Process ............. 162

446.book Seite 10 Donnerstag, 3. Oktober 2013 7:31 19

Contents

11

8.4 Faster, Collaborative Intercompany Reconciliation withSAP Intercompany .......................................................................... 1638.4.1 Web-Based, Peer-to-Peer Communication ......................... 1638.4.2 Collaboration, Monitoring, and Approval ........................... 164

8.5 SAP Intercompany Deployment Options ......................................... 1658.5.1 Data Entry and Adjustments in SAP Intercompany ............. 1668.5.2 No Data Entry or Adjustments in SAP Intercompany .......... 166

8.6 Security and Configuration .............................................................. 1678.7 Summary ........................................................................................ 168

9 Financial Consolidation .............................................................. 169

9.1 Data Collection ............................................................................... 1719.1.1 Customer Story: Altron Consolidates Financial Data

to Better Manage Assets and Risk ...................................... 1729.1.2 Loading Data ..................................................................... 1739.1.3 Data Mapping/Central Chart of Accounts ........................... 1749.1.4 Dimensionality: Identifying the Level of Detail to Collect ... 1759.1.5 Data Validation and Control ............................................... 1799.1.6 Collecting Commentary with Data ...................................... 1809.1.7 Workflow and Approval of Data ......................................... 1809.1.8 Periodicity of Data (Collecting Year to Date versus

Periodic) ............................................................................ 1819.1.9 Currency (Local, Transaction, Group) .................................. 182

9.2 Processing Data .............................................................................. 1839.2.1 Customer Story: HMY Group Enables More

Comprehensive and Up-to-Date Reporting with SAP Financial Consolidation ............................................... 184

9.2.2 Managing Organizational Structures ................................... 1859.2.3 Consolidation Adjustments ................................................ 1899.2.4 Intercompany Eliminations ................................................. 1909.2.5 Elimination of Investments ................................................. 1929.2.6 Foreign Currency Conversion and Currency

Translation Adjustments ..................................................... 1929.2.7 Rounding ........................................................................... 1939.2.8 Workflow and Approval of Adjustments ............................. 1949.2.9 Consolidation Versions ....................................................... 194

9.3 Differentiation between Consolidation Solutions ............................ 1969.3.1 Business Suite Solutions ..................................................... 197

446.book Seite 11 Donnerstag, 3. Oktober 2013 7:31 19

Contents

12

9.3.2 SAP Business Planning and Consolidation (BPC) ................. 1999.3.3 Customer Story: Russian Railways Gets On the

Right Track with Planning and Consolidation ..................... 2009.3.4 SAP Financial Consolidation ............................................... 2019.3.5 Customer Story: Bekaert Standardizes Global

Financial Reporting ............................................................ 2039.3.6 Engaging with SAP experts ................................................. 204

9.4 Starter Kits ..................................................................................... 2049.4.1 Customer Story: Bank of Cyprus Group Achieves

Clear Audits with SAP Solutions ......................................... 2079.4.2 SAP Disclosure Management Consolidation Starter Kits ..... 2089.4.3 SAP Financial Close and Disclosure Management

Rapid Deployment Solution (RDS) ..................................... 2109.5 Summary ........................................................................................ 210

10 Disclosure Management and XBRL Filings ................................ 213

10.1 Collect Information from Source Systems ........................................ 21710.1.1 Financial Figures for Disclosure Reports ............................. 21810.1.2 Unstructured Information in Financial Statements .............. 22010.1.3 Customer Story: Metcash Delivers the Goods in

Corporate Governance ....................................................... 22210.2 Manage Financial Statements and Reports ...................................... 224

10.2.1 Tracking the Progress of the Disclosure Process .................. 22410.2.2 Manage Report Documents ............................................... 225

10.3 Collaboration and Workflow ........................................................... 22810.3.1 Role Definitions and Configuration of Workflow ................ 22810.3.2 Document Control ............................................................. 22910.3.3 Workflow and Status Management .................................... 23010.3.4 Approvals .......................................................................... 23210.3.5 Customer Story: GEA Group Produces Audit-Compliant

Financial Statements Faster ................................................ 23310.4 Publish Disclosure Statements and Reports ..................................... 23410.5 Create and File XBRL Statements .................................................... 236

10.5.1 Tagging Data for Filing Financial Statement and Forms ....... 23910.5.2 XBRL Instance Documents ................................................. 24010.5.3 Customer Story: SAP Speeds Up the Last Mile of Financial

Reporting with SAP Disclosure Management ..................... 24110.6 Summary ........................................................................................ 243

446.book Seite 12 Donnerstag, 3. Oktober 2013 7:31 19

Contents

13

11 Financial Reporting .................................................................... 245

11.1 Reporting Requirements ................................................................. 24511.1.1 Balance sheet, P&L, and Cash Flow Reporting .................... 24611.1.2 Management versus Statutory Reporting ............................ 24811.1.3 Variance Reporting ............................................................ 24911.1.4 Periodic Comparison .......................................................... 24911.1.5 Budget, Plan, and Forecast ................................................. 25011.1.6 Versioning and What If Statements .................................... 25011.1.7 Drill Down versus Drill Though .......................................... 252

11.2 Reporting Delivery Methods ........................................................... 25411.2.1 Business Intelligence .......................................................... 25511.2.2 SAP Crystal Reports ............................................................ 25511.2.3 SAP BusinessObjects Dashboards ....................................... 25611.2.4 SAP BusinessObjects Web Intelligence ............................... 25611.2.5 SAP BusinessObjects Analysis ............................................. 25611.2.6 SAP BusinessObjects Explorer ............................................ 25711.2.7 SAP BusinessObjects BI platform ........................................ 25711.2.8 Mobility ............................................................................. 257

11.3 Summary ........................................................................................ 258

12 The Future of Finance and Its Impact on the Financial Close ... 259

12.1 Economic Environment and the Role of Finance ............................. 25912.2 Financial Operations ....................................................................... 262

12.2.1 SAP Business Suite Powered by SAP HANA ........................ 26412.2.2 Embedded Analytics .......................................................... 264

12.3 Managing Stakeholder Expectations ............................................... 26512.3.1 In-Memory Powered Planning, Budgeting, and

Forecasting ........................................................................ 26912.3.2 Predictive Analytics and Data Discovery ............................. 26912.3.3 Mobilizing Finance ............................................................. 270

12.4 Ensuring Regulatory Compliance ..................................................... 27112.4.1 Taxation ............................................................................. 27212.4.2 Integrated Reporting .......................................................... 273

12.5 Summary ........................................................................................ 275

13 Conclusion .................................................................................. 277

446.book Seite 13 Donnerstag, 3. Oktober 2013 7:31 19

Contents

14

Appendices ....................................................................................... 281

A Glossary .................................................................................................... 283B References ................................................................................................ 287C The Authors .............................................................................................. 289

Index ................................................................................................................ 291

446.book Seite 14 Donnerstag, 3. Oktober 2013 7:31 19

19

Preface

Accelerated Financial Closing with SAP spans SAP’s portfolio of finance and analyt-ics solutions, including applications from its market-leading enterprise perfor-mance management, business intelligence, and governance risk and complianceportfolios. It aims to explain how these solutions can be deployed alongside exist-ing SAP ERP Financials implementations and break down traditional barriers to afast, high-quality financial close process. This title provides a comprehensiveguide for finance and controlling professionals seeking to understand how theirexisting and future investments in SAP solutions can be leveraged to help theirorganizations run a best-in-class finance close process.

Target Audience

This book intends to address two key audiences in today’s enterprise. First,finance executives will benefit from an up-to-date overview of the complete end-to-end financial close process. Leveraging industry best practices and real casestudy examples, we will do the following:

� Provide insight into the business drivers for and the benefits of a fast, high-quality financial close process.

