9 city rept murrieta

TRANSCRIPT

So much news, so little time. I just returned from Dr. John Husing’s forecast delivered to the EWDCentitled ‘Start of the Recovery’. You can read all 56 pages by clicking the link but I’ve included acouple charts I found most interesting. Dr. Husing’s take? There are lots of little bits of positive news– but very little bits. It’s likely to be 2012 before we start to feel ‘normal’ again as a country, and theInland Empire might even lag that a little.

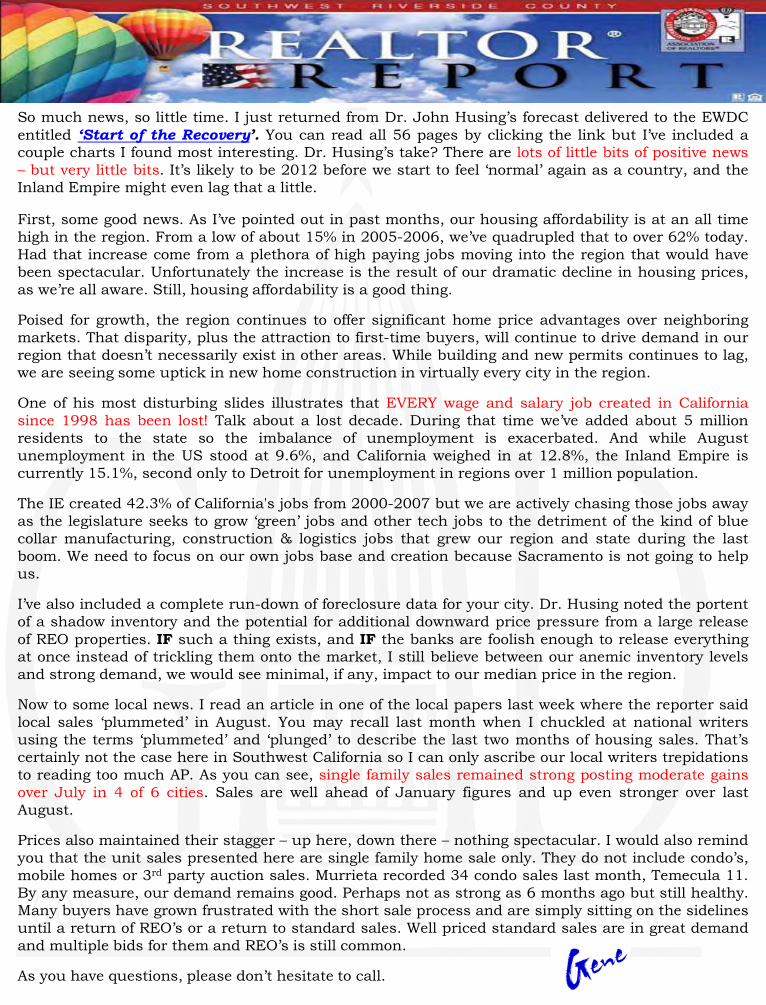

First, some good news. As I’ve pointed out in past months, our housing affordability is at an all timehigh in the region. From a low of about 15% in 2005-2006, we’ve quadrupled that to over 62% today.Had that increase come from a plethora of high paying jobs moving into the region that would havebeen spectacular. Unfortunately the increase is the result of our dramatic decline in housing prices,as we’re all aware. Still, housing affordability is a good thing.

Poised for growth, the region continues to offer significant home price advantages over neighboringmarkets. That disparity, plus the attraction to first-time buyers, will continue to drive demand in ourregion that doesn’t necessarily exist in other areas. While building and new permits continues to lag,we are seeing some uptick in new home construction in virtually every city in the region.

