a study on brand awareness and customer preferences about icici prudential life insurance ect

TRANSCRIPT

A Project Report On

“A STUDY ON BRAND AWARENESS AND CUSTOMER PREFERENCES ABOUT ICICI PRUDENTIAL LIFE INSURANCE IN

CHENNAI CITY.”

By

Mr. S.ANTONY PRABHU (Registration number: 32006631004)

Of

SRR ENGINEERING COLLEGE, PADUR, CHENNAI-603103

A project report (BA-1719 Summer Project Report)

Submitted to

FACULTY OF MANAGEMENT SCIENCES In partial fulfillment of the requirementsfor the award of the degree of

MASTER OF BUSINESS ADMINISTRATION ANNA UNIVERSITY

AUGUST-2008

SRR ENGINEERING COLLEGE PADUR, CHENNAI-603103

DEPARTMENT OF MANAGEMENT STUDIES

15.04.2008

CERTIFICATE

This is to certify that the project report on “A STUDY ON BRAND AWARENESS AND CUSTOMER PREFERENCES ABOUT ICICIPRUDENTIAL LIFE INSURANCE IN CHENNAI CITY.” Is a bonafide summer project work done by Mr. S.ANTONY PRABHU, a full

time student of the department of management studies, SRR Engineering

College, in partial fulfillment of the requirements for the award of the degree of

Master Of Business Administration of Anna University, during the year 2006-

2008.

PROF.G.DILEEPHead of the Department MR.R. RADHAKRISHANAN

Faculty Guide

DECLARATION

I , S.ANTONY PRABHU a bonafide student of Department of

management Studies, S.R.R Engineering college, Old Mamallapuram Road, Padur, Chennai-603103,Would like to declare that the project entitled “A STUDY ON BRAND AWARENESS AND CUSTOMER PREFERENCES ABOUT ICICIPRUDENTIAL LIFE INSURANCE IN CHENNAI CITY.”in partial fulfillment of MBA Degree course of the ANNA UNIVERSITY is my original work.

Place: S.ANTONY PRABHU Date: (Reg.No.32006631004)

ACKNOWLEDGEMENT

At the outset, I praise the lord. The almighty for his abundance of grace in giving me health, knowledge, wisdom and strength to take up this project and complete it in time. I was fortunate to have the assistance of many people in this effort.I am immense pleasure to thank my family to help me to finish my

projects

I am indebted to Honorable Founder & chairman Dr.JEPPIAAR, M.A.,

B.L., PhD, for his sincere endeavor in educating us in his Premier

Institution.

My sincere regards are also due to our beloved & Head of the Department,

prof.G. DILLEP for giving necessary support during this project.

I would like to thank, MR. MR.R. RADHAKRISHANAN

Faculty Guide, for successful completion of the project work.

I wish to express my thanks to all our Department staffs, for their valuable suggestion during the period of my project work.

I would like to place my graceful thanks to SPA Capital Service for

allowing me to carry out the study for motivating me to complete the project

work in time.

I would like to thank my colleagues and my friends for the valuable support

and contribution to the completion of my project.

S.J.ANTONY PRABHU

TABLE OF CONTENTS

S.NO. CONTENTSPAGE

NO

University title format I

Company Certificate II

List of Tables VII

List of Charts IX

List of abbreviationsXI

1 Introduction 1

2 Company profile 4

3 Industry profile 7

4 Product profile 15

5

RESEARCH METHODLOGY

a. statement of the problem

b. Need of the Study

c. Objectives of the Study

d. Sampling size and type

e. Methodology

18

19

20

21

22

6

f. Tools for data collection

g. Tools for data analysis

h. Scope of the Study

i. Limitations of the Study

Analysis and interpretation

23

24

26

27

7 FINDINGS & CONCLUSION

Findings

Suggestions

Conclusion

55

56

5657

8 BIBLIOGRAPHY 58

9 APPENDIX & ANNEXURES 59

57

LIST OF TABLES

S.No. TITLE OF THE TABLEPage

No.