� Give an overview of the technology landscape that is now available to supportit.

� Examine the impact of the latest changes to regulatory reporting and the per-formance management process.

� Demonstrate how industry peers have improved their financial close pro-cesses, reduced risks, and enabled finance to become a strategic partner to thebusiness.

Second, we will address the needs of business process owners and program direc-tors charged with running and optimizing the financial close process within theirorganization. For this reader, this book will do the following:

446.book Seite 19 Donnerstag, 3. Oktober 2013 7:31 19

Preface

20

� Set out a clear action plan for how corporate finance teams can approach thechallenge of improving the financial close process.

� Demonstrate how a new generation of solutions from SAP can systematicallybreak down barriers to a fast, efficient financial close process.

� Explain how by converging the previously disparate disciplines of businessintelligence; governance, risk, and compliance; and enterprise performancemanagement on a solid foundation of SAP ERP, finance teams can seek toimprove service quality and reduce costs.

The chapters in this book break out the key components of the financial close anddiscuss how finance solutions from SAP can be leveraged alongside process bestpractices to achieve immediate yet sustainable improvements to the financialclose.

Chapter Overview

The chapters in this book are designed to systematically help you with actionablesteps to improve the financial close process in your organization. The first chap-ters provide an overview of the key concepts surrounding a fast, accurate closeprocess, including an understanding of the drivers for an improved process andthe most commonly cited barriers to it. We examine the ways in which you canbuild a business case for future investment and outline a simple four-step actionplan that can be used to design a fast close initiative from the first initial bench-marking processes through to ongoing improvements.

The subsequent chapters then dissect the most important parts of the financialclose process and examine in details how the process should function as a practiceand how technology from SAP can be used to help improve the process. Real-lifeexamples help to illustrate how SAP customers are already benefiting from imple-mentations of these technologies.

The book closes with a look to the future, highlighting key developments financeprofessionals need to be aware to drive long-term sustainable value from thefinancial close process and how this positions finance professionals to better part-ner with the business, driving not just sound stewardship but entrepreneurship,positioning finance as a true strategic partner to the business.

446.book Seite 20 Donnerstag, 3. Oktober 2013 7:31 19

Preface

21

Summary

Ultimately, this book is designed as a practical guide that enables finance and con-trolling professionals to optimize their financial close process using SAP solu-tions. Today this portfolio is broader and more extensive than it has ever beenand by deploying an end-to-end solution for your financial close, not only willyou achieve a faster more accurate close, but you will provide the basis forbroader finance transformation whereby the cost of finance is reduced and thefinance function is positioned as a driver of strategic change across the organiza-tion.

446.book Seite 21 Donnerstag, 3. Oktober 2013 7:31 19

41

For all transformational projects, it’s critically important that you define a project plan that helps you set out your objectives, demonstrate success, manage change, and ultimately drive a long-term business outcome. This chapter examines the need for such an approach and proposes a structure readers can implement as part of their own fast-close project.

2 Creating an Action Plan for Improving Your Financial Close

Understanding the drivers and barriers for a faster close process is important, butbefore you can start your project, you need to plan for it effectively. A financialclose project, like any other corporate initiative, requires a structured approachwith a methodology that’s supported by people, process, and technology; is man-ageable; and has clear but realistic objectives. A full financial close project canand, in most cases, must extend beyond corporate-centric processes and func-tions and therefore involve a broad community that adds complexity to the pro-cess.

That being said, the project doesn’t necessarily have to result in a major changeprogram and—provided you structure your approach, deliver the appropriateand sponsored resources, and manage the project—it’s possible to make signifi-cant gains relatively easily.

As a result and based on our experiences working with our partners and custom-ers, we advise that you create an action plan for your project that breaks downthe transformation process into meaningful but manageable steps. There are anumber of ways to create and build such a plan, and many consultancies andindeed SAP partners will be able to offer their own approach. Typically, however,they all focus around four principal steps. For the purposes of this book, we havecreated our own action plan, which represents these market best practices andspans the following four steps. We will go on to explain each of these in moredetail in this chapter.

446.book Seite 41 Donnerstag, 3. Oktober 2013 7:31 19

Creating an Action Plan for Improving Your Financial Close

42

2

1. Establish vision, benchmarking, and sponsorship.

2. Implement quick wins.

3. Identify and deliver big wins.

4. Establish a framework for continuous improvements.

The aim is very simple: to create a project plan that can be delivered based onyour existing or budgeted resources and that guides you through the process toset out your objectives, demonstrate success, manage change, and ultimatelydrive to a long-term business outcome.

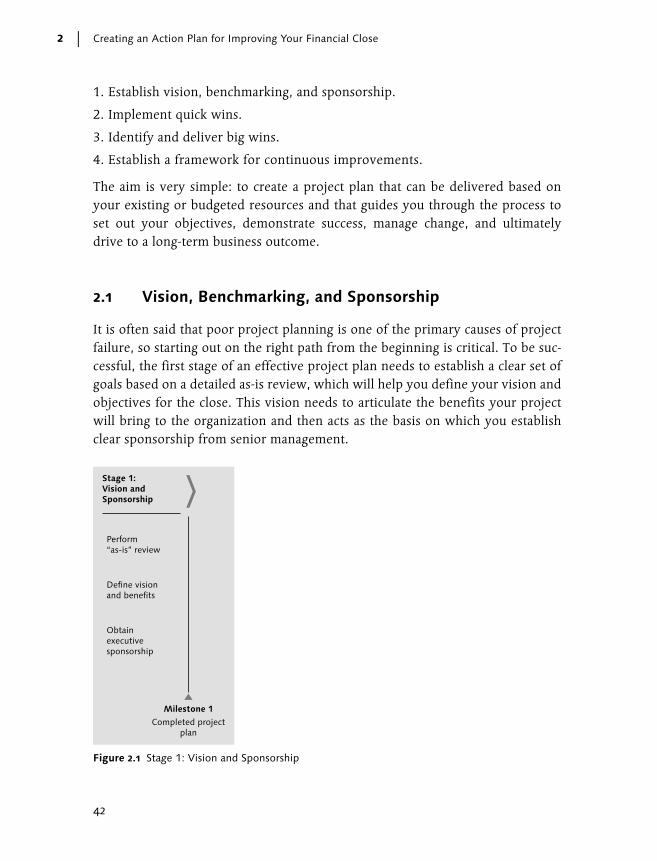

2.1 Vision, Benchmarking, and Sponsorship

It is often said that poor project planning is one of the primary causes of projectfailure, so starting out on the right path from the beginning is critical. To be suc-cessful, the first stage of an effective project plan needs to establish a clear set ofgoals based on a detailed as-is review, which will help you define your vision andobjectives for the close. This vision needs to articulate the benefits your projectwill bring to the organization and then acts as the basis on which you establishclear sponsorship from senior management.

Figure 2.1 Stage 1: Vision and Sponsorship

Milestone 1Completed project

plan

Stage 1:Vision andSponsorship

Perform“as-is” review

Define visionand benefits

Obtainexecutivesponsorship

446.book Seite 42 Donnerstag, 3. Oktober 2013 7:31 19

Vision, Benchmarking, and Sponsorship

43

2.1

Figure 2.1 demonstrates this stage, the core components, and how a completeproject plan needs to be aligned around a continuum of change management. Wewill detail each of these core components in the subsequent sections of this book.

2.1.1 Perform “As-Is” Review

As discussed in Chapter 1, there is no 100% right or wrong answer as to how fasta company should close and report. As a result, you need to determine this basedon a number of factors (typically industry, size, and geography), which are spe-cific to your own organization. However, before you can define a target, you firstneed to conduct a review of your own processes and benchmark those withpeers.

