acca ifrs changes 1506

TRANSCRIPT

ACCA

IFRS Member CPD – 9th June 2015

IFRS Changes

By Simon Fisher

RSM Ashvir is an independent member firm of RSM International, an affiliation of independent accounting and consulting firms.

This slide presentation has been prepared for general guidance

only, and does not constitute professional advice. You should

not act upon the information contained in these slides without

obtaining specific professional advice. Accordingly, to the extent

permitted by law, RSM Ashvir (and its employees and agents)

accept no liability, and disclaim all responsibility, for the

consequences of anyone acting, or refraining from acting, in

reliance on the information contained in these slides or for any

decision based on it, or for any consequential, special or similar

damages even if advised of the possibility of such damages.

Background

• Convergence with US GAAP is “dead” - no new projects planned. However,

in May 2014 for the first time in history IASB and FASB simultaneously

issued a converged standard on revenue recognition – IFRS 15. IFRS 9 is

also closely aligned with US GAAP

• Key projects remain ‘Leases’ and ‘Insurance’, on which IASB continues to

seek convergence with FASB.

• Review of the conceptual framework continues

• No major change until 1 January 2017 (likely to be put back to 2018)

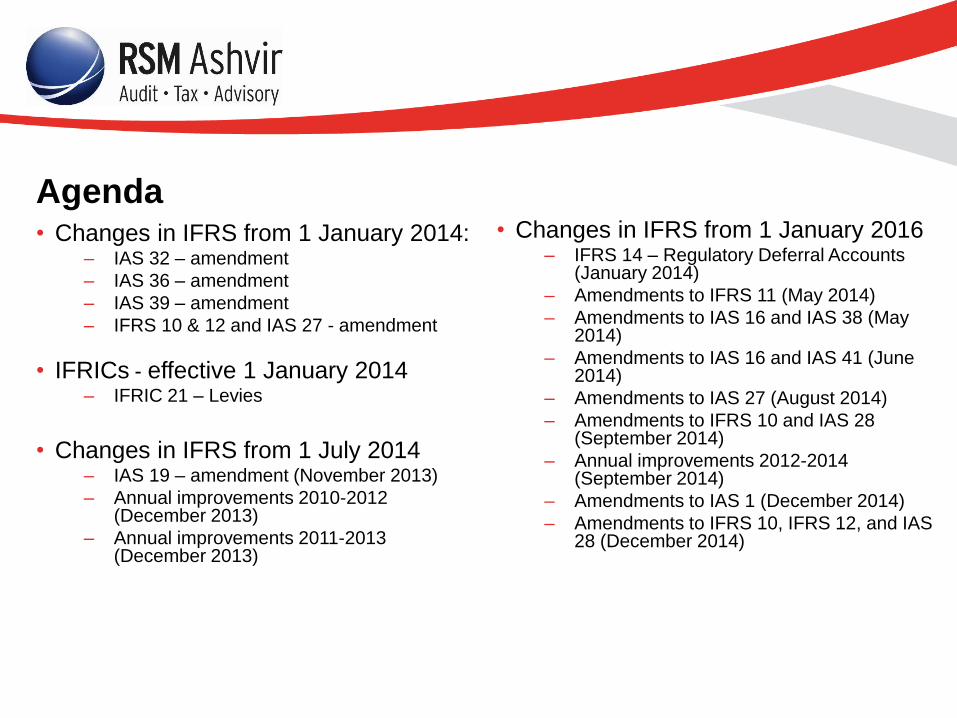

Agenda • Changes in IFRS from 1 January 2014:

– IAS 32 – amendment

– IAS 36 – amendment

– IAS 39 – amendment

– IFRS 10 & 12 and IAS 27 - amendment

• IFRICs - effective 1 January 2014 – IFRIC 21 – Levies

• Changes in IFRS from 1 July 2014 – IAS 19 – amendment (November 2013)

– Annual improvements 2010-2012 (December 2013)

– Annual improvements 2011-2013 (December 2013)

Agenda • Changes in IFRS from 1 January 2014:

– IAS 32 – amendment

– IAS 36 – amendment

– IAS 39 – amendment

– IFRS 10 & 12 and IAS 27 - amendment

• IFRICs - effective 1 January 2014 – IFRIC 21 – Levies

• Changes in IFRS from 1 July 2014 – IAS 19 – amendment (November 2013)

– Annual improvements 2010-2012 (December 2013)

– Annual improvements 2011-2013 (December 2013)

• Changes in IFRS from 1 January 2016 – IFRS 14 – Regulatory Deferral Accounts

(January 2014)

– Amendments to IFRS 11 (May 2014)

– Amendments to IAS 16 and IAS 38 (May 2014)

– Amendments to IAS 16 and IAS 41 (June 2014)

– Amendments to IAS 27 (August 2014)

– Amendments to IFRS 10 and IAS 28 (September 2014)

– Annual improvements 2012-2014 (September 2014)

– Amendments to IAS 1 (December 2014)

– Amendments to IFRS 10, IFRS 12, and IAS 28 (December 2014)

