ab sg (singapore edition) – november/december 2012

DESCRIPTION

AB SG (Singapore edition) – November/December 2012 of Accounting and Business magazine (ACCA)TRANSCRIPT

finance challenge

insights from pwc-acca finance effectiveness survey 2012

added valuewhat do directors want from audit?

technical hedge accountingbanking fstep’s lee khee joo

opinion the war for talent

cPdget verifiable cpd units by reading technical articles

beyond these shoressingapore’s companies look for international opportunities

driving force kop group’s unstoppable ceo ong chih ching

euro what happens if greece exits?reorting a guide for the perplexedfraud auditors fight back

absg sg.a

b a

cc

ou

ntin

g a

nd

bu

sine

ss 11

/20

12

the magazine for business and finance professionals accounting and business singapore 11/2012

SG_cover.indd 1 12/10/2012 16:21

A&B NovDec 2012 (Generic) ol_output.pdf 1 27/9/12 2:35 PM

-Lexis AB Asia adverts1-Nov12.indd 3 08/10/2012 12:35

Have very good friends who will support and help you is the advice Ong Chih Ching, CEO of KOP Group, would give to anyone wishing to emulate her success in real estate. Her legal training has helped as well. See page 12

EXPANDING HORIZONSSingapore companies are expanding their wings regionally. Faced with a small and mature local market, companies seeking to grow their revenues are looking outside. Most of the firms tend to favour doing business in South-East Asia and China due to geographical proximity and cultural similarities, according to International Enterprise (IE) Singapore, the agency spearheading Singapore’s external economy.

This is a sector of the economy policy-makers are keen to explore. Over the years, the authorities have been exhorting local companies to venture abroad, backing up the call with a plethora of grants and schemes to give the enterprises a leg-up. Early this year, IE Singapore launched the Global Company Partnership (GCP) initiative to better understand companies’ business plans and to formulate comprehensive solutions for their international growth through capability building, market access and financing. Last year, over 34,400 companies approached the agency for help in understanding overseas markets, connecting to the right business partners and developing capabilities. It partnered companies on 336 overseas projects, with two thirds taking place in developing regions such as Indonesia, United Arab Emirates and Vietnam. China saw the most interest, accounting for 104 overseas projects.

Our feature on page 16 explores the challenges local companies face in their push to expand. It also looks at companies that have succeeded in building their brands overseas. Singapore companies have cited keen competition, lack of manpower to manage overseas operations and difficulty in finding business partners as the top three challenges. In spite of the complexities, the trend can only increase. The rise of new emerging markets such as Myanmar, Africa and Latin America means huge market potential because of their rapid development, growing population and rising standard of living. Local players are salivating over the overseas prospects, given the pie is getting bigger and the opportunities to grow are only going to get wider.

Sumathi Bala, [email protected]

BIG AMBITIONS?For your next move, check out www.accacareers.com/singapore

CRIME FIGHTERSThe latest set of revised global recommendations means that accountants have an even greater role in battling fiscal crimePage 40

HEDGE TRIMMINGAn IASB draft is seeking improved links between the rationale for hedging and its impact on financial statementsPage 48

TECHNICALLY BRILLIANT?There are over a hundred technical articles with multiple-choice questions on the ACCA website –

demonstrate your understanding and get verifiable CPDwww.accaglobal.com/cpd

3Editor’s choice

SG_B_Edletter.indd 3 12/10/2012 16:23

Audit period July 2009 to June 2010138,255

Features12 Team player Ong Chih Ching has conquered a diverse range of markets – and taken her friends with her

16 New horizons Singapore’s businesses have much to gain from overseas expansion

20 Exit strategy What are the implications of Greece leaving the eurozone?

23 Dismantling the euroCapital Economics’ Roger Bootle offers some practical suggestions

26 Future vision Sustainability and fi nancial results can go hand in hand, says KPMG’s Yvo de Boer, a former UN climate chief

28 Cloud control Remote technology will revolutionise the boardroom

VOLUME 15 ISSUE 10

Asia editor Colette [email protected] +44 (0)20 7059 5896

Editor-in-chief Chris [email protected] +44 (0)20 7059 5966

International editor Lesley [email protected] +44 (0)20 7059 5965

Singapore editor Sumathi [email protected]

Sub-editors Dean Gurden, Eva Peaty, Vivienne Riddoch

Design manager Jackie Dollar

Designers Robert Mills, Zack Starkey

Production manager Anthony Kay

Advertising James [email protected] +44 (0)20 7902 1210

Head of publishing Adam Williams

Printing Times Printers

Pictures Corbis

ACCAPresident Barry Cooper FCCADeputy president Martin Turner FCCAVice president Anthony Harbinson FCCAChief executive Helen Brand OBE

ACCA [email protected] +44 (0)141 582 2000

ACCA Singapore435 Orchard Road#15-04/05 Wisma AtriaSingapore 238877+65 6734 8110 [email protected]

Accounting and Business is published 10 times per year. All views expressed within the title are those of the contributors.

The Council of ACCA and the publishers do not guarantee the accuracy of statements by contributors or advertisers, or accept responsibility for any statement that they may express in this publication.

Copyright ACCA 2012 Accounting and Business. No part of this publication may be reproduced, stored or distributed without the express written permission of ACCA.

Accounting and Business is published by Certifi ed Accountant (Publications) Ltd, a subsidiary of the Association of Chartered Certifi ed Accountants.

29 Lincoln’s Inn FieldsLondon, WC2A 3EE, UK+44 (0) 20 7059 5000

www.accaglobal.com

AB SINGAPORE EDITIONCONTENTSNOVEMBER/DECEMBER 2012

SG_B_Contents.indd 4 12/10/2012 16:25

TECHNICAL42 Update The latest from the standard-setters

45 Accounting solutions PwC experts answer questions on employee incentive plans and agent versus principal

46 A guide for the perplexed The fi rst of a two-part series examines recent innovations in corporate reporting

48 CPD: hedge accounting A look at the rationale for hedging and its impact on fi nancial statements

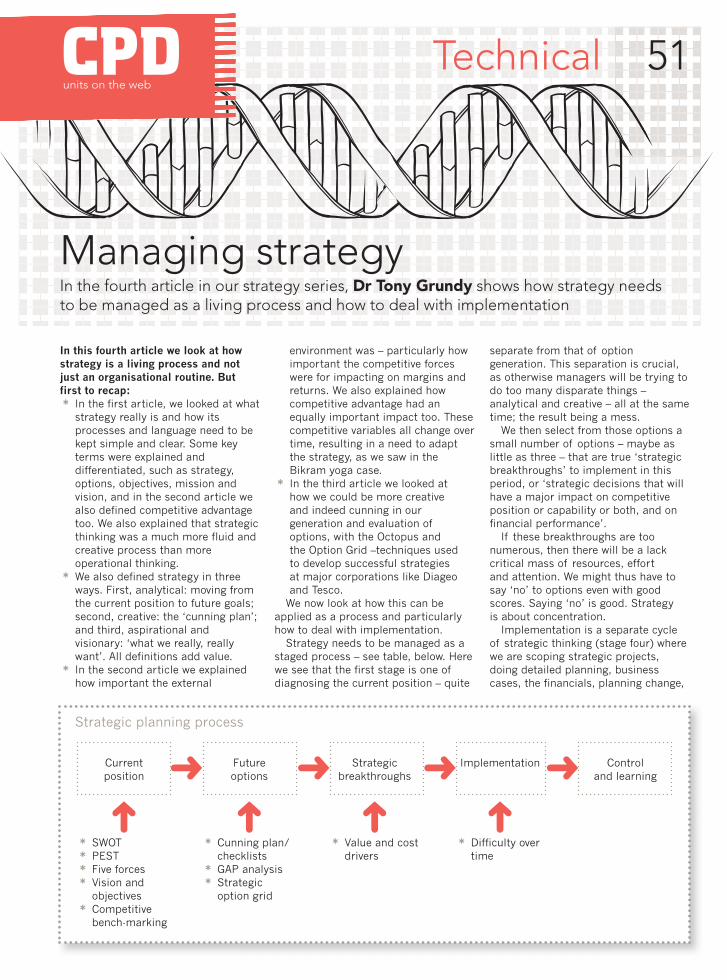

51 CPD: strategy How strategy needs to be managed as a living process and how to deal with implementation

BRIEFING06 News in pictures A different view of recent headlines

08 News in graphicsWe show a story as well as tell it using innovative graphs

10 News round-upA digest of all the latest news and developments

VIEWPOINT30 Cesar Bacani ASEAN is set to become a regional driver for growth

31 Errol Oh Audit employees at large fi rms are voicing their concerns

32 Barry Cooper Accounting for the Future was a valuable event for members, says the ACCA president

33 CORPORATE33 The view from Douglas Young of Goods of Desire, plus news in brief

34 A passion for learning FSTEP’s Lee Khee Joo is helping to nurture Malaysia’s future accountants

38 Reporting for duty Our new series looks at how companies can improve their corporate reporting

39 PRACTICE39 The view from Tan Siow Ming of PwC Malaysia, plus news in brief

40 Fraud fi ghters Accountants have an increased role to play in the global crackdown

Regulars

CPDAccounting and Business is a rich source of CPD. If you read it to keep yourself up to date, it will contribute to your non-verifi able CPD. If you read an article, learn something new and apply that learning in some way, it will contribute to your verifi able CPD. Each month, we also publish an article or two with related questions to answer. If they are relevant to your development needs, they can also contribute to your verifi able CPD. One hour of learning equates to one unit of CPD. For more, go to www.accaglobal.com/members/cpd