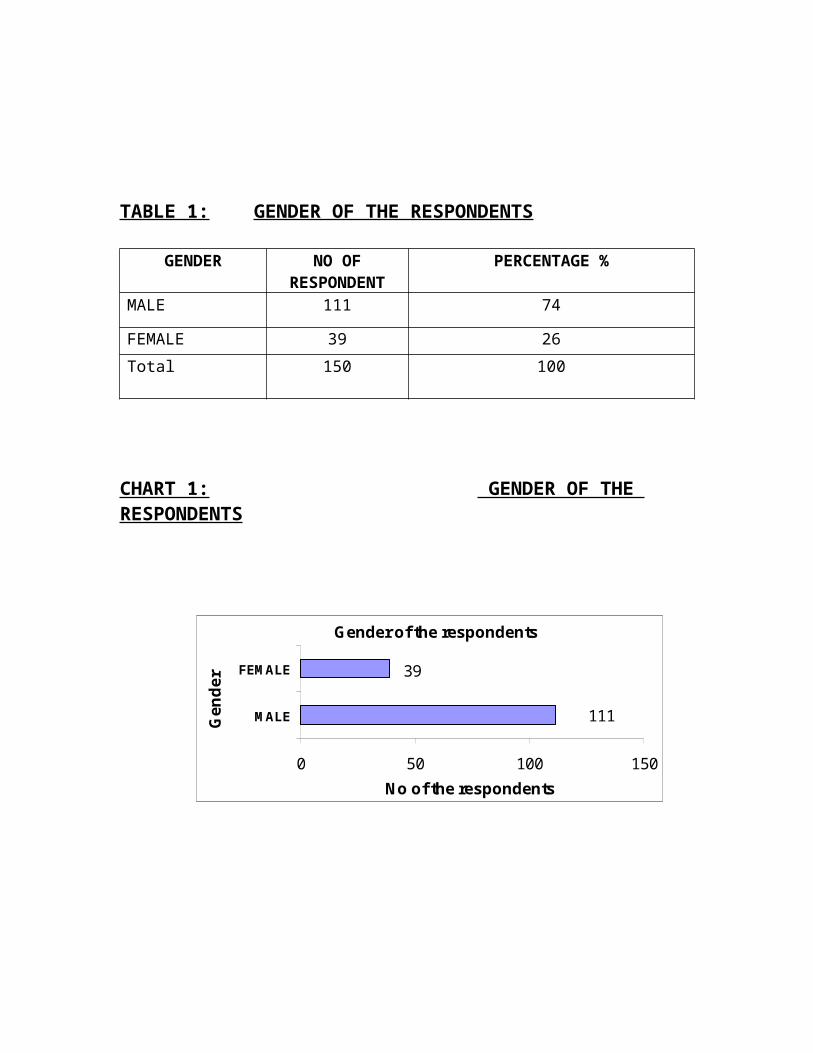

1 GENDER 28

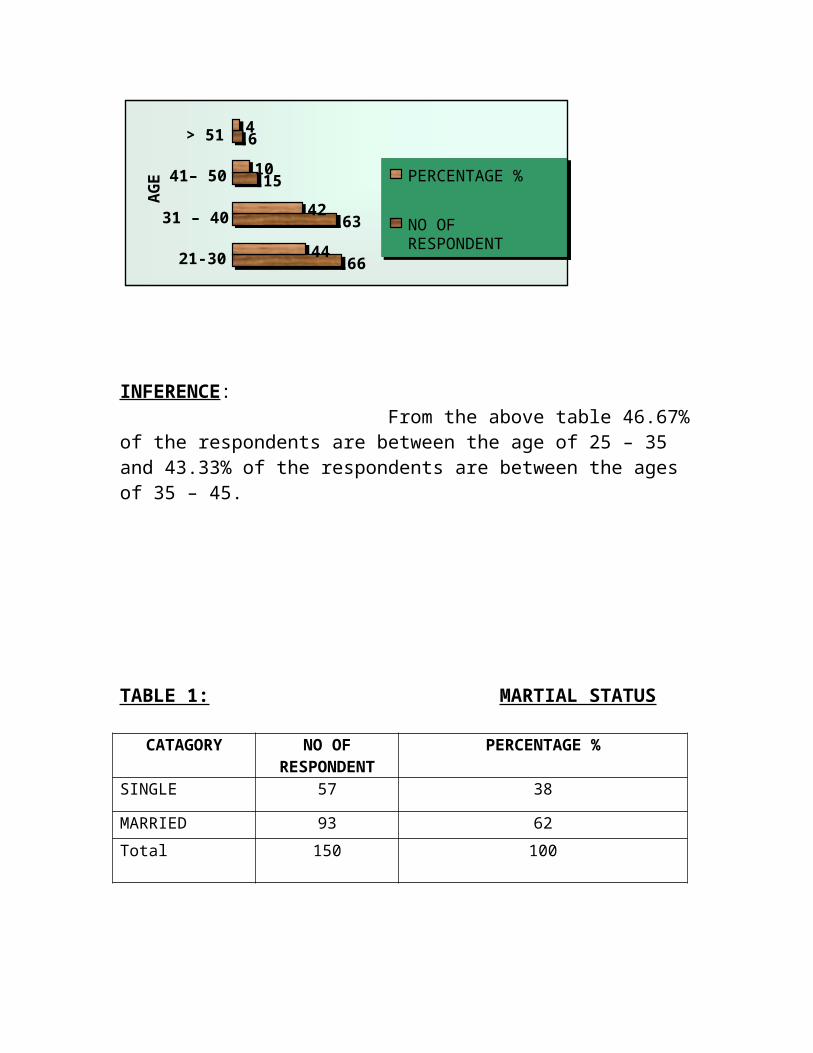

2 AGE OF THE RESPONDENTS 29

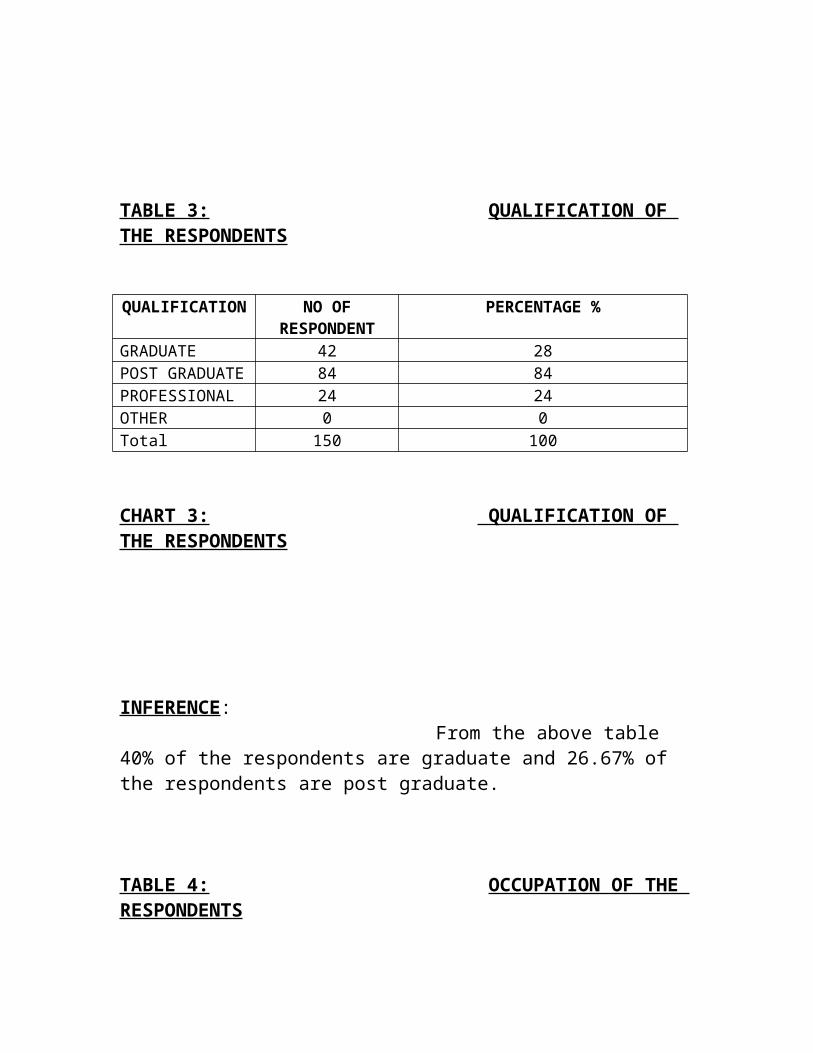

3 GRADE LEVEL/OCUPATION 30

4 EDUCATION QULIFICATION 31

5 INCOME PER MONTH 32

6AWARENESS ABOUT THE HL OF ICICI

ANGAYARKANNI MARKETING PVT LTD33

7WHICH BANKS COMES YOUR MIND FIRST

TO GET HOME LOAN34

8 HOW DO YOU KNOW ABOUT A.M.P.LTD 35

9TO WHAT EXTEND YOU GO BY GETTING HL

FROM THE BANK36

10INTEREST RATE OF ICICI ANGAYARKANNI

MARKETING PVT LTD37

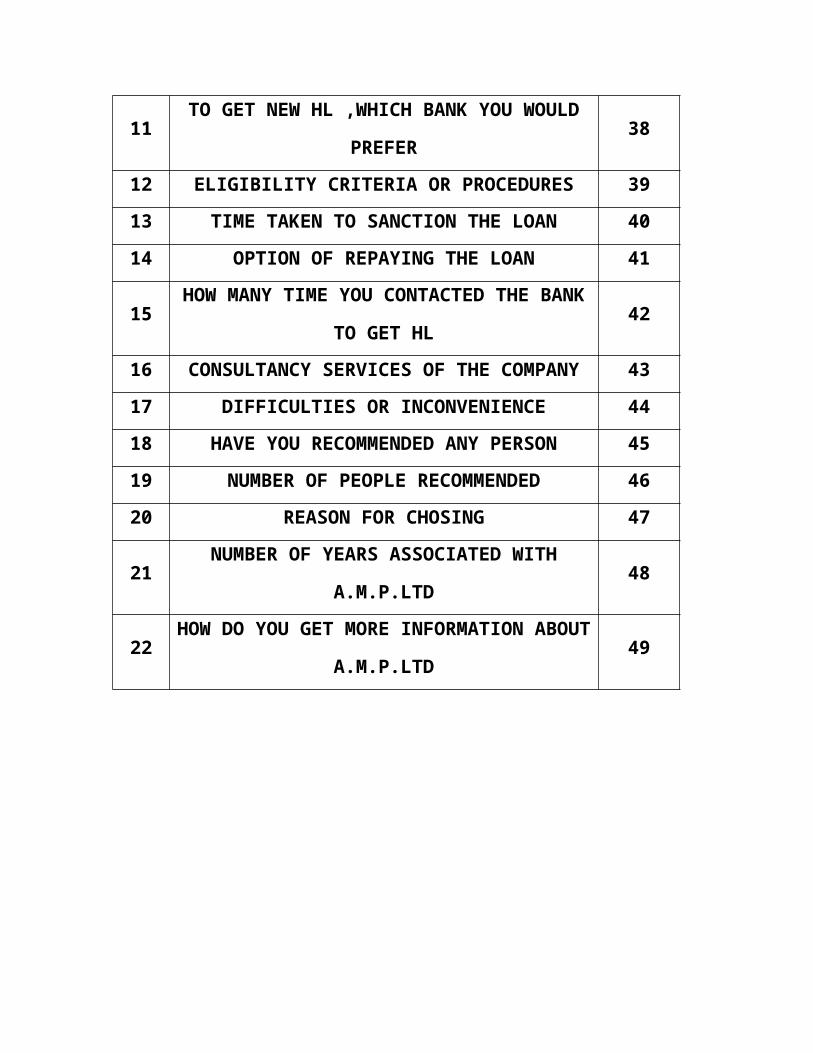

11TO GET NEW HL ,WHICH BANK YOU WOULD

PREFER38

12 ELIGIBILITY CRITERIA OR PROCEDURES 39

13 TIME TAKEN TO SANCTION THE LOAN 40

14 OPTION OF REPAYING THE LOAN 41

15 HOW MANY TIME YOU CONTACTED THE 42

BANK TO GET HL

16CONSULTANCY SERVICES OF THE

COMPANY43

17 DIFFICULTIES OR INCONVENIENCE 44

18 HAVE YOU RECOMMENDED ANY PERSON 45

19 NUMBER OF PEOPLE RECOMMENDED 46

20 REASON FOR CHOSING 47

21NUMBER OF YEARS ASSOCIATED WITH

A.M.P.LTD48

22HOW DO YOU GET MORE INFORMATION

ABOUT A.M.P.LTD49

LIST OF CHARTS

S.No. TITLE OF THE CHARTSPage

No.

1 GENDER 28

2 AGE OF THE RESPONDENTS 29

3 GRADE LEVEL/OCUPATION 30

4 EDUCATION QULIFICATION 31

5 INCOME PER MONTH 32

6AWARENESS ABOUT THE HL OF ICICI

ANGAYARKANNI MARKETING PVT LTD33

7WHICH BANKS COMES YOUR MIND FIRST

TO GET HOME LOAN34

8 HOW DO YOU KNOW ABOUT A.M.P.LTD 35

9TO WHAT EXTEND YOU GO BY GETTING HL

FROM THE BANK36

10INTEREST RATE OF ICICI ANGAYARKANNI

MARKETING PVT LTD37

11TO GET NEW HL ,WHICH BANK YOU WOULD

PREFER38

12 ELIGIBILITY CRITERIA OR PROCEDURES 39

13 TIME TAKEN TO SANCTION THE LOAN 40

14 OPTION OF REPAYING THE LOAN 41

15 HOW MANY TIME YOU CONTACTED THE 42

BANK TO GET HL

16CONSULTANCY SERVICES OF THE

COMPANY43

17 DIFFICULTIES OR INCONVENIENCE 44

18 HAVE YOU RECOMMENDED ANY PERSON 45

19 NUMBER OF PEOPLE RECOMMENDED 46

20 REASON FOR CHOSING 47

21NUMBER OF YEARS ASSOCIATED WITH

A.M.P.LTD48

22HOW DO YOU GET MORE INFORMATION

ABOUT A.M.P.LTD49

LIST OF ABBREVIATIONS

ICICI- INDUSTRIAL CREDIT AND INVESTMENT CORPORATION OF INDIAA.M.P.LTD- ANGAYARKANNI MARKETING PRIVATE LIMTEDPL- PERSONAL LOANCL- CAR LOANCC- CREDIT CARDSAL- AGRICULTURAL LOANSSBL- SMART BUSINESS CARDSBS- BUSINESS CARDSTW- TWO WHEELERESHL- HOME LOANCVL- COMMERCIAL VEHICLE LOANLAC- LAKESDOF- DEGREES OF FREEDOMNRI- NON RESIDENTIAL INDIAN

CRM- CUSTOMER RELATIONSHIP MANAGEMENT

1. INTRODUCTION

1.1ABOUT THE INSURANCE INDUSTRY

Insurance is primarily collective cooperation to share a particular risk. This concept is as old as the dawn of human civilization. The joint family system in India is an example of concept of life insurance is considered to be the oldest branch of insurance for providing protection against loss/damage in sea voyages.

