acc 424 financial reporting ii lecture 13 accounting for derivative financial instruments

TRANSCRIPT

ACC 424Financial Reporting II

Lecture 13

Accounting for

Derivative financial instruments

2

Agenda

• Derivative financial instruments• FASB 133• Examples of accounting for

– Futures contracts

– Options

– Financial swaps

– Currency swaps

– Interest rate swaps

• Disclosure requirements

3

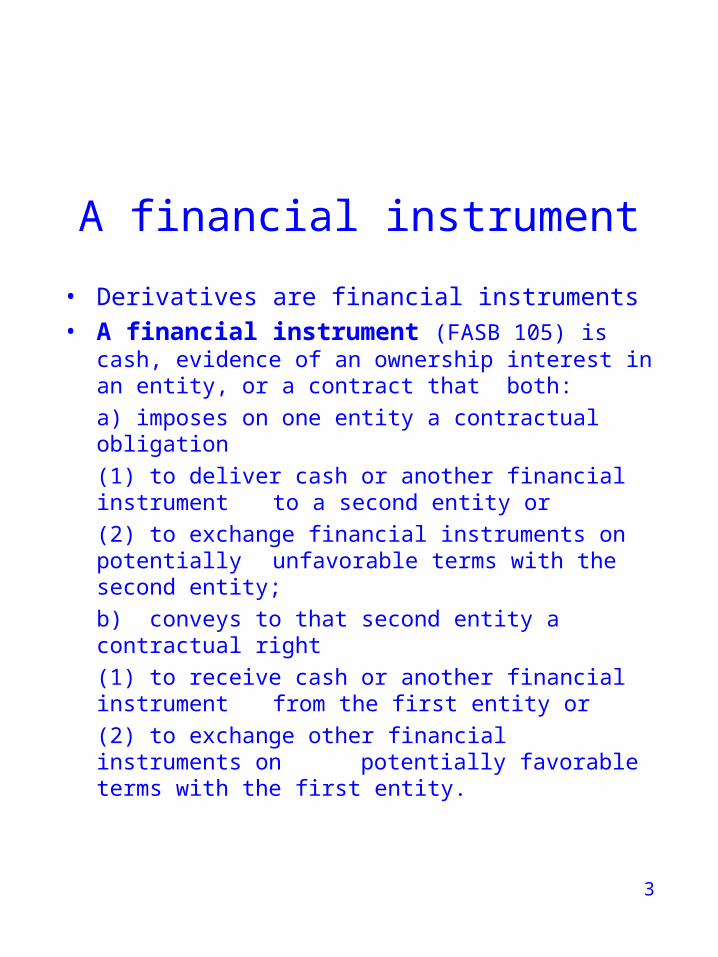

A financial instrument

• Derivatives are financial instruments • A financial instrument (FASB 105) is cash, evidence

of an ownership interest in an entity, or a contract that both:

a) imposes on one entity a contractual obligation

(1) to deliver cash or another financial instrument to a second entity or

(2) to exchange financial instruments on potentially unfavorable terms with the second entity;

b) conveys to that second entity a contractual right

(1) to receive cash or another financial instrument from the first entity or

(2) to exchange other financial instruments on potentially favorable terms with the

first entity.

4

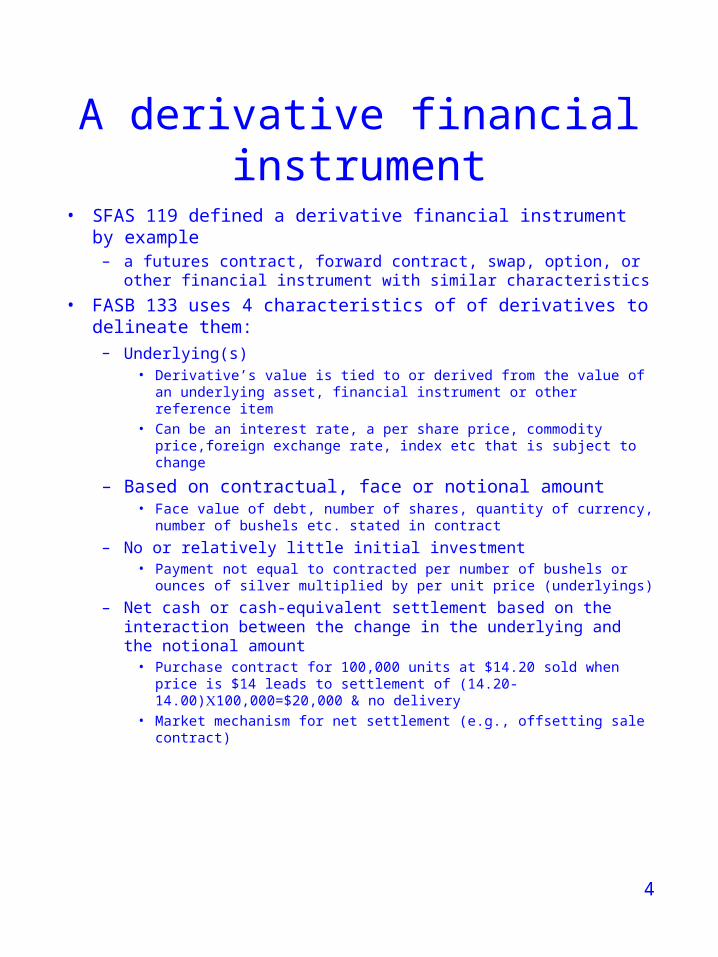

A derivative financial instrument

• SFAS 119 defined a derivative financial instrument by example

– a futures contract, forward contract, swap, option, or other financial instrument with similar characteristics

• FASB 133 uses 4 characteristics of of derivatives to delineate them:

– Underlying(s) • Derivative’s value is tied to or derived from the value of an

underlying asset, financial instrument or other reference item• Can be an interest rate, a per share price, commodity price,foreign

exchange rate, index etc that is subject to change

– Based on contractual, face or notional amount• Face value of debt, number of shares, quantity of currency, number

of bushels etc. stated in contract

– No or relatively little initial investment• Payment not equal to contracted per number of bushels or ounces of

silver multiplied by per unit price (underlyings)

– Net cash or cash-equivalent settlement based on the interaction between the change in the underlying and the notional amount

• Purchase contract for 100,000 units at $14.20 sold when price is $14 leads to settlement of (14.20-14.00)100,000=$20,000 & no delivery

• Market mechanism for net settlement (e.g., offsetting sale contract)

5

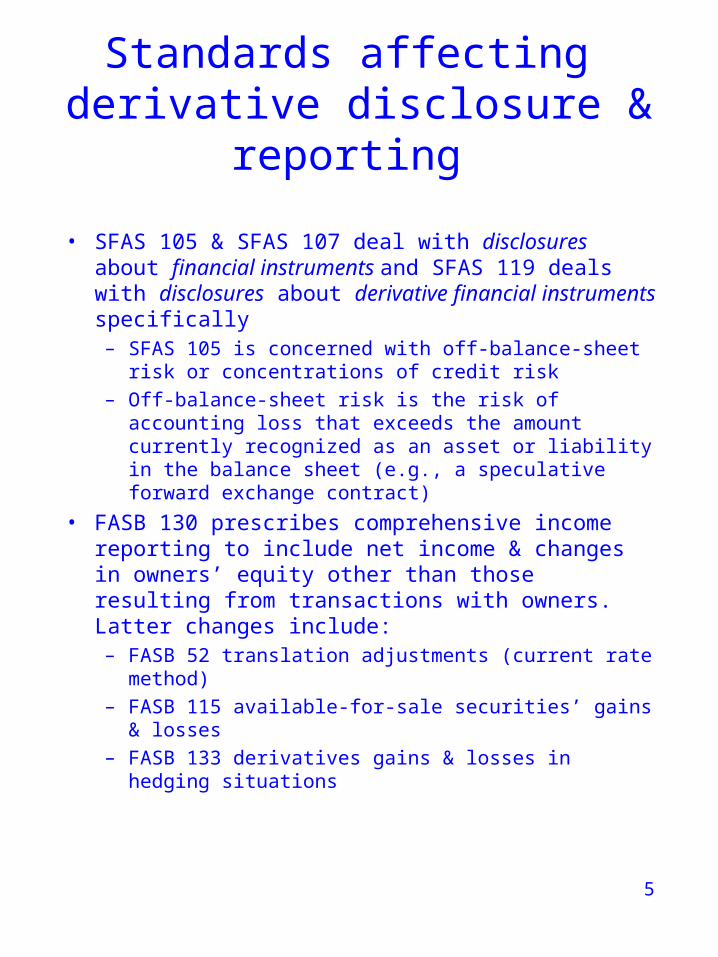

Standards affecting derivative disclosure & reporting

• SFAS 105 & SFAS 107 deal with disclosures about financial instruments and SFAS 119 deals with disclosures about derivative financial instruments specifically