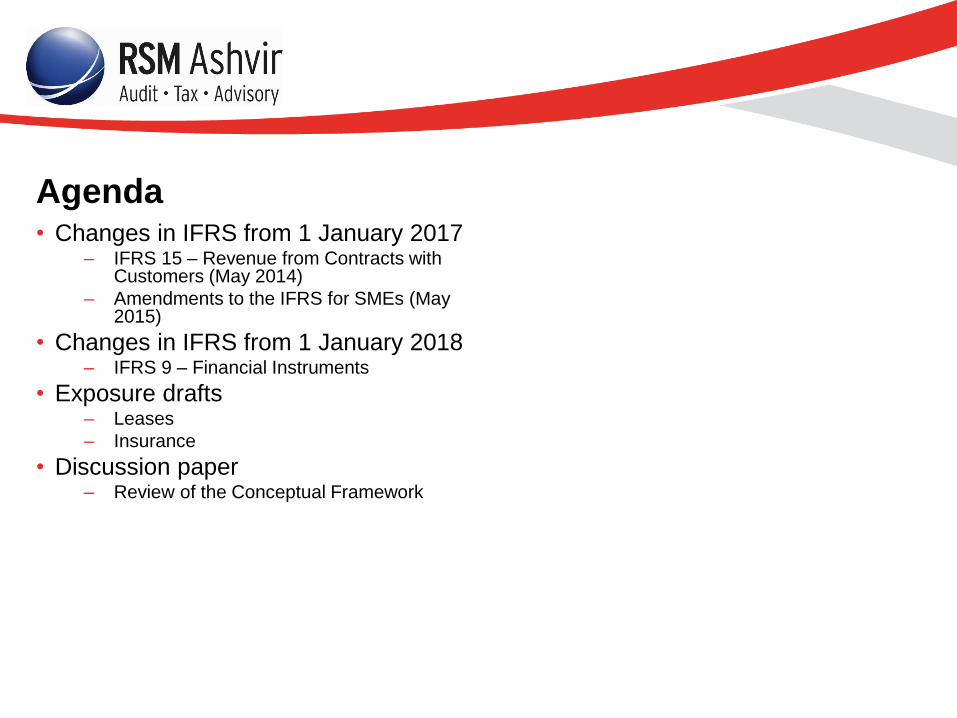

Agenda • Changes in IFRS from 1 January 2017

– IFRS 15 – Revenue from Contracts with Customers (May 2014)

– Amendments to the IFRS for SMEs (May 2015)

• Changes in IFRS from 1 January 2018 – IFRS 9 – Financial Instruments

• Exposure drafts – Leases

– Insurance

• Discussion paper – Review of the Conceptual Framework

Changes effective from 1

January 2014

IAS 32 – Amendment

• The amendments are to the Application Guidance only, and clarify the application of the offsetting requirements

IAS 36 – Amendment

Recoverable amount disclosures for non-financial assets

• The amendments:

– reduce the circumstances in which the recoverable amount of assets or cash-generating units are required to be disclosed

– Clarify the disclosures required

– Introduce an explicit requirement to disclose the discount rate used when using a present value technique

IAS 39 – Amendment

Novation of derivatives and continuation of hedge accounting

• The amendments permit the continuation of hedge accounting in a situation where the counterparty to a derivative designated as a hedging instrument is replaced by a new central counterparty as a consequence of laws and regulations

IFRS 10 and 12, and IAS 27 – Amendment

Investment entities

• The amendments define ‘investment entities’ and provide them with exemption from the consolidation of subsidiaries. Instead, an investment entity is required to measure the investment in each eligible subsidiary at fair value through profit or loss.

Changes to IFRICs

IFRIC 21 – Levies

Issued in May 2013 – effective 1 January 2014

• When to recognise a liability to pay a levy?

• The obligating event is the activity that triggers the payment of the

levy.

• The fact that the levy might be calculated based on revenue in, or

assets at the end of, the previous period does not make it a liability

at the end of that period.

Changes effective from 1 July

2014

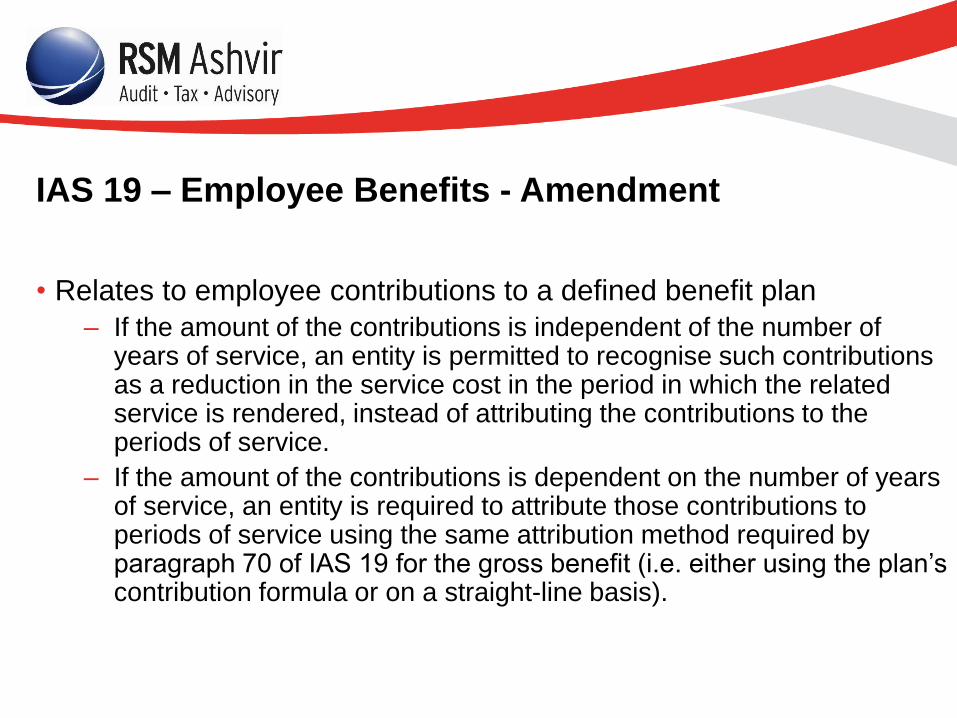

IAS 19 – Employee Benefits - Amendment

• Relates to employee contributions to a defined benefit plan

– If the amount of the contributions is independent of the number of years of service, an entity is permitted to recognise such contributions as a reduction in the service cost in the period in which the related service is rendered, instead of attributing the contributions to the periods of service.

– If the amount of the contributions is dependent on the number of years of service, an entity is required to attribute those contributions to periods of service using the same attribution method required by paragraph 70 of IAS 19 for the gross benefit (i.e. either using the plan’s contribution formula or on a straight-line basis).

Annual improvements 2010 - 2012

• IFRS 2 – Share based payment: definition of a vesting condition (7 pages of Basis for Conclusions!)

