8 | 1 chapter 4: consumer purchasing section 4.1 consumer purchasing today’s agenda: 1.what...

TRANSCRIPT

8 | 1

Chapter 4: Consumer Purchasing

Section 4.1 Consumer Purchasing

Today’s Agenda:1. What influences your buying decisions?

2. Examine a research-based approach to buying

3. Strategies for making wise buying decisions

Goal:Learning how to use various techniques to get the best

value for your money!

8 | 2

Economic Factors

Social Factors

Personal Factors

Factors that Influence Buying Decisions

Figure 4.1

How might each of these factors affect

our purchases?

Why do we buy what we buy?

8 | 3

Convenience

Cash vs. Credit

Price vs. Quality

Online Purchasing

Forces us to think about priorities, consequences.

Unless money is unlimited,

Buying decisions involve trade-offs!How do

You shop?

8 | 4

Phase 1: Before You Shop, Ask…

What do I really need?

What information will help me?

Do I know enough to make an informed decision?

What does pre-shopping research involve?

A Research-Based Approach

8 | 5

1. Identify Your Needs

–WANTS vs. NEEDS Have an open mind; think of ALL your options

2. Gather Information

– Brands? Costs? Options/Features? Consequences

– Where can you find reliable information?

– Do you spend enough time? Too much time?

3. Know the Marketplace

Knowledge = POWER

8 | 6

Phase 2: Weighing the Alternatives

There are usually lots of options! Consider all of them!

1. Compare Features (what is important to you?)

–Design? Quality? Performance? LOOK?

2. Compare Prices

– Does Price = Quality?

3. Compare Vendors– Go to different stores, look online

– When is this especially useful?

8 | 7

Phase 3: Making the Purchase

1. Negotiate the Price (if possible!)

2. Decide on Credit or Cash

– Costs?

– Benefits?

3. Know the Real Price– Does the listed price include everything?

Phase 4: After the Purchase

4. Rethink your purchase

5. Did you make the right choice? Why evaluate?

8 | 8

1.Time Your Purchases

Law of supply and demand

2. Store Selection

Benefits vs. Limitations

3. Compare Brands

Generic vs. National Brands?

Smart Buying Strategies

Can you tell the difference?

8 | 9

Impulse Buying can ruin a budget!

Try a 2-day cool-down period

Pg. 100

4. Examine Labels

Cool Advertising

5. Compare Prices

Unit Pricing

Is bigger always better?

$45

$9

8 | 10

Unit = VolumeUnit = Weight

8 | 11

Supplement to Chapter 4

Purchasing a Vehicle

Today’s Agenda: Learn what it means to “LEASE” a vehicle

Goals: Understand how a lease works & how it compares to

buying a vehicle

Recognize the factors that affect the cost of a lease

Identify the advantages / disadvantages of leasing

8 | 12

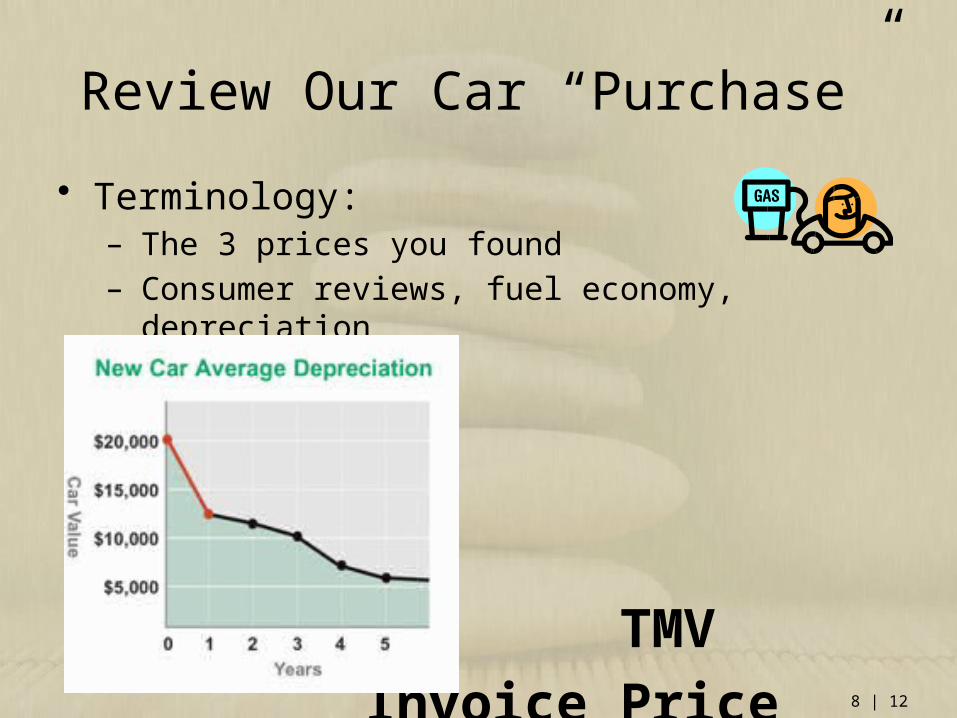

Review Our Car “Purchase”

• Terminology: – The 3 prices you found– Consumer reviews, fuel economy, depreciation

MSRP TMV

Invoice Price

8 | 13

What happens to the value of my car over time?