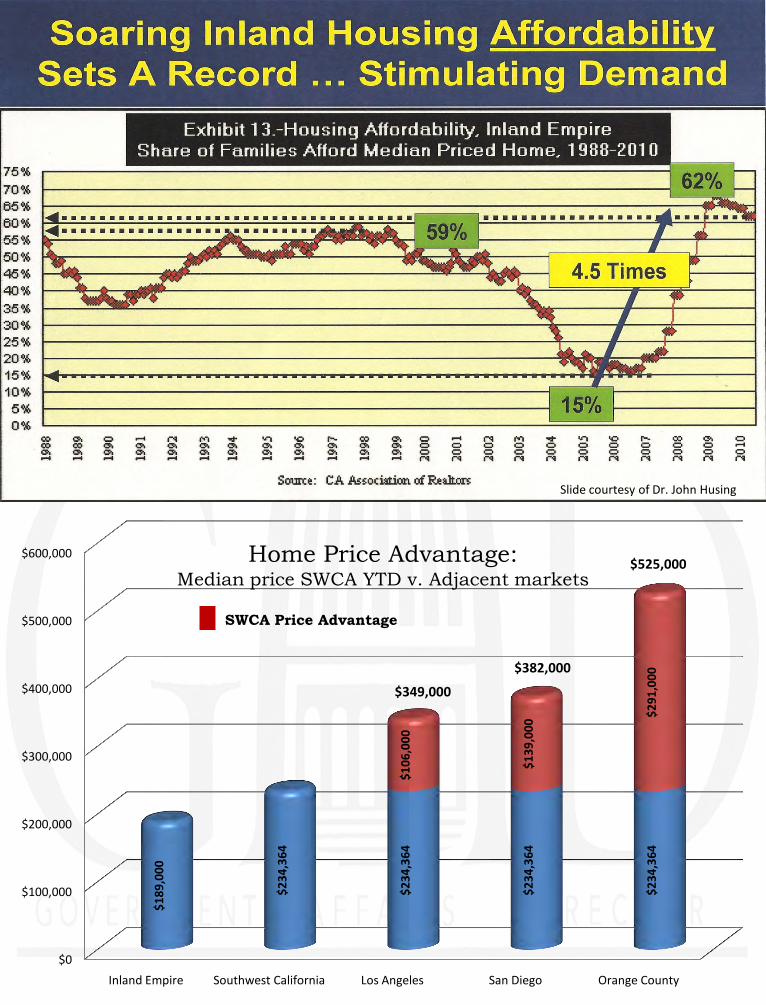

One of his most disturbing slides illustrates that EVERY wage and salary job created in Californiasince 1998 has been lost! Talk about a lost decade. During that time we’ve added about 5 millionresidents to the state so the imbalance of unemployment is exacerbated. And while Augustunemployment in the US stood at 9.6%, and California weighed in at 12.8%, the Inland Empire iscurrently 15.1%, second only to Detroit for unemployment in regions over 1 million population.

The IE created 42.3% of California's jobs from 2000-2007 but we are actively chasing those jobs awayas the legislature seeks to grow ‘green’ jobs and other tech jobs to the detriment of the kind of bluecollar manufacturing, construction & logistics jobs that grew our region and state during the lastboom. We need to focus on our own jobs base and creation because Sacramento is not going to helpus.

