a global love affair - the economist · a global love affair ... brazil,russia,indiaandchina(theso...

TRANSCRIPT

A global love affairA special report on cars in emerging markets

November 15th 2008

CarsCOV.indd 1CarsCOV.indd 1 4/11/08 14:08:134/11/08 14:08:13

The Economist November 15th 2008 A special report on cars in emerging markets 1

Emerging markets are the car industry’s big hope. But it won’t be aneasy ride, says Matthew Symonds

sales in the BRICs, at around 14m, are likelyto overtake those in America, which are expected to be the worst since 1992. As recently as 2005 America outsold them by over10m. By the end of this decade China, already the world’s secondbiggest market,will probably overtake America’s sales of16m17m in a �normal� year. In Brazil saleshave increased by nearly 30% in each ofthe past two years. Russia is likely to overtake Germany as Europe’s biggest marketwithin the next two years, with sales ofaround 3.5m. Meanwhile, Tata’s $2,500Nano, due to be launched in early 2009, isdesigned to do for India what the Model TFord did for America 90 years ago.

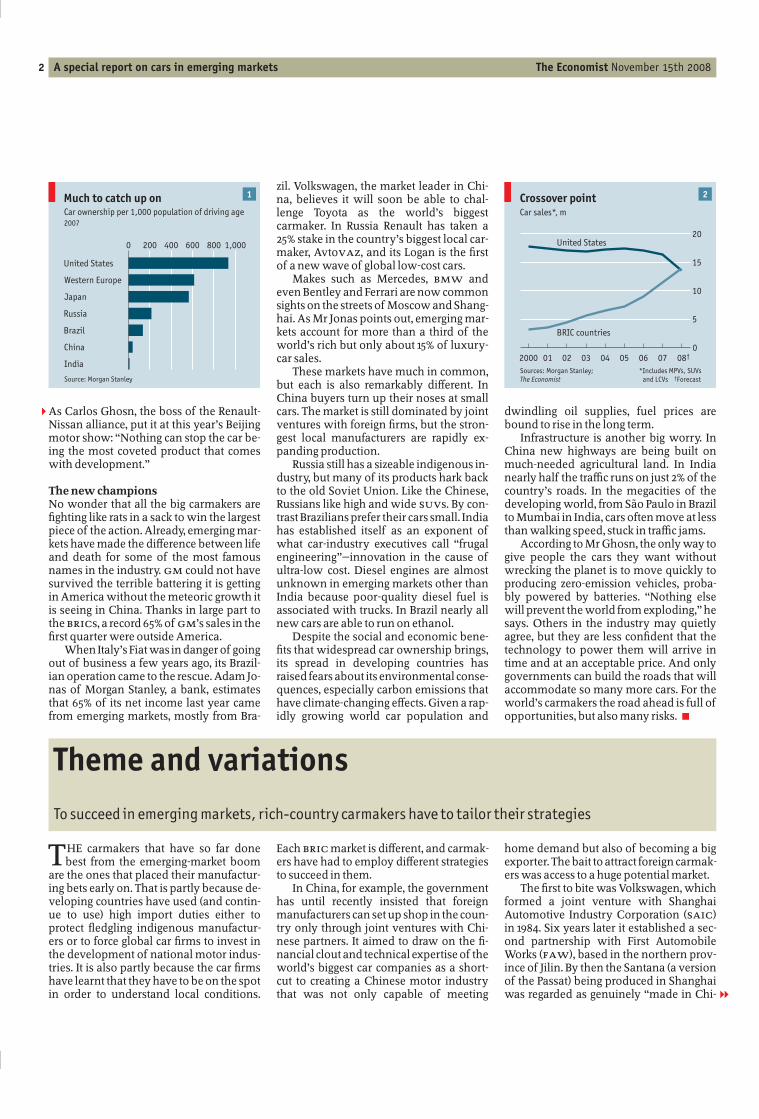

It is the irresistible combination of rapid economic growth, favourable demographics and social change in the BRICsthat is coming to the carmakers’ rescue andthat is likely to account for nearly all theirgrowth for the foreseeable future. Americahas more than 900 cars (including lighttrucks) for every 1,000 people of drivingage. In the big western European countriesand Japan, where public transport is betterand population is denser, the �gure is a little over 600. But in Russia it is below 200,in Brazil about 130, in China around 30 andin India less than ten.

When times are hard, an Americanfamily that already has two or three carswill simply postpone buying a new one.But a potential customer in an emergingmarket who has been saving for years tobuy his �rst car will still want to go ahead.

A global love a�air

THERE has rarely been a tougher time tobe a carmaker. Squeezed by the credit

crunch, rocked by the seesawing price ofoil and now faced with a nasty recession asthe banking crisis infects the real economy,the traditional markets of North America,western Europe and Japan, already sluggish for several years, have all but packedup. In America car sales are running atabout 16% below last year’s level. Detroit’sstruggling big three�General Motors, Fordand Chrysler�have just wrung a $25 billion bailout from Congress and couldsoon become just two. In Europe the decline has been less steep but the market isnow contracting. Sales in Japan this yearare expected to be the lowest since 1974.

However, not all is doom and gloom.Mature vehicle markets may be close tosaturation, but there is huge unsatis�ed demand in the big emerging car markets ofBrazil, Russia, India and China (the socalled BRICs). Although not immune fromthe rich countries’ troubles, they are likelyto su�er much less. For one thing, levels ofpersonal debt are far lower and a smallerproportion of cars are bought on credit. Foranother, the BRIC economies have beenexpanding so fast that even a slowdownshould still leave them with growth ratesthat look respectable to Western eyes.

One measure of the BRIC countries’new importance to the car industry is that,recession or not, global car sales in 2008may still hit an alltime record of about59m. For the �rst time passengervehicle

An audio interview with the author is at

www.economist.com/audiovideo

A list of sources is at

www.economist.com/specialreports

Theme and variationsTo succeed in emerging markets, richcountry carmakers have to tailor their strategies.Page 4

The home teamIndigenous carmakers are working their wayup. Page 8

Pile them highThe cheapandcheerful end of the market.Page 11

Kings of the roadCheaper than four wheels, better than twofeet. Page 13

The art of the possibleThe question is not whether the world cancope with three billion cars�but how. Page 14

Also in this section

AcknowledgmentsApart from those quoted in the text, the author would liketo thank the following for their help in the preparation ofthis report: Kumar Bhattacharyya of WarwickManufacturing Group; Cecil Dewars of TVS; RichardGadeselli of Fiat; David Herman and Nikolay Sobolov ofSeverstal Auto; Andrew Lorenz of Financial Dynamics; TomMalcolm and Irina Sharovatova of Ford; C. Narasimham ofSundaramClayton; Jackson Schneider of ANFAVEA;JosefFidelis Senn of Volkswagen Brazil; Edoardo Spina ofMorgan Stanley; and Carlos Tavares of Nissan.

1

More articles about cars are at

www.economist.com/cars

2 A special report on cars in emerging markets The Economist November 15th 2008

2

1

As Carlos Ghosn, the boss of the RenaultNissan alliance, put it at this year’s Beijingmotor show: �Nothing can stop the car being the most coveted product that comeswith development.�

The new championsNo wonder that all the big carmakers are�ghting like rats in a sack to win the largestpiece of the action. Already, emerging markets have made the di�erence between lifeand death for some of the most famousnames in the industry. GM could not havesurvived the terrible battering it is gettingin America without the meteoric growth itis seeing in China. Thanks in large part tothe BRICs, a record 65% of GM’s sales in the�rst quarter were outside America.

When Italy’s Fiat was in danger of goingout of business a few years ago, its Brazilian operation came to the rescue. Adam Jonas of Morgan Stanley, a bank, estimatesthat 65% of its net income last year camefrom emerging markets, mostly from Bra

zil. Volkswagen, the market leader in China, believes it will soon be able to challenge Toyota as the world’s biggestcarmaker. In Russia Renault has taken a25% stake in the country’s biggest local carmaker, AvtoVAZ, and its Logan is the �rstof a new wave of global lowcost cars.

Makes such as Mercedes, BMW andeven Bentley and Ferrari are now commonsights on the streets of Moscow and Shanghai. As Mr Jonas points out, emerging markets account for more than a third of theworld’s rich but only about 15% of luxurycar sales.

These markets have much in common,but each is also remarkably di�erent. InChina buyers turn up their noses at smallcars. The market is still dominated by jointventures with foreign �rms, but the strongest local manufacturers are rapidly expanding production.

Russia still has a sizeable indigenous industry, but many of its products hark backto the old Soviet Union. Like the Chinese,Russians like high and wide SUVs. By contrast Brazilians prefer their cars small. Indiahas established itself as an exponent ofwhat carindustry executives call �frugalengineering��innovation in the cause ofultralow cost. Diesel engines are almostunknown in emerging markets other thanIndia because poorquality diesel fuel isassociated with trucks. In Brazil nearly allnew cars are able to run on ethanol.

Despite the social and economic bene�ts that widespread car ownership brings,its spread in developing countries hasraised fears about its environmental consequences, especially carbon emissions thathave climatechanging e�ects. Given a rapidly growing world car population and

dwindling oil supplies, fuel prices arebound to rise in the long term.