– SFAS 105 is concerned with off-balance-sheet risk or concentrations of credit risk

– Off-balance-sheet risk is the risk of accounting loss that exceeds the amount currently recognized as an asset or liability in the balance sheet (e.g., a speculative forward exchange contract)

• FASB 130 prescribes comprehensive income reporting to include net income & changes in owners’ equity other than those resulting from transactions with owners. Latter changes include:

– FASB 52 translation adjustments (current rate method)– FASB 115 available-for-sale securities’ gains & losses – FASB 133 derivatives gains & losses in hedging

situations

6

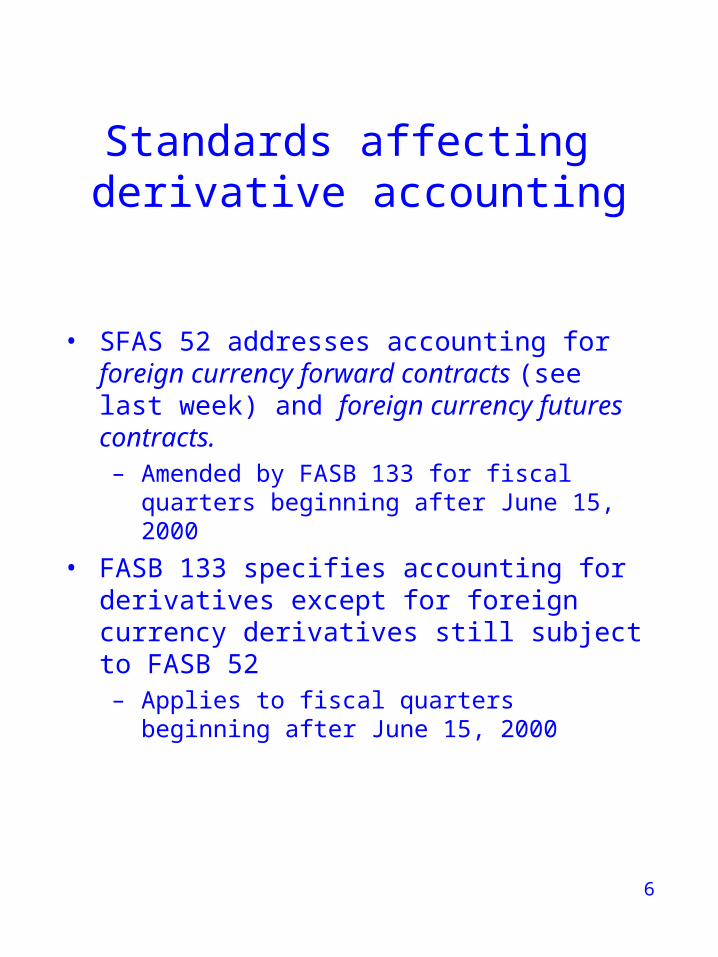

Standards affecting derivative accounting

• SFAS 52 addresses accounting for foreign currency forward contracts (see last week) and foreign currency futures contracts. – Amended by FASB 133 for fiscal quarters beginning

after June 15, 2000

• FASB 133 specifies accounting for derivatives except for foreign currency derivatives still subject to FASB 52– Applies to fiscal quarters beginning after June 15,

2000

7

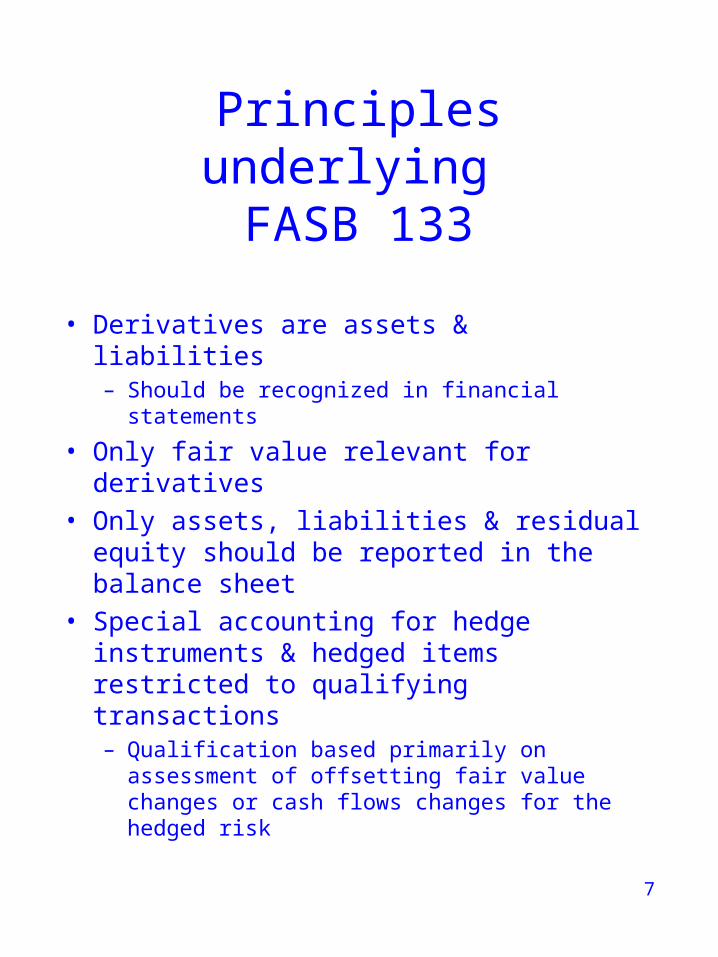

Principles underlying FASB 133

• Derivatives are assets & liabilities– Should be recognized in financial statements

• Only fair value relevant for derivatives

• Only assets, liabilities & residual equity should be reported in the balance sheet