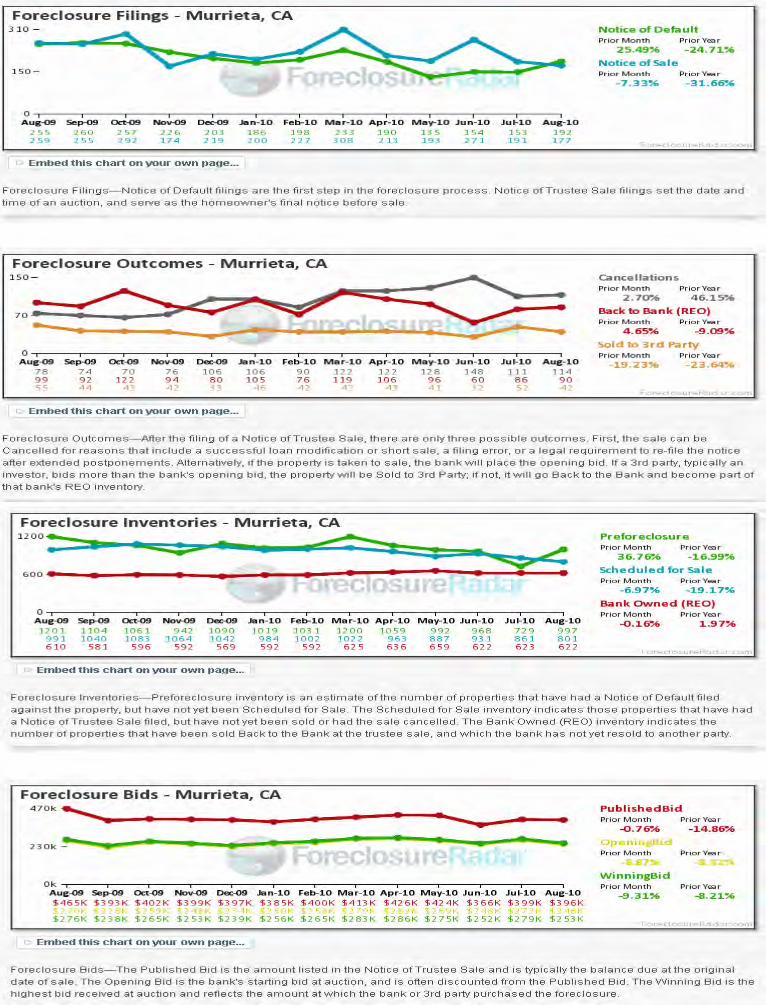

I’ve also included a complete run-down of foreclosure data for your city. Dr. Husing noted the portentof a shadow inventory and the potential for additional downward price pressure from a large releaseof REO properties. IF such a thing exists, and IF the banks are foolish enough to release everythingat once instead of trickling them onto the market, I still believe between our anemic inventory levelsand strong demand, we would see minimal, if any, impact to our median price in the region.