Your sector

WorldwideThere are six different versions of Accounting and Business: China, Ireland, International, Malaysia, Singapore and UK. See them all at www.accaglobal.com/ab

ACCA NEWS54 CPD Annual CPD declarations are now due for submission

58 Compact considerations ACCA has signed up to the UN Global Compact

60 Room for improvement Finance functions have yet to embrace their new role as business partners, a new PwC-ACCA report fi nds

62 Adding value Auditors play a vital role in providing an independent picture of a company, delegates at the launch of a new ACCA report hear

64 Wilson Woo Providing opportunities for those less fortunate will help build the Singapore of the future, says the ACCA Singapore branch president

65 Council ACCA holds its 107th AGM in London

66 News Barry Cooper formally elected as ACCA president

SG_B_Contents.indd 5 12/10/2012 16:29

01 A ceremony in Taipei, Taiwan,

commemorates the anniversary of the birth of Chinese philosopher, Confucius, whose teachings focused on charity, justice, propriety, wisdom and loyalty

02 Zong Qinghou, of drinks company

Wahaha, has topped the Hurun Rich List as China’s richest man, worth US$12.6bn

03 Legoland Malaysia,

constructed using more than 50 million bricks, opens. Models include the Petronas Towers and the Great Wall of China

News in pictures6

AP_newsinpix.indd 6 11/10/2012 11:13

04 Imelda Marcos, pictured

celebrating the birthday of her late husband and president Ferdinand Marcos, is seeking re-election to a second term as congresswoman, continuing her family’s political comeback

05 Singapore has agreed a deal

with Formula One to extend the country’s Grand Prix contract until 2017. Its night race has been a highlight of the Formula One calendar since the event came to Singapore in 2008

06 Malaysian Prime Minister

Najib Razak, pictured at Independence Day celebrations, has announced a voter-friendly 2013 Budget ahead of next April’s general election

07 Two new art museums have

opened on the site of the 2010 Shanghai World Expo. The China Art Museum and the Power Station of Art began trial operations during the National Day holiday

7

AP_newsinpix.indd 7 11/10/2012 11:15

SINGAPORE SOARS ABOVE HONG KONG ON CORPORATE GOVERNANCESingapore came out ahead of Hong Kong again in a corporate governance survey by the Asian Corporate Governance Association and CLSA Asia-Pacific Markets that examined 11 markets and more than 800 listed companies. Singapore ranked 69th (67th in 2010) and Hong Kong came 66th (65th in 2010).

Singapore Hong Kong Thailand Japan Malaysia Taiwan India South Korea China

251The number of Chinese US dollar billionaires in 2012 (2011: 271; 2006: 15), according to the Hurun Report.

78%Uptake of smartphones across South-East Asia over the past year.

92%The number who say China’s slowdown is affecting their business, according to a Retail in Asia poll.

80%The number of staff who plan to stay with their current employer in the next year, according to Deloitte’s Talent 2020 report.

Mon

th

in fi

gur

es

6949

23 34

43

6173

75

55

39

42

63 85

5566

58

51

53 45

55

23Philippines

39India

42Indonesia

63Pakistan

85China

73Vietnam

75Burma

43Malaysia

55

Sri Lanka

34SouthKorea

61Thailand

FREE AS A BIRD?Malaysia has fallen two places since last year in the Washington-based thinktank Freedom House’s latest Freedom on the Net (FOTN) report, which measures internet freedom in 47 countries. This places Malaysia on the 23rd spot, in the same league as Libya and Jordon, and maintains its ‘partly free’ label in the thinktank’s FOTN status. In the region, Malaysia ranks behind the Philippines (7th place) and Indonesia (21st) but is ahead of Thailand (35th), Vietnam (40th) and Burma (41st).

KEYFree (0-30)Partly free (31-60)Not free (61-100)

News in graphics8

AP_B_graphics08.indd 8 12/10/2012 16:54

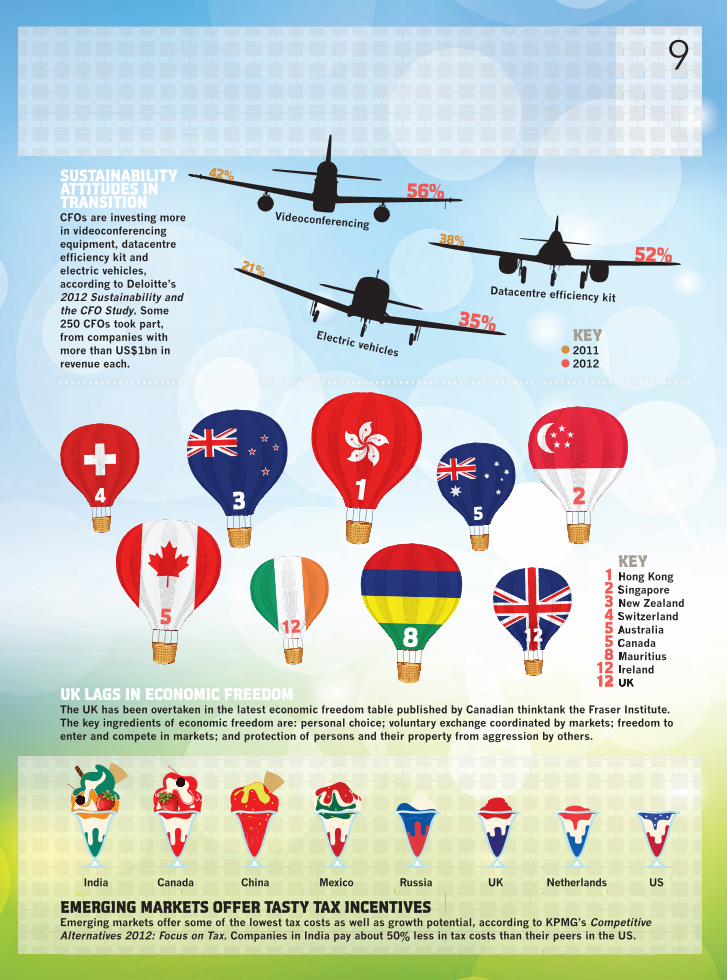

SUSTAINABILITY ATTITUDES IN TRANSITION CFOs are investing more in videoconferencing equipment, datacentre efficiency kit and electric vehicles, according to Deloitte’s 2012 Sustainability and the CFO Study. Some 250 CFOs took part, from companies with more than US$1bn in revenue each.

KEYHong KongSingaporeNew ZealandSwitzerlandAustraliaCanadaMauritiusIrelandUK

KEYHong KongSingaporeNew ZealandSwitzerlandAustraliaCanadaMauritiusIrelandUK

1234558

1212 UKUK1212

UK LAGS IN ECONOMIC FREEDOMThe UK has been overtaken in the latest economic freedom table published by Canadian thinktank the Fraser Institute. The key ingredients of economic freedom are: personal choice; voluntary exchange coordinated by markets; freedom to enter and compete in markets; and protection of persons and their property from aggression by others.

EMERGING MARKETS OFFER TASTY TAX INCENTIVES Emerging markets offer some of the lowest tax costs as well as growth potential, according to KPMG’s Competitive Alternatives 2012: Focus on Tax. Companies in India pay about 50% less in tax costs than their peers in the US.