• Special accounting for hedge instruments & hedged items restricted to qualifying transactions– Qualification based primarily on assessment of

offsetting fair value changes or cash flows changes for the hedged risk

8

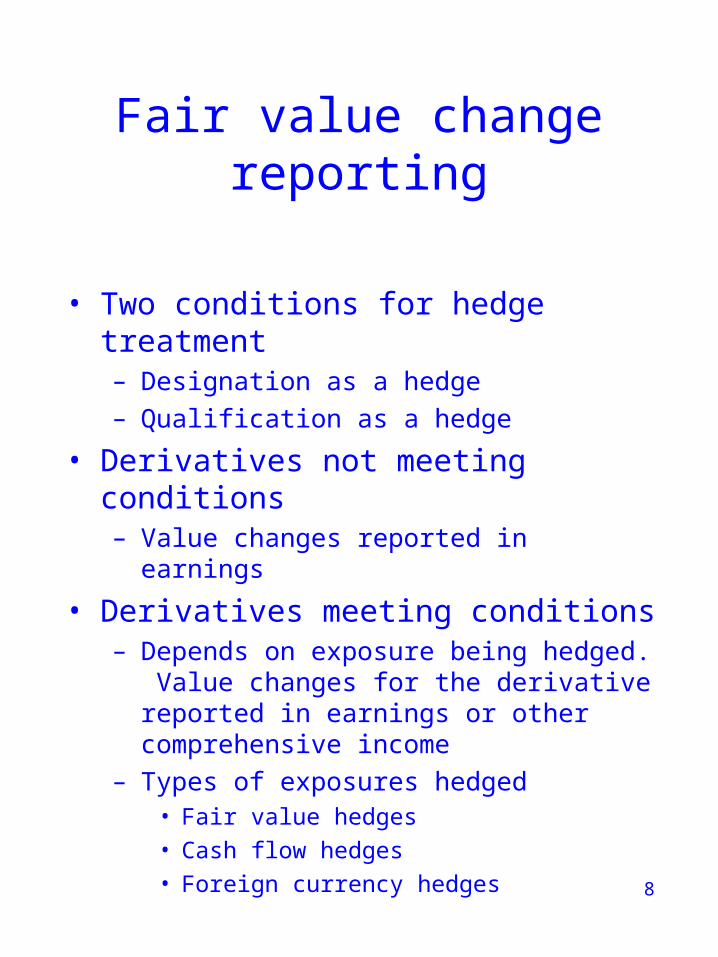

Fair value change reporting

• Two conditions for hedge treatment– Designation as a hedge

– Qualification as a hedge

• Derivatives not meeting conditions– Value changes reported in earnings

• Derivatives meeting conditions– Depends on exposure being hedged. Value

changes for the derivative reported in earnings or other comprehensive income

– Types of exposures hedged• Fair value hedges

• Cash flow hedges

• Foreign currency hedges

9

Derivatives meeting hedge treatment conditions

• Fair value hedges of existing assets liabilities & firm commitments not otherwise recognized under GAAP

– Derivative value changes reported in earnings concurrent with offsetting change in value of hedged item

– Changes in value of hedge item that are not offset by derivative value changes reported in earnings when they occur

• Cash flow hedges. Hedges of cash flows expected from forecasted or probably anticipated transactions

– Portion of derivative change effective in hedging risk initially reported in other comprehensive income & reclassified to earnings during the period in which the forecasted transaction affects earnings

– Portion of change not effective in hedging risk reported to earnings directly

• Foreign currency hedges. Hedges of foreign currency denominated firm commitments and forecasted transactions, available-for-sale (AFS) securities & net investments in foreign operations

– Commitments & AFS value changes reported in earnings– Forecasted transactions & investment in foreign operations

value changes reported in other comprehensive income

10

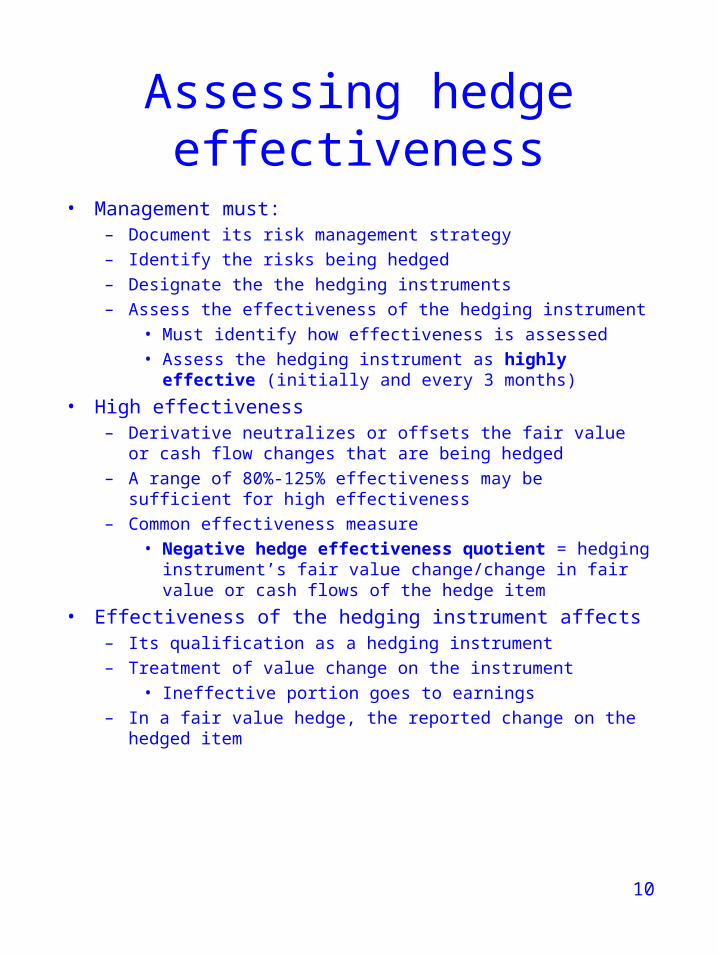

Assessing hedge effectiveness

• Management must:– Document its risk management strategy

– Identify the risks being hedged

– Designate the the hedging instruments

– Assess the effectiveness of the hedging instrument

• Must identify how effectiveness is assessed

• Assess the hedging instrument as highly effective (initially and every 3 months)

• High effectiveness– Derivative neutralizes or offsets the fair value or cash flow changes

that are being hedged

– A range of 80%-125% effectiveness may be sufficient for high effectiveness

– Common effectiveness measure

• Negative hedge effectiveness quotient = hedging instrument’s fair value change/change in fair value or cash flows of the hedge item

• Effectiveness of the hedging instrument affects– Its qualification as a hedging instrument

– Treatment of value change on the instrument

• Ineffective portion goes to earnings

– In a fair value hedge, the reported change on the hedged item

11

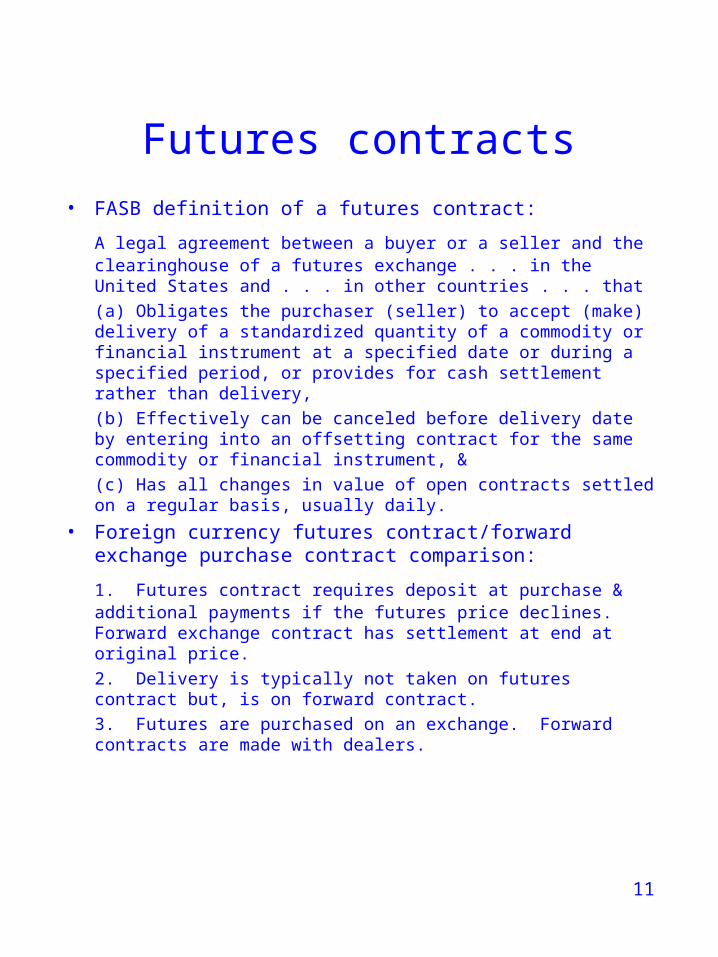

Futures contracts

• FASB definition of a futures contract:

A legal agreement between a buyer or a seller and the clearinghouse of a futures exchange . . . in the United States and . . . in other countries . . . that

(a) Obligates the purchaser (seller) to accept (make) delivery of a standardized quantity of a commodity or financial instrument at a specified date or during a specified period, or provides for cash settlement rather than delivery,

(b) Effectively can be canceled before delivery date by entering into an offsetting contract for the same commodity or financial instrument, &

(c) Has all changes in value of open contracts settled on a regular basis, usually daily.