Infrastructure is another big worry. InChina new highways are being built onmuchneeded agricultural land. In Indianearly half the tra�c runs on just 2% of thecountry’s roads. In the megacities of thedeveloping world, from São Paulo in Brazilto Mumbai in India, cars often move at lessthan walking speed, stuck in tra�c jams.

According to Mr Ghosn, the only way togive people the cars they want withoutwrecking the planet is to move quickly toproducing zeroemission vehicles, probably powered by batteries. �Nothing elsewill prevent the world from exploding,� hesays. Others in the industry may quietlyagree, but they are less con�dent that thetechnology to power them will arrive intime and at an acceptable price. And onlygovernments can build the roads that willaccommodate so many more cars. For theworld’s carmakers the road ahead is full ofopportunities, but also many risks. 7

1Much to catch up on

Source: Morgan Stanley

Car ownership per 1,000 population of driving age2007

0 200 400 600 800 1,000

United States

Western Europe

Japan

Russia

Brazil

China

India

2Crossover point

Sources: Morgan Stanley;

The Economist

*Includes MPVs, SUVs

and LCVs †Forecast

Car sales*, m

2000 01 02 03 04 05 06 07 08†0

5

10

15

20United States

BRIC countries

THE carmakers that have so far donebest from the emergingmarket boom

are the ones that placed their manufacturing bets early on. That is partly because developing countries have used (and continue to use) high import duties either toprotect �edgling indigenous manufacturers or to force global car �rms to invest inthe development of national motor industries. It is also partly because the car �rmshave learnt that they have to be on the spotin order to understand local conditions.

Each BRIC market is di�erent, and carmakers have had to employ di�erent strategiesto succeed in them.

In China, for example, the governmenthas until recently insisted that foreignmanufacturers can set up shop in the country only through joint ventures with Chinese partners. It aimed to draw on the �nancial clout and technical expertise of theworld’s biggest car companies as a shortcut to creating a Chinese motor industrythat was not only capable of meeting

home demand but also of becoming a bigexporter. The bait to attract foreign carmakers was access to a huge potential market.

The �rst to bite was Volkswagen, whichformed a joint venture with ShanghaiAutomotive Industry Corporation (SAIC)in 1984. Six years later it established a second partnership with First AutomobileWorks (FAW), based in the northern province of Jilin. By then the Santana (a versionof the Passat) being produced in Shanghaiwas regarded as genuinely �made in Chi

Theme and variations

To succeed in emerging markets, richcountry carmakers have to tailor their strategies

The Economist November 15th 2008 A special report on cars in emerging markets 3

2

1

na�. By the end of the 1990s VW was selling over 300,000 cars a year in China.VW’s share of the market has fallen from apeak of 56% to around 18% today, but itsvolume has tripled. Despite slowing salessince July the �rm still expects to sell morethan a million cars in China this year�more than it sells in Germany, and enoughto justify its $10 billion investment.

Showing unusual �eetness of foot, GM

followed VW into the Chinese market inthe mid1990s by forming a joint ventureof its own with SAIC. Like VW, it has prospered by establishing its brands (especiallyBuick) and its distribution network beforeother foreign �rms rushed into the market,and with a 10% share is now second only toVW. Last year GM sold twice as manyBuicks in China as it did in America, wherethe brand is considered a bit staid.

But the competition is getting more intense. Despite a late start, Toyota, with itsmain partner, FAW, is threatening to topple GM from its second spot in China and isaiming to produce 1m units by 2010. Another relative latecomer is Nissan. With Dongfeng Motor, it has been producing carssince 2004 from a new integrated factoryat Huadu near Guangzhou that can churnout 360,000 a year. This year Nissan addeda 6,140squaremetre (69,000squarefoot)training centre for its dealers, a bow to thegrowing importance of service in a marketwhere consumers have more models tochoose from than in America.

In theory foreign carmakers are no longer legally obliged to work through jointventures in China, but in practice they stilldo. Adrian Hallmark, VW’s head of salesin Asia, explains that a few years ago VW

had an opportunity to pull out of one of itsjoint ventures but decided against it:�When you don’t have the cultural and political connections, it is suicidal to go italone.� Over time, he says, VW’s partners,SAIC and FAW, are likely to emerge aspowerful companies in their own rightand will have bene�ted from the experience of working with VW. He sees no reason why they should want to abandon thejoint ventures if they continue to workwell for both parties, which he believesthey will. Chinese customers, says MrHallmark, will always want to buy the bestproducts, so the foreign brands should continue to do well from market growth.

Nick Reilly, the head of GM’s AsiaPacific operations, concedes that joint venturesare never easy to manage and that manyfail. �The moment it ceases to be a winwinfor both sides, it will go,� he says. �Yourpartner must do well too.� GM puts a lot of

e�ort into its relationship with SAIC. Itschief executive, Rick Wagoner, meets upwith his Chinese counterparts at leastthree times a year. Mr Reilly is also philosophical about the inevitable transfer ofintellectual property to its partner, sayingGM does not want to be �too precious�about it. He concedes that there could betensions when SAIC’s own brands, such asRoewe, start competing directly withGM’s, but says that money will still becoming in from royalties and components.

All the foreign carmakers are wellaware that the Chinese government is prepared to play a long game. For now and forthe foreseeable future the foreigners arepart of the plan, but when a handful of potential winners emerge from among the local champions life might well get morecomplicated. �In the end�, says one seniorforeign car executive, �it will come downto politics. It always does here.�

All Brazilians nowThere are no such fears in Brazil. The Brazilian market is still dominated by the four�rms that have been there longest�GM,Ford, VW and Fiat�and they have alwaysmanaged without local partners. Last yeartheir combined share of a market of 2.45mlight passenger vehicles was 80%.

At Fiat’s Betim factory near the industrial city of Belo Horizonte in Brazil a new carrolls o� the production line every 20 seconds. To meet surging domestic demandfor new cars, Fiat, the market leader in Bra

zil, is working Betim �at out, three shifts aday. It is one of the most productive car factories in the world, capable of churningout 800,000 vehicles a year. The biggestconcern for Cledorvino Belini, head ofFiat’s operations in Latin America, is thatthe furious pace of production is puttingthe complex �justintime� logistical system under strain. Cars awaiting transfer �llevery corner of the 2.25msquaremetre(24.22msquarefoot) site, and new unloading bays are being constructed at breakneck speed to accommodate the endless�ow of trucks delivering the parts.

Fiat, which began manufacturing inBrazil 32 years ago, allows its Brazilian arma lot of autonomy. All its senior managersare Brazilian. They say they want Fiat to beseen as a Brazilian brand�an ambitionthey back up by sponsoring the shirts of nofewer than ten of Brazil’s best footballteams. VW is even more of a veteran, having been in the country for 55 years. Although the top management is mostly German, it claims that Brazilians have stronglyidenti�ed with the VW brand since thedays when the Beetle was the country’smost popular car. More than 3m were produced at the �rm’s giant Anchieta factorynear São Paulo between 1959 and 1986.

With import taxes still at a swingeing35% and other car taxes averaging morethan 30%, depending on engine size andtype, vehicle makers have little choice butto manufacture in Brazil. There was a timewhen Brazilians could be o�ered discon

Churning them out at Betim

4 A special report on cars in emerging markets The Economist November 15th 2008

2

1

tinued models from Europe, but apart fromthe very cheapest cars that is no longer acceptable. Both Fiat and VW now makesome of their newest cars in Brazil, including some produced specially for the Brazilian market, such as the Fiat Palio and VW

Gol. Both are rugged and small but roomycars with a range of ��exfuel� engines thatrun on any combination of ordinary petroland canebased ethanol.

The development of �exfuel engines isthe most striking example of the carmakers’ willingness to invest to meet the Brazilian market’s particular needs. The technology was developed by the Brazilian arm ofMagneti Marelli, a wholly owned subsidiary of Fiat, and Robert Bosch, a Germancomponentmaker that has a close relationship with VW. Both car �rms beganequipping their vehicles with �exfuel engines in 2003, and now such engines power nearly every car being made in Brazil.About half the fuel used by cars today inBrazil is ethanol.

For ordinary Brazilians the attraction isthat it sells for little more than half theprice of normal petrol, although its range isslightly shorter. The government is alsokeen on ethanol because the industry employs over a million people, saves on imports and provides insurance against highoil prices. It is also relatively clean, producing lower �welltowheel� emissions thanpetrol, unlike the cornbased ethanol being sold in America; and it is sustainable,taking up only 2% of land currently in agricultural use.

Both Fiat and VW emphasise the needto develop their cars locally. Bumpy, unmetalled roads call for good ground clearance and heavyduty suspensions. Carsdesigned for European conditions wouldfall apart in just a few months in Brazil,says Fiat. Both makers have recently takento producing what are known as �SUVlite� versions of ordinary cars. There is atoughlooking Palio �Adventure� and abeefedup small VW hatchback called theCrossFox. But the market is dominated byfairly spacious cars with small engines.Cars with engines up to one litre attract alower level of purchase tax, making themthe choice of more than half of Braziliansbuying a new car. Cheapest of the lot is aBrazilian version of Fiat’s Uno, the Mille.Although it falls some way short of modern safety standards, the Mille has rackedup sales of more than 2m in Brazil and isstill going strong.