India Canada China Mexico Russia UK Netherlands US

45

8

3 1

5

2

12 12

56%

35%

52%

42%

21%

38%

Videoconferencing

Electric vehicles

Datacentre efficiency kit

KEY20112012

9

INT_B_graphics09.indd 9 12/10/2012 17:09

VAT ROLL OUT MOVES UP A GEARChina’s roll out of value-added tax (VAT) for service industries has stepped up, with implementation in Beijing in September, followed by Jiangsu and Anhui last month. Shanghai was the first city to roll out the tax in January. ‘The ultimate scenario is for the VAT system to be implemented nationwide – and across all industries,’ Peter Law, senior manager, tax advisory services at international audit and advisory firm Mazars told China Daily. ‘It is anticipated that this will occur before the end of the 12th Five-year Plan, which is 2015.’ He noted that while in the past, large amounts of tax in China were collected from land sales, the future seems to focus on VAT collection, ‘which promises to be the richest source of revenue in the world once the programme is implemented in all cities’.

MIND THE GAPMid-tier management salaries in Malaysia are about 10% to 30% lower than those of their counterparts in Singapore, Hong Kong and Australia, according to a survey by Kelly Services. Drawing on the findings of Kelly Services Asia Pacific Professional

and Technical Salary Guide 2012, Melissa Norman, Kelly Services managing director in Malaysia, told The Star that while new graduates in Singapore are commanding a starting salary of around S$2,500 (RM6,200), many Malaysian graduates are ‘still hovering between RM1,800 and RM2,000’. She added: ‘You need to go one step further and ask: “Why are [Singaporeans] getting paid a little more, and why are we paid a little less?” This brings you to the quality of the students. The majority of graduates here come out lacking in skills.’

INDUSTRIAL PROFITS FLAGChinese industrial companies’ profits fell for the fifth consecutive month in August, indicating that the economic downturn is set to continue, Bloomberg reported. Quoting the National Bureau of Statistics, it found company profits dropped 6.2%, a decline accelerating since the 5.4% drop in July, and a 1.7% fall in June. The figures, based on a survey of 41 industries, suggest that China is heading towards its weakest annual expansion in 22 years.

RICH GET POORERThe number of super-rich in China has fallen over the past year, with fewer US

dollar-billionaires for the first time in seven years. According to the Hurun Rich List’s latest annual report, there are now 251 Chinese billionaires, down 20 on a year ago, and 37 of the richest 1,000 saw a 50% drop in their wealth. Rupert Hoogewerf, Hurun Report chairman and chief researcher, said that although this year has seen ‘some significant wealth bloodletting, it is worth remembering that these entrepreneurs are still up 40% on two years ago and almost 10 times 10 years ago.’ Solar, textiles and retail have been the hardest hit this year, while entertainment, IT, natural gas and property developers with large landbanks have had a good year.

HUNGRY FOR GROWTHUS food giant Kellogg is tapping China’s growing appetite for Western-style cereals and snacks. The company has announced a joint venture with Singapore-based Wilmar to further the distribution of its Kellogg’s and Pringles brands. Kellogg chief executive John Bryant said that the project positions the company’s China business for growth ‘and fundamentally changes our game in China’. China’s snack-food market is expected to reach an estimated US$12bn by year-end, up 44% from 2008.

ASIA DRIVES LUXURY SALESSales of luxury goods in Asia continue to drive growth for top-end European brands. Italian label Prada has reported a nearly 60% growth in first-half earnings, with Asia-Pacific’s share accounting for nearly 36%. Sales in the region for Miu Miu brand – also owned by Prada – rose 34.7%. Group-wide, revenues from Asia Pacific recorded the highest growth of all markets, up 43.9%. Paris-based luxury house Hermès is also cashing in, reporting a 25% rise in sales in mainland China, Hong Kong and Singapore, compared with 21% globally.

HK AND CHILE SIGN AGREEMENTHong Kong and Chile have signed a historic free trade agreement, the first

STANDARDS STILL IMPROVINGCorporate governance standards are improving in Asia, according to the Asian Corporate Governance Association-CLSA Asia-Pacific Markets’ Corporate Governance Watch 2012. However, the report found that some standards have slipped since the last report in 2010, the scope ranging from ‘relatively minor corporate transgressions to growing concerns about the reliability of financial statements and, at the extreme, outright fraud’. Singapore topped the rankings, followed by Hong Kong and Thailand, all with improved scores. China dropped four percentage points, and Japan and Taiwan by two. Indonesia was placed at the bottom, with The Philippines second from last.

Singapore ranks highest in Asia for corporate governance standards

10 News round-up

AP_newsroundup.indd 10 11/10/2012 11:16

P20

between the special administrative region and a Latin American country. Inked at the Asia-Pacific Economic Cooperation leaders’ summit in Vladivostok, Russia, in September, the agreement will markedly improve the business environment for entities involved in economic activity between the two territories. The resultant liberalised access to services is expected to boost Hong Kong’s financial services industry and may potentially serve as a gateway to the Central and South American markets. Currently, Chile ranks 29th among Hong Kong's worldwide goods trading partners, and 32nd for services.

CFOS CONFIDENT IN ASIACFOs working across Asia Pacific are more confident about market conditions and career opportunities compared with their global counterparts, according to the Michael Page International Global CFO Barometer 2012. When surveyed, 83% of Asia-Pacific respondents believed that economic conditions in their country were either satisfactory or good, compared with 59% globally. And 88% of respondents based in Asia Pacific rated the region as the most attractive for business in 2012. The survey also found that Asia-based CFOs are focused on career opportunities, with 59% looking to broaden the scope of their current role in the next two years. Salary continues to play a key factor in career choice, as indicated by 59% of Asia Pacific and 51% of global respondents.

IPOS ‘ON ICE’Hong Kong is having its worst year for initial public offerings (IPOs) in a decade, the South China Morning Post reported in an article describing the much-hyped market as currently being ‘on ice’. Disappointing outcomes of listings, the eurozone crisis and slowing growth in the mainland have all taken their toll, compounded by the bad experience of investors who lost money in Hong Kong listings in 2011. Peter

Burnett, Asian global capital markets chairman at UBS, was quoted as saying: ‘There is plenty of cash, there is a history of great deals, but investor confidence is thin on the ground at the moment. Once that is restored there will be no shortage of attractive IPOs’ Only 32 IPOs were completed in Hong Kong in the first six months of 2012, according to Deloitte.

Cooperation summit meeting in Vladivostok, Russia, in September.

R&D RAMPS UPEmerging Asia is starting to produce significant amounts of its own innovation after years of playing research and development (R&D) ‘catch-up’, according to Coming of Age: Asia’s Evolving R&D Landscape, a new report

STRESS LEVELS SOARWorkers in Hong Kong and China are becoming more stressed, according to the latest global survey by flexible workspace provider Regus. From Distressed to De-stressed revealed that 75% of workers in China say their stress levels have risen in the past

year – the highest increase among the world’s top 50 economies. In Hong Kong, the figure was lower, at 55%, but still higher than the global average of 48%.

Respondents identified work as the biggest trigger of stress, with half

of Hong Kong respondents and 55% of those in mainland China wanting more flexibility in their jobs. In response, Robin Bishop, chief operating officer at Community Business – which promotes community social responsibility in Asia – said that

companies cannot ignore the impact of poor work-life balance

on their bottom lines.

CONFIDENCE TAKES A KNOCKEconomic disruption, including possible recession in the US, the eurozone crisis and China’s slowing economy have taken a toll on the confidence of CEOs in the Asia Pacific region, according to PwC. Just 36% of executives surveyed by the firm say they are ‘very confident’ of business growth over the next 12 months. Their prospects, however, improve in the longer term, with more than half (54%) expressing a high level of confidence for the next three to five years. Asia Pacific CEOs also believe that the region is on track to achieve greater economic integration, a top priority of the Asia Pacific Economic

from the Economist Intelligence Unit, commissioned by Mercer. For 50 years, Asia’s emerging markets have largely adopted ideas developed elsewhere in the world, but this is now changing, the report found. ‘As Asia and the emerging markets become increasingly important growth engines for the global economy, R&D and innovation in Asia have taken on increasing prominence. Global technology companies investing in R&D in the region do so not only to tap the growth markets but the disruptive innovation coming from the region,’ said Joon Tan, principal consultant, information product solutions, at Mercer.