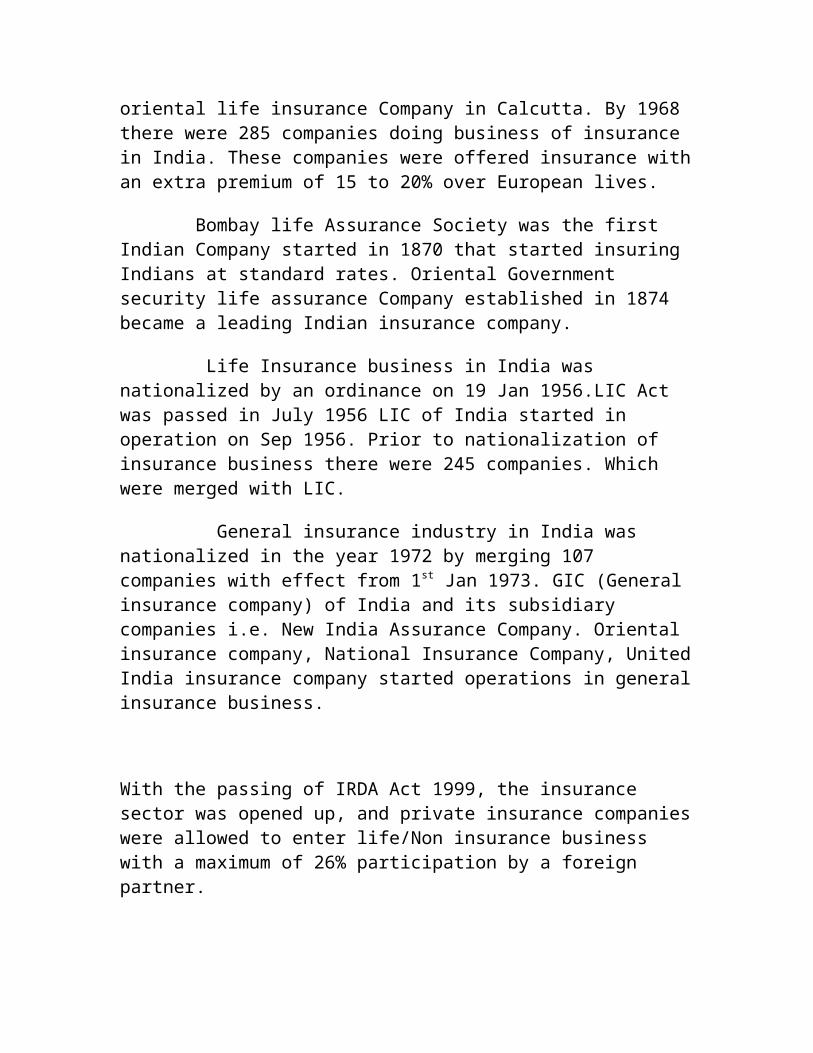

Life insurance in its modern from came to India from England in 1818 with the formation of oriental life insurance Company in Calcutta. By 1968 there were 285 companies doing business of insurance in India. These companies were offered insurance with an extra premium of 15 to 20% over European lives.

Bombay life Assurance Society was the first Indian Company started in 1870 that started insuring Indians at standard rates. Oriental Government security life assurance Company established in 1874 became a leading Indian insurance company.

Life Insurance business in India was nationalized by an ordinance on 19 Jan 1956.LIC Act was passed in July 1956 LIC of India started in operation on Sep 1956. Prior to nationalization of insurance business there were 245 companies. Which were merged with LIC.

General insurance industry in India was nationalized in the year 1972 by merging 107 companies with effect from 1st Jan 1973. GIC (General insurance company) of India and its subsidiary companies i.e. New India Assurance Company. Oriental insurance company, National Insurance Company, United India insurance company started operations in general insurance business.

With the passing of IRDA Act 1999, the insurance sector was opened up, and private insurance companies were allowed to enter life/Non insurance business with a maximum of 26% participation by a foreign partner.

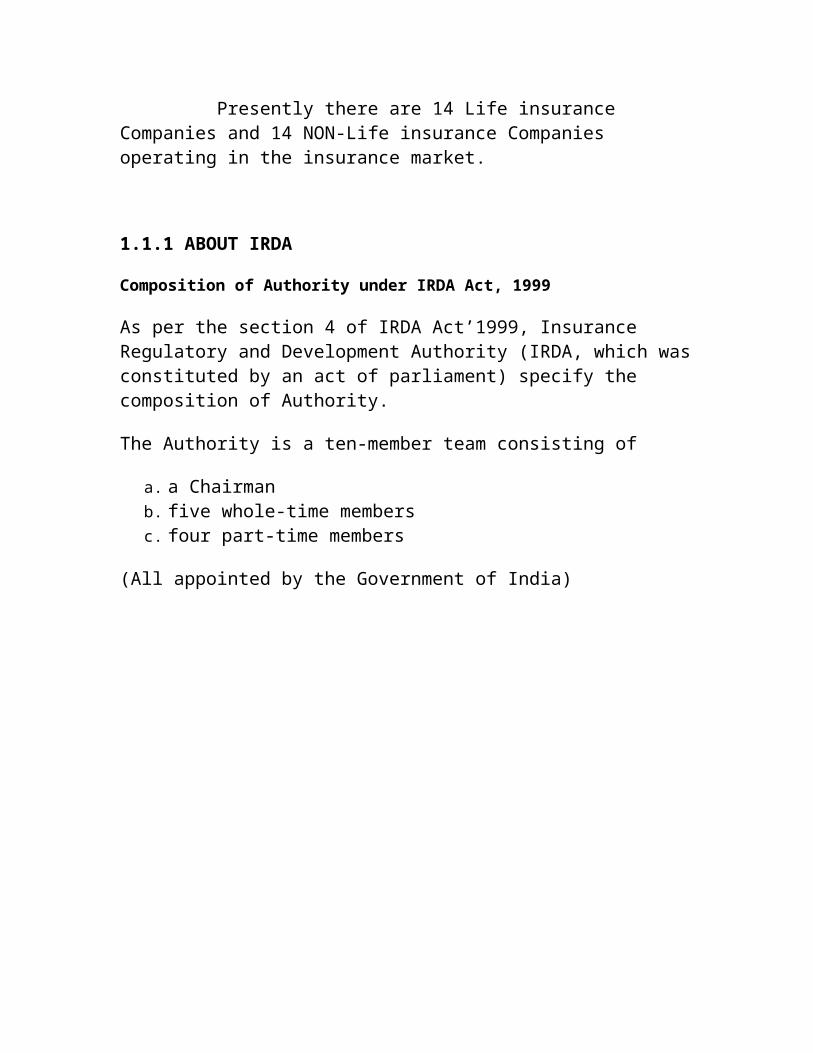

Presently there are 14 Life insurance Companies and 14 NON-Life insurance Companies operating in the insurance market.

1.1.1 ABOUT IRDA

Composition of Authority under IRDA Act, 1999

As per the section 4 of IRDA Act’1999, Insurance Regulatory and Development Authority (IRDA, which was constituted by an act of parliament) specify the composition of Authority.

The Authority is a ten-member team consisting of

a. a Chairman b. five whole-time members c. four part-time members

(All appointed by the Government of India)

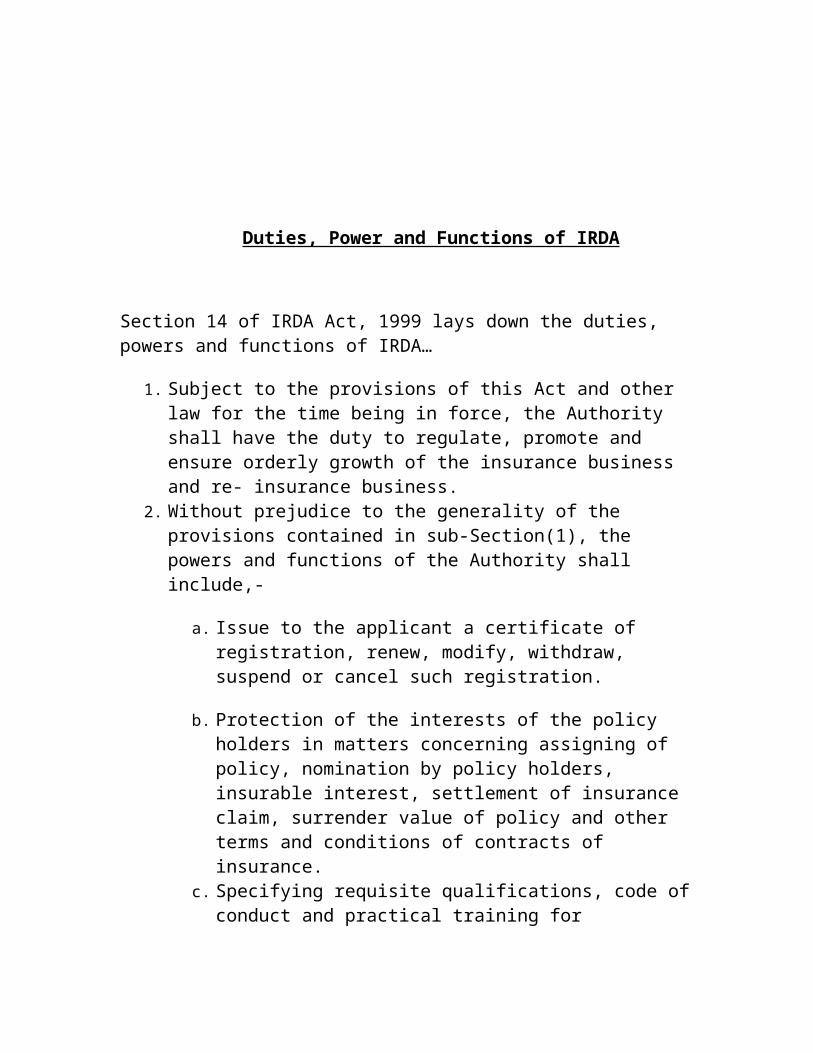

Duties, Power and Functions of IRDA

Section 14 of IRDA Act, 1999 lays down the duties, powers and functions of IRDA…

1. Subject to the provisions of this Act and other law for the time being in force, the Authority shall have the duty to regulate, promote and ensure orderly growth of the insurance business and re- insurance business.

2. Without prejudice to the generality of the provisions contained in sub-Section(1), the powers and functions of the Authority shall include,-

a. Issue to the applicant a certificate of registration, renew, modify, withdraw, suspend or cancel such registration.

b. Protection of the interests of the policy holders in matters concerning assigning of policy, nomination by policy holders, insurable interest, settlement of insurance claim, surrender value of policy and other terms and conditions of contracts of insurance.

c. Specifying requisite qualifications, code of conduct and practical training for intermediary or insurance intermediaries and agents.

d. Specifying the code of conduct for surveyors and loss assessors. e. Promoting efficiency in the conduct of insurance business.

IMPORTANT OF THE STUDY

The study is immense important to analyze the various products

of icici prudential in Chennai city

Comparative study will clearly tell the positive and negative

side of the statements.

Firstly the important of study is to find out customer preference

towards the ICICI prudential insurance in Chennai.

Secondly the study is important to give the brand awareness

about the products of icici prudential life insurance..

Thirdly the important of study is to find the investment

objective and expectation of customer towardes icici prudential

life insurance.

Last but not the least study is also important for providing good

Services to icici prudential life insurance customers

3. OBJECTIVES

3.1 PRIMARY OBJECTIVE:

To study the customer preferences and brand awareness of ICICI Prudential products in Chennai city.

3.2 SECONDARY OBJECTIVE:

a) To compare the ICICI Prudential insurance product with other insurance product.

b) To know the perception of ICICI Prudential insurance products.

c) To identify the promotional strategies of ICICI product.