• IFRS 3 – Business combinations: accounting for contingent consideration in a business combination

• IFRS 8 – Operating segments: aggregation of operating segments; reconciliation of the total of the reportable segments’ assets to the entity’s assets

• IFRS 13 – Fair value measurement: short-term receivables and payables – confirming that face value of such receivables can be taken as fair value if effect of discounting is not material

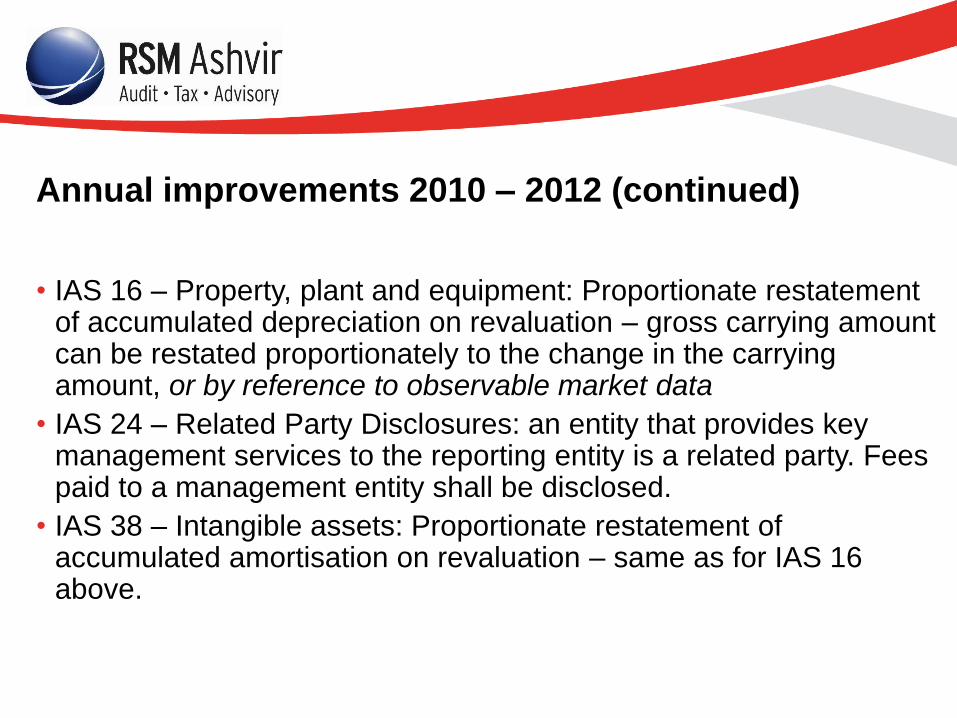

Annual improvements 2010 – 2012 (continued)

• IAS 16 – Property, plant and equipment: Proportionate restatement of accumulated depreciation on revaluation – gross carrying amount can be restated proportionately to the change in the carrying amount, or by reference to observable market data

• IAS 24 – Related Party Disclosures: an entity that provides key management services to the reporting entity is a related party. Fees paid to a management entity shall be disclosed.

• IAS 38 – Intangible assets: Proportionate restatement of accumulated amortisation on revaluation – same as for IAS 16 above.

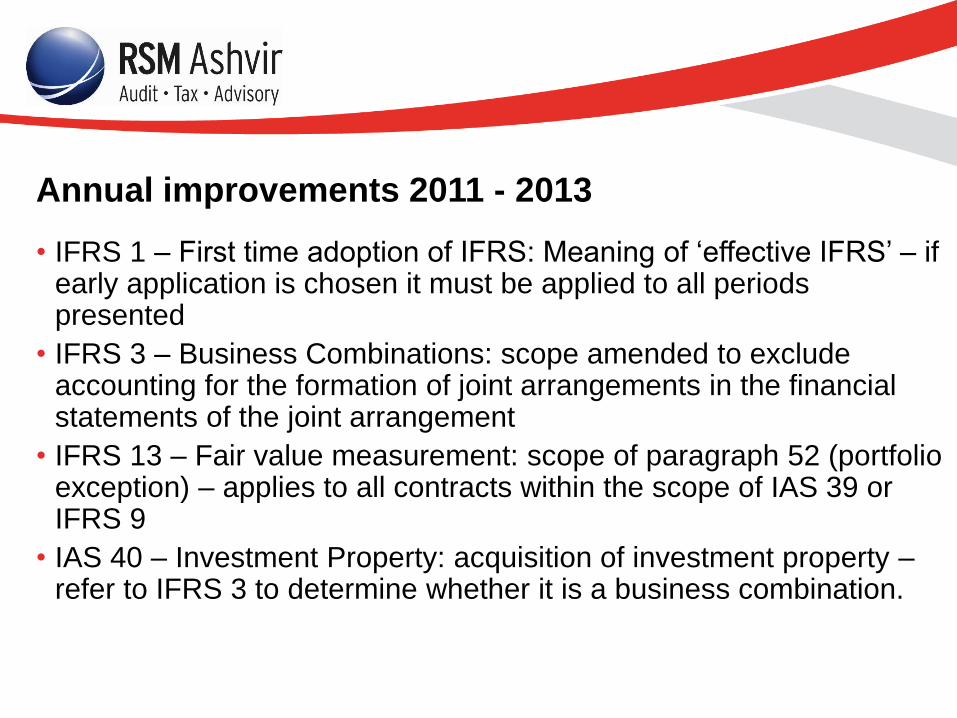

Annual improvements 2011 - 2013

• IFRS 1 – First time adoption of IFRS: Meaning of ‘effective IFRS’ – if early application is chosen it must be applied to all periods presented

• IFRS 3 – Business Combinations: scope amended to exclude accounting for the formation of joint arrangements in the financial statements of the joint arrangement

• IFRS 13 – Fair value measurement: scope of paragraph 52 (portfolio exception) – applies to all contracts within the scope of IAS 39 or IFRS 9

• IAS 40 – Investment Property: acquisition of investment property – refer to IFRS 3 to determine whether it is a business combination.