The value of my car at any given point in time is it’s “RESIDUAL VALUE”

MSRP = $18,350

8 | 14

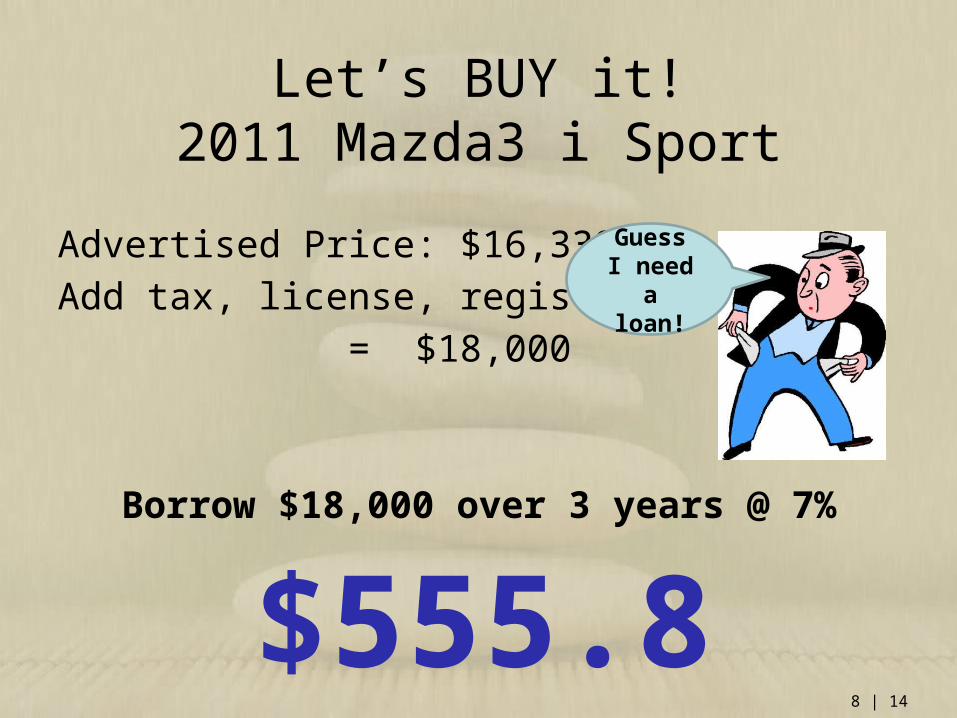

Let’s BUY it!2011 Mazda3 i Sport

Advertised Price: $16,338

Add tax, license, registration:

= $18,000

Borrow $18,000 over 3 years @ 7%

$555.80

Guess I need a loan!

8 | 15

$233

8 | 16

What does it mean to“LEASE” this car for 3 years?

I will “rent” this car…

it will depreciate as I drive it.

Value after 3 years?

When my lease is up, I simply return vehicle to dealership.

8 | 17

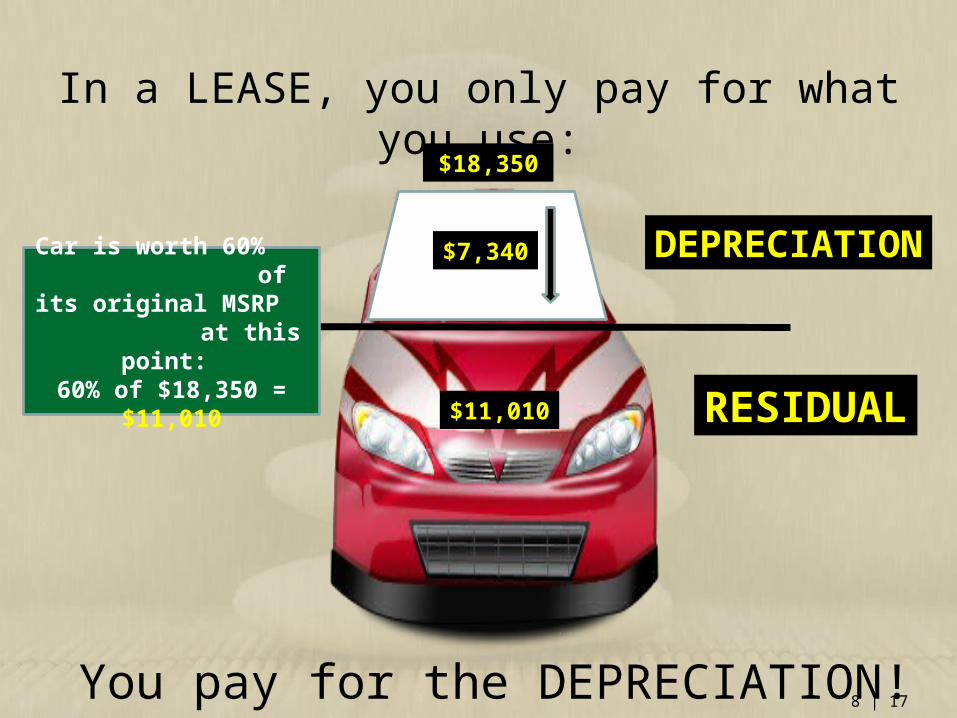

In a LEASE, you only pay for what you use:

Car is worth 60% of its original MSRP

at this point: 60% of $18,350 =

$11,010$11,010

$7,340 DEPRECIATION

RESIDUAL

$18,350

You pay for the DEPRECIATION!

