a primer on bankruptcy law and trends in corporate ... · a primer on bankruptcy law and trends in...

TRANSCRIPT

Ken Ayotte

A Primer on Bankruptcy Law and Trends in Corporate Bankruptcy

Research

Ken Ayotte U.C. Berkeley School of Law

Ken Ayotte

Outline

1. Historical origins of corporate reorganization 2. What are the goals of Chapter 11? 3. Major features of the bankruptcy code 4. Research trends and developments

Ken Ayotte

Early corporate reorganization: railroads

• The major building blocks of corporate bankruptcy law today come from railroad reorganizations in the late 1800s.

• Characteristics of railroads: – Large amounts of capital required up front – Financed by bond issues, dispersed investor base – “Mortgage bonds” secured by cars and track

• Though heavily indebted, RR worth more as going-concern than liquidated (who wants to pull up track from the ground?)

• But hard to get all parties around the table to agree to a workout: small creditors may hold out.

• What do we do?

For a detailed discussion see David A. Skeel, Debt’s Dominion

Ken Ayotte

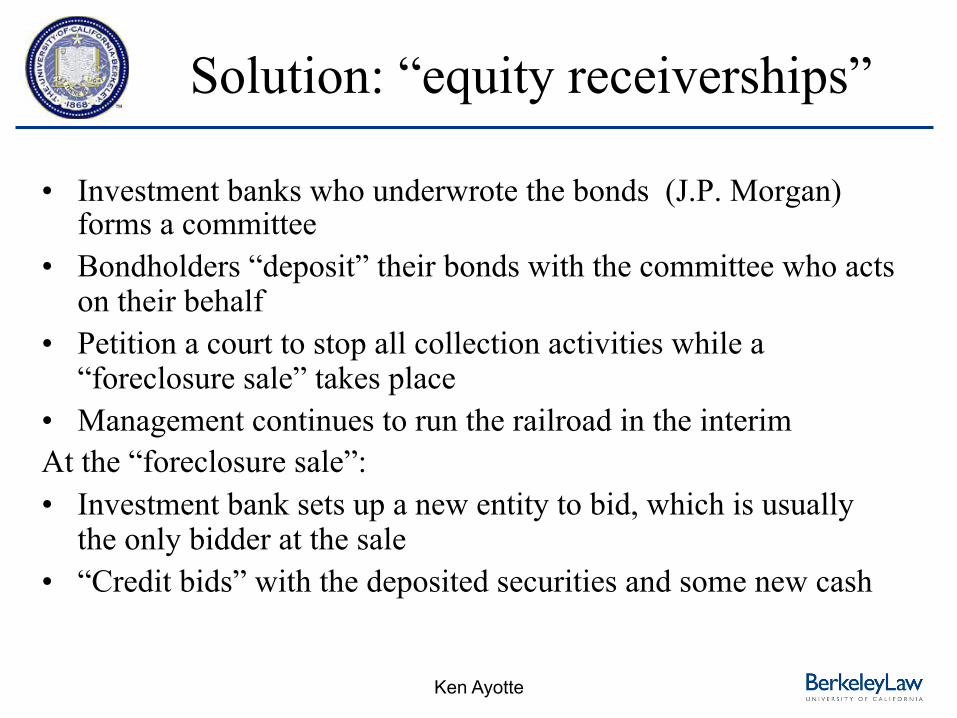

Solution: “equity receiverships”

• Investment banks who underwrote the bonds (J.P. Morgan) forms a committee

• Bondholders “deposit” their bonds with the committee who acts on their behalf

• Petition a court to stop all collection activities while a “foreclosure sale” takes place

• Management continues to run the railroad in the interim At the “foreclosure sale”: • Investment bank sets up a new entity to bid, which is usually

the only bidder at the sale • “Credit bids” with the deposited securities and some new cash

Ken Ayotte

Later additions to the process

At the end of the process: • The new entity owns the railroad, and sets up a new, less-

levered capital structure with old bondholders as new equity • Cash from foreclosure sale is paid to holdout creditors, old

entity extinguished Later developments: • Suppliers to the railroad were given priority claims to

encourage them to continue supplying during the foreclosure process

• Courts added “upset prices”: minimum floor price that holdouts must receive

Most of the features of this informal process are codified today in the bankruptcy code!