The biggest worry for Brazil’s big four isthat the car business is rapidly becomingmore competitive. Two French makers,

PSA Peugeot Citroën and Renault, tooknearly 8% of the market last year, followedby the Japanese, led by Toyota and Honda.Toyota is building a second factory in SãoPaulo that will come on stream in 2010 andproduce a smaller, cheaper car than the Corolla it currently makes. The South Koreansare beginning to take an interest too. Jackson Schneider, the president of ANFAVEA,a trade body, predicts that by 2013 Brazilwill be the world’s sixthbiggest car producer, turning out more than 5m cars, 4mof them for the domestic market.

Still guzzling in RussiaThe rapid rise in oil prices that draggedmost vehicle markets down this year hadthe opposite e�ect in Russia. Thanks toabundant natural resources the economyhas grown at an average of 7% a year for thepast decade and only now shows somesigns of �agging as commodities pricesdrop. In the past �ve years real disposableincomes have doubled. Speaking earlierthis year, Heidi McCormack, GM’s head ofbusiness development in Russia, notedthat compared with more developed markets Russia had been �magically isolated.�

When the economy began to recoverfrom the crisis of the late 1990s, Russians,scornful of their own car industry’s Sovietera products, began buying ever more usedimported cars. In 2002 they snapped upnearly 500,000 of them, mainly from Germany and Japan. Even quite elderly VWsand Toyotas were a revelation of modernity, quality and price compared with the Ladas of AvtoVAZ and the Volgas of Gaz. In

response to desperate pleas from Russiancarmakers the government agreed to slap asteep duty and VAT on imported cars tochoke o� the supply.

However, the domestic carmakers werein no position to take advantage of thebreathing space. Three years later new imports were taking nearly half the market,despite high duties. Impatient with the local �rms but determined to revive its domestic industry, the government in 2005passed a law designed to entice foreignmanufacturers to assemble their productsin Russia. To qualify for relief from importduty, foreign carmakers had to build a factory with a capacity of more than 25,000vehicles a year and invest at least $100m.Within �ve years the local content of eachcar had to reach 30%. But unlike in China�rms were not required to establish partnerships with local producers.

The pioneers in Russia have been Fordand GM. In 1999 Ford dipped a toe in thewater with a small assembly plant near StPetersburg, and in the same year GM wentfor a seemingly risky joint venture withAvtoVAZ (at the time a byword for corruption and gangsterism) to produce an improved version of the Niva, a cheap SUV.More recently others have joined thescramble. Renault, as part of a deal withMoscow’s city government, took over anold Moskvich factory in 2004 to build itslowcost Logan, and VW in 2006 beganconstruction of a new factory in Kaluga,120 miles (190km) southwest of Moscow,where Mitsubishi and PSA Peugeot Citroën are also setting up.

Most of the others have gone to the StPetersburg area, where Ford and GM havebeen steadily expanding their capacity.Toyota is now producing Camrys thereand will soon be joined by Nissan, Suzukiand Hyundai. St Petersburg owes its popularity to its icefree port, good rail links andwelleducated workforce, as well as thecando approach of the governor, Valentina Matviyenko, who has promised toturn the city into Russia’s Detroit. Much ofthe tra�c on the 450mile road to Moscowis made up of car transporters. GM andFord still have about 20% and 10% respectively of the market, but competition ishotting up.

By 2012 ten of the world’s biggest carcompanies will be manufacturing up to1.6m vehicles a year in Russia, with a largecomponents industry growing up aroundthem. Eduard Faritov, an analyst at Renaissance Capital, an investment bank, thinksthat Russians will be buying nearly 5mnew cars a year by then, and 80% of them

3A vital ingredient

Source: Morgan Stanley

Companies’ sales in emerging markets% of total sales

0 10 20 30 40 50

Hyundai

Fiat

VW

Renault

GM

PSA

Toyota

Nissan

Ford

Porsche

Daimler

BMW

Operating profit,% of total

35.0

56.8

21.9

15.8

na

7.2

20.6

10.3

na

43.1

28.1

19.9

The Economist November 15th 2008 A special report on cars in emerging markets 5

2

1

will be foreign brands. Nigel Brackenbury,head of Ford’s operations in Russia, notesthat for most of the past decade foreignbrands have mopped up all the growth inthe market. Ford, he says, now sells morecars in a week than it did in a year when it�rst started out. Over time Mr Faritov expects the foreign manufacturers based inRussia to supply an increasing proportionof the market as their capacity increases.New imports will continue to make up alarge segment of the market, but will beconcentrated at the top end and in nichemarkets. The future of the biggest domesticmaker, AvtoVAZ, will depend on the outcome of a joint venture with Renaultsealed this year in which the French �rmacquired a 25% stake for $1billion.

What Indians wantFew joint ventures between a local �rmand a foreign manufacturer have been asenduring and pro�table as that of Marutiof India and Suzuki, a Japanese smallcarspecialist. Set up in the early 1980s as a government project to produce a cheap modern car for middleclass Indians, Maruti Suzuki still dominates the Indian market,with a 54% share in 200708. Indians stillthink of Maruti as an Indian company, butthe company’s range now consists almostentirely of modern Suzukis, such as thebestselling Alto and the more expensiveSwift. With 54% of the equity the Japanesecompany is �rmly in the driving seat.

A more recent success story is that ofHyundai, one of many foreign manufacturers that entered the Indian market afterthe economy was liberalised in the 1990s.Faced with an import duty of 91% on smallcars assembled from �semiknockdown�and 31% even for assembly from �completeknockdown�, Hyundai, in common withits foreign rivals, decided to move straightto full manufacturing in India. But it did soon a much grander scale than others, investing an initial $1.2 billion there.

A decade ago Hyundai began production of the Santro, a small car with a highroo�ine for added space, from a stateoftheart factory on the outskirts of thesouthern city of Chennai. The South Korean �rm now occupies second place in themarket with an 18% share, pushing TataMotors, India’s only big entirely indigenous maker, into third place with 14%. Hyundai India’s managing director, HeungSoo Lheem, claims that Hyundai is theonly car �rm in India to manufacture acomplete range of cars locally. At the end oflast year it doubled its capacity to 600,000units with the opening of a second assem

bly line to build an important new car, thei10.

According to Mr Heung, this is the �rstfruit of Hyundai’s decision to make Indiaits world production centre for cars under1.5 litres. Up to half of the i10s producedwill be exported. M. Inderjith, the factory’smanager, says that means the quality willhave to be worldclass. The car is alreadyon sale in Europe, where it has won excellent reviews. For India it is also a step forward in sophistication at an importantprice point. Even basic models selling for350,000 rupees ($7,000, or just over£4,000) have airconditioning and tintedglass (airbags and antilock brakes are reserved for more expensive versions). Although the i10 factory is highly automated,low labour costs still make it 10% cheaperto manufacture in India than in Korea.

GM has doubled its sales in the pastyear, growing even faster than Hyundai,though from a lower base. But what is win

ning over the Indians is not GM’s American or European models but the small,cheap cars badged as Chevrolets and madein Gujarat by its South Korean subsidiary,Daewoo. Ford, which has invested only arelatively modest $150m in the country, hasstruggled to build up a signi�cant volume,despite its early arrival in India. It o�ers theIkon, a saloon based on an old Fiesta platform which is sold only in India, as well asa more uptodate booted version of the Fiesta and the chunkily styled Fusion, but itsIndian production this year will be onlyabout 35,000 units.

Michael Boneham, an Australian whohas been sent to turn round Ford’s fortunesin India, expects this to change soon. Be

tween now and 2010 Ford will spend$500m, doubling its capacity to 200,000units and developing a new small car tocompete with Chevrolet’s Spark and Hyundai’s i10 in the 300,000500,000 rupeesprice range that accounts for nearly 70% ofcar sales in India. Mr Boneham says thatwith greater choice Indian customers havebecome more demanding, expecting evenfairly lowcost cars to be well speci�ed.Getting costs down to the lowest possiblelevel is only the �rst, albeit essential, stepto providing the right quality and value.Like Hyundai, Ford intends to export itsnew small car in quantity, mainly to theAsiaPaci�c region and parts of Africa.

Five lessonsWhat wider lessons can the world’s carcompanies learn from their experiences inthe four markets that will provide most oftheir growth in the years to come? The �rstis that they must show commitment. Getting there early brings big advantages, butthey have to be built on. Fiat has done wellin Brazil�even though it arrived after Fordand GM�because it understood the market better, trusted its local managementand invested heavily. Hyundai and Fordpitched their tents in India at about thesame time, but Hyundai took the country’spotential far more seriously and is reapingthe bene�ts.

The second lesson is that no single business model works in every country or forevery company. In China the ability tomanage joint ventures has paid o� handsomely for VW and GM. To make upground in China, the Japanese, never previously comfortable in joint ventures, arehaving to learn new skills and be more relaxed about the transfer of intellectualproperty. In Russia most of the new foreignbrand entrants, except for Renaultand Fiat, are going it alone. Both �rmswooed AvtoVAZ when others decided togive the Russian carmaker a wide berth.Although Fiat lost that contest, it hasteamed up with another local company,Severstal Auto.