The review piece is critical, and you need to clearly map out your financial closeprocess. It might be prudent to do this in the form of a project plan or processflow diagram where you determine who is involved, the flow of data and finan-cial information through the process, the critical path, and key milestones. Youshould make careful notes of the resources, costs, and time frames involved ateach stage of the process, as well as the IT systems that support it. It’s unlikelythat all of the information you will need will reside in one system.

You also need to understand where you sit compared to your peers—by geogra-phy, industry, or organizational size—and how this relates to the relative com-plexity of your performance management and financial reporting process.Benchmarking is something individuals do relatively easily by determining stan-dard metrics (such as how long the close takes) and simply comparing to adefined peer group. Alternatively, most consulting organizations with establishedfinancial close practices will have more complex benchmarking processes thatthey can apply to your organization. By combining peer benchmarking at variousstages of the financial close process with your detailed as-is review, you shouldcreate a solid foundation on which you can identify which of the typical barriersto a fast close (as discussed in Section 1.4) apply to your organization and in turnwhich of these you need to focus your efforts on. You can then start to define thenext part of the process relating to how you want to improve and address thesebarriers.

446.book Seite 43 Donnerstag, 3. Oktober 2013 7:31 19

Creating an Action Plan for Improving Your Financial Close

44

2

2.1.2 Define Vision and Benefits

After you have reviewed your own processes, the next step is to define yourvision, which primarily equates to a description of how you want your closeprocess to run and in doing so set out the benefits you expect to deliver for thebusiness based on those we discussed in Section 1.1.

Your targets should represent resources, timelines, and costs, and although takinga view across the entire process may be easier, you may find it more effectivelong term to break your targets down by subprocesses. For example, you maydetermine that you should receive financials into the group HQ by working day 3,and complete the corporate close by working day 5, as opposed to simply sayingthe entire process should take 8 days.

As we first discussed in Section 1.3, objectives should be “SMART” (specific, mea-surable, achievable, relevant, and time-bound) and ultimately should become theyardstick for your entire project by which you measure progress and success. Formore information, Paul J. Meyer describes the characteristics of SMART objec-tives in Attitude Is Everything (The Meyer Resource Group, 2003).

Specific

When defining objectives its first important that you select a specific goal overand against a more general one. This means the goal is clear and unambiguous;without vagaries and platitudes. To make goals specific, they must tell an individ-ual or team exactly what is expected, why is it important, who’s involved, whereis it going to happen, and which attributes are important. A specific goal will usu-ally answer the five “W” questions:

� What: What do I want to accomplish?

� Why: Specific reasons, purposes, or benefits of accomplishing the goal.

� Who: Who is involved?

� Where: Identify a location.

� Which: Identify requirements and constraints.

Measurable

Its also critically important that you leverage concrete criteria for measuringprogress toward the attainment of the goal. It goes without saying that if a goal is

446.book Seite 44 Donnerstag, 3. Oktober 2013 7:31 19

Vision, Benchmarking, and Sponsorship

45

2.1

not measurable, it is not possible to know whether a team is making progresstoward successful completion. Measuring progress is supposed to help a teamstay on track, reach its target dates, and experience the exhilaration of achievementthat spurs it on to the continued effort required to reach the ultimate goal. A mea-surable goal will usually answer questions such as the following:

� How much?

� How many?

� How will I know when it is accomplished?

Achievable

Setting objectives that teams cannot possibly meet is not motivational so althoughan goal may stretch a team in order to achieve it,it must be realistic and attain-able. When you identify goals that are most important to you, you begin to figureout ways you can make them come true. You develop the attitudes, abilities,skills, and financial capacity to reach them. The theory states that an attainablegoal may cause goal-setters to identify previously overlooked opportunities tobring themselves closer to the achievement of their goals. An attainable goal willusually answer these questions:

� How can the goal be accomplished?

� What resources do I need to accomplish it?

Relevant

Its also important that you choose goals that matter. In the context of a fast closeproject, a goal to “Ensure 75% of sales orders are delivered within 3 workingdays” may be specific, measurable, attainable, and time-bound, but it lacks rele-vance to project in hand. Many times, you will need support to accomplish a goal:resources, a champion voice, someone to knock down obstacles. Goals that arerelevant to your boss, your team, and your organization will receive that neededsupport. Relevant goals (when met) drive the team, department, and organizationforward. A goal that supports or is in alignment with other goals would be con-sidered a relevant goal. A relevant goal can answer yes to these questions:

� Does this seem worthwhile?

� Is this the right time?

446.book Seite 45 Donnerstag, 3. Oktober 2013 7:31 19

Creating an Action Plan for Improving Your Financial Close

46

2

� Does this match our other efforts/needs?

� Are you the right person?

Time-bound

Finally the use of a specific time frame in goal setting is important as it gives a tar-get date for which an individual and team and work towards. A commitment to adeadline helps a team focus its efforts on completion of the goal on or before thedue date. This part of the SMART goal criteria is intended to prevent goals frombeing overtaken by the day-to-day crises that invariably arise in an organization.A time-bound goal is intended to establish a sense of urgency. A time-bound goalwill usually answer these questions:

� When?

� What can I do six months from now?

� What can I do six weeks from now?

� What can I do today?

By defining SMART objectives as outlined, we can now have a definite idea of ourvision for our financial close process and clearly articulate the benefits to ourbusiness of such an undertaking. The next step in our action plan is sponsorship.

2.1.3 Sponsorship

This is a critical part of the project, and while there is some evidence to suggestthat a lack of sponsorship will hinder your chances of success, there is signifi-cantly more evidence to demonstrate that the most successful projects haveextremely strong executive project sponsorship.

It’s important at this point not to confuse project sponsorship and project man-agement. The latter manages the project day to day and is responsible for deliv-ery. The role of the executive sponsor is a role within the project managementfunction. Usually a senior member of the project board and often the chair, thesponsor will typically be a senior executive who will be responsible to the busi-ness for the success of the project. Depending on your size of organization andthe scope of the project, exactly who this is may, of course, vary.

446.book Seite 46 Donnerstag, 3. Oktober 2013 7:31 19

Vision, Benchmarking, and Sponsorship

47

2.1

The sponsor has a number of responsibilities for the project:

� Provides leadership on the organization culture

� Owns the overall business case

� Keeps the project aligned with the organization’s strategy and direction

� Governs risk associated with the project

� Focuses on realizing benefits

� Identifies opportunities to optimize cost/benefits

� Drives sponsorship

� Provides feedback and lessons learned

The sponsor will therefore become a primary stakeholder for the project man-ager, and typically they will interact around things such as the decision-makingframework, the business priorities and strategy, support for communication tothe wider business, and a host of other associated governance activities. The exec-utive sponsor needs a range of skill sets, including appreciation of corporate strat-egy, ability to prepare a business case, and profound knowledge of theorganization’s operations. The sponsor also needs to know his way around theorganization and command respect within it. The project sponsor and projectmanager should form an effective partnership with each other. The project man-ager should orchestrate all players involved in delivering the project while theproject sponsor coordinates all departments of the organization and associatedstakeholders to ensure the full benefits from the business case. Again, the precisestructure of the project team is somewhat dependent on your organization andscope of the project. Although the roles are distinct, it may be possible for oneperson to drive both roles in smaller projects.

Ultimately, however, in the case of the financial close, the more senior the spon-sor the better. Although in most organizations the financial controller owns theoverall close process, the most successful fast-close projects are typically spon-sored by the CFO. Some level of reporting to the CEO on large transformationprojects is also not uncommon.