History of Banking in India

Without a sound and effective banking system in India it cannot have

a healthy economy. The banking system of India should not only be hassle

free but it should be able to meet new challenges posed by the technology

and any other external and internal factors.

For the past three decades India’s banking system has several

outstanding achievements to its credit. The most striking is its extensive

reach. It is no longer confined to only metropolitans or cosmopolitans in

India. I fact; Indian banking system has reached even to the remote corners

of the country. This is one of the main reasons of India’s growth process.

The government’s regular policy for Indian Bank since 1969 has paid

rich dividends with the Nationalization of 14 major private banks of India.

Not long ago, an account holder had to wait for hours at the bank

counters for getting a draft or for withdrawing his own money. Today, he

has a choice. Gone are days when the most efficient bank transferred money

from one branch to other in two days.

Now it is simple as instant messaging or dial a pizza. Money have

become the order of the day.

The first bank in India, though conservative, was established in 1786.

from 1786 till today, the journey of Indian Banking System can be

segregated into three distinct phases. They are as mentioned below.

Early phase from 1786 to 1969 of Indian banks

Nationalization of Indian banks and up to 1991 prior to Indian

banking sector reforms

New phase of Indian banking system with the advent of Indian

financial & banking sector reforms after 1991.

To make this write-up more explanatory, I prefix the scenario as phase

I, phase II and phase III.

Phase I

The general bank of India was set up in the year 1786. Next came

bank of Hindustan and Bengal bank. The east India company established

bank of Bengal (1809), bank of Bombay (1840) and bank of madras (1843)

as independent units and called it presidency banks. These three banks were

amalgamated in 1920 and imperial bank of India was established which

started shareholders bank, mostly Europeans shareholders.

In 1865 Allahabad bank was established and first time exclusively be

Indians, Punjab national bank was set up in 1894 with headquarters at

Lahore. Between 1906 and 1913, bank of India, bank of baroda, canara

bank, Indian bank, and bank of mysore were set union bank of India came in

1935.

During the first phase the growth was very slow and banks also

experienced periodic failure 1913 and 1948. There were approximately 1100

banks, mostly small. To streamline the and activities of commercial banks.

The government of India came up with the banking act 1949 which was later

changed to banking regulation act 1949 as per amending act no 23 of 1965 ).

Reserve bank of India was vested with extensive powers for the superior

banking in India as the central banking authority.

During those days public has lesser confidence in the banks. As an

aftermath deposit mobil slow. Abreast of it the savings bank facility

provided by the postal department was comparative moreover, funds were

largely given to traders.

Phase II

Government took major steps in this Indian banking sector reform

after independence. Nationalized imperial bank of India with extensive

banking facilities on a large scale special and semi-urban areas. It formed

state bank of India to act as the principal agent of RBI an banking

transactions of the union and state governments all over the country.

Seven banks forming subsidiary of state bank of India was

nationalized in 1960 on 19th major process of nationalization was carried out.

It was the effort of the then prime minister Mrs. Indira Gandhi. 14 major

commercial banks in the country was nationalized.

Second phase of nationalization Indian banking sector reform was

carried out in 1980 more banks. This step brought 80% of the banking

segment in India under government own.

The following are the steps taken by the government of India to

regulate banking institute country.

1949: enactment of banking regulation act.

1955: nationalization of state bank India.

1959: nationalization of SBI subsidiaries.

1961: insurance cover extended to deposits.

1969: nationalization of 14 major banks.

1971: creation of credit guarantee corporation.

1975: creation of regional rural banks.

1980: nationalization of seven banks with deposits over 200 crore.

After the nationalization of banks, the branches of the public sector

bank India rose to apply 800% in deposits advances took a huge jump by

11,000%.

Banking in the sunshine of government ownership gave the public

implicit faith and confidence about the sustainability of these institutions.

Phase III

This phase has introduced many products and facilities in the banking

sector in measure. In 1991, under the chairmanship of M Narasimhan, a

committed was set up by which worked for the liberalization of baking

practices.

The country is flooded with foreign banks and their ATM stations.

Efforts are being satisfactory service to customers. Phone banking and net

banking is introduced. The end become more convenient and swift. Time is

given more importance than money.

The financial system of India has shown a great deal of resilience. It is

sheltered from triggered by any external macroeconomics shock as other

east asian countries suffered due to a flexible exchange rate regime, the

foreign reserves are high, the capital account is convertible, and banks and

their customers have limited foreign exchange exposure.

In India there are 27 Public sector banks, 31 Private banks and 29 Foreign banks. The

Indian banking sector is headed for consolidation. The presence of many regional

players will see few banks emerging as global competitors.

The following are the Scheduled Banks in India (Public Sector):

State Bank of India

State Bank of Bikaner and Jaipur

State Bank of Hyderabad

State Bank of Indore

State Bank of Mysore

State Bank of Patiala

State Bank of Saurashtra

State Bank of Travancore

Andhra Bank

Allahabad Bank

Bank of Baroda

Bank of India

Bank of Maharashtra

Canara Bank

Central Bank of India

Corporation Bank

Dena Bank

Indian Overseas Bank

Indian Bank

Oriental Bank of Commerce

Punjab National Bank

Punjab and Sind Bank

Syndicate Bank

Union Bank of India

United Bank of India

UCO Bank

Vijaya Bank

The following are the Scheduled Banks in India (Private Sector):

Vysya Bank Ltd

UTI Bank Ltd

Indusind Bank Ltd

ICICI Banking Corporation Bank Ltd

Global Trust Bank Ltd

HDFC Bank Ltd

Centurion Bank Ltd

Bank of Punjab Ltd

IDBI Bank Ltd

The following are the Scheduled Foreign Banks in India:

American Express Bank Ltd.

ANZ Gridlays Bank Plc.

Bank of America NT & SA

Bank of Tokyo Ltd.

Banquc Nationale de Paris

Barclays Bank Plc

Citi Bank N.C.

Deutsche Bank A.G.

Hongkong and Shanghai Banking Corporation

Standard Chartered Bank.

The Chase Manhattan Bank Ltd.

Dresdner Bank AG.

Reserve Bank of India (RBI)

Reserve bank of India (RBI) is the central bank of the country and is different from central bank of India.

The central bank of the country is the reserve bank of India (RBI). It

was established in April 1935 with a share capital of Rs.5crores on the basis

of the recommendations of the Hilton Young Commission. The share capital

was dividend into share of Rs.100 each fully paid which was entirely owned

by private shareholders in the beginning. The government held shares of

nominal value of Rs.2, 20,000.

Reserve bank of India was nationalized in the year 1949. the general

superintendence and direction of the bank is entrusted to central board

directors of 20 members, the governor and four deputy governors, one

government official from the ministry of finance, ten nominated directors by

the government to give representation to import elements in the economics

life of the country, and four nominated directors by the central government

of represent the four local boards with the headquaters at Mumbai, Kolkotta,

Chennai and New Delhi. Local boards consist of five members each central

government appointed for a term of four years to represent territorial and

economic interests and the interests of cooperative and indigenous banks.

The reserve bank of India act, 1934 was commenced on April 1, 1935.

The act 1934 (II of 1934) provides the statutory basis of the functioning of

the bank.

The bank was constituted for the need of following:-

To regulate the issued of banknotes

The maintain reserves with a view to securing monetary stability.

To operate the credit and currency system of the country to its

advantage.

Functions of Reserve bank of India

The Reserve bank of India act of 1934 entrust all the important

functions of a central bank the Reserve Bank of India.

Bank of issue

Under section 22 of the reserve bank of India act, the bank has sole

right to issue all denominations. The distribution of one rupee notes and

coins and small coins all over the undertaken by the reserve bank as agent of

the government. The reserve bank has issue department which is entrusted

with the issue of currency notes. The assets and liabilities issue department

are kept separate from those of the banking department. Originally, the

issue department were to consist of not less than two-fifths of gold coin,

gold bullion securities provided the amount of gold was not less than Rs.40

crores in value. The remain fifths of the assets might be held in rupees coins,

government of India rupee securities, eligible exchange and promissory

notes payable in India. Due to the exigencies of the second word the post-

was period, these provisions were considerably modified. Since 1957, the

reserve bank of India is required to maintain gold and foreign exchange

reserves of Rs.200of which Rs.115 crores should be in gold. The system as

it exists today is known as the minimum system.

Banker to government

The second important function of the reserve bank of India is to act as

government bank and advice. The reserve bank is agent of central

government and of all state government excepting that of jammu and

Kashmir. The reserve bank has the obligation to transact business, via. To

keep the cash balances as deposits free of interest, to receive and to make on

behalf of the government and to carry out their exchange remittances and

other operations. The reserve bank of India helps the government-both the

union and the state new loans and to manage public debt. The bank makes

ways and means advance governments for 90 days. It makes loans and

advances to the states and local authorities adviser to the government on all

monetary and banking matters.

Bankers’ bank and lender of the last resort

The reserve bank of India acts as the bankers’ bank. According to the

provisions of the companies act of 1949, every scheduled bank was required

to maintain with the reserve bank balance equivalent to 5% of its demand

liabilities and 2 per cent of its time liabilities in amendment of 1962, the

distinction between demand and time liabilities was abolished have been

asked to keep cash reserves equal to 3 percent of their aggregate deposit

liabilities minimum cash requirements can be changed by the reserve bank

of India.

The scheduled bank can borrow from the reserve bank of India on the

basis of eligible get financial accommodation in times of need or stringency

by rediscounting bill of exchange commercial banks can always expect the

reserve bank of India to come to their help banking crisis the reserve bank

becomes not only the banker’s bank but also the lender resort.

Controller of credit

The reserve bank of India is the controller of credit i.e. it has the

power to influence the credit created by banks in India. It can do so through

change the bank rate or through of operations. According to the banking

regulation act of 1949, the reserve bank of India come particular bank or the

whole banking system not to lend to particular groups or persons on the

certain types of securities. Since 1956, selective controls of credit are

increasingly being reserve bank.

The reserve bank of India is armed with many more powers to control

the Indian money every bank has to get a licence from the reserve bank of

India to do banking business the licence can be cancelled by the reserve

bank of certain stipulated conditions are every bank will have to get the

permission of the reserve bank before it can open a new scheduled bank

must send a weekly return to the reserve bank showing. In detail, its

liabilities. This power of the bank to call for information is also intended to

give it effective credit system. The reserve bank has also the power to

inspect the accounts of any commence.