The third lesson is that local conditionsand local tastes must be catered for whenadapting existing models that have donewell in mature markets. In Brazil and Indiathat has meant building small, fuele�cient cars that are also spacious and ruggedenough to withstand bad roads and someof the world’s most vicious speed bumps.In China it has meant indulging newly af�uent and highly statusconscious customers who like biggish saloons with smart interiors and lots of gadgets but are less

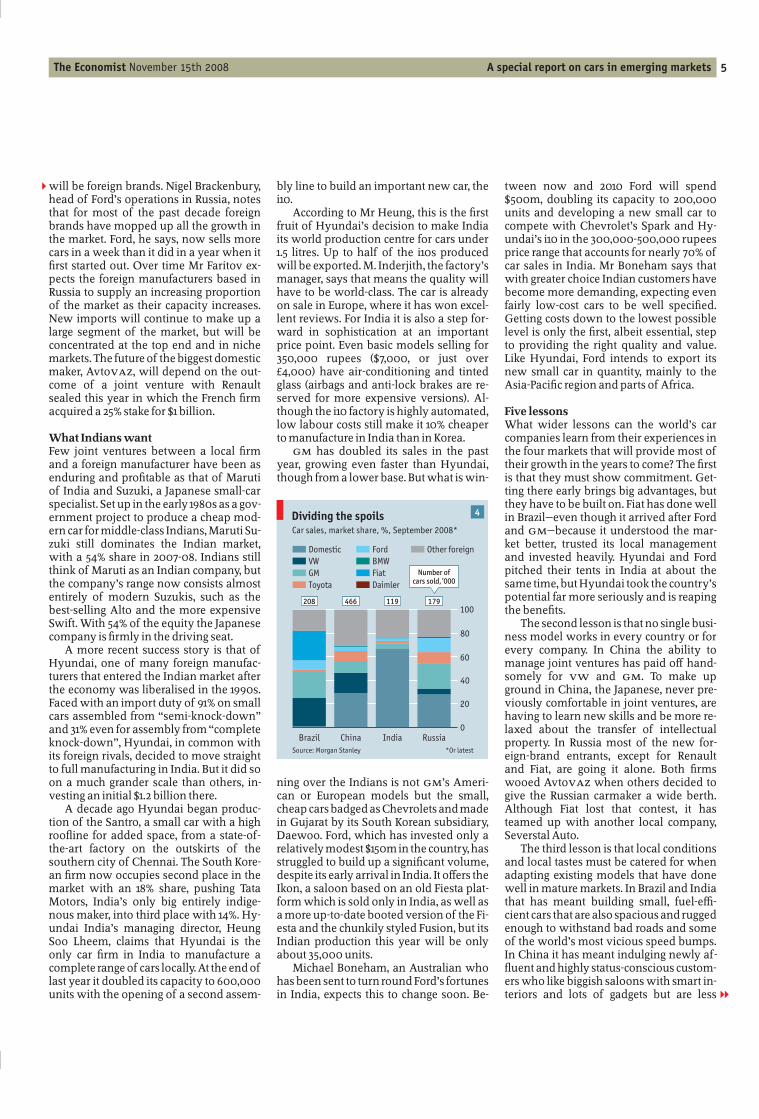

4Dividing the spoils

Source: Morgan Stanley *Or latest

Car sales, market share, %, September 2008*

0

20

40

60

80

100

Brazil China India Russia

Domestic

VW

GM

Toyota

Ford

BMW

Other foreign

Fiat

Daimler

Number ofcars sold, ’000

208 466 119 179

6 A special report on cars in emerging markets The Economist November 15th 2008

2

1

interested in performance because thereare few decent roads outside the big cities.Russians, for their part, love SUVs in allshapes and sizes. Even though most owners never leave Moscow or St Petersburg,they like the idea of a goanywhere vehiclethat can take Russian winters in its stride.

The fourth lesson is that although theirtastes may di�er, BRIC customers are nolonger prepared to put up with outdated orinferior o�erings unless they are very

cheap indeed, like the Fiat Mille in Brazil orthe Maruti 800 in India. Specialist magazines, the internet and, above all, increasing competition among the manufacturershave greatly raised buyers’ expectations injust a few years.

The �nal lesson is not to get carriedaway by big numbers. Although it seemsalmost certain that sales will grow on ascale never seen before, the sheer intensityof the competition may make large pro�ts

elusive. China is already on the verge ofpro�tless growth. Last year average pricesfell by 5.7% and now a new wave of pricecutting is under way to boost �agging demand. Dealers in China increasingly depend on �nancial contributions from themanufacturers to make any money onsales of new cars. As Sergio Marchionne,the boss of Fiat, recently remarked: �Whenit comes to China you’re either damned ifyou do or damned if you don’t.� 7

RATAN TATA may be the patriarch of Indian business and head of the sprawl

ing conglomerate that bears the familyname, but few doubt that his �rst love isTata Motors. The company dominates theIndian commercialvehicle market, produced India’s �rst entirely indigenousmodern car and has captured the world’simagination with the Nano�the onelakh(100,000 rupee, $2,500) �people’s car�.

Sitting in his o�ce on the top �oor ofthe building in central Mumbai fromwhich he controls his empire, Mr Tata recalls what brought him into the car business a decade ago. In the era known as the�Licence Raj�, from independence in 1947until 1990, when India attempted to operate a planned economy, the Indian car industry was su�ocated by red tape. Untilthe birth of Maruti in the 1980s the marketwas supplied by just two manufacturers:Hindustan, which made a version of the1950s Morris Oxford, and Premiere, whichproduced the similarly elderly Fiat 1100.

Hindustan and Premiere were licensedto make just 50,000 cars a year betweenthem. Imports, other than personal ones,were virtually unknown. If the companiesexceeded their licence quotas they couldbe prosecuted and �ned. �These two �rmswere able to keep everyone else out of themarket. If you wanted a car, you had towait for seven years,� says Mr Tata. Whenthe governmentbacked Maruti appearedon the scene, it applied for a licence tomake 150,000 cars a year, which at the timeseemed a huge number. O�ering India its�rst modern car for 30 years, Maruti quickly became preeminent in the mid1980s.

As the market was gradually liberalised, Tata found itself courted �rst byHonda and then by VW and Toyota. But in

stead Mr Tata decided that Tata Engineering and Locomotive Company (Telco), theforerunner of Tata Motors, should developand manufacture its own car, believingthat Telco had the scale and the knowledgenot to depend on a jointventure partner.

The aim was to produce a vehicle withthe internal dimensions of the stately Ambassador (because most Indian carowners have drivers and sit in the back) and thefuele�ciency of the Maruti 800. The result was the Tata Indica, a modern hatchback with a diesel engine, styled by IDEA

in Italy. Launched in January 1999 in themiddle of a recession, the Indica soon established itself as the market leader in itsprice band, despite some early quality problems. Ravi Kant, Tata Motors’ managingdirector, concedes that �as a �rst attempt itwas OK, but there were weaknesses in �nish and handling that needed improving.�

Now approaching its 10th birthday, theIndica, in all its versions, has sold nearly1.4m units and is still the secondbiggestselling car in India. Yet despite its competitive price the car is beginning to slip behind newer rivals, such as Hyundai’s i10and the more expensive Maruti SuzukiSwift. Tata’s answer is the recentlylaunched Indica Vista, a bigger, more sophisticated car built on an allnew platform and available with Fiat’s advancedmultijet diesel engine.

Mr Kant describes the Vista as a quantum leap that Tata had to make to competewith the foreign brands as they introducemore cars in the important 300,000500,000 rupee price band. He also believes that the Vista is good enough to appeal to budgetconscious buyers in Europe.Early reviews have been positive, but Tatawill have to work hard to come closer to

the build quality of its South Korean, Japanese and European rivals and still beatthem on value.

The modern factory in Pune where theVista is assembled is noticeably less automated than Hyundai’s Chennai facilitywhere, for example, bodywelding is carried out almost exclusively by robots. Tatareckons that because of relatively low Indian wages it is still worth doing certainthings manually that would be automatedelsewhere. But it means that more than20% of the cars made by Tata require somerecti�cation before they leave the factory,against under 5% of Hyundai’s i10s.

The joys of joint venturesIf India has only one fully indigenous carmaker that competes with the world’sgiants, China has perhaps as many as �vethat see themselves as potential rivals tothe foreign brands which last year tookmore than 70% of the Chinese passengercar market. Mr Ghosn of the RenaultNissan alliance says that in a country with amanufacturing base as strong as China’s itis �abnormal� for foreign �rms to be sodominant and that �at least one� Chinesemaker will become a big force with a market share of around 20%. Yet predictingwho will be the winners in this huge market is not easy.

The Chinese car industry began to takeshape in the mid1980s as the economic reforms of Deng Xiaoping gathered pace andthe country opened for business with therest of the world. Until then the country’smotor industry had concentrated almostentirely on trucks and buses. When Maodied in 1976, vehicle production was running at about 150,000 a year. First AutoWorks (FAW), the country’s biggest maker,

The home team

Indigenous carmakers are working their way up

The Economist November 15th 2008 A special report on cars in emerging markets 7

2

1

had been producing Hongqi (Red Flag) limousines for party bigwigs since the late1950s, and Shanghai Auto Works turnedout the slightly smaller Shanghai SH760

saloon for less important o�cials. Neitherchanged much during its 30year production run. In the absence of any competition they did not need to.

The arrival of VW and then GM asjointventure partners for the stateownedFAW and for Shanghai Tractor and Automotive (today’s Shanghai Automotive Industry Corporation, or SAIC) marked thestart of a new era. The bargain was that inexchange for access to the vast Chinesemarket the foreigners would supply the investment and knowhow to create a modern car industry from the scorched remains of the Great Leap Forward and theCultural Revolution.