Sponsorship from the outset of the project is critical, but it is possible to growsponsorship over the duration of the project. This is critically important as wemove into the more complex and challenging parts of the transformation. Thestarting point is to focus on a series of quick wins.

446.book Seite 47 Donnerstag, 3. Oktober 2013 7:31 19

Creating an Action Plan for Improving Your Financial Close

48

2

2.2 Quick Wins

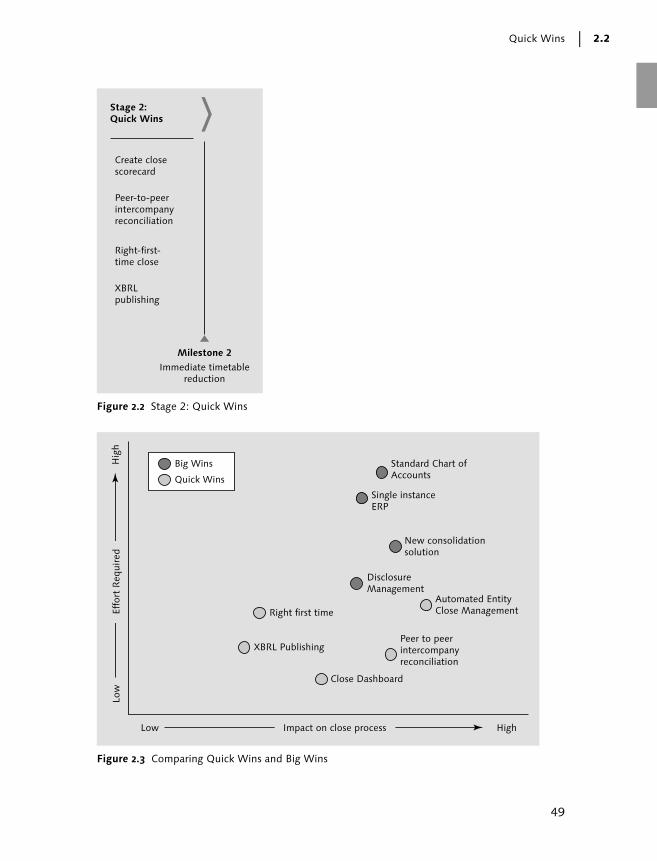

The second stage in the action plan covers the implementation of your quickwins, and essentially this is where most people will feel the rubber hit the roadand where you start to actually make changes to your financial reporting processthat will result in tangible benefits in both the speed and quality of your financialclose process. Figure 2.2 sets out this stage of the process and shows four of themost common quick wins to consider:

� Creating a close scorecard

� Peer-to-peer intercompany reconciliation

� Right-first-time close

� XBRL publishing

Before we explain these in more detail, it’s critical to understand why quick winsare so important to your project. Ultimately, it is simply not possible to changethe entire close process in one go, so quick wins serve to demonstrate that timesavings are achievable, which in itself reinforces the level of executive sponsor-ship a project receives and puts people into a positive and determined frame ofmind for delivering the bigger wins. The key is to understand that not all of thebarriers to a close require huge amounts of effort to improve. In some cases, it ispossible to very easy make significant gains. Keep in mind that the position ofeach win will vary based on the specifics of your organization.

The trick is to evaluate the options open to you and prioritize them according tothe amount of time and effort needed to implement and the size of the impact onyour close cycle. Those with the least required effort but maximum impact are themost attractive and should be your quick wins. Conversely, those that require asignificant event but are also deemed to have a big impact are known as big wins(discussed further in Section 2.3). Naturally, anything that requires a big effortand that will have very little impact on the performance of your close processshould be considered out of scope unless there is another compelling reason toaddress this, such as cost, for example. Figure 2.3 represents a simple way to com-pare and contrast the various efforts and can be used to help select which wins tofocus on.

446.book Seite 48 Donnerstag, 3. Oktober 2013 7:31 19

Quick Wins

49

2.2

Figure 2.2 Stage 2: Quick Wins

Figure 2.3 Comparing Quick Wins and Big Wins

Milestone 2Immediate timetable

reduction

Stage 2:Quick Wins

Create closescorecard

Peer-to-peerintercompanyreconciliation

Right-first-time close

XBRLpublishing

Impact on close process

Effo

rt R

equi

red

Big Wins

Quick Wins

Peer to peerintercompanyreconciliation

Standard Chart ofAccounts

New consolidationsolution

XBRL Publishing

Close Dashboard

DisclosureManagement

Single instanceERP

Right first timeAutomated EntityClose Management

Low High

Low

Hig

h

446.book Seite 49 Donnerstag, 3. Oktober 2013 7:31 19

Creating an Action Plan for Improving Your Financial Close

50

2

While later chapters will look at a number of these quick and big wins in moredetail, particularly showing how SAP solutions can support them, it’s worth illus-trating a few to fully explain how they work as quick wins and add value.

2.2.1 Creating a Close Scorecard

It is often said that what gets measured gets managed, and this holds very true forthe financial close process. Although a reasonable proportion of the customers wework with measure and record different aspects of the close process, it’s surpris-ing how few, in fact, the vast majority, simply fail to report on this data and putit to good use. Those organizations that are typically best in class at the financialclose, on the other hand, do make good use of the data.

They do this by creating a close scorecard, which serves to collect data and reporton the effectiveness of different stages in the reporting process. The most com-mon approach is to report on the time it takes for operating units to report finan-cials to the central team. This information can then be used to show the best andworst performers in a group. Such a scorecard need not be complicated and in itssimplest form can simply be a league table showing who is fastest or on time andwho is lagging and slowing the process. Repeated monthly, this soon becomes astrong motivational tool as no one likes being held out as a poor performer.

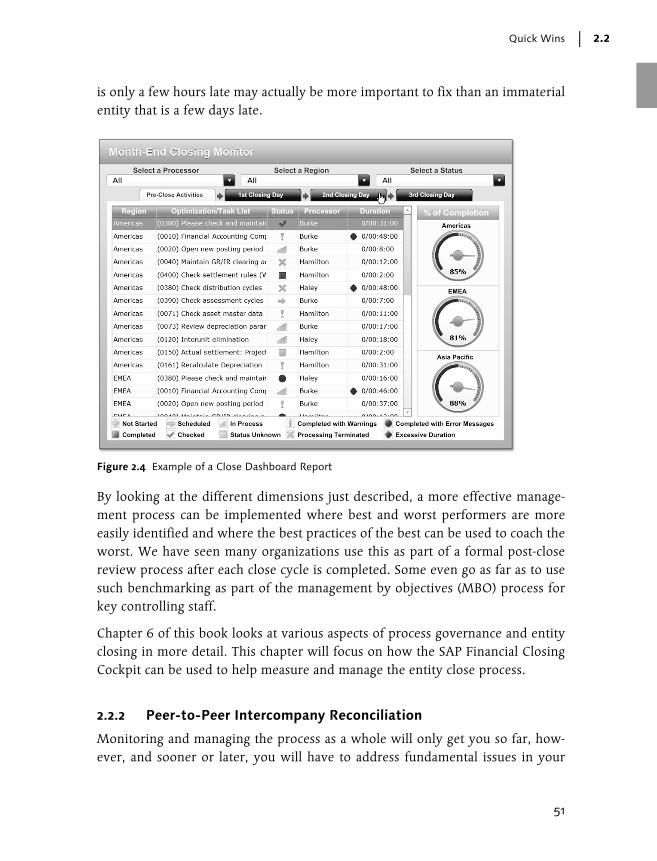

It’s of course possible to create more complex models as Figure 2.4 illustrates, butone of the most effective we have seen is still relatively simple provided yourfinancial reporting systems are capable of recording and collecting the data.Essentially, central teams collect data on a number of dimensions spanning thetime it takes for an entity to report, the number of errors associated with the sub-mission, and the materiality of the entity to the overall group’s financial position.Then, they can plot this on a bubble chart with speed and error representing thetwo axes and the size of the bubble representing materiality. As indicated, theexample in Figure 2.4 is more complex and records many more details, includingdata points on individual subprocesses and owners of those processes. The depthof complexity is again up to the organization and the scope of the project, butclearly, any level of monitoring has a significant impact.