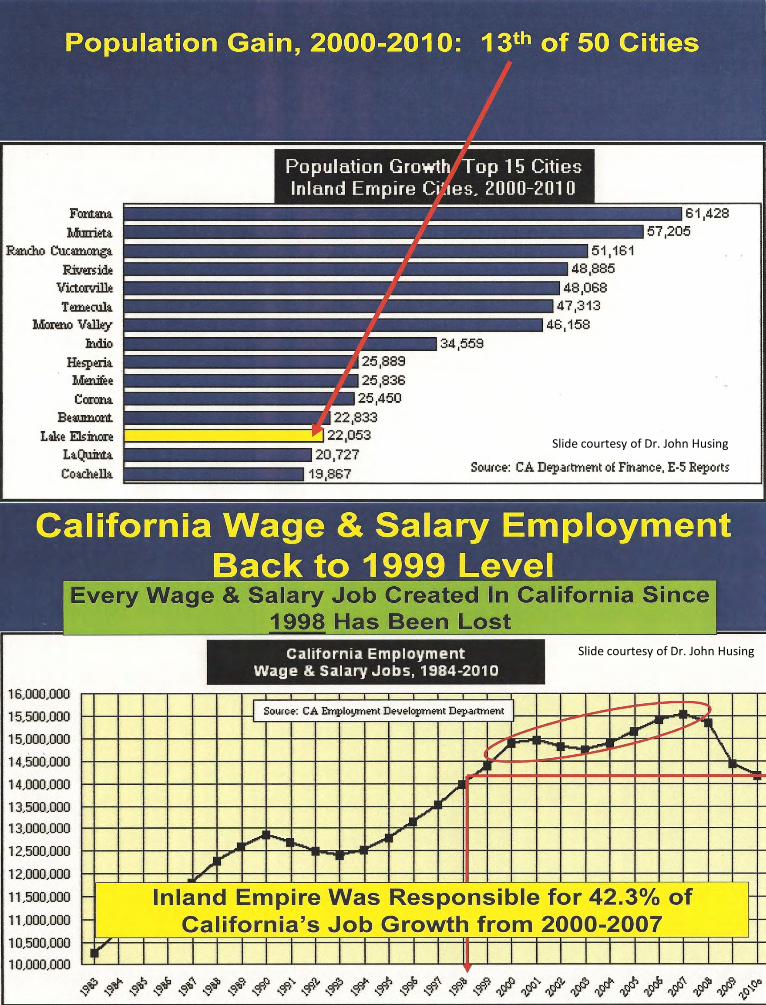

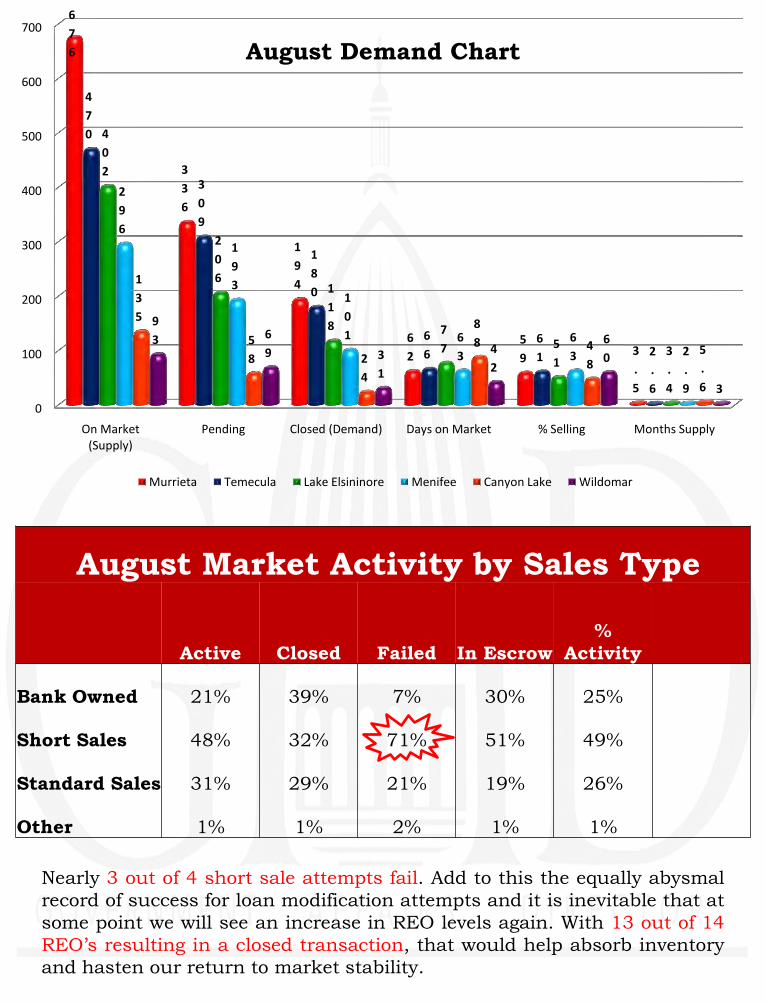

Now to some local news. I read an article in one of the local papers last week where the reporter saidlocal sales ‘plummeted’ in August. You may recall last month when I chuckled at national writersusing the terms ‘plummeted’ and ‘plunged’ to describe the last two months of housing sales. That’scertainly not the case here in Southwest California so I can only ascribe our local writers trepidationsto reading too much AP. As you can see, single family sales remained strong posting moderate gainsover July in 4 of 6 cities. Sales are well ahead of January figures and up even stronger over lastAugust.