As supreme banking authority in the country, the reserve bank of

India, therefore, has the powers:

a) It holds the cash reserves of all the scheduled banks.

b) It controls the credit operations of banks through quantitative and

qualitative controls.

c) It controls the banking system through the system of licensing,

inspection and information.

d) It acts as the lender of the last resort by providing rediscount facilities

to scheduled bank.

Custodian of Foreign Reserves

The reserve bank of India has the responsibility to maintain the

official rate of exchange. A reserve bank of India act of 1934, the bank was

required to by and sell at fixed amount of sterling in lots of not less than

Rs.10,000. The rate of exchange fixed was since 1935 the bank was able to

maintain the exchange rate fixed at lsh.6d. Though there was of extreme

pressure in favour of or against.

The rupee. After India became a member of the international monetary fund

in 1946, the bank has the responsibility of maintaining fixed exchange rates

with all other member court I.M.F

Besides maintaining the rate of exchange of the rupee, the reserve bank has

to act as the of india’s reserve of international currencies. The vast sterling

balances were acquired and by the bank. Further, the RBI has the

responsibility of administering the exchange country.

Supervisory functions

In addition to its traditional central banking function, the reserve bank

has certain not functions of the nature of supervision of banks and promotion

of sound banking in India. The bank act, 1934, and the banking regulation

act.1949 have given the RBI wide powers of the control over commercial

and cooperative bank, relating to licensing and establishment expansion,

liquidity of their assets, management and methods of working,

reconstruction, and liquidation. The RBI is authorized to carry out periodical

inspections and to call for returns and necessary information from them. The

nationalization of 14 scheduled banks in july 1969 has imposed new

responsibilities on the RBI for directing the banking and credit policies

towards more rapid development of the economy and realization desired

social objectives. The supervisory functions of the RBI have helped a great

deal in the standard of banking in India to develop on sound lines and to

improve the method operation.

Promotional functions

With economic growth assuming a new urgency since independence,

the range of the reserve functions has steadily widened. The bank now

performs a variety of developmental functions, which, at one time, were

regarded as outside the normal scope of central bank reserve bank was asked

to promote banking habit, extend banking facilities to rural and urban areas,

and establish and promote new specialized financing agencies. Accordingly,

the reserve bank has helped in the setting up of the IFCI and the SFC; it set

up the deposit insurance company in1962, the unit trust of India in 1964, the

industrial development bank of India also increase agricultural refinance

corporation of India in 1963 and the industrial reconstruction corporation

India in 1972. These institutions were set up directly or indirectly by the

reserve bank saving habit and to mobilize savings, and to provide industrial

finance as well as agricultural. As far back as 1935, the reserve bank of India

set up the agricultural credit department agricultural credit. But only since

1951the bank’s role in this field has become extreme. The bank has

developed the co-operative credit movement to encourage saving, money

lenders from the villages and to route its short term credit to agriculture. The

RBI has agricultural refinance and development corporation to provide long-

term finance to farmers.

Classification of RBIs functions

The monetary functions also known as the central banking functions

of the RBI are related and regulation of money and credit, ie, issue of

currency, control of bank credit, control exchange operations, banker to the

government and to the money market. Monetary function RBI are

signification as they control and regulate the volume of money and credit in

the country.

Equally important, however, are the non-monetary functions of the

RBI in the context economic backwardness. The supervisory function of the

RBI may be regarded as a non function (though many consider this a

monetary function). The promotion of sound banking an important goal of

the RBI, the RBI has been given wide and drastic powers, under the

regulation Act of 1949 – these powers relate to licencing of banks, branch

expansion, liquid assets, management and methods of working inspection

amalagamation reconstruct liquidation. Under the RBI’s supervision and

inspection, the working of banking has greatly commercial banks have

eveloped into financially and operationally sound and viable units powers of

supervision have now been extended to non-banking financial intemedia

independence, particularly after its nationalization 1949, the RBI has

followed the promotion vigorously and has been responsible for strong

financial support to industrial and development in the country.

1.2 COMPANY PROFILE:

ICICI Prudential Life Insurance Company is a joint venture between ICICI Bank, a premier financial powerhouse and prudential plc, a leading

international financial services group headquartered in the United Kingdom. ICICI Prudential was amongst the first private sector insurance companies to being operations in December 2000 after receiving approval from Insurance Regulatory Development Authority (IRDA).

ICICI Prudential’s equity base stands at Rs.11.85 billion with ICICI Bank and Prudential plc holding 74% and 26% stake respectively. In the financial year ended March 31,2005, the company garnered Rs.1584crore of new business premium for a total sum assured of Rs.13, 780 crore and wrote nearly 615,000 policies. The company has a network of about 56,000 advisors; as well as 7-bank assurance and 150 corporate agent tie-ups. For the past four years, ICICI Prudential has retained its position as the No.1 private life insurer in he country, with a wide range of flexible products that meet the needs of the Indian customer at every step in life.

1.2.1HISTORY:

ICICI Prudential Life Company Limited is a 74:26 joint venture between ICICI Bank and Prudential plc, UK. The company brings together the local market expertise and financial strength of ICICI Bank and Prudential’s international life insurance experience. The company was granted a Certificate of Registration by the IRDA on November 24, 2000 and eighteen days later. Issued its first policy on December 12.

From its early days, ICICI Prudential seemed to have the wherewithal for a large-scale business. By March 31, 2002, a little over a year since its launch, the company had issued 100,00 policies translating into a premium income of approximately Rs.1, 200 million on a sum assured of over Rs.23 billion.

When the company began its operations, the need was to build a brand that was relatable to, symbolized trust and was easily recognized and understood. It launched a corporate campaign using the theme of ‘Sin door’ to epitomize protection, trust, togetherness and all that is Indian; endearing itself to the masses. The success of the campaign, ‘the calling card of the company’, saw the brand awareness scores almost at par with its 40-year-old competitor. The theme of protection was also extended to subsequent product and category specific campaigns – from child plans to retirement solutions – which highlight how the company will be with its customers at every step of life.

From day one, the company has unflinchingly focused on being a mass-market player, developing products, creating a distribution network and deploying resources that would further its goal. Apart from ramping up and thoroughly training its advisors, the company has twelve ‘Banc assurance’ partners – the largest in the country. It swiftly revised and added to its initial range of products, pioneering market-linked products and pension plans, to offer customer the most flexible life insurance policies in the country.

In February 2004, ICICI prudential increased its capital base by Rs.500 million, its ninth capital hike, bringing the total paid-up equity capital to Rs.6, 750 million. With the authorized capital of the company standing at Rs.12 billion, ICICI prudential continues to have the highest capital base amongst all life insurance in the country. The challenge ICICI prudential now faces is to retain its top-notch position and continue to deliver the finest life insurance and pension solution to its ever-growing customer base.

2. DISTRIBUTION:

ICICI prudential has one of the largest distribution networks amongst private life insurers in India, having commenced operations in 110 cities and towns in India, stretching from Bhuj in the west to Guwahati in the east, and Amristsar in the north to Trivandrum in the south.

The company has seven banc assurance tie-ups, having agreements with ICICI Bank, Federal Bank, South Indian Bank, Bank of India, Lord Krishna Bank and some co-operative banks, as well as about 290 corporate agents and brokers. It has also tied up with NGOs, MFIs and corporates for the distribution of rural policies and organizations like Dhan for distribution of Salaam Zindagi, a policy for the socially and economically underprivileged sections of society.

ICICI prudential has recruited and trained about 60,000 insurance advisors to interface with and advise customers. Further, it leverages its state-of-the-art IT infrastructure to provide superior quality of service to customers.

3. ABOUT THE PROMOTERS:

ICICI BANK:

ICICI Bank (NYSE:IBN) is India’s second largest bank and largest private sector bank with over 50 years of financial experience and with assets of Rs. 1812.27 billion as on 30th June, 2005.ICICI Bank offers a wide range of banking products and financial services to corporate and retail customers through a variety of delivery channels and through its specialized subsidiaries and affiliates in the areas of investment banking, life and non-life insurance, venture capital and asset management. ICICI Bank is a leading player in the retail banking market and has over 13 million retail customer accounts. The Bank has a network of over 570 branches and extension counters, and 2,000 ATMs.

Overview

ICICI Bank is India's second-largest bank with total assets of about

Rs.1,67,659 crore at March 31, 2005 and profit after tax of Rs. 2,005 crore

for the year ended March 31, 2005 (Rs.1,637 crore in fiscal 2004). ICICI

Bank has a network of about 560 branches and extension counters and over

1,900 ATMs.

ICICI Bank offers a wide range of banking products and financial

services to corporate and retail customers through a variety of delivery

channels and through its specialised subsidiaries and affiliates in the areas of

investment banking, life and non-life insurance, venture capital and asset

management. ICICI Bank set up its international banking group in fiscal

2002 to cater to the cross border needs of clients and leverage on its

domestic banking strengths to offer products internationally. ICICI Bank

currently has subsidiaries in the United Kingdom, Canada and Russia,

branches in Singapore and Bahrain and representative offices in the United

States, China, United Arab Emirates, Bangladesh and South Africa.

ICICI Bank's equity shares are listed in India on the Stock Exchange,

Mumbai and the National Stock Exchange of India Limited and its American

Depositary Receipts (ADRs) are listed on the New York Stock Exchange

(NYSE).

ICICI Bank was originally promoted in 1994 by ICICI Limited, an

Indian financial institution, and was its wholly-owned subsidiary. ICICI's

shareholding in ICICI Bank was reduced to 46% through a public offering of

shares in India in fiscal 1998, an equity offering in the form of ADRs listed

on the NYSE in fiscal 2000, ICICI Bank's acquisition of Bank of Madura

Limited in an all-stock amalgamation in fiscal 2001, and secondary market

sales by ICICI to institutional investors in fiscal 2001 and fiscal 2002.

ICICI was formed in 1955 at the initiative of the World Bank, the

Government of India and representatives of Indian industry. The principal

objective was to create a development financial institution for providing

medium-term and long-term project financing to Indian businesses. In the

1990s, ICICI transformed its business from a development financial

institution offering only project finance to a diversified financial services

group offering a wide variety of products and services, both directly and

through a number of subsidiaries and affiliates like ICICI Bank. In 1999,

ICICI become the first Indian company and the first bank or financial

institution from non-Japan Asia to be listed on the NYSE.

