a ‘no-forecast’ price forecast: forward prices versus actuals the charts compare lme 15-month...

Post on 21-Dec-2015

216 views

TRANSCRIPT

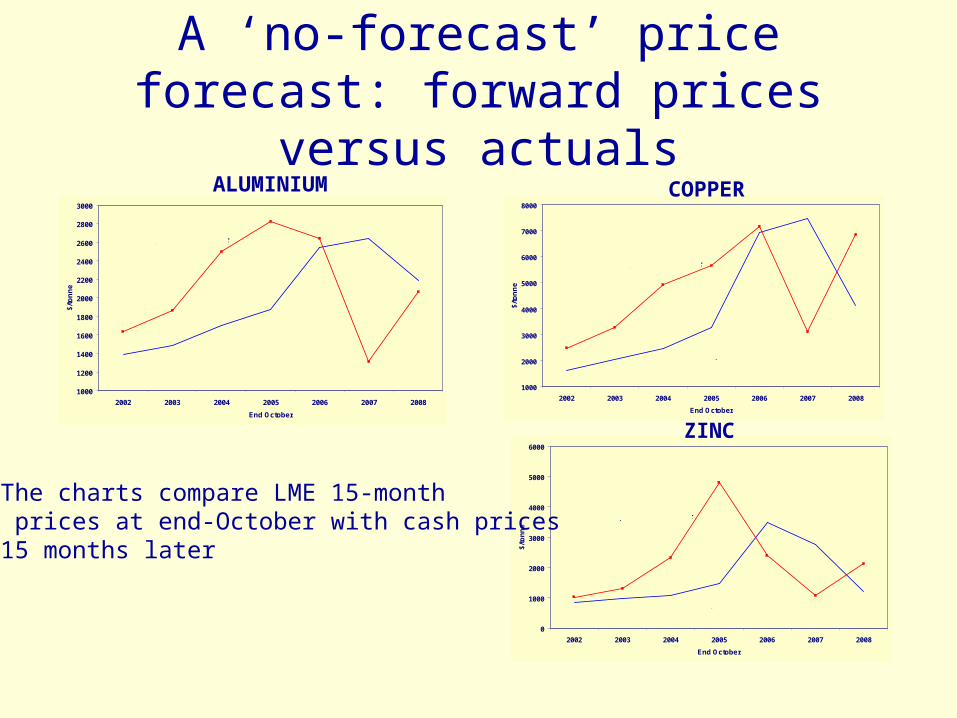

A ‘no-forecast’ price forecast: forward prices versus actuals

1000

1200

1400

1600

1800

2000

2200

2400

2600

2800

3000

2002 2003 2004 2005 2006 2007 2008

End October

$/t

on

ne

15 month forward price

Cash price 15 months later

1000

2000

3000

4000

5000

6000

7000

8000

2002 2003 2004 2005 2006 2007 2008

End October

$/to

nn

e

15 month forward price

Cash price 15 months later

0

1000

2000

3000

4000

5000

6000

2002 2003 2004 2005 2006 2007 2008

End October

$/to

nn

e

15 month forward price

Cash price 15 months later

The charts compare LME 15-month prices at end-October with cash prices15 months later

ALUMINIUM COPPER

ZINC

Analysts’ forecasts of metal prices

Forecasts by analysts published in the LME Ringsider in October for future years

ALUMINIUM COPPER

LEAD ZINC

0

500

1000

1500

2000

2500

3000

3500

4000

2004 2005 2006 2007 2008 2009 2010

US

$/t

on

ne

Oct 05

Oct 06

Oct 09

Oct 08

Oct 07

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

2004 2005 2006 2007 2008 2009 2010

US

$/t

on

ne

Oct 05

Oct 06

Oct 09

Oct 08

Oct 07 B

Oct 07 A

0

500

1000

1500

2000

2500

3000

2004 2005 2006 2007 2008 2009 2010

US

$/t

on

ne

Oct 05

Oct 06

Oct 09

Oct 08

Oct 07

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2004 2005 2006 2007 2008 2009 2010

US

$/t

on

ne

Oct 05

Oct 06

Oct 09

Oct 08

Oct 07

Projecting historic trends - one

0

50

100

150

200

250

300

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51

Year

US

Cen

ts/l

b i

n r

eal

term

s

Projecting historic trends – one !

0

50

100

150

200

250

300

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51

Year

US

Cen

ts/l

b i

n r

eal

term

s

Projecting historic trends - two

0

50

100

150

200

250

300

350

400

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37

Year

US

Cen

ts/l

b i

n r

eal

term

s

Projecting historic trends – two !