Prices also maintained their stagger – up here, down there – nothing spectacular. I would also remindyou that the unit sales presented here are single family home sale only. They do not include condo’s,mobile homes or 3rd party auction sales. Murrieta recorded 34 condo sales last month, Temecula 11.By any measure, our demand remains good. Perhaps not as strong as 6 months ago but still healthy.Many buyers have grown frustrated with the short sale process and are simply sitting on the sidelinesuntil a return of REO’s or a return to standard sales. Well priced standard sales are in great demandand multiple bids for them and REO’s is still common.

As you have questions, please don’t hesitate to call.

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

Inland Empire Southwest California Los Angeles San Diego Orange County

$189

,000

$234

,364

$234

,364

$234

,364

$234

,364

$106

,000

$139

,000

$291

,000

Home Price Advantage:Median price SWCA YTD v. Adjacent markets

$349,000

$382,000

$525,000

SWCA Price Advantage

Slide courtesy of Dr. John Husing

Slide courtesy of Dr. John Husing

Slide courtesy of Dr. John Husing

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

3/09 6/09 9/09 12/09 3/10 6/10

Temecula Murrieta Lake Elsinore Menifee Wildomar Canyon Lake

Southwest CaliforniaMedian Price

Southwest CaliforniaSingle Family Unit Sales

0

50

100

150

200

250

3/09 6/09 9/09 12/09 3/10 6/10

Temecula Murrieta Lake Elsinore Menifee Wildomar Canyon Lake

August Market Activity by Sales Type

Active Closed Failed In Escrow%

Activity

Bank Owned 21% 39% 7% 30% 25%

Short Sales 48% 32% 71% 51% 49%

Standard Sales 31% 29% 21% 19% 26%

Other 1% 1% 2% 1% 1%

0

100

200

300

400

500

600

700

On Market (Supply)

Pending Closed (Demand) Days on Market % Selling Months Supply

676

336

194

62

59 3

.5

470

309

180

66

61 2

.6

402

206

118 7

7 51

3.4

296

193

101 6

363 2

.9

135

58 2

4

88 4

85.6

93 6

9 31

42

60

3

Murrieta Temecula Lake Elsininore Menifee Canyon Lake Wildomar

August Demand Chart

Nearly 3 out of 4 short sale attempts fail. Add to this the equally abysmalrecord of success for loan modification attempts and it is inevitable that atsome point we will see an increase in REO levels again. With 13 out of 14REO’s resulting in a closed transaction, that would help absorb inventoryand hasten our return to market stability.

