absolute return: is your investment portfolio ready for...

TRANSCRIPT

1

Absolute return: Is your Investment Portfolio ready for

structural change?

Danske Invest

2

October 2014

Alternative Investments Is your investment portfolio ready for structural change ?

Danske Invest Europe Absolute SICAV

3

Economics and finance are sciences that try to fit a chaotic and ever changing world into a logical

mathematical model

4

PARADIGM SHIFTS

Evolutions of Ideas 1. A theory is laid out in order to explain a phenomenon 2. Scientists test the theory and find facts that counter it 3. The original theory is stretched to accommodate new findings 4. A new theory supersedes the old theory Critical points in complex adaptive systems Large changes occur as the result of cumulative small stimuli

It is at the borderline between two parts of regimes that dynamism is larger that is a fact in nature and economics

5

Complex Adaptive System: Sand Pile

Drawing by Ms. Elaine Wiesenfield. Source: Hoe Nature Works, Per Bak, 1996

6

Behavioural Finance- investors are not rational

• Overconfidence and optimism • Regret and hindsight bias • Anchoring and conservatism

”Much of the real world is controlled as much by the ”tails of distribution as the means or averages: by the exceptional, not the mean; by the catastrophe, not the steady drip; by the very rich not the middle class” We need to free ourselves from ”average” thinking.”

Philip Anderson, a Nobel-prize-winning physicist.

7

Inflection point

When technology changes have significant impact on the economic development of companies and share prices.