0

50

100

150

200

250

300

350

400

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37

Year

US

Cen

ts/l

b i

n r

eal

term

s

Copper prices in real terms1900-2009

0

50

100

150

200

250

300

350

400

450

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000

US

cen

ts/l

b i

n r

eal

2009

ter

ms

US producer

LME

There are probable world mine reserves of more than 100 Mt of copper, or enough for 80 years at the 1933 rate of consumption. All present knowledge indicates that in spite of the most extensive improvements in technology which can be expected, the second half of this reserve will cost a good deal more to extract than the first half. If consumption should expand at a rate approaching that of 1830 to 1930, there promises to be an acute shortage within a generation. (Skelton, 1934)

‘Ultimately recoverable’ reserves of copper 1930-2010

0

100

200

300

400

500

600

700

800

900

1000

1100

1200

Cumulative output from 1726 Remaining reserves

Forecasts of copper’s intensity of use

90

91

92

93

94

95

96

97

98

99

Chase Brook Hunt Actual Chase Brook Hunt Actual

Ind

ex

nu

mb

ers

19

80

= 1

00

1985 1990United States

75

80

85

90

95

100

105

Chase Brook Hunt Actual Chase Brook Hunt Actual

Ind

ex

nu

mb

ers

19

80

= 1

00

1985 1990Japan

Sources: Chase Econometrics’ World Copper Outlook, March 1984. Brook Hunt evidence to the US International Trade Commission, May 1984. WBMS and IMF for actuals.

Refined zinc usage: a 1982 forecast

0

1000

2000

3000

4000

5000

6000

7000

8000

1980 2000 forecast 2000 actual

'00

0 t

on

ne

s

Western Europe(+0.6%)

Rest of World(-0.03%)

Sources: ILZSG, SRI Metallic Minerals Programme 1982

Refined zinc usage: details

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

1980 2000 forecast 2000 actual

'00

0 t

on

ne

s

Eastern Countries(+31.2%)

Other countries(-17.2%)

Latin America(+62.2%)

Japan(+32.7%)

North America(-14.9%)

Western Europe(+0.6%)

Sources: ILZSG, SRI Metallic Minerals Programme 1982

Copper usage, production & capacity

10000

11000

12000

13000

14000

15000

16000

17000

18000

19000

20000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

'000

to

nn

es c

op

per

Mine production

Refined copper usage

Mine capacity

Primary copper usage

Source: ICSG press releases, July 2008 & June 2009

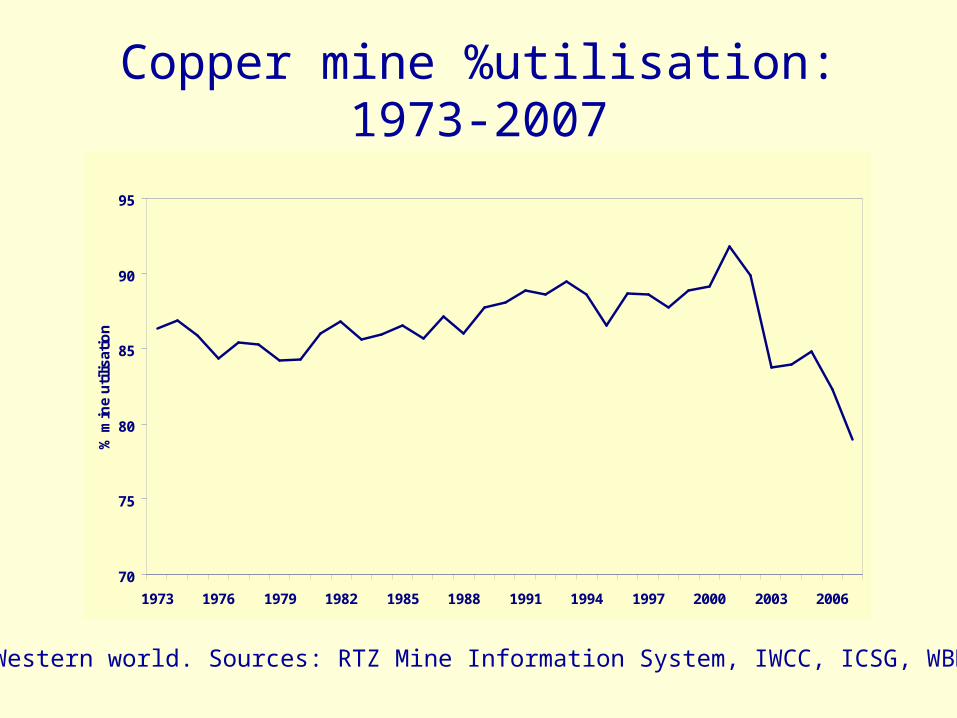

Copper mine %utilisation: 1973-2007

70

75

80

85

90

95

1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006

% m

ine

uti

lisat

ion

Western world. Sources: RTZ Mine Information System, IWCC, ICSG, WBMS.

Output of Escondida & Grasberg: 1989 to 2007

0

500

1000

1500

2000

2500

3000

1989 1991 1993 1995 1997 1999 2001 2003 2005 2007

'000

to

nn

es c

on

tain

ed c

op

per

Output

Capacity

Source: IWCC Survey of Copper Capacity, March 2008

Output of mines producing both copper and molybdenum

90

100

110

120

130

140

150

160

170

180

190

200

210

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Ind

ex

nu

mb

ers

19

96

=1

00

Copper

Molybdenum

Ore

Source: Raw Materials Database, Raw Materials Group, Sweden