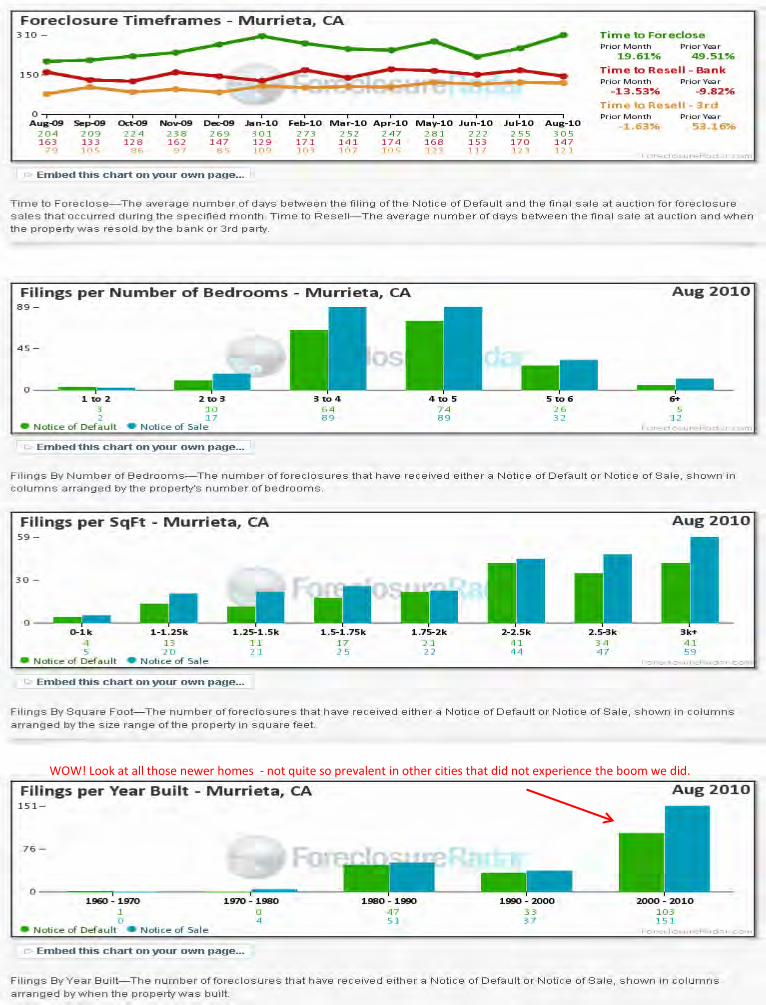

WOW! Look at all those newer homes - not quite so prevalent in other cities that did not experience the boom we did.

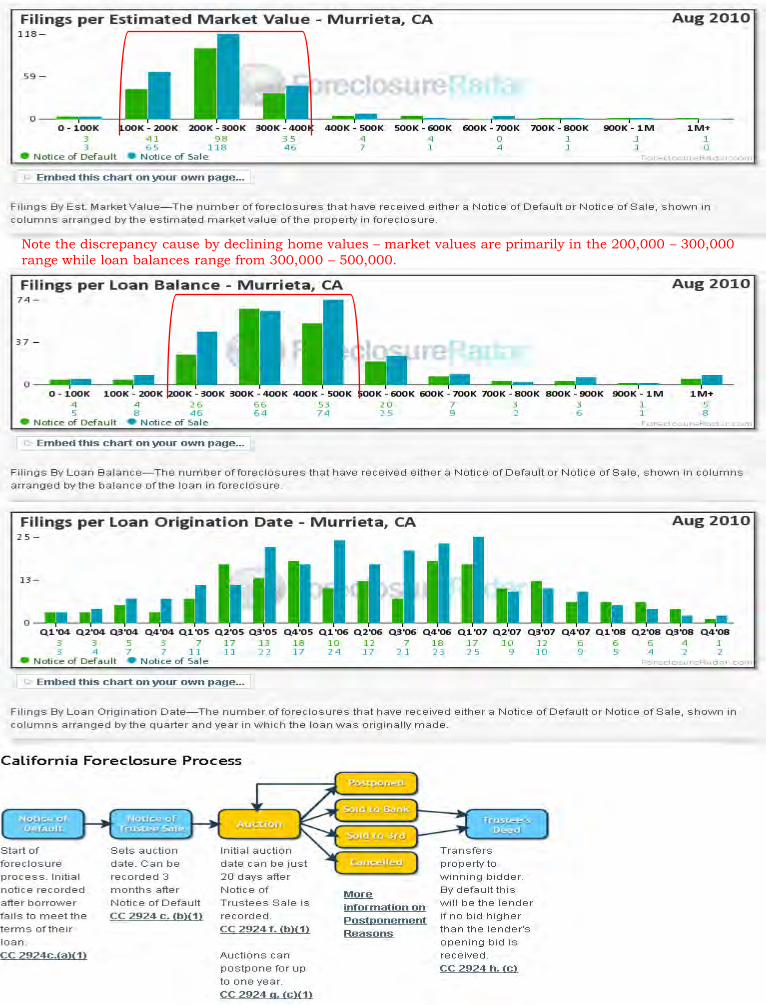

Note the discrepancy cause by declining home values – market values are primarily in the 200,000 – 300,000 range while loan balances range from 300,000 – 500,000.