Although more complicated, such an approach allows for a further level of man-agement and ultimately coaching. Clearly submitting on or ahead of deadlines isgood, but if the process is full of errors, then it’s a wasted effort. In addition, anentity that is highly material to the overall financial position of the business and

446.book Seite 50 Donnerstag, 3. Oktober 2013 7:31 19

Quick Wins

51

2.2

is only a few hours late may actually be more important to fix than an immaterialentity that is a few days late.

By looking at the different dimensions just described, a more effective manage-ment process can be implemented where best and worst performers are moreeasily identified and where the best practices of the best can be used to coach theworst. We have seen many organizations use this as part of a formal post-closereview process after each close cycle is completed. Some even go as far as to usesuch benchmarking as part of the management by objectives (MBO) process forkey controlling staff.

Chapter 6 of this book looks at various aspects of process governance and entityclosing in more detail. This chapter will focus on how the SAP Financial ClosingCockpit can be used to help measure and manage the entity close process.

2.2.2 Peer-to-Peer Intercompany Reconciliation

Monitoring and managing the process as a whole will only get you so far, how-ever, and sooner or later, you will have to address fundamental issues in your

Figure 2.4 Example of a Close Dashboard Report

446.book Seite 51 Donnerstag, 3. Oktober 2013 7:31 19

Creating an Action Plan for Improving Your Financial Close

52

2

close process, including accounting practices. In all the time that we have workedin the financial close process, the area that has consistently been identified as amajor cause of delay is intercompany reconciliation. As Section 1.4.3 highlights,the intercompany process all too often sits on the critical path for the close cyclecausing significant delays while operating units resolve unmatched intercompanytransactions and balances.

Time spent at both the head office and local operations contributes to a significantnumber of man-days, which are needlessly wasted on this essential but cumber-some process. To some extent, this is hardly surprising considering the complex-ity of the process. In the past, the technology to support the process was highlymanual with email and faxes forming the basis of communication between thecounter parties to ensure intercompany balances matched. Often errors wereonly discovered during the consolidation process when intercompany elimina-tion reports were run.

Chapter 8 of this book looks at how today’s web-based solutions, such as SAPIntercompany, can be implemented extremely quickly as a quick win to removethe intercompany process from the critical path. Significant gains can be madevery quickly by implementing a peer-to-peer based communication processensuring that intercompany balances and transactions (as shown in Figure 2.5)match prior to starting the consolidation process.

Figure 2.5 Peer-to-Peer Intercompany Reconciliation with SAP Intercompany

446.book Seite 52 Donnerstag, 3. Oktober 2013 7:31 19

Quick Wins

53

2.2

2.2.3 Right-First-Time Close

Errors in the financial close process are of course not just limited to errors in theintercompany process. There are numerous other points of failure. As Section1.4.2 describes, the inability of many to achieve a “right-first-time” close processis a critical barrier to the fast close and is a symptom of many broken or failingprocesses and systems. It’s linked to manual data entry, late delivery from report-ing units, a lack of validation and controls, poor integration with source systems,and a lack of integration across multiple close processes.

As a result, taking simple steps to ensure the accuracy of data coming into thefinancial close process can have a huge impact, which is why it’s identified as aquick win. Later chapters in this book will examine this in much more detail, buta combination of using a good data integration solution that draws data fromsource systems, validates it, and loads it automatically into reporting and consol-idation environments is extremely powerful. Chapter 3 of this book examineshow solutions such as SAP Financial Information Management can be quicklyimplemented to deliver these capabilities in such a way that finance teams canown and manage this process with the additional benefit from enhanced auditcapabilities. Chapter 7 will go on to look at how more controls can be imple-mented to ensure additional levels of accuracy. For example, delays to the finan-cial close process are caused not just by erroneous data (such as assets notequaling liabilities) but also by missing data or analysis. A common failure, forexample, occurs when an entity forgets to include commentary explaining why agiven number varies from a plan or budget number. The ability to check this atthe point of submission and ensure that this information is provided before theprocess progresses too far significantly improves the speed and quality of theoverall close process.

2.2.4 XBRL Publishing

Unlike the intercompany process, which has been around as part of the close pro-cess from the outset and is a well-known target for quick wins, the XBRL processis relatively new. However, just like the intercompany process, XBRL also pre-sents an opportunity for a quick win. XBRL is one of the biggest changes to impactthe world of financial reporting in the past 10 years, apart from perhaps the intro-duction of IFRS, and its use for filing financial and business information to keyregulators, banks, and tax authorities is increasingly becoming standard practice.

446.book Seite 53 Donnerstag, 3. Oktober 2013 7:31 19

Creating an Action Plan for Improving Your Financial Close

54

2

Chapter 10 in this book looks in more detail at the role of XBRL in the so-called“last mile of finance,” the stage in the process that takes place at the end of thefinancial close, as described in Section 1.2. Typically, this stage of the processtakes a lot of time, effort, and money, and it is often the least automated part ofthe financial close.

Although we would typically regard the implementation of a broad reporting anddisclosure solution as a big win given the breadth of the solution coverage, it ispossible to streamline the XBRL filing process relatively easily. Implementing asolution such as SAP Disclosure Management just for XBRL filing can be achievedquickly and without the need for extensive outsourcing of the filing process,which is the common alternative.

As described earlier, these are just a few examples of typical quick wins. In yourorganization, these may be different; after all, what is easy for some may be chal-lenging for others. As with the process of defining your financial close objectives,it’s about reviewing your processes and identifying what works for your busi-ness. What is clear is that using quick wins to demonstrate success and drive addi-tional sponsorship for bigger wins is often overlooked but always valuable.

2.3 Big Wins

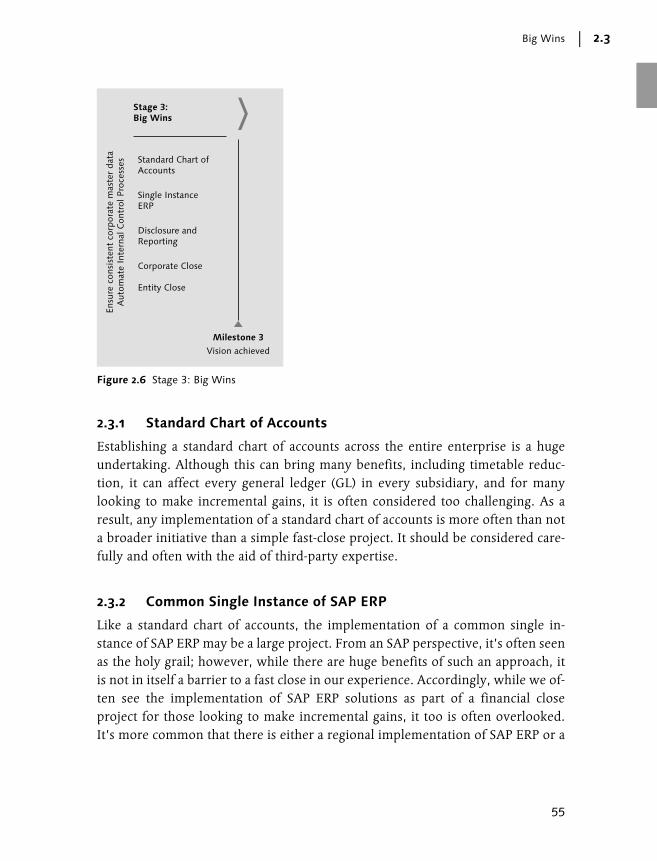

As we described earlier, the third stage of the action plan is to identify and deliverbig wins. This is based on the assumption that quick wins by themselves may notlead you to achieve all your targets or that more often than not, you’re unable toimplement quick wins given your current system’s landscape. Big wins requiregreater resources and more time but often enable significant reductions in thetime the close process takes. The subsequent chapters in this book look in muchmore detail at how financial close solutions from SAP can help you address andimplement big wins in your organizations, but for now, here are some examplesof big wins, as detailed in Figure 2.6:

� Establishing a standard chart of accounts

� Implementing a common single instance of SAP ERP

� Implementing a broad reporting and disclosure framework

� Addressing major issues in the corporate and local close processes

446.book Seite 54 Donnerstag, 3. Oktober 2013 7:31 19

Big Wins

55

2.3

2.3.1 Standard Chart of Accounts

Establishing a standard chart of accounts across the entire enterprise is a hugeundertaking. Although this can bring many benefits, including timetable reduc-tion, it can affect every general ledger (GL) in every subsidiary, and for manylooking to make incremental gains, it is often considered too challenging. As aresult, any implementation of a standard chart of accounts is more often than nota broader initiative than a simple fast-close project. It should be considered care-fully and often with the aid of third-party expertise.

2.3.2 Common Single Instance of SAP ERP

Like a standard chart of accounts, the implementation of a common single in-stance of SAP ERP may be a large project. From an SAP perspective, it’s often seenas the holy grail; however, while there are huge benefits of such an approach, itis not in itself a barrier to a fast close in our experience. Accordingly, while we of-ten see the implementation of SAP ERP solutions as part of a financial closeproject for those looking to make incremental gains, it too is often overlooked.It’s more common that there is either a regional implementation of SAP ERP or a

Figure 2.6 Stage 3: Big Wins

Stage 3:Big Wins

Milestone 3Vision achieved

Standard Chart ofAccounts

Single InstanceERP

Disclosure andReporting

Corporate Close

Entity Close

Ensu

re c

onsi

sten

t co

rpor

ate

mas

ter

data

Aut

omat

e In

tern

al C

ontr

ol P

roce

sses

446.book Seite 55 Donnerstag, 3. Oktober 2013 7:31 19

Creating an Action Plan for Improving Your Financial Close

56

2

consolidation of multiple instances into fewer regional deployments. Chapter 4in this book addresses GL and sub-GL close processes in more detail.

2.3.3 Reporting and Disclosure Framework

As introduced in Section 2.2.4, a broad solution that addresses the last mile offinance can have a significant impact on your financial close process. The XBRLcomponent is actually the easiest part of this, which is why it is included as aquick win. However, even more significant gains and cost savings are possible bytaking a broader view and developing a more established and controllable report-ing and disclosure framework, which also has a significant impact on data quality.The basis for this big win is to move beyond manual, error-prone last mile offinance processes using Microsoft Word and Excel documents, separated fromthe secure and auditable financial reporting and consolidation systems and tomove to implementing a full collaborative disclosure management system such asSAP Disclosure Management. As mentioned earlier, Chapter 10 in this bookexamines this in more detail.

2.3.4 Corporate and Entity Close

The final area of big wins relates to a broad range of solutions to common barriersto a fast close within the corporate and local close processes. These are classifiedas big wins because they often require the implementation of new consolidationsoftware to be the foundation on which they are implemented. Existing applica-tions are often unable to deliver suitable quick wins or to provide a sustainableinfrastructure for the fast close in your organization.

For example, implementing new systems that facilitate the harmonizing of packsand processes across reporting cycles can have significant benefits. Standardizingon the same data flow each month helps to avoid discrepancies and reduces time-tables because the increased volumes this standardization typically producesforces subsidiaries into automating processes and standardizing their own sys-tems. The end result is often better data quality and shorter timetables. Imple-menting a new framework will allow you to support this if your current systemsare not able to.

Similarly, where manual data entry processes exist, replacing them with directintegration between source SAP ERP or GL applications and EPM applications

446.book Seite 56 Donnerstag, 3. Oktober 2013 7:31 19

Continuous Improvements

57

2.4

reduces errors. The same is true when establishing a control environment identi-fying the most effective and efficient controls for the financial close processes andthen streamlining and automating them to minimize the compliance burden. Thedevelopment of a framework to monitor and control the entire close processfrom local close activities in an SAP ERP application through to final statementproduction in consolidation applications offers significant opportunities toimprove quality and reduce the time the close takes. Subsequent chapters in thisbook address these points further and demonstrate how technology can helpdeliver these best practices.

2.4 Continuous Improvements

After you have completed the implementation of quick wins and big wins, it isassumed that you have met your objectives. If that is not the case, then as aproject team, you need to decide if you have achieved enough or if additionalsteps, still under the guise of quick wins and big wins, need to be implemented.Even if you have met your goals and celebrated that success, your journey is notover. In many respects, it’s the start of a whole new one as one of the best piecesof advice we share with our customers is that a fast-close initiative should not beregarded as a one-time project. Yes, you need to establish a project and run thiswith SMART objectives over a given period of time, but the final stage of theproject should look to establish, as part of your ongoing financial close process, aframework for continuous improvement.

This is critically important because as Chapter 12 in this book demonstrates, theonly certainty we have in the world of financial reporting and regulation is thatthere will be more change to come. These changes could easily—as we have seenin the past with say the introduction of IFRS in Europe and the adoption of XBRLreporting in the United States—have a profound impact on the process and sys-tem landscapes that you ultimately design in your fast-close project.

The example of IFRS in Europe is particularly interesting. In the preceding years,many organizations had invested in fast-close initiatives and had made promisinggains in terms of speed, quality, and the costs of their financial close processes.When it came to implementing IFRS, many applied the accounting changes and indoing so added more resources to the overall process. At the same time, therequirements compelled organizations to collect and report on more information,

446.book Seite 57 Donnerstag, 3. Oktober 2013 7:31 19

Creating an Action Plan for Improving Your Financial Close

58

2

and many did this by reverting to manual data collection processes often involv-ing spreadsheets, which their earlier financial close project had sought to eradi-cate. These manual processes took longer, were less auditable, and thereforeextended the close process.

Being able to plan and predict such changes is of course challenging, but two keylessons emerge. First is that many who reverted to manual processes did so sim-ply because they had not implemented flexible solutions, and therefore the col-lection of the additional data was challenging. As later chapters in this book willdemonstrate, financial close solutions such as SAP Business Planning and Consol-idation are designed to be owned and managed by finance, giving them the flex-ibility to change and evolve processes as requirements dictate. The second ismore cultural in the sense that people simply lost sight of the investment andgains they had previously made and threw everything, including the proverbialkitchen sink, at the problem without looking at it in the context of the overallclose process.

Best practice would dictate that when looking to accommodate such a change,you plan to do so in such a way that you further optimize the close. This requiresmore flexibility and up-front planning, but it is possible. This is why the best inclass will typical look for post-close reviews after each close. They review the bestin class practices and use this knowledge to coach the weaker performers. Theyuse the review to spot potential issues early and adjust processes so it does notimpact the critical path. In doing so, many businesses not only maintain the closetimes they had previously established, even in light of changing requirements,but further optimized them.