Changes effective from 1

January 2016

IFRS 14 – Regulatory deferral accounts

A “regulatory deferral account balance” is:

– The balance of any expense (or income) account that would not be recognised as an asset or a liability in accordance with other Standards, but that qualifies for deferral because it is included, or is expected to be included, by the rate regulator in establishing the rate(s) that can be charged to customers.

• Allows entities to continue to apply existing policy for regulatory deferral account balances, but specifies certain disclosures

IFRS 11 – Joint arrangements - Amendment

The amendment requires the acquirer of an interest in a joint operation in which the activity constitutes a business, as defined in IFRS 3 Business Combinations, to apply all of the principles on business combinations accounting in IFRS 3 and other IFRSs except for those principles that conflict with the guidance in IFRS 11. In addition, the acquirer shall disclose the information required by IFRS 3 and other IFRSs for business combinations.

IAS 16 and IAS 38 - Amendments

The amendments clarify that the use of revenue-based methods to calculate the depreciation of an asset is not appropriate because revenue generated by an activity that includes the use of an asset generally reflects factors other than the consumption of the economic benefits embodied in the asset.

The amendments also clarify that revenue is generally presumed to be an inappropriate basis for measuring the consumption of the economic benefits embodied in an intangible asset. This presumption however, can be rebutted in certain limited circumstances.

IAS 16 and IAS 41 – Bearer plants

The amendments define a bearer plant and include bearer plants within the scope of IAS 16. A bearer plant is defined as a living plant that is used in the production or supply of agricultural produce, is expected to bear produce for more than one period and has a remote likelihood of being sold as agricultural produce, except for incidental scrap sales. Previously, bearer plants were not defined and bearer plants related to agricultural activity were included within the scope of IAS 41.

IAS 16 and IAS 41 – Bearer plants (continued)

Bearer plants are used solely to grow produce. The only significant future economic benefits from bearer plants arise from selling the agricultural produce that they create. Bearer plants meet the definition of property, plant and equipment in IAS 16 and their operation is similar to that of manufacturing. Accordingly, the amendments require bearer plants to be accounted for as property, plant and equipment and included within the scope of IAS 16, instead of IAS 41.

The produce growing on bearer plants will remain within the scope of IAS 41.

IAS 27– Equity method in separate financial

statements

Allows a parent to account for investments in subsidiaries, joint ventures and associates using the equity method in its separate financial statements

IFRS 10 and IAS 28 – Sale or Contribution of Assets

between an Investor and its Associate or Joint Venture

Prior to the amendments, IFRS 10 required full gain or loss recognition on the loss of control of a subsidiary, whereas IAS 28 restricted the gain or loss resulting from the sale or contribution of assets to an associate or a joint venture to the extent of the interests that were attributable to unrelated investors in that associate or joint venture.

IFRS 10 and IAS 28 – Sale or Contribution of Assets

between an Investor and its Associate or Joint Venture

The amendments require that the full gain or loss on the sale of a group of assets that constitute a business (as defined by IFRS 3) to an associate or joint venture should be recognised.

On the other hand, if a subsidiary that does not constitute a business is sold to an associate or joint venture, the gain or loss recognised should be restricted to the extent of the interests that were attributable to unrelated investors in that associate or joint venture.

Annual improvements 2012 - 2014

• IFRS 5 – clarifies that when an entity reclassifies an asset (or disposal group) directly from held for sale to held for distribution to owners (or vice versa), such a reclassification shall not be treated as a change to a plan of sale (or distribution to owners) and an entity shall not follow the guidance in paragraphs 27–29 of IFRS 5 to account for this change. The amendments also clarify that an entity should cease to apply held-for-distribution accounting in the same way as it ceases to apply the held-for-sale accounting when it no longer meets the held-for-sale criteria.

Annual improvements 2012 – 2014 (continued)

• IFRS 7 – additional guidance on how to determine whether a service contract gives rise to ‘continuing involvement’ in a derecognised financial asset

• IFRS 7 - clarification that the additional disclosure required by the amendments to IFRS 7 concerning offsetting is not specifically required for all interim periods.

• IAS 19 - clarification that the depth of the market for high quality corporate bonds should be assessed at a currency level (not country level as previously required).

IAS 1 – Disclosure initiative

• Additional guidance on aggregation and materiality

• Emphasis that an entity need not provide a specific disclosure required by an IFRS if the information resulting from that disclosure is not material

• Notes can be presented in a way that gives prominence to the areas of its activities that the entity considers to be most relevant to an understanding of its financial performance and financial position, such as grouping together information about particular operating activities, rather that presenting them in the order they appear in the primary financial statements

IFRS 10, IFRS 12, and IAS 28 – Investment entities:

applying the consolidation exception

• Extends the exemption from consolidation given in paragraph 4 of IFRS 10, and from applying the equity method given in paragraph 17 of IAS 28, to subsidiaries (which are themselves parents) of parents that are investment entities that do not prepare consolidated financial statements

Changes effective from 1

January 2017

IFRS 15 – Revenue from contracts with customers

• A single, principle-based revenue standard – 5 step process

• Issued in May 2014, simultaneously with an identical standard issued by FASB

• Will replace IAS 18 and IAS 11 and related interpretations

• Early application permitted

IFRS 15 – Revenue from contracts with customers

Scope – all contracts with customers, except:

• Leases

• Insurance

• Financial instruments

• Non-monetary exchanges (e.g. Oil swaps)