11AnalysisGOODBYE GREECE?A Greek exit – dubbed ‘Grexit’ – from the eurozone is considered more likely than not by some commentators. With the implications for Greece almost beyond comprehension, could other countries also follow suit?

AP_newsroundup.indd 11 11/10/2012 11:17

Just as a general’s mettle is forged in battle, the mettle of a modern CEO is forged in times of financial crisis. For Ong Chih

Ching, a corporate lawyer and property investor who left her successful law practice in 2008 to become CEO of KOP Group, her battle-hardened experience came with the collapse of Lehman Brothers and the widespread financial crisis that ensued.

In 2006, the then 37-year-old, with two friends, co-founded KOP Capital, a private equity management firm. Within two years, business was expanding so fast Ong decided it was time to dedicate herself full time to the company. ‘Our first investment was to buy the land for our Ritz-Carlton Residences project, which at the time was quite different from the other branded residences around because this one was going to be managed by the actual hotel operators.

‘Then in 2007, we invested in four other projects in Singapore, including what would become Hamilton-Scotts. Leny [Suparman], my business partner, said to me: ‘This is other people’s money; we have to be responsible and you have to concentrate on this full time,’ Ong recalls.

As soon as she took over, Ong restructured the company, establishing KOP Group as the main company and creating KOP Properties, a new division that would develop properties, along with the private equity management arm, KOP Capital.

She was soon approached by one of her former clients, Dubai Group – the financial services arm of Dubai Holding

– which took a 51% stake in KOP Group. ‘I knew them well as I’d been their lawyer for over 10 years,’ Ong explains. ‘They were in an expansion mode, and the deal was that we would do any single real estate project they had in Asia. That was very palatable to us. They were well funded, we had great chemistry working together.’

GROUP EFFORTFrom hotels to horology, Ong Chih Ching has used her legal skills to conquer a diverse range of markets – and she’s achieved all this with a little help from her friends

The tips*Have very good friends who will support and help you – ‘not just people who work directly with me, but people whom I can call and ask for help,’ Ong says.

*You need self-discipline and must be focused.

*You have to persevere when you believe it is right, but also be willing to cut your losses.

Flush with new cash, Ong decided that KOP should acquire a 50% stake in Stein Group, a management company of small luxury lifestyle hotels across Europe (today renamed Franklyn Hotels and Resorts).

‘We wanted the expertise of hospitality,’ Ong recalls. ‘We weren’t planning on going into hotels but we felt we were lacking the software to support our residential plans. So we acquired 50% of Stein and the idea was that they would do the management for our real estate.

‘Bite the bullet’However, the Lehman crisis changed the picture. ‘The company was based in Europe with all their properties there. It needed new capital, but they didn’t have the funds, and we couldn’t come to a reasonable agreement, so in the end we had to bite the bullet and take them over,’ Ong explains.

The financial crisis also created tensions between Ong’s vision for KOP Group and that of its main financial partner. ‘In 2009-2010, the Dubai Group team changed drastically. Because of the Lehman crisis, they were in a consolidation mode and we needed to expand so there was a definite mismatch,’ she recalls. Eventually, the partners parted ways, amicably, with Ong engineering a management buy-out with the help of Thai businessman Chanchai Ruayrungruang, chairman of conglomerate Reignwood Group.

Ong believes her training as a lawyer helped her weather the crisis. ‘Lawyers are very quick at identifying the issues

12 CEO interview

SG_F_Ong.indd 12 12/10/2012 17:05

13

SG_F_Ong.indd 13 12/10/2012 17:05

The CV2008

Becomes CEO of KOP Group.

2006Founds KOP Capital with Leny Suparman and Geraldine Ong.

2003Founds watch collectors’ guild Bezel with Leny Suparman.

1998Starts up Lush Cosmetics in Singapore (sold back to principal in 2001).

1996Founds law firm Koh Ong & Partners with one partner.

1994Admitted as advocate and solicitor by the Singapore Law Society.

1990Bachelor of Laws from the University of Buckingham.

and giving a solution. That’s very much up my alley. As a result, I think I probably was less stressed than other CEOs during Lehman. In hindsight, the experience was good. We were on a high between 2006 and 2008, but once you’ve experienced difficulties, it provides you with the experience, the patience and the requisite abilities to walk the longer road,’ Ong reflects.

‘I’ve learned from all this that you must persevere – which I hadn’t done before with other personal business investments – but you must also be ready to cut your losses. You have to be focused and you have to be the one in the driving seat; you can’t rely on someone else,’ she adds.

shui but we had won every single case we’d had for two years and we were feeling pretty invincible,’ she recalls.

The retail venture would, however, be a humbling experience. The company had opened three shops within four months, but it was not successful. ‘As lawyers we were charging S$400 an hour, the soaps were selling for S$4 apiece and it was taking about the same amount of time. The law firm was thriving and so we had to make a choice,’ she says. ‘From this experience we learned that human resources is the most important thing and that if you want to succeed you have to be there. The moment we weren’t there, sales were going down.’

In 2009, KOP took on the exclusive distribution of Princess Yachts in Singapore and China, but decided to disengage after a year and a half. ‘We felt it wasn’t the right thing to do, so we got out of it,’ she says.

Throughout her career, Ong has seized opportunities wherever they lay and even though they have not always been successful, she feels that she has always gained valuable experience. For example, with a friend, Koh Geok Jen, she set up a joint venture with UK company Lush Cosmetics to bring products to Singapore.

‘Back in 1998, our law firm was two years old and we felt that it was on a good track. Maybe it was good feng

‘YOU MUST PERSEVERE BUT YOU MUST ALSO BE READY TO CUT YOUR LOSSES. YOU HAVE TO BE THE ONE IN THE DRIVING SEAT’

14

SG_F_Ong.indd 14 12/10/2012 17:06

In 2003, Ong set up another venture, Bezel, with her friend and CEO of KOP Properties, Leny Suparman. Initially started as a watch club because they felt the world of horology was too cliquish, they saw a retail opportunity and struck a deal for the distribution rights to Italian brand U-Boat Watches in most of Asia. Today, the two women remain investors in Bezel, although the business is run by a partner.

A matter of trustFor her part, Suparman believes they have managed to make their collaborations work because they fully trust and complement each other. ‘Chih Ching looks at the big picture; I look into the details,’ she says. ‘She gets excited about opportunities; I also do, but with more caution.’

Ong believes that a company’s boardroom benefits from diversity. ‘Women are more down to earth and

don’t have so many ego issues, so it’s often easier to talk to them, but I feel they don’t offer each other the support that men will. Men are more cliquish and more supportive of each other.’

Today, the KOP Group’s annual turnover is around S$100m, with several projects on the go. Besides the 58-unit Ritz-Carlton Residences and the 56-unit Hamilton-Scotts, the company has recently opened Montigo Resorts in Batam, Indonesia, and is now working on a major new project, 10 Trinity Square – a mixed-use development with luxury residences and a hotel in the heart of London.

Both Montigo and 10 Trinity Square are bringing Ong back full circle, in different ways. The CEO admits she had always wanted to be an architect, but was not strong enough in maths so chose law instead. With Montigo, she got the opportunity to express her creativity in the design of the villas.

Meanwhile, Trinity Square provides a link with her first real estate investment experiences while studying in London. ‘Even when I was studying I was buying and selling properties there for my mother,’ she recalls. ‘Even after I left London, I was going back once a year and still investing. At the peak I had seven properties there.’

Ong says that while many people assume that the London development is KOP’s most difficult project, Montigo Resorts has actually been the hardest, which is probably why it is the one of which she is the most proud. ‘First of all, the destination itself has its baggage, and then Indonesia wasn’t a place I was familiar with. Finally, the skill set that you can find in Indonesia versus what you find here or in London is very different. So yes, it’s been difficult, but it’s finally completed and nearly sold,’ she says.

Besides real estate, KOP Group also runs LUX Legion, an alliance providing members a platform to showcase their products and services. There is

The basicsKOP GROUP The diversified real estate investment, development and management company has three arms: KOP Capital, a private equity unit investing in real estate; KOP Properties, an investment company that develops properties; and KOP Hotels and Resorts, the hospitality and leisure division that includes Franklyn Hotels and Resorts, Aqua Voyage and Sealine Yachts Asia.