The success of those �rst joint venturesprompted a stampede of the world’s otherbig carmakers to form partnerships in China. The terms were largely dictated by theChinese government, which knows fullwell that there are a dozen big car manufacturers but only one Chinese market. Every foreign manufacturer has been prodded into creating and expanding localtechnical centres, partly to modify Western and Japanese designs for the Chinesemarket but also to train Chinese engineersand speed up the transfer of both productand manufacturing technology.

Since only China’s big �ve carmakers(SAIC, FAW, Dongfeng, ChangAn andChery) have the heft to be e�ective partners for the big international car �rms,there has been some doubling up. For example, SAIC works with both VW and

GM; FAW with VW and Toyota; Dongfengwith Nissan, PSA PeugeotCitroën, Kia andHonda; and ChangAn with Suzuki, Fordand Mazda (which is 34% owned by Ford).This has allowed the Chinese companiesto play one partner o� against anotherwhen they were not getting exactly whatthey wanted.

Doing their own thingIt is clear that one of the things they want isto be fullrange carmakers in their ownright. At this year’s Beijing motor showDongfeng, which is investing $1.3 billion ina new R&D centre and a factory in Wuhanwith an eventual capacity of 333,000 unitsa year, displayed its �rst ownbranded car,the Jingyi, a crisply styled compact minivan that looks a bit like Renault’s Scenic.

FAW, recognising that its old Red Flagbrand may not be quite right for the times,has started building a range of vehicles under the name Besturn. It already has a largish saloon that competes with the BuickRegal and will be introducing a clutch ofnew models over the next year or so, including a smaller saloon and an SUV. FAW

is planning a model lineup that runs fromsmall to luxury cars. One of those cars willbe a version of the highly successful �rstgeneration Yaris. FAW has committed$1.83 billion to developing the vehicles between now and 2015.

SAIC has taken a slightly di�erent path.In 2004, as part of negotiations to try tosave the nowdefunct MG Rover from collapse, it acquired the intellectualpropertyrights to most of the formerly BMWowned Birminghambased company’stechnology. At about the same time it did a

deal with a British automotive consultancy, Ricardo, to set up an R&D operation inChina. The �rst fruit of SAIC’s British connection was the Roewe 750, an updatedversion of the Rover 75 (Ford, then ownerof Land Rover, refused SAIC permission touse the Rover brand) that was launchedtwo years ago.

Since then, with strong government encouragement, it has acquired China’s oldest car �rm, the much smaller cashstrapped Nanjing Auto, which had boughtRover’s MG brand, some blueprints andthe factory where the MG roadster wasbuilt. SAIC is now building the ageingsports car in Birmingham again and haskept Nanjing’s MG version of the Rover 75going, perhaps to sell in export markets.

SAIC’s latest car, the handsome Roewe550, developed from MG Rover plans withhelp from Ricardo, made its debut at theBeijing show earlier this year. Althoughpowered by the slightly longinthetoothRover Kseries engines, the 550 is the �rstChinese car that might appeal to Europeantastes. And being built on a cutdown version of the impressively strong 75’s platform, it should stand up well to crash tests,which is more than can be said for some ofthe other Chinese hopefuls.

Among China’s horde of independentcarmakers, the most promising appear tobe Chery and Geely. At the Beijing motorshow Geely showed 23 di�erent vehicles(including a bizarrely modi�ed Londontaxi), 13 of them entirely new designs. The�rm, which sold 220,000 units last year, isdeveloping no fewer than �ve new platforms and says it will launch 42 new models between now and 2015. By then, says itsvicepresident, Frank Zhao, Geely willhave the capacity to turn out 1.7m cars ayear from nine di�erent factories in Chinaand more from overseas plants, probablyin Mexico, South Africa, Indonesia, Ukraine and Russia.

Geely su�ered a setback to its worldconquering plans when a Russian car magazine crashtested a Geely CK small saloonat 64kph (40mph). Both driver and passenger were given a survival chance of only10%, dashing hopes that exports to America might begin in late 2007. Geely still talksbullishly about launching in America by2010, but 2013 now seems more realistic.

Chery, Geely’s bigger but less brash rival for the title of local hero, recognises thatbefore it can sell cars in developed countries it needs to do much more work.�North America and Europe have very demanding safety and emission laws thatour vehicles do not meet yet,� says Yin Time for Cherypicking

8 A special report on cars in emerging markets The Economist November 15th 2008

2

1

Tongyao, the company’s president. Part ofthe problem, he says, is the quality of theChinese suppliers of components thatChery has depended on: �It is improving,but it is still not as good as it should be.�The answer may be to buy more from thebig global partsmakers. Several of themhave set up shop near Chery’s Wuhu baseand established joint ventures in the hopeof pro�ting from the �rm’s future growth.

The shortcomings identi�ed by Mr Yinundermined a deal with Chrysler last yearto help the troubled American �rm build amuchneeded small car for the Americanmarket. Chrysler subsequently turned toNissan, but Chery will supply a Chryslerbadged small saloon for Latin America.Most recently Chery has signed an agreement with Fiat, left without a partner inChina after SAIC’s takeover of Nanjing, toassemble kits of the Linea, Grande Puntoand Alfa 159 from next year.

This summer Chery announced itwould soon start building a fourth factorywith an annual capacity of 200,000 cars.That will bring its total capacity to 850,000units by 2010, making it one of the biggestmanufacturers in the country. This year itexpects to sell nearly 500,000 cars in China and has started to introduce a wave ofnew models to keep customers interested.

Last year China’s homegrown brandstook 29% of the market, increasing theirshare by only one point over the previousyear. That was partly because the independent carmakers’ o�erings were largelysmall and cheap at a time when statushungry buyers were turning increasinglyto bigger cars. Sales of luxury cars increased by 35% and those of SUVs by 50%,whereas sales of small cars rose by only4%. But another reason was that the Chinese still look down on their nativebrands, often with good cause. Still, thingsare changing. Government o�cials talk ofChinese domestic brands taking up to 60%of the market in a few years’ time.

For the moment that seems like wishfulthinking. But the Chinese are learning fastand rapidly gaining scale. Cynics say thatthe foreign makers have never been morethan a means to an end, and once theyhave served their purpose the market willslowly be stacked against them.

They are probably wrong. China is conscious of its obligations as a member of theWorld Trade Organisation, and Chineseconsumers are brand snobs who increasingly expect to be able to buy the best. Yetwith its gigantic home market and a supportive government (which directly or indirectly owns most Chinese car �rms), it

would be surprising if in ten years’ timeChina did not have at least a couple of car�rms competing on equal terms with theworld’s giants.

By contrast, the chances of any Russiancarmaker becoming a global force are remote. In 1990 Russian car manufacturersproduced 1.2m passenger vehicles. Lastyear they sold just 756,000.

Bearish outlookGorkybased Gaz, maker of the big, toughVolga saloons beloved by Soviet o�cialdom (which are still being produced), hasjust started building the more modernVolga Siber, based on the platform of theprevious Chrysler Sebring. However, Gazsees its future not so much in cars as inheavy trucks, buses and light commercialvehicles. Severstal Auto, which makes theSovietera UAZ Hunter 4x4 as well as somemore modern utility vehicles and a rangeof truck engines, has reached a similar conclusion. Although it assembles SsangYongSUVs under licence from the South Koreanmaker and has a joint venture with Fiat toproduce its Albea and Linea sedans, itthinks commercial vehicles are a safer bet.

AvtoVAZ, which owns Lada and makesmore than 90% of Russianbranded cars,has had a torrid recent history. In the 1990sit became a byword for the gangsterismthat characterised much of postSovietRussian capitalism. Many of the �rm’sdealers operated as a criminal network,buying cars cheaply, paying late and selling them to Russian consumers at a hugemarkup. AvtoVAZ managers were well rewarded for their cooperation. Criminalgangs roamed the factory, removing �nished cars from the assembly line and delivering them to shadowy third parties.Dealers who refused to participate in thescam would �nd the cars they receivedhad been vandalised. There were frequentshootouts at the giant Togliatti factorybuilt with Fiat’s help in the 1960s. Since

1992 over 500 people associated with AvtoVAZ have been murdered.

By 2005 the Putin government had hadenough. It got the stateowned armsexport company, Rosoboronexport, to buy acontrolling stake in the car �rm for $700m.AvtoVAZ’s ownership remains tangled,but in e�ect the company was renationalised. Rosoboronexport’s boss, Sergei Chemezov, an old KGB friend of Mr Putin’s,turned up in Togliatti with 300 heavilyarmed policemen to seize control of thefactory and replace the management withKremlin trusties.

Mr Chemezov may not have knownmuch about the car business, but he andhis chief executive, Boris Alyoshin, appearto have brought some stability to AvtoVAZ

and cleaned it up su�ciently to lure MrGhosn’s Renault into taking a stake of justover 25% in the business earlier this year.As part of the $1 billion deal, Renault hascommitted itself to help turn AvtoVAZ intoa modern car company. Senior Renaultmanagers, including some of those whocontributed to the revival of Nissan’s fortunes, have been arriving at Togliatti sinceMarch. Mr Ghosn is also one of three Renault executives on the AvtoVAZ board.