IFRS 15 – Revenue from contracts with customers

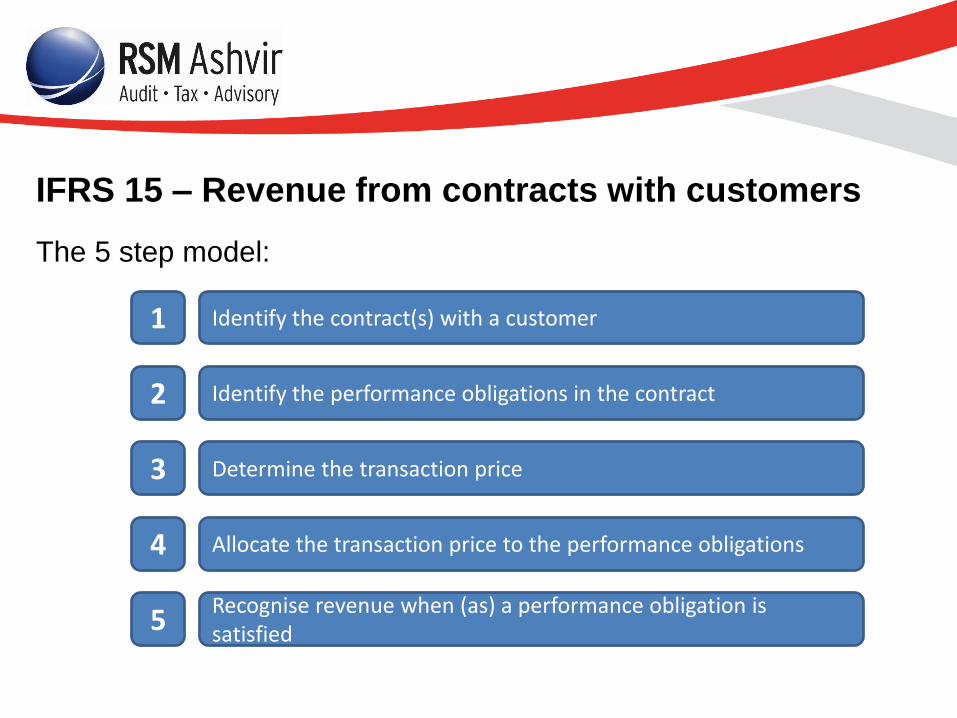

The 5 step model:

Identify the contract(s) with a customer

Identify the performance obligations in the contract

Determine the transaction price

Allocate the transaction price to the performance obligations

Recognise revenue when (as) a performance obligation is satisfied

1

2

3

4

5

IFRS 15 – Revenue from contracts with customers

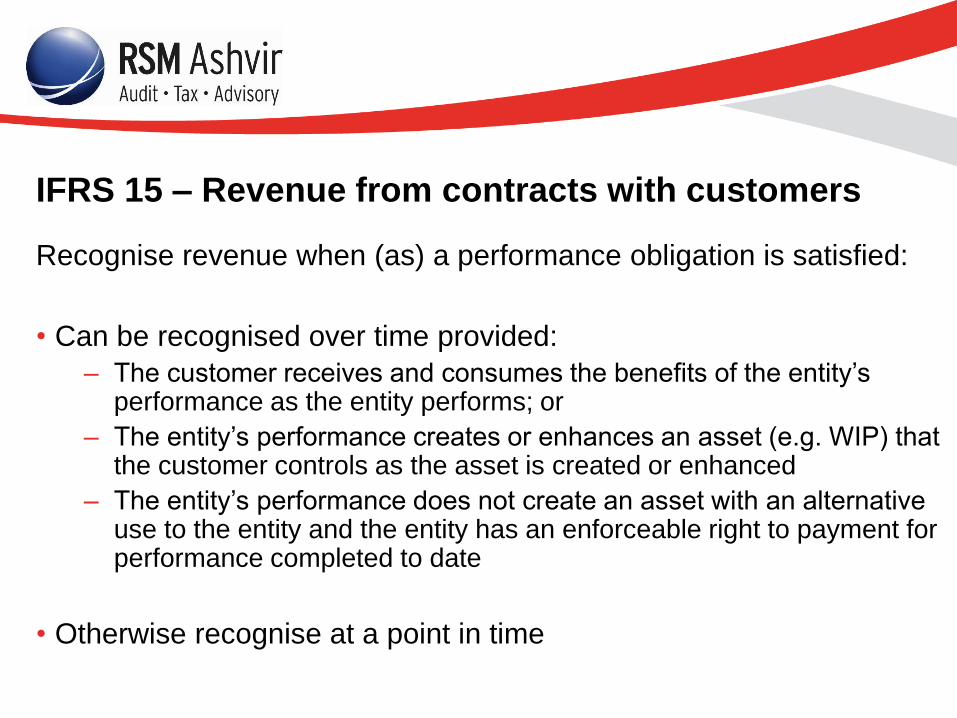

Recognise revenue when (as) a performance obligation is satisfied:

• Can be recognised over time provided:

– The customer receives and consumes the benefits of the entity’s performance as the entity performs; or

– The entity’s performance creates or enhances an asset (e.g. WIP) that the customer controls as the asset is created or enhanced

– The entity’s performance does not create an asset with an alternative use to the entity and the entity has an enforceable right to payment for performance completed to date