• Foreign currency futures contract/forward exchange purchase contract comparison:

1. Futures contract requires deposit at purchase & additional payments if the futures price declines. Forward exchange contract has settlement at end at original price.

2. Delivery is typically not taken on futures contract but, is on forward contract.

3. Futures are purchased on an exchange. Forward contracts are made with dealers.

12

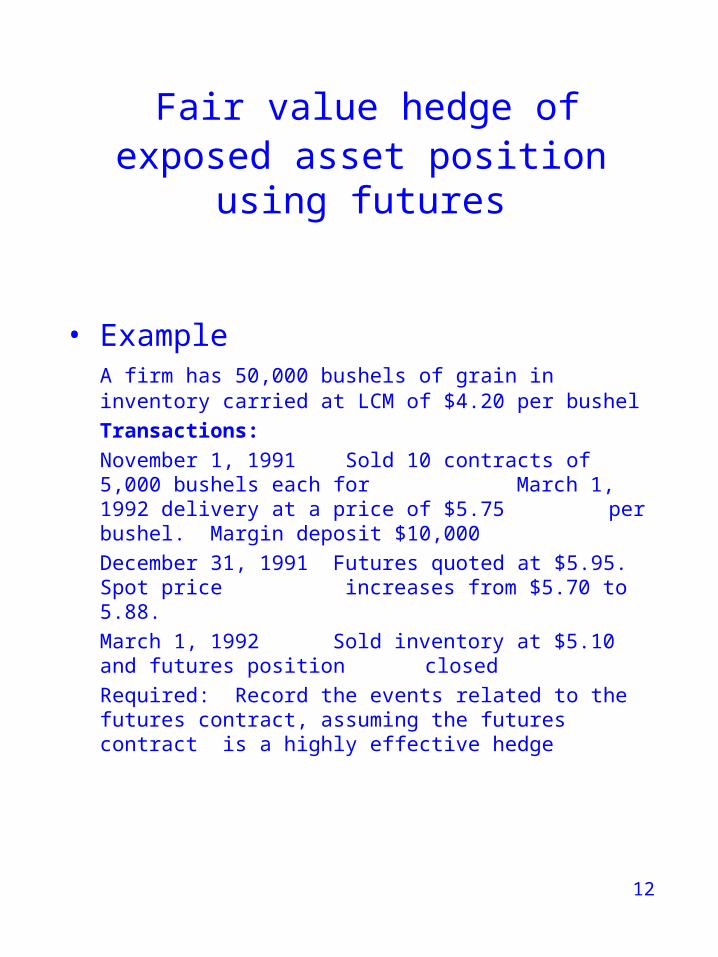

Fair value hedge of exposed asset position using futures

• ExampleA firm has 50,000 bushels of grain in inventory carried at LCM of $4.20 per bushel

Transactions:

November 1, 1991 Sold 10 contracts of 5,000 bushels each for March 1, 1992 delivery at a price of

$5.75 per bushel. Margin deposit $10,000

December 31, 1991 Futures quoted at $5.95. Spot price increases from $5.70 to

5.88.

March 1, 1992 Sold inventory at $5.10 and futures position closed

Required: Record the events related to the futures contract, assuming the futures contract is a highly effective hedge

13

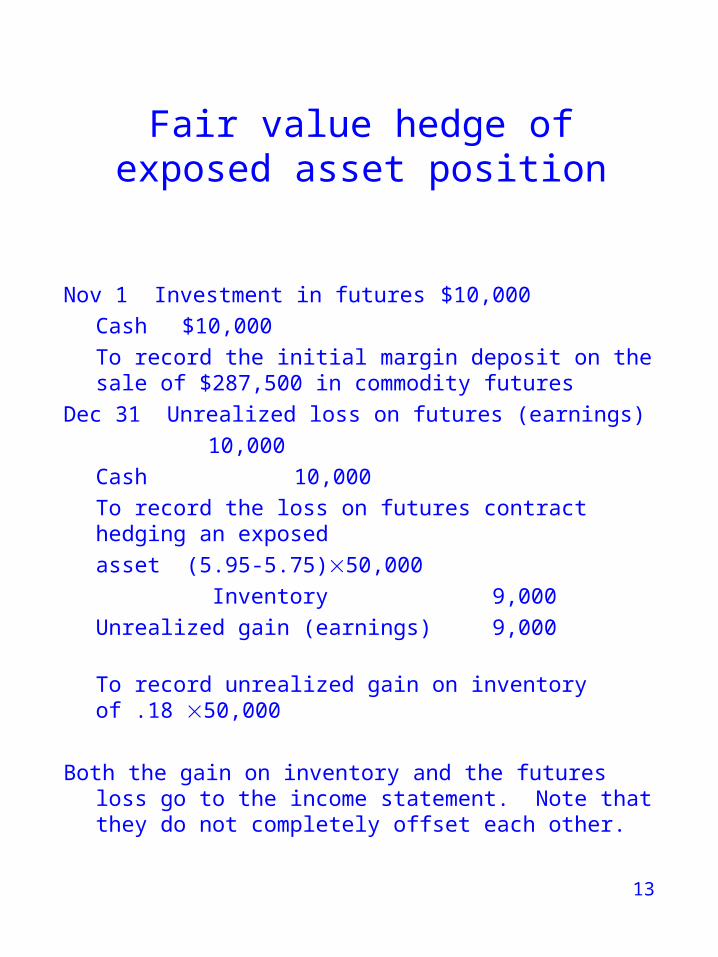

Fair value hedge of exposed asset position

Nov 1 Investment in futures $10,000

Cash $10,000

To record the initial margin deposit on the sale of $287,500 in commodity futures

Dec 31 Unrealized loss on futures (earnings)

10,000

Cash 10,000

To record the loss on futures contract hedging an exposed

asset (5.95-5.75)50,000

Inventory 9,000

Unrealized gain (earnings) 9,000

To record unrealized gain on inventory of .18 50,000

Both the gain on inventory and the futures loss go to the income statement. Note that they do not completely offset each other.