Mr Ghosn says this is a relationship�whose time has de�nitely come�. He believes that it will give Renault access to capacity that it would otherwise have had tobuild expensively for itself, as well as to thelarge (and supposedly decriminalised) AvtoVAZ dealer network that stretches acrossthe country’s 11 time zones. Mr Chemezovsays that Renault will bring modern technology and knowhow, and Mr Alyoshinreckons that with Renault’s help a sales target of 2m units may not be too far away.

With its long experience of workingwithin an automotive alliance, Renault isprobably the best partner the ailing Russian �rm could have found. But the task isdaunting. AvtoVAZ’s share of the Russianmarket is in rapid retreat. When Mr Che

A Lada for all seasons

The Economist November 15th 2008 A special report on cars in emerging markets 9

2 mezov arrived, it was 37%; this year, withluck, it may remain at 20%. Ladas, both theold Fiat 125based �Classic� and the newerbut still substandard Samara, have continued to sell in provincial Russia because thecars are very cheap, lots of dealers sellthem and there are still few alternatives.

One big threat to the Lada is the incipient invasion of lowpriced locally assembled Chinese cars. Several Chinese companies have applied for licences to buildassembly plants in Russia, but so far onlyChery has been given the goahead,whereas Western or Japanese �rms havenever been refused. This is not because theChinese do not meet Russian safety standards, as is sometimes argued, but becausethe Chinese compete with AvtoVAZ onprice. In the longer run such discrimination may not be sustainable.

The second threat is that the dynamicsof the usedcar market are about to changeagain. AvtoVAZ was given a breathingspace in 2002 when the government imposed heavy import duties on used carscoming from Japan and Europe, and wasalso helped by an 18% valueadded tax lev

ied on all used sales through dealers. Aftermuch lobbying by the car industry the government appears ready to lift that tax soon.With ever larger numbers of highqualityRussianbuilt foreignbrand cars likely tocome on to the secondhand market in theyears ahead, much of Lada’s price advantage will disappear.

Renault says it aims to launch a succession of new Ladas using its lowcost Loganbased platforms that will be competitively priced and o�er much higher qualitythan AvtoVAZ does at present. The �rstshould reach the market by 2010. Yann Vincent, a Renault executive who is now thechief operating o�cer at Togliatti, says thatof the four assembly lines at the rundownfactory only one is usable; the other threeare obsolete. Though he does not say so,the factory is also extraordinarily ine�cient. It needs 104,000 people to maintainits current production of around 700,000vehicles a year. For comparison, about10,000 workers will produce up to400,000 cars at Renault’s Dacia factory inRomania next year.

Nor is it just a matter of bringing in new

machines. The biggest problem, accordingto Mr Vincent, is the supply of components. Most Lada parts are shoddily madeinhouse; others are brought in from Latviamore than 1,200 miles away. Patrick Pelata,a veteran of the Nissan turnaround, sayshe wants to attract �global parts suppliers�to Togliatti. He hopes that within �ve years95% of the parts for �LoganLadas� will bemade locally.

Renault’s involvement should ensurethat AvtoVAZ can avoid a collapse in salesand output. But Eduard Faritov of Renaissance Capital, who has studied the �rm’sprospects, thinks that AvtoVAZ will haveto run hard just to stand still. Intensifyingcompetition combined with rising safetyand environmental standards will pushmost of today’s Ladas out of the marketand shorten the life cycle of new models.He forecasts that by 2015, although AvtoVAZ will still be selling around the samenumber of cars as it does today, its marketshare will have fallen to 11%. Not even theresurgence of Russian nationalism, itseems, can save the country’s last important carmaker from its steady decline. 7

WHEN in 1999 Renault spent $50m toacquire a controlling stake in Dacia, a

sickly Romanian carmaker formerlyowned by the state, it was unimaginablethat it would become one of the jewels inthe French car �rm’s crown. This year, at itsfactory in Pitesti, not far from Bucharest,Dacia will churn out more than 300,000RenaultDacia Logan saloons and its cousins. In 2009 the number is expected to riseto 400,000, including kits exported to other Renault assembly plants. Five monthsago the millionth Logan since its launch in2004 rolled o� the line. The chances arethat it was a car from Pitesti, the Logan’s�mother plant�, but it could have comefrom any one of seven other productionsites in Russia, India, Iran (with two), Morocco, Brazil or Colombia.

Conceived as a lowcost car for emerging markets, the boxylooking Logan hasbecome one of Renault’s most pro�tablevehicles. Whereas Renault’s marginsacross its range are an anaemic 3%, the Logan earns at least twice as much. By 2010Renault expects to be making more than a

million Logans a year, despite its failure to�nd a partner in China to build them. Nowonder most global manufacturers arejostling to get into the lowcost game.

But what exactly is a lowcost car? MarkBursa, the emergingmarkets commentator of Justauto, a carindustry website, argues that the term can include anythingfrom Fiat’s rather upmarket Linea saloon

and the Logan to �legacy� cheapies such asthe ancient Lada Zighuli and the Maruti800, a �veyearold VW Golf or Tata’s innovative �onelakh car�, the Nano. Butused cars imported by poor countries fromrich ones become expensive whenweighed down with high duties and taxesto protect indigenous industries. And MrBursa acknowledges that cars such as the

Pile them high

The cheapandcheerful end of the market

5Future perfect

Source: A.T. Kearney *2007 estimates based on cars in range $3,100-$7,800

Low-cost cars*, forecast global sales, m

0

5

10

15

20

2007 08 09 10 11 12 13 14 15 16 17 18 19 20

Rest of world

South America

India

Africa

Rest of Asia

China

1

10 A special report on cars in emerging markets The Economist November 15th 2008

2

1

Lada and the Maruti, both based on 40yearold designs, will not be rolling o� theproduction lines for much longer. They arecheap because all the investment to makethem was written o� long ago, but they�nd it increasingly hard to comply withevertightening emissions laws and safetyregulations. Fiat’s Mille, sold in Brazil,which evolved from the Uno of the early1980s, has a clean �exfuel engine, but thecompany accepts that there is little that canbe done to make it safer in a crash and isworking on a successor.

The genuinely lowcost cars of todayare those, like the Logan, that were designed from the outset to come close to thestandards of their manufacturers’ latestmainstream models but to be much cheaper to develop and make. The Nano is in adi�erent category, of which more later.

Although Renault has earned considerable kudos for having made a success ofthe Logan, the real pioneer was Fiat with itsProject 178, born at the beginning of the1990s. With the collapse of the Soviet Union and the opening up of India and China, Fiat reckoned it could use its experienceof the Brazilian market to develop a rangeof tough, inexpensive but modern carsthat could be built and sold almost anywhere in the world. The results were thePalio hatchback, the Siena saloon, alsoknown as the Albea, an estate car and apickup. The cars have been a success inBrazil and the Albea has also done well inTurkey, but neither made the expected impact in Russia or China. Fiat says that it haslearnt valuable lessons which it has applied to the Linea and the allnew successor platform to the 178, due next year.

The lure of the LoganHowever, it is the Logan that has come tobe seen as the �rst lowcost world car. Likethe Palio, the Logan uses a strengthenedand stretched version of an existing smallcar platform, but Renault had a morerounded strategy than Fiat did in the 1990s.It set out to build a car that could sell for$6,000 by keeping down developmentcosts and taking almost everything thatwould go into the car from existing or earlier models. Renault also made the Logancheap to produce by keeping it simple (forexample, its dashboard is a onepiecemoulding). Most of the machinery at Pitesti is refurbished kit from Renault’s factories in France. Research by DeutscheBank in 2005 suggested that productioncosts of the Logan were less than half thoseof a standard European compact car. MrBursa reckons that as volume has in

creased, bringing greater economies ofscale, the comparison may now be evenmore favourable.

In some ways even Renault has beensurprised by the car’s success. For example,it has had an enthusiastic reception inwestern Europe, where it is sold as a Dacia.Its spaciousness, rugged build and relativesimplicity appeal to buyers who prefer awellpriced new vehicle to a secondhandone. A second, and even more welcome,surprise has been that the Logan hasachieved its planned volume without having to be sold at a price anywhere near aslow as the frugal $6,000 it was designedfor. Renault claims the average selling priceis nearer to $9,000, and in Europe almost$13,000 because buyers want extras suchas airconditioning, electric windows andantilock brakes.

How long Renault will be able to go onmaking such a handsome pro�t from theLogan is debatable. Its market is growingby leaps and bounds. According to RL Polk,a marketresearch �rm, sales of cars below$14,000 will grow by 70% in the next nineyears, compared with an increase of 30%for all vehicles. And Robert Bosch, a components supplier, forecasts that sales ofcars priced at $10,000 or less will havegrown to 10m by 2010, making up about13% of the world market. But other makersare getting ready to crash Renault’s party.

Toyota’s eagerly awaited lowcost competitor, known as EFC (Entry Family Car),is expected to make its debut in 2010. Littleis known about the EFC, but it is thought tohave a target price of $6,500 and is likely tobe built in both Brazil and India to startwith. Toyota’s boss, Katsuaki Watanabe,says he is using the EFC project to bringabout a revolution in manufacturing e�ciency at the already famously lean Japanese �rm.