• Otherwise recognise at a point in time

IFRS 15 – Revenue from contracts with customers

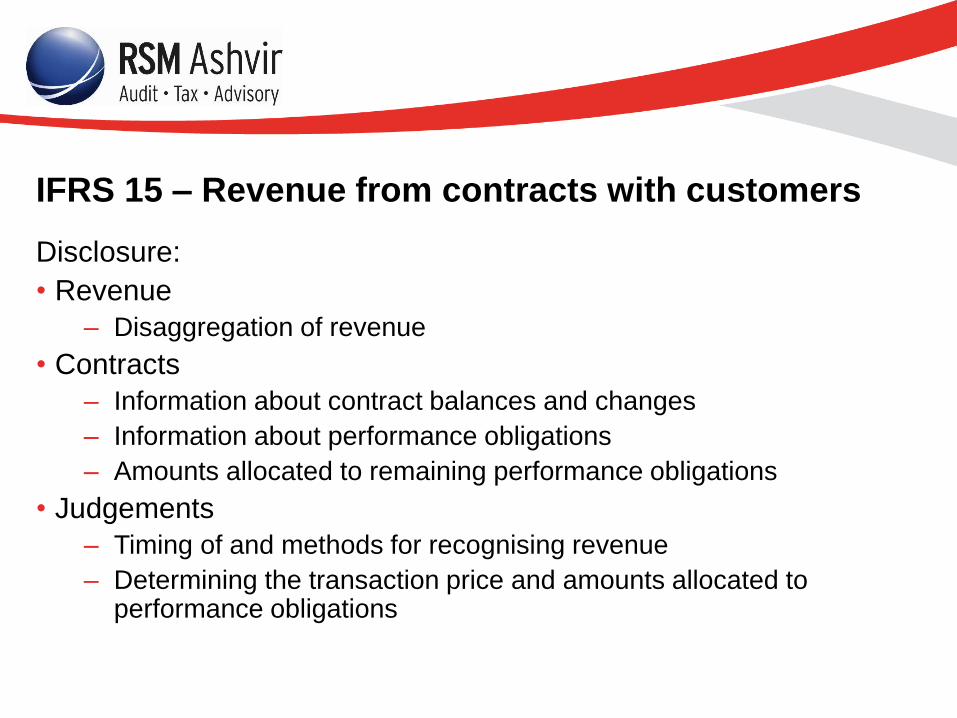

Disclosure:

• Revenue

– Disaggregation of revenue

• Contracts

– Information about contract balances and changes

– Information about performance obligations

– Amounts allocated to remaining performance obligations

• Judgements

– Timing of and methods for recognising revenue

– Determining the transaction price and amounts allocated to performance obligations

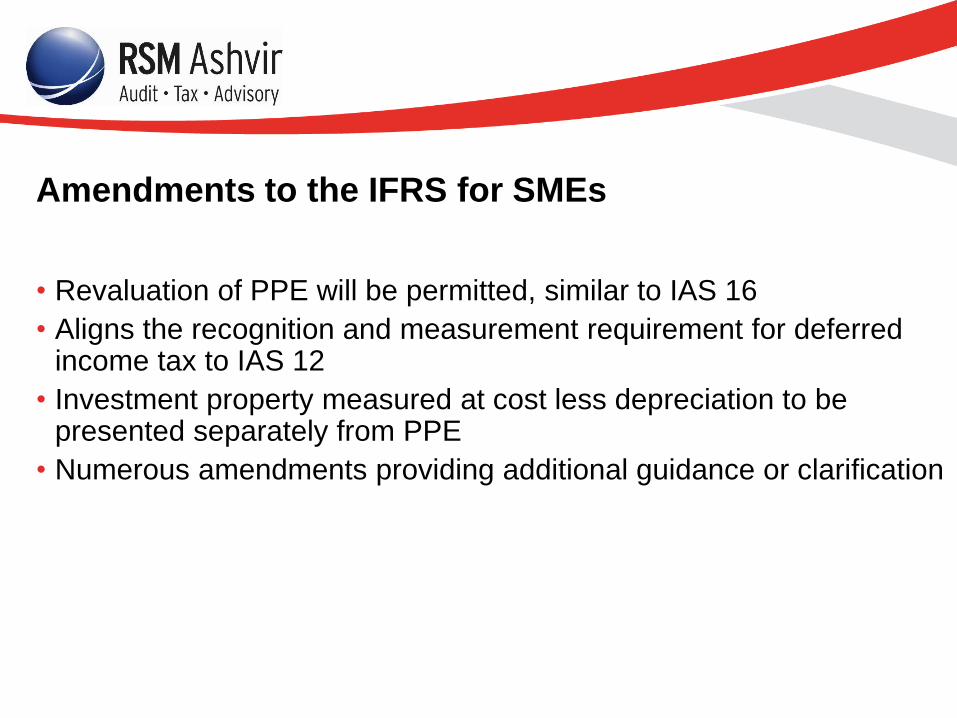

Amendments to the IFRS for SMEs

• Revaluation of PPE will be permitted, similar to IAS 16

• Aligns the recognition and measurement requirement for deferred income tax to IAS 12

• Investment property measured at cost less depreciation to be presented separately from PPE

• Numerous amendments providing additional guidance or clarification

Changes effective from 1

January 2018

IFRS 9 – Financial instruments

• IFRS 9 will replace IAS 39 in its entirety

• Complete version (including hedge accounting and impairment) issued in July 2014

• Effective date – accounting periods beginning on or after 1 January 2018

• More ‘principles based’ than IAS 39

IFRS 9 – Financial instruments

• Classification based on business model and nature of cash flows

• Business model-driven reclassification

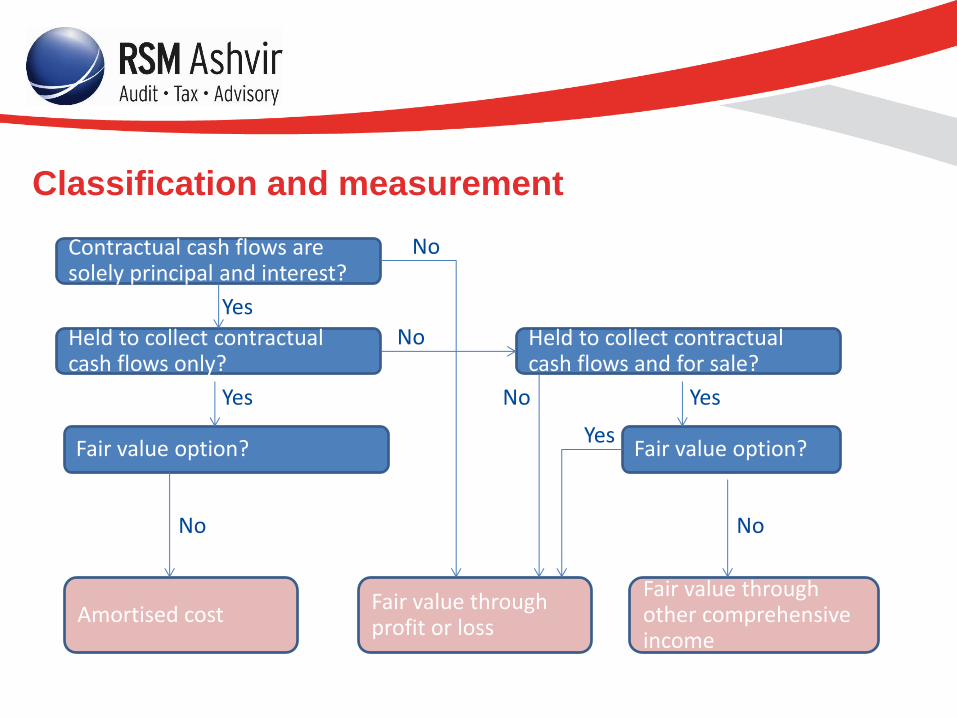

Classification and measurement

Contractual cash flows are solely principal and interest?