14

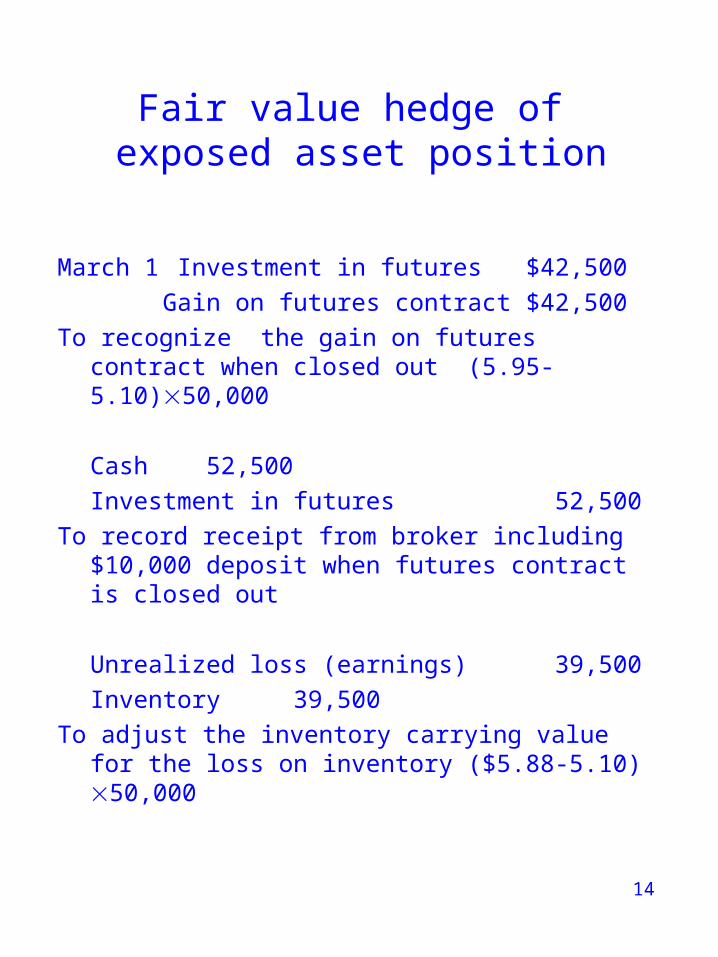

Fair value hedge of exposed asset position

March 1 Investment in futures $42,500

Gain on futures contract $42,500

To recognize the gain on futures contract when closed out (5.95-5.10)50,000

Cash 52,500

Investment in futures 52,500

To record receipt from broker including $10,000 deposit when futures contract is closed out

Unrealized loss (earnings) 39,500

Inventory 39,500

To adjust the inventory carrying value for the loss on inventory ($5.88-5.10) 50,000

15

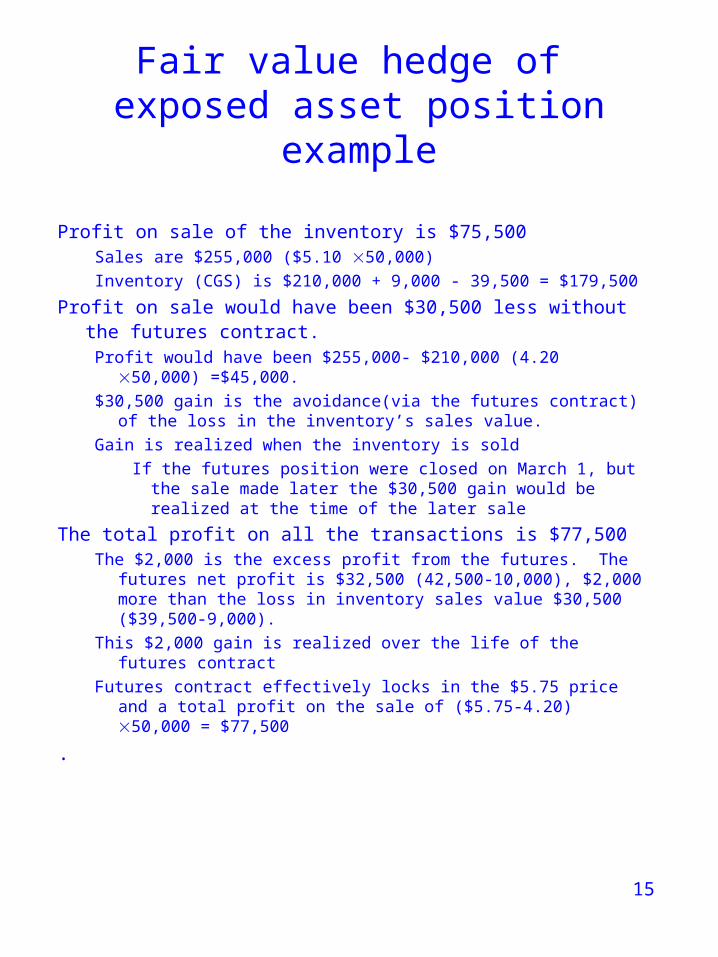

Fair value hedge of exposed asset position example

Profit on sale of the inventory is $75,500Sales are $255,000 ($5.10 50,000)

Inventory (CGS) is $210,000 + 9,000 - 39,500 = $179,500

Profit on sale would have been $30,500 less without the futures contract.

Profit would have been $255,000- $210,000 (4.20 50,000) =$45,000.

$30,500 gain is the avoidance(via the futures contract) of the loss in the inventory’s sales value.

Gain is realized when the inventory is sold

If the futures position were closed on March 1, but the sale made later the $30,500 gain would be realized at the time of the later sale

The total profit on all the transactions is $77,500The $2,000 is the excess profit from the futures. The futures net

profit is $32,500 (42,500-10,000), $2,000 more than the loss in inventory sales value $30,500 ($39,500-9,000).

This $2,000 gain is realized over the life of the futures contract

Futures contract effectively locks in the $5.75 price and a total profit on the sale of ($5.75-4.20) 50,000 = $77,500

.

16

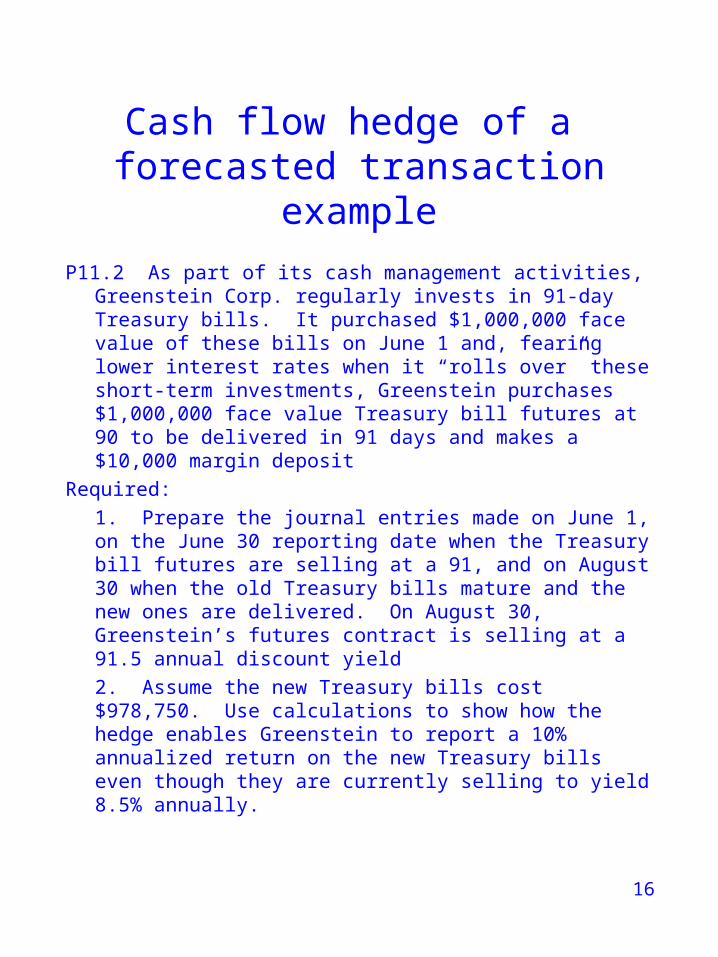

Cash flow hedge of a forecasted transaction example

P11.2 As part of its cash management activities, Greenstein Corp. regularly invests in 91-day Treasury bills. It purchased $1,000,000 face value of these bills on June 1 and, fearing lower interest rates when it “rolls over” these short-term investments, Greenstein purchases $1,000,000 face value Treasury bill futures at 90 to be delivered in 91 days and makes a $10,000 margin deposit

Required:

1. Prepare the journal entries made on June 1, on the June 30 reporting date when the Treasury bill futures are selling at a 91, and on August 30 when the old Treasury bills mature and the new ones are delivered. On August 30, Greenstein’s futures contract is selling at a 91.5 annual discount yield

2. Assume the new Treasury bills cost $978,750. Use calculations to show how the hedge enables Greenstein to report a 10% annualized return on the new Treasury bills even though they are currently selling to yield 8.5% annually.