8 8

Portfolio Exposure - Strategies based on Structural changes

As of Sep 23

Strategies Long Short Net Gross

Big Data 10,74 -1,98 8,76 12,72

Demand Destruction -18,69 -18,69 18,69

Emerging Consumers -7,31 -7,31 7,31

Energy Efficiency 16,00 -0,88 15,12 16,88

Geopolitical Change -2,72 -2,72 2,72

Growing Niche 1,17 1,17 1,17

Media Change 16,83 -1,93 14,90 18,76

New Credit Cycle -3,93 -3,93 3,93

New Normal 14,85 14,85 14,85

Western Consumers 2,68 -6,07 -3,39 8,75

Wireless World 20,49 -1,38 19,11 21,87

Hedge Overlay -8,88 -8,88 8,88

TOTAL 82,76 -53,77 28,99 136,53

Top Long Exposure Weight

SAP SE (Ord) 3,35%

Wacker Chemie AG 3,44%

Opera Software ASA 3,97%

AMS AG New 2014 5,22%

CRS Plc 3,39%

Top Short Exposure Weight

CFD on I-DJ Euro Stoxx 50 -7,81%

CFD on Marks & Spencer Group Plc Ord -2,73%

CFD on Rio Tinto Ord -2,72%

CFD on KGHM Polska Miedz S.A. -2,63%

CFD on HSBC Holdings Plc Ord (UK reg) 2,31%

9

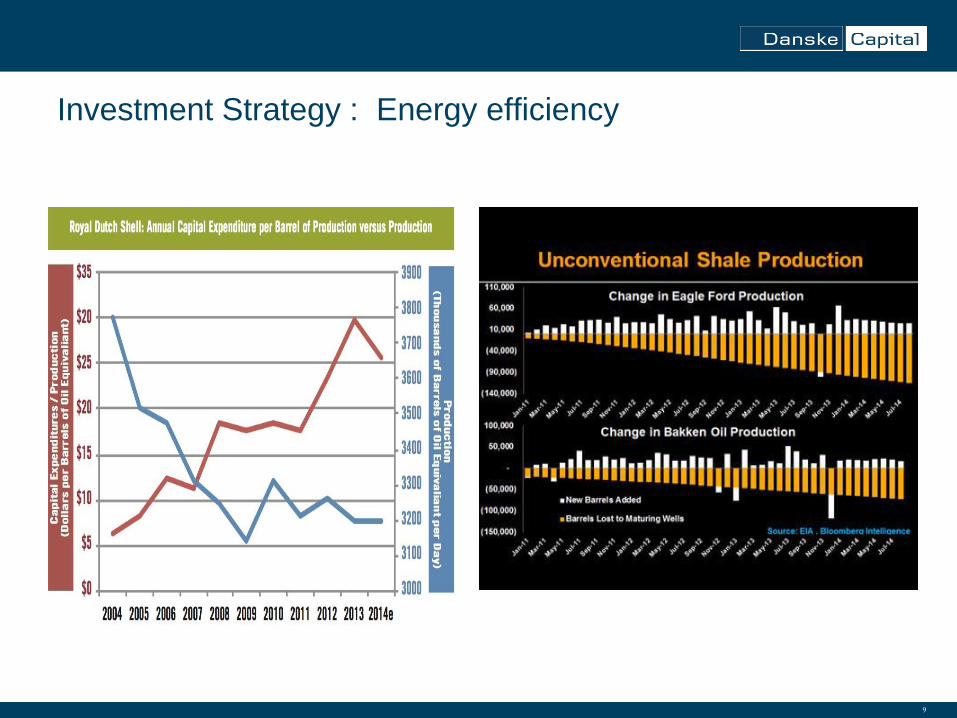

Investment Strategy : Energy efficiency

10 10

Investment strategy: Energy effeciency – Solar Inflection

Point

11

Investment Strategy: Energy efficiency

12

MEYER BURGER TECHNOLOGY AG (MBTN) Industrial Machinery Price: 9.16 (Sep 24, 2014)

Market Cap: 0.801 CHF Warranted Price: 19.34 CHF (+111%)

2010 2011 2012 2013 t + 1 t + 5

CFROI % 41.89 37.05 -1.74 -18.28 -0.01 15.00

Real Asset Growth % 76.64 44.88 13.66 -3.74 12.49 10.61

Discount Rate 5.04 6.19 6.30 5.23 4.84

CFROI & Asset Growth Inputs

Warranted Valuation Amount (MM) Per Share

+ PV Cash Flow Existing Assets 721 8.24

+ NPV Cash Flow Future Investments 1,161 13.27

+ Market Value Investments NA 0

Total Economic Value 1,882 21.51

- Market Value of Debt & Equivalents 171 1.96

- Market Value of Minority Interest 19 0.21

Warranted Equity Value 1,692 19.34

Winddown Value/Share 6.07

Winddown Ratio 1.51

Shares Outstanding 87 upside

+111%

13 13

Online

Source: Frontofstore.org

Strategy : Western

Consumers

Private debt level

Demographic

14

Strategy : Western Consumers

15

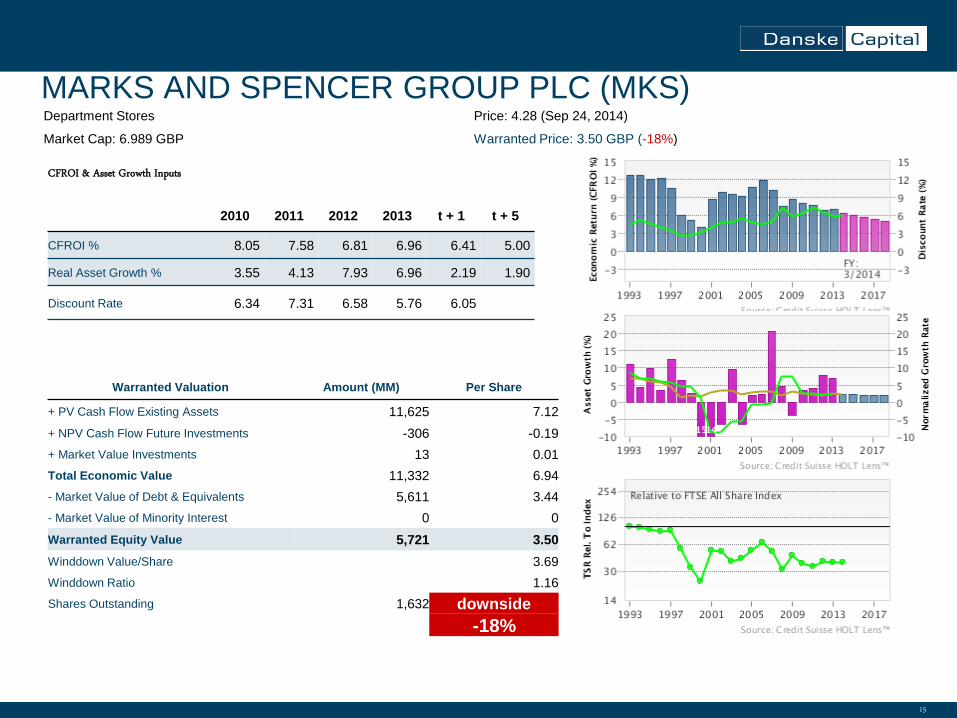

MARKS AND SPENCER GROUP PLC (MKS) Department Stores Price: 4.28 (Sep 24, 2014)