Ken Ayotte

Types of bankruptcy Three chapters in the U.S. bankruptcy code that are most

commonly used in business context: • Chapter 7: Liquidation

– Management is replaced by a trustee who sells the assets • Chapter 13: Adjustment of debts

– Available only to individuals, but sole proprietorships can use it to restructure small business debts. May be cheaper than Ch 11.

• Chapter 11: Reorganization – Most relevant chapter for corporate debtors if survival is possible. – Liquidation can occur in Ch 11, or case can be converted to Ch 7 later

in the process.

Ken Ayotte

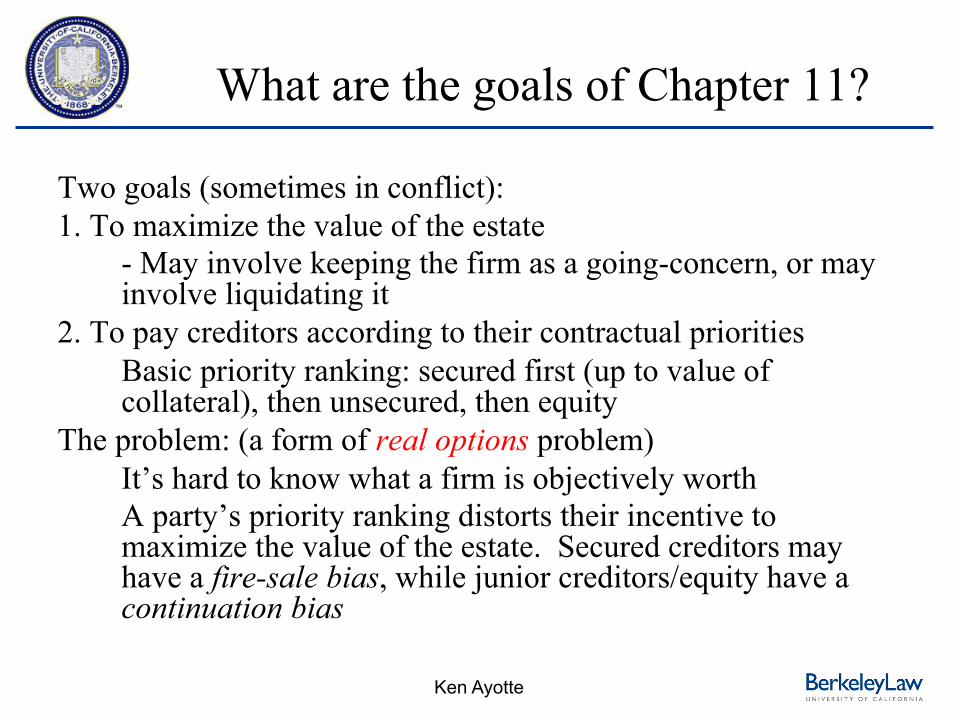

What are the goals of Chapter 11?

Two goals (sometimes in conflict): 1. To maximize the value of the estate

- May involve keeping the firm as a going-concern, or may involve liquidating it

2. To pay creditors according to their contractual priorities Basic priority ranking: secured first (up to value of collateral), then unsecured, then equity

The problem: (a form of real options problem) It’s hard to know what a firm is objectively worth A party’s priority ranking distorts their incentive to maximize the value of the estate. Secured creditors may have a fire-sale bias, while junior creditors/equity have a continuation bias

Ken Ayotte

When is Chapter 11 useful? • The railroad case is instructive because it describes a

situation where a Chapter 11 filing is most useful: – The business may be worth more as a going-concern than

liquidated – Creditors are dispersed and uncoordinated: possibility of

creditor runs, negotiations are challenging • The firm needs:

– Time/ breathing space (to sort out its affairs, decide what to do with the firm and who gets what, find potential buyers)

– Cash (to continue operations while decisions are made) – Restructuring (shedding assets and unprofitable operations) – Reduction in debt burden (so that the firm can operate

profitably going forward, if it chooses to reorganize)