17

Cash flow hedge of a forecasted transaction example

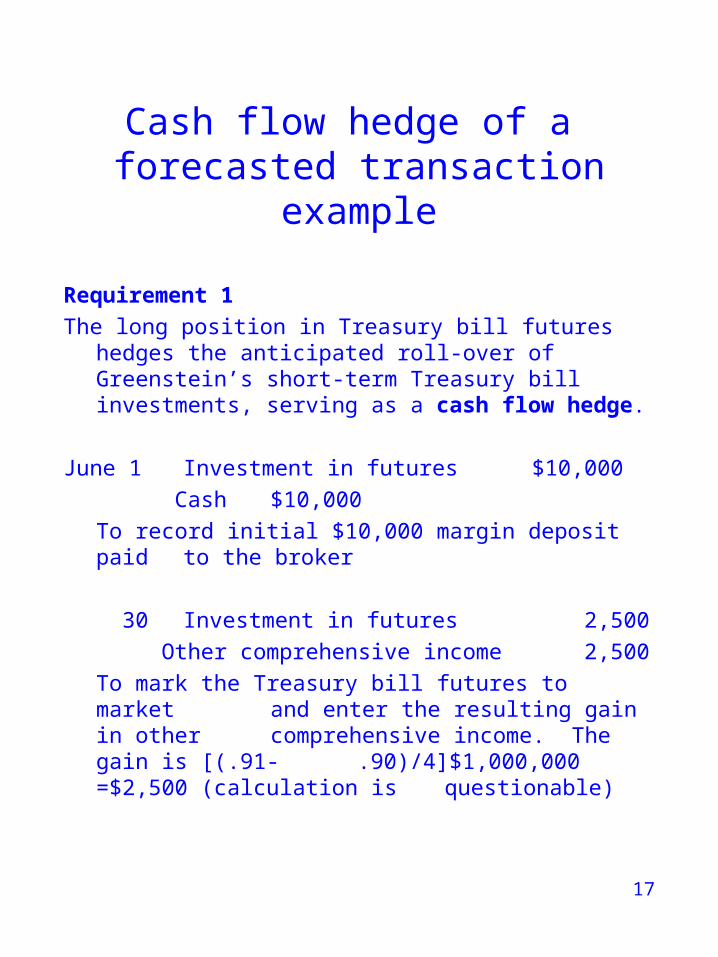

Requirement 1

The long position in Treasury bill futures hedges the anticipated roll-over of Greenstein’s short-term Treasury bill investments, serving as a cash flow hedge.

June 1 Investment in futures $10,000

Cash $10,000

To record initial $10,000 margin deposit paid to the broker

30 Investment in futures 2,500

Other comprehensive income 2,500

To mark the Treasury bill futures to market and enter the resulting gain in other

comprehensive income. The gain is [(.91- .90)/4]$1,000,000 =$2,500 (calculation is questionable)

18

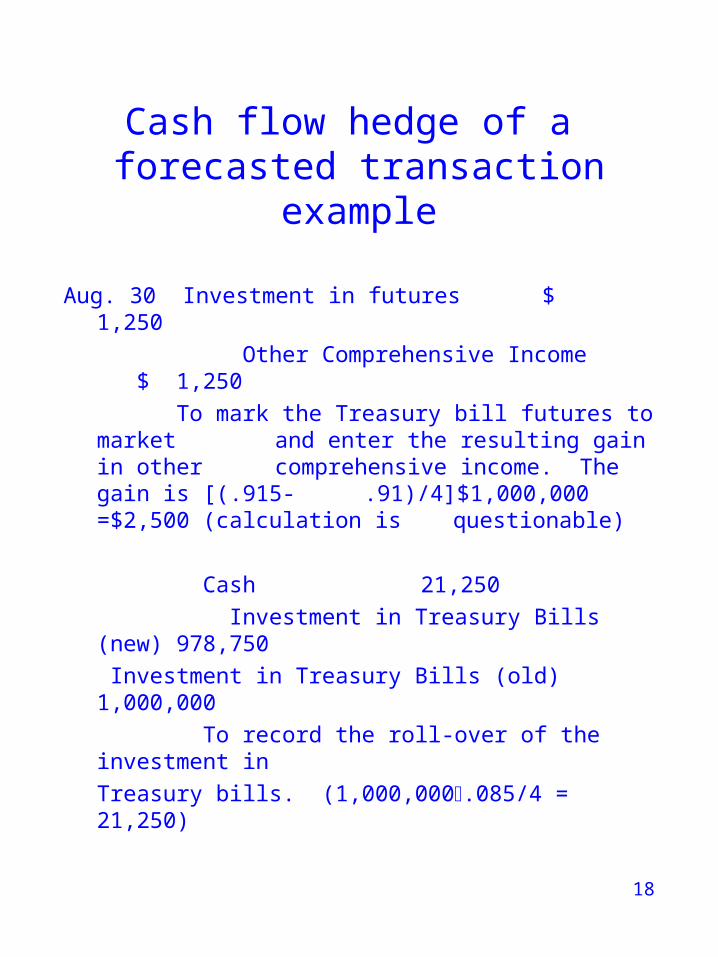

Cash flow hedge of a forecasted transaction example

Aug. 30 Investment in futures $ 1,250

Other Comprehensive Income $ 1,250

To mark the Treasury bill futures to market and enter the resulting gain in other

comprehensive income. The gain is [(.915- .91)/4]$1,000,000 =$2,500 (calculation is questionable)

Cash 21,250

Investment in Treasury Bills (new) 978,750

Investment in Treasury Bills (old) 1,000,000

To record the roll-over of the investment in

Treasury bills. (1,000,000.085/4 = 21,250)

19

Cash flow hedge of a forecasted transaction example

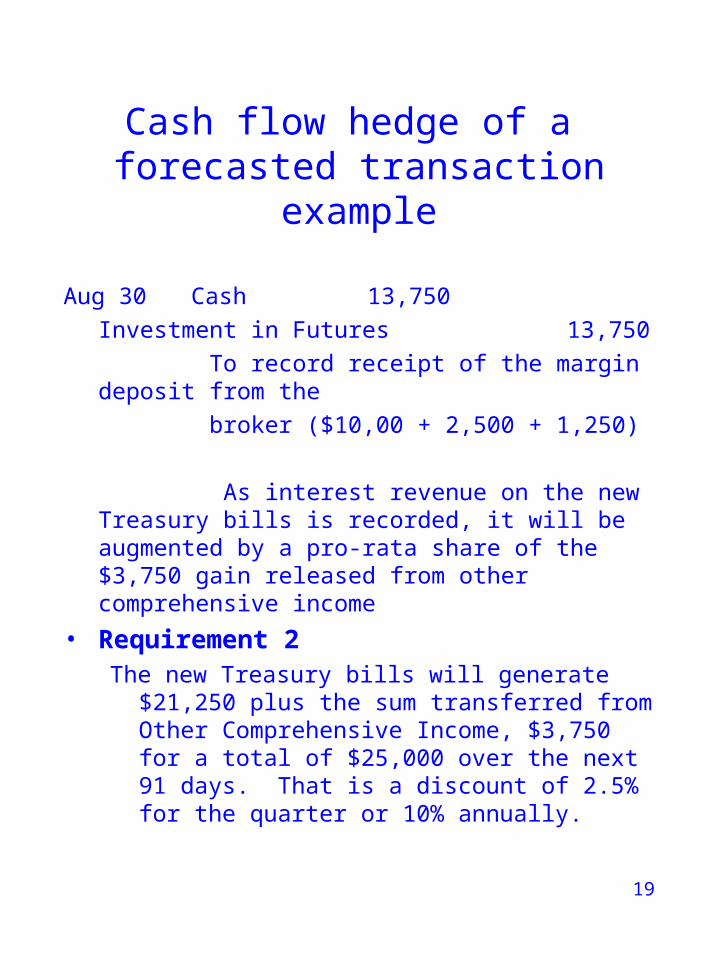

Aug 30 Cash 13,750

Investment in Futures 13,750

To record receipt of the margin deposit from the

broker ($10,00 + 2,500 + 1,250)

As interest revenue on the new Treasury bills is recorded, it will be augmented by a pro-rata share of the $3,750 gain released from other comprehensive income

• Requirement 2The new Treasury bills will generate $21,250 plus the

sum transferred from Other Comprehensive Income, $3,750 for a total of $25,000 over the next 91 days. That is a discount of 2.5% for the quarter or 10% annually.