Held to collect contractual cash flows only?

Held to collect contractual cash flows and for sale?

Fair value option?

Amortised cost Fair value through profit or loss

Fair value through other comprehensive income

Fair value option?

Yes

No

No

Yes

No

Yes No

No

Yes

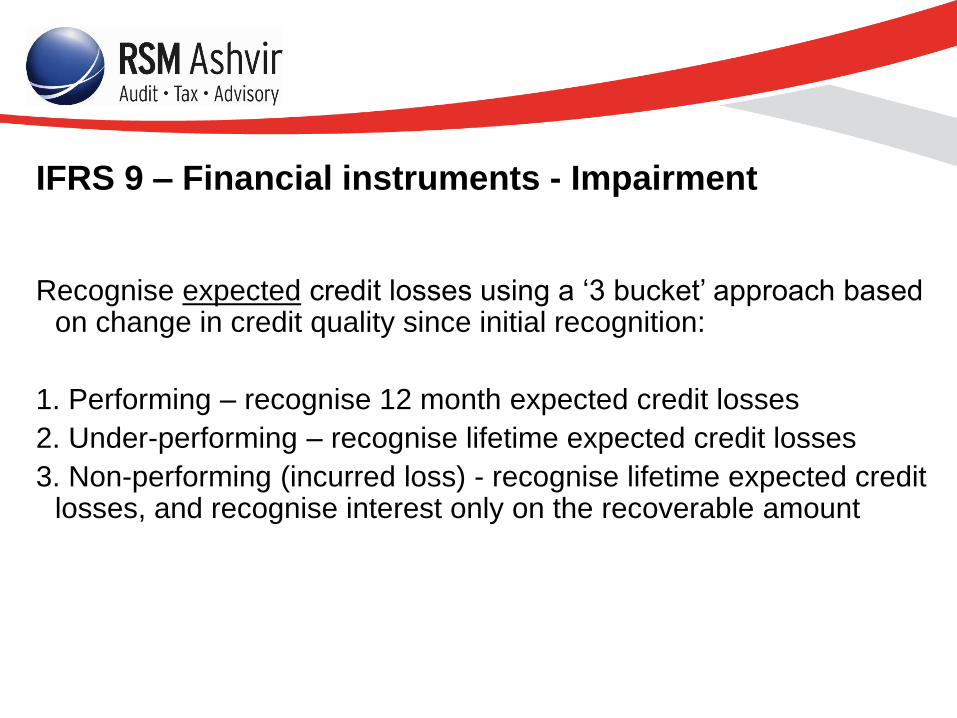

IFRS 9 – Financial instruments - Impairment

Recognise expected credit losses using a ‘3 bucket’ approach based on change in credit quality since initial recognition:

1. Performing – recognise 12 month expected credit losses

2. Under-performing – recognise lifetime expected credit losses

3. Non-performing (incurred loss) - recognise lifetime expected credit losses, and recognise interest only on the recoverable amount

IFRS 9 – Financial instruments – hedge accounting

• Links economics of risk management with accounting treatment

• Reduces accounting considerations that affect risk management decisions

• Easier to qualify for hedge accounting

• Ability to account for more hedges of non-financial items

What does the future hold?

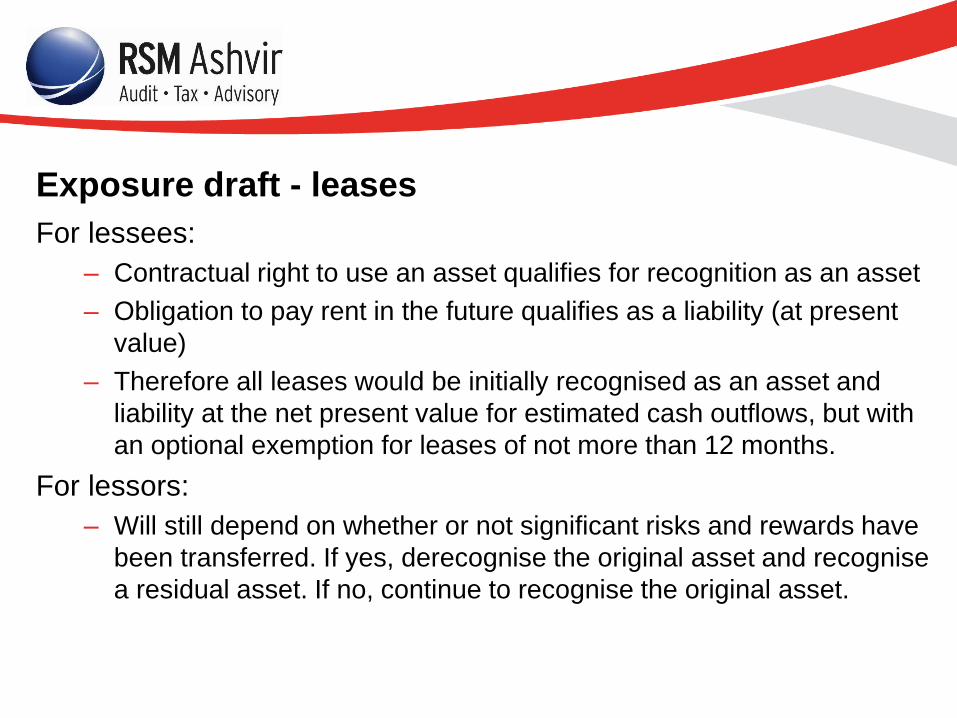

Exposure draft - leases

For lessees:

– Contractual right to use an asset qualifies for recognition as an asset

– Obligation to pay rent in the future qualifies as a liability (at present

value)

– Therefore all leases would be initially recognised as an asset and

liability at the net present value for estimated cash outflows, but with

an optional exemption for leases of not more than 12 months.