Ken Ayotte

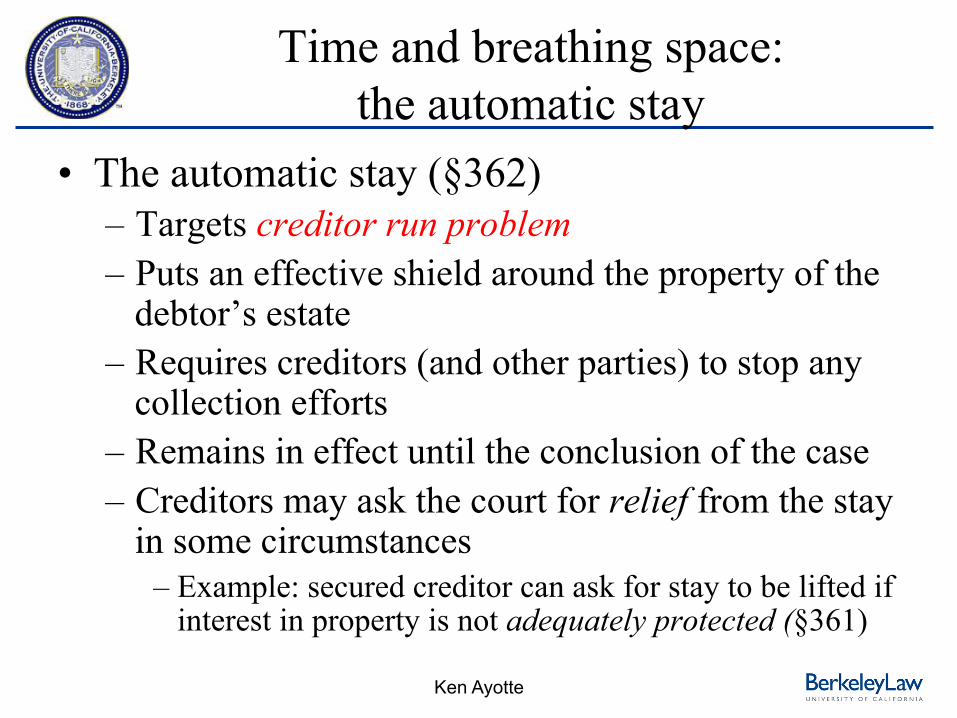

Time and breathing space: the automatic stay

• The automatic stay (§362) – Targets creditor run problem – Puts an effective shield around the property of the

debtor’s estate – Requires creditors (and other parties) to stop any

collection efforts – Remains in effect until the conclusion of the case – Creditors may ask the court for relief from the stay

in some circumstances ‒ Example: secured creditor can ask for stay to be lifted if

interest in property is not adequately protected (§361)

Ken Ayotte

New cash: Debtor-in-possession financing

• Debtor in possession financing (§364) – Targets debt overhang problem – Allows new money to come into the firm at a

higher priority than the firm could offer a lender outside of bankruptcy

– Usually, DIP loan is secured by any free assets, or by a second-lien on asset where a first-lien creditor is “oversecured”

– Overrides any contractual terms (like negative pledge clauses in bonds) that attempt to prevent firm from granting security to new lender

Ken Ayotte

Restructuring: Sale of assets “free and clear”

• Selling assets “free and clear of liens” (§363) – Targets adverse selection (lemons) problem – Outside of bankruptcy, a lien follows the asset to

the buyer – Subjects potential buyers to costly investigations,

due diligence, etc. to know what they are getting – Bankruptcy allows for buyers to purchase assets

“free and clear”—lienholder consent not always required

– In today’s environment, common for the entire going concern to be sold via a §363 sale

Ken Ayotte

Restructuring: Assumption, rejection, and assignment

• Leases and other executory contracts (§365) – Debtor decides whether to assume (keep), reject (abandon),

or assign (transfer) its leases and executory contracts. ‒ Another real option: debtor has time to decide, and must

perform while deciding

– If it assumes, firm must cure defaults and continue paying according to its lease contract

– If it rejects, lessor can seize the leased asset ‒ Also gets damages for breach, but the claim is unsecured!