The company started with just one full-time employee, Leny Suparman, and has now grown to about 300 employees worldwide. According to its CEO Ong Chih Ching, KOP has around S$3.1bn in assets under management and the annual turnover is about S$100m.

also Aqua Voyage, a provider of luxury yacht management and private cruise services, and Sealine Yachts Asia, which has the exclusive distribution rights of the UK boat brand in Singapore and China.

For the next five years, Ong’s ambition as a CEO is to refocus the KOP Group on its core business: real estate. ‘I think we’ve had enough expansion, so we need to consolidate and then expand within the scope of businesses we have,’ she says. ‘I’m not planning to cut out some of the businesses, but I will pay less attention to them. These businesses are doing very well; we’ll let them run their course and see where they are going.’

As for listing KOP, Ong says that it’s not on her radar right now. ‘It will happen,’ she says. ‘It’s just a question of when.’

Sonia Kolesnikov-Jessop, journalist

15

SG_F_Ong.indd 15 12/10/2012 17:07

Sushi on conveyor belts from Sakae Sushi, OSIM International’s high-tech massage chairs and

BreadTalk’s prestigious buns. These are among the products gaining cachet overseas as Singapore’s companies extend their footprints beyond the confines of a small local market.

According to government agency International Enterprise (IE) Singapore, companies tend to favour doing business in South-East Asia and China due to geographical proximity and cultural similarities. ‘However, we are constantly on the lookout for new regions for Singapore companies to diversify their investments,’ IE Singapore’s group director of customer services, Tan Li Lin, says.

The agency considers emerging markets such as Myanmar and Latin America, as well as second-tier cities in China and Africa, as potential bright spots against the current economic backdrop. These markets are promising because of their rapid development, growing population and rising standard of living, Tan says.

Singaporean companies can turn to this global network for market

intelligence, including knowledge on new sector opportunities, market players, attractiveness, structure and risks. In May IE Singapore opened its 36th overseas centre, in Istanbul, Turkey, and has set its sights on Yangon in Myanmar and Ghana next.

‘With increasing volatilities and global competition, we recognise the need to engage Singapore companies even more closely and help them grow into globally competitive companies (GCCs),’ Tan says. ‘GCCs are Singapore’s engine for long-term sustainable growth. Besides contributing to Singapore’s economies, they create high-value jobs with regional or global responsibilities for Singaporeans, building a workforce with a global outlook.’

IE Singapore launched the Global Company Partnership (GCP) initiative earlier this year to engage companies more strategically and proactively. ‘By better understanding companies’ business plans, we can formulate comprehensive solutions for their international growth through capability building, market access and financing,’ Tan says.

Singaporean companies have cited keen competition, lack of manpower to manage overseas operations and difficulty in finding business partners as the top three challenges when doing business abroad, based on the findings of IE Singapore’s Internationalisation Survey 2011/2012.

A recent Ernst & Young report –Beyond Asia: Strategies to Support

the Quest for Growth – stated that in internationalising their businesses, there are several areas where Singaporean executives feel less optimistic about their abilities than their Asian counterparts. For example, 52% of Singapore respondents believed that making corporate culture more international is the most critical change needed for their international plans to succeed, compared with 42% for Asia as a whole. Only a quarter thought that their top management has an international outlook in decision making (the survey average was 34%).

Joshua Yim, CEO of local recruitment and employment agency Achieve Group, expressed surprise at the findings. ‘The senior executives whom I have been personally in touch with generally have a strong international outlook,’ he says. But in the case of homegrown multinational corporations (MNCs), he added that ‘some of them may still be shy of a strong international mindset’.

Yim believes that Singaporean companies have a great deal of ambition to grow worldwide and create a regional and global footprint – but they must be prepared. ‘To go global, management will need to broaden their mindset, especially with regards to handling diversity and ambiguity,’ he says. ‘This includes dealing with different cultures.’

Talent scoutOne of the problems that companies face when venturing overseas is finding

ACROSS THE MILESSingapore’s companies are being urged to increase their global competitiveness – and reap the rewards. But they must fi rst gain the confi dence to make the international leap

‘TO GO GLOBAL, MANAGEMENT NEED TO BROADEN THEIR MINDSET, INCLUDING DEALING WITH DIVERSITY’ JOSHUA YIM

‘TO GO GLOBAL, MANAGEMENT NEED TO BROADEN THEIR ‘TO GO GLOBAL, MANAGEMENT NEED TO BROADEN THEIR MINDSET, INCLUDING DEALING WITH DIVERSITY’ MINDSET, INCLUDING DEALING WITH DIVERSITY’ JOSHUA YIM

16

SG_F_expansion.indd 16 08/10/2012 16:19

available talent; many Singaporeans are averse to overseas postings, being comfortable in their current environment, or they may have family commitments, Yim adds.

Last year, more than 34,400 companies approached IE Singapore for help in understanding overseas markets, connecting to the right business partners and developing capabilities. It partnered companies on 336 overseas projects, with two-thirds taking place in developing regions such as Indonesia, United Arab Emirates and Vietnam, Tan says. China saw the most interest, accounting for 104 overseas projects.

Indeed, companies such as OSIM International and BreadTalk Group, both listed on the Singapore Exchange (SGX), have been making a beeline for the world’s second largest economy. BreadTalk, which has a presence in 16 countries, made its first foray into China in 2003 and plans to double the number of bakery outlets there to more than 500 in the next two years, according to a recent Straits Times report. This is in line with plans to boost its global network of stores to 1,000 by 2014, the report said.

China’s increasing affluence and market size is also a draw for OSIM, which has 267 outlets in 45 cities in the country. In a 2008 survey by international market research firm Synovate, OSIM came up as the top healthy lifestyle products brand across Asia. There are more than 1,000 OSIM outlets in 228 cities across 31 countries, and OSIM’s founder and chief executive Ron Sim is among the 40 richest Singaporeans, according to a ranking by Forbes.

Local optical retail chain Nanyang Optical, which has four stores in

Beijing under a joint venture, also sees potential growth in Asia, especially China, its managing director Bernard Yang says.

While venturing overseas can reap rewards, it is not without its problems, as Yang can attest to; he cites finding the right person to take care of the group’s overseas business as a key challenge. ‘Getting the right partner who has experience in the industry, is reliable, and shares the same vision and objectives for the business makes it smoother,’ he notes.

Positive reputationOn the plus side, ‘being known as a Singapore home-grown brand has given our business added confidence due to Singapore’s positive global reputation,’ Yang says. Nanyang Optical has benefited from grants from Spring Singapore – the governmental agency dedicated to the promotion of Singapore’s economic growth and

‘SINGAPOREANS MUSTHAVE THAT SPIRIT OF ENTERPRISE AND TAKE ANY GOVERNMENT SUPPORT AS A BONUS. DO NOT WAIT FOR SUPPORT TO COME’CHAN CHONG BENG

17

SG_F_expansion.indd 17 08/10/2012 16:20

productivity – to defray some of its research and development costs for frame design and innovation.

For Goodrich Global Holdings, heading overseas was a given as it sought a bigger market. Its chairman Chan Chong Beng, one of two founders of the interior furnishings company, made the first overseas foray back in 1986, to Malaysia. The company now has about 30 offices across eight countries, including Indonesia, China and United Arab Emirates, with annual sales expected to cross S$100m this year.

Chan’s experience navigating the ups and downs of operating overseas epitomises the challenges of venturing abroad. He first entered the China market in 1994 with a partner but wound up the business there two years later as things did not work out with that party. ‘I realised that handling China from Singapore was too far,’ he recalls. ‘So I started a Hong Kong office, and from there expanded to China.’

Chan, who is also president of the Association of Small and Medium Enterprises (ASME) which has five global centres supporting members overseas, stresses that ‘finding the right partner is very, very important.’ His advice to businesses eyeing overseas markets is to spend as much time as possible in those places in order to understand the local conditions.

There can, he notes, be a multitude of issues. For example, the wallcoverings that Goodrich distributes are fire-rated to British standards that are not recognised in China, where each province applies its own regulation. In addition, the issue of copying led Goodrich to target the high-end market such as five-star hotels.

Chan says that venturing overseas is a matter of survival for the long term. Small and medium-sized enterprises face problems in Singapore such as a labour crunch and high rentals, with many eking out razor-thin profits. This can make expansion overseas more difficult, he says.