Market Cap: 6.989 GBP Warranted Price: 3.50 GBP (-18%)

2010 2011 2012 2013 t + 1 t + 5

CFROI % 8.05 7.58 6.81 6.96 6.41 5.00

Real Asset Growth % 3.55 4.13 7.93 6.96 2.19 1.90

Discount Rate 6.34 7.31 6.58 5.76 6.05

CFROI & Asset Growth Inputs

Warranted Valuation Amount (MM) Per Share

+ PV Cash Flow Existing Assets 11,625 7.12

+ NPV Cash Flow Future Investments -306 -0.19

+ Market Value Investments 13 0.01

Total Economic Value 11,332 6.94

- Market Value of Debt & Equivalents 5,611 3.44

- Market Value of Minority Interest 0 0

Warranted Equity Value 5,721 3.50

Winddown Value/Share 3.69

Winddown Ratio 1.16

Shares Outstanding 1,632 downside

-18%

16 16

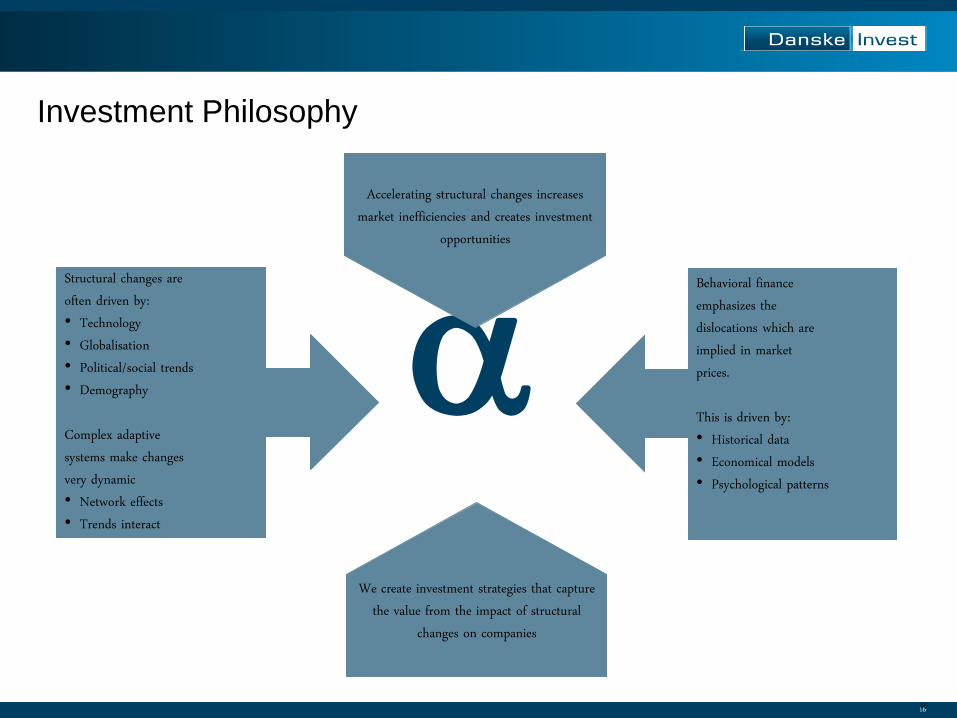

Structural changes are often driven by: • Technology • Globalisation • Political/social trends • Demography Complex adaptive systems make changes very dynamic • Network effects • Trends interact

Behavioral finance emphasizes the dislocations which are implied in market prices. This is driven by: • Historical data • Economical models • Psychological patterns