– Debtor can assign the lease to a third-party, even if an anti-assignment clause in the lease contract

Ken Ayotte

Reducing debt burden: confirming a plan of reorganization

• Targets holdout/free rider problems • Basic requirements of confirming a consensual plan

of reorganization (§1129(a)): – Creditors grouped into classes, must be “substantially

similar” – Classes vote: for creditors, 2/3 in value and ½ in number

for a class to approve (just 2/3 in value for equity) – All “impaired” classes must approve – Debtor has exclusive rights to propose a plan for the first

120 days of the case. ‒ Prior to 2005 act, exclusivity period could be extended at judge’s

discretion, now 18 month limit

Ken Ayotte

Cramdown

• Alternatively, a party can propose a cramdown (§1129(b)): – Done when consensual plan is not attainable—

does not require approval by all impaired classes – Judge can confirm plan only if it satisfies the

absolute priority rule: ‒ For each class, either paid in full, or ‒ No lower class of claims (or interests) receives any

value

Ken Ayotte

Current topics in corporate bankruptcy research

• The rise of secured creditor control and creditor conflict

• Theory of the firm/theory of corporate groups • The influence of activist investors

Bankruptcy narratives

• Early narrative: Debtor control – Managers/shareholders use “debtor-friendly” features of

bankruptcy to delay, extract concessions from creditors – Too many reorganizations of companies that should have

liquidated, deviations from priority, low creditor recoveries – Example: Eastern Airlines (Weiss and Wruck 1998)

• Recent narrative: Secured creditor control – Baird and Rasmussen (2002), Skeel (2003) – Secured lender controls access to cash – All assets subject to liens – Uses covenants in pre-bankruptcy and DIP loans to steer

case outcomes – Concerns about “fire sales” and inefficient liquidations.

Ken Ayotte

Ken Ayotte

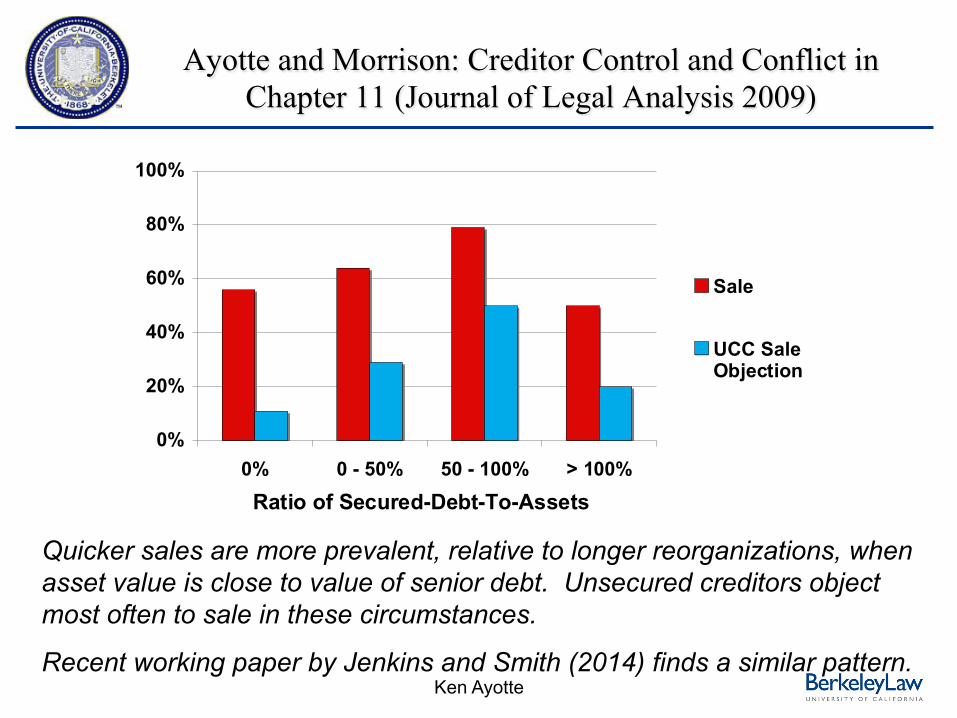

Ayotte and Morrison: Creditor Control and Conflict in Chapter 11 (Journal of Legal Analysis 2009)

0%

20%

40%

60%

80%

100%

0% 0 - 50% 50 - 100% > 100%Ratio of Secured-Debt-To-Assets

Sale

UCC SaleObjection

Quicker sales are more prevalent, relative to longer reorganizations, when asset value is close to value of senior debt. Unsecured creditors object most often to sale in these circumstances.

Recent working paper by Jenkins and Smith (2014) finds a similar pattern.