Conversely, with the cost of doing business in Singapore set to rise further, companies will come under

When Douglas Foo switched from the garment business to food in the late 1990s, his ambition right from the start was to build a global brand.

‘When we decided to go into food, the dream was big, really big,’ he says. How big? Think the likes of McDonald’s, KFC, Starbucks and Pizza Hut.

Now, Singapore Exchange-listed Sakae Holdings, the company he founded, has more than 80 outlets in Asia, the bulk of them in Singapore and Malaysia and under its flagship Sakae Sushi brand. The group also has a presence in Thailand, Vietnam, Indonesia, the Philippines and China.

Famous for offering sushi via conveyor belts and making the Japanese cuisine affordable for many, Sakae opened the first Sakae Sushi outlet in Singapore in 1997, when the Asian financial crisis was raging. Soon after, Foo, who is Sakae’s chief executive, travelled to Jakarta, Indonesia, during a period of unrest and rioting. The faint-hearted might have found the situation daunting, but not Foo. He saw opportunities instead, viewing the problems in the country then as isolated incidents.

During troubled times, the cost of opening a business is lower, he says. ‘You get more opportunities and access to talent. Not many people would go in and fight with you to hire people,’ he says. With this in mind, Foo went on to open Sakae Sushi’s first overseas outlet in Indonesia.

Foo wants to grow a global brand with a presence in all five continents – just like McDonald’s, Starbucks, Pizza Hut and KFC – and for people to think of Sakae whenever they think of sushi.

The overseas expansion has not been without snags. He opened two outlets in New York before the Lehman crisis broke out and had to stop operations due to high rentals secured prior to the financial crisis. He is in the midst of renegotiating the rentals with the landlord.

Currently, Foo’s focus is more on Asia rather than elsewhere as the regional economy is more robust. But, he emphasises, the overriding factor in any decision to enter a new market would be the availability of the right talent.

According to a recent survey by Ernst & Young – Beyond Asia: Strategies to Support the Quest for Growth – about half of Singapore executives feel that their organisation’s management needs more insight into local cultures and ways of doing business in order to excel in the global marketplace.

Sakae gets round the problem by turning to local hires to manage its overseas outlets instead of posting Singaporeans abroad. Local managers on site will be more familiar with conditions there and can better deal with any challenges that might crop up. Foo says he is building a global team of people with a global outlook who would have the network and resources in the various places Sakae is operating in. ‘That would be the edge that we will have against others,’ he says.

‘If you try and understand the local culture within a short time frame, the learning curve is steep,’ he adds. ‘That’s why our strategy is to hire a person who has grown up in that market.’

*HIRE LOCAL TALENT

garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start garment business to food in the late 1990s, his ambition right from the start

pressure to relocate production overseas and target markets outside Singapore, he says. Goodrich itself is considering shifting its headquarters from Singapore to China, where the market is huge and costs are lower, Chan reveals.

While Chan hails the wide range of government grants and schemes

available to help Singapore firms go global, ‘Singaporeans must have that spirit of enterprise and take any government support as a bonus,’ he says. ‘Do not wait for the support to come before you move. You must find a way to survive first.’

Suki Lor, journalist

18

SG_F_expansion.indd 18 08/10/2012 16:21

Swiss know-how

Independence

Tradition

Discretion

Customisation

Reliability

Asset Management Trusts & Foundations Multi-Family Office International Trade

Hong Kong Lugano Zurich Amsterdam Luxembourg Malta Dubai Sao Paolo Panama London

Address: 3204-05 32F Alexandra House, Central, Hong Kong Telephone: +852 31082720 Email: [email protected] www.vecogroup.ch

AB_2012.06-Veco Group SA.indd 1 2012/5/18 2:24:12 PM

Ads-JulyAug12.indd 6 12/06/2012 15:11

Aspectre is haunting Europe: that of a possible Greek default and exit from the euro. A Grexit, as it has

been called, could have catastrophic repercussions for the economies of Europe – and possibly the world too – or it could provide some kind of solution for the troubled eurozone and the heavily indebted country. Amid the uncertainty, one thing seems certain: nobody really knows what such an event will mean.

‘Nobody has ever gone to hell or to paradise and returned to tell us how it was,’ Harilaos Alamanos, president of Greece’s Institute of Certified Public Accountants (SOEL), told Accounting and Business. ‘Nobody knows how an exit will be achieved. And the experience of entering the euro does not help with how an exit from the currency might go.’

For professional accountants, a Greek euro exit could mean an upgrade of their role, according to Alamanos. ‘We will have to assess the implementation of all the changes that will be imposed on businesses or in the wider public sector companies. But while this may be good for the sector, as it will bring more jobs, it is obviously bad for the country.’

Jonathan Loynes, chief European economist and director at London-

based Capital Economics, the company whose Roger Bootle won the Wolfson Economics Prize on the smoothest process by which a member state could exit the eurozone (see pages 23–24), says that his firm’s view is that ‘a Greek exit is more likely than not’.

Exit ‘80% likely’Unlike most other forecasters, Capital Economics has built such an event into its central economic projections. Loynes says: ‘It’s hard to put an exact number on it, but I would estimate something like an 80% chance that Greece will be out by the end of 2013. There are few signs as yet of policymakers taking the steps we mapped out in the Wolfson entry but that is not surprising as the entry dealt with how to manage a country’s exit, which has not yet commenced.’

Much of how a Greek exit might look depends on whether the country defaults in an orderly or disorderly fashion. Dr Vassilis Monastiriotis, senior lecturer at the London School of Economics and affiliate at the Hellenic Observatory, believes that the catastrophe of a disorderly exit would bring upheaval to the markets.

He says: ‘The immediate effect would be that bank accounts would be frozen so the Greek economy would collapse until a new currency was issued. Hyper-

inflation will intensify problems of poverty in the population, destabilising the situation socially and politically. The country will operate basically on a cash economy and foreign investment will stop.

‘Imports will become hugely expensive as importers would have to pay cash in a very devalued currency. All domestic companies would find it impossible to operate in the international market unless they hold liquidity in foreign reserves, which very few companies do. Not many companies would survive this for long.’

This, however, is a scenario that most analysts, including Monastiriotis, consider unlikely. What is expected is an orderly exit where the eurozone

GREXITGRIEFWhat would be the effects of a Greek exit from the eurozone for accountants and Greece’s trading partners?

20

AP_F_Grexit.indd 20 08/10/2012 10:47

caption style

partners agree with Greece a procedure to phase the country out of the eurozone. Monastiriotis says he expects the European Central Bank (ECB) to guarantee liquidity in the Greek banking system during a transition period.

‘There will be a combination of measures that control capital movements with a number of guarantees to ease the pressures arising from that,’ he says. ‘Liquidity will be provided to the banking system,

and, I imagine, there would also be measures to provide liquidity directly to large companies through loan guarantees or short-term lending.’

Who gets the reserves?Greece’s foreign reserves would be put in the spotlight. ‘If a country is to exit the eurozone, do they get their initial allocation of foreign reserves? Is the ECB going to keep them as collateral against the Greek debt held by the ECB or other member states? These

are issues that cannot be resolved overnight,’ says Monastiriotis.

Constitutional issues may also arise for the EU about the extent to which a euro exit could be accommodated without breaching the rules that underpin the European single market.

Monastiriotis explains: ‘Legally there are ways to allow for a temporary deviation and non-implementation of specific regulations and we have had examples of that in the EU context before. But of course these may be challenged in court by different companies or individuals that may be affected, and it may not be an easy situation for Greece or the EU.’

Foreign exchange markets are already assessing the possibility of a

‘LIQUIDITY WILL BE PROVIDED TO THE BANKING SYSTEM, AND TO LARGE COMPANIES THROUGH LOAN GUARANTEES OR SHORT-TERM LENDING’

21

AP_F_Grexit.indd 21 08/10/2012 10:47

‘SPAIN, ITALY AND PORTUGAL COULD EASILY FOLLOW THE GREEK PATH. BUT THE REAL QUESTION IS: WHEN WILL IT STOP? WILL FRANCE BE THE NEXT?’

Greek exit and how that would affect the euro and a new Greek currency. In June, Bloomberg shocked foreign exchange dealers by testing on its live exchange rates system a post-euro Greek drachma code (XGD) as part of ‘contingency planning exercises in the normal course of business’.