After consideration of various corporate structuring alternatives in the

context of the emerging competitive scenario in the Indian banking industry,

and the move towards universal banking, the managements of ICICI and

ICICI Bank formed the view that the merger of ICICI with ICICI Bank

would be the optimal strategic alternative for both entities, and would create

the optimal legal structure for the ICICI group's universal banking strategy.

The merger would enhance value for ICICI shareholders through the

merged entity's access to low-cost deposits, greater opportunities for earning

fee-based income and the ability to participate in the payments system and

provide transaction-banking services. The merger would enhance value for

ICICI Bank shareholders through a large capital base and scale of

operations, seamless access to ICICI's strong corporate relationships built up

over five decades, entry into new business segments, higher market share in

various business segments, particularly fee-based services, and access to the

vast talent pool of ICICI and its subsidiaries.

In October 2001, the Boards of Directors of ICICI and ICICI Bank

approved the merger of ICICI and two of its wholly-owned retail finance

subsidiaries, ICICI Personal Financial Services Limited and ICICI Capital

Services Limited, with ICICI Bank. The merger was approved by

shareholders of ICICI and ICICI Bank in January 2002, by the High Court of

Gujarat at Ahmedabad in March 2002, and by the High Court of Judicature

at Mumbai and the Reserve Bank of India in April 2002. Consequent to the

merger, the ICICI group's financing and banking operations, both wholesale

and retail, have been integrated in a single entity.

History of ICICI

1955 : The Industrial Credit and Investment Corporation of India Limited

(ICICI) incorporated at the initiative of the World Bank, the

Government of India and representatives of Indian industry, with the

objective of creating a development financial institution for

providing medium-term and long-term project financing to Indian

businesses. Mr.A.Ramaswami Mudaliar elected as the first Chairman

of ICICI Limited

1955: ICICI emerges as the major source of foreign currency loans to

Indian industry. Besides funding from the World Bank and other

multi-lateral agencies, ICICI also among the first Indian companies

to raise funds from International markets.

1956 : ICICI declared its first Dividend at 3.5%.

1958 : Mr.G.L.Mehta was appointed the 2nd Chairman of ICICI Ltd.

1960 : ICICI building at 163, Backbay Reclamation was inaugurated.

1961 : The first West German loan of DM 5 million from Kredianstalt was

obtained by ICICI.

1967 : ICICI made its first debenture issue for Rs.6 crore, which was

oversubscribed.

1969 : First two regional offices in Calcutta and Madras were opened.

1972 : Second entity in India to set-up merchant banking services.

1972: Mr. H. T. Parekh appointed as the third Chairman of ICICI.

1977 : ICICI sponsors the formation of Housing Development Finance

Corporation. Managed its first equity public issue

1978 : Mr. James Raj appointed as the fourth Chairman of ICICI.

1979 : Mr.Siddharth Mehta appointed as the fifth Chairman of ICICI.

1982 : Becomes the first ever Indian borrower to raise European Currency

Units.

1982: ICICI commences leasing business.

1984 : Mr. S. Nadkarni appointed as the sixth Chairman of ICICI.

1985 : Mr.N.Vaghul appointed as the seventh Chairman and Managing

Director of ICICI.

1986 : ICICI first Indian Institution to receive ADB Loans. First public

issue by an Indian entity in the Swiss Capital Markets.

1986:

ICICI along with UTI sets up Credit Rating Information Services of

India Limited, (CRISIL) India's first professional credit rating

agency.

1986: ICICI promotes Shipping Credit and Investment Company of India

Limited. (SCICI)

1986: The Corporation made a public issue of Swiss Franc 75 million in

Switzerland, the first public issue by any Indian equity in the Swiss

Capital Market.

1987 : ICICI signed a loan agreement for Sterling Pound 10 million with

Commonwealth Development Corporation (CDC), the first loan by

CDC for financing projects in India.

1988 : ICICI promotes TDICI - India's first venture capital company.

1993 : ICICI sets-up ICICI Securities and Finance Company Limited in

joint venture with J. P. Morgan.

1993: ICICI sets up ICICI Asset Management Company.

1994 : ICICI sets up ICICI Bank.

1996 : ICICI becomes the first company in the Indian financial sector to

raise GDR.

1993: ICICI announces merger with SCICI.

1993: Mr.K.V.Kamath appointed the Managing Director and CEO of

ICICI Ltd

1997 : ICICI was the first intermediary to move away from single prime

rate to three-tier prime rates structure and introduced yield-curve

based pricing.

1997: The name "The Industrial Credit and Investment Corporation of

India Limited " was changed to "ICICI Limited".

1997: ICICI announces takeover of ITC Classic Finance.

1998 : Introduced the new logo symbolizing a common corporate identity

for the ICICI Group.

1998: ICICI announces takeover of Anagram Finance.

1999 : ICICI launches retail finance - car loans, house loans and loans for

consumer durables.

1999: ICICI becomes the first Indian Company to list on the NYSE

through an issue of American Depositary Shares.

2000 : ICICI Bank becomes the first commercial bank from India to list its

stock on NYSE.

2000: ICICI Bank announces merger with Bank of Madura.

2001 : The Boards of ICICI Ltd and ICICI Bank approved the merger of

ICICI with ICICI Bank.

2002 : Moodys' assign higher than sovereign rating to ICICI.

2002: Merger of ICICI Limited, ICICI Capital Services Ltd and ICICI

Personal Financial Services Limited with ICICI Bank.

Prudential:

Established in London in 1848, Prudential plc, through its business in UK and Europe, US and Asia, provides retail financial services products and services to more than 16 million customers, policyholder and unit holders worldwide. As of June 30, 2004, the company had over US$300 billion in funds under management.

Prudential has brought to market an integrated range of financial services products that now includes life assurance, pensions, mutual funds, banking, investment management and general insurance. In Asia, prudential is the leading European life insurance company with a vast network of 24 life and mutual fund operations in twelve countries – China, Hong Kong, India, Indonesia, Japan, Korea, Malaysia, Philippines, Singapore, Taiwan, Thailand and Vietnam.

1.2.4 MANAGEMENT:

Board of Directors:

The ICICI prudential Life Insurance Company Limited Board comprises reputed people from the finance industry both India and abroad…

Mr. K.V. Kamath, Chairman

Mr. Mark Norbom

Mrs. Lathika D.Gupte

Mrs.Kalpana Morparia

Mrs.Chanda Kochhar

Mr.Kevin Holmgren

Mr.M.P.Modi

Mr. Narayanan

Ms.Shikha Sharma, Managing Director

Mr.N.S.Kannan, Executive Director

Management Team:

Ms.Shikha Sharma, Managing Director & CEO

Mr.N.S.Kannan, Executive Director

Mr.V.Rajagopalan, Chief – Actuary

Mr.Sandeep Batra, Chif Financial Officer & Company Secretary

Ms.Anita Pai, Chif – Customer Service and Operations

Mr.Puneet Nanda, Chif – Investments

Mr.Dipan Bhattacharya – Chif Information Technology

1.3PRODUCT PROFILE

ICICI prudential Life Insurance offers a range of innovative, customer-centric products that meet the needs of customer at every life stage. Its products can be enhanced with up to 5 riders, to create a customized solution for each policyholder.

1.2.3SAVINGS SOLUTIONS:

Secure Plus is a transparent and feature-packed savings plan that offer 3 levels of protection.

Cash Plus is a Transparent, feature-packed savings plan that offers 3 levels of protection as well as liquidity options.

Save “n” Protect is a traditional endowment savings plan that offers life protection along with adequate returns.

Cash Bank is an anticipated endowment policy ideal for meeting milestone expenses like a child’s marriage, expenses for a child’s higher education or purchase of an asset.

Lifetime & Lifetime II offer customer the flexibility and control top customize the policy to meeting the changing needs at different life stages. Each offer 4 fund options? Preserver, Protector, Balancer and Maxi miser.

Life link II is a single premium Market Linked Insurance Plan which combines life insurance cover with the opportunity to stay invested in the stock market.

Premier Life is a limited premium – paying plan that offers customers life insurance cover till the age of 75.

Invest Shield Life is a Market Linked plan that provides capital guarantee on the invested premiums and declared bonus interest.

Invest Shield Cash is a Market Linked plan that provides capital guarantee on the invested premiums and declared bonus interest along with flexible liquidity options.

Invest shield Gold is a Market Linked plan that provides capital guarantee on the invested premiums and declared bonus interest along with limited premium payment terms.

Protection Solutions

Life Guard is a protection plan, which offers life covers at very low cost.

It is available in 3 options – level term assurance, level term assurance with return of premium and single premium.

Child Plans

Smart Kid education plans guaranteed educational benefits to a child

along with life insurance cover for the parent who purchases the policy. The policy is designed to provide money at important milestones in the child’s life. Smart Kid plans are also available in unit-linked form-both single premium and regular premium.

Retirement Solutions

Forever life is a retirement product targeted at individuals in their

thirties. SecurePlus Pension is a flexible pension plan that allows one to select

between 3 levels of cover.

1.3.2 MARKET-LINKED RETIREMENT PRODUCTS

Life Time Pension II is a regular premium market-linked pension plan. Life Link Pension II is a single premium market-linked pension plan. Invest Shield Pension is a regular premium pension plan with a capital

guarantee on the ingestible premium and declared bonuses. Golden Years is a limited premium paying retirement solution that

offers tax benefits up to Rs.100, 000 u/s 80 c, with flexibility in both the accumulation and payout stages.

ICICI Prudential also launched “salaam Zindagi”, a social sector group insurance policy targeted at the economically underprivileged sections of the society.

1.3.3 GROUP INSURANCE SOLUTIONS:

ICICI Prudential also offers Group Insurance Solutions for companies seeking to enhance benefits to their employees.

ICICI Prudential Group Gratuity Plan:

ICICI Prudential group gratuity plan helps employers fund their statutory gratuity obligation in a scientific manner. The plan can also be customized to structure schemes that can provide benefits beyond the statutory obligations.

ICICI Prudential Group Superannuation Plan:

ICICI prudential offers a flexible defined contribution superannuation scheme to provide a retirement kitty for each member of the group.

Employees have the option of choosing from various annuity options or opting for a partial commutation of the annuity at the time of retirement.