As Figure 2.7 illustrates, the final stage of a close project can, if the motivation isthere, be applied to other areas of the business, such as planning, budgeting, andforecasting. Planning and budgeting is an area that—like the financial close—isoften criticized for taking too long, costing too much, and often resulting in con-flicting results. Many of the lessons from a financial close project, particularly interms of the application of a similar action plan, can be used to shorten planningand budgeting cycles. It is also possible to create immediate benefits directly outof the steps you take to streamline your financial close.

One such approach relates to the use of integrated planning and consolidationsystems. Not only do solutions such as SAP Business Planning and Consolidationoffer benefits during the close because actual and plan data exists in the same

446.book Seite 58 Donnerstag, 3. Oktober 2013 7:31 19

Summary

59

2.5

environment, but the reporting processes, collaboration tools, and validations,which should all form part of a best practice close process, can be used to addresscommon issues in the planning cycle as well. As part of a post-financial closeproject review process, we encourage you to think of how the lessons you learnedwithin your own organization can be applied in other areas of the business.

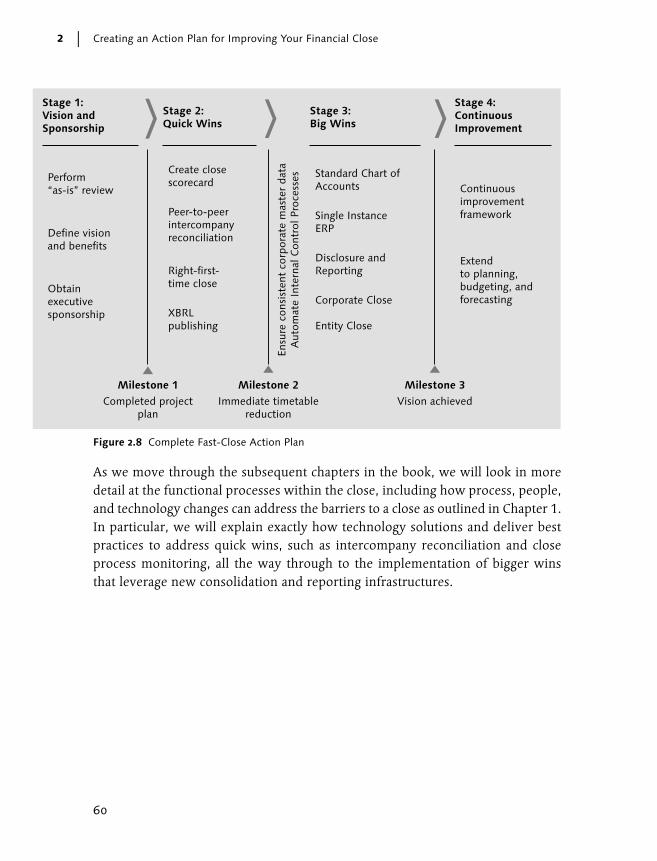

2.5 Summary

The four-step action plan we have outlined (see Figure 2.8) is just one example ofa number of ways in which a project team can structure a financial close project.There are numerous examples of actions plans out in the market as well. Accord-ingly, you should select an approach that works for your organization becauselike much of this, there is no single right or wrong answer. However, the criticalmessage is that the plan needs a structure and needs to be a managed project thatstarts with benchmarking and sponsorship, maps clear steps and actions todeliver against a target and objective, and prepares a culture of ongoing focus andimprovement.

Figure 2.7 Stage 4: Continuous Improvement

Milestone 3Vision achieved

Stage 4:ContinuousImprovement

Continuousimprovementframework

Extendto planning,budgeting, andforecasting

446.book Seite 59 Donnerstag, 3. Oktober 2013 7:31 19

Creating an Action Plan for Improving Your Financial Close

60

2

As we move through the subsequent chapters in the book, we will look in moredetail at the functional processes within the close, including how process, people,and technology changes can address the barriers to a close as outlined in Chapter 1.In particular, we will explain exactly how technology solutions and deliver bestpractices to address quick wins, such as intercompany reconciliation and closeprocess monitoring, all the way through to the implementation of bigger winsthat leverage new consolidation and reporting infrastructures.

Figure 2.8 Complete Fast-Close Action Plan

Stage 3:Big Wins

Milestone 1Completed project

plan

Milestone 2Immediate timetable

reduction

Milestone 3Vision achieved

Stage 1:Vision andSponsorship

Perform“as-is” review

Define visionand benefits

Obtainexecutivesponsorship

Stage 4:ContinuousImprovement

Continuousimprovementframework

Extendto planning,budgeting, andforecasting

Standard Chart ofAccounts

Single InstanceERP

Disclosure andReporting

Corporate Close

Entity Close

Stage 2:Quick Wins

Create closescorecard

Peer-to-peerintercompanyreconciliation

Right-first-time close

XBRLpublishing

Ensu

re c

onsi

sten

t co

rpor

ate

mas

ter

data

Aut

omat

e In

tern

al C

ontr

ol P

roce

sses

446.book Seite 60 Donnerstag, 3. Oktober 2013 7:31 19

291

Index

A

Accelerated financial closebenefits, 29

Access Requests, 144Access risk management, 144Accounting

subledger, 77Accounts Payable

balance confirmation, 89close process, 88transactions, 157

Accounts Receivableclose process, 88interest calculation, 89reserve for bad debt, 89transactions, 157

Accruals, 110, 131Acquisitions, 195Activity Types, 111Activity-Based Costing module, 114Adjustments

approval, 194automatic, 190manual, 189

Adobe PDF, 234Advanced analytics, 269Allocations, 112

assessments, 112distributions, 112

Application Link Enabling, 65Approvals, 232As-Is Review, 43Asset Accounting, 91

asset class, 91asset master record, 91posting depreciation, 91

Audit Management, 151Audit trail, 39, 213

B

balance sheet, 178accounts, 125

Basis for Cost Center Allocations, 111Benchmarking, 42, 262

data, 262peer, 43

Benefits of a fast close, 29, 44Big data, 267, 269, 270Big Wins, 42, 54BPC � SAP Business Planning and

ConsolidationBusiness case for a financial close project, 26Business Rules Framework, 67BusinessObjects Business Intelligence, 19, 33,

264, 277

C

Central Chart of Accounts, 78, 83, 103, 174CFO Priorities, 25Classic General Ledger, 128Close Dashboard Report, 51Close process monitoring, 60Close scorecard, 48, 50Collaboration, 228Company code, 78, 79Configuration controls, 149Consolidation application, 38Continuous Improvements, 42, 57, 265, 266Control monitoring, 148Controlling, 103

master data, 105Organizational Hierarchy, 104

Controlling objects, 106Corporate Close, 56Cost Centers, 110Cost Element

primary, 113secondary, 113

446.book Seite 291 Donnerstag, 3. Oktober 2013 7:31 19

Index

292

Cost Element Accounting, 105primary cost elements, 106secondary cost elements, 107

Cost Elements, 111Cost Profitability Analysis

Co-PA Accelerator, 126Currency, 182

considerations, 171conversion rules, 192Example, 251group, 182impacts, 195local, 182rate table, 183transaction, 182Translation Adjustments, 192

D

Dashboardsaccess risk, 154access rule review, 154alert, 154review emergency access, 154role, 154

Data approval, 171Data collection, 171Data discovery, 269Data extraction, 67Data Management