Ken Ayotte

The changes: creditor control

• While the bankruptcy code has not changed substantially, creditors (particularly, secured bank creditors) have learned how to protect themselves

• Evidence on creditor control from large bankruptcies: – CEO turnover: 70% of CEOs in place two years prior to

filing are out by the filing date – “Deviations from absolute priority” toward equity are rare

(only about 6% of cases) – Sales of the business (either piece-meal or going concern)

much more common than traditional reorganization (about 2/3 are sales)

See Ayotte and Morrison, “Creditor Control and Conflict in Chapter 11.” Journal of Legal Analysis 2009.

Digital Domain in Chapter 11

Ken Ayotte

Theory of the firm/corporate groups

• Theory of the firm literature in economics (Grossman/Hart/Moore, Williamson, etc) asks: why are assets under common ownership or separate ownership

• Legal scholarship confronts a different question: Why are commonly owned assets held in corporate groups? – Hansmann and Kraakman (2000): entity shielding and

creditor monitoring costs – Baird and Casey (2013), Casey (2015), Ayotte and

Gaon (2011), Ayotte (2015): stronger creditor rights in bankruptcy

Ken Ayotte

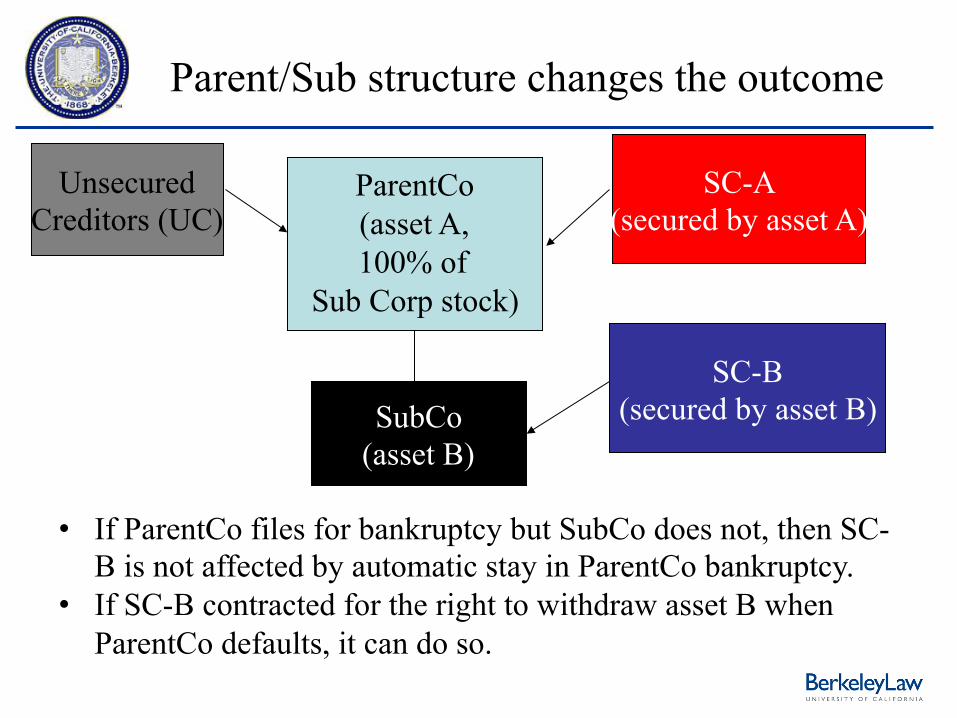

Debtor Corp (assets: A,B)

Secured Creditor (asset A)

Unsecured Creditors

Ayotte (2015): The Double-Edged Sword of Withdrawal Rights

Secured Creditor (asset B)

• If Debtor Corp files for bankruptcy, all secured and unsecured creditors are subject to an automatic stay.

• Cannot seize collateral without court permission • Stay is mandatory: can not waive by contract

ParentCo (asset A, 100% of

Sub Corp stock)

SubCo (asset B)

SC-A (secured by asset A)

Unsecured Creditors (UC)

Parent/Sub structure changes the outcome

SC-B (secured by asset B)

• If ParentCo files for bankruptcy but SubCo does not, then SC-B is not affected by automatic stay in ParentCo bankruptcy.

• If SC-B contracted for the right to withdraw asset B when ParentCo defaults, it can do so.