Igor Drobnjak, director of markets at foreign exchange specialist Tempus UK, part of the Monex Group, says: ‘In some ways the markets have already included the potential Greek default in the price of the euro. Only in 2012 we saw the euro drop against a basketful of currencies. Although this depreciation of the euro makes European goods more competitive on international markets, it is making eurozone debt less attractive. This means that most of the major investors and the banks, especially in the US, are carrying their positions on a Greek debt, which brings additional volatility.

‘Eurozone debt is mainly traded within peripheral countries. You don’t have so much exposure of Greek, Italian or Spanish debt in the global markets. It became more localised and in a way that is a natural hedge for these countries because they can devalue on their own the bonds they have issued. However, European banks – especially those that have the majority of exposure to that debt – will have to take the loss and put it on their balance sheet.’

And the kitchen sink too…A Greek exit would also raise issues of liquidity in other European countries. All the responsibility for providing liquidity in eurozone countries hit by a Greek exit ‘will be held by the ECB, which will likely need to resume bond buying, move rates to 0%, and apply any other non-conventional tool, if not all of them’, says Valeria Bednarik, chief analyst at Barcelona-based independent forex portal Fxstreet.com.

As for the fallout in exchange rates, Bednarik says that ‘among currencies, [US] dollar and yen will be the first beneficiaries probably followed by commodity currencies, Australian and Canadian dollars – the new market safe

havens. The pound, on the other hand, will likely feel the weight of a European crisis and be pressured lower. The most benefited will be the Swiss franc, as the SNB [Swiss National Bank] will regain some air after the recent struggle to control the Swiss strength and establishing the EUR/CHF peg.’

Credit insurance costs have also been affected. A spokesperson for UK Export Finance, Britain’s official export credit agency, says that as market risk

appetite varies for different countries, businesses interested in exporting to Greece have been asked to get in touch for a case-by-case assessment, unlike what happens with other advanced markets. UK Export Finance now accepts ‘applications for short-term cover for export contracts between UK exporters and buyers in Greece’ after the European Commission lifted for Greece a restriction on providing trade credit insurance cover for exports to buyers in the EU where the risk horizon is under two years.

Meanwhile, trade-related insurance provider Euler Hermes says it will stick to a May statement that anticipated Greece remaining in the eurozone. It has, however, reduced its export cover on Greece as continued economic uncertainties make exporting to Greece substantially more risky. The company says it ‘is currently not covering new shipments to Greece, although shipments scheduled for delivery before the end of July remain insured’.

Drobnjak says: ‘The major question now is to see whether the Greek scenario is a separate case or if it endangers [other eurozone] states. A Greek exit could create a vicious spiral endangering the core of the single region; in that case the only countries that could stay in the eurozone would be Germany, the Netherlands, France and Finland – not the best-case scenario for the euro per se.’

Noemí Jansana, head of content at Fxstreet, says the big problem for Spain is that a Greek exit ‘would set a precedent that could favour the exit of other European peripheral countries and Spain, Italy and Portugal could easily follow the Greek path. But the real question is: when is it going to stop? Will France be the next? And then what?’ She believes that European leaders will do whatever it takes to preserve the euro’s integrity.

Monastiriotis says: ‘The transactional cost, the cost in political capital, the reputational cost that will be suffered by the EU, let alone the consequences for Greece itself, will all be huge. This is why all players will try to avoid a Greek exit.’

More power for troika The Greek government, Monastiriotis says, ‘will either find somehow the capacity to implement some of the measures to take forward the remaining reforms, in which case the measures may be softened, or we will move eventually into stricter forms of monitoring, so the troika of lenders [the EU, the ECB and the IMF] will be more involved in decision-making, controlling the government finances to resolve the deadlock’.

Meanwhile Greece is the country feeling the burden the most. Alamanos says: ‘The businesses that are closing are usually the healthy ones, which pay their taxes, salaries, contributions to pension funds, etc. The rogue ones just don’t bother. They pay nothing and they are an unfair competition to the healthy ones.’

Whatever the outcome, an outcome should be reached soon as the euro and Greece itself are paying a heavy price for uncertainty.

Michael Kosmides, journalist based in Athens

22

AP_F_Grexit.indd 22 08/10/2012 10:47

BREAKING UP IS HARD TO DO……but not impossible. Roger Bootle, winner of the Wolfson Economics Prize to create a blueprint for dismantling the euro, has written a meticulous instruction manual

One of the cardinal rules of firefighting is always identify your exit before entering a blaze. Several

eurozone nations must wish they had followed this advice when joining the continent’s bold experiment in currency union. Since the euro was intended to be a club that none could leave, no emergency escape plans were ever made.

Lord Wolfson, a eurosceptic, wants to change that. He issued a challenge to economists to draw up a blueprint on how best to dismantle the currency. The £250,000 prize attracted 400 entries and was won by veteran commentator Roger Bootle, founder of the consultancy Capital Economics

and former chief economic adviser to Deloitte. His winning submission is a meticulous instruction manual on how failing states can extract themselves from the zone in an orderly manner.

Whitewash-freeThe first merit of Bootle’s 156-page handbook is that it doesn’t sugarcoat the risks. Any nation wishing to exit the crumbling structure will confront a huge range of dangers. For a start, all hell would break loose if news of an imminent departure were to leak to the press. Citizens would make a beeline for the bank and immediately withdraw their savings, provoking an instant financial crisis. The replacement currency would plunge on the foreign

exchange markets – in the case of Greece possibly by up to 50%.

Of course, currency devaluation is the ultimate goal of leaving the zone as it would eventually boost exports and promote economic growth. In the short term, however, it would raise the risk of hyperinflation. Rampant price rises would undo any gains in competitiveness and leave the hapless state back where it started.

Then there are the practical issues of printing a new currency. A country could be left without cash in circulation for up to six months.

One ironic effect of leaving the zone would also be to boost the real value of the nation’s foreign debts. So far from solving a debt crisis, leaving the euro

23

AP_F_eurobreakup.indd 23 11/10/2012 10:51

caption style

‘CASH MACHINES WOULD NEED TO SHUT DOWN.OTHERWISE RESIDENTS WOULD TRY TO WITHDRAWAS MANY EUROS AS POSSIBLE FROM ACCOUNTS’

would actually make matters worse – at least in the short term.

‘Our goal in the euro paper was to find a way around some of these perils,’ says Jonathan Loynes, chief European analyst at Capital Economics and one of the co-authors of the plan. ‘We looked to the history of currency break-ups – such as the collapse of the Soviet Union and Czechoslovakia – for clues about how this adjustment could be made with the least possible trauma.’

Keep it under your hatThe first challenge is to keep secession plans secret for as long as possible. Ideally, a momentous decision like leaving the euro should be democratic, taking the pulse of all political parties as well as the public.

Sadly, such an inclusive approach is not practical, Bootle warns. Advanced notice of such plans could precipitate ‘large capital outflows as international investors and domestic residents withdraw their funds’. Bond yields would surge and banks quickly run out of cash. So Bootle’s first tip is to keep the exit plan hush-hush until the last possible moment.

The Czech government, for example, decided to break up its currency union with Slovakia on 19 January 1993, following the dissolution of Czechoslovakia in 1992. It concealed this decision from citizens until 2 February, just six days before the two new states adopted separate national currencies.

In his plan Bootle says the key to making a success of the clandestine approach ‘would be to keep the number of people who knew as small as possible and the delay between the decision and implementation fairly short’. Printing a whole new currency ahead of time is probably out of the question, given the lengthy period that such an operation would require.

Closing the hole in the wallOnce the cat is out of the bag, capital and banking controls would be needed to prevent money fleeing the country. ‘Cash machines… would need to be shut down,’ advises Bootle’s plan. ‘Otherwise, realising that the euro would become more valuable than the drachma, most Greek residents [for example] would attempt to withdraw as many euros as possible from their bank accounts.’

Currency controls could be supplemented by forbidding residents from buying foreign assets overseas or setting up bank accounts outside the country. Foreign businesses in the country might also be barred from repatriating profits back to the home office. Capital Economics argues that such radical steps could be avoided if plans are kept hidden – especially if the transition takes place over a weekend when banks are closed.

The most obvious practical issue in leaving the euro is that of minting new notes and coins. Since this might take months, the departing country would be left in limbo. One stopgap solution would be to stamp existing euro notes with a drachma symbol. This is not an option favoured by Bootle. Instead, the Capital Economics plan argues that a country like Greece could largely do without cash for a while.