Around the same time Fiat’s successor

to the Palio/Siena should also have surfaced. Meanwhile GM is using its South Korean subsidiary, Daewoo, to develop a carwhich it hopes will be even cheaper thanthe EFC. To meet the challenge, Renault isaiming to get its nextgeneration lowcostcar ready by 2011, although the Logan islikely to continue in production for a whileafter that. According to Gerard Detourbet,the head of the Logan programme, the Logan’s successor will be bigger, betterlooking and even cheaper. It may need to be.

What it will not be is competition to theTata Nano. Ratan Tata, the boss of the Tatagroup and the driving force behind theNano, says that he was �amused� to discover that when the Logan went on sale inIndia last year the price of the basic modelwas around 500,000 rupees (nearly$11,000). �It was just another car,� says MrTata sni�ly. Nobody could say that of theNano. Conceived by Mr Tata �ve years agoas a safer and more comfortable alternative to transporting a family of four on asmall twowheeler, a common sight on Indian roads, he was determined to price ithalfway between a motorcycle and India’s cheapest new car, the venerable Maruti 800. Mr Tata later promised that theNano would be a real car that could bebought for just one lakh (about $2,500)�acommitment he triumphantly honouredwhen the little jellybeanshaped car wasrevealed at the Delhi motor show in January this year.

A legend before its lifetimeThe Nano is not just very cheap; to be socheap it also has to be very clever. Mr Tata,who remained closely involved with theenthusiastic young development teamduring the car’s gestation, says there werethree possible ways they could have gone:work down from a car design, work upfrom a scooter or start with a clean sheet ofpaper. By going for the third option, Tatahas created a new template for developingultralowcost cars that others will almostcertainly have to follow.

The Nano team, led by Girish Wagh,says that one of the keys to success wasthat they were ready to try di�erent ideasand accept that some of them might notwork. The team even asked whether therewas a need for doors and whether plasticinstead of steel could be used for the bodywork. According to Mr Tata, the answerswere respectively yes and no. The overalloutcome was a culture de�ned by frugalityand a willingness to challenge convention,dubbed �Gandhian engineering�.

The Nano’s body was completely rede

Ratan’s baby

The Economist November 15th 2008 A special report on cars in emerging markets 11

2

1

signed twice and the engine three times. Acritical decision was to simplify assemblyby mounting the engine, exhaust systemand gearbox in a single module in thespace behind the rear seats. Indeed most ofthe car is broken down into modules thatcan easily be assembled from kits. Mr Tatahopes to �create entrepreneurs across thecountry that would assemble the car�.Costs were shaved by keeping everythinglight and simple. The car has only onewindscreen wiper; its wheels are held onby three bolts, not four; the steering column is hollow; instead of longlife head

light bulbs designed to last ten years,cheaper bulbs are �tted that can be easilyreplaced. Even the number of tools neededto make the car was cut down.

Suppliers were urged to adopt the samefrugal engineering. Some concluded thatthe cost goals were just too onerous andwalked away. Others, such as Lumax Industries, an Indian automotive lightingspecialist, was pleased to be involved fromthe outset of the project. According to Deepak Jain, the chairman of Lumax, �the opportunity to work on this car gave our engineers the chance to showcase their skill.

Because most other car products are designed abroad, we just have to manufacture components to a speci�c blueprint. Inthis project we designed light �xtures thatmeet all regulatory needs, �t the car andare lowcost.� Perhaps more surprisingly,Robert Bosch, the world’s biggest components company, agreed to supply astrippeddown version of its Motronic enginemanagement system.

The immediate prospects for the Nanohave been somewhat clouded by two developments. First, the steep climb in pricesof raw materials, especially steel and poly

THE morning rush hour in the southernIndian city of Chennai (formerly Ma

dras) is much like those in other big SouthEast Asian towns. A throng of mostlysmall cars hoot and jostle in a race againstthreewheeled autorickshaws, dilapidated buses, fumebelching lorries and theodd bullock cart. But the real kings ofthese roads are the hordes of commutermotorcycles that swarm in and out of thechoking tra�c at daredevil speed.

Asia is home to nearly 80% of theworld’s 315m motorcycles. About 45m ofthose are in India, the region’s secondbiggest �eet after China, with more than100m. Sales of twowheelers in India arerunning at about 7m a year, outstrippingthose of cars by nearly �ve to one. Noteven one in a hundred Indians owns a car,but one in 20 owns a twowheeler.

The TVS group has a foot in both thecar industry, as one of India’s most successful makers of automotive components, and the motorcycle business,through TVS Motors, the country’s thirdlargest manufacturer of twowheelers,with a 16% market share. Venu Srinivasan,the autocratic chairman of TVS, which isfamilycontrolled, still sees plenty of potential for growth in the Indian motorcycle market. After a slight contraction lastyear because of tighter credit, business appears to be picking up again.

Among Mr Srinivasan’s reasons for optimism are the much greater levels ofownership in other South Asian countrieswhere income levels are higher, such asMalaysia, Thailand and Indonesia (where

TVS has recently opened a factory that canbuild 300,000 units a year). In Thailand,for example, more than a quarter of thepopulation owns a twowheeler. Most developing countries �nd that when GDP

per person reaches about $5,000, motorcycle sales begin to decline as peopleswitch to cars. Thailand has nearlyreached that point, but India is only abouthalfway there.

The dominance of two over fourwheels is explained mostly by cost. Untilthe arrival of the Tata Nano the cheapestnew car on sale in India had been the$5,000 Maruti 800, whereas the relativelysmall motorcycles that account for 85% ofthe Indian twowheel market sell for$800$1,500. Petrol in India is also expensive by developingcountry standards.Even the lightweight Nano is unlikely todo better than 60 miles per gallon, where

as some of TVS’s machines will do about190mpg, says Mr Srinivasan. Maintenance, too, is much cheaper than for cars,and bikes can cope more easily both withpoor roads and with congestion.

Since breaking with Suzuki, its jointventure partner, in 2001, TVS has been theonly big Indian motorcycle manufacturerto rely entirely on its own designs (themarket leader is Hero Honda with a 47%share, and Kawasaki is a technologypartner of secondplaced Bajaj). As Mr Srinivasan sees it, parting from Suzuki hasgiven TVS the freedom to design productsthat are suitable for the local market butalso to build an export presence. By 2013,he says, 40% of TVS’s sales will be outsideIndia. He reckons that Indian motorcycleshave an advantage over Chinese rivals incountries with poor infrastructure because they are more heavily built: �Ourbikes cope with the worst roads and oftenhave to carry three people. Chinese quality is not as good.�

TVS’s pristine factory at Hosur outsideBangalore (one of three in India) with itsimpressively disciplined workforce suggests that there is nothing wrong with theway the company makes its bikes. Keeping pace with the technology of its twoheavyweight rivals may be more of achallenge. Mr Srinivasan concedes thatTVS lost market share last year becausesome of its products were �not so good�.Seven new bikes launched in Septembershould help to �x that, but �there is nosuch thing as patriotic buying here, andHonda just keeps grinding away.�

Cheaper than four wheels, better than two feetKings of the road

An eye on the competition

12 A special report on cars in emerging markets The Economist November 15th 2008

2

1

propylene (used to make plastic), after thecar was unveiled in January raised fearsthat Tata might lose up to $90 on every basic $2,500 Nano it sold. An analysis by A.T.Kearney, a consulting �rm, suggested thatthe cost of producing the little car had risenby about $165. But those fears have eased alittle in the past month or so as commodityprices have fallen back in response to adrop in global demand.

The onelakh bindThe second, and more serious, setback hasbeen the decision to abandon the factorybuilt specially for the Nano in Singur, WestBengal. Violent protests by farmers overthe state’s forced purchase of their land forthe 1,000acre site, at prices they said werebelow market value, left Tata with an invidious choice: negotiate directly with thefarmers and buy them o�, or walk away.

On October 7th Mr Tata con�rmed thatproduction of the Nano, and the 10,000jobs that went with it, would be moved toa new site in Gujarat where, crucially, thestate government already owned the land.Tata is thinking of shifting some of the initial production to its existing factories inPune or Pantnagar, but even so the Nano’slaunch will now be delayed until early2009. Once under way, however, production at the new factory will quickly climbto 250,000 a year and can be expanded to500,000 a year.

Mr Tata is clearly distressed by what hashappened. He says that bringing the$400m Nano investment to West Bengal

was �a leap of faith� intended to bring thecar industry back to a state that had beenstarved of investment because of its history of leftwing politics. Impressed by thestate’s businessfriendly chief minister,Buddhadeb Bhattacharjee, Mr Tata hopedthat other �rms would follow his lead incoming to West Bengal. Now they are morelikely to stay away.

It should be possible to move all themachine tooling from Singur, albeit at considerable expense and disruption for Tata,as well as for the suppliers who were setting up nearby. Mr Tata concedes that �wewill limp initially, and at a higher cost.�Ravi Kant, managing director of Tata Motors, hopes that any additional costs fromdearer raw materials and the exodus fromSingur will be compensated for by mostcustomers opting for the highermargin,pricier �de luxe� Nano that comes with airconditioning, electric windows and littlealloy wheels.

In the longer term, the Nano’s successwill depend on how people react to the carand whether Mr Tata is right that there is abig gap between what he calls �the lowend of the car market and the high end ofthe twowheel market�.