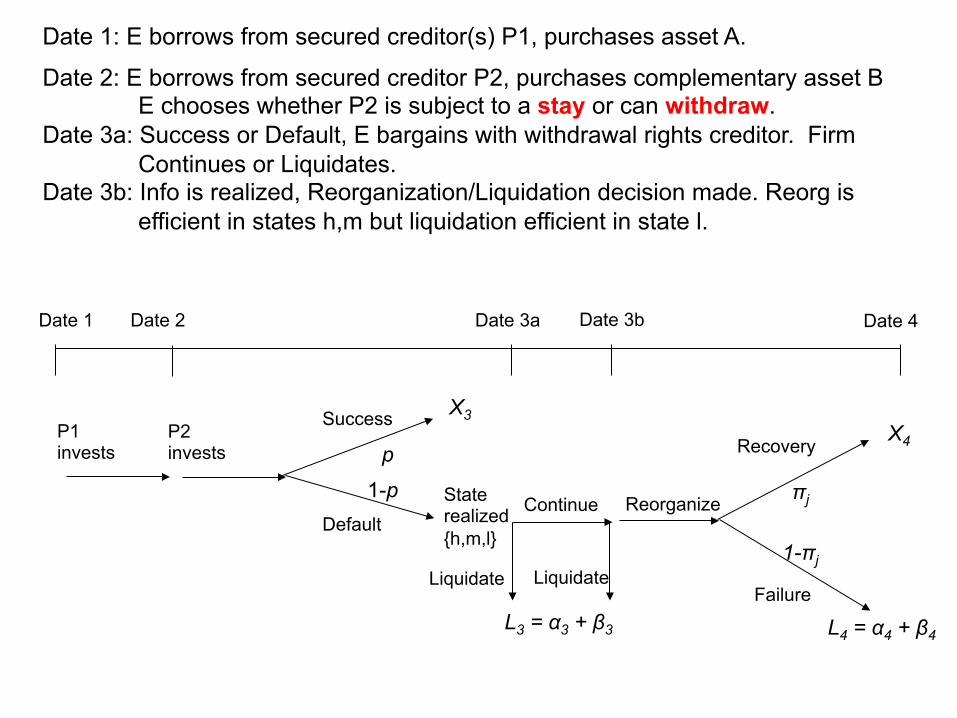

X3

Default

P1 invests

Liquidate

p

1-p

X4

L4 = α4 + β4

Success

Continue

L3 = α3 + β3

πj

1-πj

Recovery

Failure

P2 invests

State realized{h,m,l}

Date 1 Date 2 Date 3a Date 4 Date 3b

Liquidate

Reorganize

Date 1: E borrows from secured creditor(s) P1, purchases asset A.

Date 2: E borrows from secured creditor P2, purchases complementary asset B E chooses whether P2 is subject to a stay or can withdraw.

Date 3a: Success or Default, E bargains with withdrawal rights creditor. Firm Continues or Liquidates.

Date 3b: Info is realized, Reorganization/Liquidation decision made. Reorg is efficient in states h,m but liquidation efficient in state l.