A recent survey by the European Central Bank showed that cash

accounted for just 5% of total transactions for the majority of businesses. For the small amounts of cash that are needed, the euro could continue to be used until a new currency was ready, Bootle argues.

Another question is the potentially inflationary threats posed by a new currency. Retailers might take advantage of the changeover to raise prices. Many shoppers suspected this happened when the British shifted to a decimal system in 1971. To avoid such covert hikes, Bootle recommends introducing the new currency at parity to the euro, so an item that used to sell for 1.5 euros would sell for 1.5 drachma, although the new currency’s real value could soon fall sharply.

Most crucially, however, the public would have to be quickly convinced that price rises were not going to get out of hand. A new inflation target would need to be set, to kick in after an initial adjustment phase. The nation could also consider issuing indexed bonds, whose interest payments would rise along with prices. This would reduce a government’s incentive to let inflation rip, Bootle says, and so reassure investors and the public.

Return to growthPoliticians could offer another guarantee of good behaviour by setting up an independent auditor to monitor public borrowing. A departing sovereign should also organise an orderly default on foreign debt, writing down debts to a sustainable level so the nation could resume economic growth.

The Wolfson Economics Prize ended up underlining many of the dangers of a euro split. But thanks to the Tory peer, discussing the practicalities of a breakup is no longer a taboo.

Christopher Alkan, journalist

would actually make matters worse – at

Bootle: euro exit masterplan

24

AP_F_eurobreakup.indd 24 11/10/2012 10:51

19 Oct 2012th

Lexis AB Asia adverts1-Nov12.indd 1 08/10/2012 12:26

Over the past two decades we have recognised that the way we do business has a serious impact on the world

around us. It is now apparent that the state of the world affects the way we do business. The central challenge of our age – maintaining human progress while minimising resource use and environmental decline – can simultaneously be one of the biggest sources of future success for business.

Given the unprecedented natural resource scarcity, skyrocketing food prices, escalating energy security issues and an expected population of up to 10 billion in 2100, the private sector is ever more challenged to overhaul its strategy and make its business models futureproof. For example, if companies had to pay for the full environmental costs of their production, they would lose 41 cents for every US$1 in earnings on average. External environmental costs of 11 key industry sectors (including upstream supply chain) rose by 50% between 2002 and 2010. They include things like pollution – external costs that society will likely have to pay for in the future but are not included in transaction prices.

Today’s leaders are struggling with complexity. Until now, we found global trends on energy, water security and

food scarcity complex enough. The convergence of other forces such as population growth, deforestation and a surging middle class is impacting on business and the world around us.

Leaders are overwhelmed by the sheer scale of these problems and are struggling to act. There are ways to solve these problems, and that includes harnessing the capacity of business. Policymakers and the business community should ramp up collaboration and demonstrate renewed leadership in order to achieve sustainable and equitable growth objectives.

Government policies, investor values and consumer preferences are also altering rapidly, thus impacting businesses’ bottom line and demanding a long-term vision, supported by immediate action. Is this forced by stakeholder demand, or primarily driven by sound entrepreneurship? It is up to each and every company to decide for itself.

Rather than attempting to survive risks resulting from global megaforces, business leaders can do much more. Indeed, with foresight and planning, and by undertaking pioneering actions to prepare for an uncertain future, they can thrive by turning risks into new opportunities. Companies need to develop resilience and flexibility for an

unpredictable future and build capacity to anticipate and adapt.

Understand the risksFirst and foremost, businesses need to fully assess and understand future sustainability risks, for example by integrating them into an enterprise risk management tool, defining their responses to deal with them, and analysing opportunities for efficiency, substitution or adaptation.

Integrated strategic planning and strategy development are needed as well; this requires business management to make sustainability central to their corporate strategy and incorporate it at all levels. Put simply, businesses must manage risks and capitalise on opportunities by turning strategic plans and strategies into ambitious targets and actions. One can think of energy and resource efficiency improvements, sustainable supply chain management, and investment into innovation on sustainable products and services, as well as gaining access to new markets for greener products, services and technologies. It is also imperative to explore tax incentives tailored to alternative energy, energy efficiency and other areas related to sustainability.

Another much discussed but less implemented tool for success in this area is measuring performance and

A CLARITYOF VISIONCompanies are starting to see the link between sustainability and fi nancial results, says KPMG special adviser and former UN climate chief Yvo de Boer

26

AP_F_Yvo.indd 26 12/10/2012 16:55

reporting on sustainability, as well as the related benefits. The growing trend of integrated reporting is an example of how companies are building frameworks for sustainability reporting processes, stronger information systems and appropriate governance and control mechanisms on a par with those currently used in financial reporting.

Time to talkOrganisations cannot do this alone. Collaboration with partners on sustainability issues is vital to enhance leverage and improve the cost-benefit ratio of action. Business leaders should seek opportunities for genuine dialogue with governments and demonstrate new and innovative approaches to public-private partnerships. Improved dialogue could focus on economic instruments and market barriers that could be reduced to make sustainable business operation easier. Good management used to be about preparing for the expected; now it is just as much about preparing for the unexpected. Without action and strategic planning, risks will multiply and opportunities will be lost.

KPMG’s clients and business all over the world are seeing the link between sustainability and financial results becoming increasingly clear. Companies that recognise the external influences on their organisations and leverage them as opportunities are realising a competitive advantage. To that end, the exercise of measuring and reporting sustainability activities to stakeholders with clear, accurate data is increasingly relevant and quickly becoming a priority.

Competitive advantage can be carved out of emerging risk. It is clearly no longer in question that we must transcend to a more sustainable economy. The question is the pace in which we are able, and especially willing, to achieve it.

To thrive, or even just to survive, businesses need to understand the root causes of what affects their operations, not just the symptoms. The bold, the visionary and the innovative recognise that what is good for people and the planet will also be good for the long-term bottom line and shareholder value. This is how we can make our common economy futureproof.

Yvo de Boer is KPMG’s special global adviser on climate change and sustainability, responsible for driving the development of the firm’s Sustainability Service. He is former executive secretary to the UN Framework Convention on Climate Change (UNFCCC), and currently chairs the World Economic Forum’s Global Agenda Council on Climate Change. De Boer helped to prepare the position of the European Union in the lead-up to negotiations on the Kyoto Protocol; assisted in the design of the EU’s internal burden sharing; and has led delegations to UNFCCC negotiations.

MEASURING AND REPORTING SUSTAINABILITYACTIVITIES TO STAKEHOLDERS WITH CLEAR,ACCURATE DATA IS QUICKLY BECOMING A PRIORITY

*YVO DE BOER

27

AP_F_Yvo.indd 27 12/10/2012 16:56

SILVER LININGFOR THE BOARD

The cloud is all about computing as a service rather than a product. It supports the sharing of resources – both

hardware and software – through a web browser over the internet. This makes it ideal for companies of all shapes and sizes. By treating IT as a commodity, they can get what they need, when they need it, without heavy investment.

Years ago, the largest part of the IT investment by far was the hardware. This is no longer the case. Software, along with licences, maintenance, upgrades, staff training and technical support, is a significant consideration. But cloud computing and, in particular, software-as-a-service (SaaS) can also take the sting out of the software budget.

The advantages of SaaS range from low cost of entry to global accessibility, but also include ‘softer’ features such as easy administration and collaboration. The choice of applications is growing too, and includes sales tracking, accounting, customer relationship management, enterprise resource planning, invoicing, human resources and more.

Board portalsOne excellent example of cloud-based SaaS is the board portal. This technology, which is increasingly finding favour inside and outside the boardroom, is actually a secure website, which addresses some of the major challenges facing corporate boards: timely compilation, review,

dissection, analysis and approval of corporate information.

Company directors have long been awash with paper, primarily in the form of the board books that are required reading before every full board and many committee meetings, and although some may pigeonhole them as a group of Dickensian technophobes, this stereotype couldn’t be further from the truth.

Today’s directors are not only tech-savvy and fully aware of the efficiencies that notebooks, smartphones and tablets can offer, they are already using these tools in the office, on the road and at home. The idea that technology can streamline board preparation is far from alien.

An organisation’s board materials can run into hundreds of thousands of

Cloud computing is revolutionising business and one particular development is allowing board members to dispense with cumbersome books, explains Eslinda Hamzah

28

AP_F_cloud.indd 28 15/10/2012 11:51