8 | 18

You pay depreciation + sales tax (on this amount)

+ interest (for borrowing)~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

$600

$450

$7,340

$8390

36 payments

What is my monthly cost to lease this vehicle for 3 years?

$233

8 | 19

Let’s look at the “BUY” option again… After 3 years I

have paid $18,000

and

the car is

MINE.

After7 years,Residual value is

$3000

If I sell for $3000 after 7 years, what was my overall cost?

$18,000 paid - $3,000 received = $15,000(or $178 per month)

8 | 20

LEASING…The good and the bad:

Advantages:

Lower monthly payment

Save on sales tax

Always under warranty

Afford nicer car

Disadvantages:

Restrictions on mileage

No equity (ownership)

Charges for excess “wear”

Always a payment!

8 | 21

CONCLUSIONS…

• Leasing can be confusing!• Cost to lease depends on a car’s depreciation• Leasing is wise in certain situations…

– Decide if it is right for YOU!

Long-Term: Buying is Cheaper

Middle (4-5 yrs): Even

Short-Term: Leasing Wins

8 | 22

• Information = Power

• Smart shoppers do their homework!

• Why gather information before interacting with sellers????

• Remember: sellers are highly skilled; not objective

• The key to successful negotiating: enough knowledge and accurate information

Shopping for a Vehicle

8 | 23

1. Pre-Shopping Thoughts:• Determine your affordability (look at budget)

• Think about your choices: buy used; buy new; lease; bus! (what works with your budget?)

2. Start Research• Investigate makes, models (talk to friends, read

reviews)

• Narrow down choices based on what is important to YOU:

=> Safety, features, fuel efficiency, warranty?

Where to Begin…

8 | 24

• Examine your financing options

Remember: If you are taking out a car loan, what 2 factors will affect your monthly payments?

1. Interest rate:– Check with local bank/credit union

– Know your credit score!

– Is manufacturer or dealer offering any special financing deals?

2. Term: how many months to pay off loan– Trend: longer-term financing--what does this do?

8 | 25

• Other things to research:

– Available rebates / incentives?

– Reviews?

– Comparable vehicles / feature comparisons?

– Depreciation?

– Warranty?

• Do you have a vehicle to trade-in?

(Find out its value BEFORE talking to salesperson)

Tips on Negotiating your trade-in:

•Treat the purchase and trade-in as separate transactions

•Come to agreement on purchase price of new car

•Then, negotiate a price for your trade-in

•Sell the vehicle yourself if they come in too low

8 | 26

• Get Organized? 3 Basic Options to Consider:

Sheet One: New Car Buy• Negotiate one thing at a time.

• With many other variables (new car price, trade-in, rebates, options, interest rate) the dealer can APPEAR to be cooperative on one aspect and make up the difference elsewhere!

– MSRP vs. Invoice Price vs. TMV

– What do each of these mean?

Know exactly how themonthly figure was

calculated!

8 | 27

Sheet Two: Used Car Buy• Remember: Late model used car with

low mileage = practically “new” !

• Research pricing: www.edmunds.com

- Trade-In vs. Dealer Retail vs. Private Party

- What do each of these mean?

• Most research, including inventory searches, can be done online / in newspapers

Sheet Three: Leasing a Vehicle• What is an automobile lease? Read handout

8 | 28

Leasing Terminology1. Capitalized Cost [Cap Cost]

Negotiated price of vehicle

2. Cap Cost Reduction Down payment, trade-in, or rebate that

will reduce the amount being financed

3. Adjusted Cap Cost Cap cost – cap cost reductions:

the actual amount being financed

4. Residual Value The projected value of the vehicle at the end of the lease

5. Money Factor Similar to APR to finance vehicle (multiply by 2400 to compare)

6. Price of Vehicle – Residual Value = Depreciation

DEPRECIATED VALUE = $7,000

RESIDUALVALUE = $13,000

8 | 29

Leasing Advantages:

• More car for the money because lower monthly payments

• Best when depreciation is low (residual value is high)

• Cheaper in the short-run

Leasing Disadvantages:

• At the end of lease you don’t own the car

• Usually more expensive in the long-run

• Mileage allowance

7. Open-end lease vs. Closed-end leases

8. Excess mileage charges

9. Acquisition fee

10. Disposition fee

11. Early termination fee

In general, be cautious about leasing:

It is complicated.

Remember: Knowledge = Power