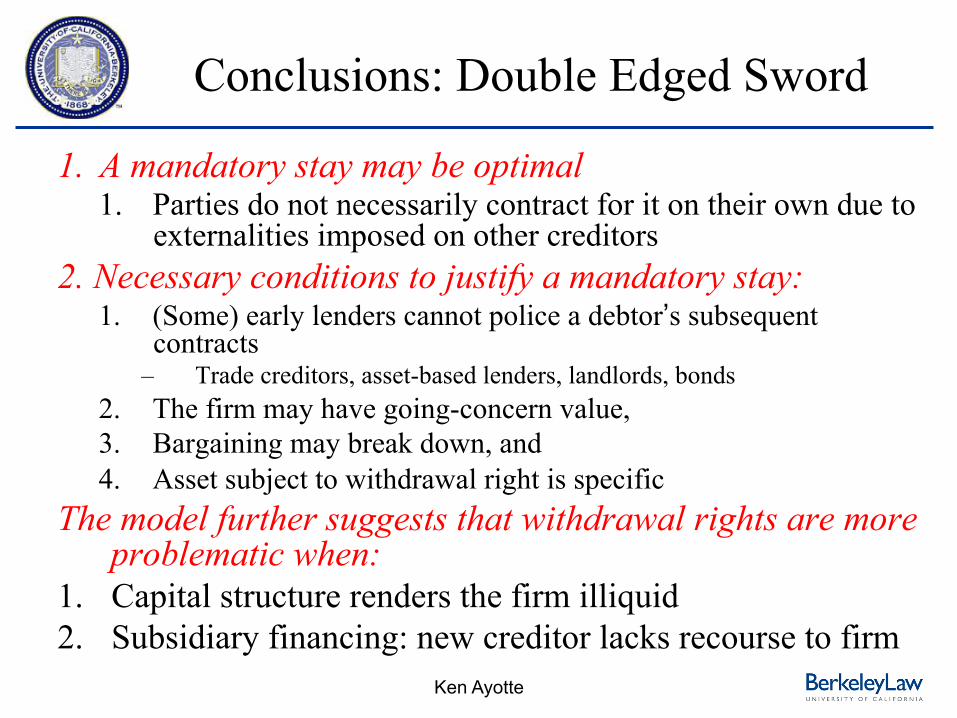

Conclusions: Double Edged Sword

1. A mandatory stay may be optimal 1. Parties do not necessarily contract for it on their own due to

externalities imposed on other creditors 2. Necessary conditions to justify a mandatory stay:

1. (Some) early lenders cannot police a debtor’s subsequent contracts ‒ Trade creditors, asset-based lenders, landlords, bonds

2. The firm may have going-concern value, 3. Bargaining may break down, and 4. Asset subject to withdrawal right is specific

The model further suggests that withdrawal rights are more problematic when:

1. Capital structure renders the firm illiquid 2. Subsidiary financing: new creditor lacks recourse to firm Ken Ayotte

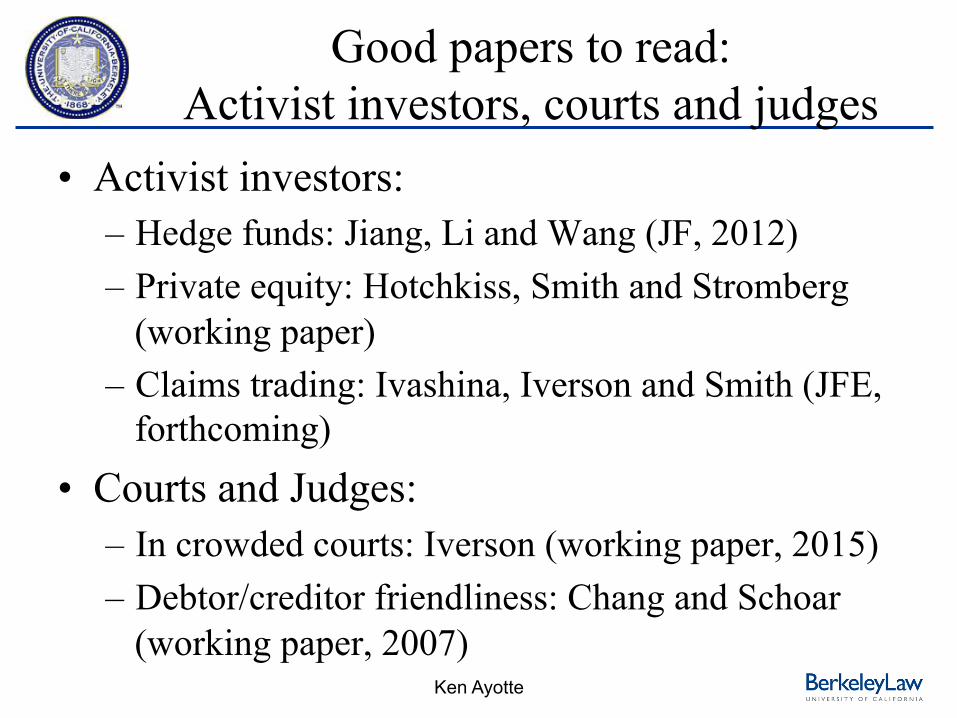

Good papers to read: Activist investors, courts and judges

• Activist investors: – Hedge funds: Jiang, Li and Wang (JF, 2012) – Private equity: Hotchkiss, Smith and Stromberg

(working paper) – Claims trading: Ivashina, Iverson and Smith (JFE,

forthcoming) • Courts and Judges:

– In crowded courts: Iverson (working paper, 2015) – Debtor/creditor friendliness: Chang and Schoar

(working paper, 2007) Ken Ayotte

(Somewhat messy) citations, I • Ayotte, K. and S. Gaon (2011). Asset Backed Securities: Costs and

Benefits of Bankruptcy Remoteness. Review of Financial Studies. • Ayotte, K. (2015) The Double-Edged Sword of Withdrawal Rights.