ICICI Prudential Group Term Plan:

ICICI Prudential flexible group term solution helps provides affordable cover to members of a group. The cover could be uniform or based on designation/rank or a multiple of salary. The benefit under the policy is paid to the beneficiary nominated by the member on his/her death. Flexible Rider Options

ICICI Prudential Life offers flexible riders, which can be added to the basic policy at a marginal cost, depending on the specific needs of the customer.

o Accident & disability benefit: If death occurs as the result of an accident during the tern of the policy, the beneficiary receives an additional amount equal to the sum assured under the policy. If the death occurs while traveling in an authorized mass transport vehicle, the beneficiary will be entitled to twice the sum assured as additional benefit.

o Accident Benefit: This rider option pays the sum assured under

the rider on death due to accident.

1.4 ABOUT THE PROJECT

The aim of the project is the customer preferences and brand awareness of ICICI Prudential Life insurance in Chennai city.

The project mainly deals with the comparative study of the preference to ICICI Prudential products with the other insurance.

1.5 TITLE OF THE STUDY

Customer Preference:

This truth is no different from raising a small child. Once a child understands (perceives) that negative actions swiftly results in negative consequences, the child will change his or her behavior. And once a child understands (perceives) that positive actions will earn positive rewards he will want to continue to behave appropriately in order to be rewarded. The same concept applies to customer’s preference.

“It is not who you are, its who people think you are”

Your company’s success can be measured in only one way, the perceived value to your customer. Everything else is secondary.

It provides you with a way to accurately measure how customers which of your company, products & services.

1.6 STATEMENT OF PROBLEM

ICICI Prudential is the no.1 company among the private players. ICICI prudential apart from other companies have come out with the latest version of market link products available in international plans.

These plans have become very popular because of the transparency and the flexibility it offers to the client.

1.7 NEED FOR THE STUDY

Every organization has its own vision. To achieve that various policies, rules and regulations have been constructed by the company management to improve the productivity and performance among the customers that will affect the organizational goals.

So this survey on analysis of facts influencing performance and response of customers were come out with an intention to find out the ICICI Prudential products.

INDUSTRY PROFILE

ABOUT US: SPA Group was promoted by a team of finance professionals in 1995 with an objective to provide value added financial services. Initially, the Group focused as a niche financial solutions provider in corporate finance and wealth management to Indian companies and high net worth individuals. In January 2000, the Group expanded its operations and the range of services. Today, SPA provides services for securities broking, merchant banking, wealth management, financial advisory, corporate finance , risk management and insurance broking.

SPA is being managed by its promoters along with a young and dynamic team of over 200 professionals with rich experience, in their respective fields. The Group has established itself as one of India’s leading financial advisory house, offering various financial solutions to its Institutional, corporate and individual clients.

Customer centric approach of Spa’s dedicated professional team has helped carve a niche for itself in financial services arena and won confidence of its clients. Clients of SPA are from a wide spectrum and comprise of Banks and other financial institutions, Mutual funds, Insurance companies, foreign institutional investors, public sector undertakings and government departments, private corporates, trusts and individuals

BUSINESS AREA:

I.MERCHANT BANKING

SPA Merchant Bankers Limited is engaged in private placement of debt instruments, structuring of the various financial products as per the requirements of the borrowers along with various other pre-issue and post issue services.

The Company has made notable and considerable progress in a short span in the debt-oriented merchant banking activities by successful placement of various debt primary issues. This is also reflected through the ranking by Prime Database, which has ranked the Group amongst the top 10 service providers in this segment. The Company was able to achieve above ranks on the basis of its performance in just two financial years since it commenced investment & merchant banking activities.

Since the commencement of merchant banking services, the Company has syndicated funds for various Public Sector Undertakings (PSUs), Designated Financial Institutions (DFIs), Banks and several State Level Undertakings (SLUs).

The Company for its Merchant & Investment Banking activities has found patronage as an Arranger with various central public sector undertakings like HUDCO, NTC, ITI, MECON, IISCO SAIL, REC, KRCL, public sector banks and financial institutions. Also the Company has had privilege to provide its services to various state level undertakings of Andhra Pradesh, Karnataka, Kerela, TamilNadu, West Bengal, Punjab, Haryana, Himachal Pradesh, Jammu & Kashmir, Maharashtra, Gujarat and Rajasthan. In the private sector, the Company has provided its services to various domestic and MNC corporates.

The achievements corroborate our untiring and sincere efforts towards building and preserving mutually rewarding and sustainable relationships with our clients and giving them our value added services with meaningful performance.

Now, the Company has started providing Equity Oriented Merchant Banking services to its customers on strength of its research based structuring capabilities and strong distribution network. Presently, the Company is providing services for private placement of equities, public issues and right issues.

II. PROJECT FINANCING:

Driving strengths from its institutional relationships and the position in this segment, SPA Merchant Bankers Limited has been acting as arranger for syndication of loans for various corporate in the public and private sectors. Successful execution of mandates for arranging corporate finance has helped the Company to earn confidence from its clients and generated further referrals. The Company has the pleasure to be associated with some of the leading corporate of Indian business world and has executed mandates for syndication of rupee term loans aggregating Rs. 5000 cores, including Narmada Hydroelectric Development Corporation Limited, ITI Ltd., Andhra Pradesh Water Resources Development. Corporation, Punjab State Electricity Board and various corporate houses in the private sector.

III.INVESTMENT BANKING AND DEBT ADVISORY:

SPA Merchant Bankers Limited has proved its strengths in the field of Investment Banking services including merger and amalgamation related advisory services, structured financing through various mechanisms and financial restructuring.

In short span the Company has been able to execute debt advisory related mandates for more than Rs. 2500 Crs for esteemed clientele like NTC, ITI, HUDCO, CUPGL, TNEB, CMWSSB, RSRDC.

IV.SECURITESBROKING:

SPA Securities Ltd. is registered member of NSE-WDM segment, Capital Market segment and Futures and Options segment. The company is also a member of The Stock Exchange, Mumbai. SPA Comrades Pvt. Ltd. is the commodities broking company of the group and is a member of NCDEX and MCX. The Company has dedicated teams operating from a state of the art dealing room in Mumbai for equity, debt and derivatives broking supported by a strong in-house research team. Debt Broking: The division is engaged in providing debt advisory and broking services to institutional, semi-institutional and retail customers. The

company caters to a wide range of investors across the country ranging from Provident Funds, Banks, Corporate Treasuries, Financial Institutions, Mutual Funds, Educational, Religious and Charitable Trusts, Insurance Companies, HNI's etc. The company deals in Government Securities, Treasury Bills, Commercial Papers, Certificate of Deposits, PSU, SLU and Corporate Bonds and other debt instruments. With its nationwide network providing institutional broking services the company has executed business of over Rs. 300 Billion in last 3 years.

V.MUTUAL FUND:

The SPA Group, on strength of its research based customer centric approach and impeccable servicing, is recognized as one of the leading financial advisory service providers in the country.

SPA Capital Services Ltd., the flagship company of the group provides investment advisory services. The company is engaged in advisory and distribution services of mutual funds and is ranked amongst top 10 intermediaries in the country. The Company provides customized solutions to the requirements of High Net worth Individuals and Corporate clients. Our strength lies in our ability to advice on investment strategies and structures develop innovative products and distribute amongst a wide network of investors across the country. We have constantly endeavored to develop new instruments, tailor made to the requirements of our clients, enabling them to earn efficient post tax returns in accordance with their specific risk, return and maturity profiles. The company also has a distribution network of 200 sub-brokers across India being serviced by its eight branches.

The company has mobilized more than Rs.7 trillion for various Mutual Funds during the last 7 years and is currently having Asset under Management of over Rs.50 billion with satisfied customers.

Additionally, the company provides advisory services for alternate investment options like portfolio management services in equity, debt and commodities besides investment in venture capital funds.

VI. INSURANCE:

SPA Insurance Broking Services Ltd is the insurance broking company of the group providing life and general insurance advisory services.

Life Insurance advisory services are process oriented, which include identification of the needs of the clients, offering the best product available, resolution of their queries and post sales service. The company has covered over 2000 lives in 18 months of business with sum assured of over Rs. 20 billion and premium collection of over Rs.3.5 billion.

In General Insurance we believe in servicing clients after assessment of their need and the risk involved and cover

required and offer the best insurance cover available in the market supported by strong after sales services to the clients. The Company is empanelled with all the general insurance companies operating in the Country enabling it to provide best insurance solutions suitable for the clients. The company has provided insurance coverage across assets classes of over Rs. 200 billion with impeccable claims and other after sales services.

RESEARCH:

Research, undertaken on a continuing basis, forms foundation for all services provided by us. At SPA we have focused on building a strong research team which functions with an exhaustive approach to understand and analyze underlying market dynamics for equities, fixed income, and mutual funds.

To provide customized solutions our operation and sales team shares customer expectations and requirements with the research team which supports them with various relevant solutions.

VISION & VALUES

SPA believes in attaining customer satisfaction, on continuing basis, by providing highest standard of financial services in India. The philosophy at SPA is to provide services to clients after assessment of their profile, needs and risk-appetite. The basic work theme at SPA is:

- Dedicated, competent and honest team of professionals- Customer centric work environment- Insight of customers’ perspectives- Strong research base- Clear understanding of applicable laws - Consistency and passion to excel- Technology savvy

REVIEW OF LITERATURE

2.1 CUSTOMER PREFERENCES

Conceptually, a customer preference is a simply notion. It is the relation between the output of an organization and the value the customer attaches to it. We can quantify customer preferences through market survey methods, either through the retail outlet surveys or the final customer surveys s has been done in this report. The companies can increase the customer preference based on the suggestions and recommendations received directly from the customers themselves. The most important this that has to be borne in mind is to see how true to their self the customers are while giving their opinions. This can be serious drawback to any opinion poll. Care should be taken to select customers from all quarters of the society. The sample has to considerable big so as to represent the society in true terms.

Though customer preferences appear simple, misconceptions about it are many. Some of them are as under:

Customer wants a product that is cheap and is of acceptable quality and shelf life. He doesn’t care if it aesthetically well designed or packed or has excellent quality over others.

It is considered that customer a preference is fast too dynamic a property based on which marketing strategies cannot base on. In fact, it is quite an important factor which decides whether a brand survives in the market or not.

Apart from this, many practical complexities exist. The cost per unit of the product/service depends on the cost price at which the inputs are procured and the effectiveness with which those inputs are put to use produces the outputs. Therefore wastage elimination and improved productivity also indirectly impact the customer preferences levels.