Transaction, 67Data Mapping, 174Data periodicity, 171Data quality and collection errors, 38Data Validation, 171, 179Days payables outstanding, 264Days sales outstanding, 264, 279Dependencies, 133Dimensionality, 171, 175, 252

flow dimension, 177movement dimension, 177

Disclosure Framework, 56Disclosure Management, 213

Key Performance Indicators, 215Microsoft Office, 217

Disclosure Statements, 234

Document Control, 229Document principle, 79

corresponding entry, 80Double-entry bookkeeping, 25Drill Down, 252Drill Though, 252Dunning process, 90

E

Economic environment, 259EDGAR, 238Elimination of Investments, 192Embedded analytics, 264Enterprise Performance Management, 19, 32,

68, 265, 269, 277Entity Close, 56, 131

alerts, 134closing cycles, 131execution, 134legal entity, 131monitoring, 137planning, 132tasks, 132, 133template, 132

Equity accounts, 192Event based close, 134Executive sponsor, 46eXtensible Business Reporting Language

(XBRL), 26, 28, 48, 53, 56, 57, 272Electronic Filings, 213, 237filing process, 54format, 236instance documents, 237, 240Publishing, 53Standard taxonomies, 237Statements, 236Tagging Data, 239Trends, 242

External Stakeholders, 248

F

Fast-close action plan, 41Financial Close

benchmark, 36

446.book Seite 292 Donnerstag, 3. Oktober 2013 7:31 19

Index

293

Financial Close (Cont.)components, 32definition, 25drivers, 26drivers, regulatory, 27

Financial closebarriers, 36

Financial Consolidation, 169approval of Data, 180calculating ending balances, 182commentary, 180consolidation adjustments, 189consolidation units, 170cost method, 187entities, 186equity method, 187loading data, 173loading ending balances, 182majority-owned entities, 187minority interest, 188periodicity of data, 181solution differentiation, 196standard thresholds, 186versions, 194

Financial excellence, 25Financial governance, 32Financial Information Management

application connectivity, 70data integration, 69Database Connectivity, 70deployment, 69EPM integration, 72job log history, 73Non-SAP Data Sources, 74process transparency, 72SAP Data Sources, 74

Financial Operations, 259, 262Financial Statements, 220, 224, 239

Unstructured Information, 220Firefighter ID, 155Foreign currency conversion, 192Foreign currency valuation, 85

open item, 85Fraud Management, 156

G

GAAP � Generally Accepted Accounting Principles

Gantt chart, 138General Ledger, 77, 103, 158, 172

account balance, 100Accounting, 83classic, 86document report, 100financial statement report, 100line item report, 100master data report, 100new, 86

Generally Accepted Accounting Principles, 39, 64, 86, 179, 208

Goods receipt, 95Governance, Risk and Compliance, 19,

33, 277access controls, 142process management, 142

GR/IR reconciliation, 95GRC analytics, 153

I

IFRS � International Financial Reporting Standard

Integrated International Reporting Council, 273

Integrated reporting, 29, 273, 274Integration, operations and controlling, 108Intercompany Reconciliation, 38, 48, 51, 60,

158, 190account balances, 158balances, 52Eliminations, 190matching, 157One Source System, 159peer-to-peer, 48, 51Peer-to-Peer Process, 162Process, 161, 165reporting units, 161

Internal and external stakeholders, 27internal audit, 151Internal Orders, 115

446.book Seite 293 Donnerstag, 3. Oktober 2013 7:31 19

Index

294

Internal Stakeholders, 248International Financial Reporting Standard,

25, 27, 28, 57, 64, 86, 194, 205, 272Inventory Management, 94Inventory valuation, 94, 96

actual costing, 94actual costs, 97lean accounting, 94moving average, 94standard cost, 94, 96

Investment Management (IM), 92Investor relations, 31Invoice receipt, 95

J

Journal entry, 84, 131, 262accrual, 84recurring expense, 84

K

Key performance indicators, 279Key risk indicators, 142

L

Last mile of finance, 56Legal entity, 78Legal reporting unit, 185Logistics Information System, 112

M

Mappingdata reuse, 70Multiple target, 71rules for automation, 70simplified, 70Tables, 71

Master data, 63, 65management, 64

Master data controls, 149Material ledger, 94, 97

actual costs, 97

Materials Management, 109Mergers, 195Microsoft Office, 226Microsoft Word, 234Mobility, 257

Finance, 270Multiple GAAPs, 194

N

Notes Management, 221

O

Open item clearing, 89Organizational hierarchy, 132Organizational structures, 185Overhead allocations, 114

P

P&L statements � Profit and LossParallel ledgers, 86Planning and budgeting, 58, 266, 269Posting period, 97Predictive Analytics, 269Process Automation, 39Process flows, 133Product Costing, 119, 122Production Planning, 109, 120Professional Services, 267Profit and Loss, 106, 182Profit Center Accounting, 127Profit Centers, 127Profitability Analysis, 114, 124

account-based, 125cost-based, 125

Profitability and cost management, 266, 269Project management, 46

Q

Quick wins, 42, 48

446.book Seite 294 Donnerstag, 3. Oktober 2013 7:31 19

Index

295

R

Rapid Deployment Solution, 77, 97, 210SAP Financial Close, 210

rate effect, 251RDS � Rapid Deployment SolutionReceivables Management, 90, 264Reconciliation, 129, 131Reconciliation of accounts, 88Recurring entries, 88Redwood, 135Regulatory Compliance, 271Regulatory disclosures, 242Regulatory drivers for the accelerated

financial close, 27Remediation, 148Reorganization, 85Report Documents, 225Reporting

balance sheet, 245, 246cash flow, 245cash flow statement, 246drill-down, 246drill-through, 246entity, 169income statement, 246legal reporting requirements, 196management, 245management reporting requirements, 196periodic comparision, 246, 249periods, 34publishing, 234requirements, 245statutory, 246, 248variance, 246versioning, 246, 250what-if statements, 246, 250

Reporting delivery methodsBusiness Intelligence, 255SAP BusinessObjects Analysis, 256SAP BusinessObjects Dashboard, 256SAP BusinessObjects Explorer, 257SAP BusinessObjects Web Intelligence, 256SAP Crystal Reports, 255

Revenue-based results analysis, 118Role Definition, 228

Administrator, 229

Role Definition (Cont.)Editor, 228Manager / Approver, 228

Role of Finance, 259Rounding, 193

S

Sales and Distribution (SD), 88, 109SAP Access Control, 144

Dashboard, 154SAP Business Planning and Consolidation, 58,

74, 199, 218, 269, 271SAP HANA, 269

SAP Business Suite, 264SAP BusinessObjects Business Intelligence,

101, 264, 270SAP BusinessObjects Financial Information

Management, 53SAP BusinessObjects Intercompany, 52SAP Central Process Scheduling, 134, 135, 137SAP CRM Interaction Center, 99SAP Customer Financial Fact Sheet, 271SAP Disclosure Management, 54, 56, 214,

218, 228, 230Starter Kits, 240

SAP Disclosure Management add-in, 238SAP Enterprise Controlling-Consolidation, 197SAP Enterprise Performance Management,

170business rules, 192EPM consolidation starter kits, 206Unwired, 271

SAP ERP Financials, 19, 32, 55, 264SAP ERP Human Capital Management, 109SAP Financial Closing Ccockpit

automated tasks, 138SAP Financial Closing Cockpit, 51, 132SAP Financial Consolidation, 74, 170,

201, 218SAP Financial Information Management, 68,

173SAP HANA, 126, 156, 264, 269, 270SAP Intercompany, 52, 158

Adjustments, 166data entry, 166Deployment options, 165

446.book Seite 295 Donnerstag, 3. Oktober 2013 7:31 19

Index

296

SAP Intercompany (Cont.)Landscape Scenarios, 165Peer-to-Peer Communication, 163Security, 167

SAP Master Data Governance, 65data model, 66