Working paper, U.C. Berkeley School of Law. • Ayotte, K. and E. Morrison. (2009) Creditor Control and Conflict in

Chapter 11. Journal of Legal Analysis. • Baird, D. and A. Casey (2013) No Exit? Withdrawal Rights and the

Law of Corporate Reorganizations. Columbia Law Review. • Baird, D. and R. Rasmussen (2002) The End of Bankruptcy.

Stanford Law Review • Casey, A. (2015) The New Corporate Web: Tailored Entity

Partitions and Creditors’ Selective Enforcement. Yale Law Journal, forthcoming.

• Chang, T. and A. Schoar (2007). The Effect of Judicial Bias in Chapter 11 Reorganization.

Ken Ayotte

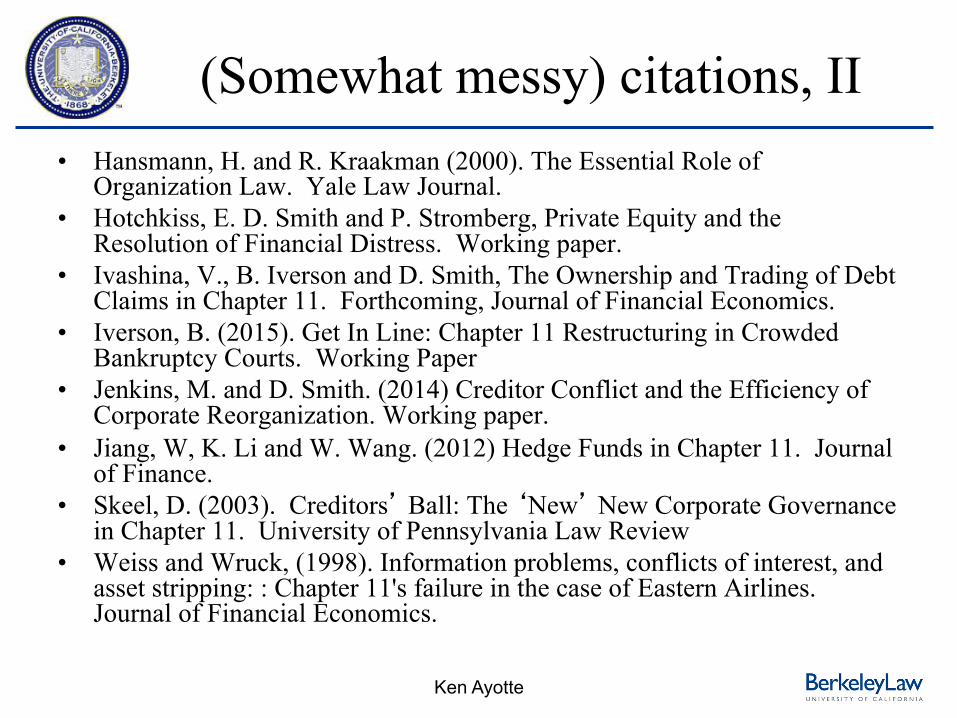

(Somewhat messy) citations, II • Hansmann, H. and R. Kraakman (2000). The Essential Role of

Organization Law. Yale Law Journal. • Hotchkiss, E. D. Smith and P. Stromberg, Private Equity and the

Resolution of Financial Distress. Working paper. • Ivashina, V., B. Iverson and D. Smith, The Ownership and Trading of Debt

Claims in Chapter 11. Forthcoming, Journal of Financial Economics. • Iverson, B. (2015). Get In Line: Chapter 11 Restructuring in Crowded

Bankruptcy Courts. Working Paper • Jenkins, M. and D. Smith. (2014) Creditor Conflict and the Efficiency of

Corporate Reorganization. Working paper. • Jiang, W, K. Li and W. Wang. (2012) Hedge Funds in Chapter 11. Journal

of Finance. • Skeel, D. (2003). Creditors’ Ball: The ‘New’ New Corporate Governance

in Chapter 11. University of Pennsylvania Law Review • Weiss and Wruck, (1998). Information problems, conflicts of interest, and

asset stripping: : Chapter 11's failure in the case of Eastern Airlines. Journal of Financial Economics.

Ken Ayotte