Assuming that all companies get the input at the same price, the inescapable conclusion is that the company that is most productive will have the lowest cost product. The concept of productivity becomes all the more important for those organizations that face severe competition from high tech organizations.

This suggests productivity is the only weapon which companies have to tackle price rise in inputs without increasing the sale price of the products. It has been seen in the last year that prices of some products had to be reduced by as much as 30%. In such situations, productivity improvement is the only way by which brands can stay in the market and still be profitable.

2.2 AIM, SCOPE AND POTENTIALITY OF THE CONCEPT OF CUSTOMER PREFERENCES

Customer preferences aim at thoroughly cleaning up the production/service facilities of an organization by undermining its basic functions. All wasteful areas can be identified and redundant activities that do not add value to the products/services could be limited or curtailed. The organization can give the customers what he wants through an objective survey.

The scope for customer preferences is enormous considering the why the market is moving. The FMCG market is flooded with brands and the

people are not ignorant of the various new entrants. Gone are the days when a family goes in for a particular brand for generations. The concept

Of huge family is gone and it is the time of smaller, separate families. Every person is having his or her own preferences heard. So, it has become incumbent on the brands to suit every person’s tastes, like and dislikes. As the saying goes, ‘A satisfied customer is the best advertisement’.

The more effective and efficient production process employed the more the production and profitability. And hence, the government gains by more importantly, the shareholders get more profits and dividends being the owners of the company. Employees also gain higher production related incentives. In all, through productivity improvement everybody related to the organization gains. And so do the customers. The customers also get to have products that are very high in quality and longer shelf life. Extravagancies creep up into the organizational set up helps us to locate and eliminate the extravagant expenses in the company. Reduction of such extravagancies allows the organization to the customers. In a global market there are no preferences for supplies.

In the words of Mr. Lee Young, the former Editor-in-chief of business world, customer preferences is the most ignored area in business today. He says, probably the most important management fundamental that is being ignored today is staying close to the customer to satisfy his needs and anticipate his wants. In too many companies, the customer has become a bloody nuisance whose unpredictable behavior damages carefully made strategies plans, whose activities mess up computer operations and who stubbornly insists that purchased product should work.

That a business ought to be close to its customers seems to be benign message. So the question arises, why does a topic like this need to be discussed at all? The answer is that, despite all the lip service given to market orientation these days., Lee Young and other management stalwarts are right. The customer is either ignored or considered a bloody nuisance.

All business success rests on something labeled for sale, which at least momentarily weds company to the customer. A research conducted in the US by two management gurus uncovered on the customer attribute is this: the excellent companied ‘really’ are close to their customers. Tht is it. Other companies talk about it. Excellent companies do it.

In excellent companies and specifically the way they interact with their customers, the most striking feature was the consistent presence of an obsession. Being customer oriented doesn’t mean that excellent companies are slouches when it comes to technological or cost performance. But they do seem to be more driven by their direct orientation to their customers rather than by technology or by a desire to be the low cost producer. IBM has not been a leader in technology for decades. Its dominance resets on its commitment to service.

Service, quality, reliability are strategies aimed at loyalty and long term revenue stream growth and importantly, maintenance. It seems that winners focus specially on the revenue generation side. The one follows the other.

As suggested by Peters and Waterman, customer orientation depends on three fundamental issues and they have shown how excellent companies do it. Now the question arises, how that is going to affect the preferences level of the company’s customers. The answer to this is, we can learn from the companies that have faced the same problem some decades ago and have come out tops. We need not learn the hard way. We have a way and we only need to find it.

A satisfied customer is the best advertisement of a company’s product. The customers not only provide the company with revenues, but they are also vital source of suggestions and product performance evaluation. This is the role of the customer as the mentor of an organization should be given due importance.

2.3 SERVICE OBESSION:

Keep communications flowing? This concept is one, which is most ignored under Indian circumstances. Believe that a real sale begins after sales and not before. The companies have to be really caring for the customers. Feel for the customer when it hurts him. IBM has adopted this concept of service during the 60sand it learned

this through a man who used to sell cars. If a computer giant can learn from a car salesman, then a pickle manufacturer can learn from a shopkeeper.

Dinah Nemeroff of Citibank, N.A.while talking about service obsession says that the principal themes are:

Intensive, active involvement on the part of senior management Remarkable people orientation High intensity measurement and feedback.

She calls it service statesmanship. With service as their top goal ‘profitability naturally follows’.

Late Mr. David Ogilvy, founder of the O and M reminds us that in best institutions, promises are kept no matter what the cost in agony and over time.

2.4 QUALITY OBSESSION:

Companies that had been excelling during the 60s have had a strong obsession about giving the customers products of very high quality. It is pleasing to give some of the examples about companies and let them explain the concept of quality obsession. Quality products are a result of quality systems and quality processes. Quality is never an accident. One never stumbles upon a quality product.

A serious and systematic effort is needed to produce a quality product. In order to maintain market share in a competitive world, quality of the product as well as processes should be given prime importance. A quality product helps the organization in increasing its market share and winning the trust of the customers. High quality of process results in few rejections and improves the productivity of the organization as a whole. Also quality ensures reduction in wastage of materials, labor, time, etc.

The Boy Scout law says that the main principles are excellence in quality, reliability of performance and loyalty in dealer relationships.

Based on these guiding principles, many excellent companies have scaled the peaks of customer preferences.

2.5 OBJECTIVE PLANNING AND CONTROL:

It is planning on what to produce, when to produce and how best to produce the products required by the customer.

Delivery on time; every time. Flexibility in manufacturing process to suit the quality needs. Develop and issue c0-ordinated schedules and order to production

department. Keep prices under control. Adopt a good marketing strategy to meet the market demands.

2.6 KEYS TO HIGH CUSTOMER PREFERENCES:

Basic factor common to high customer preferences totally complete the factors common to high creativity and the quality service provided to the customers. It should be emphasized that to ensure high organization productivity, creativity and quality should permeate every discipline and every job with in the organization.

1. Skilled responsible management:

The critical tie between the organization’s management and customer preferences is evident in the definition of customers preferences it self. Basically, customer preferences is the preferences the customer derives by using the company’s product in the comparison with which its competitors’ products; that is the efficiency and effectiveness with which available resource-men, machine, material, capital, facilities, energy and time are utilized to achieve a valuable output. As can be seen, it is a very relative measure. It is dynamic too. So, the organization should be constantly evaluating customer’s preferences as apart of its

Routine assessment process to upgrade its performance and market knowledge.

Virtually any one could manage if resource were unlimited. How ever, as we are all aware, this is seldom, if ever, the case and therefore the challenge of creative management is to get the job done optimally if the available resources. And in the times to come, management are going to get fewer resource rather then abundant resources, thus creating an even grater challenge.

Inherently, all markets are bipolar; that is, they can be fully engaged and productively of management is and always has been the development or stewardship of availed resources, thus making management the key link in the entire customer preferences chain.

The markets these days are far more demanding requiring grater professionalism in management. Tomorrow’s manager, in addition to being technically qualified in his field, must be a respected, people oriented leader, skilled in the latest techniques of behavioral sciences and sound business practices.

2. Outstanding market leadership:

Of all factors, market leadership has, by far, the greater leverage on the customer’s minds. Ultimately, the destiny of any organization hinges on the quality of its leadership. True leaders bring the best in organizations and the Markey share.

This is largely because leaders elicit strong positive emotional reactions, and people tend to fulfill their needs and grow under their effective leadership. Such leaders have an uncanny Knack for cutting through complexity, providing practical solutions to difficult problems successfully communicating these solutions to others and insisting enthusiasm and a ‘can do’ attitude.

Mr. Dravid Gergen, while talking about leadership qualities said, “a leader’s role is to raise people’s aspiration for what they can become and to realize their energies so they will try to get there”.

It is important therefore, that the management be catalytic in enhancing the leadership potential already presents in the market by selecting for advancement in key improvement areas which offers promise for future potential.

3. Higher variety:

Variety goes against Cost Reduction. But the market is poised in such a way that each individual has a sphere of wants and needs. To meet this need, organizations have to go in for variety based on intelligent market segmentation and discrimination.

This is particularly needs creativity and innovative process manipulation. The optimal combination of quality and variety creates a resonance with in a person. On the other hand if one’s product does not provide fulfillment, a person will frequently divert his or her attention and shift to other brands and other pursuits.

Special attention should be given to newer markets since it introduces the company to newer people and paths of communication that can significantly influence long term effectiveness and ultimate position of the company and the band.

RESEARCH METHODOLOGY

INTODUCTION:

According to the oxford advanced Learners Dictionary of current English the meaning of research is a “careful Study or investigation especially in order to discover new facts or information”.

Research is defined as movement from the known to the unknown. It is an effort to discover something. According to Clifford Woody, Research comprise defining and redefining problems formulating hypothesis or suggested solutions, collecting/organizing and evaluating data making deduction and research conclusions and at last carefully testing the conclusion to determine whether they fit the formulation hypothesis.

4.1 Research design:

Research design is a plan of action that guides the entire research. There are four types of research design available. They are

1. Exploratory Research Design 2. Descriptive Research Design 3. Diagnostic Research Design 4. Experimental Research Design

In their study Descriptive Research Design has been adopted.

The purpose of the research methodology is to describe the research

procedure. This includes the over all research design. The sampling

procedure, the data collection method field & analysis procedure. This

selection is importance because it is hard to discuss methodology without

using technical terms.

Meaning of research

The advanced learner’s dictionary of current English says the meaning

of research as “A careful investigation of inquiry especially through search

for new facts in any branch of knowledge.

Research design

A research design is the specification of methods & procedure for

accounting the information needed to structure or to solve problem. It is the

overall operational pattern of frame works of the project that stipulation

procedure.

Type of research

i. Descriptive research

ii. Applied research

iii. Quantitative research

iv. Conceptual research

v. Analytical research

vi. Fundamental research

vii. Qualitative research

viii. Empirical research

Data collection

The researches should keep in mind two types of data while collecting

data viz primary & secondary data.

Primary data

The primary data are those which collected a fresh & fir the first time

& thus happen to be original in chapter. The source of primary data is the

field hand information or data from the business people who located their

shops in mount road, periamadu, Airport, G.P road and Spencer plaza.

Secondary data

The secondary data are those which have already been through the

statistical process.

Sample