For lessors:

– Will still depend on whether or not significant risks and rewards have

been transferred. If yes, derecognise the original asset and recognise

a residual asset. If no, continue to recognise the original asset.

Exposure draft - Insurance

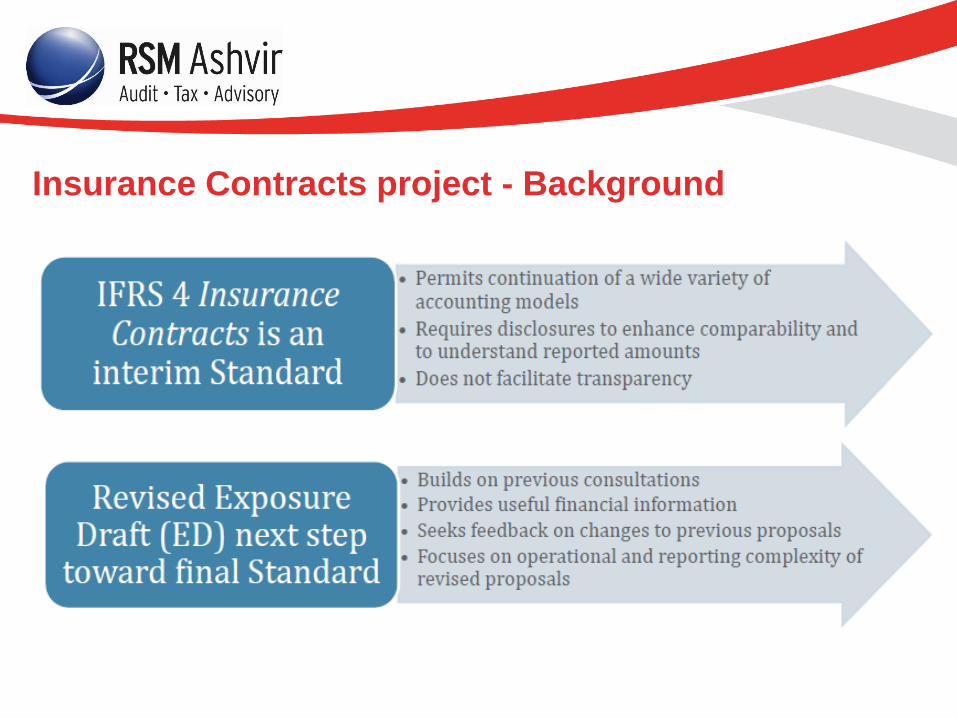

Insurance Contracts project - Background

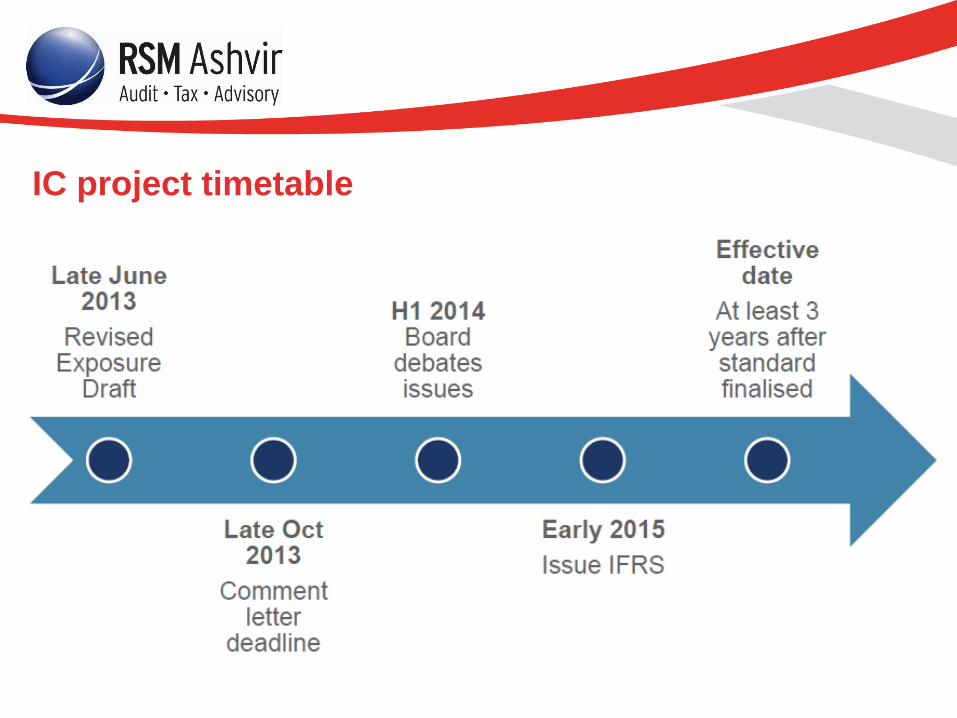

IC project timetable

Review of the Conceptual framework

• The Conceptual Framework sets out the concepts that underlie the

preparation and presentation of financial statements. It is a

practical tool that assists the IASB when developing and revising

IFRSs. The objective of the Conceptual Framework project is to

improve financial reporting by providing the IASB with a complete

and updated set of concepts to use when it develops or revises

standards

Review of the Conceptual framework

Discussion paper (issued July 2013) dealt with, inter alia:

– Definitions of assets and liabilities

– Guidance on appropriate measurement bases

– Meaning of Other Comprehensive Income, and when to recycle

– Objectives of disclosures

Closed for comments in January 2014. IASB is deliberating.

Thank you Any questions?