20

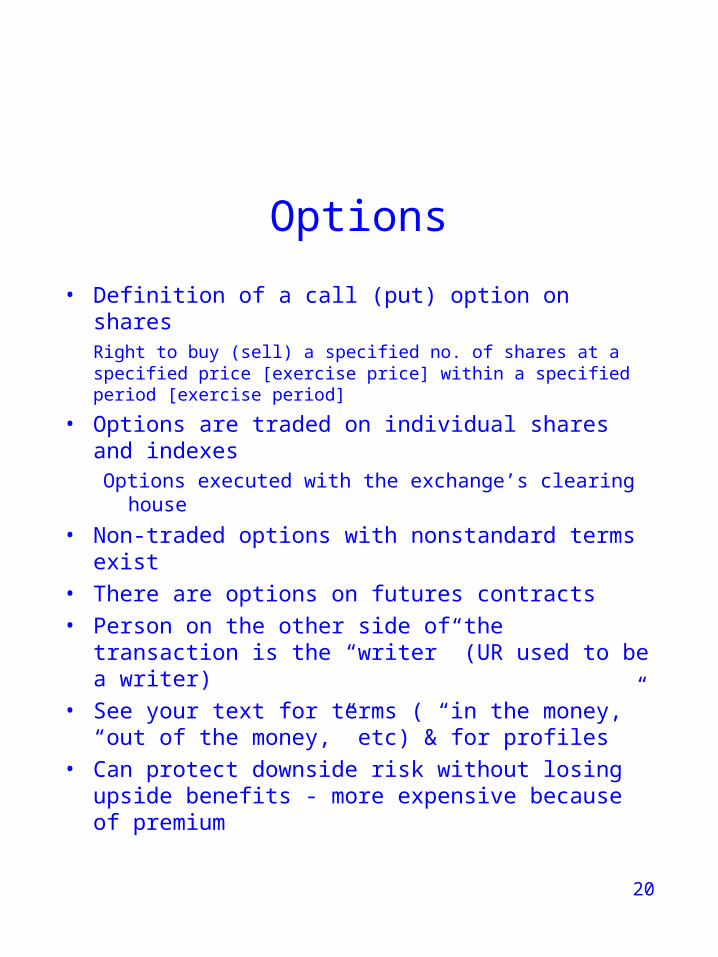

Options

• Definition of a call (put) option on sharesRight to buy (sell) a specified no. of shares at a specified price [exercise price] within a specified period [exercise period]

• Options are traded on individual shares and indexesOptions executed with the exchange’s clearing house

• Non-traded options with nonstandard terms exist

• There are options on futures contracts

• Person on the other side of the transaction is the “writer” (UR used to be a writer)

• See your text for terms ( “in the money,” “out of the money,” etc) & for profiles

• Can protect downside risk without losing upside benefits - more expensive because of premium

21

Options

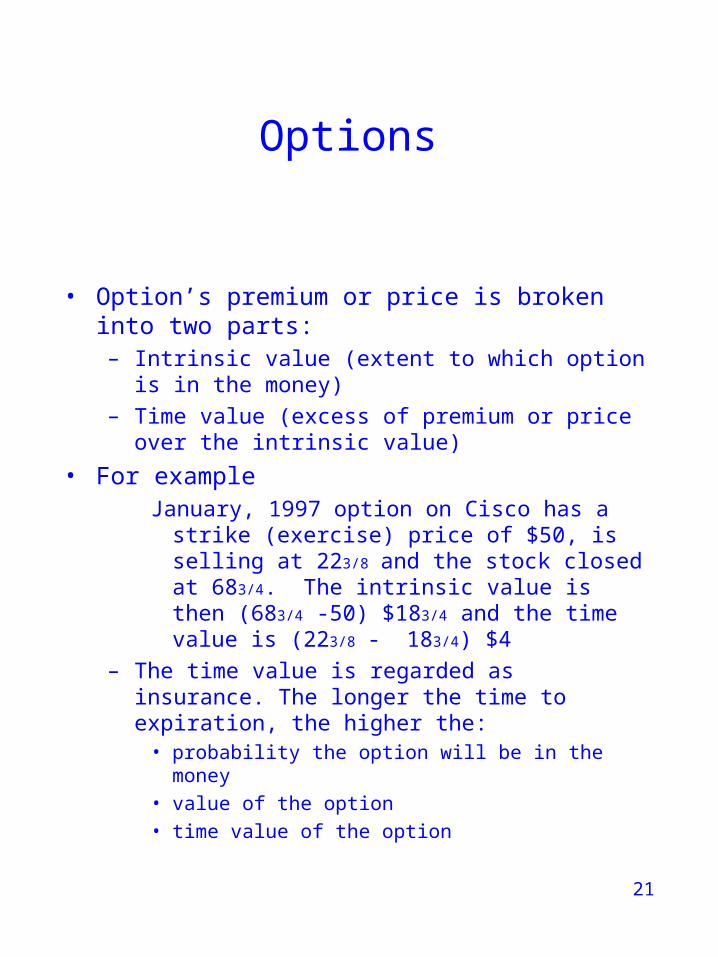

• Option’s premium or price is broken into two parts:– Intrinsic value (extent to which option is in the

money)

– Time value (excess of premium or price over the intrinsic value)

• For exampleJanuary, 1997 option on Cisco has a strike

(exercise) price of $50, is selling at 223/8 and the stock closed at 683/4. The intrinsic value is then (683/4 -50) $183/4 and the time value is (223/8 - 183/4) $4

– The time value is regarded as insurance. The longer the time to expiration, the higher the:

• probability the option will be in the money

• value of the option

• time value of the option

22

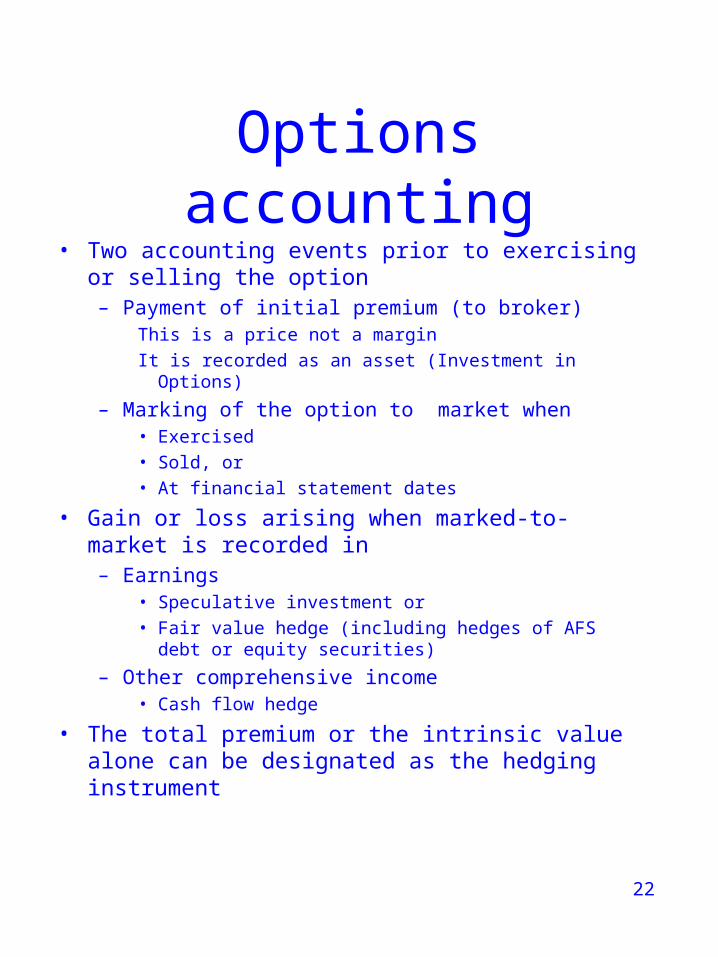

Options accounting• Two accounting events prior to exercising or selling

the option– Payment of initial premium (to broker)