A handful of sneak reports on what theNano is like to drive are already circulatingon the web. They suggest that the goal ofmaking a �proper� car has been achieved.Although noisy, the tiny 32bhp engine provides enough pu� to reach the claimedmaximum speed of about 60mph. Despitethe tall roof and the weight carried over

the rear wheels, the Nano handles quitepredictably and is particularly nimble atcity speeds. Given its tiny size it is astonishingly spacious inside and comfortablyseats �ve people. The interior plastics andthe �ttings look cheap, but then the car ischeap. However, the overall feeling of �imsiness is harder to shrug o�. Still, Mr Tatasays the Nano has been engineered to passa variety of crash tests.

The potential market could be huge.Sales of twowheelers in India are runningat about 7m a year (see box, previous page).Although it will be more expensive to buyand run than a motorcycle, the Nano o�ersa new way for people on relatively low incomes to become carowners. A.T. Kearneyforecasts that sales of cars in India and therest of Asia (but excluding China) priced at$3,1007,800 will reach 10.5m by 2020. MrTata thinks that the Nano could quitequickly sell between 500,000 and 1m ayear in India alone.

For now, most of the top brass at the global car �rms are just watching and waitingto see whether Tata can pull it o�. The oneexception is Carlos Ghosn. Renault hasformed a joint venture with Bajaj, thePunebased maker of motorcycles andautorickshaws, to develop a car with acost base of about $2,500, which will makeit slightly more expensive than the Nano.Mr Tata says the prospect of a nearrivalfrom RenaultBajaj only adds to his con�dence: �Carlos was the only one in the industry who said the Nano could be done,�he says. �He was my secret motivator.� 7

UNTIL recently the biannual Beijingmotor show was a bit of a backwater,

a place where Chinese makers displayedtheir cheap but not very cheerful little carsand where the supposedly new o�eringsfrom the jointventure manufacturerswere in fact warmedup Buicks and VWsfrom a previous generation. However, thisyear’s Beijing show, the 10th, was a matchfor any of the industry’s traditional showcases, not only for its crowds and glitz butalso for the number of new cars launched,the size of the display stands and the headcount of big wheels from the global �rms.Yet there were clear warning signals too.

Foreigners �ying into Beijing, Shanghai

or Guangzhou are impressed by the wideexpressways from the modern airport terminals to their downtown hotels. Yet thejourney from the centre of Beijing to theshow in nearby Shunyi told a di�erentstory. As the fourlane highway leaving thecity narrowed to a single lane, the showbound tra�c came to a grinding halt. Anhour or so later, outside the newly built exhibition halls, chaos reigned. With nowhere to stop, coaches dumped their passengers in the middle of the road wherethey had to negotiate giant potholesturned into ponds by rain falling from aleaden, polluted sky. It made the show’sslogan��Dream, harmony, new vision��

seem not just silly but almost mocking. It is not much di�erent in the other

main emerging car markets. In the big cities where the growing wealth is most concentrated, any pleasure in car ownership iscounterbalanced by the increasing awfulness of the roads, the choking fumes andthe nearimpossibility of parking. In SãoPaulo the tra�c is relatively disciplined,but the morning and evening rush hourshave merged into one. In Mumbai peopleoften allow two or three hours to get to abusiness meeting in another part of town.In both cities the spread of slums makesany kind of rational town planning impossible. In Moscow the excellent Stalinera

The art of the possible

The question is not whether the world can cope with three billion cars�but how

The Economist November 15th 2008 A special report on cars in emerging markets 13

2

1

metro takes some of the strain, but the twobig ring roads that encircle the town areconstantly jammed.

Congestion, a mounting number oftra�c accidents and worsening air pollution are the most obvious local problemsassociated with rapidly increasing carownership. Given the will, governmentpolicies can ease some of them. In Brazilo�cial encouragement of ethanolpowered engines has had some impact on airquality in the overcrowded São Paulo area.Both China and India hope to cut the emissions that cause smog and health problems by insisting that all new cars willhave to meet the tough Euro IV standardwithin the next few years. Attitudes tosafety in most developing countries aremore casual than in the rich West, but China has been rigorously enforcing the wearing of seat belts, and consumers now expect at least a couple of airbags even infairly basic vehicles.

Seizing upCongestion is more intractable. In theory,better public transport systems, tollschemes, restrictions on registration permits and, where feasible, new �yovers andunderpasses can all help to ease urbangridlock. Developing countries with cheaplabour should also be able to �nd the resources to build plenty of new roads outside the towns. India, for instance, is in desperate need of better highways connectingbig urban centres. The �expressway� thatlinks Mumbai with Pune, an industrial citywith a population of 6m, runs straightthrough crowded villages, with tra�csometimes slowing to walking speed.About 40% of India’s road tra�c is carriedon just 2% of its roads, most of which leavemuch to be desired. As Ravi Kant of Tata

Motors puts it: �India doesn’t need fewercars; it does need more roads.�

What makes infrastructure investments in developing countries tricky ispolitics. Even in China, where agriculturalland has been ruthlessly acquired for newroads, opposition is growing. In democracies the obstacles are even greater. Mr Kantsays that in the �ve decades after independence India built almost no new roads.That changed when the probusiness Bharatiya Janata Party came to o�ce in 1999.But since a Congressled coalition tookover in 2004, roadbuilding has droppedo� again.

Yet infrastructure problems are dwarfed by the likely e�ect of a huge increase inthe worldwide number of cars on climatechanging carbon emissions and future oilprices. Research shows that $5,000 a yearis the earnings threshold at which carownership takes o�. On that basis, economists at the IMF have calculated that thenumber of cars worldwide will grow from600m in 2005 to 2.9 billion in 2050. By2030, they believe, China’s car �eet willhave overtaken America’s (which itselfwill have increased by 60%), and by 2050China will have almost as many cars as theentire world has today. India will be catching up fast, with a �eet of 367m, 45 timesthe number on its congested roads today.

Those cars will pump an immensequantity of greenhouse gases into theearth’s atmosphere. According to the 2006Stern Review on the economics of climatechange, in 2000 cars were responsible for6.3% of global CO2 emissions. If car emissions were to grow in line with ownership,by 2050 they would raise total world emissions so much that scientists believe temperatures would rise by an alarming 3°Cfrom preindustrial levels.

In practice, it is inconceivable that caremissions will increase at this sort of pace.For one thing, the growth in the world’s car�eet will put unremitting upward pressureon the price of petrol and diesel. Eventhough oil prices have more than halvedsince their midyear peak of $150 a barrel,no carmaker is willing to bet that they willnot rise again when the global economy recovers. Luckily for the car manufacturers,although higher fuel prices can make a difference to what kind of cars people buyand how much they use them, they do notdissuade them from buying cars altogether. Taxes on fuel at the pump in Britain andGermany are more than six times those inAmerica, but levels of car ownership areonly slightly lower�and might be similar ifpublic transport in Europe were as bad and

commuting distances as long as they areon the other side of the Atlantic.

For all the problems they bring, carsalso confer large social and economicbene�ts. As the IMF economists note,�mass car ownership has historically beenan integral component of the transition toan advanced economy. Workers can coverlonger distances in their daily commutes,e�ectively increasing the size of the labourmarket and facilitating specialisation inproduction; consumers can purchasegoods from shops farther from theirhomes, which results in greater competition in the retail sector; remote �shing villages can develop as tourist resorts with(mostly) positive e�ects on incomes andwelfare; and so on.� And at a more emotional level, most people simply like cars,even if the environmentalists disapprove.

A green glowBut if that yearning is to be satis�ed without destroying the planet, the cars themselves will have to change a great deal. MrGhosn of RenaultNissan reckons that theindustry has to develop vehicles with verylow or zero emissions as quickly as resources and technology will allow. It iswidely believed that the market for suchcars for the foreseeable future will be con�ned to rich countries with wellorganisedenvironmental lobbies and politicianswho want to establish green credentials�and indeed much of the pressure on thecarmakers to reduce carbon emissions iscoming from legislators in Europe and California. But two powerful forces are atwork to ensure that emerging markets willget the new clean technologies soonerrather than later.

The �rst is the global nature of the car

6The new world order

Source: IMF

Worldwide car fleet, bn

F O R E C A S T

2005 10 20 30 40 50

0

0.5

1.0

1.5

2.0

2.5

3.0

United States

Otheradvancedeconomies

China

India

Otherdevelopingeconomies

7A question of affordability

Source: EIU

GDP per person, $, 2007

0 2 4 6 8 10

Russia

Mexico

Brazil

Argentina

Thailand

Malaysia

China

Indonesia

Philippines

India

14 A special report on cars in emerging markets The Economist November 15th 2008

2

Previous special reports and a list offorthcoming ones can be found online

www.economist.com/specialreports

Future special reportsCountries and regionsRussia November 29thIndia December 13th

Business, �nance, economics and ideas The sea January 3rd 2009The future of �nance Jan 31st 2009Growth in emerging markets February 14th 2009Waste February 28th 2009

www.economist.com/rights

O�er to readersReprints of this special report are available at aprice of £3.50 plus postage and packing. A minimum order of �ve copies is required.

Corporate o�erCustomisation options on corporate orders of 100or more are available. Please contact us to discussyour requirements.

Send all orders to:

The Rights and Syndication Department26 Red Lion SquareLondon WC1R 4HQ

Tel +44 (0)20 7576 8148Fax +44 (0)20 7576 8492email: [email protected]

For more information and to order special reportsand reprints online, please visit our website