Accelerating structural changes increases market inefficiencies and creates investment

opportunities

We create investment strategies that capture

the value from the impact of structural changes on companies

Investment Philosophy

17 17

Appendix

18 18

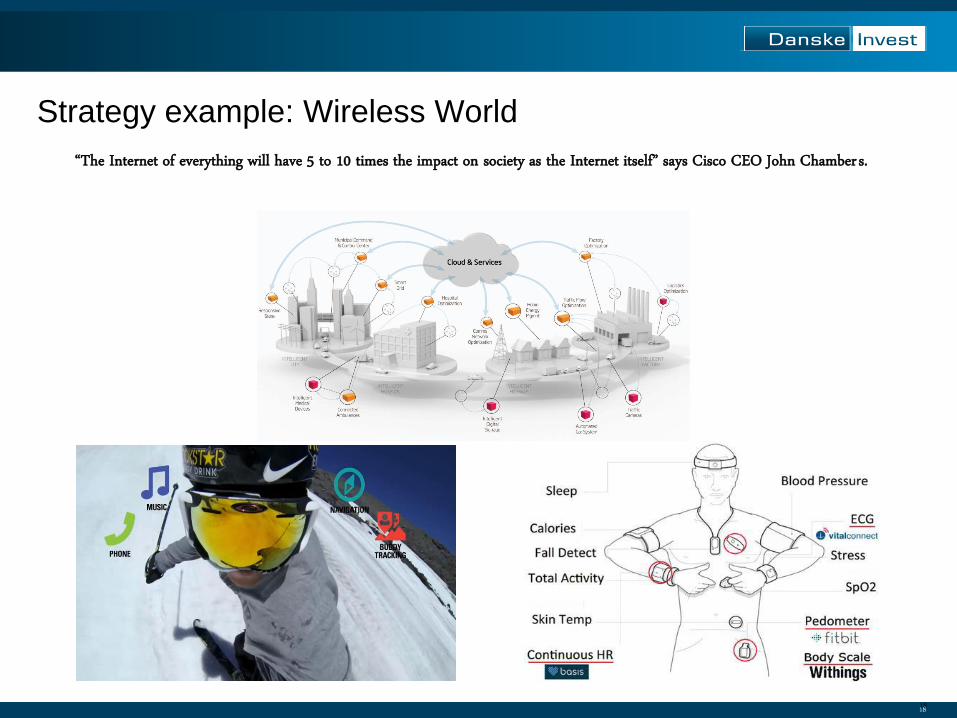

Strategy example: Wireless World

“The Internet of everything will have 5 to 10 times the impact on society as the Internet itself” says Cisco CEO John Chamber s.

19 19

Services

Strategy example: Wireless World

Strategy

Structural change

Sector dynamics

Moore’s Law Data traffic is exploding, while prices for

access of data/voice are coming down Free voice services

Data growth (S-curve) More people on smartphones, tablets

and laptops New demand for movies and “Internet

of things” Mobile data revenue are axpected to

grow from 21% to 44% between 2012–2016

New technology Next 4G mobile broad-band networks,

cloud computing, tablets and smart-phones will cause a boom for new data apps

Mobile services are at the beginning of their growth curve. Smartphones, tablets and laptops are causing a boom for movies, social media and gaming data. In addition, there is a huge growth potential in “Internet of things” where data connects cars or security systems to the Internet. Mobile data revenues are forecasted to grow from $220bn to $650bn between 2012–2016. Massive disruptive changes will impact many sectors – retail, media and communication, logistics and financial transactions. Companies in Europe are particularly strong in analogue chip design for “Internet of things”, mobile banking , capital goods for digital manufacturing. Big global players are a significant risk to many European companies in this space.

Ericsson Nokia ASML

STM CSR

Dialog AMS

Apple- Samsung Logitech Ingenico

IOS-Android SAP

Gemalto

Opera Gameloft Parrot

Monitise Wirecard Blinkx

Identify long and short candidates

Network effects Social networks in media reach critical

mass “Machine to Machine” networks are

gaining momentum connecting with cloud data management and storage

Applications Software Hardware Suppliers Equipment

20 20

Disclaimer & contact information

This publicat ion has been prepared by Danske Capital for informat ion purposes only. The presentat ion

must be read in conjunct ion with the oral presentat ion provided by Danske Capital.

Danske Capital

Parallelvej 17

DK-2800 Kgs. Lyngby

Tel. +45 45 13 96 00

Fax +45 45 14 98 03

http:/ / www.danskecapital.com