This is a price not a margin

It is recorded as an asset (Investment in Options)

– Marking of the option to market when• Exercised• Sold, or• At financial statement dates

• Gain or loss arising when marked-to-market is recorded in

– Earnings• Speculative investment or• Fair value hedge (including hedges of AFS debt or equity

securities)

– Other comprehensive income• Cash flow hedge

• The total premium or the intrinsic value alone can be designated as the hedging instrument

23

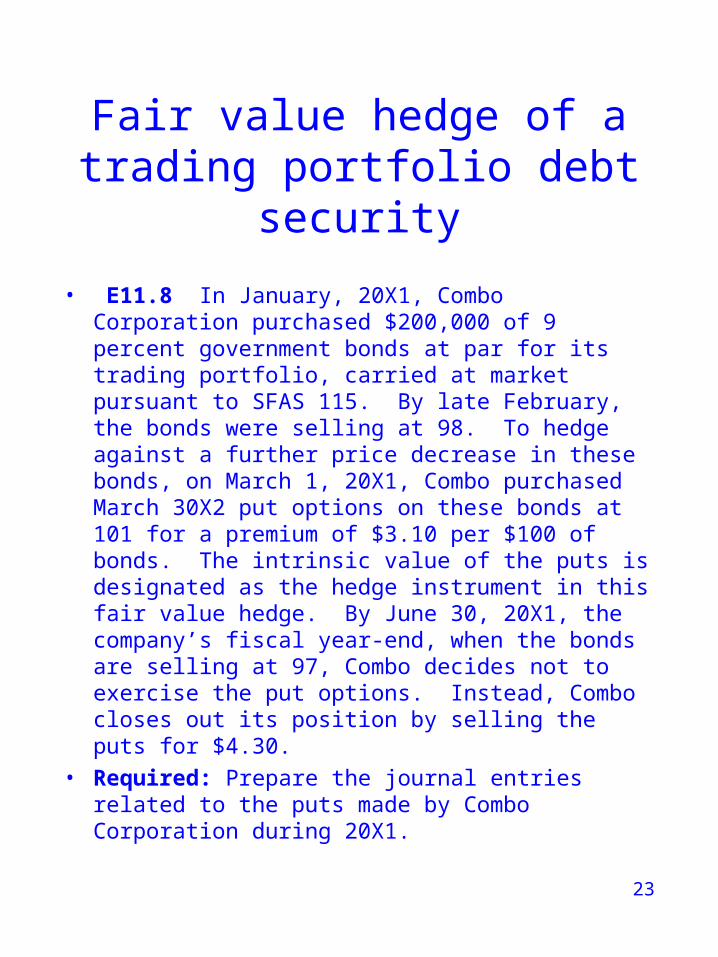

Fair value hedge of a trading portfolio debt security

• E11.8 In January, 20X1, Combo Corporation purchased $200,000 of 9 percent government bonds at par for its trading portfolio, carried at market pursuant to SFAS 115. By late February, the bonds were selling at 98. To hedge against a further price decrease in these bonds, on March 1, 20X1, Combo purchased March 30X2 put options on these bonds at 101 for a premium of $3.10 per $100 of bonds. The intrinsic value of the puts is designated as the hedge instrument in this fair value hedge. By June 30, 20X1, the company’s fiscal year-end, when the bonds are selling at 97, Combo decides not to exercise the put options. Instead, Combo closes out its position by selling the puts for $4.30.

• Required: Prepare the journal entries related to the puts made by Combo Corporation during 20X1.

24

Fair value hedge of a trading portfolio debt security

March 1, 20X1

Investment in Options $6,200

Cash $6,200

To record purchase of put options; 2,000$3.10

June 30, 20X1

Loss on Hedge Activity 3,600

Investment in Options 3,600

To record the loss on options hedging

an investment in bonds 2,000 (3.10-1.30)

Investment in Bonds 4,000

Gain on Hedge Activity 4,000

To adjust the carrying value of the bond

Investment by the increase in intrinsic value

200,000 (1.00-.98)

25

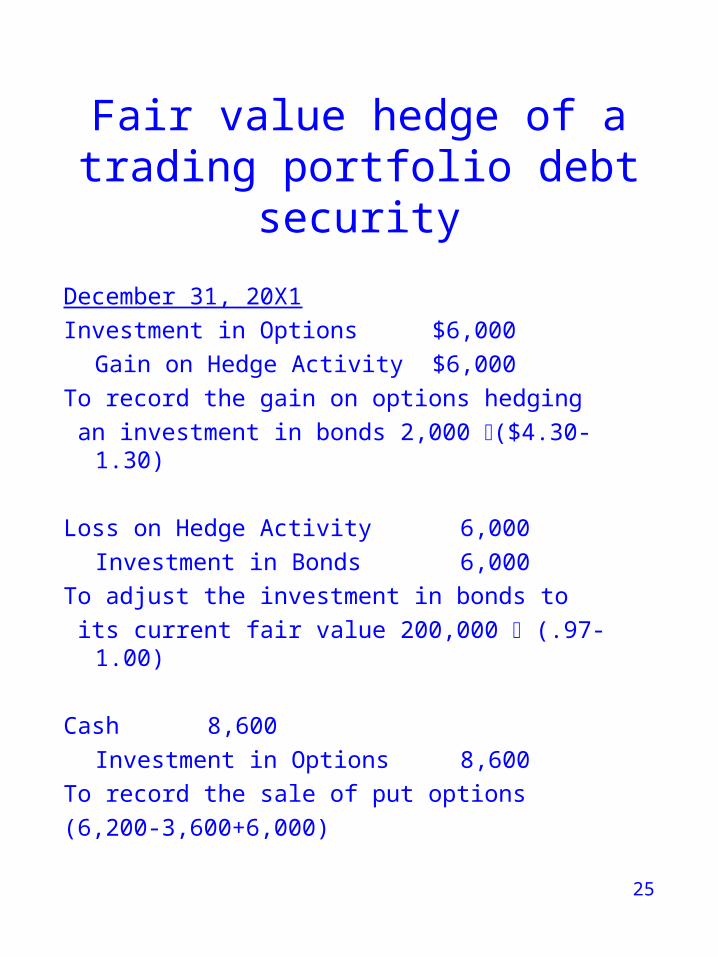

Fair value hedge of a trading portfolio debt security

December 31, 20X1

Investment in Options $6,000

Gain on Hedge Activity $6,000

To record the gain on options hedging

an investment in bonds 2,000 ($4.30-1.30)

Loss on Hedge Activity 6,000

Investment in Bonds 6,000

To adjust the investment in bonds to

its current fair value 200,000 (.97-1.00)

Cash 8,600

Investment in Options 8,600

To record the sale of put options

(6,200-3,600+6,000)